Embed Size (px)

Citation preview

8/7/2019 75 Business Outlook Survey

http://slidepdf.com/reader/full/75-business-outlook-survey 1/10

[ ]

75th CII BUSINESS OUTLOOK January– March 2010-11

75th

CII BUSINESS OUTLOOK January- March 2011

8/7/2019 75 Business Outlook Survey

http://slidepdf.com/reader/full/75-business-outlook-survey 2/10

[ 2 ]

75th CII BUSINESS OUTLOOK January– March 2010-11

• 75% of the respondents expect their sales to rise

while 59% of the respondents foresee an increase in

production and 67% expect increase in new orders in

January-March 2011 compared to the previous

quarter. Also, majority of the respondents (52%)

expect raw material prices to go up in the coming

quarter.

• 65% of the respondents do not expect their

inventory levels to decline.

• 44% of the respondents expect employment to

increase during the next three months

• The survey revealed that 52% of the respondents

do no expect availability of credit to increase, while

71% feel that the cost of credit will not fall in January-

March 2011.

• 37% of the respondents expect export volumes to

increase in January-March 2011.

• High Fiscal Deficit and Slackening Consumer

Demand are the top concerns.

• Business Confidence Index (CII-BCI) for

January-March 2011 stood almost flat at 66.7 as

compared to 66.2 in the 74th Business Outlook Survey

for October-December 2010 when the index had

increased by 1.4 points.

• Sectoral break-up shows that BCI for Primary

sector is highest followed by Services and then

Manufacturing as in the previous survey.

• A majority of respondents (68%) expect GDP

growth rate above 8.0%, of this, 41% expect the

growth rate to be in the range of 8.0 to 8.5% and 27%

expect it to be higher than 8.5% in 2010-11.

• 78% of the respondents expect inflation to be

above 6.0% in 2010. Of this, the majority (29%) expect

it to be in the range of 7.0 - 8.0%.

• 63% of the respondents would like to increase

their spending on capacity expansion during January-

March 2011 as compared to the previous quarter.

• 74% of respondents expect capacity utilization to

exceed 75% in the quarter ending March 2011.

HIGHLIGHTS

8/7/2019 75 Business Outlook Survey

http://slidepdf.com/reader/full/75-business-outlook-survey 3/10

[ 3 ]

75th CII BUSINESS OUTLOOK January– March 2010-11

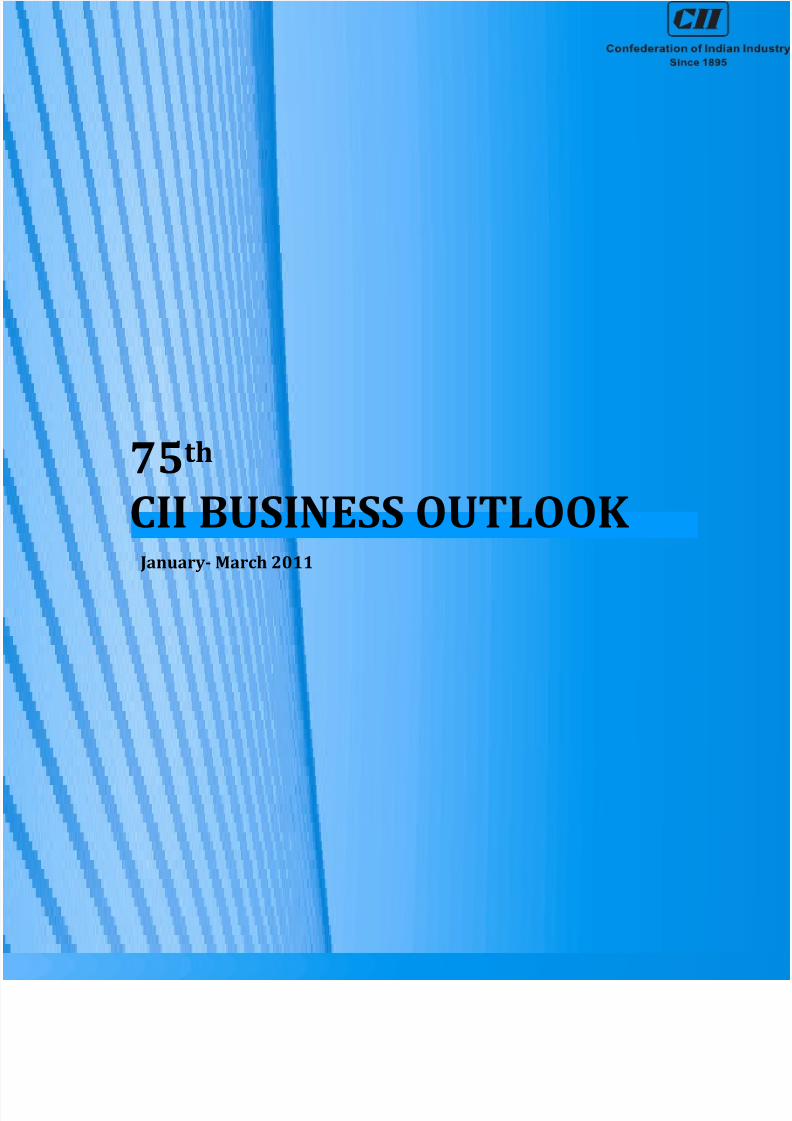

I. CII Business Confidence Index

The CII Business Confidence Index (CII-BCI) for the

fourth quarter (January-March) of the financial year2010-11 stood at 66.7, a modest 0.5 points higher than

that in the previous quarter. This is in comparison with

a 1.4 points decline in the previous quarter. Comparing

the BCI from earlier surveys to that of the current

survey, we observe that after a big jump in the second

half of 2009-10, the BCI has remained steady.

The respondents in the survey are asked to provide a

view on the performance of their company, their

sector and the economy based on their perceptions.

The CII-BCI is then constructed as a weighted average

of the Current Situation Index (CSI) and the

Expectation Index (EI). The Current Situation Index(CSI) compares the current business conditions in

relation to the previous quarter. The CSI fell to 62.7 for

the third quarter of this financial year as compared to

64.0 for the second quarter. The expectation index, on

the other hand reflects the expectation of respondents

about the coming quarter in comparison to the current

quarter. The expectation index for January-March 2011

stood at 68.7 as compared to 67.3 in October-

December 2010. The decline in the CSI can be

explained by tightening monetary policy, higher

inflation and rising input costs in the past quarter.

However the prospect for the coming quarter

(January-March 2011) appears to be brighter as

depicted by the EI.

Sectoral Break Up

Sectoral break up into three major sectors namely

primary, industry and services reveal that BCI is lower

for the manufacturing and services sector while BCI is

way above the overall BCI for the primary sector. This

can be explained by the fact that better monsoons this

year as compared to drought like situation last year

has improved the prospects for the primary sector.

Consequently, in the first half of 2010-11 agriculturalgrowth increased to 3.8% as compared to a mere 1.0%

a year earlier.

Overall BCI for Manufacturing and Services stood at

57.5 and 65.2 respectively in the current survey.

Current Situation Index for both the sectors has been

lower than the expectation index as business

environment in the last quarter has been tough for

IndexOct–Mar

2008-09

Apr-Sept

2009-10

Oct–Mar

2009-10

Apr-Sept

2010-11

Jan-Mar

2010-11

BusinessConfidence Index

56.3 58.7 66.1 67.6 66.7

Current Situation

Index55.9 53.4 59.3 64.8 62.7

(a) Overall Economy 48.3 48.6 56.4 65.1 59.9

(b) Own ActivitySector

52.3 50.1 57.5 64.4 63.0

(c) Own Company 60.9 57.2 61.6 64.9 63.4

Expectation Index 56.5 61.4 69.5 69.1 68.7

(a) Overall Economy 47.6 56.8 67.4 69.9 65.6

(b) Own ActivitySector

53.8 58.6 68.0 67.7 68.8

(c) Own Company 61.4 64.7 71.1 69.7 69.7

Business Confidence Index

Oct-Dec

2010-11

66.2

64.0

65.0

63.2

64.3

67.3

66.0

66.3

68.4

Sectors Current Index Expectation

Index

Overall

BCI

All 62.7 68.7 66.7

Primary 73.4 89.4 84.1

Manufacturing 49.5 61.5 57.5

Services 62.7 66.4 65.2

Sector wise BCI

CII Business Confidence Index

02040

6080

H 2 2 0

0 8 - 0 9

H 1 2 0 0 9

- 1 0

H 2 2 0 0 9

- 1 0

H 1 2 0 1 0

- 1 1

Q 3 2 0 1 0

- 1 1

Q 4 2 0 1 0

- 1 1

8/7/2019 75 Business Outlook Survey

http://slidepdf.com/reader/full/75-business-outlook-survey 4/10

[ 4 ]

75th CII BUSINESS OUTLOOK January– March 2010-11

firms. The Manufacturing sector has been hit the worst

due to significant increase in raw material costs,

inflationary expectations in the economy and shortage

of liquidity, as a result the BCI for Manufacturingslowed down by 8.6 points to 57.5 in the current

survey as compared to the previous survey.

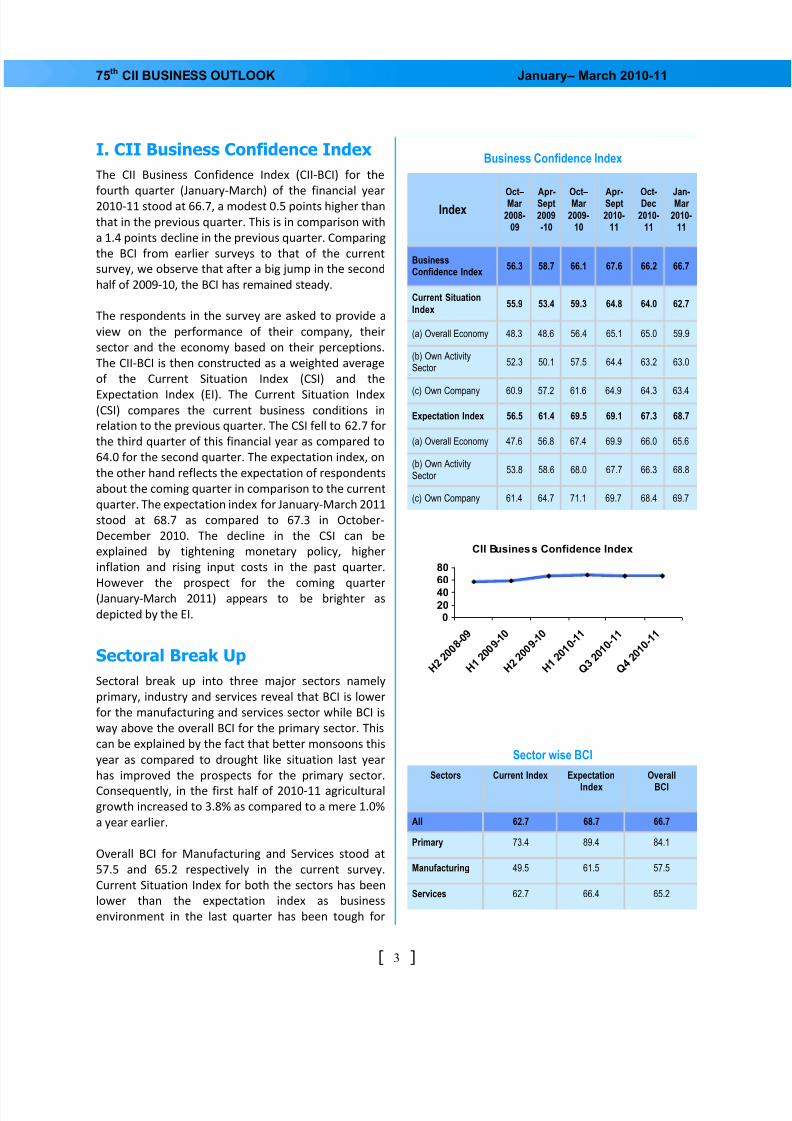

Outlook on the economy

The Indian economy saw a strong growth of 8.9% in

the first half (April-September) of 2010-11 as

compared to 7.5% in the same period last year, driven

by strong growth in all three sectors- agriculture,

industry and services. Consistent with this strong

growth rate, the 75th BOS revealed that 68.0% of the

respondents expect GDP growth in the 8.0% plus range

for 2010-11. Of this, the majority (41%) expect it to bein 8.0-8.5% range, 24.0% in the 8.5-9.0% range and

3.0% expect it to be greater than 9.0%. These numbers

are consistent with the previous Business Outlook

Survey, when 58.5% of the respondents expected GDP

growth in the 8.0% plus region, while only 3.0%

expected it to be lower than 7.0%.

On the inflation front, 78% of the respondents expect

average inflation to be above 6.0% in 2010-11. Of

these, 24% expect inflation to be above 8.0%, while

majority of respondents (28%) expect it to be in the

range of 7.0-8.0% and 25% expect it to be in the range

of 6.0-7.0%. An optimistic 15% expects it to decline to

within 5.0-6.0% while a mere 7% of the respondents

are hopeful that inflation will be below 5.0%. With the

average headline inflation remaining above 9.0% for

the first nine months of the current fiscal year

2010-11, inflation has become a primary concern for

the economy. Although inflation moderated to 7.5% in

November 2010, it shot up to 8.4% in December 2010

once again as food inflation surged to 13.6%. Thus, it is

not surprising that the majority of the respondents

continue to expect inflation to remain high.

II. Business Prospects

The prospects for investment, capacity utilization,

production, employment and exports are some vital

elements that build up the business confidence. Here,

we briefly analyze the expectations of the respondents

on the above mentioned constituents of business

confidence. The responses are also analyzed according

Highlights Highlights HighlightsHighlights Highlights Highlights

Highlights Highlights Highlights

Highlights Highlights Highlights

Highlights

Expectation on GDP Growth (2010-11)(% of Respondents)

10%19%

41%

24%

3%

2%

1%

<7.0%

7.0% -7.5%

7.5% -8.0%

8.0% - 8.5%

8.5% - 9.0%

> 9.0%

Expectation on Average Inflation (2010-11)

(% of Respondents)

7%

15%

25%29%

24% <5.0%

5.0 -6.0%

6.0% - 7.0%

7.0% - 8.0%

>8.0%

8/7/2019 75 Business Outlook Survey

http://slidepdf.com/reader/full/75-business-outlook-survey 5/10

[ 5 ]

75th CII BUSINESS OUTLOOK January– March 2010-11

to the size classification of respondents. Amongst the

total respondents, 28.0% were small enterprises while

36.0% and 24.0% were medium and large enterprises

respectively.

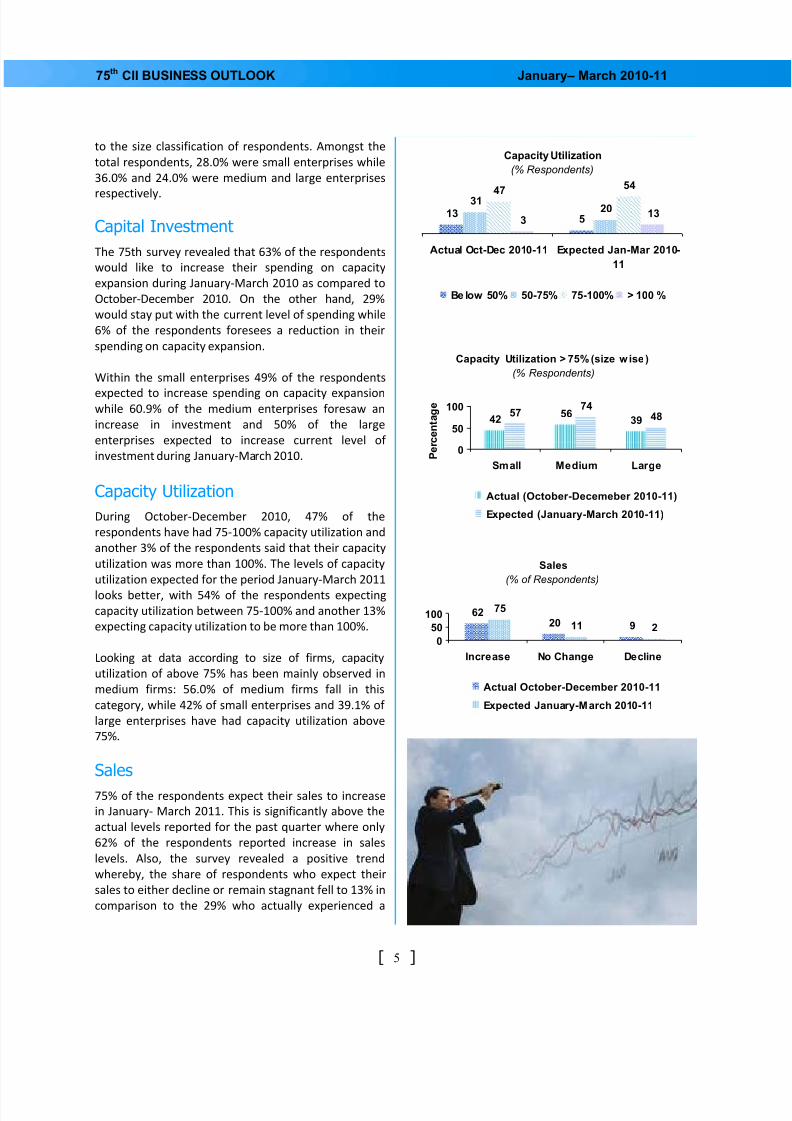

Capital Investment

The 75th survey revealed that 63% of the respondents

would like to increase their spending on capacity

expansion during January-March 2010 as compared to

October-December 2010. On the other hand, 29%

would stay put with the current level of spending while

6% of the respondents foresees a reduction in their

spending on capacity expansion.

Within the small enterprises 49% of the respondents

expected to increase spending on capacity expansionwhile 60.9% of the medium enterprises foresaw an

increase in investment and 50% of the large

enterprises expected to increase current level of

investment during January-March 2010.

Capacity Utilization

During October-December 2010, 47% of the

respondents have had 75-100% capacity utilization and

another 3% of the respondents said that their capacity

utilization was more than 100%. The levels of capacity

utilization expected for the period January-March 2011

looks better, with 54% of the respondents expecting

capacity utilization between 75-100% and another 13%

expecting capacity utilization to be more than 100%.

Looking at data according to size of firms, capacity

utilization of above 75% has been mainly observed in

medium firms: 56.0% of medium firms fall in this

category, while 42% of small enterprises and 39.1% of

large enterprises have had capacity utilization above

75%.

Sales

75% of the respondents expect their sales to increase

in January- March 2011. This is significantly above the

actual levels reported for the past quarter where only

62% of the respondents reported increase in sales

levels. Also, the survey revealed a positive trend

whereby, the share of respondents who expect their

sales to either decline or remain stagnant fell to 13% in

comparison to the 29% who actually experienced a

Capacity Utilization > 75% (size wise)

(% Respondents)

4256

3957

7448

0

50

100

Small Medium Large P e r c e n t a g e

Actual (October-Decemeber 2010-11)

Expected (January-March 2010-11)

Sales

(% of Respondents)

6220 9

75

11 2

0

50

100

Increase No Change Decline

Actual October-December 2010-11

Expected January-March 2010-11

Capacity Utilization

(% Respondents)

135

3120

4754

313

Actual Oct-Dec 2010-11 Expected Jan-Mar 2010-

11

Be low 50% 50-75% 75-100% > 100 %

8/7/2019 75 Business Outlook Survey

http://slidepdf.com/reader/full/75-business-outlook-survey 6/10

[ 6 ]

75th CII BUSINESS OUTLOOK January– March 2010-11

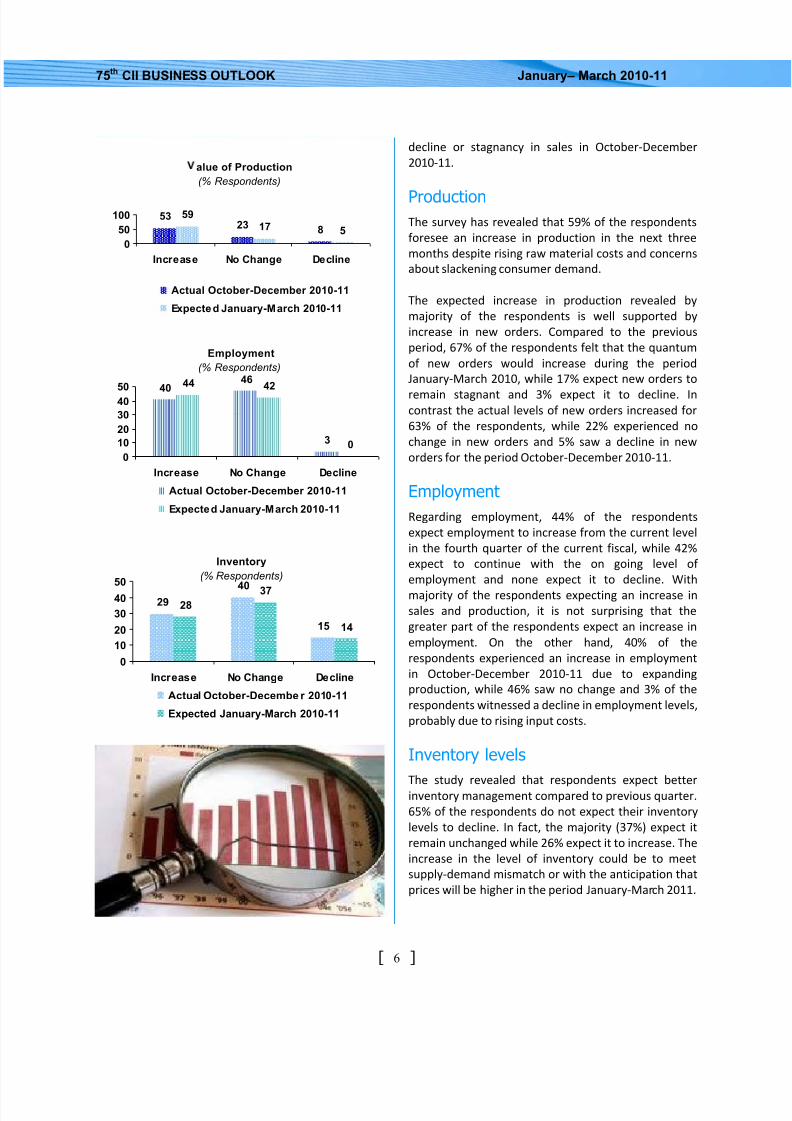

decline or stagnancy in sales in October-December

2010-11.

ProductionThe survey has revealed that 59% of the respondents

foresee an increase in production in the next three

months despite rising raw material costs and concerns

about slackening consumer demand.

The expected increase in production revealed by

majority of the respondents is well supported by

increase in new orders. Compared to the previous

period, 67% of the respondents felt that the quantum

of new orders would increase during the period

January-March 2010, while 17% expect new orders to

remain stagnant and 3% expect it to decline. Incontrast the actual levels of new orders increased for

63% of the respondents, while 22% experienced no

change in new orders and 5% saw a decline in new

orders for the period October-December 2010-11.

Employment

Regarding employment, 44% of the respondents

expect employment to increase from the current level

in the fourth quarter of the current fiscal, while 42%

expect to continue with the on going level of

employment and none expect it to decline. With

majority of the respondents expecting an increase in

sales and production, it is not surprising that the

greater part of the respondents expect an increase in

employment. On the other hand, 40% of the

respondents experienced an increase in employment

in October-December 2010-11 due to expanding

production, while 46% saw no change and 3% of the

respondents witnessed a decline in employment levels,

probably due to rising input costs.

Inventory levels

The study revealed that respondents expect betterinventory management compared to previous quarter.

65% of the respondents do not expect their inventory

levels to decline. In fact, the majority (37%) expect it

remain unchanged while 26% expect it to increase. The

increase in the level of inventory could be to meet

supply-demand mismatch or with the anticipation that

prices will be higher in the period January-March 2011.

Employment

(% Respondents)

40

46

3

44 42

0

0

10

20

30

40

50

Increase No Change Decline

Actual October-December 2010-11

Expected January-March 2010-11

Inventory

(% Respondents)

2940

15

2837

14

0

10

20

30

40

50

Increase No Change Decline

Actual October-Decembe r 2010-11

Expected January-March 2010-11

alue of Production

(% Respondents)

5323 8

5917 5

0

50

100

Increase No Change Decline

Actual October-December 2010-11

Expected January-March 2010-11

8/7/2019 75 Business Outlook Survey

http://slidepdf.com/reader/full/75-business-outlook-survey 7/10

[ 7 ]

75th CII BUSINESS OUTLOOK January– March 2010-11

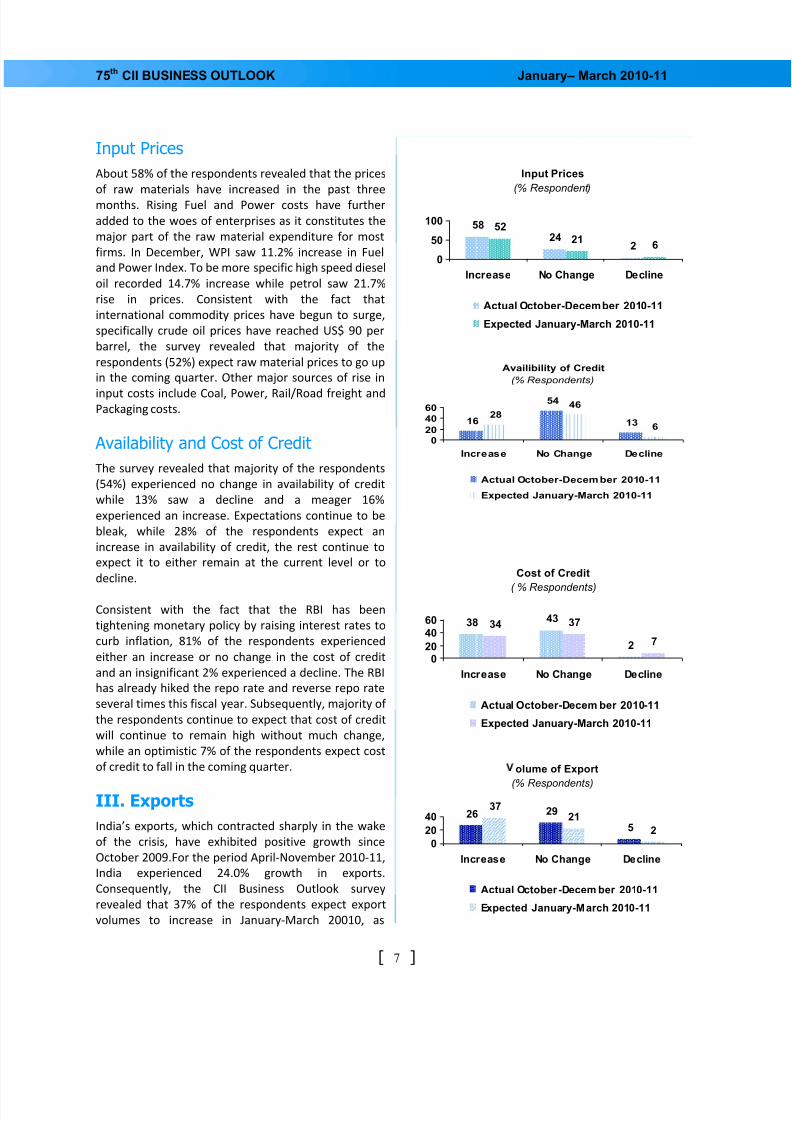

Input Prices

About 58% of the respondents revealed that the prices

of raw materials have increased in the past three

months. Rising Fuel and Power costs have further

added to the woes of enterprises as it constitutes the

major part of the raw material expenditure for most

firms. In December, WPI saw 11.2% increase in Fuel

and Power Index. To be more specific high speed diesel

oil recorded 14.7% increase while petrol saw 21.7%

rise in prices. Consistent with the fact that

international commodity prices have begun to surge,

specifically crude oil prices have reached US$ 90 per

barrel, the survey revealed that majority of the

respondents (52%) expect raw material prices to go up

in the coming quarter. Other major sources of rise in

input costs include Coal, Power, Rail/Road freight andPackaging costs.

Availability and Cost of Credit

The survey revealed that majority of the respondents

(54%) experienced no change in availability of credit

while 13% saw a decline and a meager 16%

experienced an increase. Expectations continue to be

bleak, while 28% of the respondents expect an

increase in availability of credit, the rest continue to

expect it to either remain at the current level or to

decline.

Consistent with the fact that the RBI has been

tightening monetary policy by raising interest rates to

curb inflation, 81% of the respondents experienced

either an increase or no change in the cost of credit

and an insignificant 2% experienced a decline. The RBI

has already hiked the repo rate and reverse repo rate

several times this fiscal year. Subsequently, majority of

the respondents continue to expect that cost of credit

will continue to remain high without much change,

while an optimistic 7% of the respondents expect cost

of credit to fall in the coming quarter.

III. Exports

India’s exports, which contracted sharply in the wake

of the crisis, have exhibited positive growth since

October 2009.For the period April-November 2010-11,

India experienced 24.0% growth in exports.

Consequently, the CII Business Outlook survey

revealed that 37% of the respondents expect export

volumes to increase in January-March 20010, as

Availibility of Credit

(% Respondents)

16

54

1328

46

6

020

40

60

Increase No Change Decline

Actual October-December 2010-11

Expected January-March 2010-11

Cost of Credit

( % Respondents)

38 43

2

34 37

7

020

40

60

Increase No Change Decline

Actual October-Decem ber 2010-11

Expected January-March 2010-11

olume of Export

(% Respondents)

26 29

5

3721

2

0

20

40

Increase No Change Decline

Actual October -Decem ber 2010-11

Expected January-March 2010-11

Input Prices

(% Respondent)

5824

2

52

216

0

50

100

Increase No Change Decline

Actual October-December 2010-11

Expected January-March 2010-11

8/7/2019 75 Business Outlook Survey

http://slidepdf.com/reader/full/75-business-outlook-survey 8/10

[ 8 ]

75th CII BUSINESS OUTLOOK January– March 2010-11

compared to the 26% respondents who actually

experienced an increase in volume of export in

October-December 2010. The better export scenario is

also visible from the increase in new ordersexperienced by many firms (47%) in October-

December 2010 .The survey also revealed that 29% of

the respondents experienced no change in export

volumes while 5% witnessed a decline in the volume of

exports. We also observed that the percent of

respondents that expect export volumes to decline has

fallen to 2%, while 21% of the respondents expect no

change in trade volumes in the coming three months.

Procedural Delays

The 75th Business Outlook Survey revealed that

procedural delays remained as the major problemfaced by exporters and a major consequence of this is

the increase in transaction costs. In fact, 53% of the

respondents felt that there was no decline in

procedural delays for the period October-December

2010. By transaction cost we mean increase in cost of

exports beside the cost associated with the production

process, such as procedural complexities associated

with the gambit of export procedures starting from

Import-Export licenses to the realization of the export

receivables. The procedural complexities in the export

process in a country may also lead to a change in

preference of an importer to an alternative country

with less procedural complexities. Thus, a very high

transaction cost, if it exists, may encumber the export

growth even if other policy related measures are in

place. Despite various measures taken by the

government to reduce bureaucratic delays, it still

remains a major impediment. However, on thebrighter side 11% of the respondent are positive that

procedural delays will decline in January-March 2011

as compared to 5% who actually experienced a decline

in procedural delay in October-December 2010.

IV. Business Outlook: Concerns

The 75th CII Business Outlook Survey also revealed

certain major concerns of the respondents. The

respondents were asked to rank the following issues:

Slackening Consumer Demand, Cost of Compliance,

Currency risks, global Economic Instability, High

Interest Rates, Surge in Imports/IncreasingCompetition, infrastructural and Institutional shortage,

cost and availability of labor, Inflationary Conditions

and High Fiscal deficit. The average score of responses

identifies high fiscal deficit as the top concern followed

by slackening consumer demand and surge in imports/

increased competition respectively.

High fiscal deficit has appeared as a major concern in

the 75th Business Outlook Survey, unlike the previous

survey when it was ranked 10th. This is probably

because respondents feel that if the Government does

not moderate its fiscal deficit then there would

pressure on interest rates to increase. The surprising

finding of the survey is that despite consistent high

8/7/2019 75 Business Outlook Survey

http://slidepdf.com/reader/full/75-business-outlook-survey 9/10

[ 9 ]

75th CII BUSINESS OUTLOOK January– March 2010-11

inflation and consequent high raw material costs for

the first half of the fiscal year, respondents do not

consider inflationary condition as a major concern.

However, slackening consumer demand hasappeared as one of the major concerns, which is in

turn linked to inflationary conditions. Consumer

demand is also feared to be affected adversely as the

advanced economies show sluggish recovery. Other

major concerns include Cost of Compliance, Currency

Risks and Global Economic Instability. The increased

liquidity in the global market as a consequence of the

Quantitative easing policy of the US, whereby the Fed

had announced to buy $600 billion in long term

treasuries has resulted in a surge in capital into

emerging countries. The increased inflow of capital

has put countries like India and China at the risk of

currency appreciation, inflation and asset price

bubble.

Also, with dual rate of growth, with emerging

economies showing robust growth and advanced

economies struggling to stay afloat in the midst of

low demand and high unemployment, the global

economy is at a risk of uncoordinated action in the

form of protectionist policies.

VI. Coverage and Methodology

CII’s 75th

Business Outlook Survey is based on a largesample size of 180 companies covering all industry

sectors, including small, medium and large

enterprises from different regions. The survey also

enumerated responses across the spectrum of

industry groups both in public and private sectors

engaged in primary sector, manufacturing activities

Business Outlook: Major Concerns

6.5 6.2 6 5.9 5.85.2 4.8 4.4 4.3

3.9

H i g h F i s c a l

d e f i c i t

S l a c k e n i n g

C o n s u m e r

D e m a n d

S u r g e i n

I m p o r t s / I n c r e a s

i n g c o m p e t i t i o n

C o s t o f

C o m p l i a n c e

C u r r e n c y

R i s k s

G l o b a l

E c o n o m i c

I n s t a b i l i t y

I n f r a s t r u c t u r a l

a n d i n s t i t u t i o n a l

s h o r t a g e

H i g h I n t e r e s t

R a t e s

I n f l a t i o n a r y

C o n d i t i o n s

C o s t a n d

A v a i l a b i l t y o f

l a b o u r

A v e r a g e s c o

r e s

and in service sector.

28.0% of the respondents were from small

enterprises while 36.0% and 23.0% were frommedium and large firms respectively. Sectoral break

up shows that 63.0% of the respondents were from

the manufacturing sector while 31.0% and 4.5% were

from the services and primary sector respectively.

CII-BCI is calculated as a weighted average of the

Current Situation Index (CSI) and the Expectation In-

dex (EI), with greater weight given to EI as compared

to CSI. These indices are based on three questions on

the performance of the economy, respondent’s

industry sector and respondent’s company.

Respondents are asked to rate the current and

expected performance on a scale of 0 to 100. A score

above 50 indicates positive confidence while a score

above 75 would indicate strong positive confidence.

In the construction of the two sub indices, the highest

weight is given to the questions related to the

performance of the individual company, and the

lowest weight is assigned to the questions on the

economy. The weights are assigned on the basis of

the premise that the average respondents would

possess more detailed and accurate knowledge on

the current and expected performance of his own

company than the economy as a whole.

8/7/2019 75 Business Outlook Survey

http://slidepdf.com/reader/full/75-business-outlook-survey 10/10

[ 10 ]

75th CII BUSINESS OUTLOOK January– March 2010-11

Notes: figures may not add up to the total due to rounding off

Business Outlook Survey is a quarterly report prepared by the CII Economic Research Group.

Reach us at: [email protected]

249-F, Sector 18, Udyog Vihar, Phase IV, Gurgaon- 122015, Haryana, INDIA

Tel: +91-124-4014060-67 • Fax: +91-124-4014080 • Email: [email protected] • Website: www..cii.in

Reach us via our unique Membership Helpline: 00-91-11-435 46244 / 00-91-99104 46244