Embed Size (px)

Citation preview

BOURSE AFRICA CLEAR LIMITED

1

Bourse Africa Clear Ltd

Contents Pages

Corporate data 2

Annual report 3-7

Statement of compliance with the Code of Corporate Governance 8

Certificate from the secretary 9

Independent auditors' report 10 - 14

Statement of financial position 15

Statement o f profit and loss and other comprehensive income 16

Statement of changes in equity 17

Statemen t of cash flows 18

Notes to the financial statements 19- 30

Bourse Africa Clear Ltd

Corporate data

Directors

Registered office

Secretary

Auditors

Bankers

Mr Rinsy Ansalam

Mr Prashant Desai

Mr Soundaram Rajendran

1st Floor, Ebene House

33 Cybercity

Ebene 72201

Republic of Mauritius

Date appointed

14 Febmary 2013

18 February 2014

11 April 2017

Stanhope Corporate and Management Services Ltd

Ebene Tower

52 Cybercity

Ebene 72201

Republic of Mauritius

Grant Thornton

Ebcne Tower

52 Cybercity

Ebene 72201

Republic of Mauritius

Barclays Bank Mauritius Limited

6th Floor, Barclays House

68-68A, Cybercity

Ebene 72201

Republic of Mauritius

SBI (Mauritius) Ltd

6th & 7th Floor, SBI Tower Ivlindspace

Bhumi Park, 45

Ebene 72201, Cybercity

Republic of Mauritius

2

Date resigned

13 April2017

3

Bourse Africa Clear Ltd

Annual report

The directors have the pleasure in submitting their annual report together with the audited financial sta tements of Bourse Africa Clear Ltd, the "Company" or "I3ACL", for the year ended 31 March 2017.

I ncorporation

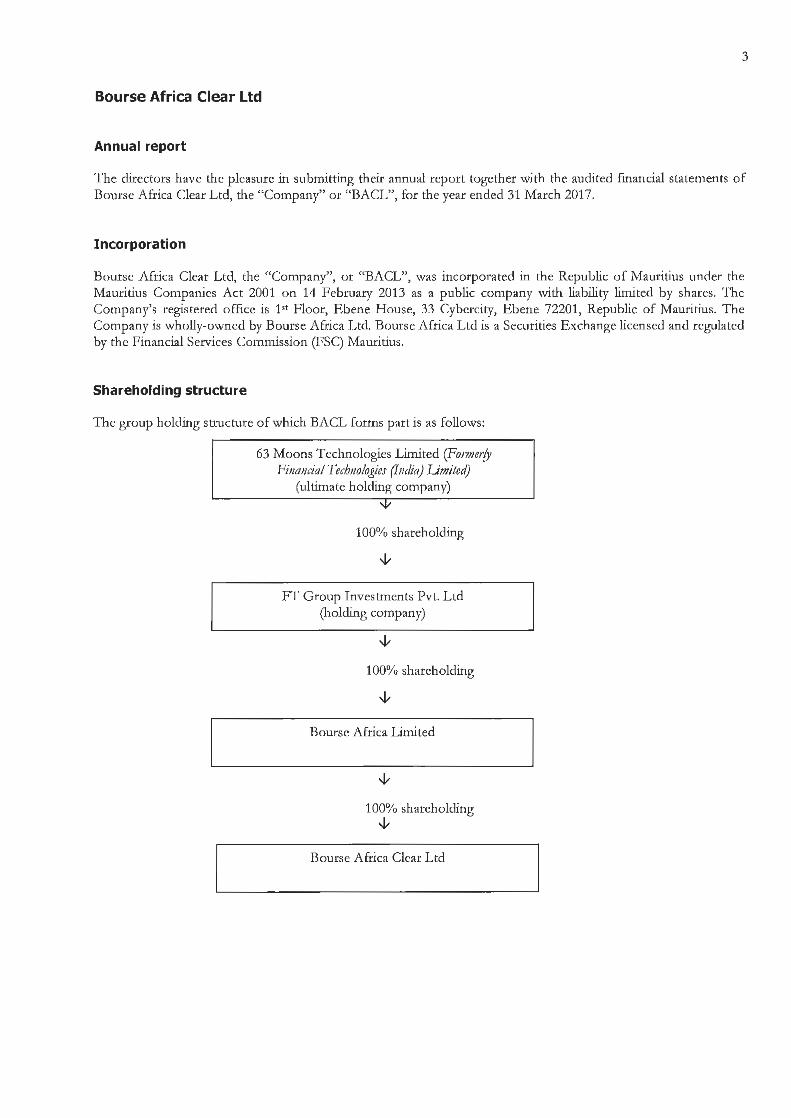

Bourse Africa Clear Ltd, the "Company", or "BACL", was incorporated in the Republic of Mauritius under the Mauritius Companies Act 2001 on 14 l'ebruaq 2013 as a public company with liability limited by shares. The Company's registered office is 1'1 Floor, Ebene House, 33 Cybercity, Ebene 72201, Republic of Mauritius. The Company is wholly-owned by Bourse Africa Ltd. Bourse Africa Ltd is a Securities Exchange licensed and regulated by the Financial Services Commission (FSC) Mauritius.

Shareholding structure

The group holding structure of which BACL forms part is as follows:

63 Moons Technologies Limited (Fonner!J Finandal TedJIIologies (India) Limiteclj

(ultimate holding company)

100% shareholding

F f Group Investments Pvt. Ltd (holding company)

100% shareholding

Bourse Africa Limited

100% shareholding --v

Bourse Africa Clear Ltd

4

Bourse Africa Clear Ltd

Annualreport{Contd)

Principal activity

The principal activity of the Company is to provide clearing and settlement facility to Bourse Africa Ltd. The Company is licensed by the Financial Services Commission of Mauritius, the regulator for non-bank financial services sector. The Company has commenced its operations on 02 September 2013. The non-core areas relating to Human Resources, Legal, Finance, General administration are handled by Bourse Africa Limited.

For the year under review, tl1e Company was dormant.

Results and dividends

The results for the year are as shown in the statement of profit or loss and other comprehensive income.

The directors do not recommend the payment of a dividend for the year under review.

Directors and their profile

The present membership of the Board is as follows:

Mr Rinsy Ansalam Mr Prashant Desai Mr Soundaram Rajendran

Profile of directors

Rinsy Ansalam

Appointed on

14 February 2013 18 February 2014 11 April 2017

Resigned on

13 April 2017

Mr. Rinsy Ansalam has a Post Graduate Diploma in Finance (MBA), has 19 years of experience in the Financial Market, whereby he has acceded to senior management position in various companies. He owns a rich and broad professional background that spans derivatives exchanges, clearing houses, structuring business and financing models, business consulting, information technology and trade finance, contract design for derivatives contracts including energy sector.

Prashant Desai

lv1r. Prashant Desai is an Associate Chartered Accountant. H e is 4'h ranker Graduate in Cost & Work Accountant (all India 4tl1). He has over 21 years of rich experience out of which 10 years of experience is in Investors Relations. He was the founder of Seagull IR Solutions Pvt Ltd which is one of India's leading Investor Relations Companies, which has represented various companies like Financial Technologies, Pipavav Defense, Phoenix Mills, Talwalkars, Provogue, Prozone CSC, Everstone, Dhunseri Petrochem, DQ Entertainment, Supreme Infrasuucture, etc.

Prior to tl1at he was heading IR & Investments at Future Group (Pantaloons Retail, Future Capital Holdings & Future Ventures, Mumbai) and was working as Head of Research RARE Enterprises, a Rakesh Jhunjhunwala partnership, Mumbai. He was also tl1e Board Member in Pantaloons Talwalkars, Future Staples, Future ECommerce, Pan-India Foods and Industree Crafts.

Mr. Desai has tendered his resignation letter on 13 J\pril 2017 after having served tl1e Board for three years.

5

Bourse Africa Clear Ltd

Annual report (Contd)

Profile of directors (Contd)

Mr. Soundaram Rajendran

Mr. Rajendran joined the Board of Directors on 11 April 2017 as a Non-Executive Director. He is the Managing Director and CEO of 63 Moons Technologies Limited. Mr. Rajendran is a post graduate in Commerce and a CAIB, with more than 36 years of rich experience as a senior banking professional and multi-functional experience covering most areas of conunercial banking and Enterprise-wise Risk Management. At the time of superannuation, he was the General Manager of Union Bank of India.

Mr. Rajendran has been MD and CEO of a deemed public company for Data Warehousing for more than four years and has exposure to management o f technology company.

He has extensive experience in Corporate Credit, Treasury and Investment Management, Risk Management, International Banking, Overseas Expansion, Skill Development and T raining, Business Development, Branch banking set-up and operations and Customer Relationship Management, Internal controls, regulatory Compliance and Audits and Training, Research and Knowledge Management.

Statement of directors' responsibilities in respect of the financial statements

Company law requires the directors to prepare financial statements for each financial year which present fairly the financial position financial performance, changes in equity and cash flows of the Company. In preparing those financial statements, the directors are required to:

• Select suitable accounting policies and then apply them consistently;

• Make judgements and estimates that are reasonable and prudent;

• State whether International Financial Reporting Standard have been followed, subject to any material departures disclosed and explained in the financial statements; and

• Prepare the fmancial statements on the going concern basis unless it is inappropriate to presume that the Company will continue in business.

The directors confu:m that they have complied with the above requirements in preparing this financial statements.

The directors arc responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financial position of the Company to enable them to ensure that the financial statements comply with the Mauritius Companies Act 2001. They are also responsible for safeguarding the assets of the Company and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

Directors' service contracts

The directors have no service contract with the Company.

Directors' share interests

The directors have no shares in the Company.

Directors' remuneration

No remunerations and other benefits were paid to the directors of the Company during the year under review.

6

Bourse Africa Clear Ltd

Annual report (Contd)

Corporate governance

The Company being a wholly-owned subsidiaty of Bourse Africa Ltd, all matters pertammg to its corporate governance and audit & risk management are dealt, where applicable, by the parent company viz., Bourse Africa Limited, through its sub-committees.

BACL's Board meetings

During the financial year ended 31 March 2017 the following Directors sat on the Board.

Total number of Meetings held/Written Resolution signed

N arne of Directors

Mr Rinsy Ansalam Mr. Prashant Desai

Category

NED NED

Board Meetings/ Written

Resolution 1/2

1 1

Subsequent to year end, Mr. Prasant Desai resigned as Director on 13 April 2017 and N1r. Soundaram Rajendran joined the Board as a Non-Executive Director on 11 April 2017.

Risk management report

The Company has well-established risk management policies, procedures and systems which are detailed in its Business Rules approved by the FSC. The Business Rules of the Company ensures all aspects related to:

• Membership;

• Capital Adequacy Norms;

• Process and procedures about clearing and settlement;

• Prevention of Settlement failures;

• Settlement guarantee fund;

• Enforceability of its rules; and

• Investor grievance redressal mechanism.

The Audit Committee of the Bourse Africa Limited oversees, monitors and supervises the risk management framework and system of internal controls.

The suitability and effectiveness of the system of the risk management framework and internal controls are audited by the internal auditors. No major and significant exceptions were found by the internal auditors.

No internal audit was performed during the year ended 31 March 2017 since the Company was dormant.

This report complies with the requirements of Section 20(4) of the Securities Act 2005 .

7

Bourse Africa Clear Ltd

Annual report (Contd)

Donations

The Company has not made any donations for the year under review.

Auditors

Fees payable to the auditors, Grant Thornton, for the year under review amounted to USD 3,000 0' AT exclusive) and arc entirely for audit services provided.

On behalf of the Board of Directors

Director

8

Bourse Africa Clear Ltd

Statement of compliance with the Code of Corporate Governance

\Ve, the directors of Bourse Africa Clear Ltd, confum to the best of our knowledge that the Company has complied with all of its obligations and requirements under the Code of Cmporate Governance under Section 75 (3) of the Financial Reporting Act 2004 as described in d1e annual report.

~~ Direct

S'

Director

Date: 1 2 MAY 2017

9

Bourse Africa Clear Ltd

Certificate from the Secretary to the member of Bourse Africa Clear Ltd

We certify, to the best of our knowledge and belief, that we have ftled with the Registrar of Companies all such returns as are required of Bourse Africa Clear Ltd, under the Mauritius Companies Act 2001, in terms of Section 166 (d), during the fmancial year ended 31 March 2017.

orate and Management Services Ltd e t· ary

Registered office:

EbeneTower 52 Cybercity Ebene 72201 Republic of Mauritius

Date: 1 2 MA \' 2017

Grant Thornton 10

Independent auditors' report (Contd) To the member of Bourse Africa Clear Ltd

Report on the Audit of the Financial Statements

Qualified Opinion

We have audited the financial statements of Bourse Africa Clear Ltd, the "Company", which comprise the statement of financial position as at 31 March 2017, and the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies.

In our opinion, except for the effects of the matters described in the Basis for Qualified Opinion section of our report, the accompanying financial statements on pages 15 to 30 give a tm e and fair view of the financial position of the Company as at 31 March 2017, and of its f.tnancial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards and the requirements of the Mauritius Companies Act 2001 and the Financial Reporting Act 2004.

Basis for Qualified Opinion

Licence

The Company holds a Clearing and Settlement Facility Licence ("Licence") issued by the Financial Services Commission (FSC) to provide Clearing and Settlement services to its holding company.

Further to issues affecting the ultimate holding company, a Company incorporated in India, since the f.tnancial year 2014/2015, the FSC had requested the latter to dispose of its stake in the Company, which is held via two intermediate companies. As at date of this report, the disposal has not yet taken place. However, the ultimate holding company being an Indian entity, the completion of the stake sale could be subject to certain regulatmy / judicial approvals in India.

In the meantime, the negotiation has started with a potential buyer for the disposal of the ultimate holding company's stake in the two intermediate companies. However, due to some procedural reasons at the level of the acquirer, the transaction is still not yet completed as at tl1e date of this report.

The FSC is kept informed on the progress of the negotiation and to that effect the directors have requested the FSC to maintain the licence valid until the positive completion of the transaction.

Because of the significance of the licence, we believe that any failure to maintain the validity of the licence will deeply affect the very reason for existence of the Company in its capacity to provide depository, clearing and settlement services.

Going concern

Since incorpora tion the Company relies on the f.tnancial support of its ultimate holding company as its level of activity does not generate sufficient cash to support the operations and to meet capital expenditure.

However, failure to obtain tl1e continuing financial support from the ultimate holding company up to date of its disposal of its stake in the Company or failure to change shareholding within a reasonable period as already requested by tl1e FSC will affect the ability of the Company to continue as a going concern.

Grant Thornton Mauritius is ~ member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. Serv1ces are delivered by the member firms. GTIL and its member firms are not agents of and do not obligate, one another and are not liable for one another's acts or omissions. '

Please see www.gtmu.com for further details.

11

Grant Thornton Independent auditors' report (Contd) To the member of Bourse Africa Clear Ltd

Report on the Audit of the Financial Statements (Contd)

Basis for Qualified Opinion (Contd)

We conducted our audit in accordance with International Standards on Auditing. Our responsibilities under those standards are further described in the Auditors' Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the ethical requirements that arc relevant to our audit of the financial statements, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified opinion.

Information Other than the Financial Statements and Auditors' Report Thereon ("Other Information")

Management is responsible for the Other Information. The Other Information comprises the information included in the Corporate Data, and the Annual Report, but does not include the financial statements and our auditors' report thereon.

Our opinion on the financial statements does not cover the Other Information and, except to the extent otherwise explicitly stated in our report, we do not express any form of assurance conclusion thereon.

In connection with our audit of tl1e financial statements, our responsibility is to read the Other Information and, in doing so, consider whether the Other Information is materially inconsistent with the ftnancial statements or our knowledge obtained in the audit or otl1envise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this Other Information, we are required to report that fact. \Ve have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation of tl1e ftnancial statements in accordance with Intemational Financial Reporting Standards and the requirements o f the Mauritius Companies Act 2001 and the Financial Reporting Act 2004, and for such internal control as management determines is necessaty to enable the preparation of the financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company's ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or have no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company's ftnancial reporting process.

Grant Thornton Mauritius is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. Services are delivered by the member firms. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another's acts or omissions.

Please see www.gtmu.com for further details.

12

Grant Thornton Independent auditors' report (Contd) To the member of Bourse Africa Clear Ltd

Report on the Audit of the Financial Statements (Contd)

Auditors' Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material rrusstatement, whether due to fraud or error, and to issue an auditors' report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with International Standards of Auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the econorruc decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with International Standards of Auditing, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material rrusstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material rrusstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional orrussions, rrusrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that arc appropriate in the circumstances, but not for the putposc of expressing an opinion on the effectiveness of the Company's internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

• Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company's ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor's report to the related disclosures in the fmancial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors' report. However, future events or conditions may cause the Company to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the fmancial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Grant Thornton Mauritius is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. Services are delivered by the member firms. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another's acts or omissions.

Please see www.gtmu.com for further details.

13

Grant Thornton Independent auditors' report (Contd) To the member of Bourse Africa Clear Ltd

Report on the Audit of the Financial Statements (Contd)

Report on Other Legal and Regulatory Requirements

(a) Matm'tius Companies Ad 2001

In accordance with the requirements of the Mauritius Companies Act 2001, we report as follows:

• we have no relationship with, or any interests in, the Company other than in our capacity as auditors;

• we have obtained all the information and explanations we have required; and

• in our opinion, proper accounting records have been kept by the Company as far as it appears from our examination of those records.

(b) FtiJanda/ Repo11ingAtt 2004

T he directors are responsible for preparing the Corporate Governance Repor t. O ur responsibility is to repor t on the extent of compliance with the Code of Cmporate Governance as disclosed in the annual report and on whether the disclosure is consistent with the requirements of the Code.

In our opinion, the disclosure in the annual report is consistent with the requirements of the Code.

{t) Smoities Ad 2005

The directors arc responsible for preparing the Risk Management Report. O ur responsibility is to report on the extent of compliance with Section 20(4) of the Securities Act 2005 as disclosed in the annual report.

In our opinion, the disclosure in the annual report is consistent with the requiremen ts of Section 20(4) of the Securities Act 2005.

Grant Thornton Mauritius is a member fi rm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. Services are delivered by the member firms. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another's acts or omissions.

Please see www.gtmu.com for further details.

14

Grant Thornton Independent auditors' report (Contd) To the member of Bourse Africa Clear Ltd

Report on the Audit of the Financial Statements (Contd)

Other matter

Our report is made solely to the member of the Company as a body in accordance with Section 205 of the Mauritius Companies Act 2001. Our audit work has been undertaken so that we might state to the Company's member those matters we are required to state to it in an auditors' report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company's member as a body, for our audit work, for this report, or for the opinion we have formed.

Grant Thornton Chartered Accountants

Date: 1 2 MAY 2017

Ebene 72201, Republic ofMauririus

Grant Thornton Mauritius is a member firm of Grant Thornton International Ltd (GTIU. GTIL and the member firms are not a worldwide partnership. Services are delivered by the member firms. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another's acts or omissions.

Please see www.gtmu.com for further details.

Bourse Africa Clear Ltd

Statement of financial position as at 31 March

Assets

Current assets

Prepayments

Cash and cash equivalents

Total assets

Equity and liabilities

Stated capital

Accumulated losses

Total equity

Current liabilities

Payables and accruals

Total liabilities

Total equity and liabilities

Notes

7

8

9

2017

uso

3,475

480,733

484,208

510,312

{111,434)

398,878

85,330

85,330

484,208

1 2 MAY 2017 Approved by the Board of Directors on - - - ------and signed on its behalf by:

Director Director

The notes on pages 19 to 30 form an integral part of these financial statements.

15

2016

uso

3,671

664,368

668,039

510,312

(90,400)

419,912

248,127

248,127

668,039

Bourse Africa Clear Ltd

Statement of comprehensive March

Income

Administrative expenses

Finance income

other financial gain

Loss before taxation

Tax expense

Loss for the year

Other comprehensive income:

profit 1ncome

Items that wt71 not be reclassified subsequently to profit or loss

Items that will be reclassified subsequently to profit or loss

Other comprehensive income for the year, net of tax

Total comprehensive loss for the year

16

and loss and other for the year ended 31

Notes

11

10

12

2017

USD

(22,787)

1,814

(61)

(21,034)

(21,034)

(21,034)

2016

USD

(20,818)

5,103

153

(15,562)

(15,562)

(15,562)

T he notes on pages 19 to 30 form an integral part of these financial statements .

17

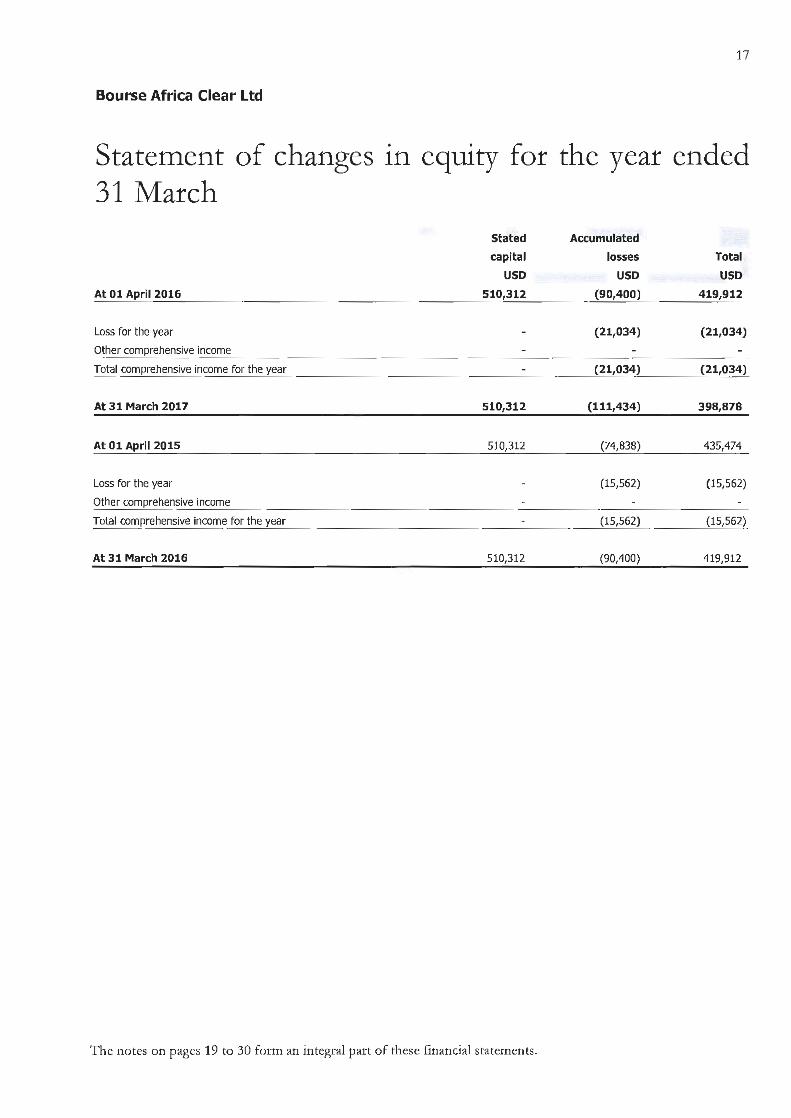

Bourse Africa Clear Ltd

Statement of changes in equity for the year ended 31 March

At 01 April 2016

Loss for the year

Other comprehensive income

Total comprehensive income for the year

At 31 March 2017

At 01 April 2015

Loss for the year

Other comprehensive income

Total comprehensive income for the year

At 31 March 2016

Stated

capital

USD 510,312

510,312

510,312

510,312

T he notes on pages 19 to 30 form an integral part of these financial statements.

Accumulated

losses Total

USD USD (90,400) 419,912

(21,034) (21,034)

(21,034) (21,034)

(111,434) 398,878

(74,838) 435,474

(15,562) (15,562)

(15,562) (15,562)

(90,400) 419,912

Bourse Africa Clear Ltd

Statement 31 March

Operating activities

Loss before tax

Adjustment:

Interest income

Net changes in working capital:

of cash

Decrease in prepayments

Decrease in payables and accruals

Net cash used in operating activities

Investing activities

Interest received

Net cash generated from investing activities

Net change in cash and cash equivalents

Cash and cash equivalents at start of the year

Cash and cash equivalents at end of the year

Cash and cash equivalents made up of:

Cash and bank balances (Note 7)

flows for the

The notes on pages 19 to 30 form an integral part of these financial statements.

year

2017

USD

(21,034)

(1,814)

196

(162,797)

(185,449)

1,814

1,814

(183,635)

664,368

480,733

480,733

18

ended

2016

USD

(15,562)

(5,103)

660

(405,803)

(425,808)

5,103

5,103

(420,705)

1,085,073

664,368

664,368

19

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

1. General information and statement of compliance with International Financial Reporting Standards

Bourse Africa Clear Ltd, the "Company", was incorporated in the Republic of Mauritius under the Mauritius Companies Act 2001 on 14 Februaq 2013 as a public company with liability limited by shares. The Company's registered o ffice is 1st Floor, Ebene House, 33 Cybercity, Ebene 72201, Republic of Mauritius.

The principal activity of the Company is to provide depository, clearing and settlement senrices to its holding company, Bourse Africa Limited. The Company is licensed by tl1e financial Services Commission of Mauritius, tl1e regulator for non-bank financial services sector.

The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as issued by tl1e International Accounting Standards Board (IASB).

2 Application of new and revised IFRS

2.1 New and revised standards that are effective for the year beginning on 01 April 2016

In the current year, the following new and revised standards issued by the International Accounting Standards Board ("IASB") became mandatoty for tl1e first time adoption for tl1e financial year beginning on 01 April 2016:

IAS 16 and IAS 38, Clarification of Acceptable Methods of Depreciation and Amortisation (Amendments to IAS 16 and IAS 38)

These amendments clarify that the use of revenue-based methods to calcula te the depreciation of an asset is no t appropriate because revenue generated by an activity that includes the use of an asset generally reflects factors other than tl1e consumption o f the economic benefits embodied in the asset.

IAS 16 and IAS 41, Agriculture: Bearer Plants (Amendments to IAS 16 and IAS 41)

These amendments change the reporting for bearer plants, such as grape vines, tubber trees and oil palms. Bearer plants should be accounted for in tl1e same way as property, plant and equipment because their operation is sinlliar to that of manufacturing.

IAS 27, Equity Method in Separate Financial Statements (Amendments to IAS 27)

The amendment allows en tities to use the equity method to account for investments in subsidiaries, joint ventures and associates in their separate financial statements.

IFRS 11, Accounting of Acquisitions of Interests in Joint Operations (Amendments to IFRS 11)

T his amendment provides new guidance on how to account for the acquisition of an interest in a joint venture operation that constitutes a business. T he amendments require an investor to apply the principles of business combination accounting when it acquires an interest in a joint operation that constitutes a 'business'.

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

2 Application of new and revised IFRS (Contd)

2.1 New and revised standards that are effective for the year beg inning on 01 April2016 (Contd)

IFRS 14, Regulatory D eferral Accounts

20

This standard permits first-time adopters of IFRS to continue to recognise amounts related to rate regulation in accordance with their previous GAAP requirements when they adopt IFRS. However, to enhance comparability with entities that already apply IFRS and do not recognise such amounts, the standard requires that the effect of rate regulation must be presented separately from other items.

IFRS 10, IFRS 12 and IAS 28, Investment Entities: Applying the Consolidation Exception (Amendments to IFRS 10, IFRS 12 and IAS 28)

The amendments address issues that have arisen in the con text of applying the consolidation exception for investment entities.

IAS 1, Disclosure Initiative (Amendments to IAS 1 Presentation of Financial Statements)

The amendments represent the firs t authoritative output from the IASB's Disclosure Initiative project. The disclosure initiative itself is in part a reaction to the growing clamour over disclosure overload in financial statements. It consists of a number of projects, both short and medium-term, and ongoing activities that explore how presentation and disclosure principles and requirements in existing standards can be improved.

Various, Annual Improvements to IFRS 2012-2014 Cycle

These improvements include amendments to IFRS 5: Non-current Assets Held for Sale and Discontinued Operations, IFRS 7: Financial Instruments: Disclosures, lAS 19: Employee Benefits and lAS 34: Interim Financial Reporting.

The directors have assessed the impact of the new and revised standards and concluded that none of these standards have a significant impact on the disclosures of these financial statements.

2.2 Standards, amendments to existing s tandards and interpretations tha t are not yet effective and have not been adopted early by the Company

At the date of authorisation of these financial statements, certain new standards, amendments to existing standards and one interpretation have been published by the IASB but not yet effective, and have not been adopted early by the Company.

Management anticipates that all of the relevant pronouncements as applicable to the Company's activity will be adopted in the Company's accounting policies for the first period beginning after the effective date of the pronouncements. Information on new standards, amendments and interpretation is provided below.

IAS 12, R ecognition of Deferred Tax Assets for Unrealised Losses (Amendments to IAS 12)

T he focus of the amendments to lAS 12 is to clarify how to account for deferred tax assets related to debt instruments measured at fair value, particularly where changes in the market interest rate decrease the fair value of a debt insuument below cost.

IAS 7, Disclosure Initiative (Amendments to IAS 7)

The amendments are designed to improve the quality of information provided to users of financial statements about changes in an entity's debt and related cash flows (and non-cash changes).

21

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

2 Application of new and revised IFRS (Contd)

2.2 Standards, amendments to existing standards and interpretations that are not yet effective and have not been adopted early by the Company (Contd)

IFRS 15, Revenue from Contracts with Customers

This is the converged standard on revenue recognition. It replaces lAS 11, 'Constmction contracts', l AS 18, 'Revenue' and related interpretations.

IFRS 9 Financial instruments (2014)

The complete version of IFRS 9 replaces most of the guidance in lAS 39. IFRS 9 retains but simplifies the mixed measurement model and establishes three primaty measurement categories for financial assets: amortised cost, fair value through other comprehensive income and fair value through profit and loss.

IFRS 4, Applying IFRS 9 Financial Instruments with IFRS 4 Insurance Contracts (Amendments to IFRS4)

The amendments in Applying IPRS 9 'Financial Instruments' with Il'RS 4 'Insurance Contracts' (Amendments to IFRS 4) provide two options for entities that issue insurance contracts within the scope of IFRS 4.

IFRS 2, Classification and Measurement of Share-based Payment Transactions (Amendments to IFRS2)

The amendments bring clarification on the following matters:

• the accounting for cash-settled share-based payment transactions that include a performance condition; • the classification of share-based payment transactions with net settlement features; and

• tl1e accounting for modifications of share-based payment transactions from cash-settled to equitysettled.

IAS 40, Transfer of Investment Property (Amendments to IAS 40)

Under these amendments an entity shall transfer a property to, or from, investment property when, and only when, there is evidence of a change in use. A change of use occurs if property meets, or ceases to meet, the definition of investment property. A change in management's intentions for the use of a property by itself does not constitute evidence of a change in use.

IFRS 16, Leases

The new standard requires lessees to account for leases 'on-balance sheet' by recognising a 'right of use' asset and a lease liability. It will affect most companies that report under IFRS and are involved in leasing, and will have a substantial impact on the financial statements of lessees of property with high value equipment.

IFRIC 22, Foreign Currency Transactions and Advance Consideration

IFRIC 22 clarifies the accounting for transactions that include the receipt or payment of advance consideration in a foreign currency.

Management has yet to assess the impact of the above standards, amendments and intetpretation on the Company's fmancial statements.

22

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

3. Summary of accounting policies

3.1 Overall considerations

The financial statements have been prepared using the significant accounting policies and measurement bases summarised below.

3.2 Financial instruments

Recognition, initial measurement and derecognition

Financial assets and financial liabilities are recognised when the Company becomes a party to the contractual provisions of the financial instmment and are measured initially at fair value adjusted by transactions costs, except for those carried at fair value through profit or loss which are measured initially at fair value. Subsequent measurement of financial assets and financial liabilities are described below.

Financial assets are derecognised when the contractual rights to the cash flows from the financial asset expire, or when the financial asset and all substantial risks and rewards are transferred. A financial liability is derecognised when it is extinguished, discharged, cancelled or expires.

Classification and subsequent measurement of financial assets

For the p01pose of subsequent measurement, the Company's fmancial assets are classified into loans and receivables.

All financial assets of the Company are subject to review for impairment at least at each reporting date to identify whether there is any objective evidence that a financial asset or a Company of financial assets is impaired. Different criteria to determine impairment are applied for each category of financial assets.

All income and expenses relating to financial assets arc recognised in statement of profit or loss and other comprehensive income.

Loans and !Ueivab/es

Loans and receivables are non-derivative financial assets with foced or determinable payments that are not quoted in an active market. After initial recognition, these arc measured at amortised cost using the effective interest method, less pwvision for impairment. Discounting is omitted where the effect of discounting is immaterial. The Company's cash and cash equivalents fall into this category of fmancial insuuments.

Classification and subsequent measurement of financial liabilities

The Company's financial liabilities include payables and accruals.

financial liabilities are measured subsequently at amortised cost using the effective interest method. All interest-related charges on financial liabilities are included \vithin 'finance costs'.

23

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.2 Financial instruments (Contd)

Classification and subsequent measurement of financial liabilities (Contd)

The category determines subsequent measurement and whether any resulting mcome and expense 1s recognised in profit or loss or in other comprehensive income.

All income and expenses relating to fmancial assets that are recognised in statement of profit or loss and other comprehensive income arc presented with finance income and finance costs.

Offsetting financial instruments

Financial assets and liabilities are offset and the net amount reported in the statement of financial position when there is a legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis or realise the asset and settle the liability simultaneously.

3 .3 Foreign currency

Functional and presentation currency

T he financial statements are presented in United States Dollars (USD), which is also the functional currency of tl1e Company.

Foreign currency transactions and balances

Foreign currency transactions are translated into the functional currency of the Company, using the exchange rates prevailing at the dates of the transactions (spot exchange rate). Foreign exchange gains and losses resulting from the settlement of such transactions and from the re-measurement o f monetary items denominated in foreign currency at year-end exchange rates are recognised in the statement of profit or loss and other comprehensive income.

Non-monetary items are not retranslated at year-end and are measured at historical cost (translated using the exchange rates at the transaction date), except for non-monetaty items measured at fair value which are translated using the exchange rates at the date when fair value was determined.

3.4 Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and cash at bank, togetl1er with other short term, highly liquid investments maturing within 90 days from the date of acquisition tl1at are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value.

3.5 Equity and reserves

Stated capital represents the nominal values of shares that have been issued.

Accumulated losses include all current and prior years' results.

24

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.6 Revenue recognition

Revenue is recognised upon performance of services.

Interest income is recorded on the accrual basis unless collectability is in doubt.

3.7 Operating expenses

O perating expenses are recognised in the statement o f profit or loss and other comprehensive income upon utilisation of the service or at the date of their origin.

3.8 Taxation

Tax expense recognised in the statement of profit or loss and other comprehensive income comprises the sum of deferred tax and current tax not recognised in other comprehensive income or directly in equity.

Current income tax assets and/ or liabilities comprise those obligations to, or claims from, fiscal authorities relating to the current or prior reporting periods, that are unpaid at the reporting date. Current tax is payable on taxable profit, which differs from profit or loss in the financial statements. Calculation of current tax is based on tax rates and tax laws that have been enacted or substantively enacted by the end of tl1e reporting date.

Deferred income taxes are calculated using the liability method on temporary differences between the can ying amounts of assets and liabilities and their tax bases.

3.9 Provisions

Provisions are recognised when the Company has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and a reliable estimate of the amount of tl1e obligation can be made. At the time of the effective payment, the provision is deducted from the corresponding expenses. All known risks at reporting date are reviewed in detail and provision is made where necessary.

3.10 Related p arties

A related party is a person or company where tl1at person or company has control or joint control of the reporting company; has significant influence over the reporting company; or is a member of the key management personnel of the reporting company or of a parent of the reporting company.

3.11 Comparatives

\'(!here necessaty, comparative figures have been adjusted to conform to changes in presentation in the current year.

3.12 Significant m anagement judgem ents in applying accounting policies and estimation uncertainty

\'(!hen preparing the fmancial statements, management undertakes a number of judgements, estimates and assumptions about the recognition and measurement of assets, liabilities, income and expenses.

25

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.12 Significant management judgements in applying accounting policies and estimation uncertainty (Contd)

Significant management judgement

The following are significant management judgements in applying the accounting policies of the Company that have the most significant effect on the financial statements.

Determination of fimdional mmnry

The determination of the functional currency of the Company is critical since recording of transactions and exchange differences arising therefrom are dependent on the functional currency selected. The directors have considered those factors and have determined that the functional currency of the Company is the USD.

4. Financial instrument risk

Risk m anagement objectives and policies

The Company is exposed to vat:ious risks in relation to fmancial instmment risk. The main types of risks are market risk (including currency risk and interest rate risk), credit risk and liquidity risk.

The Company's risks are managed at the level of the Board of Directors.

The most significant financial risks to which the Company is exposed are desctibed below.

4.1 Market risk analysis

Foreign currency sensitivity

The Company is not exposed to any currency risk as most of its fmanc:ial assets and financial liabilities are denomina ted in the USD, its functional currency.

The currency profile of the Company's financial assets and liabilities is summarised as follows:

Financial Financial Financial Financial

assets liabilities assets liabilities 2017 2017 2016 2016

USD USD USD USD Mauritian Rupee (MUR) 8,534 8,624

United States Dollar (USD) 472,199 5,545 655,744 68,127

Total 480,733 5,545 664,368 68,127

At the reporting date, the Company has fmancialliabilities denominated in USD. However, any change of MUR/ USD exchange rate, will not have a significant impact on equity.

Interest rate sensitivity

The Company has interest bearing financial assets in the form of cash at bank. T he impact o f changes in interest rates on the interest income derived from these cash at bank :is not significant.

26

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

4. Financial instrument risk (Contd)

Risk management objectives and policies (Contd)

4.2 Credit risk analysis

Credit risk refers to the risk that countetparty will default on its obligations resulting in financial loss to the Company. The Company has, as far as it is practicable, significantly tightened its credit policy so as to deal with counterparties whom it believes are creditworthy in order to reduce the risk of financial loss from defaults. The Company's exposure and the credit ratings of its counterparties are continuously monitored.

The Company's exposure to credit risk is limited to the carrying amount of financial assets recognised at the reporting date, as summarised below:

Current assets

Cash and cash equivalents

Total

2017

USD

480,733

480,733

2016

USD

664,368

664,368

The Company does not have significant credit risk exposure to any single counterparty or group of counterparties having similar characteristics.

The credit risk for the bank balances is considered negligible, since the countetparties are reputable banks with high guality external credit ratings.

The Company's bank balances have not been pledged as collateral or for other credit enhancements.

4.3 Liquidity risk analysis

LiguidiLy risk is the risk that the Company will not be able to meet its financial obligations as they fa ll due.

The Company's approach to managing liguidity risk is to ensure, as far as possible, that it will always have sufficient liguidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Company's reputation.

The Company manages its liguidity needs by carefully monitoring its cash outflows due in day-to-day business. The Company relies on the financial support of its holding company to meet its commitments and operating expenses.

The following are the contractual maturities of financial liabilities, including interest payments where applicable.

Carrying Contractual Less than

31 March 2017 amount cash flows one year

USD USD USD Payables and accruals 5,545 5,545 5,545

Total 5,545 5,545 5,545

27

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

4. Financial instrument risk (Contd)

Risk management objectives and policies (Contd)

4.3 Liquidity risk analysis (Contd)

Carrying Contractual Less than

31 March 2016 amount cash flows one year

USD USD USD Payables and accruals 68,127 68,127 68,127

Total 68,127 68,127 68,127

5. Fair value measurement

.Fair valtte measurement o/ flnamial inJtrtmtents

The Company's financial assets and financial liabilities are measured at their carrymg amounts which approximate their fair values .

.Fair value measurement qf nonjinamial assets

The Company's non-fmancial assets consist of only prepayments and its non-financial liabilities consist of only members' deposits.

For both non-financial assets and non-financial liabilities, fair value measurement is not applicable since these are not measured at fair value on a recurring or non-recurring basis in the statement of fmancial position.

6. Capital m anagement policies and procedures

The Company's capital management by pricing services commensurately with the level of risk.

The Company's capital is managed at the level of the ultimate holding company and the capital sttucture is adjusted or maintained by the issue of new shares.

The Company is required to maintain an unimpaired capital in accordance with the Securities Act 2005. At 31 March 2017, the capital of the Company was USD 398,878. Hence the Company meets the unimpaired capital requirement of the Securities Act 2005.

The Company was not geared at 31 March 2017 as it does not have any external borrowings.

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

7. Cash and cash equivalents

Cash at bank:

USD

MUR

Total

8. Stated capital

Number

Equity shares:

Ordinary shares of USD 0.10 each 5,000,000

Ordinary shares at MUR 303,400 100,000

Total 5,100,000

9. Payables and accruals

Due to the holding company

Accruals

Deposits from members (Note below)

Total

2017

USD

472,199

8,534

480,733

2017

USD

500,000

10,312

510,312

2017

USD 2,096

3,449

79,785

85,330

28

2016

USD

655,744

8,624

664,368

2016

USD

500,000

10,312

510,312

2016

USD 64,386

3,741

180,000

248,127

The Company has financial risk management policies in place to ensure that all payables are paid within the credit timeframe.

'n1e canying amounts of payables are considered to be a reasonable approximation of the fair values.

The deposits from members are for the Settlement Guaranteed Fund and are refundable.

10. F inance incom e

Interest on fixed deposits

2017

USD 1,814

2016

USD 5,103

29

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

11.

12.

12.1

12.2

Administrative expenses

2017 2016

USD USD Registration fees 14,625 15,439

Professional fees 7,457 4,902

Others 705 477

Total 22,787 20,818

Taxation

Income tax expense

The Company is liable to income tax at the rate of 15% and at 31 March 2017, it had no income tax liability due to tax losses of USD 110,970 (31 March 2016: USD 89,936) carried forward.

The income tax on the Company's loss before tax differs from the theoretical amount that would arise using the effective rate of the Company as follows:

2017 2016

USD USD

Loss before tax (21,034) (15,562)

Tax calculated at the rate of 15% (3,155) (2,334)

Deferred tax asset not recognised 3,155 2,334

At end of the year

Deferred taxation

Deferred income tax is calculated on all temporaty differences under the liability method at the rate of 15%. At 31 March 2017, no deferred tax asset has been recognised in respect of the tax losses carried forward as it is not probable that future taxable profits will be available against which the unused tax losses can be utilised.

13 . Related party transaction

Dw1ng the year ended 31 March 2017, the Company had transactions with a related party. The nature, volume of transactions and balance are as follows:

Credit Credit

Nature of Nature of Volume of balance at balance at

relationship transactions transactions 31 March 2017 31 March 2016

USD USD USD

Holding company Loan 62,290 2,096 64,386

The terms and conditions are as shown in Note 9 to the financial statements.

30

Bourse Africa Clear Ltd

Notes to the financial statements For the year ended 31 March 2017

14. Holding and ultimate holding companies

At 31 March 2017, the directors regard Bourse Africa Limited, a company incorporated in the Republic of Mauritius, as the Company's immediate holding company and 63 Moons Technologies (India) Limited (formerly Financial Technologies (India) Limited), a listed company incorporated in the Republic of India, as the Company's ultimate holding company.