Embed Size (px)

Citation preview

CENTURY 21 ACCOUNTING © Thomson/South-Western

LESSON 1-2LESSON 1-2

How Business Activities Change the Accounting Equation

Original created by M.C. McLaughlin, Thomson/South-WesternModified by Deborah L. Burns, Johnston County Schools, West Johnston High School

CENTURY 21 ACCOUNTING © Thomson/South-Western

2

LESSON 1-2

What are Business Activities?What are Business Activities?

Business activities change the amounts in the accounting equation.

Transaction – a business activity that changes assets, liabilities, or owner’s equity

Unit of Measurement – business transactions are stated in numbers that have common values

CENTURY 21 ACCOUNTING © Thomson/South-Western

3

LESSON 1-2

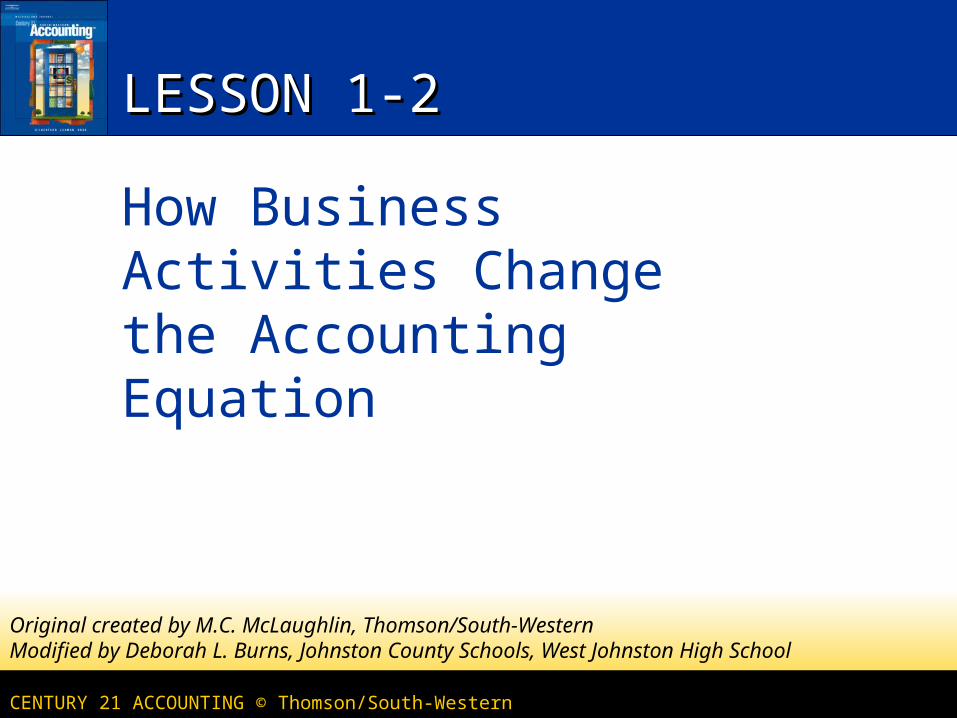

REVIEW OF TYPES OF REVIEW OF TYPES OF ACCOUNTSACCOUNTS

ASSETS Cash Supplies Accounts Receivable Prepaid Insurance Buildings Equipment

LIABILITIES Accounts Payable

(A/P) Mortgage Payable Notes Payable (N/P)

OWNER’S EQUITY (O/E) Capital

CENTURY 21 ACCOUNTING © Thomson/South-Western

4

LESSON 1-2

About AccountsAbout Accounts

Account – a record summarizing all the information pertaining to a single item in the accounting equation

Account Title – the name given to an accountAccount Balance – the amount in an account Capital – the account used to summarize the

owner’s equity in a business

CENTURY 21 ACCOUNTING © Thomson/South-Western

5

LESSON 1-2

The Accounting EquationThe Accounting Equation

ASSETS = LIABILITIES + OWNERS EQUITY

You must always keep the accounting equation in balance.

CENTURY 21 ACCOUNTING © Thomson/South-Western

6

LESSON 1-2

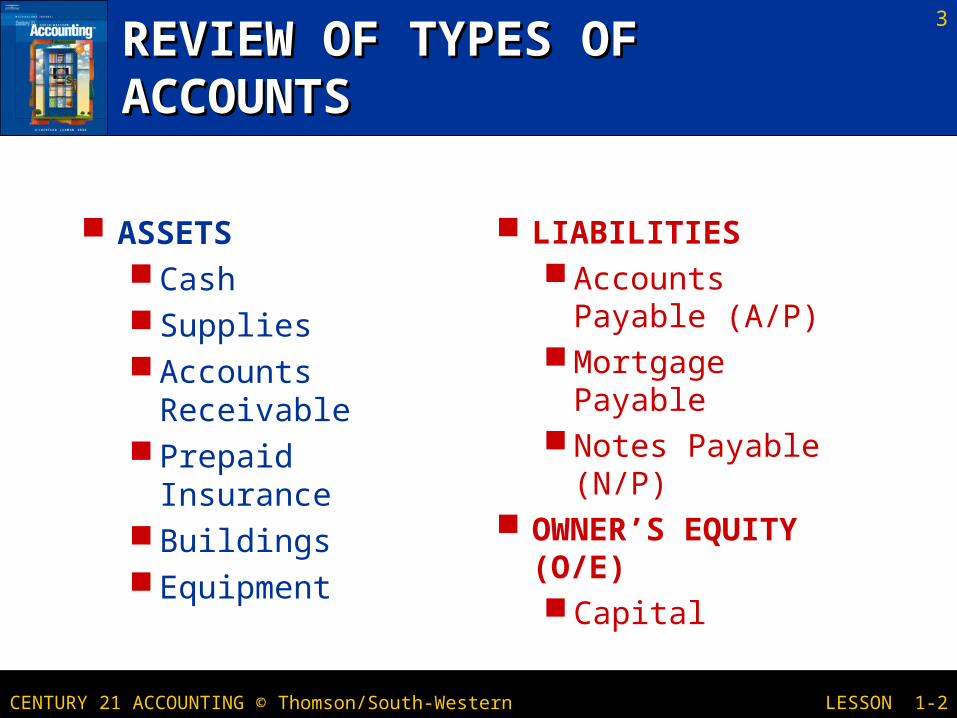

RECEIVING CASH FROM THE OWNERRECEIVING CASH FROM THE OWNER

We are receiving cash which is an asset. It is increasing.

The owner is investing in the business so they are increasing their equity (owners equity) in the business.

Analyze the transaction: What accounts will the transaction affect?

CENTURY 21 ACCOUNTING © Thomson/South-Western

7

LESSON 1-2

RECEIVING CASHRECEIVING CASH

Transaction 1 August 1. Received cash from owner as an investment, $5,000.00.

page 10

CENTURY 21 ACCOUNTING © Thomson/South-Western

8

LESSON 1-2

PAYING CASH FOR SUPPLIESPAYING CASH FOR SUPPLIES

We are paying cash which is an asset. It is decreasing.

We are buying supplies which are assets. Our supplies are increasing.

Analyze the transaction: What accounts will the transaction affect?

CENTURY 21 ACCOUNTING © Thomson/South-Western

9

LESSON 1-2

PAYING CASHPAYING CASH

Transaction 2 August 3. Paid cash for supplies, $275.00.

Transaction 3 August 4. Paid cash for insurance, $1,200.00.

page 11

CENTURY 21 ACCOUNTING © Thomson/South-Western

10

LESSON 1-2

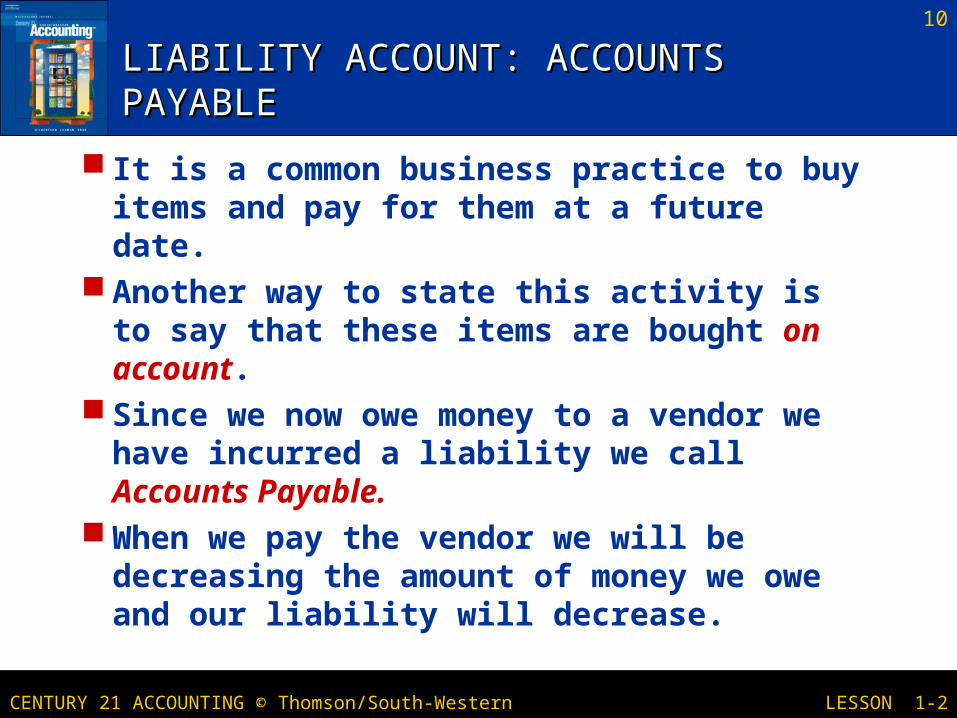

LIABILITY ACCOUNT: ACCOUNTS LIABILITY ACCOUNT: ACCOUNTS PAYABLEPAYABLE

It is a common business practice to buy items and pay for them at a future date.

Another way to state this activity is to say that these items are bought on account.

Since we now owe money to a vendor we have incurred a liability we call Accounts Payable.

When we pay the vendor we will be decreasing the amount of money we owe and our liability will decrease.

CENTURY 21 ACCOUNTING © Thomson/South-Western

11

LESSON 1-2

TRANSACTIONS ON ACCOUNTTRANSACTIONS ON ACCOUNT

Transaction 4 August 7. Bought supplies on account from Supply Depot, $500.00.

Transaction 5 August 11. Paid cash on account to Supply Depot, $300.00.

page 12

CENTURY 21 ACCOUNTING © Thomson/South-Western

12

LESSON 1-2

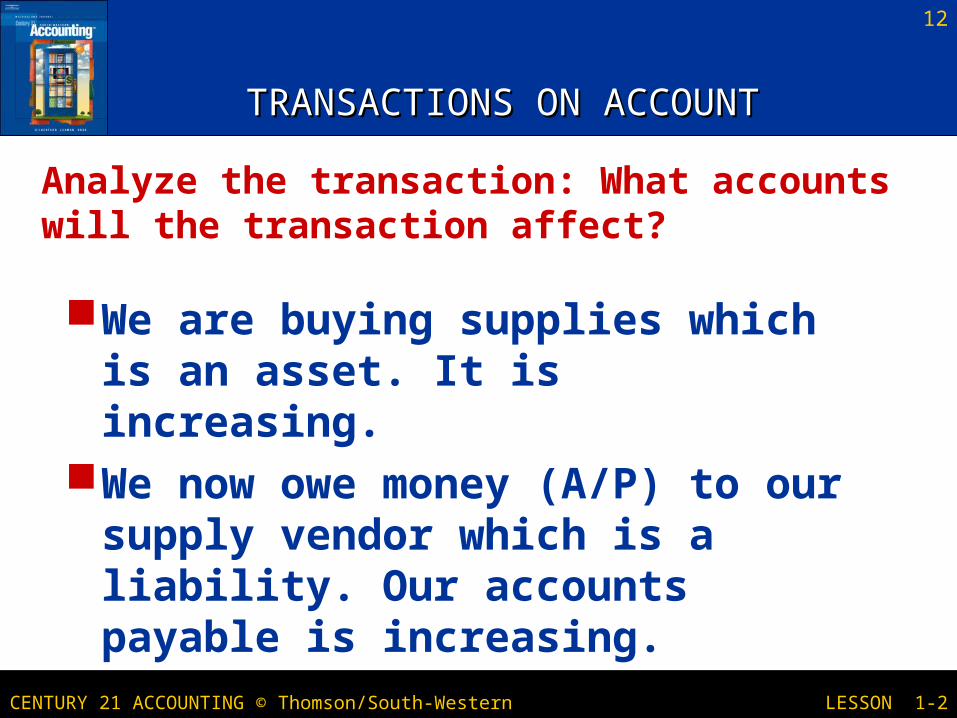

TRANSACTIONS ON ACCOUNTTRANSACTIONS ON ACCOUNT

We are buying supplies which is an asset. It is increasing.

We now owe money (A/P) to our supply vendor which is a liability. Our accounts payable is increasing.

Analyze the transaction: What accounts will the transaction affect?

CENTURY 21 ACCOUNTING © Thomson/South-Western

13

LESSON 1-2

TERMS REVIEWTERMS REVIEW

transaction account account title account balance capital

page 13