Embed Size (px)

Citation preview

abcGlobal Research

Investment thesis: CKI is a high-quality company but, in our view, is currently fully

valued. We believe earnings have a high level of certainty because they are from businesses

operating under transparent, stable and predictable regulations. As with bonds, we expect

outperformance to be challenging in a rising interest rate environment.

Regulatory accounts show CKI is doing well: Since the UK assets are reported as

associates by CKI, there is a high level of opaqueness to the earnings make-up of these

assets. We have reviewed the recently released full financial statements of CKI’s UK

associates for the year ending March 2013. The full set of accounts shows an increase in

margins and cash flows for UK Power Networks (UKPN). The operating cost to turnover

ratio has declined, and working capital management has been strong. Northern Gas

Networks (NGN) and Northumbrian Water Group (NWG) continue to have stable growth

and margins while there is a scope for improvement at Wales & West Utilities (WWU),

which was acquired in 2012. The regulatory accounts show that tax advantages in the UK

are achieved mainly through UKPN, with an effective tax rate of 2% in FY13 (if this were

to change to the statutory rate of 24%, the impact on CKI’s 2012 net profit would be -5%).

Forensic accounting: The associate earnings reported under Hong Kong Financial

Reporting Standards (HK FRS) are substantially higher than the regulatory earnings

reported under UK GAAP, mainly due to accounting differences. This accounting

difference is a key reason why the dividend payout from associates was low, at 32%, in

FY12 (we forecast it will increase to 35% in FY13e on improving cash flow) and the cash

coverage of CKI’s dividend was low, at 1.2x, while earnings coverage was high, at 2.5x.

N with a target price of HKD53: We maintain our sum-of-the-parts target price of

HKD53 for CKI, based on a premium to the regulated asset values (RAVs) for the UK

(37% of TP) and Australia (11% of TP) assets. Upside risks: a large, value-accretive

acquisition and dividend surprises. Downside risk: regulatory resets that reduce the

allowed return on equity.

Cheung Kong Infra (1038 HK)

N: Dissection of UK regulatory assets

Recently released regulatory accounts show improvement in margins and cash flows for UKPN

NGN and NWG continue to have stable growth and margins while there is scope for improvement at WWU

Remain Neutral with a SOTP-based TP of HKD53

Natural Resources & Energy Electric Utilities Equity – Hong Kong

Company report

Index^ HANG SENG INDEXIndex level 22,974RIC 1038.HKBloomberg 1038 HK

Source: HSBC

Neutral Target price (HKD) 53.00 Share price (HKD) 53.80 Forecast dividend yield (%) 3.7 Potential return (%) 2.2

Note: Potential return equals the percentage difference between the current share price and the target price, plus the forecast dividend yield

Dec 2012 a 2013 e 2014 e

HSBC EPS 3.80 4.14 4.06 HSBC PE 14.2 13.0 13.2

Performance 1M 3M 12M

Absolute (%) 3.1 0.9 15.7 Relative^ (%) 1.5 -8.4 5.8

Enterprise value (HKDm) 61,804Free float (%) 23Market cap (USDm) 17,315Market cap (HKDm) 134,276

Source: HSBC

9 October 2013

Jenny Cosgrove* Head of Utilities & Alternative Energy Research, Asia Pacific The Hongkong and Shanghai Banking Corporation Limited +852 2996 6619 [email protected]

Gloria Ho* Analyst The Hongkong and Shanghai Banking Corporation Limited +852 2996 6941 [email protected]

Ankit Gupta* Associate Bangalore View HSBC Global Research at: http://www.research.hsbc.com

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/qualified pursuant to FINRA regulations

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

Disclaimer & Disclosures This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

2

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

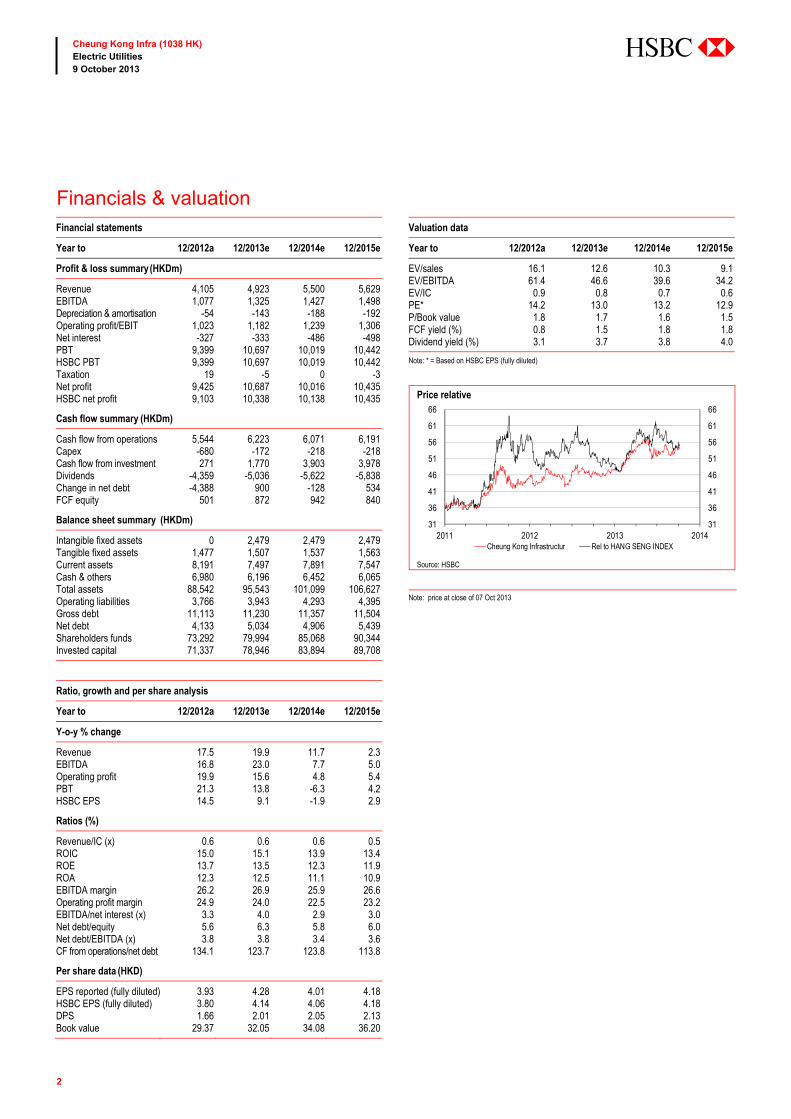

Financials & valuation Financial statements

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Profit & loss summary (HKDm)

Revenue 4,105 4,923 5,500 5,629EBITDA 1,077 1,325 1,427 1,498Depreciation & amortisation -54 -143 -188 -192Operating profit/EBIT 1,023 1,182 1,239 1,306Net interest -327 -333 -486 -498PBT 9,399 10,697 10,019 10,442HSBC PBT 9,399 10,697 10,019 10,442Taxation 19 -5 0 -3Net profit 9,425 10,687 10,016 10,435HSBC net profit 9,103 10,338 10,138 10,435

Cash flow summary (HKDm)

Cash flow from operations 5,544 6,223 6,071 6,191Capex -680 -172 -218 -218Cash flow from investment 271 1,770 3,903 3,978Dividends -4,359 -5,036 -5,622 -5,838Change in net debt -4,388 900 -128 534FCF equity 501 872 942 840

Balance sheet summary (HKDm)

Intangible fixed assets 0 2,479 2,479 2,479Tangible fixed assets 1,477 1,507 1,537 1,563Current assets 8,191 7,497 7,891 7,547Cash & others 6,980 6,196 6,452 6,065Total assets 88,542 95,543 101,099 106,627Operating liabilities 3,766 3,943 4,293 4,395Gross debt 11,113 11,230 11,357 11,504Net debt 4,133 5,034 4,906 5,439Shareholders funds 73,292 79,994 85,068 90,344Invested capital 71,337 78,946 83,894 89,708

Ratio, growth and per share analysis

Year to 12/2012a 12/2013e 12/2014e 12/2015e

Y-o-y % change

Revenue 17.5 19.9 11.7 2.3EBITDA 16.8 23.0 7.7 5.0Operating profit 19.9 15.6 4.8 5.4PBT 21.3 13.8 -6.3 4.2HSBC EPS 14.5 9.1 -1.9 2.9

Ratios (%)

Revenue/IC (x) 0.6 0.6 0.6 0.5ROIC 15.0 15.1 13.9 13.4ROE 13.7 13.5 12.3 11.9ROA 12.3 12.5 11.1 10.9EBITDA margin 26.2 26.9 25.9 26.6Operating profit margin 24.9 24.0 22.5 23.2EBITDA/net interest (x) 3.3 4.0 2.9 3.0Net debt/equity 5.6 6.3 5.8 6.0Net debt/EBITDA (x) 3.8 3.8 3.4 3.6CF from operations/net debt 134.1 123.7 123.8 113.8

Per share data (HKD)

EPS reported (fully diluted) 3.93 4.28 4.01 4.18HSBC EPS (fully diluted) 3.80 4.14 4.06 4.18DPS 1.66 2.01 2.05 2.13Book value 29.37 32.05 34.08 36.20

Valuation data

Year to 12/2012a 12/2013e 12/2014e 12/2015e

EV/sales 16.1 12.6 10.3 9.1EV/EBITDA 61.4 46.6 39.6 34.2EV/IC 0.9 0.8 0.7 0.6PE* 14.2 13.0 13.2 12.9P/Book value 1.8 1.7 1.6 1.5FCF yield (%) 0.8 1.5 1.8 1.8Dividend yield (%) 3.1 3.7 3.8 4.0

Note: * = Based on HSBC EPS (fully diluted)

Price relative

Source: HSBC Note: price at close of 07 Oct 2013

31

36

41

46

51

56

61

66

31

36

41

46

51

56

61

66

2011 2012 2013 2014Cheung Kong Infrastructur Rel to HANG SENG INDEX

3

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

No place to hide

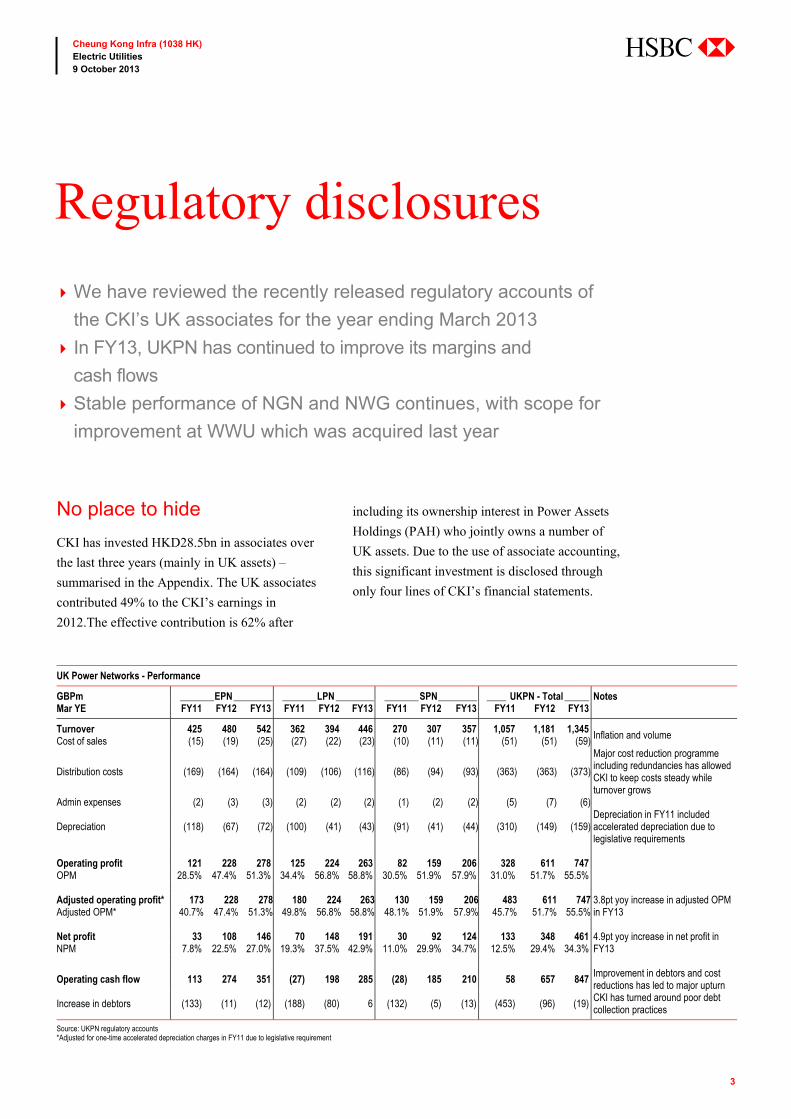

CKI has invested HKD28.5bn in associates over

the last three years (mainly in UK assets) –

summarised in the Appendix. The UK associates

contributed 49% to the CKI’s earnings in

2012.The effective contribution is 62% after

including its ownership interest in Power Assets

Holdings (PAH) who jointly owns a number of

UK assets. Due to the use of associate accounting,

this significant investment is disclosed through

only four lines of CKI’s financial statements.

Regulatory disclosures

We have reviewed the recently released regulatory accounts of

the CKI’s UK associates for the year ending March 2013

In FY13, UKPN has continued to improve its margins and

cash flows

Stable performance of NGN and NWG continues, with scope for

improvement at WWU which was acquired last year

UK Power Networks - Performance

GBPm _______ EPN ________ _______ LPN ________ _______ SPN ________ ____ UKPN - Total _____ Notes Mar YE FY11 FY12 FY13 FY11 FY12 FY13 FY11 FY12 FY13 FY11 FY12 FY13

Turnover 425 480 542 362 394 446 270 307 357 1,057 1,181 1,345 Inflation and volume Cost of sales (15) (19) (25) (27) (22) (23) (10) (11) (11) (51) (51) (59)

Distribution costs (169) (164) (164) (109) (106) (116) (86) (94) (93) (363) (363) (373)

Major cost reduction programme including redundancies has allowed CKI to keep costs steady while turnover grows

Admin expenses (2) (3) (3) (2) (2) (2) (1) (2) (2) (5) (7) (6)

Depreciation (118) (67) (72) (100) (41) (43) (91) (41) (44) (310) (149) (159)Depreciation in FY11 included accelerated depreciation due to legislative requirements

Operating profit 121 228 278 125 224 263 82 159 206 328 611 747

OPM 28.5% 47.4% 51.3% 34.4% 56.8% 58.8% 30.5% 51.9% 57.9% 31.0% 51.7% 55.5% Adjusted operating profit* 173 228 278 180 224 263 130 159 206 483 611 747 3.8pt yoy increase in adjusted OPM

in FY13 Adjusted OPM* 40.7% 47.4% 51.3% 49.8% 56.8% 58.8% 48.1% 51.9% 57.9% 45.7% 51.7% 55.5% Net profit 33 108 146 70 148 191 30 92 124 133 348 461 4.9pt yoy increase in net profit in

FY13 NPM 7.8% 22.5% 27.0% 19.3% 37.5% 42.9% 11.0% 29.9% 34.7% 12.5% 29.4% 34.3%

Operating cash flow 113 274 351 (27) 198 285 (28) 185 210 58 657 847 Improvement in debtors and cost reductions has led to major upturn

Increase in debtors (133) (11) (12) (188) (80) 6 (132) (5) (13) (453) (96) (19) CKI has turned around poor debt collection practices

Source: UKPN regulatory accounts *Adjusted for one-time accelerated depreciation charges in FY11 due to legislative requirement

4

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

However, UK regulators – Ofgem (Office of Gas &

Electricity Markets) and Ofwat (Office of Water

Services) – require full financial statements from

the regulated businesses to be publically released.

We have reviewed and analysed the recently

released regulatory accounts of the Cheung Kong

Group’s UK associates for the year ending

March 2013.

UK Power Networks

FY13 result was strong which highlights a 3.8pt

y-o-y increase in operating profits, as costs remain

stable on higher turnover and a significant

increase in cash flow.

Good cost control

UK Power Networks’ (UKPN) regulatory

accounts show strong cost control and rising

turnover (due to inflation and volumes) in FY13,

which led to a 3.8pt expansion in the operating

profit margin.

Distribution costs (excluding depreciation) as a % of

turnover decreased from 34.4% in FY11 to 27.7% in

FY13. Moving this ratio by so much is a very strong

performance from a stable regulated utility.

In 2011, there was a one-time accelerated

depreciation charge following the legislative

requirement for energy suppliers to replace

domestic meters with smart meters by 2020. In

2012, earnings increased substantially as

depreciation returned to a more sustainable level.

Cash flow improvement

CKI has also overhauled the poor debt collection

practices of UKPN, with the addition in debtors

decreasing from GBP453m in FY11 to GBP19m

in FY13. Improvement in debtors combined with

cost reduction and increase in profitability have

led to large upturn in cash flow from operating

activities, which increased from GBP58m in

FY11 to GBP847m in FY13. In FY13, cash flow

from operating activities increased by 29%.

Asset description

UKPN owns, operates and manages three of the

14 regulated electricity distribution networks in

the UK – the London, the South East and the East

of England – spanning a total length of

186,000km. It is one of the largest electricity

distribution network owners in the country, with

service area of 30,000 sq km and over 8m

connected customers. CKI and PAH each own a

40% interest in the company.

Northern Gas Networks

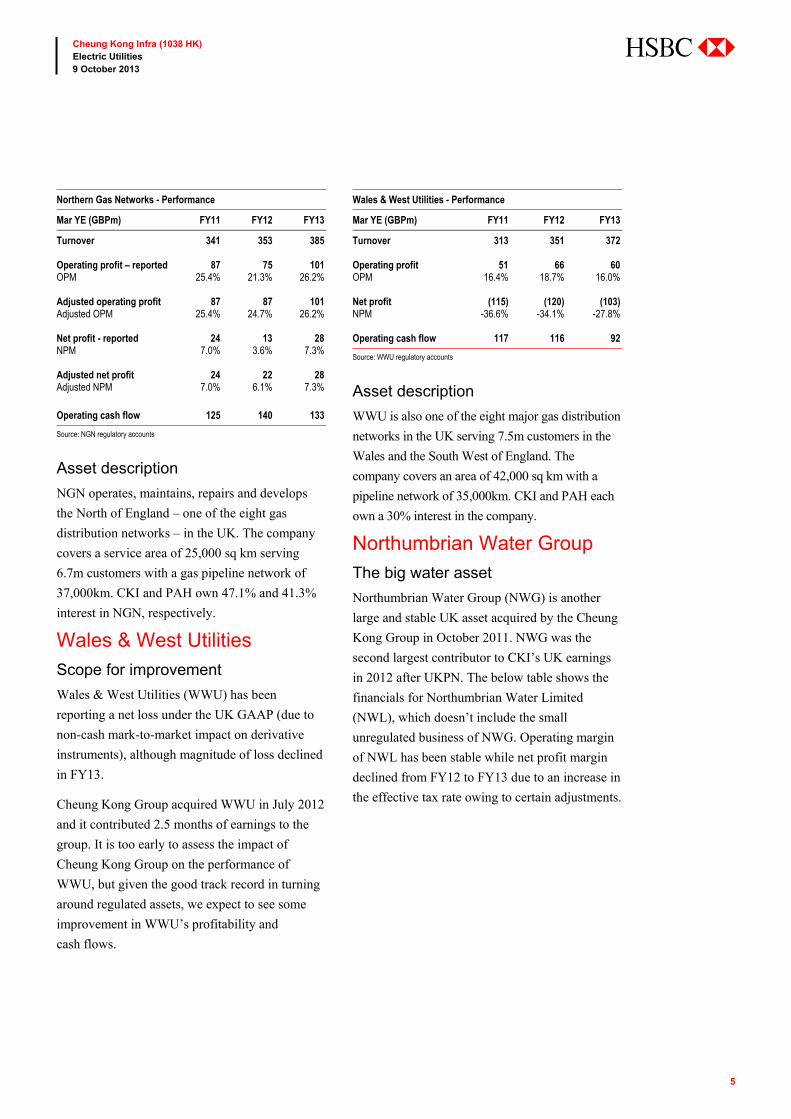

Stable margins and cash flows

Northern Gas Networks (NGN) has generated

stable margins and cash flows over the last three

years. Reported operating and net profit declined

in FY12 primarily due to exceptional restructuring

cost of GBP11.9m (GBP8.9m post-tax) related to

the organisational structure following the

acquisition of Northern Gas Networks Operations

in 2010 to realign core activities and remove

duplication. This restructuring resulted in

efficiency gains for the company in FY13 with

adjusted OPM increasing 1.5% mainly through

voluntary severance programme.

The company has also generated a steady cash

flow of GBP125-140m from operating activities

over the last three years.

5

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

Northern Gas Networks - Performance

Mar YE (GBPm) FY11 FY12 FY13

Turnover 341 353 385 Operating profit – reported 87 75 101 OPM 25.4% 21.3% 26.2% Adjusted operating profit 87 87 101 Adjusted OPM 25.4% 24.7% 26.2% Net profit - reported 24 13 28 NPM 7.0% 3.6% 7.3% Adjusted net profit 24 22 28 Adjusted NPM 7.0% 6.1% 7.3%

Operating cash flow 125 140 133

Source: NGN regulatory accounts

Asset description

NGN operates, maintains, repairs and develops

the North of England – one of the eight gas

distribution networks – in the UK. The company

covers a service area of 25,000 sq km serving

6.7m customers with a gas pipeline network of

37,000km. CKI and PAH own 47.1% and 41.3%

interest in NGN, respectively.

Wales & West Utilities

Scope for improvement

Wales & West Utilities (WWU) has been

reporting a net loss under the UK GAAP (due to

non-cash mark-to-market impact on derivative

instruments), although magnitude of loss declined

in FY13.

Cheung Kong Group acquired WWU in July 2012

and it contributed 2.5 months of earnings to the

group. It is too early to assess the impact of

Cheung Kong Group on the performance of

WWU, but given the good track record in turning

around regulated assets, we expect to see some

improvement in WWU’s profitability and

cash flows.

Wales & West Utilities - Performance

Mar YE (GBPm) FY11 FY12 FY13

Turnover 313 351 372

Operating profit 51 66 60 OPM 16.4% 18.7% 16.0%

Net profit (115) (120) (103) NPM -36.6% -34.1% -27.8%

Operating cash flow 117 116 92

Source: WWU regulatory accounts

Asset description

WWU is also one of the eight major gas distribution

networks in the UK serving 7.5m customers in the

Wales and the South West of England. The

company covers an area of 42,000 sq km with a

pipeline network of 35,000km. CKI and PAH each

own a 30% interest in the company.

Northumbrian Water Group

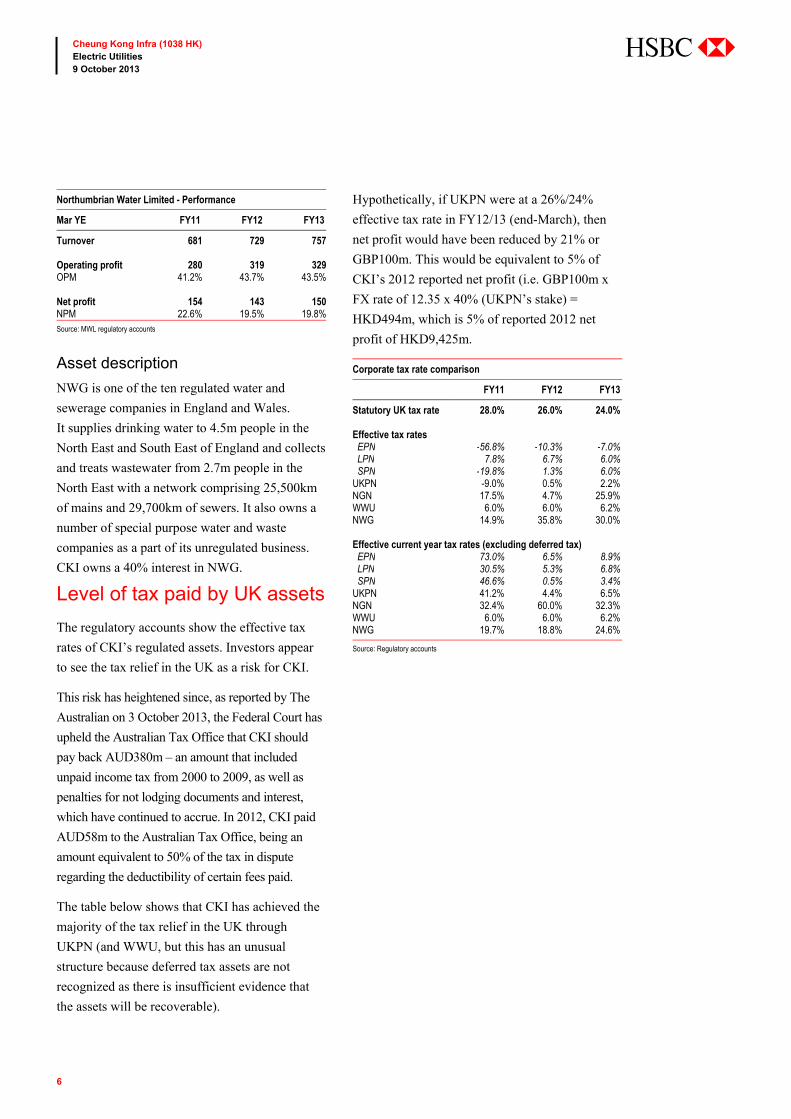

The big water asset

Northumbrian Water Group (NWG) is another

large and stable UK asset acquired by the Cheung

Kong Group in October 2011. NWG was the

second largest contributor to CKI’s UK earnings

in 2012 after UKPN. The below table shows the

financials for Northumbrian Water Limited

(NWL), which doesn’t include the small

unregulated business of NWG. Operating margin

of NWL has been stable while net profit margin

declined from FY12 to FY13 due to an increase in

the effective tax rate owing to certain adjustments.

6

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

Northumbrian Water Limited - Performance

Mar YE FY11 FY12 FY13

Turnover 681 729 757 Operating profit 280 319 329OPM 41.2% 43.7% 43.5% Net profit 154 143 150NPM 22.6% 19.5% 19.8%Source: MWL regulatory accounts

Asset description

NWG is one of the ten regulated water and

sewerage companies in England and Wales.

It supplies drinking water to 4.5m people in the

North East and South East of England and collects

and treats wastewater from 2.7m people in the

North East with a network comprising 25,500km

of mains and 29,700km of sewers. It also owns a

number of special purpose water and waste

companies as a part of its unregulated business.

CKI owns a 40% interest in NWG.

Level of tax paid by UK assets

The regulatory accounts show the effective tax

rates of CKI’s regulated assets. Investors appear

to see the tax relief in the UK as a risk for CKI.

This risk has heightened since, as reported by The

Australian on 3 October 2013, the Federal Court has

upheld the Australian Tax Office that CKI should

pay back AUD380m – an amount that included

unpaid income tax from 2000 to 2009, as well as

penalties for not lodging documents and interest,

which have continued to accrue. In 2012, CKI paid

AUD58m to the Australian Tax Office, being an

amount equivalent to 50% of the tax in dispute

regarding the deductibility of certain fees paid.

The table below shows that CKI has achieved the

majority of the tax relief in the UK through

UKPN (and WWU, but this has an unusual

structure because deferred tax assets are not

recognized as there is insufficient evidence that

the assets will be recoverable).

Hypothetically, if UKPN were at a 26%/24%

effective tax rate in FY12/13 (end-March), then

net profit would have been reduced by 21% or

GBP100m. This would be equivalent to 5% of

CKI’s 2012 reported net profit (i.e. GBP100m x

FX rate of 12.35 x 40% (UKPN’s stake) =

HKD494m, which is 5% of reported 2012 net

profit of HKD9,425m.

Corporate tax rate comparison

FY11 FY12 FY13

Statutory UK tax rate 28.0% 26.0% 24.0%

Effective tax rates EPN -56.8% -10.3% -7.0% LPN 7.8% 6.7% 6.0% SPN -19.8% 1.3% 6.0% UKPN -9.0% 0.5% 2.2% NGN 17.5% 4.7% 25.9% WWU 6.0% 6.0% 6.2% NWG 14.9% 35.8% 30.0%

Effective current year tax rates (excluding deferred tax) EPN 73.0% 6.5% 8.9% LPN 30.5% 5.3% 6.8% SPN 46.6% 0.5% 3.4% UKPN 41.2% 4.4% 6.5% NGN 32.4% 60.0% 32.3% WWU 6.0% 6.0% 6.2% NWG 19.7% 18.8% 24.6%

Source: Regulatory accounts

7

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

UK vs HK earnings

In this section, we do some forensic accounting,

comparing the UK regulatory accounts (recently

released for year ending March FY13) to CKI’s

associate accounting.

Our conclusions are:

earnings reported in HK from the UK assets

are substantially higher than the earnings

reported in the UK regulatory accounts

the earnings difference is largely due to

accounting differences but this does not fully

explain the gap

the accounting differences are a major reason

why the dividend payout from non-PAH

associates was relatively low at 32% of

earnings in FY12 (we forecast an increase to

35% in FY13e on stronger cash flows).

Because of the low dividend payout from

associate, CKI has high earnings coverage

(2.5x) but a low cash coverage (1.2x)

Because earnings are inflated into Hong Kong,

CKI’s UK assets should trade with a lower PE.

In our SOTP valuation on page 11, the implied

FY14e PE for the UK assets is 8.4x. Our

valuation compared to the earnings reported in

the UK would imply a PE of 12.7x.

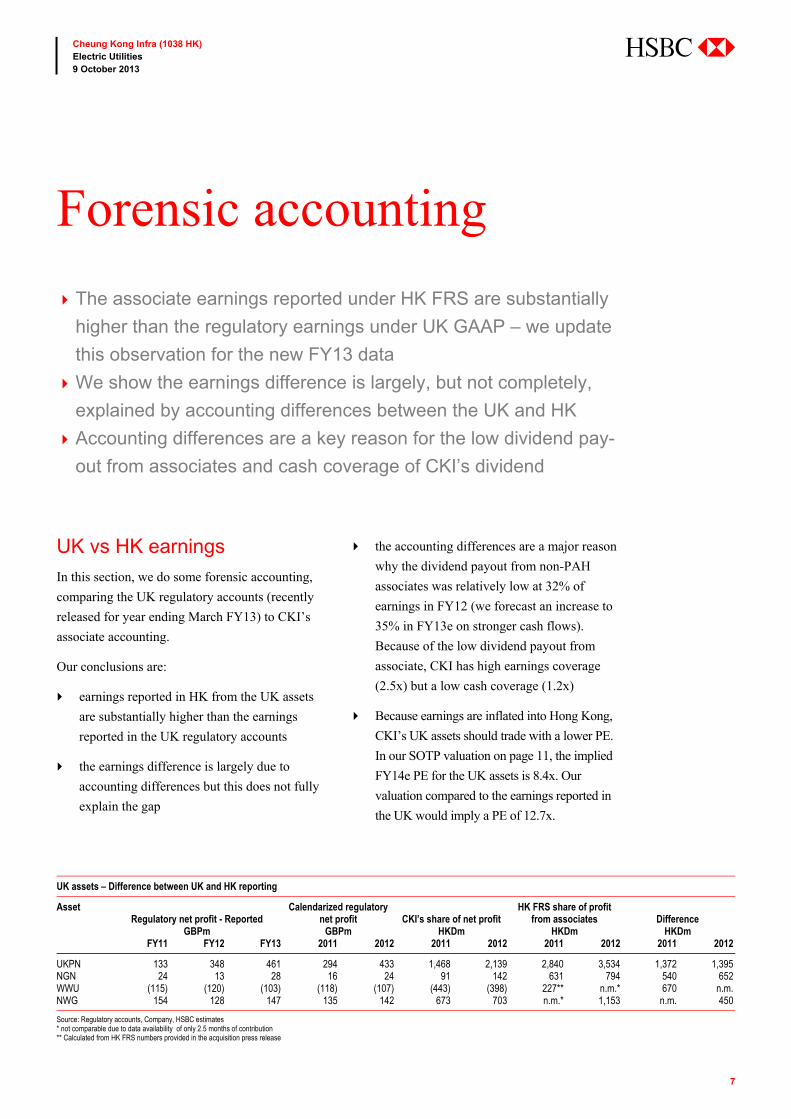

Forensic accounting

The associate earnings reported under HK FRS are substantially

higher than the regulatory earnings under UK GAAP – we update

this observation for the new FY13 data

We show the earnings difference is largely, but not completely,

explained by accounting differences between the UK and HK

Accounting differences are a key reason for the low dividend pay-

out from associates and cash coverage of CKI’s dividend

UK assets – Difference between UK and HK reporting

Asset Regulatory net profit - Reported

Calendarized regulatory net profit

CKI’s share of net profit

HK FRS share of profit from associates

Difference

GBPm GBPm HKDm HKDm HKDm FY11 FY12 FY13 2011 2012 2011 2012 2011 2012 2011 2012

UKPN 133 348 461 294 433 1,468 2,139 2,840 3,534 1,372 1,395NGN 24 13 28 16 24 91 142 631 794 540 652WWU (115) (120) (103) (118) (107) (443) (398) 227** n.m.* 670 n.m.NWG 154 128 147 135 142 673 703 n.m.* 1,153 n.m. 450

Source: Regulatory accounts, Company, HSBC estimates * not comparable due to data availability of only 2.5 months of contribution ** Calculated from HK FRS numbers provided in the acquisition press release

8

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

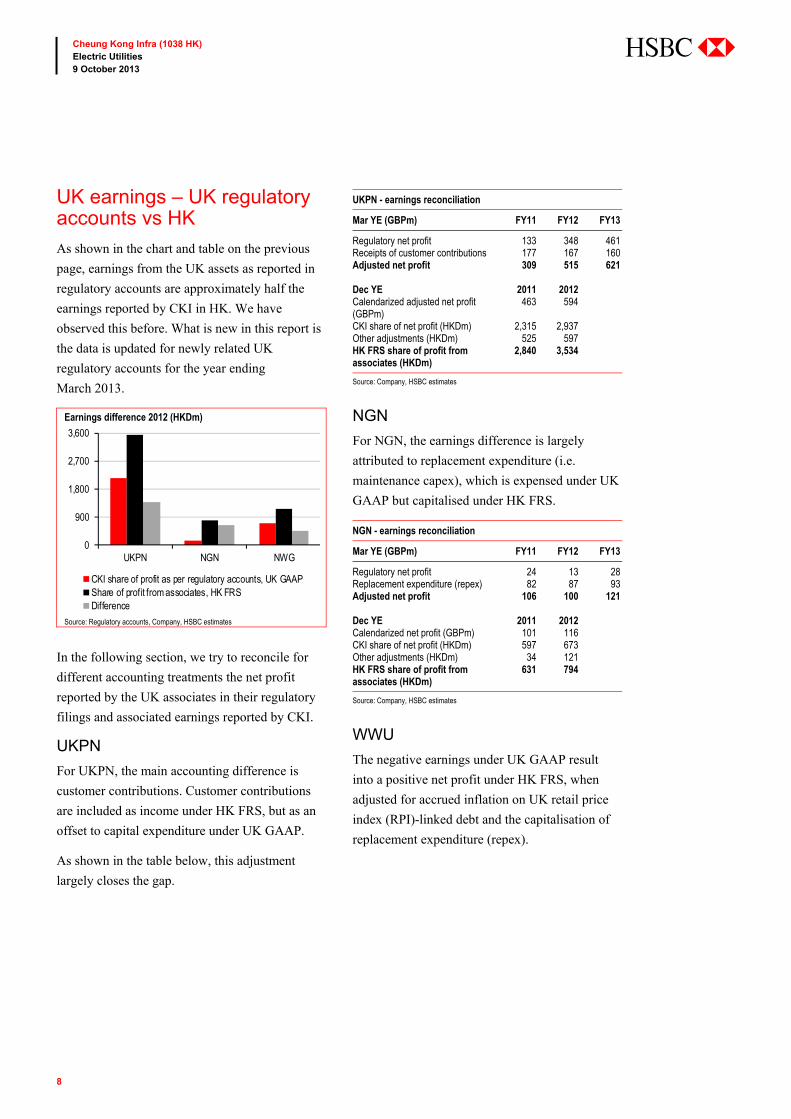

UK earnings – UK regulatory accounts vs HK

As shown in the chart and table on the previous

page, earnings from the UK assets as reported in

regulatory accounts are approximately half the

earnings reported by CKI in HK. We have

observed this before. What is new in this report is

the data is updated for newly related UK

regulatory accounts for the year ending

March 2013.

Earnings difference 2012 (HKDm)

Source: Regulatory accounts, Company, HSBC estimates

In the following section, we try to reconcile for

different accounting treatments the net profit

reported by the UK associates in their regulatory

filings and associated earnings reported by CKI.

UKPN

For UKPN, the main accounting difference is

customer contributions. Customer contributions

are included as income under HK FRS, but as an

offset to capital expenditure under UK GAAP.

As shown in the table below, this adjustment

largely closes the gap.

UKPN - earnings reconciliation

Mar YE (GBPm) FY11 FY12 FY13

Regulatory net profit 133 348 461 Receipts of customer contributions 177 167 160 Adjusted net profit 309 515 621

Dec YE 2011 2012 Calendarized adjusted net profit (GBPm)

463 594

CKI share of net profit (HKDm) 2,315 2,937 Other adjustments (HKDm) 525 597 HK FRS share of profit from associates (HKDm)

2,840 3,534

Source: Company, HSBC estimates

NGN

For NGN, the earnings difference is largely

attributed to replacement expenditure (i.e.

maintenance capex), which is expensed under UK

GAAP but capitalised under HK FRS.

NGN - earnings reconciliation

Mar YE (GBPm) FY11 FY12 FY13

Regulatory net profit 24 13 28 Replacement expenditure (repex) 82 87 93 Adjusted net profit 106 100 121

Dec YE 2011 2012 Calendarized net profit (GBPm) 101 116 CKI share of net profit (HKDm) 597 673 Other adjustments (HKDm) 34 121 HK FRS share of profit from associates (HKDm)

631 794

Source: Company, HSBC estimates

WWU

The negative earnings under UK GAAP result

into a positive net profit under HK FRS, when

adjusted for accrued inflation on UK retail price

index (RPI)-linked debt and the capitalisation of

replacement expenditure (repex).

0

900

1,800

2,700

3,600

UKPN NGN NWG

CKI share of profit as per regulatory accounts, UK GAAPShare of profit from associates, HK FRSDifference

9

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

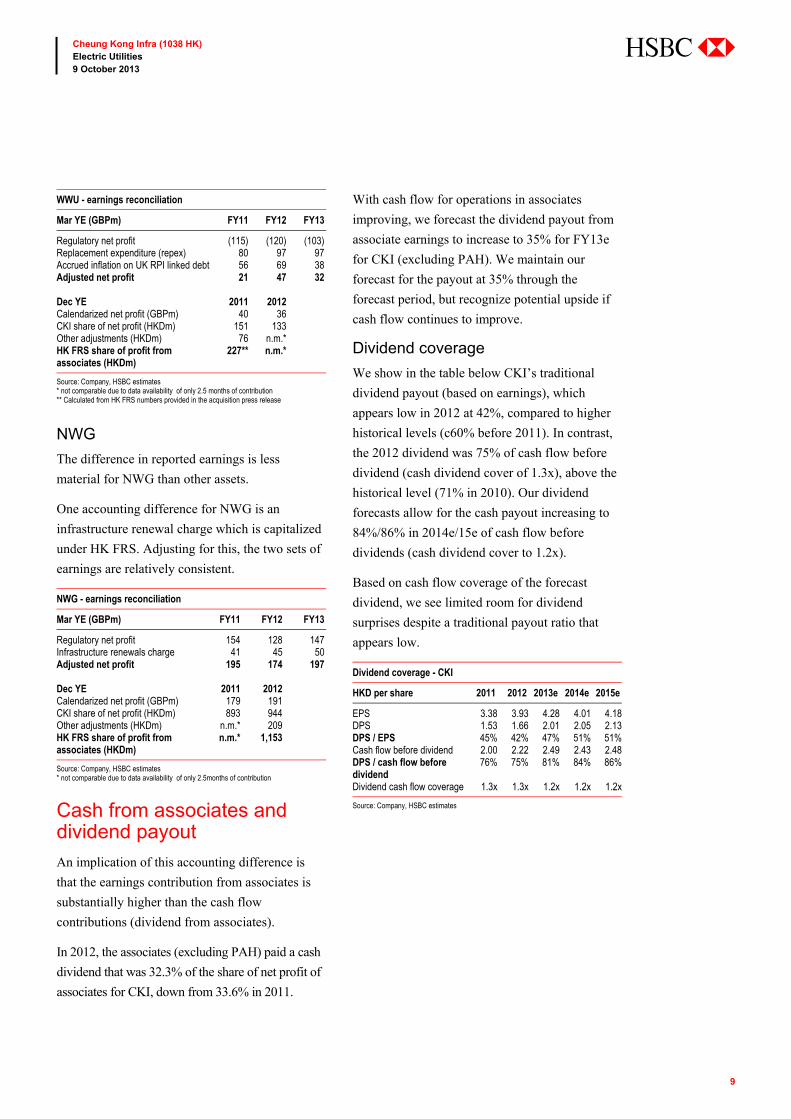

WWU - earnings reconciliation

Mar YE (GBPm) FY11 FY12 FY13

Regulatory net profit (115) (120) (103) Replacement expenditure (repex) 80 97 97 Accrued inflation on UK RPI linked debt 56 69 38 Adjusted net profit 21 47 32 Dec YE 2011 2012 Calendarized net profit (GBPm) 40 36 CKI share of net profit (HKDm) 151 133 Other adjustments (HKDm) 76 n.m.* HK FRS share of profit from associates (HKDm)

227** n.m.*

Source: Company, HSBC estimates * not comparable due to data availability of only 2.5 months of contribution ** Calculated from HK FRS numbers provided in the acquisition press release

NWG

The difference in reported earnings is less

material for NWG than other assets.

One accounting difference for NWG is an

infrastructure renewal charge which is capitalized

under HK FRS. Adjusting for this, the two sets of

earnings are relatively consistent.

NWG - earnings reconciliation

Mar YE (GBPm) FY11 FY12 FY13

Regulatory net profit 154 128 147 Infrastructure renewals charge 41 45 50 Adjusted net profit 195 174 197 Dec YE 2011 2012 Calendarized net profit (GBPm) 179 191 CKI share of net profit (HKDm) 893 944 Other adjustments (HKDm) n.m.* 209 HK FRS share of profit from associates (HKDm)

n.m.* 1,153

Source: Company, HSBC estimates * not comparable due to data availability of only 2.5months of contribution

Cash from associates and dividend payout

An implication of this accounting difference is

that the earnings contribution from associates is

substantially higher than the cash flow

contributions (dividend from associates).

In 2012, the associates (excluding PAH) paid a cash

dividend that was 32.3% of the share of net profit of

associates for CKI, down from 33.6% in 2011.

With cash flow for operations in associates

improving, we forecast the dividend payout from

associate earnings to increase to 35% for FY13e

for CKI (excluding PAH). We maintain our

forecast for the payout at 35% through the

forecast period, but recognize potential upside if

cash flow continues to improve.

Dividend coverage

We show in the table below CKI’s traditional

dividend payout (based on earnings), which

appears low in 2012 at 42%, compared to higher

historical levels (c60% before 2011). In contrast,

the 2012 dividend was 75% of cash flow before

dividend (cash dividend cover of 1.3x), above the

historical level (71% in 2010). Our dividend

forecasts allow for the cash payout increasing to

84%/86% in 2014e/15e of cash flow before

dividends (cash dividend cover to 1.2x).

Based on cash flow coverage of the forecast

dividend, we see limited room for dividend

surprises despite a traditional payout ratio that

appears low.

Dividend coverage - CKI

HKD per share 2011 2012 2013e 2014e 2015e

EPS 3.38 3.93 4.28 4.01 4.18DPS 1.53 1.66 2.01 2.05 2.13DPS / EPS 45% 42% 47% 51% 51%Cash flow before dividend 2.00 2.22 2.49 2.43 2.48DPS / cash flow before dividend

76% 75% 81% 84% 86%

Dividend cash flow coverage 1.3x 1.3x 1.2x 1.2x 1.2x

Source: Company, HSBC estimates

10

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

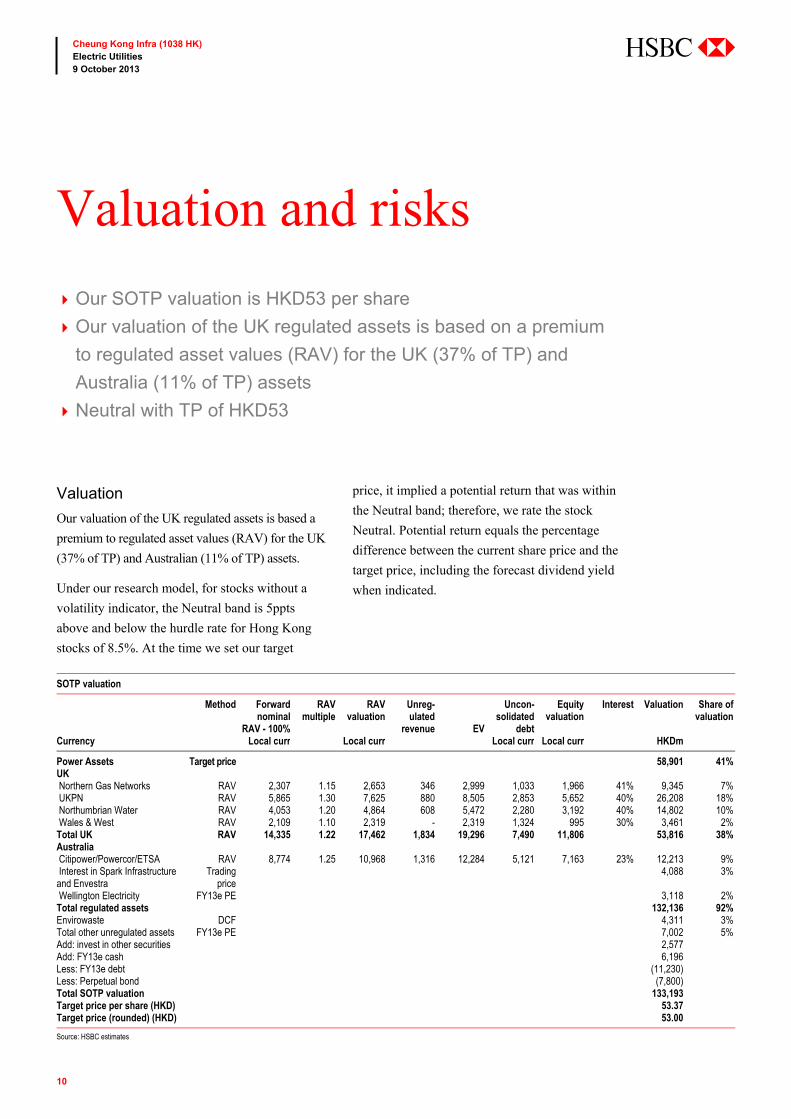

Valuation

Our valuation of the UK regulated assets is based a

premium to regulated asset values (RAV) for the UK

(37% of TP) and Australian (11% of TP) assets.

Under our research model, for stocks without a

volatility indicator, the Neutral band is 5ppts

above and below the hurdle rate for Hong Kong

stocks of 8.5%. At the time we set our target

price, it implied a potential return that was within

the Neutral band; therefore, we rate the stock

Neutral. Potential return equals the percentage

difference between the current share price and the

target price, including the forecast dividend yield

when indicated.

SOTP valuation

Method Forward nominal

RAV - 100%

RAV multiple

RAV valuation

Unreg-ulated

revenue EV

Uncon-solidated

debt

Equity valuation

Interest Valuation Share of valuation

Currency Local curr Local curr Local curr Local curr HKDm

Power Assets Target price 58,901 41%UK Northern Gas Networks RAV 2,307 1.15 2,653 346 2,999 1,033 1,966 41% 9,345 7% UKPN RAV 5,865 1.30 7,625 880 8,505 2,853 5,652 40% 26,208 18% Northumbrian Water RAV 4,053 1.20 4,864 608 5,472 2,280 3,192 40% 14,802 10% Wales & West RAV 2,109 1.10 2,319 - 2,319 1,324 995 30% 3,461 2%Total UK RAV 14,335 1.22 17,462 1,834 19,296 7,490 11,806 53,816 38%Australia Citipower/Powercor/ETSA RAV 8,774 1.25 10,968 1,316 12,284 5,121 7,163 23% 12,213 9% Interest in Spark Infrastructure and Envestra

Trading price

4,088 3%

Wellington Electricity FY13e PE 3,118 2%Total regulated assets 132,136 92%Envirowaste DCF 4,311 3%Total other unregulated assets FY13e PE 7,002 5%Add: invest in other securities 2,577Add: FY13e cash 6,196Less: FY13e debt (11,230)Less: Perpetual bond (7,800)Total SOTP valuation 133,193Target price per share (HKD) 53.37Target price (rounded) (HKD) 53.00

Source: HSBC estimates

Valuation and risks

Our SOTP valuation is HKD53 per share

Our valuation of the UK regulated assets is based on a premium

to regulated asset values (RAV) for the UK (37% of TP) and

Australia (11% of TP) assets

Neutral with TP of HKD53

11

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

Risks

Upside risks: a large and value-accretive

acquisition and dividend surprises.

Downside risk: regulatory resets that reduce the

allowed return on equity.

12

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

Appendix

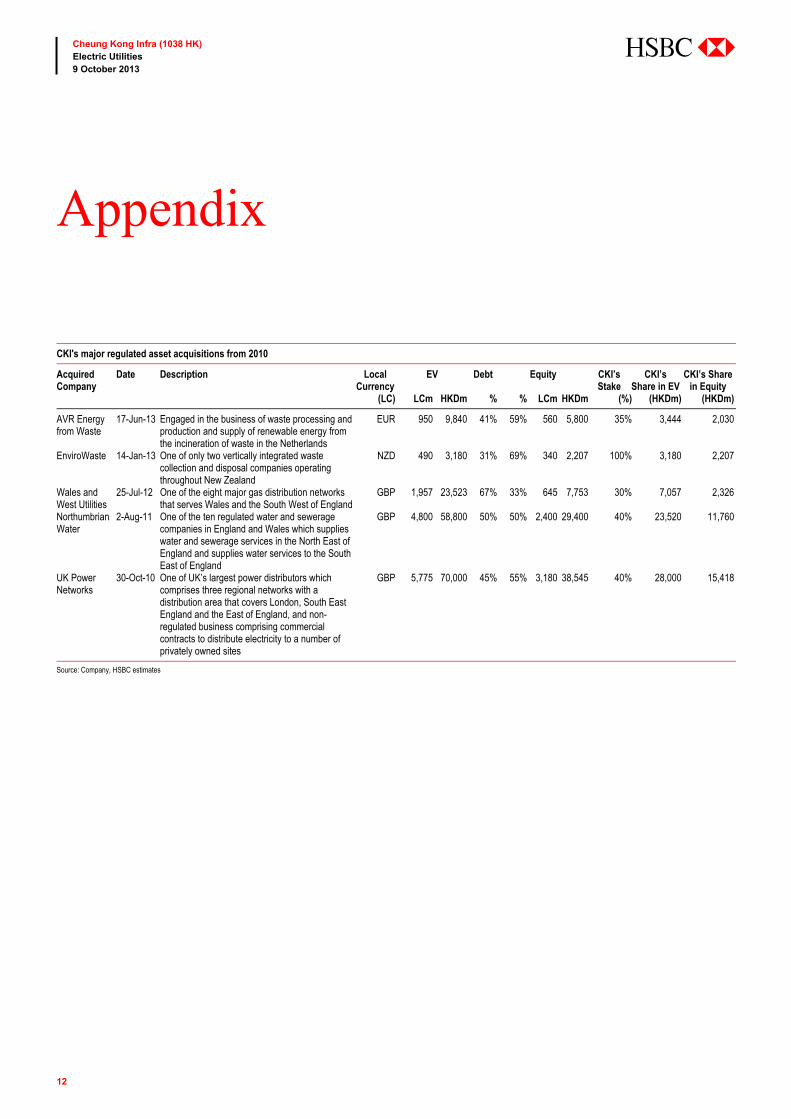

CKI's major regulated asset acquisitions from 2010

Acquired Company

Date Description Local Currency

EV Debt Equity CKI’s Stake

CKI’s Share in EV

CKI’s Share in Equity

(LC) LCm HKDm % % LCm HKDm (%) (HKDm) (HKDm)

AVR Energy from Waste

17-Jun-13 Engaged in the business of waste processing and production and supply of renewable energy from the incineration of waste in the Netherlands

EUR 950 9,840 41% 59% 560 5,800 35% 3,444 2,030

EnviroWaste 14-Jan-13 One of only two vertically integrated waste collection and disposal companies operating throughout New Zealand

NZD 490 3,180 31% 69% 340 2,207 100% 3,180 2,207

Wales and West Utilities

25-Jul-12 One of the eight major gas distribution networks that serves Wales and the South West of England

GBP 1,957 23,523 67% 33% 645 7,753 30% 7,057 2,326

Northumbrian Water

2-Aug-11 One of the ten regulated water and sewerage companies in England and Wales which supplies water and sewerage services in the North East of England and supplies water services to the South East of England

GBP 4,800 58,800 50% 50% 2,400 29,400 40% 23,520 11,760

UK Power Networks

30-Oct-10 One of UK’s largest power distributors whichcomprises three regional networks with a distribution area that covers London, South East England and the East of England, and non-regulated business comprising commercial contracts to distribute electricity to a number of privately owned sites

GBP 5,775 70,000 45% 55% 3,180 38,545 40% 28,000 15,418

Source: Company, HSBC estimates

13

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

UK water distribution network operators

Source: Water UK, HSBC

Water Only Companies

1 - Sembcorp Bournemouth Water

2 - Bristol Water

3 - Cambridge Water

4 - Cholderton and District Water

5 - Dee Valley Water

6 - Essex and Suffolk Water

7 - Hartlepool Water (Anglian Water)

8 - Portsmouth Water

9 - South East Water (Mid Kent)

10 - South Staffordshire Water

11 - Sutton and East Surrey Water

12 - Veolia Water Central

13 - Veolia Water East

14 - Veolia Water Southeast

Water and Sewerage Companies

15 - Anglian Water

16 - Dwr Cymru (Welsh Water)

17 - Northumbrian Water (CKI)

18 - Scottish Water

19 - Severn Trent

20 - South West Water (Pennon)

21 - Southern Water

22 - Thames Water

23 - United Utilities

24 - Wessex Water

25 - Yorkshire Water

26 - Northern Ireland Water

Water Only Companies

1 - Sembcorp Bournemouth Water

2 - Bristol Water

3 - Cambridge Water

4 - Cholderton and District Water

5 - Dee Valley Water

6 - Essex and Suffolk Water

7 - Hartlepool Water (Anglian Water)

8 - Portsmouth Water

9 - South East Water (Mid Kent)

10 - South Staffordshire Water

11 - Sutton and East Surrey Water

12 - Veolia Water Central

13 - Veolia Water East

14 - Veolia Water Southeast

Water and Sewerage Companies

15 - Anglian Water

16 - Dwr Cymru (Welsh Water)

17 - Northumbrian Water (CKI)

18 - Scottish Water

19 - Severn Trent

20 - South West Water (Pennon)

21 - Southern Water

22 - Thames Water

23 - United Utilities

24 - Wessex Water

25 - Yorkshire Water

26 - Northern Ireland Water

14

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

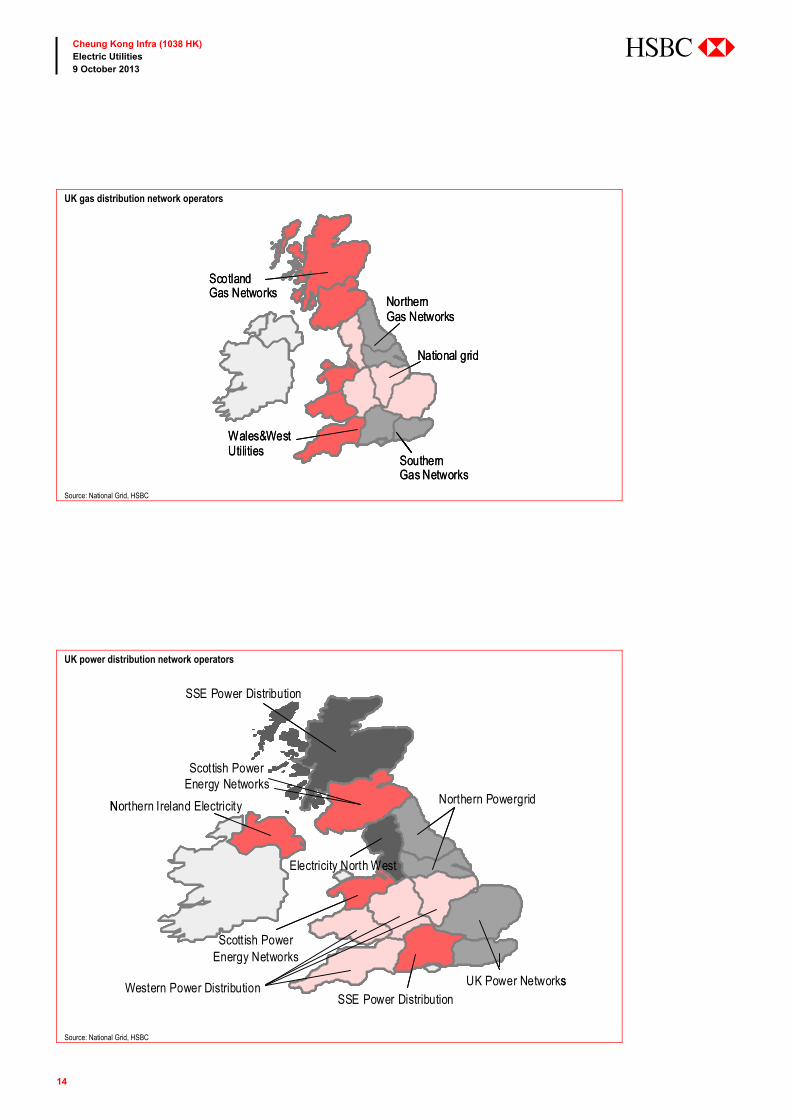

UK gas distribution network operators

Source: National Grid, HSBC

UK power distribution network operators

Source: National Grid, HSBC

NorthernGas Networks

SouthernGas Networks

ScotlandGas Networks

National grid

Wales&WestUtilities

NorthernGas Networks

SouthernGas Networks

ScotlandGas Networks

National grid

Wales&WestUtilities

SSE Power Distribution

CE Electric UK

SSE Power Distribution

Scottish PowerEnergy Networks

Electr icity

enwe-on

eDFENERGYnetworks

Scottish PowerEnergy Networks

Western Power Distribution

SSE Power Distribution

CE Electric UK

SSE Power Distribution

Scottish PowerEnergy Networks

Electr icity

ENW

E.ON Central Networks

EDFEnergyNetworks

Scottish PowerEnergy Networks

Western Power Distribution

SSE Power Distribution

CE Electric UK

SSE Power Distribution

Scottish PowerEnergy Networks

Electr icity

enwe-on

eDFENERGYnetworks

Scottish PowerEnergy Networks

Western Power Distribution

SSE Power Distribution

Northern Powergrid

SSE Power Distribution

Scottish PowerEnergy Networks

UK Power Networks

Scottish PowerEnergy Networks

Western Power Distribution

Northern Ireland Electricity

Electricity North West

SSE Power Distribution

CE Electric UK

SSE Power Distribution

Scottish PowerEnergy Networks

Electr icity

enwe-on

eDFENERGYnetworks

Scottish PowerEnergy Networks

Western Power Distribution

SSE Power Distribution

CE Electric UK

SSE Power Distribution

Scottish PowerEnergy Networks

Electr icity

ENW

E.ON Central Networks

EDFEnergyNetworks

Scottish PowerEnergy Networks

Western Power Distribution

SSE Power Distribution

CE Electric UK

SSE Power Distribution

Scottish PowerEnergy Networks

Electr icity

enwe-on

eDFENERGYnetworks

Scottish PowerEnergy Networks

Western Power Distribution

SSE Power Distribution

Northern Powergrid

SSE Power Distribution

Scottish PowerEnergy Networks

UK Power Networks

Scottish PowerEnergy Networks

Western Power Distribution

Northern Ireland Electricity

Electricity North West

15

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

Disclosure appendix Analyst Certification The following analyst(s), economist(s), and/or strategist(s) who is(are) primarily responsible for this report, certifies(y) that the opinion(s) on the subject security(ies) or issuer(s) and/or any other views or forecasts expressed herein accurately reflect their personal view(s) and that no part of their compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report: Jenny Cosgrove and Gloria Ho

Important disclosures

Equities: Stock ratings and basis for financial analysis

HSBC believes that investors utilise various disciplines and investment horizons when making investment decisions, which depend largely on individual circumstances such as the investor's existing holdings, risk tolerance and other considerations. Given these differences, HSBC has two principal aims in its equity research: 1) to identify long-term investment opportunities based on particular themes or ideas that may affect the future earnings or cash flows of companies on a 12 month time horizon; and 2) from time to time to identify short-term investment opportunities that are derived from fundamental, quantitative, technical or event-driven techniques on a 0-3 month time horizon and which may differ from our long-term investment rating. HSBC has assigned ratings for its long-term investment opportunities as described below.

This report addresses only the long-term investment opportunities of the companies referred to in the report. As and when HSBC publishes a short-term trading idea the stocks to which these relate are identified on the website at www.hsbcnet.com/research. Details of these short-term investment opportunities can be found under the Reports section of this website.

HSBC believes an investor's decision to buy or sell a stock should depend on individual circumstances such as the investor's existing holdings and other considerations. Different securities firms use a variety of ratings terms as well as different rating systems to describe their recommendations. Investors should carefully read the definitions of the ratings used in each research report. In addition, because research reports contain more complete information concerning the analysts' views, investors should carefully read the entire research report and should not infer its contents from the rating. In any case, ratings should not be used or relied on in isolation as investment advice.

Rating definitions for long-term investment opportunities

Stock ratings HSBC assigns ratings to its stocks in this sector on the following basis:

For each stock we set a required rate of return calculated from the cost of equity for that stock’s domestic or, as appropriate, regional market established by our strategy team. The price target for a stock represents the value the analyst expects the stock to reach over our performance horizon. The performance horizon is 12 months. For a stock to be classified as Overweight, the potential return, which equals the percentage difference between the current share price and the target price, including the forecast dividend yield when indicated, must exceed the required return by at least 5 percentage points over the next 12 months (or 10 percentage points for a stock classified as Volatile*). For a stock to be classified as Underweight, the stock must be expected to underperform its required return by at least 5 percentage points over the next 12 months (or 10 percentage points for a stock classified as Volatile*). Stocks between these bands are classified as Neutral.

Our ratings are re-calibrated against these bands at the time of any 'material change' (initiation of coverage, change of volatility status or change in price target). Notwithstanding this, and although ratings are subject to ongoing management review, expected returns will be permitted to move outside the bands as a result of normal share price fluctuations without necessarily triggering a rating change.

16

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

*A stock will be classified as volatile if its historical volatility has exceeded 40%, if the stock has been listed for less than 12 months (unless it is in an industry or sector where volatility is low) or if the analyst expects significant volatility. However, stocks which we do not consider volatile may in fact also behave in such a way. Historical volatility is defined as the past month's average of the daily 365-day moving average volatilities. In order to avoid misleadingly frequent changes in rating, however, volatility has to move 2.5 percentage points past the 40% benchmark in either direction for a stock's status to change.

Rating distribution for long-term investment opportunities

As of 08 October 2013, the distribution of all ratings published is as follows: Overweight (Buy) 45% (33% of these provided with Investment Banking Services)

Neutral (Hold) 38% (34% of these provided with Investment Banking Services)

Underweight (Sell) 17% (25% of these provided with Investment Banking Services)

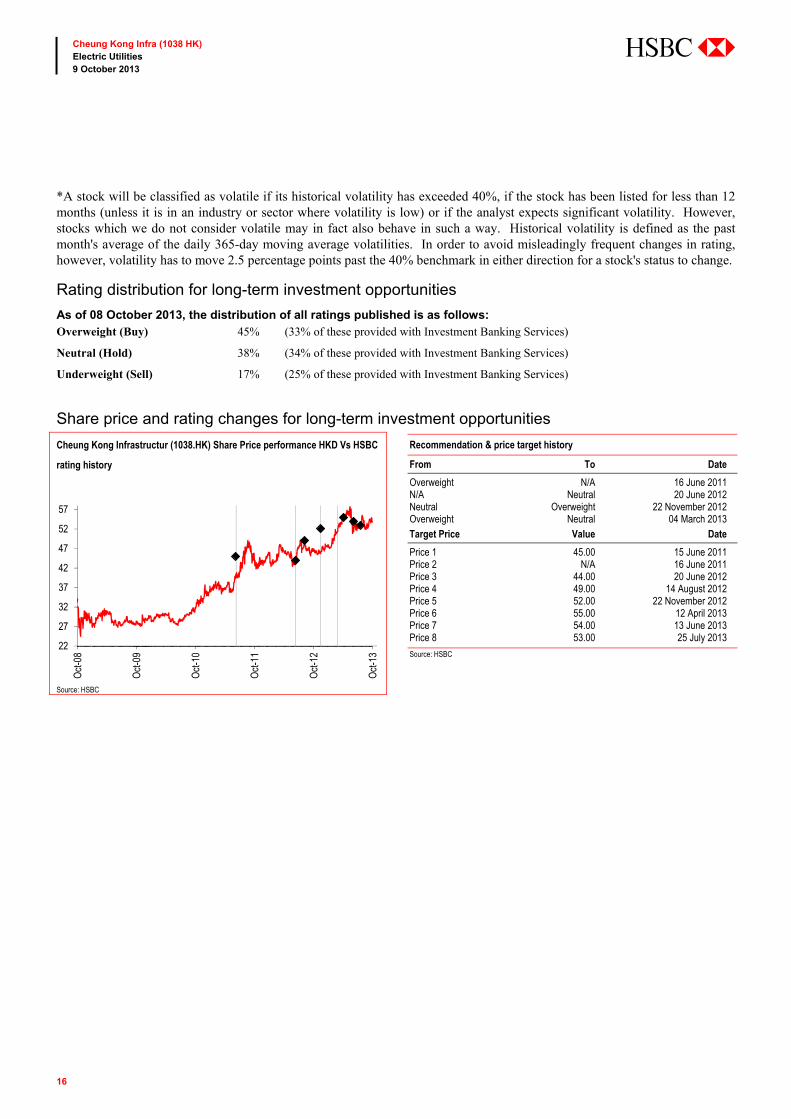

Share price and rating changes for long-term investment opportunities

Cheung Kong Infrastructur (1038.HK) Share Price performance HKD Vs HSBC

rating history

Recommendation & price target history

From To Date

Overweight N/A 16 June 2011 N/A Neutral 20 June 2012 Neutral Overweight 22 November 2012 Overweight Neutral 04 March 2013 Target Price Value Date

Price 1 45.00 15 June 2011 Price 2 N/A 16 June 2011 Price 3 44.00 20 June 2012 Price 4 49.00 14 August 2012 Price 5 52.00 22 November 2012 Price 6 55.00 12 April 2013 Price 7 54.00 13 June 2013 Price 8 53.00 25 July 2013

Source: HSBC

Source: HSBC

22

27

32

37

42

47

52

57

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

17

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

HSBC & Analyst disclosures Disclosure checklist

Company Ticker Recent price Price Date Disclosure

CHEUNG KONG INFRASTRUCTUR 1038.HK 53.80 07-Oct-2013 1, 2, 5, 6, 7, 11Source: HSBC

1 HSBC has managed or co-managed a public offering of securities for this company within the past 12 months. 2 HSBC expects to receive or intends to seek compensation for investment banking services from this company in the next

3 months. 3 At the time of publication of this report, HSBC Securities (USA) Inc. is a Market Maker in securities issued by this

company. 4 As of 31 August 2013 HSBC beneficially owned 1% or more of a class of common equity securities of this company. 5 As of 31 August 2013, this company was a client of HSBC or had during the preceding 12 month period been a client of

and/or paid compensation to HSBC in respect of investment banking services. 6 As of 31 August 2013, this company was a client of HSBC or had during the preceding 12 month period been a client of

and/or paid compensation to HSBC in respect of non-investment banking securities-related services. 7 As of 31 August 2013, this company was a client of HSBC or had during the preceding 12 month period been a client of

and/or paid compensation to HSBC in respect of non-securities services. 8 A covering analyst/s has received compensation from this company in the past 12 months. 9 A covering analyst/s or a member of his/her household has a financial interest in the securities of this company, as

detailed below. 10 A covering analyst/s or a member of his/her household is an officer, director or supervisory board member of this

company, as detailed below. 11 At the time of publication of this report, HSBC is a non-US Market Maker in securities issued by this company and/or in

securities in respect of this company HSBC and its affiliates will from time to time sell to and buy from customers the securities/instruments (including derivatives) of companies covered in HSBC Research on a principal or agency basis.

Analysts, economists, and strategists are paid in part by reference to the profitability of HSBC which includes investment banking revenues.

For disclosures in respect of any company mentioned in this report, please see the most recently published report on that company available at www.hsbcnet.com/research.

Additional disclosures 1 This report is dated as at 09 October 2013. 2 All market data included in this report are dated as at close 07 October 2013, unless otherwise indicated in the report. 3 HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its

Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking and Research businesses to ensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4 HSBC is acting as Joint Sponsor, Joint Global Co-ordinator and Joint Bookrunner regarding the proposed listing of Power Asset Holding's Hong Kong Electric assets.

18

Cheung Kong Infra (1038 HK) Electric Utilities 9 October 2013

abc

Disclaimer * Legal entities as at 8 August 2012 ‘UAE’ HSBC Bank Middle East Limited, Dubai; ‘HK’ The Hongkong and Shanghai Banking Corporation Limited, Hong Kong; ‘TW’ HSBC Securities (Taiwan) Corporation Limited; 'CA' HSBC Bank Canada, Toronto; HSBC Bank, Paris Branch; HSBC France; ‘DE’ HSBC Trinkaus & Burkhardt AG, Düsseldorf; 000 HSBC Bank (RR), Moscow; ‘IN’ HSBC Securities and Capital Markets (India) Private Limited, Mumbai; ‘JP’ HSBC Securities (Japan) Limited, Tokyo; ‘EG’ HSBC Securities Egypt SAE, Cairo; ‘CN’ HSBC Investment Bank Asia Limited, Beijing Representative Office; The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch; The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch; The Hongkong and Shanghai Banking Corporation Limited, Seoul Branch; HSBC Securities (South Africa) (Pty) Ltd, Johannesburg; HSBC Bank plc, London, Madrid, Milan, Stockholm, Tel Aviv; ‘US’ HSBC Securities (USA) Inc, New York; HSBC Yatirim Menkul Degerler AS, Istanbul; HSBC México, SA, Institución de Banca Múltiple, Grupo Financiero HSBC; HSBC Bank Brasil SA – Banco Múltiplo; HSBC Bank Australia Limited; HSBC Bank Argentina SA; HSBC Saudi Arabia Limited; The Hongkong and Shanghai Banking Corporation Limited, New Zealand Branch incorporated in Hong Kong SAR

Issuer of report

The Hongkong and Shanghai Banking Corporation Limited Level 19, 1 Queen’s Road Central

Hong Kong SAR

Telephone: +852 2843 9111

Telex: 75100 CAPEL HX

Fax: +852 2596 0200

Website: www.research.hsbc.com

This document has been issued by The Hongkong and Shanghai Banking Corporation Limited (“HSBC”) in the conduct of its Hong Kong regulated business for the information of its institutional and professional investor (as defined by Securities and Future Ordinance (Chapter 571)) customers; it is not intended for and should not be distributed to retail customers in Hong Kong. The Hongkong and Shanghai Banking Corporation Limited is regulated by the Hong Kong Monetary Authority. All enquires by recipients in Hong Kong must be directed to your HSBC contact in Hong Kong. If it is received by a customer of an affiliate of HSBC, its provision to the recipient is subject to the terms of business in place between the recipient and such affiliate. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. HSBC has based this document on information obtained from sources it believes to be reliable but which it has not independently verified; HSBC makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of the Research Division of HSBC only and are subject to change without notice. HSBC and its affiliates and/or their officers, directors and employees may have positions in any securities mentioned in this document (or in any related investment) and may from time to time add to or dispose of any such securities (or investment). HSBC and its affiliates may act as market maker or have assumed an underwriting commitment in the securities of companies discussed in this document (or in related investments), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform investment banking or underwriting services for or relating to those companies. HSBC Securities (USA) Inc. accepts responsibility for the content of this research report prepared by its non-US foreign affiliate. All U.S. persons receiving and/or accessing this report and wishing to effect transactions in any security discussed herein should do so with HSBC Securities (USA) Inc. in the United States and not with its non-US foreign affiliate, the issuer of this report. In the UK this report may only be distributed to persons of a kind described in Article 19(5) of the Financial Services and Markets Act 2000 (FinancialPromotion) Order 2005. The protections afforded by the UK regulatory regime are available only to those dealing with a representative of HSBC Bank plc in the UK. In Singapore, this publication is distributed by The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch for the general information of institutional investors or other persons specified in Sections 274 and 304 of the Securities and Futures Act (Chapter 289) (“SFA”) and accredited investors and other persons in accordance with the conditions specified in Sections 275 and 305 of the SFA. This publication is not a prospectus as defined in the SFA. It may not be further distributed in whole or in part for any purpose. The Hongkong and Shanghai Banking Corporation Limited Singapore Branch is regulated by the Monetary Authority of Singapore. Recipients in Singapore should contact a "Hongkong and Shanghai Banking Corporation Limited, Singapore Branch" representative in respect of any matters arising from, or in connection with this report. In Australia, this publication has been distributed by The Hongkong and Shanghai Banking Corporation Limited (ABN 65 117 925 970, AFSL 301737) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). Where distributed to retail customers, this research is distributed by HSBC Bank Australia Limited (AFSL No. 232595). These respective entities make no representations that the products or services mentioned in this document are available to persons in Australia or are necessarily suitable for any particular person or appropriate in accordance with local law. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. This publication is distributed in New Zealand by The Hongkong and Shanghai Banking Corporation Limited, New Zealand Branch incorporated in Hong Kong SAR. In Japan, this publication has been distributed by HSBC Securities (Japan) Limited. It may not be further distributed in whole or in part for any purpose. In Korea, this publication is distributed by The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch ("HBAP SLS") for the general information of professional investors specified in Article 9 of the Financial Investment Services and Capital Markets Act (“FSCMA”). This publication is not a prospectus as defined in the FSCMA. It may not be further distributed in whole or in part for any purpose. HBAP SLS is regulated by the Financial Services Commission and the Financial Supervisory Service of Korea. In Canada, this document has been distributed by HSBC Bank Canada and/or its affiliates. Where this document contains market updates/overviews, or similar materials (collectively deemed “Commentary” in Canada although other affiliate jurisdictions may term “Commentary” as either “macro-research” or “research”), the Commentary is not an offer to sell, or a solicitation of an offer to sell or subscribe for, any financial product or instrument (including, without limitation, any currencies, securities, commodities or other financial instruments). © Copyright 2013, The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited. MICA (P) 118/04/2013, MICA (P) 068/04/2013 and MICA (P) 110/01/2013

abc

Metals and Mining

EMEA Andrew Keen Global Sector Head, Metals and Mining +44 20 7991 6764 [email protected]

Thorsten Zimmermann, CFA +44 20 7991 6835 [email protected]

Vladimir Zhukov +7 495 783 8316 [email protected]

Emma Townshend +27 21 794 8345 [email protected]

Derryn Maade + 27 11 676 4519 [email protected]

North America & Latin America James Steel +1 212 525 3117 [email protected]

Patrick Chidley, CFA +1 212 525 4915 [email protected]

Botir Sharipov, CFA +1 212 525 5150 [email protected]

Howard Wen +1 212 525 3726 [email protected]

Leonardo A Correa +55 11 3847 5433 [email protected]

Luiz G Fornari + 55 11 3847 5436 [email protected]

Asia Simon Francis Regional Head of Metals and Mining, Asia Pacific +852 2996 6620 [email protected]

Thomas Zhu, CFA +852 2822 4325 [email protected]

Chris Chen +852 2822 4277 [email protected]

Jeff Yuan +852 3941 7010 [email protected]

Brian Cho +822 3706 8750 [email protected]

Jigar Mistry, CFA +91 22 2268 1079 [email protected]

Jena Han +822 3706 8772 [email protected]

Energy

Europe David Phillips Global Sector Co-head, Oil and Gas +44 20 7991 2344 [email protected]

Peter Hitchens +44 20 7991 6822 [email protected]

Phillip Lindsay +44 207 991 2577 [email protected]

Kirtan Mehta, CFA +91 80 3001 3779 [email protected]

CEEMEA Bülent Yurdagül +90 212 376 46 12 [email protected]

Ildar Khaziev, CFA +7 495 645 4549 [email protected]

Latam Luiz F Carvalho + 55 11 3371 8178 [email protected]

Filipe M Gouveia + 55 11 3847 5451 [email protected]

Asia Thomas Hilboldt Regional Head of Oil, Gas and Petrochemical Research, Asia Pacific +852 2822 2922 [email protected]

Dennis Yoo, CFA +852 2996 6917 [email protected]

Kumar Manish +91 22 2268 1238 [email protected]

Alok P Deshpande +91 22 681245 [email protected]

SI Tingting +852 2996 6590 [email protected]

Chemicals

Europe Dr Geoff Haire +44 20 7991 6892 [email protected]

Sebastian Satz, CFA +44 20 7991 6894 [email protected]

Jesko Mayer-Wegelin, CFA +49 211 910 3719 [email protected]

CEEMEA Yonah Weisz +972 3 710 1198 [email protected]

Sriharsha Pappu, CFA +971 4 423 6924 [email protected]

Nicholas Paton, CFA + 971 4 423 6923 [email protected]

Asia Dennis Yoo, CFA +852 2996 6917 [email protected]

Utilities

Europe Adam Dickens +44 20 7991 6798 [email protected]

Verity Mitchell +44 20 7991 6840 [email protected]

Asia Jenny Cosgrove Regional Head of Utilities and Alternative Energy, Asia Pacific +852 2996 6619 [email protected]

Arun Kumar Singh Analyst +91 22 2268 1778 [email protected]

Gloria Ho +852 2996 6941 [email protected]

Summer Y Y Huang +852 2996 6976 [email protected]

Latin America Sandra Boente +1 212 525 4441 [email protected]

Osmar Camilo +55 11 3847 9502 [email protected]

CEEMEA Levent Bayar Analyst +90 212 376 46 17 [email protected]

Dmytro Konovalov +7 495 258 3152 [email protected]

Alternative Energy

Jenny Cosgrove Regional Head of Utilities and Alternative Energy, Asia Pacific +852 2996 6619 [email protected]

Charanjit Singh +91 80 3001 3776 [email protected]

Gloria Ho +852 2996 6941 [email protected]

Specialist Sales

Annabelle O'Connor +44 20 7991 5040 [email protected]

James Lesser +44 207 991 1382 [email protected]

Global Natural Resources & Energy Research Team