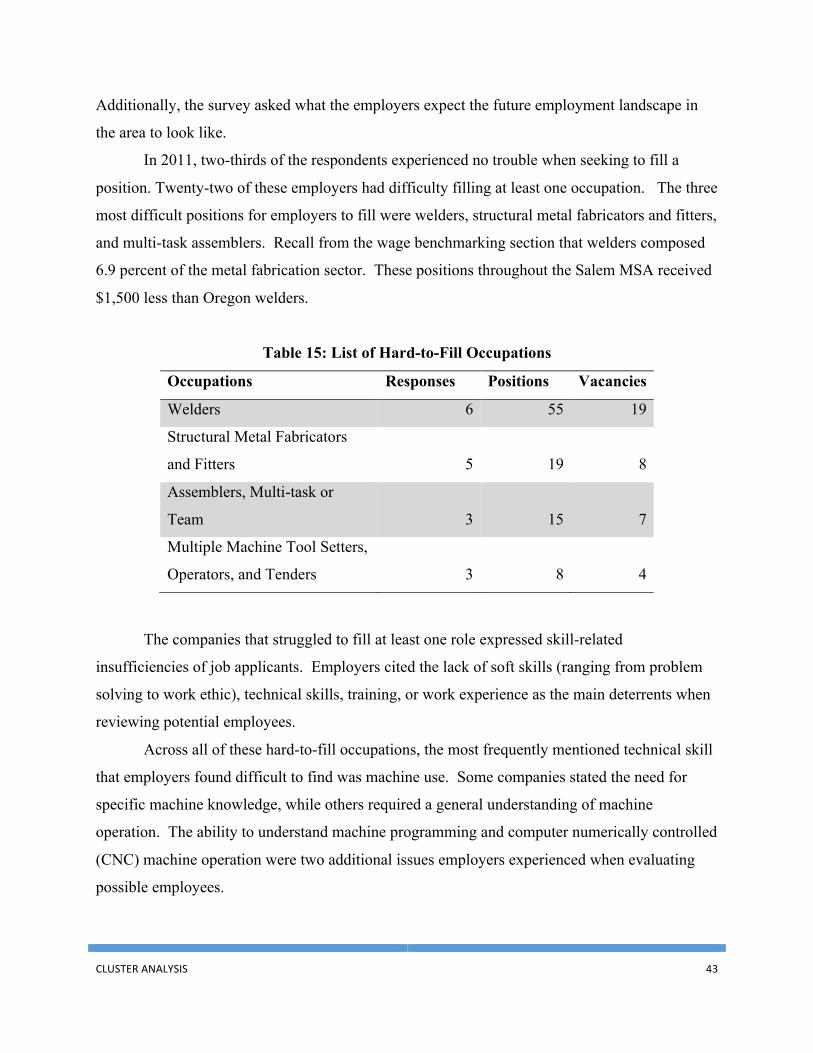

Embed Size (px)

Citation preview

CLUSTER ANALYSIS 1

Cluster Analysis of the Fabricated Metals

Manufacturing Sector in Salem, Oregon

Prepared by:

Phillip Andrews

Spencer Gibson

Under the supervision of

Professor Bruce Blonigen

Prepared for:

City of Salem, Urban Development

CLUSTER ANALYSIS 2

Executive Summary

This study examines the potential for growth and development of a cluster of economic activity

in the metal fabrication industry in the Salem, Oregon area. After surveying the literature to

understand the factors that affect the size of a manufacturing cluster, we proceed to examine

growth potential in Salem’s metal fabrication sector from a number of perspectives. We first go

through a series of benchmarking exercises to understand how Salem’s metal fabrication sectors

compare in various dimensions to other areas in Oregon and even nationally. This allows one to

not only identify current strengths and weaknesses of the current sector, but also provide a

perspective on how much the sector could realistically expect to grow and strengthen. The

second part of our analysis takes a closer look at specific features of the Salem’s fabrication

metal sector that the cluster literature would suggest is important for evolving a healthy cluster.

The first is linkages between upstream and downstream sectors. We undertake an input-output

analysis of the metal fabrication industry to identify the importance of these vertical relationships

for the sector. Second, the cluster literature stresses the importance of a specialized and trained

shared workforce. We examine the current education and training programs in the Salem area to

support the types of workers required by the metal fabrication sector.

Benchmarking

We begin by benchmarking the state of the Salem metal fabrication labor force at three levels:

national, state, and county. We examine the data not only across regions, but also examine

trends over time. Additionally, the wages of the highest concentrated occupations within the

industry of these separate regions are examined to understand wage implications for potential

employees in the Salem area. Finally, we undertake a statistical analysis of the size of

fabricated metal sectors nationally to better understand how the Salem area compares, as well as

inform us as to how much larger it could conceivably become.

Employment Benchmarking

Using Census Bureau data on employment and wages in Salem and other comparison regions,

we find:

CLUSTER ANALYSIS 3

• From 1998 to 2011 employment in the the fabricated metals sector in the U.S. and

Oregon decreased by 27% and 20%, respectively. Over the same time period, the

fabricated metals sector diminished by 61% in Marion Country, the largest drop of

the top metal fabricating counties in the state. The next largest declines in fabricated

metals employment in the state were Multnomah and Lane counties at 31.2% and 12.6%,

respectively.

• Metal fabrication employment as a percentage of manufacturing employment in the U.S.

shifted from 10.7% to 12.1% over the same time period. In Oregon, this shift was from

9% to 12.3%. Marion County was the only county to show a decrease in fabricated

metals share of manufacturing employment of all those analyzed in this research.

This decrease was from 15.2% of manufacturing employment to 8.3%.

• In 2012, the U.S. industry grew by 3.48% and Oregon by 3.3%. Marion County's metal

fabrication sector grew by 7.6%, the highest of all counties analyzed. This suggests

that there is some rebound now occurring in the sector in Marion county.

Wage Benchmarking

Our analysis also benchmarks wages in Salem to those throughout the nation, Oregon, and the

Portland area. The top four production positions of the industry and first-line supervisor role are

used to understand the disparity of wages in Salem.

• The top production occupation, machinist, received a salary $6,720 higher in the

Portland area compared to Salem.

• Lower wages occur in three of the top four production positions, or 25 percent of

employment, in Salem when compared to all three regions.

Statistical Analysis

Using employment and population data at the MSA level, an empirical model can be developed

that explains most of the variation within the data. Our regression analysis finds:

CLUSTER ANALYSIS 4

• In 2010, employment within the fabricated metals industry in the Salem metro area was

946. Our model predicts that Salem, based only on the size of its population and

manufacturing sector, should have 1,134 employees within this sector. This simple

model suggests that Salem has the opportunity to increase employment by at least

188 employees.

• For the size of Salem’s fabricated metal industry, relative to the size of their

manufacturing sector, to be equal with the national mean, employment would have to

increase by 299.

• Continuing with this same benchmarking process, if Salem wanted to be one standard

deviation above the national mean, employment in the fabricated metal sector would

have to increase by 1,104.

After understanding and measuring the prospects for growth in Salem, we now turn our attention

to an empirical review of the cluster traits, namely demand conditions and the existence of

related and supporting industries.

Micro Analysis: Input-Output

Porter’s (1990) diamond of competitive advantages framework explains the importance of

demand conditions and the presence of related and supporting industries as being imperative to

fostering competitive advantages within industries. The input-output analysis examines both of

these traits and we find.

• Primary metals is the largest upstream industry (or supplier) for the fabricated metals,

consisting of 35.58% of total inputs within the industry.

• The largest downstream industries (or consumers) of fabricated metals are construction;

motor vehicle bodies, trailers, and parts manufacturing; and machinery. These

industries consume 16.10%, 13.34%, and 11.87% of total fabricated metal products

output, respectively.

• Architectural and structural metal products industry is the largest fabricated metals

subsector within the Salem metropolitan region. Detailed level construction industries

consume approximately 41.7% of all output in the platework and fabricated

CLUSTER ANALYSIS 5

structural products industry, and 44.3% of total output in the architectural and

structural.

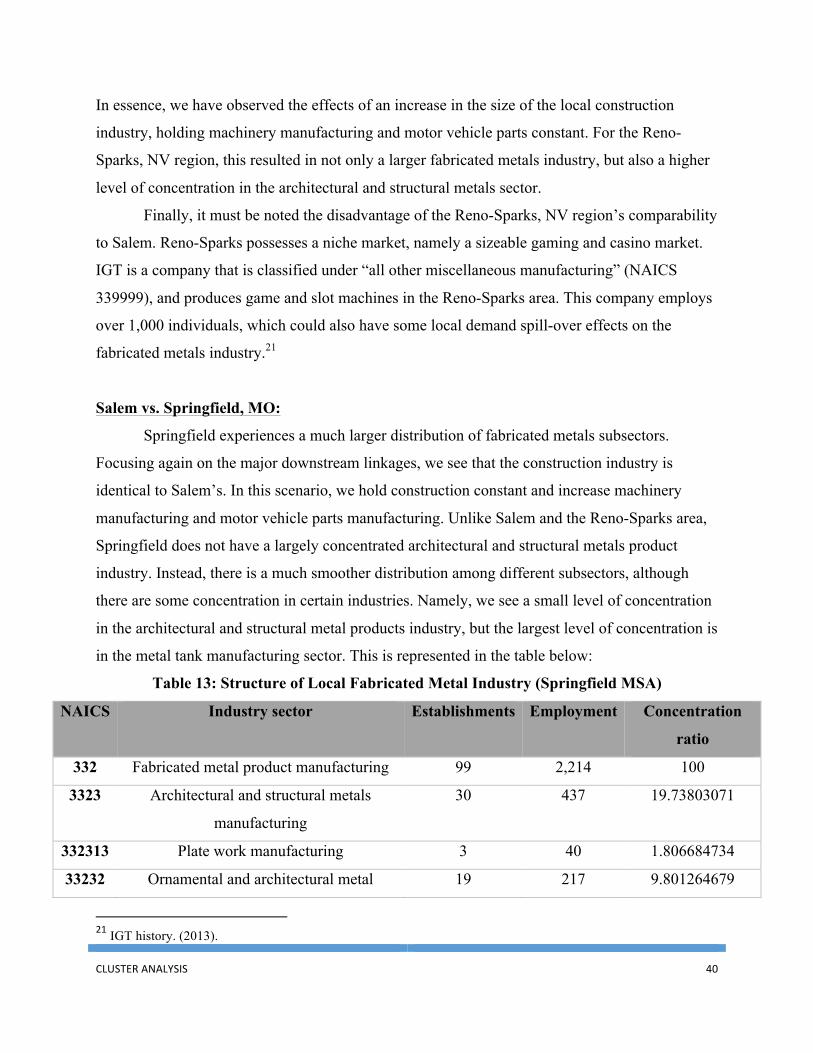

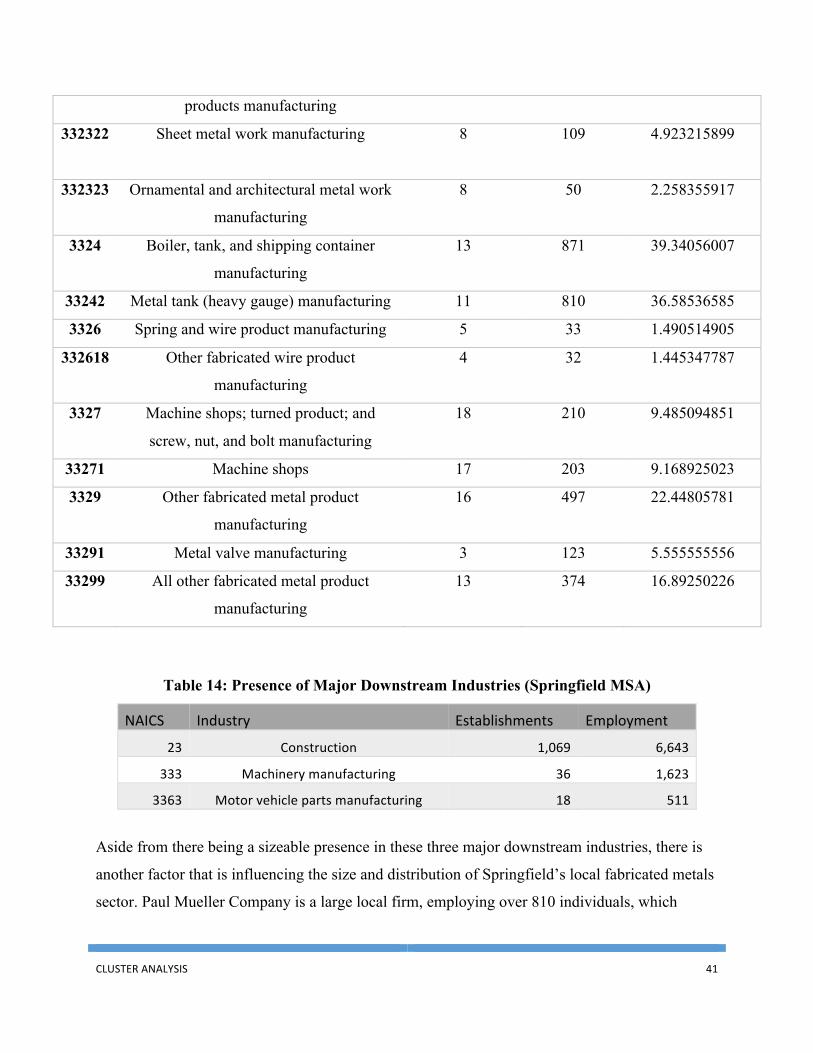

Case Study

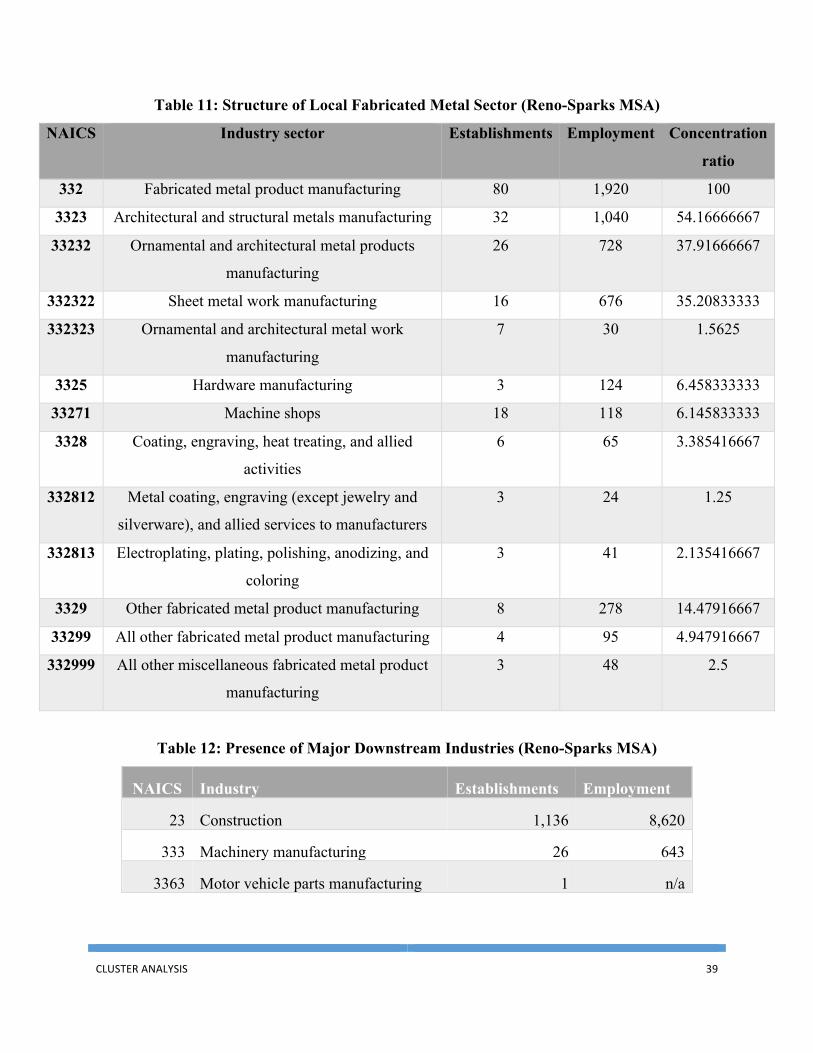

To better understand the role of downstream consumers for the size and health of the fabricated

metals sector, we examined a couple cities of similar size to Salem that had much larger

fabricated metals sectors. From our statistical analysis we found that comparable regions with

unusually high levels of employment in the fabricated metals sector were the Reno-Sparks, NV

and Springfield, MO regions. These regions can be compared and contrasted to Salem to identify

important discrepancies that may explain these differences in employment.

• Similar to Salem, the fabricated metal products industry in the Reno-Sparks, NV region is

heavily concentrated in architectural and structural metal products. However, the Reno-

Sparks region has almost 1,000 more employees in the fabricated metal industry

relative to Salem. The construction industry is larger in the Reno-Sparks area by just

over 2,000 employees, with identical levels of machinery and motor vehicle parts

manufacturing. Furthermore, gaming machines and systems to land-based casinos

provides a niche market with possible demand spillover effects.

• Similar to Salem, the Springfield, MO area has almost an equal level of employment

within their construction industry, yet has over 1,000 more employees in the

machinery manufacturing sector, with a measureable motor vehicle parts

manufacturing of 511 employees. Springfield has nearly 1,300 more employees in

the fabricated metal industry relative to Salem, with 810 of these employees working

in the metal tank manufacturing sector. Of the 810 employees within this metal

fabrication subsector, a single firm, Paul Mueller Company, employs between 250 to

499 workers.

These results reveal three major findings. First, the presence of downstream industries appears to

have an impact on a region’s local fabricated metals sector. Second, local niche markets may

have demand spillover effects. Finally, historical endowment, such as the presence of a large

preexisting firm can also result in large levels of employment.

CLUSTER ANALYSIS 6

Micro Analysis of Training Programs

Porter (1990) and others stress that specialized labor market can be crucial for the development

and maintenance of a large and healthy cluster. Thus, a final analysis in the paper examined the

existing workforce training programs in the Salem area. The process of comparing the

curriculums of the welding and manufacturing oriented programs at three schools within the state

(Chemeketa CC, Clackamas CC, and Mt. Hood CC) yields a comprehensive viewpoint of how

the regional labor force becomes specialized. Examination of these three schools curricula for

workers important to the fabricated metals sectors produced various conclusions about the state

of Chemeketa Community College.

• At Chemeketa, the training focuses on welding and CNC machining, whereas Mt. Hood

balances the distribution of training across welding and manual and CNC machining.

• The manufacturing and machining programs at Clackamas address a much larger range of

techniques and additional concentrations when compared to Chemeketa.

• The welding degree at Clackamas builds more advanced welding skills in the second year

of studies, unlike Chemeketa which instructs individuals in the techniques of CNC

machining.

This analysis shows that there is some variation in the training programs throughout the state and

that the programs at Chemekata may be inferior to others.

Policy Conclusions:

The findings from our micro analyses have lead us to the following policy implications:

• Develop a larger local supply chain, focusing on instigating growth within downstream

industries – the consumers of fabricated metal products.

• Improve the perception of manufacturing careers by linking high school students to

opportunities that incorporate them in the local industry.

• Reevaluate local training programs at Chemeketa Community College. Reach out to

local businesses to understand how important these training programs are (or could be).

Investigate policy options to strengthen the local vocational system's ability to provide

the necessary skills for workers required in the fabricated metals sector.

CLUSTER ANALYSIS 7

• Facilitate a professional network of local industry business owners and managers to build

a local flow of industry and technological knowledge.

These recommendations have the capability to promote growth, but may not have the influence

to fully develop, by themselves, the metal fabrication sector. Global, national, and statewide

factors can hinder the effectiveness of local development policy. We believe that positive and

negative external influences, both observable and unobservable, heavily drive industries like the

metal fabrication sector towards success or failure. This analysis has identified traits of the

industry that show potential for growth within Salem, but Salem's current position creates

challenges for economic developers.

CLUSTER ANALYSIS 8

I. Introduction The subject of industry agglomeration (or “clustering”) has been of great interest in

recent years to policy makers, and for good reason. If industries do tend to cluster, and if policy

and other economic incentives can help facilitate clustering, then there is the potential for urban

developers to expand their economies. Such knowledge is also valuable to business planners

when competing in a market. We see the importance of this issue given the potential it has in

creating economic value for different regions. If industries don’t cluster, the information is still

valuable because it may reduce unnecessary expenditures resulting from a city trying to form a

cluster that cannot occur.

This study seeks to analyze and understand the process and life cycle of industry

agglomeration with respect to fabricated metal production in Salem, Oregon. The United States

Census Bureau North American Industry Classification System (NAICS) defines fabricated

metals production as a subsector of manufacturing that transforms metals into intermediate or

end products. Firms in this sector take primary metal products (such as steel sheets or rods) and

then further modify them into a wide variety of more sophisticated metal products, from bolts

and screws to cell phone towers. Our study will examine the industry features of the fabricated

metals sector and its presence in Salem in order to analyze the prospects of growing a more

vibrant fabricated metals sector in this region.

An academic literature review provides a theoretical framework for understanding when,

where and why firms in different industries might cluster together. A benchmarking process of

employment and wages will build a standard for Salem’s metal fabrication industry. From there a

statistical analysis measures different degrees of concentration of various metro regions

throughout the nation, and provide additional benchmarks of growth for Salem.

We study the more prominent subsectors that occupy the Salem area by analyzing

national input-output accounts to understand the demand conditions of the industry. This is

benchmarked to the nation as a whole, and then compared to other areas that are comparable

with respect to population and manufacturing characteristics. We want to know if there are

unexploited opportunities for Salem developers, and if Salem can foster the agglomeration of this

industry. To explore such possibilities, we examine similar metro regions with higher levels of

metal manufacturing employment and compare their related downstream industries.. Factor

CLUSTER ANALYSIS 9

conditions, such as a specialized labor pool and educational institutions, can also influence

agglomeration. To understand both of these conditions, we employ a technique to compare

training programs in Salem to other local regions. Possible policy recommendations are derived

from these analyses.

The city of Salem wants to expand their economy through diversification of their

manufacturing sector. The food and beverage industry dominates the manufacturing sector of

Salem's economy, which has one of the lowest average wages of all manufacturing sectors.1 In

order to expand their economy, economic developers want to grow and diversify the

manufacturing sector, starting with the metals industry. If they can understand how this industry

functions, then they hope to exploit opportunities through effective policy that would act as a

catalyst to facilitate growth in the fabricated metals sector.

Paper Organization and Structure

In order to more easily digest the information within this paper, the analyses will be

broken down into different sections. The sections will be categorized as follows:

II. Literature Review and Framework: We first examine the preexisting literature on

the topic of industry agglomeration in order to gain a theoretical framework in which to analyze

our research question. This is followed by a discussion of our methodology, sources of data, and

limitations regarding the data and subsequent conclusions.

III. Benchmarking: We begin by looking at employment and wage trends within Salem

and contrast these them to our benchmark regions. After examining these trends, we conduct a

statistical analysis that utilizes an empirical model to generate predicted employment levels

given population and manufacturing statistics. We generate residual values and a deviation

variable to measure how Salem’s employment levels differ from its predicted value, and then

assess the prospects for growth.

IV. Micro Analysis: After understanding where Salem is relative to other regions, we

begin to analyze why it is where it is. First, we conduct an input-output analysis at both the

summary and detailed level. The detailed level input-output accounts will be constructed by first

identifying which subsectors are located in the Salem area and which sectors are large buyers

1 Oregon Employment Department, (2013).

CLUSTER ANALYSIS 10

and sellers of fabricated metals products. Once we have developed an understanding of the

supply chain, we look at education and training programs to evaluate the strength and quality of

the local labor pool.

V. Case Study: Up to this point, we have analyzed employment and wage trends over

time; measured how employment in the local industry deviates from what our empirical model

predicts; constructed a national supply chain using the relevant subsectors within the Salem

region; and how education and training programs affect the quality of the labor pool. In this

section we return to the empirical model to create a sample of regions comparable to Salem with

respect to population and manufacturing statistics. We then conduct a case study of those

comparable regions that experience higher levels of deviation between their observed levels of

employment and their predicted levels of employment.

VI. Policy Recommendations: Using the case study and our analyses, we derive

different policy recommendations that economic developers in Salem can utilize to grow their

fabricated metals sector. The recommendations drawn stay consistent with both the theoretical

framework and the empirical evidence.

VII. Conclusion: A review of the work and its limitations, as well as possible work to be

done moving forward.

Appendix: Contains additional information regarding the sources of data for the input-

output analysis. A visual representation of the national industry supply chain is also provided.

along with a comprehensive account of the detailed level input-output linkages.

II. Framework We begin by developing a theoretical understanding of a cluster, and the factors that lead

to clusters, through a comprehensive literature review. Previous theoretical and empirical work

provides the foundation for applying a cluster analysis of the fabricated metal manufacturing

industry within Salem. A methodology section frames the analytical process and their respective

purposes. In short, the framework section provides a background understanding of the empirical

analysis and its applications in the use of policy.

Cluster Identification:

CLUSTER ANALYSIS 11

As we begin to investigate the possibilities of expanding the metal industry of Salem, a

developed understanding of business cluster formation and activity will guide our analysis. In

2006, Joseph Cortright of the Brookings Institution finds that the literature produces a range of

definitions for an agglomeration, industrial district, and various other terms that equate to the

term "cluster."2 Instead of creating a hard definition for cluster activity, Cortright finds

characteristics in the industrial structures of firms that lead to agglomeration, ranging from labor

market pooling to a firm's competitive strategy.

Alfred Marshall

Alfred Marshall, an early 20th century economist, is widely recognized as the first

pioneer in understanding agglomeration. In his Principles of Economics text, he observed the

industrial district of England and determined three reasons for why firms of similar industries

locate close together: labor market pooling, supplier specialization, and knowledge spillovers.3

These three explanations for industrial organization became known as Marshall's Trinity. The

first, labor market pooling, benefits both firms and workers, as firms have a large labor force to

choose from and workers can optimize the employment of their specialized skills. Secondly,

close proximity allows for the scale necessary in creating a goods market that harbors

specialization of firms. Finally, these industrial districts that Marshall observed create an

environment that allows for easy transfer of knowledge from firm to firm.

Localization vs. Urbanization Economies

The 1950s ushered in the organization of thoughts that formed the field of regional

science building on the ideas of Marshall and others. In his book, The Location of Economic

Activity, E.M Hoover developed the distinction between two types of agglomeration—

localization and urbanization economies4. A localization economy represents a cluster that

forms because of the gains firms obtain from locating near similar firms. An urbanization

economy produces positive externalities from locating near firms in various industries, a quality

associated with large urban areas. These distinctions allow for economists to understand how a

2Cortright, J., & Brookings Institution. (2006). 3 Marshall, A. (1920). 4 Hoover, E. M. (1948).

CLUSTER ANALYSIS 12

particular industrial structure formed. An urban area may grow because of a localization

economy, or agglomeration may occur because of the diverse labor market in a large city. The

differentiation between the two economies of scale helps identify the factors that lead to the

development of an industrial district.

The ideas of regional scientists led to a deeper understanding of urbanization economies

by historian Jane Jacobs. In her book The Economies of Cities, Jacobs concluded that the size

and diversity of cities promote the formulation of new ideas and technologies5. The

accumulation of diverse people, industries, and traded goods play a large role in the incubation

of human capital. This idea relates to the large urban setting of an industry, but also has

credence in explaining the formation of new ideas in a localization economy. Similar firms

organizing in close proximity and interacting through flows of goods and labor can develop new

ideas to advance their local industry.

Flexible Specialization

As geographers, urban economists, and sociologists continued to research the dynamics

of regional economics, Michael Piore and Charles Sabel believed the concentration of mass

markets was leading to increased consumer demand for variety and quality. In 1984 Piore and

Sabel published a book, The Second Industrial Divide, which stated that this increased demand

and the current technological improvements allowed for smaller, craft-oriented firms to beat out

larger, inflexible firms6. The two social scientists did a case study of the Italian industrial

districts and found that these regions were not dominated by big firms with large economies of

scale, but rather by smaller businesses who took on a flexible specialization. These firms were

able to take advantage of market niches and evolving demand in industries that ranged from

ceramics to industrial manufacturing. The institutions and culture of the communities these

firms organized in dissipated some of the advantages of scale through group buying, technology

development, and market research. This way of organizing business is an alternative to large-

scale production and highlights the advantages that specialized clusters can create.

5 Jacobs, J. (1969). 6 Piore, M. J., & Sabel, C. F. (1984).

CLUSTER ANALYSIS 13

"The Diamond of Competitive Advantage"

In 1990, Michael Porter developed the "diamond of competitive advantage" in The

Competitive Advantage of Nations, which highlighted four factors responsible for industry

clusters7:

• Factor Conditions: These factors of production are ones that all firms can benefit from.

For example, a specialized labor market, strong infrastructure, educational institutions,

and other externalities. If these factors are only present in one area, the probability of

agglomeration greatly increases.

• Demand Conditions: An established set of sophisticated and demanding local customers

is required for clustered firms to remain productive and keep technology up to date.

• Related and Supporting Industries: A strong base of local suppliers and related

industries will allow firms to have a connected web of upstream and downstream

relationships. This will lead to greater efficiency as firms evolve and improve their own

technological progression.

• Firm strategy, structure, and rivalry: If firms continually update their strategy and

invest in new capital, they will remain competitive. Firms with similar strategies

competing in close proximity will create a strong industrial structure. Healthy rivalry can

motivate firms to compete regionally and improve the industry dynamics.

Porter emphasized the importance firms put in understanding how location will affect

their strategy and performance. These four factors influence firms and explain why industry

clusters can be more competitive than isolated firms.

Cluster Traits

These studies propose a range of possible characteristics that lead to the formation of an

industrial cluster. Porter identifies factor conditions, demand conditions, related and supporting

industries, and regional strategy and competition as key determinants of how firms choose where

to locate. The difference between localization and urbanization economies shows that

agglomeration can occur because of labor market conditions, supplier localization, or the

potential for technological progress. Another trait of a cluster is specialization because the close 7 Porter, M. E. (1990).

CLUSTER ANALYSIS 14

proximity can create the scale necessary in developing a specific product of a regionally

integrated supply chain. Flexible specialization is an alternative form of business organization

and forms because firms look to take advantage of market niches and changing demand.

Cluster Ambiguity

Finally, Cortright stresses the controversy that pertains to cluster analysis in both the

theoretical and political realm. In Cortright's view, "Academics are looking to simplify, to

abstract, and to generalize: to find relationships that are consistent across a wide range of firms

and context."8 On the other hand, policymakers take a pragmatic approach that looks for an

explanation of challenges they see in their economic community. Feser and his colleagues, in

their paper, "Incorporating Spatial Analysis in Applied Industry Cluster Studies," explain this

ambiguity as "the complexity of the cluster concept as well as the significant range of policies

that clusters might inform dictate that no single definition is appropriate for all analytical or

policy needs."9 We keep this in mind as we explore the wide spectrum that encompasses cluster

analysis in the policy arena.

National Industry Cluster Templates

Edward Feser and Edward Bergman's study, "National Industry Cluster Templates: A

Framework for Applied Regional Cluster Analysis," attempts to create templates for the different

manufacturing clusters in the nation by using information on the 1994 input-output accounts

released by the Bureau of Economic Analysis10. They use the Standard Industrial Classification

(SIC) system, which defines the subsectors of various industries, to establish the direct and

indirect linkages between firms. Correlation analysis techniques based on patterns of sales and

purchases across 362 industries are used to develop a national set of benchmarks for industrial

clusters that have no regional context. These benchmarks "represent strategically important

alignments of detailed sectors."

Feser and Bergman found the metalworking cluster to be the largest in the nation due to

the large number of sectors that encompass primary metal, fabricated metal, and industrial

8Cortright, J., & Brookings Institution (2006). 9Feser, E. J., and others. (2001). 10 Feser, E., & Bergman, E. (February 01, 2000).

CLUSTER ANALYSIS 15

machinery industries, as well as sectors that spill into the electronic and electrical equipment

industries. The metalworking cluster shares component industries with 14 of the other 23

clusters in the nation that they identified.

In their conclusion, Feser and Bergman state, "The national templates do not constitute a

definitive 'vision' of the industry mix that could or even should develop in a region, but rather a

baseline picture of the regional industry mix across broad supply chains." The industries that

they have used in this study dip into a multitude of clusters and show an overarching view of the

possibilities of agglomeration in particular regions.

Christina Kelton, Margaret Pasquale, and Robert Rebelein update the work of Feser and

Bergman because of the change from collecting industry data using the SIC system to NAICS11.

Their study uses the 1997 input-output tables, which are based on the NAICS industrial

classifications. Using the same industrial correlation techniques as Feser and Bergman, the

NAICS industries produce substantially more concentrated results. The improved data allows

for the identification of 61 national cluster templates. In the study they used 483 different

NAICS classification, 88 of them occupying the metalworking cluster. Fabricated Metal

Products was the 41st ranked cluster, dipping into 19 various industries. Industrial Machinery

and Equipment was the 15th ranked cluster, encompassing 40 of the NAICS industries.

Kelton, Pasquale, and Rebelein concluded that these templates of the various national

clusters will create a foundation for more in depth regional analyses. This study has more

specific industry data, but creates a similar perspective of the cluster framework in the U.S that

Feser and Bergman found. The templates in both studies give analysts and policymakers

interested in cluster formation in a region a starting point to develop a more detailed

investigation.

Methodology In order to understand what types of industry characteristics and relationships would

determine a cluster we first examine the fabricated metal industry and all of its relevant

subsectors in the Salem region. From there, it becomes a matter of how to analyze the industry in

11 Kelton, C. M. L., Pasquale, M. K., & Rebelein, R. P. (April 01, 2008).

CLUSTER ANALYSIS 16

a meaningful way. We will do this by benchmarking Salem against other regions and further

analyzing its prospects for growth within this industry. Following this, we conduct a series of

micro analyses to develop an empirical review of the theoretical framework, including demand

conditions, factor conditions, and existence of related and supporting industries. Each of these

techniques will build the foundation for possible policy recommendations.

Benchmarking

This approach includes analyzing national, state, and county level trends. Specifically, we

begin by examining the past and present state of the fabricated metals industry in terms of

employment. By understanding these different regions we create a benchmark for growth within

Salem. Next, we conduct a brief analysis of the current state of wages within the industry. Using

U.S., Oregon, and Portland wage statistics, we build a thorough understanding of the wage

structure in Salem.

After having developed an understanding of where this industry has been and where it is

headed, we then begin to estimate and measure the prospect for growth in Salem. Using data

aggregated at the metropolitan (MSA) level, we construct an empirical model which uses the

level of fabricated metal employment across all MSAs relative to employment in the

manufacturing sector. We use this model to compare Salem’s actual level of employment to what

the model predicts. . Finally, we measure how much growth is required to reach both a national

level, and a cluster level of employment.

Micro Analysis

After understanding the potential for growth in Salem, we undergo a series of micro

analyses. Using the diamond of competitive advantagedeveloped by Porter, we evaluate Salem’s

capacity to foster a cluster. We begin by examining demand conditions and the existence of

related and supporting industries by means of an input-output analysis. Once a supply chain is

developed, we can apply these national linkages on a regional level to determine whether or not

the existence of downstream industries promotes growth within the industry at the MSA level.

The analysis of the Salem area concludes by assessing the local development of a quality

labor pool. Training programs throughout the state are compared and contrasted to establish a

thorough evaluation of relative fabricated metals training in Salem. Moreover, the disparities

CLUSTER ANALYSIS 17

between the different programs may suggest what the local training programs do well and how

they can improve.

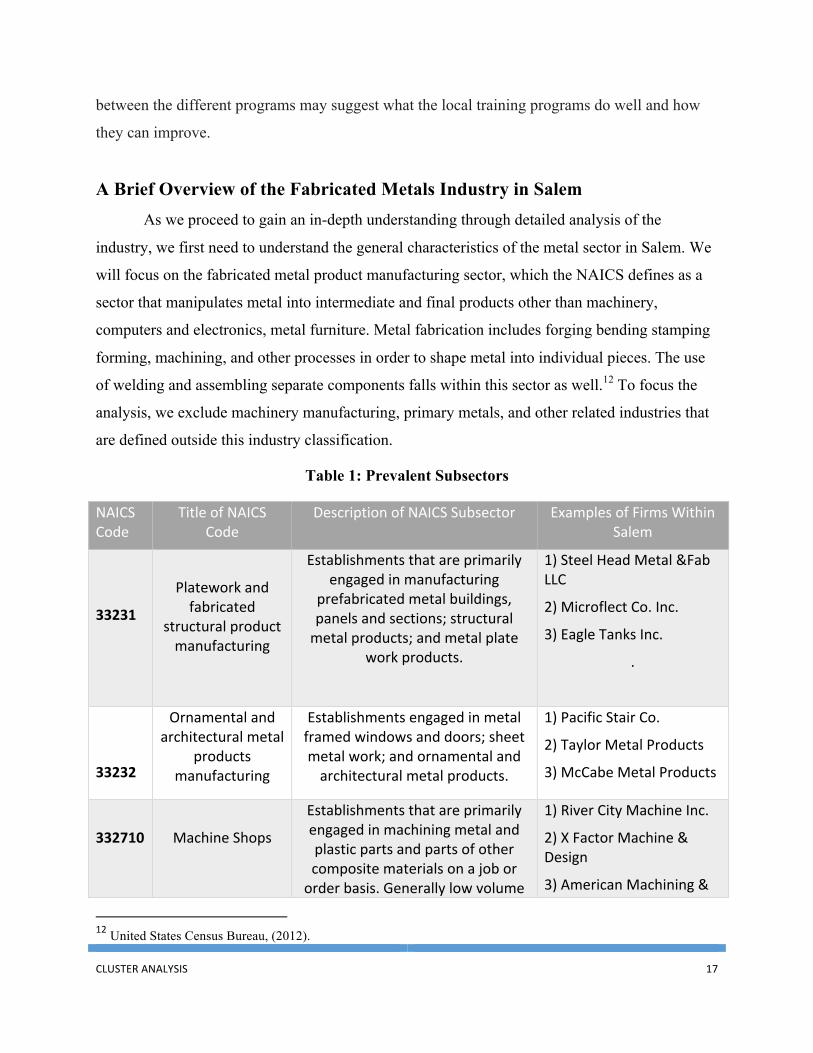

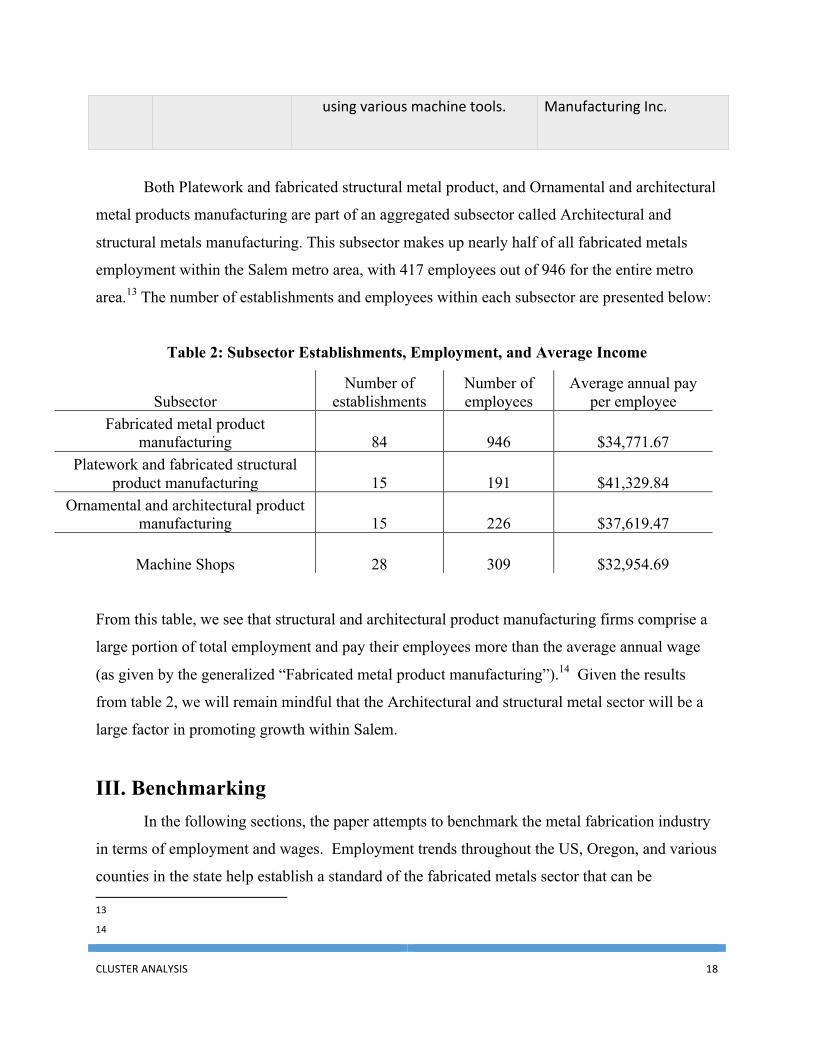

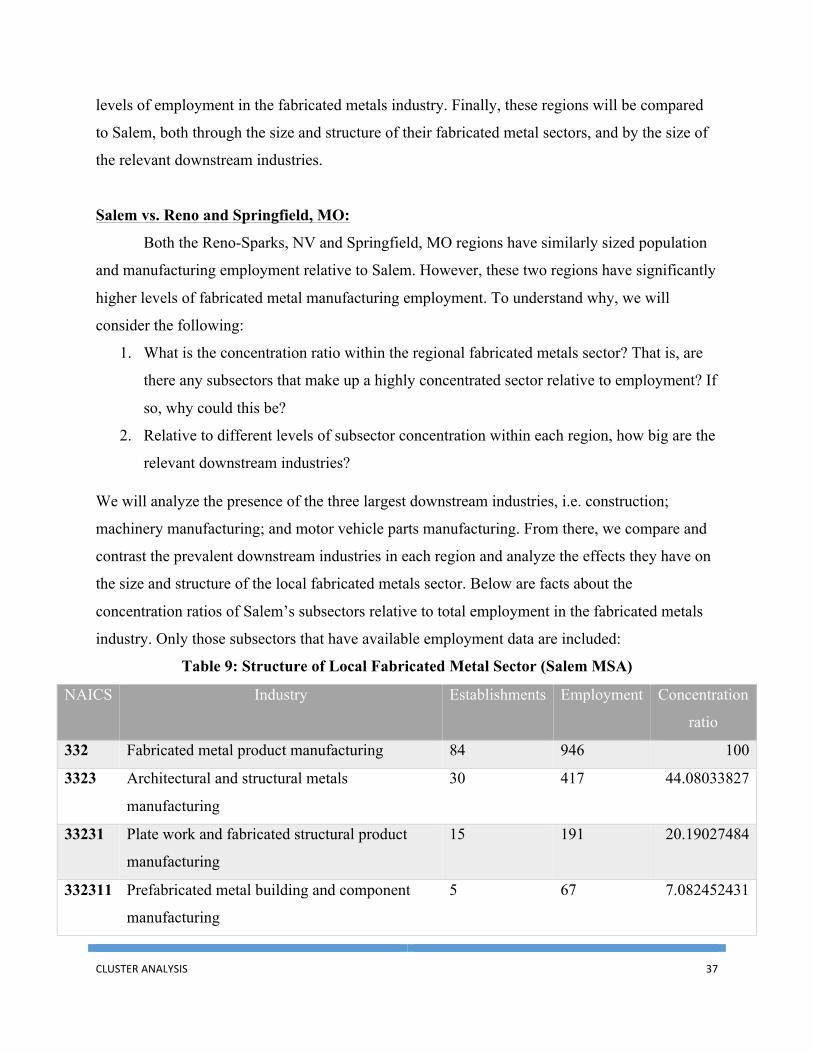

A Brief Overview of the Fabricated Metals Industry in Salem As we proceed to gain an in-depth understanding through detailed analysis of the

industry, we first need to understand the general characteristics of the metal sector in Salem. We

will focus on the fabricated metal product manufacturing sector, which the NAICS defines as a

sector that manipulates metal into intermediate and final products other than machinery,

computers and electronics, metal furniture. Metal fabrication includes forging bending stamping

forming, machining, and other processes in order to shape metal into individual pieces. The use

of welding and assembling separate components falls within this sector as well.12 To focus the

analysis, we exclude machinery manufacturing, primary metals, and other related industries that

are defined outside this industry classification.

Table 1: Prevalent Subsectors

NAICS Code

Title of NAICS Code

Description of NAICS Subsector Examples of Firms Within Salem

33231

Platework and fabricated

structural product manufacturing

Establishments that are primarily engaged in manufacturing

prefabricated metal buildings, panels and sections; structural metal products; and metal plate

work products.

1) Steel Head Metal &Fab LLC

2) Microflect Co. Inc.

3) Eagle Tanks Inc.

.

33232

Ornamental and architectural metal

products manufacturing

Establishments engaged in metal framed windows and doors; sheet metal work; and ornamental and architectural metal products.

1) Pacific Stair Co.

2) Taylor Metal Products

3) McCabe Metal Products

332710

Machine Shops

Establishments that are primarily engaged in machining metal and plastic parts and parts of other composite materials on a job or order basis. Generally low volume

1) River City Machine Inc.

2) X Factor Machine & Design

3) American Machining &

12 United States Census Bureau, (2012).

CLUSTER ANALYSIS 18

using various machine tools. Manufacturing Inc.

Both Platework and fabricated structural metal product, and Ornamental and architectural

metal products manufacturing are part of an aggregated subsector called Architectural and

structural metals manufacturing. This subsector makes up nearly half of all fabricated metals

employment within the Salem metro area, with 417 employees out of 946 for the entire metro

area.13 The number of establishments and employees within each subsector are presented below:

Table 2: Subsector Establishments, Employment, and Average Income

Subsector Number of

establishments Number of employees

Average annual pay per employee

Fabricated metal product manufacturing 84 946 $34,771.67

Platework and fabricated structural product manufacturing 15 191 $41,329.84

Ornamental and architectural product manufacturing 15 226 $37,619.47

Machine Shops 28 309 $32,954.69 From this table, we see that structural and architectural product manufacturing firms comprise a

large portion of total employment and pay their employees more than the average annual wage

(as given by the generalized “Fabricated metal product manufacturing”).14 Given the results

from table 2, we will remain mindful that the Architectural and structural metal sector will be a

large factor in promoting growth within Salem.

III. Benchmarking In the following sections, the paper attempts to benchmark the metal fabrication industry

in terms of employment and wages. Employment trends throughout the US, Oregon, and various

counties in the state help establish a standard of the fabricated metals sector that can be 13 14

CLUSTER ANALYSIS 19

compared to the current and present state of Salem. Though regional circumstances shape each

area differently, building a standard of the industry allows for a systematic analysis of Salem's

opportunities to grow.

Employment Trends: United States, Oregon State, and Select Oregon Counties

Employment in the US manufacturing sector has decreased significantly since the late

1990s. Both the recession of the early 2000s and the Great Recession multiplied the effect of an

already shrinking manufacturing labor force. Market trends show an industry that continues to

grow out of the trough it reached at the beginning of 2010. This modest employment growth is

observed in a range of manufacturing industries: food, chemical, plastic and rubber products,

primary metals, fabricated metal products, machinery, and transportation equipment.

One of the manufacturing industries that experienced the post-recession advances of

interest is the metal fabrication sector. Since 1998, employment in the metal fabrication industry

decreased by roughly 300,000 jobs.15 In line with this decrease in employment, the number of

establishments has decreased by roughly 8,000 firms since 1998. The fall in employment was

mild at the beginning of the new millennium, but experienced a large drop off from 1.76 million

to 1.51 million jobs from 2001 to 2003 due to a recession and mill consolidation.16 The industry

never fully recovered because of globalization and the emergence of Asian markets. Following

2008, the labor force began to plummet and hit a low of 1.27 million employees in 2010. The

U.S. experienced significant job growth in the metal fabrication industry, adding 60,000 workers

to the labor force over the course of the next year. Since then, the Federal Reserve Bank of St.

Louis reported 2.3% growth in the last quarter of the 2011 and 3.48% growth over the course of

2012.

As the fabricated metals sector changed over the course of this time period, so did the

manufacturing industry. Manufacturing throughout the U.S. experienced a 32 percent decrease

in employment whereas the metal fabrication sector experienced an 18 percent drop in the

number of employees. With this information, we see that metal fabrication improved as a

percentage of manufacturing employment throughout the U.S. from 9.9 to 11.9 percent

15 United States Census Bureau, (1998-2011). 16 Duensing, L. (2013, March 21).

CLUSTER ANALYSIS 20

(FRED)17. Metal fabrication in the U.S. is one of the manufacturing sectors that improved since

the recent recession, Sustained growth over the past three years demonstrates the capability of

this manufacturing sector to improve into the future.

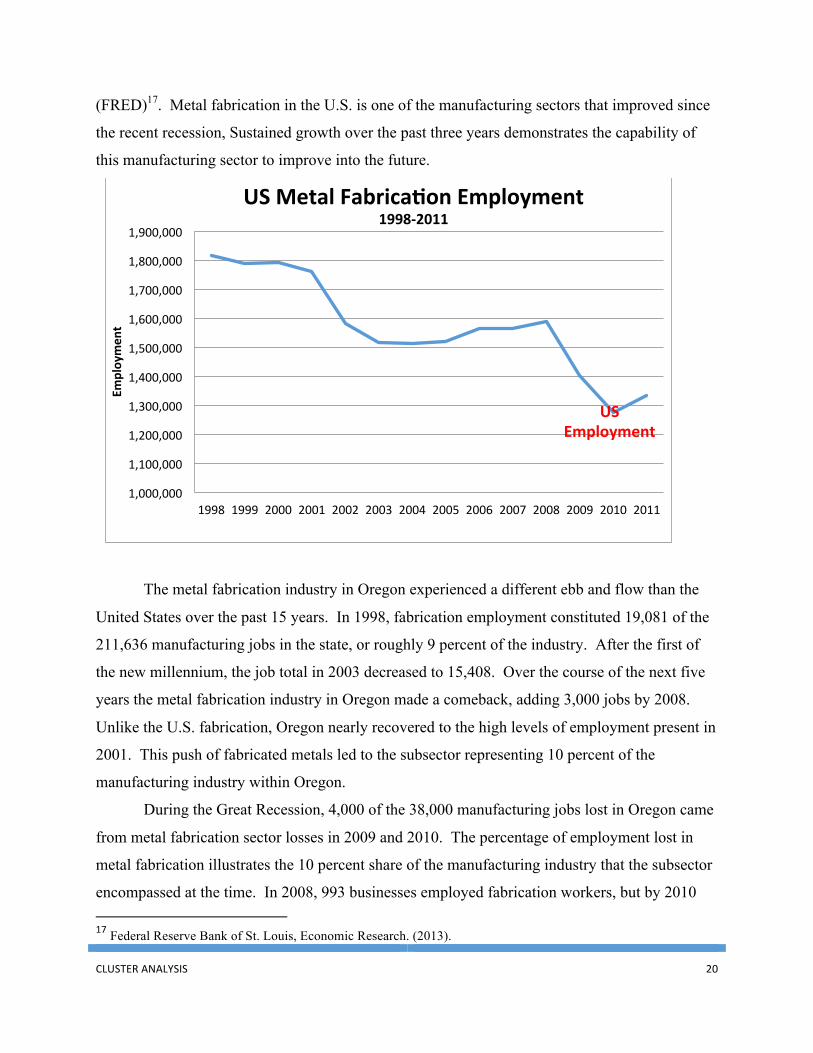

The metal fabrication industry in Oregon experienced a different ebb and flow than the

United States over the past 15 years. In 1998, fabrication employment constituted 19,081 of the

211,636 manufacturing jobs in the state, or roughly 9 percent of the industry. After the first of

the new millennium, the job total in 2003 decreased to 15,408. Over the course of the next five

years the metal fabrication industry in Oregon made a comeback, adding 3,000 jobs by 2008.

Unlike the U.S. fabrication, Oregon nearly recovered to the high levels of employment present in

2001. This push of fabricated metals led to the subsector representing 10 percent of the

manufacturing industry within Oregon.

During the Great Recession, 4,000 of the 38,000 manufacturing jobs lost in Oregon came

from metal fabrication sector losses in 2009 and 2010. The percentage of employment lost in

metal fabrication illustrates the 10 percent share of the manufacturing industry that the subsector

encompassed at the time. In 2008, 993 businesses employed fabrication workers, but by 2010 17 Federal Reserve Bank of St. Louis, Economic Research. (2013).

US Employment

1,000,000

1,100,000

1,200,000

1,300,000

1,400,000

1,500,000

1,600,000

1,700,000

1,800,000

1,900,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Employmen

t

US Metal Fabrica9on Employment 1998-‐2011

CLUSTER ANALYSIS 21

the number of firms decreased to 901. The manufacturing industry slowly crept out of the hole

that the recession created, gaining 700 new jobs from 2010 to 2011. Metal fabrication in Oregon

injected nearly 800 of these jobs into the Oregon economy.

Since the latest Census County Business Patterns (CBP) data, the Oregon Employment

Department (OED) reports 3.3 percent growth throughout 2012.18 The OED also reports that the

metal fabrication sector represents 9 percent of the manufacturing employment in the state. Like

the U.S., Oregon grew in 2012 which gives the signal of possible growth in the future.

Finally, a thorough investigation of the counties with the most metal fabrication

employment will create a better understanding of the statewide industry performance over this

time period. Knowledge that pertains to the various counties within Oregon in addition to the

information above allows this analysis to create a comprehensive benchmark of where Salem

stands in regards to other regions of industry.

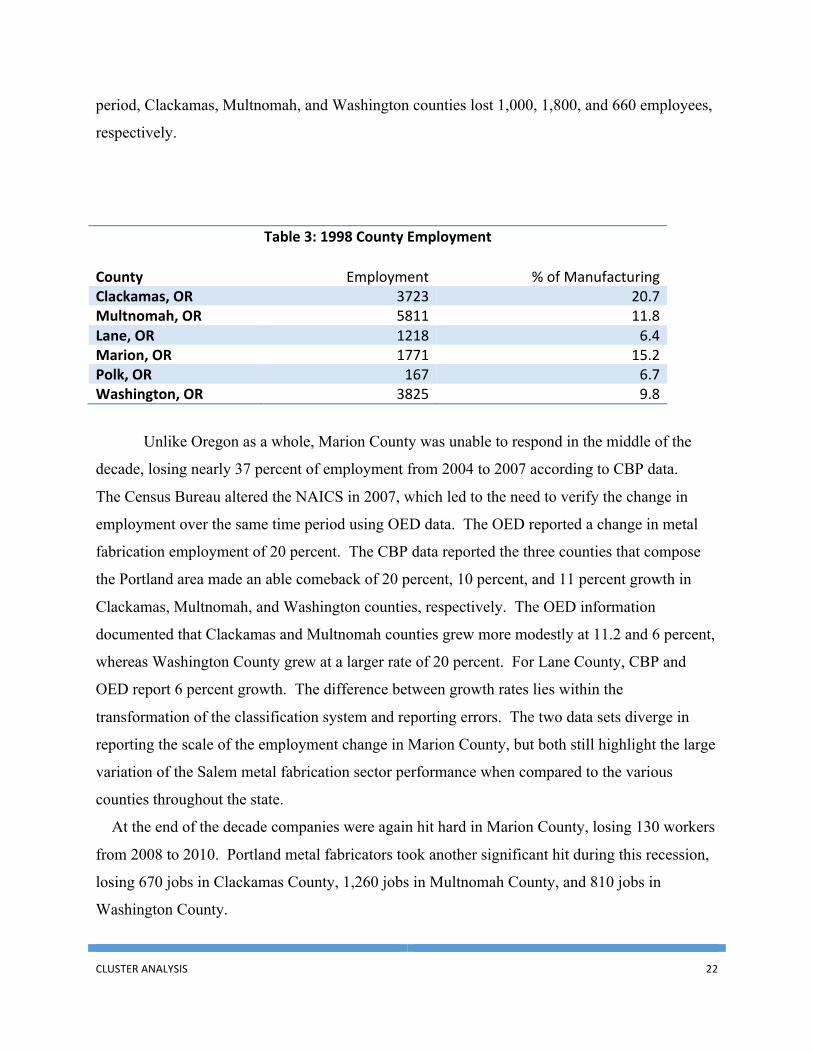

Marion County, the prominent metal fabrication location in the Salem MSA, housed 64

establishments that employed 1,771 workers in 1998. Employment in the subsector represented

15 percent of manufacturing throughout the county, second only to Clackamas County whose

metal fabrication sector embodied 20 percent of manufacturing (see table 3). From 1998 to 2003

the county lost 500 employees, though 64 businesses still operated there. Over the same time

18 Oregon Employment Department, (2013).

Oregon Employment

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Employmen

t

Oregon Metal Fabrica9on Employment

CLUSTER ANALYSIS 22

period, Clackamas, Multnomah, and Washington counties lost 1,000, 1,800, and 660 employees,

respectively.

Table 3: 1998 County Employment

County Employment % of Manufacturing Clackamas, OR 3723 20.7 Multnomah, OR 5811 11.8 Lane, OR 1218 6.4 Marion, OR 1771 15.2 Polk, OR 167 6.7 Washington, OR 3825 9.8

Unlike Oregon as a whole, Marion County was unable to respond in the middle of the

decade, losing nearly 37 percent of employment from 2004 to 2007 according to CBP data.

The Census Bureau altered the NAICS in 2007, which led to the need to verify the change in

employment over the same time period using OED data. The OED reported a change in metal

fabrication employment of 20 percent. The CBP data reported the three counties that compose

the Portland area made an able comeback of 20 percent, 10 percent, and 11 percent growth in

Clackamas, Multnomah, and Washington counties, respectively. The OED information

documented that Clackamas and Multnomah counties grew more modestly at 11.2 and 6 percent,

whereas Washington County grew at a larger rate of 20 percent. For Lane County, CBP and

OED report 6 percent growth. The difference between growth rates lies within the

transformation of the classification system and reporting errors. The two data sets diverge in

reporting the scale of the employment change in Marion County, but both still highlight the large

variation of the Salem metal fabrication sector performance when compared to the various

counties throughout the state.

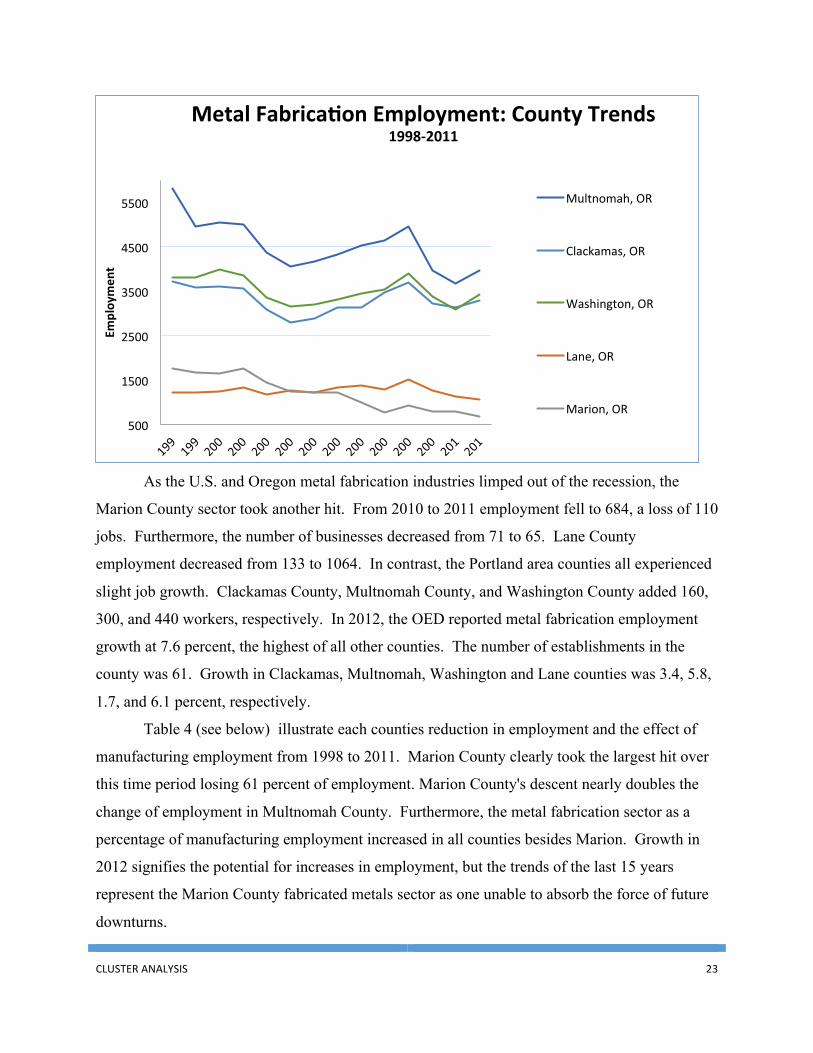

At the end of the decade companies were again hit hard in Marion County, losing 130 workers

from 2008 to 2010. Portland metal fabricators took another significant hit during this recession,

losing 670 jobs in Clackamas County, 1,260 jobs in Multnomah County, and 810 jobs in

Washington County.

CLUSTER ANALYSIS 23

As the U.S. and Oregon metal fabrication industries limped out of the recession, the

Marion County sector took another hit. From 2010 to 2011 employment fell to 684, a loss of 110

jobs. Furthermore, the number of businesses decreased from 71 to 65. Lane County

employment decreased from 133 to 1064. In contrast, the Portland area counties all experienced

slight job growth. Clackamas County, Multnomah County, and Washington County added 160,

300, and 440 workers, respectively. In 2012, the OED reported metal fabrication employment

growth at 7.6 percent, the highest of all other counties. The number of establishments in the

county was 61. Growth in Clackamas, Multnomah, Washington and Lane counties was 3.4, 5.8,

1.7, and 6.1 percent, respectively.

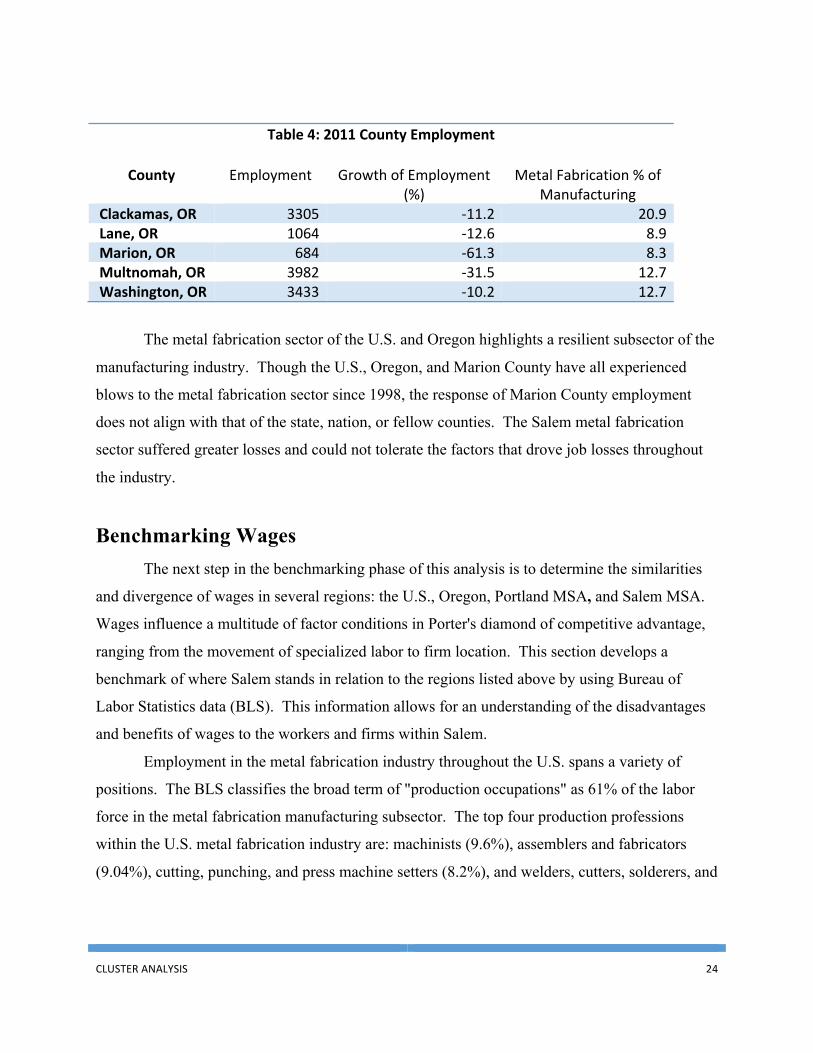

Table 4 (see below) illustrate each counties reduction in employment and the effect of

manufacturing employment from 1998 to 2011. Marion County clearly took the largest hit over

this time period losing 61 percent of employment. Marion County's descent nearly doubles the

change of employment in Multnomah County. Furthermore, the metal fabrication sector as a

percentage of manufacturing employment increased in all counties besides Marion. Growth in

2012 signifies the potential for increases in employment, but the trends of the last 15 years

represent the Marion County fabricated metals sector as one unable to absorb the force of future

downturns.

500

1500

2500

3500

4500

5500

Employmen

t Metal Fabrica9on Employment: County Trends

1998-‐2011

Multnomah, OR

Clackamas, OR

Washington, OR

Lane, OR

Marion, OR

CLUSTER ANALYSIS 24

Table 4: 2011 County Employment

County Employment Growth of Employment (%)

Metal Fabrication % of Manufacturing

Clackamas, OR 3305 -‐11.2 20.9 Lane, OR 1064 -‐12.6 8.9 Marion, OR 684 -‐61.3 8.3 Multnomah, OR 3982 -‐31.5 12.7 Washington, OR 3433 -‐10.2 12.7

The metal fabrication sector of the U.S. and Oregon highlights a resilient subsector of the

manufacturing industry. Though the U.S., Oregon, and Marion County have all experienced

blows to the metal fabrication sector since 1998, the response of Marion County employment

does not align with that of the state, nation, or fellow counties. The Salem metal fabrication

sector suffered greater losses and could not tolerate the factors that drove job losses throughout

the industry.

Benchmarking Wages The next step in the benchmarking phase of this analysis is to determine the similarities

and divergence of wages in several regions: the U.S., Oregon, Portland MSA, and Salem MSA.

Wages influence a multitude of factor conditions in Porter's diamond of competitive advantage,

ranging from the movement of specialized labor to firm location. This section develops a

benchmark of where Salem stands in relation to the regions listed above by using Bureau of

Labor Statistics data (BLS). This information allows for an understanding of the disadvantages

and benefits of wages to the workers and firms within Salem.

Employment in the metal fabrication industry throughout the U.S. spans a variety of

positions. The BLS classifies the broad term of "production occupations" as 61% of the labor

force in the metal fabrication manufacturing subsector. The top four production professions

within the U.S. metal fabrication industry are: machinists (9.6%), assemblers and fabricators

(9.04%), cutting, punching, and press machine setters (8.2%), and welders, cutters, solderers, and

CLUSTER ANALYSIS 25

brazers (6.9%).19 Of the four occupations within the U.S., machinists are paid the highest hourly

and yearly wages, whereas assemblers and fabricators are paid the lowest wages (See table 5).

Also, this benchmarking chooses to analyze the variations in wages of first-line supervisors to

determine the variations in wages of production managers. The national information will

become more relevant as we begin to benchmark the wages of the U.S., Oregon, and the Portland

MSA to each other and finally contrast each to the wages of the Salem MSA.

As the wage benchmarking begins two caveats must be put in place. Firstly, the first-line

supervisor data does not adjust for the cost of living of these individuals. Different cost of living

arrangements occur across the nation and Oregon which makes this analysis effective only if this

is taken into consideration. Secondly, the wage data for all five occupations in Oregon, Portland,

and Salem ranges across all manufacturing production. This skews the data upward for a large

metropolitan area like Portland when compared to one smaller like Salem. Certain types of

manufacturing fields will pay individuals higher wages, as this data does not generate a

difference between higher skilled labor with similar production position titles. The

benchmarking proceeds with these two cautions in mind.

Compared to the U.S., Oregon wages for the four top positions in the metal fabrication

industry experienced some disparity. Employers in Oregon compensated machinists with a

salary $6,210 greater than the national average and welders with a $1,300 higher yearly wage.

Assemblers and fabricators also received a salary $560 greater than the national average.

Median yearly wage for press machine setters were slightly lower in Oregon when compared to

the U.S. The first-line supervisors in Oregon received a salary $3,250 less than national

averages.

In Portland, all five production positions paid higher wages when compared to Oregon.

This can be expected as Portland encompasses the largest production area in Oregon, drawing

many of the high skilled workers in the state. Also, the large manufacturers within the area

harbor some of the most efficient and skilled first-line supervisors who in turn will receive

higher than average wages. One of the benefits of a large, urbanized area is the ability to pull

from a large labor pool which leads to manufacturers obtaining some of the most skilled workers

in the region.

19 Bureau of Labor Statistics, (2012).

CLUSTER ANALYSIS 26

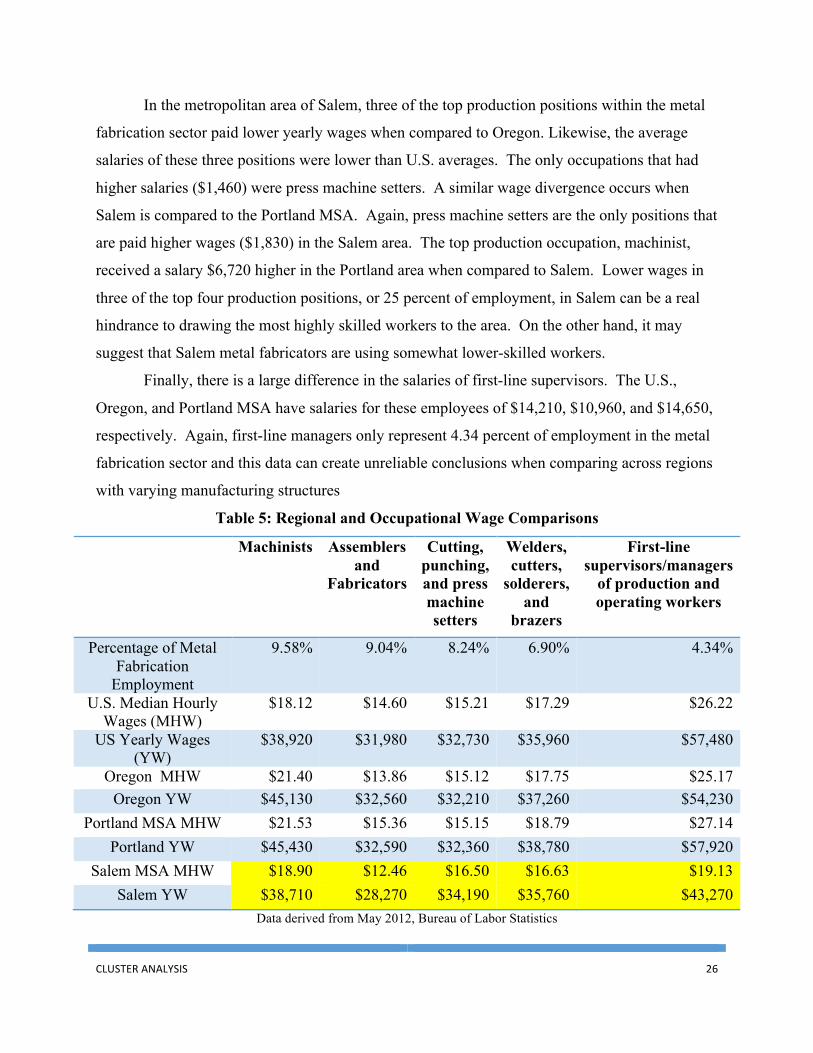

In the metropolitan area of Salem, three of the top production positions within the metal

fabrication sector paid lower yearly wages when compared to Oregon. Likewise, the average

salaries of these three positions were lower than U.S. averages. The only occupations that had

higher salaries ($1,460) were press machine setters. A similar wage divergence occurs when

Salem is compared to the Portland MSA. Again, press machine setters are the only positions that

are paid higher wages ($1,830) in the Salem area. The top production occupation, machinist,

received a salary $6,720 higher in the Portland area when compared to Salem. Lower wages in

three of the top four production positions, or 25 percent of employment, in Salem can be a real

hindrance to drawing the most highly skilled workers to the area. On the other hand, it may

suggest that Salem metal fabricators are using somewhat lower-skilled workers.

Finally, there is a large difference in the salaries of first-line supervisors. The U.S.,

Oregon, and Portland MSA have salaries for these employees of $14,210, $10,960, and $14,650,

respectively. Again, first-line managers only represent 4.34 percent of employment in the metal

fabrication sector and this data can create unreliable conclusions when comparing across regions

with varying manufacturing structures

Table 5: Regional and Occupational Wage Comparisons

Machinists Assemblers and

Fabricators

Cutting, punching, and press machine setters

Welders, cutters,

solderers, and

brazers

First-line supervisors/managers

of production and operating workers

Percentage of Metal Fabrication

Employment

9.58% 9.04% 8.24% 6.90% 4.34%

U.S. Median Hourly Wages (MHW)

$18.12 $14.60 $15.21 $17.29 $26.22

US Yearly Wages (YW)

$38,920 $31,980 $32,730 $35,960 $57,480

Oregon MHW $21.40 $13.86 $15.12 $17.75 $25.17 Oregon YW $45,130 $32,560 $32,210 $37,260 $54,230

Portland MSA MHW $21.53 $15.36 $15.15 $18.79 $27.14 Portland YW $45,430 $32,590 $32,360 $38,780 $57,920

Salem MSA MHW $18.90 $12.46 $16.50 $16.63 $19.13 Salem YW $38,710 $28,270 $34,190 $35,760 $43,270

Data derived from May 2012, Bureau of Labor Statistics

CLUSTER ANALYSIS 27

Many conditions drive these differences, which makes it difficult to draw conclusions as

to why these variations occur. The landscape of the wage situation in Salem, Portland, Oregon,

and the U.S. shows an environment where Salem lags behind in most of the top employment

categories. The wages of the top production occupations shed light on the composition of the

labor force in Salem. With this understanding of the past and current state of the industry, we can

begin measuring the potential Salem has for growth.

Statistical Analysis

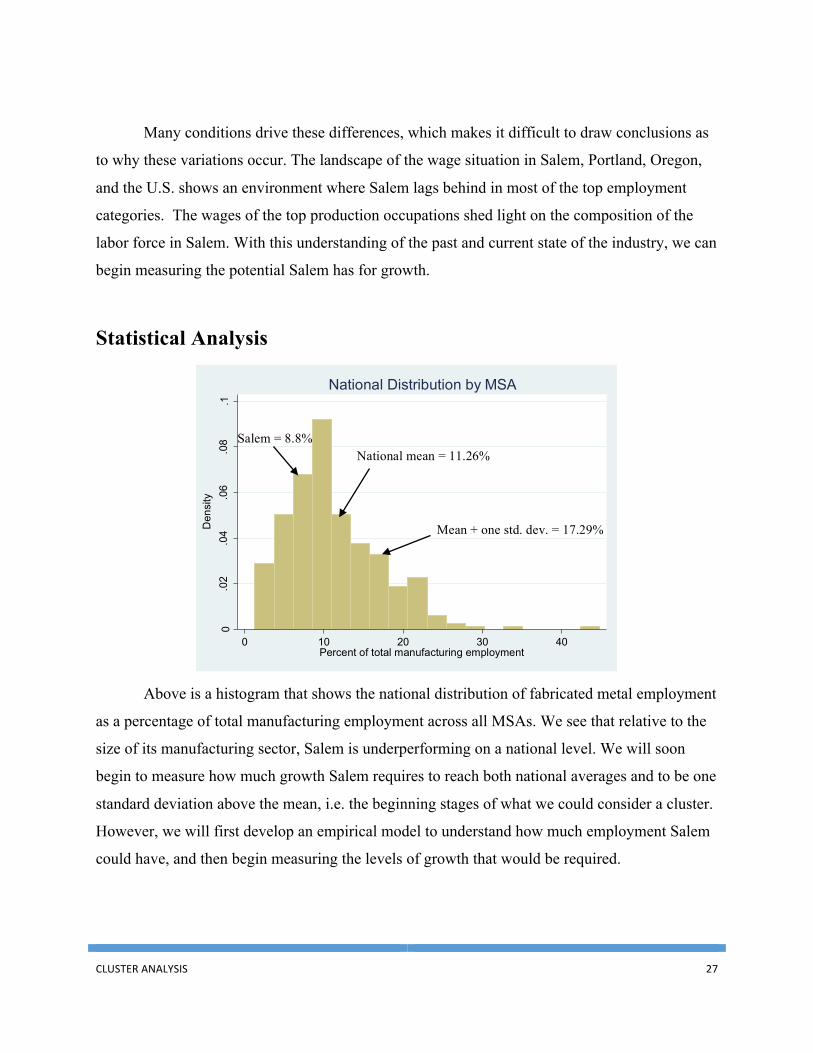

Above is a histogram that shows the national distribution of fabricated metal employment

as a percentage of total manufacturing employment across all MSAs. We see that relative to the

size of its manufacturing sector, Salem is underperforming on a national level. We will soon

begin to measure how much growth Salem requires to reach both national averages and to be one

standard deviation above the mean, i.e. the beginning stages of what we could consider a cluster.

However, we will first develop an empirical model to understand how much employment Salem

could have, and then begin measuring the levels of growth that would be required.

0.0

2.0

4.0

6.0

8.1

Den

sity

0 10 20 30 40Percent of total manufacturing employment

National Distribution by MSA

Salem = 8.8%National mean = 11.26%

Mean + one std. dev. = 17.29%

CLUSTER ANALYSIS 28

Baseline Model

This section is intended to analyze how employment in the fabricated metals sector

deviates from expected levels within regions. To do this, we have gathered data at the MSA

level, which includes levels of employment in the fabricated metals industry; employment levels

in the manufacturing industry; and the size of the population. In order to measure how a given

region deviates from what we would expect, we will run an ordinary least squares regression

using fabricated metals employment as the dependent variable, with population and

manufacturing employment as our explanatory variables. Once we have generated a model that

explains a large portion of the data, i.e. a high R-squared, we can then generate predicted values

based on the size of the population and manufacturing sectors of each MSA. Using predicted

levels of employment and their residuals, we can see how the observed levels of employment in

each region deviates from what our model predicts. This allows us to benchmark Salem on a

national level, as well as against other similar regions. We will also be able to identify clusters

by examining regions that deviate substantially from its predicted values. Finally, regions with

very large observed deviations can be used as a point of reference in terms of what may cause a

region to have large concentrations of employment in the fabricated metals industry.

To begin the analysis, we look at the most basic variables that would influence

employment of the fabricated metals industry within an MSA, i.e. the size of the population and

manufacturing sector. From this, we have a baseline model:

𝐹𝑎𝑏𝑀𝑒𝑡𝑎𝑙! = 𝛽! + 𝛽!𝑃𝑜𝑝! + 𝛽!𝑀𝑎𝑛𝑢𝑓𝑎𝑐𝑡𝑢𝑟𝑖𝑛𝑔! + 𝑢!

Where 𝐹𝑎𝑏𝑀𝑒𝑡𝑎𝑙! is total employment in the fabricated metals industry in metropolitan area i;

𝑃𝑜𝑝! is total population in metropolitan area i; and 𝑀𝑎𝑛𝑢𝑓𝑎𝑐𝑡𝑢𝑟𝑖𝑛𝑔! is total manufacturing

employment in area i.

Theoretically, we would expect the coefficients for the population and manufacturing

variables to be positive. For the simple model, it is intuitive to assume that largely populated

metropolitan areas would have greater amounts of employment in the fabricated metals industry.

Likewise, increased manufacturing employment would increase employment in the industry.

This could be for various reasons, one of which might be that metro areas with larger

manufacturing sectors may have environments that foster competitive advantages for local

businesses. Other manufacturing sectors are also key suppliers, while others are large buyers of

fabricated metals products, meaning sizeable demand for these products requires more

CLUSTER ANALYSIS 29

employment to meet that demand. Another reason could be that geographic endowments, such as

convenient access to bodies of water, offer competitive advantages to manufacturing industry

businesses that locate in those regions.

Controlling for Region

We are interested in locating and understanding all of the relevant factors that would

contribute to a cluster forming. Doing so would requires analyzing how different regions in the

United States might affect levels of fabricated metals employment. Expanding our baseline

model to include different regions, we have the following model:

𝐹𝑎𝑏𝑀𝑒𝑡𝑎𝑙! = 𝛽! + 𝛽!𝑃𝑜𝑝! + 𝛽!𝑀𝑎𝑛𝑢𝑓𝑎𝑐𝑡𝑢𝑟𝑖𝑛𝑔! + 𝛽!𝑅𝑒𝑔𝑖𝑜𝑛!! + 𝑢!,

where 𝑅𝑒𝑔𝑖𝑜𝑛!!is a set of dummy variables that control for various region-specific effects. Each

region is defined by the Census Bureau, and consists of the following:

• New England = New Hampshire, Vermont, Massachusetts, Rhode Island, Connecticut,

and Maine.

• Mid-Atlantic = New York, Pennsylvania, and New Jersey.

• East North Central = Wisconsin, Michigan, Illinois, Indiana, and Ohio.

• West North Central = Missouri, North Dakota, South Dakota, Nebraska, Kansas,

Minnesota, and Iowa.

• South Atlantic = Delaware, Maryland, Virginia, West Virginia, North Carolina, South

Carolina, Georgia, and Florida.

• East South Central = Kentucky, Tennessee, Mississippi, and Alabama.

• West South Central = Oklahoma, Texas, Arkansas, and Louisiana.

• Mountain = Idaho, Montana, Wyoming, Nevada, Utah, Colorado, Arizona, and New

Mexico.

• Pacific = Alaska, Washington, Oregon, California, and Hawaii.

The regression will not be able to include all of the regions. In order to avoid multicollinearity

between these dummy variables and the constant, we excluded the metro regions that cross state

boarders. The constant will then be largely representative of the region that will be left out from

the regression.

CLUSTER ANALYSIS 30

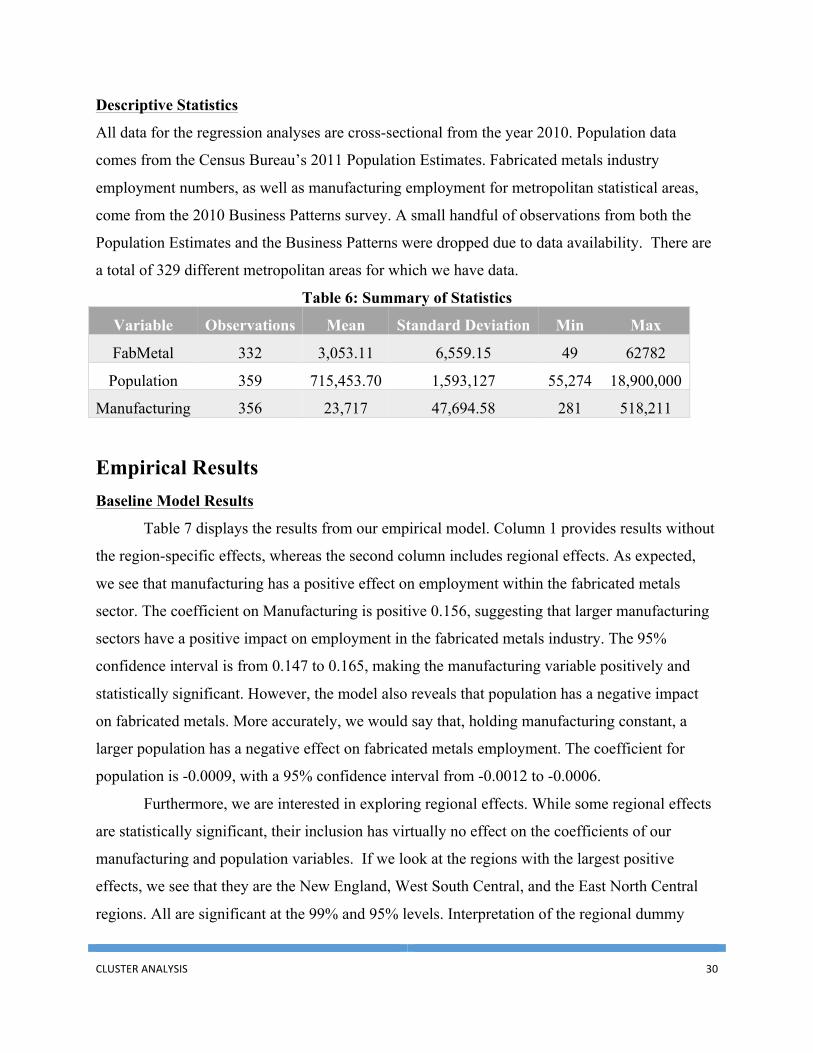

Descriptive Statistics

All data for the regression analyses are cross-sectional from the year 2010. Population data

comes from the Census Bureau’s 2011 Population Estimates. Fabricated metals industry

employment numbers, as well as manufacturing employment for metropolitan statistical areas,

come from the 2010 Business Patterns survey. A small handful of observations from both the

Population Estimates and the Business Patterns were dropped due to data availability. There are

a total of 329 different metropolitan areas for which we have data.

Table 6: Summary of Statistics

Variable Observations Mean Standard Deviation Min Max

FabMetal 332 3,053.11 6,559.15 49 62782

Population 359 715,453.70 1,593,127 55,274 18,900,000

Manufacturing 356 23,717 47,694.58 281 518,211

Empirical Results Baseline Model Results

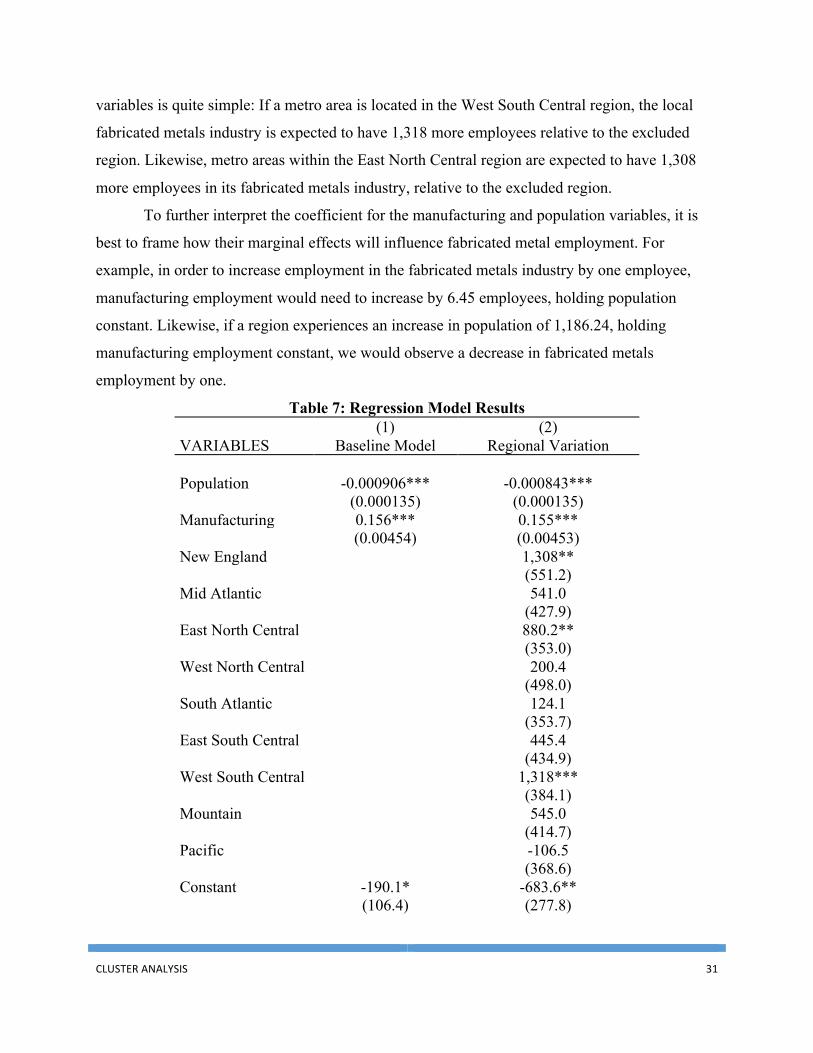

Table 7 displays the results from our empirical model. Column 1 provides results without

the region-specific effects, whereas the second column includes regional effects. As expected,

we see that manufacturing has a positive effect on employment within the fabricated metals

sector. The coefficient on Manufacturing is positive 0.156, suggesting that larger manufacturing

sectors have a positive impact on employment in the fabricated metals industry. The 95%

confidence interval is from 0.147 to 0.165, making the manufacturing variable positively and

statistically significant. However, the model also reveals that population has a negative impact

on fabricated metals. More accurately, we would say that, holding manufacturing constant, a

larger population has a negative effect on fabricated metals employment. The coefficient for

population is -0.0009, with a 95% confidence interval from -0.0012 to -0.0006.

Furthermore, we are interested in exploring regional effects. While some regional effects

are statistically significant, their inclusion has virtually no effect on the coefficients of our

manufacturing and population variables. If we look at the regions with the largest positive

effects, we see that they are the New England, West South Central, and the East North Central

regions. All are significant at the 99% and 95% levels. Interpretation of the regional dummy

CLUSTER ANALYSIS 31

variables is quite simple: If a metro area is located in the West South Central region, the local

fabricated metals industry is expected to have 1,318 more employees relative to the excluded

region. Likewise, metro areas within the East North Central region are expected to have 1,308

more employees in its fabricated metals industry, relative to the excluded region.

To further interpret the coefficient for the manufacturing and population variables, it is

best to frame how their marginal effects will influence fabricated metal employment. For

example, in order to increase employment in the fabricated metals industry by one employee,

manufacturing employment would need to increase by 6.45 employees, holding population

constant. Likewise, if a region experiences an increase in population of 1,186.24, holding

manufacturing employment constant, we would observe a decrease in fabricated metals

employment by one.

Table 7: Regression Model Results (1) (2) VARIABLES Baseline Model Regional Variation Population -0.000906*** -0.000843*** (0.000135) (0.000135) Manufacturing 0.156*** 0.155*** (0.00454) (0.00453) New England 1,308** (551.2) Mid Atlantic 541.0 (427.9) East North Central 880.2** (353.0) West North Central 200.4 (498.0) South Atlantic 124.1 (353.7) East South Central 445.4 (434.9) West South Central 1,318*** (384.1) Mountain 545.0 (414.7) Pacific -106.5 (368.6) Constant -190.1* -683.6** (106.4) (277.8)

CLUSTER ANALYSIS 32

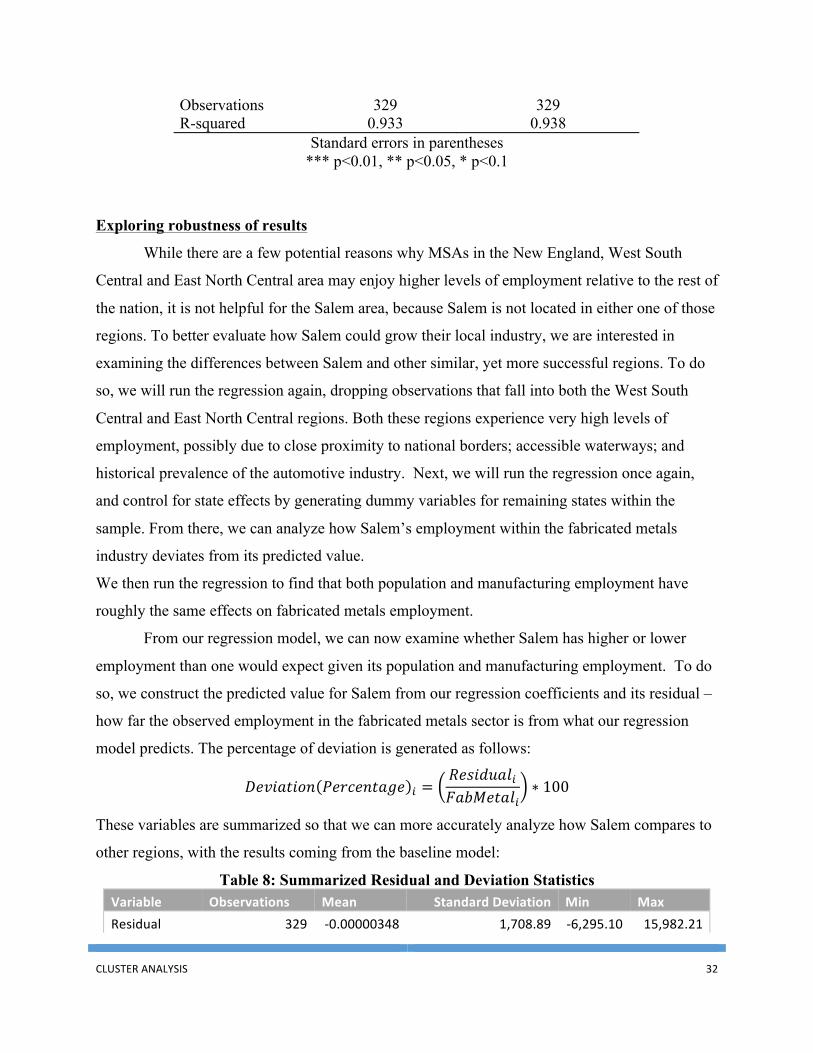

Observations 329 329 R-squared 0.933 0.938

Standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1

Exploring robustness of results

While there are a few potential reasons why MSAs in the New England, West South

Central and East North Central area may enjoy higher levels of employment relative to the rest of

the nation, it is not helpful for the Salem area, because Salem is not located in either one of those

regions. To better evaluate how Salem could grow their local industry, we are interested in

examining the differences between Salem and other similar, yet more successful regions. To do

so, we will run the regression again, dropping observations that fall into both the West South

Central and East North Central regions. Both these regions experience very high levels of

employment, possibly due to close proximity to national borders; accessible waterways; and

historical prevalence of the automotive industry. Next, we will run the regression once again,

and control for state effects by generating dummy variables for remaining states within the

sample. From there, we can analyze how Salem’s employment within the fabricated metals

industry deviates from its predicted value.

We then run the regression to find that both population and manufacturing employment have

roughly the same effects on fabricated metals employment.

From our regression model, we can now examine whether Salem has higher or lower

employment than one would expect given its population and manufacturing employment. To do

so, we construct the predicted value for Salem from our regression coefficients and its residual –

how far the observed employment in the fabricated metals sector is from what our regression

model predicts. The percentage of deviation is generated as follows:

𝐷𝑒𝑣𝑖𝑎𝑡𝑖𝑜𝑛 𝑃𝑒𝑟𝑐𝑒𝑛𝑡𝑎𝑔𝑒 ! =𝑅𝑒𝑠𝑖𝑑𝑢𝑎𝑙!𝐹𝑎𝑏𝑀𝑒𝑡𝑎𝑙!

∗ 100

These variables are summarized so that we can more accurately analyze how Salem compares to

other regions, with the results coming from the baseline model:

Table 8: Summarized Residual and Deviation Statistics Variable Observations Mean Standard Deviation Min Max Residual 329 -‐0.00000348 1,708.89 -‐6,295.10 15,982.21

CLUSTER ANALYSIS 33

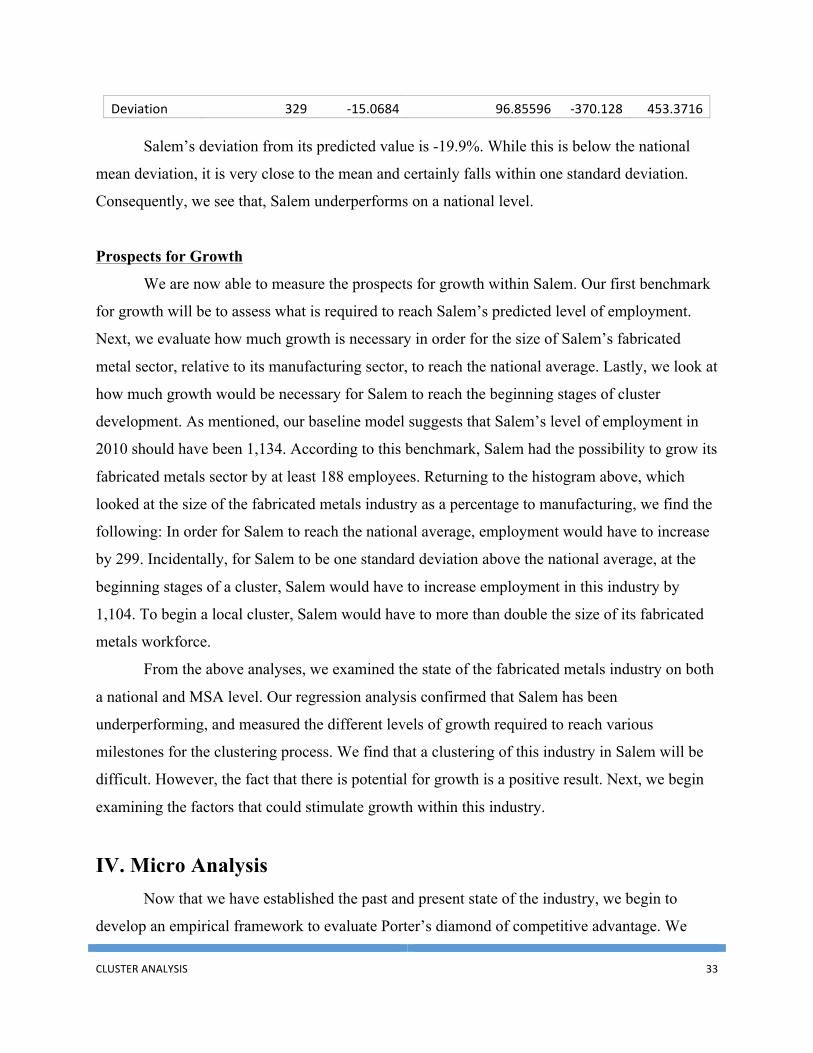

Deviation 329 -‐15.0684 96.85596 -‐370.128 453.3716

Salem’s deviation from its predicted value is -19.9%. While this is below the national

mean deviation, it is very close to the mean and certainly falls within one standard deviation.

Consequently, we see that, Salem underperforms on a national level.

Prospects for Growth

We are now able to measure the prospects for growth within Salem. Our first benchmark

for growth will be to assess what is required to reach Salem’s predicted level of employment.

Next, we evaluate how much growth is necessary in order for the size of Salem’s fabricated

metal sector, relative to its manufacturing sector, to reach the national average. Lastly, we look at

how much growth would be necessary for Salem to reach the beginning stages of cluster

development. As mentioned, our baseline model suggests that Salem’s level of employment in

2010 should have been 1,134. According to this benchmark, Salem had the possibility to grow its

fabricated metals sector by at least 188 employees. Returning to the histogram above, which

looked at the size of the fabricated metals industry as a percentage to manufacturing, we find the

following: In order for Salem to reach the national average, employment would have to increase

by 299. Incidentally, for Salem to be one standard deviation above the national average, at the

beginning stages of a cluster, Salem would have to increase employment in this industry by

1,104. To begin a local cluster, Salem would have to more than double the size of its fabricated

metals workforce.

From the above analyses, we examined the state of the fabricated metals industry on both

a national and MSA level. Our regression analysis confirmed that Salem has been

underperforming, and measured the different levels of growth required to reach various

milestones for the clustering process. We find that a clustering of this industry in Salem will be

difficult. However, the fact that there is potential for growth is a positive result. Next, we begin

examining the factors that could stimulate growth within this industry.

IV. Micro Analysis Now that we have established the past and present state of the industry, we begin to

develop an empirical framework to evaluate Porter’s diamond of competitive advantage. We

CLUSTER ANALYSIS 34

begin by examining demand conditions and related and supporting industries through an input-

output analysis. These two cluster traits are tested using a case study to see if their presence is

imperative at a local level. Following these analyses, we analyze factor conditions, namely those

that affect the quality of the local labor pool through a series of training program analyses in the

Oregon region.

Input-Output Analysis

Clusters of firms occur because those firms are related in such a way that proximate

location to each other is beneficial. An important way that firms may be related is through their

purchases of each other’s products for inputs. Being close to each other lowers the costs of

transporting inputs and outputs. It can also facilitate close communication about specialization

of inputs for each other. Understanding these supply-chain links can be quite important for

developing regional policies to encourage business clusters.

For example, platework and fabricated structure manufacturing is a relatively strong

subsector in the fabricated metals industry in Salem. To encourage more firms in the fabricated

metals industry to locate in Salem, one possible policy option would be to strengthen the

presence of this sector’s primary downstream and upstream industries in the Salem area.

Input-output analysis is a standard method to examine upstream and downstream supply-

chain links. It involves examination of data on input purchases one sector makes from other

sectors in order to produce its output. In the following, we conduct an input-output analysis of

the fabricated metals sector in the U.S., as well as a similar analysis of the sub-sectors in

fabricated metals that are most common in the Salem area.

Summary Level

We first begin with an analysis of the upstream and downstream relationships for the

fabricated metals sector in aggregate. Upstream industries are those that provide inputs into the

fabricated metals sector, whereas downstream industries are those that purchase fabricated

metals products as inputs. The data for these input and output relationships between sectors of

the economy come from the BEA’s website20. For our purposes, we use data from “The Use of

20 www.bea.gov.

CLUSTER ANALYSIS 35

Commodities before Redefinitions”, which includes data scaled to producer’s prices in millions

of dollars. By analyzing relatively large levels of purchases between industries, we can identify

the major downstream and upstream sectors for the fabricated metals sector, thereby deriving a

basic supply chain.

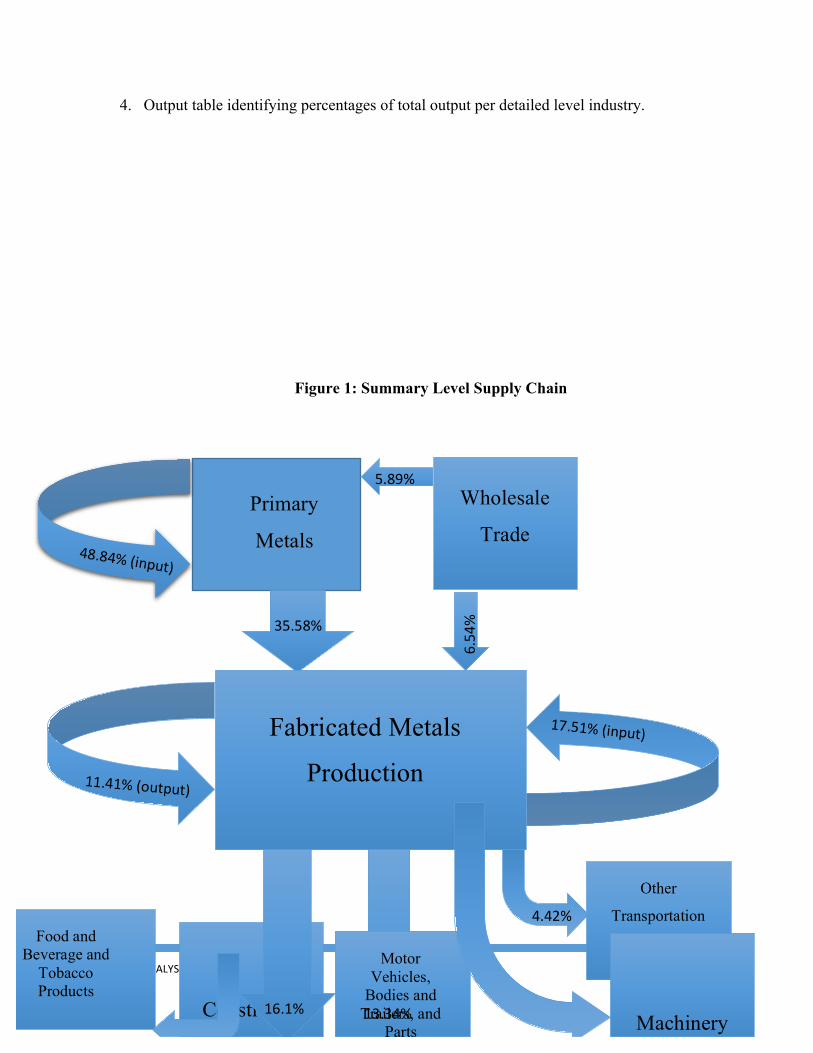

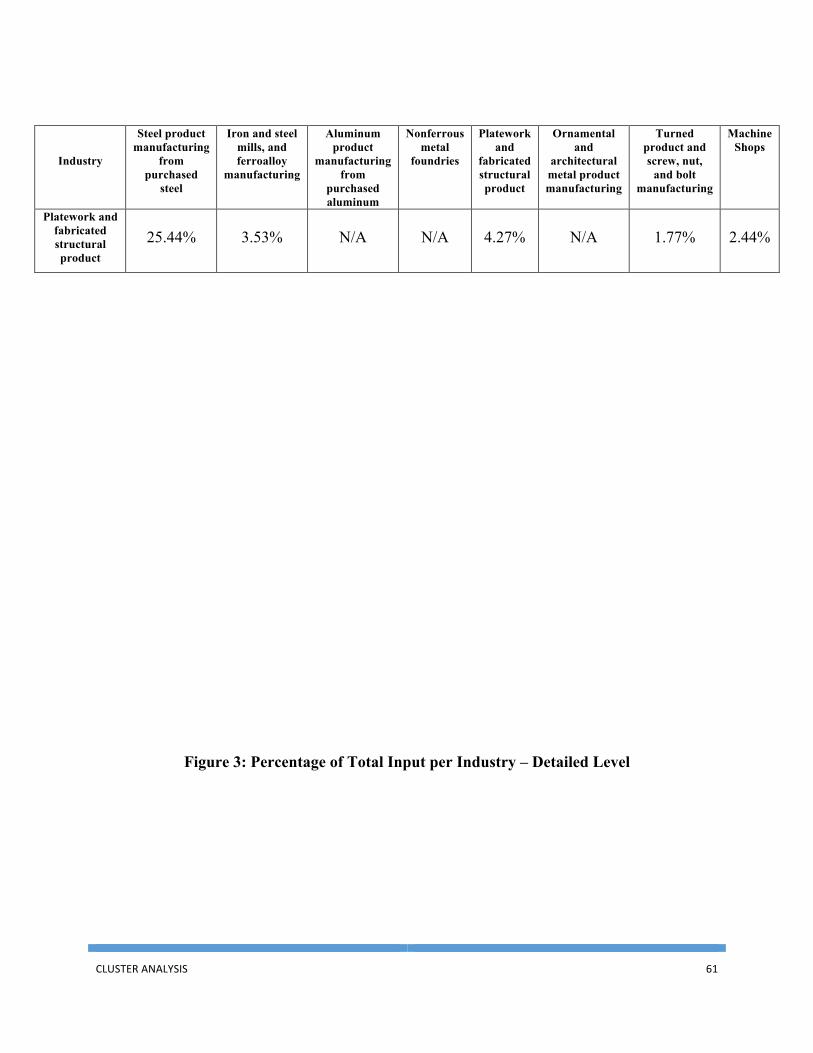

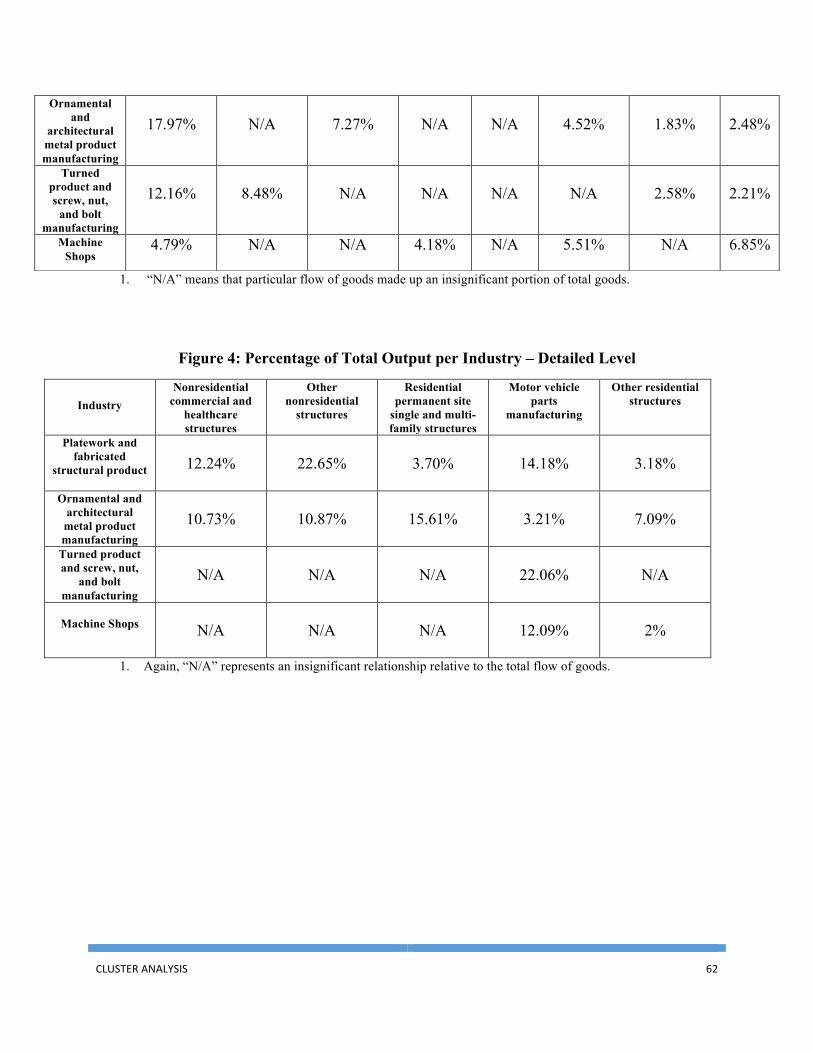

Figure__ diagrams the major supply chain relationships for the fabricated metals sector. The

percentages show what percent each specific industry flow makes up of the sum of all upstream

or downstream purchases. For example, we see that primary metals makes up 35.58% of total

fabricated metal inputs, and the construction industry makes up 16.1% of total fabricated metal

output.

• Upstream Industries:

o Primary metals (35.58%)

o Fabricated metals (17.51%)

o Wholesale trade (6.54%)

• Downstream Industries:

o Construction (16.1%)

o Motor vehicles, bodies and trailers, and parts (13.34%)

o Machinery (11.87%)

o Fabricated metals (11.41%)

o Food and beverage and tobacco products (4.37%)

o Other Transportation Equipment (4.42%)

The supply-chain diagram shows the basic flow of goods between different industries. The

percentages show what portion that specific industry flow makes up of all flows. Notice with the

list above that fabricated metals is both a downstream and upstream industry to itself. The reason

is pretty simple: the data is at a summary level, and so within the fabricated metals industry are

more detailed subsectors that act as upstream industries to other subsectors and so on.

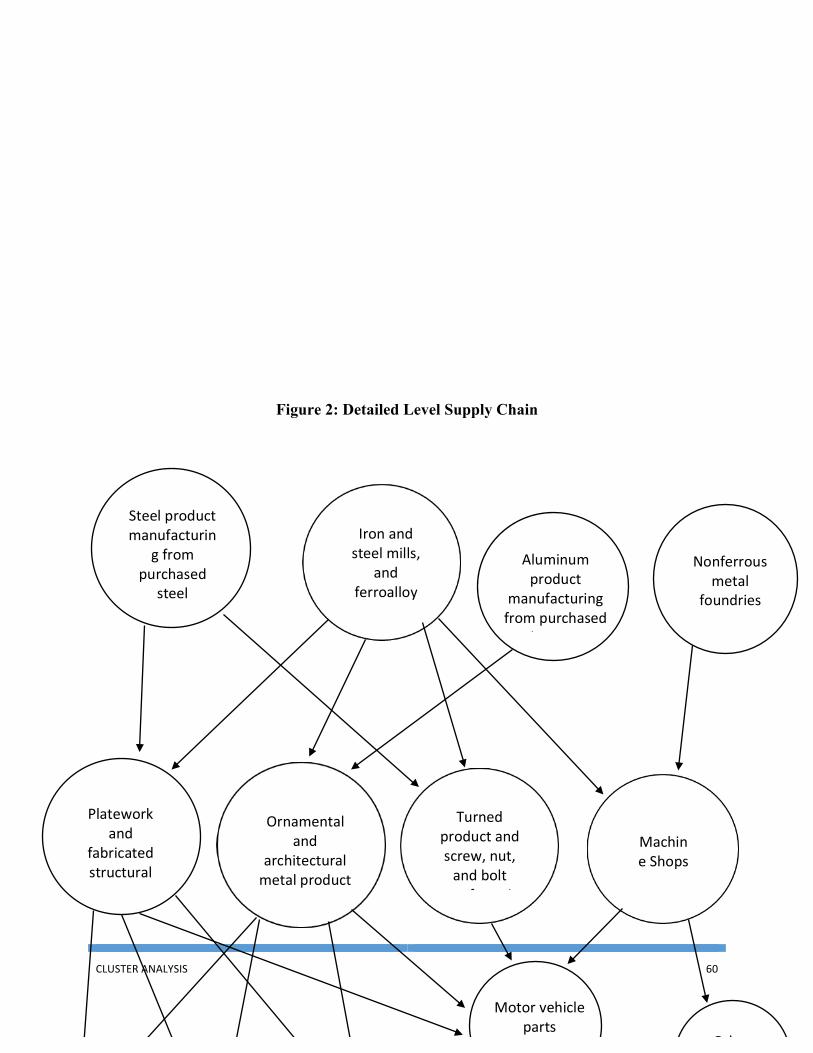

Detailed Level

We can further explore a more detailed level supply-chains for subsectors of the

fabricated metals sector. To get this level of detail, we must turn to historical benchmark input-

output from the BEA, which are only available up until 2002. We discuss some of the

CLUSTER ANALYSIS 36

disadvantages of using data from different time periods in the appendix, but for now we will

continue our analysis with the assumption that the industry relationships have not changed

substantially since 2002.

The input-output analysis is conducted in the same way for the detailed level data as it

was for the summary level data. We identify relatively large purchases of inputs between sectors,

and then draw conclusions regarding the relevant upstream and downstream industries. To keep

the analysis concise, we will not examine all subsectors in the fabricated metals sector, only

those that are prevalent in the Salem metro area. These subsectors are included below, with their

respective NAICS code in parentheses:

• Plate work and fabricated structural product manufacturing (332310)

• Ornamental and architectural metal products manufacturing (332320)

• Machine Shops (332710)

• Turned product and screw, nut, and bolt manufacturing (332720).

The detailed analysis yields interesting results. We see that, given the prevalent

subsectors in Salem, the major detailed level downstream industries come from the construction

industry. If the presence of major downstream industries within a given region does affect the

local fabricated metal industry, then we should observe construction as being the dominant

downstream industry within Salem. We will apply this supply-chain on a regional level within

Salem and to other comparable regions and observe the variations and their effects. This will

indicate to what extent the presence of major downstream industries affects the local fabricated

metals sector. (For a visual representation of both the summary level and detailed level supply-

chains, see the appendix.)

Case Study After developing an empirical understanding of national demand conditions, as well as

the related and supporting industries, we must now focus the analysis on a regional level. That is

to say, we must know if a large presence of highly linked downstream industries has a sizeable

effect on the size and structure of the local fabricated metals sector. To do so, we will study two

regions that are similar to Salem in terms of population and total employment in their

manufacturing industry. The selected regions will be those that experience significantly larger

CLUSTER ANALYSIS 37

levels of employment in the fabricated metals industry. Finally, these regions will be compared

to Salem, both through the size and structure of their fabricated metal sectors, and by the size of

the relevant downstream industries.

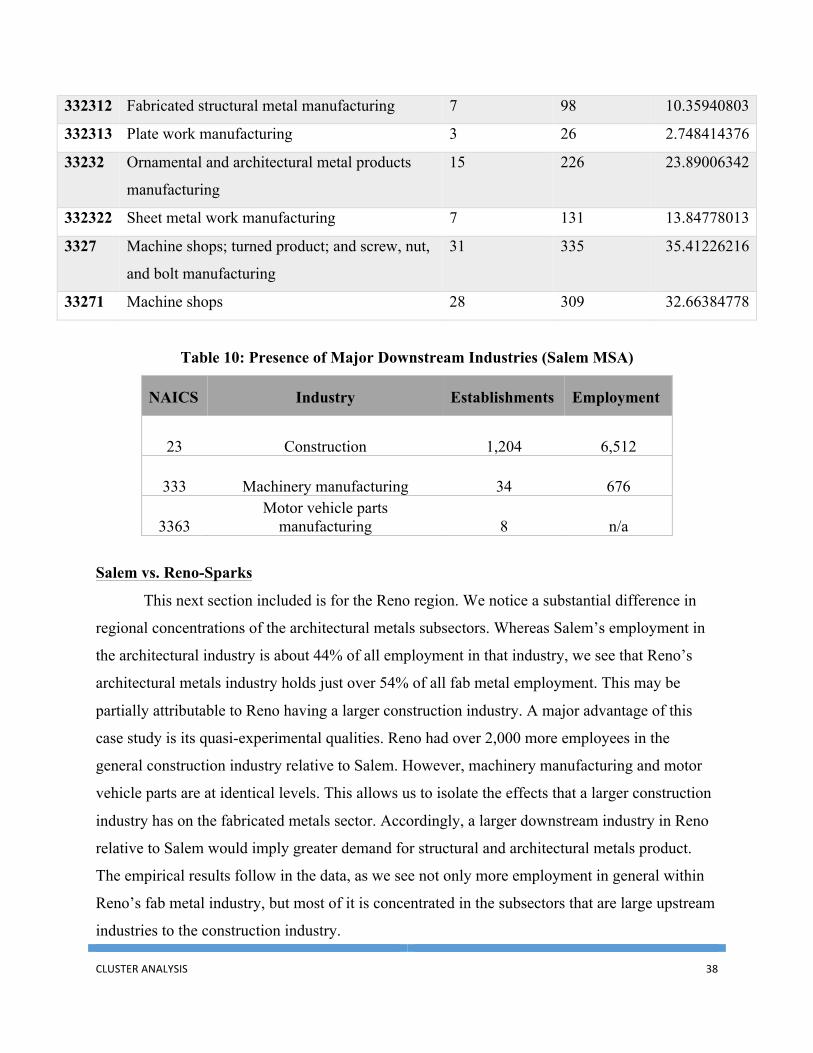

Salem vs. Reno and Springfield, MO:

Both the Reno-Sparks, NV and Springfield, MO regions have similarly sized population

and manufacturing employment relative to Salem. However, these two regions have significantly

higher levels of fabricated metal manufacturing employment. To understand why, we will

consider the following:

1. What is the concentration ratio within the regional fabricated metals sector? That is, are

there any subsectors that make up a highly concentrated sector relative to employment? If

so, why could this be?

2. Relative to different levels of subsector concentration within each region, how big are the

relevant downstream industries?

We will analyze the presence of the three largest downstream industries, i.e. construction;

machinery manufacturing; and motor vehicle parts manufacturing. From there, we compare and

contrast the prevalent downstream industries in each region and analyze the effects they have on

the size and structure of the local fabricated metals sector. Below are facts about the

concentration ratios of Salem’s subsectors relative to total employment in the fabricated metals

industry. Only those subsectors that have available employment data are included:

Table 9: Structure of Local Fabricated Metal Sector (Salem MSA)

NAICS Industry Establishments Employment Concentration

ratio

332 Fabricated metal product manufacturing 84 946 100

3323 Architectural and structural metals

manufacturing

30 417 44.08033827

33231 Plate work and fabricated structural product

manufacturing

15 191 20.19027484

332311 Prefabricated metal building and component

manufacturing

5 67 7.082452431

CLUSTER ANALYSIS 38