-

8/13/2019 CNBC Fed Survey, December 17, 2013

1/36

CNBC Fed Survey December 17, 2013Page 1 of 36

FED SURVEYDecember 17, 2013

These survey results represent the opinions of 42 of the nations

top money managers, investment

strategists, and professional economists.

They responded to CNBCs invitation to participate in our online

survey. Their responses were collecte

on December 12-13, 2013. Participants were not required to

answer every question.

Results are also shown for identical questions in earlier

surveys.

This is not intended to be a scientific poll and its results

should not be extrapolated beyond those who

did accept our invitation.

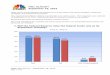

1.For all of 2013, 2014, and 2015 (and only in those years),

whais the total amount of additional asset purchases the

Federal

Reserve will have made?

$858.8

$917.0 $936.6

$883.6$921.9 $941.9

$948.5

$1,023.7 $1,017.7

$370.6 $367.1 $373.5 $374.8 $381.9

$646.1

$497.0

$96.3

$0

$200

$400

$600

$800

$1,000

$1,200

1/29/2013 4/30/2013 7/30/2013 9/17/2013 12/17/2013

Billions

2013 2014 2015

-

8/13/2019 CNBC Fed Survey, December 17, 2013

2/36

CNBC Fed Survey December 17, 2013Page 2 of 36

FED SURVEYDecember 17, 2013

2.In what month do you expect the Fed to begin tapering

itspurchases?

0%

10%

20%

30%

40%

50%

60%

Sept 17 Oct 29 Dec 17

AveragesJan 29: Dec 2013

March 19: Jan 2014

April 30: Feb 2014

June 18: Dec 2013

July 30: November 2013Sep 6: November 2013

Sept 17: November 2013

Oct 29: April 2014

Dec 17: February 2014

(Plurality of 33% saidJanuary)

-

8/13/2019 CNBC Fed Survey, December 17, 2013

3/36

CNBC Fed Survey December 17, 2013Page 3 of 36

FED SURVEYDecember 17, 2013

3.By how much do you believe the Fed will reduce its

assetpurchases in that first month?

$22.1

$19.2

$12.6

$14.5 $14.2$15.2

$0

$5

$10

$15

$20

$25

July 5 July 30 Sept 6 Sept 17 Oct 29 Dec 17

Billions

On average, respondents

believe the Fed willmaintain its new level ofasset purchases for

3.34months.

-

8/13/2019 CNBC Fed Survey, December 17, 2013

4/36

CNBC Fed Survey December 17, 2013Page 4 of 36

FED SURVEYDecember 17, 2013

4.What mix of Treasuries vs. mortgage-backed securities do

youexpect in the Federal Reserve's taper?

72% 71%64%

28% 29%36%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sep 17 Oct 29 Dec 17

Treasuries MBS

-

8/13/2019 CNBC Fed Survey, December 17, 2013

5/36

CNBC Fed Survey December 17, 2013Page 5 of 36

FED SURVEYDecember 17, 2013

5.When do you expect the Federal Reserve will completely

stoppurchasing assets?

0%

5%

10%

15%

20%

25%

30%

June 18 July 30 Sept 6 Sept 17 Oct 29 Dec 17

AveragesJan 29: Nov 2013

Mar 19: May 2014Apr 30: July 2014Jun 18: July 2014July 30: Aug

2014

Sept 6: Aug 2014

Sept 17: Aug 2014

Oct 29: Dec 2014

Dec 17: Dec 2014

-

8/13/2019 CNBC Fed Survey, December 17, 2013

6/36

CNBC Fed Survey December 17, 2013Page 6 of 36

FED SURVEYDecember 17, 2013

6.Based on your expectations for tapering, what percentage ofthe

ultimate impact on each market is already discounted inthe overall

prices of that market?

66%

58%

68%

81%

73%

82%81%

70%

81%

58%

50%

57%

75%

63%

71%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Treasuries Equities Mortgages

July 30 Sept 6 Sept 17 Oct 29 Dec 17

-

8/13/2019 CNBC Fed Survey, December 17, 2013

7/36

CNBC Fed Survey December 17, 2013Page 7 of 36

FED SURVEYDecember 17, 2013

7.Compared to Ben Bernanke, Fed chair nominee Janet Yellenwill

be:

15%

44%

28%

3%

0%

10%

2%

52%

33%

10%

0%

2%

0%

10%

20%

30%

40%

50%

60%

Much moredovish

Somewhatmore dovish

No different Somewhatmore

hawkish

Much morehawkish

Don'tknow/unsure

Oct 29 Dec 17

-

8/13/2019 CNBC Fed Survey, December 17, 2013

8/36

-

8/13/2019 CNBC Fed Survey, December 17, 2013

9/36

CNBC Fed Survey December 17, 2013Page 9 of 36

FED SURVEYDecember 17, 2013

Comments on this question:

Dean Baker, Center for Economic and Policy Research: (C) He

should havehighlighted to the public and Congress that he was using

his post to keep Wall Streetbanks solvent that the market would

have sank. There could and should have been

major quid pro quos, like an agreement to downsize within 5

years, for being keptalive.

Alan Blinder, Princeton University: (B) W/o Lehman, would be

A

Tony Crescenzi, PIMCO: (A) Ben Bernanke should be called The

Decider for the bo

decisions he made when the fiscal authority failed to act to

take measures to promotgrowth.

John Donaldson, Haverford Trust Co.: (A) He was the right person

at what was aparticularly difficult time.

Mike Dueker, Russell Investments: (B) The grade for

post-September 2008 woulbe A-plus.

Stephen Gallagher, Societe Generale: (A) He always did what he

believed wasright for the country. Time may tell us that his

monetary policy took pressure off fisc

policy, and therefore contributed to poor fiscal policy.

Dennis Gartman, The Gartman Letter: (B) His actions in the

autumn of '08 were"world saving" in nature and we all owe him a

debt of gratitude.

Stuart Hoffman, PNC: (A) National hero!

Hugh Johnson, Hugh Johnson Advisors: (A) His thorough knowledge

of financialand economic history as well as his quite sensible,

practical approach to conduct ofmonetary policy as well as ability

to ignore the noise of critics has been indispensable

during the crisis and recovery.

John Kattar, Ardent Asset Advisors: (C) Grade reduced because QE

overstayed itwelcome.

Barry Knapp, Barclays PLC: (B) A for the crisis, incomplete from

2010-2013 as thecosts will be realized over time.

-

8/13/2019 CNBC Fed Survey, December 17, 2013

10/36

CNBC Fed Survey December 17, 2013Page 10 of 36

FED SURVEYDecember 17, 2013

David Kotok, Cumberland Advisors: (C) Too slow to change before

Lehman-AIGdebacle. Then, and after, he reacted decisively.

Guy LeBas, Janney Montgomery Scott: (A) The Fed is the only

central bank thatmanaged a "first in, first out" policy when it

comes to supporting the economy during

the Financial Crisis/Great Recession.

Donald Luskin, Trend Macrolytics: (B) Bernanke is a great

patriot, and thank Godhe was on duty when the crisis hit. But no

one is perfect, even him, so cant give an

Rob Morgan, Fulcrum Securities: (B) I might have given him an

'A' if he hadn't

discussed interest rate policy with a CNBC anchor at the White

House CorrespondentAssociation Dinner in 2006.

Lynn Reaser, Point Loma Nazarene University: (B) Chairman

Bernanke excelledpreventing a financial crisis from engulfing the

world economy, but policies were

launched without a total game plan in mind.

John Roberts, Hilliard Lyons: (B) Would probably offer a B+ if

the answer wasavailable. He definitely learned in the position, and

became better as time went on.

John Ryding, RDQ Economics: (C) A for handling the financial

crisis but a D for thmonetary policy leading up to the crisis (too

easy) and the continuation of QE.

Robert Shapiro, Sonecon: (B) A for crisis management and its

aftermath, C formissing the crisis was coming.

Stephen Stanley, Pierpont Securities: (C) Great in 2008 and

2009, horrible afterthe crisis.

Diane Swonk, Mesirow Financial: (A) He averted the equivalent of

a nuclear bomfor capitalism, although still damaged.

Mark Zandi, Moody's Analytics: (A) We got lucky Bernanke was

chairman duringthe Great Recession. He had the exact right skill

set to navigate through the worst

downturn since the depression.

-

8/13/2019 CNBC Fed Survey, December 17, 2013

11/36

-

8/13/2019 CNBC Fed Survey, December 17, 2013

12/36

-

8/13/2019 CNBC Fed Survey, December 17, 2013

13/36

CNBC Fed Survey December 17, 2013Page 13 of 36

FED SURVEYDecember 17, 2013

11.Since September 2012, market functioning in the governmenbond

market has:

2%

8%

4%3%

0%

19%

11%12%

17%

20%

24%

15%

60%

65%

47%46%

42%

50%

58%

15%

15%

29%

25%27%

16%

20%

2% 2% 2% 2%

3% 3%0%

10%

20%

30%

40%

50%

60%

70%

March 19 April 30 June 18 July 30 Sept 17 Oct 29 Dec 17

Worsened somewhat

Improved somewhat

Improved a lot

Sta ed the same

Worsened a lot

-

8/13/2019 CNBC Fed Survey, December 17, 2013

14/36

CNBC Fed Survey December 17, 2013Page 14 of 36

FED SURVEYDecember 17, 2013

12.Since September 2012, market functioning in the

mortgage-backed security market market has:

4%

2%

5%4% 5%

3%

31%

22%

21%

31%

23%

29%

20%

29%

39%

21%

31%

41%

37%

42%

20% 20%

32%

20%18% 18%

22%

2%

4%5%

6%

5%5% 5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

March 19 April 30 June 18 July 30 Sept 17 Oct 29 Dec 17

Stayed the same

Worsened a lot

Improved a lot

Worsened somewhat

Improved somewhat

-

8/13/2019 CNBC Fed Survey, December 17, 2013

15/36

CNBC Fed Survey December 17, 2013Page 15 of 36

FED SURVEYDecember 17, 2013

13.Compared with the debate that just ended in the fall, the

nexround of discussions to raise the debt ceiling and fund

thegovernment will be:

19%

44%

35%

2%

24%

49%

27%

0%

10%

23%

67%

0%2%

7%

91%

0%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

More contentious About the same Less contentious Don't

know/unsure

July 30 Sept 17 Oct 29 Dec 17

-

8/13/2019 CNBC Fed Survey, December 17, 2013

16/36

CNBC Fed Survey December 17, 2013Page 16 of 36

FED SURVEYDecember 17, 2013

14.What best describes your current attitude toward the

effectsof the financial crisis?

10%

90%

0% 0%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

It's over Effects still linger Effects still in fullforce

Don't know/unsure

-

8/13/2019 CNBC Fed Survey, December 17, 2013

17/36

CNBC Fed Survey December 17, 2013Page 17 of 36

FED SURVEYDecember 17, 2013

15.Where do you expect the S&P 500 stock index will be on

?

1547

15891612

1655

1691

1654

1685

1753

1773

1723

1751

1709

1752

1816 1814

1857

1,500

1,550

1,600

1,650

1,700

1,750

1,800

1,850

1,900

Jan 292013

Mar 19 Apr 30 Jun 18 Jul 30 Sep 6 Sep 30 Oct 29 Dec 17

Survey Dates

December 31, 2013 June 30, 2014 December 31, 2014

-

8/13/2019 CNBC Fed Survey, December 17, 2013

18/36

-

8/13/2019 CNBC Fed Survey, December 17, 2013

19/36

CNBC Fed Survey December 17, 2013Page 19 of 36

FED SURVEYDecember 17, 2013

17.What is your forecast for the year-over-year percentagechange

in real U.S. GDP for ?

January

23,2012

Mar

16

Apr

24

Jul

31

Sep

12

Dec

11

Jan

29,

2013

Mar

19

Apr

30

Jun

18

Jul

30

Sep

17

Oct

29

Dec

17

2013 +2.6 +2.7 +2.6 +2.3 +2.2 +1.9 +2.1 +2.1 +2.1 +2.1 +1.9 +2.0

+1.9 +2.2

2014 +2.6 +2.6 +2.6 +2.6 +2.5 +2.6 +2.5 +2.6

1.0%

1.5%

2.0%

2.5%

3.0%

Survey Dates

2013 2014

-

8/13/2019 CNBC Fed Survey, December 17, 2013

20/36

CNBC Fed Survey December 17, 2013Page 20 of 36

FED SURVEYDecember 17, 2013

18.Compared to last year, the holiday shopping season will

be:

8%

23%

35%

31%

0%

4%

0%

51%

17%

29%

2%

0%0%

10%

20%

30%

40%

50%

60%

A lot better Somewhatbetter

The same Somewhatworse

A lot worse Don'tknow/unsure

Oct 29 Dec 17

-

8/13/2019 CNBC Fed Survey, December 17, 2013

21/36

CNBC Fed Survey December 17, 2013Page 21 of 36

FED SURVEYDecember 17, 2013

19.What impact will the new health care law have on

near-termeconomic growth?

63.4%

29.3%

0.0%

7.3%

0%

10%

20%

30%

40%

50%

60%

70%

Lower growth No effect on growth Stronger growth Don't

know/unsure

-

8/13/2019 CNBC Fed Survey, December 17, 2013

22/36

CNBC Fed Survey December 17, 2013Page 22 of 36

FED SURVEYDecember 17, 2013

What are the primary channels for that impact?

32%

3%

19%

13%

7% 7% 7%

13%

0%

5%

10%

15%

20%

25%

30%

35%

-

8/13/2019 CNBC Fed Survey, December 17, 2013

23/36

-

8/13/2019 CNBC Fed Survey, December 17, 2013

24/36

CNBC Fed Survey December 17, 2013Page 24 of 36

FED SURVEYDecember 17, 2013

20.What impact will the new health care law have on

long-termeconomic growth?

58%

23%

13%

8%

0%

10%

20%

30%

40%

50%

60%

70%

Lower growth No effect on growth Stronger growth Don't

know/unsure

-

8/13/2019 CNBC Fed Survey, December 17, 2013

25/36

CNBC Fed Survey December 17, 2013Page 25 of 36

FED SURVEYDecember 17, 2013

What are the primary channels for that impact?

Other responses:

Stronger growth: Healthier workforce Lower growth: Higher taxes

and government spending No effect on growth: Improved efficiency No

effect on growth: More long-term impact on access than on

economic

growth

23%

10%

23%

3% 3%

10% 10%

3%

16%

0%

5%

10%

15%

20%

25%

-

8/13/2019 CNBC Fed Survey, December 17, 2013

26/36

CNBC Fed Survey December 17, 2013Page 26 of 36

FED SURVEYDecember 17, 2013

Comments:

Dean Baker, Center for Economic and Policy Research: We will

also see morebusiness start-ups.

Subodh Kumar, Subodh Kumar & Associates: Long-term impact is

one to improvhealth care spending efficiency by companies and

government alike.

Guy LeBas, Janney Montgomery Scott: Requiring consumers to buy

health carereduces the uncertainty of future earnings and should

improve spending marginally,

but much of the impact will be offset by shifts in the cost of

labor on the part ofbusinesses.

John Lonski, Moody's: Will function as an effective tax hike for

middle- to upper-income consumers who do the bulk of the

spending.

Donald Luskin, Trend Macrolytics: People won't be as productive

when theirgovernment treats them as slaves.

Lynn Reaser, Point Loma Nazarene University: The Affordable Care

Act does littto control costs but only increases demand. That will

strain both public and private

finances.

-

8/13/2019 CNBC Fed Survey, December 17, 2013

27/36

CNBC Fed Survey December 17, 2013Page 27 of 36

FED SURVEYDecember 17, 2013

21.When do you think the FOMC will first increase the fed

fundsrate?

Increase fed funds rate

(Average response)

Survey Date

Dec

11,

2012

Jan

29,

2013

Mar

19,

2013

Apr

30,

2013

Jun

18,

2013

Jul

30,

2013

Sept

6,

2013

Sept

17,

2013

Oct

29,

2013

Dec

17,

2013

2013 Q2

Q3

Q4

2014 Q1

Q2

Q3

Q4

2015 Q12015

Q12015

Q12015

Q1

Q22015

Q22015

Q22015

Q2

Q32015

Q32015

Q32015

Q32015

Q3

Q4

2016 Q1

Q2

Q3

Q4

2017 or later

-

8/13/2019 CNBC Fed Survey, December 17, 2013

28/36

-

8/13/2019 CNBC Fed Survey, December 17, 2013

29/36

CNBC Fed Survey December 17, 2013Page 29 of 36

FED SURVEYDecember 17, 2013

24.Where do you expect the fed funds target rate will be on

?

Jul31

Sep12

Dec11

Jan

29'13

Mar19

Apr30

Jun18

Jul30

Sep6

Sep17

Oct29

Dec17

Dec 31, 2013

0.330.270.210.170.190.190.160.150.130.130.110.12June 30, 2014

0.200.180.160.140.130.14

Dec 31, 2014 0.28 0.21 0.21 0.20

Dec 31, 2015 0.97 0.92 0.82 0.70

0.33%

0.27%

0.21%

0.17%0.19% 0.19%

0.16%0.15%

0.13% 0.13%0.11%

0.12%

0.20%

0.18%

0.16%

0.14% 0.13% 0.14%

0.28%

0.21%0.21%

0.20%

0.97%0.92%

0.82%

0.70%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

-

8/13/2019 CNBC Fed Survey, December 17, 2013

30/36

-

8/13/2019 CNBC Fed Survey, December 17, 2013

31/36

-

8/13/2019 CNBC Fed Survey, December 17, 2013

32/36

CNBC Fed Survey December 17, 2013Page 32 of 36

FED SURVEYDecember 17, 2013

27.What is your primary area of interest?

Comments:

Tony Crescenzi, PIMCO:Twas the night before the September Fed

meeting, when all throughthe house,Not a computer was stirring, not

even its mouse;The sell tickets were stacked throughout the trade

floor with care,In fret that Ben Scrooge Bernanke soon would be

there.Then on the wires there arose a surprise clatter,The Fed said

no taper it wants to make wallets fatter!Into the dustbin went the

red tickets in a flash,

Today there is joy the Feds printing cash!

In May, Federal Reserve Chairman Ben Bernanke surprised

manyinvestors when he hinted that the Fed might reduce its monthly

bondbuying. His words sent the markets into turmoil, in particular

theglobal bond market, sending one of the strongest messages of

2013

Economics42%

Equities17%

Fixed Income20%

Currencies2%

Other20%

-

8/13/2019 CNBC Fed Survey, December 17, 2013

33/36

CNBC Fed Survey December 17, 2013Page 33 of 36

FED SURVEYDecember 17, 2013

to the Fed and markets. What the Fed hoped would happen didnt.It

hoped that its cumulative bond buying would keep interest rates

stable even if it hinted at a reduction in monthly purchases. In

otherwords, the Fed expected the stock effect of its purchases to

be morepotent than the flow effect. This makes intuitive sense,

after all. Whyshould a reduction of, say, billion out of billion in

monthly purchasesupset the bond market when the Fed had already

bought trillions ofdollars worth of bonds, bonds that the Fed may

never sell, therebyleaving investors with plenty of money to invest

in their wish list offavorite things? This is why it is pivoting to

place emphasis onforward guidance. The Fed thought it did something

nice. But

instead, something nice turned into something naughty, because

theFed spoiled investors with its bond buying and lulled them to

sleepbefore awakening them with the taper clatter. So, when

Santachecks his list, he might just decide to put coal instead of

gifts in theFeds stock-ing. The summer turbulence showed that the

Fed in theend seems to have about as much to give to the global

economy asa mall Santa can give to a curlicued little girl.

John Donaldson, Haverford Trust Co.: The budget deal makes a

taper more likely. Bernanke was very pointed during his

Septemberpress conference that the budget/debt ceiling mess was a

concern tothe FOMC. This deal removes that concern and opens the

door to ataper.

Mike Dueker, Russell Investments: The U.S. economy shouldachieve

nominal GDP growth next year of 4.5 percent after beingstuck barely

above 3 percent for several years. The Fed'squantitative easing

policy should be considered a smashing success

by this measure, especially relative to Europe and Japan.

Dennis Gartman, The Gartman Letter: Dr. Bernanke truly

savedcapitalism with his aggressive injection of reserves in the

autumn of'08, and although the 2nd and 3rd rounds of QE were

perhaps a steptoo far what he did then should never be forgotten

and always be

-

8/13/2019 CNBC Fed Survey, December 17, 2013

34/36

CNBC Fed Survey December 17, 2013Page 34 of 36

FED SURVEYDecember 17, 2013

congratulated.

Kevin Giddis, Raymond James/Morgan Keegan: While all signsseem

to indicate that we have turned the corner, I remain concernedover

the quality of the jobs created, and their ability to pushspending

upward beyond the current levels. Growth...slow. QualityJobs...few.

Rates...low.

Stuart Hoffman, PNC: The U.S. economy is ending 2013 on a

solidnote and that will continue throughout 2014 in harmony with

globaleconomic improvement. This will be beautiful music to the

ears of

stock investors but static to the ears of bond investors.

John Kattar, Ardent Asset Advisors: Tapering is coming, and

Iexpect QE to be reduced by 40% for the full year 2014 vs. 2013.But

that's still a lot of money. After some early volatility around

thetaper announcement, stocks should have another good year.

Barry Knapp, Barclays PLC: The timing of the first hike

discountedby the eurodollar market is reasonable however the

expected pace of

removal of policy accommodation from 2015-2018 is way

toopassive. For this reason any offsetting compensation in forward

rateguidance for the reduction in asset purchases is likely to

beunsuccessful. In other words the belly of the Treasury curve

isvulnerable to rate hikes getting pulled forward. Equities will

correctthrough this process as they have in every business cycle

sinceWWII when Fed policy attempts to catch-up to the improvement

inthe outlook that has already been discounted by the yield curve

andstock market.

David Kotok, Cumberland Advisors: In 100 years of history,

theFed has never confronted anything like the present policy

transition.The Yellen Fed will be writing a new chapter in central

bankingarchives.

-

8/13/2019 CNBC Fed Survey, December 17, 2013

35/36

-

8/13/2019 CNBC Fed Survey, December 17, 2013

36/36

FED SURVEYDecember 17, 2013

whereby a consensus believes the draining of QE-created

excessreserves needs to be accomplished quickly. What may start out

as a

controlled taper probably mutates into a panic taper as the

yearprogresses. Why? Because money velocity turns up for the

firsttime in this recovery causing Fed policy to instantly look

behind thecurve and overdone.

Lynn Reaser, Point Loma Nazarene University: After five yearsof

extraordinary monetary ease, Federal Reserve officials are wary

ofremoving the "training wheels" too soon. At some point,

theeconomy will need to ride on its own, but policymakers are

worried

about inflicting too many scrapes and bruises along the way.

John Roberts, Hilliard Lyons: Easy money could continue

longerthan the market currently anticipates as Chairman

Bernanke'spolicies give new Chairman Yellen cover to be

accommodative for alonger period of time to more quickly reduce

unemployment. This isespecially salient if the neutering of the

filibuster allows thepresident to stock the Fed with more dovish

members. Recentimproving economic statistics does, however, lessen

this risk to

some degree.

John Ryding, RDQ Economics: What else does the Fed need tosee to

announce a taper? Job growth is running at 200K per month,real GDP

was 3.6% in Q3 and Q4 is looking fairly strong (ISM, jobs,retail

sales, jobless claims).

Diane Swonk, Mesirow Financial: The Fed's intent will be to

taperasset purchases without tapering stimulus; the trick will be

for them

effectively convey that message.