Embed Size (px)

DESCRIPTION

These survey results represent the opinions of 33 of the nation’s top money managers, investment strategists, and professional economists.They responded to CNBC’s invitation to participate in our online survey. Their responses were collected on January 22-23, 2015. Participants were not required to answer every question.Results are also shown for identical questions in earlier surveys.This is not intended to be a scientific poll and its results should not be extrapolated beyond those who did accept our invitation.

Citation preview

CNBC Fed Survey – January 27, 2015 Page 1 of 30

FED SURVEY January 27, 2015

These survey results represent the opinions of 33 of the nation’s top money managers, investment strategists, and professional economists. They responded to CNBC’s invitation to participate in our online survey. Their responses were collected

on January 22-23, 2015. Participants were not required to answer every question. Results are also shown for identical questions in earlier surveys.

This is not intended to be a scientific poll and its results should not be extrapolated beyond those who did accept our invitation.

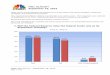

1. What is the probability the Fed will begin a new QE program in the next year/two years? (0%=No chance of new QE, 100%=Certainty

of new QE)

Note: In some previous surveys, this question was: “What is the probability the Fed will begin a new QE

program in the 12/24 months after it concludes the current QE program?”

10%

14%

9%

10%

14%

18%

14%

17%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Sep 16 Oct 28 Dec 16 Jan 27Chance of new QE

Next year Next two years

CNBC Fed Survey – January 27, 2015 Page 2 of 30

FED SURVEY January 27, 2015

2. The Fed will remove the phrase “patient” from its monetary

policy statement in ...

0%

0%

33%

27%

21%

0%

0%

3%

3%

0% 5% 10% 15% 20% 25% 30% 35%

January

February

March

April

June

July

August

September

October or later

CNBC Fed Survey – January 27, 2015 Page 3 of 30

FED SURVEY January 27, 2015

3. Relative to an economy operating at full capacity, what best describes your view of the amount of resource slack in the U.S. right now for labor?

48%

34%

20% 18%

16% 16%

36%

40%

60%

69%

55%

50%

4% 6%

3%

0% 0%

6%

8%

11%

6%

5%

24%

19%

4%

9% 9% 8%

5%

9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

July 29 August 20 Sep 16 Oct 28 Dec 16 Jan 27

Considerably more slack now Modestly more slack now

No difference Modestly less slack now

Considerably less slack now

Modestly less slack

Modestly more slack

Considerably less slack

No difference

Considerably more slack

CNBC Fed Survey – January 27, 2015 Page 4 of 30

FED SURVEY January 27, 2015

Relative to an economy operating at full capacity, what best describes your view of the amount of resource slack in the U.S. right now for production capacity?

8%

0%

56%

60%

64% 64%

55% 59%

13%

19%

24%

13%

9%

0%

10%

20%

30%

40%

50%

60%

70%

July 29 August 20 Sep 16 Oct 28 Dec 16 Jan 27

Considerably more slack now Modestly more slack now

No difference Modestly less slack now

Considerably less slack now

No difference

Modestly more slack

Modestly less slack

Considerably less slack

Considerably more slack

CNBC Fed Survey – January 27, 2015 Page 5 of 30

FED SURVEY January 27, 2015

4. Where do you expect the S&P 500 stock index will be on … ?

2017 2029

2053

2109

2066

2093

2122 2075

2149

2111

2194

2187

2250 2248

2311 2296

1,800

1,900

2,000

2,100

2,200

2,300

2,400

Apr 28 Jun 4 July 29 Sep 16 Oct 28 Dec 16 Jan 27

Survey Dates

June 30, 2015 December 31, 2015

June 30, 2016 December 31, 2016

CNBC Fed Survey – January 27, 2015 Page 6 of 30

FED SURVEY January 27, 2015

5. What do you expect the yield on the 10-year Treasury note will be on … ?

3.54%

3.24%

3.15% 3.16%

2.90%

2.63%

2.14%

3.43% 3.45%

3.19%

2.96%

2.54%

3.30%

2.80%

3.52%

3.04%

2.0%

2.5%

3.0%

3.5%

4.0%

Apr 28 Jun 4 Jul 29 Sep 16 Oct 28 Dec 16 Jan 27

Survey Dates

June 30, 2015 December 31, 2015

June 30, 2016 December 31, 2016

CNBC Fed Survey – January 27, 2015 Page 7 of 30

FED SURVEY January 27, 2015

6. Which of the following reasons primarily account for low interest rates on U.S. government debt? (Select one or two reasons)

72%

19%

13%

19%

28%

3%

9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Other responses: - High demand relative to supply - Higher U.S. growth and interest rate 0utlook relative to other countries - Low competitive yields on other Sovereigns

CNBC Fed Survey – January 27, 2015 Page 8 of 30

FED SURVEY January 27, 2015

7. What is your forecast for the year-over-year percentage change in real U.S. GDP for …?

Jan 28,'14

Mar 18 Apr 28 Jun 4 Jul 29 Sep 16 Oct 28 Dec 16Jan 27,

'15

2015 +2.90% +3.02% +3.00% +2.81% +2.75% +2.90% +2.90% +3.02% +2.99%

2016 +2.88% +2.80%

+2.90%

+3.02%

+3.00%

+2.81%

+2.75%

+2.90% +2.90%

+3.02%

+2.99%

+2.88%

+2.80%

2.7%

2.8%

2.8%

2.9%

2.9%

3.0%

3.0%

3.1%

2015 2016

CNBC Fed Survey – January 27, 2015 Page 9 of 30

FED SURVEY January 27, 2015

8. What is your forecast for the year-over-year percentage change in the headline U.S. CPI for …?

2.02%

2.29% 2.27%

2.01%

1.74%

1.17%

2.17%

2.07%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2.2%

2.4%

Jun 4 Jul 29 Sep 16 Oct 28 Dec 16 Jan 27, '15

Survey Dates

2015 2016

CNBC Fed Survey – January 27, 2015 Page 10 of 30

FED SURVEY January 27, 2015

9. When do you expect the Fed to allow its balance sheet to decline?

Note: In the April survey, the question was phrased as: “When do you believe the Fed will begin

reducing the size of its balance sheet?”

0%

5%

10%

15%

20%

25%

30%

35%

Oct

Nov

Dec

Jan

'1

5

Feb

Mar

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

Nov

Dec

Jan

'1

6

Feb

Mar

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

Nov

Dec

Jan

'1

7

Aft

er J

an…

Apr 28 Jun 4 Jul 29 Sep 16 Oct 28 Dec 16 Jan 27 '15

Averages: April 28 survey: Oct '15

June 4 survey: Mar '16

June 29 survey: Dec '15

Sept. 16 survey: Dec '15

Oct. 28 survey: Jan '16

Dec. 16 survey: Feb '16

Jan. 27 survey: Apr '16

CNBC Fed Survey – January 27, 2015 Page 11 of 30

FED SURVEY January 27, 2015

10. When do you think the FOMC will first increase the fed funds rate?

0%

10%

20%

30%

40%

50%

60%

Au

g

Sep

Oct

Nov

Dec

Jan '1

5

Feb

Mar

Ap

r

May

Ju

n

Ju

l

Au

g

Sep

Oct

Nov

Dec

Jan '1

6

Feb

Mar

Ap

r

May

Ju

n

Ju

l

Au

g

Sep

Oct

Nov

Dec

Jan '1

7

Aft

er

Jan

'1

7

Feb

Mar

Aft

er

Mar '17

April 28 Jun 4 Jun 29 Aug 20

Sep 16 Oct 28 Dec 16 Jan 27 '15

Averages: April 28 survey:

July 2015

June 4 survey:

August 2015

July 29 survey:

August 2015

Aug 20 survey:

July 2015

Sep 16 survey:

June 2015

Oct 28 survey:

July 2015

Dec 16 survey:

July 2015

Jan 27 '15 survey:

Sep 2015

CNBC Fed Survey – January 27, 2015 Page 12 of 30

FED SURVEY January 27, 2015

11. How would you characterize the Fed's current monetary policy?

28%

49%

46%

49%

44%

39%

50%

43% 43%

49%

43%

49% 50%

47%

17%

6%

3% 3% 3%

6%

0%

13%

3% 3%

6% 5% 6%

3%

0%

10%

20%

30%

40%

50%

60%

Jul 31, '12 Jul 29, '14 Aug 20 Sep 16 Oct 28 Dec 16 Jan 27, '15

Too accommodative Just right Too restrictive Don't know/unsure

Too accomodative

Don't know/unsure

Too restrictive

Just right

CNBC Fed Survey – January 27, 2015 Page 13 of 30

FED SURVEY January 27, 2015

12. Where do you expect the fed funds target rate will be on … ?

Jul

30

Sep

17

Oct

29

Dec

17

Jan

28

'14

Mar

18

Apr

28

Jun

4

Jul

29

Aug

20

Sep

16

Oct

28

Dec

16

Jan

27,

'15

Jun 30, 2015 0.50%0.39%0.40%0.33%0.31%0.25%

Dec 31, 2015 0.97%0.92%0.82%0.70%0.72%0.83%0.99%0.68%1.05%0.89%0.98%0.89%0.83%0.73%

Jun 30, 2016 1.53%1.56%1.48%1.38%1.26%

Dec 31, 2016 1.99%2.13%2.04%1.93%1.75%

0.50%

0.39% 0.40%

0.33% 0.31%

0.25%

0.97% 0.92%

0.82%

0.70% 0.72%

0.83%

0.99%

0.68%

1.05%

0.89%

0.98%

0.89%

0.83%

0.73%

1.53% 1.56%

1.48%

1.38%

1.26%

1.99%

2.13%

2.04%

1.93%

1.75%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Dec 2016

June 2016

Dec 2015

June 2015

CNBC Fed Survey – January 27, 2015 Page 14 of 30

FED SURVEY January 27, 2015

13. At what fed funds level will the Federal Reserve stop hiking rates in the current cycle? That is, what will be the terminal rate?

3.16% 3.20% 3.30%

3.17% 3.11%

Aug 20 Sep 16 Oct 28 Dec 16 Jan 27, '15

CNBC Fed Survey – January 27, 2015 Page 15 of 30

FED SURVEY January 27, 2015

14. When do you believe fed funds will reach its terminal rate?

0%

5%

10%

15%

20%

25%

30%

35%

40%

Aug 20 Sep 16 Oct 28 Dec 16 Jan 27 '15

Average:

Aug 20 survey:

Q4 2017

Sep 16 survey

Q3 2017

Oct 28 survey

Q4 2017

Dec 16 survey

Q1 2018

Jan 27 survey

Q1 2018

CNBC Fed Survey – January 27, 2015 Page 16 of 30

FED SURVEY January 27, 2015

15. How will lower oil prices affect U.S. GDP/core inflation in 2015?

0.27

-0.28

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

GDP Inflation

Pct

. po

ints

CNBC Fed Survey – January 27, 2015 Page 17 of 30

FED SURVEY January 27, 2015

17. What is your forecast for WTI crude oil's lowest price in the current downturn?

$40

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

Average Forecast

CNBC Fed Survey – January 27, 2015 Page 18 of 30

FED SURVEY January 27, 2015

18. The current decline in oil prices is primarily the result of:

56%

13%

28%

3%

0%

10%

20%

30%

40%

50%

60%

Excess supply Weak demand Equal parts excess

supply and weakdemand

Don't know/unsure

CNBC Fed Survey – January 27, 2015 Page 19 of 30

FED SURVEY January 27, 2015

19. Over the course of the announced new program, what will be the effect of European QE in the following areas relative to their current level?

6%

56%

50%

22%

31%

34%

41%

16%

44%

6%

31%

63%

66%

3%

34%

34%

94%

69%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

European inflation

European economic growth

European unemployment

European interest rates

U.S. interest rates

European stocks

U.S. stocks

Lower No change Higher

CNBC Fed Survey – January 27, 2015 Page 20 of 30

FED SURVEY January 27, 2015

20. Relative to your expectations, the QE program announced by the ECB was:

63%

9%

28%

0%

10%

20%

30%

40%

50%

60%

70%

More aggressive Less aggressive As expected

CNBC Fed Survey – January 27, 2015 Page 21 of 30

FED SURVEY January 27, 2015

21. The ECB will hit its 2% inflation target within:

3%

22%

34%

13% 13%

16%

0%

5%

10%

15%

20%

25%

30%

35%

40%

One year Two years Three years Four years Five or moreyears

Don'tknow/unsure

CNBC Fed Survey – January 27, 2015 Page 22 of 30

FED SURVEY January 27, 2015

22. European QE announced Thursday makes a Fed rate hike:

25%

13%

63%

0%

10%

20%

30%

40%

50%

60%

70%

More likely Less likely No effect

CNBC Fed Survey – January 27, 2015 Page 23 of 30

FED SURVEY January 27, 2015

23. How much concern do you have that economic weakness in Europe could create wider global risks? (1=Not concerned at all, 10=Highest level of concern)

5.4 5.4

4.8 5.0

0

1

2

3

4

5

6

7

8

9

10

Sep 16 Oct 28 Dec 16 Jan 27 '15

CNBC Fed Survey – January 27, 2015 Page 24 of 30

FED SURVEY January 27, 2015

24. Has the U.S. stock market already discounted a fed funds rate hike by the Federal Reserve next year?

56%

36%

8%

53%

38%

9%

0%

10%

20%

30%

40%

50%

60%

Yes No Don't know/unsure

Dec 16 Jan 27

CNBC Fed Survey – January 27, 2015 Page 25 of 30

FED SURVEY January 27, 2015

25. What is the single biggest threat facing the U.S. economic recovery?

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

European recession/financial crisis

Tax/regulatory policies

Slow job growth

Inflation

Deflation

Debt ceiling

Rise in interest rates

Geopolitical risks

Global economic weakness

Slow wage growth

Other

Don't know/unsure

Europeanrecession/financial

crisis

Tax/regulatory

policies

Slow jobgrowth

InflationDeflationDebt

ceiling

Rise ininterest

rates

Geopolitical risks

Globaleconomicweakness

Slow wagegrowth

OtherDon't

know/unsure

Apr 30 20%31%20%0%2%2%11%0%

Jun 18 15%28%20%3%3%0%13%0%

Jul 30 8%30%22%0%2%2%10%14%4%

Sep 17 4%27%22%2%0%4%18%7%2%

Oct 29 8%29%24%3%3%3%8%13%0%

Dec 17 5%32%29%2%0%2%15%2%2%

Jan 28 '14 7%21%30%2%0%0%12%21%0%

Mar 18 10%23%26%3%5%0%5%18%0%

Apr 28 3%26%21%3%5%0%8%18%13%0%

Jul 29 12%29%12%6%3%0%12%12%12%3%

Sep 16 6%26%29%6%3%0%6%11%11%3%

Oct 28 31%18%15%3%3%0%10%8%8%3%

Dec 16 40%14%14%3%6%0%3%14%3%0%

Jan 27 '15 0%13%9%0%0%0%6%16%41%6%16%0%

Apr 30 Jun 18 Jul 30 Sep 17 Oct 29 Dec 17 Jan 28 '14

Mar 18 Apr 28 Jul 29 Sep 16 Oct 28 Dec 16 Jan 27 '15

CNBC Fed Survey – January 27, 2015 Page 26 of 30

FED SURVEY January 27, 2015

FED SURVEY April 30,

Other responses:

"Fears" of inflation/overheat/is Fed behind the curve

Chinese economic or fiscal problems

Congress

Entitlements Rising dollar

26. In the next 12 months, what percent probability do you

place on the U.S. entering recession? (0%=No chance of recession, 100%=Certainty of recession)

Aug

11,201

1

Sep

19

Oct

31

Jan

23,201

2

Mar

16

Apr

24

Jul

31

Sep

12

Dec

11

Jan

29,201

3

Mar

19

Apr

30

Jun

18

Jul

30

Sep

6

Oct

29

Dec

17

Jan

28201

4

Mar

18

Apr

28

Jul

29

Sep

16

Oct

28

Dec

16

Jan

27'15

Series1 34.0 36.1 25.5 20.3 19.1 20.6 25.9 26.0 28.5 20.4 17.6 18.2 15.2 16.2 16.9 18.4 17.3 15.3 16.9 14.6 16.2 15.0 15.1 13.6 13.0

34.0%

36.1%

25.5%

20.3%

19.1%

20.6%

25.9%

26.0%

28.5%

20.4%

17.6%

18.2%

15.2%

16.2% 16.9%

18.4%

17.3%

15.3%

16.9%

14.6%

16.2%

15.0% 15.1%

13.6% 13.0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Survey Dates

CNBC Fed Survey – January 27, 2015 Page 27 of 30

FED SURVEY January 27, 2015

FED SURVEY April 30,

27. What is your primary area of interest?

Comments: John Donaldson, Haverford Trust Co.: The FOMC is in a terrible spot here. They need to begin to normalize rates so they have the

full range of tools available if/when they need them in the next cycle. The markets seem to think that even adjusting policy rates to 1% is equivalent to an economy-choking tightening. No matter where the Fed takes the Funds rate, it would still be an exceptionally

accommodative policy. Mike Englund, Action Economics: As the world's central banks continue to swap sovereign term-debt with overnight central bank

reserve credit, forcing lenders to bid up the price of the remaining debt and equity instruments, it is likely that central banks are inflating term-asset values, but unlikely that they are increasing the willingness of investors to take risk. Indeed, risk-taking behavior for

direct investment is likely being trimmed, leaving these global strategies counter-productive at best.

Economics 53%

Equities 9%

Fixed Income 16%

Currencies 0%

Other 22%

CNBC Fed Survey – January 27, 2015 Page 28 of 30

FED SURVEY January 27, 2015

FED SURVEY April 30,

Kevin Giddis, Raymond James/Morgan Keegan: The U.S. economy is battling different forces in 2015 vs. 2014. Low wage growth and a lack of inflation pose more than idle threats to economic growth. If progress isn't made on both of these fronts,

then there is a risk, coupled with a global slowdown, that the U.S. growth rate would retreat to levels that could be compared to a recession.

Hugh Johnson, Hugh Johnson Advisors: Prospects for the U.S. stock market remain quite modest given (a) a growth rate for 2015 and 2016 S&P earnings of 4.4% and 4.5% respectively and (b) a modest shift toward restraint by the Fed (preventing multiple

expansion). This forecast is of course consistent with common sense after double-digit gains in each of the last two years. A higher return than 5% is possible if (a) earnings are stronger than forecast or (b) there is a surge in speculation in U.S. financial markets driven in part

by a stronger dollar. Not to be taken lightly or dismissed. The biggest risk, from the decline in oil and commodity prices, is the transmission of a Russian recession (deep recession in 2015) to Europe, China, and beyond although it is unlikely to derail the U.S.

expansion. With luck, we will muddle through. John Kattar, Ardent Asset Advisors: The Fed seems to have

decided to raise rates later this year, almost irrespective of the data. The greatest risk to that scenario is further and persistent dollar strength.

David Kotok, Cumberland Advisors: There is much more longer- term upside ahead from Eurozone QE. The bull market in stocks is not over.

Rob Morgan, V2V Associates: The media has focused intently on deflation lately. I think the most serious deflation problem involves the New England Patriots and footballs, not the deflation problem with worldwide economies.

CNBC Fed Survey – January 27, 2015 Page 29 of 30

FED SURVEY January 27, 2015

FED SURVEY April 30,

Joel Naroff, Naroff Economic Advisors: QE in Europe will only add to U.S. growth, lowering the unemployment rate and adding to the wage pressures that should ultimately raise inflation.

James Paulsen, Wells Capital Management: We enter 2015 with broad-based concerns about global deflation. Given the massive declines in sovereign bond yields about the globe and a large decline in energy costs, international and U.S. economic growth is likely to

improve in 2015. If global growth bounces, current deflation fears will likely fade and within the U.S., overheat fears may materialize as the unemployment rate heads below 5%. That is, could 2015 begin with deflationary fears and end with inflationary fears?

Lynn Reaser, Point Loma Nazarene University: As the Fed parts company with other central banks, it faces a potentially hazardous road. Oil could be especially slippery, giving the economy either

more or less growth and more or less headline inflation. John Ryding, RDQ Economics: In my judgment markets are underestimating the degree to which falling unemployment will push

the Fed to hiking rates and overestimating the influence of factors such as events in the euro area

Allen Sinai, Decision Economics: The ECB and other central banks are still running the show. The best is yet to come in global stock markets. The ECB action was absolutely brilliant monetary policy making.

Mark Vitner, Wells Fargo: We expect single-family homebuilding to be an upside surprise in 2015. On the downside, the dramatic rise in the value of the dollar and the global economic slowdown are

taking a toll on U.S. manufacturing. Exports are faltering and imports are rising. Scott Wren, Wells Fargo Advisors: The magnitude of the ECB's

CNBC Fed Survey – January 27, 2015 Page 30 of 30

FED SURVEY January 27, 2015

FED SURVEY April 30,

announced QE program is not a cure-all for Euro zone woes. It is likely more QE will follow the already announced amount. Structural issues in terms of the labor market and sovereign debt levels need to be addressed. The ECB is merely "pushing on a string" with this first

stab at reviving the economy and avoiding deflation. Solid, dependable improvement is going to likely take years....and more extreme action from the ECB and Euro zone governments.

Mark Zandi, Moody's Analytics: Despite all the cross-currents and heightened volatility in global financial and commodity markets, U.S. economic growth prospects remain strong.