-

8/13/2019 CNBC Fed Survey results, January 28, 2014

1/26

CNBC Fed Survey January 28, 2014Page 1 of 26

FED SURVEYJanuary 28, 2014

These survey results represent the opinions of 45 of the nations

top money managers, investment

strategists, and professional economists.

They responded to CNBCs invitation to participate in our online

survey. Their responses were collecte

on January 23-24, 2014. Participants were not required to answer

every question.

Results are also shown for identical questions in earlier

surveys.

This is not intended to be a scientific poll and its results

should not be extrapolated beyond those who

did accept our invitation.

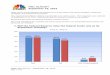

1.For all of 2014 and 2015 (and only in those years), what is

thetotal amount of additional asset purchases the Federal

Reserve

will have made?

$370.6 $367.1 $373.5 $374.8$381.9

$646.1

$497.0

$466.6

$96.3 $94.2

$0

$100

$200

$300

$400

$500

$600

$700

Apr 30,2013

Jun 18 Jul 30 Sep 6 Sep 17 Sep 29 Dec 17 Jan 28,2014

Billions

2014 2015

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

2/26

CNBC Fed Survey January 28, 2014Page 2 of 26

FED SURVEYJanuary 28, 2014

2.Do you expect the Federal Reserve to taper its purchases

ofassets at the January meeting?

87%

11%

2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Yes No Don't know/unsure

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

3/26

CNBC Fed Survey January 28, 2014Page 3 of 26

FED SURVEYJanuary 28, 2014

By how much do you expect the Federal Reserve to taper at

its

January meeting?(Only asked of those who said yes to Q2.)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$5 $10 $15 $20 $25 $30 $35 $40 $45 $50 More

than

$50

Billions

Average:

$9.868billion

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

4/26

CNBC Fed Survey January 28, 2014Page 4 of 26

FED SURVEYJanuary 28, 2014

What mix of Treasuries vs. mortgage-backed securities do you

expect in the Federal Reserve's taper?(Only asked of those who

saidyes to Q2.)

Treasuries52.27%

MBS47.73%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

5/26

CNBC Fed Survey January 28, 2014Page 5 of 26

FED SURVEYJanuary 28, 2014

3.Do you expect the Federal Reserve to reduce its purchases

ateach of its post-January meetings this year?

72%

28%

0%0%

10%

20%

30%

40%

50%

60%

70%

80%

Yes No Don't know/unsure

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

6/26

CNBC Fed Survey January 28, 2014Page 6 of 26

FED SURVEYJanuary 28, 2014

What is the average amount of tapering you expect at each

meeting? (Only asked of those who said yes to Q3.)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$5 $10 $15 $20 $25 $30 $35 $40 $45 $50

Billions

Average:

$10.65billion

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

7/26

CNBC Fed Survey January 28, 2014Page 7 of 26

FED SURVEYJanuary 28, 2014

4.The Federal Reserve should:

29%

19%

50%

2%

0%

10%

20%

30%

40%

50%

60%

Taper faster Taper slower Taper at the samepace

Don't know/unsure

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

8/26

CNBC Fed Survey January 28, 2014Page 8 of 26

FED SURVEYJanuary 28, 2014

5.What impact will tapering have on ?

56%

35%

7%

2%

7%

54%

35%

5%

14%

83%

2%0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Move higher Have no effect Move lower Don't know/unsure

Bond yields Stock values Unemployment rate

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

9/26

CNBC Fed Survey January 28, 2014Page 9 of 26

FED SURVEYJanuary 28, 2014

6.The Federal Reserve has strengthened its guidance aboutkeeping

rates lower for longer, at least in part as an offset tothe effects

of tapering. When it comes to keeping interest rateslow:

21%

35%

40%

5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Guidance is a good

substitute for asset

purchases

Guidance is more

effective than asset

purchases

Guidance is less

effective than asset

purchases

Don't know/unsure

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

10/26

CNBC Fed Survey January 28, 2014Page 10 of 26

FED SURVEYJanuary 28, 2014

7.Given what you know about new presidential appointees to

theFederal Reserve Board and the bank presidents who will votethis

year on the Federal Open Market Committee, would youcharacterize

the voting members of the committee in 2014compared to 2013 as:

0%

26%

38%

33%

2%

0%0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Much moredovish

Somewhatmore dovish

About thesame

Somewhatmore

hawkish

Much morehawkish

Don'tknow/unsure

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

11/26

CNBC Fed Survey January 28, 2014Page 11 of 26

FED SURVEYJanuary 28, 2014

8.Compared to Ben Bernanke, Fed chair nominee Janet Yellen

wibe:

15%

44%

28%

3%

0%

10%

2%

52%

33%

10%

0%

2%

7%

40%

51%

0% 0%

2%

0%

10%

20%

30%

40%

50%

60%

Much moredovish

Somewhatmore dovish

No different Somewhatmore

hawkish

Much morehawkish

Don'tknow/unsure

Oct 29 Dec 17 Jan 28

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

12/26

CNBC Fed Survey January 28, 2014Page 12 of 26

FED SURVEYJanuary 28, 2014

9.Overall, how do you rate the clarity and credibility of

Fedcommunications?

5%

55%

21%

18%

0%

7%

54%

24%

15%

0%

7%

56%

26%

12%

0%0%

10%

20%

30%

40%

50%

60%

Very clear andcredible

Somewhat clearand credible

Somewhat notclear and

credible

Not very clearand credible

Don'tknow/unsure

Oct 29 Dec 17 Jan 28

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

13/26

CNBC Fed Survey January 28, 2014Page 13 of 26

FED SURVEYJanuary 28, 2014

10. Which of these is the bigger risk to your forecast for

Fedpolicy this year?

28%

37%

35%

0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Fed will be moredovish than I

expect

Fed will be morehawkish than I

expect

Risks are balanced Don't know/unsure

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

14/26

CNBC Fed Survey January 28, 2014Page 14 of 26

FED SURVEYJanuary 28, 2014

11. Where do you expect the S&P 500 stock index will be on

?

1723

1751

1709

1752

1816 1814

18441857

1913

1,500

1,550

1,600

1,650

1,700

1,750

1,800

1,850

1,900

1,950

Jun 18 Jul 30 Sep 6 Sep 30 Oct 29 Dec 17 Jan 28

Survey Dates

June 30, 2014 December 31, 2014

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

15/26

CNBC Fed Survey January 28, 2014Page 15 of 26

FED SURVEYJanuary 28, 2014

12. What do you expect the yield on the 10-year Treasury

notewill be on ?

2.80%

3.10%

3.33%3.39%

3.00%

3.18%

3.08%

3.44%

3.37%

2.0%

2.5%

3.0%

3.5%

4.0%

Jun 18 Jul 30 Sep 6 Sep 30 Oct 29 Dec 17 Jan 28

Survey Dates

June 30, 2014 December 31, 2014

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

16/26

CNBC Fed Survey January 28, 2014Page 16 of 26

FED SURVEYJanuary 28, 2014

13. What is your forecast for the year-over-year

percentagechange in real U.S. GDP for ?

January

23,2012

Mar16

Apr24

Jul31

Sep12

Dec11

Jan29,

2013

Mar19

Apr30

Jun18

Jul30

Sep17

Oct29

Dec17

Jan28,

2014

2013 +2.6 +2.7 +2.6 +2.3 +2.2 +1.9 +2.1 +2.1 +2.1 +2.1 +1.9 +2.0

+1.9 +2.2 +2.32014 +2.6 +2.6 +2.6 +2.6 +2.5 +2.6 +2.5 +2.6 +2.8

2015 +2.9

+2.9%

1.0%

1.5%

2.0%

2.5%

3.0%

2013 2014 2015

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

17/26

CNBC Fed Survey January 28, 2014Page 17 of 26

FED SURVEYJanuary 28, 2014

14. When do you think the FOMC will first increase the fed

fundsrate?

Increase fed funds rate

(Average response)

Survey Date

Dec

11

Jan

29

13

Mar

19

Apr

30

Jun

18

Jul

30

Sept

6

Sept

17

Oct

29

Dec

17

Jan

28

14

2013 Q2

Q3

Q4

2014 Q1

Q2

Q3

Q4

2015 Q12015

Q12015

Q12015

Q1

Q22015

Q22015

Q22015

Q2

Q32015

Q32015

Q32015

Q32015

Q32015

Q3

Q4

2016 Q1

Q2

Q3

Q4

2017 orlater

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

18/26

CNBC Fed Survey January 28, 2014Page 18 of 26

FED SURVEYJanuary 28, 2014

15. Currently, Fed policy is not to raise interest rates until

theunemployment rate is at least 6.5%. Will the Fed change

thatguidance?

30%

60%

10%

44%

51%

4%

47%

42%

11%

49%

44%

7%

51%

42%

7%

0%

10%

20%

30%

40%

50%

60%

70%

Yes No Don't know/unsure

Jul 30 Sep 17 Oct 29 Dec 17 Jan 28

On average, those answeringyes thought the new rate will

be 6.0%

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

19/26

CNBC Fed Survey January 28, 2014Page 19 of 26

FED SURVEYJanuary 28, 2014

24.Where do you expect the fed funds target rate will be on

?

Jul 31Jun

18Jul 30 Sep 6

Sep

17

Oct

29

Dec

17

Jan

28June 30, 2014 0.20% 0.18% 0.16% 0.14% 0.13% 0.14% 0.16%

Dec 31, 2014 0.28% 0.21% 0.21% 0.20% 0.19%

Dec 31, 2015 0.97% 0.92% 0.82% 0.70% 0.72%

0.20%

0.18%

0.16%

0.14%0.13% 0.14%

0.16%

0.28%

0.21% 0.21%0.20%

0.19%

0.97%

0.92%

0.82%

0.70%0.72%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

20/26

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

21/26

CNBC Fed Survey January 28, 2014Page 21 of 26

FED SURVEYJanuary 28, 2014

26.What is the single biggest threat facing the U.S.

economicrecovery?

0% 5% 10% 15% 20% 25% 30% 3

European recession/financial crisis

Tax/regulatory policies

Slow job growth

High gasoline prices

Overall inflation

Deflation

Debt ceiling

Too little budget deficit reduction

Too much budget deficit reduction

Rise in interest rates

Other

Don't know/unsure

Europ

reces

/finan

cris

Tax/regul

atory

policies

Slow job

growth

High

gasoline

prices

Overall

inflationDeflation

Debt

ceiling

Too little

budget

deficit

reduction

Too

much

budget

deficit

reduction

Rise in

interest

rates

Other

Don't

know/un

sure

Apr 30 20%31%20%2%0%2%2%2%9%11%0%

Jun 18 15%28%20%2%3%3%0%2%13%13%0%

Jul 30 8%30%22%4%0%2%2%0%4%10%14%4%

Sep 17 4%27%22%7%2%0%4%2%4%18%7%2%

Oct 29 8%29%24%3%3%3%3%3%5%8%13%0%

Dec 17 5%32%29%5%2%0%2%2%2%15%2%2%

Jan 28 7%21%30%2%2%0%0%2%2%12%21%0%

Apr 30 Jun 18 Jul 30 Sep 17 Oct 29 Dec 17 Jan 28

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

22/26

CNBC Fed Survey January 28, 2014Page 22 of 26

FED SURVEYJanuary 28, 2014

27.What is your primary area of interest?

Comments:

Robert Brusca, Fact and Opinion Economics: The economy isupbeat

on the data and trend but end-2013 growth was too much onthe back

of inventories and we do not yet have reliable servicesector

spending OR job growth. Until we get that, strongerexpectations for

job growth are on thin ice. The waffling in auto salesat year-end

is getting NO attention whatsoever. Should it???

Tony Crescenzi, PIMCO: Janet Yellen enters a position shaped

by100 years of challenges, and she is as qualified as any incoming

Fed

chair to lead the Fed through the next set, a comforting thought

forinvestors. The attainment of price stability also means

protectingagainst an inflation rate that is too low, which is why

todayslowinflation rate will be one of Janet Yellensmost important

guidinglights. When Janet Yellen was nominated Fed chair, many

focusedon how she differed from her predecessor, Ben Bernanke. Many

still

Economics

45%

Equities19%

Fixed Income14%

Currencies0%

Other

21%

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

23/26

CNBC Fed Survey January 28, 2014Page 23 of 26

FED SURVEYJanuary 28, 2014

do. This is appropriate but only to a point. It is important

toremember that when Janet dons her cloaks as Fed chair, her

actions

will be guided by powerful precedents including the central

banksplethora of experiences, the institutionalization of its

processes, itssuccess in acting as a lender of last resort, and its

hard-won gains inachieving price stability.

Lou Crandall, Wrightson: Asset purchases are likely to be

negativein 2015, as the Fed is likely to start to let MBS run off

by the secondhalf of the year.

Frederic Dickson, D.A. Davidson & Co.: Economic

growthdepends in large part on regulatory stability--no new

surprises andgradual growth of our major European trading partners.

Increasedenergy production from the Bakken field is a huge positive

wild cardfor 2014 and 2015.

John Donaldson, Haverford Trust Co.: Rather than changing

theunemployment rate in their guidance, the FOMC will remove

aspecific target due to the issues with computation as a result

of

people leaving the labor force. I would not be surprised to

seecommentary that references a reversal in the trend to

actuallyincrease the labor force as a revised indicator for their

policydecisions.

Mike Dueker, Russell Investments: 2013 was a year in

whichmarkets re-evaluated recession risks. After the Great

Recessionmany people bought into the stall-speed story of more

frequentrecessions this decade. 2013 was the year in which the

stall-speed

story lost credence and the market realized that recession risks

arelow and should remain low for several years. Thus, 2014 is

like1996---a mid-cycle acceleration in the economy with low

perceivedrecession risks.

Kevin Giddis, Raymond James/Morgan Keegan: We are slowly

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

24/26

CNBC Fed Survey January 28, 2014Page 24 of 26

FED SURVEYJanuary 28, 2014

moving away from interest rates, the Fed, and job growth as

thecatalyst for and sustaining economic growth, to how much

Federal

debt and a lack of a budget deal are going to limit the

upsidepotential to the economy.

Hugh Johnson, Hugh Johnson Advisors: As stated previously,the

end of QE3 has been fully priced into the level of interest

ratesand equity prices. Equity prices moving from being 6%

overvalued(Q4 2013) to having been 4% overvalued. Likely to become

5%undervalued or reach 1700-1750 (S&P 500) before

correctionends...over time.

John Kattar, Ardent Asset Advisors: Markets are too shaky

totaper now, especially with the looming Bernanke-Yellen

transition.

Barry Knapp, Barclays PLC: The belly of the Treasury curve

ispricing too passive a rate normalization cycle. This is not a

questionof when the rate hikes begin but how fast they will

increase ratesonce the process starts. 100bp per year is discounted

by theEurodollar curve and 5-year Treasury yields. It is unlikely

to be less

than 2. This implies curve flattening which will curb equity

investors'late-2013 enthusiasm.

David Kotok, Cumberland Advisors: It is time to normalizecentral

banking in the United States. 2014 is the year.

Guy LeBas, Janney Montgomery Scott: If nothing else, 2014 isthe

"year of the consensus" among forecasters (bullish on

stocks,bearish on bonds), which increases the risks that stocks

underperform and bonds outperform expectations.

Fundamentalevents in emerging markets are increasingly concerning.

In 2013,we blamed capital flows for EM problems, but it appears

there aresome legitimate governance issues in China, Argentina,

Turkey, andThailand in particular.

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

25/26

CNBC Fed Survey January 28, 2014Page 25 of 26

FED SURVEYJanuary 28, 2014

John Lonski, Moody's: A 3% 10-year Treasury yield is

tooburdensome for the world economy. 2014-to-date's -4.2% drop

by

housing-sector share prices (that's deeper than the overall

-2.8%decline by the market value of US common stock) and the

-6.9%yearly drop by homebuyer mortgage applications of the latest

13-week span reinforce the view that Treasury bond yields are too

high.Eventually, markets will come to appreciate the

disinflationarynature of the unprecedented change in US

demographics, whereduring the next 10 years the number of Americans

aged 16 to 64years grows by less 0.5% annually, on average, while

the 65-yearsand older cohort expands by a much faster 3.5%

annually.

Drew Matus, UBS Investment Research: A key concern formarkets

should be the Fed's forward guidance for rates seemshistorically

abnormal, i.e. too slow and too long. A Taylor rule usingthe Fed's

forecasts shows a much sharper pace of tighteninghappening much

sooner. The outcome could be higher volatility.

Rob Morgan, Fulcrum Securities: Janet Yellen's biggest

challengemay be reducing the size of the Fed's balance sheet.

Joel Naroff, Naroff Economic Advisors: The unemployment rateis

likely to be below 6% by year's end and that should triggersharper

wage gains and a surge in spending and economic growth.By this time

next year, we will be talking about rate hikes, if theyhaven't

already occurred.

James Paulsen, Wells Capital Management: For me, it alreadyfeels

like Fed policy has dropped in importance among most

investors. Now that the Fed has decided to begin tapering,

otherissues seem to have become more important in shaping

theinvestment/economic climate this year including whether

moneyvelocity begins to rise, whether capital spending finally

emerges andwhether the emerging world economies do indeed

reaccelerate.

-

8/13/2019 CNBC Fed Survey results, January 28, 2014

26/26

FED SURVEYJanuary 28, 2014

Lynn Reaser, Point Loma Nazarene University: The Fed's

crystalball will need to be extra clear this month, as the FOMC

meeting

takes place just one week ahead of new jobs figures.

Policymakersare likely to decide to dismiss December's weak report

as ananomaly and press ahead with more tapering. This will be a big

bet.

John Roberts, Hilliard Lyons: Declining corporate

profitabilitycombined with some economic distortions could very

well lead to arecession late this year or early in 2015.

Indications of corporateprofit issues are already arising with a

higher level than normal ofearnings warnings and fewer companies

exceeding expectations than

typical. Profit margins will eventually regress to the norm.

Expect adown market for 2014, driven by a significant second-half

decline.

Allen Sinai, Decision Economics: The basic prospect for the

U.S.and world economy is bright but out of the blue crises are

possible;in particular EMG.

Hank Smith, Haverford Investments: The equity markets are duefor

a pullback/correction and it has nothing to do with Fed policy.

The pullback/correction should be short-lived as the

fundamentalsare good and there is a ton of cash looking for this

opportunity.

Diane Swonk, Mesirow Financial: The gap between what the Fedsays

and what financial markets are hearing appears to havenarrowed. It

is unclear they will stay on same page as forwardguidance becomes a

more important policy tool

Peter Tanous, Lynx Investment Advisory: The risk I worry

about

is a negative world reaction to the $4 trillion Fed balance

sheet andinvestors demanding higher interest rates on U.S. debt.

This couldcause a spike in rates that would lead to a cascade of

financialinstability around the world.