-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

1/27

CNBC Fed Survey July 31, 2012Page 1 of 27

FED SURVEYJuly 31, 2012

These survey results represent the opinions of 50of the nations

top money managers,investment strategists, and professional

economists.

They responded to CNBCs invitation to participate in our online

survey. Their responses werecollected on July 27-28, 2012, after

the U.S. Q2 GDP report was released. Participants were not

required to answer every question.

Results are also shown for identical questions in earlier

surveys.

This is not intended to be a scientific poll and its results

should not be extrapolated beyond those

who did accept our invitation.

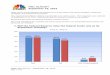

1.Will there be another Federal Reserve quantitative

easingprogram in the next year (12 months)?

19%

68%

13%

46%

37%

17%

34%

59%

7%

48%

46%

7%

48%

44%

8%

33%

63%

4%

33%

56%

12%

58%

32%

10%

78%

18%

4%

Yes

No

Don't know/unsure

July 20, 2011 August 11, 2011 September 19, 2011

October 31, 2011 January 23, 2012 March 16, 2012

April 24, 2012 June 4, 2012 July 31, 2012

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

2/27

CNBC Fed Survey July 31, 2012Page 2 of 27

FED SURVEYJuly 31, 2012

2.For those respondents who replied Yes to question #1:How large

do you expect the new quantitative program

will be over the next year (12 months)? Please do notinclude

reinvestment of maturing securities.

$377

$628

$527

$457

$567

$448 $456 $451

$532

$0

$100

$200

$300

$400

$500

$600

$700

Average (In Billions)

July 20, 2011 August 11, 2011 September 19, 2011

October 31, 2011 January 23, 2012 March 16, 2012

April 24, 2012 June 4, 2012 July 31, 2012

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

3/27

CNBC Fed Survey July 31, 2012Page 3 of 27

FED SURVEYJuly 31, 2012

3.For those respondents who replied Yes to question #1: Atwhich

meeting of the Federal Open Market Committee do you

think the Fed is most likely to announce a new QE program?

The Before June Meeting option has only been offered in the June

4 survey.

3%

33%

22%

28%

8%

6%

0%

0%

18%

45%

9%

9%

9%

9%

0%

0%

65%

18%

6%

6%

6%

0%

3%

42%

47%

8%

0%

0%

0%

26%

56%

3%

5%

10%

0% 10% 20% 30% 40% 50% 60% 70%

January 2012

March

April

Before June Meeting

June

July

September

October

December 2012

2013

January 23, 2012 March 16, 2012 April 24, 2012 June 4, 2012 July

31, 2012

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

4/27

CNBC Fed Survey July 31, 2012Page 4 of 27

FED SURVEYJuly 31, 2012

4.If the Fed does additional QE, how do you think it wouldbe

executed?

36%

46%

8%10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

As a lump sum In monthly sums

adjusted meeting

by meeting

In monthly sums

tied to specific

economic targets

Don't Know/Unsure

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

5/27

CNBC Fed Survey July 31, 2012Page 5 of 27

FED SURVEYJuly 31, 2012

5.If the Fed does additional QE, what form would it take?(Please

answer this question without regard to actions the

Fed is taking in Operation Twist.)

2%

74%

20%

4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Purchase onlyTreasuries

Purchase a mix ofTreasuries and

mortgage-backed

securities

Purchase onlymortgage-backed

securities

Don't Know/Unsure

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

6/27

CNBC Fed Survey July 31, 2012Page 6 of 27

FED SURVEYJuly 31, 2012

6.If the Federal Reserve announced a $500 billion QEprogram,

what effect would it have on the following rates,

in basis points?

12%

5%

7%

2%

2%

5%

23%

14%

23%

5%

0%

0%

2%

0%

5%

3%

0%

11%

3%

11%

16%

16%

16%

11%

8%

3%

0% 5% 10% 15% 20% 25%

Up 26 or more

Up 21-25

Up 16-20

Up 11-15

Up 6-10

Up 1-5

No effect

Down 1-5

Down 6-10

Down 11-15

Down 16-20

Down 21-25

Down 26 or more

10-Year Treasury 30-Year Mortgage

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

7/27

CNBC Fed Survey July 31, 2012Page 7 of 27

FED SURVEYJuly 31, 2012

7.If the Federal Reserve announced a $500 billion QEprogram,

what effect would it have on the S&P 500 stock

index?

11%

0%

2%

28%

23%

17%

9%

11%

0%

0%

0%

0%

0%

0%

0%

0% 5% 10% 15% 20% 25% 30%

Up more than 10%

Up 9-10%

Up 7-8%

Up 5-6%

Up 3-4%

Up 1-2%

Up less than 1%

No Effect

Down less than 1%

Down 1-2%

Down 3-4%

Down 5-6%

Down 7-8%

Down 9-10%

Down 10% or more

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

8/27

CNBC Fed Survey July 31, 2012Page 8 of 27

FED SURVEYJuly 31, 2012

8.Which, if any, of the following additional actions do youthink

the Fed will take to drive down long-term yields?

Respondents were able to select more than one response, so

percentages total more than 100%

Other responses:

Additional purchase program Open refinancing window wider Reduce

IOER by 10 bps

11%

24%

4%

51%

11%

31%

18%

7%

0% 10% 20% 30% 40% 50% 60%

Reduce the interest rate paid on excessreserves by half

Reduce the interest rate paid on excessreserves to zero

Offer a negative interest rate on excess

reserves

Forecast that rates will remainexceptionally low through

late-2015

Open a discount window program for smallbusiness loans (similar

to what the Bank

of England recently announced):

Forecast that it will keep rates

exceptionally low until specific economic

targets are met

None

Other

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

9/27

CNBC Fed Survey July 31, 2012Page 9 of 27

FED SURVEYJuly 31, 2012

10.How would you characterize the Fed's current

monetarypolicy?

Too

accommodativeJust right Too restrictive

Dont

know/Unsure

July 20, 2011 41% 52% 3% 5%

August 11, 2011 26% 52% 12% 10%

September 19, 2011 39% 40% 12% 9%

October 31, 2011 34% 48% 10% 8%

January 23, 2012 37% 45% 12% 5%

March 16, 2012 53% 38% 6% 4%

April 24, 2012 36% 51% 8% 6%

June 4, 2012 33% 52% 10% 5%

July 31, 2012 28% 43% 17% 13%

0%

10%

20%

30%

40%

50%

60%

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

10/27

CNBC Fed Survey July 31, 2012Page 10 of 27

FED SURVEYJuly 31, 2012

11.Where do you expect the S&P 500 stock index will be on

?

This is the first survey in which we asked for a June 30, 2013

forecast.

1387

1436

14001396

1451

December 31, 2012 June 30, 2013

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

11/27

CNBC Fed Survey July 31, 2012Page 11 of 27

FED SURVEYJuly 31, 2012

12.What do you expect the yield on the 10-year Treasurynote will

be on ?

This is the third survey in which we asked for a December 31,

2012 forecast.

2.52%2.59%

2.40%

1.69%

1.98%

December 31, 2012 June 30, 2013

January 23, 2012 March 16, 2012 April 24, 2012 July 31, 2013

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

12/27

CNBC Fed Survey July 31, 2012Page 12 of 27

FED SURVEYJuly 31, 2012

13.What is your forecast for the year-over-year percentagechange

in real U.S. GDP?

+2.85%

+2.47%

+2.24%+2.37%

+2.45%

+2.59%

+2.46%

+2.74%

+2.39%

+2.55%

+1.93%

+2.26%

2012

2013

July 20, 2011 August 11, 2011 September 19, 2011

October 31, 2011 January 23, 2012 March 16, 2012

April 24, 2012 July 31, 2012

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

13/27

CNBC Fed Survey July 31, 2012Page 13 of 27

FED SURVEYJuly 31, 2012

14.When do you think the FOMC will first increase the fedfunds

rate?

Note: In the July 31 survey, the choice of 2015 or later was

replacedwith choices for each quarter and 2016 or later was

added.

2012

- Q1Q2 Q3 Q4

2013

- Q1Q2 Q3 Q4

2014

- Q1Q2 Q3 Q4

2015

or

later

2015

- Q1

2015

- Q2

2015

- Q3

2015

- Q4

2016

or

later

April 24, 2012 0% 0% 4% 4% 9% 11% 9% 13% 9% 15% 8% 13%

July 31, 2012 0% 0% 2% 2% 13% 4% 4% 9% 4% 11% 13% 15% 7% 2%

11%

0%

2%

4%

6%

8%

10%

12%

14%

16%

April 24, 2012 July 31, 2012

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

14/27

CNBC Fed Survey July 31, 2012Page 14 of 27

FED SURVEYJuly 31, 2012

15.When do you think the FOMC will make its first planned

decrease in the size of its balance sheet?

Note: In the July 31 survey, the choice of 2015 or later was

replacedwith choices for each quarter and 2016 or later was

added.

2012

- Q1Q2 Q3 Q4

2013

- Q1Q2 Q3 Q4

2014

- Q1Q2 Q3 Q4

2015

or

later

2015

- Q1

2015

- Q2

2015

- Q3

2015

- Q4

2016

or

later

April 24, 2012 0% 0% 4% 4% 9% 11% 9% 13% 9% 15% 8% 13%

July 31, 2012 0% 0% 2% 4% 11% 9% 16% 4% 2% 16% 4% 7% 2% 4%

16%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

April 24, 2012 July 31, 2012

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

15/27

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

16/27

CNBC Fed Survey July 31, 2012Page 16 of 27

FED SURVEYJuly 31, 2012

17.In the next 12 months, what percent probability do you

place on the U.S. entering recession? (0%=No chance ofrecession,

100%=Certainty of recession)

34.0%36.1%

25.5%

20.3%19.1%

20.6%

25.9%

August 11, 2011 September 19, 2011 October 31, 2011

January 23, 2012 March 16, 2012 April 24, 2012

July 31, 2012

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

17/27

CNBC Fed Survey July 31, 2012Page 17 of 27

FED SURVEYJuly 31, 2012

18.What is the single biggest threat facing the U.S.

economic recovery?

This is the first survey in which deflation and fiscal cliff

have been offered as choices.

Other response:

Emerging world recession

17%

36%

4%

26%

4%

2%

11%

37%

27%

8%

8%

4%

0%

17%

30%

16%

7%

0%

0%

5%

41%

0%

2%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

European recession/financial crisis

Tax/regulatory policies

Slow job growth

High gasoline prices

Overall inflation

Deflation

"Fiscal Cliff"

Don't know/unsure

Other:

March 16, 2012 April 24, 2012 July 31, 2012

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

18/27

CNBC Fed Survey July 31, 2012Page 18 of 27

FED SURVEYJuly 31, 2012

19.When it comes to the "Fiscal Cliff," do you believe that:

78%

18%

4%0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

It is already havinga negative effect on

business and theeconomy

It will have aneffect later this year

It will have noeffect

Don't know/unsure

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

19/27

CNBC Fed Survey July 31, 2012Page 19 of 27

FED SURVEYJuly 31, 2012

20.Which, if any, of the following actions do you believe

theEuropean Central Bank will take in the next six months?

(You may check more than one box.)

Respondents were able to select more than one response, so

percentages total more than 100%

Other responses:

Begin to fund ESM More explicitly guarantee debt of crisis

countries

66%

14%

43%

89%

0%

5%

2%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Undertake another long-term repo

operation

Offer a negative interest rate on deposits

Cut its main refinancing rate

Purchase additional sovereign debt

Take no additional action

Other

Don't know/unsure

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

20/27

CNBC Fed Survey July 31, 2012Page 20 of 27

FED SURVEYJuly 31, 2012

22.What is your outlook for the European Monetary Unionfive

years from now?

42%

53%

0%

5%

47%

52%

2%

0%

24%

63%

6%

8%

29%

69%

0%

2%

11%

82%

5%

2%

0% 20% 40% 60% 80% 100%

No countries will be ejected or leave

Some countries will be ejected or leave

It will be largely dissolved and mostEuropean countries will

have their own

currency

Don't know/unsure

July 21, 2011 October 31, 2011 January 23, 2012 March 16, 2012

July 31, 2012

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

21/27

CNBC Fed Survey July 31, 2012Page 21 of 27

FED SURVEYJuly 31, 2012

23.What is the probability, in your opinion, that each of

thefollowing countries will default on its debt in the next

three years? (0%=No chance of default, 100%=Certaintyof

default)

Germany, France, and United Kingdom were not included in the

July 20, 2011 survey.For Greece, respondents to the March 16 and

July 31, 2012 surveys were asked for the

probability of a second default beyond the March

creditevent.

Portugal Ireland Italy Greece Spain Germany FranceUnited

States

United

Kingdom

July 20, 2011 52% 48% 24% 83% 28% 4%

August 11, 2011 45% 37% 23% 70% 25% 2% 3% 2% 2%

September 19, 2011 41% 34% 23% 82% 24% 2% 4% 1% 2%

October 31, 2011 47% 33% 28% 84% 26% 2% 4% 2% 3%

January 23, 2012 49% 33% 28% 88% 30% 2% 6% 1% 2%

March 16, 2012 53% 31% 25% 72% 29% 2% 5% 3% 3%

July 31, 2012 39% 23% 25% 79% 38% 1% 5% 2% 2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

22/27

CNBC Fed Survey July 31, 2012Page 22 of 27

FED SURVEYJuly 31, 2012

What is your primary area of interest?

Comments:

John Augustine, Fifth Third Asset Management: Wwe need

three things: 1) sane US fiscal policy, 2) Fed using its balance

sheetto help get as many US mortgages down near 3% as possible;

3)ECB buys sovereign debt in near-term; funds ESM next year.

Richard Bernstein, Richard Bernstein Advisors: The Feddoesn't

have to do further QE because the problems in Europe andthe

emerging markets are doing it for them. After all, the 10-year

isbelow 1.5% courtesy of Greece and Spain.

Mike Dueker, Russell Investments: The Fed needs to meet

itsimplicit nominal GDP growth target of 4.5 percent. July's GDP

reportrevised the numbers back to 2009 Q1. They show that at no

time inthis recovery has nominal GDP growth reached 4.5 percent on

afour-quarter rolling basis. Thus, the basic rationale for a third

roundof Quantitative Easing is that it appears inescapable to

conclude that

Economics

50%

Equities20%

Fixed

Income11%

Currencies

4%

Other15%

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

23/27

CNBC Fed Survey July 31, 2012Page 23 of 27

FED SURVEYJuly 31, 2012

the Fed needs to do more to do its part and end this period of

sub-par nominal GDP growth.

Kevin Ferry, Cronus Futures Management: The sun will comeup

tomorrow.

Dennis Gartman, The Gartman Letter: The biggest test facingthe

U.S. economy is that we shall do something truly stupid: raisetaxes

and cut spending aggressively, doing immeasurable damage tothe

economy in the process. We should be flattening and cuttingtaxes...

aggressively, while cutting spending marginally. But we

won't; we'll do something truly stupid, along the lines of

AndrewMellon in the middle 1930s, who cut spending/raised taxes and

gaveus the Depression.

Lee Hoskins, Pacific Research Institute: The Ffed has doneQE1,

QE2, Twist 1, and Twist 2. Each time it expects to

stimulateeconomic growth and each time its actions have failed to

do so.Doing QE3 and expecting a different outcome borders on

theirrational.

Hugh Johnson, Hugh Johnson Advisors: The level of concernabout

the impact of the contraction in Europe or higher U.S.

taxesscheduled to begin on January 1st is so high and the level of

stockmarket optimism is so low that the outlook (near term) has

shiftedtoward positive for U.S. equities. Do equity prices "climb a

wall ofworry?" We are about to find out. It is unlikely that the

contraction inthe European economy or the "fiscal cliff" (which

should beeffectively postponed) is likely to directly cause the end

of the

current stock market-economic-interest rate cycle. That may be

"themessage" of the financial markets collectively since June

1.

John Kattar, Eastern Investment Advisors: Although I thinkmore

QE is coming, it will not be this year. The economy is not

weakenough, the stock market is doing well, and interest rates are

low

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

24/27

CNBC Fed Survey July 31, 2012Page 24 of 27

FED SURVEYJuly 31, 2012

enough. The Fed is on hold until 2013, or at least should be.

Also ofnote is the fact that excess reserves have decreased by $100

billion

y/y. The Fed has chosen to replace this with other liabilities

so asnot to shrink its balance sheet.

Barry Knapp, Barclays PLC: Financial conditions have

nottightened sufficiently such that stimulus via the portfolio

balancechannel can loosen conditions. In other words, the policy

will haveno macroeconomic impact, it will spark a rally in fixed

incomespreads but pass through to grow will be close to zero. It

will makeexiting the stimulus more difficult and as a result the

costs of any

additional stimulus outweigh the benefits.

Alan Kral, Trevor Stewart Burton & Jacobsen: The Fed will

doall it can to cause noticeable market and/or economic

changebetween now and the election.

Guy LeBas, Janney Montgomery Scott: We've entered into

theultimate "muddling along" period when it comes to the

markets.

Given the fiscal constraints, there's simply no reliable way to

juicedomestic economic activity, save for waiting for conditions to

slowlyimprove. That means we're talking about low growth through

2015,perhaps longer.

John Lonski, Moody's: The outcome of the November electionsmay

give considerable shape to the resolution of the "fiscal

cliff."

Larry McMillan, McMillan Analysis: Once you go Keynesian,

you

never go back.

Rob Morgan, Fulcrum Securities: On Thursday ECB head MarioDraghi

said the ECB is 'ready to do whatever it takes to preserve

theEuro.' It is time to translate that statement into action.

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

25/27

CNBC Fed Survey July 31, 2012Page 25 of 27

FED SURVEYJuly 31, 2012

Joel Naroff, Naroff Economic Advisors: With theTheater of

theTotally Absurdcontinuing to play in Washington, the slow

recovery

will continue. No matter who is elected, it will continue

anyway.

Michael Painchaud, Market Profile Theorems: 2013 - 2014could

well be the worst economic environment for the U.S. andglobally

since 2008-2009.

James Paulsen, Wells Capital Management: The U.S. FederalReserve

has become increasingly irrelevant surrounding any furthereasing

efforts but has also become increasingly important as to how

and when they will tighten monetary conditions. The

financialmarkets will likely respond less and less to Fed

discussionssurrounding additional easing efforts but may become

increasinglysensitive to any discussions/i.e., Fedspeak as to

monetarytightening.

Lynn Reaser, Point Loma Nazarene University: The Fed nowfaces

the possibility of trying to offset policy errors not only in

theEurozone but also mistakes in its own backyard on Capitol

Hill.

David Resler, Nomura: The question of biggest threat is a

closecall between the crisis in Europe (already underway) and the

"fiscalcliff." While I judge it (only marginally) more likely than

not thatsome sort of stop-gap measure is adopted, the odds that we

reachthe "cliff" with no action taken is rising.

John Roberts, Hilliard Lyons: We currently perceive downsiderisk

to both the economy and equity markets and are very worried

that investors are in particular ignoring valuations and risk,

and to alesser degree fundamentals, when purchasing many

income-orientedsecurities in the same way they ignored business

fundamentalsduring the tech bubble.

Hank Smith, Haverford Investments: Comprehensive tax reform

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

26/27

CNBC Fed Survey July 31, 2012Page 26 of 27

FED SURVEYJuly 31, 2012

that lowers rates and eliminates many deductions along

withreducing regulations is the key spurring U.S. GDP growth and is

the

key to allowing the Fed to start taking its foot off the

pedal.

Diane Swonk, Mesirow Financial: Timing additional easing

iscomplicated by the need to leverage what the Fed has left to

itsfullest. It doesnt want to pull the trigger until it can get its

bestshots in. Feels a little like the Alamo at the moment, although

theFed has a few more gunners.

Peter Tanous, Lynx Investment Advisory: The Draghi rally

this

week (week ending July 27) should be followed by the Bernanke

rallynext week. Gold will rise as the world realizes that what is

happeningis ultimately inflationary. Here's the simple reality:

There is moredebt in the world than can ever be repaid. There are

only two waysto solve this problem: devaluation or inflation. For

most countries,especially ours, the answer will be inflation. It is

simply the onlyway out.

Robert Tipp, Prudential Fixed Income: European policy makers

have arrived at their next key decision point. Undoubtedly

themarket stress to date has damaged economic prospects in

Europe.To prevent more serious international spill-over, though, it

is criticalthat European policy makers take steps to bring down

peripheralyields over the near term. Overall, the highly uncertain

environmentcontinues to stimulate flows into the fixed income

market, and isultimately very positive for the fixed income

markets. We believethe best absolute return opportunities are in

high yield and emergingmarkets. Additionally, prospects for

outperformance relative to

Treasuries remain favorable for structured products and

investmentgrade corporates, especially financials. Lastly, the

large swings inmarket sentiment are creating excellent tactical

opportunities in boththe U.S. Treasury market, as well as in

foreign currencies.

Scott Wren, Wells Fargo Advisors: We are going to be in a

-

7/31/2019 CNBC Fed Survey Results: July 31, 2012

27/27