-

CNBC Fed Survey June 16, 2015 Page 1 of 31

FED SURVEY June 16, 2015

These survey results represent the opinions of 39 of the nations

top money managers, investment strategists, and professional

economists. They responded to CNBCs invitation to participate in

our online survey. Their responses were collected on June 11-12,

2015. Participants were not required to answer every question.

Results are also shown for identical questions in earlier

surveys.

This is not intended to be a scientific poll and its results

should not be extrapolated beyond those who did accept our

invitation.

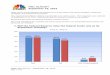

1. Will the Federal Reserve raise the federal funds rate in

2015?

84%

11%

5%

92%

5% 3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Yes No Don't know/unsure

Apr 28 Jun 16

-

CNBC Fed Survey June 16, 2015 Page 2 of 31

FED SURVEY June 16, 2015

2. Relative to an economy operating at full capacity, what best

describes your view of the amount of resource slack in the U.S.

right now for labor?

July 29August

20Sep 16 Oct 28 Dec 16 Jan 27 Mar 17 Apr 28 Jun 16

Considerably more slack now 48% 34% 20% 18% 16% 16% 13% 6%

5%

Modestly more slack now 36% 40% 60% 69% 55% 50% 63% 64% 54%

No difference 4% 6% 3% 0% 0% 6% 11% 0% 15%

Modestly less slack now 8% 11% 6% 5% 24% 19% 11% 22% 15%

Considerably less slack now 4% 9% 9% 8% 5% 9% 3% 8% 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Modestly less slack

Modestly more slack

Considerably less slack

No difference

Considerably more slack

-

CNBC Fed Survey June 16, 2015 Page 3 of 31

FED SURVEY June 16, 2015

Relative to an economy operating at full capacity, what best

describes your view of the amount of resource slack in the U.S.

right now for production capacity?

July 29August

20Sep 16 Oct 28 Dec 16 Jan 27 Mar 17 Apr 28 Jun 16

Considerably more slack now 12% 9% 8% 8% 8% 0% 14% 8% 10%

Modestly more slack now 56% 60% 64% 64% 55% 59% 57% 57% 62%

No difference 8% 14% 8% 15% 13% 19% 14% 5% 8%

Modestly less slack now 16% 9% 14% 8% 24% 13% 11% 19% 13%

Considerably less slack now 4% 9% 3% 5% 0% 9% 5% 11% 8%

0%

10%

20%

30%

40%

50%

60%

70%

No difference

Modestly more slack

Modestly less slack

Considerably less slack

Considerably more slack

-

CNBC Fed Survey June 16, 2015 Page 4 of 31

FED SURVEY June 16, 2015

3. What is your measure of full employment in the U.S.?

0%

5%

10%

15%

20%

25%

30%

35%

Unemployment rate

Apr 28 Jun 16

Averages:

Apr 28: 4.8%

Jun 16: 4.8%

-

CNBC Fed Survey June 16, 2015 Page 5 of 31

FED SURVEY June 16, 2015

4. At what level of year-over-year wage growth would you become

concerned that inflationary pressures are building?

15% chose Theres little connection between wages and overall

price inflation.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0% 1% 2% 3% 4% 5% 6% 7%

Wage growth

Average:

3.6%

-

CNBC Fed Survey June 16, 2015 Page 6 of 31

FED SURVEY June 16, 2015

5. At the current level of wage growth, are you ...?

10%

5%

62%

21%

3%

0%

10%

20%

30%

40%

50%

60%

70%

Concernedabout inflation

Concernedabout deflation

Believe therisks areneutral

Theres little connection

between wages and overall

price inflation

Don'tknow/unsure

-

CNBC Fed Survey June 16, 2015 Page 7 of 31

FED SURVEY June 16, 2015

6. How do you view the recent productivity slowdown?

23%

31%

36%

10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

A temporarydevelopment

without much long-term consequence

A more permanentdevelopment that

creates concern forlong-term growth

The statistics do notcorrectly capturingreal productivity

growth in theeconomy

Don't know/unsure

-

CNBC Fed Survey June 16, 2015 Page 8 of 31

FED SURVEY June 16, 2015

7. How do you think the productivity slowdown will affect Fed

policy?

17%

14%

69%

29%

38%

33%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Hike sooner Hike later No effect ontiming

Hike faster Hike slower No effect onspeed

Timing Speed

-

CNBC Fed Survey June 16, 2015 Page 9 of 31

FED SURVEY June 16, 2015

8. What is most responsible for the slowdown in

productivity?

Government tax and regulatory policy

Lack of capital deepening Lack of capital deepening Lower

productive returns to technology Mis-measurement of the data on

GDP

More services jobs in the economy Reluctance to spend on

PP&E that would increase productivity Temporary issues that

should have limited impact on longer term

growth

Unclear Underinvestment by businesses Bad statistical

analysis

Demographics and technology Incorrect output measuring Lack of

strong capital spending Low wages and fewer skilled workers

available

Lower rates may have overstated prior productivity; more picky

labor force e.g. on life quality

Near full level of productivity and lack of skilled workers

Output growth

Slack aggregate demand + rising inventory/sales ratio Temporary

factors Weak demand and weak labor markets cause companies to be

less

concerned about economizing on labor. Therefore we get weak

productivity growth. The current wave of technological

innovation appears to be benefiting

consumers more than businesses We are likely over stating

inflation due the vast improvements in the

quality of long-standing goods and service as well as new goods

and services that improve utility and satisfaction.

Lower long-term fixed capital investment by corporations, which

is in

-

CNBC Fed Survey June 16, 2015 Page 10 of 31

FED SURVEY June 16, 2015

turn cause by economic and policy uncertainty Demographics, old

people on fixed incomes buy less, and there are

more of them; Fed, state & local government spending is

less

In rank order, measurement error, soft business investment

particularly in info processing equipment, slowing in pace of

innovation.

Output continues to be constrained by excesses (primarily

debt

levels) built during 2000-2006 both domestically and

internationally. Some of it is the legacy of weak investment during

the recovery;

dominant factor is measurement problems regarding impact of

sharing economy and tech change

Weak capital spending plus turnover in labor as boomers retire

and replaced by double the number of rookies

The methodology of the payroll survey was changed in 2012 and

it

now overstates payroll growth (aggregate labor)

-

CNBC Fed Survey June 16, 2015 Page 11 of 31

FED SURVEY June 16, 2015

9. Should the New York Federal Reserve president be approved by

the Senate?

10. Should the FOMC, not the Board of Governors, control the

rate of interest on excess reserves?

11. Should the Fed release FOMC transcripts three years after

the meeting instead of five?

27%

68%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Yes

No

50%

18%

29%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Yes

No

Doesn't matter

71%

18%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Yes

No

-

CNBC Fed Survey June 16, 2015 Page 12 of 31

FED SURVEY June 16, 2015

12. Where do you expect the S&P 500 stock index will be on

?

2075

2149

2111

2194 2187

2128

2156 2159

2311 2296

2247 2259

2293

1,800

1,900

2,000

2,100

2,200

2,300

2,400

Jul 29 Sep 16 Oct 28 Dec 16 Jan 27'15

Mar 17 Apr 282 Jun 16

Survey Dates

December 31, 2015 December 31, 2016

-

CNBC Fed Survey June 16, 2015 Page 13 of 31

FED SURVEY June 16, 2015

13. What do you expect the yield on the 10-year Treasury note

will be on ?

3.43% 3.45%

3.19%

2.96%

2.54%

2.57%

2.33%

2.64%

3.52%

3.04%

3.14%

2.89%

3.24%

2.0%

2.5%

3.0%

3.5%

4.0%

Jul 29 Sep 16 Oct 28 Dec 16 Jan 27'15

Mar 17 April 28 Jul 16

Survey Dates

December 31, 2015 December 31, 2016

-

CNBC Fed Survey June 16, 2015 Page 14 of 31

FED SURVEY June 16, 2015

14. What is your forecast for the year-over-year percentage

change in real U.S. GDP for ?

Jan 28,

'14Mar 18 Apr 28 Jun 4 Jul 29 Sep 16 Oct 28 Dec 16

Jan 27,

'15Mar 17

April

28Jun 16

2015 +2.90% +3.02% +3.00% +2.81% +2.75% +2.90% +2.90% +3.02%

+2.99% +2.69% +2.70% +2.25%

2016 +2.88% +2.80% +2.84% +2.81% +2.78%

+2.90%

+3.02% +3.00%

+2.81%

+2.75%

+2.90% +2.90%

+3.02% +2.99%

+2.69% +2.70%

+2.25%

+2.88%

+2.80%

+2.84% +2.81%

+2.78%

2.0%

2.2%

2.4%

2.6%

2.8%

3.0%

3.2%

3.4%

2015 2016

-

CNBC Fed Survey June 16, 2015 Page 15 of 31

FED SURVEY June 16, 2015

15. What is your forecast for the year-over-year percentage

change in the headline U.S. CPI for ?

2.02%

2.29% 2.27%

2.01%

1.74%

1.17%

1.01% 1.00%

1.17%

2.17%

2.07% 2.08%

1.96%

2.29%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2.2%

2.4%

Jun 4 Jul 29 Sep 16 Oct 28 Dec 16 Jan 27,'15

Mar 17 April 28 Jun 16

Survey Dates

2015 2016

-

CNBC Fed Survey June 16, 2015 Page 16 of 31

FED SURVEY June 16, 2015

16. When do you expect the Fed to hike the fed funds rate

and allow its balance sheet to decline?

Survey Date Fed Funds Hike

Average Forecast

Balance Sheet

Average Forecast

April 28, 2014 survey July 2015 October 2015

June 4 survey August 2015 March 2016

July 29 survey August 2015 December 2015

August 20 survey July 2015 Not asked

September 16 survey June 2015 December 2015

October 28 survey July 2015 January 2016

December 16 survey July 2015 February 2016

Jan. 27, 2015 survey September 2015 April 2016

March 17 survey August 2015 April 2016

April 28 survey October 2015 May 2016

June 16 survey October 2015 July 2016

-

CNBC Fed Survey June 16, 2015 Page 17 of 31

FED SURVEY June 16, 2015

17. How would you characterize the Fed's current monetary

policy?

28%

49%

46%

49%

44%

39%

50%

54%

50%

60%

43%

43%

49%

43%

49% 50%

47%

32%

44%

35%

17%

6%

3% 3% 3%

6% 5%

3%

13%

3%

3%

6% 5% 6%

3%

8%

6%

3%

0%

10%

20%

30%

40%

50%

60%

70%

Jul 31,'12

Jul 29,'14

Aug 20 Sep 16 Oct 28 Dec 16 Jan 27,'15

Mar 17 Apr 28 Jun 16

Too accommodative Just right Too restrictive Don't

know/unsure

Too accomodative

Don't know/unsure

Too restrictive

Just right

-

CNBC Fed Survey June 16, 2015 Page 18 of 31

FED SURVEY June 16, 2015

18. Where do you expect the fed funds target rate will be on

?

Jul

30

Sep

17

Oct

29

Dec

17

Jan

28

'14

Mar

18

Apr

28Jun 4

Jul

29

Aug

20

Sep

16

Oct

28

Dec

16

Jan

27,

'15

Mar

17

April

28

Jun

16

Dec 31, 2015

0.97%0.92%0.82%0.70%0.72%0.83%0.99%0.68%1.05%0.89%0.98%0.89%0.83%0.73%0.71%0.54%0.53%

Dec 31, 2016 1.99%2.13%2.04%1.93%1.75%1.84%1.46%1.56%

0.97% 0.92%

0.82%

0.70% 0.72%

0.83%

0.99%

0.68%

1.05%

0.89%

0.98%

0.89%

0.83%

0.73% 0.71%

0.54% 0.53%

1.99%

2.13%

2.04%

1.93%

1.75%

1.84%

1.46%

1.56%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Dec 2016

Dec 2015

-

CNBC Fed Survey June 16, 2015 Page 19 of 31

FED SURVEY June 16, 2015

19. At what fed funds level will the Federal Reserve stop hiking

rates in the current cycle? That is, what will be the terminal

rate?

3.16% 3.20%

3.30%

3.17% 3.11%

3.04%

2.85%

3.06%

2.0%

2.5%

3.0%

3.5%

4.0%

Aug 20 Sep 16 Oct 28 Dec 16 Jan 27,

'15

Mar 17 Apr 28 Jun 16

Survey Dates

-

CNBC Fed Survey June 16, 2015 Page 20 of 31

FED SURVEY June 16, 2015

20. When do you believe fed funds will reach its terminal

rate?

Survey Date Forecast

August 20 survey Q4 2017

September 16 survey Q3 2017

October 28 survey Q4 2017

December 16 survey Q1 2018

Jan. 27, 2015 survey Q1 2018

March 17 survey Q4 2017

April 28 survey Q1 2018

June 16 survey Q1 2018

-

CNBC Fed Survey June 16, 2015 Page 21 of 31

FED SURVEY June 16, 2015

21. What is the percentage chance each of the following

countries will leave the euro zone in the next 3 years? (0%=No

chance of leaving, 100%=Certainty of leaving):

41%

13%

12%

9%

8%

3%

39%

11%

8%

7%

5%

3%

5%

50%

12%

10%

8%

5%

2%

3%

0% 10% 20% 30% 40% 50% 60%

Greece

Portugal

Spain

Italy

Ireland

Germany

France

Mar 17 Apr 28 Jun 16

-

CNBC Fed Survey June 16, 2015 Page 22 of 31

FED SURVEY June 16, 2015

22. Has the U.S. stock market already discounted a fed funds

rate hike by the Federal Reserve this year?

56%

36%

8%

53%

38%

9%

53%

47%

0%

47%

50%

3%

61%

39%

0%

0% 10% 20% 30% 40% 50% 60% 70%

Yes

No

Don't know/unsure

Dec 16 Jan 27 Mar 17 Apr 28 Jun 16

-

CNBC Fed Survey June 16, 2015 Page 23 of 31

FED SURVEY June 16, 2015

Has the U.S. bond market already discounted a fed funds rate

hike by the Federal Reserve this year?

42%

56%

3%

67%

33%

0%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Yes

No

Don't know/unsure

Apr 28 Jun 16

-

CNBC Fed Survey June 16, 2015 Page 24 of 31

FED SURVEY June 16, 2015

23. What is the single biggest threat facing the U.S. economic

recovery?

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

European recession/financial crisis

Tax/regulatory policies

Slow job growth

Inflation

Deflation

Debt ceiling

Rise in interest rates

Geopolitical risks

Global economic weakness

Slow wage growth

Other

Don't know/unsure

Europeanrecession/financial

crisis

Tax/regulatory

policies

Slow jobgrowth

InflationDeflationDebt

ceiling

Rise ininterest

rates

Geopolitical risks

Globaleconomicweakness

Slow wagegrowth

OtherDon't

know/unsure

Apr 30 20%31%20%0%2%2%11%0%

Jun 18 15%28%20%3%3%0%13%0%

Jul 30 8%30%22%0%2%2%10%14%4%

Sep 17 4%27%22%2%0%4%18%7%2%

Oct 29 8%29%24%3%3%3%8%13%0%

Dec 17 5%32%29%2%0%2%15%2%2%

Jan 28 '14 7%21%30%2%0%0%12%21%0%

Mar 18 10%23%26%3%5%0%5%18%0%

Apr 28 3%26%21%3%5%0%8%18%13%0%

Jul 29 12%29%12%6%3%0%12%12%12%3%

Sep 16 6%26%29%6%3%0%6%11%11%3%

Oct 28 31%18%15%3%3%0%10%8%8%3%

Dec 16 40%14%14%3%6%0%3%14%3%0%

Jan 27 '15 0%13%9%0%0%0%6%16%41%6%16%0%

Mar 17 6%14%0%3%6%0%6%8%28%17%14%0%

April 28 3%11%8%3%0%0%6%11%28%8%19%3%

Jun 16 3%17%3%0%0%0%14%25%22%6%11%0%

Apr 30 Jun 18 Jul 30 Sep 17 Oct 29 Dec 17 Jan 28 '14 Mar 18 Apr

28

Jul 29 Sep 16 Oct 28 Dec 16 Jan 27 '15 Mar 17 April 28 Jun

16

-

CNBC Fed Survey June 16, 2015 Page 25 of 31

FED SURVEY June 16, 2015

FED SURVEY April 30,

24. In the next 12 months, what percent probability do you place

on the U.S. entering recession? (0%=No

chance of recession, 100%=Certainty of recession)

Aug11,

'11

Sep19

Oct31

Jan23,

'12

Mar16

Apr24

Jul31

Sep12

Dec11

Jan29,

'13

Mar19

Apr30

Jun18

Jul30

Sep6

Oct29

Dec17

Jan28

'14

Mar18

Apr28

Jul29

Sep16

Oct28

Dec16

Jan27

'15

Mar17

April28

Jun16

Series1 34.0 36.1 25.5 20.3 19.1 20.6 25.9 26.0 28.5 20.4 17.6

18.2 15.2 16.2 16.9 18.4 17.3 15.3 16.9 14.6 16.2 15.0 15.1 13.6

13.0 16.4 14.7 15.1

34.0%

36.1%

25.5%

20.3%

19.1%

20.6%

25.9%

26.0%

28.5%

20.4%

17.6%

18.2%

15.2%

16.2% 16.9%

18.4%

17.3%

15.3%

16.9%

14.6%

16.2%

15.0%

15.1%

13.6% 13.0%

16.4%

14.7%

15.1%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Survey Dates

-

CNBC Fed Survey June 16, 2015 Page 26 of 31

FED SURVEY June 16, 2015

FED SURVEY April 30,

25. What is your primary area of interest?

Comments: Marshall Acuff, Silvercrest Asset Management: The bond

market is leading the Federal Reserve. A hike in short-term rates

is

already priced into markets. Language from the Fed about future

rate hikes, especially their pace of increase, will become more

important to markets than their most immediate action to increase

the Fed Funds rate.

Dean Baker, Center for Economic and Policy Research: The trade

deficit is the major drag on growth at present. It is remarkable

more people are not talking about the need for a lower-valued

dollar.

Jim Bianco, Bianco Research: The Fed will not hike rates

unless/until it is priced in. They do not want a repeat of 1994

(hike when not priced in, the bond market collapsed). Since the

(fed fund

futures) market is pricing in a December hike, not September as

generally forecasted, this matters.

Economics

47%

Equities 19%

Fixed Income 17%

Currencies 0%

Other 17%

-

CNBC Fed Survey June 16, 2015 Page 27 of 31

FED SURVEY June 16, 2015

FED SURVEY April 30,

Thomas Costerg, Standard Chartered Bank: We think the 16-17 June

FOMC meeting will be all about preparing the ground for a

post-summer rate hike. This should support our scenario that the

first rate hike will be in September. A July rate hike remains

unlikely,

however, as the Fed probably wants to see more evidence of a Q2

GDP rebound, and more wage data. The Fed may also gauge market

reaction over the summer. We think current low core PCE inflation

may be dismissed given the likely belief that inflation will

grind

higher in coming months. We think some underlying concerns about

financial stability are emerging; Yellen might claim these remain

secondary in the Feds thought process about the hike; still they do

matter, in our view.

John Donaldson, Haverford Trust Co.: There has been much

commentary that the Fed will be embarking down a path with no prior

experience (raising rates from zero). We believe this is a good

reason to get started early; sooner and gradual moves will leave

time and policy room to adjust to unexpected consequences. The

absolute last thing the FOMC wants is to feel like they are behind

the curve and need to move quickly and in bigger increments.

Neil Dutta, Renaissance Macro Research: The Fed's reasonable

confidence threshold is being achieved. Labor market slack has

dried

up enough to pressure wages. Inflation expectations have

stabilized in the market and remain stable among households. The

dollar has declined and oil prices have advanced.

Mark Elenowitz, TriPoint Global Equities: It is no secret that

the Fed will raise rates in the near future. We believe that the

markets will be resilient and continue to grow, despite being 6

years into a bull market cycle. While many people continue to draw

comparisons

between todays market and the markets leading up to the tech

crash and 2008 recession, we trust that the underlying fundamentals

of today are stronger.

-

CNBC Fed Survey June 16, 2015 Page 28 of 31

FED SURVEY June 16, 2015

FED SURVEY April 30,

Kevin Giddis, Raymond James/Morgan Keegan: The bond market

appears to be challenging the Fed to "prove it" with their desire

to raise rates. Almost all of the shifts in the yield curve have

happened on the long end of the curve, which is more about

Europe

than it is about a rate hike and the Fed. During all of this,

the short end of the curve has barely budged. This bears the

question: who is running this thing?

Stuart Hoffman, PNC Financial Services Group: What weak consumer

spending?? Real PCE up just over 2% in 1Q and close to 3% in 2Q.

Savings rate headed back to near 5%. GDP revisions on July 30 will

cause a significant upward revision to market consensus

forecast for real GDP growth in 2015. This will be the final

piece of data to give the FOMC needed "confidence" to raise funds

rate by 25 bps at its Sept. meeting.

Art Hogan, Wunderlich Securities: More than 35% of active market

participants have never seen an increase in the fed funds rate.

That is why there is so much trepidation. It will be much less of

an issue once we start the normalization process. It's the

anticipation that causes so much dislocation. Constance Hunter,

KPMG LLP: Despite an abundance of guidance

to the market that the Fed will leave ZIRP and get to a more

normal accommodative policy stance, the bond market has been slow

to believe the economy can take it. As always the impact of central

bank action depends on if said bank is acting from a position

of

strength or weakness. By acting in September, the Fed will be

acting from a position of strength. Hugh Johnson, Hugh Johnson

Advisors: I anticipate (guess) the

Fed will begin to raise rates in September but it remains far

from certain and data dependent. The justification for raising

rates before inflation rates reach/approach target is, as

Chairperson Yellen says, Fed policy needs to be "forward looking."

Hence, the Fed has given

-

CNBC Fed Survey June 16, 2015 Page 29 of 31

FED SURVEY June 16, 2015

FED SURVEY April 30,

itself considerable flexibility in the timing of a move toward

restraint. That is as it should be. John Kattar, Ardent Asset

Advisors: The Yellen Fed has been

consistent and clear in signaling its intentions. I expect the

strongest indication yet that a rate hike is likely late this year,

as early as September.

Subodh Kumar, Subodh Kumar & Associates: Changing the

signpost does not change the distance to be travelled, in real nor

financial endeavors. Geopolitics simmer. Greece trials and

tribulations reflect worldwide tendencies for politicians to

procrastinate and to use easily availed money not to restructure

but instead to ingrain munificence. In quantitative ease reliance,

central banks may have underestimated such procrastination. On

potential volatility in markets, complacency about present

minuscule rates

could be a mirror image of complacency back in 1981, when high

fixed income yield risk premiums and low equity P/E ratios showed

similar conviction, misplaced then about high inflation being

stubborn. Institutional memory of such may be lost. Currency

volatility as harbinger, liquidity in fixed income credit

following the money management adage of sell what you can and

resistance to valuation expansion in equities indicate change. We

favor tangible

quality of delivery and of restructuring. Joseph LaVorgna,

Deutsche Bank: As the economic slack rapidly dissipates, the Fed

should be forward-looking.

Guy LeBas, Janney Montgomery Scott: In the short term, the

biggest threat to economic growth is the dollar--one need look no

further than 1Q 2015 to get an idea of how the dollar can

impact

economic output. Longer term, we're in the midst of secular

stagnation, marked by lower income-earning population growth and

reduced productivity growth. Perhaps 2.5% GDP growth is as good as

we can expect for the next several decades.

-

CNBC Fed Survey June 16, 2015 Page 30 of 31

FED SURVEY June 16, 2015

FED SURVEY April 30,

Ward McCarthy, Jefferies: The timing of Liftoff will be

opportunistically data dependent. The FOMC wants to end ZIRP with

as little disruption to financial markets as possible.

Rob Morgan, Sethi Financial Group: The minutes from the last

FOMC meeting said rates wouldn't rise until participants saw labor

market improvement and were confident inflation would hit 2 percent

in the medium term. I don't think we're there yet.

James Paulsen, Wells Capital Management: By waiting so long to

start raising the funds rate, the Fed has increased the difficulty

of the exit plan. Normally, the Fed begins tightening much sooner

in

the recovery cycle when profits and margins are still expanding

strongly after the previous recession. Today, the profit cycle is

already mature and the Fed will be raising interest rates against

relatively slow-growing corporate earnings and with weak

productivity. Consequently, the impact on the financial markets

may be more extreme than most seem to appreciate. Lynn Reaser,

Point Loma Nazarene University: If a September

rate hike depends on the data, that data is arriving. It will

take more than El Nio to keep the Fed on hold.

Chris Rupkey, Bank of Tokyo-Mitsubishi: Waiting for unemployment

to fall a little further so the Fed can liftoff, which would be a

"celebration" in some policymakers minds, celebrating that the US

economy has shaken off all the headwinds from the

Great Recession. The Great Recession the Fed caused by letting

Lehman go under. John Ryding, RDQ Economics: The economy is close

to full

employment and there are no signs that lower oil prices have

produced broader deflation pressures. Banks are well-capitalized

and the stock market has been hitting record highs. Fed policy has

overstayed its welcome at zero rates but, alas, will likely

continue to

-

CNBC Fed Survey June 16, 2015 Page 31 of 31

FED SURVEY June 16, 2015

FED SURVEY April 30,

do so for the next three months. Allen Sinai, Decision

Economics: The next big thing is Fed Policy rate hike -- the second

and beyond.

Hank Smith, Haverford Investments: If the next presidential

administration enacts pro-growth tax reform and regulatory relief,

we may be in the middle innings of this economic expansion and

equity bull market Diane Swonk, Mesirow Financial: When the

history on liftoff is written, the Fed is likely to be judged more

on the trajectory of rates

after liftoff, not the act itself. The next decisions that the

Fed makes could very well be more important than the month it times

liftoff. Robert Tipp, Prudential Fixed Income: We still see value

in

bonds. At this point, the bond market has gone a long way

towards pricing in the Fed's likely path of rate hikes, and we view

spreads on select issuers in the non-government sectors, such as

high yield and investment grade corporates, structured products and

emerging

markets are attractive. As a result, we continue to expect fixed

income to add value and provide ballast to investors' portfolios.

While modest compared to decades past, we nonetheless expect

that

over the intermediate to long term fixed income, especially the

higher yielding sectors, will continue to post respectable returns.

Mark Zandi, Moody's Analytics: The U.S. economy has reached

escape velocity. It would take a sizable shock to derail it.

Odds are high the economy will be back to full-employment by this

time next year. All the pieces are in place for the Fed to steadily

normalize interest rates.