-

7/30/2019 CNBC Fed Survey - April 30, 2013

1/38

CNBC Fed Survey April 30, 2013Page 1 of 38

FED SURVEYApril 30, 2013

These survey results represent the opinions 46 of the nations

top money managers, investment

strategists, and professional economists.

They responded to CNBCs invitation to participate in our online

survey. Their responses were collecte

on April 25-26, 2013. Participants were not required to answer

every question.

Results are also shown for identical questions in earlier

surveys.

This is not intended to be a scientific poll and its results

should not be extrapolated beyond those whodid accept our

invitation.

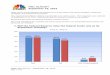

1.For all of 2013 and for all of 2014 (and only in 2014), what

isthe total amount of additional asset purchases the Federal

Reserve will have made?

$858.8

$917.0

$936.6

$370.6

$0 $200 $400 $600 $800 $1,000 $1,200 $1,40

2013

2014

Billions

January 29 March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

2/38

CNBC Fed Survey April 30, 2013Page 2 of 38

FED SURVEYApril 30, 2013

2.What mix of Treasuries vs. mortgage-backed securities do

youexpect the Federal Reserve to purchase?

52.2% 51.5% 53.3%

47.8% 48.5%46.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

January 29 March 19 April 30

Survey Dates

Treasuries MBS

-

7/30/2019 CNBC Fed Survey - April 30, 2013

3/38

-

7/30/2019 CNBC Fed Survey - April 30, 2013

4/38

CNBC Fed Survey April 30, 2013Page 4 of 38

FED SURVEYApril 30, 2013

4.The Federal Reserve will:

22%

76%

2%

8%

89%

4%4%

94%

2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

End its purchases in asingle month

Gradually reduce (taper)its purchases

Don't know/unsure

January 29 March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

5/38

CNBC Fed Survey April 30, 2013Page 5 of 38

FED SURVEYApril 30, 2013

(For those who believed the Fed will taper) In what month do

you expect the Fed to begin tapering its purchases?

0%

5%

10%

15%

20%

25%

January 29 March 19 April 30

Averages

Jan. 29:Dec 2013

March 19:Jan 2014

April 30:Feb 2014

-

7/30/2019 CNBC Fed Survey - April 30, 2013

6/38

CNBC Fed Survey April 30, 2013Page 6 of 38

FED SURVEYApril 30, 2013

5.At what unemployment/inflation rate will the Fed halt its

assepurchases?

6.5%6.8% 6.7%

6.4%

3.4%

2.6% 2.6% 2.7%

0%

1%

2%

3%

4%

5%

6%

7%

December 11, 2012 January 29, 2013 March 19, 2013 April 30,

2013

Survey Dates

Unemployment Inflation

-

7/30/2019 CNBC Fed Survey - April 30, 2013

7/38

CNBC Fed Survey April 30, 2013Page 7 of 38

FED SURVEYApril 30, 2013

6.When it comes to how you think the Fed will exit from

itscurrent monetary policy, do you believe it WILL:

4%6%

29%

53%

8%

4%

9%

26%

54%

7%

0%

10%

20%

30%

40%

50%

60%

Sell Treasuriesonly

Sell MBS only Sell both Not sell anyassets at all

Don'tknow/unsure

March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

8/38

CNBC Fed Survey April 30, 2013Page 8 of 38

FED SURVEYApril 30, 2013

When it comes to how you think the Fed will exit from its

curren

monetary policy, do you believe it SHOULD:

6%

2%

41%

37%

14%

7%

9%

35%

37%

13%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Sell Treasuriesonly

Sell MBS only Sell both Not sell anyassets at all

Don'tknow/unsure

March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

9/38

CNBC Fed Survey April 30, 2013Page 9 of 38

FED SURVEYApril 30, 2013

7.When it comes to the Feds use of economic

targetsspecifically:

38%

48%

10%

4%

45%

28% 28%

0%

41% 41%

15%

2%0%

10%

20%

30%

40%

50%

60%

The Fed is clear The Fed could be

more clear

The Fed is not clear

at all

Don't know/unsure

January 29 March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

10/38

CNBC Fed Survey April 30, 2013Page 10 of 38

FED SURVEYApril 30, 2013

Comments on Question 7:

Dean Baker, Center for Economic and Policy Research: The Fed has

been very clear as to what iwill look at. It is keeping options

open since it does not know exactly what the future will look

like.

Lou Brien, DRW Trading Group: I think the Fed should more

clearly state that it is not completely

clear to them how they will react to economic data in regards to

their quantitative easing programs. Imore likely they will know it

when they see it but it is not likely they will know it before

then.

Robert Brusca, Fact and Opinion Economics: Targets? Thresholds?

Triggers?

Stephen Gallagher, Societe Generale: Fed has clearly stated

6.5%, but risks credibility if they tie

falling unemployment to technical factors later on.

Hugh Johnson, Hugh Johnson Advisors: There are two important

components of Federal Reserve

policy. The first is the target for the federal funds rate,

which is unlikely to change until 2015 even

though (a) the unemployment rate should be at or near 6.5% Q4

2014 and the outlook for 2015inflation should be near 2.5% Q4 2014.

The second component is QE (asset purchases). My expectatiis that,

depending on economic variables, the process of "tapering" asset

purchases could begin in

September 2013 and essentially lead toward the end of QE

mid-2014.

Alan Kral, Trevor Stewart Burton & Jacobsen: The Fed can

justify anything it wants at any time.

William Larkin, Cabot Money Management: Targets change as

economic conditions shift.

Guy LeBas, Janney Montgomery Scott: It's hard to trust an

economic target, when the Fed, in the

same day as issuing a target, also qualified it heavily.

Donald Luskin, Trend Macrolytics: The targets are a sham. They

create the illusion of precision in

regime of total discretion.

Rob Morgan, Fulcrum Securities: The Fed is clear in its use of

economic targets. I'm just not sure

they are wise in using economic targets.

Joel Naroff, Naroff Economic Advisors: The Fed needs to make it

clearer that 6.5% is a soft, not a

hard, target. A rapid decline to the target could and should

lead to a quicker ending of the policy.

Phil Orlando, Federated Investors: The Fed should make clear

that its inflation and unemploymentargets are more directly tied to

their fed funds target rate decision, rather than their "QE to

Infinity"

asset-purchase decision, which appears to be more qualitative in

nature.

James Paulsen, Wells Capital Management: I think the Fed builds

unrealistic expectations publicl

basing its future policies on a specific variable and thereby

exposes the economy and the financialmarkets to an abrupt and

unexpected shift in policy when economic conditions warrant a

response evthough "specific preordained variables" have not yet

reached critical levels. The Fed would be better

served by sticking to more generalized commentary as to how

their policies are being guided, e.g.

-

7/30/2019 CNBC Fed Survey - April 30, 2013

11/38

CNBC Fed Survey April 30, 2013Page 11 of 38

FED SURVEYApril 30, 2013

inflation pressures, speed of growth and degree of resource

slack or output gap and not be more

specific than that.

Chris Rupkey, Bank of Tokyo-Mitsubishi: Clear when it should not

be. This is art, not science.

John Ryding, RDQ Economics: The Fed is ambiguous in (i)

describing the 6 1/2% unemployment ra

and the 2 1/2% inflation rate as thresholds rather than triggers

and the description of 'balanced'response. Also, unemployment is an

actual variable but inflation is a forecast over 1-2 years. In

addition, the Fed has also said it will look at a range of labor

market indicators. What happens ifunemployment falls to 6 1/4%

because of falling labor market participation? Will the Fed look at

U-6?The employment-population ratio?

Ellen Zentner, Nomura: The challenge at this point is twofold.

The views of FOMC participants appevery diverse. That is evident in

the discussion of prospects for LSPAs. In addition, what

constitutes t

"outlook for the labor market" is relatively complex. This makes

it difficult for the committee to send clear signal about the most

immediate issue, i.e., the likely course of the current LSPA

program.

-

7/30/2019 CNBC Fed Survey - April 30, 2013

12/38

CNBC Fed Survey April 30, 2013Page 12 of 38

FED SURVEYApril 30, 2013

8.Do you believe further quantitative easing can help lower

theunemployment rate?

36%37%

34%

21%

28%

59% 59% 58%

69%

65%

5% 4%

8%10%

7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Sept 12, 2012 Dec 11 Jan 29, 2013 March 19 April 30

Survey Dates

Yes No Don't know/unsure

-

7/30/2019 CNBC Fed Survey - April 30, 2013

13/38

CNBC Fed Survey April 30, 2013Page 13 of 38

FED SURVEYApril 30, 2013

Do you believe further quantitative easing can help mortgage

rates?

59%

54%

44%

46%

33%

42%

48%

44%

9%

4%

8%

11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Dec 11, 2012 Jan 29, 2013 March 19 April 30

Survey Dates

Yes No Don't know/unsure

-

7/30/2019 CNBC Fed Survey - April 30, 2013

14/38

CNBC Fed Survey April 30, 2013Page 14 of 38

FED SURVEYApril 30, 2013

Do you believe further quantitative easing can help lower

bond

yields?

58%

47%

44%

54%

30%

47%48%

35%

13%

6%8%

11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

December 11, 2012 January 29, 2013 March 19 April 30

Survey Dates

Yes No Don't know/unsure

-

7/30/2019 CNBC Fed Survey - April 30, 2013

15/38

CNBC Fed Survey April 30, 2013Page 15 of 38

FED SURVEYApril 30, 2013

Do you believe further quantitative easing can help increase

stock prices?

69%

75%

83%

20%17%

9%

10%8% 9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

January 29, 2013 March 19 April 30Survey Dates

Yes No Don't know/unsure

-

7/30/2019 CNBC Fed Survey - April 30, 2013

16/38

CNBC Fed Survey April 30, 2013Page 16 of 38

FED SURVEYApril 30, 2013

9.Since September 2012, market functioning in the governmentbond

market has:

0%

19%

60%

15%

2%

4%

0%

11%

65%

15%

2%

7%

0% 10% 20% 30% 40% 50% 60% 70%

Improved a lot

Improved somewhat

Stayed the same

Worsened somewhat

Worsened a lot

Don't know/unsure

March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

17/38

CNBC Fed Survey April 30, 2013Page 17 of 38

FED SURVEYApril 30, 2013

Since September 2012, market liquidity in the government

bond market has:

0%

29%

48%

15%

4%

4%

4%

17%

52%

17%

2%

7%

0% 10% 20% 30% 40% 50% 60%

Improved a lot

Improved somewhat

Stayed the same

Worsened somewhat

Worsened a lot

Don't know/unsure

March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

18/38

CNBC Fed Survey April 30, 2013Page 18 of 38

FED SURVEYApril 30, 2013

10.Since September 2012, market functioning in the

mortgage-backed security market market has:

4%

31%

29%

20%

2%

14%

2%

22%

39%

20%

4%

13%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Improved a lot

Improved somewhat

Stayed the same

Worsened somewhat

Worsened a lot

Don't know/unsure

March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

19/38

CNBC Fed Survey April 30, 2013Page 19 of 38

FED SURVEYApril 30, 2013

Since September 2012, market liquidity in the mortgage-

backed security market market has:

4%

21%

40%

19%

0%

15%

2%

28%

28%

22%

7%

13%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Improved a lot

Improved somewhat

Stayed the same

Worsened somewhat

Worsened a lot

Don't know/unsure

March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

20/38

CNBC Fed Survey April 30, 2013Page 20 of 38

FED SURVEYApril 30, 2013

11.When it comes to the debate over the U.S. debt

ceiling,Congress will:

86%

8%6%

92%

4% 4%

89%

4%7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Increase the debt ceilingevery time it is reached

this year

Refuse at some point thisyear to raise it

Don't know/unsure

January 29 March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

21/38

CNBC Fed Survey April 30, 2013Page 21 of 38

FED SURVEYApril 30, 2013

12.When it comes to the Sequester, Congress should:

Comments on changing the makeup of spending cuts:

Replace the sequester with a Bowles-Simpson-type formula for

reducing government spendingover an extended period of time.

The sequester = political dysfunction = activist Fed Give

president discretion to target cuts. Carefully target where the

cuts are to be made. If you think that mindless cutting of the

budget is good, this is your policy.

25%

33%

17%

21%

4%

35%

33%

20%

9%

4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Continue withthe current

spending cuts

Continue withthe current

level of thespending cuts,but change the

makeup

Reduce theamount of

spending cuts

Increase theamount of

spending cuts

Don'tknow/unsure

March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

22/38

CNBC Fed Survey April 30, 2013Page 22 of 38

FED SURVEYApril 30, 2013

Congress and the White House are seemingly incapable of

negotiating a more effective spendincut strategy than

sequestration, so sequestration has become "a good thing."

You don't seem to understand what is happening here. Congress

DIDN'T "INCREASE" the debtceiling in January. It SUSPENDED it. Huge

difference.

Every stakeholder has a different belief in what should be cut,

so choosing specific cuts is aprocess that would be mired in

debate. Across the board cuts, while less than ideal for all

involved, are the only evident way to short-circuit that debate.

We need to have a 10-year plan to dramatically reduce deficit

spending. The sequester was w

too small of an amount. We need to get serious. Fix

entitlements, instead of the sequester related to defense and

non-defense discretionary

spending.

Provide more flexibility regarding how the sequester is

implemented. The makeup of Congress is what needs changing; the

budget process should emphasize what i

best for the entire country, not to place blame in a highly

partisan manner.

The government could easily allow the FAA to more efficiently

allocate the cuts with FAR lessdisruption to travel. The U.S. runs

a risk of over tightening fiscal policy. This mornings report on

GDP highlights th

aspect. Overall, real GDP was up 2.5%...but real GDP excluding

government (private GDP) ro4%! In the last two quarters, real

private investment and consumption have risen at 3.7% an

3.3% annual rates respectively while overall real GDP has only

risen 0.4% and 2.5%. The mathing holding back U.S. growth is the

"Government!" Moreover, the emergency to balancegovernment is no

longer an emergency. The deficit to GDP ratio was about 10.5% in

2009 an

is now close to 6%. The deficit as a percentage of GDP has been

declining by more than 1% ayear in this recovery all on its own due

to the invisible hand of Adam Smith. At this rate, with12 to 24

months the deficit as a percentage of GDP will fall below 5% at

which point it may we

be less than the rate of nominal GDP, implying that the debt/GDP

ratio (which everyone is so

worried about) will peak and begin to decline all on its own.

The government should stand dow

and allow the invisible hand to continue dealing with the

deficit. One of the biggest risks to theconomy right now is that

government cutbacks become too extreme and cause the economy

stall. Let's stop the public cuts and allow the economy to grow

at the speed that "private activiis growing, which is about 3.5% to

4%.

Someone has to explain to them very slowly that they are just

slowing growth and increasingunemployment.

Prioritize the cuts within each agency rather than implement

across-the-board same percentagcuts.

Congress should provide flexibility to the administration on the

makeup. More targeted cuts including tax expenditures; shift more

to out-years when the economy is

healthier.

The administration messed up badly with the FAA by creating an

unnecessary problem with fligdelays to show that the sequester

hurts. The House and Senate took almost instant action to sdown the

administration and give the FAA flexibility to not cut controllers.

So keep the sequestbut give departments flexibility to make cuts.

THEN TACKLE ENTITLEMENTS!

Give agencies more flexibility to reallocate cuts within

departments. Some prioritizing is needed.

-

7/30/2019 CNBC Fed Survey - April 30, 2013

23/38

CNBC Fed Survey April 30, 2013Page 23 of 38

FED SURVEYApril 30, 2013

13.What impact, if any, do you believe recent

revenueincreases/the Sequester will have on U.S. GDP this year?

Note: We did not ask about the Sequester in the January 29

survey.

-0.61%

-0.32%-0.40%

-0.28%-0.20%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%Revenue Increases The Sequester

January 29 March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

24/38

CNBC Fed Survey April 30, 2013Page 24 of 38

FED SURVEYApril 30, 2013

14.When it comes to the budget deficit, the United States:

80%

16%

4%

0%

67%

25%

4% 4%

52%

39%

9%

0%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Should urgentlyenact a plan that

puts it on a path

toward asustainable budget

deficit

Has at least acouple of years

before it must enact

such a plan

Does not need toenact a plan that

puts it on a path

toward asustainable budget

deficit

Don't know/unsure

January 29 March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

25/38

CNBC Fed Survey April 30, 2013Page 25 of 38

FED SURVEYApril 30, 2013

15.When it comes to Europe, do you believe the lack of a

currencrisis mentality is:

30%

62%

8%

29%

64%

8%

36%

64%

0%0%

10%

20%

30%

40%

50%

60%

70%

A sign of real progress Only temporary Don't know/unsure

January 29 March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

26/38

CNBC Fed Survey April 30, 2013Page 26 of 38

FED SURVEYApril 30, 2013

16.The recent decline in the price of gold is mostly the result

of:

Other responses:

Slower global economic growth Many things Lower inflation and

global economic

expectations

Latest chapter in secular commoditydecline that began in

2011

Possible Cyprus selling Technical factors Lower inflation/lower

risk Combination of all above Strong dollar and rumor regarding

Cyprus liquidation

Fear of central bank sales Momentum trading Cyprus' gold sales

may have been a

preview of what other, larger, central

banks may do

BOJ policy Freak of nature sell-off Concerns over a movement

toward larg

active sellers

Large European Central Bank forced sa

15.6% 15.6%

24.4%

35.6%

8.9%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Lower inflationexpectations

Less concernabout global

risk

Popping of aprice bubble

Other Don'tknow/unsure

-

7/30/2019 CNBC Fed Survey - April 30, 2013

27/38

CNBC Fed Survey April 30, 2013Page 27 of 38

FED SURVEYApril 30, 2013

17.Twelve months from now the price of gold will be:

2%

33%

22%

33%

0%

9%

0%

5%

10%

15%

20%

25%

30%

35%

Much lower Lower About thesame

Higher Much higher Don'tknow/unsure

-

7/30/2019 CNBC Fed Survey - April 30, 2013

28/38

CNBC Fed Survey April 30, 2013Page 28 of 38

FED SURVEYApril 30, 2013

18.Which one of two of the following do you think are the

bestinvestments right now? (Respondents could chose up to

twochoices.)

Other responses:

Non-agency mortgage backed securities Commodities all except

gold Long Nikkei, short yen EM local debt Industrial commodities

Developing economy equities

73%

62%

4%

4%

7%

7%

13%

4%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Stocks

Real estate

Gold

U.S. Treasury bonds

Savings accounts and other cashinstruments

Corporate bonds

Other

Don't know/unsure

-

7/30/2019 CNBC Fed Survey - April 30, 2013

29/38

CNBC Fed Survey April 30, 2013Page 29 of 38

FED SURVEYApril 30, 2013

19.Where do you expect the S&P 500 stock index will be on

?

1451

14971480

1505

1539

15771547

1589

1612

1,350

1,400

1,450

1,500

1,550

1,600

1,650

July 31 2012 Sept 12 Dec 11 Jan 29 2013 March 19 April 30

Survey Dates

June 30, 2013 December 31, 2013

-

7/30/2019 CNBC Fed Survey - April 30, 2013

30/38

CNBC Fed Survey April 30, 2013Page 30 of 38

FED SURVEYApril 30, 2013

20.What do you expect the yield on the 10-year Treasury notewill

be on ?

1.98%2.06%

1.90%

2.09% 2.09%

1.83%

2.31% 2.35%

2.10%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

July 31 2012 Sept 12 Dec 11 Jan 29 2013 March 19 April 30

Survey Dates

June 30, 2013 December 31, 2013

-

7/30/2019 CNBC Fed Survey - April 30, 2013

31/38

CNBC Fed Survey April 30, 2013Page 31 of 38

FED SURVEYApril 30, 2013

21.What is your forecast for the year-over-year percentagechange

in real U.S. GDP for ?

+2.6%

+2.7%

+2.6%

+2.3%

+2.2%

+1.9%

+2.1% +2.1% +2.1%

+2.6%+2.6% +2.6%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

January23,

2012

March16

April 24 July 31 Sept 12 Dec 11 Jan 29,2013

Mar 19 April 30

Survey Dates

2013 2014

-

7/30/2019 CNBC Fed Survey - April 30, 2013

32/38

CNBC Fed Survey April 30, 2013Page 32 of 38

FED SURVEYApril 30, 2013

22.When do you think the FOMC will first increase the fed

fundsrate and when will it make its first planned decrease in the

sizof its balance sheet?

Increase fed funds rate

Decrease balance sheet

(Average response)

Survey Date

December

11, 2012

January 29,

2013

March 19,

2013

April 30,

2013

2013 Q2

Q3

Q4

2014 Q1

Q2

Q3

Q42014

Q42014

Q4

2015 Q12015

Q12015

Q12015

Q12015

Q1

Q22015

Q22015

Q2

Q3

Q4

2016 Q1

Q2

Q3

Q4

2017 or later

-

7/30/2019 CNBC Fed Survey - April 30, 2013

33/38

CNBC Fed Survey April 30, 2013Page 33 of 38

FED SURVEYApril 30, 2013

24.Where do you expect the fed funds target rate will be on

?

0.41%

0.42%

0.27%

0.20%

0.14%

0.16%0.16%

0.14%

0.16%

0.33%

0.27%

0.21%

0.17%

0.19% 0.19%

0.0%

0.1%

0.1%

0.2%

0.2%

0.3%

0.3%

0.4%

0.4%

0.5%

Jan 232012

Mar 16 Apr 24 Jul 31 Sep 12 Dec 11 Jan 292013

Mar 19 Apr 30

Survey Dates

June 30 2013 Dec 31 2013

-

7/30/2019 CNBC Fed Survey - April 30, 2013

34/38

CNBC Fed Survey April 30, 2013Page 34 of 38

FED SURVEYApril 30, 2013

25.In the next 12 months, what percent probability do you

placeon the U.S. entering recession? (0%=No chance of

recession,100%=Certainty of recession)

34.0%

36.1%

25.5%

20.3%

19.1%

20.6%

25.9%

26.0%

28.5%

20.4%

17.6%

18.2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Aug

11,

2011

Sep

19

Oct

31

Jan

23,

2012

Mar

16

Apr

24

Jul

31

Sep

12

Dec

11

Jan

29,

2013

Mar

19

Apr

30

Survey Dates

-

7/30/2019 CNBC Fed Survey - April 30, 2013

35/38

CNBC Fed Survey April 30, 2013Page 35 of 38

FED SURVEYApril 30, 2013

26.What is the single biggest threat facing the U.S.

economicrecovery?

Other responses: Sharper global economic slowdown Washington Not

enough FUTURE deficit

reduction...then jobs

Geopolitical risk Fiscal policy in general

10%

42

20%

0%

2%

0%

2%

6%

6%

12%

0%

10%

29%

12%

0%

4%

2%

0%

10%

16%

16%

2%

20%

31%

20%

2%

0%

2%

2%

2%

9%

11%

0%

0% 5% 10% 15% 20% 25% 30% 35% 40% 4

European recession/financial crisis

Tax/regulatory policies

Slow job growth

High gasoline prices

Overall inflation

Deflation

Debt ceiling

Too little budget deficit reduction

Too much budget deficit reduction

Other

Don't know/unsure

January 29 March 19 April 30

-

7/30/2019 CNBC Fed Survey - April 30, 2013

36/38

CNBC Fed Survey April 30, 2013Page 36 of 38

FED SURVEYApril 30, 2013

27.What is your primary area of interest?

Comments:

Robert Brusca, Fact and Opinion Economics: The SNAFU over the

air trafficcontrollers tells it all. The president, who should be

looking out for our bestinterests, is instead using sequestration

where he did not get his way to punish

us so we know that sequestration hurts. Congress is at a log

jam. We the peoplehave become expendable, pawns in a big-time game

of Republican-Democrat

politics. Were now like Europe, ruled by an elite with its own

agenda. We thepeople- what a joke...we the peons is more like

it.

Tony Crescenzi, PIMCO: Is Ben Bernanke skipping Jackson Hole in

August toinstead go fishing with Steve Liesman?

Mark Elenowitz, TriPoint Global Equities: In 2011, I stated that

we believed

the risk of persistent unemployment and other economic headwinds

could leadto yet another round of QE. We were the minority but were

right. Today in

2013, not much has changed other than a sequestration that is

causing harm,debt ceilings that are broken thru, a standoff among

politicians, and continued

unemployment. Until all parties focus on a practical solution

rather than blameand policies that are not working, this cycle and

Fed actions will continue.

Economics41%

Equities24%

Fixed Income

15%

Currencies

2%

Other

17%

-

7/30/2019 CNBC Fed Survey - April 30, 2013

37/38

CNBC Fed Survey April 30, 2013Page 37 of 38

FED SURVEYApril 30, 2013

Hugh Johnson, Hugh Johnson Advisors: Although there are

significant risks(Europe, China, U.S. fiscal policy) none will

derail the current bull market-

economic expansion. The most significant risk that we know that

faces the U.S.equity markets currently (and it is not a large risk)

is valuation. The equity

markets remain 3-4% overvalued or above the level they "should"

average inthe current quarter. Additionally, the returns for

equities and fixed income are

likely to be subdued between now and end of 2014 (0.2% for

fixed; 5.5% forequities total returns). But currently we do not see

risks that will derail recovery,

although the debt ceiling issue will again be a factor in

September! Summer willbe quiet.

John Kattar, Ardent Asset Advisors: The economy is struggling.

The datahave been weak, and continued growth in free reserves is

indicative of risk

aversion and lack of credit demand. I now believe an extension

of QE into 2014is somewhat more likely than any tapering before

year end.

Barry Knapp, Barclays PLC: The portfolio balance effect has been

effective inraising stock prices but primarily those with bond-like

characteristics. For 1Q13the best performing sectors were the 4

defensives. While this doesn't necessarily

alter the wealth effect it does imply that the policy

transmission channel of stockprices boosting business investment

won't work as well as would be the case if

share prices were rising due to improving fundamentals.

David Kotok, Cumberland Advisors: Washington policy restrains

U.S. growth.Fix Washington and the U.S. economy will soar.

Alan Kral, Trevor Stewart Burton & Jacobsen: Monetary policy

has lost itseffectiveness.

Subodh Kumar, Subodh Kumar & Associates: Edict by

policymakers like thegovernment or the Fed cannot establish value

in capital markets but do risk

distorting them. Investors need to focus on quality of execution

by companies

(and governments).

William Larkin, Cabot Money Management: As investors we need to

keep inmind that recoveries can often come unexpectedly.

Guy LeBas, Janney Montgomery Scott: With commodities prices

falling,there's been greater discussion of disinflation of late.

Fed asset purchases canstill be effective in stemming corrosive

disinflation, but their ability to stimulate

economic growth is nearing its end.

-

7/30/2019 CNBC Fed Survey - April 30, 2013

38/38

FED SURVEYApril 30, 2013

Rob Morgan, Fulcrum Securities: The use of economic targets by

the Fed is

not wise because if the committee raises rates because a target

has beenreached, they are already behind the inflation

eight-ball.

Chad Morganlander, Stifel Nicolaus (Washington Crossing

Advisors):Unfortunately, the economy has not reached the point of a

self-sustainedrecovery. The Federal Reserve will continue easing

well beyond street

expectations. Its paramount that we make a transition from a

liquidity-inducedrally to an environment with above-trend economic

growth.

Joel Naroff, Naroff Economic Advisors: The Fed, by deed if not

by word, ismaking it clear that a little extra inflation is not a

bad thing.

Chris Rupkey, Bank of Tokyo-Mitsubishi: If the Fed keeps rates

down atzero until 2016, there won't be a fixed income market for

you to report on, or at

least the number of sales and trading staff needed Street-wide

will be cut in

half.

Hank Smith, Haverford Investments: The key for a successful Fed

exit lieswith better pro-growth fiscal policy. That won't happen

with this administration.

Mark Vitner, Wells Fargo: We see the continued recovery in home

sales and

residential construction offsetting the drag from higher taxes,

reducedgovernment spending, and the global economic slowdown.

Scott Wren, Wells Fargo Advisors: 1Q earnings results have

little to do withthe continuation of the rally we have seen.

Reasonable valuations, the Fed'seasy money policies, and the fact

that the economy continues to move ahead

are the biggest factors. The market is comfortable with this

modestgrowth/modest inflation environment. It also helps in the

near term that

"everyone" is waiting for a pullback and some investors are

starting to jump into

the market, worried they will miss more upside.

Mark Zandi, Moody's Analytics: The next few months will be

uncomfortableas economic growth slows in the face of intensifying

fiscal headwinds. But theeconomy will grow strongly next year as

the fiscal headwinds fade and thestrength of the private economy is

able to shine through.