Embed Size (px)

Citation preview

Coffee Market Outlook Mauricio Galindo International Coffee Council March 2015

Supply & Demand

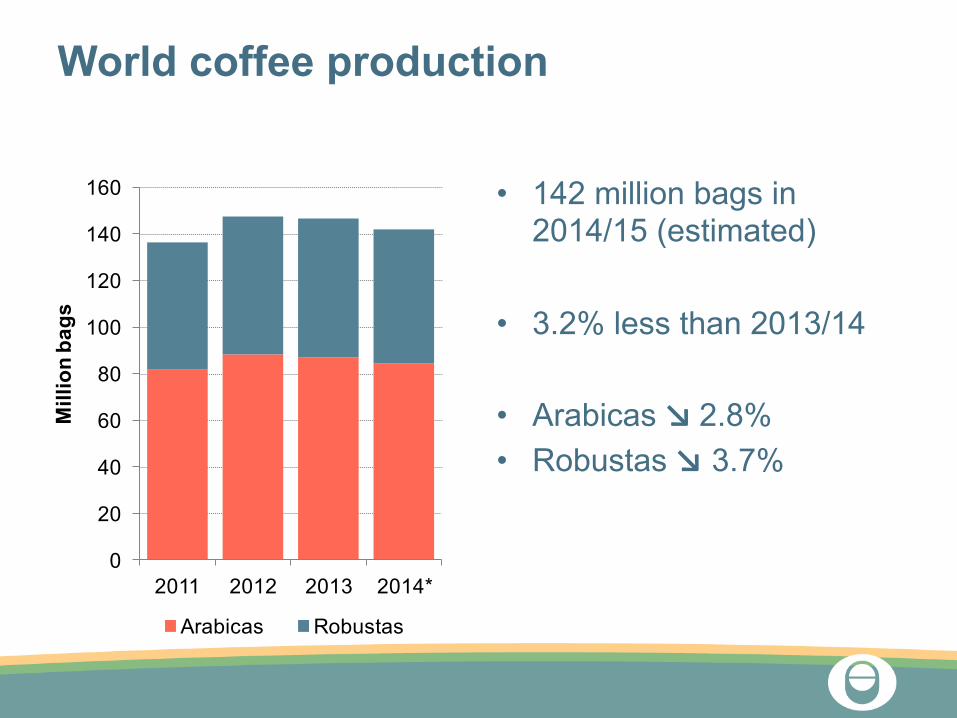

World coffee production

• 142 million bags in 2014/15 (estimated)

• 3.2% less than 2013/14

• Arabicas ↘ 2.8% • Robustas ↘ 3.7%

0

20

40

60

80

100

120

140

160

2011 2012 2013 2014*

Mill

ion

bags

Arabicas Robustas

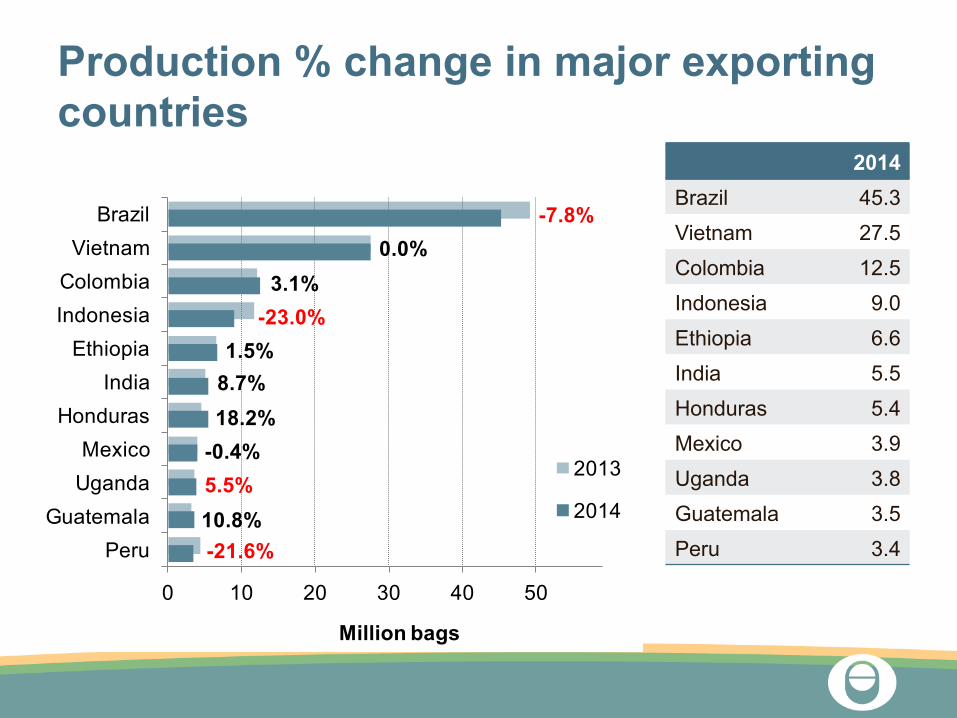

Production % change in major exporting countries

2014 Brazil 45.3 Vietnam 27.5 Colombia 12.5 Indonesia 9.0 Ethiopia 6.6 India 5.5 Honduras 5.4 Mexico 3.9 Uganda 3.8 Guatemala 3.5 Peru 3.4

-7.8%0.0%

3.1%-23.0%

1.5%8.7%18.2%

-0.4%5.5%10.8%-21.6%

0 10 20 30 40 50

BrazilVietnamColombiaIndonesiaEthiopiaIndia

HondurasMexicoUganda

GuatemalaPeru

Million bags

2013

2014

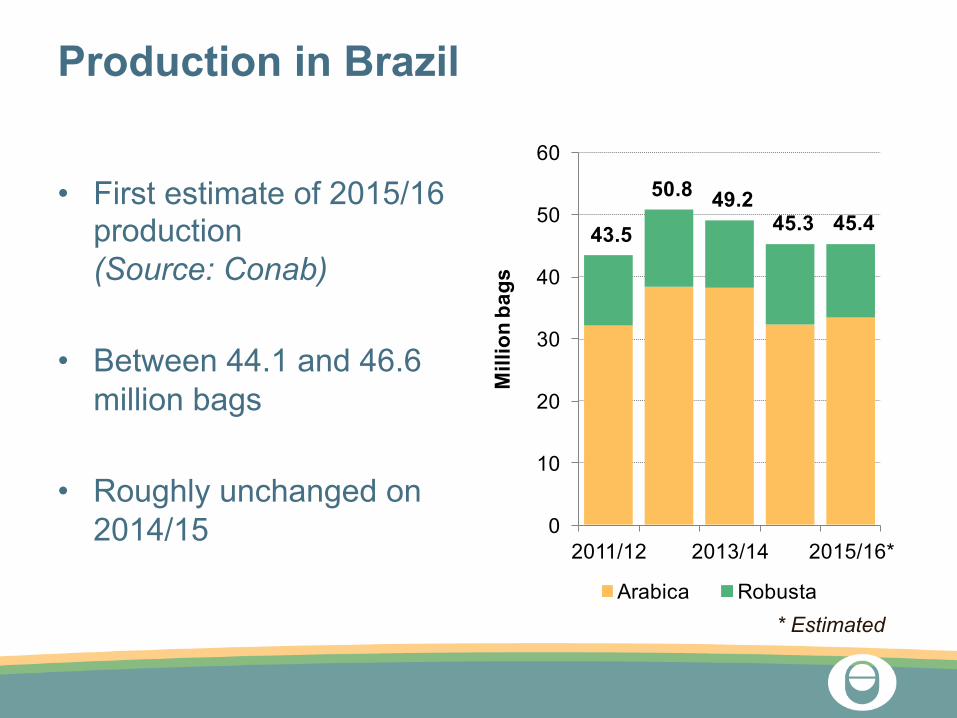

Production in Brazil

• First estimate of 2015/16 production (Source: Conab)

• Between 44.1 and 46.6 million bags

• Roughly unchanged on 2014/15

43.5

50.8 49.245.3 45.4

0

10

20

30

40

50

60

2011/12 2013/14 2015/16*

Mill

ion

bags

Arabica Robusta* Estimated

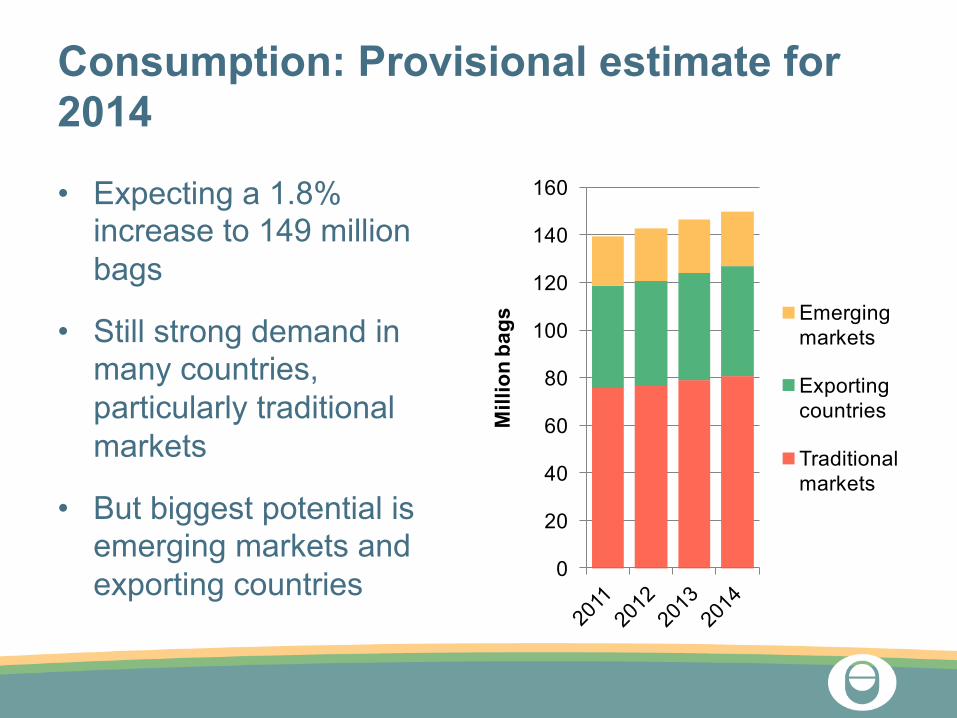

Consumption: Provisional estimate for 2014

• Expecting a 1.8% increase to 149 million bags

• Still strong demand in many countries, particularly traditional markets

• But biggest potential is emerging markets and exporting countries 0

20

40

60

80

100

120

140

160

Mill

ion

bags Emerging

markets

Exporting countries

Traditional markets

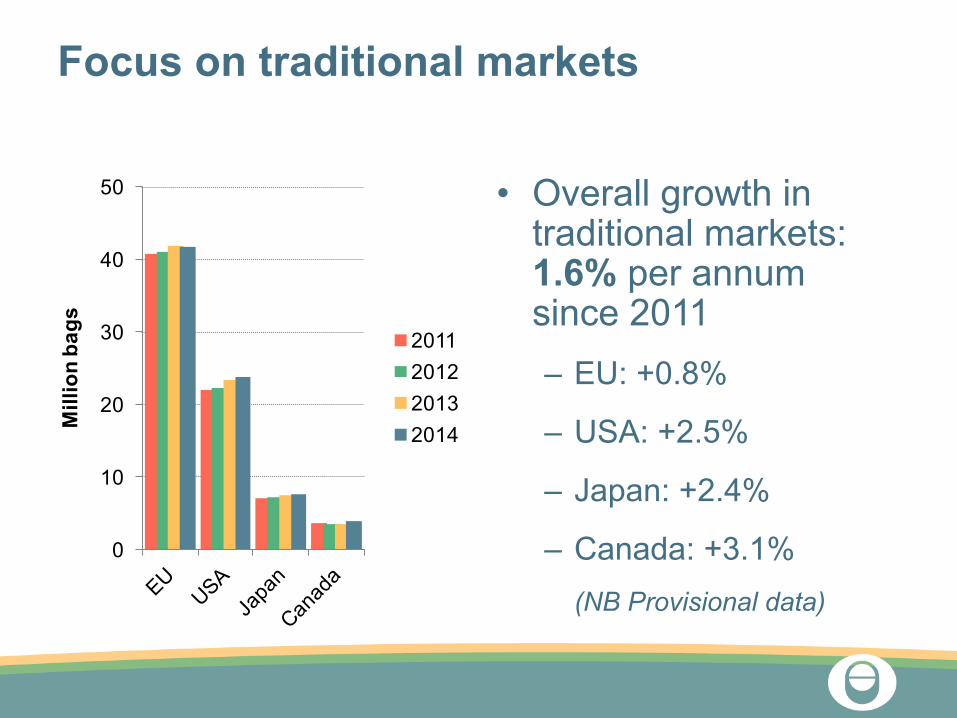

Focus on traditional markets

• Overall growth in traditional markets: 1.6% per annum since 2011 – EU: +0.8%

– USA: +2.5%

– Japan: +2.4%

– Canada: +3.1% (NB Provisional data)

0

10

20

30

40

50

Mill

ion

bags

2011201220132014

Prices

120

130

140

150

160

170

180

190

US

cent

s/lb

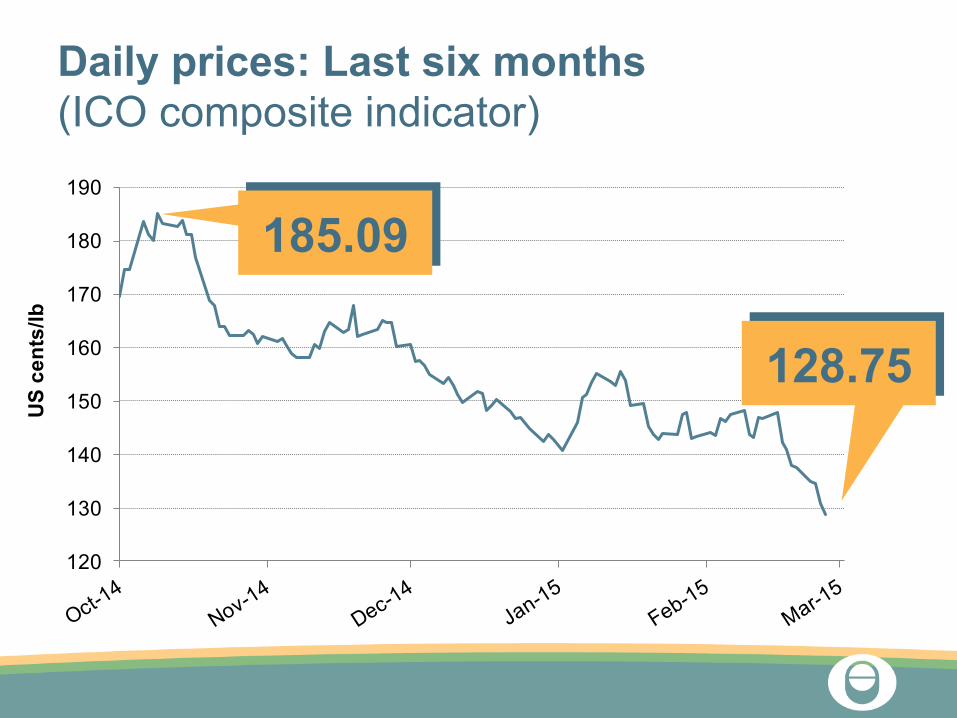

Daily prices: Last six months (ICO composite indicator)

185.09

128.75

80

100

120

140

160

180

200

US

cent

s/lb

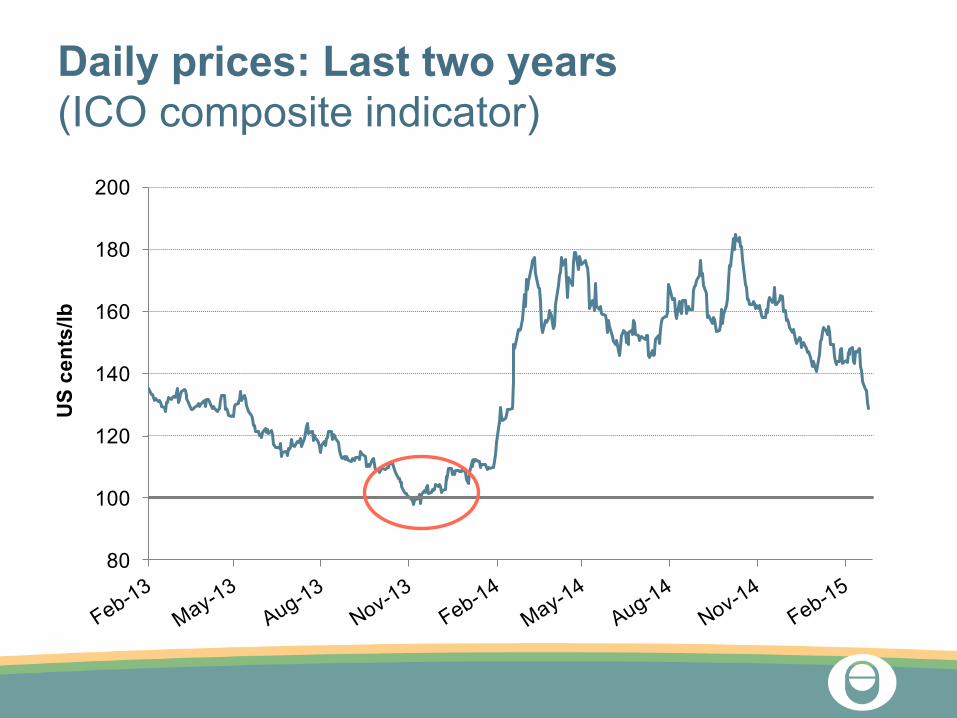

Daily prices: Last two years (ICO composite indicator)

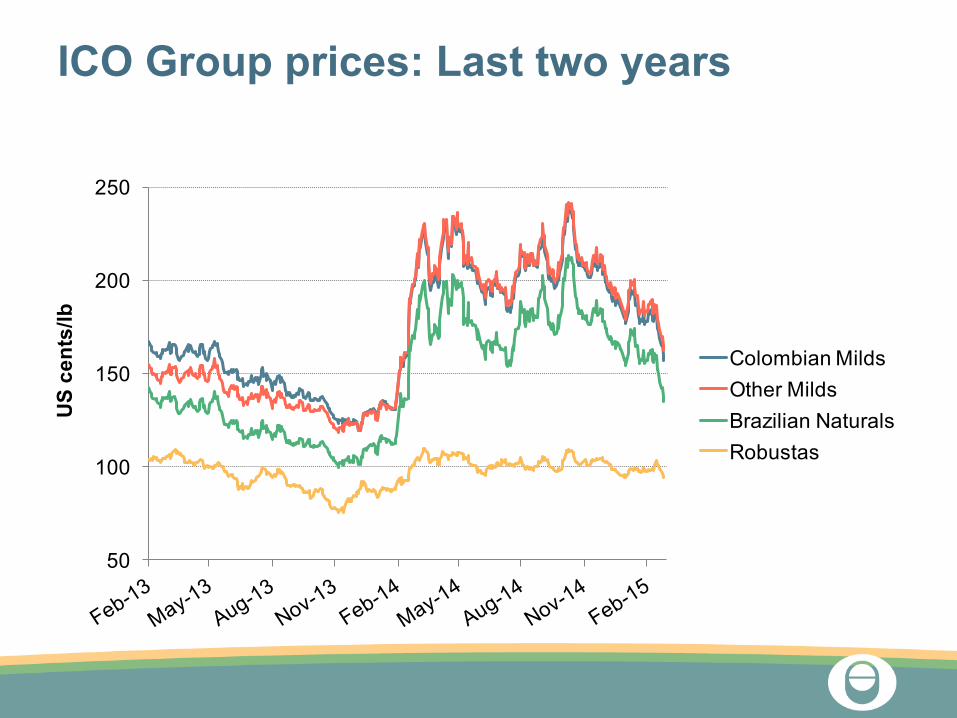

ICO Group prices: Last two years

50

100

150

200

250

US

cent

s/lb

Colombian MildsOther MildsBrazilian NaturalsRobustas

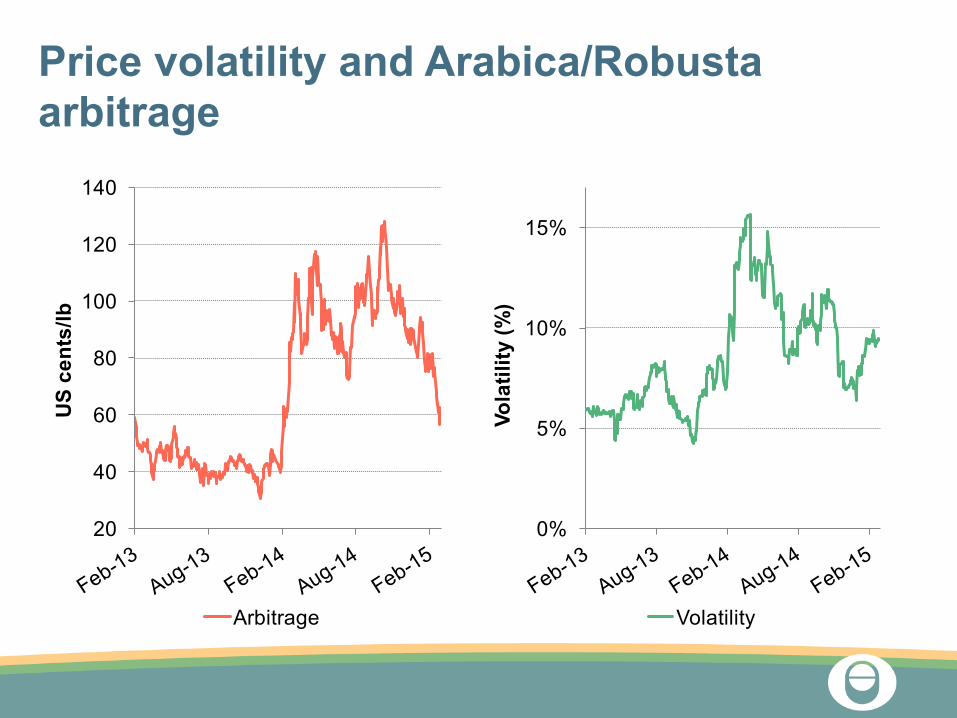

Price volatility and Arabica/Robusta arbitrage

20

40

60

80

100

120

140

US

cent

s/lb

Arbitrage

0%

5%

10%

15%

Vola

tility

(%)

Volatility

So, why have prices been falling?

7

8

9

10

11

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mill

ion

bags

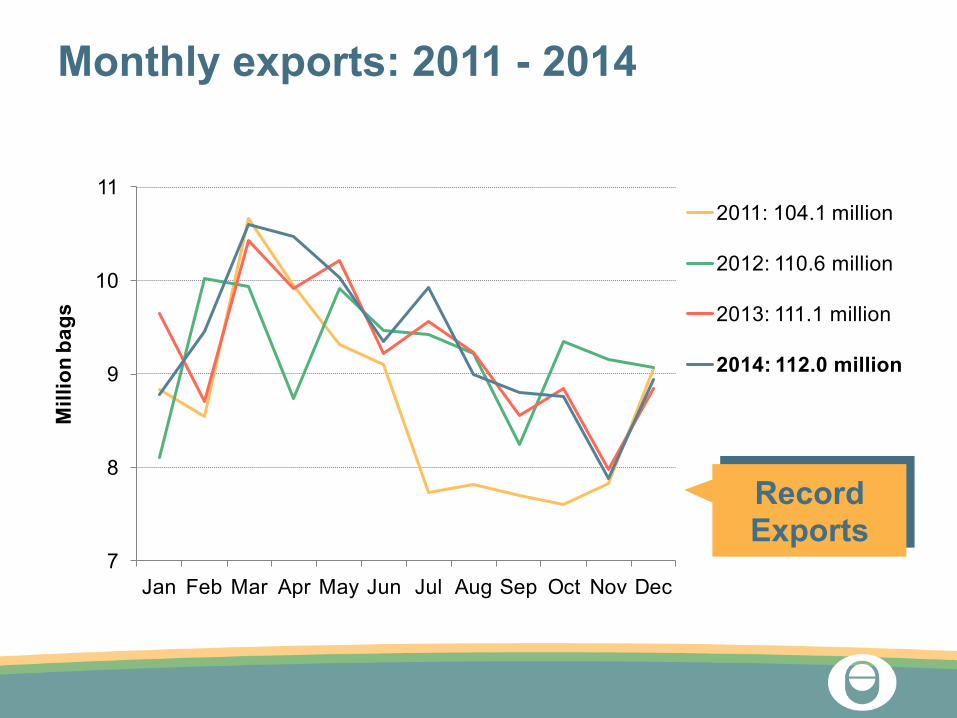

2011: 104.1 million

2012: 110.6 million

2013: 111.1 million

2014: 112.0 million

Monthly exports: 2011 - 2014

Record Exports

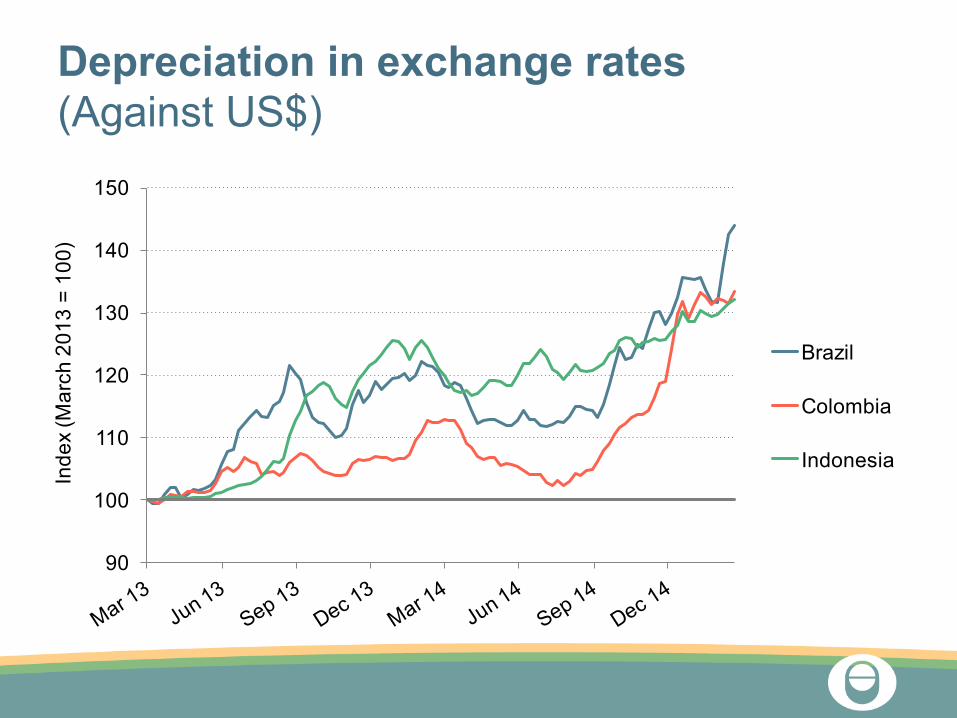

Depreciation in exchange rates (Against US$)

90

100

110

120

130

140

150

Inde

x (M

arch

201

3 =

100)

Brazil

Colombia

Indonesia

70

80

90

100

110

120

Inde

x (0

1-O

ct-1

4 =

100)

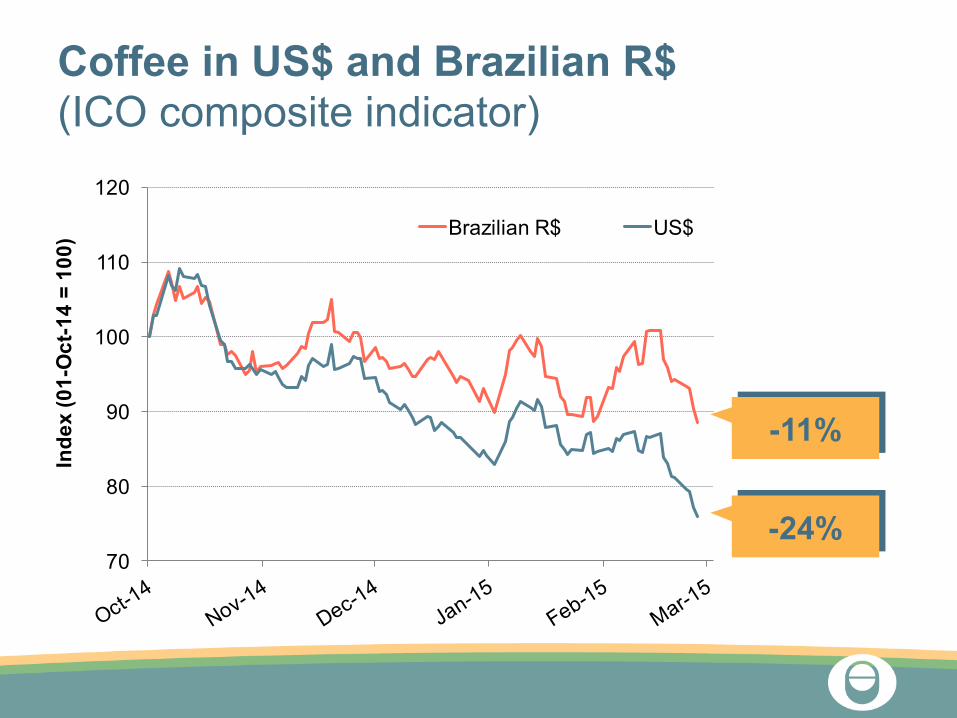

Brazilian R$ US$

Coffee in US$ and Brazilian R$ (ICO composite indicator)

-11%

-24%

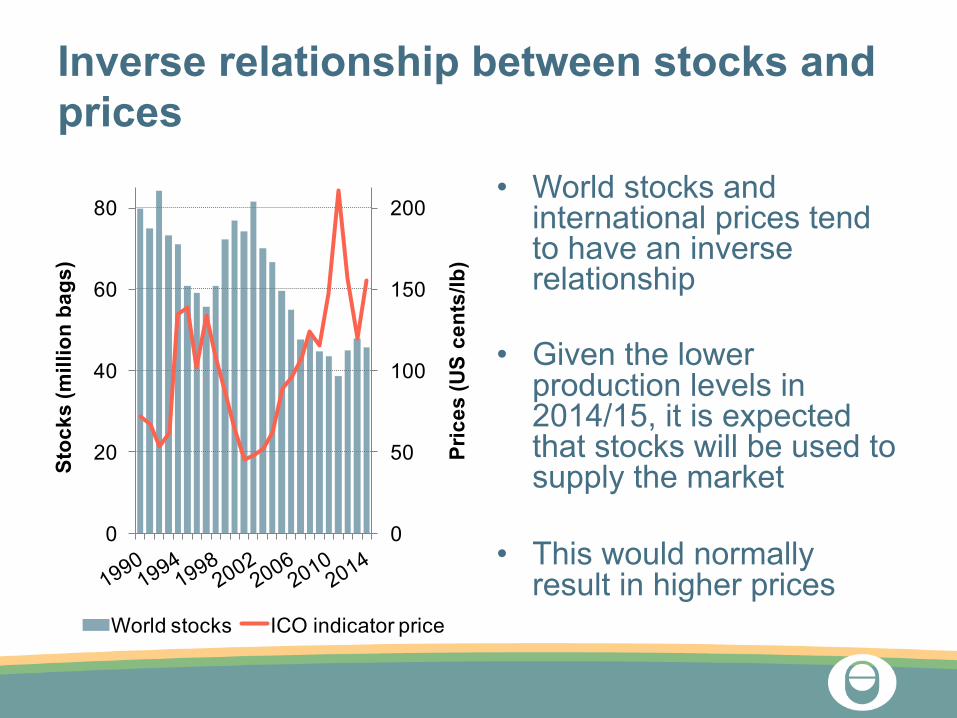

Inverse relationship between stocks and prices

• World stocks and international prices tend to have an inverse relationship

• Given the lower production levels in 2014/15, it is expected that stocks will be used to supply the market

• This would normally result in higher prices

0

50

100

150

200

0

20

40

60

80

Pric

es (U

S ce

nts/

lb)

Stoc

ks (m

illio

n ba

gs)

World stocks ICO indicator price

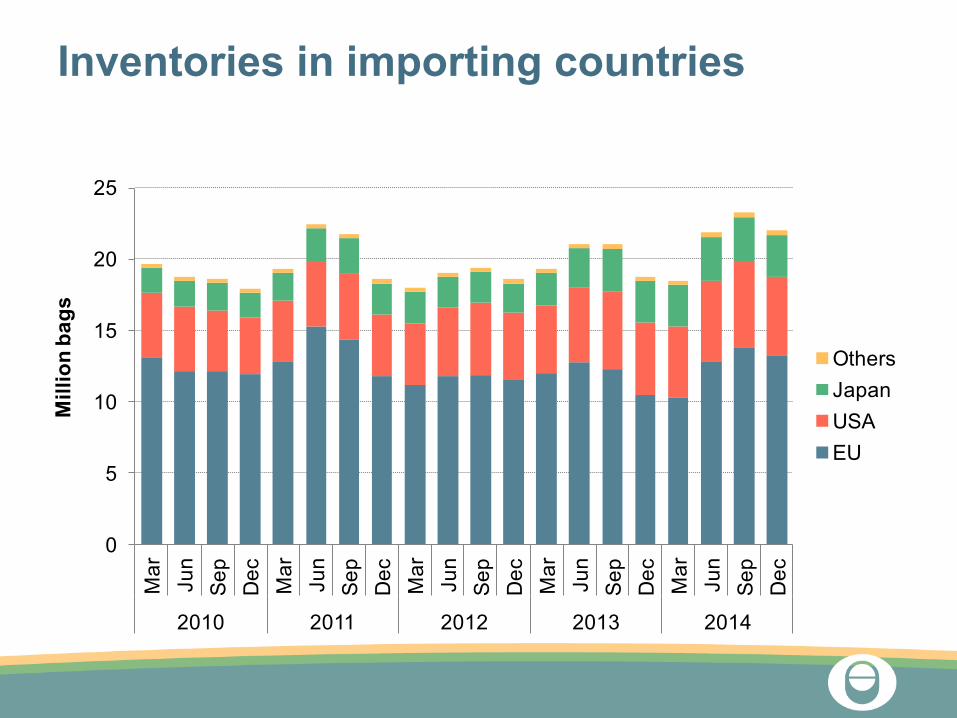

Inventories in importing countries

0

5

10

15

20

25

Mar

Jun

Sep Dec Mar

Jun

Sep Dec Mar

Jun

Sep Dec Mar

Jun

Sep Dec Mar

Jun

Sep Dec

2010 2011 2012 2013 2014

Mill

ion

bags

OthersJapanUSAEU

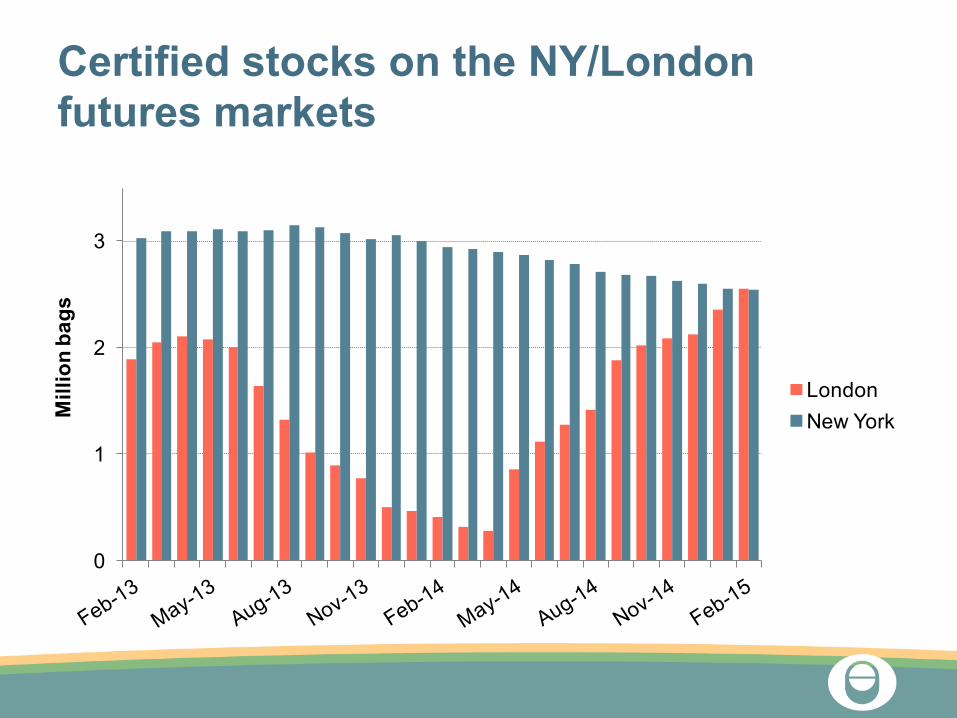

Certified stocks on the NY/London futures markets

0

1

2

3

Mill

ion

bags

LondonNew York

Conclusions

Global deficit in 2014/15, after two consecutive

surpluses

Accumulation of stocks will help supply the

market for now

But this cannot be maintained indefinitely, and will put pressure on

prices

Thank you