Embed Size (px)

Citation preview

Dexia Annual Report 2001

1

Business Profile .......................................................................................... p. 2

Message from the Chairmen .................................................................... p. 4

Financial Highlights .................................................................................... p. 6

Organization, Corporate Governance and Management........................ p. 8

Corporate Spirit .......................................................................................... p. 24

Shareholders’ Review ................................................................................ p. 28

Businesses

Know-how and Expertise, Public / Project Finance

and Credit Enhancement............................................................................ p. 38

Availability and Service, Retail Financial Services .................................. p. 50

Professionalism and Discernment, Investment Management Services.. p. 58

Mastery and Creativity, Capital Markets and Treasury Activities .......... p. 66

Anticipation and Control, Risk Management .......................................... p. 70

Financial Performance ................................................................................ p. 78

Where to find Dexia .................................................................................. p. 86

Contents

>>>>>>

>

>>>

>>>

The “Annual Report 2001” and the “Accounts and Reports 2001” together constitute the annual report of the Dexia holding company.

Foreign exchange rates

1 EUR =40.3399 LUF6.55957 FRF40.3399 BEF1.95583 DEM1,936.27 ITL166.386 ESP13.7603 ATS2.20371 NLG200.482 PTE

The foreign exchange ratesapplied between the euro andother currencies are the rateson December 31, 2001.

The foreign exchange ratesapplied between the euro andEuroland currencies are theofficial exchange rates set onDecember 31, 1998.

1 EUR =

0.8813 USD7.4365 DKK

3.853659 ILS9.3012 SEK0.6085 GBP42.78 SKK

>

>

Creative concept

Dexia’s Annual Report 2001 illustrates the Group’s fundamental values, which are shared and lived

by its 25,800 employees in 25 countries. These values, which cut across the different business lines

and nationalities, give Dexia its specific character. The Group’s personality is shaped by six

complementary values which interact and support one another – performance, balance, expertise,

enthusiasm, innovation and discipline.

Business Profile

Public / Project Financeand Credit Enhancement

Retail Financial Services

Investment Management Services

Capital Markets and Treasury Activities

World leader MARKET SHARE: 17% in Europe 25% in the United States

Second largest in Belgium, third largest in Luxembourg

MARKET SHARE: 24% in Belgium 13% in Luxembourg

RATING FROM AA TO AAA

Active in 25 countries, with a solid base in Europe, Dexia has implemented a

growth strategy focused on creating value since it was founded. With high

profitability in all its lines of business, Dexia applies a strict oversight policy that

allows it to keep a low risk profile.

Customized financial arrangements, long-term loans, creditenhancement, account management, investment and insuranceproducts – Dexia provides its public-sector clients with a fullrange of products and services adapted to their specific needs.

Responding to the financing, savings and insurance needs of itsretail banking customers by offering them diversity andperformance is one of the priorities of Dexia’s network of branches.Besides a strong position in Belgium and Luxembourg, the Groupalso develops this line of business in the Netherlands through DexiaBank Nederland, a company formed by the merger of Labouchereand Kempen&Co and in Slovakia, through Prvá Komunálna Banka.

Offering its private and institutional clients quality financialmanagement services (private banking, asset management, fundadministration and equity-related activities), Dexia confirms itsposition as one of the eurozone’s main banking groups active inthis sector.

Operating in many international financial markets, Dexia is arecognized player in the capital markets with expertise thatbenefits both the Group, for its refinancing needs, and its clients.

(1) Long-term, including off-balance sheet items.(2)Excluding Artesia BC.(3)PV of gross premiums collected by Financial Security Assurance in the United States.

New loans (1) (2): EUR 30.5 billion + 16.1%

Outstanding commitments (1): EUR 154.4 billion + 1.9%

Credit enhancement(3): EUR 790 million + 55.4%

Customer deposits and investment products:

EUR 79.7 billion + 34.7%

Outstanding customer loans: EUR 20.7 billion + 45.5%

Insurance premiums: EUR 1.9 billion + 95.3%

Assets under management: EUR 82.8 billion + 48.1%

Private banking client assets: EUR 37.5 billion + 22.2%

Administered funds(managed as a custodian bank): EUR 99.7 billion + 1.8%

Volume of long-term refinancing EUR 23.8 billion

of which EUR 13.3 billion in bonds rated AAA

Created in 1996, in anticipation of the introduction of

the euro, Dexia is a profoundly European banking

group. Very rapidly, it succeeded in developing an

authentic European identity beyond the diversity of the

national cultures of its 25,800 employees. As a forward-

looking banking group that has always been a pioneer,

Dexia is, of course, proud that the long awaited single

currency is today a reality for the 400 million citizens of

the European Union. The euro is the major event in

Europe at the beginning of the 21st century, and the

continent must benefit from this spectacular success to

pursue its integration and, in particular, its institutional

and fiscal reforms.

The year 2001 was the scene of major upheavals in the

world economy, from the bursting of the Internet

bubble to the decline in the financial markets and the

general economic slowdown which occurred after the

tragic events of September 11, 2001. The serenity that

characterized western economies at the end of the last

century gave way to uncertainty in 2001. In particular,

the financial markets became more chaotic and the

world’s stock exchanges recorded violent fluctuations.

In this turbulent environment, the group nevertheless

continued to grow and succeeded in posting good

results.

Dexia has expanded significantly over the last few years,

especially through external growth, by making many

acquisitions in Europe and the United States. This

development assures the Group of a strong presence

in Europe and throughout the world in its various

business lines. After the acquisition of Financial Security

Assurance (FSA) in the United States in 2000, a move

which allowed Dexia to become the world leader in

financial services to the public sector, the Group focused

on external growth in 2001 to develop its activities

in its two other businesses, Retail Financial Services

and Investment Management Services. Through the

acquisition of the Artesia Banking Corporation group

in Belgium, Dexia became a leader in bancassurance

in that national market. The merger in Belgium of Dexia

Bank and Artesia BC is currently moving forward, and

their new legal status was confirmed on April 1, 2002.

The acquisition of Kempen&Co. in the Netherlands,

followed by its merger with Bank Labouchere to form

Dexia Bank Nederland, makes Dexia a leading player

in Investment Management Services in Europe.

Today, Dexia aims to integrate its many acquisitions.

The company’s Board of Directors is proud to promote

the best practices in corporate governance. It has

created three specialized committees which report

regularly. These committees assure the Board of

objective and independent oversight of the Group’s

business and operations. At the six meetings it held in

2001, the Board of Directors approved Dexia’s growth

strategy, which should allow Dexia to pursue its

harmonious development in order to play a major role

in the Europe of tomorrow and more generally in the

world of banking, while continuing to increase its

profitability under strict conditions of risk management

and, as it has done in the last six years, create value for

its shareholders.

François Narmon,Chairman of the Board of Directors

Message from the Chairmen

Dexia Annual Report 2001

4/5

Pierre Richard,Chief Executive Officer, Chairman of the Management Board2001 was once again a decisive year in Dexia’s development.

The Group truly moved up to another echelon as a result of

significant strategic external growth that has enabled Dexia

to figure in the principal international stock market indices and

to be recognized by investors throughout the world. With stock

market capitalization of approximately EUR 20 billion, Dexia is

now one of the top ten banking groups in the eurozone.

The Group had already strengthened its activities in 2000 in

public finance and credit enhancement through the acquisition

of a specialized insurance company in the United States,

Financial Security Assurance (FSA). Dexia is now the world

leader in this sector. The acquisition of Artesia Banking

Corporation in Belgium and of Kempen&Co. in the Netherlands,

which merged at the end of the year with Bank Labouchere to

become Dexia Bank Nederland, allowed Dexia to assume a new

dimension, that of a leading player in the European banking and

financial industry.

The integration of these new companies into the Group was

a major focus and it mobilized the efforts of all the employees

involved, in particular with regard to the merger of Dexia Bank

and Artesia Banking Corporation. A dozen work groups made

rapid progress on several fronts, including the merger of the

trading rooms, the creation of a single IT platform and the

reorganization of the departments at headquarters. The year

2002 will be particularly dedicated to the integration of the

banking networks in Belgium in order to offer the Group’s

expanded customer base a coherent range of quality products

and services.

At the same time, and to deal with these new priorities, Dexia

reinforced its management team by drawing in the reins at the

level of the Management Board. The sovereign functions of

general audit, compliance, risk management, management

control and the management of executive officers are now

centralized, without however breaking with the entrepreneurial

spirit that exists in all of the Group’s businesses and constitutes

the force of the operating subsidiaries, which are fully responsible

for day-to-day management.

The pursuit of Dexia’s growth strategy once again produced

positive results in 2001. Despite a particularly difficult economic

and financial environment, the Group reported significant growth

in results for the thirteenth year in a row since it began to be

traded on the stock exchange, with net income of EUR 1,426

million, up 42.5% from 2000. Earnings per share increased

by 9.1%, in line with the Group’s objective to double this figure

between 1999 and 2005. Return on equity rose for the fifth

consecutive year to 18.7%, again in line with the Group’s

medium-term objective of 20%. The cost-control measures

implemented in all of the Group’s entities allow the Group to

confirm its commitment for 2002 with confidence – this year,

operating expense on a constant basis should be less than in 2001.

Dexia again confirmed its profile, that of European banking

group specialized in three of business lines which make a

balanced contribution to its results. The Group is in excellent

shape with a solid capital base and a low risk profile. Its principal

characteristic is to offer its shareholders predictable prospects for

growth in income.

Backed by the enthusiasm of its 25,800 employees in 25 countries,

whom I here want to thank for what they have accomplished,

Dexia intends to pursue its growth strategy with confidence and

dynamism. In 2002, the Group’s results should continue to grow.

Dexia will thus remain one of the leading European banking

groups that create the most value.

4/5

Cost/incomeratio

Balance sheet total

Financial Highlights

Total regulatorycapital

Tier I ratio

Net income Return on equity(ROE)

Capital adequacy ratio

186 199 245258

351

11.9

7.2

8.6

7.7

EUR billion

528605

761

1,001

1,426

13.214.0

15.7

17.7

18.7

56.356.1

53.9

55.1

59.5%

14.4 13.0

12.8

9.811.5

10.2

9.6

9.09.3 9.3

19992000

20011998

1997

EUR billion

% %

EUR million

%

19992000

20011998

19971999

20002001

19981997

19992000

20011998

1997

19992000

20011998

19971999

20002001

19981997

19992000

20011998

1997

V

7.7

Long-term ratings2

Dexia Dexia Dexia FSA Dexia Bank Crédit Local BIL MA

Moody’s Aa2 Aa2 Aa2 Aaa Aaa

Standard & Poor’s AA AA AA AAA AAA

Fitch AA+ AA+ AA+ AAA AAA

Customer deposits anddebt securities1

Total outstandingloans1

Stock marketcapitalization

Earningsper share

EUR billion

136.6

179.2

143.8 100.6

128.5

134.4

156.4

106.0

8.4

12.7

18.818.9

10.10.75

0.981.15

1.25

0.85

EUR billion EUR

EUR billion

19992000

20011998

19971999

20002001

19981997

19992000

20011998

19971999

20002001

19981997

186.8

224.9

Dexia Annual Report 2001

8/96/7(1) Outstanding loans on the balance sheet(2) As of December 31, 2001(3) Including the branch network of Dexia Bank Belgium and of Artesia Banking Corporation

Workforce3

25,838 employees, including:

ab in Belgium3 16,363

ab in France 2,211

ab in Luxembourg 3,134

ab International 4,130

Organization,Corporate Governance

By its location in Brussels, in the heart of the

European Union office district, Dexia’s head office

and its counterpart in Paris, the Crystal Tower,

symbolize the Group’s European identity. Half of

the staff of the holding company, Dexia Group,

works in Brussels, and the other half in Paris,

thereby respecting Dexia’s French and Belgian

roots.

Board of Directors

As of December 31, 2001, Dexia’s Board of Directors is

composed of twenty members, seven of whom (more than

a third) are independent. Dexia’s Board of Directors reflects

the Group’s European identity – five nationalities are

represented. Its composition is also in line with Dexia’s

French-Belgian corporate structure. It counts an equal

number of Belgian and French members, with each

nationality representing at least a third of the Board.

Dexia has implemented corporate governance since the Group was created in 1996, and has made it a

priority to apply best practices by adapting or modifying its organization, discipline and regulatory

guidelines to comply with the many recent developments in this area. Dexia aims to spearhead progress

in the field of corporate governance at the international level to ensure shareholders of comprehensive

oversight and transparency.

and Management

Dexia Bank BelgiumHeadquarters : Brussels

Dexia Crédit LocalHeadquarters : Paris

Financial Security AssuranceHeadquarters : New York

Dexia Bank NederlandHeadquarters : Amsterdam

Dexia Banque Internationale à LuxembourgHeadquarters : Luxembourg

100%

8.4% 22.2%

65.7%

69.3%

5.8%

90%

100% 10%

28.4%

Dexia Annual Report 2001

8/98/9

)

Corporate

Board of Directors as of December 31, 2001(1)

Beginning and Prime Other functionsend of mandate function

François Narmon 1996-2002 Chairman of the Chairman of the Board of Directors:67 years old Board of Directors, Dexia - Dexia BIL Belgian - DVV Insurance

Member of the Strategy Committee Chairman:and the Compensation Committee - Belgian Olympic and Interfederal CommitteeHolds 7,000 Dexia shares Member:

- International Olympic Committee

Pierre Richard 1996-2002 Group Chief Executive Director:60 years old Officer and Chairman of the - Crédit du NordFrench Management Board, Dexia - Le Monde

Member of the Strategy Committee - Air FranceHolds 20,000 Dexia shares - European Investment Bank

- Generali France Holding

Gilles Benoist 1999-2006 Chairman of the Executive Member of the Executive Board:55 years old Board, CNP Assurances - Groupe Caisse des depôtsFrench Member of the Supervisory Board:

Member of the Audit Committee - CDC IXIS

Philippe Bourguignon 1999-2006 Chairman of the Executive Director:53 years old Board, Club Méditerranée - eBayFrench Member:

Member of the Compensation Committee - Mouvement des entreprises de FranceIndependent director Former Chief Executive Officer:Holds 2,350 Dexia shares - Euro Disney

Rik Branson 2001-2002 Chairman of the Executive Chairman of the Executive Committee:57 years old Committee, Arcofin - Arcopar Belgian - Arcoplus

Member of the Strategy Committee - AuxiparCensor:- National Bank of Belgium

Thierry Breton 2000-2007 Chief Executive Officer and Director:46 years old Chairman, Thomson and - Schneider Electric French Thomson Multimedia - Rhodia

Independent director - Bouygues TélécomHolds 1,230 Dexia shares Member of the Supervisory Board:

- AXA

Guy Burton 2001-2003 Chief Executive Officer Chairman of the Board of Directors:53 years old Société Mutuelle - Union des associations Belgian des Administrations d’assurance mutuelle

Publiques - Belfinance

François-Xavier deDonnéa de Hamoir 1996-2002 Municipal Councillor,60 years old Brussels CityBelgian

Member of the Strategy CommitteeHolds 700 Dexia shares

Karel De Gucht 1996-2002 Municipal Councillor, Director:47 years old Berlare - Gemeentelijk Havenbedrijf AntwerpenBelgian

Member of the Strategy Committee

Didier Donfut 1999-2006 Burgomaster, Vice-Chairman45 years old Frameries of the Board of Directors:Belgian - Société Publique d’Électricité

Holds 500 Dexia shares

(1) Article 2 of the law of August 6, 1931 (M.B. August 14, 1931) forbids ministers, former ministers and State ministers, as well as members and former membersof Legislative Assemblies to mention their status as such in acts and publications of profit-making companies.

Ingénieur commercial (degree similar toMBA). Joined Crédit Communal in1957. Chairman of the ManagementCommittee of Crédit Communal (thenof Dexia) from 1979 to 1999. Co-Chairman of the Dexia group from 1996to 1999. Chairman of the Board ofDirectors of Dexia since 1999.

Studied at the Ecole polytechnique, Ecolenationale des Ponts et Chaussées andPennsylvania University. Chairman ofthe Executive Board of Crédit Local deFrance in 1987. Chief Executive Officer in1993. Co-Chairman of the Dexia Groupfrom 1996 to 1999. Since 1999, ChiefExecutive Officer of the Dexia Group andChairman of the Management Board.

Law degree. Graduate from the Institutd’Etudes Politiques and the Ecole Nationaled’Administration. Appointed SecretaryGeneral of Crédit Local de France in 1987.Member of the Executive Committee of Caissedes dépôts et consignations from 1993 to 1998.

Trained as an economist. Before joiningClub Méditerranée, he was ChiefExecutive Officer of Euro Disney, as wellas Executive Vice-Chairman of The WaltDisney Company (Europe).

Degree in economics. Worked in severalcapacities at the Regional InvestmentCompany of Flanders between 1980 and1989. Joined the Arco group in 1989, andbecame Chairman of the ExecutiveCommittee in 1992.

Engineer. Chief Executive Officer of theCGI group from 1990 to 1993. ExecutiveChairman and Vice-Chairman of theBoard of Directors of the Bull group from1993 to 1997. President of the Universitéde Technologie in Troyes.

Law degree. Joined Société Mutuelle desAdministrations Publiques in 1974.Appointed General Secretary in 1991 andChief Executive Officer in 1995.

Degree in Commercial and FinancialSciences (University of Louvain) Masterin Business Administration (Universityof California at Berkeley) HonoraryProfessor at the University of Louvain.Active in Belgian politics since 1981.

Law degree. Lawyer from 1976 to 2000.Active in national politics. TeachesEuropean law at the Vrije UniversiteitBrussel.

Ingénieur commercial (degree similar toMBA). Active in national politics and theBelgian energy sector. Burgomaster ofFrameries since 1992.

governance10/11

Beginning and Prime Other functionsend of mandate function

Denis Kessler 1999-2006 Chairman, Executive Vice-Chairman:49 years old FédérationFrançaise - Mouvement des Entreprises de FranceFrench des Sociétés d’Assurances Member of the Supervisory Board:

Member of the Strategy Committee - BNP ParibasIndependent director Member:Holds 1,000 Dexia shares - Commission Economique de la Nation

Daniel Lebègue 1998-2004 Chef executive officer, Director:58 years old and Chairman, - Thales French Caisse des dépôts - CNP

Member of the Strategy Committee et consignations - Gaz de France- C3D

André Lévy-Lang 2000-2006 Director, Director:64 years old AGF - SchlumbergerFrench - Fondation pour la recherche médicale

Member of the Strategy Committee Former Chairman of the Executive Board:Independent director - ParibasHolds 38,000 Dexia shares Professor:

- Université Paris-Dauphine

Roberto Mazzotta 2001-2002 Chairman, Banca Vice-Chairman of the Board of Directors:61 years old Popolare di Milano - Associazione Bancaria ItalianaItalian Director:

- Associazione Nazionale Banche Popolari

Theo Rombouts 2001-2002 Chairman of the Board of Chairman:60 years old Directors, Arco group - ACW Belgian - Institut Supérieur du Travail

- Conseil Fédéral pour le Développement Durable

Gaston Schwertzer 1999-2006 Doctor of law69 years old Companies DirectorLuxembourg

Member of the Compensation CommitteeIndependent directorHolds 55,660 Dexia shares

Anne-Claire Taittinger 2001-2007 Chairman of the Executive Chief Executive Officer:52 years old Board, Société du Louvre - - BaccaratFrench Groupe du Louvre - Société Immobilière de la Tour La Fayette

Independent director Director:Holds 850 Dexia shares - Marengo

Director:Marc Tinant 2001-2002 Member of the Executive - Arcopar 47 years old Committee, Arcofin - Arcoplus Belgian - Auxipar

Member of the Audit Committee Chief Executive Officer and Vice-Chairmanof the Board of Directors:- EPC

Sir Brian Unwin 2000-2006 Honorary President, Chairman:66 years old European Investment Bank - European Centre for Nature ConservationBritish Director:

Independent director - English National Opera CompanyMember:- British Institute of Management

Pieter Paul 1999-2006 Chairman, Director:Van Besouw Bank Nederlandse - Nederlandse Vereniging van Banken55 years old Gemeenten Commissioner:Dutch - N.V. Trustinstelling Hoevelaken

Member of the Audit Committee Secretary-General:Holds 10,760 Dexia shares - Centre international pour le crédit communal

Observer: Observer Burgomaster of GhentFrank Beke 1996-200154 years old Director:Belgian 2001-2002

Holds 1,400 Dexia shares

Degrees in political science, economicsand philosophy. Member of the Conseiléconomique et social, the EuropeanInsurance Committee and the ConseilNational des Assurances.

Law degree. Graduate from the EcoleNationale d’Administration. Before joiningCaisse des dépôts et consignations in 1997,he was a member of the Board of Directorsand Vice-Chairman of Banque Nationale deParis. Chairman of the Board of Directorsof the Institut d’Etudes Politiques in Lyon.

Graduate from the Ecole Polytechniqueand Ph.D. in Business Administrationfrom Stanford University. After workingas Chairman of the Executive Board ofParibas, he is now a member of theBoards of Directors of several compa-nies and a professor at the University ofParis-Dauphine.

Trained as an economist. Former profes-sor at the University of Genoa. Active inpolitics for 20 years. Began his bankingcareer in 1987.

Law degree and degree in economics.Before becoming Chairman of ACW, hewas Chief Executive Officer of theRegional Development Company ofAntwerp. Member of the Board ofDirectors of the Fondation Roi Baudouin.

Law degree. Long active in the gas indus-try. Member of the Board of Directors ofDexia BIL since 1984. Honorary Consulof the Republic of Nicaragua.

Graduate from the Institut d’EtudesPolitiques de Paris. Before becomingChairwoman of Société du Louvre -Groupe du Louvre, she was successivelySecretary General, Deputy ChiefExecutive Officer and Chief ExecutiveOfficer.

Master’s degree in economics. Beforejoining the Arco group in 1991, he wasgeneral advisor to the ExecutiveCommittee of the Regional InvestmentCompany of Wallonia.

Studied at Oxford and Yale. Worked as adiplomat and held several positions atthe Finance Ministry and on the PrimeMinister’s staff in the United Kingdom.Appointed Chairman of the EuropeanInvestment Bank in 1993. HonoraryChairman since 2000.

Economist and specialist in informationtechnology. After working for NCRNederland and Elsevier, he joined BankNederlandse Gemeenten in 1985. Hebecame Chairman of the ExecutiveCommittee in 1992.

Degree in philology and com-munication sciences. Beforebecoming Burgomaster ofGhent in 1995, he was a munic-ipal councilor and alderman.

10/11

Independent members of the Boardof DirectorsThe Board of Directors counts seven independent members,

representing a third of the Board: Anne-Claire Taittinger,

Thierry Breton, Philippe Bourguignon, Denis Kessler,

André Lévy-Lang, Gaston Schwertzer and Sir Brian Unwin.

The criterion of independence is based on the definition

given in the Viénot II white paper according to which

directors are considered to be independent if they have no

relation whatsoever with the company or the Group which

may compromise their impartial judgment. In any case,

and notwithstanding the general character of the above-

mentioned rule, members of the Board cannot be considered

to be independent if they represent a reference shareholder

and/or exercise executive functions in the company

or a Group entity.

Non-executive membersof the Board of DirectorsNon-executive members of the Board of Directors exercise

no management functions in the company or any of its

subsidiaries. Except for Pierre Richard, who is both Chief

Executive Officer and Chairman of the Management Board,

the other members of the Board of Directors are all non-

executive members.

Responsibilities of the Boardof DirectorsThe Board of Directors determines the strategic objectives

and the general policy of both the holding company

and the Group. It oversees and sets guidelines for

management. The Board of Directors appoints the members

of the Management Board, approves the measures required

to achieve the strategic targets it defines, monitors

implementation of the company’s management and control

programs, and reports to shareholders.

Operation of the Board of DirectorsThe Board of Directors met six times in 2001. The rate of

attendance at Board meetings was 85.3%.

Since its creation in 1999, the Board of Directors has operated

according to a code of internal rules. Amended on several

occasions, these rules and recommendations are designed

to guarantee the full exercise of power by the Board

of Directors and to optimize the contribution of each member

of the Board. The code defines the rights and obligations of

the members of the Board in the exercise of their mandate,

operating and evaluation guidelines, relations with the

Management Board and the organization and operation of the

Board’s specialized committees.

In addition to statutory appointments, the Board primarily

addressed the following issues in 2001:

>

>

>

>

Corporate

Dexia Annual Report 2001

12/13

… discussion and approval of the parent-company and

consolidated financial statements and the 2000 business

results;

… discussion and approval of the Dexia Group’s budget for

2001;

… acquisition of Artesia BC (approval of the acquisition,

capital increase and merger);

… acquisition of Kempen&Co (approval of the acquisition

and merger);

… Dexia share split;

… approval of the protocol relating to Dexia’s prudential

control;

… employee share issue and stock option plan for 2001;

… reorganization of the Group’s internal audit and

compliance units;

… interim reports by the Audit Committee.

Each quarter, the Chief Executive Officer reports to the Board

of Directors on the activities of the different entities and their

subsidiaries. The report is organized around the Group’s three

business lines and gives a detailed picture of Dexia’s position

in these sectors.

Internal assessmentIn 2001, the Board of Directors conducted an evaluation of its

operations by means of a questionnaire that was sent to each

member of the Board. Overall, the Board members said they

were satisfied with the pertinence and quality of the

information provided. They decided to reinforce the role of

the Audit Committee to allow it to deal with cross-division

topics in addition to auditing the accounts. It also approved

the creation of a committee to prepare for the appointment

of a certain number of Board members in 2002.

Compensation of the membersof the Board of DirectorsEach member of the Board of Directors receives annual

compensation of EUR 30,000 for a full calendar year.

This amount was determined at the Annual Shareholders’

Meeting of May 10, 2000. For members of the Board

who have not held their positions for a full year, this amount

is reduced on a prorata basis according to the number of

quarters actually worked. The Chief Executive Officer receives

no compensation as a member of the Board of Directors, but

is paid for his contribution as Chief Executive Officer and

Chairman of the Management Board.

The Directors together hold 138,050 shares.

>

>

governance

Specialized committeesThe Board of Directors has three specialized committees

which report on a regular basis. These committees assure

the Board of objective and independent oversight

of the Group’s business and operations.

Strategy CommitteeThe Strategy Committee is composed of eight members of the

Board of Directors, including the Chairman and the Chief

Executive Officer.

… François Narmon, Chairman of the Board of Directors

… Pierre Richard, Chief Executive Officer

… André Lévy-Lang (independent member of the Board)

… Denis Kessler (independent member of the Board)

… François-Xavier de Donnéa de Hamoir

… Karel De Gucht

… Daniel Lebègue

The Strategy Committee meets annually to review the Dexia

Group’s strategic position and study its further development.

In 2001, this meeting took place on June 22.

The Strategy Committee may also be convened at any time

upon the initiative of the Chief Executive Officer to discuss

market-sensitive issues before they are presented to the Board

of Directors. In 2001, the Strategy Committee met on

March 9 and May 2 to discuss, respectively, the acquisition

of Artesia BC and of Kempen&Co.

No compensation is paid to the members of the Strategy

Committee for their work on this committee.

The Audit CommitteeThe Audit Committee is composed of Gilles Benoist,

Marc Tinant and Pieter Paul Van Besouw. It assists the Board

of Directors in the exercise of its mission to oversee

the business and management of the Dexia Group. It verifies

that Dexia’s parent company and consolidated financial

statements (including Dexia Bank Belgium and Dexia Crédit

Local) are accurate and fairly stated. In particular,

its responsibilities involve analyzing the financial information

and accounting procedures and examining the conclusions,

comments and recommendations of the auditors.

In this connection, it may suggest that additional studies

be conducted. As well, it verifies the annual and semiannual

financial statements before they are approved by the Board of

Directors and published. The committee also gives advice on

the appointment of the auditors proposed to the shareholders’

meeting.

It verifies the existence and implementation of risk

management and control procedures for credit, market

and operating risks. To this end, the Audit Committee

oversees internal audit operations, in particular through

meetings with the Group’s audit division which presents

the conclusions of the audits conducted, the main files

analyzed and, more generally, for the Management Board,

a report on internal control procedures throughout the Group.

It may request complementary audit reports.

It also ensures compliance with regulations issued by stock

market authorities. In addition, the Audit Committee

is consulted on compliance rules in force throughout the Group.

>

…

…

Corporate

Dexia Annual Report 2001

14/15

The Audit Committee meets at least three times per year.

In 2001, meetings were held on March 8 and September 7,

and a third meeting to discuss the 2001 fiscal year took place

in January 2002.

The main subjects reviewed in 2001 included the following:

… Group financial statements and results as of

December 31, 2000, and June 30, 2001;

… 2001 report on oversight within the Group;

… 2001 report on internal audit activities in Group entities;

… 2001 report on risk assessment and management;

… organization and operation of internal audit activities

in the Group and updating of the Group’s audit charter;

… organization and operation of compliance in the Group

and introduction of a compliance charter for the Group;

… steering committees for the merger of Artesia BC and

Dexia Bank;

… operating risks linked to market activities.

No compensation is paid to the members of the Audit

Committee for their work on this committee.

Compensation CommitteeThe Compensation Committee is composed of members

of the Board, two of whom are independent – François

Narmon, Philippe Bourguignon (independent) and

Gaston Schwertzer (independent).

The committee’s role is to determine the amount and

nature of the compensation to be paid to the Chairman

of the Board of Directors and the Chief Executive Officer,

as well as, on the basis of the proposal of the Chief Executive

Officer, to the members of the Management Board

and of the subsidiaries’ executive committees. In addition,

the Compensation Committee decides how stock options are

to be granted in application of the general principles defined

by the Board of Directors. It makes recommendations on the

compensation of the members of the Board of Directors and

employee profit-sharing.

The Committee met three times in 2001. It discussed

the following subjects:

… guidelines for the 2001 stock option plan;

… proposals for the fixed and discretionary compensation

of the Chief Executive Officer, the members of Dexia’s

Management Board, the members of the Management

Board of Dexia Bank, Dexia BIL and Dexia Crédit Local;

… comparative analysis of the compensation of the members

of Dexia’s Management Board; regulations governing the

2001 capital increase reserved to employees.

…

governance

Corporate

Management

Management BoardThe Management Board is composed of a maximum

of eight members. They are appointed and removed

from office by the Board of Directors acting on

the recommendation of the Chief Executive Officer.

In the framework of the strategic objectives and general

policy guidelines defined by the Board of Directors,

the Management Board runs the holding company

and the Group and pilots the different business lines.

To this end, each member of the Management Board

is invested with operating responsibilities at the level

of the company or Group entities (by business, activity

or function).

The Management Board is chaired by the Chief Executive

Officer, whom the Board of Directors entrusts with the daily

management of the company and the implementation of the

decisions taken by the Board of Directors.

The Management Board meets at least once a week

and decides issues in a collegial manner under the authority

of the Chief Executive Officer.

Since its creation in 1999, the Management Board has operated

according to a code of internal rules. Amended on several

occasions, these rules and recommendations define its role and

mode of operation. The collegial decision-making process,

the Board’s powers and certain regulations governing the

status of members are also the object of specific provisions in

the protocol on the prudential control of the Dexia Group

signed with the Belgian Banking and Finance Commission.

>)

Management Board

Pierre Richard,

Chef Executive Officer,

Chairman of the Management Board

Chief Financial Officer;Vice-Chairman of the Supervisory Board,Dexia Crédit Local

Investment Management Services;Chairman of the Management Board,Dexia Banque Internationale à Luxembourg

Vice-Chairman of the Management Board;Retail Financial Services;Chairman of the Management Board,Dexia Bank Belgium

Chief Executive Officer;Chairman of the Management Board;Chairman of the Supervisory Board, Dexia Crédit Local;Vice-Chairman of the Board of Directors, Dexia BankBelgiumVice-Chairman of the Board of Directors, Dexia BanqueInternationale à Luxembourg

General Counsel;Member of the Management Board, Dexia Bank Belgium

Public/Project Finance and Credit Enhancement;Chairman of the Management Board,Dexia Crédit Local

Capital Markets and Treasury Activities

From left to right:

Rembert von Lowis

Marc Hoffmann

Luc Onclin

Pierre Richard

Axel Miller

Jacques Guerber

Dirk Bruneel

governance

Dexia Annual Report 2001

16/17

Dexia Group holding company staffTo meet its operational needs, the Management Board relies

on a dozen small teams, 90 highly-educated people in all,

based in either Brussels or Paris. These teams are responsible

for ensuring and coordinating the Group’s vital functions,

especially in audit and oversight, risk management and

strategic planning, but also for defining and implementing

Dexia’s policies in corporate communications, human

resources, information technology, etc.

General audit activities are under the responsibility of

Alain Delouis (see page 20).

The strategic planning and management information unit

participates in the definition of Dexia’s long-term strategy.

Under the responsibility of Yves Guérit, this team, which

draws up Dexia’s preliminary budget, also monitors business

results and the profitability of the Group’s businesses.

Under Philippe Ducos, risk management defines, organizes

and manages the Group’s risk profile. It is also in charge

of adjusting and updating economic equity (see page 70).

Jacques Bellut coordinates Dexia’s activities in the capital

markets (see page 66).

The financial communication and investor relations unit,

directed by Robert Boublil, provides financial and strategic

information about the group to investors, financial analysts

and rating agencies.

Corporate communications, under the responsibility of

Françoise Lefebvre, enhances Dexia’s image with the general

public and particularly journalists, trendsetters and

individual shareholders.

Under the responsibility of Bernard-Franck Guidoni-Tarissi,

human resources and in-house communications develop

a group spirit and create a work community by implementing

a policy that fosters mobility, compensation, career

management and communication within the company.

Michel Van Schingen is responsible for information

technologies, which coordinates computer systems and tools

throughout the Group and ensures that they meet Dexia’s

strategic needs.

Xavier de Walque’s team manages and evaluates proposals

for mergers, acquisitions and sales, and studies the internal

reorganization of Dexia’s subsidiaries and affiliates.

The Chairman’s personal staff, under the management

of Mireille Eastwood, coordinates and monitors the activities

of the Chief Executive Officer and the Management Board

in cooperation with the secretary-general. This cell also

serves as an interface between the Group’s different units.

The secretary-general (Edouard du Roy de Blicquy) is in

charge of Dexia’s regulatory and legal organization. He is

responsible for the management of the Group’s cash reserves

and budgets as well as of logistics of the holding company in

cooperation with the Chairman’s personal staff.

>

Corporate

Management compensation

Management BoardCompensation for the members of the Management Board

is determined by the Board of Directors on the recommendation

of the Chairman of the Management Board and after approval

by the Compensation Committee.

In 2001, the Compensation Committee conducted a study on

the compensation of the members of the Management Board,

with the help of a specialized consultant, and its conclusions

were adopted by the Board of Directors.

The fixed portion of compensation is determined on the

basis of the nature and importance of the responsibilities

exercised by each member with a market benchmark for

comparable positions. The capped discretionary part is linked

to the Group’s performance, which is measured by the change

in earnings per share between 2000 and 2001. Members’

individual contributions to the company’s future success are

also taken into account.

The Chief Executive Officer received net compensation after

taxes and charges equivalent to EUR 490,500. This sum

corresponded to annual gross income of EUR 1,137,500. His

gross fixed compensation totaled EUR 750,000 and his

discretionary compensation was EUR 387,500.

The seven members of the Management Board (six members

in 2000) received a total of EUR 5.670 million in gross

compensation in 2001.

The members of the Management Board were granted

540,000 Dexia stock options in the framework of the

2001 stock option plan, of which 150,000 were granted

to the Chief Executive Officer.

Executive ManagementCompensation is reviewed once a year in the first quarter

for company managers in the Group’s different subsidiaries

in line with the general policy guidelines issued by

the respective compensation committees in compliance

with the recommendations of the Group’s Compensation

Committee.

Fixed salaries are determined on the basis of local market

benchmarks and individual levels of responsibility.

Discretionary compensation takes into account

the competitive practices observed in the Group’s different

business lines (financial markets, private banking, asset

management, retail banking, etc.). It also reflects individual

performance, which is assessed on the basis of the achievement

of the financial and business objectives set in the annual

budget process.

…

…>

Dexia Annual Report 2001

18/19

governance

Internal audit

Dexia has a consistent audit unit that respects the highest

standards. The audit unit was bolstered in 2001 to enable

it to promote internal control in the Group and to monitor

the performance and effective application of internal audit

procedures.

This focus expresses the Group’s determination to maintain

its reputation and guarantee the coherence and efficiency of

its structures as core values.

In this framework, the internal audit unit verifies that

the risks incurred by Dexia in its activities and in all its

entities have been identified, analyzed and sufficiently hedged.

Internal audit also promotes continuous improvement

in Group operations.

The organization of internal audit adopted at the end of 2000

is based on three fundamental principles:

… internal audit’s strategy, level of requirements and

operating rules are defined by the Management Board

in a framework approved by Dexia’s Audit Committee;

… internal audit functions are exercised by a network of

audit divisions which operate under the authority of the

Group’s general auditor, who reports directly to the Chief

Executive Officer and Chairman of the Management

Board;

… each audit division in company subsidiaries reports to

the chairman of the entity’s executive committee, and also

to the Group’s general auditor.

This new organization, which is more structured than in the

past, will also make it easier to integrate new entities into the

audit system.

The Group’s comprehensive approach to risks, the common

audit policies introduced and the reporting and tracking

procedures conducted at the level of the holding company

also contribute to the efficiency of Dexia’s internal control

system. Finally, a new audit charter has been drawn up.

After final approval by the Board of Directors, it will be

distributed to the Group’s employees to allow them to be fully

aware of the role and practices of internal audit in the Dexia

Group.

Compliance

Operating in the highly-regulated sectors of finance

and insurance, Dexia complies with all legal, regulatory

and prudential standards. Such compliance is one of the first

conditions of client confidence. Beyond respect for the letter

of the law, in 2001 the Group continued to implement

efficient oversight procedures.

In fact, Dexia’s reputation is also based on its efforts

to ensure the integrity of the Group as a whole and of

all the employees in their banking or insurance activities.

These ethical principles have been codified in a charter

drawn up in 2001 and submitted to the Group’s Management

Board and to the Audit Committee of Dexia’s Board of

)

)

Corporate

Dexia Annual Report 2001

20/21

Directors. The requirements defined in this framework aim

to match the highest standards in the financial world.

After approval by the bodies which represent the Group’s

operating entities, the charter will be distributed to the whole

workforce. The operating entities will be able to amend

the charter to integrate stricter local legal and regulatory

requirements.

Basic compliance principlesThe Dexia Group’s compliance policy is based on

the following principles:

… compliance with legal and regulatory requirements,

… professionalism and confidentiality,

… reliability and respect in dealing with clients,

… loyalty to the Dexia Group,

… mutual respect for people and opinions.

Each of the chapters presents the rules in force and gives

concrete applications.

Compliance proceduresOversight is an independent function that aims to ensure

the effective application of the compliance principles defined

by the Dexia Group. The definition, implementation and

updating of these principles are the responsibility of

compliance officers, who are named in the Group’s main

subsidiaries and who report to the Group’s chief compliance

officer. Correspondents are appointed in the other

subsidiaries, branches and representative offices.

Dexia’s chief compliance officer organizes regular meetings

with his counterparts in the three main operating entities to

monitor their activities, share information and experience

and seek appropriate solutions for the problems posed.

…

…

governance

Dexia employees are proud to participate in the construction of a company

that is a pioneer in many fields and has never stopped growing. In order to

enable its employees to benefit from the company’s growth and to reinforce

Enthus ias

Si meliora dies, ut vina, poemata reddit, scire velim, chartis pretium quotus arroget annus. scriptor abhinc annos centum quidecidit, inter perfectos veteresque referri debet an inter vilis atque novos Excludat iurgia finis, Est vetus atque probus,centum qui perficit annos. Deperiit minor uno mense vel anno.

Dexia rapport annuel 2001

14/15

the sense of belonging to a dynamic group, Dexia has introduced an

attractive employee shareholding plan.

m

22/23

As a result of sustained external growth, the

number of employees in the Group rose from

10,000 in 1996 to more than 25,800 at the end

of 2001. Working in 25 countries, the men and

women who make up Dexia are, for the most

part, located in Europe and particularly in

Belgium, France and Luxembourg, the three

countries in which the Group originally operated.

A priority at Dexia has always been to develop

a corporate spirit based on shared values,

to create a work community and to promote

commitment to the Group’s development

strategy. A major contribution is made by

the many projects conducted in cooperation

with the operating companies in the fields of

inhouse communications, human resources

and employee savings plans.

Corporate Spirit

Dexia Annual Report 2001

24/25

Informing and promotingcommitment

Convinced of the importance of in-house communications

in the building of a common culture, Dexia uses a variety

of tools to promote employee commitment to projects and

corporate strategy. Complementary to the information

channels utilized in the operating companies and developed

in cooperation with “local” internal communications teams,

these media tools keep employees up to date on what is going

on in the Group – news, strategy, work organization, social

events, businesses, etc. Three supports (a quarterly magazine,

a video magazine and an intranet site) develop a feeling

of belonging to a unified social structure with common

objectives. In order to be accessible to the greatest number,

these tools are produced in three languages: English, French

and Dutch.

Since the objectives of in-house communications and

of human resources are increasingly complementary,

it was decided to merge the two functions in 2002.

Ensuring their coherence represents a key step forward

in the implementation of a powerful, clearly defined strategy.

Portrait of the Group

The event of the year 2001 was, without a doubt,

the merger of the teams of Artesia Banking Corporation

and Dexia Bank in Belgium. The consolidation of other

companies, like Kempen&Co in the Netherlands, Ely Fund

Managers in the United Kingdom and Financière Opale in

France, also had an impact on the profile of the Group’s

staff. Altogether, no fewer than 9,600 employees came to

work for Dexia in 2001.

Geographic breakdown1

… Belgium2: 16,363

… Luxembourg3: 3,134

… France: 2,211

…The Netherlands: 1,729

… Slovakia: 623

… United States: 414

… Italy: 265

… Switzerland: 250

… Spain: 195

… United Kingdom: 164

… Ireland: 144

… Singapore: 81

… Germany: 67

… Monaco: 66

… Jersey: 34

… Denmark: 27

… Israel: 26

… Sweden: 17

… Australia: 17

… Other: 9

)

)

Gender breakdown (1) & (2)

ab44%56%

6,0327,478

)

(1) As of December 31, 2001(2) Employees of Dexia Bank Belgium, including Artesia

Banking Corporation, Dexia Crédit Local and Dexia BILonly

(1) As of December 31, 2001(2) Including the branch network of Dexia Bank Belgium and Artesia Banking

Corporation

Development and internationalmobility

One of the principal missions of the Group’s human

resources department is to ensure that Dexia has the staff

it needs to meet the challenges of tomorrow. To achieve

this objective, it is first necessary to identify the skills

required to further the Group’s strategy, to find people

who have the needed potential, to help them develop

the required know-how and, finally, to build career plans

that are adapted and motivating.

The Group’s human resources department thus introduced

a comprehensive process for managers who will be Dexia’s

executive officers tomorrow.

Launched in 2001, the Dexia Executive Assessment

Leadership (DEAL) project is the first stage in the process.

DEAL is based on a univocal system that is fair and objective.

It is now common to Dexia Bank, Dexia BIL and Dexia

Crédit Local and will be progressively extended to the other

Group entities. This development tool will make evaluation

criteria and career prospects more transparent for employees.

Training programs are also offered, particularly in management

and languages. More than 25% of the Group’s employees

work outside of the three countries in which Dexia first

operated (Belgium, France and Luxembourg) and some

14 different languages are spoken every day in the Group.

English has thus become the language of business and, in

particular, of the financial world in which Dexia operates.

“Discovering Dexia” programs were again organized

in 2001. These two-day training programs allow new

employees to meet and discover the organization and

history of the Group, its businesses and human resources

and communications policies.

Dexia gives special importance to international mobility,

which makes it possible to transfer certain know-how

from one entity to another. A passport for mobility was

introduced to serve as a reference document, defining

the procedures to be followed in the two types of mobility –

assignment and expatriation – and answering practical

questions concerning taxation, social security and housing.

Merger of Artesia BankingCorporation and Dexia Bank Belgium

In 2001, Dexia faced a major challenge in Belgium,

as it sets out to merge the teams of Artesia BC and Dexia

Bank. Although the merger of the two structures has begun

(for example, the trading rooms were merged at the end

of 2001), the process is not expected to be completed until

2005, with a major step in 2003.

Coordinated by an ad hoc committee composed of

representatives of the two entities’ executive committees,

the merger involved 14 project groups which piloted

approximately 75 work groups and a hundred sub-groups.

Altogether, the process required the active participation

of 600 to 700 people.

Specific information channels were developed and employed

to keep employees up to date on almost a daily basis

concerning the progress realized.

In addition, in order to make sure employees were treated

fairly in terms of job status, job stability, working conditions

and corporate culture, Dexia consulted and involved labor

representatives.

C o r p o r a

)

)

Age Men Women

Breakdown by age (1) & (2) Breakdown by seniority (1) & (2)

(1) As of December 31, 2001.(2) Employees of Dexia Bank Belgium, including Artesia Banking

Corporation, Dexia Crédit Local and Dexia BIL only.

(1) As of December 31, 2001.(2) Employees of Dexia Bank Belgium, including Artesia Banking

Corporation, Dexia Crédit Local and Dexia BIL only.

> 60

56-60

51-55

46-50

41-45

36-40

31-35

26-30

21-25

< 21

17

276

851

1,100

1,223

1,418

1,069

1,035

476

13

4

81

270

705

805

1,241

1,106

1,006

751

63

Age Men Women> 4036-4031-3526-3021-2516-2011-156-100-5

2

39

167

487

600

669

1,137

533

2,398

8

54

326

638

816

968

1,437

757

2,474

Dexia Annual Report 2001

26/27

Encouraging employee savings plans

The objectives of the employee shareholding plan launched

by the group in 2000 were to reinforce the feeling of

belonging to a socially unified group, involve employees

in the Group’s strategy and growth, and encourage

the creation of employee savings plans under favorable

conditions.

After the success of the first operation, the Board of

Directors decided, at the suggestion of the Management

Board, to launch a new plan in 2001. The second capital

increase reserved to employees was likewise successful.

Almost six out of ten employees subscribed Dexia shares

for a total of approximately EUR 167 million. The plan

was well received in Belgium, with subscribers representing

approximately 65% of total staff. In France, 72%

of the employees participated, while in the international

subsidiaries (excluding Belgium, France and Luxembourg),

participation increased by more than 50% over 2000.

Employees now own almost 2.3% of Dexia’s capital.

The objective targets 5% of the capital in employees’ hands

in five years.

Pioneer in European labor relations

Dexia’s European Works Council was set up in 1998.

It is composed of management representatives and

26 statutory employee representatives and 17 alternates

from seven Dexia entities.

The European Works Council is a forum for consultation

and the exchange of information. It meets twice a year,

alternately in Brussels and Paris, to study economic,

financial and labor questions, such as the employment

situation, business trends, major organization changes,

mergers and acquisitions.

In 2001, the European Works Council met in February,

June and December. The February meeting was dedicated to

the Group’s organization and the creation of Dexia

Financial Markets, the acquisitions made in 2000, IT

synergies and Internet strategy. In June, the agenda included

the introduction of the Group’s compliance charter, the

merger of Artesia BC and Dexia Bank, the Group’s financial

and labor situation and employee shareholding. Finally, in

December, the Works Council focused on the acquisition of

Kempen&Co. and decided to convene a work group to draw

up a Dexia labor charter which will be submitted

to management at the end of the first half of 2002.

The objective of such a charter is to set minimum labor

standards, primarily in terms of labor negotiations

and employment management, in all Group companies,

whatever the legislation in the individual country.

t e S p i r i t

) )

An information portal and data base as much as

a forum to share best practices, the Group’s

intranet system was launched at the beginning of

2001. This internal communications tool allows

employees to access the latest company news, the

price of Dexia shares in real time, financial

information, labor statistics, available job offers,

electronic press reviews and an employee

directory.

Creating value for both individual and

institutional shareholders over the long term

through regular growth in income is a priority

for the Dexia Group. For 13 years in a row,

earnings per share have grown more than 10%

per year, increasing regularly from one year to

the next.

Dexia is committed to transparency in its

relations with shareholders. To this end, the

Group develops and makes available a large

number of tools, involves shareholders in its

communications strategy via a European advi-

sory committee and organizes meetings on a

regular basis.

Shareholders’ Review

Dexia Annual Report 2001

28/29

) Shareholding structure

By the terms of the agreement signed by Dexia and Arcofin

on March 13, 2001, Arcofin transferred to Dexia on July 3,

2001, the shares it held of Artesia Banking Corporation

in exchange for new Dexia shares. Arcofin received

178,934,630 new Dexia shares through a reserved capital

increase. After this operation, Arcofin owned 15.34% of

Dexia’s capital. In keeping with the terms of the agreement,

Arcofin committed to support Dexia’s strategy fully and to

remain a stable shareholder of the Group for a period of at

least 18 months.

At the end of 2001, Dexia launched a second capital increase

reserved to its 25,800 employees in 25 countries. With six out

of ten employees subscribing, almost EUR 170 million were

invested. Subsequent to this operation, Dexia employees own

2.3% of the Group’s capital, versus 1.5% at the end of 2000.

Dexia counts approximately 400,000 individual

shareholders, mostly in Belgium and France, who own

13.9% of the Group’s capital.

As of December 31, 2001, Dexia’s equity totaled

EUR 4,684,744,917 and the number of shares

was 1,166,813,164.

Dexia and the stock market

Dexia shares are traded in the Euronext Paris and Euronext

Brussels markets as well as on the Luxembourg stock

exchange. With stock market capitalization of approximately

EUR 19 billion at the end of 2001, the Group ranks among

the twenty largest European banks and among the top ten

in the eurozone.

Dexia is included in the main European stock market indexes

– Euronext 100, FTSE Eurotop 100, MSCI Europe Banks,

Dow Jones EuroStoxx Banks, ASPI Eurozone and FTSE4

Good Europe and Global Index, as well as the CAC 40

in Paris and the BEL20 in Brussels.

Dexia share split After approval by the shareholders at the Extraordinary

Shareholders’ Meeting of June 6, 2001, Dexia divided

the par value of its share by ten. The exchange of one

share for ten shares began on June 14, 2001.

This division was also applied to VVPR strips, warrants

and certificates. The new share was quoted in Brussels

and Paris on June 18.

This operation increased the liquidity of the shares

and also facilitates the access of individual shareholders

to Dexia shares.

A difficult year for the stock market In addition to the global economic slowdown, the events

of September 11, the crisis in Argentina and the bankruptcy

of Enron adversely affected an already lackluster market

environment. In the United States, the Dow-Jones was

down 7.1% at the end of the year, its biggest decline since

1990, while in Europe, the Dow-Jones EuroStoxx50 index

fell 20.3%, the CAC 40 22.0% and the BEL20 8.0%.

)

41.25%

13.90% 15.34%

7.00%

5.17%

15.04%

>

>2.30%

As of December 31, 2001

Holding Communal

Institutionaland otherinvestors

SMAPgroup

Individual shareholders

Caisse desdépôts etconsignations

Arcofin

Dexia Group employees

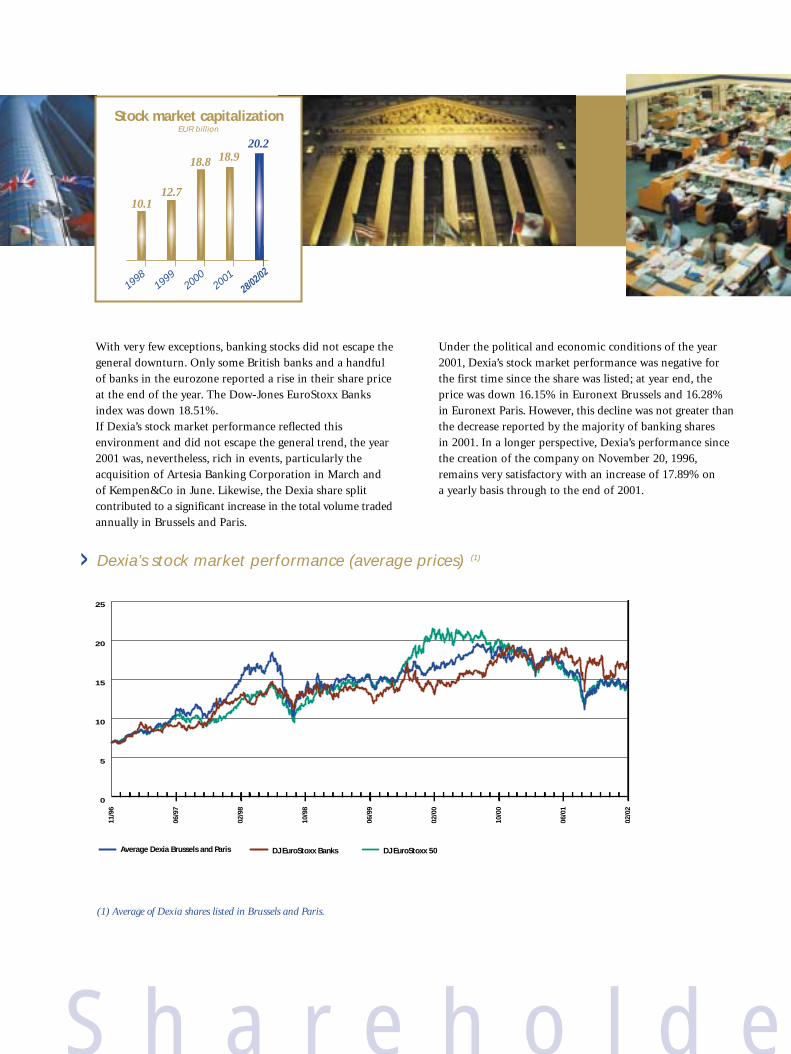

With very few exceptions, banking stocks did not escape the

general downturn. Only some British banks and a handful

of banks in the eurozone reported a rise in their share price

at the end of the year. The Dow-Jones EuroStoxx Banks

index was down 18.51%.

If Dexia’s stock market performance reflected this

environment and did not escape the general trend, the year

2001 was, nevertheless, rich in events, particularly the

acquisition of Artesia Banking Corporation in March and

of Kempen&Co in June. Likewise, the Dexia share split

contributed to a significant increase in the total volume traded

annually in Brussels and Paris.

Under the political and economic conditions of the year

2001, Dexia’s stock market performance was negative for

the first time since the share was listed; at year end, the

price was down 16.15% in Euronext Brussels and 16.28%

in Euronext Paris. However, this decline was not greater than

the decrease reported by the majority of banking shares

in 2001. In a longer perspective, Dexia’s performance since

the creation of the company on November 20, 1996,

remains very satisfactory with an increase of 17.89% on

a yearly basis through to the end of 2001.

DJ EuroStoxx Banks DJ EuroStoxx 50Average Dexia Brussels and Paris

0

5

10

15

20

25

11/9

6

06/9

7

02/9

8

10/9

8

06/9

9

02/0

0

10/0

0

06/0

1

02/0

2

Dexia’s stock market performance (average prices) (1)

Stock market capitalization EUR billion

12.7

18.8

19992000

200128/02/02

18.920.2

10.1

1998

(1) Average of Dexia shares listed in Brussels and Paris.

S h a r e h o l d e

>

Dexia Annual Report 2001

30/310

18,000,000

36,000,000

54,000,000

72,000,000

90,000,000

0

18000000

36000000

54000000

72000000

90000000

CAC 40 Total daily trading volume (monthly average)Dexia

11/9

6

06/9

7

02/9

8

10/9

8

06/9

9

02/0

0

10/0

0

06/0

1

02/0

2

Feb. 2, 2002EUR 17.34

0

5

10

15

20

25

Dexia’s stock market performance in Brussels

Dexia’s stock market performance in Paris

r s ’ R e v i e w

>

>

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

BEL20 Total daily trading volume (monthly average)Dexia

11/9

6

06/9

7

02/9

8

10/9

8

06/9

9

02/0

0

10/0

0

06/0

1

02/0

2

Feb. 2, 2002EUR 17.32

0

5

10

15

20

25

Brussels ParisShare price Dec. 29, 2000 (EUR) 19.26 8 19.35

Share price Dec. 29, 2001 (EUR) 16.15 16.20

Highest/lowest price (EUR) (1) 19.50-13.02 19.55-13.12

Average daily trading volume (in millions of EUR) (1) 24.91 25.74

Number of shares traded daily1 (thousands of shares) (1) 1,105 1,489

EUR 1998 1999 2000 2001Earnings per share 0.85 0.98 1.15 1.25

Net assets excluding generalbanking risks reserve (group share) 6.37 6.69 7.02 6.84

Net assets including general banking risksreserve (group share) 8.08 8.51 8.78 8.53

Gross dividend - 0.39 0.43 0.48 (7)

Net dividend (2) - 0.29 0.32 0.36 (7)

Stock market performance

Data per share

EUR million 1998 1999 2000 2001Payout ratio % (3) 40.9 41.4 41.9 39.3

Price earnings ratio P/E (4) 16.1 16.5 16.8 12.9

Price to book ratio (5) 2.2 2.4 2.8 2.4

Annual yield % (6) 2.5 2.4 2.2 3.0

Stock market ratios

(1) For 2001.(2) After payment of Belgian withholding tax (précompte mobilier) at a rate of 25%, reduced to 15% for shares with a VVPR strip(3) Ratio between total dividend and net income.(4) Ratio between the average share price as of December 31 and net earnings per share.(5) Ratio between the average share price as of December 31 and net assets (excluding the general banking risks reserve - group

share) per share as of December 31.(6) Ratio between the gross dividend per share and the share price as of December 31.(7) Proposed to the annual shareholder’s meeting on May 7, 2002(8) As of December 28, 2000.

S h a r e h o l d e

Dexia Annual Report 2001

32/33

)

)

Creation of value

Dexia has developed a value-based management approach,

which is used to adjust the targets and measure the performance

of the 40 business sectors in which the Group operates.

The results allow the Management Board to optimize the

allocation of equity capital based on the potential of each

activity to create value over the long term. This method also

makes it possible to identify and develop value creation

levers.

This approach is based on discounted cash flows, segment by

segment. Future cash flows are estimated by breaking down

the timeframe into three periods:

… the first five years, for which detailed business plan

projections are used;

… the next five years, for which, following discussion with

each business line manager, cash flow projections are

carried out, based on medium-term trends;

… the final period, for which external macroeconomic

criteria are employed, with a highly conservative bias.

Customized tools for shareholders

In 2001, Dexia upgraded the system it employs to provide

individual shareholders with regular, transparent

and interactive information. This system comprises

a shareholders’ club, an international advisory board

of shareholders, meetings in different cities, a telephone

information service and specific publications.

The Group makes a particular effort to ensure that

shareholders in Belgium and France are treated on an equal

footing in the framework of the very different tax regulations

and shareholder cultures of the two countries.

Shareholders’ clubDexia’s shareholders’ club serves as a financial information

forum. Mainly made up of Belgian and French shareholders,

it has more than 15,000 members who benefit from

information and publications designed specifically for club

members. Dexia shareholders can join the club by e-mail,

over the telephone (there is a toll-free number in France:

0 800 35 50 00) or via the Group’s website. There is no charge

for membership.

Shareholders’ meetingsIn order to discuss the Group’s businesses, strategy and

results with individual shareholders, Dexia regularly organizes

information meetings. In 2001, Pierre Richard, Chief

Executive Officer and Chairman of the Management Board,

met with a total of 3,000 shareholders in Lille, Paris and Lyon

at events organized in partnership with French financial

newspapers. Shareholders meetings with individual Belgian

shareholders are also planned in 2002.

The Group also participated, together with other firms, in

meetings organized by Euronext and the Centre de liaison

des informateurs financiers. In 2001, shareholder meetings

were also held in Poitiers, Reims, Paris, Nancy, Montpellier

and Nantes.

Every year, Dexia has a stand at the Forum de l’investissement

and the Actionaria shareholder convention, in partnership

with Dexia Banque Privée. Pierre Richard takes part in the

plenary sessions which are attended by several thousand

shareholders.

>

r s ’ R e v i e w

>

Targeted informationDexia publishes a shareholders’ letter in French and Dutch

three or four times a year. This publication keeps individual

shareholders up to date on developments in the Group,

its results and decisions taken at shareholders’ meetings.

Sent to members of the shareholders’ club and to anyone

who so requests, these newsletters are also available on

the Group’s website.

Dexia also produces a condensed annual report, which

is greatly appreciated by individual shareholders.

Internet site The Internet site www.dexia.com is a complete information

tool that is updated in real time. In addition to the share

price, statistics and a daily commentary on trends in

Dexia’s stock market performance, shareholders may

also access press releases and download detailed semiannual

and annual reports and financial statements.

In 2001, the creation of a multimedia area dedicated to

shareholders allows them to watch information meetings

and the Annual Shareholders’ Meeting live or at a later date.

Telephone information serviceShareholders can take advantage of the Group’s telephone

information service, which is accessible via a toll-free

number in France (0 800 35 50 00). This service frequently

answers questions concerning VVPR strips, the share price,

taxation of Dexia shares, the French PEA savings plan,

taxation of dividends and the French-Belgian tax

agreement.

Annual Shareholders’ MeetingA major event in the life of a listed company, the Annual

Shareholders’ Meeting is the occasion for Dexia to make

use of specific forms of communication, such as

announcements in major financial newspapers in France

and Belgium, reminders via the telephone information

service and shareholder information kits distributed with

invitations to the meeting, which are available in English,

French and Dutch. This information is also available

on the company’s website, and Dexia was one of the first

companies, as of 2000, to broadcast the Shareholders’

Meeting live over the Internet.

European advisory board ofindividual shareholdersIn June 2001, Dexia created one of the first European

advisory boards of individual shareholders, which took

over from the shareholders’ advisory board of Dexia

France, formed in 1992. Its composition reflects the

Group’s European identity; there are 11 shareholders – four

from Belgium, four from France and three from Luxembourg.

Dexia plans to open this board to other European

nationalities.

A meeting, chaired by Pierre Richard, was held in Brussels

on October 16, 2001, to launch the board.

Through the proposals and studies in which its members

participate, this advisory board plays an important role in

optimizing Dexia’s communication with individual

shareholders.

Dexia, best shareholder services in 2001 In 2001, Dexia was awarded first prize for the quality of itsshareholder services out of the forty companies in theCAC 40 stock market index (Euronext Paris). The eventwas organized by the French financial magazine La Vie

financière and Synerfil, a company specialized inshareholder relations. The Group was selected by anindependent jury composed of CEOs of major firms andrepresentatives of individual shareholders and thespecialized press. Dexia won particular note for thequality of its dedicated telephone service, its Web site andits publications.

>

>

>

>

>

S h a r e h o l d e

Dexia Annual Report 2001

34/35

Eligibility of Dexia sharesin the French PEA savings planSince January 1, 2002, the French PEA savings plan allows

investments in European shares, including Dexia shares,

of course. This new legislation should benefit French

shareholders and Dexia, prompting a significant rise

in the number of individual shareholders.

Investor relationsThroughout the year, Dexia organizes meetings on specific

subjects, conference calls, Web conferences and road shows

for institutional investors and financial analysts, especially

when results are published. About 750 contacts were made

in this respect during the year. The Group produces

financial reports and posts all pertinent economic, strategic

and financial data concerning the Group in a section on its

website, which has been upgraded in 2001.

SHAREHOLDERS’ CALENDAR>

>

r s ’ R e v i e w

… April 4, 2002: shareholders’ meeting in Marseillesin partnership with Journal des Finances

… May 7, 2002: Shareholders’ Meetings inBrussels broadcast live on Dexia’s Internetsite (www.dexia.com)

… May 14, 2002: meeting of individual shareholdersin Paris in partnership with Investir

… May 23, 2002: publication of first quarterresults

… June 1, 2002: Dexia takes part in the dayof the share in Brussels, in cooperation with Cash!