Embed Size (px)

Citation preview

Carbon Accounting Research

Qingliang Tang

Scientific Evidence of global warming

Damage of global warming

Kyoto Protocol

Cost of carbon emission control

Clean energy: e.g. Solar power generator, wind power, etc.

Emission Trading Scheme

The role of Carbon accounting

This is summary of review of carbon accounting

research in the recent literature.

The topics of the carbon accounting research include:

Carbon disclosure,

Carbon performance,

Carbon tax,

Corporate governance and carbon activity,

Cultural factors and carbon transparency

propensity,

Carbon management systems,

Carbon assurance and carbon auditing

The results of the review suggest carbon accounting

research is an extension of environmental or

sustainability study.

But carbon accounting is a unique dimension, so

should be separately studied, rather than combined

in a basket in sustainability research.

Luo, Qingliang Tang and Y Lan

Corporate Incentives to Disclose Carbon Information:

Evidence from the CDP Global 500 Report

Journal of International Financial Management

& Accounting 2012

Why companies voluntarily disclose

Co2 information? Large companies play a key role in carbon activity. Significant: 1 Emissions (economic pressure), 2 (GHG) intensive sectors (institutional pressure), 3 firm size (social pressure) Not significant: Information needs of investors The major driving force: general public and government

Luo and Qingliang Tang. Does Voluntary Carbon

Disclosure Reflect Underlying Carbon Performance?

JOURNAL OF CONTEMPORARY ACCOUNTING AND ECONOMICS, 10 (2014)

Whether voluntary carbon disclosure

reflects firms’ carbon performance (or

just greening washing)? Is

sustainability accounting really for

sustainability? (U.S., U.K., and

Australian firms)

Co2 disclosure: content analysis of

carbon reports;

Co2 performance: Co2 emissions and

mitigation

Result: a positive association between

Co2 disclosure and performance,

consistent with signalling theory

Liao, Luo, Qingliang Tang

Gender Diversity, Board Independence, Environmental Committee and

Greenhouse Gas Disclosure

British Accounting Review 2014

Corporate board’s characteristics and

Co2 voluntary disclosure

329 largest companies in the UK

We find a significant positive

association between gender diversity

and GHG disclosure.

A board with more independent

directors or environmental committee

show a higher tendency.

Theoretical contribution:

The results are consistent with

stakeholder theory

A diversified and independent board

and the existence of an environmental

committee may balance a firm’s

financial and non-financial goals

Such as board may moderate the

possible conflicting expectations of

stakeholders who have disparate

interests.

Luo, Qingliang Tang, Lan

Comparison of propensity for carbon disclosure

between developing and developed countries: A

resource constraint perspective

Accounting Research Journal, 2013, Best paper of

the year

This paper investigates differences in

voluntary carbon disclosure between

developing and developed countries

A sample consisting of 2,045 large

firms from 15 countries

Profitability, leverage and growth

were used as proxies for the degree of

resource availability

Results show that the carbon

disclosure propensity is correlated in

the right direction with resource

availability proxies

This relationship is stronger in

developing nations, suggesting that

the shortage of resources is one

reason for the lack of commitment to

carbon mitigation and disclosure in

these countries.

So resource restriction provides a

complementary explanation – largely

ignored in the existing literature – for

variation in the carbon-disclosure

propensity of firms.

Luo and Qingliang Tang

Does National Culture Influence Corporate Carbon

Disclosure Propensity?

Journal of International Accounting Research

Forthcoming 2015

National culture impacts managerial

attitudes and philosophies about

environmental protection, and thus

affects their actions about emissions

control and disclosure.

A sample of 1,762 firms from 33

countries

We found that cultural dimensions of

masculinity (negative), power distance

(negative) and uncertainty avoidance

(positive) are related to carbon

disclosure propensity

This is regardless of whether Hofstede

or Global Leadership and

Organizational Behaviour

Effectiveness (GLOBE) culture

measures are used.

Our results also show individualism

and long-term orientation has

significant impact under Hofstede

measure though not under GLOBE

measure.

In addition, our evidence implies that

national culture may moderate the

effect of carbon control mechanisms,

such as emissions trading schemes.

Finally, the empirical evidence

indicates the impact of culture is not

sensitive to national wealth and

industry membership.

Theoretical contribution

The findings suggest culture exerts

incremental influences beyond

economic and regulatory incentives.

The result is useful in negotiation for

an international climate agreement

that is more acceptable to societies

with disparate cultural backgrounds.

Luo and Qingliang Tang. Carbon Tax, Corporate

Carbon Profile and Financial Return. Pacific Accounting

Review 2014, Volume 26, Issue 3

The impact of the proposed carbon

tax (big event in history) on the

financial market return of Australian

firms

We utilise the event-study method.

Sample includes 336 firm-event

observations.

The proposed tax has negative

impact on abnormal returns,

particularly for the materials,

industrial and financial sectors.

Scope 1 emission is significantly

associated with abnormal returns,

but not Scope 2.

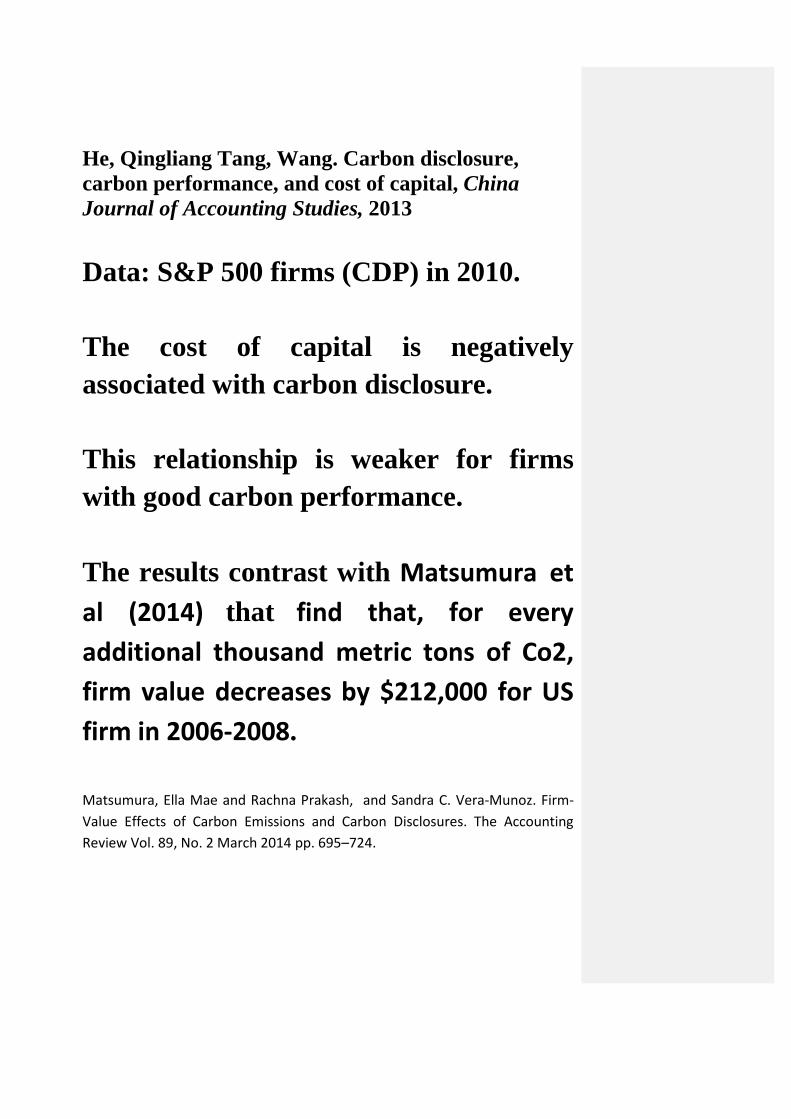

He, Qingliang Tang, Wang. Carbon disclosure,

carbon performance, and cost of capital, China

Journal of Accounting Studies, 2013

Data: S&P 500 firms (CDP) in 2010.

The cost of capital is negatively

associated with carbon disclosure.

This relationship is weaker for firms

with good carbon performance.

The results contrast with Matsumura et

al (2014) that find that, for every

additional thousand metric tons of Co2,

firm value decreases by $212,000 for US

firm in 2006-2008.

Matsumura, Ella Mae and Rachna Prakash, and Sandra C. Vera-Munoz. Firm-

Value Effects of Carbon Emissions and Carbon Disclosures. The Accounting

Review Vol. 89, No. 2 March 2014 pp. 695–724.

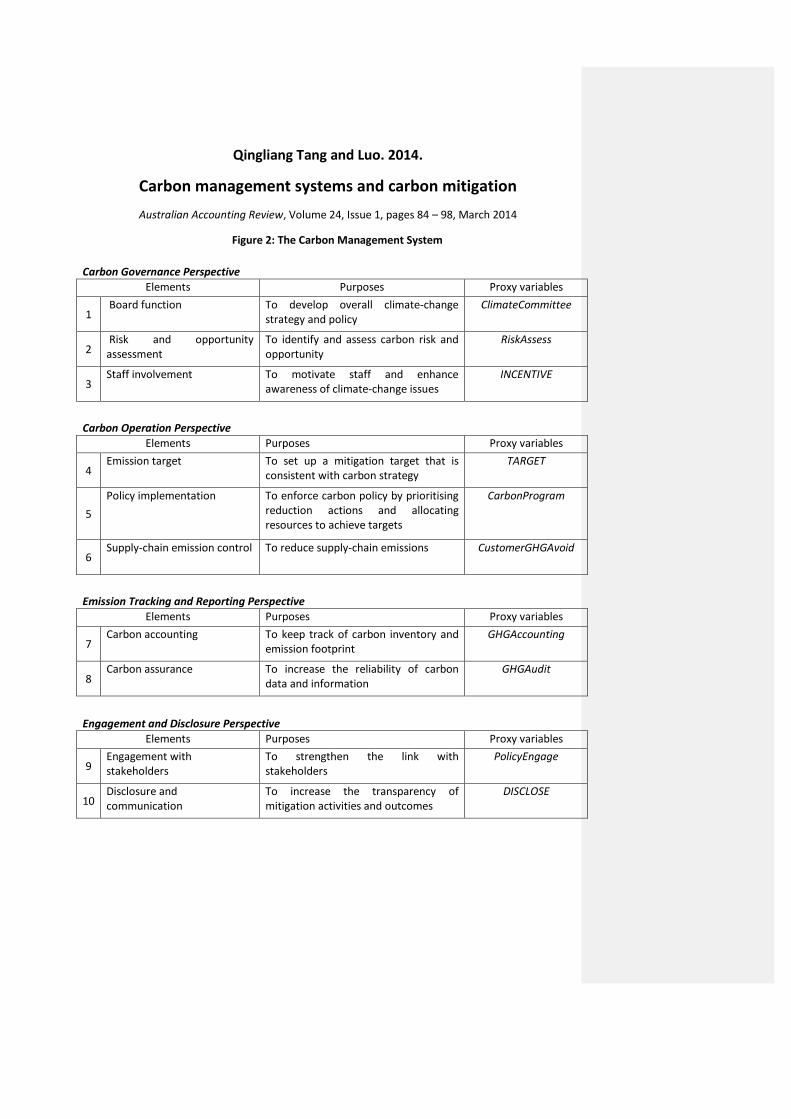

Qingliang Tang and Luo. 2014.

Carbon management systems and carbon mitigation

Australian Accounting Review, Volume 24, Issue 1, pages 84 – 98, March 2014

Figure 2: The Carbon Management System

Carbon Governance Perspective

Elements Purposes Proxy variables

1 Board function To develop overall climate-change

strategy and policy ClimateCommittee

2 Risk and opportunity assessment

To identify and assess carbon risk and opportunity

RiskAssess

3 Staff involvement To motivate staff and enhance

awareness of climate-change issues INCENTIVE

Carbon Operation Perspective

Elements Purposes Proxy variables

4 Emission target To set up a mitigation target that is

consistent with carbon strategy TARGET

5

Policy implementation To enforce carbon policy by prioritising reduction actions and allocating resources to achieve targets

CarbonProgram

6 Supply-chain emission control To reduce supply-chain emissions CustomerGHGAvoid

Emission Tracking and Reporting Perspective

Elements Purposes Proxy variables

7 Carbon accounting To keep track of carbon inventory and

emission footprint GHGAccounting

8 Carbon assurance To increase the reliability of carbon

data and information GHGAudit

Engagement and Disclosure Perspective

Elements Purposes Proxy variables

9 Engagement with stakeholders

To strengthen the link with stakeholders

PolicyEngage

10 Disclosure and communication

To increase the transparency of mitigation activities and outcomes

DISCLOSE

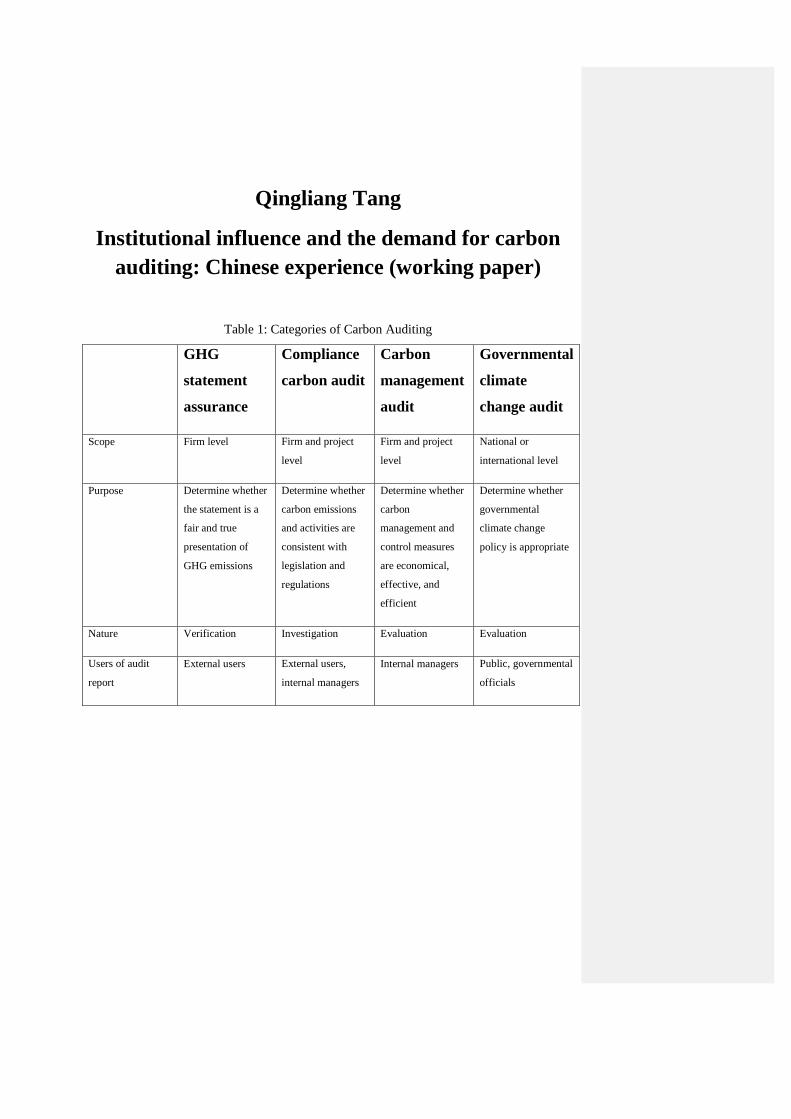

Qingliang Tang

Institutional influence and the demand for carbon

auditing: Chinese experience (working paper)

Table 1: Categories of Carbon Auditing

GHG

statement

assurance

Compliance

carbon audit

Carbon

management

audit

Governmental

climate

change audit

Scope Firm level Firm and project

level

Firm and project

level

National or

international level

Purpose Determine whether

the statement is a

fair and true

presentation of

GHG emissions

Determine whether

carbon emissions

and activities are

consistent with

legislation and

regulations

Determine whether

carbon

management and

control measures

are economical,

effective, and

efficient

Determine whether

governmental

climate change

policy is appropriate

Nature Verification Investigation Evaluation Evaluation

Users of audit

report

External users External users,

internal managers

Internal managers Public, governmental

officials

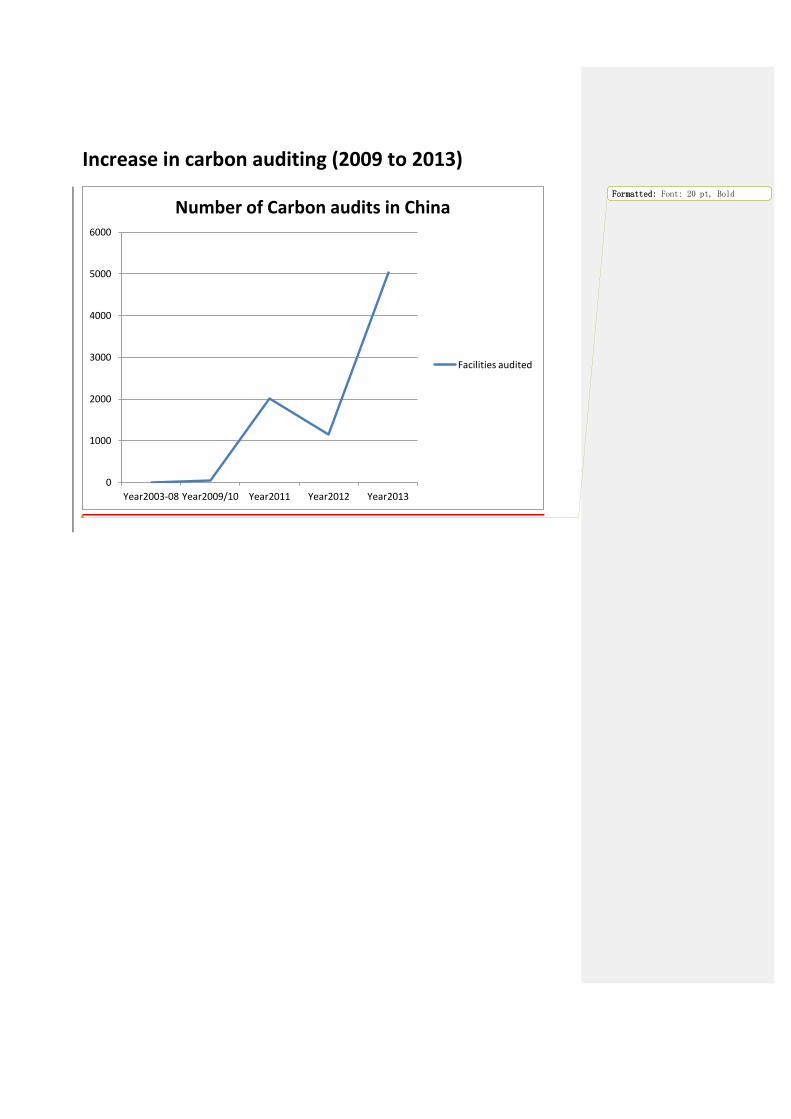

Why is a significant increase in

demand for carbon auditing (2009 -

2013)?

A change in economic development

model, and the institution of business

An explosion of carbon and energy

laws and regulations prior to the audit

An increasing governmental greening

investment

Institutional changes make carbon

auditing from rhetoric to practice

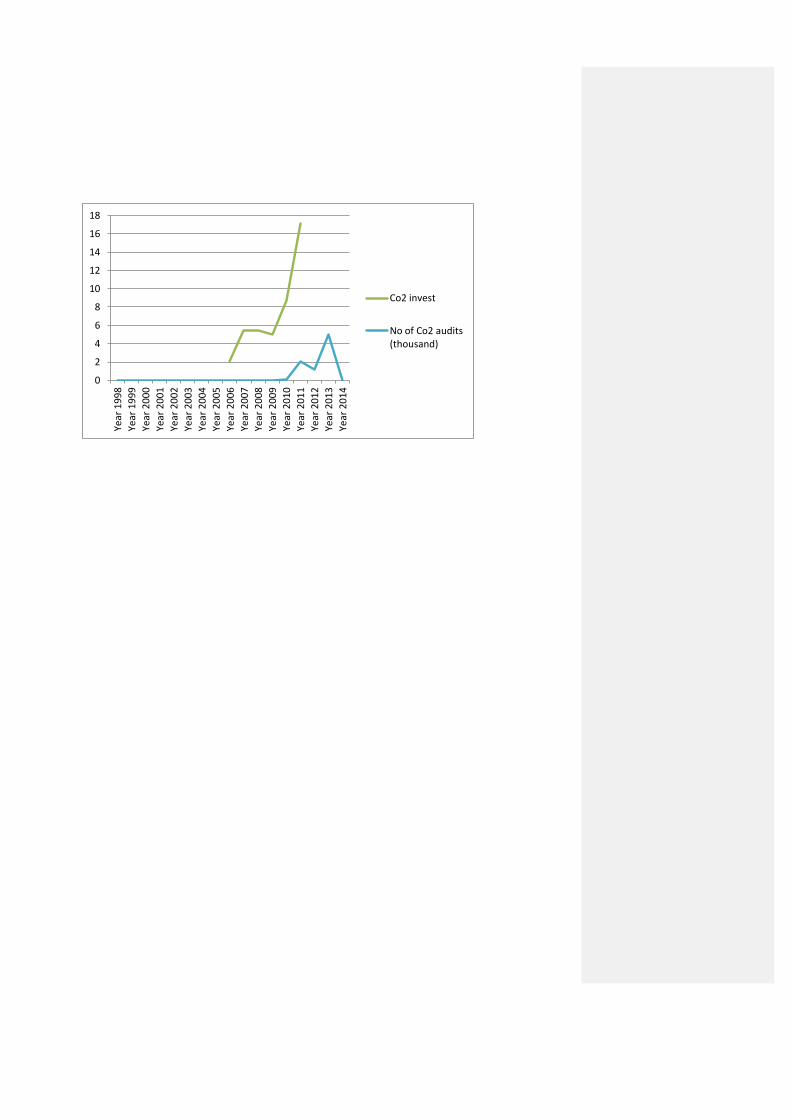

Increase in carbon auditing (2009 to 2013)

0

1000

2000

3000

4000

5000

6000

Year2003-08 Year2009/10 Year2011 Year2012 Year2013

Number of Carbon audits in China

Facilities audited

Formatted: Font: 20 pt, Bold

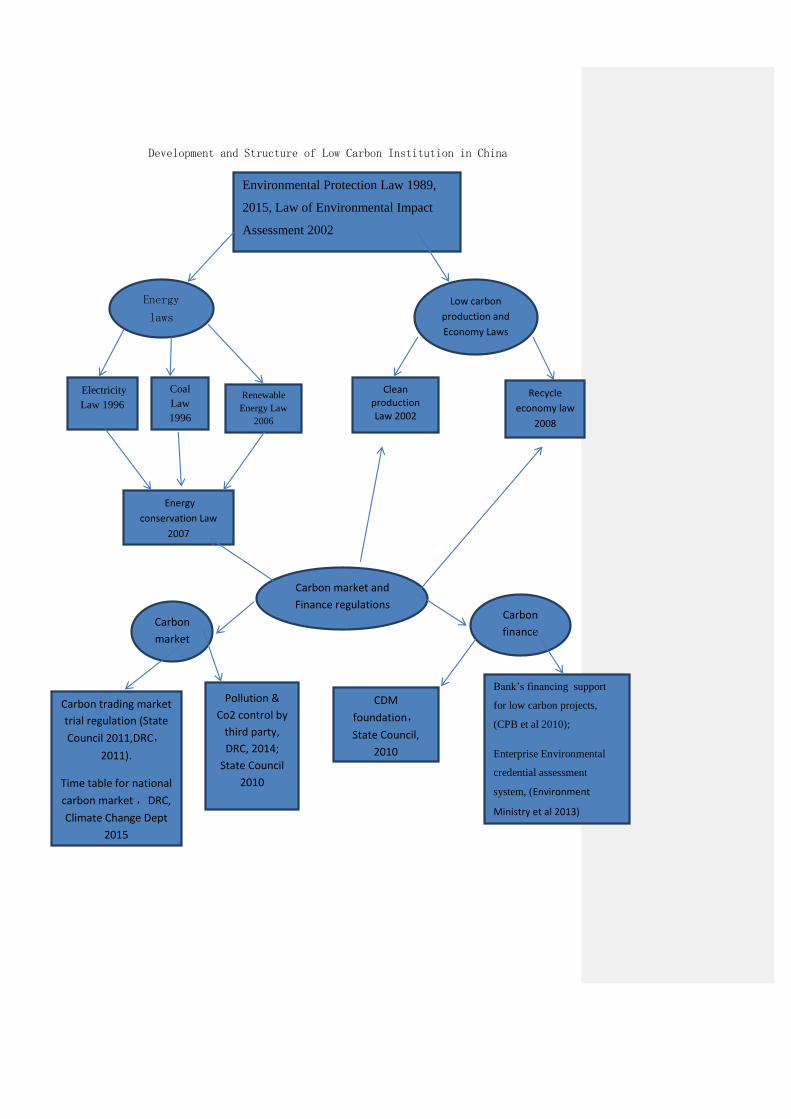

Development and Structure of Low Carbon Institution in China

Environmental Protection Law 1989,

2015, Law of Environmental Impact

Assessment 2002

Electricity

Law 1996

Coal

Law

1996

Renewable

Energy Law

2006

Energy

laws

Low carbon

production and

Economy Laws

Clean production Law 2002

Recycle

economy law

2008

Energy

conservation Law

2007

Carbon market and

Finance regulations

CDM

foundation,

State Council,

2010

Carbon trading market

trial regulation (State

Council 2011,DRC,

2011).

Time table for national

carbon market ,DRC,

Climate Change Dept

2015

Bank’s financing support

for low carbon projects,

(CPB et al 2010);

Enterprise Environmental

credential assessment

system, (Environment

Ministry et al 2013)

Carbon

market

Carbon

finance

Pollution &

Co2 control by

third party,

DRC, 2014;

State Council

2010

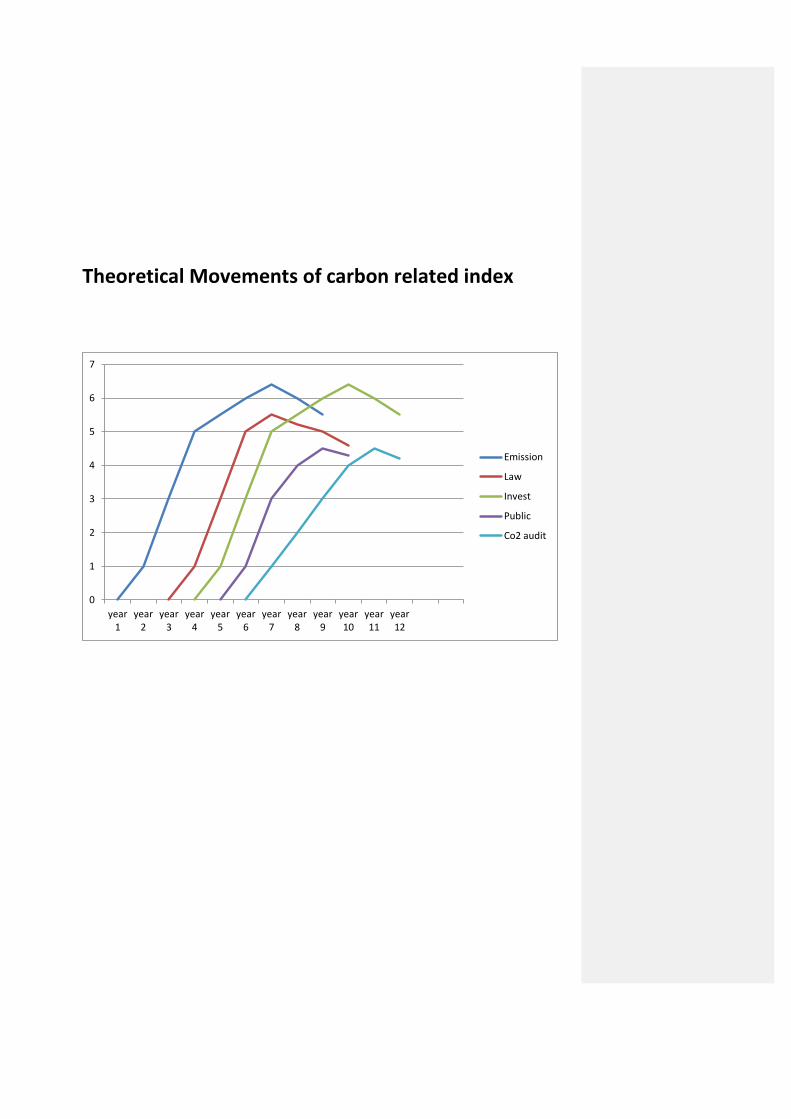

Theoretical Movements of carbon related index

0

1

2

3

4

5

6

7

year 1

year 2

year 3

year 4

year 5

year 6

year 7

year 8

year 9

year 10

year 11

year 12

Emission

Law

Invest

Public

Co2 audit

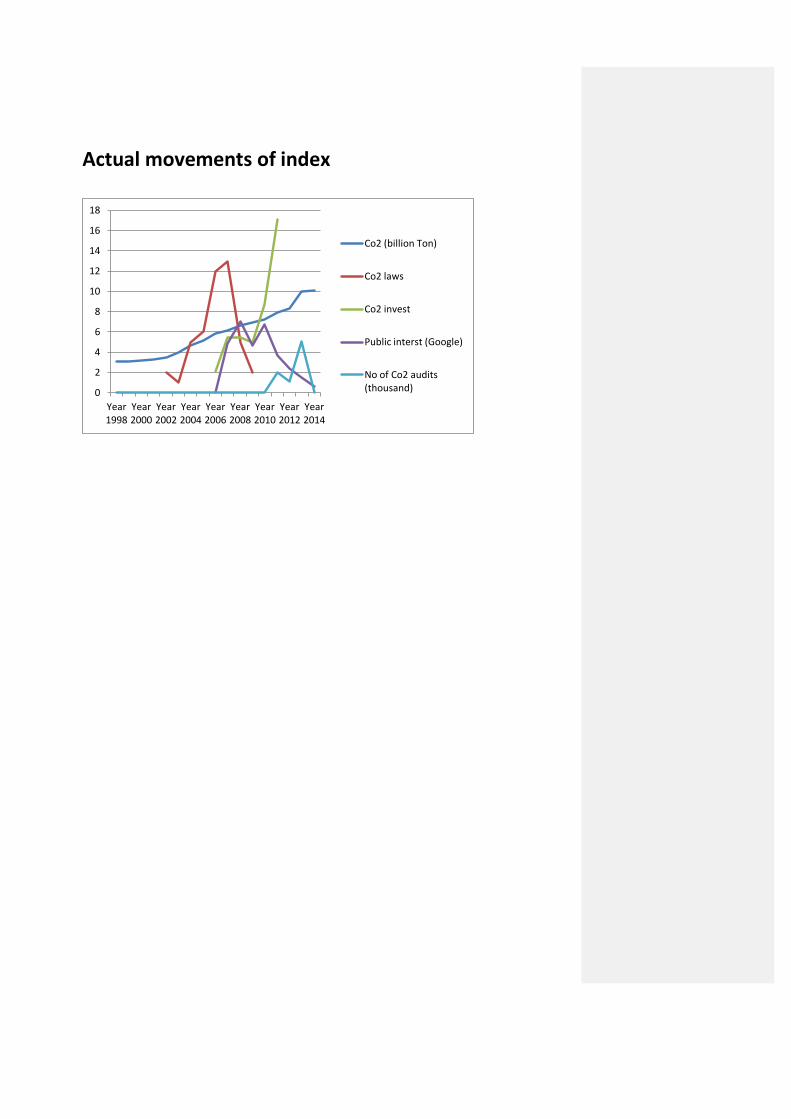

Actual movements of index

0

2

4

6

8

10

12

14

16

18

Year 1998

Year 2000

Year 2002

Year 2004

Year 2006

Year 2008

Year 2010

Year 2012

Year 2014

Co2 (billion Ton)

Co2 laws

Co2 invest

Public interst (Google)

No of Co2 audits (thousand)

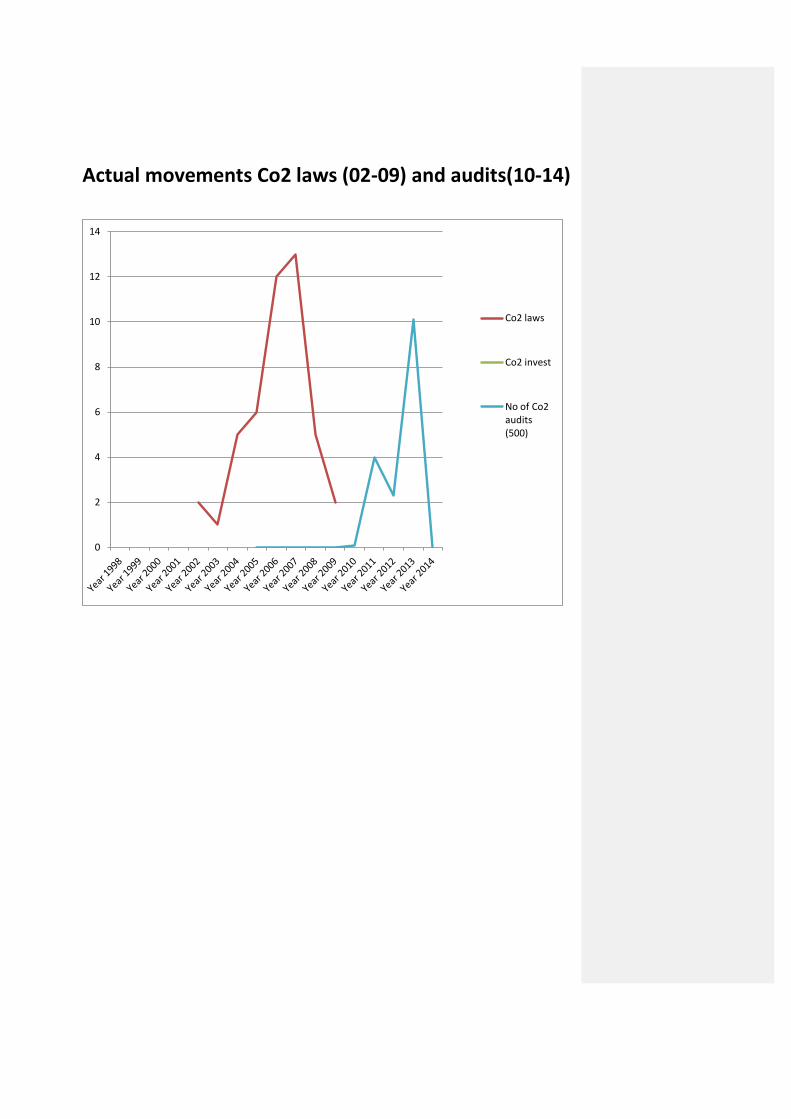

Actual movements Co2 laws (02-09) and audits(10-14)

0

2

4

6

8

10

12

14

Co2 laws

Co2 invest

No of Co2 audits (500)

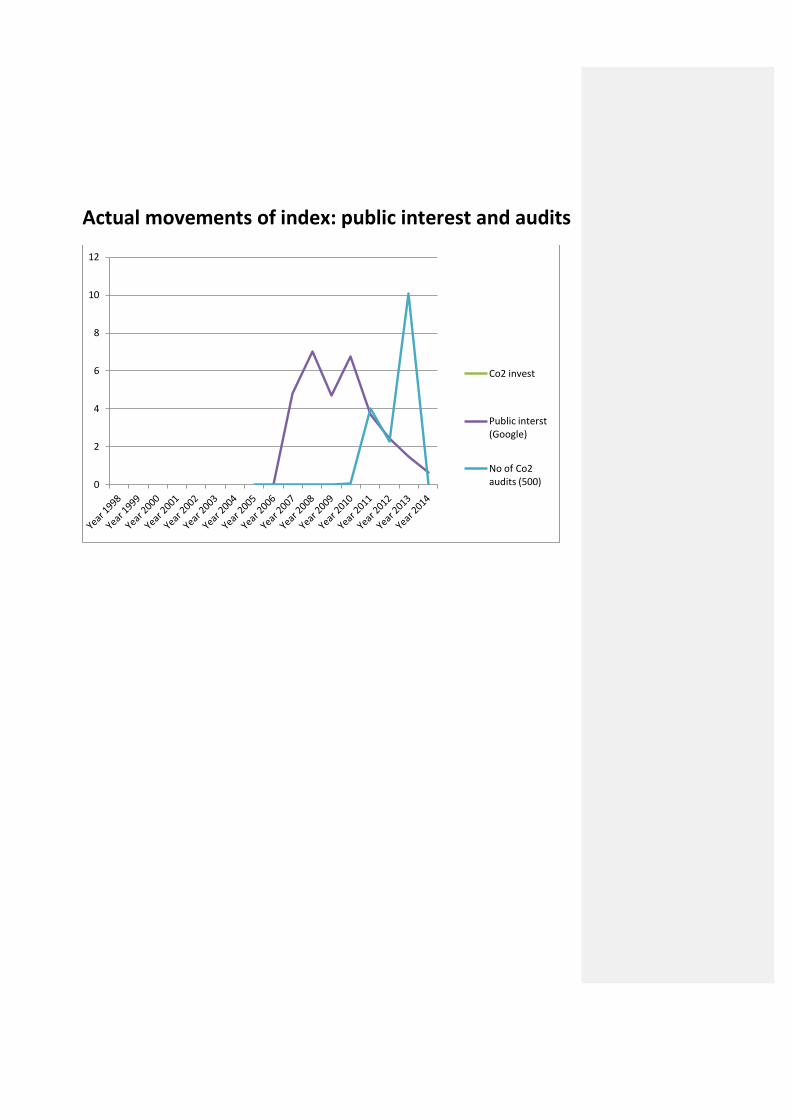

Actual movements of index: public interest and audits

0

2

4

6

8

10

12

Co2 invest

Public interst (Google)

No of Co2 audits (500)

0

2

4

6

8

10

12

14

16

18

Year

19

98

Year

19

99

Year

20

00

Year

20

01

Year

20

02

Year

20

03

Year

20

04

Year

20

05

Year

20

06

Year

20

07

Year

20

08

Year

20

09

Year

20

10

Year

20

11

Year

20

12

Year

20

13

Year

20

14

Co2 invest

No of Co2 audits (thousand)

Pacific Accounting Review, 2014, Volume 26, Issue 3

Carbon Tax, Corporate Carbon Profile and Financial Return

Le Luo, University of Newcastle

Qingliang Tang, University of Western Sydney

Abstract

Purpose: This study investigates the impact of the proposed carbon tax on the financial market

return of Australian firms. We also consider the differential tax effect on individual firms with

different carbon profiles, including factors such as emissions costs, carbon disclosure and climate-

change policies.

Design/methodology/approach: Utilising the event-study method, we examine the market reaction

to seven key carbon legislative information events that occurred from February 2011 to November

2011. Our sample includes 48 different firms whose emissions-related data are available from

Carbon Disclosure Project reports; thus, 336 firm-event observations are employed for our cross-

sectional analysis.

Findings: The paper documents evidence that the proposed tax has an overall negative impact on

shareholder wealth as measured by abnormal returns. The negative impact varies across sectors,

with the most significant effect found in the materials, industrial and financial sectors. We also

found that a firm’s direct carbon exposure (as measured by Scope 1 emissions) is significantly

associated with abnormal returns, whereas the indirect exposure (as measured by Scope 2 emissions)

is not, because Scope 2 emissions are not covered by the tax. In addition, our findings suggest that

the information content of the events is more notable during the early stages of the development of

the carbon tax.

Research limitations/implications: Our sample is restricted to the largest firms with relevant carbon

profile information. Thus, caution should be exercised when generalising our inferences.

Practical implications: The introduction of the carbon tax was largely unexpected and most firms

were unprepared for it; thus, their carbon policy appears inadequate and does not impress investors.

An understanding of how the carbon tax affects shareholder value and welfare will encourage

management to take proactive actions to mitigate the compliance costs of carbon legislation.

Originality/Value: The enactment of the Australian carbon tax perhaps represents one of the biggest

social and economic restructuring events in the country’s history. Our results offer initial insight into

its impact and suggest that investors would penalise firms with heavy direct operational emissions.

In addition, Australian corporate carbon policy seems inadequate, so does not reverse the negative

effect of the tax on the value of a firm.

Keywords: carbon tax, corporate carbon profile, greenhouse gas (GHG) emissions, Carbon Disclosure

Project (CDP), carbon reduction target

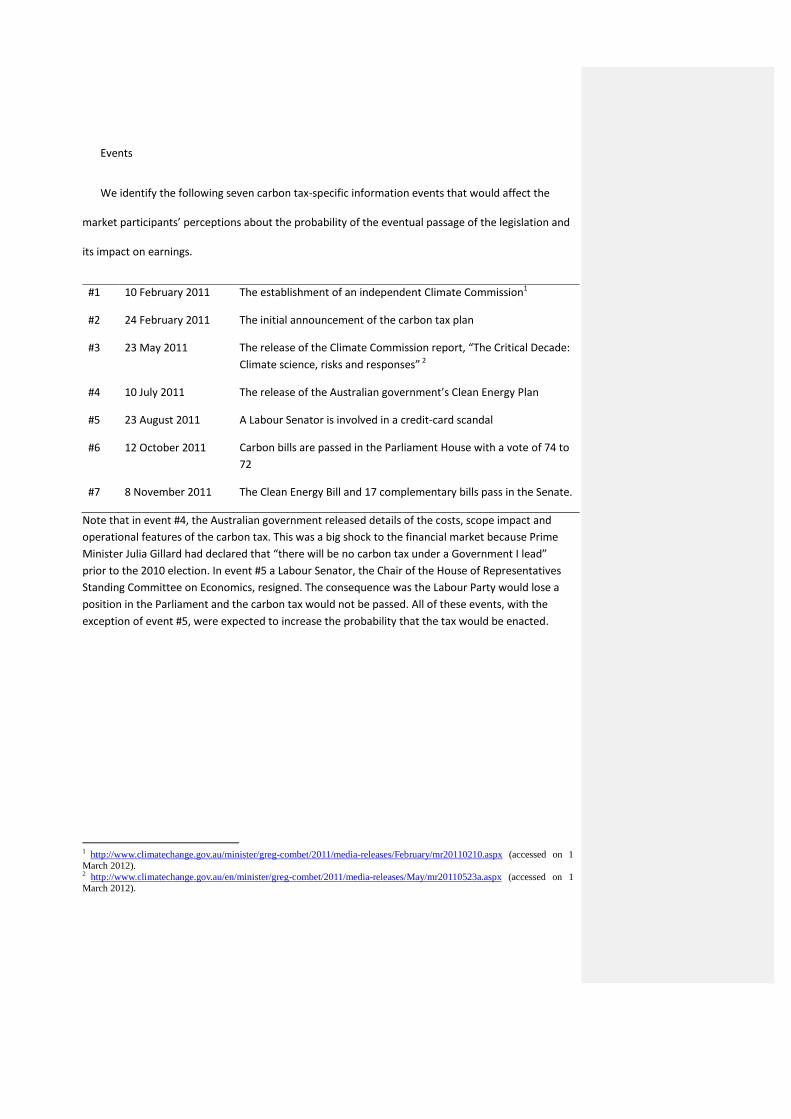

Events

We identify the following seven carbon tax-specific information events that would affect the

market participants’ perceptions about the probability of the eventual passage of the legislation and

its impact on earnings.

#1 10 February 2011 The establishment of an independent Climate Commission1

#2 24 February 2011 The initial announcement of the carbon tax plan

#3 23 May 2011 The release of the Climate Commission report, “The Critical Decade:

Climate science, risks and responses” 2

#4 10 July 2011 The release of the Australian government’s Clean Energy Plan

#5 23 August 2011 A Labour Senator is involved in a credit-card scandal

#6 12 October 2011 Carbon bills are passed in the Parliament House with a vote of 74 to

72

#7 8 November 2011 The Clean Energy Bill and 17 complementary bills pass in the Senate.

Note that in event #4, the Australian government released details of the costs, scope impact and

operational features of the carbon tax. This was a big shock to the financial market because Prime

Minister Julia Gillard had declared that “there will be no carbon tax under a Government I lead”

prior to the 2010 election. In event #5 a Labour Senator, the Chair of the House of Representatives

Standing Committee on Economics, resigned. The consequence was the Labour Party would lose a

position in the Parliament and the carbon tax would not be passed. All of these events, with the

exception of event #5, were expected to increase the probability that the tax would be enacted.

1 http://www.climatechange.gov.au/minister/greg-combet/2011/media-releases/February/mr20110210.aspx (accessed on 1

March 2012). 2 http://www.climatechange.gov.au/en/minister/greg-combet/2011/media-releases/May/mr20110523a.aspx (accessed on 1

March 2012).

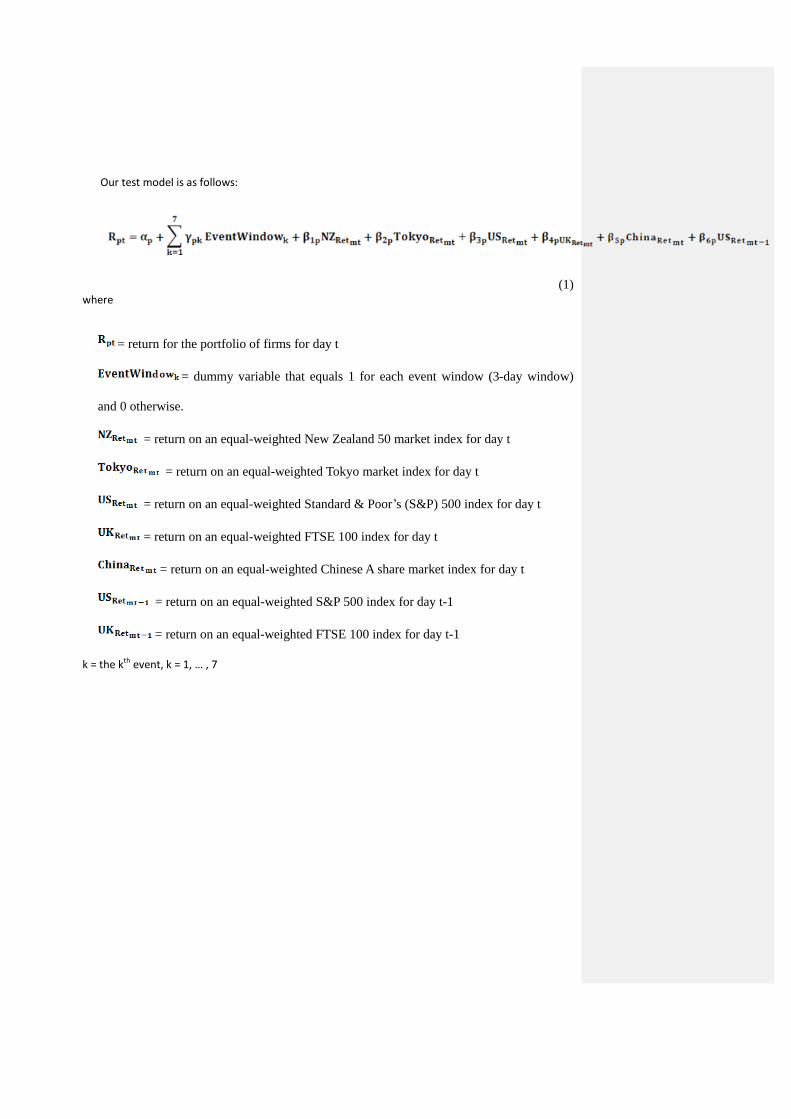

Our test model is as follows:

(1) where

= return for the portfolio of firms for day t

= dummy variable that equals 1 for each event window (3-day window)

and 0 otherwise.

= return on an equal-weighted New Zealand 50 market index for day t

= return on an equal-weighted Tokyo market index for day t

= return on an equal-weighted Standard & Poor’s (S&P) 500 index for day t

= return on an equal-weighted FTSE 100 index for day t

= return on an equal-weighted Chinese A share market index for day t

= return on an equal-weighted S&P 500 index for day t-1

= return on an equal-weighted FTSE 100 index for day t-1

k = the kth event, k = 1, … , 7

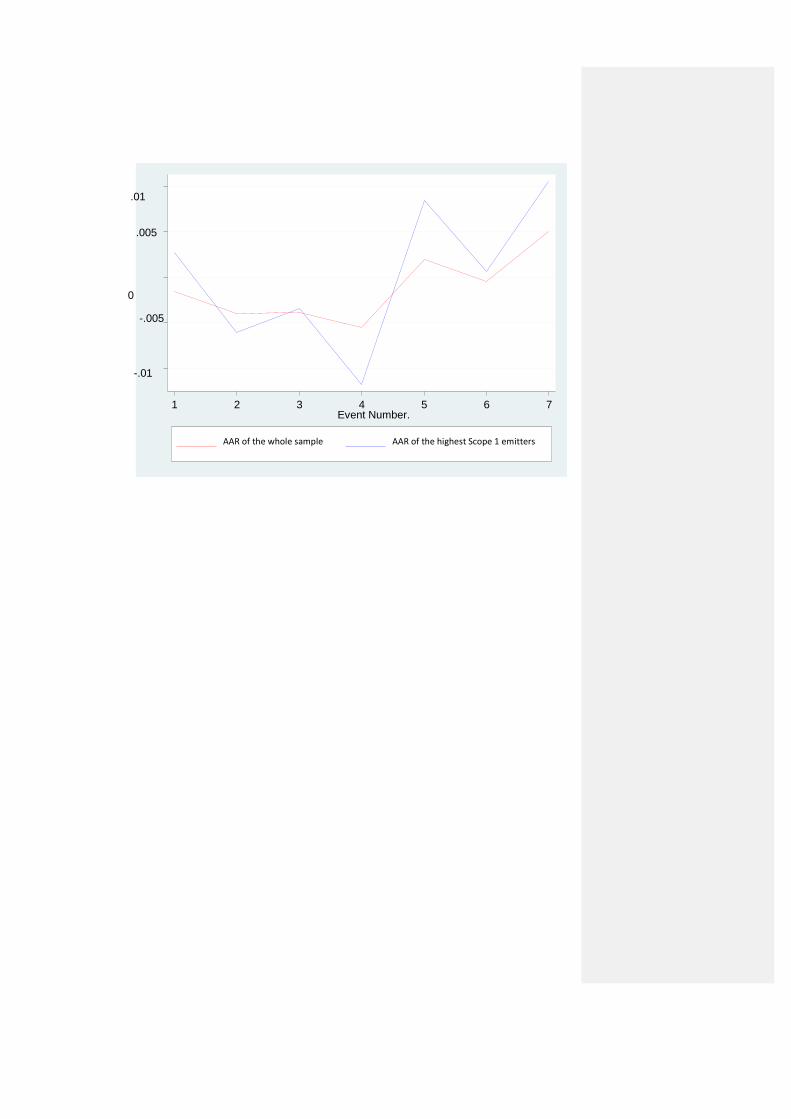

-.01

-.005

0

.005

.01

1 2 3 4 5 6 7 Event Number.

AAR of the whole sample AAR of the highest Scope 1 emitters