Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No: 56837-IN

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED CREDIT

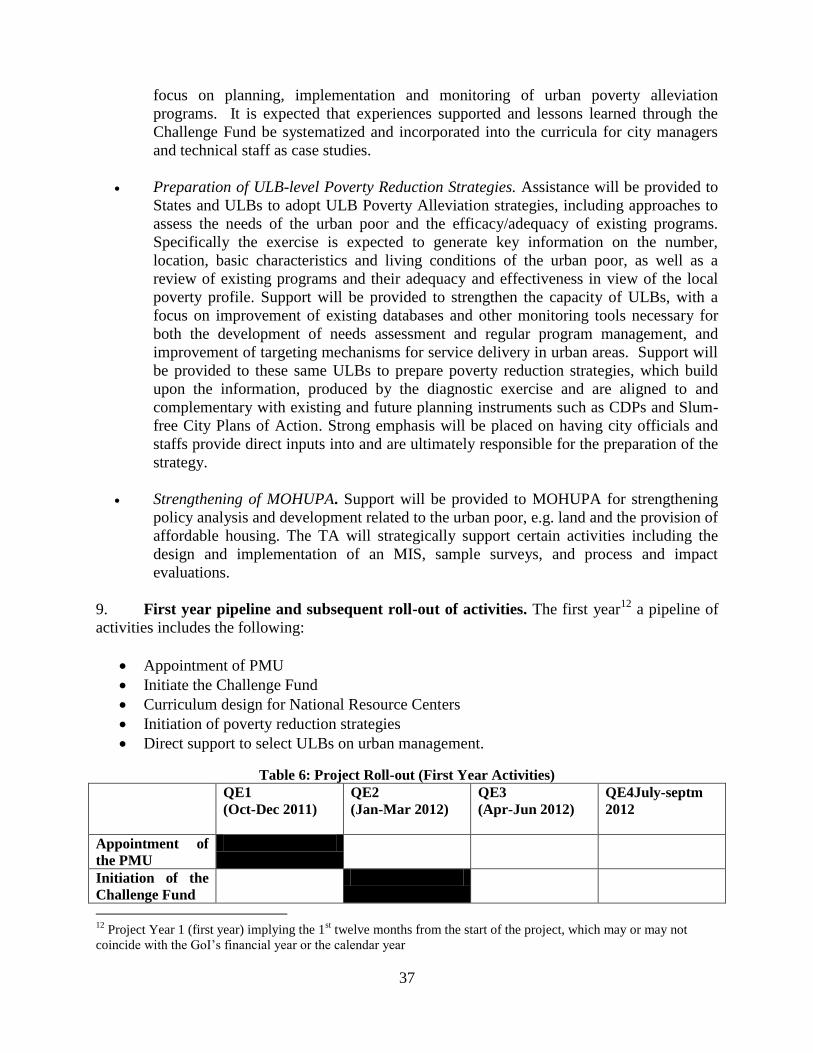

IN THE AMOUNT OF SDR 37.1 MILLION

(US$60 MILLION EQUIVALENT)

TO

INDIA

FOR A

CAPACITY BUILDING FOR URBAN DEVELOPMENT PROJECT

June 17, 2011

Sustainable Development Unit

India Country Management Unit

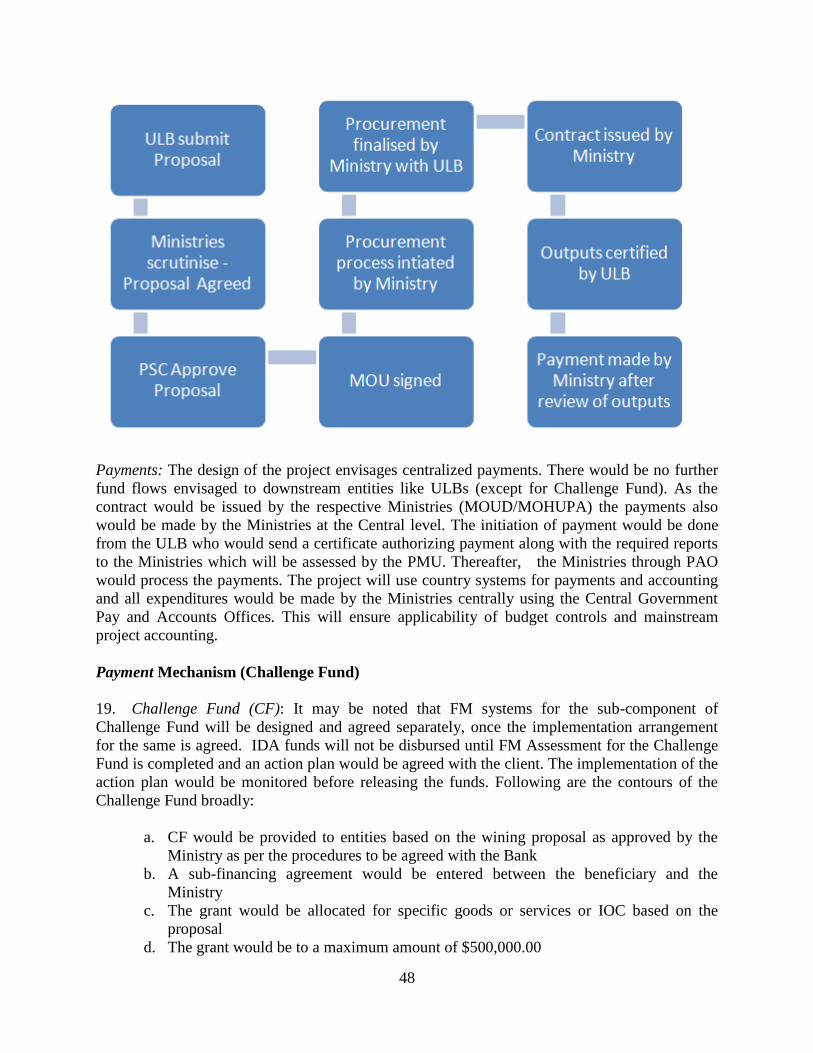

South Asia Regional Office

This document has a restricted distribution and may be used by recipients only in the

performance of their official duties. Its contents may not otherwise be disclosed without World

Bank authorization.

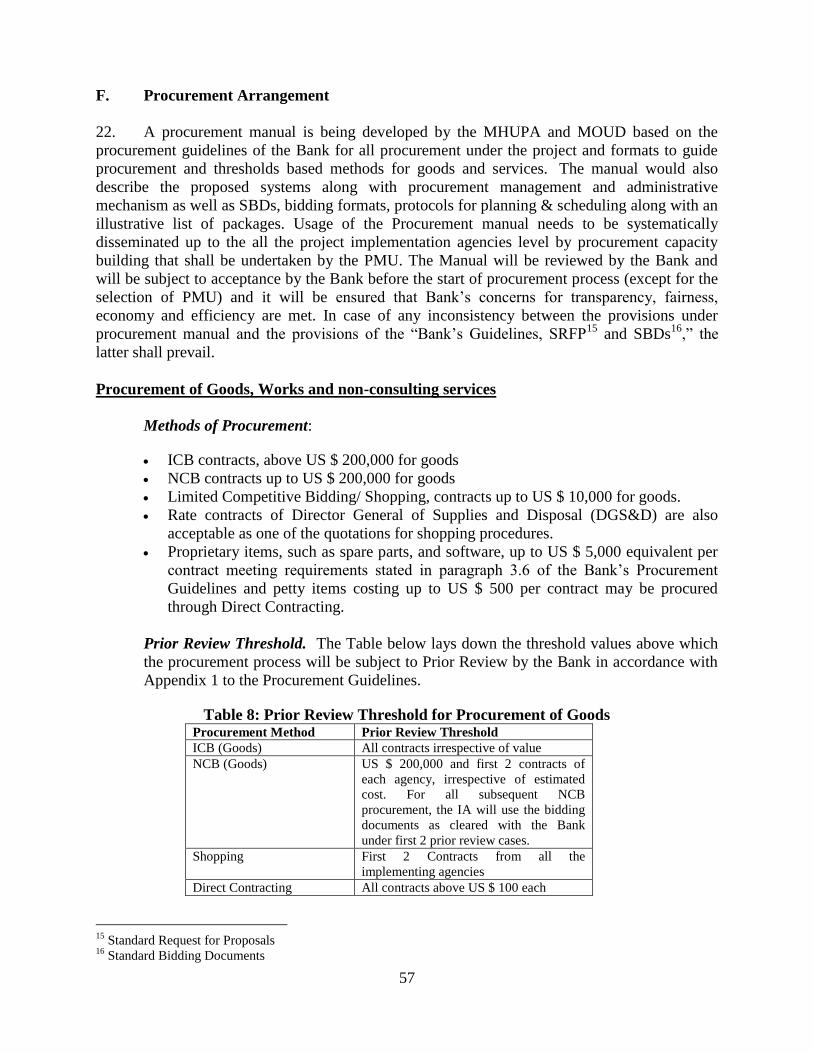

Pub

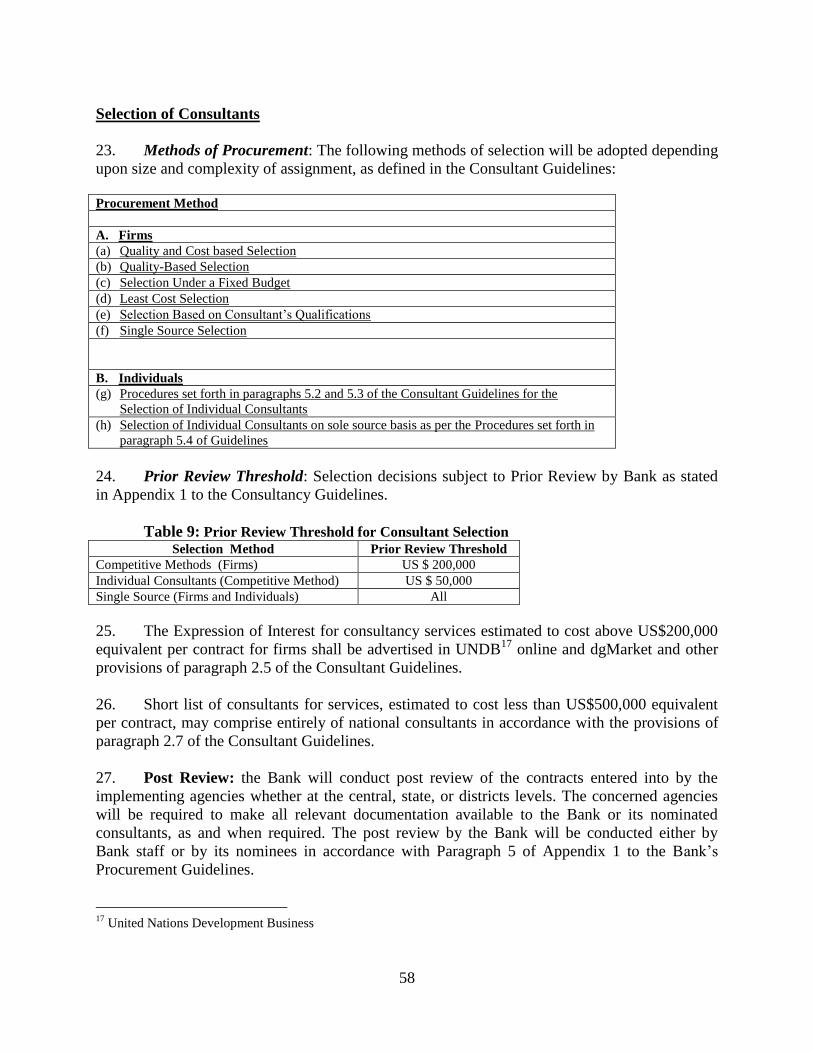

lic D

iscl

osur

e A

utho

rized

Pub

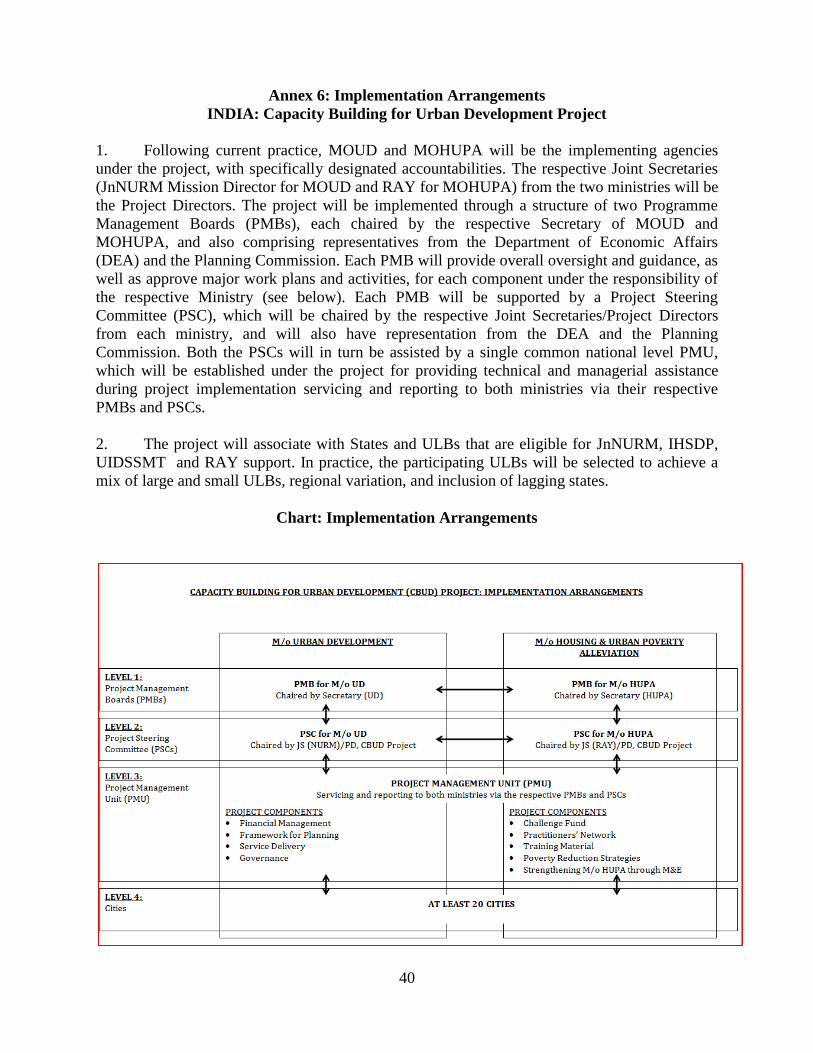

lic D

iscl

osur

e A

utho

rized

Pub

lic D

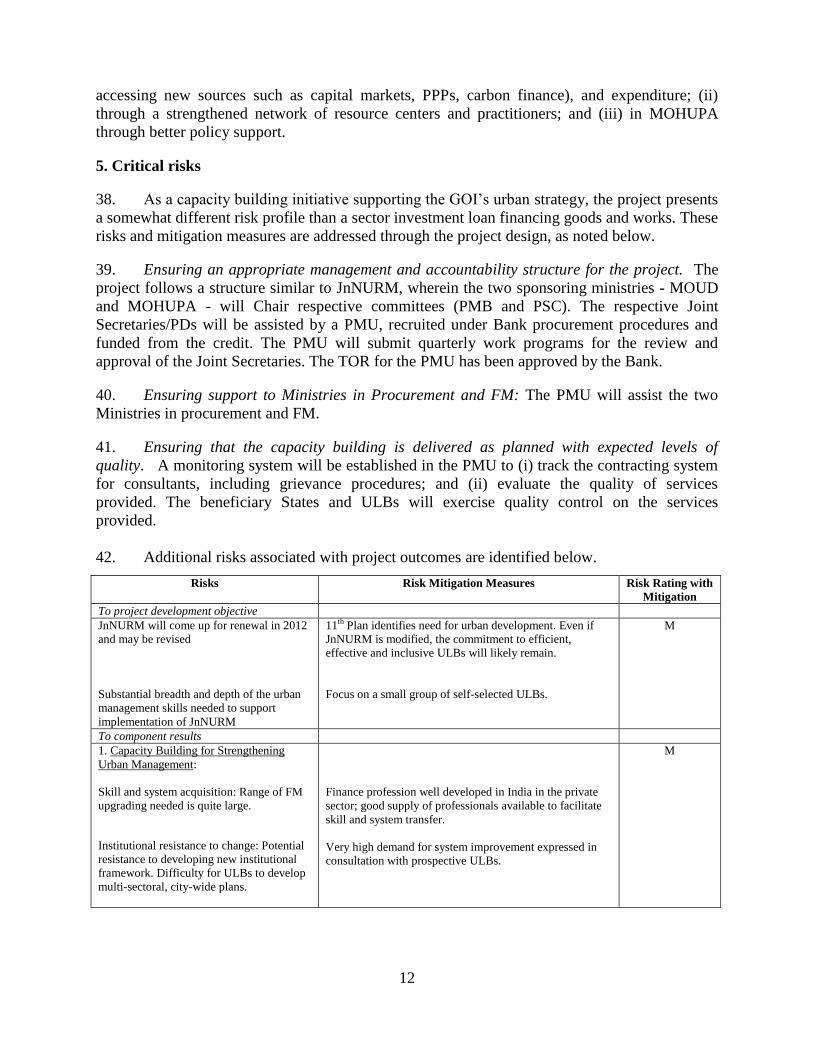

iscl

osur

e A

utho

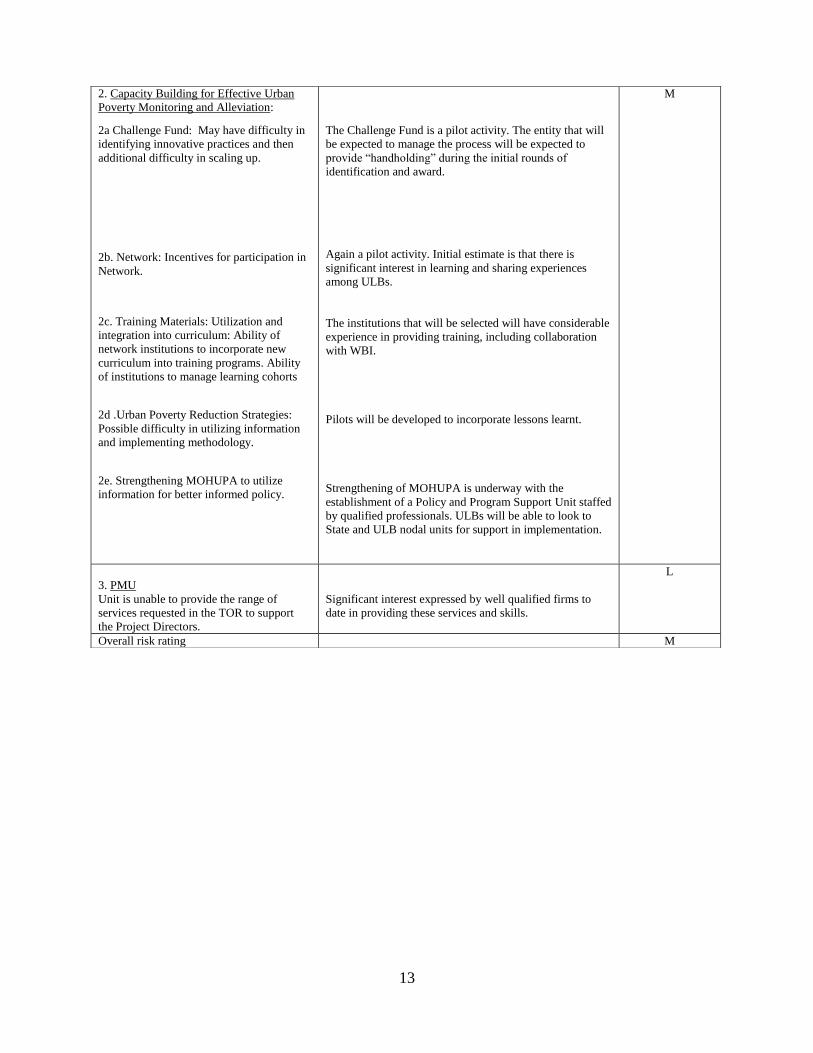

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

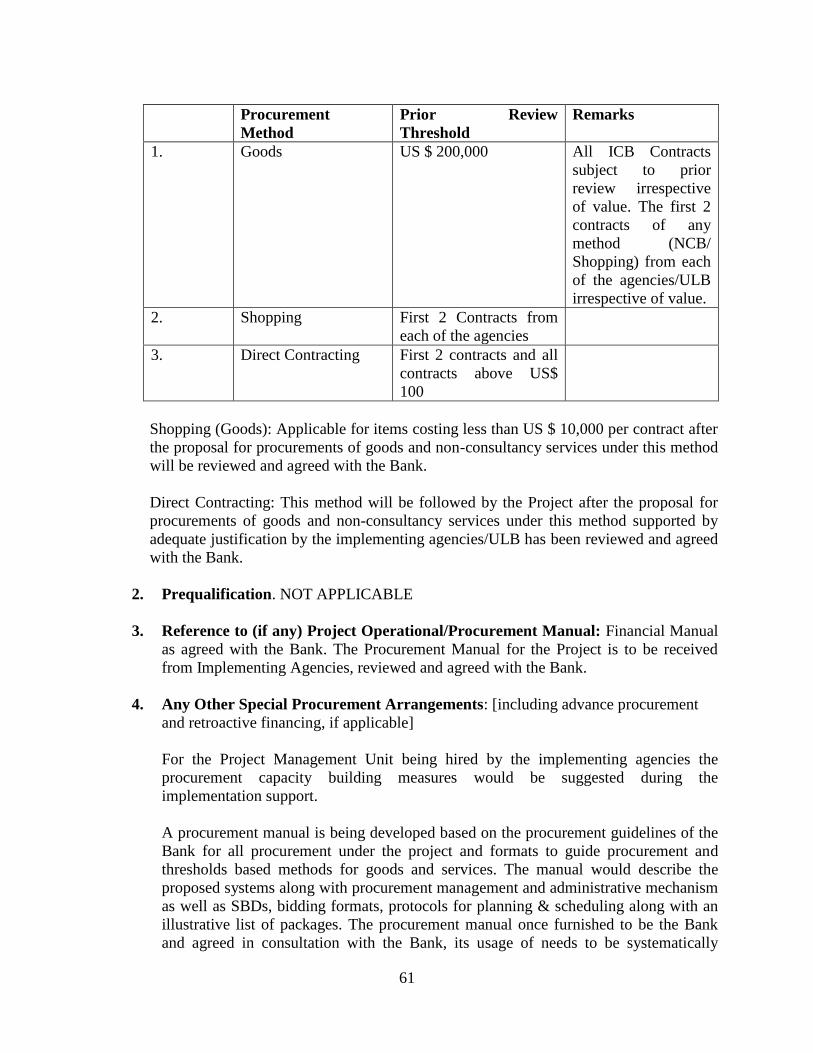

e A

utho

rized

Pub

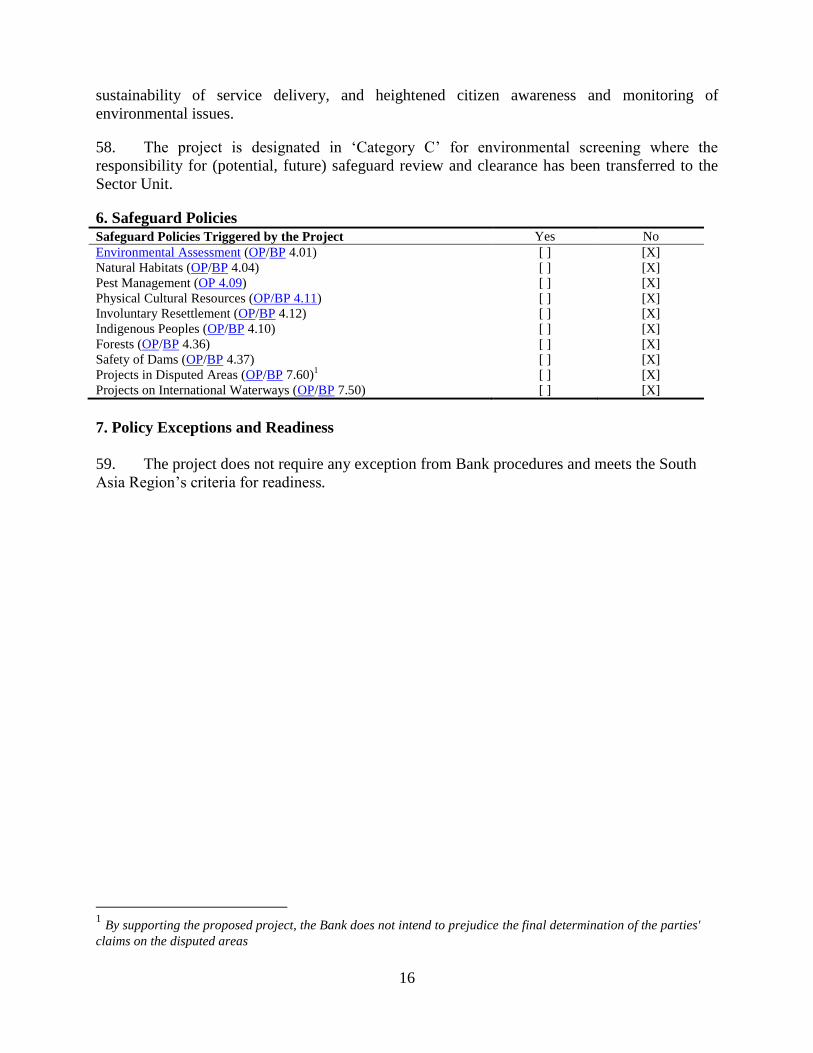

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

i

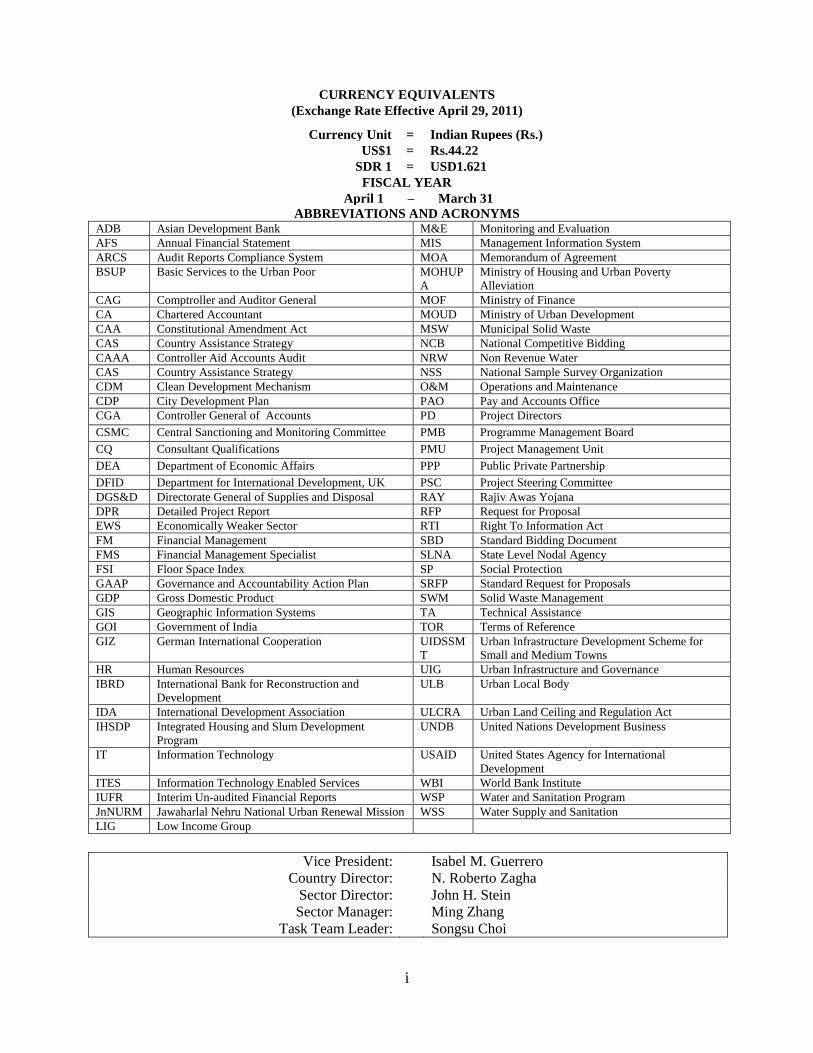

CURRENCY EQUIVALENTS

(Exchange Rate Effective April 29, 2011)

Currency Unit = Indian Rupees (Rs.)

US$1 = Rs.44.22

SDR 1 = USD1.621

FISCAL YEAR

April 1 – March 31

ABBREVIATIONS AND ACRONYMS ADB Asian Development Bank M&E Monitoring and Evaluation

AFS Annual Financial Statement MIS Management Information System

ARCS Audit Reports Compliance System MOA Memorandum of Agreement

BSUP Basic Services to the Urban Poor MOHUP

A

Ministry of Housing and Urban Poverty

Alleviation

CAG Comptroller and Auditor General MOF Ministry of Finance

CA Chartered Accountant MOUD Ministry of Urban Development

CAA Constitutional Amendment Act MSW Municipal Solid Waste

CAS Country Assistance Strategy NCB National Competitive Bidding

CAAA Controller Aid Accounts Audit NRW Non Revenue Water

CAS Country Assistance Strategy NSS National Sample Survey Organization

CDM Clean Development Mechanism O&M Operations and Maintenance

CDP City Development Plan PAO Pay and Accounts Office

CGA Controller General of Accounts PD Project Directors

CSMC Central Sanctioning and Monitoring Committee PMB Programme Management Board

CQ Consultant Qualifications PMU Project Management Unit

DEA Department of Economic Affairs PPP Public Private Partnership

DFID Department for International Development, UK PSC Project Steering Committee

DGS&D Directorate General of Supplies and Disposal RAY Rajiv Awas Yojana

DPR Detailed Project Report RFP Request for Proposal

EWS Economically Weaker Sector RTI Right To Information Act

FM Financial Management SBD Standard Bidding Document

FMS Financial Management Specialist SLNA State Level Nodal Agency

FSI Floor Space Index SP Social Protection

GAAP Governance and Accountability Action Plan SRFP Standard Request for Proposals

GDP Gross Domestic Product SWM Solid Waste Management

GIS Geographic Information Systems TA Technical Assistance

GOI Government of India TOR Terms of Reference

GIZ German International Cooperation UIDSSM

T

Urban Infrastructure Development Scheme for

Small and Medium Towns

HR Human Resources UIG Urban Infrastructure and Governance

IBRD International Bank for Reconstruction and

Development

ULB Urban Local Body

IDA International Development Association ULCRA Urban Land Ceiling and Regulation Act

IHSDP Integrated Housing and Slum Development

Program

UNDB United Nations Development Business

IT Information Technology USAID United States Agency for International

Development

ITES Information Technology Enabled Services WBI World Bank Institute

IUFR Interim Un-audited Financial Reports WSP Water and Sanitation Program

JnNURM Jawaharlal Nehru National Urban Renewal Mission WSS Water Supply and Sanitation

LIG Low Income Group

Vice President: Isabel M. Guerrero

Country Director: N. Roberto Zagha

Sector Director: John H. Stein

Sector Manager: Ming Zhang

Task Team Leader: Songsu Choi

ii

INDIA

CAPACITY BUILDING FOR URBAN DEVELOPMENT

CONTENTS

Page

A. STRATEGIC CONTEXT AND RATIONALE .................................................... 1 1. Country and sector issues........................................................................................... 1 2. Rationale for Bank Group Involvement ..................................................................... 5

3. Higher level objectives to which the project contributes ........................................... 5

B. PROJECT DESCRIPTION .................................................................................... 5 1. Lending instrument .................................................................................................... 5 2. Project development objective and key indicators..................................................... 5 3. Project components .................................................................................................... 6

4. Lessons learned and reflected in the project design ................................................... 8

5. Alternatives considered and key choices made ......................................................... 8

C. IMPLEMENTATION ............................................................................................. 9 1. Partnership arrangements ........................................................................................... 9 2. Institutional and implementation arrangements (Annex 6). ...................................... 9 3. Monitoring and evaluation (Annex 3)....................................................................... 11

4. Sustainability............................................................................................................. 11 5. Critical risks .............................................................................................................. 12

6. Credit conditions ....................................................................................................... 14

D. APPRAISAL SUMMARY .................................................................................... 14 1. Economic and Financial Analyses ............................................................................ 14

2. Technical ................................................................................................................... 14 3. Fiduciary ................................................................................................................... 14

4. Social......................................................................................................................... 15 5. Environment .............................................................................................................. 15

6. Safeguard Policies ..................................................................................................... 16 7. Policy Exceptions and Readiness.............................................................................. 16

Annex 1: Country and Sector Background .................................................................. 17

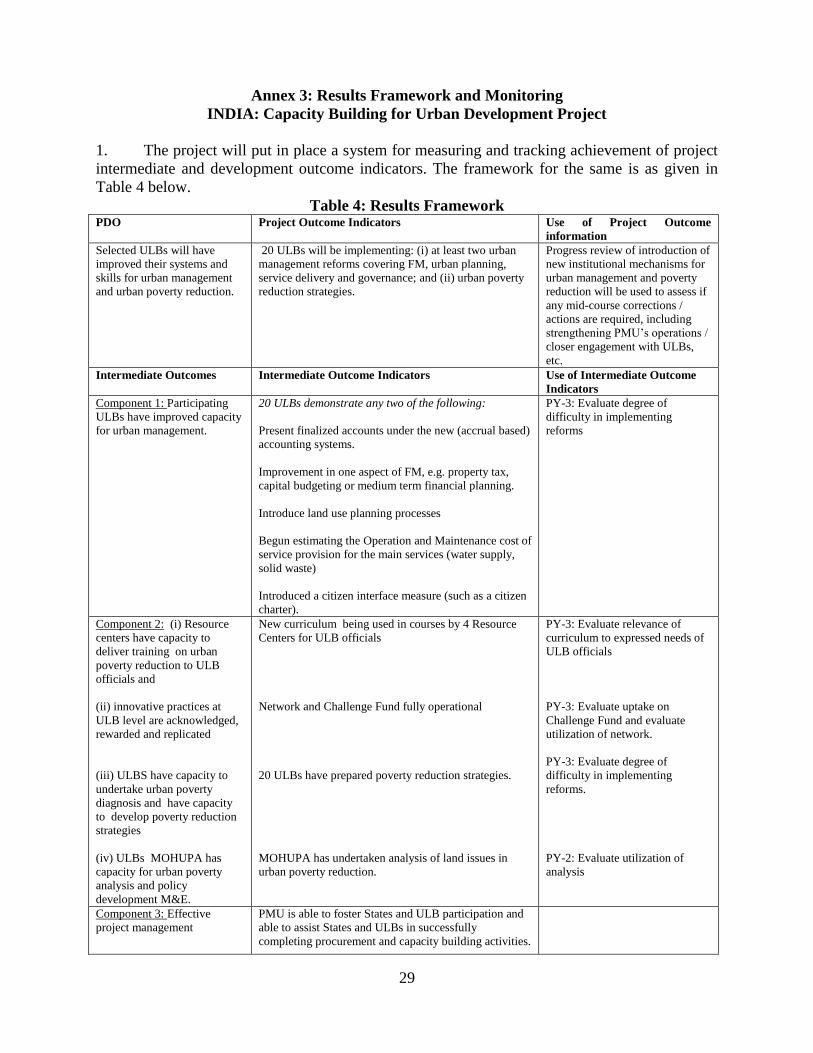

Annex 2: Major Related Projects Financed by the Bank and/or other Agencies ..... 28 Annex 3: Results Framework and Monitoring ............................................................ 29 Annex 4: Detailed Project Description .......................................................................... 33

Annex 5: Project Costs ................................................................................................... 39 Annex 6: Implementation Arrangements ..................................................................... 40 Annex 7: Financial Management and Disbursement Arrangements ......................... 43 Annex 8: Procurement Arrangements .......................................................................... 52

Annex 9: Governance and Accountability Plan ........................................................... 65 Annex 10: Economic and Financial Analysis ............................................................... 70 Annex 11: Safeguard Policy Issues ................................................................................ 71 Annex 12: Project Preparation and Supervision ......................................................... 72 Annex 13: Documents in the Project File ..................................................................... 73

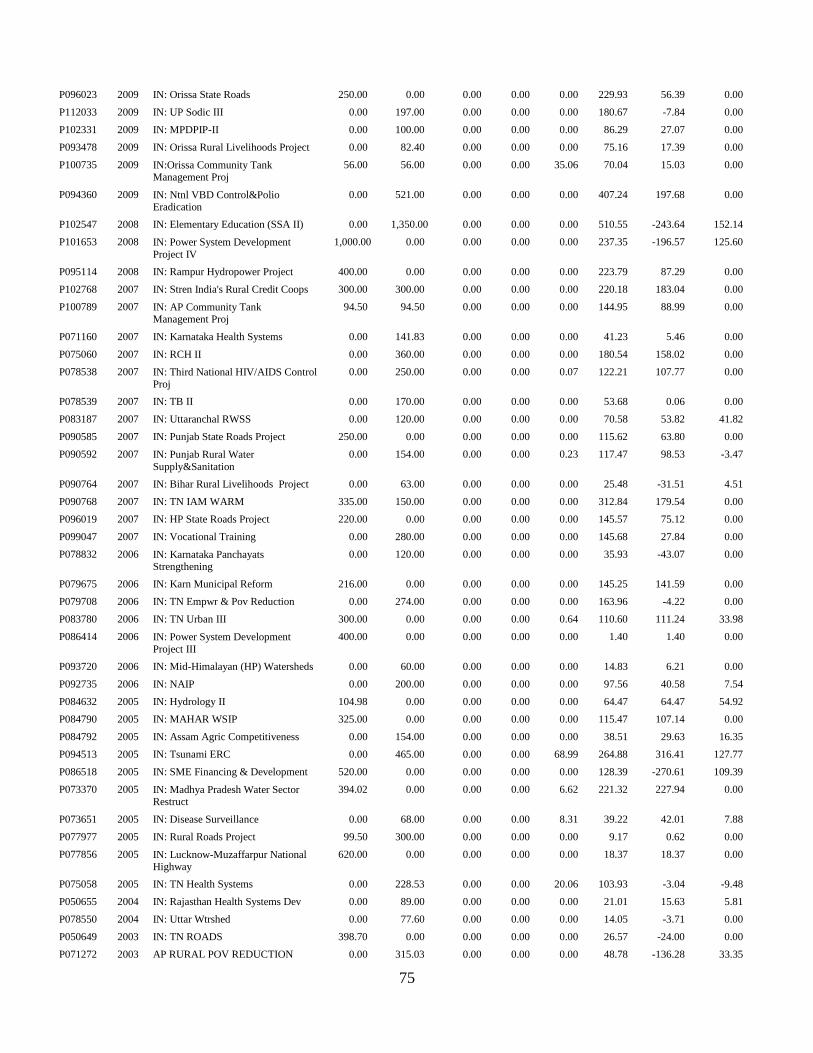

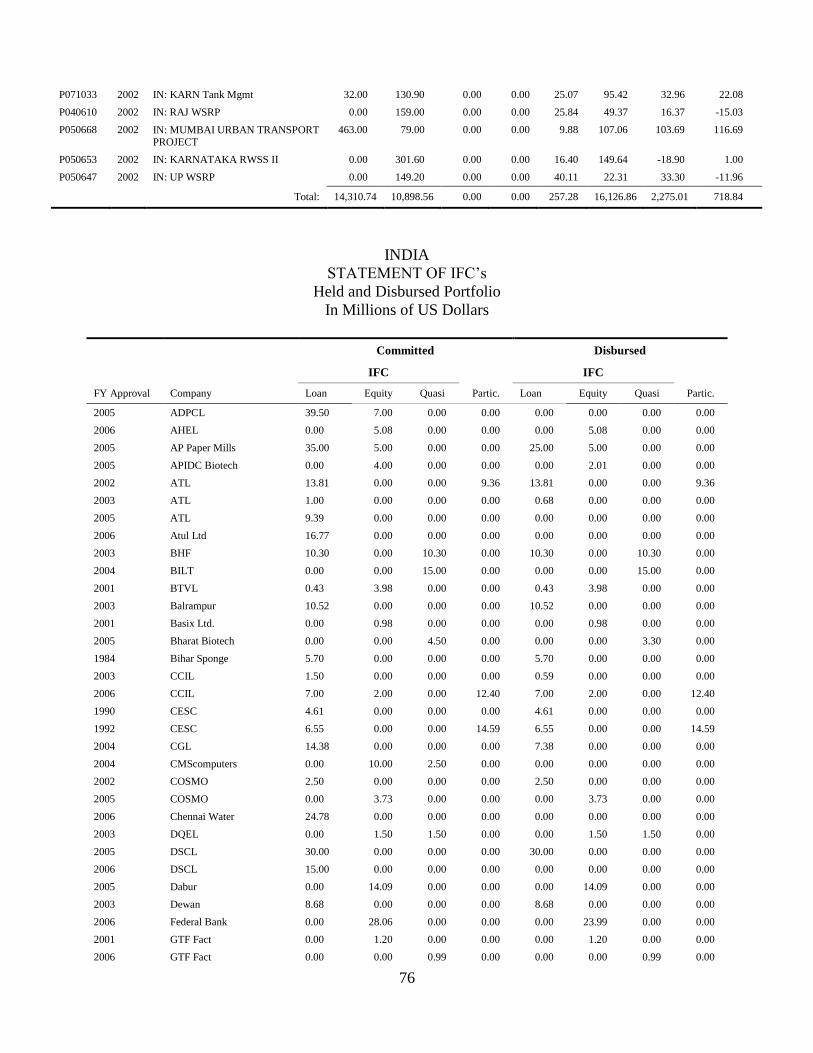

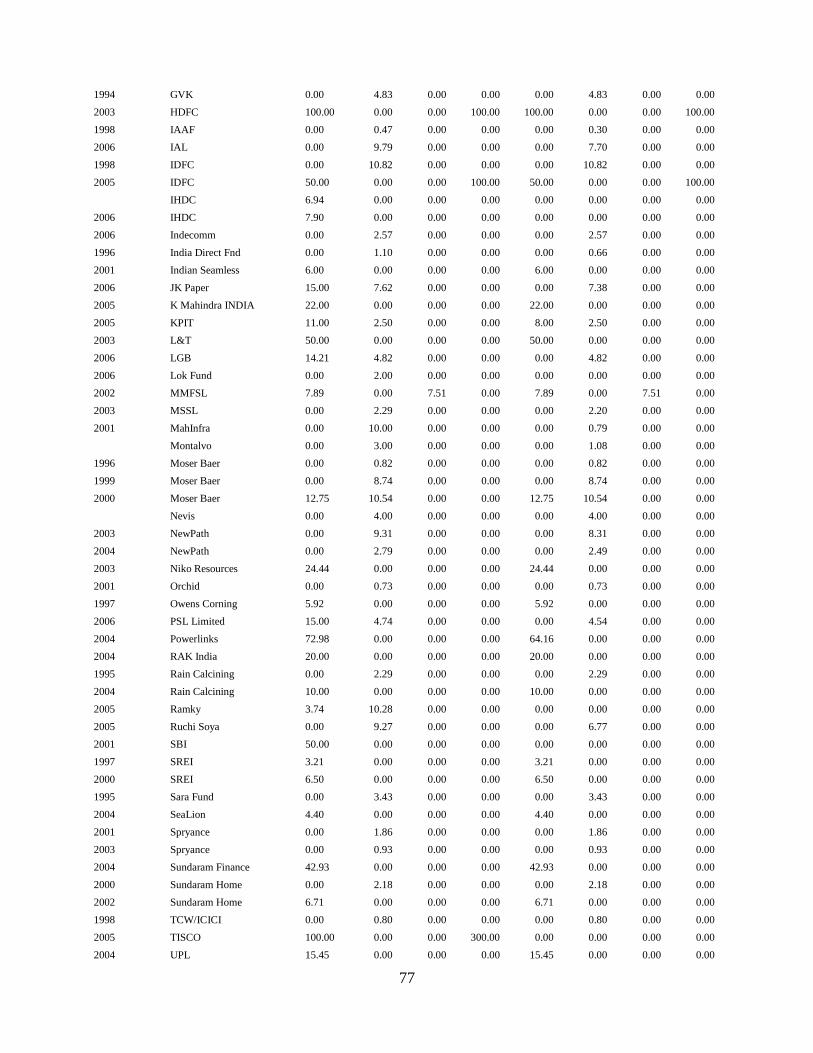

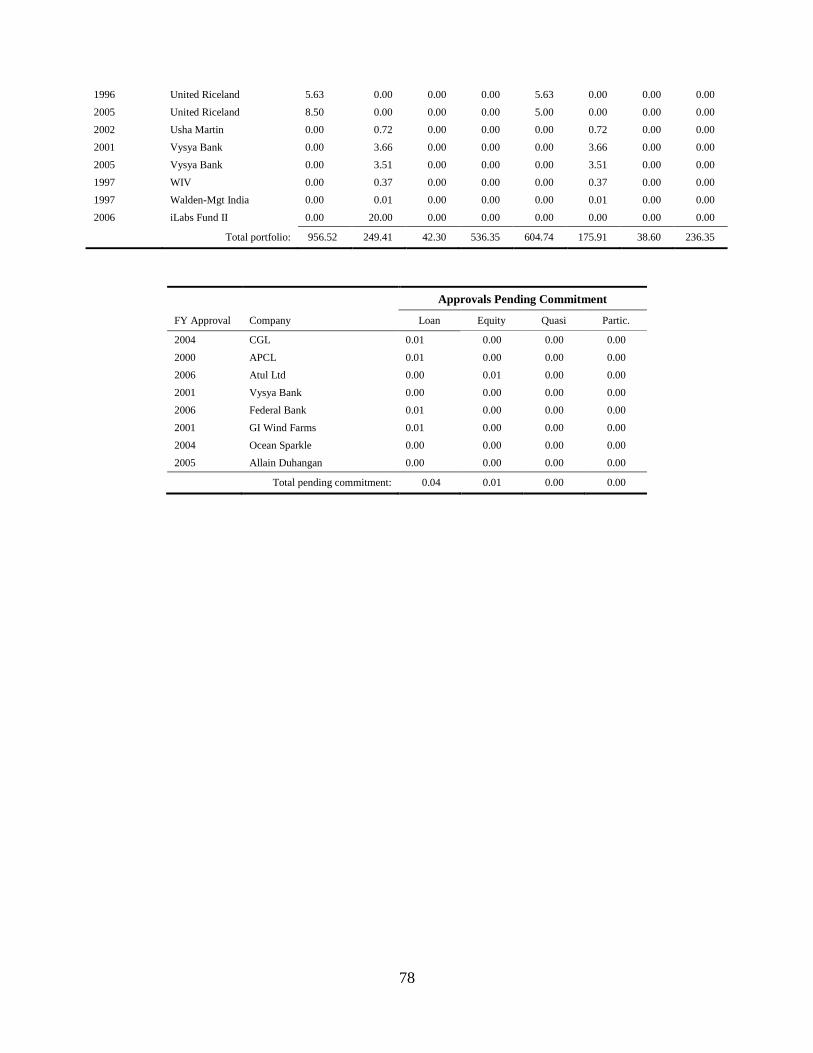

Annex 14: Statements of Loans and Credits ................................................................ 74 Annex 15: Country at a Glance ..................................................................................... 79

iii

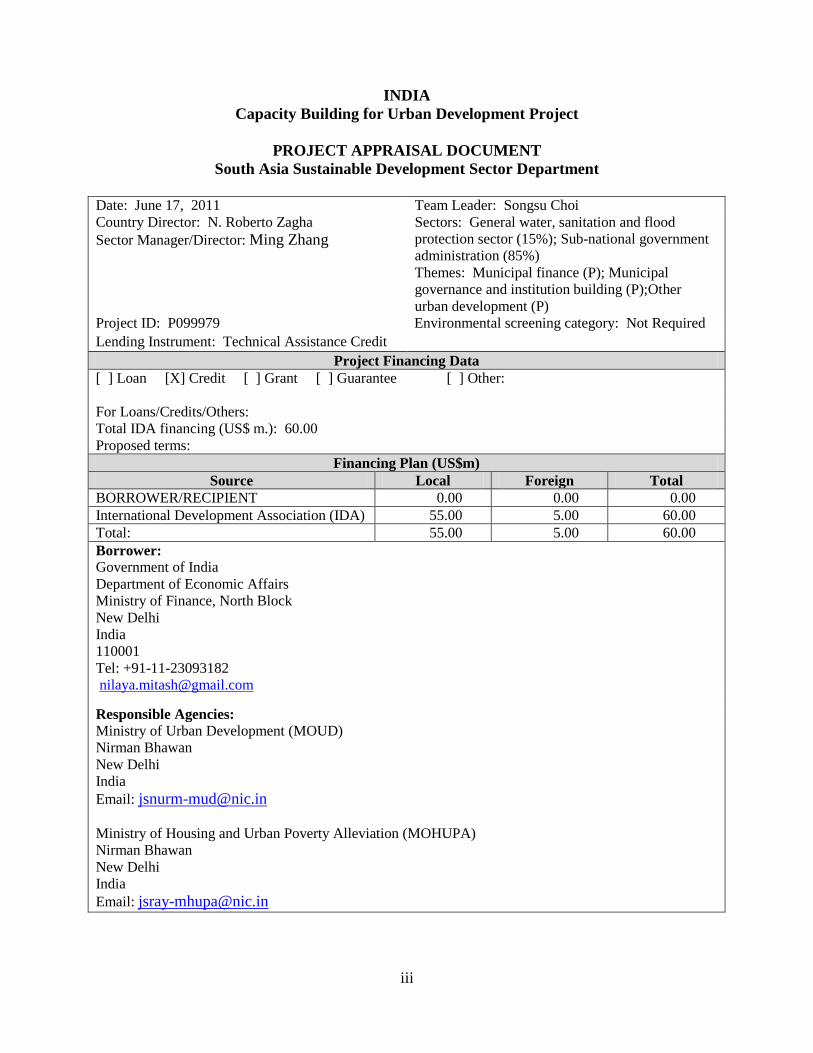

INDIA

Capacity Building for Urban Development Project

PROJECT APPRAISAL DOCUMENT

South Asia Sustainable Development Sector Department

Date: June 17, 2011 Team Leader: Songsu Choi

Country Director: N. Roberto Zagha

Sector Manager/Director: Ming Zhang

Sectors: General water, sanitation and flood

protection sector (15%); Sub-national government

administration (85%)

Themes: Municipal finance (P); Municipal

governance and institution building (P);Other

urban development (P)

Project ID: P099979 Environmental screening category: Not Required

Lending Instrument: Technical Assistance Credit

Project Financing Data

[ ] Loan [X] Credit [ ] Grant [ ] Guarantee [ ] Other:

For Loans/Credits/Others:

Total IDA financing (US$ m.): 60.00

Proposed terms:

Financing Plan (US$m)

Source Local Foreign Total

BORROWER/RECIPIENT 0.00 0.00 0.00

International Development Association (IDA) 55.00 5.00 60.00

Total: 55.00 5.00 60.00

Borrower:

Government of India

Department of Economic Affairs

Ministry of Finance, North Block

New Delhi

India

110001

Tel: +91-11-23093182

Responsible Agencies: Ministry of Urban Development (MOUD)

Nirman Bhawan

New Delhi

India

Email: [email protected]

Ministry of Housing and Urban Poverty Alleviation (MOHUPA)

Nirman Bhawan

New Delhi

India

Email: [email protected]

iv

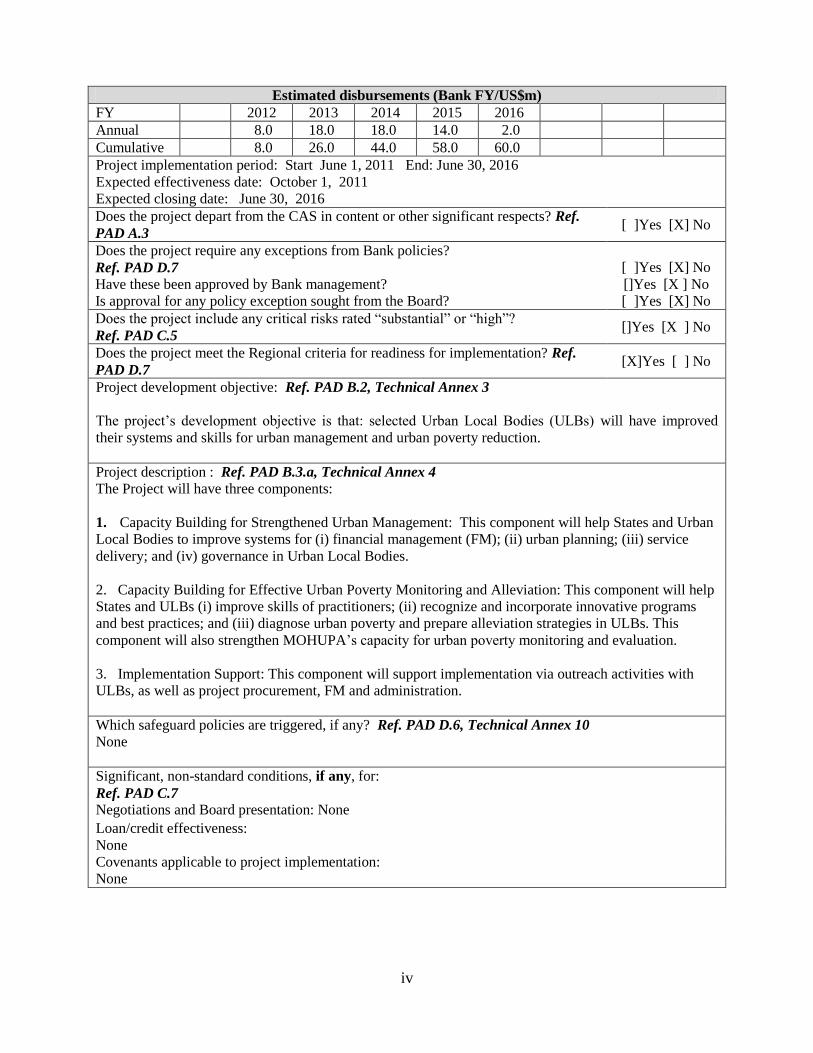

Estimated disbursements (Bank FY/US$m)

FY 2012 2013 2014 2015 2016

Annual 8.0 18.0 18.0 14.0 2.0

Cumulative 8.0 26.0 44.0 58.0 60.0

Project implementation period: Start June 1, 2011 End: June 30, 2016

Expected effectiveness date: October 1, 2011

Expected closing date: June 30, 2016

Does the project depart from the CAS in content or other significant respects? Ref.

PAD A.3 [ ]Yes [X] No

Does the project require any exceptions from Bank policies?

Ref. PAD D.7 Have these been approved by Bank management?

Is approval for any policy exception sought from the Board?

[ ]Yes [X] No

[]Yes [X ] No

[ ]Yes [X] No

Does the project include any critical risks rated ―substantial‖ or ―high‖?

Ref. PAD C.5 []Yes [X ] No

Does the project meet the Regional criteria for readiness for implementation? Ref.

PAD D.7 [X]Yes [ ] No

Project development objective: Ref. PAD B.2, Technical Annex 3

The project‘s development objective is that: selected Urban Local Bodies (ULBs) will have improved

their systems and skills for urban management and urban poverty reduction.

Project description : Ref. PAD B.3.a, Technical Annex 4

The Project will have three components:

1. Capacity Building for Strengthened Urban Management: This component will help States and Urban

Local Bodies to improve systems for (i) financial management (FM); (ii) urban planning; (iii) service

delivery; and (iv) governance in Urban Local Bodies.

2. Capacity Building for Effective Urban Poverty Monitoring and Alleviation: This component will help

States and ULBs (i) improve skills of practitioners; (ii) recognize and incorporate innovative programs

and best practices; and (iii) diagnose urban poverty and prepare alleviation strategies in ULBs. This

component will also strengthen MOHUPA‘s capacity for urban poverty monitoring and evaluation.

3. Implementation Support: This component will support implementation via outreach activities with

ULBs, as well as project procurement, FM and administration.

Which safeguard policies are triggered, if any? Ref. PAD D.6, Technical Annex 10

None

Significant, non-standard conditions, if any, for:

Ref. PAD C.7

Negotiations and Board presentation: None

Loan/credit effectiveness:

None

Covenants applicable to project implementation:

None

1

A. STRATEGIC CONTEXT AND RATIONALE

1. Country and sector issues

1. Background and key sector issues. Indian Urban Local Bodies (ULBs) play a

particularly important role in the country‘s economic life, with about sixty percent of India‘s

Gross Domestic Product (GDP) produced in urban agglomerations. Though the urban population

represents only twenty eight percent of the total population, India counts three of the world‘s

twenty-one mega-ULBs (Mumbai, 19mn; Delhi, 15mn; Kolkata, 14mn). Four other ULBs have a

population between four and ten million (Chennai 6.5mn; Hyderabad 5.7mn; Bangalore 5.7mn;

and Ahmedabad 4.05mn) and twenty eight other ULBs have a population between one and four

million. In total there are over 5,000 ULBs, 300 of which have a population greater than

100,000. Looking to the future, the urban population is expected to increase from 282 million in

2000 to 590 million people in 2030. Larger ULBs will continue to look for ways to strengthen

their participation in the global economy, while smaller ULBs will absorb most of the rural-

urban migration and seek to strengthen linkages to the rural economy.

2. Indian policy makers face two key challenges in achieving the benefits associated with an

urban agglomeration economy: (i) managing the urban space and (ii) alleviating urban poverty.

3. Managing the urban space. While Indian ULBs continue to attract millions of people,

they have not fully achieved the development and economic benefits that urbanization could

bring. This is evident from the high land prices, inadequate housing, congestion and weak

service delivery in urban areas. Today, Indian ULBs are becoming centers of economic growth

and yet have challenges of poverty alleviation. International benchmarks show Indian ULBs to

be lagging on service delivery, and few Indian ULBs are creditworthy to access capital markets

for funds for urban infrastructure. The areas that require urgent focus are water supply and

sanitation, urban transportation, environment, affordable housing and the development of the

capacity of ULBs to function successfully in a decentralized environment. Slums (informal

settlements) have grown very fast over the last two decades, reaching about twenty five percent

of urban housing over the last two decades. In some ULBs, such as Mumbai, the slum population

is over one half of the total. These impediments are the result of weaknesses in the policy,

financing and institutional frameworks that govern key aspects of urban management, i.e. urban

finance, land use planning and regulation, and service delivery. Together, they negate the

benefits of agglomeration economies in Indian ULBs by distorting land and housing markets,

rendering ULBs non-creditworthy, and leaving them with expensive, yet poorly functioning,

urban services.

4. Weak finances: ULBs suffer from a range of financial constraints: (i) a lack of buoyant

and dynamic revenue streams, inadequate and poorly mobilized local revenues (e.g. property tax,

user charges) and inadequate fiscal transfers from higher levels; (ii) weak asset/liability

management; (iii) inadequate financial management (FM), assurance and information systems,

and; (iv) non-transparent subsidy mechanisms. These foster a dependency on concessional or

public finance. In principle, central and state support for ULBs is supposed to be matched by

contributions from own source revenues and funds leveraged from private sector lender. In

reality though, local revenue sources like property taxes and user charges are not effectively

raised, and access to market finance is limited as ULBs lack credibility with potential lenders.

2

5. Outdated planning: Urban planning frameworks are weak in many local governments.

Planning is often done by multiple agencies with overlapping responsibilities and inadequate

coordination between them. Counterproductive urban planning regulations, including rigid

master plans, zoning regulations, floor space indexes (FSI) and development controls are overly

restrictive with respect to densities and spatial structure. Additionally, planning and land use

management weaknesses are at the core of slum formation: (i) current land use and spatial

planning (and enforcement) practices limit the supply of land available for building; and (ii)

building regulations (e.g. floor space requirements) limit the density and supply of homes. At the

same time, urban expansion and renewal often calls for restructuring city space, thus requiring

redevelopment of existing settlements and activity zones. Resettlement is not adequately

integrated into urban planning and appropriately factored into urban development institutions.

Urban planning has also traditionally been approached through a top-down, narrow sectoral

perspective. This has omitted topics such as environmental health and broader quality of life

issues. These need better integration into the planning framework and decision making process.

Further, an approach that includes the ULB and urban citizens as the key players in the planning

process needs to be evolved.

6. Weak service delivery institutions (Water and Sanitation Services, Solid Waste

Management): In the current institutional structure there is considerable overlap in responsibility

for the functions of policy making, regulation and service provision. These require accountability

and performance improvement. Service delivery is usually provided by departments within the

city administration, which often are not financially independent, client-oriented or professionally

specialized. There is a strong bias toward providing physical infrastructure (pipes, vehicles,

collection bins) rather than providing financially and environmentally sustainable services to

urban areas. Basic services are hampered by financial weaknesses, due to an inability to recover

operations and maintenance (O&M) costs, as a minimum, from users and inefficiencies in

service provision. Though under the Jawaharlal Nehru Urban Renewal Mission (JnNURM, see

below) service level benchmarks have been introduced, the weak capacity of the ULBs is an

impediment in the realization of optimum service delivery levels and efficiencies.

7. Governance and Intergovernmental constraints: The 74th

Constitutional Amendment Act

of 1993 (CAA) gives urban local bodies an independent status within the Constitution, with a

key role to play in the provision of services. Nevertheless, systemic institutional weaknesses

continue to be a challenge. The 11th

Plan (Approach Paper, December 2006) cites the need for

good governance and transparency. In the urban sector specific governance challenges affect

performance. ULBs lack functional jurisdiction as responsibilities for urban services are

fragmented and overlap considerably across state and local agencies leading to a lack of

coordination. In many states, devolution of functions and responsibilities from states to ULBs

has been done, but the transfer of funds and functionaries is partial and limited, while fiscal

dependence on state governments remains high. Most Municipal Acts do not provide appropriate

incentives for accountability. Citizen involvement in city decisions is low and needs further

improvement in transparency and a systematic approach. The reforms under JnNURM,

especially the Community Participation Law, and the introduction of an e-governance system are

some of the initiatives taken by Government of India (GoI) to enhance participation and

transparency in urban local bodies.

8. Alleviating urban poverty. Following national poverty trends, urban poverty has

decreased steadily over the last 25 years, but the absolute numbers of urban poor continue to

3

grow. Urban poverty rates declined from 43.6 percent in 1983 to 25.7 percent in 2005 (NSSO

1983-84 and 2004-05 rounds). This decline in total and urban poverty incidence has been

accompanied by an ―urbanization of poverty‖, as the urban poor account for a larger fraction of

the total poor today than they did decades ago. This phenomenon, combined with overall

population growth, has translated into increasing numbers of urban poor. Vulnerability—

understood as the extent of susceptibility to poverty—has also increased in urban areas as a

result of the rising pressure on urban amenities and facilities, growing informality in the labor

market and the erosion of traditional informal support networks.

9. Determinants of urban poverty and vulnerability. Urban poverty is a complex

phenomenon and there are specific characteristics of poverty and deprivation that are particular

to the circumstances in which the urban poor live. Although far from constituting a homogenous

group, the urban poor and vulnerable are generally characterized by a greater income volatility

associated with informal employment, higher exposure to shocks arising from expenditure

shocks such as increases in prices or expenditure on health needs, insecure living conditions, and

poor service delivery compared to their rural counterparts.

10. Access to social services among the urban poor. Quality of social service delivery is

generally poor in urban areas due to a variety of reasons. On the supply side, inadequate

institutional arrangements, insufficient financing, and poor quality and quantity of inputs

provided are important factors. On the demand side, factors affecting social service access

include limited awareness about the availability of services, differing levels of ‗urban literacy‘

(familiarity with local language, common urban technologies and institutions and prior

experience among the users of facilities), and the relatively high (implicit and explicit) costs of

different services.

11. Access to social protection programs among the urban poor. While India has a range of

central and state-specific social protection programs, the urban social protection system has been

traditionally less focused and consequently, under financed.

12. Government’s urban development strategy. The Government‘s overarching urban

development objective is to create economically productive, efficient, inclusive and responsive

ULBs, by focusing on six strategic outcomes: (i) universal access to a minimum level of

services; (ii) establishment of city wide frameworks for planning and governance; (iii) modern

and transparent budgeting, accounting and FM; (iv) financial sustainability for ULBs and service

delivery institutions; (v) utilization of e-governance; and (vi) transparency and accountability in

urban service delivery and management.

13. The Government‘s flagship urban development program is the Jawaharlal Nehru National

Urban Renewal Mission (JnNURM), which was launched in December 20051. The Mission

targets 65 ULBs (7 with populations greater than 4 million, 28 greater than 1 million and 30

other ULBs of religious, historic or tourist importance). JnNURM is reform and incentive based:

1 Concurrent with the two sub-missions of JNNURM i.e. UIG and BSUP, the Government launched the Urban

Infrastructure Scheme for Small and Medium Towns (UIDSSMT), with a similar policy and investment design,

covering all ULBs/towns as per 2001 census except those covered under JNNURM. Similarly, the MOHUPA runs

the Integrated Housing and Slum Development Program (IHSDP), with a similar policy and investment design as

BSUP, covering all ULBs/towns as per the 2001 census except the 65 mission ULBs of JNNURM. Throughout the

PAD references to JNNURM reforms are understood to include UIDSSMT and IHDSP.

4

in return for a commitment to adopt the obligatory reforms over a period of seven years, ULBs

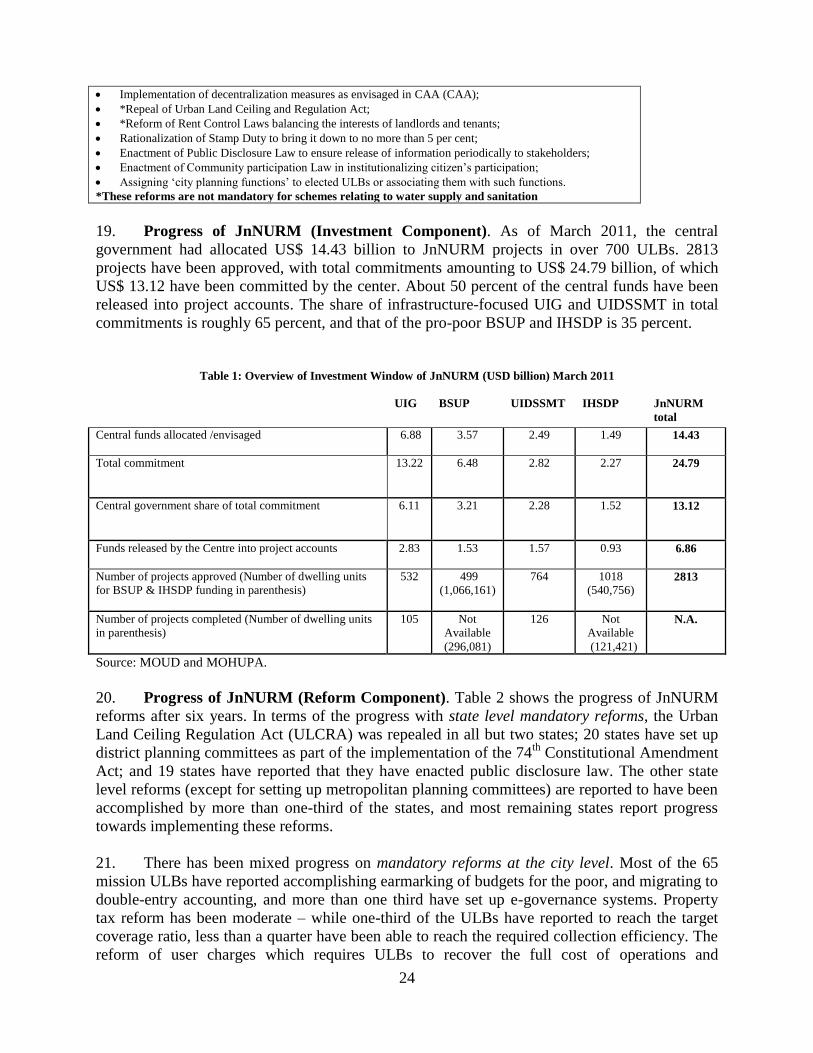

may access funds for investment and capacity building. As of March 2011, the Government of

India (GOI) had committed to provide up US$ 14.43 billion in federal resources for these

investments for qualifying ULBs a seven year period. States and ULBs are then expected to

match the federal grants from own-source funds, the capital markets, public private partnerships

(PPP), and bilateral and multilateral agencies. The investment component of the Mission consists

of two sub-missions: (i) Urban Infrastructure and Governance (UIG), implemented by the

Ministry of Urban Development (MOUD), with investments including (a) water, sanitation,

sewerage and drainage; (b) solid waste management (SWM); (c) urban transport; (d) street

lighting; and (e) environmental protection; and (ii) Basic Services to the Urban Poor (BSUP),

implemented by the Ministry of Housing and Urban Poverty Alleviation (MOHUPA), with

investments supporting integrated development of slums. More recently GOI launched the Slum-

free City Planning Scheme (SFCP) of Rajiv Awas Yojana (RAY) a scheme working towards the

goal of a slum-free India.

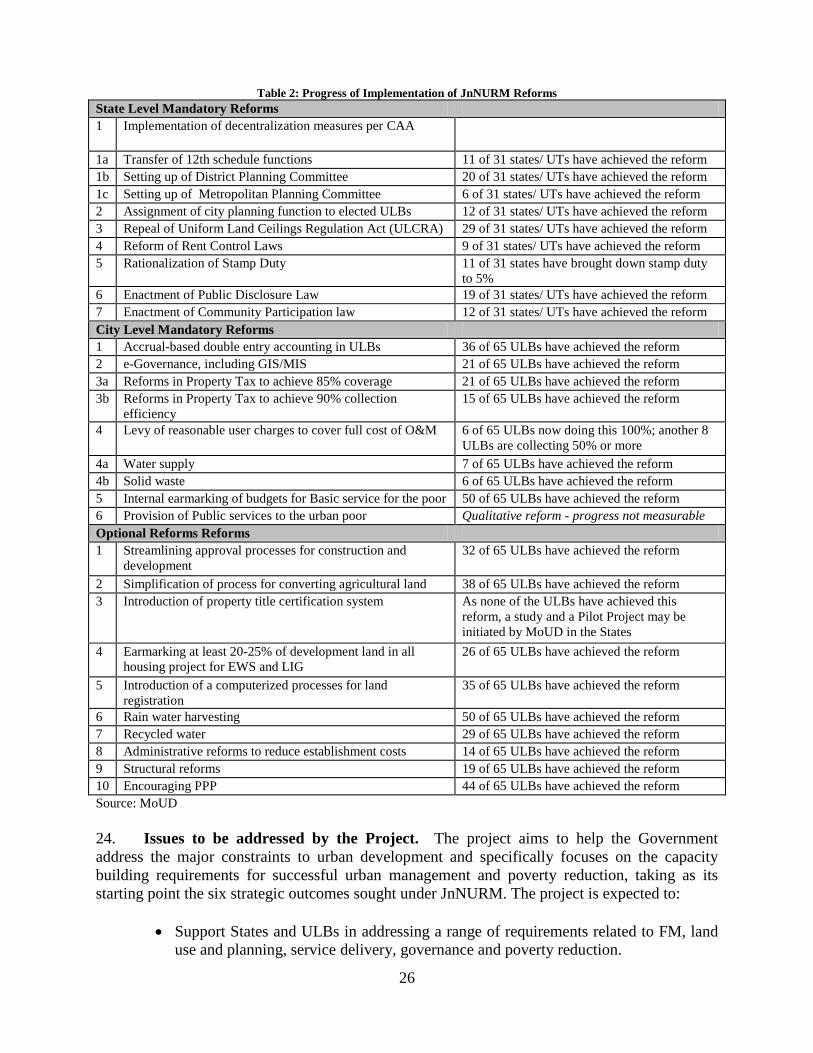

14. The essential building block of JnNURM is the reform program. The major element of

the mandatory reform program relates to urban management; (i) adoption of modern accrual-

based double entry system of accounting; (ii) introduction of a system of e-governance using IT

applications, such as Geographic Information Systems (GIS); (iii) reform of property tax; and

(iv) levy of reasonable user charges for municipal services. In addition, the JnNURM has been

designed to assist in pro-poor development of Indian ULBs by enabling the provision of basic

services to the poor and supporting integrated development of slums. These include: (i) internal

earmarking of at least 25% funds within local body budgets for basic services to the urban poor;

(ii) reservation of at least 20-25% of developed land in all housing projects (both public and

private agencies) for Economically Weaker Sector (EWS)/ Low Income Group (LIG) category

with a system of cross-subsidization; and (iii) States and ULBs are required to formulate and

adopt an overarching policy on the provision of basic services to the urban poor addressing the 7-

point charter pertaining to: provision of security of tenure at affordable prices, improved

housing, water supply, sanitation, education, health and social security; the last three are to be

tackled in convergence with departments dealing with education, health and social security as

applicable. These reforms have been introduced to ensure that a dedicated budget is created at

the city and state level for urban poverty alleviation and slum upgrading; the urban poor have

access to land and are not squeezed out of the housing market due to mounting land prices; and

that poor are systematically provided with basic services based on agreed milestones.

15. The weak capacity in ULBs, however, is slowing the implementation of both the urban

management and poverty reduction reforms in many Mission ULBs, and thus hampering the

achievement of the strategic outcomes sought by the Government. The scope and complexity of

these urban capacity challenges is only now emerging. Many ULBs need a comprehensive

package of assistance covering both urban management and poverty reduction. Others,

particularly large urban areas, need more targeted assistance, e.g. in revenue management,

capital budgeting or tariff design. While ULBs generally have a good understanding of the need

to introduce reforms, many lack the capacity to prepare a credible step by step implementation

plan to carry out the reforms. While the high level officials like Municipal Commissioners are

often drawn from the national and State level administrative services and have considerable

technical expertise and public administration backgrounds, many ULBs lack staff with the

specialized professional training relevant to the management of ULBs and the services they need

to offer. This is not only a matter of project management capacity, but also of the lack of systems

5

and policy tools to take strategic decisions, plan ahead, involve citizens, and monitor services.

Basic information on the poor in ULBs is lacking, and systems are under developed to either

improve the information or ensure that it gets strategically interpreted and utilized. There is also

a tendency to treat urban poverty separately from the wider development of ULBs, which results

in short-term and fragmented interventions, rather than strategic city-wide plans and approaches,

and the systems to implement them. Most municipal officials have had little exposure to

domestic and international best practices, which hampers the professionalization of ULB

management.

2. Rationale for Bank Group Involvement

16. CAS linkage. The project is consistent with the Bank Group Country Strategy (CAS)

discussed by the Executive Directors on December 11, 2008. The CAS aims to foster rapid and

inclusive growth, sustainable development and service delivery. The proposed project would

directly contribute to these CAS objectives by strengthening capacity for urban management and

poverty alleviation, and by improving learning and innovation systems related to urban

development.

17. Rationale for Group involvement. The critical issue now for India‘s urban sector is to

implement a complex process of policy reform, institutional capacity, and investments through

the third tier of government in urban areas i.e. the ULBs. The Bank is already providing support

to urban development through lending, advisory work and knowledge building activities, and has

on-the-ground experience of the main capacity constraints. Bank support for the project links this

wide ranging experience directly with the Government‘s flagship programs for urban

development. In doing so it supports the development of a requisite framework for action on

capacity development that will assist the planning, delivery and monitoring of these efforts in

India‘s ULBs.

3. Higher level objectives to which the project contributes

18. The project will contribute to the achievement of GOI‘s objective of creating

economically productive, efficient, equitable, inclusive and responsive ULBs. Achieving this

objective will help sustain high rates of economic growth, accelerate poverty reduction, and

improve services, especially to the urban poor.

B. PROJECT DESCRIPTION

1. Lending instrument

19. The lending instrument proposed is a free standing Technical Assistance (TA) Credit.

2. Project development objective and key indicators

20. The project‘s development objective is that: selected ULBs will have improved their

systems and skills for urban management and urban poverty reduction. Successful completion of

this project will result in: (i) more ULBs are able to better plan and manage resources and

services; (ii) more ULBs are equipped to analyze local conditions and formulate comprehensive

poverty alleviations strategies; (iii) more ULBs have access to knowledge and best practices on

urban development and (iv) urban poverty policies and program guidelines that are informed by

6

international and domestic best practices and by data that has been systematically collected and

analyzed.

21. The project will target 20 ULBs looking to improve both urban management and

poverty reduction. A demand-driven approach is part of the project design, which is manifested

in an element of self-selection among the ULBs. Notwithstanding this, regional variation will be

sought, as will variation in city size. Similarly, lagging states may be targeted, though this will

be subject to some constraints as some of these states have small urban populations and others

are already receiving assistance from other donors. A certain amount of state clustering will also

be incorporated for greater efficiency in implementation, and to improve ULB-level capacity for

participating in the intergovernmental finance system. Finally, depending on local circumstances

and expressed need, additional ULBs may participate in the project and opt for more targeted

interventions, e.g. capacity building only for service delivery.

22. A detailed results framework to measure the impact of capacity building activities has

been designed as part of the project and is presented in Annex 3. The project outcome will be

that: 20 ULBs will be implementing (i) at least two urban management reforms, covering FM,

urban planning, service delivery and governance; and (ii) urban poverty reduction strategies.

3. Project components

23. The project will have three components.

(i) Capacity Building for Strengthened Urban Management (US$37.5 million). This

component will support TA across several urban management topics. ULBs will select the

desired package of assistance, based on an assessment of needs which will be undertaken with

support from the Project Management Unit (PMU, see below). This demand driven, menu

approach is in response to the variable capacity building needs faced by ULBs.

Financial and FM Reform: The project would support ULBs in the key areas of

improving budgeting and planning, expenditure management, procurement planning and

execution, revenue mobilization (including property tax, development charges and user

charges), asset/liability management, accrual accounting, internal controls, auditing, FM

information systems, procurement, capacity enhancement of municipal accountants, and

IT standardization. Implementation and operational planning including developing

strategies for project execution, and monitoring and review including effective quality

control procedures will also be supported.

Framework for Urban Planning: The project would support ULB reforms to the urban

planning process and land management, including pro-poor planning approaches.

Service Delivery: The project would support institutional design in ULBs for service

delivery, tariff and subsidy design, the financing framework (including access to capital

markets, public private partnerships (PPPs), and carbon finance), service delivery for the

poor, strengthening project planning, implementation, performance planning and

benchmarking, and monitoring, training and professionalization of service delivery and

efficient management of social impacts.

7

Framework for Governance: The project would seek to improve the quality of the

interactions between local officials and citizens through support for citizen awareness and

participation (e.g. citizen scorecards, stakeholder forums government) and skills

development for elected officials. In addition, to improve transparency, public

consultations, citizens‘ forums and measures such as disclosure of finalized audited

financial statements would be supported.

(ii) Capacity Building for Effective Urban Poverty Alleviation and Monitoring ($18.5 million) These capacity building initiatives reflect the need to strengthen MOHUPA, share urban poverty

alleviation experiences, and design strategies on urban poverty alleviation. It is anticipated that

this component will further assist in the effective implementation of RAY.

Challenge Fund for Urban Poverty Alleviation. Grant funding will be provided to ULBs

working on urban poverty alleviation via two windows: (i) to recognize and award

particularly innovative practices in this area; and (ii) to government departments and

institutions and parastatals interested in adopting and scaling up one or more of the ―best

practices‖ identified through the first window. The sub-component will also provide

funding for the administration of the Challenge Fund.

Creation of a Practitioners Network. Support will be provided to the Challenge Fund to

constitute a network of practitioners with the objective of promoting information sharing

and capacity building. The network will include government officials from the selected

ULBs, academics and other actors active in the area of urban poverty alleviation both

nationally and internationally, and is envisioned to serve as a platform for both peer-to-

peer learning and the delivery of formal training. The network will also facilitate the

dissemination and discussion of best practices identified and/or developed through the

Challenge Fund.

Development of Training Materials on Urban Poverty and Service Delivery. Support will

be provided to 4 National Resource Centers to develop training modules on urban

poverty reduction and service delivery.

Preparation of ULB level Poverty Reduction Strategies. Support will be provided to

ULBs to prepare diagnostics and poverty reduction strategies which build upon the

existing and future planning instruments such as City Development Plans and Slum-free

City Action Plans. Support will also be provided to improve databases and other tools

needed for targeting and monitoring of service delivery in urban areas.

Strengthening of MOHUPA: The technical assistance will support policy analysis and

development as well as build a comprehensive monitoring and evaluation (M&E) system

in MOHUPA in coordination with the Resource Centers and ULBs.

(iii) Implementation Support (US$4 million):

This component will support a national PMU for providing overall technical and

managerial assistance during implementation. The PMU will assist in supporting the

project, in the areas of (i) pipeline development; (ii) quality assurance; (iii) procurement

8

and procurement advisory services; (iv) FM; (v) reporting; (vi) M&E; and (vii) project

administration.

4. Lessons learned and reflected in the project design

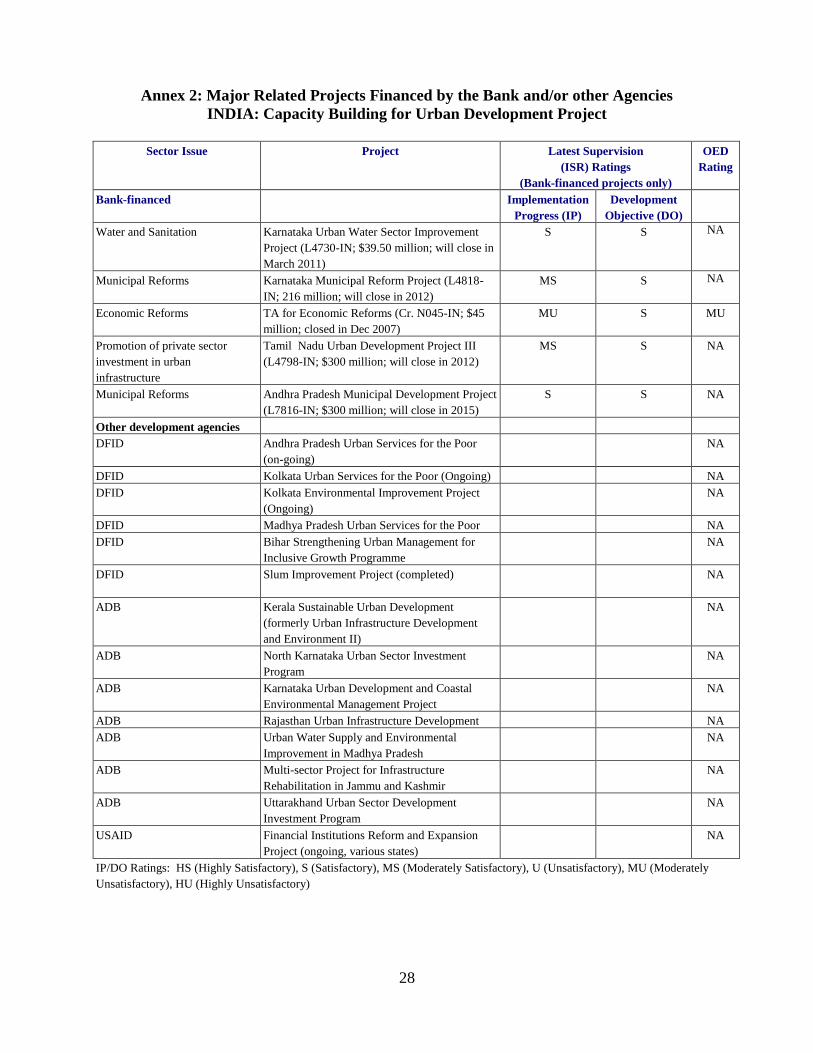

24. Past Bank-financed urban development projects in India focused on asset creation and

expanding access to services. The current Bank projects take a different approach, recognizing

that policy reform and institutional capacity must be addressed in a comprehensive fashion to

ensure the efficiency and effectiveness of investments in infrastructure and service delivery.

(Karnataka Municipal Reform Project, approved March 2006; $216mn; Third Tamil Nadu Urban

Development Project, approved July 2005; $300mn; Karnataka Urban Water Sector

Improvement Project, approved July 2005; $39.5mn; Andhra Pradesh Urban Reforms and

Municipal Services Project, approved Dec 2009; $300mn). Though the Capacity Building for

Urban Development project focuses exclusively on institutional development, it also reflects the

essential lesson of linking project activities to the larger policy framework.

25. Technical Assistance projects (TA) projects have had mixed results for several reasons:

(i) over-ambitious and complex designs have hampered the achievement of development

objectives; (ii) weak links to reform programs have weakened the results chain; and (iii) supply

driven TA has resulted in low demand. The project has incorporated these lessons into the

design. This project focuses on achieving outcomes in selected ULBS, where those outcomes

are linked to the aims of the GOIs flagship programs. The implementation design also calls for

the PMU to undertake significant outreach activities to ensure that States and ULBs are taking

advantage of capacity building opportunities under the project. Additionally, where "process

steps" involved for accessing TA are cumbersome, disbursements may fail to meet expectations

and the effectiveness of intervention may be diluted. Involving multiple tasks and agencies may

result in delays in reaching physical and financial targets. The design of the project framework

seeks to streamline the management of numerous requests to allow easy access and fast

disbursement of the TA funds.

5. Alternatives considered and key choices made

26. Flexible multi-sector v. single-sector: Given the inter-linked, multi-sectoral range of the

reform challenges facing the urban sector, a single sector design (e.g. service delivery) was

considered too narrow and restrictive. To enhance the sustainability of this initiative, the design

of the facility is diversified, multi-sectoral and open to States and ULBs that fit within the terms

of the agreed development/ reform agenda. 27. State and ULB focus: Consideration was given to focusing project outcomes on

improving capacity in the States as well as ULBs. While it was agreed that States may need to

enhance capacity, it was decided to orient project outcomes to ULBs, where capacity weaknesses

are sharpest.

9

C. IMPLEMENTATION

1. Partnership arrangements

28. The project has been developed within a capacity building framework in which other

donors are currently participating. The Water and Sanitation Program (WSP) and the World

Bank Institute (WBI) have participated in the conceptualization and design of the project, and,

through their regular programs, will support complementary capacity building activites during

implmentation. Other bilateral donors (Asian Development Bank (ADB), German International

Cooperation (GIZ), and United States Agency for International Development (USAID) also have

complementary capacity building programs under way.

29. The UK Department for International Development (DFID) has been particularly active

in capacity building, especially in lagging states. Building on these lessons learned, it has

committed approximately US$20 milliion to support a policy unit in MOHUPA, the

development of state and ULB poverty reduction units, skills development for local officials and

the development of pro-poor approaches on finance, planning and service delivery. These

proposals are complementary to the World Bank Group‘s proposed project, particularly to help

forge the state-local linkages required to approach the local government challenges in a federal

system.

2. Institutional and implementation arrangements (Annex 6).

30. Following current practice, MOUD and MOHUPA will be the implementing agencies

under the project, with specifically designated accountabilities. The respective Joint Secretaries

(JnNURM Mission Director for MOUD and RAY for MOHUPA1) from the two ministries will

be the Project Directors (PDs). The project will be implemented through a structure of two

Programme Management Boards (PMBs), each chaired by the respective Secretary of MOUD

and MOHUPA, and also comprising representatives from the Department of Economic Affairs

(DEA) and the Planning Commission. Each PMB will provide overall oversight and guidance, as

well as approve major work plans and activities, for each component under the responsibility of

the respective Ministry (see below). Each PMB will be supported by a Project Steering

Committee (PSC), which will be chaired by the respective Joint Secretaries from each ministry,

and will also have representation from the DEA and the Planning Commission. Both the PSCs

will in turn be assisted by a single common national level PMU, which will be established under

the project for providing technical and managerial assistance during project implementation

servicing and reporting to both ministries via their respective PMBs and PSCs. The

organizational schematic for the project is shown in the chart below and detailed implementation

arrangements are summarized in Annex 6.

1 After the present JnNURM Mission period is over the MoUD may nominate an officer not below the rank of Joint

Secretary.

10

Chart: Implementation Arrangements

31. The project will associate with States and ULBs that are eligible for JnNURM, IHSDP,

UIDSSMT and RAY support. In practice, as noted above, the participating States and ULBs will

be selected to achieve a mix of large and small ULBs, as well as regional variation.

32. Component 1: Capacity Building for Strengthened Urban Management. Implementation

of this component will be under the purview of MOUD, utilizing its PMB and PSC. Proposals

for TA under this component will be reviewed by MOUD and sanctioned by its PMB. In

reviewing these proposals MOUD will draw on the PMU. The MOUD may also call upon State

Level Nodal Agencies (SLNAs, which already exist under JnNURM) to assist the ULBs in

preparing capacity building projects and advising on procurement. This role is already within the

purview of the SLNAs. Once the technical sanction for the TA proposals are received from the

PSC and MOUD agrees to fund such proposals, MOUD would sign an MOU1 with the States

and ULBs which would outline the following key areas: (i) objective of the study; (ii) expected

outcomes; (iii) estimated cost and timeline; (iv) reporting requirements and (v) procurement and

FM arrangements including the process of selection of consultants, certification of work,

evaluation of the reports and outputs, and payment arrangements.

33. Component 2: Capacity Building for Effective Urban Poverty Monitoring and

Alleviation. This component will be under the purview of MOHUPA, utilizing its PMB and

PSC. Proposals for TA under this component will be reviewed by MOHUPA and sanctioned by

its PMB. Four resource centers will also be selected by MOHUPA on the basis of an evaluation

1 The MOU format would be designed by the Ministries within three months of project launch. The sample MOU

would be used as a base document and would be customized according to the relevant proposals.

11

of capacity and experience, and thus will oversee the development and installation of the training

modules in these institutions. Other activities associated with ULBs – Challenge Fund,

development of a practitioner‘s network, and poverty reduction strategies – will also be overseen

by MOHUPA and directed at the same target group of participating ULBs. Once the technical

sanction for the TA proposals are received from the PSC and MOHUPA agrees to fund such

proposals, MOHUPA would sign an MOU with the State and ULBs which would outline the

following key areas: (i) objective of the study; (ii) expected outcomes; (iii) estimated cost and

timeline; (iv) reporting requirements and (v) procurement and FM arrangements including the

process of selection of consultants, certification of work, evaluation of the reports and outputs,

and payment arrangements.

34. The Challenge Fund would be provided to entities based on the wining proposal as

approved by the Ministry as per the procedures agreed with the Bank. A sub-financing

agreement would be entered between the beneficiary and the Ministry which will govern the

usage of proceeds.

35. Component 3: Implementation Support. To strengthen the quality of the capacity building

proposals and the achievement of desired outcomes, and to improve internal controls, the project

will draw on the services of a Project Management Unit that will be financed under the project to

augment the capacity of both Ministries to manage the project. The PMU will provide

comprehensive management and administrative support to MOUD and MOHUPA for this

project. Quarterly work plans and implementation reports in respect to Component 1 will be

prepared by the PMU for the review and approval of the Joint Secretary (Mission Director)

MOUD/PD, CBUD Project. Similarly, for Component 2, quarterly work plans and

implementation reports will be submitted to the Joint Secretary (RAY) MOHUPA/PD, CBUD

Project. The TOR of the PMU include: (i) implementation support, including startup and pipeline

development; (ii) technical advisory services; (iii) quality assurance (iv) procurement and

procurement advisory services; (v) M&E and reporting; (vi) project administration; (vii) project

FM and (viii) reporting.

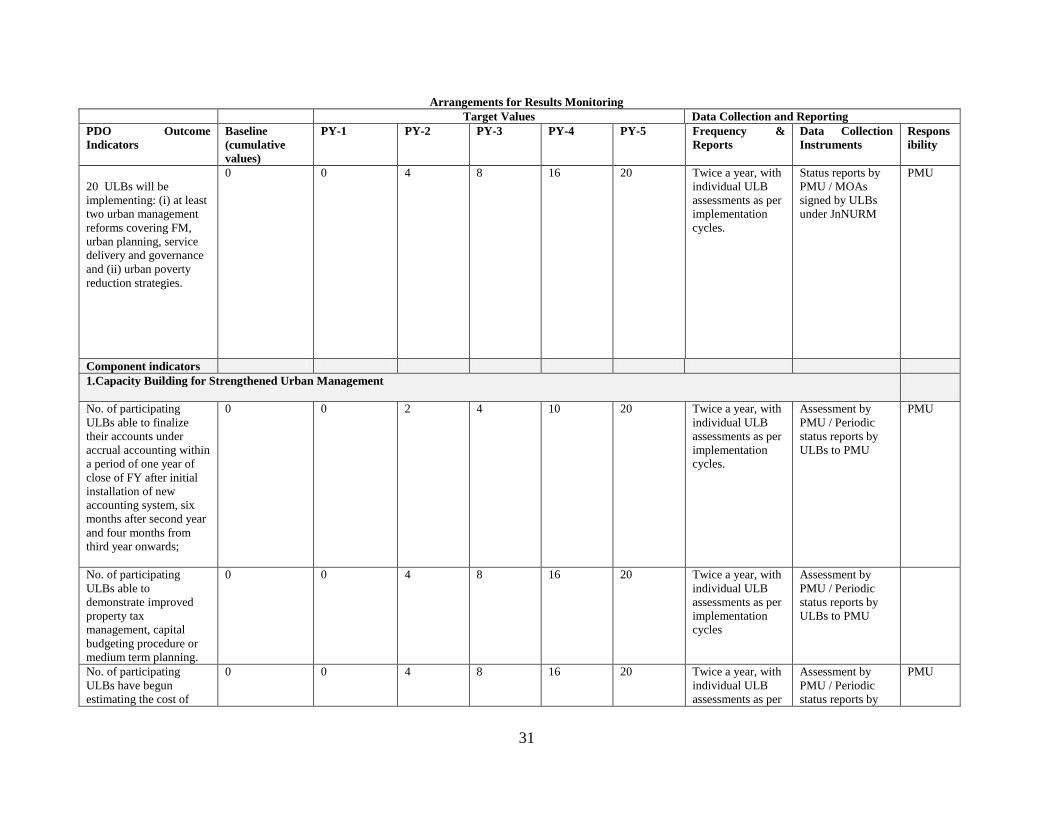

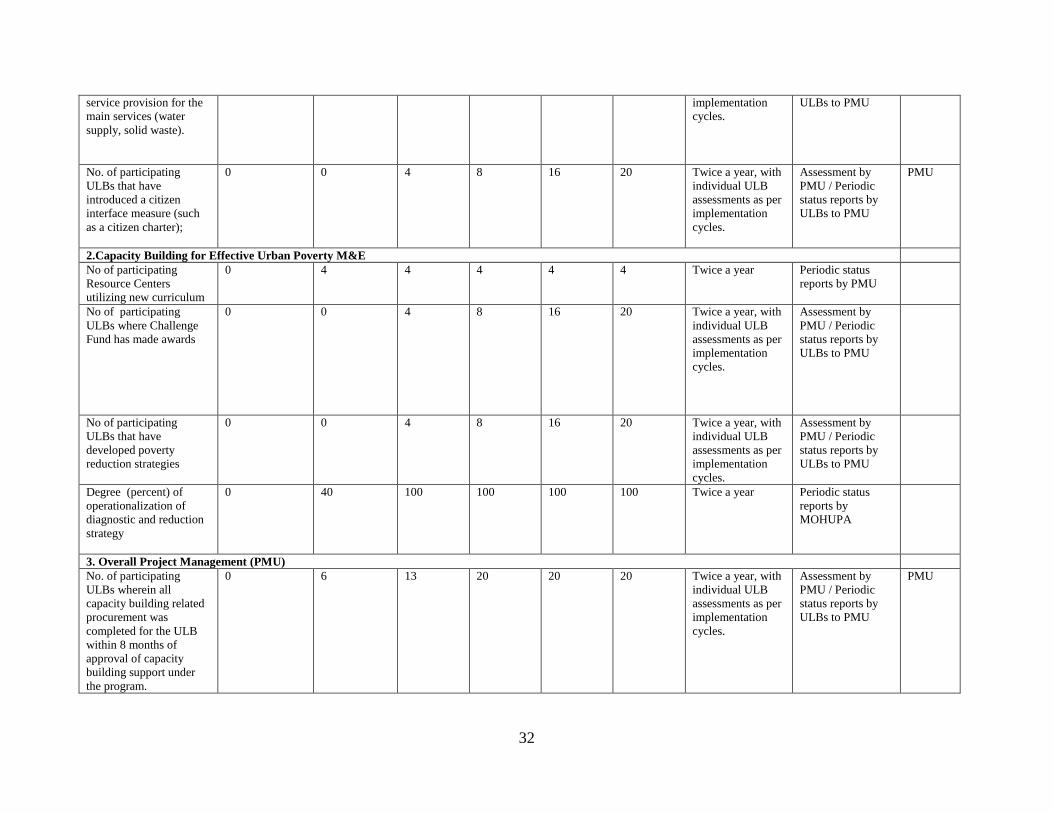

3. Monitoring and evaluation (Annex 3)

36. Broadly, the M&E system seeks to measure the outcomes associated with the various

capacity building components under the project as well as the overall program management

(institutional arrangements). Since under this program participating States and ULBs are not pre-

identified and could potentially join the program anytime through the period of implementation,

for the purposes of this M&E system certain assumptions have been made. These assumptions

will also be informed by the needs assessments / consultations / dialogue with States and ULBs.

State and ULBs would participate under this capacity building program over the implementation

period of 5 years, with no new States and ULBs joining the program after year 4 so that the

actual implementation gets completed in all States and ULBs by the end of the project period.

4. Sustainability

37. The project aims to improve sustainability in three ways: (i) at the ULB level through

skills development, scaling up of good practices and improved systems for poverty reduction

through good governance, better management, planning, and accountability, improved service

delivery and strengthened FM. The latter aims to help ULBs better manage revenue (including

12

accessing new sources such as capital markets, PPPs, carbon finance), and expenditure; (ii)

through a strengthened network of resource centers and practitioners; and (iii) in MOHUPA

through better policy support.

5. Critical risks

38. As a capacity building initiative supporting the GOI‘s urban strategy, the project presents

a somewhat different risk profile than a sector investment loan financing goods and works. These

risks and mitigation measures are addressed through the project design, as noted below.

39. Ensuring an appropriate management and accountability structure for the project. The

project follows a structure similar to JnNURM, wherein the two sponsoring ministries - MOUD

and MOHUPA - will Chair respective committees (PMB and PSC). The respective Joint

Secretaries/PDs will be assisted by a PMU, recruited under Bank procurement procedures and

funded from the credit. The PMU will submit quarterly work programs for the review and

approval of the Joint Secretaries. The TOR for the PMU has been approved by the Bank.

40. Ensuring support to Ministries in Procurement and FM: The PMU will assist the two

Ministries in procurement and FM.

41. Ensuring that the capacity building is delivered as planned with expected levels of

quality. A monitoring system will be established in the PMU to (i) track the contracting system

for consultants, including grievance procedures; and (ii) evaluate the quality of services

provided. The beneficiary States and ULBs will exercise quality control on the services

provided.

42. Additional risks associated with project outcomes are identified below.

Risks Risk Mitigation Measures Risk Rating with

Mitigation

To project development objective

JnNURM will come up for renewal in 2012

and may be revised

Substantial breadth and depth of the urban

management skills needed to support

implementation of JnNURM

11th Plan identifies need for urban development. Even if

JnNURM is modified, the commitment to efficient,

effective and inclusive ULBs will likely remain.

Focus on a small group of self-selected ULBs.

M

To component results

1. Capacity Building for Strengthening

Urban Management:

Skill and system acquisition: Range of FM

upgrading needed is quite large.

Institutional resistance to change: Potential

resistance to developing new institutional

framework. Difficulty for ULBs to develop

multi-sectoral, city-wide plans.

Finance profession well developed in India in the private

sector; good supply of professionals available to facilitate

skill and system transfer.

Very high demand for system improvement expressed in

consultation with prospective ULBs.

M

13

2. Capacity Building for Effective Urban

Poverty Monitoring and Alleviation:

2a Challenge Fund: May have difficulty in

identifying innovative practices and then

additional difficulty in scaling up.

2b. Network: Incentives for participation in

Network.

2c. Training Materials: Utilization and

integration into curriculum: Ability of

network institutions to incorporate new

curriculum into training programs. Ability

of institutions to manage learning cohorts

2d .Urban Poverty Reduction Strategies:

Possible difficulty in utilizing information

and implementing methodology.

2e. Strengthening MOHUPA to utilize

information for better informed policy.

The Challenge Fund is a pilot activity. The entity that will

be expected to manage the process will be expected to

provide ―handholding‖ during the initial rounds of

identification and award.

Again a pilot activity. Initial estimate is that there is

significant interest in learning and sharing experiences

among ULBs.

The institutions that will be selected will have considerable

experience in providing training, including collaboration

with WBI.

Pilots will be developed to incorporate lessons learnt.

Strengthening of MOHUPA is underway with the

establishment of a Policy and Program Support Unit staffed

by qualified professionals. ULBs will be able to look to

State and ULB nodal units for support in implementation.

M

3. PMU

Unit is unable to provide the range of

services requested in the TOR to support

the Project Directors.

Significant interest expressed by well qualified firms to

date in providing these services and skills.

L

Overall risk rating M

14

6. Credit conditions

43. Project Covenant: The Challenge Fund will disburse money only after the proposals are

cleared as per the Challenge Fund procedures and the required fiduciary assessment and

reporting arrangements are agreed with the proposed Beneficiary.

44. Project Covenant: Internal Audit to be in place throughout the life of the project and

conducted at periodic intervals.

45. Project Covenant: An FM Specialist to be in place throughout the life of the project.

D. APPRAISAL SUMMARY

1. Economic and Financial Analyses

46. No economic and financial appraisals have been carried out as the ULBs have not been

identified prior to loan negotiation. However, an economic analysis would be undertaken of

capacity building in a selected ULB during project implementation. 2. Technical

47. The project directly supports the Borrower‘s flagship program for urban development,

and more specifically, it strengthens local capacity for implementing critical urban policy

reforms. Additionally, the project will support the development of capacity in ULBs to plan,

implement and monitor investment projects consistent with the objectives of JnNURM and RAY

for improving service delivery. This will include strengthening capital budgeting procedures,

improving project planning, improving contracting, and developing supervision procedures.

3. Fiduciary

48. Financial Management (Annex 7) FM systems for this project will be based on

government systems of accounting and reporting with all the controls and oversight that exists in

the government system. It may be noted that FM systems for the Challenge Fund will be

designed and agreed separately, once the implementation arrangement for the same is agreed. As

a part of the due diligence, the FM assessment for the Challenge Fund would be conducted and

an action plan would be agreed with the MOHUPA, and based on the implementation of the

action plan the funds would be released for this sub-component. The assessment concludes that

the proposed FM systems are satisfactory to support the project (assuming satisfactoriness of

arrangements to support the Challenge Fund).

49. The two Ministries will operate two separate budget heads for expenditure under the

project. Financial Adviser of the two Ministries, assisted by Director (Finance) and Chief

Controller of Accounts will provide oversight over the financial management aspects of the

project. The FM Specialist in the PMU will be a professional accountant who will oversee the

FM aspects of the project and liaise with the Bank.

50. The funds flow system for the project will be simple and based on reimbursement of

expenditures based on quarterly Interim Un-audited Financial Reports (IUFRs). These IUFRs

will be reconciled annually with audited Annual Financial Statements (AFS).

15

51. Expenditures will be centralized1 (except for Challenge Fund) and will be made by the

MOUD/MOHUPA as applicable on activities, through the Pay and Accounts Office (PAO)

system. Quarterly reports submitted by the Ministries to the Controller General of Accounts

(CGA) will comprise the accounting records for the project. Accounting for the project will be

carried out on cash basis of accounting. The AFS for the project will be maintained by the PMU

based on expenditure reported to the CGA by the two Ministries. The PMU would maintain

detailed records which would be reconciled with PAO on a regular basis.

52. A single consolidated annual audit report will be submitted to the Bank. The audit will be

carried out by the Comptroller and Auditor General (CAG), based on Terms of Reference (TOR)

agreed with the Bank.

53. Internal control will be strengthened through procedures laid out in a Project FM Manual,

which will be predicated on controls in government system. In addition, internal audit will be in

place throughout the life of the project by a firm of Chartered Accountants empanelled with the

CAG, as per a TOR which will be agreed with the Bank.

54. Procurement (Annex 8). The procurement capacity will be built by hiring a PMU with a

dedicated procurement staff that will assist the implementing agencies in all procurement

activities, including advisory support to the ULBs for the procurement related reforms. No

procurement (other than the procurement of PMU) will take place until the PMU has been

established.

55. States and ULBs may elect to improve their capacity for procurement under the project.

Where the need is identified, the project may support working towards adoption of unified

procurement regulations that apply to any use of public funds for the purchase of goods, works,

and services, define appropriate management structures for procurement at the States and ULB

level and help create a timeline for adoption of e-government procurement. These initiatives are

geared towards improving the overall effectiveness of procurement by ULBs and help building

their capacities.

4. Social

56. No specific social safeguards issues have been identified. The project will, however,

provide TA for improving the capacity of ULBs to manage the social impact of urban

development. The project will support a pro-poor approach to urban planning, budgeting, and

service delivery. Governance improvements will give greater voice to urban stakeholders,

especially the poor.

5. Environment

57. The activities directly supported by the project are not likely to cause any significant

adverse environmental impacts and none of the safeguards are likely to be triggered. Indeed,

through capacity building, the project has the potential to ameliorate significant issues related to

the urban environment, e.g. lack of integrated planning, land use planning, environmental

1 It is envisaged that all payments would be done by the ministries at the Central level. (FM Annex).

16

sustainability of service delivery, and heightened citizen awareness and monitoring of

environmental issues.

58. The project is designated in ‗Category C‘ for environmental screening where the

responsibility for (potential, future) safeguard review and clearance has been transferred to the

Sector Unit.

6. Safeguard Policies

Safeguard Policies Triggered by the Project Yes No

Environmental Assessment (OP/BP 4.01) [ ] [X]

Natural Habitats (OP/BP 4.04) [ ] [X]

Pest Management (OP 4.09) [ ] [X]

Physical Cultural Resources (OP/BP 4.11) [ ] [X]

Involuntary Resettlement (OP/BP 4.12) [ ] [X]

Indigenous Peoples (OP/BP 4.10) [ ] [X]

Forests (OP/BP 4.36) [ ] [X]

Safety of Dams (OP/BP 4.37) [ ] [X]

Projects in Disputed Areas (OP/BP 7.60)1 [ ] [X]

Projects on International Waterways (OP/BP 7.50) [ ] [X]

7. Policy Exceptions and Readiness

59. The project does not require any exception from Bank procedures and meets the South

Asia Region‘s criteria for readiness.

1 By supporting the proposed project, the Bank does not intend to prejudice the final determination of the parties'

claims on the disputed areas

17

Annex 1: Country and Sector Background

INDIA: Capacity Building for Urban Development Project

1. Urban sector background. Indian ULBs will be the locus and engine of much of the

country‘s economic growth over the next two decades. Since 1960 India‘s total population has

increased three fold, and the urban share has risen from seventeen percent to almost thirty

percent. This population is spread across over 5,000 ULBs including three of the world‘s twenty

one mega-ULBs, four ULBs with a population between four and ten million and another twenty

eight with populations of more than one million. Between 2000 and 2030 the UN projects that

India‘s urban population will increase from 282 million to 590 million persons (UN-HABITAT).

Mega-city growth has and will continue to play a key role in driving Indian urban population

growth. Therefore, it can be inferred that one facet of India‘s urban planning challenge is to

accommodate an additional 10 million urban dwellers per year, provide them with adequate

public services and infrastructure, create opportunities for economic development and ensure that

urbanization is environmentally sustainable. However, rising urban inequality and deceleration in

the pace of urban poverty reduction may hinder the achievement of the Plan target.

2. Managing the urban space. While Indian ULBs continue to attract millions of people,

they have not been able to completely achieve the development and economic benefits that

urbanization could bring. This is evident from the high land prices, inadequate housing,

congestion and weak service delivery in urban areas. The high cost of urbanization is a critical

constraint to urban development, the result of weaknesses in the policy, financing and

institutional frameworks that govern key aspects of urban management, i.e. urban finance, land

use planning and regulation, service delivery and governance.

3. Urban finance. The critical issue facing policy makers in the context of urban finance is:

how can ULBs become financially viable entities that can raise the financial resources required

to operate urban services effectively as well as undertake the capital investments to meet the

demand supply gap? Five interconnected problems in urban finance need to be addressed:

ULBs are not sufficiently empowered and in most cases, do not have the autonomy of

fiscal powers and full devolution of responsibility for delivering the urban services

expected of them;

There is a mismatch between ULB revenue capacity and their expenditure requirement:

they lack buoyant sources of own revenue because their tax bases and data are weak,

and they are unable to fully recover charges for services rendered;

Most of the ULBs are not creditworthy on a stand-alone basis and, in most cases, lack

an adequate supply of bankable projects that could be financed in domestic capital

markets;

Due to these structural failures, ULBs are dependent on an inadequately targeted system

of intergovernmental transfers, and borrowing from government owned financial

institutions. These impose very little financial discipline and thus reinforce the lack of

creditworthiness; and

ULB accounting system reforms and upgradation of systems are not yet fully in place.

This hampers the possibility of ULBs successfully accessing credit, allowing for

efficient budgeting and financial management.

18

4. A key reason for the financial weakness of ULBs in India has been the low levels of own

source revenues - primarily property taxes and user charges. Property tax remains a vastly under-

utilized source of revenue by ULBs, largely because property taxes rely on a valuation

methodology that does not reflect market values. Similarly, user charges are another greatly

under-utilized source of own revenue in ULBs. Water supply tariffs rarely cover O&M

expenditures and many other urban services (such as sewerage) traditionally do not have a user

charge associated with them. Expenditure management is also cause for concern. Expenditure

assignments tend to be highly fragmented, and the absence of clear assignments diminishes the

authority delegated to local government to make autonomous expenditure decisions. This is

evident, for instance, from the assignment of expenditure responsibility for water supply across

various states. The dichotomy wherein the capital expenditures are carried out by state level

utilities (parastatals) and O&M by ULBs creates a number of distortions. This leads to an

inability to do capital investment planning (since no single entity can be held accountable for the

system as a whole), a bias towards undertaking capital investments over improving O&M of

urban systems, and lack of incentives for cost recovery since the capital financing is not done in

transparent manner and reflected on ULBs‘ balance sheets.

5. The High Powered Expert Committee has estimated investment for urban infrastructure

over the 20-year period from 2012 to 2031 at USD 886 billion (Rs. 39.2 lakh crore at 2009-10

prices), which includes Rs. USD771 billion (Rs. 34.1 lakh crore) for a) asset creation, out of

which the investment for the eight major sectors is USD701 billion (Rs. 31 lakh crore); b) USD

92 billion (Rs. 4.1 lakh crore) for renewal and redevelopment including slums; and c) USD22

billion (Rs. 1 lakh crore) for capacity building. The O&M requirements for the new and the old

assets are projected at USD 450 billion (Rs. 19.9 lakh crore) over the 20-year period. ULBs need

to access financial markets but their weak creditworthiness is the main constraint. What these

various estimates serve to highlight is the fact that the enormous financing needs are unlikely to

be met by current budgetary flows/fiscal transfers (from state and central government) into this

sector and ULBs/Infrastructure entities would have to increasingly access debt/equity from

financial markets. However, this has proved to be difficult primarily due to two demand side

issues – weak ULB finances leading to lack of creditworthiness for borrowings and lack of a

strong pipeline of bankable urban projects. The primary reason for the insufficient pipeline of

bankable projects is the weak institutional capacity of ULBs and the unclear expenditure

assignments, especially for capital expenditures. This has resulted in only a handful of ULBs

raising bonds from the capital markets. The High Powered Expert Committee on Urban

Infrastructure has reported the issue of just 22 municipal bonds (including taxable, tax-free and

pooled finance) amounting to USD 276.79 million (Rs. 1224 crores).

6. Finally, the quality of FM in ULBs is widely recognized to be highly variable. While the

governing federal and state legislation is comprehensive in areas such as financial control,

budgeting and audit, there are significant weaknesses in implementation of the same at ULBs.

Also, aspects of participatory planning and public accountability are weak in the present

legislative framework. In most ULBs the current system of municipal accounting remains a

single entry system and on a cash basis. The current accounting practices lead to certain

problems: (i) no segregation between revenue and capital expenses; (ii) inability to prepare a

complete balance sheet; (iii) limited information about assets and liabilities; (iv) non-recognition

of depreciation and other non-cash expenses; and (v) omission of receivables and payables

distorting the true and fair performance reporting of the urban local bodies. Apart from

19

individual city efforts, not all states have implemented double entry accrual-based accounting in

all its urban local bodies.

7. Planning and land use regulations. A common trend across India is that most ULBs and

metropolitan agglomerations are relying on outdated master plans. Planning surveys, projections

of population, employment and land development do not provide an accurate basis for planning

future urban development. Most plans are snap-shots of what the future should look like. Most

plans do not sufficiently integrate economic assessments of the rapidly evolving structure of the

local economy.

8. Historically, Indian ULBs were not able to adequately access funds and decision making

power, which resulted in the current land use situation where planners impose a restrictive policy

regime to attempt to bring down costs, limit infrastructure investments and impose controls on

the spatial patterns of the city. Among the policies used to implement this system were a broad

range of regulations. For instance, to protect tenants from the sorts of rent increases that would

occur in such supply–constrained housing markets, binding rent controls were introduced in all

major ULBs.1 Finally, in an effort to ―decongest‖, almost all Indian ULBs enacted FSI

regulations, which effectively constrained building heights. FSI restrictions of one-fifth to one-

tenth of the level of other ULBs in the world are common in Indian ULBs, with the result that

India does not have as many high rise ULBs when compared to countries of comparable

population size.2 An FSI set significantly below the level of its market equilibrium has a number

of negative consequences and imposes large costs on the city‘s economy. It increases the

demand for land across the city as more land is required for the same amount of floor space, and

increases land prices. A uniform restriction on the FSI encourages non-productive use of

housing capital, raises equilibrium housing prices and lowers city growth. Estimates suggest that

the costs associated with low FSIs e.g. in Bangalore (India) may be as high as 3-6 percent of

household wealth.

9. Service delivery institutions. There is a strong bias toward providing physical

infrastructure (pipes, vehicles, collection bins, and flyovers) rather than providing reliable,

affordable, and financially and environmentally sustainable services to urban areas. This bias is

evident in water and sanitation where access to drinking water rose from 82% of the population

in 1991 to 90% in 2001, but few cities have water service twenty four hours a day, seven days a

week.3 Solid Waste Management (SWM) faces similar performance issues. A 2004 review of

the status of SWM at the end of three years under the government issued Municipal Solid Waste

(MSW) Rules revealed that in Class-1 ULBs the rate of compliance with MSW Rules ranged

1 In 1976 the Urban Land Ceiling and Regulation Act was implemented to prevent land speculation by putting a

ceiling of 500 square meters on vacant land that could be held in private ownership. All land holdings in excess of

the was to be returned to the government which could use it to house the poor. 2 Floor Area Ratios (FAR) (or Floor Space Indices, or FSI as they are referred to in India) are a common zoning

regulation that limits the amount of floor area that can be constructed on a particular plot. They are set at 2.0 or less

in many Indian ULBs, whereas they are 15 in Hong Kong and Portland, and 5 in Jakarta. For instance, in

Ahmedabad the FAR is 1.8, in Hyderabad it is 1.75, and in Chennai it ranges from 1.0 to 1.75. ULBs in developed

economies also had FAR restrictions that affected city development in the 19th

century. For instance, Montgomery

(2003) describes the situation in New York City in the 1800s showing how the restrictions affected the city‘s

development. However, the New York City FAR was more than three times higher than Mumbai‘s level over most

of the past 30 years. 3 Bridging the Gap between Infrastructure and Service Report by World Bank, January 2006

20

between 72% and 1% for the different aspects of SWM1. The issues in this sector are related to

technical viability, costs sustainability and institutional structures to manage them.

10. For both water and sanitation services and SWM, six principal constraints to improve

service delivery are apparent:

Sector level governance is compromised by overlapping institutions and lack of

accountability. By and large, multiple state and local government agencies are involved

in most aspects of municipal service delivery, and the policy making and service

delivery functions are mostly not separated. Basic services generally are provided by

departments within a municipal corporation, which leads to more overlap, and makes it

difficult to know either revenues or the costs of service provision. In this environment,

Regulatory arrangements are ineffective so that tariffs for basic services and quality

standards are neither set clearly nor robustly enforced. In this environment, existing

Regulatory arrangements have not resulted in clean/robust enforcement of tariffs for

basic services and quality standards.

Service is unreliable: Despite installed water production capacity often sufficient to

provide a permanent water service, piped water is never distributed more than a few

hours per day, including the seven mega-ULBs of Delhi, Mumbai, Kolkata, Hyderabad,

Chennai, Ahmedabad and Bangalore. Most households, forced to cope with poor

quality water supply and sanitation service, spend time and money on substitutes and

treatment for waterborne diseases. User charges are low by international standards, but

the cost of the alternatives on which users must rely far exceeds the full cost of

providing good quality service.

Current management of service is not financially sustainable: Most urban basic

services operations survive on large operating subsidies and capital grants provided by

the states. Only a few mega-ULBs are able to recover the cost of water supply and

sanitation or solid waste services from user charges.

Current management of service is not environmentally sustainable: Most ULBs

compete with the agricultural sector to secure surface water rights and tend to deplete

local aquifers used as substitute sources. Almost no city contributes significantly to the

abatement of pollution in receiving bodies (despite the existence of waste water

treatment capacity) and aquifers are being depleted by households and businesses

developing their own sources.

The social dimension, involving basic services to slums or the very large informal

sector in SWM, has been difficult to address. Large ULBs have indicators which reflect

urban poverty and employment of its inhabitants in unorganized sectors including

collection and recycling part of the solid waste. For efficiency and social reasons, these

people need a more structured role in the overall SWM business. Ideally, they would be

helped to perform their existing role better and with some increased rewards.