Embed Size (px)

Citation preview

1

Etisalat Group

A Profitable Growth Story

EFG-Hermes- 2nd London MENA Conference

November 1st-2nd 2012, London.

2

Emirates Telecommunications Corporation and its subsidiaries

(“Etisalat” or the “Company”) have prepared this presentation

(“Presentation”) in good faith, however, no warranty or representation,

express or implied is made as to the adequacy, correctness,

completeness or accuracy of any numbers, statements, opinions or

estimates, or other information contained in this Presentation.

The information contained in this Presentation is an overview, and

should not be considered as the giving of investment advice by the

Company or any of its shareholders, directors, officers, agents,

employees or advisers. Each party to whom this Presentation is made

available must make its own independent assessment of the Company

after making such investigations and taking such advice as may be

deemed necessary.

Where this Presentation contains summaries of documents, those

summaries should not be relied upon and the actual documentation

must be referred to for its full effect.

This Presentation includes certain “ forward-looking statements”. Such

forward looking statements are not guarantees of future performance

and involve risks of uncertainties. Actual results may differ materially

from these forward looking statements.

Disclaimer

3

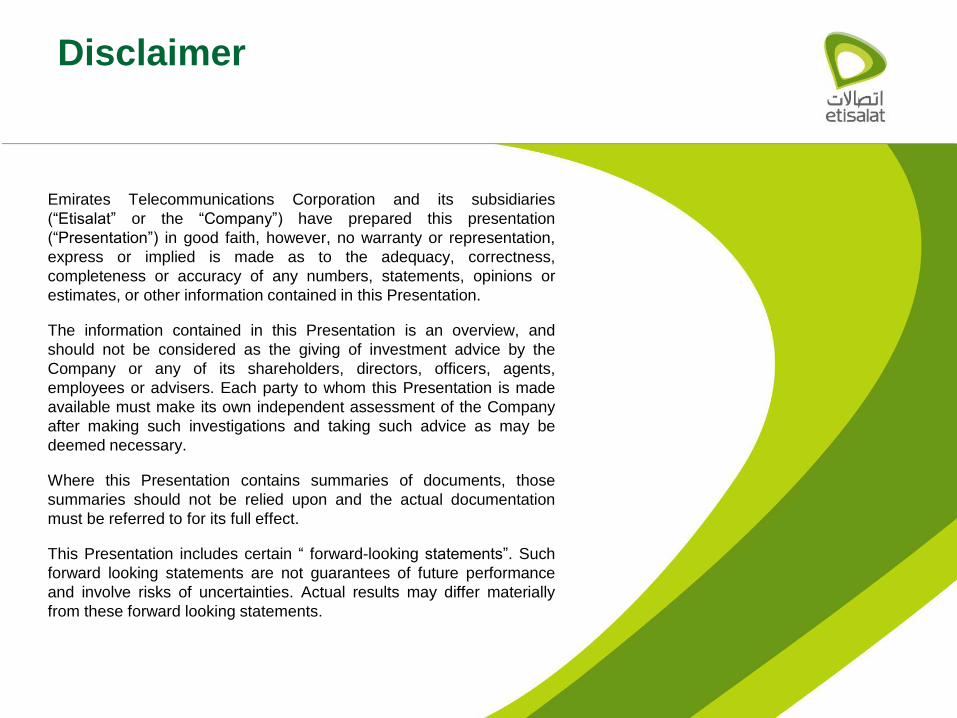

Etisalat Snapshot

• Etisalat listed in Abu Dhabi Stock Exchange (ADX) since 2002.

• Reporting currency of AED pegged to USD (USD 1 = AED 3.67)

• Stock ownership currently restricted to only UAE nationals.

• 11 BoD members; 7 representing the Federal Government and

4 free float.

• Etisalat is the largest corporate contributor outside oil sector to

the UAE economy. Etisalat contributed 21% of the Federal

Government budget for 2011 through dividend and royalty

payments.

• With a market capitalisation of USD20 bn, Etisalat is the second

largest telecom operator in GCC and ME region.

• Etisalat has operations in 15 countries including UAE, with an

aggregate subscriber base of 130 million (1).

• Etisalat has achieved a CAGR of 11% growth in consolidated

revenues to USD8.8 bn (AED32.2 bn) during 2007-11.

• Investment grade ratings from all agencies

Moody’s: Aa3 / stable

S&P: AA- / stable

Fitch: A+ / stable

Emirates

Investment

Authority

60%

Free float

40%

Notes: (1) Aggregate subscribers, including subsidiaries and associates.

USD billion 2011

Revenue 8.8

EBITDA 4.3

EBITDA % 49%

Net Income 1.6

Net Income % 18%

CapEx 1.2

FCF 1.6

(2) Operating cash flow defined as (EBITDA – CAPEX) in all subsidiaries with the exception of UAE since 50% Federal Royalty on

consolidated net profits is also included in the formula (i.e. EBITDA – CAPEX – Federal Royalty).

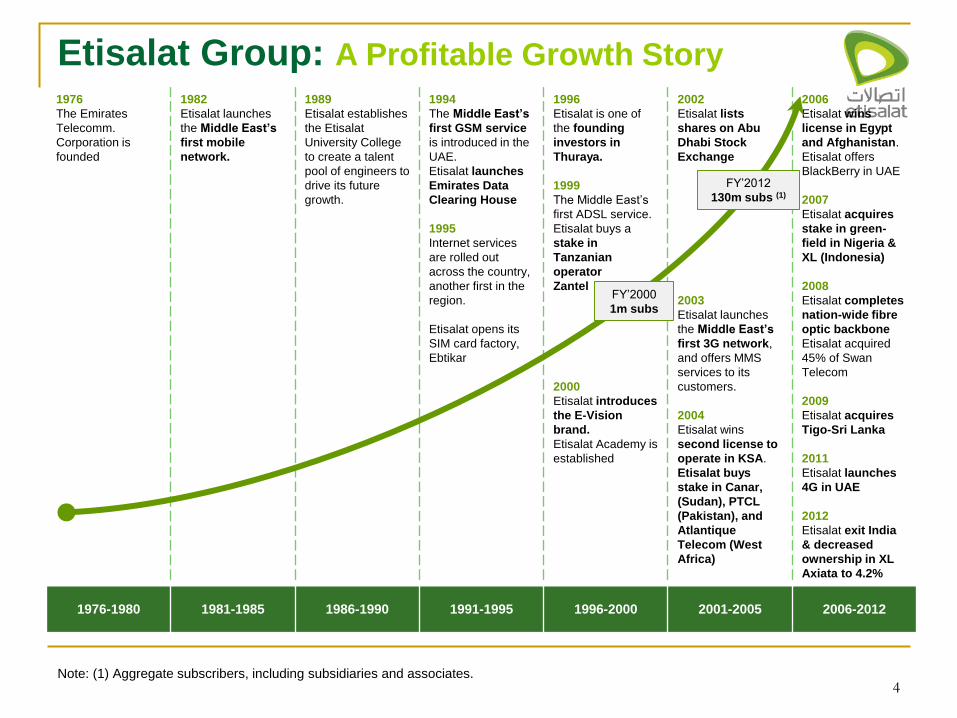

1976

The Emirates

Telecomm.

Corporation is

founded

1982

Etisalat launches

the Middle East’s

first mobile

network.

1989

Etisalat establishes

the Etisalat

University College

to create a talent

pool of engineers to

drive its future

growth.

1994

The Middle East’s

first GSM service

is introduced in the

UAE.

Etisalat launches

Emirates Data

Clearing House

1995

Internet services

are rolled out

across the country,

another first in the

region.

Etisalat opens its

SIM card factory,

Ebtikar

1996

Etisalat is one of

the founding

investors in

Thuraya.

1999

The Middle East’s

first ADSL service.

Etisalat buys a

stake in

Tanzanian

operator

Zantel

2000

Etisalat introduces

the E-Vision

brand.

Etisalat Academy is

established

2002

Etisalat lists

shares on Abu

Dhabi Stock

Exchange

2003

Etisalat launches

the Middle East’s

first 3G network,

and offers MMS

services to its

customers.

2004

Etisalat wins

second license to

operate in KSA.

Etisalat buys

stake in Canar,

(Sudan), PTCL

(Pakistan), and

Atlantique

Telecom (West

Africa)

2006

Etisalat wins

license in Egypt

and Afghanistan.

Etisalat offers

BlackBerry in UAE

2007

Etisalat acquires

stake in green-

field in Nigeria &

XL (Indonesia)

2008

Etisalat completes

nation-wide fibre

optic backbone

Etisalat acquired

45% of Swan

Telecom

2009

Etisalat acquires

Tigo-Sri Lanka

2011

Etisalat launches

4G in UAE

2012

Etisalat exit India

& decreased

ownership in XL

Axiata to 4.2%

1976-1980 1981-1985 1986-1990 1991-1995 1996-2000 2001-2005 2006-2012

4

Etisalat Group: A Profitable Growth Story

FY’2012

130m subs (1)

FY’2000

1m subs

Note: (1) Aggregate subscribers, including subsidiaries and associates.

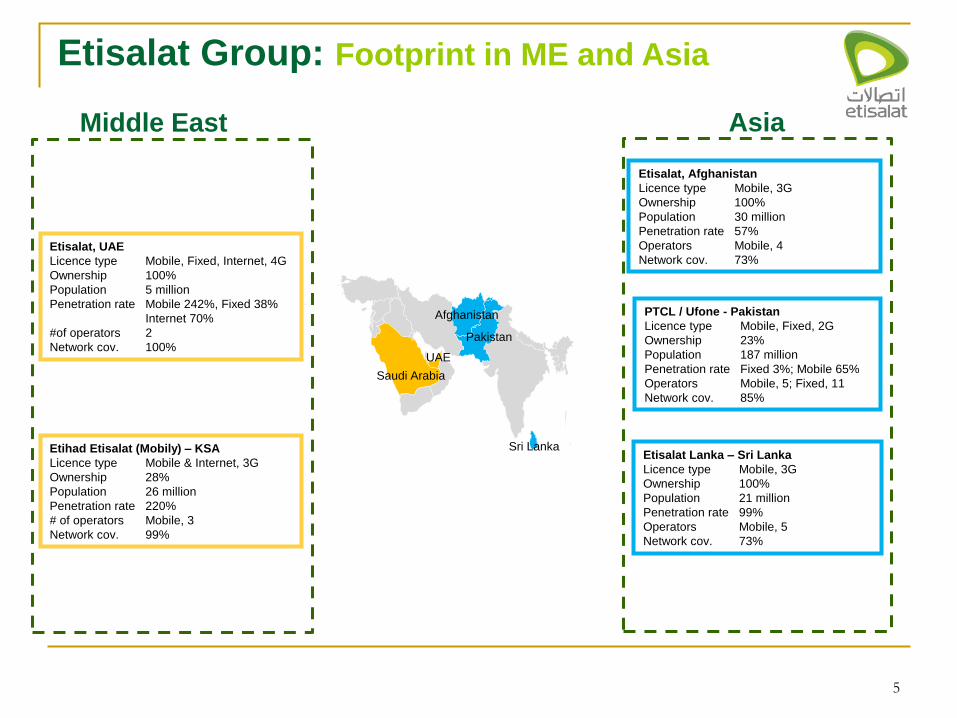

Sri Lanka

Saudi Arabia

UAE

Pakistan

Afghanistan

5

Etisalat Group: Footprint in ME and Asia

Etisalat, UAE

Licence type Mobile, Fixed, Internet, 4G

Ownership 100%

Population 5 million

Penetration rate Mobile 242%, Fixed 38%

Internet 70%

#of operators 2

Network cov. 100%

Etihad Etisalat (Mobily) – KSA

Licence type Mobile & Internet, 3G

Ownership 28%

Population 26 million

Penetration rate 220%

# of operators Mobile, 3

Network cov. 99%

Etisalat, Afghanistan

Licence type Mobile, 3G

Ownership 100%

Population 30 million

Penetration rate 57%

Operators Mobile, 4

Network cov. 73%

PTCL / Ufone - Pakistan

Licence type Mobile, Fixed, 2G

Ownership 23%

Population 187 million

Penetration rate Fixed 3%; Mobile 65%

Operators Mobile, 5; Fixed, 11

Network cov. 85%

Etisalat Lanka – Sri Lanka

Licence type Mobile, 3G

Ownership 100%

Population 21 million

Penetration rate 99%

Operators Mobile, 5

Network cov. 73%

Middle East Asia

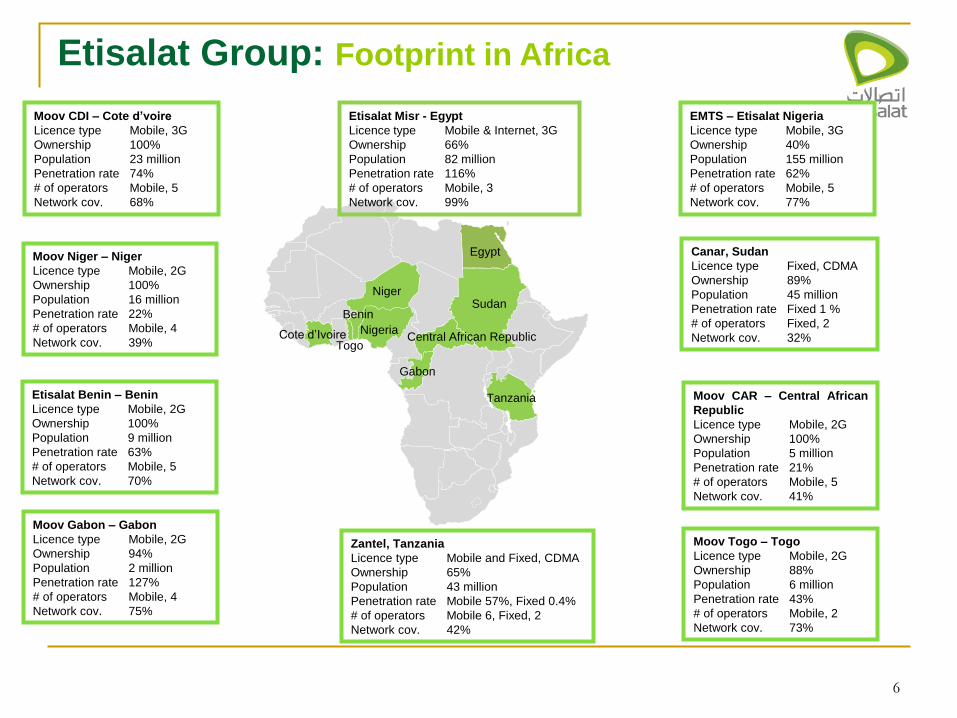

Niger

Central African Republic

Gabon

Nigeria

Togo Cote d’Ivoire

Benin

Egypt

Sudan

Tanzania

6

Etisalat Group: Footprint in Africa

Etisalat Misr - Egypt

Licence type Mobile & Internet, 3G

Ownership 66%

Population 82 million

Penetration rate 116%

# of operators Mobile, 3

Network cov. 99%

Canar, Sudan

Licence type Fixed, CDMA

Ownership 89%

Population 45 million

Penetration rate Fixed 1 %

# of operators Fixed, 2

Network cov. 32%

EMTS – Etisalat Nigeria

Licence type Mobile, 3G

Ownership 40%

Population 155 million

Penetration rate 62%

# of operators Mobile, 5

Network cov. 77%

Zantel, Tanzania

Licence type Mobile and Fixed, CDMA

Ownership 65%

Population 43 million

Penetration rate Mobile 57%, Fixed 0.4%

# of operators Mobile 6, Fixed, 2

Network cov. 42%

Moov CDI – Cote d’voire

Licence type Mobile, 3G

Ownership 100%

Population 23 million

Penetration rate 74%

# of operators Mobile, 5

Network cov. 68%

Etisalat Benin – Benin

Licence type Mobile, 2G

Ownership 100%

Population 9 million

Penetration rate 63%

# of operators Mobile, 5

Network cov. 70%

Moov Gabon – Gabon

Licence type Mobile, 2G

Ownership 94%

Population 2 million

Penetration rate 127%

# of operators Mobile, 4

Network cov. 75%

Moov Niger – Niger

Licence type Mobile, 2G

Ownership 100%

Population 16 million

Penetration rate 22%

# of operators Mobile, 4

Network cov. 39%

Moov Togo – Togo

Licence type Mobile, 2G

Ownership 88%

Population 6 million

Penetration rate 43%

# of operators Mobile, 2

Network cov. 73%

Moov CAR – Central African

Republic

Licence type Mobile, 2G

Ownership 100%

Population 5 million

Penetration rate 21%

# of operators Mobile, 5

Network cov. 41%

7

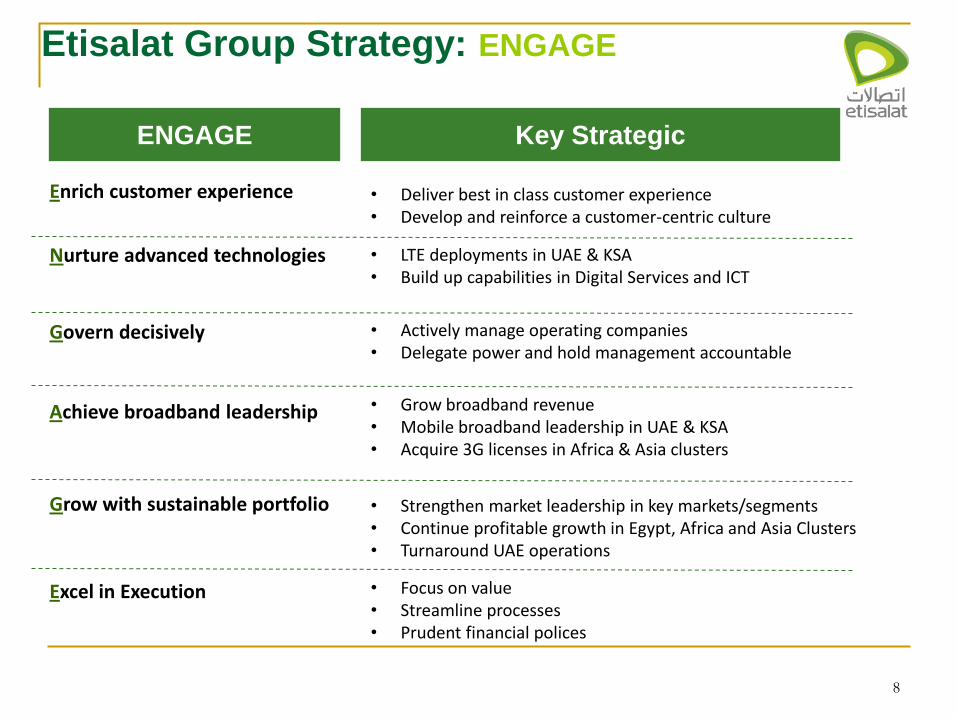

Etisalat Group Strategy Going Forward..

ENGAGE

Enrich customer

experience

Nurture advanced

technologies

Govern decisively

Achieve broadband leadership

Grow with sustainable

portfolio

Excel in execution

Strategy focus and priorities

• Maximize commercial and operational

performance in the UAE, return to

growth and defend market leadership

• Continue to capture profitable growth in

our existing international operations

• Push innovation in the digital space,

leveraging our assets and partnerships

• Pursue group-wide initiatives to extract

synergies and share best practices

• Pursue active portfolio management,

focus on reinforcing existing operations,

be selective in footprint expansion

• Strengthen management resources and

accountability

8

Enrich customer experience

Nurture advanced technologies

Govern decisively

Achieve broadband leadership

Grow with sustainable portfolio

Excel in Execution

ENGAGE Key Strategic

• LTE deployments in UAE & KSA • Build up capabilities in Digital Services and ICT

• Actively manage operating companies • Delegate power and hold management accountable

• Grow broadband revenue • Mobile broadband leadership in UAE & KSA • Acquire 3G licenses in Africa & Asia clusters

• Strengthen market leadership in key markets/segments • Continue profitable growth in Egypt, Africa and Asia Clusters • Turnaround UAE operations

• Focus on value • Streamline processes • Prudent financial polices

• Deliver best in class customer experience • Develop and reinforce a customer-centric culture

Etisalat Group Strategy: ENGAGE

9

Etisalat Recognized for Innovation The first and only operator worldwide awarded three GSMA Global

Mobile Awards

Best Mobile Health Innovation and ‘mWomen Best

Mobile Product’ categories for its mobile health

innovation

Etisalat Mobile Baby – that is helping to combat

maternal mortality in developing countries

Best Mobile Money Innovation’ award for its Etisalat

Commerce commercial platform enabling customers

to use the mobile phone as a payment instrument

anywhere , anytime.

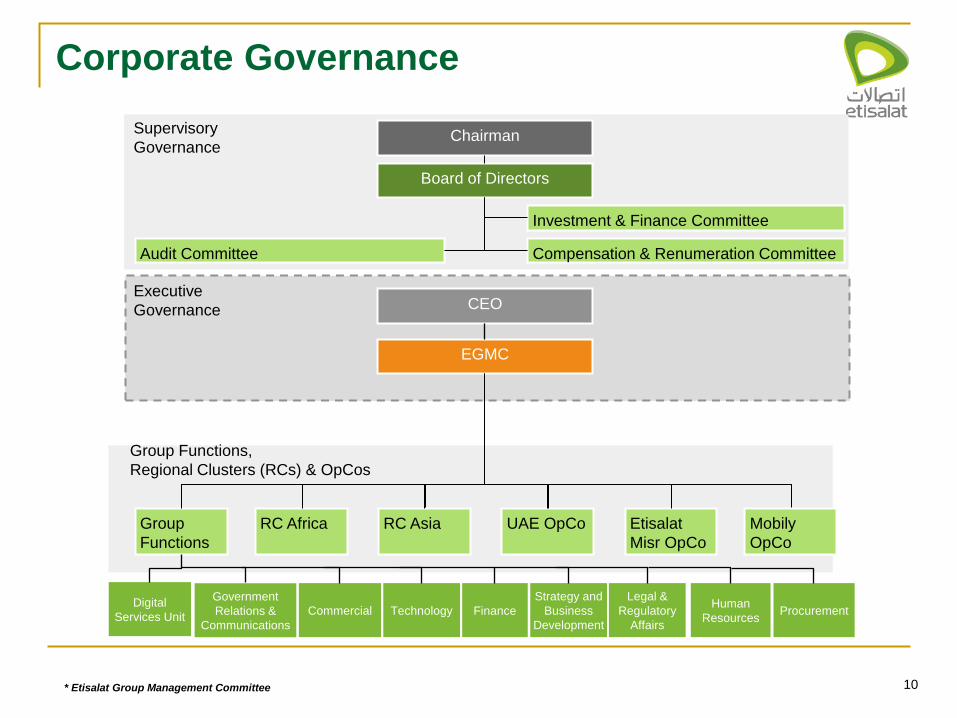

EGMC

Board of Directors

CEO

Chairman

Compensation & Renumeration Committee Audit Committee

Investment & Finance Committee

Supervisory

Governance

Executive

Governance

Group

Functions

UAE OpCo

Group Functions,

Regional Clusters (RCs) & OpCos

RC Africa

10

RC Asia Etisalat

Misr OpCo

Mobily

OpCo

* Etisalat Group Management Committee

Corporate Governance

Commercial Technology Finance

Strategy and

Business

Development

Legal &

Regulatory

Affairs

Human

Resources Procurement

Government

Relations &

Communications

Digital

Services Unit

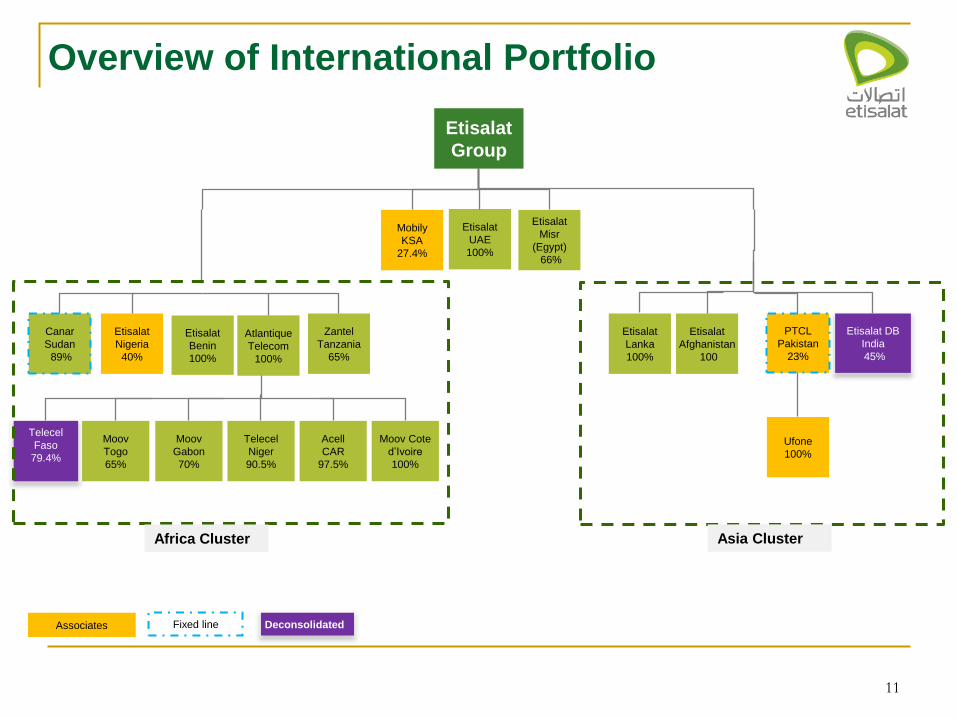

Etisalat

Group

Canar

Sudan

89%

Etisalat

Nigeria

40%

Zantel

Tanzania

65%

Mobily

KSA

27.4%

Etisalat

UAE

100%

Etisalat

Misr

(Egypt)

66%

Etisalat

Lanka

100%

Etisalat

Afghanistan

100

PTCL

Pakistan

23%

Etisalat DB

India

45%

Moov

Togo

65%

Moov

Gabon

70%

Telecel

Niger

90.5%

Acell

CAR

97.5%

Moov Cote

d’Ivoire

100%

Telecel

Faso

79.4%

Atlantique

Telecom

100%

Overview of International Portfolio

Etisalat

Benin

100%

Ufone

100%

Deconsolidated Fixed line Associates

11

Africa Cluster Asia Cluster

12

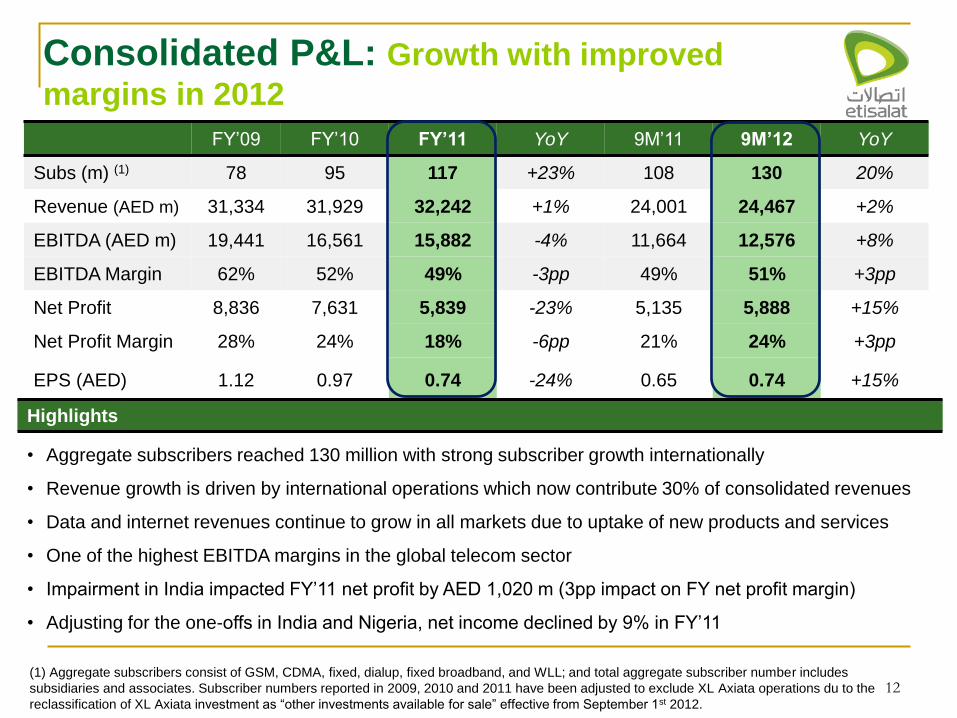

Consolidated P&L: Growth with improved

margins in 2012

FY’09 FY’10 FY’11 YoY 9M’11 9M’12 YoY

Subs (m) (1) 78 95 117 +23% 108 130 20%

Revenue (AED m) 31,334 31,929 32,242 +1% 24,001 24,467 +2%

EBITDA (AED m) 19,441 16,561 15,882 -4% 11,664 12,576 +8%

EBITDA Margin 62% 52% 49% -3pp 49% 51% +3pp

Net Profit 8,836 7,631 5,839 -23% 5,135 5,888 +15%

Net Profit Margin 28% 24% 18% -6pp 21% 24% +3pp

EPS (AED) 1.12 0.97 0.74 -24% 0.65 0.74 +15%

Highlights

• Aggregate subscribers reached 130 million with strong subscriber growth internationally

• Revenue growth is driven by international operations which now contribute 30% of consolidated revenues

• Data and internet revenues continue to grow in all markets due to uptake of new products and services

• One of the highest EBITDA margins in the global telecom sector

• Impairment in India impacted FY’11 net profit by AED 1,020 m (3pp impact on FY net profit margin)

• Adjusting for the one-offs in India and Nigeria, net income declined by 9% in FY’11

(1) Aggregate subscribers consist of GSM, CDMA, fixed, dialup, fixed broadband, and WLL; and total aggregate subscriber number includes

subsidiaries and associates. Subscriber numbers reported in 2009, 2010 and 2011 have been adjusted to exclude XL Axiata operations du to the

reclassification of XL Axiata investment as “other investments available for sale” effective from September 1st 2012.

13

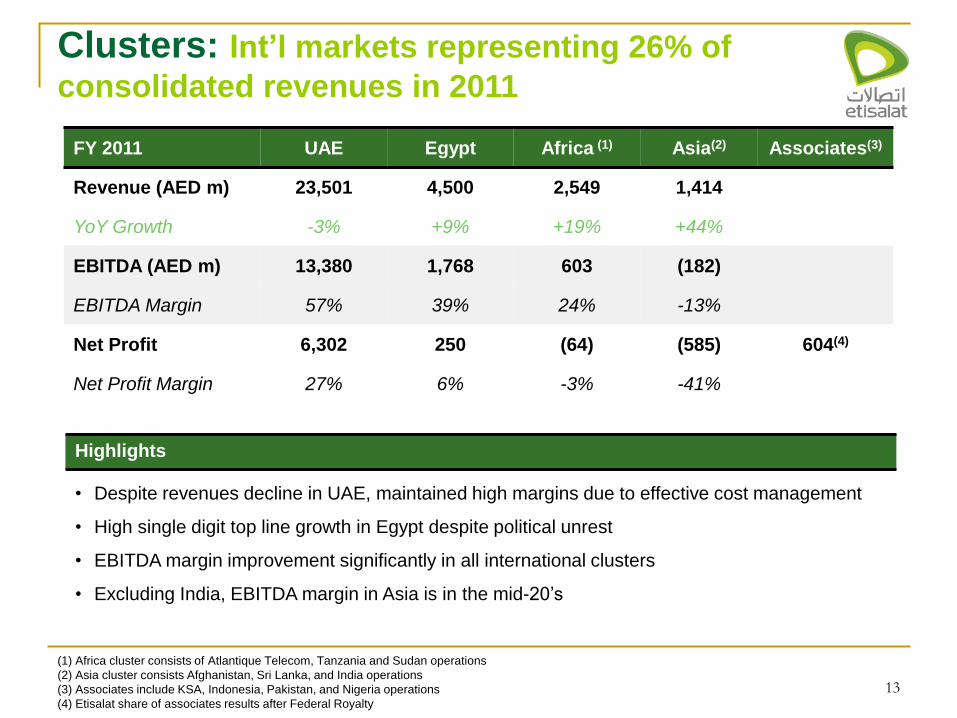

Clusters: Int’l markets representing 26% of

consolidated revenues in 2011

FY 2011 UAE Egypt Africa (1) Asia(2) Associates(3)

Revenue (AED m) 23,501 4,500 2,549 1,414

YoY Growth -3% +9% +19% +44%

EBITDA (AED m) 13,380 1,768 603 (182)

EBITDA Margin 57% 39% 24% -13%

Net Profit 6,302 250 (64) (585) 604(4)

Net Profit Margin 27% 6% -3% -41%

(1) Africa cluster consists of Atlantique Telecom, Tanzania and Sudan operations

(2) Asia cluster consists Afghanistan, Sri Lanka, and India operations

(3) Associates include KSA, Indonesia, Pakistan, and Nigeria operations

(4) Etisalat share of associates results after Federal Royalty

Highlights

• Despite revenues decline in UAE, maintained high margins due to effective cost management

• High single digit top line growth in Egypt despite political unrest

• EBITDA margin improvement significantly in all international clusters

• Excluding India, EBITDA margin in Asia is in the mid-20’s

14

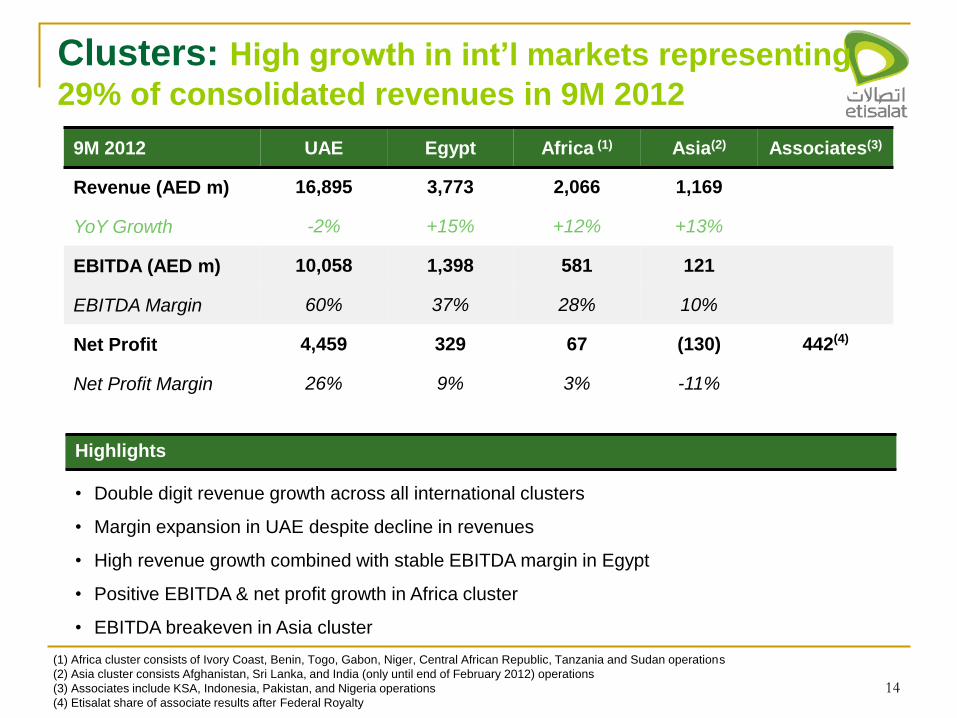

Clusters: High growth in int’l markets representing

29% of consolidated revenues in 9M 2012

9M 2012 UAE Egypt Africa (1) Asia(2) Associates(3)

Revenue (AED m) 16,895 3,773 2,066 1,169

YoY Growth -2% +15% +12% +13%

EBITDA (AED m) 10,058 1,398 581 121

EBITDA Margin 60% 37% 28% 10%

Net Profit 4,459 329 67 (130) 442(4)

Net Profit Margin 26% 9% 3% -11%

Highlights

• Double digit revenue growth across all international clusters

• Margin expansion in UAE despite decline in revenues

• High revenue growth combined with stable EBITDA margin in Egypt

• Positive EBITDA & net profit growth in Africa cluster

• EBITDA breakeven in Asia cluster

(1) Africa cluster consists of Ivory Coast, Benin, Togo, Gabon, Niger, Central African Republic, Tanzania and Sudan operations

(2) Asia cluster consists Afghanistan, Sri Lanka, and India (only until end of February 2012) operations

(3) Associates include KSA, Indonesia, Pakistan, and Nigeria operations

(4) Etisalat share of associate results after Federal Royalty

32.231.931.3

15

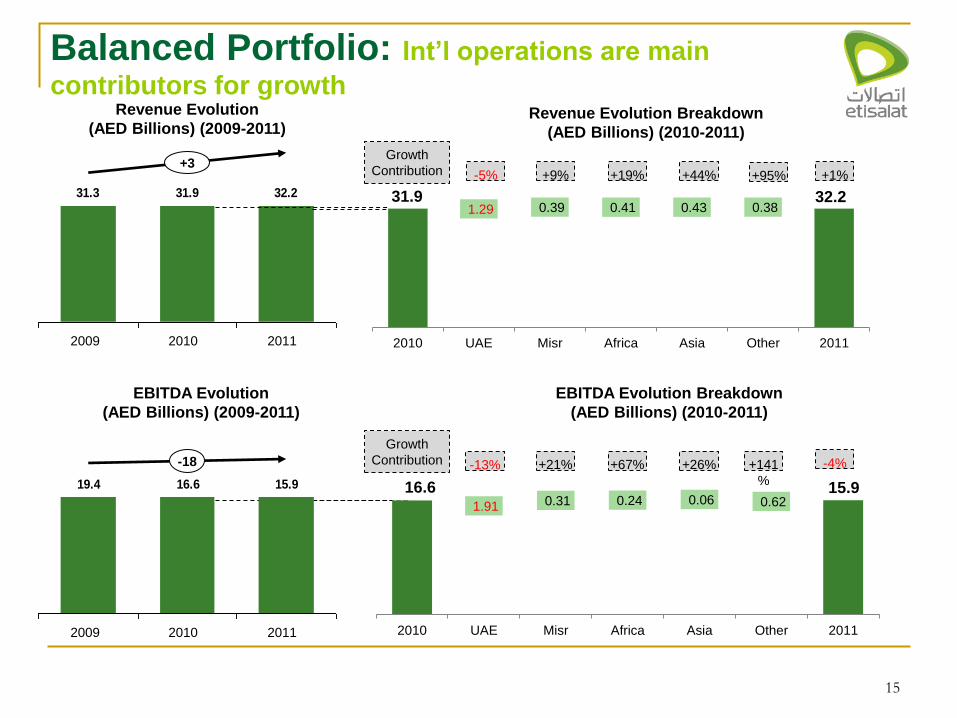

Balanced Portfolio: Int’l operations are main

contributors for growth Revenue Evolution

(AED Billions) (2009-2011) Revenue Evolution Breakdown

(AED Billions) (2010-2011)

EBITDA Evolution

(AED Billions) (2009-2011)

EBITDA Evolution Breakdown

(AED Billions) (2010-2011)

+21% +67% +26% +141

%

Growth

Contribution

-5% +9% +19% +44%

Growth

Contribution +1% +95% +3

2011 2010 2009

15.916.619.4

-18

2011 2010 2009

-13%

1.29 0.39 0.41 0.43 0.38

2010 UAE Misr Africa Asia Other 2011

31.9 32.2

1.91 0.31 0.24 0.06 0.62

2010 UAE Misr Africa Asia Other 2011

16.6 15.9

-4%

Revenue (AED b) and YoY growth (%)

Sources of Revenue growth – 9M’11 vs 9M’12

16

Revenue: Increasing revenue contribution from

international markets

31.93 32.24

24.01 24.47

3%

2%

2%

1%

-0.01

0.01

0.03

0.05

(5.00)

5.00

15.00

25.00

35.00

FY'10 FY'11 9M'11 9M'12

Revenue YoY growth %

24,011

23,590 23,590

24,081 24,305 24,406

24,467

421 491

224 132 31

23,000

23,200

23,400

23,600

23,800

24,000

24,200

24,400

24,600

9M'11 UAE Egypt Africa Asia Other 9M'12

Note: “Other revenues” consist of non-telecom revenues, management fees, etc.

Highlights

• 3pp YoY increase in revenue share of

international operations reaching to 29% of

consolidated revenues

• Continued high growth in data / internet

revenues despite decline in voice revenues

in UAE

• Subscriber base increase accompanied by

strong revenue growth in Egypt

• Significant revenue growth contribution from

Benin, Togo, Gabon and Niger in Africa

• Continued growth momentum in Sri Lanka

and Afghanistan in Asia

17

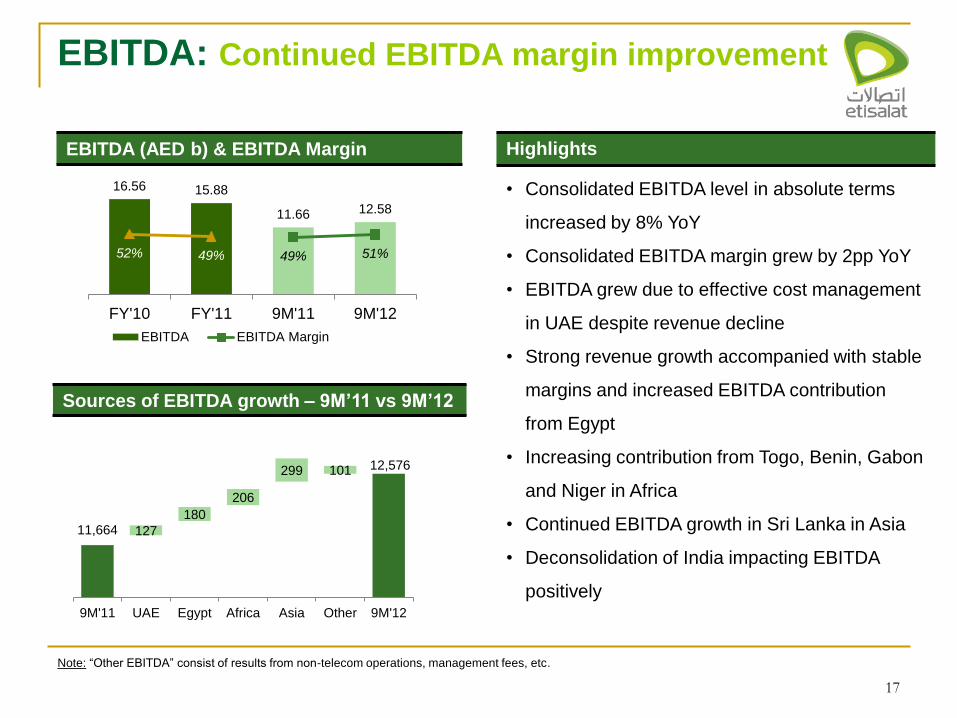

EBITDA (AED b) & EBITDA Margin

Sources of EBITDA growth – 9M’11 vs 9M’12

EBITDA: Continued EBITDA margin improvement

Highlights

• Consolidated EBITDA level in absolute terms

increased by 8% YoY

• Consolidated EBITDA margin grew by 2pp YoY

• EBITDA grew due to effective cost management

in UAE despite revenue decline

• Strong revenue growth accompanied with stable

margins and increased EBITDA contribution

from Egypt

• Increasing contribution from Togo, Benin, Gabon

and Niger in Africa

• Continued EBITDA growth in Sri Lanka in Asia

• Deconsolidation of India impacting EBITDA

positively

16.56 15.88

11.66 12.58

49% 51% 52% 49%

-0.15

0.05

0.25

0.45

0.65

0.85

0.00

5.00

10.00

15.00

FY'10 FY'11 9M'11 9M'12

EBITDA EBITDA Margin

11,664

11,791 11,971

12,177 12,475 12,576

12,576

127

180

206

299 101

11,000

11,200

11,400

11,600

11,800

12,000

12,200

12,400

12,600

12,800

13,000

9M'11 UAE Egypt Africa Asia Other 9M'12

Note: “Other EBITDA” consist of results from non-telecom operations, management fees, etc.

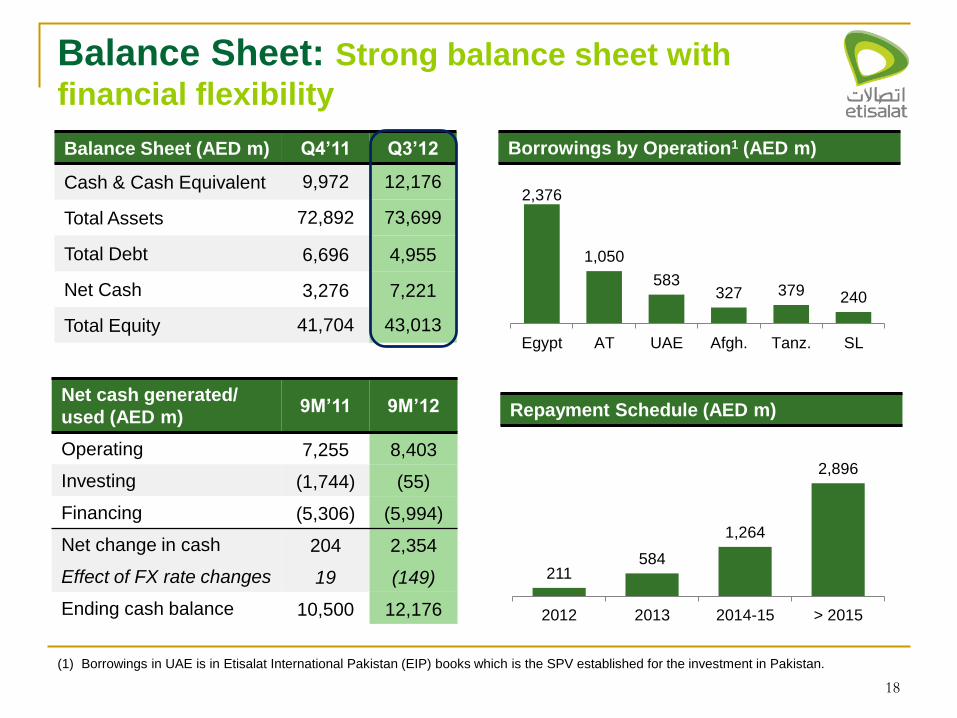

Balance Sheet (AED m) Q4’11 Q3’12

Cash & Cash Equivalent 9,972 12,176

Total Assets 72,892 73,699

Total Debt 6,696 4,955

Net Cash 3,276 7,221

Total Equity 41,704 43,013

18

Balance Sheet: Strong balance sheet with

financial flexibility

Borrowings by Operation1 (AED m)

2,376

1,050

583 327 379 240

0

500

1,000

1,500

2,000

2,500

Egypt AT UAE Afgh. Tanz. SL

Repayment Schedule (AED m)

211 584

1,264

2,896

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2012 2013 2014-15 > 2015

(1) Borrowings in UAE is in Etisalat International Pakistan (EIP) books which is the SPV established for the investment in Pakistan.

Net cash generated/

used (AED m) 9M’11 9M’12

Operating 7,255 8,403

Investing (1,744) (55)

Financing (5,306) (5,994)

Net change in cash 204 2,354

Effect of FX rate changes 19 (149)

Ending cash balance 10,500 12,176

19

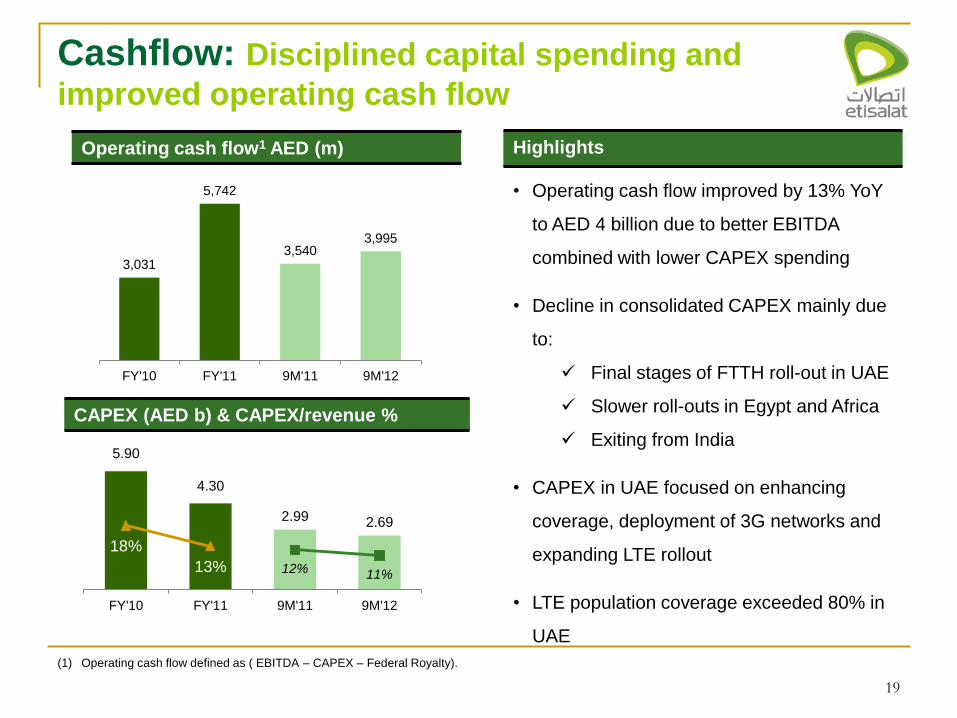

CAPEX (AED b) & CAPEX/revenue %

Cashflow: Disciplined capital spending and

improved operating cash flow

5.90

4.30

2.99 2.69

12% 11%

18%

13%

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

(0.50)

0.50

1.50

2.50

3.50

4.50

5.50

6.50

FY'10 FY'11 9M'11 9M'12

Highlights

• Operating cash flow improved by 13% YoY

to AED 4 billion due to better EBITDA

combined with lower CAPEX spending

• Decline in consolidated CAPEX mainly due

to:

Final stages of FTTH roll-out in UAE

Slower roll-outs in Egypt and Africa

Exiting from India

• CAPEX in UAE focused on enhancing

coverage, deployment of 3G networks and

expanding LTE rollout

• LTE population coverage exceeded 80% in

UAE

(1) Operating cash flow defined as ( EBITDA – CAPEX – Federal Royalty).

Operating cash flow1 AED (m)

3,031

5,742

3,540 3,995

FY'10 FY'11 9M'11 9M'12

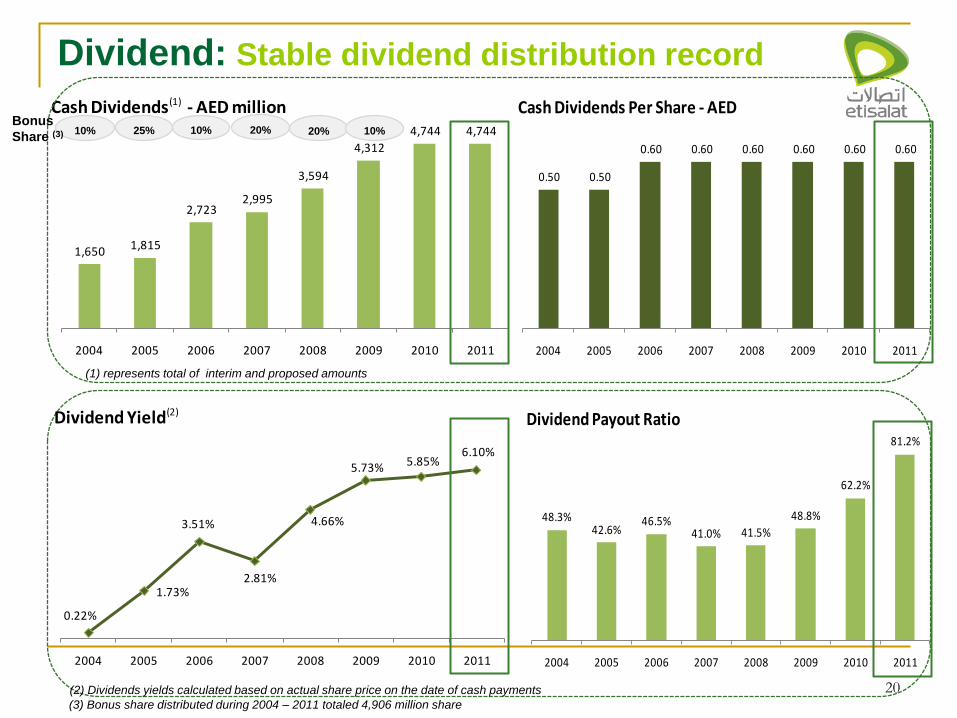

1,650 1,815

2,723 2,995

3,594

4,312

4,744 4,744

2004 2005 2006 2007 2008 2009 2010 2011

Cash Dividends(1) - AED million

20

Dividend: Stable dividend distribution record

(1) represents total of interim and proposed amounts

(2) Dividends yields calculated based on actual share price on the date of cash payments

0.50 0.50

0.60 0.60 0.60 0.60 0.60 0.60

2004 2005 2006 2007 2008 2009 2010 2011

Cash Dividends Per Share - AED

0.22%

1.73%

3.51%

2.81%

4.66%

5.73% 5.85%6.10%

2004 2005 2006 2007 2008 2009 2010 2011

Dividend Yield(2)

48.3%42.6%

46.5%41.0% 41.5%

48.8%

62.2%

81.2%

2004 2005 2006 2007 2008 2009 2010 2011

Dividend Payout Ratio

10% Bonus

Share (3) 25% 10% 20% 20% 10%

(3) Bonus share distributed during 2004 – 2011 totaled 4,906 million share

21

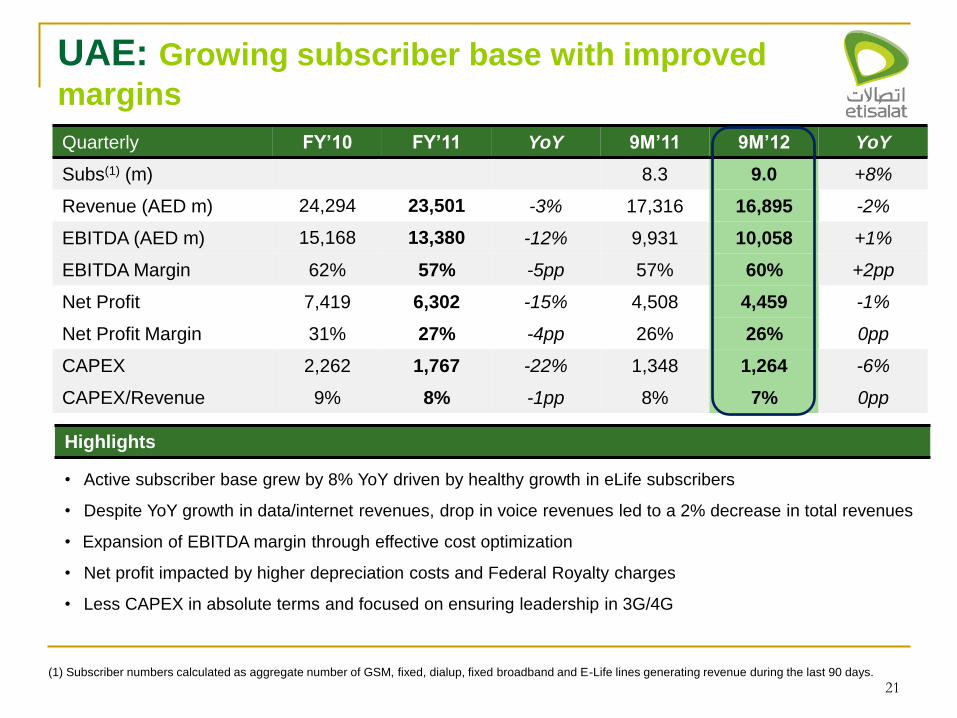

UAE: Growing subscriber base with improved

margins

Quarterly FY’10 FY’11 YoY 9M’11 9M’12 YoY

Subs(1) (m) 8.3 9.0 +8%

Revenue (AED m) 24,294 23,501 -3% 17,316 16,895 -2%

EBITDA (AED m) 15,168 13,380 -12% 9,931 10,058 +1%

EBITDA Margin 62% 57% -5pp 57% 60% +2pp

Net Profit 7,419 6,302 -15% 4,508 4,459 -1%

Net Profit Margin 31% 27% -4pp 26% 26% 0pp

CAPEX 2,262 1,767 -22% 1,348 1,264 -6%

CAPEX/Revenue 9% 8% -1pp 8% 7% 0pp

Highlights

• Active subscriber base grew by 8% YoY driven by healthy growth in eLife subscribers

• Despite YoY growth in data/internet revenues, drop in voice revenues led to a 2% decrease in total revenues

• Expansion of EBITDA margin through effective cost optimization

• Net profit impacted by higher depreciation costs and Federal Royalty charges

• Less CAPEX in absolute terms and focused on ensuring leadership in 3G/4G

(1) Subscriber numbers calculated as aggregate number of GSM, fixed, dialup, fixed broadband and E-Life lines generating revenue during the last 90 days.

22

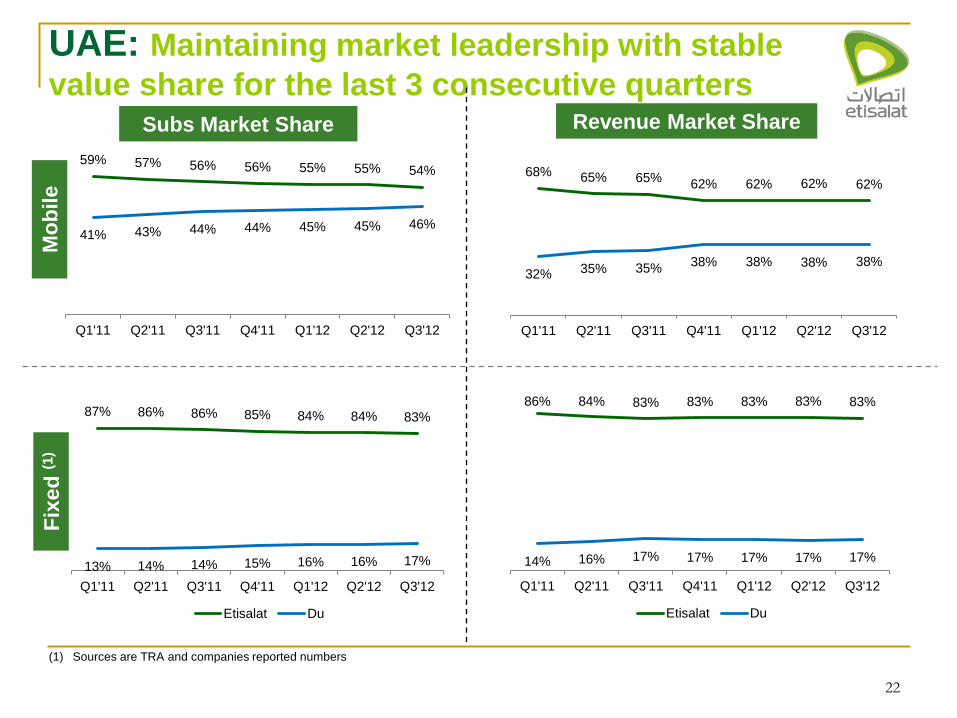

UAE: Maintaining market leadership with stable

value share for the last 3 consecutive quarters

(1) Sources are TRA and companies reported numbers

Mo

bile

Subs Market Share

Fix

ed

(1)

Revenue Market Share

59% 57% 56% 56% 55% 55% 54%

41% 43% 44% 44% 45% 45% 46%

Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12 Q3'12

87% 86% 86% 85% 84% 84% 83%

13% 14% 14% 15% 16% 16% 17%

Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12 Q3'12

Etisalat Du

68% 65% 65% 62% 62% 62% 62%

32% 35% 35% 38% 38% 38% 38%

Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12 Q3'12

86% 84% 83% 83% 83% 83% 83%

14% 16% 17% 17% 17% 17% 17%

Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12 Q3'12

Etisalat Du

23

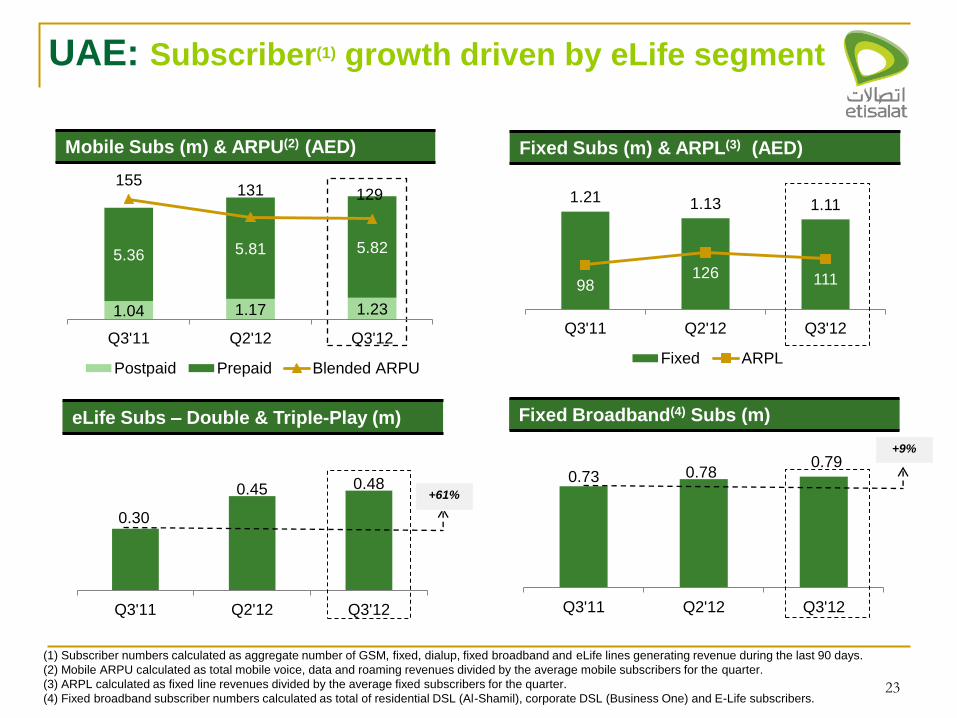

UAE: Subscriber(1) growth driven by eLife segment

(1) Subscriber numbers calculated as aggregate number of GSM, fixed, dialup, fixed broadband and eLife lines generating revenue during the last 90 days.

(2) Mobile ARPU calculated as total mobile voice, data and roaming revenues divided by the average mobile subscribers for the quarter.

(3) ARPL calculated as fixed line revenues divided by the average fixed subscribers for the quarter.

(4) Fixed broadband subscriber numbers calculated as total of residential DSL (Al-Shamil), corporate DSL (Business One) and E-Life subscribers.

Mobile Subs (m) & ARPU(2) (AED)

1.04 1.17 1.23

5.36 5.81 5.82

155 131 129

0

20

40

60

80

100

120

140

160

180

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Q3'11 Q2'12 Q3'12

Postpaid Prepaid Blended ARPU

Fixed Subs (m) & ARPL(3) (AED)

1.21 1.13 1.11

98 126 111

0

50

100

150

200

250

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Q3'11 Q2'12 Q3'12

Fixed ARPL

Fixed Broadband(4) Subs (m)

0.73 0.78 0.79

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Q3'11 Q2'12 Q3'12

eLife Subs – Double & Triple-Play (m)

0.30

0.45 0.48

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Q3'11 Q2'12 Q3'12

+61%

+9%

24

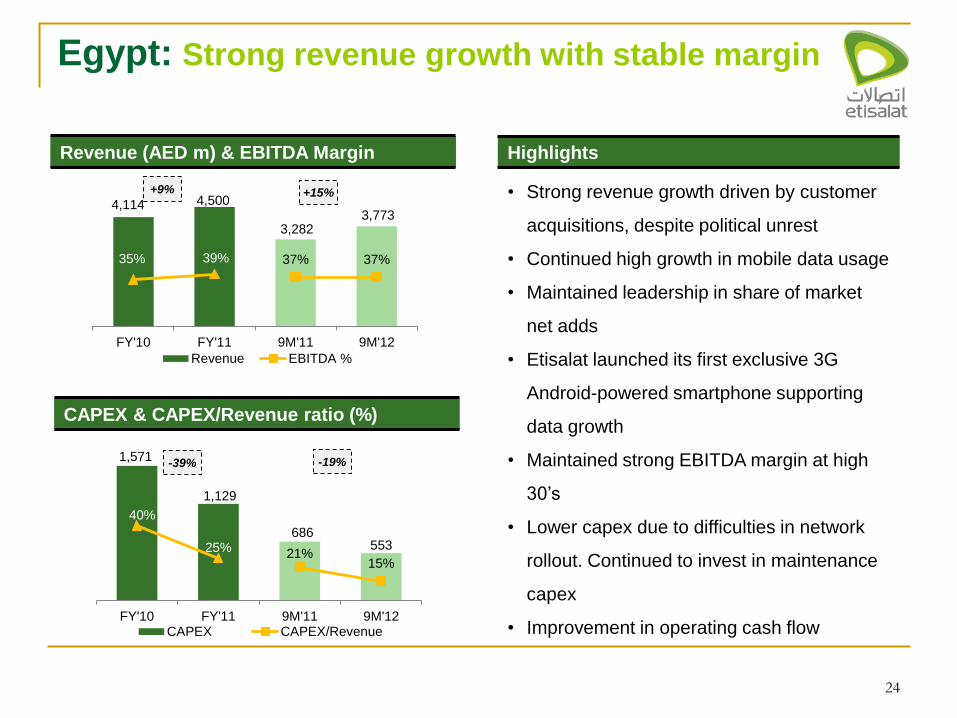

Egypt: Strong revenue growth with stable margin

Revenue (AED m) & EBITDA Margin

4,114 4,500

3,282 3,773

37% 37% 35% 39%

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

FY'10 FY'11 9M'11 9M'12

Revenue EBITDA %

+9% +15%

CAPEX & CAPEX/Revenue ratio (%)

1,571

1,129

686 553

21% 15%

40%

25%

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

(150)

50

250

450

650

850

1,050

1,250

1,450

1,650

FY'10 FY'11 9M'11 9M'12CAPEX CAPEX/Revenue

-39% -19%

Highlights

• Strong revenue growth driven by customer

acquisitions, despite political unrest

• Continued high growth in mobile data usage

• Maintained leadership in share of market

net adds

• Etisalat launched its first exclusive 3G

Android-powered smartphone supporting

data growth

• Maintained strong EBITDA margin at high

30’s

• Lower capex due to difficulties in network

rollout. Continued to invest in maintenance

capex

• Improvement in operating cash flow

25

Asia: Revenue growth with significantly improved

EBITDA margin Afghanistan, Sri Lanka, and India(1)

Highlights

• Strong revenue and subscriber growth in Sri Lanka

and Afghanistan

• 3G launched in Afghanistan

• Excluding India, Annual EBITDA margin from high-

10’s to mid-20’s

• Deconsolidation of India in Q1’12, impacted YoY

comparison of subscribers and EBITDA margin

Revenue (AED m) / EBITDA Margin

983

1,414

1,037 1,169

-17%

10%

-25% -13%

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

0

200

400

600

800

1,000

1,200

1,400

1,600

FY'10 FY'11 9M'11 9M'12

Revenue EBITDA %

+44 +13%

CAPEX & CAPEX/Revenue ratio (%)

Subscribers (m)

1,379

655

472 440

46% 38%

140%

46%

0.3

0.5

0.7

0.9

1.1

1.3

1.5

0

200

400

600

800

1,000

1,200

1,400

FY'10 FY'11 9M'11 9M'12

CAPEX

-52% -7%

8.5 8.2

9M'11 9M'12

-3%

(1) Financial statements of Etisalat DB in India were deconsolidated effective from March 1st 2012.

26

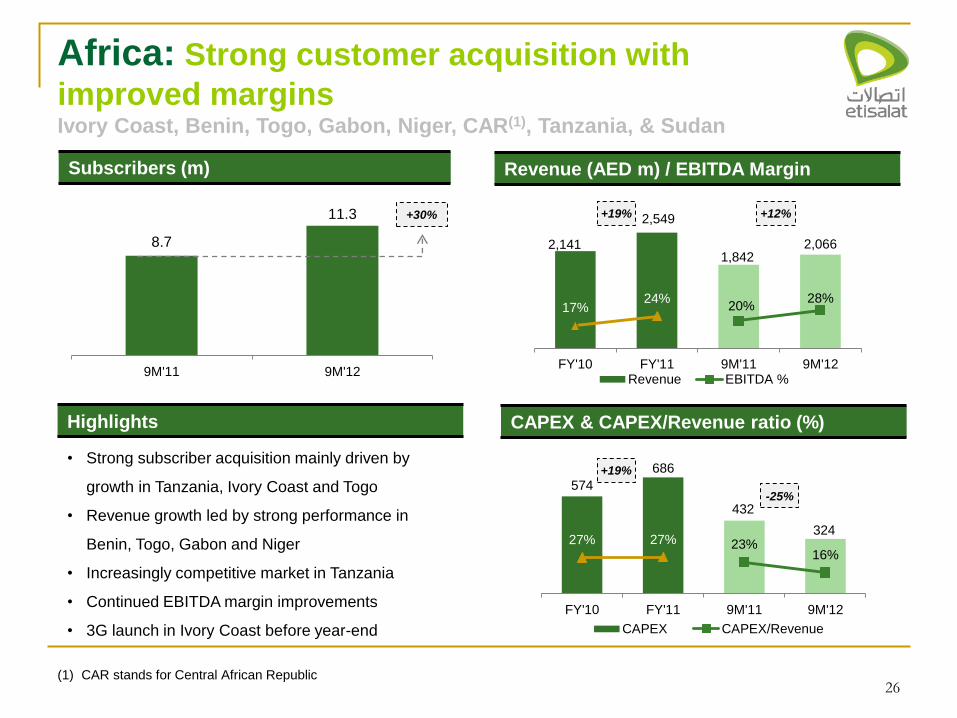

Highlights

• Strong subscriber acquisition mainly driven by

growth in Tanzania, Ivory Coast and Togo

• Revenue growth led by strong performance in

Benin, Togo, Gabon and Niger

• Increasingly competitive market in Tanzania

• Continued EBITDA margin improvements

• 3G launch in Ivory Coast before year-end

Africa: Strong customer acquisition with

improved margins Ivory Coast, Benin, Togo, Gabon, Niger, CAR(1), Tanzania, & Sudan

Revenue (AED m) / EBITDA Margin

2,141

2,549

1,842 2,066

20% 28%

17% 24%

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0

500

1,000

1,500

2,000

2,500

3,000

FY'10 FY'11 9M'11 9M'12Revenue EBITDA %

+19% +12%

CAPEX & CAPEX/Revenue ratio (%)

Subscribers (m)

8.7

11.3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

9M'11 9M'12

+30%

574

686

432

324 23%

16% 27% 27%

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0

100

200

300

400

500

600

700

800

FY'10 FY'11 9M'11 9M'12

CAPEX CAPEX/Revenue

+19%

-25%

(1) CAR stands for Central African Republic

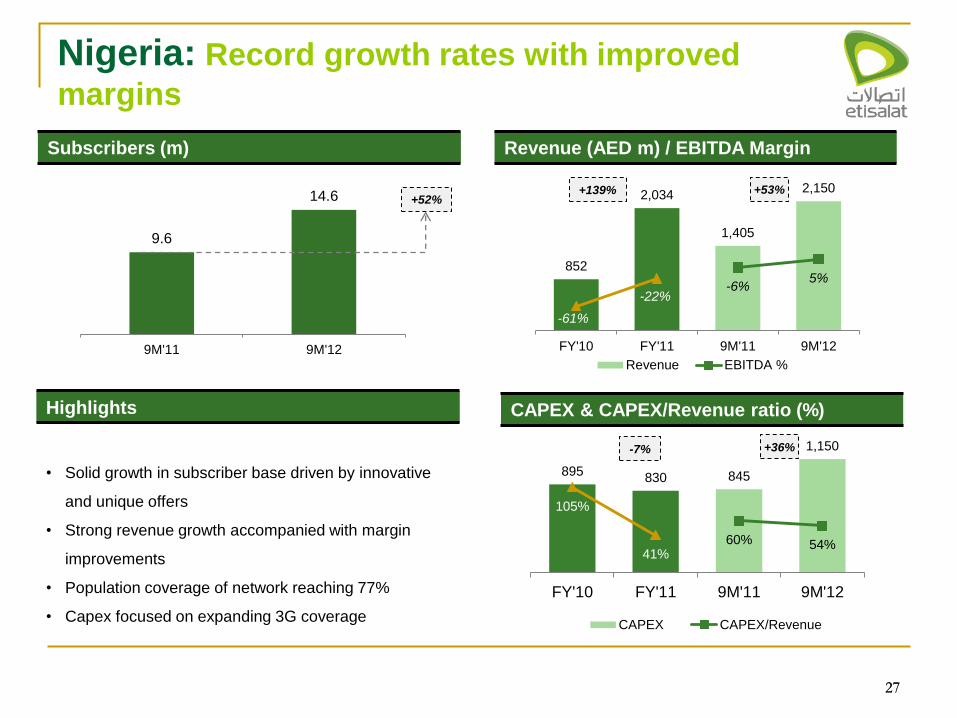

Subscribers (m)

9.6

14.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

9M'11 9M'12

27 27

Nigeria: Record growth rates with improved

margins

Highlights

• Solid growth in subscriber base driven by innovative

and unique offers

• Strong revenue growth accompanied with margin

improvements

• Population coverage of network reaching 77%

• Capex focused on expanding 3G coverage

+52%

Revenue (AED m) / EBITDA Margin

852

2,034

1,405

2,150

-6% 5%

-61%

-22%

(1)

(1)

(1)

(0)

(0)

0

0

0

1

1

0

500

1,000

1,500

2,000

FY'10 FY'11 9M'11 9M'12

Revenue EBITDA %

CAPEX & CAPEX/Revenue ratio (%)

+53%

895 830 845

1,150

60% 54%

105%

41%

(0)

0

0

1

1

1

1

1

2

0

200

400

600

800

1,000

1,200

FY'10 FY'11 9M'11 9M'12

CAPEX CAPEX/Revenue

+36%

+139%

-7%

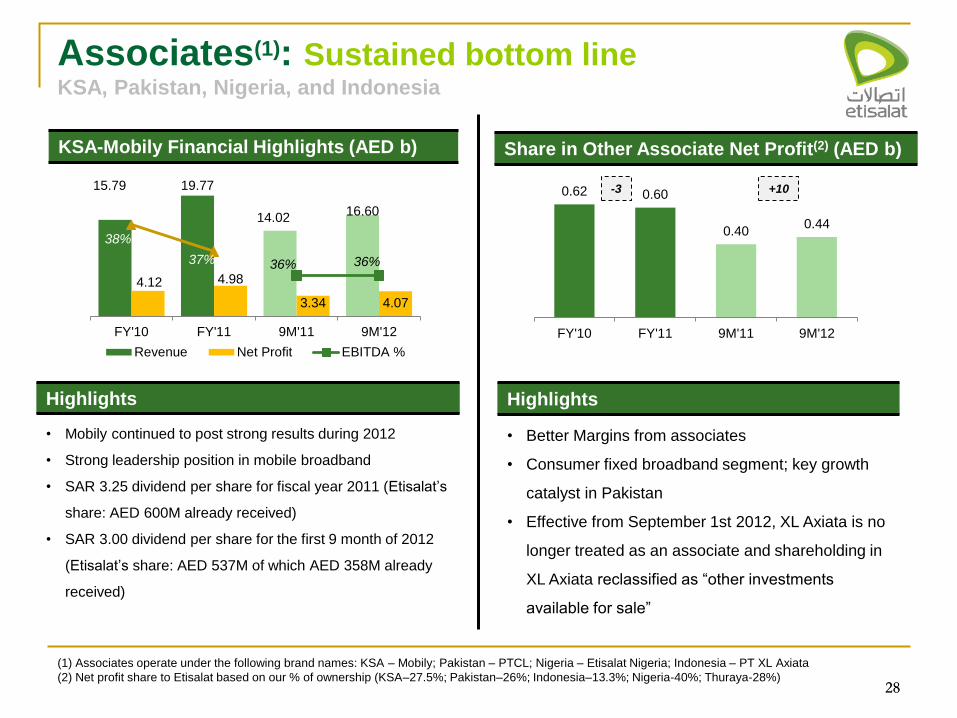

28

Share in Other Associate Net Profit(2) (AED b) KSA-Mobily Financial Highlights (AED b)

28

Associates(1): Sustained bottom line KSA, Pakistan, Nigeria, and Indonesia

(1) Associates operate under the following brand names: KSA – Mobily; Pakistan – PTCL; Nigeria – Etisalat Nigeria; Indonesia – PT XL Axiata

(2) Net profit share to Etisalat based on our % of ownership (KSA–27.5%; Pakistan–26%; Indonesia–13.3%; Nigeria-40%; Thuraya-28%)

Highlights

• Mobily continued to post strong results during 2012

• Strong leadership position in mobile broadband

• SAR 3.25 dividend per share for fiscal year 2011 (Etisalat’s

share: AED 600M already received)

• SAR 3.00 dividend per share for the first 9 month of 2012

(Etisalat’s share: AED 537M of which AED 358M already

received)

Highlights

• Better Margins from associates

• Consumer fixed broadband segment; key growth

catalyst in Pakistan

• Effective from September 1st 2012, XL Axiata is no

longer treated as an associate and shareholding in

XL Axiata reclassified as “other investments

available for sale”

15.79 19.77

14.02 16.60

4.12 4.98

3.34 4.07

36% 36%

38%

37%

0.34

0.35

0.36

0.37

0.38

0.39

0.4

0.002.004.006.008.00

10.0012.0014.0016.0018.0020.00

FY'10 FY'11 9M'11 9M'12

Revenue Net Profit EBITDA %

0.62 0.60

0.40 0.44

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

FY'10 FY'11 9M'11 9M'12

-3 +10

29

Etisalat Investor Relations

Email: [email protected]

Website: www.etisalat.com/html/ir

ADX ticker: Etisalat

ADX website: www.adx.ae