Embed Size (px)

Citation preview

FDI trends and APEC performance

2

FDI in the current market FDI in the current market

GIPB ResultsGIPB Results

Implications for IPIsImplications for IPIs

Learning Objectives of the CourseLearning Objectives of the Course

3

FDI in the recent economic recession

Source: World Investment Report 2012, United Nations Conference on Trade and Development UNCTAD Global Investment Trends Monitor, Issue No. 9, 2012

Recession Most severe recession since the Great

Depression

Global FDI flows dropped by about 40% between 2007 and 2009.

Recovery FDI inflows increased across all major

economic groupings in 2011

In developing and transition economies driven by robust greenfield investments, in developed countries due largely to cross-border M&As

Slower FDI growth predicted in 2012

Business response Significant decrease in access to credit

Re-capitalization of banks is taking place slowly in many countries

Lower corporate profits

Leading site selection firms report slowdown and postponement of investment projects

Companies restructuring to deal with the crisis; cautious about recovery

Investment plans frozen or discarded

De-locations and outright plant closures

4

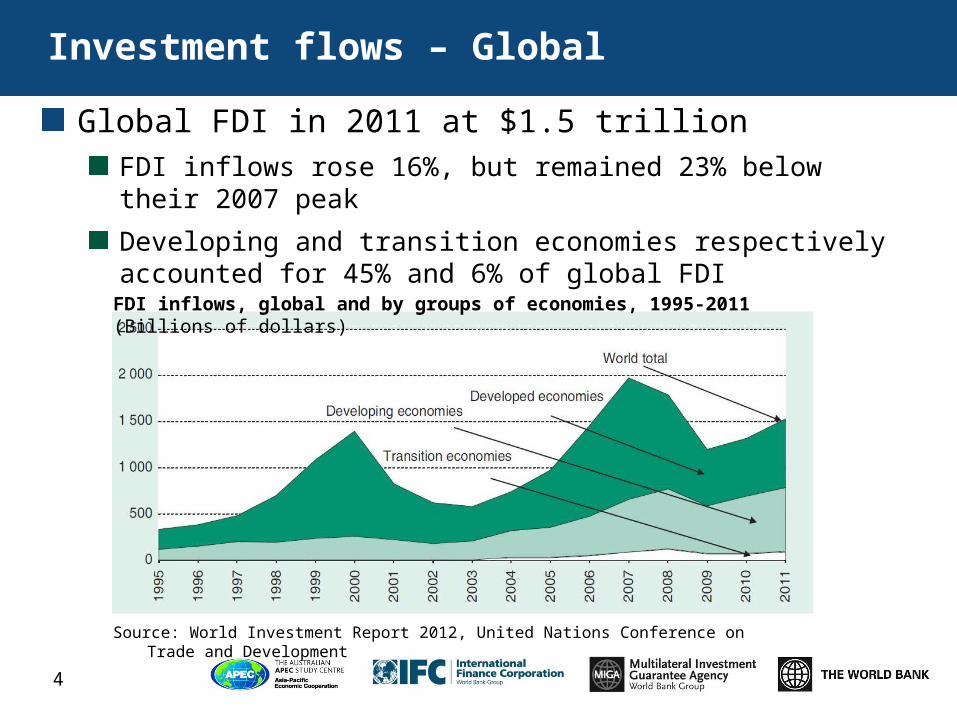

Investment flows – Global

Global FDI in 2011 at $1.5 trillionFDI inflows rose 16%, but remained 23% below their 2007 peak

Developing and transition economies respectively accounted for 45% and 6% of global FDI

Source: World Investment Report 2012, United Nations Conference on Trade and Development

FDI inflows, global and by groups of economies, 1995-2011 (Billions of dollars)

2011 investment flows – Developing economies and APEC

Developing economies

FDI inflows increased by 11%, reaching a record $684 billion

APEC

FDI inflows increased by 16% to $733 billion

Accounted for nearly half of the global total

APEC-8

FDI inflows increased by 6% to $82 billion

FDI inflows to China increased by 8%, to the USA by 15% and to Russia by 22%.

5

Investment flows – APEC

Like the global trend of the last 20 years, inflows have trended strongly upward with periodic setbacks.

APEC’s recovery has been stronger: 2011 only 8% under the 2007 peak

Most inflows go to the U.S. (31% of 2011 total), PR China (17%), Hong Kong, China (11%) and Russia (7%)

6

FDI Inflows to APEC, 1992-2011

US

$ bi

llion

Source: UNCTAD FDI Database

0

100

200

300

400

500

600

700

800

900

68123143

176211

250318

461

572

343

239213

382315

580

738794

478

632

733

Investment flows – APEC-8

Most FDI in 2011 went to Mexico (24%), Indonesia (23%) and Chile (21%)

Biggest % increase in FDI between 2009 and 2011 happened in Indonesia (288%), Thailand (97%), and Chile (34%)

7

Mill

ions

of

US

D

Source: UNCTAD FDI Database

FDI Inflows to the APEC-8, 2002-2011

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

-5000

0

5000

10000

15000

20000

25000

30000

35000

Chile

Indonesia

Mexico

Papua New Guinea

Peru

Philippines

Thailand

Viet Nam

Prospects for FDI recovery: 2012-2014

Slower FDI growth in 2012, with flows leveling off at about $1.6 trillion

Projections show FDI reaching $1.8 trillion in 2013 and $1.9 trillion in 2014

A resurgence in economic uncertainty and the possibility of lower growth rates in major emerging markets risks undercutting this favorable trend

Source: World Investment Report 2012, UNCTAD

Global FDI flows, 2002-2011, and projections for 2012-2014

8

Top 20 source countries for FDI in 2011

9

US = Japan + UK + France + Hong Kong

US$ billion

What can governments do to improve their chances?

Longer term:

Better infrastructure and skills ..... Expensive investments

Market size/growth and factor costs are functions of the

market - difficult to influence.

Proximity to markets, climate, resource endowments, and

other natural characteristics are what they are.

10

Short term:

A better investment climate:

Can be achieved with greater simplicity, transparency, and predictability

Is a result of better public organization, coordination, and communication with the private sector

Reduces costs and risk to investors, instantly improving the expected return on investment for your location

Good facilitation - compensates (at least to an extent) for weaknesses in the investment climate, giving investors clarity and security where there is none, through the provision of information and assistance.

11

What can governments do to improve their chances?

Why IPIs should bridge the corporate information gap

Information markets do not work perfectly. As a result, companies often limit their search to those locations they are already familiar with.

Effective IPI marketing convinces companies to consider different countries and new types of opportunities.

Current financial instability may make companies more cautious about their medium-term foreign expansions.

Making investor-relevant information easily available lessens their perceptions of risk.

Having highly relevant, accurate, and up-to-date information reduces an investor’s market entry cost.

Providing that information to investors, makes a location more competitive.

12

13

GIPB ResultsGIPB Results

FDI in the Current marketFDI in the Current market

Implications for IPIsImplications for IPIs

Learning Objectives of the CourseLearning Objectives of the Course

GIPB mirrors companies’ site selection process

Stepping in the shoes of two companies (manufacturing and software) a site location consultant assessed: IPI Websites-- The extent to which

IPIs offer country and sector information suitable to assist potential investors in their location search.

Inquiry handling -- A mystery shopper approach tested each IPI’s ability to interact with and manage two distinct investment inquiries, provide relevant information and make a business case for investment.

14

A 2011 survey of 3,600 US large companies ($25m+) conducted by DCI Consulting reveals that:

• 47% of respondents would use the IPI website in their next location search.

• Only 17% of respondents say they would not contact the IPI during the investment decision process

• Site location consultants are more likely to use the IPI services for information in the screening process.

Countries are missing investment projects and jobs

15

GIPB 2012 Regional Results: Web Site & Inquiry-Handling

Sub-Saharan Africa

South Asia

East Asia & Pacific

Middle East and N. Africa

World

APEC-8

Europe & Central Asia

Latin America & Caribbean

APEC

OECD - High Income

0% 10% 20% 30% 40% 50% 60% 70%

Web site

Inquiry Handling

APEC-8

APEC

When foreign companies come knocking, most IPIs fail even to respond.

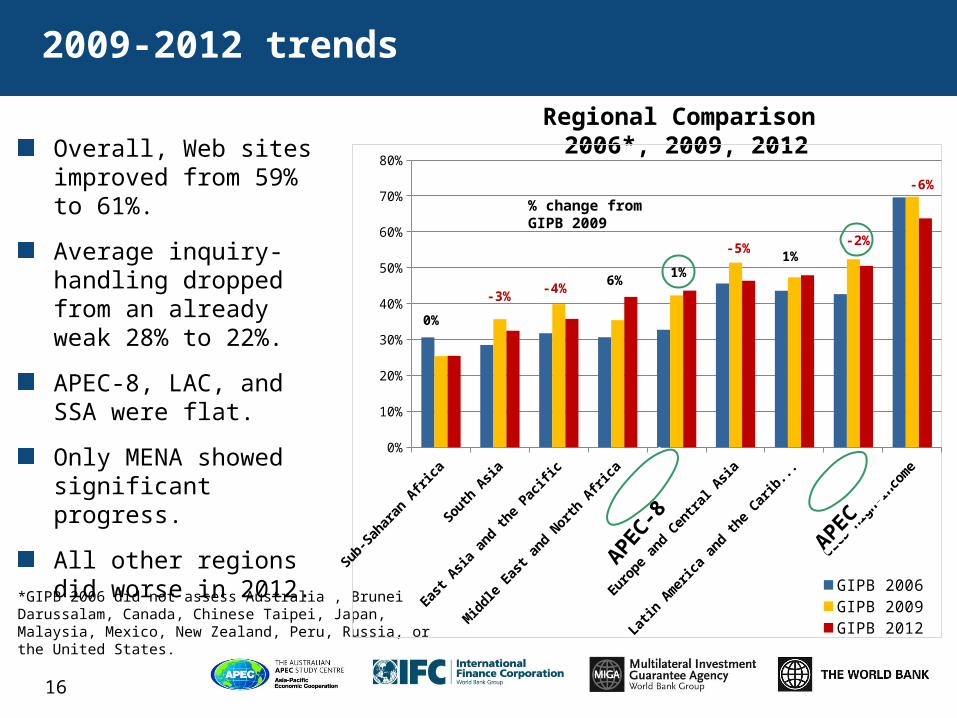

2009-2012 trends

Overall, Web sites improved from 59% to 61%.

Average inquiry-handling dropped from an already weak 28% to 22%.

APEC-8, LAC, and SSA were flat.

Only MENA showed significant progress.

All other regions did worse in 2012.

Regional Comparison 2006*, 2009, 2012

16

% change from GIPB 2009

*GIPB 2006 did not assess Australia , Brunei Darussalam, Canada, Chinese Taipei, Japan, Malaysia, Mexico, New Zealand, Peru, Russia, or the United States.

0%

10%

20%

30%

40%

50%

60%

70%

80%

GIPB 2006GIPB 2009GIPB 2012

0%

-3%-4%

6%1%

-5%1%

-2%

-6%

APEC-8

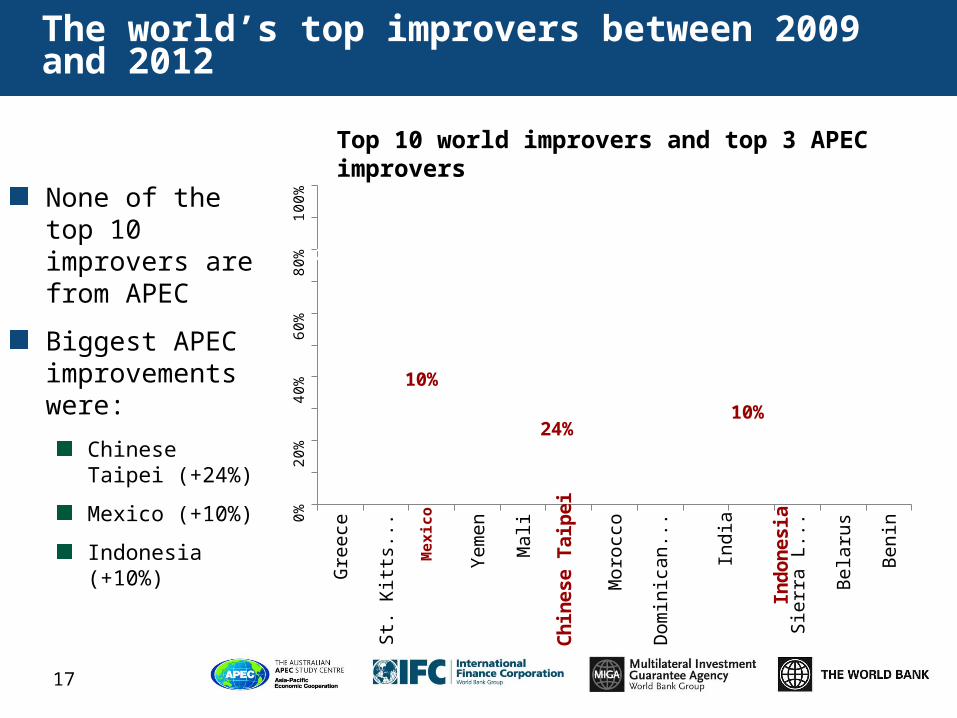

The world’s top improvers between 2009 and 2012

None of the top 10 improvers are from APEC

Biggest APEC improvements were:

Chinese Taipei (+24%)

Mexico (+10%)

Indonesia (+10%)

17

Top 10 world improvers and top 3 APEC improvers

Gre

ece

St.

Kitt

s a

nd

...

Ye

me

n

Ma

li

Mo

rocc

o

Do

min

ica

n R

...

Ind

ia

Sie

rra

Le

on

e

Be

laru

s

Be

nin0%

20%

40%

60%

80%

100%

28 %

31%

10%

40% 52%

24%

41% 36% 25%

10% 33% 26%

26%

Mex

ico

Ch

ines

e T

aip

ei

In

don

esia

Ind

ia

APEC performance (by tier)

18

BEST PRACTICE: 81-100%

GOOD: 61-80%

AVERAGE: 41-60%

WEAK: 21-40%

VERY WEAK: 0-20%

Hong Kong, China

AustraliaCanada

New Zealand Singapore

Brunei Darussalam Chile Chinese Taipei Indonesia Japan Rep. of Korea Malaysia Mexico Peru Philippines Thailand USA

Papua New GuineaPeople’s Republic of China

Viet Nam

Russia

19

GIPB ResultsGIPB Results

FDI in the Current MarketFDI in the Current Market

Implications for IPIsImplications for IPIs

Learning Objectives of the CourseLearning Objectives of the Course

20

Get the basics right …… facilitation, facilitation, facilitation

IPIs underestimate what is needed

Without proper facilitation no investment promotion effort will pay off

The smaller the IPI budget, the more sense facilitation makes

Focus on the basics: Walk before you run

Countries where doing business is more challenging

Bigger role for the IPI to inform and facilitate foreign investors

Lesser known countries

Bridge the information gap through the work of the IPI to attract investment

The Web allows all IPIs to promote cost-effectively

…... but there must also be a capacity to directly interact with investors

21

GIPB ResultsGIPB Results

FDI in the Current MarketFDI in the Current Market

Learning Objectives of the CourseLearning Objectives of the Course

Implications for IPIsImplications for IPIs

Learning objectives of the GIPB course

Day One

Understand the types of information investors need and their process for site selection decision making

Engage in a simulated investor inquiry simulation and discuss the realities and challenges of competing for investment

Review a case study of why the application of good investment facilitation techniques matters

Learn how to effectively promote your location online

22

Learning objectives of the GIPB course

Day Two

Apply learning about online investment promotion from Day One to a case on an IPI Web site

Understand the standards of performance for providing support to investors and how to evaluate the quality of responses to investor inquiries

Learn how to meet investors’ information needs through the appropriate design of IPI services and supporting systems and processes

Engage in an effective inquiry handling exercise

Develop an action plan to strengthen investment facilitation

23

Thank you.

Questions