Embed Size (px)

Citation preview

Illustrative Individual Financial Statements for a UK Parent Company applying FRS 101 (Reduced Disclosure Framework), transitioning from UK GAAPComplying with FRS 101, the Companies Act 2006, and other UK requirements extant 31 December 2013

31 December 2013

Illustrative Individual Financial

Statements for a UK Parent Company applying FRS 101 (Reduced Disclosure Framework), transitioning from UK GAAP 31 December 2013

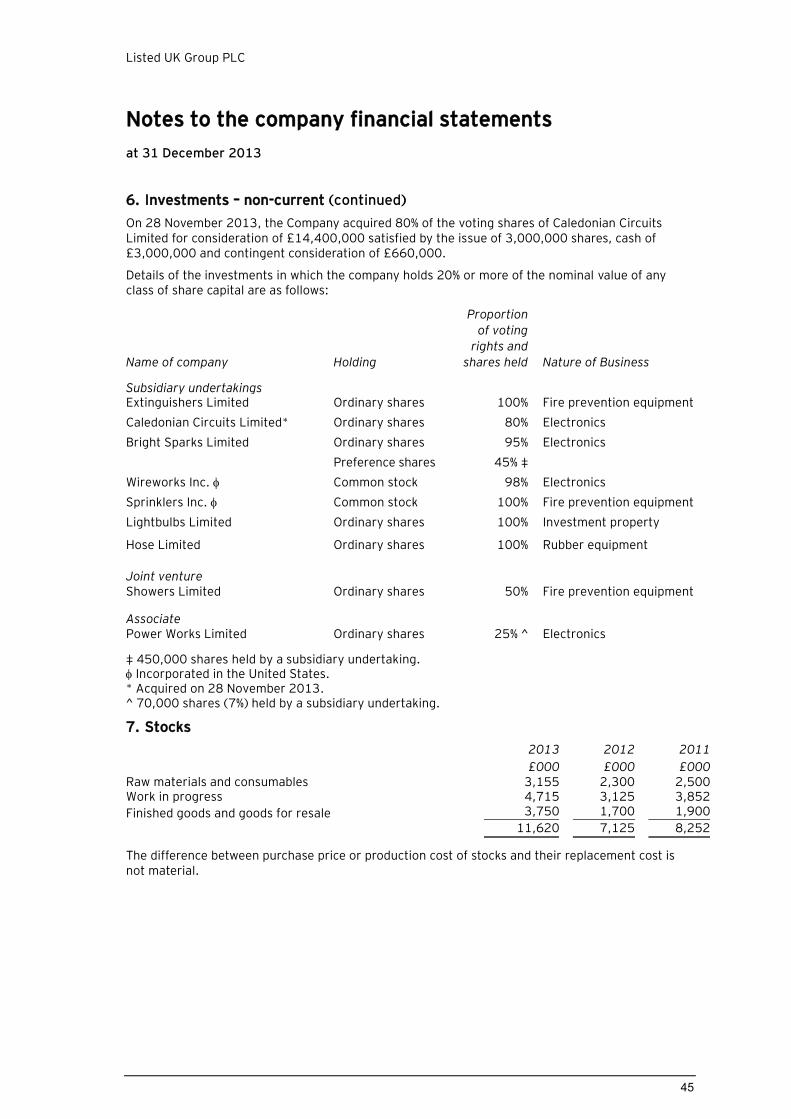

Complying with FRS 101, the Companies Act 2006, and other UK requirements extant 31 December 2013

© Copyright Ernst & Young LLP 2013.

The United Kingdom firm Ernst & Young LLP is a limited liability partnership registered in England and Wales with a registered number OC300001 and is a member practice of Ernst & Young Global.

Apart from any fair dealing for the purposes of research or private study, or criticism or review, as permitted under the Copyright, Designs and Patents Act, 1988, this publication may only be reproduced, stored or transmitted, in any form or by any means, with the prior permission in writing of the publishers, or in the case of reprographic reproduction in accordance with the terms of licences issued by the Copyright Licensing Agency, 90 Tottenham Court Road, London, W19 9HE, United Kingdom. Enquiries concerning reproduction outside those terms should be sent to the authors at the undermentioned address:

Financial Reporting Group Ernst & Young LLP 1 More London Place London SE1 2AF United Kingdom

Published 2013 by:

Ernst & Young LLP

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgement. Accordingly, to the fullest extent permitted by law, neither Ernst & Young LLP nor any other member of the global Ernst & Young organisation accept or assume any responsibility or liability for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate adviser.

The Illustrative Financial Statements have been prepared by the Financial Reporting Group of Ernst & Young LLP.

Contents

i

INTRODUCTION ............................................................................................................................. II

ABBREVIATIONS ........................................................................................................................... IV Strategic report and directors' report……………………………………………………………………………………………. 3

Statement of directors’ responsibilities for the parent company financial statements ............... 5 Independent auditor's report……………………………………………………………………………………………………………7

Company statement of comprehensive income……………………………………………………………………..…… 11

Company balance sheet………………………………………………………………………………………………………………….13

Company statement of changes in equity……………………………………………………………………………………..17

Notes to the company financial statements………………………………………………………………………………….19

1. Accounting policies ................................................................................................ 19 2. Deferred Tax .......................................................................................................... 39 3. Dividends paid and proposed ................................................................................... 39 4. Profit attributable to members of the parent company ............................................. 41 5. Tangible fixed assets .............................................................................................. 41 6. Investments – non-current ...................................................................................... 43 7. Stocks.................................................................................................................... 45 8. Debtors .................................................................................................................. 47 9. Creditors: amounts falling due within one year......................................................... 47 10. Creditors: amounts falling due after more than one year .......................................... 49 11. Loans .................................................................................................................... 49 12. Obligations under leases and hire purchase contracts .............................................. 51 13. Provisions for liabilities ........................................................................................... 51 14. Derivative financial instruments .............................................................................. 53 15. Called up share capital ............................................................................................ 53 16. Own Shares ............................................................................................................ 55 17. Pensions and other post-employment benefits ......................................................... 57 18. Share-based payments ........................................................................................... 59 19. Post balance sheet event ........................................................................................ 61 20. Capital commitments .............................................................................................. 61 21. Contingent liabilities ............................................................................................... 61 22. Auditors’ remuneration ........................................................................................... 63 23. Related Party Transactions ..................................................................................... 63 24. Off-balance sheet arrangements ............................................................................. 65 25. Reserves ................................................................................................................ 65 26. Transition to FRS 101 ............................................................................................. 67

ii

Introduction

This publication contains the parent company individual financial statements of a fictional UK company, Listed UK Group plc, a public company preparing consolidated financial statements under EU-adopted IFRS and individual financial statements in accordance with FRS 101 (Reduced Disclosure Framework). The IFRS Consolidated financial statements and accompanying Group directors’ report are not contained in this document. The financial statements are illustrative only and do not attempt to show all possible disclosure requirements. If there is doubt as to the applicable legal or other requirements, readers should refer to the relevant source and, where necessary, seek professional advice.

This publication is laid out with the commentary on the left hand pages and the illustrative disclosures on the right hand pages. Gaps between items exist to align commentary with the relevant disclosure item, as far as possible, for the convenience of users.

Although the illustrative financial statements attempt only to show the likely disclosure requirements of parent companies, they should not be regarded as a comprehensive checklist of statutory and accounting requirements. They comply with FRS 101, the Companies Act 2006 and with other requirements in force at 31 December 2013. The Company has transitioned from previously extant UK GAAP, and is continuing to prepare Companies Act individual accounts in accordance with s395(1)(a) of the Act.

Narrative accompanying the illustrative financial statements

The narrative accompanying the illustrative financial statements (on the left-hand pages) contains source references to the Companies Act, FRS 101, International Financial Reporting Standards, Interpretations of the IFRS Interpretations Committee, and pronouncements of the Institute of Chartered Accountants in England and Wales. When the narrative accompanying the financial statements is italicised, it indicates that the requirement discussed is not in fact illustrated. Such narrative has not been given for every conceivable disclosure requirement. Accordingly the narrative should not be regarded as a comprehensive checklist.

Listed Group UK plc

These are the financial statements of a public company preparing its individual accounts under FRS 101 and taking advantage of all of the IFRS disclosure exemptions allowed under this standard which are applicable to this entity.

Listed Group UK plc is a qualifying entity in accordance with FRS 100, and therefore these are not IAS Accounts as defined by section 395(1) (b) of the Companies Act 2006, so the entity must make amendments to EU-adopted IFRS requirements where necessary, in order that the financial statements it prepares are Companies Act individual accounts as defined by s395(1)(a) of the Act.

The financial statements are illustrative only and they should not be regarded as a pro forma set of financial statements.

These financial statements have been prepared for the year ended 31 December 2013, and therefore IFRS 13 Fair Value Measurement, IAS 19 Revised Employee Benefits and IAS 1 (Amendment) Presentation of Financial Statements have all been adopted as these are mandatory for this year end.

IFRSs 10-12 and the revised versions of IAS27 and IAS 28 have not been applied as they are not mandatory before accounting periods beginning on or after 1 January 2014.

Introduction

iii

Narrative accompanying the illustrative financial statements (continued)

FRS 101

FRS 101 was issued in November 2012 and is part of the Financial Reporting Council’s (FRC’s) revised financial reporting standards in the United Kingdom and Republic of Ireland. The revisions fundamentally reform financial reporting, replacing almost all extant standards with three Financial Reporting Standards:

FRS 100 Application of Financial Reporting Requirements (November 2012)

FRS 101 Reduced Disclosure Framework (November 2012); and

FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland (March 2013).

FRS 101 applies to the individual financial statements of a qualifying entity, as defined below, that are intended to give a true and fair view of the assets, liabilities and financial position and of the profit or loss for a period.

A qualifying entity is a “member of a group where the parent of that group prepares publicly available consolidated financial statements which are intended to give a true and fair view (of the assets, liabilities, financial position and profit or loss) and that member is included in the consolidation (as set out in s474(1) of the Companies Act.” A charity may not be a qualifying entity.

In applying FRS 101, a qualifying entity may take advantage of the disclosure exemptions in the standard. In order to take advantage of these disclosure exemptions:

Its shareholders must have been notified in writing about, and do not object to, the used of the disclosure exemptions.

It otherwise applies as its financial reporting framework the recognition, measurement and disclosure requirements of EU adopted IFRS, but makes amendments to EU adopted IFRS requirements where necessary in order to comply with the Act and the Regulations, given that the financial statements that it prepares are Companies Act accounts as defined in section 395(1)(b) of the Act.

It discloses in the notes to its financial statements:

o A brief narrative summary of the disclosure exemptions adopted; and

o The name of the parent of the group in whose consolidated financial statements it financial statements are consolidated and from where those financial statements may be obtained.

Listed Group UK plc complies with Schedule 1 of the Companies Act 2006, and is not a financial institution.

A qualifying entity which is a financial institution may not take advantage of the exemptions from IFRS 7, IFRS 13 (in respect of disclosures of financial instruments) and paragraphs 134 to 136 of IAS 1.

FRS 101 is effective for accounting periods beginning on or after 1 January 2015, although early application is permitted. If the entity applies this FRS before 1 January 2015 it must disclose this fact.

Formats

The formats used in the illustrative financial statements are taken from Schedule 1 to the Regulations. The balance sheet is in format 1.

iv

Abbreviations

The following abbreviations are used in these illustrative financial statements:

Companies Act The Companies Act 2006

s235(3) Companies Act, Section 235, paragraph 3

7 Sch 2(1) Large and Medium-Sized Companies and Groups (Accounts and Reports) Regulations 2008, Schedule 7, paragraph 2(1)

APB Auditing Practices Board

FRC Financial Reporting Council

FRS101.10 Financial Reporting Standard 101, paragraph 10

FRS 101.AG1(k) Financial Reporting Standard 101, Application Guidance paragraph AG1 subsection (k)

IFRS 1.39 International Financial Reporting Standard 1, paragraph 39

IAS 39.AG71 International Accounting Standard 39, application guidance, paragraph 71

IAS 39.G.1 Guidance on Implementing IAS 39: Financial Instruments: Recognition and Measurement, Section G, item G.1

IASB International Accounting Standards Board

ICAS The Institute of Chartered Accountants in Scotland

ISA (UK&I) 700(14) International Standard on Auditing (UK and Ireland) No. 700, paragraph 14

ICAEW The Institute of Chartered Accountants in England and Wales

IFRIC Interpretations issued by the IFRS Interpretations Committee

Regulations Large and Medium sized Companies and Groups (Accounts and Reports) Regulations 2008

SI 2011/2198 The Companies (Disclosure of Auditor Remuneration and Liability Limitation Agreements) (Amendment) Regulations 2011 (Statutory Instrument 2011 No. 2198)

SIC 12.8 SIC Interpretation 12, paragraph 8

TECH 2/10 Technical Release 02/10, issued by the ICAEW and ICAS

Listed UK Group PLC

1

Listed Parent Company Financial

Statements under FRS 101 31 December 2013

These financial statements of the parent company have been prepared in accordance with FRS 101 – Reduced Disclosure Framework. They represent the parent company financial statements that would be presented with consolidated financial statements prepared in accordance with IFRS. For this reason neither a Strategic Report nor a Directors’ Report has not been presented as this would form part of the group Annual Report.

The commentary given in respect of the parent company financial statements is restricted to the disclosures which have been made therein. It is not designed to represent a complete list of requirements for applying FRS101 with reduced disclosures.

Illustrative financial statements

Comments on the Strategic Report and Directors’ Report

2

These are the Illustrative individual financial statements of a parent which will be presented together with the Group Financial statements. As such no individual Strategic Report and Directors’ Report has been illustrated. Refer to FRS 101 Illustrative Financial Statements of Entity UK Limited for an Illustrative Strategic Report and Directors’ Report for a company preparing financial statements under FRS 101.

Listed UK Group PLC

Strategic Report and Directors’ Report

3

Refer to the Strategic Report and Directors’ Report in FRS 101 Illustrative Financial Statements Entity UK Limited, for an example of a Strategic Report and Directors’ Report for a company

preparing financial statements under FRS 101.

Illustrative financial statements

Comments on the Directors’ responsibilities statement

4

Directors’ responsibilities in respect of the financial statements

APB 2010/02 App 17

An illustrative example of a directors’ responsibilities statement for a non-publicly traded company appears in Appendix 17 of APB 2010/02. This has been replicated in Entity UK Limited except for the fourth bullet point on going concern since a separate statement on going concern is included in the Directors’ Report. The third bullet point does not apply to Small or Medium-Sized companies.

Listed UK Group PLC

Directors’ responsibilities statement

5

Statement of directors’ responsibilities for the parent company financial statements

The directors are responsible for preparing the Directors’ Report and the financial statements in accordance with applicable UK law and regulations.

Company law requires the directors to prepare financial statements for each financial year. Under that law the directors have elected to prepare the financial statements in accordance with United Kingdom Generally Accepted Accounting Practice (United Kingdom Accounting Standards and applicable law). Under company law the directors must not approve the financial statements unless they are satisfied that they give a true and fair view of the state of affairs of the Company and of the profit or loss for that period.

In preparing those financial statements, the directors are required to:

select suitable accounting policies and then apply them consistently;

make judgements and estimates that are reasonable and prudent; and

state whether applicable UK Accounting Standards have been followed, subject to any material departures disclosed and explained in the financial statements; and

prepare the financial statements on a going concern basis, unless they consider that to be inappropriate.

The directors are responsible for keeping adequate accounting records that are sufficient to show and explain the Company’s transactions and disclose with reasonable accuracy at any time the financial position of the Company and enable them to ensure that the financial statements comply with the Companies Act 2006. They are also responsible for safeguarding the assets of the Company and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

Illustrative financial statements

Comments on the independent auditor’s report

6

Independent auditor’s report

s495(1)

An auditor’s report is required to be attached to all annual accounts of the company of which copies are required to be sent to members under s423 (a private company) or which are to be laid before the company in general meeting under s437 ( a public company).

s495(2)

The auditor’s report must include:

an introduction identifying the annual accounts that are the subject of the audit and the financial reporting framework that has been applied in their preparation;

a description of the scope of the audit identifying the auditing standards in accordance with which the audit was conducted.

s495(3)

The auditor’s report must state clearly whether, in the auditor’s opinion, the annual accounts:

give a true and fair view of the company and/or group at the end of the financial year and of the profit or loss for the financial year;

have been properly prepared in accordance with the relevant financial reporting framework; and

have been prepared in accordance with the requirement of the Companies Act 2006 (and, where applicable, Article 4 of the IAS Regulation).

s495(4)

The auditor’s report must be either unqualified or qualified and must include a reference to any matters to which the auditor wishes to draw attention by way of emphasis without qualifying the report.

s496

The auditor must state in his report on the annual accounts whether in his opinion the information given in the directors’ report is consistent with the financial statements.

s497

The auditor must state in his report on the annual accounts whether in his opinion the auditable part of the directors’ remuneration report has been properly prepared in accordance with the requirements of the Companies Act 2006.

s498(2)

The auditor shall state in his report if he is of the opinion that:

adequate accounting records have not been kept, or that returns adequate for the audit have not been received from branches not visited by him;

the company’s individual accounts are not in agreement with the accounting records or returns; or

that the auditable part of the directors’ remuneration report is not in agreement with the accounting records and returns.

s498(3)

The auditor must state in his report if he fails to obtain all the information and explanations which, to the best of his knowledge and belief, are necessary for the purposes of his audit.

s498(4)

If the requirements related to disclosure of directors’ benefits under s412 and remuneration under s421 are not complied with the auditor must include a statement in his report giving the required particulars.

s503(3)

The auditor’s report must state the name of the auditor and be signed and dated. Where the auditor is an individual, the report must be signed by him. Where the auditor is a firm, the report must be signed by the senior statutory auditor in his own name, for and on behalf of the auditor.

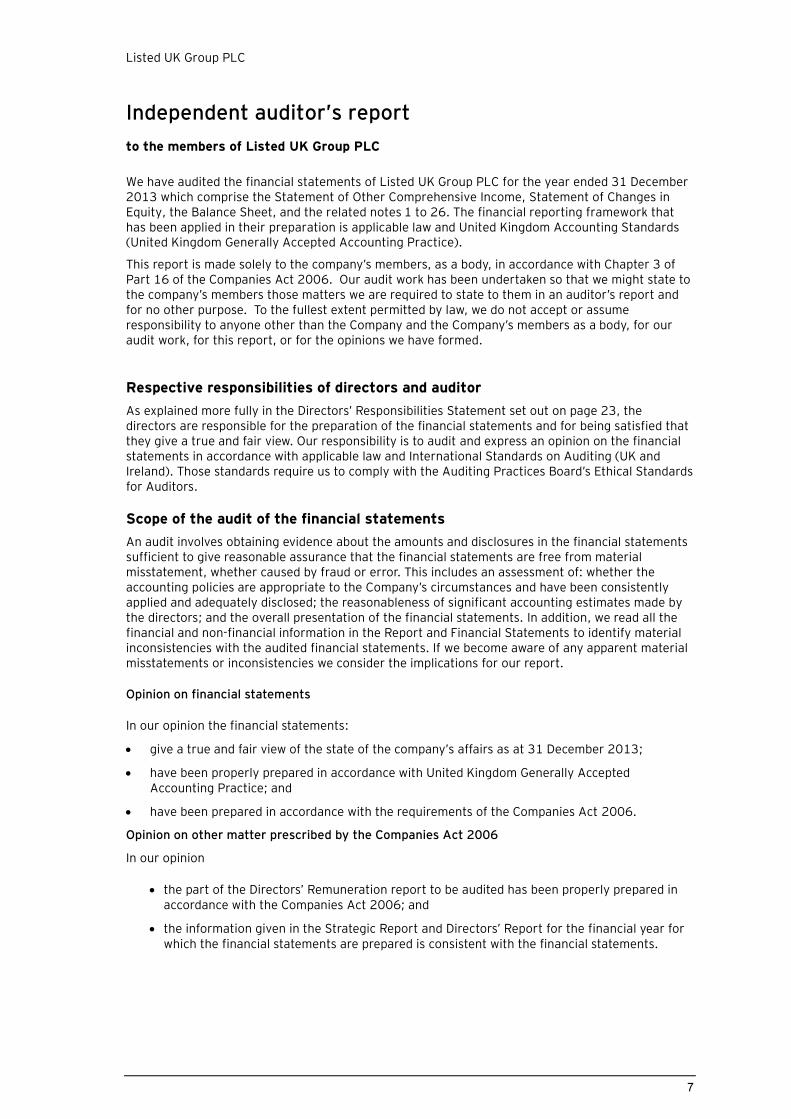

Listed UK Group PLC

Independent auditor’s report

to the members of Listed UK Group PLC

7

We have audited the financial statements of Listed UK Group PLC for the year ended 31 December 2013 which comprise the Statement of Other Comprehensive Income, Statement of Changes in Equity, the Balance Sheet, and the related notes 1 to 26. The financial reporting framework that has been applied in their preparation is applicable law and United Kingdom Accounting Standards (United Kingdom Generally Accepted Accounting Practice).

This report is made solely to the company’s members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company’s members as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of directors and auditor

As explained more fully in the Directors’ Responsibilities Statement set out on page 23, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view. Our responsibility is to audit and express an opinion on the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s Ethical Standards for Auditors.

Scope of the audit of the financial statements

An audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the Company’s circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the directors; and the overall presentation of the financial statements. In addition, we read all the financial and non-financial information in the Report and Financial Statements to identify material inconsistencies with the audited financial statements. If we become aware of any apparent material misstatements or inconsistencies we consider the implications for our report.

Opinion on financial statements

In our opinion the financial statements:

give a true and fair view of the state of the company’s affairs as at 31 December 2013;

have been properly prepared in accordance with United Kingdom Generally Accepted Accounting Practice; and

have been prepared in accordance with the requirements of the Companies Act 2006.

Opinion on other matter prescribed by the Companies Act 2006

In our opinion

the part of the Directors’ Remuneration report to be audited has been properly prepared in accordance with the Companies Act 2006; and

the information given in the Strategic Report and Directors’ Report for the financial year for which the financial statements are prepared is consistent with the financial statements.

Illustrative financial statements

8

Listed UK Group PLC

Independent auditor’s report

to the members of Listed UK Group PLC

9

Matters on which we are required to report by exception

We have nothing to report in respect of the following matters where the Companies Act 2006 requires us to report to you if, in our opinion:

adequate accounting records have not been kept, or returns adequate for our audit have not been received from branches not visited by us; or

the Company financial statements and the part of the Directors’ remuneration report to be audited are not in agreement with the accounting records and returns; or

the financial statements are not in agreement with the accounting records and returns; or

certain disclosures of directors’ remuneration specified by law are not made; or

we have not received all the information and explanations we require for our audit.

[Signature

John Smith (Senior statutory auditor)

for and on behalf of Ernst & Young LLP, Statutory Auditor

City

Date]

Preparers should ensure that the wording of the audit report complies with current guidance from the APB and PPD and is tailored to the specific circumstances of the reporting entity.

Audit teams should also ensure that they apply the most recent internal guidance on the format of the signatures required on the audit reports to be delivered to the company and to the registrar.

Companies House have issued a document detailing the most common reasons why a set of submitted annual accounts is rejected. This document can be found at www.companieshouse.gov.uk/about/pdf/commonAccountsRejections.pdf

Illustrative financial statements

Comments on the statement of comprehensive income

10

Statement of comprehensive income

IAS 1.81A

The statement of profit or loss and other comprehensive income (statement of comprehensive income) shall present, in addition to the profit or loss and other comprehensive income sections:

(a) profit or loss; (b) total other comprehensive income; (c) comprehensive income for the period, being the total of profit or loss and other comprehensive income. If an entity presents a separate statement of profit or loss it does not present the profit or loss section in the statement presenting comprehensive income.

IAS 1.81B

An entity shall present the following items, in addition to the profit or loss and other comprehensive income sections, as allocation of profit or loss and other comprehensive income for the period: (b) comprehensive income for the period attributable to:

(i) non-controlling interests, and

(ii) owners of the parent.

FRS 101.AG1(i)

A qualifying entity shall present the components of profit or loss in the statement of comprehensive income (in either a the single statement or two statement approach) in accordance with the profit and loss account formats requirements of the Act instead of paragraphs 82 and 84 to 86 of IAS 1 Presentation of financial statements. The entity may elect to apply the requirements of those paragraphs so long as the resulting statement of comprehensive income complies with the profit and loss account format requirements of the Act.

Author’s note The disclosure above is not required if it conflicts with the Companies Act.

IAS 1.90

An entity shall disclose the amount of income tax relating to each component of other comprehensive income, including reclassification adjustments, either in the statement of comprehensive income or in the notes.

IAS 1.91

An entity may present components of other comprehensive income either:

net of related tax

effects, or before related tax effects

with one amount shown for the aggregate amount of income tax relating to those components.

If the entity elects alternative (b), it shall allocate the tax between the items that might be reclassified subsequently to the profit or loss section and those that will not be reclassified subsequently to the profit and loss account.

IAS 1.92 - 94

An entity shall disclose reclassification adjustments relating to components of other comprehensive income. Other IFRSs specify whether and when amounts previously recognised in other comprehensive income are reclassified to profit or loss. Such reclassifications are referred to in this Standard as reclassification adjustments. A reclassification adjustment is included with the related component of other comprehensive income in the period that the adjustment is reclassified to profit or loss. For example, gains realised on the disposal of available-for-sale financial assets are included in profit or loss of the current period. These amounts may have been recognised in other comprehensive income as unrealised gains in the current or previous periods. Those unrealised gains must be deducted from other comprehensive income in the period in which the realised gains are reclassified to profit or loss to avoid including them in

total comprehensive income twice. An entity may present reclassification adjustments in the statement of comprehensive income or in the notes. An entity presenting reclassification adjustments in the notes presents the components of other comprehensive income after any related reclassification adjustments.

IAS 12.61A Current tax and deferred tax shall be recognised outside profit or loss if the tax relates to items that are recognised, in the same or a different period, outside profit or loss. Therefore, current tax and deferred tax that relates to items that are recognised, in the same or a different period:

in other comprehensive income, shall be recognised in other comprehensive income (examples of such items include revaluations of property, plant and equipment).

Non-publication of performance statements and related notes

Author’s note

Only the parent company balance sheet has been published by Listed UK Group PLC. The company has taken the exemption under s408 of the Companies Act not to publish the parent company profit and loss account. Practice in the United Kingdom has developed whereby an entity taking the s408 exemption does not publish a SOCI either. By virtue of s472(2), the exemption from publication under s408 extends to the notes to the profit and loss account. A SOCIE has been presented as there is no exemption in FRS 101 from the requirement under IAS 1.10(c).

Listed UK Group PLC

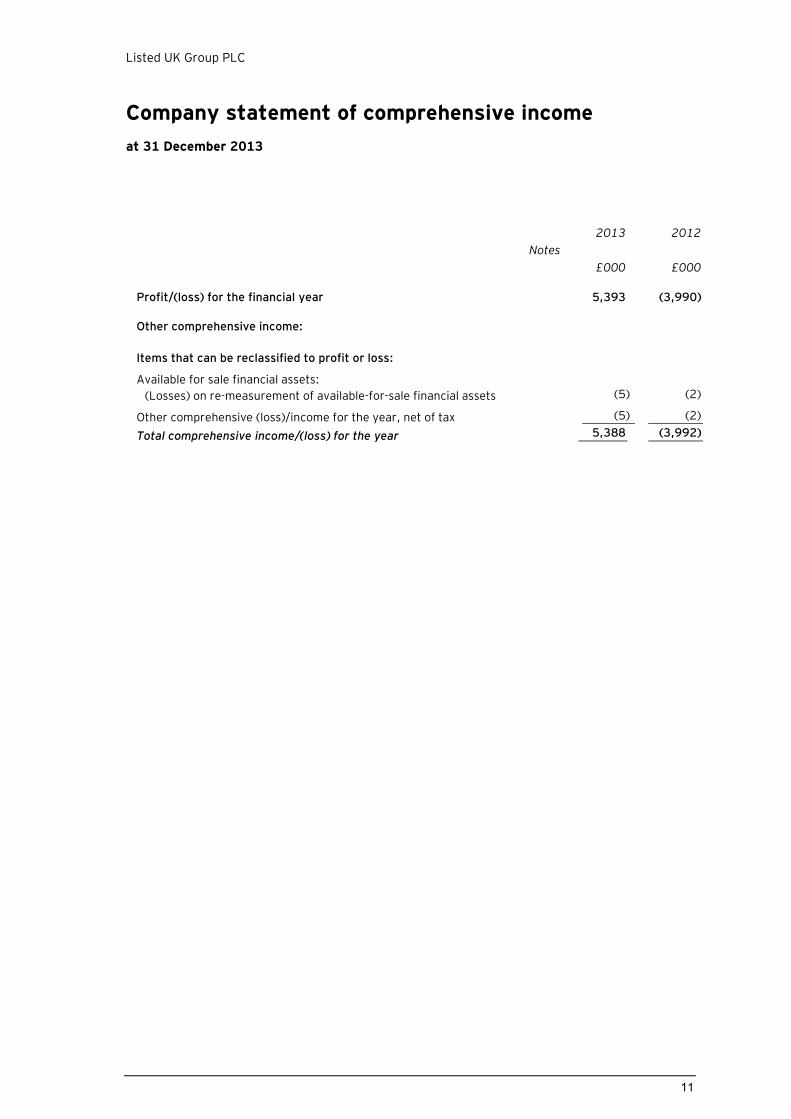

Company statement of comprehensive income

at 31 December 2013

11

Notes

2013 2012

£000 £000 Profit/(loss) for the financial year 5,393 (3,990)

Other comprehensive income:

Items that can be reclassified to profit or loss:

Available for sale financial assets:

(Losses) on re-measurement of available-for-sale financial assets (5) (2)

Other comprehensive (loss)/income for the year, net of tax (5) (2)

Total comprehensive income/(loss) for the year 5,388 (3,992)

Illustrative financial statements

Comments on the company balance sheet

12

Formats

1 Sch 1, 1 Sch 4(2), (3), 1 Sch 5, 6 Sch 17, 21

The face of every balance sheet must show the items denoted by letters or Roman numbers in the format specified by the Companies Act, unless the amounts are nil in both years. The items must be shown under the headings and subheadings specified by the formats. Items to which Arabic numbers are assigned may be combined on the face of the financial statements if they are either not material or the combination facilitates assessment (providing, in the latter case, the individual items are disclosed in the notes). With balance sheet format 1, the total can be presented at the Total Assets less Current Liabilities level or anywhere thereafter.

Author’s note

Format 1 of 1 Sch as amended by 6 Sch is illustrated opposite.

1 Sch 4(1)

The arrangement and headings of items denoted by an Arabic number in the formats should be adapted to suit any special nature of a company’s business.

1 Sch 3

Greater detail can be given in the financial statements than that prescribed by the formats. New items may be inserted for assets or liabilities not otherwise covered.

1 Sch 2

The format chosen may not be changed from year to year unless, in the directors’ opinion, there are special reasons for a change. Particulars of any change must be disclosed and the reasons for the change must be explained in a note to the financial statements.

IAS 1.53A, FRS 101 AG1(h)

A qualifying entity shall comply with the balance sheet format requirements of the Act* instead of paragraphs 54 to 76 of IAS 1 Presentation of Financial Statements, unless the entity elects to apply those paragraphs and the resulting statement of financial position

complies with the balance sheet format requirements of the Act.

*An entity shall apply, as required by company law, either Part 1 “General Rules and Formats” of Schedule 1 to the Regulations; Part 1 “General Rules and Formats” of Schedule 2 to the Regulations; Part 1 “General Rules and Formats” to Schedule 3 of the Regulations; or Part 1 “General Rules and Formats” of Schedule 1 to the LLP Regulations.

FRS 101 A2.3

Accounts prepared in accordance with EU-adopted IFRS are “IAS accounts” , and are within the scope of EU Regulation 1606/2002 (IAS Regulation). Where a qualifying entity prepares accounts in accordance with FRS 101, it prepares Companies Act accounts as referred to in section 395 of the Act. Those accounts must comply with the applicable provisions of Parts 15 and 16 of the Act and with the Regulations.

IAS 1.54

As a minimum, the statement of financial position shall include line items that present the following amounts:

property, plant and

equipment;

investment property;

intangible assets;

financial assets (excluding investments accounted for using the equity method, trade and other receivables and cash and cash equivalents);

investments accounted for

using the equity method;

biological assets;

inventories;

trade and other

receivables;

cash and cash equivalents;

the total of assets classified as held for sale and assets included in disposal groups classified as held for sale in accordance with IFRS 5 Non-current Assets Held

for Sale and Discontinued Operations;

trade and other payables;

provisions;

financial liabilities (excluding trade and other payables and provisions);

liabilities and assets for current tax, as defined in IAS 12 Income Taxes;

deferred tax liabilities and deferred tax assets as defined in IAS 12;

liabilities included in disposal groups classified as held for sale in accordance with IFRS 5.

Non-controlling interests, presented within equity; and

issued capital and reserves attributable to owners of the parent.

IAS 1.55

Additional line items, headings and subtotals shall be presented in the statement of financial position when such presentation is relevant to an understanding of the entity’s financial position.

Current/non-current presentation

IAS 1.60

An entity shall present current and non-current assets, and current and non-current liabilities as separate classifications in its statement of financial position, except when a presentation based on liquidity provides information that is reliable and is more relevant. When that exception applies, all assets and liabilities shall be presented in order of their liquidity.

IFRS 1.6

An entity shall prepare and present an opening IFRS statement of financial position at the date of transition to IFRSs. This is the starting point for its accounting in accordance with IFRSs.

Listed UK Group PLC

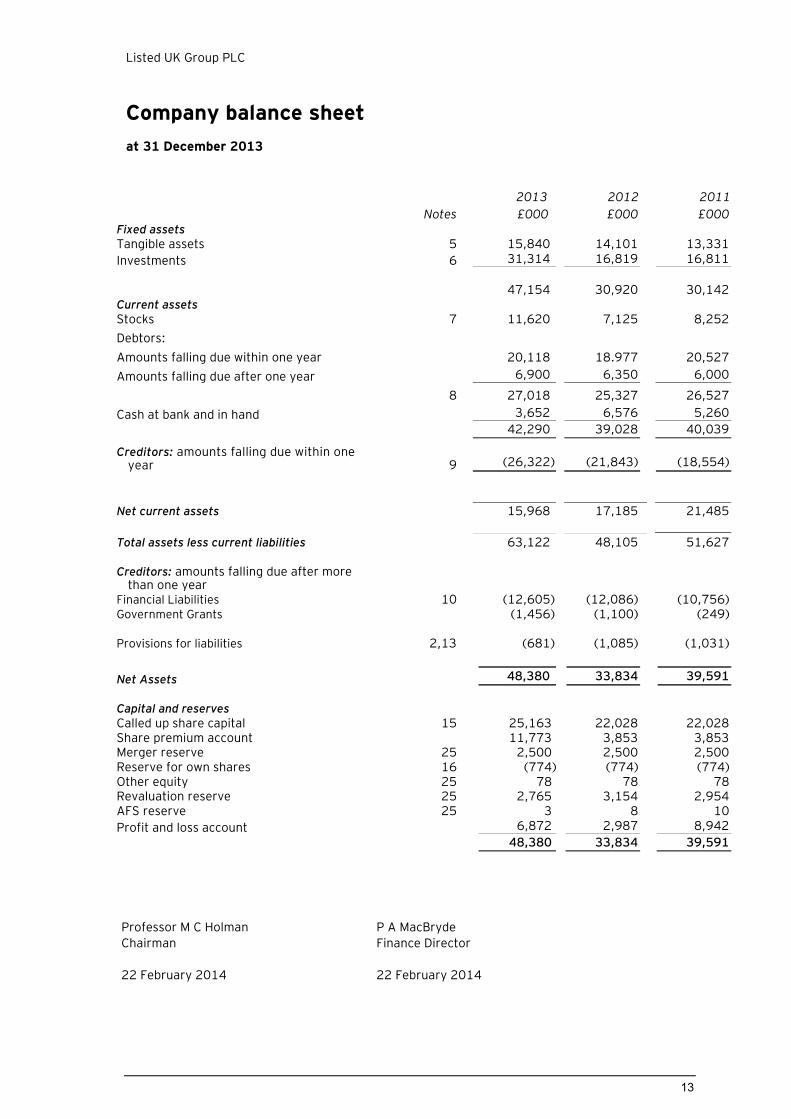

Company balance sheet

at 31 December 2013

13

2013 2012 2011

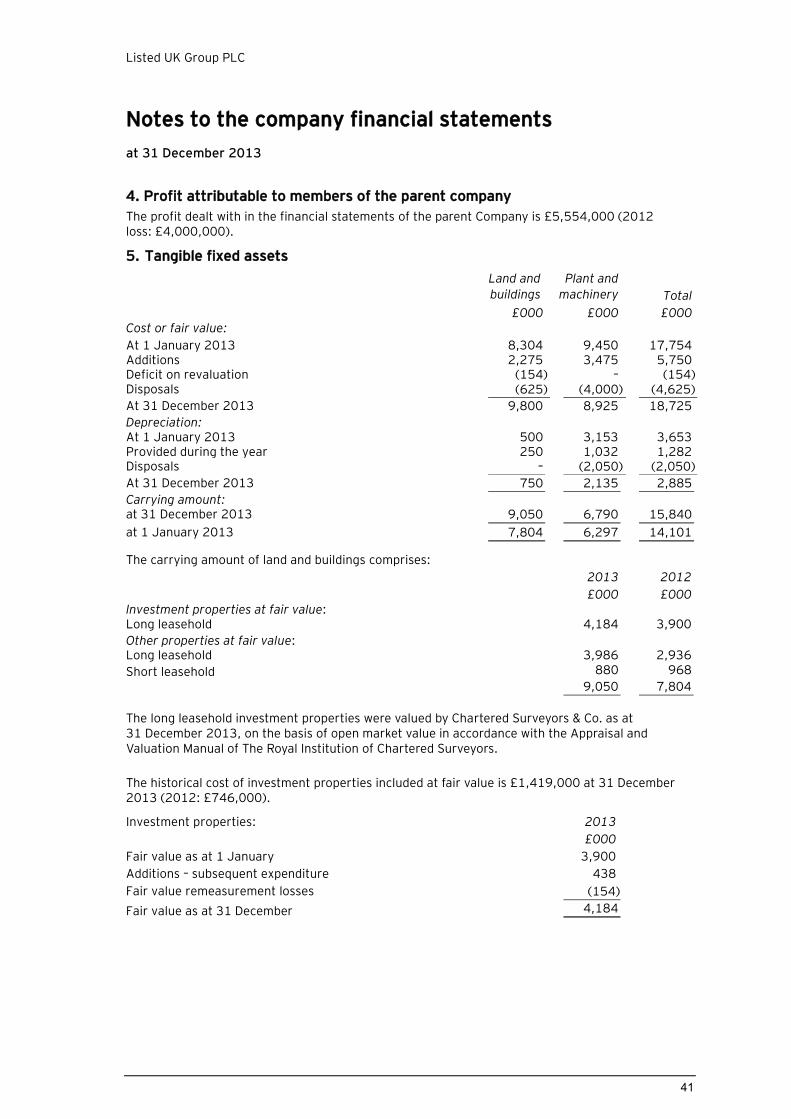

Notes £000 £000 £000 Fixed assets Tangible assets 5 15,840 14,101 13,331

Investments 6 31,314 16,819 16,811

47,154 30,920 30,142 Current assets Stocks 7 11,620 7,125 8,252

Debtors:

Amounts falling due within one year 20,118 18.977 20,527

Amounts falling due after one year 6,900 6,350 6,000

8 27,018 25,327 26,527

Cash at bank and in hand 3,652 6,576 5,260

42,290 39,028 40,039

Creditors: amounts falling due within one year 9 (26,322) (21,843)

(18,554)

Net current assets 15,968 17,185 21,485

Total assets less current liabilities 63,122 48,105 51,627

Creditors: amounts falling due after more than one year

Financial Liabilities 10 (12,605) (12,086) (10,756) Government Grants (1,456) (1,100) (249) Provisions for liabilities 2,13 (681) (1,085) (1,031)

Net Assets 48,380 33,834 39,591

Capital and reserves Called up share capital 15 25,163 22,028 22,028 Share premium account 11,773 3,853 3,853 Merger reserve 25 2,500 2,500 2,500 Reserve for own shares 16 (774) (774) (774) Other equity 25 78 78 78 Revaluation reserve 25 2,765 3,154 2,954 AFS reserve 25 3 8 10

Profit and loss account 6,872 2,987 8,942

48,380 33,834 39,591

Professor M C Holman P A MacBryde

Chairman Finance Director

22 February 2014 22 February 2014

Illustrative financial statements

Comments on the company balance sheet

14

Current/non-current presentation (continued)

IAS 1.61

Whichever method of presentation is adopted, an entity shall disclose the amount expected to be recovered or settled after more than twelve months for each asset and liability line item that combines amounts expected to be recovered or settled (a) no more than twelve months after the reporting period and (b) more than twelve months after the reporting period.

IAS 1.66 An entity shall classify an asset as current when: it expects to realise or

intends to sell or consume it in its normal operating cycle;

is held primarily for the purpose of trading;

it is expected to be realised within twelve months after the reporting period; or

it is cash or a cash equivalent unless it is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting period.

All other assets should be classified as non-current. IAS 1.69 A liability shall be classified as current when: it is expected to be settled in

the entity’s normal operating cycle;

it is held primarily for the purpose of trading;

it is due to be settled within twelve months after the reporting period; or

the entity does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting period.

All other liabilities should be classified as non-current.

IAS 1.72 An entity classifies its financial liabilities as current when they are due to be settled within twelve months after the reporting period, even if:

the original term was for a period longer than twelve months; and

an agreement to refinance, or to reschedule payments, on a long-term basis is completed after the reporting period and before the financial statements are authorised for issue.

IAS 1.77

An entity shall disclose, either in the statement of financial position or in the notes, further sub classifications of the line items presented, classified in a manner appropriate to the entity’s operations.

FRS 101.A2.10

In most cases it will be satisfactory to disclose the size of the debtors due after more than one year in the notes to the accounts. There will be some instances, however, where the amount is so material in the context of the total net current assets that in the absence of disclosure of the debtors due after more than one year on the face of the balance sheet readers may misinterpret the accounts. In such circumstances, the amount should be disclosed on the face of the balance sheet within current assets.

Offset

IAS 1.32

Assets and liabilities, and income and expenses, shall not be offset unless required or permitted by a Standard or an Interpretation.

Author’s note

As per IAS 1.53A a Company should only apply paragraphs 54 to 76 of IAS 1 if it does not conflict with the Act. Listed UK Group plc has elected not to apply these paragraphs.

Fixed assets

1 Sch 17-20

Fixed assets should be stated at purchase price or production cost, subject to provisions for depreciation or impairment in value, unless they are carried at valuation.

Current assets

1 Sch 23, 24

Current assets are to be valued at the lower of purchase price or

production cost and net realisable value.

Capital and Reserves

s610(1)

If a company issues shares at a premium, whether for cash or otherwise, a sum equal to the aggregate amount or value of the premiums on those shares shall be transferred to an account called “the share premium account”.

s612

Where the issuing company has secured at least a 90% equity holding in another company in pursuance of an arrangement providing for the allotment of equity shares in the issuing company on terms that the consideration for shares allotted is to be provided:

by the issue or transfer to the issuing company of equity shares in the other company; or

by the cancellation of any such shares not held by the issuing company

Signature and date

s414, s445(3), s446(3), s433

The parent company balance sheet published with the Group financial statements must be signed by a director of the company. Only one director need sign the balance sheet on behalf of the board. The copy of the balance sheet delivered to the Registrar of the Companies must be signed.

Every copy of the balance sheet which is laid before the company in general meeting, or which is otherwise circulated, published or issued, shall state the name of the person who signed the balance sheet on behalf of the board.

IAS 10.17

An entity shall disclose the date when the financial statements were authorised for issue and who gave that authorisation. If the entity’s owners or others have the power to amend the financial statements after issue, the entity shall disclose that fact.

Listed UK Group PLC

15

Illustrative financial statements

Comments on the balance sheet and statement of

changes in equity

16

Assets and liabilities in disposal groups held for sale

IFRS 5.38, 5.39

An entity shall present a non-current asset classified as held for sale and the assets of a disposal group classified as held for sale separately from other assets in the statement of financial position. The liabilities of a disposal group classified as held for sale shall be presented separately from other liabilities in the statement of financial position. Those assets and liabilities shall not be offset and presented as a single amount. Except in the case of a newly acquired subsidiary classified as held for sale on acquisition, the major classes of assets and liabilities classified as held for sale shall be separately disclosed either on the face of the statement of financial position or in the notes. An entity shall present separately any cumulative income or expense recognised directly in other comprehensive income relating to a non-current asset (or disposal group) classified as held for sale.

IFRS 5.40

An entity shall not reclassify or re-present amounts presented for non-current assets or for the assets and liabilities of disposal groups classified as held for sale in the statements of financial position for prior periods to reflect the classification in the statement of financial position for the latest period presented.

Author’s note

A one-line presentation of assets and liabilities held for sale on the balance sheet is not permitted by the Regulations. As a practical solution, this can be presented aggregate assets and aggregate liabilities held for sale as a memorandum cross referenced to the detailed analysis in the notes.

Statement of changes in equity

IAS 1.106

An entity shall present a statement of changes in equity showing in the statement:

total comprehensive income for the period, showing separately the total amounts attributable to owners of the parent and to non-controlling interests;

for each component of equity, the effects of changes in accounting policies and corrections of errors recognised in accordance with IAS 8;

for each component of equity, a reconciliation between the carrying amount at the beginning and the end of the period, separately disclosing changes resulting from:

- profit or loss;

- other comprehensive income: and

- transactions with owners in their capacity as owners, showing separately contributions by and distributions to owners and changes in ownership interests in subsidiaries that do not result in a loss of control.

IAS 1.106A

Disclose for each component of equity, either in the statement in changes of equity or in the notes, an analysis of other comprehensive income by item.

IAS 1.107

An entity shall present, either in the statement of changes in equity or in the notes, the amount of dividends recognised as distributions to owners during the period, and the related amount per share.

IAS 19.122

Remeasurements of net defined benefit liability (asset) recognised in other comprehensive income shall not be reclassified to profit or loss in a subsequent period. However, the entity may transfer those amounts recognised in other comprehensive income within equity.

Reserves

1 Sch 59

Disclose movements in all reserves and the opening and closing balances. Corresponding amounts are not required.

IAS 1.79(b)

An entity shall provide a description of the nature and purpose of each reserve within equity, either on the face of the balance sheet or in the notes.

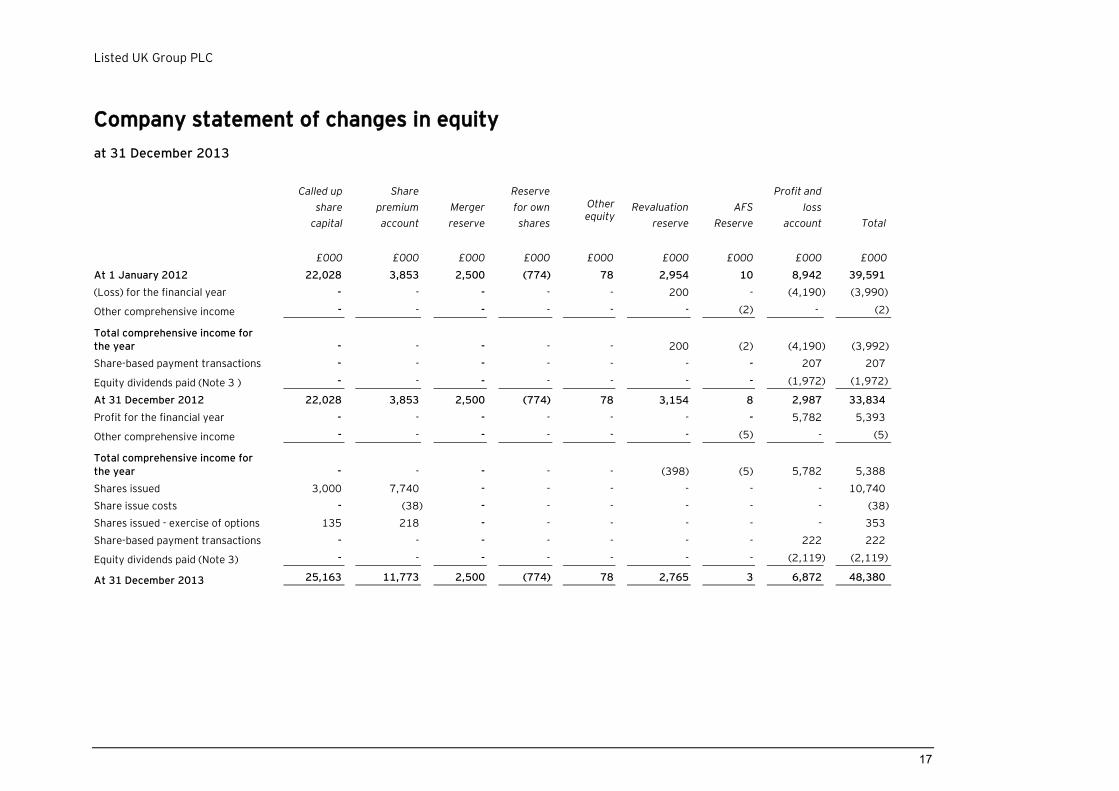

Listed UK Group PLC

Company statement of changes in equity

at 31 December 2013

17

Called up

share

capital

Share

premium

account

Merger

reserve

Reserve

for own

shares

Other equity

Revaluation

reserve

AFS

Reserve

Profit and

loss

account Total

£000 £000 £000 £000

£000

£000 £000 £000 £000

At 1 January 2012 22,028 3,853 2,500 (774) 78 2,954 10 8,942 39,591

(Loss) for the financial year - - - - - 200 - (4,190) (3,990)

Other comprehensive income - - - - - - (2) - (2)

Total comprehensive income for the year - - - -

-

200 (2) (4,190) (3,992)

Share-based payment transactions - - - - - - - 207 207

Equity dividends paid (Note 3 ) - - - - - - - (1,972) (1,972)

At 31 December 2012 22,028 3,853 2,500 (774) 78 3,154 8 2,987 33,834

Profit for the financial year - - - - - - - 5,782 5,393

Other comprehensive income - - - - - - (5) - (5)

Total comprehensive income for

the year - - - -

-

(398) (5) 5,782 5,388

Shares issued 3,000 7,740 - - - - - - 10,740

Share issue costs - (38) - - - - - - (38)

Shares issued - exercise of options 135 218 - - - - - - 353

Share-based payment transactions - - - - - - - 222 222

Equity dividends paid (Note 3) - - - - - - - (2,119) (2,119)

At 31 December 2013 25,163 11,773 2,500 (774) 78 2,765 3 6,872 48,380

Illustrative financial statements

Comments on notes to the company financial statements

18

Authorisation of financial statements and statement of compliance with FRS101

IAS 10.17

An entity shall disclose the date when the financial statements were authorised for issue and who gave that authorisation. If the entity’s owners or others have the power to amend the financial statements after issue, the entity shall disclose that fact.

IAS 1.138

An entity shall disclose the following if not disclosed elsewhere in information published with the financial statements:

the domicile and legal form of the entity, its country of incorporation and the address of the registered office (or principal place of business, if different from the registered office);

a description of the nature of the entity’s operations and its principal activities; and

the name of the parent and the ultimate parent of the group.

IAS 1.51(b), (c)

An entity shall display the following information prominently, and repeat it when necessary for the information presented to be understandable:

whether the financial statements cover the individual entity or a group of entities; and

the date of the end of the reporting period or the period covered by the financial statements or notes.

Statement of compliance

FRS101.10 Where a qualifying entity prepares its financial statements in accordance with FRS 101, it shall state in the notes to the financial statements: ‘‘These financial statements were prepared in accordance with Financial Reporting Standard 101 Reduced Disclosure Framework” The financial statements of such an entity do not comply with all of the requirements of EU-adopted IFRS and should not

therefore contain the unreserved statement of compliance set out in paragraph 3 of IFRS 1 First-time Adoption of International Financial Reporting Standards and paragraph 16 of IAS 1 Presentation of Financial Statements.

IAS 1.51(d)-(e)

An entity shall display the following information prominently, and repeat it when necessary for the information presented to be understandable:

the presentation currency, as

defined in IAS 21; and

the level of rounding used in

presenting amounts in the

financial statements.

Accounting policies – General

1 Sch 44

Disclose a description of each of the accounting policies that is material in the context of an entity’s financial statements. This must include the policies with respect to the depreciation and diminution in value of assets.

1 Sch 10-15

Disclose if any fundamental accounting concept (going concern, consistency, prudence and accruals) has not been observed, giving the nature of the departure, the reason and the effect. In the absence of such disclosure there is a presumption that the four fundamental concepts have been observed.

Basis of preparation

FRS 101.5(c)

A qualifying entity applying this FRS to its individual financial statements may take advantage of the disclosure exemptions in paragraphs 8 to 9, in accordance with paragraphs 6 to 7, provided that:

(c) It discloses in the notes to its financial statements

a brief narrative summary of the disclosure exemptions adopted; and

the name of the parent of the group whose consolidated financial statements its financial

statements are consolidated, and from where those financial statements may be obtained.

1 Sch 45

State whether the financial statements have been prepared in accordance with applicable accounting standards. The particulars of any material departure from those standards should be given along with the reason for it.

s408

The parent company’s profit and loss account, although required to be prepared and approved by the board of directors, need not be presented with the group financial statements. Where this exemption is taken, that fact must be disclosed. By virtue of s472(2), this exemption extends to omitting the related notes.

FRS 101.8 This paragraph provides details of disclosure exemptions available under the standard. The disclosure exemptions taken by this entity are listed opposite. See FRS 101 for a full list of disclosure exemptions that are available.

FRS 101.9 Reference should be made to the Application guidance to FRS 100 in deciding whether the consolidated financial statements of the group provide disclosures which are equivalent to the requirements of EU-adopted IFRS, from which relief in paragraph 8 of FRS 101.

IAS 1.112

The notes shall:

present information about the basis of preparation of the financial statements and the specific accounting policies used in accordance with paragraphs 117-124;

disclose the information required by IFRSs that is not presented elsewhere in the financial statements; and

provide information that is not presented elsewhere in the financial statements, but is relevant to an understanding of any of them.

Listed UK Group PLC

Notes to the company financial statements

at 31 December 2013

19

Authorisation of financial statements and statement of compliance with FRS 101

The parent company financial statements of Listed UK Group PLC (the “Company”) for the year ended 31 December 2013 were authorised for issue by the board of directors on 22 February 2014 and the balance sheet was signed on the board’s behalf by Professor M C Holman and P A MacBryde. Listed UK Group PLC is a public limited company incorporated and domiciled in England and Wales. The Company’s ordinary shares are traded on the London Stock Exchange.

These financial statements were prepared in accordance with Financial Reporting Standard 101 Reduced Disclosure Framework (FRS 101). The financial statements are prepared under the historical cost convention modified to include the revaluation of investment properties.

No profit and loss account is presented by the Company as permitted by Section 408 of the Companies Act 2006.

The results of Listed UK Group PLC are included in the consolidated financial statements of Listed UK Group PLC which are available from Homefire House, Ashdown Square, London EC2A 3XS.

The accounting policies which follow set out those policies which apply in preparing the financial statements for the year ended 31 December 2013. The financial statements are prepared in Sterling and are rounded to the nearest thousand pounds (£000).

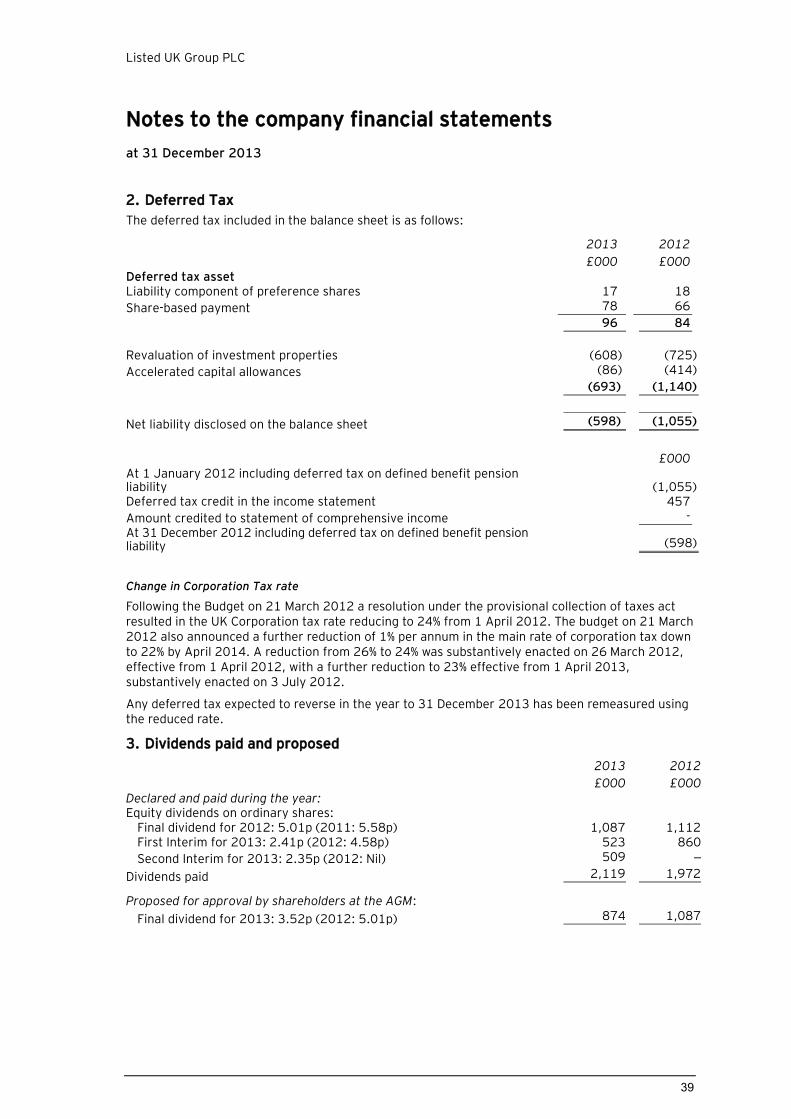

1. Accounting policies

Basis of preparation The Company has transitioned to FRS 101 from previously extant UK Generally Accepted Accounting Practice for all periods presented. The Company has adopted FRS 101 early which

is permitted under the Standard. Transition tables showing all material adjustments are disclosed in note 26. The accounting policies which follow set out those policies which apply in preparing the financial statements for the year ended 31 December 2013.

The Company has taken advantage of the following disclosure exemptions under FRS 101:

(a) the requirements of paragraphs 45(b)

and 46-52 of IFRS 2 Share based Payment: [for an ultimate parent, the share based payment arrangement must concern its own equity instruments and its separate financial statements must be consolidated financial statements of the group; And in both cases, this exemption requires that equivalent disclosures are included in the consolidated financial statements of the group in which the entity is consolidated. ] (b) The requirements of paragraphs 62, B64(d), B64(e), B64(g), B64(h), B64(j) to B64(m), B64(n)(ii), B64 (o)(ii), B64(p), B64(q)(ii), B66 and B67of IFRS 3 Business Combinations [this exemption requires that equivalent disclosures are included in the consolidated financial statements of the group in which the entity is consolidated.] (d) the requirements of IFRS 7 Financial Instruments: Disclosures, [this exemption requires that equivalent disclosures are included in the consolidated financial statements of the group in which the entity is consolidated. ] (e) the requirements of paragraphs 91-99 of IFRS 13 Fair Value Measurement,[ this exemption requires that equivalent disclosures are included in the financial statements of the group in which the entity is consolidated.]

Illustrative financial statements

Comments on the notes to the company financial statements

20

Basis of preparation (continued)

IAS 1.113

An entity shall, as far as practicable, present notes in a systematic manner. An entity shall cross-reference each item in the statements of financial position and of comprehensive income, in the separate income statement (if presented), and in the statements of changes in equity and of cash flows to any related information in the notes.

IAS 1.117

An entity shall disclose in the summary of significant accounting policies:

the measurement basis (or bases) used in preparing the financial statements; and

the other accounting policies used that are relevant to an understanding of the financial statements.

IAS 1.119

In deciding whether a particular accounting policy should be disclosed, management considers whether disclosure would assist users in understanding how transactions, other events and conditions are reflected in the reported financial performance and financial position. Disclosure of particular accounting policies is especially useful to users when those policies are selected from alternatives allowed in IFRS. Some Standards specifically require disclosure of particular accounting policies, including choices made by management between different policies they allow.

IAS 1.121

An accounting policy may be significant because of the nature of the entity’s operations even if amounts shown for current and prior periods are not material. It is also appropriate to disclose each significant accounting policy that is not specifically required by IFRSs, but selected and applied in accordance with IAS 8.

Change in accounting policy

IAS 8.28

When initial application of an IFRS has an effect on the current period

or any prior period, would have such an effect except that it is impracticable to determine the amount of the adjustment, or might have an effect on future periods, an entity shall disclose:

the title of the IFRS;

when applicable, that the change in accounting policy is made in accordance with its transitional provisions;

the nature of the change in accounting policy;

when applicable, a description of the transitional provisions;

when applicable, the transitional provisions that might have an effect on future periods;

for the current period and each prior period presented, to the extent practicable, the amount of the adjustment:

– for each financial statement line item affected; and

– if IAS 33 applies to the entity, for basic and diluted earnings per share;

the amount of the adjustment relating to periods before those presented, to the extent practicable; and

if retrospective application required by paragraph 19(a) or (b) is impracticable for a particular prior period, or for periods before those presented, the circumstances that led to the existence of that condition and a description of how and from when the change in accounting policy has been applied.

Financial statements of subsequent periods need not repeat these disclosures.

IAS 8.29

When a voluntary change in accounting policy has an effect on the current period or any prior period, would have an effect on that period except that it is impracticable to determine the amount of the adjustment, or might have an effect on future periods, an entity shall disclose:

the nature of the change in accounting policy;

the reasons why applying the new accounting policy provides reliable and more relevant information;

for the current period and each prior period presented, to the extent practicable, the amount of the adjustment:

– for each financial statement line item affected; and – if IAS 33 applies to the entity, for basic and diluted earnings per share;

the amount of the adjustment relating to periods before those presented, to the extent practicable; and

if retrospective application is impracticable for a particular prior period, or for periods before those presented, the circumstances that led to the existence of that condition and a description of how and from when the change in accounting policy has been applied.

Financial statements of subsequent periods need not repeat these disclosures.

Author’s note

In some cases, a description has been provided of changes to reporting standards effective in 2013 despite the fact that they are not relevant to the activities of Entity UK Limited and consequently have no financial effect. These illustrative disclosures have been provided to assist users of this publication who might need to implement these new or revised requirements. If in reality an entity concludes that a new requirement is not relevant to its activities, there is no benefit in making such detailed disclosure.

Author’s note

All mandatory new accounting standards have been adopted as part of the transition to FRS 101.

Listed UK Group PLC

Notes to the company financial statements

at 31 December 2013

21

1. Accounting policies (continued)

Basis of preparation (continued)

(f) the requirement in paragraph 38 of IAS 1 ‘Presentation of Financial Statements’ to present comparative information in respect of:

(i) paragraph 79(a)(iv) of IAS 1; (ii) paragraph 73(e) of IAS 16 Property, Plant and Equipment; (iii) paragraph 118(e) of IAS 38 Intangible Assets; (iv) paragraphs 76 and 79(d) of IAS 40 Investment Property; and (v) paragraph 50 of IAS 41 Agriculture.

(g) the requirements of paragraphs 10(d), 10(f), 39(c) and 134-136 of IAS 1 Presentation of Financial Statements; (h) the requirements of IAS 7 Statement of Cash Flows; (i) the requirements of paragraphs 30 and 31 of IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors; (j) the requirements of paragraph 17 of IAS 24 Related Party Disclosures; (l) the requirements in IAS 24 Related Party Disclosures to disclose related party transactions entered into between two or more members of a group, provided that any subsidiary which is a party to the transaction is wholly owned by such a member; and (m) the requirements of paragraphs 134(d)-134(f) and 135(c)-135(e) of IAS 36 Impairment of Assets, [this exemption requires that equivalent disclosures are included in the consolidated financial statements of the group in which the entity is consolidated.]

Illustrative financial statements

Comments on the notes to the company financial statements

22

Disclosure of significant judgements (apart from those involving estimation)

IAS 1.122

An entity shall disclose, in the summary of significant accounting policies or other notes, the judgements, apart from those involving estimations, that management has made in the process of applying the entity’s accounting policies and that have the most significant effect on the amounts recognised in the financial statements.

IAS 1.123

Examples of the judgments (apart from those involving estimations) that management makes and that can significantly affect the amounts recognised in the financial statements include:

whether financial assets are held-to-maturity investments;

whether substantially all the significant risks and rewards of ownership of financial assets and lease assets are transferred to other entities;

whether, in substance, particular sales of goods are financing arrangements and therefore do not give rise to revenue; and

whether the substance of the relationship between the entity and a special purpose entity indicates that the entity controls the special purpose entity.

Author’s note

Entities often combine disclosure of accounting judgements and sources of estimation uncertainty. Whilst this is not prohibited, preparers should acknowledge the very different disclosure requirements.

IAS 1.122 asks entities to describe judgements having a material effect on amounts recognised in the financial statements. This relates therefore to judgements as to whether an asset or liability exists; whether an asset of liability is derecognised; or whether an arrangement should be treated as an equity transaction. The disclosure requirement does not relate to judgements concerning the measurement of those items, which

is a matter for the disclosures about estimation uncertainty in IAS 1.125.

This does not mean that every accounting judgement should be disclosed. However, disclosure would be appropriate in cases where the accounting outcome is materially different dependent on the judgement taken. For example, when management has concluded that an entity is not a subsidiary despite holding more than 50% of the voting rights; when a significant sale and leaseback transaction has resulted in derecognition of the related asset; or when an internally developed intangible asset is determined to meet the criteria for recognition.

Disclosure of major sources of estimation uncertainty

IAS 1.125

An entity shall disclose in the notes information about the assumptions it makes about the future, and other major sources of estimation uncertainty at the end of the reporting period, that have a significant risk of resulting in a material adjustment to the carrying amounts of assets and liabilities within the next financial year. In respect of those assets and liabilities, the notes shall include details of:

their nature; and

their carrying amount as at the end of the reporting period.

IAS 1.129

An entity presents the disclosures in paragraph 125 in a manner that helps users of financial statements to understand the judgements that management makes about the future and about other sources of estimation uncertainty. The nature and extent of the information provided vary according to the nature of the assumption and other circumstances. Examples of the types of disclosures an entity makes are:

the nature of the assumption or other estimation uncertainty;

the sensitivity of carrying amounts to the methods, assumptions and estimates underlying their calculation, including the reasons for the sensitivity;

the expected resolution of an uncertainty and the range of reasonably possible outcomes within the next financial year in respect of the carrying amounts of the assets and liabilities affected; and

an explanation of changes made to past assumptions concerning those assets and liabilities, if the uncertainty remains unresolved.

IAS 1.130

IAS 1 does not require an entity to disclose budget information or forecasts in making the disclosures in paragraph 125.

Listed UK Group PLC

Notes to the company financial statements

at 31 December 2013

23

Judgements and key sources of estimation uncertainty

The preparation of financial statements requires management to make judgements, estimates and assumptions that affect the amounts reported for assets and liabilities as at the balance sheet date and the amounts reported for revenues and expenses during the year. However, the nature of estimation means that actual outcomes could differ from those estimates.

As noted opposite, IAS 1.122 requires disclosures of the significant judgements that affect the amounts recognised in the financial statements.

This does not mean that every accounting judgement should be disclosed. However, disclosure would be appropriate in cases where the accounting outcome is materially different dependent on the judgement taken.

The following estimates are dependent upon assumptions which could change in the next financial year and have a material effect on the carrying amounts of assets and liabilities recognised at the balance sheet date:

Revaluation of Land and buildings

The Company measures its land and buildings at fair value with changes in fair value being recognised through other comprehensive income. The Company engaged independent valuation specialists to determine fair value at 31 December 2013. The valuer used a valuation technique based on a discounted cash flow model due to a lack of observable market data because of the nature of the assets.

The fair value of the land and buildings equipment is most sensitive to the assumption concerning the discount rate.

Revaluation of investment properties

The Company measures its investment properties at fair value, with changes in fair values being recognised in profit and loss. The Company engaged independent valuation specialists to determine fair value as at 31 December 2013. The valuer used a valuation technique based on a discounted cash flow model due to a lack of observable market data because of the nature of the property.

The fair value of investment properties is most sensitive to the assumptions concerning discount rate and the long term vacancy rate.

Illustrative financial statements

Comments on the notes to the company financial statements

24

Investment properties

IAS 40.20

An investment property shall be measured initially at its cost. Transaction costs shall be included in the initial measurement.

IAS 40.30, IAS 40.34

Where a property interest is held by a lessee under an operating lease and is classified as an investment property, the fair value model shall be applied. In all other circumstances, an entity shall choose as its accounting policy either the fair value model or the cost model and shall apply that policy to all of its investment property.

IAS 40.66

An investment property shall be derecognised (eliminated from the balance sheet) on disposal or when the investment property is permanently withdrawn from use and no future economic benefits are expected from its disposal.

IAS 40.69

Gains or losses arising from the retirement or disposal of investment property shall be determined as the difference between the net disposal proceeds and the carrying amount of the asset and shall be recognised in profit or loss (unless IAS 17 requires otherwise on a sale and leaseback) in the period of the retirement or disposal.

Tangible fixed assets

1 Sch 18

The difference between the purchase price or production cost (or revalued amount) and estimated residual value of a fixed asset which has a limited useful economic life should be allocated on a systematic basis to each accounting period during the useful economic life of the asset. The depreciation charge for each period should be recognised as an expense in the profit and loss account unless it is permitted to be included in the carrying amount of another asset. For each major class of depreciable asset the method of depreciation and the useful economic lives (or depreciation rates) should be disclosed.

1 Sch 33, 3(1)

On revaluation of assets other than investment properties, the revalued amount less any residual value

should be depreciated over the remaining useful economic life. Depreciation charged prior to the revaluation should not be written back to the profit and loss account, except to the extent that it relates to a provision for diminution in value which is subsequently found to be unnecessary.

IAS 16.73(a)-(c)

The financial statements shall disclose, for each class of property, plant and equipment:

the measurement bases used for determining the gross carrying amount;

the depreciation methods used; and

the useful lives or the depreciation rates used.

IAS 23.8

An entity shall capitalise borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset as part of the cost of that asset. An entity shall recognise other borrowing costs as an expense in the period in which it incurs them.

IAS 16.29

An entity shall choose either the cost model or the revaluation model as its accounting policy and shall apply that policy to an entire class of property, plant and equipment.

IAS 16.67

The carrying amount of an item of property, plant and equipment shall be derecognised:

on disposal; or

when no future economic benefits are expected from its use or disposal.

IAS 16.68

The gain or loss arising from the derecognition of an item of property, plant and equipment shall be included in profit or loss when the item is derecognised. Gains shall not be classified as revenue.

Impairment of assets

IAS 36.9

An entity shall assess at each reporting date whether there is any indication that an asset may be impaired. If any such indication exists, the entity shall estimate the recoverable amount of the asset.

IAS 36.18

This Standard defines recoverable amount as the higher of an asset’s or cash generating unit’s fair value less costs to sell and its value in use.

IAS 36.119

A reversal of an impairment loss for an asset other than goodwill shall be recognised immediately in profit or loss, unless the asset is carried at revalued amount in accordance with another IFRS (for example, the revaluation model in IAS 16). Any reversal of an impairment loss of a revalued asset shall be treated as a revaluation increase in accordance with that other IFRS.

FRS 101.AG1(s)

Paragraph 124 of IAS 36 Impairment of Assets is amended as follows:

An impairment loss recognised for goodwill shall not be reversed in a subsequent period, if and only if, the reasons for the impairment loss have ceased to apply.

Intangible assets

FRS 101.A2.8

A qualifying entity preparing accounts in accordance with FRS 101 may have recognised goodwill which, in accordance with IFRS 3 Business Combinations, is not amortised. The non-amortisation of goodwill conflicts with paragraph 22 of Schedule 1 to the Regulations, which requires acquired goodwill to be reduced by provisions for depreciation calculated to write off the amount systematically over a period chosen by the directors, not exceeding its useful economic life. As such the non-amortisation of goodwill will usually be a departure, for the overriding purpose of giving a true and fair view, from the requirement of paragraph 22 of Schedule 1 to the Regulations. In this circumstance there will need to be given in the notes to the accounts ‘particulars of the departure, the reasons for it and its effect (paragraph 10(2) of Schedule 1 to the Regulations). This is not a new instance of the use of the ‘true and fair override’ as paragraph 18 of FRS 10 Goodwill and intangible assets noted that it would have been required by companies applying paragraph 17 of FRS 10 which states ‘where goodwill and intangible assets are regarded as having indefinite useful lives, they should not be amortised.

Listed UK Group PLC

Notes to the company financial statements

at 31 December 2013

25

1. Accounting policies (continued)

Investment properties

Investment properties are measured initially at cost, including transaction costs. Subsequent to initial recognition, investment properties are stated at fair value. Gains or losses arising from changes in the fair values of investment properties are included in profit or loss in the period in which they arise.

Investment properties are derecognised when either they have been disposed of or when the investment property is permanently withdrawn from use and no future economic benefit is expected from its disposal. Any gains or losses on the retirement or disposal of investment property, is recognised in the income statement in the period of derecognition.

Transfers are made to or from investment property only when there is a change in use. For a transfer from investment property to owner occupied property, the deemed cost for subsequent accounting is the fair value at the date of change in use. If owner occupied property becomes an investment property, the Group accounts for such property in accordance with the policy stated under property, plant and equipment up to the date of change in use.

Tangible fixed assets

Plant and equipment is stated at cost less accumulated depreciation and accumulated impairment losses. Cost comprises the aggregate amount paid and the fair value of any other consideration given to acquire the asset and includes costs directly attributable to making the asset capable of operating as intended. Borrowing costs directly attributable to assets under construction and which meet the recognition criteria in IAS 23 are capitalised as part of the cost of that asset.

Land and buildings are recognised initially at cost and thereafter carried at fair value less depreciation and impairment charged subsequent to the date of the revaluation. Fair value is based on periodic valuations by an external independent valuer and is determined from market-based evidence by appraisal. Valuations are performed frequently enough to ensure that the fair value of a revalued asset does not differ materially from its carrying

amount. Fair value gains and losses are recognised in other comprehensive income.

Any revaluation surplus is credited to the revaluation reserve in equity except to the extent that it reverses a decrease in the carrying value of the same asset previously recognised in profit or loss, in which case the increase is recognised in profit or loss. A revaluation deficit is recognised in profit or loss, except to the extent of any existing surplus in respect of that asset in the revaluation reserve.

An annual transfer is made from the revaluation reserve to retained earnings for the difference between depreciation based on the carrying amount of the assets and that based on the assets’ original cost. Additionally, accumulated depreciation as at the revaluation date is eliminated against the gross carrying amount of the asset and the net amount is restated to the revalued amount of the asset. Upon disposal any revaluation reserve relating to the particular asset being sold is transferred to retained earnings.

Depreciation is provided on all property, plant and equipment, other than land, on a straight-line basis over its expected useful life as follows:

Buildings – over 20 to 50 years

Plant and equipment

– over 5 to 15 years

The carrying values of property, plant and equipment are reviewed for impairment if events or changes in circumstances indicate the carrying value may not be recoverable, and are written down immediately to their recoverable amount. Useful lives and residual values are reviewed annually and where adjustments are required these are made prospectively.