Embed Size (px)

Citation preview

MANAGEMENT SCIENCEArticles in Advance, pp. 1–24

http://pubsonline.informs.org/journal/mnsc/ ISSN 0025-1909 (print), ISSN 1526-5501 (online)

InformedQ: 1 Options, 2 Trading Prior to Takeover Announcements:Insider Trading?

Q: 3 Patrick Augustin,a Menachem Brenner,b Marti G. Subrahmanyamb

aDesautels Faculty of Management, McGill University, Montreal, Quebec H3A 1G5, Canada; bLeonard N. Stern School of Business,New York University, New York, New York 10012Contact: [email protected], http://orcid.org/0000-0001-9138-4860 (PA); [email protected] (MB);[email protected] (MGS)

Received: December 3, 2015Revised: August 26, 2016; December 15, 2017Accepted: April 8, 2018Published Online in Articles in Advance:∎∎ ∎∎, 2018

https://doi.org/10.1287/mnsc.2018.3122

Copyright: © 2018 INFORMS

Abstract. We quantify the pervasiveness of informed trading activity in target companies’equity options before the announcements of 1,859 U.S. takeovers between 1996 and 2012.About 25% of all takeovers have positive abnormal volumes, which are greater for short-dated, out-of-the-money calls, consistent with bullish directional trading before the an-nouncement. Over half of this abnormal activity is unlikely due to speculation, news andrumors, trading by corporate insiders, leakage in the stock market, deal predictability, orbeneficial ownership filings by activist investors. We also examine the characteristics ofoption trades litigated by the Securities and Exchange Commission (SEC) for alleged illegalinsider trading. Although the characteristics of such trades closely resemble the patterns ofabnormal option volume in the U.S. takeover sample, we find that the SEC litigates onlyabout 8% of all deals in it.

History: Accepted by Lauren Cohen, finance.Funding: ThisQ: 4 project was supported by the Social Sciences & Humanities Research Council of Canada[SSHRC 430-2014-00747] and the ChicagoMercantile Exchange. P. Augustin acknowledges financialsupport from the Institute of Financial Mathematics of Montreal.

Supplemental Material: The online appendix is available at https://doi.org/10.1287/mnsc.2018.3122.

Keywords: civilQ: 5

litigations • derivatives • insider trading • mergers and acquisitions

1.Q: 6 IntroductionHowQ: 7 pervasive is informed options trading aroundtakeover announcements? Cao et al. (2005), for ex-ample, suggest that abnormal trading in equity op-tions prior to takeover announcements is informed, asdirectional trading activity positively foreshadowsfuture price movements.1 This finding raises questionsabout the nature of the run-up in option volumesbefore takeover announcements and the distributionof informed trading across deals. Is the run-up drivenby a few deals with significant volumes, or do all dealscontribute to the options activity that is abnormal onaverage? What information drives the individual run-ups in option volumes, and can they be explained bypublicly available sources of information besides il-legal insider trading? In this paper, we characterizethe pervasiveness of informed options trading aroundtakeover announcements and study the sources ofthe preannouncement run-up in option volumes.

We first quantify the pervasiveness of informedtrading in the equity options of target companies aheadof 1,859 U.S. takeover transactions between January1996 and December 2012. To better understand thesources of informed trading, in the second step, weexamine a large number of channels that could

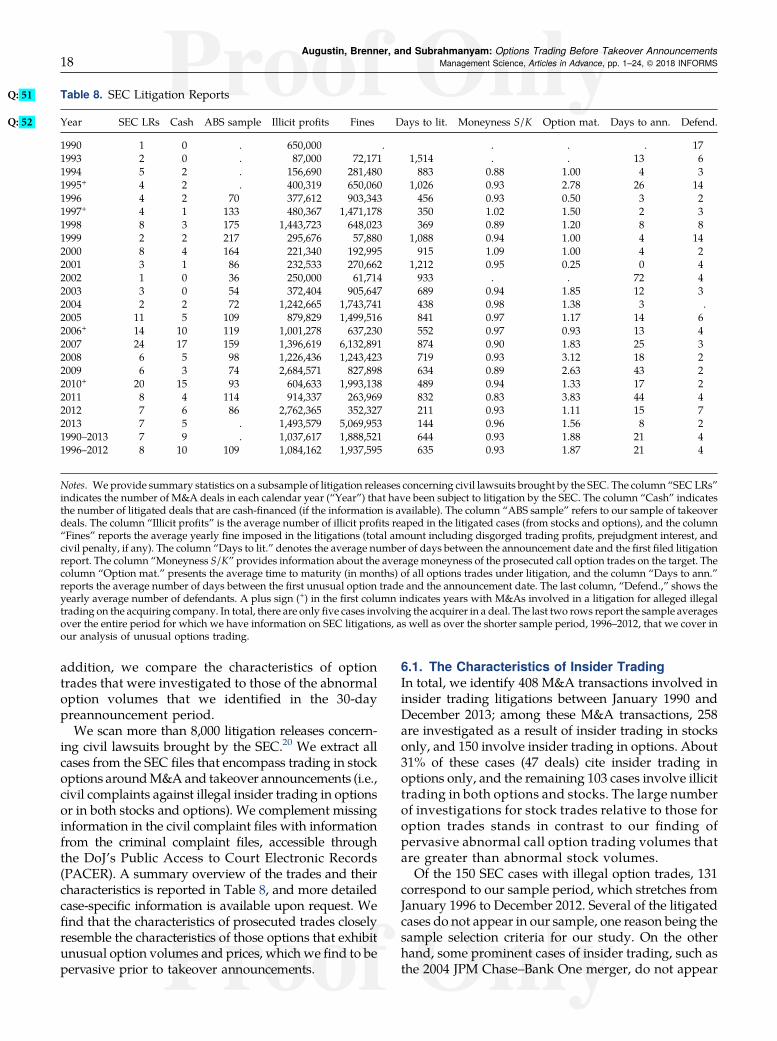

plausibly explain the abnormal trading volumes inoptions based on correct anticipation of upcomingtakeover activity. It is the deal-by-deal examination ofthe preannouncement activity that allows us to ex-amine the overlaps in explanations across deals andto identify the deals with abnormal options activitythat are unlikely to be anticipated. Third, we alsoverify whether the run-up may be the result of illegalinsider trades reported by the Securities and Ex-change Commission (SEC), and we compare thecharacteristics of all option trades litigated for allegedillegal insider trading with those of the preannouncementoptions activity. This comparison strengthens our as-sessment of the nature and sources of the preannounce-ment run-up in option volumes.We document that about 25% (467) of all deals in our

sample have abnormal volumes of equity options overthe 30-day period preceding the takeovers, which arestatistically significant at the 5% level. The proportion ofcases with abnormal volumes is relatively higher for calloptions than for put options. Stratifying the results by“moneyness,” we find that there is significantly higherabnormal trading volume in out-of-the-money (OTM)call options comparedwith at-the-money (ATM) and in-the-money (ITM) calls.2

1

An examination of the characteristics of cumulativeabnormal volume shows that informed trading is morepervasive for larger deals, those for which informedinvestors may potentially have less uncertainty aboutthe final takeover price, and in cases where target firmsreceive cash offers. We study the trading volume,implied volatility, and bid-ask spreads of equity op-tions, and we consider a number of robustness testsQ: 8 ,which support the evidence of informed investorstrading directionally in anticipation of a price jump inthe target company’s stock. It is the deal-by-deal ex-amination of the preannouncement activity that helpsus appreciate the pervasiveness of informed trading intakeover transactions.

We next explore whether the takeover announce-ments could have been anticipated based on publicsources of information.We first show that the run-up inoptions volume is unlikely due to speculative tradingactivity in response to observable stock trading ac-tivity or industry and firm characteristics. We com-pare the options activity in the takeover sample toseveral control samples that are matched either on thestock market activity or on industry and firm char-acteristics. Informed trading activity in options aheadof takeover announcements is absent from these con-trol groups.

In addition, we examine how much of the informedoptions activity can be explained by news and rumors.To identify rumors and news about upcoming take-overs, we use RavenPack News Analytics, a databasethat is constructed from textual information in majornewspaper outlets, public relations feeds, and morethan 19,000 other traditional and social media websites.We associate news with 170 takeover transactions andwith only 9% (40/467) of the deals that exhibit in-formed options activity. We find no statistically sig-nificant difference in the average cumulative abnormaloptions trading volumes between the sample of 170takeovers with news and the sample of 1,689 withoutnews. We further check whether the option tradesoriginate from corporate insider accounts. Corporateofficers, directors, or large block-holders are legallyrequired to disclose security transactions in theircompany’s options. An analysis of the derivativetransactions and holdings information in the ThomsonReuters insider filings reveals that not a single optionstransaction was executed by registered insiders in the30-day period before the announcement.

We also consider the possibility that astute optiontraders trade on information leakage in the stockmarket. However, our analysis suggests that optionvolume leads stock volume, and that past stock volumeand return performance is not significantly related tofuture abnormal options activity. In addition, we findthat only 7% of the deals in our sample exhibit ab-normal stock returns in the preannouncement period,

whereas about 44% of all deals exhibit excess impliedvolatility. Although 19% of the takeover transactionsexhibit statistically significant abnormal stock volume—a frequency somewhat lower than in the optionsmarket—the economic magnitude is substantiallysmaller. Thus, quantifying how many deals are subjectto informed trading may also be informative aboutwhether informed trading is more prevalent in theoptions or in the stock market.Next, we show that it is difficult to predict takeover

announcements based on publicly available informa-tion. Thus, the documented abnormal option tradingvolume is unlikely due to traders’ ability to time themarket. However, we observe that most of the in-formed activity arises in the 5–10 days before the in-formation gets publicly released. Finally, we screen theSchedule Q: 913D beneficial ownership reports, which needto be filed by registered active investment advisors nolater than 10 days following the acquisition of beneficialownership of more than 5% of any class of publiclytraded securities. The trading we identify by suppos-edly informed activist investors is unlikely to fullyexplain the abnormal options activity, as only 17 ofthese deals have a filing in the 30-day period prior tothe takeover announcement date.Of the 467 deals in our sample with significant cu-

mulative abnormal options volume, 13% (236) areunlikely to be associated with publicly availablesources of information. In the subsample of 236 deals,we exclude those deals that exhibit statistically sig-nificant stock volume or returns, which appear to lagthe option market in the takeover preannouncementperiod. An additional channel that may drive the run-up in options volume could be illegal insider trading.Therefore, we filter through more than 8,000 publicSEC litigation records dated between 1990 and 2013 toidentify whether the takeover transactions in oursample were subject to a litigation for alleged insidertrading. We find that the SEC litigated about 8% of thetakeovers in our sample for insider trading in optionsor stocks and only 9% (43/467) of the transactions thatwe associate with informed trading. Moreover, only10% (24/236) of the deals that we fail to associate withpublic sources of information are involved in a litiga-tion. Thus, the number of civil lawsuits for insidertrading appears modest in comparison with the per-vasive informed trading activity reflected in 25% of thetakeover transactions.Using the SEC’s litigation records, we hand-collect

information on the size, timing, and type of illegaltrades; we supplement with information in the criminalrecords from the U.S. Department of Justice (DoJ). The Q: 10

characteristics of the illegal option trades—that is,short-dated OTM call options on target companiesthat are initiated, on average, 21 days before theannouncement—closely resemble the characteristics

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover Announcements2 Management Science, Articles in Advance, pp. 1–24, © 2018 INFORMS

and timing of the abnormal options activity in a rep-resentative sample of takeover transactions. Thisresemblance, coupled with the absence of public informa-tion sources that could have led to the anticipation ofthe takeover transaction, calls for further regulatoryexamination of the informed options activity.

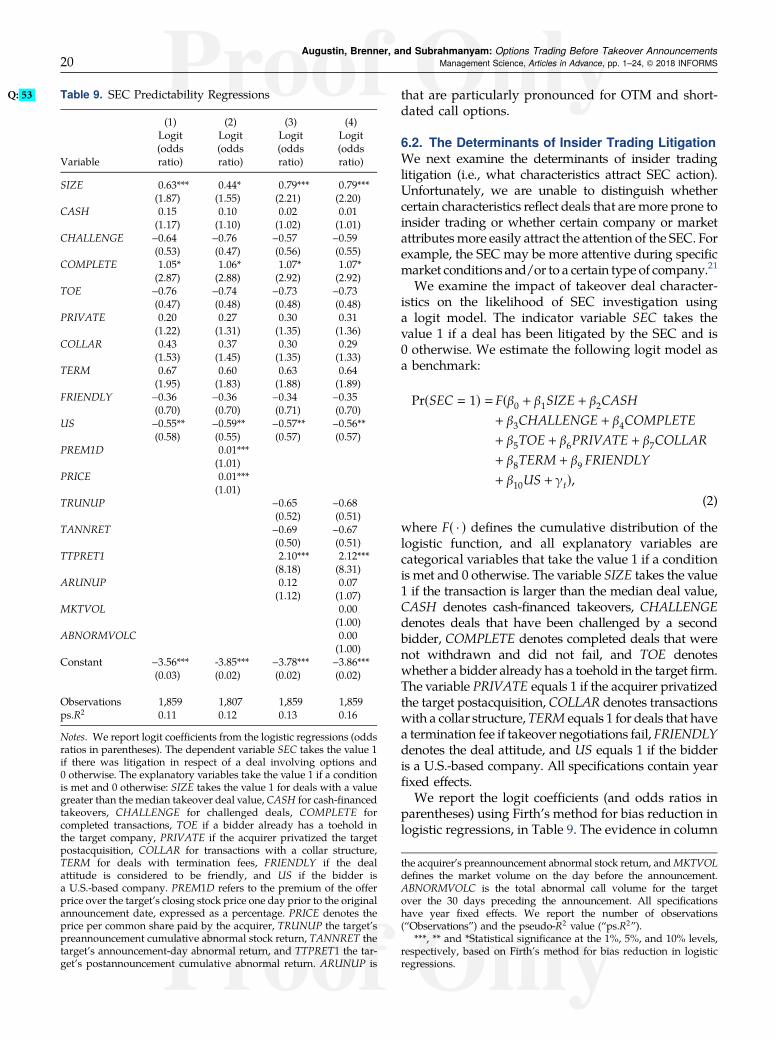

DeMarzo et al. (1998) suggest that it may be optimalto prosecute insiders only after large price moves orafter large volume transactions. We find that the SEC islikely to examine large target firms that experiencesubstantial abnormal returns after the takeover an-nouncement and in which the acquirers are head-quartered outside the United States. We find, however,no evidence that the probability of litigation is posi-tively related to the preannouncement abnormal op-tions volume.

We extend the literature along three key dimensions.FirstQ: 11 , in this paper, we quantify the prevalence of in-formed trading and document that the informed op-tions activity is driven by 25% of all deals, in contrast toprior research. Second, we diverge from previous workand examine the sources of informed trading in theoptions market and show that for at least 13% of alldeals, it is difficult to associate the abnormal optionsactivity with public sources of information. Third,a unique feature of our research is that we study thecharacteristics of SEC-litigated cases related to insidertrading in options prior to takeover announcements.This allows us to compare the nature of abnormaloptions activity to illegal option trades and examinehow the SEC’s litigation record relates to abnormaloptions trading around takeover announcements.

2. Literature ReviewThe run-up in the stock prices of target companiesbefore merger and acquisition (M&A) announcementsis well documented (Mandelker 1974, Dodd 1980,Asquith 1983, Jensen and Ruback 1983, Dennis andMcConnell 1986, Schwert 1996). A long-standing de-bate relates to whether this run-up is due to publicinformation such as, for example, media speculation(Jarrell and Poulsen 1989), or whether it is the result ofprivate information leakage and illegal insider trading(Keown and Pinkerton 1981, Meulbroek 1992, Sandersand Zdanowicz 1992).

Abnormal options volume and price activity aheadof M&A announcements have been the subject of manypapers, particularly in recent years. Jayaraman et al.(1991) are the first to document a preannouncementincrease in the option-implied volatilities of targetcompanies that precede an increase in stock returns, asconfirmed by Levy and Yoder (1993). Jayaraman et al.(2001) document that the abnormal options volume isaccompanied by abnormal open interest that is con-centrated in short-term OTM options, that it leadsabnormal stock volume, and that the increase in

abnormal options volume is greater for call than for putoptions. Using signed volume, Cao et al. (2005) supportthe presence of informed activity because prior totakeover announcements, the option volume orderimbalance contains information regarding subsequentstock price movements, greater call volume balancesare associated with greater announcement returns,and the options market displaces the stock market forinformation-based trading (see also Arnold et al.2006). Acharya and Johnson (2010) show that a largenumber of equity participants in leveraged buyoutsyndicates is associated with greater levels of suspi-cious stock and options activity. Clements and Singh(2011) argue that preannouncement options volumereflects both informed and “contraire” trading, andShafer (2012) documents a positive correlation be-tween the preannouncement option-to-stock volumeratio and the probability of being a takeover targetthat becomes weaker after Regulation Fair Disclosurein 2000.Many studies have corroborated the evidence of

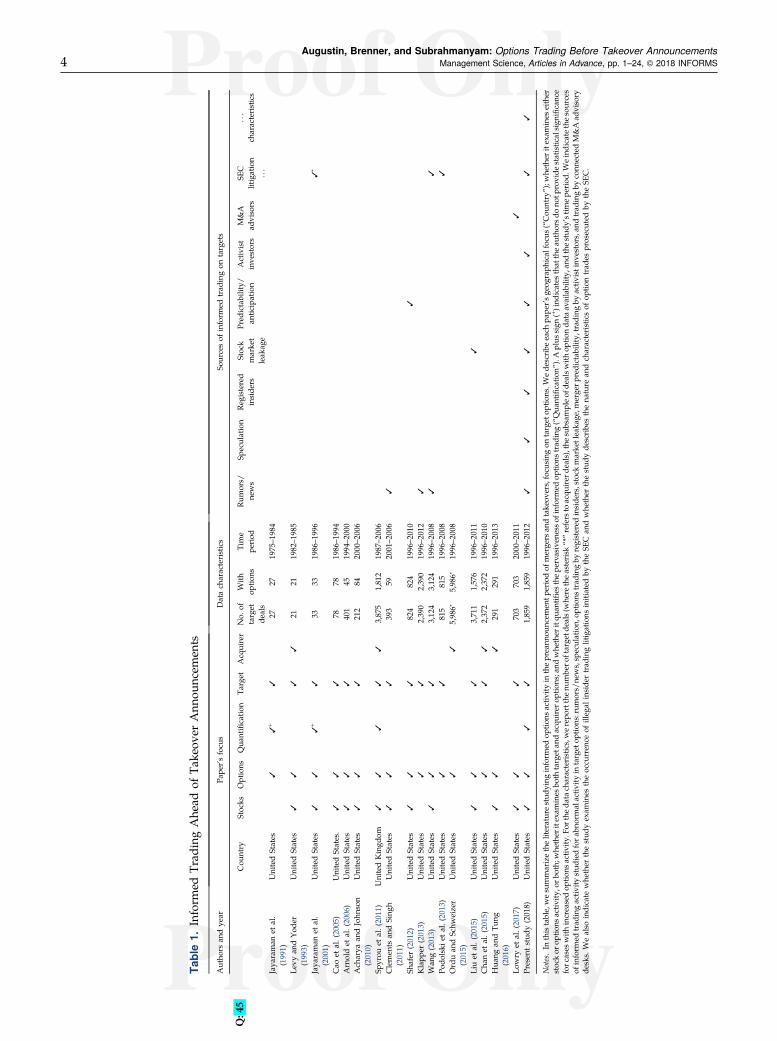

abnormal preannouncement option activity in targetcompanies in the United States and United Kingdom(Spyrou et al. 2011). The literature emphasizes differentaspects of the preannouncement activity, includingabnormal changes in the implied Q: 12volatility (IV) skew,IV spread, and the option-to-stock volume ratio(Klapper 2013); a positive correlation between pre-announcement run-up and abnormal options volume(Wang 2013); an increasing importance of options’leading role for price discovery (Liu et al. 2015); ora greater propensity of informed trading to occur inmore liquid and higher leverage options (Podolski et al.2013). Chan et al. (2015) show that the one-day pre-event implied volatility spread (the implied volatilityskew), a proxy for informed option trading, is posi-tively (negatively) associated with acquirer cumulativeabnormal returns. Ordu and Schweizer (2015) associ-ate greater abnormal volumes with greater chief Q: 13ex-ecutive officer wealth-to-performance sensitivity forstock-financed takeovers, suggesting that informed man-agers hedge anticipated negative acquirer announce-ment returns. Focusing also on acquirers, Huang andTung (2016) find a positive relation between an-nouncement returns and preannouncement option-to-stock volume ratios, which are positively related toidiosyncratic stock volatility. Chesney et al. (2015)propose a method for detecting abnormal options ac-tivity and relate six unusual transactions to M&Aannouncements. Kedia and Zhou (2014) conclude infavor of preannouncement informed trading in targetbonds. Poteshman (2006) concludes that informed in-vestors traded put options ahead of the 9/11 terroristattacks.In Table 1, we show the differences between this

study and prior work. Apart from Spyrou et al. (2011),

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover AnnouncementsManagement Science, Articles in Advance, pp. 1–24, © 2018 INFORMS 3

Tab

le1.

Inform

edTrad

ingAhe

adof

Take

over

Ann

ounc

emen

ts

Autho

rsan

dye

arPa

per’sfocu

sDatach

aracteristics

Sourcesof

inform

edtrad

ingon

targets

Cou

ntry

Stocks

Options

Qua

ntificatio

nTa

rget

Acquirer

No.

oftarget

deals

With

optio

nsTime

period

Rum

ors/

news

Speculation

Reg

istered

inside

rsStock

marke

tleak

age

Pred

ictability/

antic

ipation

Activist

inve

stors

M&A

advisors

Q:45

SEC

litigation

...

...

characteristics

Jaya

raman

etal.

(199

1)UnitedStates

33

+3

2727

1975–1

984

Levy

andYod

er(199

3)UnitedStates

33

33

2121

1982–1

985

Jaya

raman

etal.

(200

1)UnitedStates

33

3+

333

3319

86–1

996

3∗

Cao

etal.(20

05)

UnitedStates.

33

378

7819

86–1

994

Arnoldet

al.(20

06)

UnitedStates

33

340

145

1994–2

000

Ach

arya

andJohn

son

(201

0)UnitedStates

33

321

284

2000–2

006

Spyrou

etal.(20

11)

UnitedKingd

om3

33

33

3,87

51,81

219

87–2

006

Clemen

tsan

dSing

h(201

1)UnitedStates

33

339

359

2001–2

006

3

Shafer

(201

2)UnitedStates

33

382

482

419

96–2

010

3

Klapp

er(201

3)UnitedStates

33

2,39

02,39

019

96–2

012

3

Wan

g(201

3)UnitedStates

33

33,12

43,12

419

96–2

008

33

Podo

lski

etal.(20

13)

UnitedStates

33

815

815

1996–2

008

3

Orduan

dSchw

eizer

(201

5)UnitedStates

33

5,98

6∗5,98

6∗19

96–2

008

Liuet

al.(20

15)

UnitedStates

33

33,71

11,57

619

96–2

011

3

Cha

net

al.(20

15)

UnitedStates

33

32,37

22,37

219

96–2

010

Hua

ngan

dTu

ng(201

6)UnitedStates

33

329

129

119

96–2

013

Lowry

etal.(20

17)

UnitedStates

33

370

370

320

00–2

011

3

Presen

tstud

y(201

8)UnitedStates

33

33

1,85

91,85

919

96–2

012

33

33

33

33

Notes.In

thistable,wesu

mmarizetheliteraturestud

ying

inform

edop

tions

activ

ityin

thepreann

ounc

emen

tperiodof

merge

rsan

dtake

overs,focu

sing

ontarget

optio

ns.W

ede

scribe

each

pape

r’sge

ograph

ical

focu

s(“Cou

ntry”);w

hether

itexam

ines

either

stockor

optio

nsactiv

ity,o

rboth;

whe

ther

itexam

ines

both

target

andacqu

irer

optio

ns;and

whe

ther

itqu

antifi

esthepe

rvasiven

essof

inform

edop

tions

trad

ing(“Qua

ntificatio

n”).Aplus

sign

(+)ind

icates

that

theau

thorsdo

notp

rovide

statistic

alsign

ificanc

eforc

ases

with

increasedop

tions

activ

ity.F

ortheda

tach

aracteristics,werepo

rtthenu

mbe

roftarge

tdeals(w

here

theasterisk

“*”refers

toacqu

irer

deals),the

subsam

pleof

dealswith

optio

nda

taav

ailability,

andthestud

y’stim

epe

riod

.Weindicatethesources

ofinform

edtrad

ingactiv

itystud

iedfora

bnormal

activ

ityin

target

optio

ns:rum

ors/

news,sp

eculation,

optio

nstrad

ingby

registered

inside

rs,stock

marke

tleaka

ge,m

erge

rpredictab

ility,trading

byactiv

istinv

estors,and

trad

ingby

conn

ectedM&Aad

visory

desks.W

ealso

indicate

whe

ther

thestud

yexam

ines

theoccu

rren

ceof

illeg

alinside

rtrad

inglitigations

initiated

bytheSE

Can

dwhe

ther

thestud

yde

scribe

sthena

ture

andch

aracteristicsof

optio

ntrad

esprosecuted

bytheSE

C.

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover Announcements4 Management Science, Articles in Advance, pp. 1–24, © 2018 INFORMS

who examine UK data, most studies are not informa-tive about the distribution of informed options trading.For a small sample that is not representative of optiontrading over the last two decades, Jayaraman et al.(1991, 2001) identify positive changes in implied vol-atilities, without mentioning statistical significance. Bycontrast, we examine deals, case by case, and em-phasize how and where insiders trade in the optionsmarket: they engage in directional strategies for targets,which are reflected in more pronounced abnormalactivity in OTM calls and cash-financed takeovers. Inaddition, we consider synthetic option strategies thatlead to long bullish or short bearish exposures fortargets, and we review earlier evidence, as the findingsappear to be inconsistent across studies.3

Importantly, there is only scarce information on thesources of informed options trading for target firms.Klapper (2013) and Wang (2013) examine media spec-ulation and rumors, but their results are inconsistentwith each other.4 Liu et al. (2015) provide some evidenceagainst the leakage hypothesis but do not explainwhether abnormal options activity for a given dealmightbe the result of abnormal stock activity. Lowry et al.(2016) indicate that trading desks connected to M&Aadvisory desks take abnormal call option positions in thetarget companies from seven quarters to one quarterbefore the announcement. Ordu and Schweizer (2015)examine the sources of informed trading (managers) butfocus on the options of the acquirers. Our focus here is ondocumenting the abnormal options activity for the targetfirms and identifying the specific types of options tradedbefore the announcement.

Some authors examine the illegal insider trading in-vestigated by the SEC (Jayaraman et al. 2001, Podolskiet al. 2013) or study the predictability of SEC litigations(Wang 2013). Using a proprietary sample of illegal tradeslitigated by the SEC, Meulbroek (1992) and Meulbroekand Hart (1997) document that insider trades have animmediate effect on stock prices, that half of the pre-announcement run-up occurs on insider trading days,and that the announcement returns are a third largerwhen insider trading is detected. Frino et al. (2013) studyhand-collected SEC litigations and find that illegal stocktrades are positively associated with subsequent pricechanges but negatively associated with the size of thepenalties and the stock’s liquidity. However, we find noinformation in the literature on the characteristics andpatterns of option trades litigated for illegal insidertrading, nor on how prosecution relates to the degree ofabnormal options activity. In this paper, we relate ourresults to the literature associated with illegal insidertrading in stocks.

Cornell and Sirri (1992) and Chakravarty andMcConnell (1997, 1999) conduct clinical studies ofillegal stock trades ahead of the 1982 takeover ofCampbell Taggart by Anheuser-Busch and the 1984

takeover of Carnation by Nestlé. Both studies findpositive price impactsand either a positive or no effect onbid-ask spreads or depth. Fishe and Robe (2004) findthat trading by brokers, who illegally had advanceaccess to news information on 116 stocks, negativelyimpacted market depth. Guercio et al. (2017) argue thatillegal insider trading has decreased in response tomore aggressive regulatory enforcement. Ahern (2017)describes insider trading networks from civil andcriminal prosecutions initiated by the SEC and the DoJ,and Kacperczyk and Pagnotta (2016) show that marketprice and liquidity signals are impacted by illegal tradingusing SEC litigation information. Heitzman and Klasa(2016) document that investors trade quickly in stocksupon new information from nonpublic merger negoti-ations. Bhattacharya (2014) provides a comprehensiveliterature review of insider trading. For a discussionon the legal aspects of insider trading, see, for ex-ample, Arshadi (1998) and Crimmins (2013).Our focus differs from the literature examining in-

formed stock trading by corporate insiders. For ex-ample, Cohen et al. (2012) show that only opportunistictransactions, as opposed to routine transactions, havepredictive content for stock prices. Agrawal andNasser(2012) discuss widespread “passive” insider trading ontargets, whereby registered insiders increase their netexposure through reduced stock selling. Our focus is onoption trading, not stock trading.Our work broadly relates to the literature on when

and how informed agents choose to trade in the optionsmarket in the presence of asymmetric information(Easley et al. 1998), differences in opinion (Cao and Ou-Yang 2009), short-sale constraints (Johnson and So 2012),or margin requirements and wealth constraints (Johnet al. 2003) and on the predictability of option-impliedmeasures for stock returns (Easley et al. 1998, Pan andPoteshman 2006, Cremers and Weinbaum, 2010, Xinget al. 2010, Jin et al. 2012, Johnson and So 2012, Hu 2014,Tse-Chun and Xiaolong 2015). Several other papers areperipherally related to this paper. Roll et al. (2010) studythe relation Q: 14between the option-to-stock trading volumeand postearnings announcement returns. Subramanian(2004) and Bester et al. (2011) develop theoretical optionpricingmodels for the target in the case of stock-for-stockand cash mergers, respectively.

3. Data Selection and TakeoverDeal Characteristics

The data for our study come from three primarysources: the Thomson Reuters Securities Data Com-pany Platinum (SDC) database, the Center for Researchin Securities Prices (CRSP) database, and the Option-Metrics database. We start our sample selection withthe full domestic M&A data set for U.S. target firmsfrom SDC Platinum for the time period from Q: 15January

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover AnnouncementsManagement Science, Articles in Advance, pp. 1–24, © 2018 INFORMS 5

1996, the starting date for available option informationin OptionMetrics, through December 2012. Our finalsample consists of 1,859 takeover transactions for whichwe were able to identify matching stock and optioninformation for the target. These deals were undertakenby 1,279 unique acquirers on 1,669 unique targets.5

Starting from an initial sample of 185,419 trans-actions, we restrict the study to deals aimed at af-fecting a change of control, where the acquirer ownedless than 50% of the target’s stock before the trans-action andwas seeking to ownmore than 50% after it.Hence, our sample includes only M&As of majorityinterest, excluding all deals that were acquisitions ofremaining or partial interest (minority stake purchases),acquisitions of assets, recapitalizations, or buybacks/repurchases/self-tender and exchange offers. In addi-tion, we exclude deals with pending or unknown status(i.e., we only include completed, tentative, or with-drawn deals). These restrictions reduce the sample sizeto 34,350 deals. Next, we require information on thedeal value and eliminate deals with a transaction valuebelowUSD 1million, which reduces the sample furtherto 19,064 transactions. Finally, we match the infor-mation from SDC with price and volume informationin both the CRSP and OptionMetrics databases. Werequire a minimum of 90 days of valid stock and option

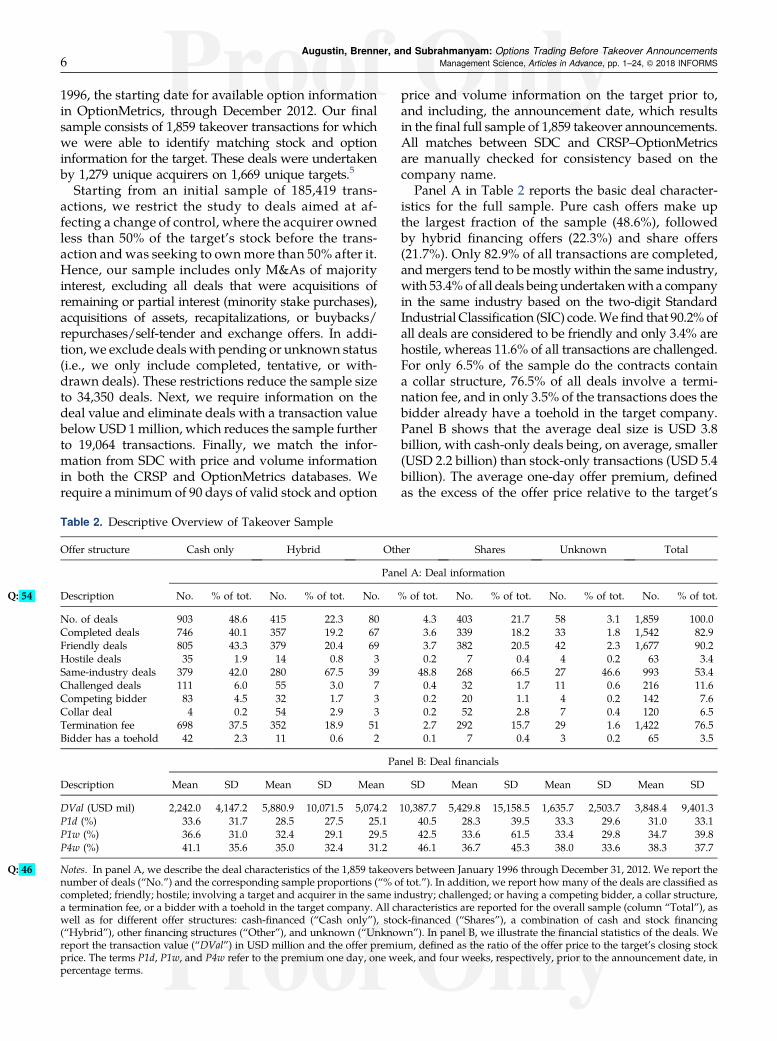

price and volume information on the target prior to,and including, the announcement date, which resultsin the final full sample of 1,859 takeover announcements.All matches between SDC and CRSP–OptionMetricsare manually checked for consistency based on thecompany name.Panel A in Table 2 reports the basic deal character-

istics for the full sample. Pure cash offers make upthe largest fraction of the sample (48.6%), followedby hybrid financing offers (22.3%) and share offers(21.7%). Only 82.9% of all transactions are completed,andmergers tend to be mostly within the same industry,with 53.4% of all deals beingundertakenwith a companyin the same industry based on the two-digit StandardIndustrial Classification (SIC) code.Wefind that 90.2%ofall deals are considered to be friendly and only 3.4% arehostile, whereas 11.6% of all transactions are challenged.For only 6.5% of the sample do the contracts containa collar structure, 76.5% of all deals involve a termi-nation fee, and in only 3.5% of the transactions does thebidder already have a toehold in the target company.Panel B shows that the average deal size is USD 3.8billion, with cash-only deals being, on average, smaller(USD 2.2 billion) than stock-only transactions (USD 5.4billion). The average one-day offer premium, definedas the excess of the offer price relative to the target’s

Table 2. Descriptive Overview of Takeover Sample

Offer structure Cash only Hybrid Other Shares Unknown Total

Panel A: Deal information

Description No. % of tot. No. % of tot. No. % of tot. No. % of tot. No. % of tot. No.Q: 54 % of tot.

No. of deals 903 48.6 415 22.3 80 4.3 403 21.7 58 3.1 1,859 100.0Completed deals 746 40.1 357 19.2 67 3.6 339 18.2 33 1.8 1,542 82.9Friendly deals 805 43.3 379 20.4 69 3.7 382 20.5 42 2.3 1,677 90.2Hostile deals 35 1.9 14 0.8 3 0.2 7 0.4 4 0.2 63 3.4Same-industry deals 379 42.0 280 67.5 39 48.8 268 66.5 27 46.6 993 53.4Challenged deals 111 6.0 55 3.0 7 0.4 32 1.7 11 0.6 216 11.6Competing bidder 83 4.5 32 1.7 3 0.2 20 1.1 4 0.2 142 7.6Collar deal 4 0.2 54 2.9 3 0.2 52 2.8 7 0.4 120 6.5Termination fee 698 37.5 352 18.9 51 2.7 292 15.7 29 1.6 1,422 76.5Bidder has a toehold 42 2.3 11 0.6 2 0.1 7 0.4 3 0.2 65 3.5

Panel B: Deal financials

Description Mean SD Mean SD Mean SD Mean SD Mean SD Mean SD

DVal (USD mil) 2,242.0 4,147.2 5,880.9 10,071.5 5,074.2 10,387.7 5,429.8 15,158.5 1,635.7 2,503.7 3,848.4 9,401.3P1d (%) 33.6 31.7 28.5 27.5 25.1 40.5 28.3 39.5 33.3 29.6 31.0 33.1P1w (%) 36.6 31.0 32.4 29.1 29.5 42.5 33.6 61.5 33.4 29.8 34.7 39.8P4w (%) 41.1 35.6 35.0 32.4 31.2 46.1 36.7 45.3 38.0 33.6 38.3 37.7

Notes. In panel A, we describe the deal characteristics of the 1,859 takeovers betweenQ: 46 January 1996 through December 31, 2012. We report thenumber of deals (“No.”) and the corresponding sample proportions (“% of tot.”). In addition, we report how many of the deals are classified ascompleted; friendly; hostile; involving a target and acquirer in the same industry; challenged; or having a competing bidder, a collar structure,a termination fee, or a bidder with a toehold in the target company. All characteristics are reported for the overall sample (column “Total”), aswell as for different offer structures: cash-financed (“Cash only”), stock-financed (“Shares”), a combination of cash and stock financing(“Hybrid”), other financing structures (“Other”), and unknown (“Unknown”). In panel B, we illustrate the financial statistics of the deals. Wereport the transaction value (“DVal”) in USD million and the offer premium, defined as the ratio of the offer price to the target’s closing stockprice. The terms P1d, P1w, and P4w refer to the premium one day, one week, and four weeks, respectively, prior to the announcement date, inpercentage terms.

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover Announcements6 Management Science, Articles in Advance, pp. 1–24, © 2018 INFORMS

closing stock price one day before the announcementdate, is 31%.

4. Informed Options Activity Priorto Takeovers

The first objective of our empirical analysis is toquantify the prevalence of informed trading usingoptions volume. Investors with private informationabout the anticipated announcement return trade offthe options’ market leverage (Black 1975) against thegreater stock market liquidity and perhaps a lowerprobability of detection. In the presence of asym-metric information (Easley et al. 1998), wealth con-straints (John et al. 2003), short-sale constraints (Johnsonand So 2012), or disagreement (Cao and Ou-Yang 2009),some informed investors will migrate toward theoption market. A necessary condition for informedpreannouncement activity is, therefore, the detection ofabnormal options volume, as stated in Hypothesis 1Q: 16 .

Hypothesis 1 (H1). There is evidence of positive abnormaltrading volume in the equity options of target firms prior totakeover announcements.

Investors with inside information would pursuedirectional trading strategies on the target firm’sstock, as it almost always goes up after a takeover an-nouncement (Andrade et al. 2001). Thus, in the presenceof superior information, a trading strategy involvingthe purchase of OTM call options should generatea significantly higher abnormal return, as a consequenceof the higher leverage (“more bang for the buck”). Hence,we expect a larger increase in abnormal trading vol-ume for OTM calls relative to ATM and ITM calls.Moreover, an informed investor, taking advantage ofhis privileged knowledge of the future direction of thetarget’s stock price, may also increase the tradingvolume through the sale of ITM puts, as these willbecome less valuable with the increase in the target’sstock price upon announcement. An alternative, andmore cash-intensive, strategy would be to mimic thestrategy of buying OTM calls by buying ITM putscoupled with the underlying stock, financed by bor-rowing. Thus, an abnormally high volume in ITM putsmay result from either mimicking the purchase ofOTM calls or taking a synthetic long position in thestock (buying a call and selling a put with the samestrike price). An informed trader may possibly engagein more complicated trading strategies to hide hisintentions. Irrespective of which strategy is employed,we should observe abnormal trading volume in OTMcall and/or ITM put options if investors with preciseinformation exploit option leverage. This leads toa sharper prediction in Hypothesis 2.

Hypothesis 2 (H2). The ratios of the abnormal tradingvolumes in (a) OTM call options to ATM and ITM call

options and (b) ITM put options to ATM and OTM putoptions, written on the target firms, are higher prior totakeover announcements.

To test H1 and H2, we examine the deal-by-dealtrading volume in equity options written on targetfirms during the 30 days preceding takeover an-nouncements. In a nutshell, we find that approximately25% of all deals in our sample exhibit statisticallysignificant abnormal options activity (at the 5% level) inthe preannouncement period. In the United Kingdom,Spyrou et al. (2011) also document abnormal pre-announcement options volume for 25% of the deals.The magnitude of abnormal volume is greater for OTMcall options than for ATM and ITM calls in our sample,confirming the results of Cao et al. (2005). Our resultssuggest that the odds of abnormal volumes beinggreater in a sample with randomized announcementdates are at most one in a million.

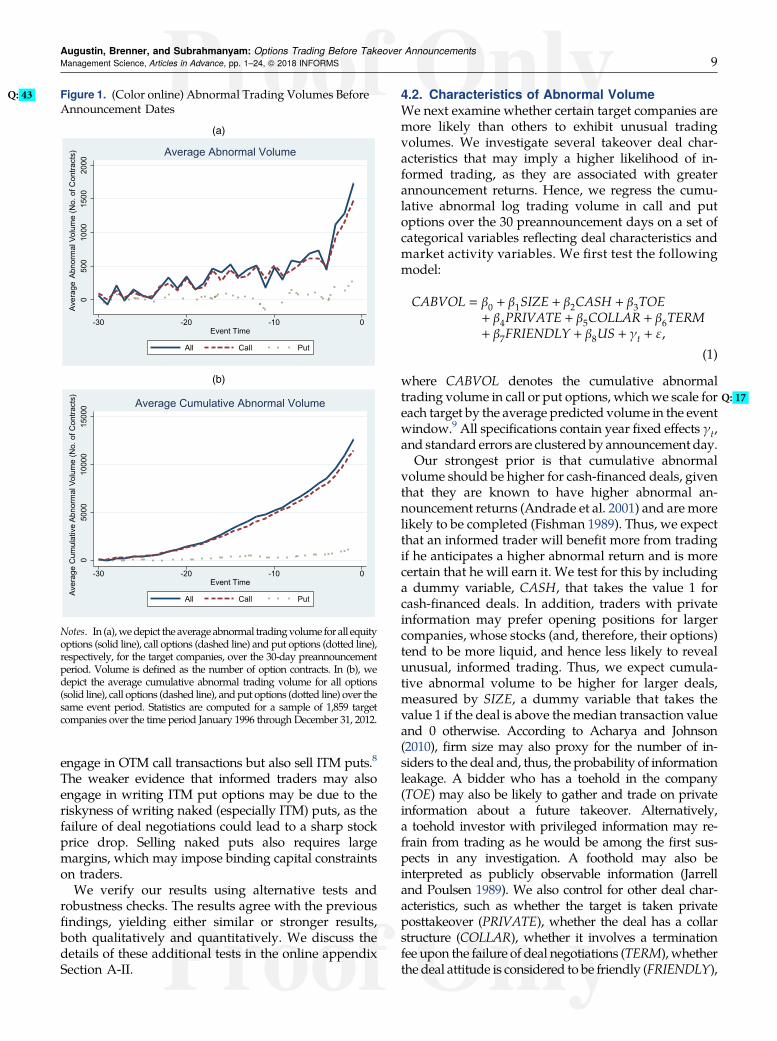

4.1. Identifying Abnormal Trading VolumesWe test H1 by applying event study methodology totrading volumes. To compute the abnormal tradingvolume, we use, as a conservative benchmark, a marketmodel for volume (MMV model), which accounts forthe market volume in options (median trading volumeacross all options in the OptionMetrics database), theChicago Board of Options Exchange Volatility Index, aswell as the contemporaneous return of the underlyingstock and the market, proxied by the return on the S&P500 Index. In addition, we control for lagged values ofthe dependent and all independent variables. The es-timation window starts 90 days before the announce-ment date andfinishes 30 days before the announcementdate. As we are interested in the abnormal tradingvolume in anticipation of the event, we use a 30-dayevent window before the announcement date. To ac-count for the possibility of clustered event dates, wecorrect standard errors in aggregate tests for cross-sectional dependence.In panel A of Table 3, we show that the average

cumulative abnormal trading volume for target firms ispositive and statistically significant. The magnitude ofthe average cumulative abnormal volume over the 30preevent days is estimated to be 8,946 contracts for calloptions. For put options on the target, the averagecumulative abnormal volume is also positive, but overthe 30 preevent days, it is much smaller, at 1,559 con-tracts, and not statistically significant. The evolutionof the average abnormal and cumulative abnormaltrading volume for the targets is illustrated in Figure 1.It is apparent that the average cumulative abnormaltrading volume in put options is quantitatively lessimportant than that in call options, which primarilydrives the results for the overall sample. The dailyaverage abnormal volume for call options is positive

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover AnnouncementsManagement Science, Articles in Advance, pp. 1–24, © 2018 INFORMS 7

and increases to approximately 1,500 contracts the daybefore the announcement. Individually, the number ofdeals with positive abnormal trading volumes, at the5% significance level, ranges from 467 for calls to 304for puts, corresponding to approximately 25% and 16%of the entire sample, respectively.6 Thus, approximately25% of the deals exhibit statistically significant cumu-lative abnormal options trading volume.7

We further stratify our sample by moneyness andconduct an event study for each category, using onlyoptions expiring after the announcement date. We findthat there is significantly higher abnormal tradingvolume for the targets in OTM call options comparedwithATMand ITM calls, in terms of both volume levelsand frequencies. Table 3 shows that the average cu-mulative abnormal volume is 3,380 (1,417) contracts forOTM calls (puts) and 1,540 (984) contracts for the ITMcalls (puts), whereas it is 1,156 (457) for ATM calls

(puts). These values correspond to 408 (343, 482) deals,or 22% (18%, 26%) of the sample, for OTM (ATM, ITM)calls, and 451 (362, 396) deals, or 24% (19%, 21%), forOTM (ATM, ITM) puts, respectively.In panel B of Table 3, we report results from paired

t-tests for the differences in themeans of the cumulativeaverage abnormal volumes across different categories.Consistent with H2, these results emphasize that there ishigher abnormal trading volume for OTM call optionsthan for ATM or ITM calls. The differences in the meansforOTMcalls relative toATMand ITMcalls are 2,224 and1,840, respectively, which are positive and statisticallydifferent from zero. On the other hand, the difference inthe means between ATM and ITM calls is slightly neg-ative (−384) but not statistically different from zero. Theaverage cumulative abnormal volume for ITM put op-tions is higher than for ATMput options, which providessome evidence that informed traders may not only

Table 3. PositiveQ: 47 Abnormal Options Trading Volume on Target Companies

Panel A: Magnitude and frequency of cumulative abnormal volume deals

All options: Target OTM options: Target

Parameter All Calls Puts All Calls Puts

Sign. t-stat 5% (no.) 446 467 304 423 408 451Sign. t-stat 5% (freq.) 0.24 0.25 0.16 0.23 0.22 0.24

E[CAV] 10,385 8,946 1,559 5,071 3,380 1,417t ¯CAV 3.76 5.77 1.04 5.44 5.46 3.34

ATM options: Target ITM options: Target

All Calls Puts All Calls PutsSign. t-stat 5% (no.) 341 343 362 393 482 396Sign. t-stat 5% (freq.) 0.18 0.18 0.19 0.21 0.26 0.21

E[CAV] 1,652 1,156 457 2,526 1,540 984t ¯CAV 2.84 2.65 1.98 4.71 6.40 2.42

Panel B: Differences in cumulative abnormal volume across moneyness

All options: Target Call options: Target

Diff SE p-value Diff SE p-valueOTM–ATM 3,419 722 0.00 2,224 531 0.00OTM–ITM 2,544 669 0.00 1,840 561 0.00ATM–ITM −874 632 0.17 −384 444 0.39

Put options: Target

Diff SE p-valueOTM–ATM 960 450 0.03 — — —OTM–ITM 433 367 0.24 — — —ATM–ITM −527 429 0.22 — — —

Notes. Panel A reports the number and frequency of deals with statistically significant positive cumulative abnormal volume at the 5% significancelevel for the target companies, as well as the average cumulative abnormal volume (E[CAV]) and corresponding t-statistic (t ¯CAV), computed usingheteroscedasticity-robust standard errors. All results are reported separately for call options, for put options, and for the aggregate option volume.Results stratified bymoneyness are based only on those options expiring after the announcement date. The estimationwindow starts 90 days beforethe announcement date and runs until 30 days before the announcement date. The event window stretches from 30 days before until one day beforethe announcement date. In panel B,we report the results of t-tests for the differences in the average cumulative abnormal volumes acrossmoneynesscategories: OTM, ITM, and ATM. We report the difference in average cumulative abnormal volume (“Diff”), the standard error, and the p-value.

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover Announcements8 Management Science, Articles in Advance, pp. 1–24, © 2018 INFORMS

engage in OTM call transactions but also sell ITM puts.8

The weaker evidence that informed traders may alsoengage in writing ITM put options may be due to theriskyness of writing naked (especially ITM) puts, as thefailure of deal negotiations could lead to a sharp stockprice drop. Selling naked puts also requires largemargins, which may impose binding capital constraintson traders.

We verify our results using alternative tests androbustness checks. The results agree with the previousfindings, yielding either similar or stronger results,both qualitatively and quantitatively. We discuss thedetails of these additional tests in the online appendixSection A-II.

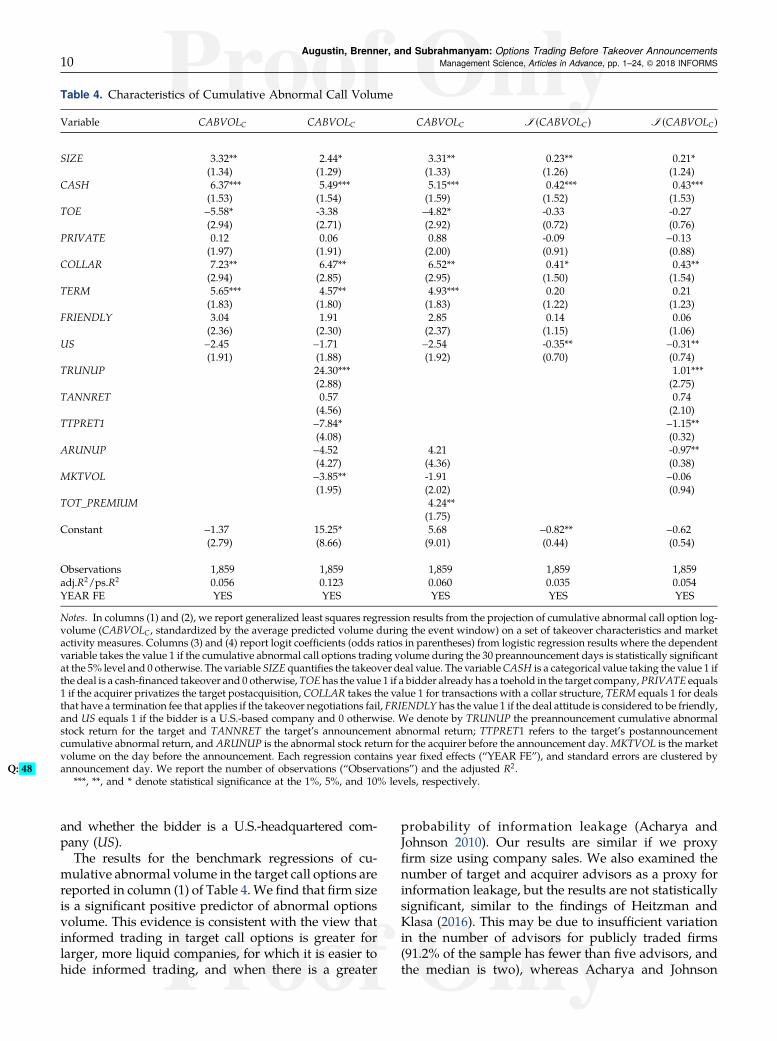

4.2. Characteristics of Abnormal VolumeWe next examine whether certain target companies aremore likely than others to exhibit unusual tradingvolumes. We investigate several takeover deal char-acteristics that may imply a higher likelihood of in-formed trading, as they are associated with greaterannouncement returns. Hence, we regress the cumu-lative abnormal log trading volume in call and putoptions over the 30 preannouncement days on a set ofcategorical variables reflecting deal characteristics andmarket activity variables. We first test the followingmodel:

CABVOL � β0 + β1SIZE + β2CASH + β3TOE+ β4PRIVATE + β5COLLAR + β6TERM+ β7FRIENDLY + β8US + γt + ε,

(1)

where CABVOL denotes the cumulative abnormaltrading volume in call or put options Q: 17, which we scale foreach target by the average predicted volume in the eventwindow.9 All specifications contain year fixed effects γt,and standard errors are clustered by announcement day.Our strongest prior is that cumulative abnormal

volume should be higher for cash-financed deals, giventhat they are known to have higher abnormal an-nouncement returns (Andrade et al. 2001) and are morelikely to be completed (Fishman 1989). Thus, we expectthat an informed trader will benefit more from tradingif he anticipates a higher abnormal return and is morecertain that he will earn it. We test for this by includinga dummy variable, CASH, that takes the value 1 forcash-financed deals. In addition, traders with privateinformation may prefer opening positions for largercompanies, whose stocks (and, therefore, their options)tend to be more liquid, and hence less likely to revealunusual, informed trading. Thus, we expect cumula-tive abnormal volume to be higher for larger deals,measured by SIZE, a dummy variable that takes thevalue 1 if the deal is above themedian transaction valueand 0 otherwise. According to Acharya and Johnson(2010), firm size may also proxy for the number of in-siders to the deal and, thus, the probability of informationleakage. A bidder who has a toehold in the company(TOE) may also be likely to gather and trade on privateinformation about a future takeover. Alternatively,a toehold investor with privileged information may re-frain from trading as he would be among the first sus-pects in any investigation. A foothold may also beinterpreted as publicly observable information (Jarrelland Poulsen 1989). We also control for other deal char-acteristics, such as whether the target is taken privateposttakeover (PRIVATE), whether the deal has a collarstructure (COLLAR), whether it involves a terminationfee upon the failure of deal negotiations (TERM), whetherthe deal attitude is considered to be friendly (FRIENDLY),

Figure 1. (Color online) AbnormalQ: 43 Trading Volumes BeforeAnnouncement Dates

Notes. In (a),wedepict theaverage abnormal tradingvolume for all equityoptions (solid line), call options (dashed line) and put options (dotted line),respectively, for the target companies, over the 30-day preannouncementperiod. Volume is defined as the number of option contracts. In (b), wedepict the average cumulative abnormal trading volume for all options(solid line), call options (dashed line), and put options (dotted line) over thesame event period. Statistics are computed for a sample of 1,859 targetcompanies over the time period January 1996 through December 31, 2012.

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover AnnouncementsManagement Science, Articles in Advance, pp. 1–24, © 2018 INFORMS 9

and whether the bidder is a U.S.-headquartered com-pany (US).

The results for the benchmark regressions of cu-mulative abnormal volume in the target call options arereported in column (1) of Table 4. We find that firm sizeis a significant positive predictor of abnormal optionsvolume. This evidence is consistent with the view thatinformed trading in target call options is greater forlarger, more liquid companies, for which it is easier tohide informed trading, and when there is a greater

probability of information leakage (Acharya andJohnson 2010). Our results are similar if we proxyfirm size using company sales. We also examined thenumber of target and acquirer advisors as a proxy forinformation leakage, but the results are not statisticallysignificant, similar to the findings of Heitzman andKlasa (2016). This may be due to insufficient variationin the number of advisors for publicly traded firms(91.2% of the sample has fewer than five advisors, andthe median is two), whereas Acharya and Johnson

Table 4. Characteristics of Cumulative Abnormal Call Volume

Variable CABVOLC CABVOLC CABVOLC I (CABVOLC) I (CABVOLC)

SIZE 3.32** 2.44* 3.31** 0.23** 0.21*(1.34) (1.29) (1.33) (1.26) (1.24)

CASH 6.37*** 5.49*** 5.15*** 0.42*** 0.43***(1.53) (1.54) (1.59) (1.52) (1.53)

TOE −5.58* -3.38 −4.82* -0.33 -0.27(2.94) (2.71) (2.92) (0.72) (0.76)

PRIVATE 0.12 0.06 0.88 -0.09 −0.13(1.97) (1.91) (2.00) (0.91) (0.88)

COLLAR 7.23** 6.47** 6.52** 0.41* 0.43**(2.94) (2.85) (2.95) (1.50) (1.54)

TERM 5.65*** 4.57** 4.93*** 0.20 0.21(1.83) (1.80) (1.83) (1.22) (1.23)

FRIENDLY 3.04 1.91 2.85 0.14 0.06(2.36) (2.30) (2.37) (1.15) (1.06)

US −2.45 −1.71 −2.54 -0.35** −0.31**(1.91) (1.88) (1.92) (0.70) (0.74)

TRUNUP 24.30*** 1.01***(2.88) (2.75)

TANNRET 0.57 0.74(4.56) (2.10)

TTPRET1 −7.84* −1.15**(4.08) (0.32)

ARUNUP −4.52 4.21 -0.97**(4.27) (4.36) (0.38)

MKTVOL −3.85** -1.91 −0.06(1.95) (2.02) (0.94)

TOT_PREMIUM 4.24**(1.75)

Constant −1.37 15.25* 5.68 −0.82** −0.62(2.79) (8.66) (9.01) (0.44) (0.54)

Observations 1,859 1,859 1,859 1,859 1,859adj.R2/ps.R2 0.056 0.123 0.060 0.035 0.054YEAR FE YES YES YES YES YES

Notes. In columns (1) and (2), we report generalized least squares regression results from the projection of cumulative abnormal call option log-volume (CABVOLC, standardized by the average predicted volume during the event window) on a set of takeover characteristics and marketactivity measures. Columns (3) and (4) report logit coefficients (odds ratios in parentheses) from logistic regression results where the dependentvariable takes the value 1 if the cumulative abnormal call options trading volume during the 30 preannouncement days is statistically significantat the 5% level and 0 otherwise. The variable SIZE quantifies the takeover deal value. The variableCASH is a categorical value taking the value 1 ifthe deal is a cash-financed takeover and 0 otherwise, TOE has the value 1 if a bidder already has a toehold in the target company,PRIVATE equals1 if the acquirer privatizes the target postacquisition, COLLAR takes the value 1 for transactions with a collar structure, TERM equals 1 for dealsthat have a termination fee that applies if the takeover negotiations fail, FRIENDLY has the value 1 if the deal attitude is considered to be friendly,and US equals 1 if the bidder is a U.S.-based company and 0 otherwise. We denote by TRUNUP the preannouncement cumulative abnormalstock return for the target and TANNRET the target’s announcement abnormal return; TTPRET1 refers to the target’s postannouncementcumulative abnormal return, and ARUNUP is the abnormal stock return for the acquirer before the announcement day.MKTVOL is the marketvolume on the day before the announcement. Each regression contains year fixed effects (“YEAR FE”), and standard errors are clustered byannouncement day. We report the number of observations (“Observations”) and the adjusted R2.Q: 48

***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively.

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover Announcements10 Management Science, Articles in Advance, pp. 1–24, © 2018 INFORMS

(2010) examine a sample of private equity buyouts,which typically feature a higher number of equityparticipants. QuantitativelyQ: 18 , we find that a target dealabove the median transaction value has, on average,3.32% greater cumulative abnormal call trading vol-ume relative to its normal volume than a target belowthe median deal size.

The results in column (1) of Table 4 suggest that cash-financeddeals have, on average, 6.37%greater cumulativeabnormal volume than noncash-financed deals. Giventhat the average cumulative abnormal volume is ap-proximately 10,000 contracts, the typical cash-financeddeal has about 637 more contracts traded during the30-day preannouncement period. The cash indicator isconsistently robust across all specifications, with similareconomic magnitudes.

If the bidder already has a toehold in the company,cumulative abnormal volume is about 5.6% smaller.The negative coefficient supports the interpretationthat investors with a toehold may make more of anattempt to keep their intentions secret, as theywould benatural suspects in the case of insider trading. Thecoefficient of TOE, however, loses its significance ina specification with additional control variables re-ported in column (2) of Table 4. Deals that embeda collar structure and a termination fee in their nego-tiations are also more likely to exhibit higher cumu-lative abnormal volume, by about 7.23% and 5.65%,respectivelyQ: 19 , on average. A collar structure implicitlydefines a target price range for the takeover agreement.Moreover, a termination fee makes it more likely thata negotiation will be concluded. Thus, both variablesare associated with greater certainty about the mag-nitude of the target’s stock price increase, conditionalon an announcement being made. This is consistentwith a greater likelihood of informed trading in thepresence of greater price certainty. All other variablesare statistically insignificant. The adjusted R2 of theregression, 6%, is reasonable, given the likely idio-syncratic nature of the derived statistic for cumulativeabnormal trading volume.

We next examine whether market activity variableshave an impact on the preannouncement cumulativeabnormal call volume. We include TRUNUP, the pre-announcement cumulative abnormal stock return for thetarget; TANNRET, the target’s announcement-day ab-normal return; TTPRET1, the target’s postannouncementcumulative abnormal return; and ARUNUP, the abnor-mal stock return for the acquirer before the announce-ment day.We denote byMKTVOL themarket volume onthe day before the announcement. These results are re-ported in column (2) of Table 4. The preannouncementrun-up in the target’s stock price is strongly positivelyrelated to the cumulative abnormal volume, consistentwith Acharya and Johnson (2010) and Wang (2013). Thisfinding suggests that abnormal options trading activity

on the target firm may be instigated by the target firm’spositive stock price momentum. We examine this pos-sibility in Section 5. On the other hand, the target’s cu-mulative abnormal announcement return is negativelyassociatedwith the cumulative abnormal trading volumefor call options. All other variables are statistically in-significant. The coefficients remain robust for largedeals that are cash-financed, that have a collar struc-ture, and that have a termination fee. In this final re-gression specification, the explanatory power increasesto 12%. We repeat the analysis for cumulative abnormalvolume in put options. Although the results are quali-tatively similar, the magnitudes of the coefficients aretypically smaller and are not reported here.The insignificant (negative) relation between ab-

normal call options volume and the abnormal an-nouncement (postannouncement cumulative) returnmay appear at odds with the notion that the abnormaloptions activity is informed. The results are never-theless consistent with the findings in Jayaraman et al.(2001), Spyrou et al. (2011), Klapper (2013), andPodolski et al. (2013). Cao et al. (2005) rely on signedvolume to show that buy-minus-sell call volume orderimbalance in the preannouncement period positivelypredicts two-day abnormal announcement returns. Inunreported regressions, we use signed options volumedata, taken from the International Securities Exchangefor a subsample of approximately 400 takeovers from2006 onwards, and confirm the positive relation be-tween preannouncement call option order imbalanceand announcement returns. Because Q: 20we use unsignedvolume, the relation is not as straightforward. If muchof the insider information gets incorporated into pricesin the preannouncement period (Meulbroek 1992), onemay expect a negative relation between the volumerun-up and the announcement return, as the stock pricerun-up and the announcement effect are negativelycorrelated for a given offer premium (−14% in oursample). A priori, the relation between an unsignedvolume metric measured over 30 days and the an-nouncement effect is unclear. Rather, we would expectapositive relation between themagnitude of the abnormalpreannouncement options volume and the total premiumpaid by the bidder, which corresponds to the sum of thepreannouncement run-up (TRUNP), the announcementeffect (TANNRET), and the postannouncement return(TTPRET1). Thus, we replace these three variableswith the total premium (TOT_PREMIUM) and find incolumn (3) in Table 4 a significantly positive relation,consistent with the interpretation that the optionsactivity is informed.In columns (4) and (5), we report the results of a

logistic regression in which we replace the dependentvariable with an indicator variable that takes the value 1if a deal has cumulative abnormal call options tradingvolume at the 5% significance level and 0 otherwise. The

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover AnnouncementsManagement Science, Articles in Advance, pp. 1–24, © 2018 INFORMS 11

evidence corroborates the positive relation between theabnormal options activity in the preannouncementperiod and variables that are positively correlated witha higher probability of informed trading.

5. Informed vs. Insider TradingThere is a long-standing debate as to whether the stockprice run-up before M&A announcements is rationallyanticipated or whether it is the result of private in-formation. The preannouncement run-up in optionsvolume may be due to rational anticipation of up-coming takeover announcements, arising throughrumors about upcoming tender offers, speculation asa result of industry-specific merger waves, or simplybecause of the superior ability of certain investorsto forecast deal activity. Alternatively, it could arisethrough trading on private information. In this sec-tion, we assess the likelihood of the informed optionsactivity being illegal. To this end, we examine deal bydeal whether publicly available information may ex-plain the preannouncement run-up in options volume.

5.1. A Legal Definition of Insider TradingIn the United States, insider trading is regulated underthe Securities Exchange Act of 1934, and the respon-sibility for enforcement lies with the SEC.10 Regis-tered insiders are bound by the “classical” theoryimplicit in the antifraud provisions in the act, whichholds them liable if they have traded based on materialnonpublic information from their company and if theyhave violated their fiduciary duty. Outsiders to the firmmay legally infer a material “mosaic” conclusion bypiecing together multiple pieces of immaterial non-public information. However, they are bound by the“misappropriation” theory implicit in the act, whichprohibits trading based on information that is mis-appropriated from a third party to whom the investorowes a fiduciary duty.

The boundaries of illegal insider trading are blurry,at best, and the bar on identifying insider trading incourt is high.11 It is difficult to draw a clear and precisedistinction between a trade that is speculative, in-formed, and legal and one that is illegal. Thus, we focuson each deal, narrowing down the possibility that theunusual/abnormal preannouncement options activitymight be explained by publicly available information.

5.2. SpeculationMerger activity is procyclical and arrives in industry-specific waves (Andrade et al. 2001). The earlier find-ings for the sources of informed trading—namely, thatcumulative abnormal volumes are significantly relatedto the run-up in stock prices—may also suggest that theabnormal options activity may simply be the result ofpositive price momentum on the target’s stock. Thus,speculation may explain the preannouncement options

activity. Such a selection bias would be consistent withthe view that takeovers are anticipated.We examine this possibility by constructing several

control samples, matching them based on either theactivity in the underlying stock or firm characteristics.12

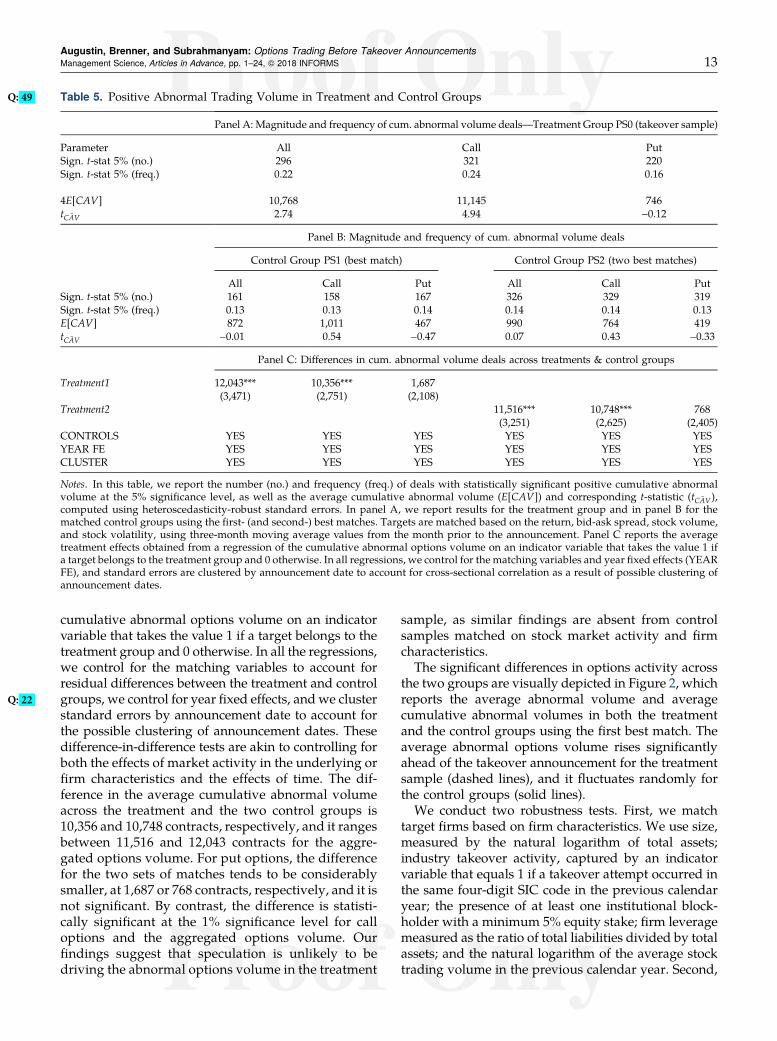

In other words, for each of the 1,859 takeover deals, atthe time of the takeover announcement, we look fora similar firm with traded options and which resemblesthe takeover firm in terms of either stockmarket activitymeasures for the underlying stock or firm characteris-tics. For the market-based control sample, we matchfirms based on three-month moving averages ofa firm’s stock return, stock return volatility using theexponential-weighted moving average model, stocktrading volume, percentage bid-ask spread to captureilliquidity, and three-month cumulative stock returnsto capture the momentum in a firm’s stock. We matchonly targets for completed deals based on the monthprior to the takeover announcement. We sample withreplacement and use the Mahalanobis distance metricto evaluate the “closeness” of the match. Table A-6 inthe online appendix documents the matching qualityfor both control samples. Most Q: 21variables are statisticallyindistinguishable between the treatment and controlgroups; those that are distinguishable resemble eachother closely in terms of economic magnitude.The findings reported in Table 5 suggest that the run-

up in options trading volume prior to the announce-ment is unlikely due to investors speculating in theoptions market after having observed (perhaps) in-formed trading activity in the underlying shares. Wereport results for aggregate options volume and sep-arately for the aggregate call and put volumes, usingthe MMV model, in which we control for the laggedvalues of both the dependent and independent vari-ables. The results in panel A of Table 5 suggest thatabout 25% of all deals in the treatment sample havepositive abnormal call options trading volume, witha lower frequency (16%) of unusual options activity forput options. The average cumulative abnormal totaloptions and call volume is 10,768 and 11,145 contracts,respectively. Both values are statistically significant atthe 1% level.In panel B of Table 5, we report the results for the

control groups using the first best (PS1) and the twofirst best (PS2) matches. The frequency of deals withstatistically significant cumulative abnormal volume atthe 5% significance level is lower than in the treatmentsample, ranging between 13% and 14%. For call op-tions, the average cumulative abnormal volume issignificantly lower in the two control groups than in thetreatment groups, as the average cumulative abnormalcall volume is only 1,011 and 764 contracts. Impor-tantly, none of the statistics is statistically significant.In panel C of Table 5, we report the average treat-

ment effects obtained from a regression of the

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover Announcements12 Management Science, Articles in Advance, pp. 1–24, © 2018 INFORMS

cumulative abnormal options volume on an indicatorvariable that takes the value 1 if a target belongs to thetreatment group and 0 otherwise. In all the regressions,we control for the matching variables to account forresidual differences between the treatment and controlgroups, weQ: 22 control for year fixed effects, and we clusterstandard errors by announcement date to account forthe possible clustering of announcement dates. Thesedifference-in-difference tests are akin to controlling forboth the effects of market activity in the underlying orfirm characteristics and the effects of time. The dif-ference in the average cumulative abnormal volumeacross the treatment and the two control groups is10,356 and 10,748 contracts, respectively, and it rangesbetween 11,516 and 12,043 contracts for the aggre-gated options volume. For put options, the differencefor the two sets of matches tends to be considerablysmaller, at 1,687 or 768 contracts, respectively, and it isnot significant. By contrast, the difference is statisti-cally significant at the 1% significance level for calloptions and the aggregated options volume. Ourfindings suggest that speculation is unlikely to bedriving the abnormal options volume in the treatment

sample, as similar findings are absent from controlsamples matched on stock market activity and firmcharacteristics.The significant differences in options activity across

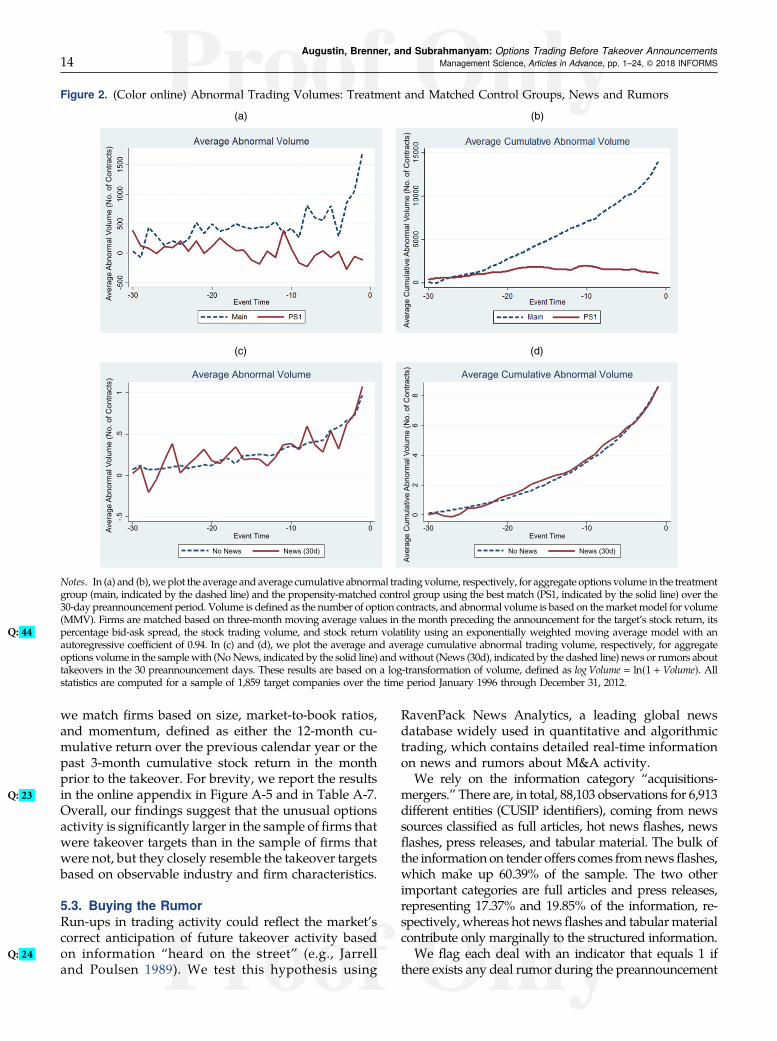

the two groups are visually depicted in Figure 2, whichreports the average abnormal volume and averagecumulative abnormal volumes in both the treatmentand the control groups using the first best match. Theaverage abnormal options volume rises significantlyahead of the takeover announcement for the treatmentsample (dashed lines), and it fluctuates randomly forthe control groups (solid lines).We conduct two robustness tests. First, we match

target firms based on firm characteristics. We use size,measured by the natural logarithm of total assets;industry takeover activity, captured by an indicatorvariable that equals 1 if a takeover attempt occurred inthe same four-digit SIC code in the previous calendaryear; the presence of at least one institutional block-holder with a minimum 5% equity stake; firm leveragemeasured as the ratio of total liabilities divided by totalassets; and the natural logarithm of the average stocktrading volume in the previous calendar year. Second,

Table 5. PositiveQ: 49 Abnormal Trading Volume in Treatment and Control Groups

Panel A: Magnitude and frequency of cum. abnormal volume deals—Treatment Group PS0 (takeover sample)

Parameter All Call PutSign. t-stat 5% (no.) 296 321 220Sign. t-stat 5% (freq.) 0.22 0.24 0.16

4E[CAV] 10,768 11,145 746t ¯CAV 2.74 4.94 −0.12

Panel B: Magnitude and frequency of cum. abnormal volume deals

Control Group PS1 (best match) Control Group PS2 (two best matches)

All Call Put All Call PutSign. t-stat 5% (no.) 161 158 167 326 329 319Sign. t-stat 5% (freq.) 0.13 0.13 0.14 0.14 0.14 0.13E[CAV] 872 1,011 467 990 764 419t ¯CAV −0.01 0.54 −0.47 0.07 0.43 −0.33

Panel C: Differences in cum. abnormal volume deals across treatments & control groups

Treatment1 12,043*** 10,356*** 1,687(3,471) (2,751) (2,108)

Treatment2 11,516*** 10,748*** 768(3,251) (2,625) (2,405)

CONTROLS YES YES YES YES YES YESYEAR FE YES YES YES YES YES YESCLUSTER YES YES YES YES YES YES

Notes. In this table, we report the number (no.) and frequency (freq.) of deals with statistically significant positive cumulative abnormalvolume at the 5% significance level, as well as the average cumulative abnormal volume (E[CAV]) and corresponding t-statistic (t ¯CAV),computed using heteroscedasticity-robust standard errors. In panel A, we report results for the treatment group and in panel B for thematched control groups using the first- (and second-) best matches. Targets are matched based on the return, bid-ask spread, stock volume,and stock volatility, using three-month moving average values from the month prior to the announcement. Panel C reports the averagetreatment effects obtained from a regression of the cumulative abnormal options volume on an indicator variable that takes the value 1 ifa target belongs to the treatment group and 0 otherwise. In all regressions, we control for the matching variables and year fixed effects (YEARFE), and standard errors are clustered by announcement date to account for cross-sectional correlation as a result of possible clustering ofannouncement dates.

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover AnnouncementsManagement Science, Articles in Advance, pp. 1–24, © 2018 INFORMS 13

we match firms based on size, market-to-book ratios,and momentum, defined as either the 12-month cu-mulative return over the previous calendar year or thepast 3-month cumulative stock return in the monthprior to the takeover. For brevity, we report the resultsin the onlineQ: 23 appendix in Figure A-5 and in Table A-7.Overall, our findings suggest that the unusual optionsactivity is significantly larger in the sample of firms thatwere takeover targets than in the sample of firms thatwere not, but they closely resemble the takeover targetsbased on observable industry and firm characteristics.

5.3. Buying the RumorRun-ups in trading activity could reflect the market’scorrect anticipation of future takeover activity basedon information “Q: 24 heard on the street” (e.g., Jarrelland Poulsen 1989). We test this hypothesis using

RavenPack News Analytics, a leading global newsdatabase widely used in quantitative and algorithmictrading, which contains detailed real-time informationon news and rumors about M&A activity.We rely on the information category “acquisitions-

mergers.” There are, in total, 88,103 observations for 6,913different entities (CUSIP identifiers), coming from newssources classified as full articles, hot news flashes, newsflashes, press releases, and tabular material. The bulk ofthe information on tender offers comes fromnewsflashes,which make up 60.39% of the sample. The two otherimportant categories are full articles and press releases,representing 17.37% and 19.85% of the information, re-spectively, whereas hot newsflashes and tabularmaterialcontribute only marginally to the structured information.We flag each deal with an indicator that equals 1 if

there exists any deal rumor during the preannouncement

Figure 2. (Color online) Abnormal Trading Volumes: Treatment and Matched Control Groups, News and Rumors

Notes. In (a) and (b),weplot the average and average cumulative abnormal trading volume, respectively, for aggregate options volume in the treatmentgroup (main, indicated by the dashed line) and the propensity-matched control group using the best match (PS1, indicated by the solid line) over the30-day preannouncement period. Volume is defined as the number of option contracts, and abnormal volume is based on themarketmodel for volume(MMV). Firms are matched based on three-month moving average values in the month preceding the announcement for the target’s stock return, itspercentage bid-ask spread, the stock trading volume, and stock return volatility using an exponentiallQ: 44 y weighted moving average model with anautoregressive coefficient of 0.94. In (c) and (d), we plot the average and average cumulative abnormal trading volume, respectively, for aggregateoptions volume in the samplewith (NoNews, indicated by the solid line) andwithout (News (30d), indicated by the dashed line) news or rumors abouttakeovers in the 30 preannouncement days. These results are based on a log-transformation of volume, defined as logVolume � ln(1 + Volume). Allstatistics are computed for a sample of 1,859 target companies over the time period January 1996 through December 31, 2012.

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover Announcements14 Management Science, Articles in Advance, pp. 1–24, © 2018 INFORMS

period and 0 if not. We find a rumor or news story on5,195 different deal-days, corresponding to 877 uniquedeals from our sample of 1,859 takeovers announcedbetween 1996 and 2012. Most of the news and rumorinformation appears on the announcement day itself,as shown in Table 6, which illustrates the total numberof observations and unique deals in different samplewindows. Rumors or news stories exist in the 30-day

preannouncement period for only 170 firms, whichcorresponds to approximately 9% of our sample, or13.72% on a proportional basis, given that 1,239takeovers were announced between January 2000 andAugust 2012. Most importantly, of the 467 takeoverannouncements with significant informed optionstrading, we associate only 8.57% (40 deals) with newsor rumors captured by RavenPack.

Table 6. Frequency of News Around Takeover Announcements

Time window [−150, −91] [−90 , −31] [−30, −21] [−20, −11] [−10, −6] [−5, −1] [0] [1,5] [5,10] [−150, −91] [−30, −1] [−90, −1]

Obs. 258 290 67 67 31 74 660 252 140 1839 239 529Deals 188 204 55 59 29 63 659 218 113 407 170 299

Notes. In this table, we report the frequency of news around takeover announcements. The information is from RavenPack News Analytics,which extracts textual information from major publishers, such as Dow Jones Newswires, the Wall Street Journal, Barron’s, regulatory and publicrelation feeds, andmore than 19,000 other traditional and social media sites. The company transforms the information into a structured data feedthat can be used in quantitative analysis. Using the data from January 2000 to August 2012, we report the number of news and rumor items(“Obs.”) and the corresponding number of takeover deals (“Deals”) recorded during different timewindows around the announcement day. Thewindow titled “[0]” relates to news and rumors on the announcement day. All other columns refer to different time windows in the pre- orpostannouncement period.

Table 7. SourcesQ: 50 of Informed Options Trading

Set No. % Cum% A B C D Description

Ω 1,859 100.00 100.00 3 3 3 3 Takeover sampleA 467 25.12 25.12 3 ✘ ✘ ✘ Abnormal options volume (A)Ω\A 1,392 74.87 100.00 ✘ 3 3 3 No abnormal options volumeB 170 9.14 9.14 ✘ 3 ✘ ✘ News and rumors (B)Ω\B 1,689 90.86 100.00 3 ✘ 3 3 No news or rumorsC 352 18.93 18.93 ✘ ✘ 3 ✘ Abnormal stock volume (C)Ω\C 1,507 81.07 100.00 3 3 ✘ 3 No abnormal stock volumeD 135 7.26 7.26 ✘ ✘ ✘ 3 Abnormal stock returns (D)Ω\D 1,724 92.74 100.00 3 3 3 ✘ No abnormal stock returns(A ∩ C ∩ D) \ B 427 22.97 22.97 3 ✘ 3 3 A, C, D; no BΩ\(A ∩ B ∩ C ∩ D) 1,036 55.73 55.73 ✘ ✘ ✘ ✘ No A, B, C, DA\(B ∪ C ∪ D) 236 12.69 68.42 3 ✘ ✘ ✘ A, C, D; no B

Notes. In this table, we document the sources of informed options trading for a sample of 1,859 takeovers from January 1996 to December 2012.Of the 1,859 takeovers, 467 (25.12, subset A) have abnormal options trading volume at the 5% significance level over the 30-daypreannouncement period. The sample of news and rumors amounts to 170 deals (9.14%, subset B); 352 of all deals (18.93%, subset C) haveabnormal stock trading volume in the run-up to the announcement, whereas 135 deals (7.26%, subsetD) have abnormal stock returns in the run-up to the announcement. In total, 427 of all deals (22.97%) have abnormal options trading volume ahead of the announcement as well asabnormal returns and volume in the underlying stock, without any news or rumors; 236 of all deals (13%, grey area) have only abnormal optionstrading volume and are difficult to associate with public sources of information.

Augustin, Brenner, and Subrahmanyam: Options Trading Before Takeover AnnouncementsManagement Science, Articles in Advance, pp. 1–24, © 2018 INFORMS 15

It is possible that rumored firms drive the unusualtrading activity we document ahead of the takeoverannouncements. Thus, we investigate whether there ismore abnormal volume in options for those firms thathave rumors compared with a control group of targetswithout rumors. Figure 2, (c) and (d), show the dif-ferences in average and average cumulative abnormaloption trading volumes for the subsamples with andwithout rumors in the 30-day preannouncement pe-riod. These tests are based on a natural log transformationof volume. The two subsamples are statistically in-distinguishable from each other, and the average ab-normal trading volume is as unusual in the subsamplewith news “heard on the street” as in the samplewithout.The same results hold if we screen the sample for newsand rumors in the 90-day preannouncement period.13

We provide a visual overview of the subsampleoverlaps using a Venn diagram embedded in Table 7.The outer square outlines the full sample of 1,859takeovers, which we label Ω. The informed tradingsubsample is characterized by the rectangle A, whichindicates that 467 deals are flagged with statisticallysignificant positive cumulative abnormal trading vol-ume at the 5% significance level, corresponding to25.12% of the entire sample. In the 30 preannounce-ment days, we identify news for 170 deals. The newssample is depicted as the rectangle B, and it accountsfor 9.14% of the overall sample. Of the 170 takeoversthat are associated with news, 40 overlap with the467 deals flagged for informed options trading,representing 8.57% of the informed trading sample.The remaining overlaps are described in the fol-lowing subsections. We also find that tests based ona natural log transformation of volume indicate no sta-tistically significant difference in abnormal trading vol-ume between the subsamples with and without news.Rumors and news about upcoming merger activities arethus unlikely to explain the full amount of directionaltrading volume on targets ahead of the announcementswe document.

5.4. Legal Insider TradingRegistered corporate insiders have access to privilegedinformation. As a result, they must file with the SECwhenever they trade in their company’s securities andtheir derivatives.14 Even though it is illegal for insidersto trade the target firm’s securities prior to a takeoverannouncement, there is some evidence of such activityin prior research. This could be explained throughlimited enforceability of insider trading laws or a lackof prosecution (Arshadi and Eyssell 1991, Bris, 2005).For example, in the United States, Agrawal and Nasser(2012) document that insiders increase their net stockpurchases prior to takeover announcements.

As prior research has not reported on transactions byregistered insiders in target firms’ options, we examine

the registered derivatives trading activity, which islogged in Table 2 of the Thomson Reuters insider filingdata feeds.15 We made an elaborate search in theThomson Reuters filings of transactions by insiders forour 1,859 target firms. We found not a single record ofa transaction, purchase, or sale of a derivative securitywithin the 30-day window preceding the announce-ment. Nevertheless, it is possible that the unusualoptions volume we document stems from tips origi-nating with senior executives at target companies orfrom former school ties (Cohen et al. 2010). Indeed,Ahern (2017) reports that tips that lead to illegal insidertrades often originate from corporate executives.

5.5. LeakageIn this subsection, we examine whether the abnormalvolume effects observed in the options market couldbe driven by preannouncement leakage or informedtrading in stock markets. There is evidence to suggestthat option volume tends to rise in response to positivestock returns (Roll et al. 2010, Johnson and So 2012).Wetest our conjecture in several ways.First, in all our abnormal volume tests, we system-

atically control for both contemporaneous and laggedstock returns of the target companies and the overallmarket. This does not affect the evidence of abnormaloptions activity in the preannouncement period.Second, Q: 25we conduct an event study for abnormal

stock returns and find that only 7.26% (135 deals) of all1,859 takeovers in our sample exhibit abnormal stockreturns at the 5% statistical significance level. Of the 467deals that we associate with informed options trading,only 9.64% (45 deals) exhibit abnormal stock returns, asis illustrated by the overlaps of the informed optiontrading subsample A and the subsample with abnor-mal stock returns D in the Venn diagram illustrated inTable 7.Third, although we do find that about 18.93% of all