Embed Size (px)

Citation preview

Intersession Project

For the Class of 2019

LOAN PORTFOLIO MANAGEMENT – YEAR 2

2018 Session

P L E A S E N O T E For any questions regarding this Loan Portfolio Management – Year 2 intersession project, please contact: Michael “Mike” Wear [email protected] 402‐871‐9067 (cell)

For any administrative questions contact the Graduate School of Banking: 800‐755‐6440

1st Letter of Your

Last NameOriginal Due Date

10/15/18

Original Due Date

12/1/2018

Original Due Date

01/15/19

Original Due Date

03/01/19

A ‐ E ALM ‐ Year 2 Strategic Ldrshp Issues Retail Banking LPM ‐ Year 2

F ‐ L Strategic Ldrshp Issues Retail Banking LPM ‐ Year 2 ALM ‐ Year 2

M ‐ R Retail Banking LPM ‐ Year 2 ALM ‐ Year 2 Strategic Ldrshp Issues

S ‐ Z LPM ‐ Year 2 ALM ‐ Year 2 Strategic Ldrshp Issues Retail Banking

All Students

Extension Due Date Penalty Pts Assigned

AT TIME OF REQUEST

Extension Due Date Penalty Pts Assigned

AT TIME OF REQUEST

11/15/2018 0 2/15/2019 012/1/2018 5 3/1/2019 512/15/2018 10 3/15/2019 101/1/2019 20 4/1/2019 206/2/2019 30 6/2/2019 30

Extension Due Date Penalty Pts Assigned

AT TIME OF REQUEST

Extension Due Date Penalty Pts Assigned

AT TIME OF REQUEST

1/1/2019 0 4/1/2019 0

1/15/2019 5 4/15/2019 5

2/1/2019 10 5/1/2019 10

2/15/2019 20 5/15/2019 20

6/2/2019 30 6/2/2019 30

You will receive a word grade from the grader which will be recorded as points in your student record as listed below:

Exceptional 96‐100 ‐ recorded as 100 Good 75‐80 ‐ recorded as 80

Excellent 91‐95 ‐ recorded as 95 Acceptable 70‐75 ‐ recorded as 75

Superior 86‐90 ‐ recorded as 90 Needs Improvement Resubmission Required

Very Good 81‐85 ‐ recorded as 85

All projects MUST receive a grade of Acceptable or better in order to return to the next GSB Session.

GSB INTERSESSION PROJECT POLICIES

* Students may collaborate with fellow classmates when completing GSB projects to seek advice and/or to discuss ideas. However, students

must submit their own final project that is unique to them (i.e. data interpretation, summaries, recommendations, etc.). If any student(s) is/are

found to have plagiarized any or all of another student’s project (or submits a nearly identical project), all students involved will automatically

receive 50 penalty points, will be required to resubmit an acceptable project, and will be disqualified from receiving any honors recognition upon

graduation. If deemed necessary, GSB administration may also enforce additional disciplinary action up to and including removal from the

program.* Projects must be submitted on or before 11:59 pm of the due date to avoid penalty points.

* Students may request one 30‐day extension, per project, without penalty.* A limited number of additional extensions may be requested and will be granted in two week increments ‐ to the next 1st or 15th of the

month.

GRADING INFORMATION

* Penalty points will be assigned for each extension requested after the first extension. See the schedule of due dates

and penalties below.* Extensions are NOT automatically granted; for each extension needed an Extension Request Form ‐ found on the Intersession Project website ‐

must be completed on or before the due date that needs extending. Failure to meet this requirement could result in 30 penalty points being

assessed for that project.

* The absolute last due date for all project submissions is Sunday, June 2, 2019 at 11:59 p.m.

* If a student has any outstanding project(s) as of 11:59 p.m. on June 2 they will be cancelled from the program and will not be allowed to

attend the 2019 Session.

CLASS OF 2019 INTERSESSION PROJECT DUE DATES

* Once an extension is requested the penalty points are assessed and will not be removed if the project is submitted earlier than the new due

date

(Assigned at the 2018 GSB Session)

EXTENSION PENALTY POINTS

ORIGINAL DUE DATE OF 10/15/18 ORIGINAL DUE DATE OF 01/15/19

ORIGINAL DUE DATE OF 12/01/18 ORIGINAL DUE DATE OF 03/01/19

There is one additional project ‐ FiSim ‐ which will be available in mid‐April. However, you MUST first complete all

other projects before you will be able to work on the FiSim project.

The due date for FiSim is June 2, 2019 at 11:59 p.m. Absolutely NO extensions will be granted for FiSim.

1

LOAN PORTFOLIO MANAGEMENT

INTERSESSION PROJECT GUIDE

INSTRUCTIONS PROJECT OVERVIEW

HOW TO SUBMIT THE PROJECT GRADING

FREQUENTLY ASKED QUESTIONS WHERE TO FIND RATIOS

ADDITIONAL TIPS & RESOURCES

August, 2018

2

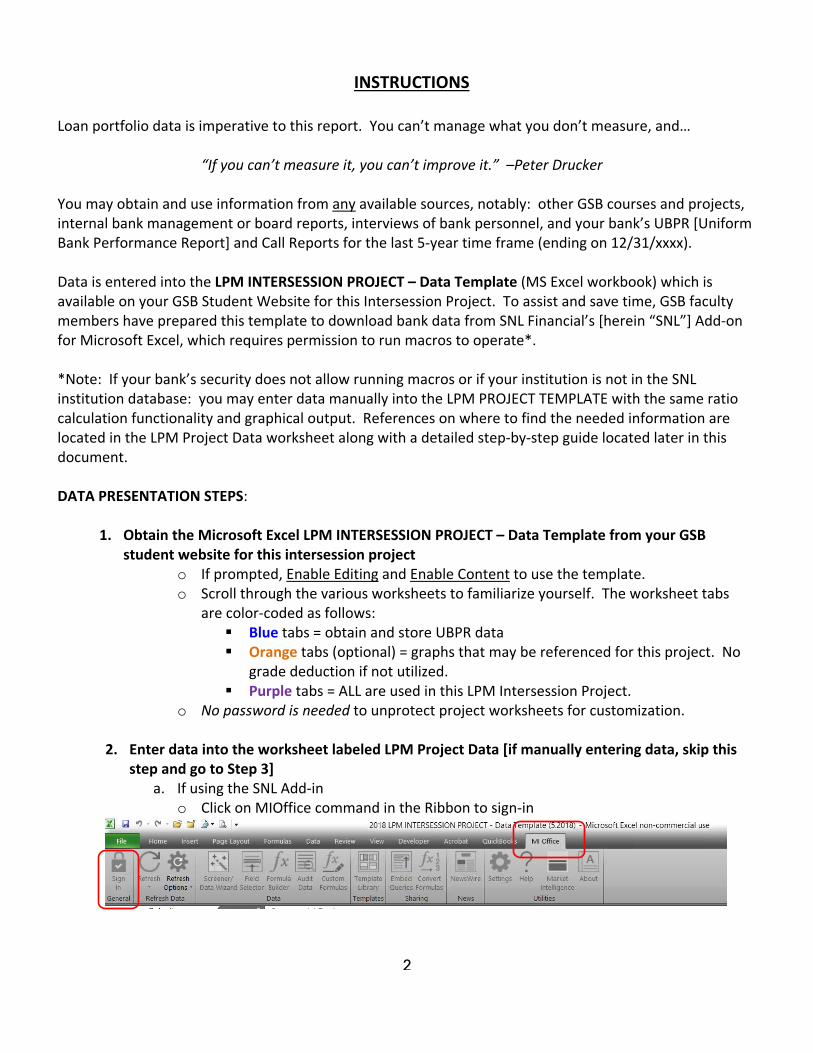

INSTRUCTIONS

Loan portfolio data is imperative to this report. You can’t manage what you don’t measure, and…

“If you can’t measure it, you can’t improve it.” –Peter Drucker You may obtain and use information from any available sources, notably: other GSB courses and projects, internal bank management or board reports, interviews of bank personnel, and your bank’s UBPR [Uniform Bank Performance Report] and Call Reports for the last 5-year time frame (ending on 12/31/xxxx). Data is entered into the LPM INTERSESSION PROJECT – Data Template (MS Excel workbook) which is available on your GSB Student Website for this Intersession Project. To assist and save time, GSB faculty members have prepared this template to download bank data from SNL Financial’s [herein “SNL”] Add-on for Microsoft Excel, which requires permission to run macros to operate*. *Note: If your bank’s security does not allow running macros or if your institution is not in the SNL institution database: you may enter data manually into the LPM PROJECT TEMPLATE with the same ratio calculation functionality and graphical output. References on where to find the needed information are located in the LPM Project Data worksheet along with a detailed step-by-step guide located later in this document. DATA PRESENTATION STEPS:

1. Obtain the Microsoft Excel LPM INTERSESSION PROJECT – Data Template from your GSB student website for this intersession project

o If prompted, Enable Editing and Enable Content to use the template. o Scroll through the various worksheets to familiarize yourself. The worksheet tabs

are color-coded as follows: Blue tabs = obtain and store UBPR data Orange tabs (optional) = graphs that may be referenced for this project. No

grade deduction if not utilized. Purple tabs = ALL are used in this LPM Intersession Project.

o No password is needed to unprotect project worksheets for customization. 2. Enter data into the worksheet labeled LPM Project Data [if manually entering data, skip this

step and go to Step 3] a. If using the SNL Add-in

o Click on MIOffice command in the Ribbon to sign-in

3

o Go to the first tab labeled: UBPR Input Cover (see below) o Follow these instructions very carefully:

Enable Macros Bank Name [select from pulldown list] Select the peer group for your bank and meaningfulness to your Bank and

your project: • National Peer Group (default) – Not best to use (too broad) • Asset Based Peer Group (better) – If your bank is an S-corp, keep

scrolling down and choose from that list • State Peer Group (better) – Compares with all commercial banks in

your state • Custom Peer Group (best) – To isolate your local competition, banks

with a similar portfolio mix, etc. (you will need to enter the SNL ID number for each)

Enter Period (default set-no need to change) Hit “Update” button. This loads your data. Be patient—this may take some

time, depending on connection speed. Optional:

• Directional indictors are helpful to spot strengths (weaknesses) and trends (default set to 20% variance)

• No need to hit “Print” as you will select project worksheets to print

b. Click on tab labeled: LPM Project Data

o Click on the Grey Box (pulls information into the purple LPM Intersession Project Data worksheet). This takes less than a minute.

o Go to Step 4

4

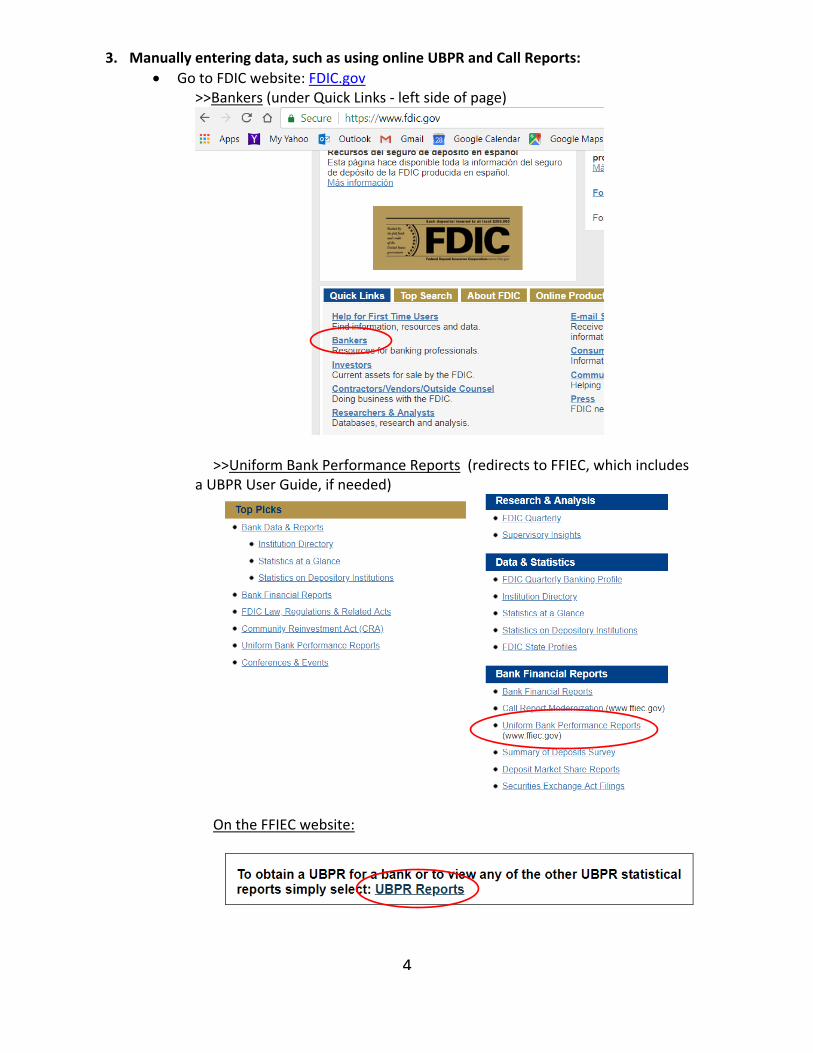

3. Manually entering data, such as using online UBPR and Call Reports: • Go to FDIC website: FDIC.gov

>>Bankers (under Quick Links - left side of page)

>>Uniform Bank Performance Reports (redirects to FFIEC, which includes a UBPR User Guide, if needed)

On the FFIEC website:

5

• Select a Report Type >>

o Uniform Bank Performance Report (UBPR) o Call (Call Report)

• DO NOT click on Grey Box on the LPM Project Data worksheet (you will lose your data!)

4. Save the Workbook (File >>> Save As) and complete your data input:

• Open the LPM Project Data worksheet • Scroll down to Loan Grades Section G:

o The Bank may not wish this information to be shared! Obtain permission to share this information; if not allowed, comment in the narrative report accordingly.

o Change “Special Mention” to your Bank’s designation, if you wish o Enter Your Bank’s criticized and classified dollar amounts for each period o Enter the nearest Regulatory Exam criticized (0 if not applicable),

classified, and loss (0 if not applicable) dollar amounts for each period • Scroll down to Reserve Information Section H:

o Amounts should be reviewed against management reports o You may wish to revise entries to re-calculate Loan Loss Reserve

adequacy ratios for extra-ordinary situations, such as: Acquisition of another bank or loan portfolio A single, large charge-off to determine ratios under normalized

conditions You can also ‘stress-test’ the adequacy ratios by increasing charge-

offs, if you wish • Scroll down to Industry Concentrations Section J:

o Enter loan portfolio concentrations for each time period (for comparison) o If information is difficult to obtain, complete for latest time period only. o Additional help is located in the Troubleshooting section of this Guide

• To Print: o Select only the Purple worksheet tabs o File >>> Print [to pdf for project submittal]

NARRATIVE REPORT STEP:

5. Open the LPM INTERSESSION PROJECT – Report Template from your GSB Intersession Project website

• Microsoft Word document • This will provide your Project Cover Page and preferred formatting of your narrative

report. • File >>> Save As

6

PROJECT OVERVIEW

Credit culture, loan policies, loan review, problem loan management, stress-testing, loan loss reserves, policy exception management, and credit administration are proactive methods of addressing portfolio risk. However, a system of tracking and monitoring loan quality indicators is necessary to insure these methods are successful. Your project is to prepare your assessment in a report that provides senior management and directors the necessary information concerning key trends in the portfolio and its significant segments.

Such reporting should indicate how the composition of the portfolio may be changing over time either as a result of changes in the market place or as a result of management initiatives.

At the same time, the reported information must include indicators of portfolio quality by

area to provide indications as to where credit policies or practices need to be tightened or strengthened.

The report should also include examples of how the bank identifies, quantifies, and

mitigates credit risk on a portfolio-wide level. Lastly, the report may include your recommendations for improvement in loan portfolio

risk management. This type of information permits management to efficiently allocate resources in order to provide an optimum return on the shareholders' investment. Your task in the intersession project will be to prepare such a report for the senior management and directors of your bank. This report may cover an individual bank or a bank holding company.

SUBMITTING YOUR PROJECT Your report should meet the following criteria and should be submitted as indicated. Failure to meet the Project requirements may result in grade reductions. The following guidelines should be adhered to when writing and presenting the Intersession Project to GSB: 1. The paper is preferred to be no more than 25 pages in length (it can and has been done very successfully in less); use Exhibits to attach examples, which do not count under the 25 page preference. 2. The project should be in PDF format only, preferably in a single file for the submitted project. a. To print to PDF in Excel: select ALL Purple tabs (worksheets). File >>> Print or Save to PDF. b. To print to PDF in Word: File >>> Print or Save to PDF.

7

Assemble your report in the following order (a single PDF file is preferred and very much appreciated!)

1. Cover Sheet [Word template provided] 2. Senior Credit Officer Memo [optional - see below] 3. Credit Project Data Presentation [Excel template provided] 4. Graphs, if not incorporated into the narrative report [Excel worksheets: LPM Graphs 1 - 8] 5. Bank Portfolio Rating [Excel worksheet] 6. Narrative Report [double-spaced please, template is provided] 7. Additional information or attachments [optional]

GRADING 1. All intersession projects must be submitted and receive a satisfactory grade prior to your submittal deadline date. It is recommended that you begin work on your projects promptly. By doing so, you will find the assignment easier, the educational value greater, and the complications fewer. 2. The Grade of “VERY GOOD” is considered well above average. 3. Do not expect to receive extended dialogue and commentary regarding the paper content or grading, the value should be derived from completion of the paper, not the grading or commentary. 4. Weighting of the Project Grading.

Presentation of the Data (30% of Grade) Data should be presented in the format shown in the Excel template. The graphs may be inserted

into the narrative instead of being printed separately—your preference. The LPM Project Data and the Bank Portfolio Rating worksheets must be submitted in their

entirety. You do not need to submit management reports outside of the data presentation. If you feel these

add value to the report, any non-public and proprietary information is held in the strictest of confidence.

If you cannot present certain data, make sure you describe in your narrative why it is not being presented. Review the FAQ Section located in this document for alternatives for missing data.

Interpretation and Analysis (70% of Grade) This is the most important part of your project. The gathering and presentation of the data is

meaningless in itself. Just like a credit analysis for a loan, the true value of the data lies in its interpretation.

“Get behind the Numbers.” “Tell a story.” What story does the data tell about the recent history and present condition of your bank’s loan portfolio and what is happening in the various parts of the loan portfolio? What lessons have been learned from the past and how has the bank made adjustments?

8

Identify and explain trends. Don’t just recite what the data is reporting. o Do not simply note significant changes, but explain them and their significance to the

bank. o Do not simply note what happened, but explain how it happened and what was done

after it happened. What LPM tools have been deployed for monitoring the portfolio quality and trends? Review the

materials from the LPM courses for examples. How effective have the tools been for your bank? What, if anything, has changed due to portfolio quality changes?

What recommendations would you suggest to help the bank strengthen its Loan Portfolio Management? If no recommendations, provide specific examples of what makes the LPM strong in your bank?

Do not include Non-Public, Private Information. Do not include your bank’s CAMELS rating, customer names, loan/account numbers, etc. [Yes, previous students have done this—warranting this advice.]

Bank Loan Portfolio Quality Rating o This worksheet will automatically calculate your bank portfolio rating. Review the

results of the Bank Portfolio Rating in your narrative. o Also comment on your bank’s quality rating components, including strong points and

weak points. Indicate what steps have been taken (or should be taken) to improve areas of weakness.

o The scale is time-tested, with grades based on over 15 years of GSB bank data research. Superior scores are tough, but achievable.

o The performance ratios and resulting rating are based only on a snapshot in time on public information.

o For smaller institutions (<$100M), one problem loan can certainly ‘move the needle.’ You may want to conduct a secondary “what if” rating based on resolution of the problem loan(s) or different scenarios.

o Other important factors, such as collateral coverage, earnings and capital, do not need to be addressed unless they relate to loan problems, reserve provisions, etc.

I’m Here to Help If you have a different question than presented here, issues obtaining information, or any other problems, please contact me:

Michael “Mike” Wear [email protected] [preferred method]

402-871-9067 (cell)

9

OPTIONAL - SENIOR CREDIT OFFICER MEMO As previously mentioned, this project is designed to be a report to senior management and/or directors. In addition to gaining insight from a senior credit officer for the content of the report, the attached letter requests his/her input on the value they see from your report. THIS IS OPTIONAL. If your report is critical of management or if a senior credit officer review is not available or utilized, please advise accordingly at the beginning of your narrative report. A request letter follows, that can be printed or emailed to the senior credit officer, if you wish to do so:

10

Date: August 15, 2018 To: Senior Credit Officer, Senior Lender or CEO Subject: Loan Portfolio Management - Intersession Project A member of your staff, as a second year student at the Graduate School of Banking has completed a Loan Portfolio Management Intersession Project involving an analysis of your bank’s loan portfolio, including composition and trends, as well as examples of how the bank identifies, measures, and manages credit risk on a portfolio-wide basis. Please review the student’s work and give them the benefit of your experience as it relates to bank priorities, credit culture, loan portfolio management and the implementation of credit administration. Interaction with bank management is an important component of this project and provides the student with valuable feedback and insight. Please write a brief memo for the student to submit with their completed Project. In this memo, please address the following four questions:

1. Does the student show an understanding of the composition, character, and trends of the loan portfolio?

2. Do you agree with the student’s assessments and conclusions?

3. Has the student successfully explained the events and circumstances which have affected the loan

portfolio over the analyzed time period?

4. Was this exercise beneficial in the professional development of the student? Thank you for participating in this Project and your assistance in the student’s professional development. Sincerely, Michael Wear Faculty and Section Leader Loan Portfolio Management Graduate School of Banking Madison, Wisconsin gsb.org

11

FREQUENTLY ASKED QUESTIONS Real Questions…Real Responses

General Topics

It’s been months since GSB, what again is the purpose of this intersession project?

In order to effectively manage a loan portfolio, there must be consistent and continuous monitoring of portfolio composition, portfolio trends and comparisons to peer group and industry standards. Too often, bank management is focused on the current portfolio status and comparisons are made only to the bank’s own loan portfolio. If only a minimal and inward focused analysis is done, subtle but important changes in the portfolio can be overlooked. The goal of the intersession project is to develop a complete and thorough analysis of your bank’s loan portfolio performance. This includes identifying portfolio trends and positive and negative changes in the portfolio. This is accompanied by a review of past due, non-accrual, non-performing, graded, and charged off loans. At the second year GSB resident session, the following components of loan portfolio management were identified: credit culture and credit policy, credit approval process, loan portfolio management, loan review, risk ratings, loan loss reserve adequacy, stress-testing, and credit administration. A thorough review of loan portfolio information will give you some indication as to how well your bank is doing in using these loan portfolio management tools. At the conclusion of the data presentation is an overall bank portfolio quality rating using 5 key ratios called quality categories. The score ratings are based upon the weighted quality categories and scaled based upon over a decade of actual scores of previous Loan Portfolio Management intersession projects submitted by GSB students. This intersession project requires a lot of data to be gathered. Isn’t there some other way to measure loan portfolio performance?

Analyzing a bank’s loan portfolio is based on numbers. I know of no other way to analyze portfolio performance. This would be similar to asking if we could analyze the financial performance of a company without having a financial statement prepared. Leverage previous GSB projects and assignments. The intersession project requires a lot of transcribing of data from various reports into a specified format. Couldn’t we just make copies of the UBPR and Call Reports and attach them to our narrative?

The Graduate School of Banking is a management school. Part of its goal is to broaden an understanding of information that can be used for management purposes and, to demonstrate how information can be put together in a concise summary fashion. If you were asked to prepare a management report for your board of directors, your Board would expect some sort of summary, not merely copied pages of data.

Writing the Narrative Portion

12

How long should the narrative portion of my intersession project be? As a general rule, if you have written less than 5 pages it’s certainly not enough and if you have written more than 25, you’ve probably included unnecessary or redundant information. Over time there will be changes and trends in your portfolio. The narrative should do a good job of identifying and explaining those changes and trends and how your bank compares to its peers. Note that this is a two-part process of identification followed by explanation. For example, if your non-accruals as a percentage of loans are considerably higher than your peer group, the first step is identification, but that needs to be followed by an explanation of why this is so. And why you believe this is acceptable or what are you doing to correct the situation. How should the narrative portion of the intersession project be structured?

Regardless of the structure you use, your narrative should begin with a few background paragraphs relating to your bank, such as history, ownership, local population, demographic factors, economic factors, and organizational structure and anything else that you feel might be useful background to explain the loan portfolio performance in your bank. Also include your position and background in banking. There is no specific or required structure for the narrative portion. However, students in the past have commonly used one of two approaches. First, start with Section A and go through the information section by section covering trends changes and peer comparisons as related to each section. This should be followed by a general summary of the identified information. The second approach would be to use the loan portfolio management tools we discussed in class as a framework and contrast and compare how well your bank is doing using those tools by analyzing the information in the data tables. Make the report your own. Note that you may need to discuss the portfolio information with your loan management staff, such as a senior loan officer, senior credit officer or CEO: as you may see a change or trend in the portfolio information, but you may not be aware of what caused it. This report gives you an opportunity to discuss and exchange ideas that you may not normally have. I work in a branch of a very large bank (or holding company). It will be difficult, if not impossible, for me to gain access to senior managers to discuss loan portfolio performance. How do I address this problem?

If you work for a large bank or holding company, you may need to interview other specialists in respective departments. Information concerning you bank’s loan portfolio can be found in your bank’s annual report. For publicly-owned institutions, there may also be information in the public filings (10Q, 10K) with the SEC. In addition, there should be a considerable amount of written information and analysis if your bank is a publicly traded company. It is important to try to get as much independent information as possible, rather than just depending on information from the bank’s annual report.

The intersession project references a review memo I am supposed to get from a senior officer of my bank. After completing my Project, I found that it is quite critical of bank management’s handling of the loan portfolio. What should I do?

13

The senior officer memo is optional. If asking your senior manager to review your intersession project would put your employment in jeopardy, you can certainly skip this part of the project requirements. The goal of the project is for you to write and honest, critical analysis of your bank’s portfolio. If you are not submitting a senior officer review, just note this in your written analysis.

Manually Gathering Information and UBPR Issues: The UBPR has many pages and many lines of data, how to I find the peer group information I need?

Attached is a detailed guide to help find data and how to calculate ratios. Page numbers may vary, depending on bank size; therefore, the guide references ratio names to look for.

Changing the Excel Template Our bank recently went through a merger (or acquisition) and I won’t have a consistent set of data for the five time periods required. What should I do?

If your bank is the surviving entity of a merger/consolidation, you need to gather the data before and after the merger/acquisition, and discuss the impact on the loan portfolio as part of your narrative. If your bank has been recently acquired by a larger organization, you may wish to base your report on the portfolio data from the acquiring bank. The Loan Management intersession project is in my last group of projects due. Can I change the reporting dates?

You may do so at your option and if there is real value to your bank. Also, be aware the Excel template’s spreadsheet is based on formulas that assume annual time frames. As such, you would have to change the formulas if you use interim time periods. To customize formulas or other changes to the Excel template, unprotect the worksheet (no password is required).

Sections A & B - Portfolio Composition: When I put in the peer group percentages for loan portfolio composition from the UBPR, they do not add to 100% or they total over 100%. Is there something wrong? The UBPR calculates percentages on average assets. Your peer group percentage composition may not add up to 100%. This is not a problem, as the main goal is to compare the percentage composition of the major parts of your loan portfolio to the UBPR.

In the second part of Section A, the template calculated percentages for my bank’s “Portfolio Composition (%)” do not match the percentages for my bank as shown on the UBPR. Why?

14

The UBPR percentages for portfolio composition for your bank, are based on an average of up to four quarterly reporting periods. The UBPR does this in order to smooth out any unusual spikes in portfolio information. The Excel template calculates the portfolio percentage composition for each individual period and does not average. As displayed, percentages are adequate for the Intersession project.

Section D – Delinquency What delinquency totals are to be included in this section? Enter only loans that are 30-89 days past due. Loans that are a) past due and on nonaccrual, or b) 90+ days past due and still on accrual are NOT included in this section as they are accounted for in Section F, “Nonperforming Assets”.

Section F - Nonperforming Assets In Section F of the Excel template, “Total Nonperforming Assets” does not include Renegotiated Loans and Other Real Estate Owned. Aren’t Renegotiated and OREO also troubled assets? The “Total Nonperforming Loans” number does not include “Renegotiated Loans” or OREO, because these two categories are not included in the UBPR definition of “Nonperforming”. However, an adverse trend in Renegotiated or ORE may be additional indicators of a poor loan portfolio quality and they should both be monitored. The Excel template provides the opportunity to track the total of Nonperforming, Renegotiated, and OREO. Any significant trends in this total should be noted and discussed in the narrative.

Section G – Loan Grades:

Where can I find my banks internal loan grading information and the regulatory classified loan information in the UBPR’s?

The internal and external loan grade amounts are not reported in the UBPR’s. You may need to obtain this information from others, such as your senior credit officer. This information is often considered proprietary information of the bank—check first before including. If, for whatever reason, you are unable to obtain the information about internal graded loans or examiner classified loans, there are two options:

1. Use non-accrual loans as a proxy for your internal adverse graded loans. This will mean you only have one adverse grade category (labeled “problem loans”) but it should be a reasonably good approximation.

2. Use total non-performing loans as a proxy for examiner classified loans. This is a reasonable approximation if the information is not available to you.

The term “Special Mention” is used for internally-criticized loans. In our bank, we call it something different. What should I do?

15

The line titles were simply used as examples. You should use whatever criticized grade designation is used in your bank. Our bank does not have a regulatory examination every year. What do I use for classified loan information for a year in which there was no examination? Once loans have been classified they generally are considered classified until they are paid off or the examiners declassify them. For example, loans classified in 2016 are still classified in 2017 even if no exam has taken place since. Therefore, the classified balances should be carried forward; in this example, using the latest exam classified balances.

Section H – Reserve Information

In Section H (Reserve Information), my ending balance is higher than in the UBPR. Make sure you are entering “Net Charge Offs” as a positive number. If you enter it as a negative, it will add to the reserve (as a Net Recovery). Of course, if you had Net Recoveries in a given time period (Recoveries were greater than Charge-Offs), you should enter the number as a negative.

Section I – Charge Offs

In Section I, how is the “Earnings Coverage of Net Charge-Offs” calculated? It is (pre-tax income for the year + loan loss provision for the year) divided by (net charge offs for the year). The calculation is done this way in order to match the way the UBPR calculates this ratio.

Section J - Concentrations My bank does not track concentration information. What should I do?

There is not enough time for you to go through and manually assign NAICS codes to most of your loans. Alternatives include pulling a list of your 20-50 largest loans and figure out the industry concentrations in those loans. This should result in a reasonable representation of your total concentrations.

Graphs

16

The lines or bars on some of my graphs exceed the top of the graph, or the scale of some of the graphs is so high that the lines or bars of the graphs are “scrunched” down on the bottom of the graph. The graphs are set to auto-scale. If a problem like this should happen: right-click on the axis and change the scale manually.

LOCATIONS OF DATA & SELECTED RATIO CALCULATIONS

IF MANUALLY ENTERING DATA: The location of the required peer information or ratio is listed first in the guides below. The UBPR or Call Report location of the needed item is listed second. UBPR page numbers can vary based on bank size: the best way to find the information is to look for the ratio’s title IN CAPS or use the ‘Find’ feature in Adobe [Ctrl F]. 1. Section A, Portfolio Composition numbers.

See: Call Reports Schedule RC-C. Note: the information required in Section A closely matches the format of Schedule RC-C, except a few lines on RC-C are added together when placed in Section A. Information on Unused Loan Commitments and Letters of Credit. See: Call Reports Schedule RC-L (#1-4).

For the second part of Section A, peer percentages for portfolio composition. See: UBPR Page 7 - 7A

2. Section B, Loans/Deposits Peer Group (%).

See: UBPR Page 10, NET LOANS & LEASES TO DEPOSITS. 3. Section B, Peer Capital/Assets (%).

See: UBPR Page 11, OTHER CAPITAL RATIOS - BANK EQ CAP + MIN INT TO ASSETS. 4. Section B, Pre Tax Operating Income.

See UBPR Page 2, PRETAX OPERATING INCOME (TE) 5. Section B, PEER ROA.

See: UBPR Page 1, PERCENT OF AVERAGE ASSETS: NET INCOME. 6. Section B, PEER ROE.

See: UBPR Page 11, PERCENT OF AVERAGE BANK EQUITY – NET INCOME. 7. Section C, Total Loan Yields (%).

See: UBPR Page 3, YIELD ON OR COST OF: TOTAL LOANS & LEASES (TE). 8. Section D, Delinquency Dollars (30-89 Days).

See: Call Report Schedule RC-N.

17

9. Section D, Total Delinquency Percentage Peer Group.

See: UBPR Page 8A-8B, TOTAL LN&LS - 30-89 DAYS P/D. 10. Section E, Total Nonaccrual Dollars.

See: Call Report Schedule RC-N. 11. Section E, Total Nonaccrual Percentage Peer Group.

See: UBPR Page 8A-8B, TOTAL LN&LS - NONACCRUAL. 12. Section F, 90 Days+ Delinquent, Still Accruing. See: Call Report Schedule RC-N. 13. Section F, Other Real Estate. See: Call Report RC-M - #3 14. Section F, Renegotiated Loans (also called “Restructured Loans”)

See: Call Report Schedule RC-C Part 1. Note: There are line numbers that run down the right hand margin. Restructured loans are the total of lines labeled M.1.xx.

15. Section F, Total Nonperforming Assets - Peer Percent of Loans.

See: UBPR Page 8A-8B, add 2 lines: (Other LN&LS-90+ Days P/D) + (-Nonaccrual)

16. Section F, Total Nonperforming Assets - Peer Percent of Capital. See: UBPR Page 8A-8B, Other Pertinent Ratios: NON-CUR LN&LS TO - EQUITY CAPITAL. 17. Section G, Internal & Regulatory Loan Grades – Dollars. See: Internal reports and regulatory examination reports 18. Section H, Loan Loss Reserve – Beginning Balance, Provision, and Net Charge-offs See: Call Report Schedule RI-B Part 2.

19. Section H, Reserve/Total Loans Peer Group (%).

See: UBPR Page 7, LN&LS ALLOWANCE TO TOTAL LN&LS. 20. Section H, Reserve/Nonaccrual Loans Peer Group (X).

See: UBPR Page 7, LN&LS ALLOWANCE TO NONACCRUAL LN&LS (X). 21. Section H, Reserve/Nonperforming Loans Peer Group (X).

See: UBPR Page 8A, Other Pertinent Ratios: NON-CUR LN&LS TO - LN&LS ALLOWANCE (X). Note: The number shown in the UBPR is the reciprocal of the ratio required for the Intersession Project. To convert, divide the UBPR number by 100 (this should give you a decimal), then divide that decimal into 1.00. The formula looks like this:

18

1.00 / (UBPR# / 100) = X.XXx For Example: 1.00 / (49.59 / 100) = 2.02x

Note: The calculated number is NOT a percent. It is a coverage ratio. That is, the reserve is (x) times larger than the total non-performing. In the example, one would say the loan loss reserve is 2.02 times larger than the amount of nonperforming loans. The higher this ratio is, the greater the ability of the reserve to absorb potential losses. For your own bank, if you have a small reserve and/or a large amount of nonperforming loans, this coverage ratio could be less than 1.00. In most cases it will be larger than 1.00.

22. Section H, Reserve/Net Charge-Offs Peer Group (x). See: UBPR Page 7, LN&LS ALLOWANCE TO NET LOSSES (x) 23. Section I, Net Charge-Offs/Total Loans Peer Group (%). See: UBPR Page 7, NET LOSS TO AVERAGE TOTAL LN&LS. 24. Section I, Earnings Coverage of Net Charge-Offs (x). See: UBPR Page 7, EARNINGS COVERAGE OF NET LOSSES (x) 25. Section J, Industry Concentrations. Use Total Capital as denominator. See: UBPR Page 4, TOTAL BANK CAPITAL & MIN INT

EVEN MORE HELP & RESOURCES I have never analyzed a bank’s loan portfolio before, is there information available that might help me?

A UBPR User Guide is available at http://www.ffiec.gov/ubprguide.htm. If your bank is audited by a CPA firm, they may have provided some information or analysis of various loan portfolio factors. If you are in a national bank, you might want to visit www.banknet.gov. It contains useful information and analysis tools; however, you must be a registered user to access it. I may need some reference books on how to write a professional paper. As this is a professional paper, proper grammar and spelling are important and reflect upon you. Take the time to review your work. A couple of writing guides that may be a resource to you: The Elements of Style (4th Edition) by William Strunk (Author), E. B. White (Author), Roger Angell (Foreword) The Hodges Harbrace Handbook (18th Edition) by Cheryl Glenn (Author), Loretta Gray (Author)

19

THREE THINGS TO REMEMBER:

• NEVER WRITE A “WHAT” WITHOUT A “WHY.”

• WHAT ARE THE “DRIVERS?” – GET BEHIND THE NUMBERS

• “TELL ME A STORY.”

Thank you for attending the Graduate School of Banking - Wisconsin