Embed Size (px)

Citation preview

Jerry E. Durham, CPA, CGFM, CFEAssistant Director, Research, Compliance, Contract AuditDivision of Local Government Audit

• GASB 77 is effective for the year ended June 30, 2017.– We should not have any abatements that relate to “Other

Governments”. The only one possible would be the State ofTennessee. (I can’t imagine this happening under anyscenario.)

– We should not have any abatements to report for ourcomponent units. (There could be a rare exception that Ican’t think of.)

– The tax abatement disclosure for the Primary Governmentshould also cover the School Department. I believe thismakes sense because the School Department cannot levytaxes, but is only allocated a portion of the County’s TaxLevy. In other words, the School Department does not have atax abatement.

• Collect– First and foremost, the Tax Abatement Agreement. This should be in

writing, but the county could be operating under some less thanformal or an oral agreement. Unwritten agreements are OK underGASB 77.

– Name of/type program. For example: Industrial Recruitment.– Purpose of the program. It should be in the agreement.– Type of Tax that is being abated. For example: Property Tax. (There

are other local taxes that could be abated but I doubt you will findany. Contact me if you find a tax abatement for a tax other thanproperty tax).

– What is the authority to abate the tax? This may not be a statestatute. It may be a County Commission Resolution or CityOrdinance.

– What are the criteria to be eligible for the tax abatement?– What mechanism is followed to abate the tax. Usually this will be

some type of process between the Property Assessor and Trustee.

• Collect– Ask if there are any “other” taxes that are being abated. (The Chart of

Accounts is a good place to look for other ideas. I don’t think we shouldexpect any).

– Ask whether there are any “claw back” or “recapture” provisions if thecompany should fail to perform under the agreement.

– “Commitments” made by the entity (industry) receiving the tax abatement.– Find out whether there are any “Commitments” the government has made

that accompany with tax abatement. For example, to build a road or abuilding or to maintain infrastructure, etc. Keep this in the note disclosureuntil the commitment is finished.

– The dollar amount of the tax abated for the current year (FYE 2017).– If a government has decided not to disclose “individual” abatements above a

certain dollar threshold, find out that threshold amount.– If a government omits tax abatement information due to legal prohibitions,

what information was omitted and by what authority.

• Perhaps even more interesting are the disclosures that are not required. For example:– The names of the entities that received a tax abatement– How an entity that received a tax abatement, spent or is spending

the money– The actual or potential benefits to the local government of granting

the tax abatement– GFOA has a best practice document that recommends using the letter of

transmittal for disclosure.– Number of Tax Abatement Agreements– Duration of Tax Abatements– Total Amount of Abatements over the duration of agreement

Brief Descriptive Information

Government’s Own Abatements

Other Government’s Abatements

Name of program

Purpose of program

Name of government

Tax being abated

Authority to abate taxes

Eligibility criteria

Abatement mechanism

Recapture provisions

Types of recipient commitments

Other Disclosures

Government’s Own Abatements

Other Government’s Abatements

Dollar amount of taxes abated

Amounts received or receivable from other governments associated with abated taxes

Other commitments by the government

Quantitative threshold for individual disclosure

Information omitted due to legal prohibitions

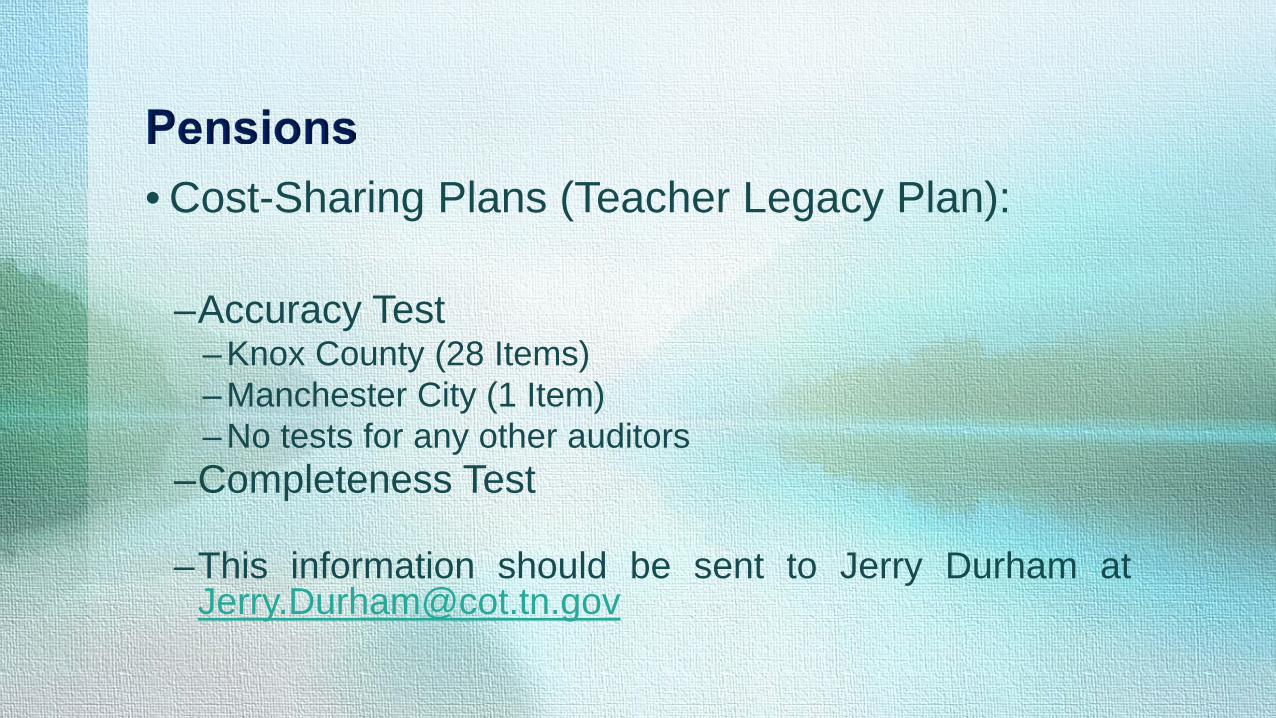

• Cost-Sharing Plans (Teacher Legacy Plan):

–Accuracy Test–Knox County (28 Items)–Manchester City (1 Item)–No tests for any other auditors

–Completeness Test

–This information should be sent to Jerry Durham [email protected]

•GASB 73, 78, and 82 are applicable for 2017

• GASB 73• Remember that GASB 24, On-BehalfPayments, applies when a nonemployergovernment fund (not in a special fundingsituation) makes payments for a Utility.

• Utilities should be making pensioncontributions since in Tennessee they arerequired to be self-sustaining.

• GASB 78• Applies mainly to Union Pension Plans• We have some Utilities that participate inUnion Plans

• GASB 68 does not apply to these types ofplans

• Pension expense will be based oncontributions

• GASB 82• Use “Covered Payroll” (i.e. Pensionable Payroll) rather than

• “Covered-Employee Payroll” (i.e. Total Payroll)

Required Supplementary Information

Note: Only 5 years are presented here; 10 years of information would be required

Net Pension Liability

GASB 82 Covered Payroll

• GASB 82• Does the government “pick-up” anypayments that the Plan officially designatesas employee contributions? If yes,paragraph 8 will apply to you

• The way you account for pick-up paymentscould affect your net pension liability

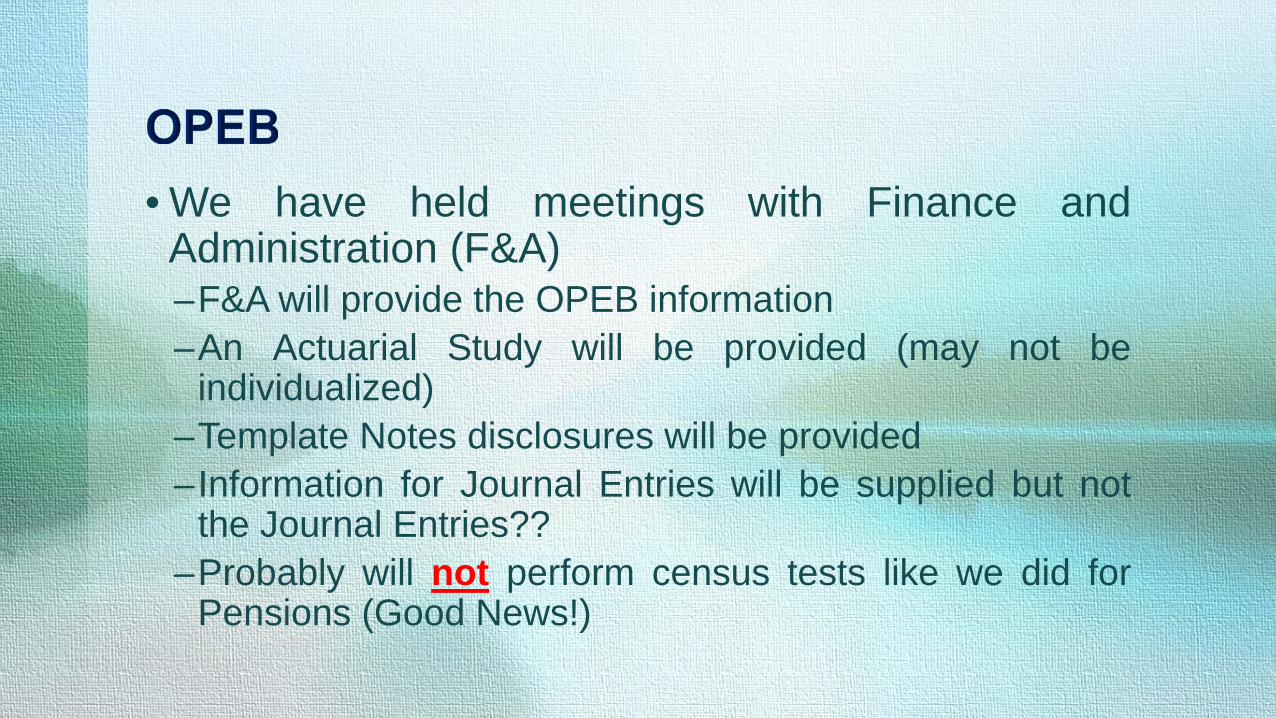

• We have held meetings with Finance andAdministration (F&A)–F&A will provide the OPEB information–An Actuarial Study will be provided (may not be

individualized)–Template Notes disclosures will be provided–Information for Journal Entries will be supplied but not

the Journal Entries??–Probably will not perform census tests like we did for

Pensions (Good News!)

• We have held meetings with Finance andAdministration (F&A) (cont’d)

–No new OPEB employees after July 1, 2015, soliabilities will eventually be decreasing

–Charter Schools are not separated at this point??–Still much to be decided! Stay tuned and hang on to

your seats!–I will prepare a memo when more final information is

available.

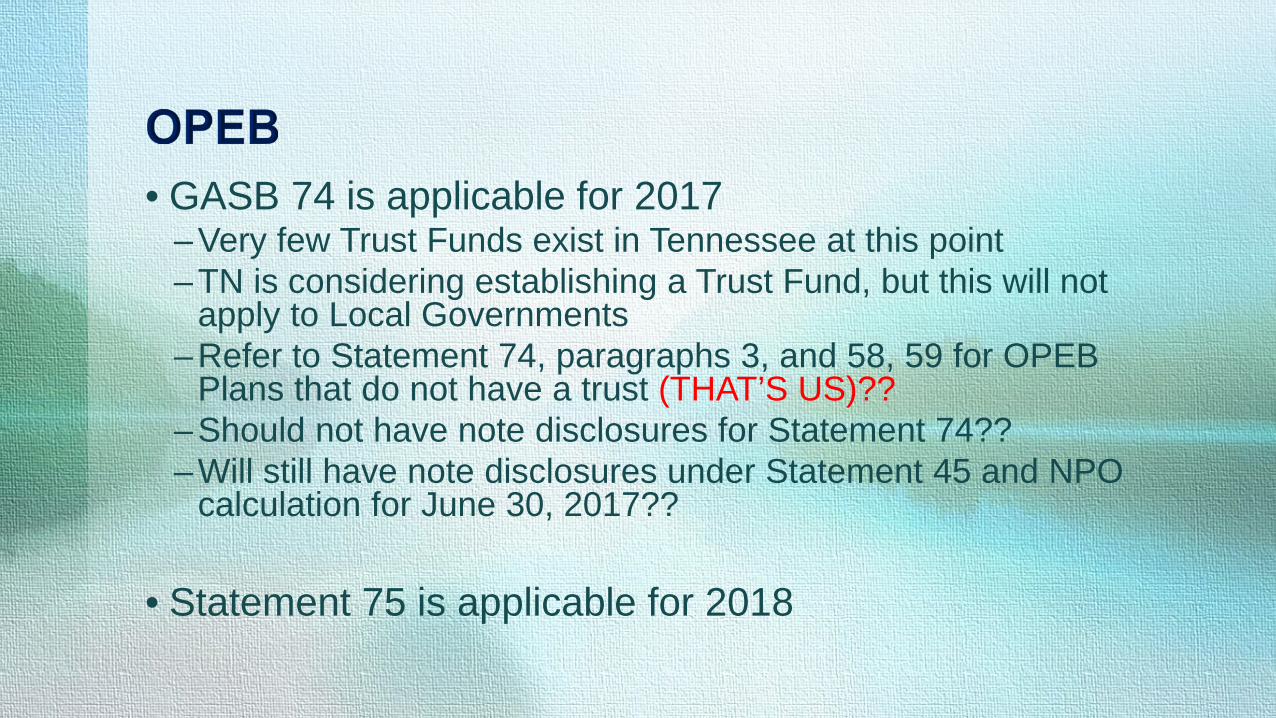

• GASB 74 is applicable for 2017–Very few Trust Funds exist in Tennessee at this point–TN is considering establishing a Trust Fund, but this will not

apply to Local Governments–Refer to Statement 74, paragraphs 3, and 58, 59 for OPEB

Plans that do not have a trust (THAT’S US)??–Should not have note disclosures for Statement 74??–Will still have note disclosures under Statement 45 and NPO

calculation for June 30, 2017??

• Statement 75 is applicable for 2018

• Should begin taking findings–Five components of internal control are required:

–Control Environment–Risk Assessment–Control Activities–Information and Communication–Monitoring

–Any finding will relate directly to Single Audit–Applies to every aspect of government regardless

of how small (i.e. remote sites)

Single Audit - Current Issues

• Uniform Guidance:–Smoothing (See Appendix 7 of the Compliance

Supplement)–GAGAS Findings [See Uniform guidance, 200.511(a)]–Separate Corrective action plan [See Uniform

Guidance, 200.511(c)]–All Grants Combined from all sources = over

$750,000 [See Uniform Guidance 200.331(f)]–23? new Q&As expected soon (or not!)

• The list was published in the TSCPA Journal for March/April 2017

• This list is also published on our website under “Guidance”

• https://www.comptroller.tn.gov/la/

• We have a new exposure draft for the Yellow Book– If you assist in the preparation of financial statements, this automatically

defaults to a significant threat that requires the use of the “conceptualframework” (3.89)

– Requirement to assign auditors “who at the time of the assignment” arecompetent to address audit objectives and their assigned roles. Applicationguidance provides explanations for Entry Level, Supervisory, and Partners andDirectors (4.02 – 4.10)

– Changes to CPE for auditors that perform Yellow Book audits. Four hoursupdate CPE each time GAO issues a new Yellow Book

– Several Changes that relate to quality control. (Chapter 5)– Waste is defined and guidance is provided for reporting waste in a Yellow Book

audit. (6.16 – 6.18) The guidance does not require procedures to detect waste,although though this is not specifically stated like it is for abuse.

• We have a new exposure draft for the Yellow Book (cont’d)– Auditors should consider potential internal control deficiencies when

developing the cause element of identified findings (6.20)– SSAE 18 is incorporated by reference into the Yellow Book (7.01)– SSARS 21, Section 90, is also incorporated by reference (7.01)– Performance Auditors should understand and document the significance of

internal control to the audit objectives (8.37 – 8.65)– Performance Auditors should report on the scope of their work on internal

control

• The Audit Manual will be updated by June 30, 2017

• Repeat Findings, Corrective Action Plan

• CCFO

• Contributions to Nonprofits by cities. Does not require thesubmission of an audit.

• GASB 84• Memo written to CPA’s dated October 2016.• Proposed Solution – Pension and OPEB Trust Funds:• The Division believes current standards support the reporting of a

fiduciary fund in the situations discussed above and we may question anentity’s financial statement presentation and a CPA’s audit response incertain obvious situations. However, the Division will continue to allowdiscretion when making determinations about fiduciary responsibility andfinancial statement presentation as it relates to Pension and OPEB TrustFunds until the effective date of the Exposure Draft. Our office will notrequire financial statements to be restated and resubmitted until theFiduciary Activities Exposure Draft is finalized into an AccountingStandard and that Standard becomes effective.

• Effective Date (Calendar Year 2019, Fiscal Year July 1, 2019 to June 30,2020

• GASB 84• The memo suggested that what Statement 84 requires is already

current guidance that is not being applied

• Must consider fiduciary component units. Control is not arequirement.

• Otherwise, control is the main criteria

• In general, control means (a) holds the assets; (b) has the ability todirect the use, exchange, or employment of the assets….

• AT-C 320

• If you cannot establish internal controls at the entity level formaterial transactions, you should obtain a SOC 1, Type 2 report.

• Auditors should finish their audits without the results of investigative reports.

• This happened to County Auditors 3 times last year.

• We include a sentence in our reports similar to the following,

• “An investigation is ongoing in the Typical County School Department’s payrolloperations. Findings, if any, resulting from the investigation will be included in asubsequent report.”

– Or, you could create your own statement such as,

• “A state investigation is ongoing in the Office of __________. We are cooperatingwith investigators as allowed under Government Auditing Standards paragraph4.09. Findings, if any, resulting from the state’s investigation will be included in asubsequent audit report.”

•New Investments Manual on the ourWebsite–We have a new investment manual on ourwebsite for counties.

–City statute is 6-56-106, TCA–The Investment Manual would be useful foreither Counties or Cities.

• What about LGIP? Should it be valued at Fair Value under GASB72 or amortized cost under GASB 79?

• Memo:– The Comptroller of the Treasury, Division of State Audit, audits compliance of

the Treasurer’s Local Government Investment Pool (LGIP) as part of the auditof the State Treasurer’s Office. For many years, Treasury’s LGIP has compliedwith SEC Rule 2a7. Now, Rule 2a7 has become the basis for the GAAPrequirements under GASB Statement 79. Treasury has advised State Auditthat it will follow GAAP and, therefore, present financial information for localgovernments, at Amortized Cost. State Audit gave an unmodified opinion onthe LGIP balances for June 30, 2016. Given the history of compliance withRule 2a7, and the Division of State Audit’s opinion, Firm Name will utilize theamount presented on the statement of account from LGIP as the amount ofassets invested at June 30, 2017. [Include evidence of LGIP’s compliance withGAAP.]