Embed Size (px)

DESCRIPTION

Net Present Value and Other Investment Rules. Percent of CFOs who say they use the following rules to evaluate projects. What Makes for a Good Investment Rule?. Recognize the time value of money Should rely solely on expected future cash flows and the opportunity cost of capital - PowerPoint PPT Presentation

Citation preview

Net Present Value and Other Investment Rules

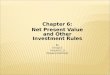

Percent of CFOs who say they use the following rules to evaluate projects

2

3

What Makes for a Good Investment Rule?

1. Recognize the time value of money2. Should rely solely on expected future cash

flows and the opportunity cost of capital-Manager discretion & accounting numbers, are easy to manipulate

3. Want to be able to rank projects, and evaluate portfolios of projects

4

Potential Investment Criteria

Payback Period Average Accounting Return IRR NPV

5

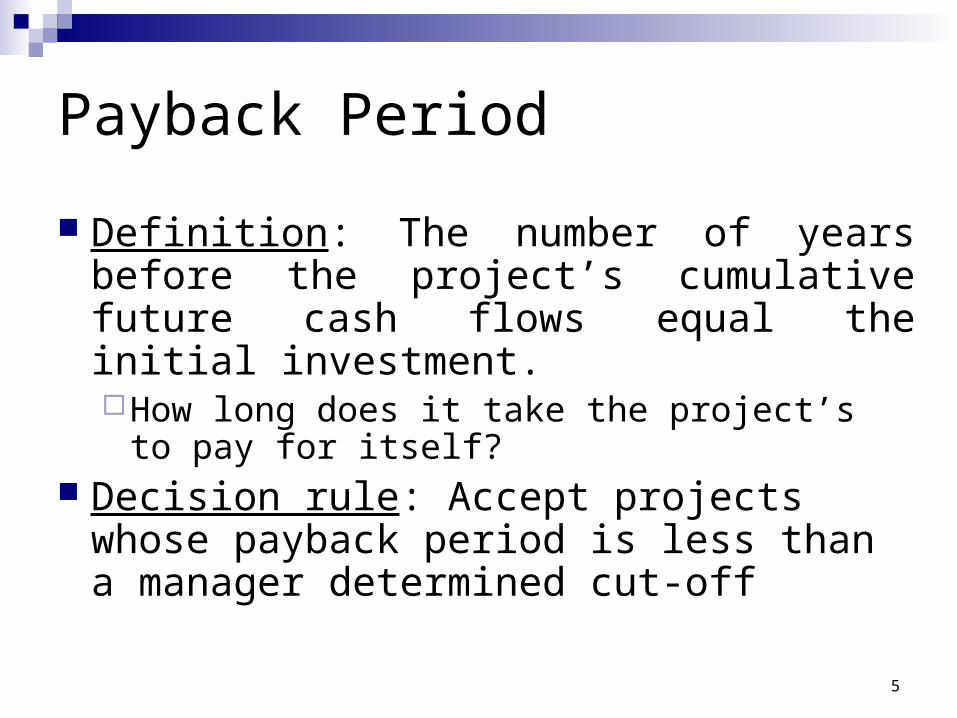

Payback Period

Definition: The number of years before the project’s cumulative future cash flows equal the initial investment.How long does it take the project’s to pay for itself?

Decision rule: Accept projects whose payback period is less than a manager determined cut-off

6

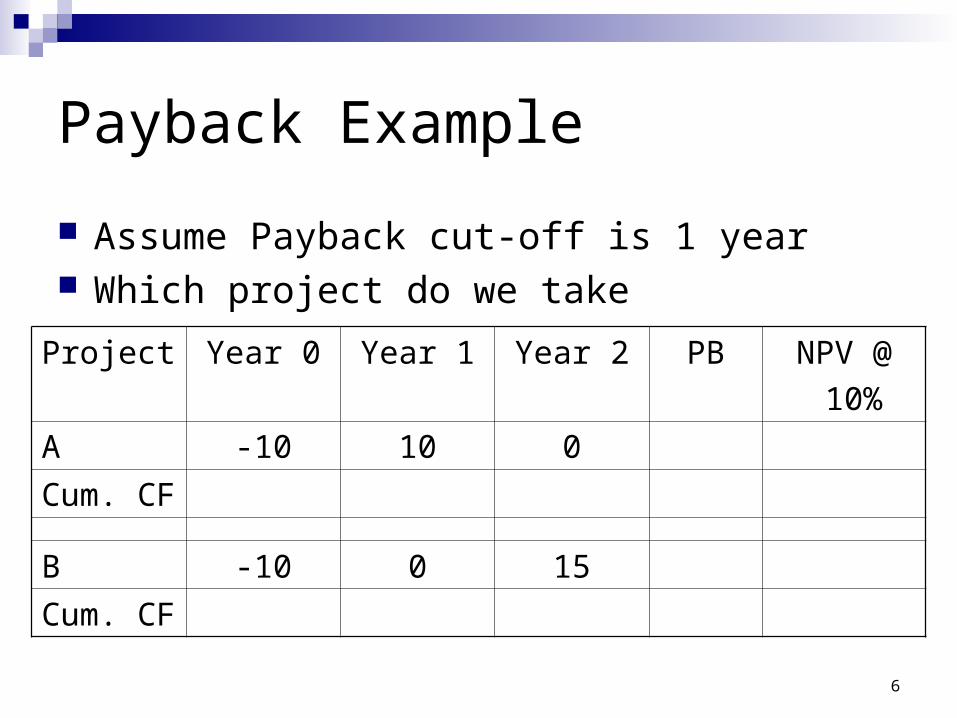

Payback Example

Assume Payback cut-off is 1 year Which project do we take

Project Year 0 Year 1 Year 2 PB NPV @

10%

A -10 10 0

Cum. CF

B -10 0 15

Cum. CF

7

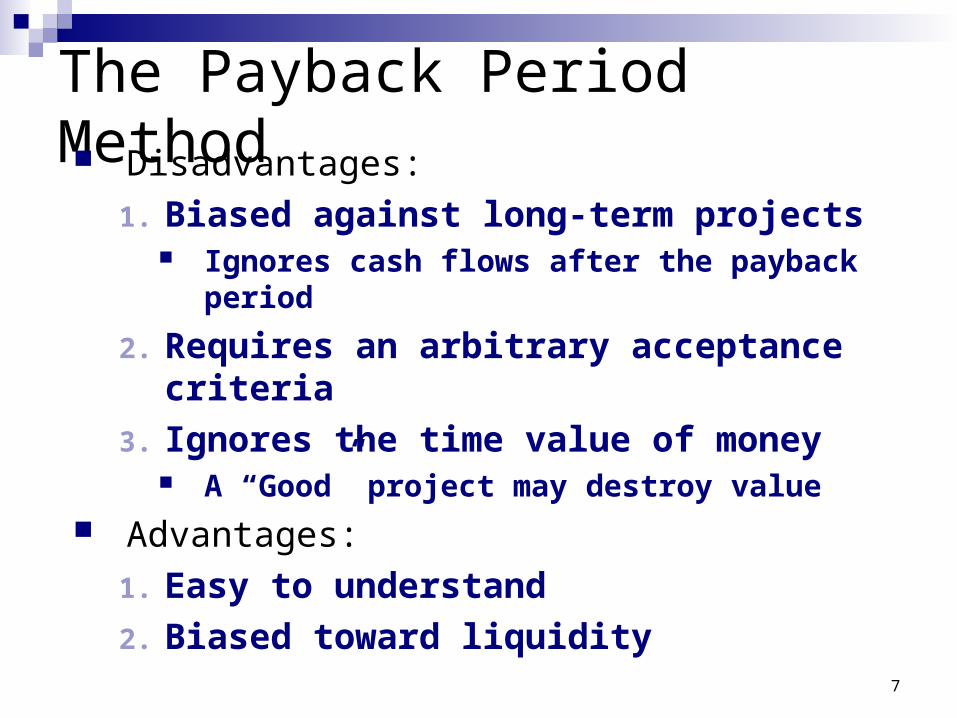

The Payback Period Method Disadvantages:

1. Biased against long-term projects Ignores cash flows after the payback period

2. Requires an arbitrary acceptance criteria

3. Ignores the time value of money A “Good” project may destroy value

Advantages:

1. Easy to understand

2. Biased toward liquidity

8

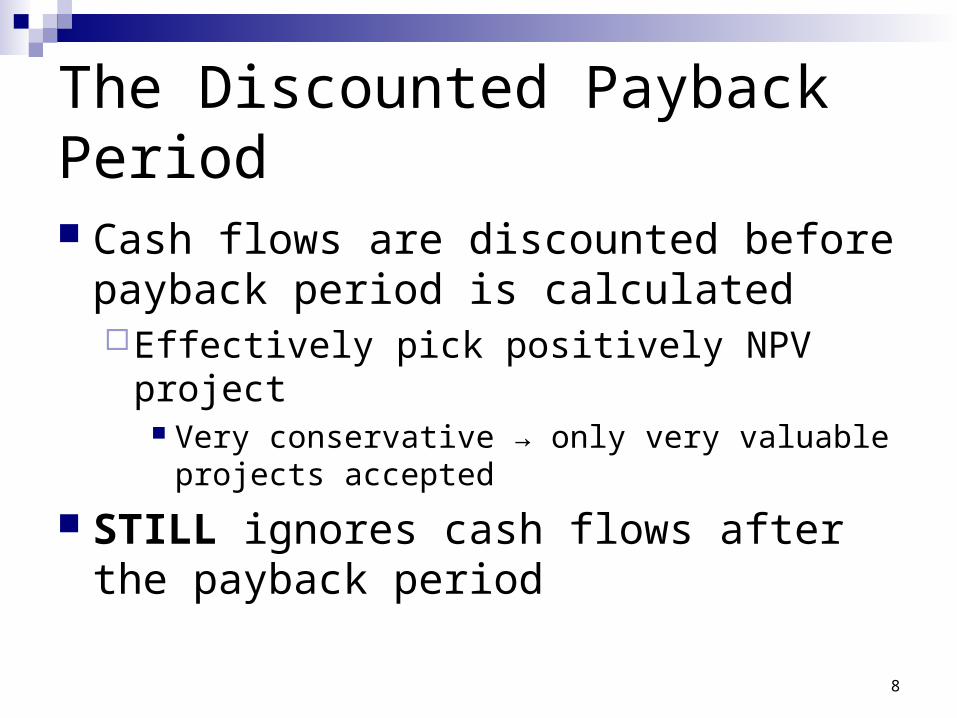

The Discounted Payback Period

Cash flows are discounted before payback period is calculatedEffectively pick positively NPV project

Very conservative → only very valuable projects accepted

STILL ignores cash flows after the payback period

9

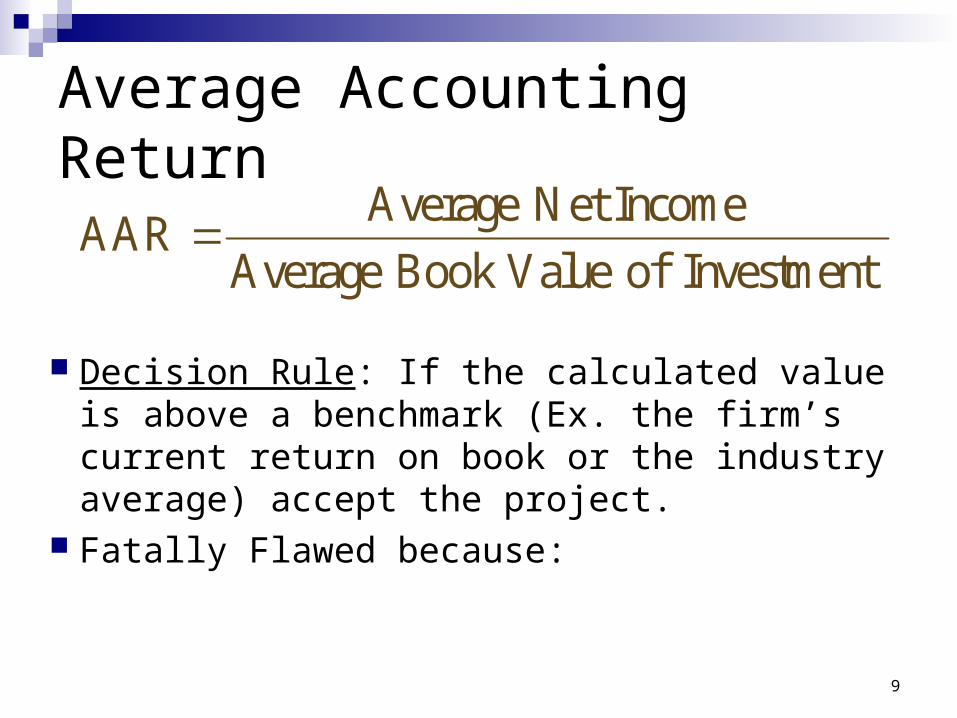

Average Accounting Return

Decision Rule: If the calculated value is above a benchmark (Ex. the firm’s current return on book or the industry average) accept the project.

Fatally Flawed because:

Investment of ValueBook Average

IncomeNet AverageAAR

10

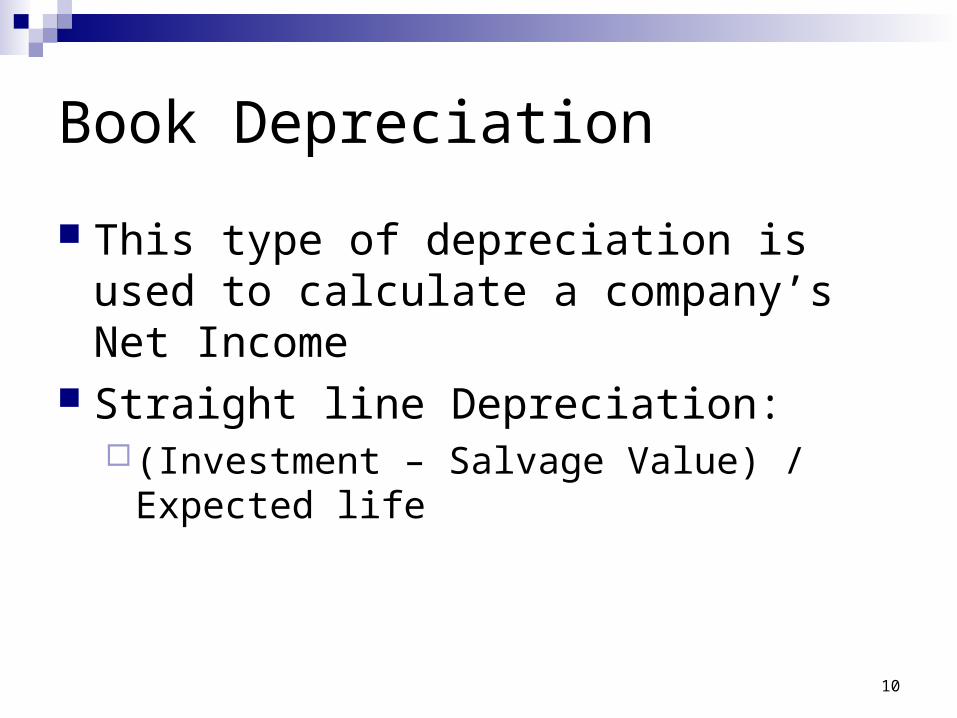

Book Depreciation

This type of depreciation is used to calculate a company’s Net Income

Straight line Depreciation: (Investment – Salvage Value) / Expected life

11

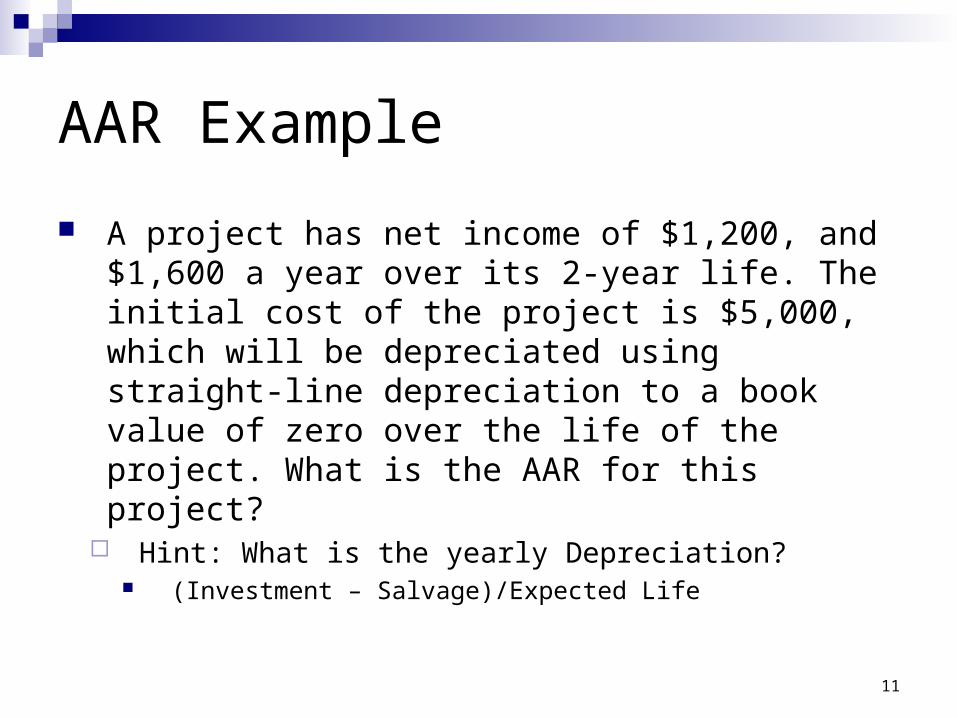

AAR Example

A project has net income of $1,200, and $1,600 a year over its 2-year life. The initial cost of the project is $5,000, which will be depreciated using straight-line depreciation to a book value of zero over the life of the project. What is the AAR for this project?

Hint: What is the yearly Depreciation? (Investment – Salvage)/Expected Life

12

AAR example A project has net income of $1,200, and $1,600 a year over its 2-year life. The

initial cost of the project is $5,000, which will be depreciated using straight-line depreciation to a book value of zero over the life of the project. What is the AAR for this project?

AAR =

0 1 2 Ave

NI

BV

13

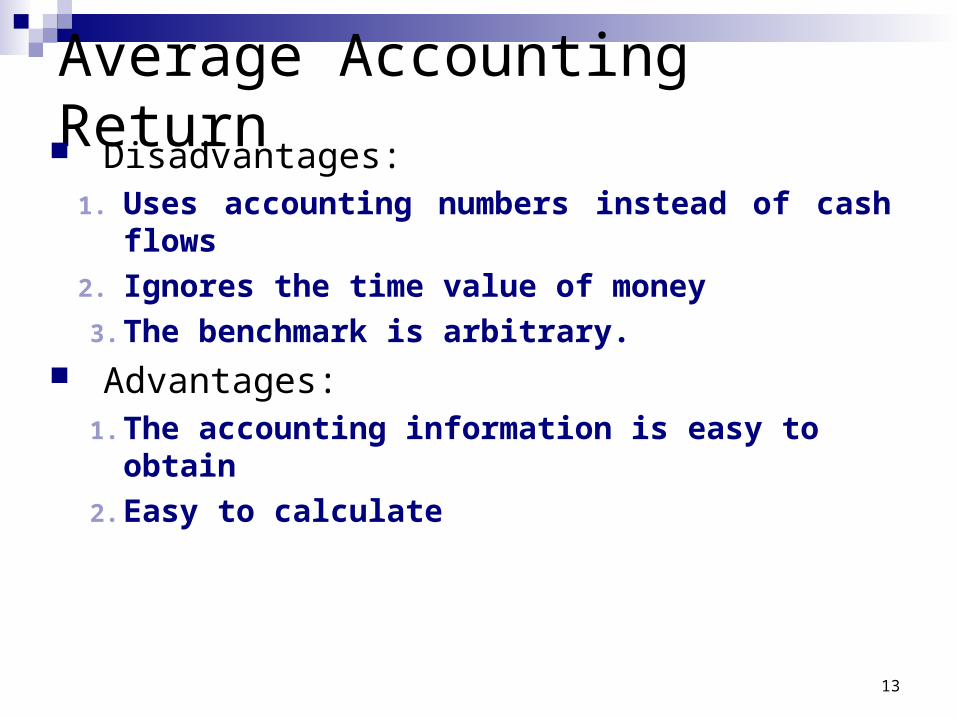

Average Accounting Return Disadvantages:

1. Uses accounting numbers instead of cash flows

2. Ignores the time value of money

3. The benchmark is arbitrary. Advantages:

1. The accounting information is easy to obtain

2. Easy to calculate

14

Internal Rate of Return (IRR)

Definition: It is the discount rate that makes a project’s NPV equal 0.

Decision Rule: Accept all projects with IRR’s greater than the opportunity cost of capital.

15

IRR’s Underlying Assumptions

All intermediate cash flows can be reinvested at the IRRIs this reasonable?

That short-term interest rates are equal to long-term interest ratesDoes not address which to use if they are not equal

16

IRR Notes To find the IRR of a project lasting t years, solve

the following equation:C0+C1/(1+IRR)+C2/(1+IRR)2+….+Ct/(1+IRR)t=0

NPV > 0 implies that IRR > Op CostIRR > Op Cost DOES NOT IMPLY that NPV > 0

IRR assumes that causality goes both ways

17

IRR & NPV Investment Example A firm has a project that requires an initial

investment of $10m. In the first year, it will return $12m, what is the IRR?

If r=10% do we accept the project based on IRR and NPV?

18

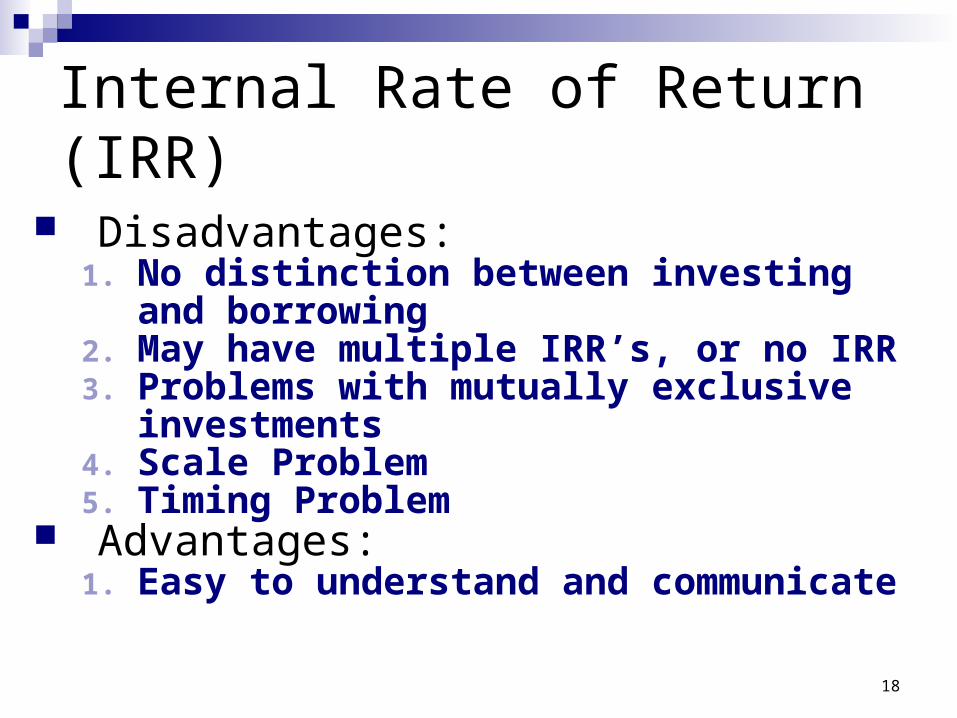

Internal Rate of Return (IRR)

Disadvantages:1. No distinction between investing and borrowing2. May have multiple IRR’s, or no IRR 3. Problems with mutually exclusive investments4. Scale Problem5. Timing Problem

Advantages:1. Easy to understand and communicate

19

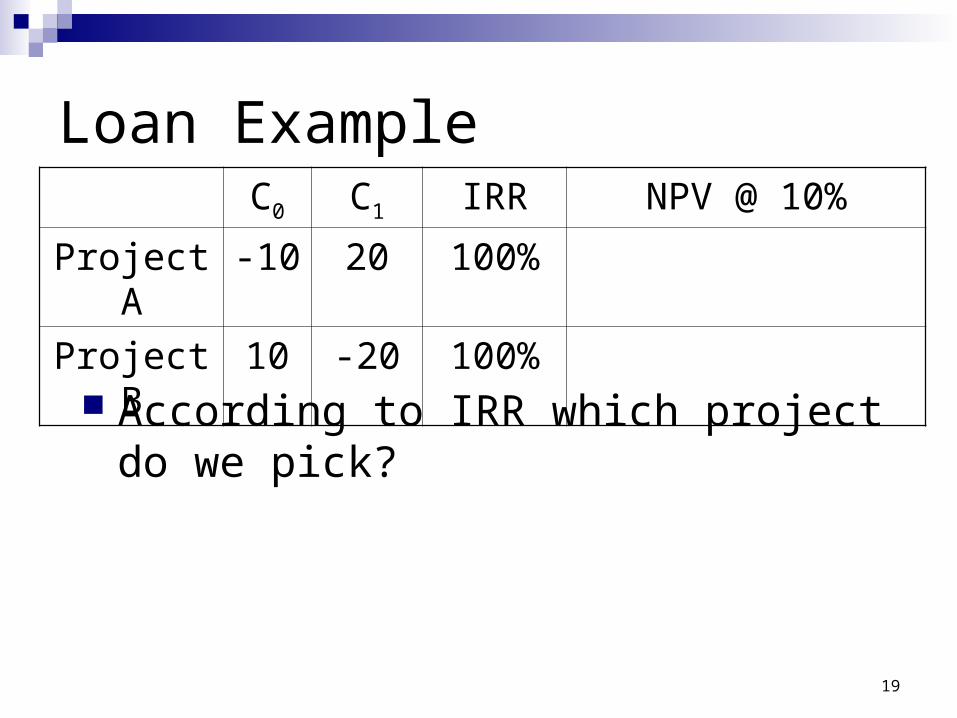

Loan Example

According to IRR which project do we pick?

C0 C1 IRR NPV @ 10%

Project A -10 20 100%

Project B 10 -20 100%

20

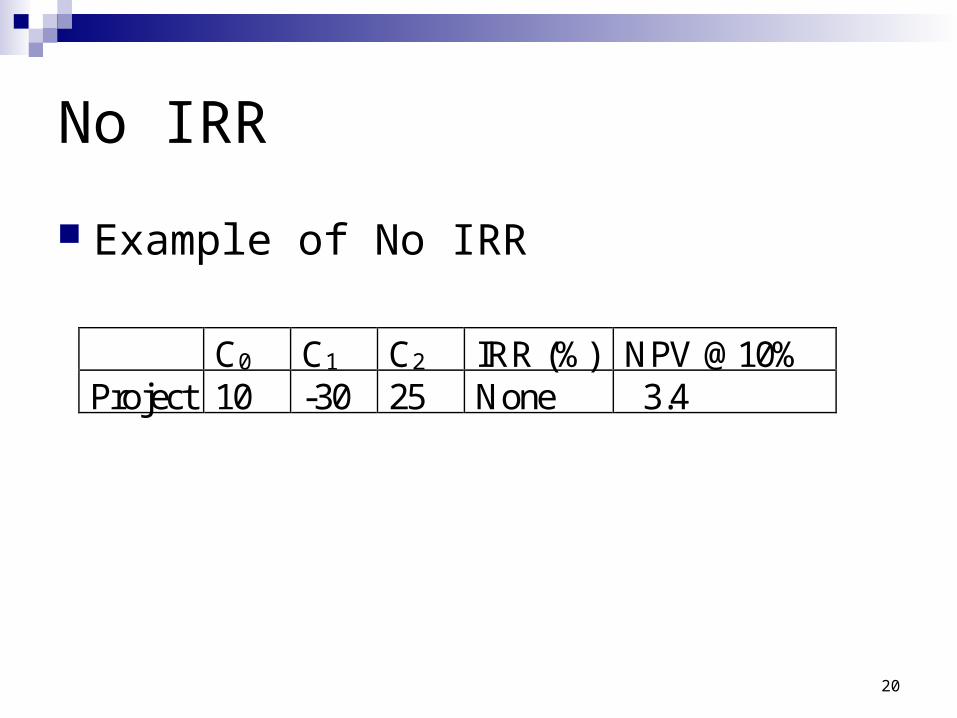

No IRR

Example of No IRR

C0 C1 C2 IRR (%) NPV @10% Project 10 -30 25 None 3.4

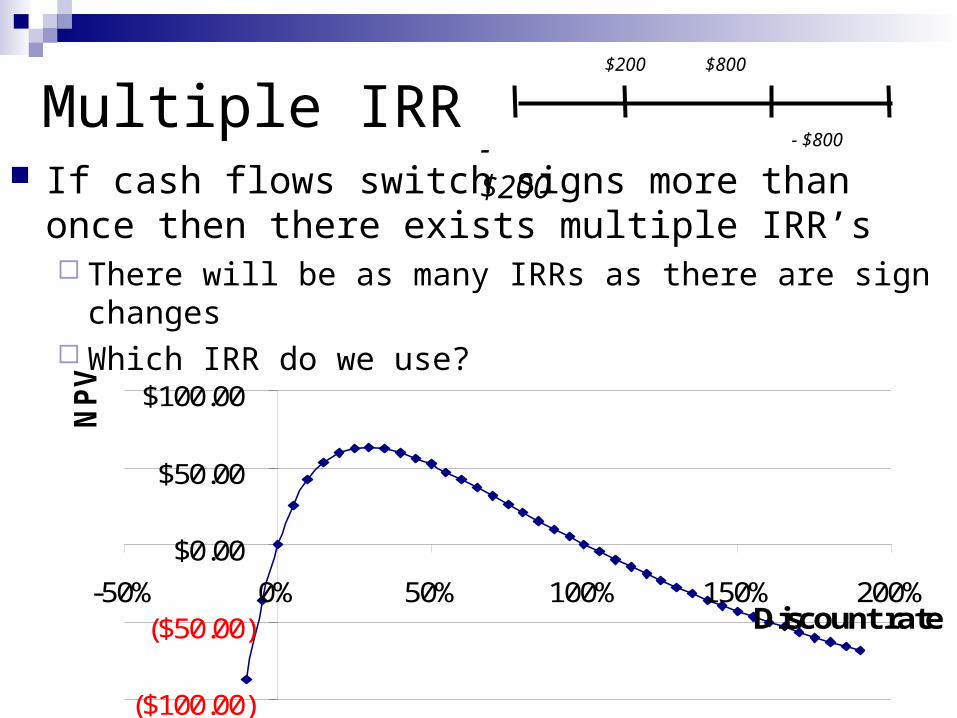

Multiple IRR If cash flows switch signs more than once then there exists

multiple IRR’s There will be as many IRRs as there are sign changes Which IRR do we use?

$200 $800

-$200

- $800

($100.00)

($50.00)

$0.00

$50.00

$100.00

-50% 0% 50% 100% 150% 200%Discount rate

NP

V

22

The Scale Problem

Would you rather make 100% or 50% on your investments?

23

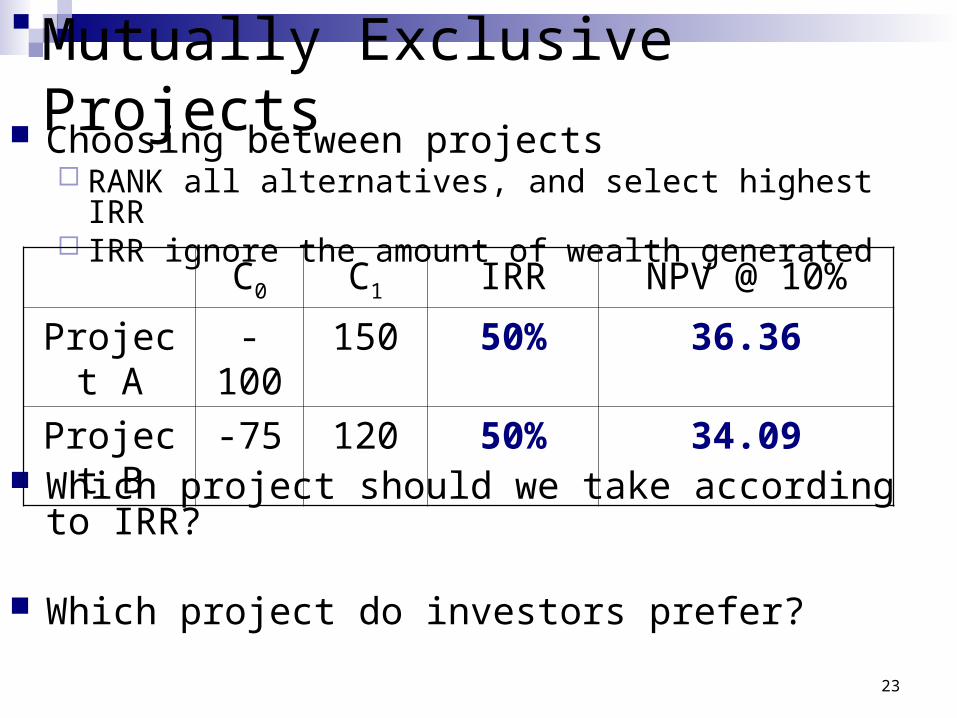

Mutually Exclusive Projects Choosing between projects

RANK all alternatives, and select highest IRR IRR ignore the amount of wealth generated

Which project should we take according to IRR?

Which project do investors prefer?

C0 C1 IRR NPV @ 10%

Project A -100 150 50% 36.36

Project B -75 120 50% 34.09

24

Resource constraint The firm has $100 to invest, what should it buy?

IRR: NPV:

Project C0 C0 C0 IRR NPV 10%

A -100 300 50 216% $210

B -50 50 200 156% $160

C -50 50 150 130% $120

25

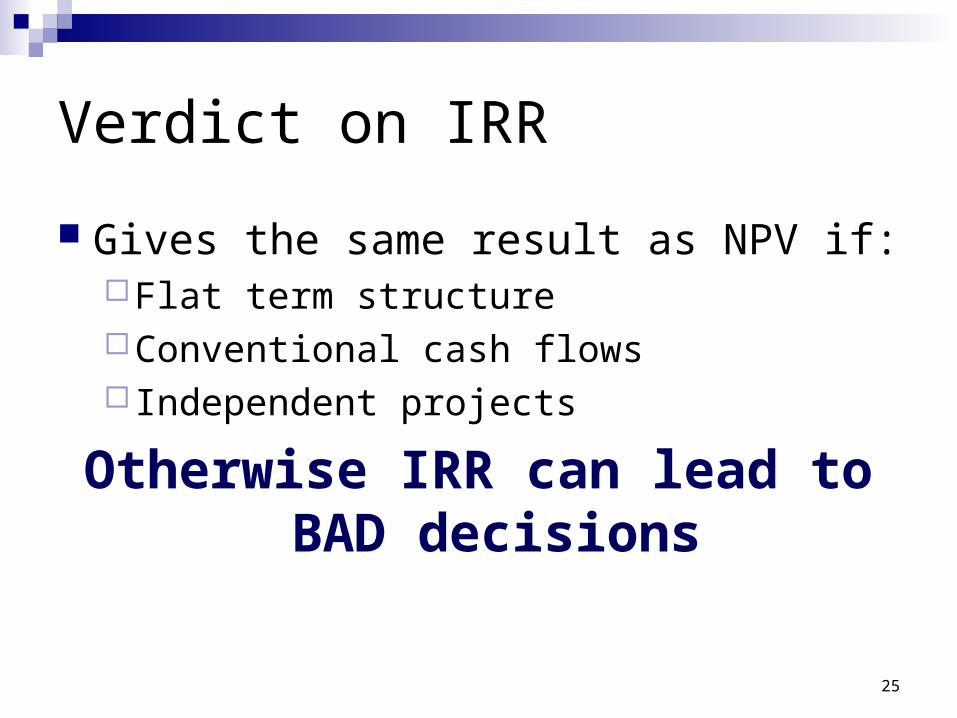

Verdict on IRR

Gives the same result as NPV if:Flat term structureConventional cash flowsIndependent projects

Otherwise IRR can lead to BAD decisions

26

The Profitability Index (PI)

Minimum Acceptance Criteria: Accept if PI > 1

Ranking Criteria: Select alternative with highest PI

Investment Initial

FlowsCash Future of PV TotalPI

27

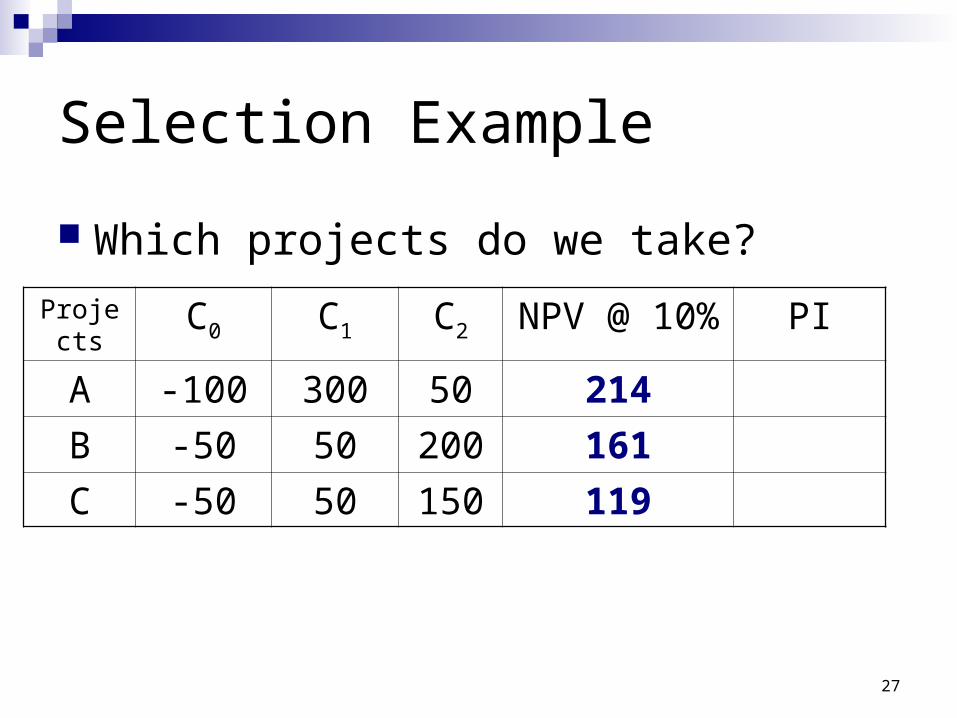

Selection Example

Which projects do we take?

Projects C0 C1 C2 NPV @ 10% PI

A -100 300 50 214

B -50 50 200 161

C -50 50 150 119

28

The Profitability Index Disadvantages:

1. Problems when there are additional constraintsUse linear or integer programming

Advantages:1. When funds limited (Capital Rationing),

provides better rankings than NPV

2. Easy to understand and communicate

29

The Net Present Value (NPV) Rule

Net Present Value (NPV) =

Total PV of future CF’s + Initial Investment Estimating NPV:

1. Estimate future cash flows: how much? and when?

2. Estimate discount rate

3. Estimate initial costs

Minimum Acceptance Criteria: Accept if NPV > 0 Ranking Criteria: Choose the highest NPV

30

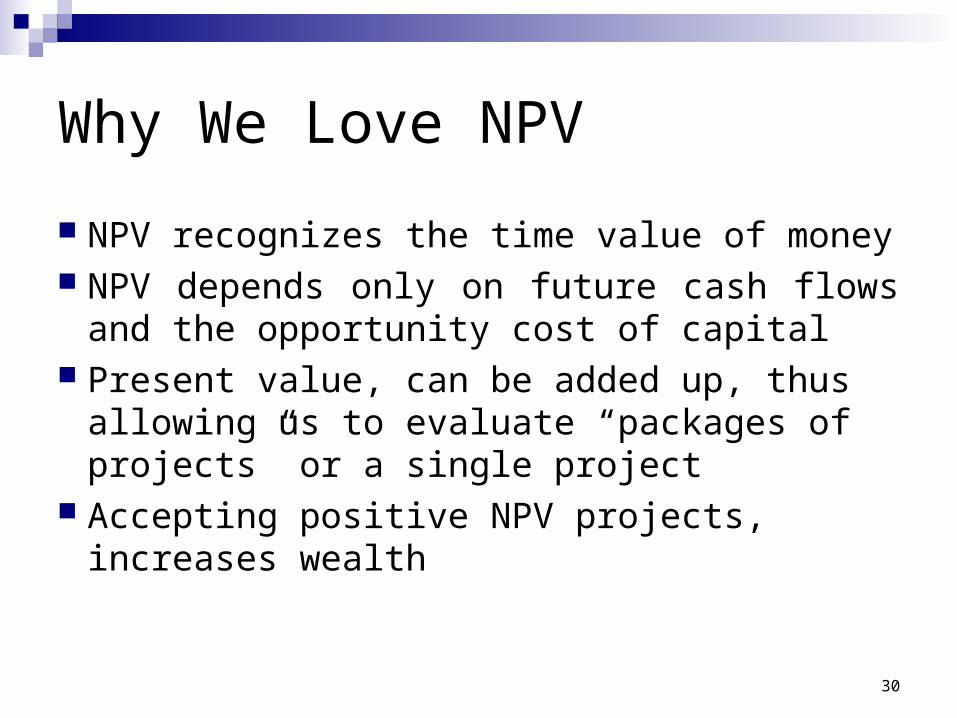

Why We Love NPV

NPV recognizes the time value of money NPV depends only on future cash flows and the

opportunity cost of capital Present value, can be added up, thus allowing us to

evaluate “packages of projects” or a single project Accepting positive NPV projects, increases wealth

31

Capital Budgeting in Practice

Varies by industry The most frequently used technique for large

corporations are: IRR or NPVHowever, many companies also consider payback

32

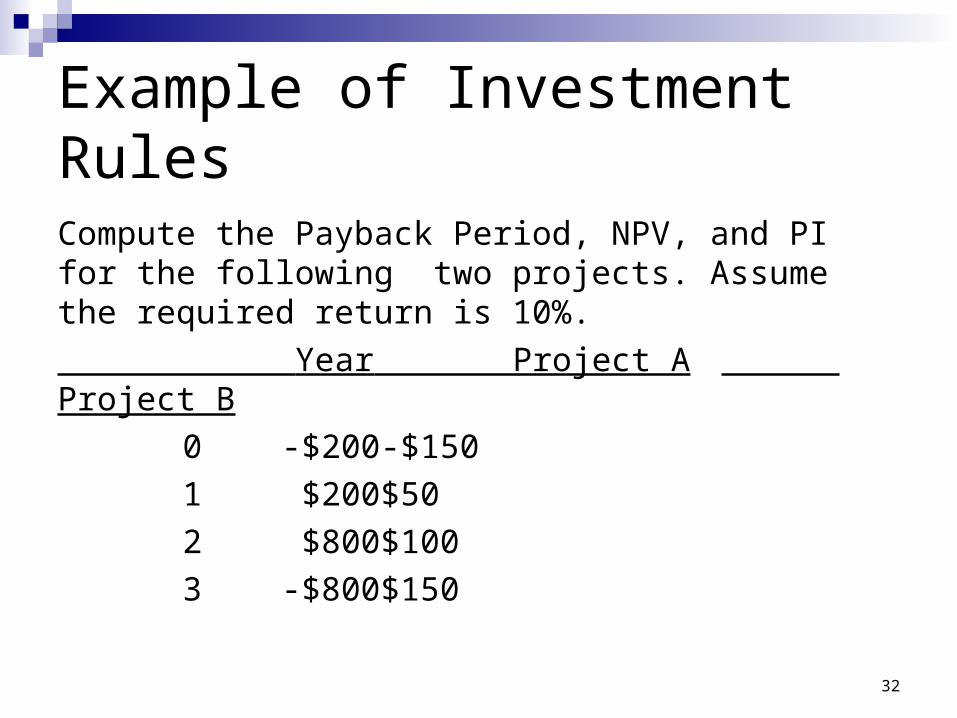

Example of Investment Rules

Compute the Payback Period, NPV, and PI for the following two projects. Assume the required return is 10%.

Year Project A Project B

0 -$200 -$150

1 $200 $50

2 $800 $100

3 -$800 $150

33

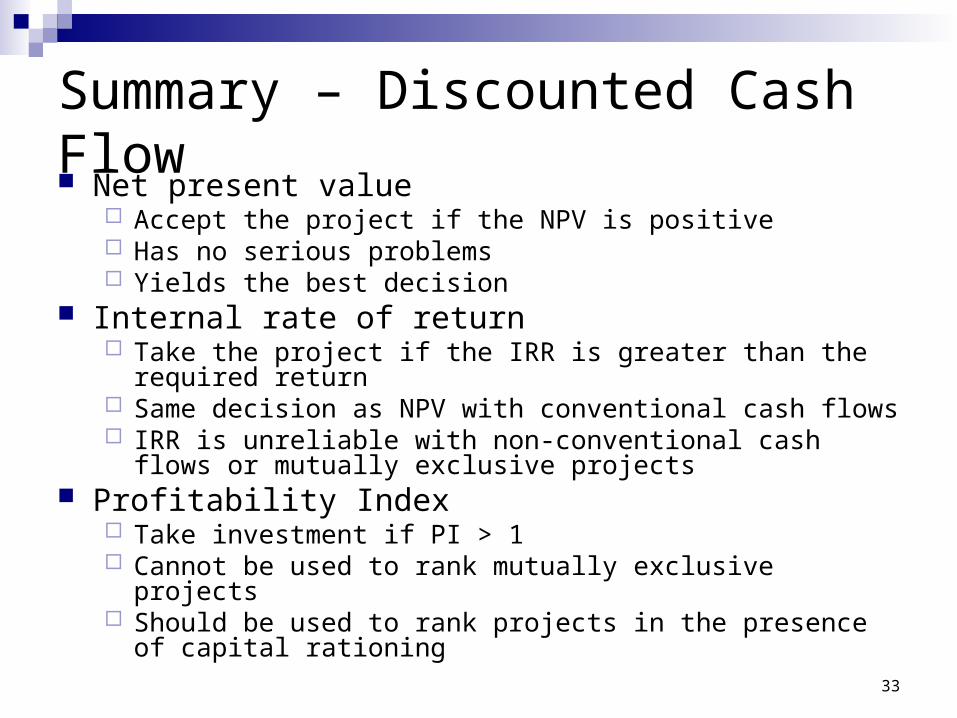

Summary – Discounted Cash Flow Net present value

Accept the project if the NPV is positive Has no serious problems Yields the best decision

Internal rate of return Take the project if the IRR is greater than the required return Same decision as NPV with conventional cash flows IRR is unreliable with non-conventional cash flows or mutually

exclusive projects Profitability Index

Take investment if PI > 1 Cannot be used to rank mutually exclusive projects Should be used to rank projects in the presence of capital rationing

34

Summary – Payback Criteria Payback period

Length of time until initial investment is recovered Take the project if it pays back in some specified period Does not account for time value of money, and there is an

arbitrary cutoff period

Discounted payback period Length of time until initial investment is recovered on a

discounted basis Take the project if it pays back in some specified period There is an arbitrary cutoff period

35

Summary – Accounting Criterion

Average Accounting ReturnMeasure of accounting profit relative to book

valueSimilar to return on assets measureTake the investment if the AAR exceeds some

specified return levelSerious problems and should not be used

36

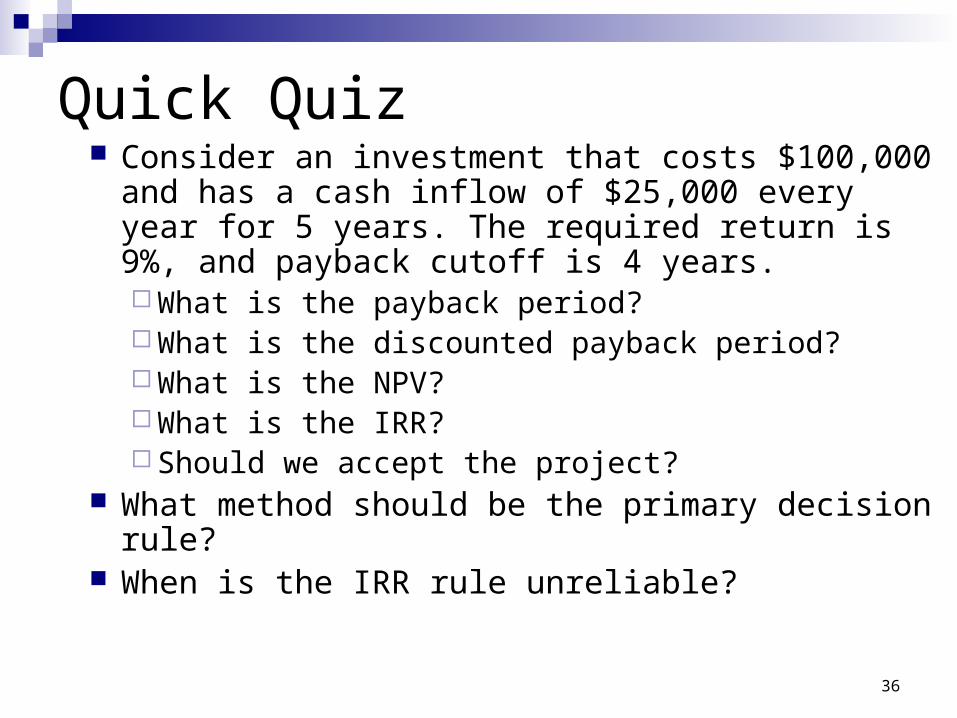

Quick Quiz Consider an investment that costs $100,000 and has a

cash inflow of $25,000 every year for 5 years. The required return is 9%, and payback cutoff is 4 years. What is the payback period? What is the discounted payback period? What is the NPV? What is the IRR? Should we accept the project?

What method should be the primary decision rule? When is the IRR rule unreliable?

Why We Care

Help you develop your finance intuition Showing you common mistakes, so that you

won’t make those mistakes

37