Embed Size (px)

Citation preview

MOODYS.COM

6 JUNE 2016

NEWS & ANALYSIS Corporates 2 » MGM Resort's Acquisition of Outstanding Stake in Borgata and

Sale/Leaseback Are Credit Positive » Jazz Pharmaceuticals' Planned Acquisition of Celator Is Credit

Negative

» Blackboard's Acquisition of Sequoia Is Credit Positive

» Coca-Cola FEMSA’s Acquisition of Ades Is Credit Positive

» Virgin Australia's Alliance with HNA Aviation Is Credit Positive

» PLDT's Planned Acquisition of San Miguel's Telecom Unit Is Credit Negative

» Suntory Holdings' Sale of First Kitchen Is Credit Positive

» Bridgestone’s Proposed Acquisition of Speedy Is Credit Positive

Infrastructure 10 » Exelon to Proceed with Credit-Negative Plan to Shutter Nuclear

Facilities in Illinois

» Landis' Equity Stake Sale Would Be Credit Positive

» China's Renewable Energy Quota Will Ease Curtailment in Wind and Solar Power Sector

Banks 16 » US Community Banks' Increasing Commercial Real Estate

Concentration Is Credit Negative

» Federal Reserve's Plan to Strengthen Stress Tests for Largest US Banks Is Credit Positive

» TBC Bank's Planned Premium London Stock Exchange Listing Is Credit Positive

» Investec plc Share Placement Improves Quality of Capital, a Credit Positive

» Vietnam's Tighter Bank Liquidity and Lending Rules Are Credit Positive

Insurers 25 » Suramericana's Acquisition of RSA Mexico Is Credit Positive

Sovereigns 26 » Japan's Consumption Tax Delay Makes Fiscal Goals More

Challenging

US Public Finance 28 » Housing Finance Agencies See HUD Position on Down Payment

Assistance as Credit Positive

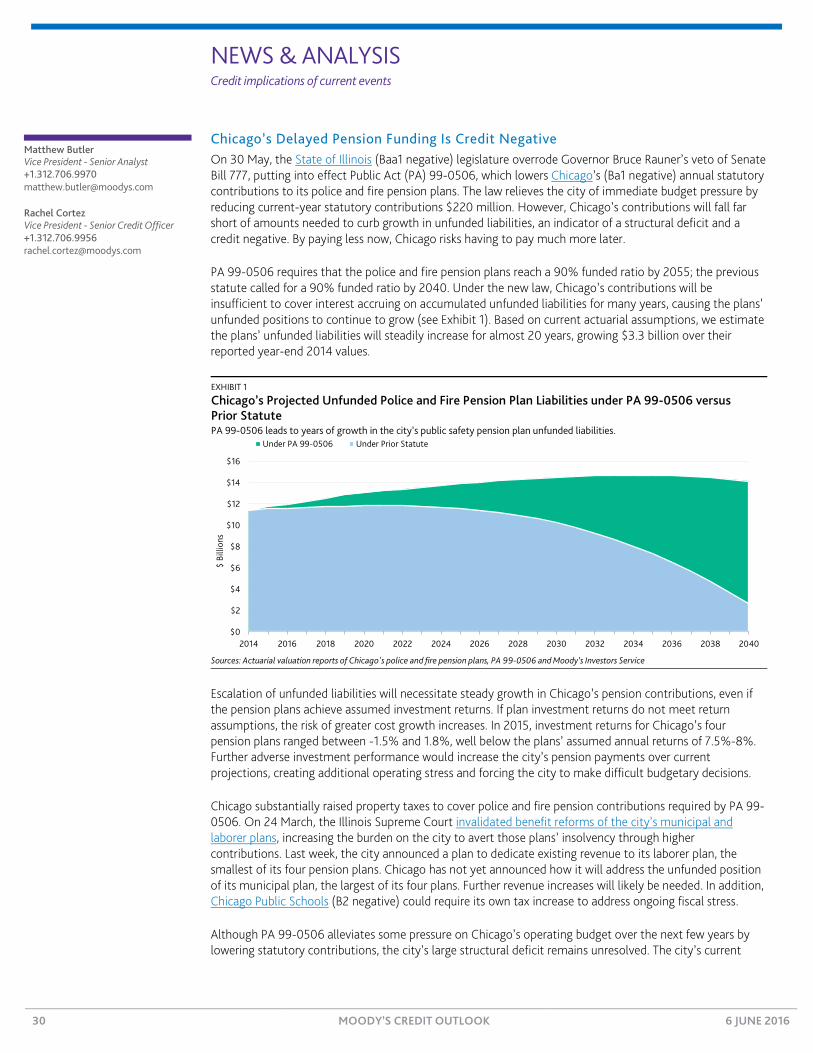

» Chicago's Delayed Pension Funding Is Credit Negative

» Montgomery County, Maryland Property Tax Increase Is Credit Positive

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Monday’s Credit Outlook 34 » Go to Last Monday’s Credit Outlook

Click here for Weekly Market Outlook, our sister publication containing Moody’s Analytics’ review of market activity, financial predictions, and the dates of upcoming economic releases.

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Corporates

MGM Resort’s Acquisition of Outstanding Stake in Borgata and Sale/Leaseback Are Credit Positive Last Tuesday, MGM Resorts International (Ba3 stable) said that it is buying Boyd Gaming Corporation’s (B2 stable) 50% interest in the Atlantic City, New Jersey-based Borgata Hotel Casino & Spa for $900 million. Combined with the 50% stake MGM already owns, MGM will gain full control of the Borgata. The purchase multiple is about 8.5x Borgata’s trailing 12-month EBITDA of $212 million, which is in line with other gaming acquisitions. MGM also said it reached an agreement with MGM Growth Properties LLC (MGP, B1 stable) for MGP to buy Borgata’s real property from MGM and then lease it back to an MGM subsidiary that will operate the property.

The deals are credit positive for MGM because owning 100% of Borgata will add about $112 million in annual EBITDA, net of the rental payment to MGP. MGM’s operational control of this east coast property will also complement its National Harbor and Springfield, Massachusetts developments and simplify MGM’s corporate structure.

MGM, which is the largest casino operator on the Las Vegas strip, will finance the acquisition with cash on hand and a bridge loan that will be repaid from the consideration received from MGP. We expect the transactions, which are due to close in the third quarter, will be leverage neutral to MGM. However, MGM’s excess cash balance will be reduced because it will receive operating partnership units for a portion of the real property purchase, as opposed to cash.

Borgata’s operations will be fully consolidated into MGM results. Separate from this transaction, we continue to estimate that MGM’s adjusted debt/EBITDA will decline to approximately 6.0x by year-end 2016 and 4.8x by year-end 2017.

MGM will pay about $600 million for Boyd’s 50% interest and will assume Borgata’s approximate $600 million of debt. MGP will purchase the real property from MGM for a total consideration of approximately $1.175 billion. MGP will finance the purchase from MGM using cash on hand, revolver drawings and issuance of operating partnership units in MGP. As a result, MGM’s ownership of MGP will increase to 76% from about 73%. Borgata will be added to the existing master lease between MGM and MGP with initial rent due to MGP of $100 million.

Peggy Holloway Senior Vice President +1.212.553.4542 [email protected]

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Jazz Pharmaceuticals’ Planned Acquisition of Celator Is Credit Negative Last Tuesday, Jazz Pharmaceuticals plc (unrated), which issues debt through its Jazz Securities Ltd. (Ba3 negative) subsidiary, said it had agreed to acquire Celator Pharmaceuticals Inc. (unrated) for $1.5 billion. The planned acquisition will increase Jazz Securities’ leverage, a credit negative. Following the announcement, we revised our outlook on Jazz’s ratings to negative from stable.

Celator does not yet generate revenue, but has recently reported promising clinical results for its leukemia drug Vyxeos. In May 2016, Vyxeos received FDA Breakthrough Therapy designation based on positive Phase III clinical trial results in older patients.

Jazz expects to complete the transaction in the third quarter and plans to finance it with existing cash and borrowings under its senior secured revolving credit facility. Pro forma for the Celator acquisition, we expect Jazz’s adjusted debt/EBITDA to increase to around 3.0x from 1.9x.

The negative outlook on Jazz’s ratings reflects the meaningful increase in the company’s financial leverage, and our expectation that the company will remain acquisitive, despite its increase in leverage to acquire Celator. Therefore, Jazz has limited cushion at the Ba3 rating to pursue additional acquisitions within the next 12 months.

Jazz’s narcolepsy medication Xyrem generates strong EBITDA growth but accounts for roughly 70% of the company’s sales. The risks associated with this product concentration are elevated by patent challenges to Xyrem, although these face regulatory and intellectual property hurdles. Jazz’s drug portfolio also includes the leukemia treatment Erwinaze and Defitelio for hepatic veno-occlusive disease.

We would consider downgrading Jazz’s ratings if the company experiences operating challenges, or if it appears likely that a generic competitor to Xyrem will emerge. We would also consider a downgrade if Jazz pursues acquisitions that increase leverage, as measured by adjusted debt/EBITDA to above 3.0x on a sustained basis.

Chedly Louis Vice President - Senior Analyst +1.212.553.4410 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Blackboard’s Acquisition of Sequoia Is Credit Positive Last Tuesday, Education technology company Blackboard Inc. (B2 negative) announced plans to buy Sequoia Retail Systems (unrated) for $22 million plus retention and incentive payments of up to $7 million over the next three years.

The credit-positive acquisition will give Blackboard a more flexible and advanced system for handling on-campus sales transactions than its own legacy software product. It will also be fully funded by Blackboard’s financial sponsor, Providence Equity Partners, which means Blackboard will gain a high-margin, high-growth software provider without having to issue any additional debt.

The purchase price is roughly 5.0x Sequoia’s pro-forma 2016 EBITDA. Providence Equity Partners will receive equity certificates in the combined company that will convert into either additional certificates or common stock upon certain events, such as a new equity financing or an initial public offering. Blackboard will issue the equity certificates at a super-holdco level.

Blackboard already has a longstanding relationship with Sequoia as a reseller of its systems piggybacked on to Blackboard's Transact, a point-of-sale (POS) system that enables students to pay for books and other items on campus with a college-issued card, mobile device, or on-line. Integrating Sequoia with Blackboard’s products in its North American higher-education segment will allow for the transition of Transact POS on-premise clients onto Sequoia’s broader, software-as-a-service POS applications. With Sequoia, Blackboard will provide deeper support of on-campus commerce transactions, including those at campus bookstores and events, dining establishments, and stadium concessions.

We project that Blackboard will have revenues of approximately $650 million in 2016, flat relative to 2015. Headquartered in Washington, DC, Blackboard is a leading provider of learning management software applications to K-12 schools, colleges and universities, government organizations, and businesses for interactive teaching, learning, course management, and campus life.

Kevin Stuebe Vice President - Senior Analyst +1.212.553.2999 [email protected]

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Coca-Cola FEMSA’s Acquisition of Ades Is Credit Positive Last Wednesday, Mexico’s Coca-Cola FEMSA, S.A.B. de C.V. (KOF, A2 negative) said that it would team up with The Coca-Cola Company (Aa3 stable) to buy Unilever PLC’s (A1 stable) soy-based beverage business AdeS for $575 million in cash. KOF will own 50% of AdeS business, while the remaining 50% will be distributed through other Coke bottlers. This transaction is credit positive for KOF because it will increase the product portfolio of the world’s largest franchise Coca-Cola bottling company without adding to its debt burden. KOF will use cash on hand to finance its half of the acquisition.

The AdeS acquisition strengthens KOF’s operation in its franchised territories, adding new beverages to its successful route-to-market platform. KOF will distribute AdeS products in large Latin American markets where both companies had operated separately, including Mexico, Brazil, Argentina and Colombia. The deal allows Coca-Cola to offer franchise agreements to bottlers in other territories where AdeS sold its products, including Uruguay, Paraguay, Bolivia and Chile. AdeS generated $284 million in revenue in 2015 from sales of 56.2 million unit cases.

KOF’s credit metrics will remain relatively unchanged with the AdeS deal. KOF has strong liquidity today, with MXN18 billion ($1 billion) on hand as of 31 March 2016, enough to cover 1.5x its short-term debt. Even after spending $287.5 million in cash for its half of the purchase, KOF’s cash on hand will cover its short-term debt 1.2x.

Historically, KOF has generated positive free cash flow (its cash from operations after dividends and capital spending), with MXN3.9 billion for the 12 months through 31 March 2016 (see exhibit). KOF’s strong cash generation and conservative financial policies support its strong liquidity.

Coca-Cola FEMSA’s Free Cash Flow, 2011-Present

Source: Moody’s Financial Metrics

KOF’s negative outlook today reflects Mexico’s (A3 negative) sovereign credit challenges rather than risks to its own business or standalone credit quality. For Coca-Cola and Unilever, the transaction is too small to have significant credit implications.

MXN 0.8

MXN 6.7

MXN 2.6

MXN 4.2

MXN 2.1

MXN 3.9

MXN 0

MXN 1

MXN 2

MXN 3

MXN 4

MXN 5

MXN 6

MXN 7

MXN 8

2011 2012 2013 2014 2015 LTM 03/16

MXN

Bill

ions

Alonso Sanchez Rosario Vice President - Senior Analyst +52.55.1253.5706 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Virgin Australia’s Alliance with HNA Aviation Is Credit Positive On 31 May, Virgin Australia Holdings Limited (Virgin, B2 review for downgrade) announced that it had entered a strategic alliance with HNA Aviation Group Co. Ltd (unrated). Pending regulatory approvals, HNA will make an equity investment of AUD159 million to take a 13% equity stake in Virgin. HNA is also committed to supporting the outcome of Virgin’s capital structure review and intends to gradually increase its stake up to 19.99%.

Both the alliance and the equity injection are credit positive for Virgin. The alliance will provide Virgin greater access to the growing Chinese travel market where HNA has an established position, while the equity injection comes as Virgin is reviewing its capital structure in order to strengthen its balance sheet.

HNA is the largest private operator of airlines in China. Accordingly, the alliance will provide Virgin with an opportunity to enhance its profitability, mainly in the international segment, which has been incurring losses. For the first half of fiscal 2016, which ended 31 December 2015, Virgin reported an underlying EBIT loss of AUD31 million, including the AUD19.2 million adverse effect of volcanic ash disruptions on flights to Bali.

We expect Virgin’s debt level to be at or above our expectations for its rating at the fiscal year end on 30 June 2016. Our expectation is based on Virgin’s weakening liquidity on account of adverse working capital movements, high capital expenses for the first half of fiscal 2016, and its considerable USD-denominated debt, which has kept rising in AUD terms because of the weakness in the local currency.

Against this background, we expect Virgin’s adjusted debt/EBITDA to remain within 6.5x-6.8x at 30 June 2016, versus our quantitative guidance of below 6.5x for the B2 rating. If the equity injection of AUD159 million is applied to debt repayment, we expect adjusted debt/EBITDA to improve to around 6.4x-6.6x.

Virgin’s credit quality and rating has, to date, benefited from its strong shareholder base. Its main shareholders (pre-HNA) are Air New Zealand Limited (Baa2 stable) with a 25.9% stake, Etihad Airways PJSC (unrated) with a 24.1% stake, Singapore Airlines Limited (unrated) with a 22.8% stake and Virgin Group Limited (unrated) with a 10% stake. They have provided liquidity and capital support in the past, increasing our tolerance for the company’s weak leverage metrics relative to our expectations for its B2 rating. However, on 30 March 2016 Air New Zealand announced that it is exploring options for its shareholding in Virgin, including a possible sale of all or part of its stake, raising uncertainty around Virgin’s future shareholder mix.

Virgin is currently reviewing its capital structure. If, as a consequence, its financial metrics improve to fall to the stipulated 6.5x for the B2 rating, we would likely affirm the rating. This assumes that any change to the composition of Virgin's key shareholders does not affect our assessment of their willingness or ability to support it.

Ian Chitterer Vice President - Senior Analyst +61.2.9270.1420 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

PLDT’s Planned Acquisition of San Miguel’s Telecom Unit Is Credit Negative Last Monday, the Philippine Long Distance Telephone Company (PLDT, Baa2 stable) announced that it and Globe Telecom Inc. (unrated) would acquire San Miguel Corporation’s (SMC, unrated) telecommunication business for PHP69.1 billion, including the assumption of PHP17.0 billion in liabilities. PLDT and Globe will also jointly acquire the shares of New Century Telecoms, Inc (unrated) and eTelco, Inc (unrated) for a total of PHP897 million, including the assumption of PHP130 million in liabilities. The total consideration for the three acquisitions is PHP70 billion, including the PHP17 billion in assumed liabilities. As a result, for its 50% equity portion, PLDT will pay PHP35 billion, composed of a PHP26 billion cash payment and PHP9 billion of assumed liabilities.

The acquisitions are credit negative because PLDT will finance part of the purchase price and additional capex with debt. The debt will raise its adjusted debt/EBITDA to the 2.5x range by year-end, which is at the upper end of our quantitative guidance for leverage for its Baa2 issuer rating. The ratio was 2.3x as of March 2016. Moreover, the transactions come as PLDT is facing intense domestic competition, persistent pricing pressure and sustained declines in high-margin mobile text messaging and toll revenues.

The transactions would provide PLDT with new spectrum frequencies, notably in the 700-megahertz, 900-megahertz and 1800-megahertz bands, which will help improve its network quality and rollout in regional and rural areas. PLDT also announced last Monday that it had planned to increase its capital expenditures by around $100 million (PHP5 billion) this year to PHP48 billion to accelerate the rollout of its services in these newly acquired bands.

The proceeds from PLDT’s sale of a 25% stake in Beacon Electric Asset Holdings Inc. (unrated) to Metro Pacific Investments Corporation (MPIC, unrated) will help offset the increased debt and support cash flows. MPIC agreed to pay PLDT PHP26.2 billion for the Beacon stake. PLDT will receive PHP17.0 billion at closing, while the remaining PHP9.2 billion will be paid over the next four years.

PLDT made its first payment of PHP13.2 billion (constituting its 50% share of the purchase price of the equity) last Monday. A second payment of PHP6.6 billion (comprising 25% of the purchase price) will be due on 1 December 2016. The remainder is due on 30 May 2017.

PLDT is the largest telecommunications operator in the Philippines. It is an integrated provider of fixed-line, broadband, cellular, and information and communications technology.

Annalisa Di Chiara Vice President - Senior Credit Officer +852.3758.1537 [email protected]

Carole Herve Associate Analyst +852.3758.1505 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Suntory Holdings’ Sale of First Kitchen Is Credit Positive Last Thursday, Suntory Holdings Limited (Baa2 stable) announced that it had signed an agreement to sell the entire stake of its wholly owned Japanese fast-food restaurant subsidiary, First Kitchen Co., Ltd (unrated), to rival hamburger chain Wendy’s Japan LLC, a joint venture between Wendy’s Company (B2 stable) and a Japanese partner. The companies expect the deal to close at the end of this month.

The sale is credit positive for Suntory Holdings since monetizing this asset will help it reduce total debt. Leverage for Suntory Holdings has been elevated since its $16 billion acquisition of Beam Inc. (renamed as Beam Suntory Inc. Baa2 stable) in May 2014.

Suntory Holding’s leverage, as measured by Moody’s-adjusted debt/EBITDA, fell to 5.4x in 2015 from 5.9x a year ago, but is above our quantitative guidance of below 5.0x for its rating. The current Baa2 rating reflects Suntory Holdings’ improved profitability and its cash flow after the Beam acquisition, which together have enhanced its ability to pay down debt, and strengthened our expectation of further deleveraging during the next 12-18 months.

Suntory Holdings has not disclosed the proceeds from the sale, but we expect it will be in the single-digit billions of yen, judging from First Kitchen’s ¥8.7 billion revenue in 2015 – a small sum relative to Suntory Holdings’ consolidated adjusted debt of ¥2.0 trillion for 2015.

At the same time, the company has sold several non-core assets or overlapping businesses, which will help expedite the deleveraging (see exhibit). Such initiatives last year included the sales of its Spanish brandy and sherry business, announced in December, for about ¥37 billion; its cognac distiller Louis Royer S.A.S., announced in July, for about ¥13 billion; and a share in its Chinese beer joint ventures, announced in October, for an undisclosed amount. We expect that Suntory Holdings will continue its initiative to streamline and increase its focus on its core alcohol and non-alcohol business globally.

Suntory Holdings’ Cash Flow and Leverage Is Improving amid Asset Sales

Sources: Moody’s Financial Metrics and Moody’s Investors Service estimate for 2016

¥0

¥20

¥40

¥60

¥80

¥100

¥120

¥140

0x

1x

2x

3x

4x

5x

6x

7x

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16E

JPY

Billi

ons

Free Cash Flow - right axis Adjusted debt / EBITDA - left axis

Beam acquisition closed in May

Motoki Yanase Vice President - Senior Analyst +81.3.5408.4154 [email protected]

Mirai Kaneuchi Associate Analyst +81.3.5408.4026 [email protected]

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Bridgestone’s Proposed Acquisition of Speedy Is Credit Positive On 30 May, Bridgestone Corporation (A2 stable) announced that its wholly owned subsidiary Bridgestone Europe NV/SA (unrated) will acquire 100% of Speedy France SAS (unrated), a leading car service retail company in France, pending regulatory approvals. The acquisition would be credit positive because it will enhance Bridgestone’s distribution network and strengthen its competitive position in Europe, while the effect on Bridgestone’s financials would be limited.

Although the company has not disclosed the acquisition cost, according to Bridgestone, which is the world’s largest tire manufacturer by sales, Speedy’s 2014 revenue was €175 million (approximately ¥21 billion), while Bridgestone’s 2015 revenue was ¥3.8 trillion. Consequently, the acquisition suggests a limited effect on Bridgestone’s financials and we expect the company’s financial metrics will remain within the parameters of its A2 rating following the acquisition. In addition, the company’s leverage – as measured by debt/EBITDA – improved to 1.1x in 2015 from 2.0x in 2012, leaving it ample headroom in its A2 rating and room for further acquisitions to expand its business globally.

The acquisition would increase Bridgestone’s retail outlets in France to more than 800 from 300 currently, and improve the company’s operating profile in Europe. The company’s European 2015 operating profit margin was 5.1%, up from 4.6% in 2014 and 0.5% in 2013, but well below the 16.6% in Japan and 11.5% in the US, reflecting intense competition from other tire manufacturers in Europe, including from Compagnie Gener. des Etablissements Michelin (A3 stable). We expect the acquisition of Speedy will enhance Bridgestone’s brand recognition in Europe by expanding its distribution network.

The Speedy acquisition follows Bridgestone’s failed October 2015 bid to acquire The Pep Boys - Manny, Moe, & Jack (unrated), a US automotive parts and service retailer: Bridgestone was ultimately outbid by Icahn Enterprises L.P. (Ba3 stable) in December last year. The Speedy acquisition is in line with the company’s strategy for global growth, as stated in its 2015 mid-term management plan.

Kenichiro Sano Associate Analyst +81.3.5408.4157 [email protected]

Takashi Akimoto Assistant Vice President - Analyst +81.3.5408.4208 [email protected]

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Infrastructure Exelon to Proceed with Credit-Negative Plan to Shutter Nuclear Facilities in Illinois Last Thursday, Exelon Corporation (Baa2 stable) announced its plan to proceed with the early retirement of its most unprofitable nuclear reactor facilities in Illinois, including the 1,069-megawatt Clinton facility in DeWitt County and the 1,871-megawatt Quad Cities facility in Rock Island County. The early retirement of these reactors is credit negative for Exelon and its unregulated merchant generation subsidiary, Exelon Generation Company, LLC (ExGen, Baa2 stable) because it threatens to hurt their balance sheets by crystalizing certain liabilities.

Because the Clinton plant is now scheduled to retire in 2017, instead of 2026, the facility will no longer meet the US Nuclear Regulatory Commission’s (NRC) minimum funding requirements with respect to its nuclear decommissioning trust fund (NDTF). Any shortfall would require some true-up funding, a credit negative.

Exelon said it might look to post more than $400 million of parental guarantees on behalf of ExGen’s Clinton and Quad Cities reactors, depending on the NRC’s funding criteria. Posting parental guarantees to its unregulated subsidiary is credit negative for Exelon and its regulated transmission and distribution utilities because it reverses the company’s previously stated plans to create some separateness and independence between the parent and ExGen. Quad Cities is 25% owned by Berkshire Hathaway Energy Company (A3 stable), so Exelon will need to discuss any plans to close the reactor with its partner, even if it has the legal authority to make operational decisions about the plant.

Closing the reactors early is also bad news for Illinois (Baa1 negative) and local governments such as the City of Clinton (unrated), DeWitt County (unrated) and the DeWitt County School District (unrated) because the reactor employs approximately 700 people with roughly $63 million in payroll. Although Quad Cities is in Illinois, the plant is in the PJM Interconnection region, not the Midwest Independent Transmission System (MISO) where Clinton is located. The PJM and MISO are regional transmission organizations that manage the supply and demand of electric loads. Both regional transmission organizations compensate generators with payments to keep their generation supplies ready to be called upon if needed, known as capacity payments. Thanks to the PJM’s better capacity payments, Quad Cities will stay operational until May 2018, shuttering a year after Clinton’s June 2017 closing.

As the largest unregulated operator of nuclear reactors in the US, the decision to pursue early retirement calls into question the longer-term business prospects for ExGen, which owns and operates approximately 19,000-megawatts of nuclear generation. There are a number of nuclear facilities across ExGen’s fleet that are now more exposed to early retirement, including the 2,347-megawatt Byron facility, located in Ogle County, Illinois. Beyond Illinois, Egan’s 625-megawatt Oyster Creek facility in New Jersey is already scheduled to close in 2019, while its 575-megawatt Gina facility in New York, which has an operating license to 2029, and its 837-megawatt Three Mile Island facility in Pennsylvania, which has an operating license to 2034, are both slated to be retired early if power prices do not improve soon.

By announcing the plans to close the plants well in advance of their actual closures, Exelon provides time for legislators, regulators and other stakeholders to take action, such as passing legislation that compensates the reactors for their unique reliability and carbon-friendly attributes, before the shutdowns occur. Exelon continues to work with state lawmakers and other stakeholders, but the clock is ticking, putting Exelon in a difficult spot because an early retirement at Clinton and Quad Cities might create a new emergency for the Illinois legislature to address (owing to the economic effect of the facility’s retirement). If this scenario pans out, Exelon could face a more hostile state regulatory environment.

Peter Giannuzzi Associate Analyst +1.212.553.2917 [email protected]

Jim Hempstead Associate Managing Director +1.212.553.4318 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

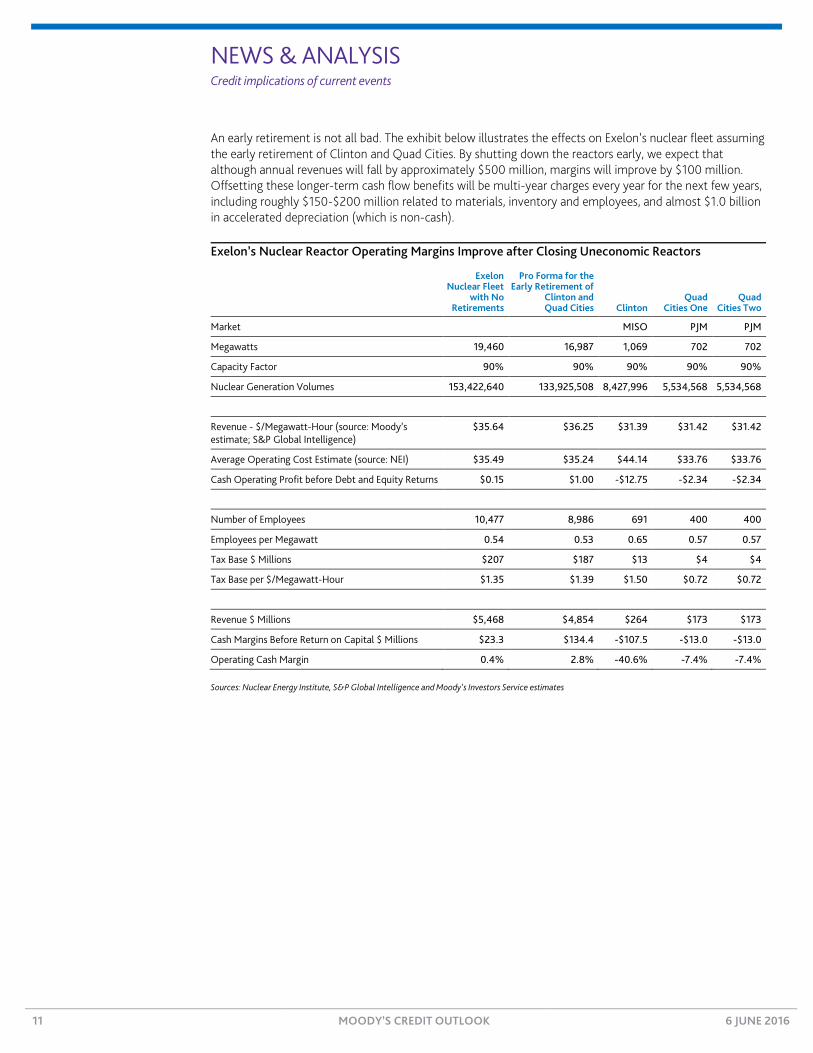

An early retirement is not all bad. The exhibit below illustrates the effects on Exelon’s nuclear fleet assuming the early retirement of Clinton and Quad Cities. By shutting down the reactors early, we expect that although annual revenues will fall by approximately $500 million, margins will improve by $100 million. Offsetting these longer-term cash flow benefits will be multi-year charges every year for the next few years, including roughly $150-$200 million related to materials, inventory and employees, and almost $1.0 billion in accelerated depreciation (which is non-cash).

Exelon’s Nuclear Reactor Operating Margins Improve after Closing Uneconomic Reactors

Exelon Nuclear Fleet

with No Retirements

Pro Forma for the Early Retirement of

Clinton and Quad Cities Clinton

Quad Cities One

Quad Cities Two

Market MISO PJM PJM

Megawatts 19,460 16,987 1,069 702 702

Capacity Factor 90% 90% 90% 90% 90%

Nuclear Generation Volumes 153,422,640 133,925,508 8,427,996 5,534,568 5,534,568

Revenue - $/Megawatt-Hour (source: Moody’s estimate; S&P Global Intelligence)

$35.64 $36.25 $31.39 $31.42 $31.42

Average Operating Cost Estimate (source: NEI) $35.49 $35.24 $44.14 $33.76 $33.76

Cash Operating Profit before Debt and Equity Returns $0.15 $1.00 -$12.75 -$2.34 -$2.34

Number of Employees 10,477 8,986 691 400 400

Employees per Megawatt 0.54 0.53 0.65 0.57 0.57

Tax Base $ Millions $207 $187 $13 $4 $4

Tax Base per $/Megawatt-Hour $1.35 $1.39 $1.50 $0.72 $0.72

Revenue $ Millions $5,468 $4,854 $264 $173 $173

Cash Margins Before Return on Capital $ Millions $23.3 $134.4 -$107.5 -$13.0 -$13.0

Operating Cash Margin 0.4% 2.8% -40.6% -7.4% -7.4%

Sources: Nuclear Energy Institute, S&P Global Intelligence and Moody’s Investors Service estimates

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Landis’ Equity Stake Sale Would Be Credit Positive Last Wednesday, Landis System Operator CVBA (Landis, A1 negative), the operating subsidiary of Belgian utility company Landis Assets (unrated), said that it had entered into exclusive talks to sell new shares amounting to a 14% equity stake in Landis Assets to a unit of State Grid Corporation of China (Aa3 negative). This development is credit positive for Landis because the proceeds from a successful execution will go toward reducing Landis’ debt.

Landis operates, maintains and develops the regulated electricity and gas distribution networks on behalf of Landis Assets, which owns the network assets. Landis operates on a cost basis, whereby all its costs, including financing costs, are passed through to Landis Assets. Landis Assets also guarantees the debt raised by Landis under its €5 billion euro medium-term note programmer.

As of 31 December 2015, Landis’ overall financial leverage (including Landis Assets), as measured by net debt to regulated asset base (RAB), was around 80%, while the ratio of funds from operations (FFO) to net debt was below 10%. Proceeds from the sale will mitigate weaker financial performance following an increase in debt in 2014 and, depending on the amount of proceeds, has the potential to restore metrics to within our quantitative guidance for the current A1 rating of no more than 70% net debt/regulated assets and FFO/net debt of at least the low teens. Exhibits 1 and 2 show the stake sale’s potential possible effect on these metrics.

EXHIBIT 1

Landis’ Stake Sale’s Effect on Funds from Operations/Net Debt and Retained Cash Flow/Net Debt

Sources: Landis Assets and Moody’s Investors Service forecasts

EXHIBIT 2

Landis’ Stake Sale’s Effect on Net Debt/Fixed Assets

Sources: Landis Assets and Moody’s Investors Service forecasts

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2012 2013 2014 2015 2016 2017 2018 2019 2020

Funds from Operations/Net Debt Retained Cash Flow/Net Debt

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2012 2013 2014 2015 2016 2017 2018 2019 2020

Stefanie Voelz Vice President - Senior Credit Officer +44.20.7772.5555 [email protected]

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Subject to the successful conclusion of the negotiations and necessary board and shareholder approvals, the transaction will likely close by the end of this year. We also note that Eandis will receive an additional net equity contribution of around €60 million from its municipal shareholder base by the end of June 2016. Municipal shareholders contributed around €100 million of additional equity in 2015.

The improvement in metrics will strengthen Eandis’ ability to confront lower revenues from 2017, following a likely reduction in allowed returns, and an uncertain recovery of outstanding regulatory receivables. In May 2016, VREG, the Flemish regulator for energy networks, announced draft proposals for the next regulatory period of 2017-20. They include a cut in the allowed return to 5.0% (nominal, pre-tax) from 6.1% currently, reflecting the low interest rate environment. More positively, VREG proposed more timely recovery of non-controllable cost items. This will allow Eandis to recover historical tariff deficits of around €450 million accumulated over 2010-14, during the 2016-20 period, albeit at a slightly slower pace than the company had envisaged.

Aside from the regulatory tariff deficits, Eandis at the end of 2015 reported €627 million in outstanding receivables linked to its obligation to buy renewable energy certificates on behalf of suppliers. Although the cost of purchasing certificates is recoverable, the company has not been able to sell adequate numbers in the market. The Flemish government is deciding on a solution that would allow affected network companies to recover outstanding receivables over 2017-21. However, although the government has introduced a customer levy on supply charges, the exact recovery mechanism remains vague.

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

China’s Renewable Energy Quota Will Ease Curtailment in Wind and Solar Power Sector Last Tuesday, China’s National Development and Reform Commission (NDRC) announced a renewable energy quota that sets minimum utilization hours on wind and solar power in select cities in eight provinces and three autonomous regions. The measure is credit positive for wind and solar power companies because it will help alleviate the current high levels of curtailment. Curtailment refers to the reduction in power generation compared to the optimal utilization of wind and solar power capacity.

Among power companies, China Longyuan Power Group Corporation Ltd. (Baa1 negative) will benefit most from the new quota owing to it being China’s largest wind power company. China Three Gorges Corporation (Aa3 negative) and China General Nuclear Power Corporation (A3 negative) will also benefit through their wind and solar power portfolios. However, companies that invest heavily in coal-fired power, such as China Resources Power Holdings Co., Ltd. (Baa2 negative) and Beijing Energy Holding Co. Ltd. (A2 negative), will be negatively affected by the quota given the likely increasing dispatch of wind power over coal-fired power in the eight provinces and three regions.

The renewable energy quota follows the regulator’s broad guidance in March 2016 on the renewable energy quota system, which aims to prioritize the dispatch of electricity generated from clean energy and supports the country’s renewable energy development and national goal to reduce carbon emissions amid low power demand.

The new system sets annual minimum utilization hours (1,800-2,000 hours of wind power and 1,300-1,500 hours of solar power) to be off-taken by grid operators in select cities in eight provinces and three autonomous regions (see Exhibits 1 and 2).

EXHIBIT 1

Annual Minimum Utilization Hours for Wind Power Off-Take by Grid Operators in Selected Regions in China Zone Regions Hours

Zone I Inner Mongolia Autonomous Region (AR), excluding Chifeng, Tongliao, Xing'anmeng, Hulunbeier 2,000

Xinjiang AR (Urumqi, Ili Kazakh, Karamay, Shihezi) 1,900

Zone II Inner Mongolia AR (Chifeng, Tongliao, Xing'an, Hulunbeier) 1,900

Hebei Province (Zhangjiakou) 2,000

Gansu Province (Jiayuguan, Jiuquan) 1,800

Zone III Gansu Province, excluding Jiayuguan, Jiuquan 1,800

Xinjiang AR, excluding Urumqi, Ili Kazakh, Karamay, Shihezi 1,800

Jilin Province (Baicheng, Songyuan) 1,800

Heilongjiang Province (Jixi, Shuangyashan, Qitaihe, Suihua, Yichun, Daxing'anling) 1,900

Ningxia AR 1,850

Zone IV Heilongjiang Province, other regions 1,850

Jilin Province, other regions 1,800

Liaoning Province 1,850

Shanxi Province (Xinzhou, Shuozhou, Datong) 1,900

Source: China’s National Development and Reform Commission

Ivy Poon Assistant Vice President - Analyst +852.3758.1336 [email protected]

Ralph Ng Associate Analyst +852.3758.1530 [email protected]

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

EXHIBIT 2

Annual Minimum Utilization Hours for Solar Power Off-take by Grid Operators in Selected Regions in China Zone Regions Hours

Zone I Ningxia Autonomous Region (AR) 1,500

Qinghai Province (Haixi) 1,500

Gansu Province (Jiayuguan, Wuwei, Zhangye, Jiuquan, Dunhuang, Jinchang) 1,500

Xinjiang AR (Hami, Tacheng, Altay, Karamay) 1,500

Inner Mongolia AR, excluding Chifeng, Tongliao, Xing'anmeng and Hulunbeier 1,500

Zone II Qinghai Province, other regions outside Zone I 1,450

Gansu Province, other regions outside Zone I 1,400

Xinjiang AR, other regions outside Zone I 1,350

Inner Mongolia A.R. (Chifeng, Tongliao, Xing'anmeng and Hulunbeier) 1,400

Heilongjiang Province 1,300

Jilin Province 1,300

Liaoning Province 1,300

Hebei Province (Chengde, Zhangjiakou, Tangshan, Qinhuangdao) 1,400

Shanxi Province (Datong, Shuozhou, Xinzhou) 1,400

Shaanxi Province (Yulin, Yan'an) 1,300

Source: China’s National Development and Reform Commission

To achieve the NDRC’s targets, grid operators are required to sign priority generation and dispatch agreements with qualified wind and solar power companies by the end of June. Most of the select provinces and autonomous regions are rich-wind regions that suffer from high curtailment. Utilization hours in these regions ranged from 1,184 hours in Gansu to 1,865 hours in Inner Mongolia in 2015, both below the minimum utilization hours required under the new quota.

Curtailment is a key constraint in the development of wind power in China. According to China’s National Energy Administration, the average curtailment rate of the country’s wind power rose to 26% in first-quarter 2016 from 15% in 2015 and 8% in 2014. In particular, Jilin, Xinjiang, and Gansu showed record-high curtailment rates of 53%, 49%, 48%, respectively, in first-quarter 2016. Rising curtailment is mainly driven by low power demand, overcapacity, inadequate grid infrastructure and limited cross-provincial coordination to support long-distance electricity transmission.

In addition to the minimum utilization hours, provinces and autonomous regions that fail to meet their quota will not be allowed to start construction of new wind and solar projects. Accordingly, the new measure should help rationalize investment and curb excess capacity. Furthermore, provincial governments and grid operators cannot lower the level of minimum utilization hours specified in the renewable energy quota without NDRC and National Energy Administration approval. This is done to support a consistent policy execution across the various provinces.

However, the latest measure does not cover any potential compensation payable by non-renewable energy companies to renewable energy companies if the provinces and autonomous regions fail to purchase the required level of power generated from renewable energy companies. Such compensation was mentioned in the broad guidance in March, but the implementation of a compensation scheme would create uncertainty for the profitability of coal-fired power companies.

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Banks US Community Banks’ Increasing Commercial Real Estate Concentration Is Credit Negative Last Wednesday, the Federal Deposit Insurance Corporation (FDIC) released its first-quarter 2016 Quarterly Banking Profile for US banks. Despite a 2% decline in net income for the overall industry, net income for community banks – banks with less than $1 billion in total assets – grew by a considerable 7.4% from a year earlier. However, this improvement was largely driven by community banks’ above-average growth in commercial real estate (CRE) lending, which is credit negative.

All banks have grown their CRE loan portfolios, but community banks’ have far higher CRE exposure relative to total assets than at larger banks. As a result, when the CRE market deteriorates, as one of our key indicators suggests has already begun, community banks’ creditworthiness will deteriorate more than larger banks, as was the case in the last recession. Community banks grew CRE loans 11.9% during the past 12 months, compared to 9.4% for all other banks. Within CRE, 19.1% growth in multifamily and 16.3% in construction/development loans led the increase. Moreover, community banks increased their unused CRE loan commitments by a substantial 22.7%.1

The rapid growth has rebuilt community banks’ CRE loan concentration, which in the last recession, caused many community bank failures. At 31 March 2016, community banks held 13% of total banking system assets, but one-third of CRE loans outstanding. Exhibit 1 compares the trends in CRE loans as a percent of total assets for community banks (green line) and all other banks (blue line) to the number of bank failures (bars). The green line shows that community banks’ recent growth has raised their CRE concentration to 29% of total assets, compared to larger banks whose exposure is 10% of assets. The exhibit clearly shows the spike in bank failures following the rapid growth in CRE leading up to the last real estate downturn. At the current growth rate, community banks will surpass their 2008 peak of 32% within two years.

EXHIBIT 1

Commercial Real Estate Loans as a Percent of Total Assets for Community Banks and All Other Banks, and Bank Failures Community banks are rebuilding their commercial real estate concentration.

Source: Federal Deposit Insurance Corporation

According to the US Government Accountability Office’s January 2013 report Causes and Consequences of Recent Bank Failures, in the ten states with ten or more bank failures between 2008 and 2011, “failures of

1 This ratio was not disclosed for other banks.

15%

32%

29%

9%

12%10%

0

25

50

75

100

125

150

175

0%

5%

10%

15%

20%

25%

30%

35%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 1Q16

Bank Failures - right axis Community Banks: CRE to Assets - left axis All Other Banks: CRE to Assets - left axis

Joseph Pucella Vice President - Senior Credit Officer +1.212.553.7455 [email protected]

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

small and medium-size banks were largely associated with high concentrations of CRE loans, and in particular, acquisition, development, and construction loans, and inadequate management of the risks associated with these loans. The rapid growth of their CRE portfolios resulted in concentrations that exceeded regulatory thresholds for heightened scrutiny and increased the banks’ exposure to the sustained real estate and economic downturn that began in 2007.”

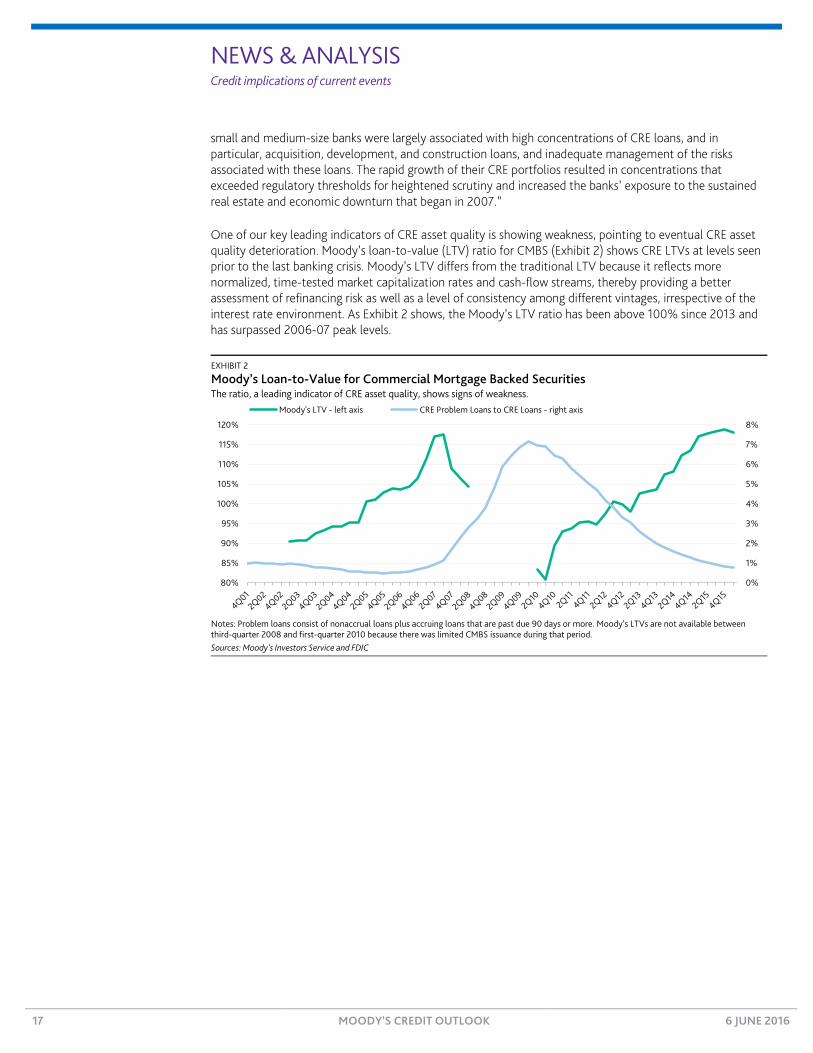

One of our key leading indicators of CRE asset quality is showing weakness, pointing to eventual CRE asset quality deterioration. Moody’s loan-to-value (LTV) ratio for CMBS (Exhibit 2) shows CRE LTVs at levels seen prior to the last banking crisis. Moody’s LTV differs from the traditional LTV because it reflects more normalized, time-tested market capitalization rates and cash-flow streams, thereby providing a better assessment of refinancing risk as well as a level of consistency among different vintages, irrespective of the interest rate environment. As Exhibit 2 shows, the Moody’s LTV ratio has been above 100% since 2013 and has surpassed 2006-07 peak levels.

EXHIBIT 2

Moody’s Loan-to-Value for Commercial Mortgage Backed Securities The ratio, a leading indicator of CRE asset quality, shows signs of weakness.

Notes: Problem loans consist of nonaccrual loans plus accruing loans that are past due 90 days or more. Moody’s LTVs are not available between third-quarter 2008 and first-quarter 2010 because there was limited CMBS issuance during that period. Sources: Moody’s Investors Service and FDIC

0%

1%

2%

3%

4%

5%

6%

7%

8%

80%

85%

90%

95%

100%

105%

110%

115%

120%

Moody's LTV - left axis CRE Problem Loans to CRE Loans - right axis

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Federal Reserve’s Plan to Strengthen Stress Tests for Largest US Banks Is Credit Positive Last Thursday, Federal Reserve Governor Daniel Tarullo signaled that the Fed plans to further strengthen the annual stress test it performs on the largest US banks. Likely beginning in 2018, the revised stress test will require the eight US-based global systemically important banks (GSIBs)2 to hold sufficient capital so that even under a severely adverse stress scenario their capital ratios would remain above not only the minimum regulatory requirements but also above the regulatory minimum plus their GSIB capital surcharges.3

The plan is credit positive because it will require the banks to hold larger capital buffers and undertake further de-risking to limit the losses to which they would be exposed under a severely adverse stress scenario. However, by further challenging these banks’ ability to generate returns on capital that will satisfy shareholders, it also risks compelling banks to consider more radical restructurings to avoid these requirements.

In an interview on Bloomberg Television, Mr. Tarullo said he was quite confident the Fed would increase the post-stress minimum capital requirements so that the amount of capital the US GSIBs are required to hold even after absorbing the losses in the Fed’s stress test includes the GSIB surcharge. The intention is to make the US GSIBs more resilient than other banks and to ensure that GSIBs have capital to absorb unanticipated losses.

Mr. Tarullo said that although the timing for the implementation had not been decided, he expected that it would not be in time for the next stress test in 2017. He noted that it was important to get a proposal out in enough time for banks to begin planning for the surcharge, and suggested that the changes might be phased in rather than implemented at once.

Based on the latest surcharges reported by each bank, adding the GSIB surcharge would require the US GSIBs to hold additional common equity equal to 1.0%-3.5% of risk-weighted assets post-stress before they could receive Fed approval to increase dividends or buy back additional shares. The exhibit below shows that State Street Corporation (A1 stable), The Bank of New York Mellon Corporation (A1 stable), and Wells Fargo & Company (A2 stable) already meet this requirement before any proposed capital actions based on the 2015 Dodd-Frank Act stress test, although for Wells Fargo the cushion was quite modest and its capital plan would not have received approval under the Comprehensive Capital Analysis and Review (CCAR) portion of the stress test in 2015 had this rule already been in effect.

2 The eight US GSIBs are Bank of America Corporation, The Bank of New York Mellon Corporation, Citigroup Inc., The Goldman

Sachs Group, Inc., JPMorgan Chase & Co., Morgan Stanley, State Street Corporation and Wells Fargo & Company. 3 See Federal Reserve Finalizes Credit Positive Capital Surcharges for Largest US Banks, 23 July 2015.

David Fanger Senior Vice President +1.212.553.4342 [email protected]

NEWS & ANALYSIS Credit implications of current events

19 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Pro Forma Effect of Global Systemically Important Bank Surcharge on 2015 Federal Reserve Stress Tests

Notes: JPMorgan Chase reported a reduction in its GSIB surcharge to 3.5% from 4.5%, while Goldman Sachs reported a reduction to 2.5% from 3.0%, although these have not been confirmed by the Fed. The exhibit uses these reduced surcharges. For Bank of America, post-stress minimum common equity Tier 1 ratio under the comprehensive capital analysis and review is from the bank’s September 2015 CCAR resubmission. Sources: US Federal Reserve and the companies

The other five GSIBs would likely have failed both stress tests in 2015 had the surcharge already been included. However, Mr. Tarullo said there would be other changes to the stress test that would partially offset the higher capital requirement imposed by the inclusion of the surcharge. Although our analysis in the exhibit thus overstates the shortfall, Mr. Tarullo insisted that notwithstanding the other changes, the inclusion of the surcharge will still result in a significant increase in the capital that these banks must hold.

Because these other changes have not yet been quantified, we cannot estimate the magnitude of the overall effect. Additionally, Mr. Tarullo’s statement that the GSIBs will be given time to plan and that the changes will be phased in suggests that the GSIBs will be able to address any potential shortfalls through increased capital retention rather than through additional issuances.

Increased capital retention would be positive for creditors, but would translate into reduced share buybacks and slower dividend growth. We believe that this would increase shareholder pressure, particularly on the five GSIBs that would need to retain more capital, to consider taking additional steps to shrink their systemic footprint or even undertake more radical restructurings to reduce the effect of these requirements. Such actions can pose greater risks for creditors to the extent that they create greater operational and execution risk, reduce earnings diversification or increase a bank’s vulnerability to a potential loss of clients or revenues.

6.3%5.3%

6.8%6.4%

6.3%5.9%

7.1%6.1% 5.8%

5.4%6.9%

5.5%8.1%

6.5%

12.6%11.1%

4.5%

8.0% 8.0% 7.5% 7.5% 7.0%6.5% 6.0%

5.5%

0%

2%

4%

6%

8%

10%

12%

14%

Shortage Current minimum With Fed GSIB surcharge

Post-stress CET1 min DFAST Post-stress CET1 min CCAR

NEWS & ANALYSIS Credit implications of current events

20 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

TBC Bank’s Planned Premium London Stock Exchange Listing Is Credit Positive Last Wednesday, JSC TBC Bank (Ba3 stable, ba34) announced a tender offer under which all existing holders of its shares and global depositary receipts (GDRs) are entitled to exchange their holdings for TBC PLC ordinary shares. This is a key step that, if completed successfully, will make TBC PLC (incorporated in England and Wales) the bank’s new holding company and list shares on the London Stock Exchange (LSE) on 10 August 2016.

TBC PLC’s listing on the LSE would be credit positive because it will lead to enhanced transparency and disclosure for the group and ensure adherence to the UK corporate governance code. It would also broaden the bank’s capital and fund-raising options to facilitate business growth.

TBC Bank is the second-largest bank in Georgia and had a domestic market share of 28% of loans and 27% of customer deposits as of 31 March. It has already received irrevocable undertakings and letters of intent to accept the offer that commenced on 2 June and expires on 4 August 2016 from shareholders accounting for 80.8% of the bank’s share capital. This amount would satisfy an 80% threshold required for a successful completion of the share transfer to the UK holding company and subsequent premium listing. The bank has had 70% of its shares quoted on the LSE via global depositary receipts since 2014 (see Exhibit 1).

EXHIBIT 1

TBC Bank’s Current Shareholding Structure Around 70% of TBC Bank’s global depositary receipts are listed on the London Stock Exchange.

Key: EBRD = European Bank for Reconstruction and Development (Aaa stable); IFC = International Finance Corporation (Aaa stable); FMO = Netherlands Development Finance Company (unrated). Source: TBC Bank

The LSE premium listing will require adherence to more rigorous ongoing reporting and compliance obligations than TBC Bank has now, which will lead to increased transparency and enhanced corporate governance infrastructure and processes, which is positive for creditors. For example the UK Corporate Governance Code, to which the company would need to adhere, requires that at least half of the board of directors be independent non-executive directors and that directors should be subject to annual re-election. The group has been working towards the implementation of these new corporate governance requirements over the past several months and is already compliant with most.

Following LSE admission, TBC PLC also intends to seek FTSE Index eligibility. The LSE listing and potential inclusion in the FTSE index will enhance investors’ awareness of TBC Bank, increase stock liquidity and allow it to broaden its investor base, facilitating potential capital increases. Increased awareness subsequent to the full listing could also improve the bank’s market funding access and the pricing of debt issuances. These will

4 The bank ratings shown in this report are the bank’s local-currency deposit rating and baseline credit assessment.

Management4.6%

Founders22.0%

Other3.5%

EBRD12.4%

IFC6.2%

FMO4.4%

Institutional and retail investors47.0%

LSE GDRs69.9%

Alexios Philippides Assistant Vice President - Analyst +357.25.693.031 [email protected]

NEWS & ANALYSIS Credit implications of current events

21 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

allow TBC Bank to continue to capture the significant new business opportunities offered in Georgia and maintain its leading market position.

Although Georgia’s operating environment presents significant challenges, including vulnerably to external shocks, geopolitical risks and a high degree of loan and deposit dollarisation that increases risks for banks, it also presents significant growth opportunities that a strong institutional framework and market-friendly reforms support. The IMF expects Georgia to grow at a faster rate than most regional countries (see Exhibit 2). Financial intermediation remains low in the country; credit equalled 45% of GDP as of December 2014. TBC Bank has grown its loan book by a compound annual growth rate of 22% between 2012 and 2015 and targets a growth rate of around 20% per year.

EXHIBIT 2

Georgia’s Average Annual Real GDP Growth 2010-15 and Forecast GDP Growth 2016-21 The IMF expects Georgia’s economy to grow at a faster rate than its regional peers.

Source: International Monetary Fund, World Economic Outlook Database April 2016

0%

1%

2%

3%

4%

5%

6%

Georgia Armenia Kazakhstan Moldova Russia Poland Romania Serbia Estonia Latvia

Average Annual Real GDP Growth Forecasted Average Annual GDP Growth

NEWS & ANALYSIS Credit implications of current events

22 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Investec plc Share Placement Improves Quality of Capital, a Credit Positive Last Thursday, Investec plc (Baa1stable) raised additional equity share capital of £138.3 million, or 4.99% of existing share capital. The additional capital will be utilised to fund the tender of existing preference shares. Under Capital Requirements Directive IV (CRD IV) capital rules, the capital calculation contribution to Investec plc from these preference shares is being phased out. With this capital raise (holding all else equal), Investec plc’s common equity Tier 1 (CET1) capital will rise to 10.4% (including the deduction of foreseeable dividends) from 9.3% at 31 March 2016. Investec’s increased CET1 capital position is credit positive for bondholders and improves the overall quality of its capital.

The UK’s Prudential Regulation Authority required Investec plc to replace share capital equivalent to the preference shares to proceed with the tender offer. This action brings capital levels above the group’s announced March 2016 CET1 target of 10%. During fiscal 2016 (ending 31 March 2016), Investec plc’s CET1 ratio fell by 40 basis points because of 5.9% growth in risk-weighted assets, largely because of increased secured corporate and residential real estate lending.

The tender offer, depending on the level of investor takeup, will reduce the subordination and loss absorbency the preference shares provide. Given the amounts considered in the tender offer, our loss given failure (LGF) analysis shows no material effect on the loss absorbency for senior creditors of either Investec plc or Investec Bank plc (IBP, A2/A2 stable, baa25). This is partly because of the existing levels of subordination in Investec’s balance sheet, as well as the loss absorbency provided by Investec Asset Management. In the event of a resolution of Investec plc’s main operating subsidiary, IBP, we would expect a potential distressed sale of Investec Asset Management to generate sufficient resources to reduce losses for senior holding company creditors.

The take out of the preference shares was unsurprising given their limited future utility as qualifying capital under the CRD IV capital rules. While optimising its capital structure, Investec plc is also likely to profit from this capital management exercise, depending upon the extent of take up among preference share investors. Through the tender offer, Investec is buying back its Sterling Preference Shares at a discount to their original issuance price.

5 The ratings shown are Investec PLC’s deposit rating and senior unsecured debt rating, and its baseline credit assessment.

Michael C. Eberhardt, CFA Vice President - Senior Credit Officer +44.20.7772.8611 [email protected]

Maxwell Price Associate Analyst +44.20.7772.1778 [email protected]

NEWS & ANALYSIS Credit implications of current events

23 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Vietnam’s Tighter Bank Liquidity and Lending Rules Are Credit Positive On 27 May, the State Bank of Vietnam (SBV) tightened its regulations on asset-liability management and real estate loans. Although the new rules are not as strict as those proposed in February, they will still be credit positive for Vietnamese banks because they will support liquidity and limit the banks’ exposure to the high-risk real estate sector.

The new rules will help moderate banks’ credit growth in the system, particularly in the real estate sector. Vietnam’s real estate sector has historically posed significant risks to banks, with the 2008-11 credit boom driven by rapid lending to this sector that culminated in heavy losses for banks. Although credit growth to the real estate sector of around 15% in 2015 was significantly lower than in 2008-11, the central bank is taking preemptive steps to limit the banks’ appetite for lending to this high-risk sector.

The new asset-liability management rule will lower the current 60% maximum ratio for short-term funding for loans longer than 12 months to 50% by the end of 2016 and to 40% by the end of 2017. This is a longer transition period than the SVB’s initial proposal to lower the maximum ratio to 40% by the end of this year. The new rule will compel banks with sizable shares of longer-dated loans to slow their credit growth or shift their focus to shorter-term loans, which will benefit their liquidity. Banks also have the option to attract longer-term funding to finance longer-term loans, but they are unlikely to find success because of higher funding costs and the intense competition for long term deposits.

Exhibit 1 shows our calculations of the share of short-term funds used for loans longer than 12 months by the Vietnamese banks we rate. Vietnam Prosperity Jt. Stk. Commercial Bank (VPB, B3 stable, caa16) and Vietnam International Bank (B2 positive, b3) had the highest share of short-term funds used for loans longer than 12 months. This suggests these banks have weaker maturity matching of their assets and liabilities than their peers. At the end of March 2016, the SBV reported that the short-term funding ratio for loans longer than 12 months was 34% for state banks and 36% for joint-stock commercial banks.

EXHIBIT 1

Vietnamese Banks’ Ratio of Short-Term Funding Used for Loans Longer than 12 Months

Key: VPB = Vietnam Prosperity Jt. Stk. Commercial Bank; TCB = Vietnam Technological and Comm'l JSB; VIB = Vietnam International Bank; Sacombank = Saigon Thuong Tin Commercial Joint Stock Bank; SHB = Saigon - Hanoi Commercial Joint Stock Bank; ABB = An Binh Commercial Joint Stock Bank; ACB = Asia Commercial Bank; Vietinbank = Vietnam Bank for Industry and Trade; BIDV = Bank for Investment and Development of Vietnam; MB = Military Commercial Joint Stock Bank. Note: Latest available data; SBV calculates the ratio as the sum of medium-term loans + long-term loans - medium-term funds - long-term funds as a percent of short-term funds. Sources: The banks and Moody’s Investors Service

6 The bank ratings shown in this report are the bank’s deposit rating, senior unsecured debt rating (where available) and baseline

credit assessment.

43%40% 39%

37% 37%

27%23%

21% 21%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Dec-15 Dec-15 Dec-15 Dec-14 Dec-15 Dec-15 Dec-15 Dec-15 Dec-14 Dec-14

VPB VIB TCB Sacom SHB BIDV ACB Vietin ABB MB

Daphne Cheng Analyst +65.6398.8339 [email protected]

Eugene Tarzimanov Vice President - Senior Credit Officer +65.6398.8329 [email protected]

Dan Pek Associate Analyst +65.6311.2601 [email protected]

NEWS & ANALYSIS Credit implications of current events

24 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

The SVB also raised the risk weights for real estate loans to 200% by the end of 2016 from 150% currently. Although this increase is lower than the 250% risk weight that the SBV proposed in February, the new rule will limit banks’ appetite to lend to this high-risk sector, given banks’ already-weak capital ratios.

As shown in Exhibit 2, Vietnamese banks most affected by the higher risk weightings are VPB and Saigon-Hanoi Commercial Joint Stock Bank (B3 stable, caa1), owing to their sizable exposures to the real estate sector. Their already-weak capital ratios, which reflect both higher credit costs and a rebound in credit growth, mean the new guidelines will compel these banks to either reduce their exposure to the real estate sector or significantly slow their credit expansion.

EXHIBIT 2

Vietnamese Banks’ Tangible Common Equity as a Percent of Risk-Weighted Assets Currently and Pro-Forma Higher Real Estate Risk Weights

Key: VPB = Vietnam Prosperity Jt. Stk. Commercial Bank; TCB = Vietnam Technological and Comm'l JSB; VIB = Vietnam International Bank; Sacombank = Saigon Thuong Tin Commercial Joint Stock Bank; SHB = Saigon - Hanoi Commercial Joint Stock Bank; ABB = An Binh Commercial Joint Stock Bank; ACB = Asia Commercial Bank; Vietinbank = Vietnam Bank for Industry and Trade; BIDV = Bank for Investment and Development of Vietnam; MB = Military Commercial Joint Stock Bank. Sources: The banks and Moody's Investors Service

-23bps

-9bps

-20bps -49bps

-16bps -45bps-25bps

-12bps

-54bps

0%

2%

4%

6%

8%

10%

12%

14%

Curr

ent

Pro-

Form

a

Curr

ent

Pro-

Form

a

Curr

ent

Pro-

Form

a

Curr

ent

Pro-

Form

a

Curr

ent

Pro-

Form

a

Curr

ent

Pro-

Form

a

Curr

ent

Pro-

Form

a

Curr

ent

Pro-

Form

a

Curr

ent

Pro-

Form

a

ABB ACB BIDV SHB Sacom Techcom Vietin VIB VPB

NEWS & ANALYSIS Credit implications of current events

25 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

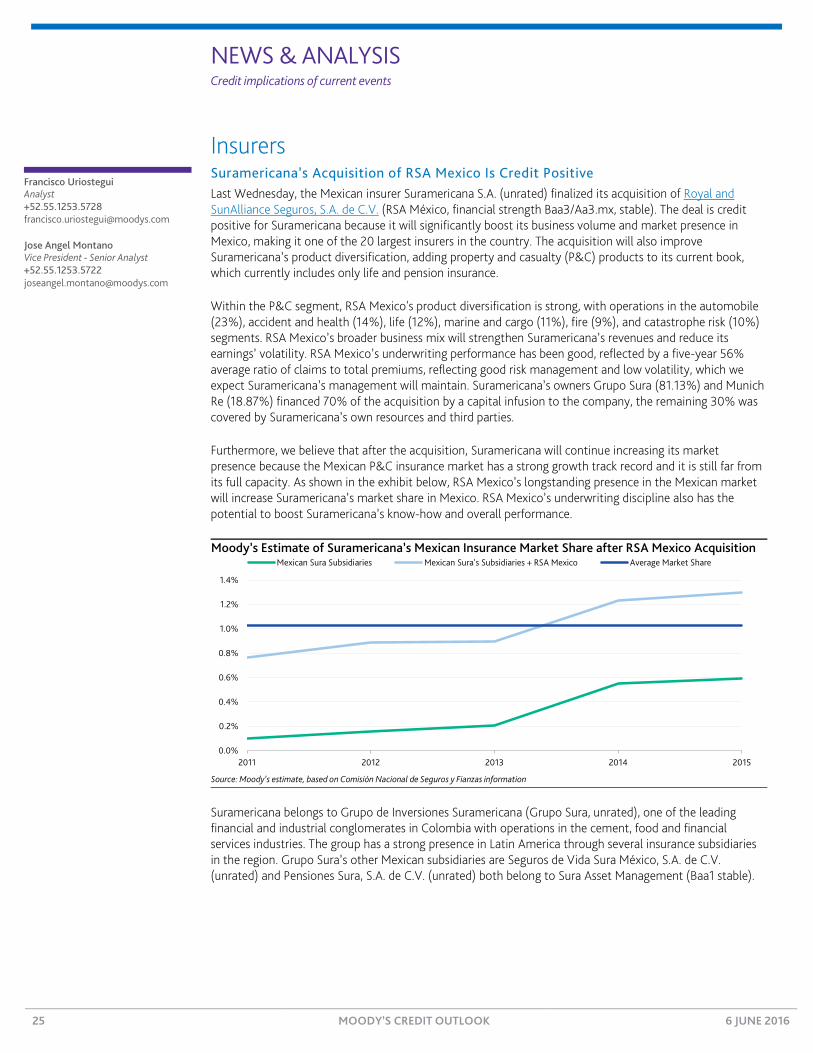

Insurers Suramericana’s Acquisition of RSA Mexico Is Credit Positive Last Wednesday, the Mexican insurer Suramericana S.A. (unrated) finalized its acquisition of Royal and SunAlliance Seguros, S.A. de C.V. (RSA México, financial strength Baa3/Aa3.mx, stable). The deal is credit positive for Suramericana because it will significantly boost its business volume and market presence in Mexico, making it one of the 20 largest insurers in the country. The acquisition will also improve Suramericana’s product diversification, adding property and casualty (P&C) products to its current book, which currently includes only life and pension insurance.

Within the P&C segment, RSA Mexico's product diversification is strong, with operations in the automobile (23%), accident and health (14%), life (12%), marine and cargo (11%), fire (9%), and catastrophe risk (10%) segments. RSA Mexico’s broader business mix will strengthen Suramericana’s revenues and reduce its earnings’ volatility. RSA Mexico’s underwriting performance has been good, reflected by a five-year 56% average ratio of claims to total premiums, reflecting good risk management and low volatility, which we expect Suramericana’s management will maintain. Suramericana’s owners Grupo Sura (81.13%) and Munich Re (18.87%) financed 70% of the acquisition by a capital infusion to the company, the remaining 30% was covered by Suramericana’s own resources and third parties.

Furthermore, we believe that after the acquisition, Suramericana will continue increasing its market presence because the Mexican P&C insurance market has a strong growth track record and it is still far from its full capacity. As shown in the exhibit below, RSA Mexico’s longstanding presence in the Mexican market will increase Suramericana’s market share in Mexico. RSA Mexico’s underwriting discipline also has the potential to boost Suramericana’s know-how and overall performance.

Moody’s Estimate of Suramericana’s Mexican Insurance Market Share after RSA Mexico Acquisition

Source: Moody’s estimate, based on Comisión Nacional de Seguros y Fianzas information

Suramericana belongs to Grupo de Inversiones Suramericana (Grupo Sura, unrated), one of the leading financial and industrial conglomerates in Colombia with operations in the cement, food and financial services industries. The group has a strong presence in Latin America through several insurance subsidiaries in the region. Grupo Sura’s other Mexican subsidiaries are Seguros de Vida Sura México, S.A. de C.V. (unrated) and Pensiones Sura, S.A. de C.V. (unrated) both belong to Sura Asset Management (Baa1 stable).

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

2011 2012 2013 2014 2015

Mexican Sura Subsidiaries Mexican Sura's Subsidiaries + RSA Mexico Average Market Share

Francisco Uriostegui Analyst +52.55.1253.5728 [email protected]

Jose Angel Montano Vice President - Senior Analyst +52.55.1253.5722 [email protected]

NEWS & ANALYSIS Credit implications of current events

26 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

Sovereigns Japan’s Consumption Tax Delay Makes Fiscal Goals More Challenging Last Wednesday, Japanese Prime Minister Shinzo Abe announced that he would postpone a hike in the consumption tax to October 2019, and said that he would unveil a fiscal stimulus package this fall. The announcement is credit negative for Japan (A1 stable) because it will likely prevent Japan from meeting its fiscal targets, which we considered optimistic even before the announcement of the delay. By delaying the tax hike, we estimate that the administration will forego additional revenues worth around 1.0% of GDP per year. The stimulus will constitute a further unknown cost.

The increase in the consumption tax to 10% from the current 8% was due to take effect in April 2017. That itself marked a delay from the original implementation date of October 2015. Mr. Abe’s rationale for the plan change was the persistent weakness of Japan’s economy, noting the effect of recent earthquakes in the southern island of Kyushu and broader pressures on global growth. He said he would use Upper House elections in the summer to confirm the Japanese public’s trust in his decision.

Some aspects of the country’s fiscal profile have improved since 2014, when Mr. Abe first made the decision to postpone the consumption tax increase to 10%. We estimate that the budget deficit tightened to 5.2% in 2015, half of its peak six years earlier. The last consumption tax increase, to 8% from 5% in April 2014, significantly bolstered revenues: consumption tax was by far the biggest contributor to growth in central government tax intake in 2015. Tax revenues as a whole are at their highest as a share of GDP and in yen terms since late 1992 (see Exhibit 1).

EXHIBIT 1

Japan’s Tax Receipts Four-quarter moving sum, tax revenue includes general and special accounts.

Sources: Japanese Cabinet Office, Haver Analytics and Moody’s Investors Service

Interest payments as a portion of revenues have also been declining. Nevertheless, Japan’s central government debt burden, at 248.1% of GDP in 2015, according to International Monetary Fund estimates, remains the highest among rated sovereigns.

The change of plan illustrates the scale of the challenge Japan’s government faces in achieving its fiscal objectives, specifically its goals of a primary deficit of 1.0% of GDP by the fiscal year starting April 2018 and a primary surplus by fiscal year starting April 2020. The prospective easing in fiscal policy also acknowledges that monetary policy has not yet revived the economy, and that fiscal tightening measures could counter efforts to spur growth. Consumer spending has struggled to regain traction since an earlier tax hike, although it shows signs of bottoming out (see Exhibit 2).

¥0

¥10

¥20

¥30

¥40

¥50

¥60

¥70

0%

2%

4%

6%

8%

10%

12%

14%

16%

81-Q

1

82-Q

1

83-Q

1

84-Q

1

85-Q

1

86-Q

1

87-Q

1

88-Q

1

89-Q

1

90-Q

1

91-Q

1

92-Q

1

93-Q

1

94-Q

1

95-Q

1

96-Q

1

97-Q

1

98-Q

1

99-Q

1

00-Q

1

01-Q

1

02-Q

1

03-Q

1

04-Q

1

05-Q

1

06-Q

1

07-Q

1

08-Q

1

09-Q

1

10-Q

1

11-Q

1

12-Q

1

13-Q

1

14-Q

1

15-Q

1

¥ Tr

illio

ns

Percent of GDP - left axis Amount - right axis

Christian de Guzman Vice President - Senior Credit Officer +65.6398.8327 [email protected]

Matthew Circosta Associate Analyst +65.6398.8324 [email protected]

NEWS & ANALYSIS Credit implications of current events

27 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

EXHIBIT 2

Japan’s Nominal Consumer Spending Before and After Tax Hikes Year-over-year change, four-quarter moving average.

Note: t0 = introduction of tax hike in April 1997 and April 2014, t- = the quarters prior to the tax hike, and t+ = the quarters after the tax hike. Sources: Japan Cabinet Office, Haver Analytics and Moody’s Investors Service

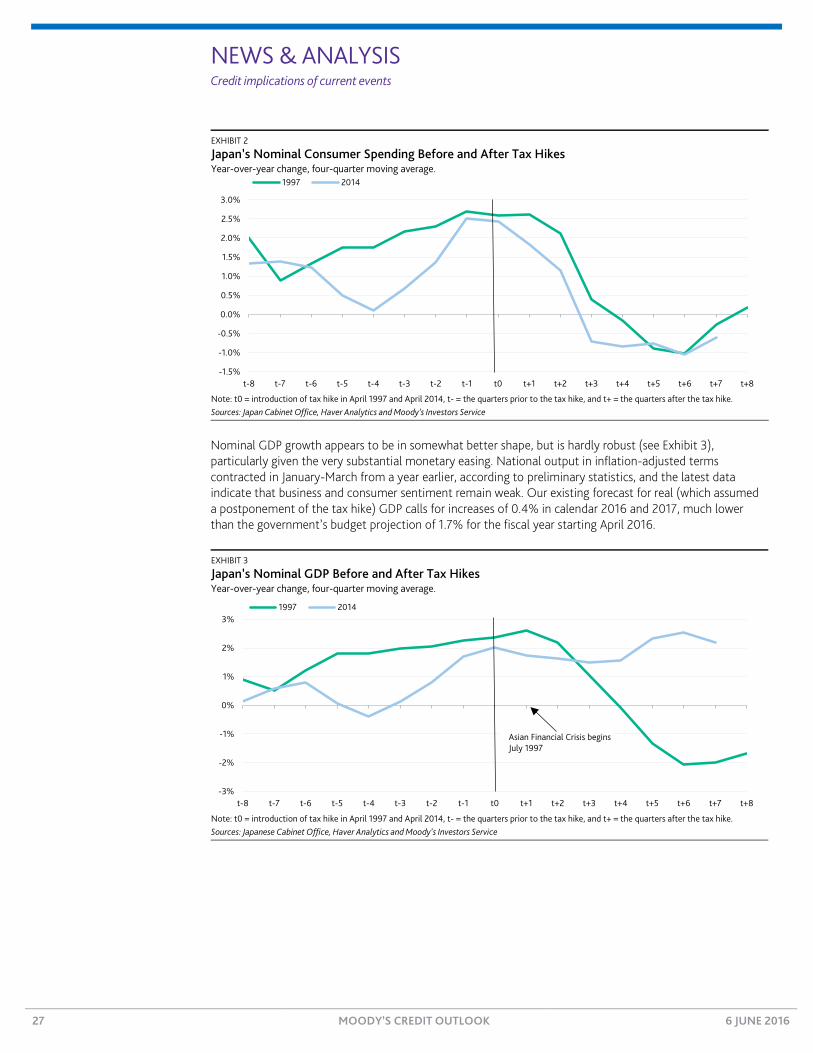

Nominal GDP growth appears to be in somewhat better shape, but is hardly robust (see Exhibit 3), particularly given the very substantial monetary easing. National output in inflation-adjusted terms contracted in January-March from a year earlier, according to preliminary statistics, and the latest data indicate that business and consumer sentiment remain weak. Our existing forecast for real (which assumed a postponement of the tax hike) GDP calls for increases of 0.4% in calendar 2016 and 2017, much lower than the government’s budget projection of 1.7% for the fiscal year starting April 2016.

EXHIBIT 3

Japan’s Nominal GDP Before and After Tax Hikes Year-over-year change, four-quarter moving average.

Note: t0 = introduction of tax hike in April 1997 and April 2014, t- = the quarters prior to the tax hike, and t+ = the quarters after the tax hike. Sources: Japanese Cabinet Office, Haver Analytics and Moody’s Investors Service

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

t-8 t-7 t-6 t-5 t-4 t-3 t-2 t-1 t0 t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8

1997 2014

-3%

-2%

-1%

0%

1%

2%

3%

t-8 t-7 t-6 t-5 t-4 t-3 t-2 t-1 t0 t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8

1997 2014

Asian Financial Crisis begins July 1997

NEWS & ANALYSIS Credit implications of current events

28 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

US Public Finance Housing Finance Agencies See HUD Position on Down Payment Assistance as Credit Positive On 25 May, Ed Golding, head of the US Department of Housing and Urban Development (HUD) Federal Housing Administration, released a memo stating “loans that include down payment assistance provided by state and local housing finance agencies continue to be eligible for [Federal Housing Administration] insurance.” The memo appears to resolve the long-running internal dispute at the HUD about whether local and state housing finance agencies (HFAs) can maintain their current down payment assistance (DPA) programs for loans with Federal Housing Administration insurance. The announcement is credit positive for HFAs because the dispute had the potential to curtail their use of DPA and reduce loan originations.

The dispute between HUD management and HUD’s Office of the Inspector General raised doubts about the legality of HFAs charging slightly higher interest rates on Federal Housing Administration-insured loans with DPA. We understand that although Mr. Golding’s memo presents HUD’s position in favor of HFAs’ DPA programs, HUD’s independent inspector general continues to disagree with HUD’s position, preserving a degree of uncertainty for HFAs. DPA is a major part of most HFAs’ affordable housing lending activities. For instance, as of 31 December 2015, 32 of the 44 state HFAs we rate provide DPA to more than 50% of their borrowers (see exhibit).

Percentage of State HFA Borrowers Receiving Down Payment Assistance at Year-end 2015

Source: Moody’s Investors Service Housing Finance Agency Survey

Under Federal Housing Administration rules, borrowers with mortgage loans insured by the agency must make a down payment of at least 3.5% of the value of the property. However, coming up with the funds needed for a down payment can be difficult for the low- to moderate- income, first-time homebuyers eligible for Federal Housing Administration insurance. As a result, HFAs provide DPA to certain borrowers. In addition to fulfilling their mission, DPA is a way in which HFAs can remain competitive with conventional lenders, facilitate their lending activities and enhance their financial strength. Their usual approach of offering lower interest rate loans funded with tax-exempt bonds is less effective in the current low interest rate environment.

Loan originations are the primary means by which HFAs generate revenue and maintain and enhance their financial stability. HFAs fund their DPA programs in part through charging slightly higher interest rates on loans with down payment assistance. The additional revenue is used by the HFAs to recoup some of the DPA they provide.

5

7

8

11

13

0

2

4

6

8

10

12

14

0% - 25% 26% - 50% 51% - 75% 76% - 90% >90%

Num

ber o

f Sta

te H

FAs

Percent of State HFA Borrowers Receiving DPA

David Teicher Senior Vice President +1.212.553.1385 [email protected]

NEWS & ANALYSIS Credit implications of current events

29 MOODY’S CREDIT OUTLOOK 6 JUNE 2016

The controversy about Federal Housing Administration insurance and DPA began in July 2015 when HUD’s Office of the Inspector General published an audit report with findings that a private lender violated certain mortgage insurance rules when originating Federal Housing Administration-insured loans in connection with two local affordable housing financing programs in Arizona. While the Inspector General’s office acknowledged that it is permissible for a lender to charge higher interest rates in exchange for covering borrower closing costs (so-called premium pricing), it concluded that the lender impermissibly used premium pricing for loans originated with down payment assistance.

Later in July and August 2015, Mr. Golding released a memo and the HUD general counsel released an opinion supporting the DPA programs in question and disagreeing with the conclusions of HUD’s Office of the Inspector General. The controversy intensified last month when HUD’s Office of the Inspector General issued a subpoena to eHousingPlus, which manages programs for certain local housing finance agencies, seeking documents in connection with Federal Housing Administration-insured loans, where borrowers received DPA provided by an HFA.

NEWS & ANALYSIS Credit implications of current events

30 MOODY’S CREDIT OUTLOOK 6 JUNE 2016