Embed Size (px)

Citation preview

MOODYS.COM

24 AUGUST 2015

NEWS & ANALYSIS Corporates 2 » Valeant’s Acquisition of Sprout Delays Deleveraging, a

Credit Negative » Pentair’s Planned Acquisition of ERICO Is Credit Negative » NN’s Planned Acquisition of Precision Engineered Products Is

Credit Negative » Surgery Partners’ Plan to Repay Debt Through IPO Is

Credit Positive » US Regulator Denies DISH Affiliates $3.3 Billion of Discounts, a

Credit Negative » Kirin’s Acquisition of Myanmar Brewery Is Credit Positive » Brookfield Infrastructure Partners’ Proposed Acquisition of

Asciano Is Credit Negative

Infrastructure 9 » Energisa’s Acquisition of Celg Would Materially Increase

Leverage, a Credit Negative

Banks 10 » By Selling, National Penn Solves a Credit-

Negative Predicament » Brazil’s Government Banks Extend Below-Market Credit Lines

to Auto Industry, a Credit Negative » Kazakhstan’s Currency Depreciation Is Credit Negative

for Banks » China Strengthens the Capital Base of Two Policy Lenders, a

Credit Positive

Insurers 16 » Higher Accident Frequency Is Credit Negative for US

Auto Insurers » Mexico City’s New Transit Regulation Is Credit Positive

for Insurers

Sovereigns 19 » Ecuador’s Reduced Spending Amid Difficult Economic

Environment Is Credit Positive » Greek Prime Minister Resigns, Clearing the Way for a

Stronger Government » Kazakhstan’s Flexible Currency Will Help Economy Adjust to

Lower Oil Prices » Israel’s Second-Quarter Slump Suggests Fragile Government

Majority Will Face Economic Headwinds » Sri Lanka’s Election Outcome Improves the Government’s

Ability to Pass Credit-Positive Reforms

Sub-sovereigns 27 » Financial Discipline Law for Mexican Sub-sovereigns Would Be

Credit Positive

RATINGS & RESEARCH Rating Changes 29

Last week we downgraded ConocoPhillips, Samson Investment Company, SandRidge Energy, Voya Holdings, two US RMBS and three US CMBS, and upgraded Consort Healthcare (Mid Yorkshire) Funding, Bank of Shanghai, Kuwait Insurance Company, 14 US RMBS and two US CMBS, among other rating actions.

Research Highlights 33

Last week we published on US payment systems, global midstream energy, Americas oil and gas, Chinese property developers, Chilean corporates and banks, US medical products and devices, EMEA and Asia building materials, European paper and forest products, Korean refiners, US speculative-grade energy issuers, Slovenian banks, US life insurers, US prime money market funds, Brazil, African Development Bank, Eastern and Southern African Trade and Development Bank, India, Jordan, Estonia, Mexican sub-sovereigns, British Columbia local governments and government-related issuers, global colleges, state housing finance agencies, letter-of-credit-backed muni transactions, Texas higher education, US CLOs, Norwegian covered bonds, US credit card ABS, Japanese credit card ABS and Russian ABS , among other reports.

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Thursday’s Credit Outlook 39 » Go to Last Thursday’s Credit Outlook

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Corporates

Valeant’s Acquisition of Sprout Delays Deleveraging, a Credit Negative Last Thursday, specialty pharmaceutical company Valeant Pharmaceuticals International, Inc. (Ba3 positive) announced that it would acquire privately owned Sprout Pharmaceuticals, Inc. (unrated) for approximately $1 billion plus a portion of future profits. The transaction is credit negative because it delays the debt reduction that we expected following earlier debt-financed acquisitions. Valeant’s rating outlook remains positive because strong organic EBITDA growth will result in deleveraging over the next 12-18 months.

The Sprout acquisition differs from many of Valeant’s previous acquisitions in that there is currently no EBITDA at the target, and cost synergies are not a major driver of the rationale or valuation. Instead, there is significant upside to Valeant in the commercial potential of Addyi, a new product to treat hypoactive, or low, sexual desire in women, and which the US Food and Drug Administration approved last Tuesday.

We expect Valeant to experience modest EBITDA burn over the next several months as it ramps up expenses to bring Addyi to market, most likely in the fourth quarter of 2015. Being the first drug of its kind to help women with female sexual dysfunction, Addyi has the potential to provide Valeant with substantial cash flow if successfully commercialized. A successful launch would also help solidify a women’s health platform at Valeant.

Addyi is Sprout’s only product in the market or in development. It acquired the drug from Boehringer Ingelheim in 2012. The FDA, in two previous review cycles, declined to approve the drug based on the then-available efficacy and safety data.

Given Valeant’s $10 billion revenue base, it will take several years before Addyi moves the needle on the company’s overall financial profile. Despite the approval, successful commercialization of the drug is not guaranteed. Although the target market is sizable and there are no approved treatments, Addyi comes with a black box warning related to side effects. For example, the use of Addyi and alcohol increases the risk of severe hypotension and syncope (fainting); therefore, alcohol use is contraindicated. Because of its side effects, the Addyi approval includes a Risk Evaluation and Mitigation Strategy, which requires prescribers and pharmacies to be certified. We expect that Valeant’s expertise in successfully marketing pharmaceutical products such as Jublia, a treatment for toenail fungus, will help it commercialize Addyi.

The Sprout acquisition follows Valeant’s recent acquisition of Egypt-based Amoun Pharmaceutical for approximately $800 million plus contingent payments. The deal further delays deleveraging associated with Valeant’s $16 billion, debt-funded acquisition of Salix Pharmaceuticals on 1 April 2015. We expect that a portion of Valeant’s funding for the Sprout acquisition will be through revolver borrowings. Valeant’s pro forma debt/EBITDA is approximately 6.5x before synergies, and 6.0x with synergies – both very high for the current rating level. Our rating and positive outlook incorporate our expectation of rapid deleveraging from both debt reduction and EBITDA growth. Management has stated a target of reducing adjusted debt/EBITDA to 4.0x by year-end 2016 and this remains attainable.

Valeant’s strong EBITDA growth provides a key source of deleveraging – and this will benefit from the FDA’s recent approval of Xifaxan, a product to treat irritable bowel syndrome. However, if EBITDA growth is the only source of Valeant’s deleveraging, the timing of any rating upgrade could be significantly prolonged.

Michael Levesque, CFA Senior Vice President +1.212.553.4093 [email protected]

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Pentair’s Planned Acquisition of ERICO Is Credit Negative Last Monday, Pentair plc, which issues debt through its Pentair Finance SA (Baa2 review for downgrade) subsidiary, said that it had agreed to acquire ERICO International Corp. (unrated) for $1.8 billion in cash. The planned transaction is credit negative because the company plans to fund the entire purchase with nearly $2 billion of incremental debt. Following the announcement of the deal, we placed Pentair Finance’s ratings under review for downgrade.

Pentair expects to close the transaction by the end of the year. We expect the acquisition to increase pro forma debt/EBITDA to more than 4x from about 3x as of 30 June 2015, with free cash flow/debt falling to the 4%-6% range from nearly 8%.

The steep decline in oil prices hobbled Pentair’s operating performance during the first half of 2015. The company’s valves and controls segment and flow and filtration segment, which together account for roughly 50% of the company’s revenues, are experiencing headwinds, with the former facing more serious, fundamental challenges. Oil- and gas-related revenues, which account for roughly 20% of total revenues, continue to weaken owing to project delays and cancellations, resulting in excess capacity and increasing price competition. The energy sector’s outlook over the next six to 12 months is very weak with no catalyst for improvement on the horizon.

Several key industrial end markets are also softening, resulting in a pullback in capital expenditures. In anticipation of continued weak volumes and volatility, the company is accelerating its efforts to reduce costs. Pentair has highly effective lean initiatives and has been successful at integrating acquisitions, such Tyco Flow Control. Although we do not expect these more recent initiatives to gain traction until 2016, margins and cash flow generation should be solid for 2015, with adjusted free cash flow likely to exceed $300 million.

These pressures, in conjunction with a steady rise in debt since the end of 2012, have weakened Pentair’s position in the Baa2 rating level. Furthermore, the new debt that Pentair is taking on to finance the ERICO acquisition comes at a time when its business model is vulnerable, raising the company’s risk profile. However, we expect that any potential downgrade would be limited to one notch, based on our expectation that Pentair will use most of its substantial free cash flow to reduce debt.

Eric Greaser Vice President - Senior Analyst +1.212.553.6031 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

NN’s Planned Acquisition of Precision Engineered Products Is Credit Negative On Monday, NN, Inc. (B2 stable) said that it had agreed to acquire Precision Engineered Products Holdings, Inc. (B1 stable) for $615 million in cash. The planned purchase is credit negative because NN will fund the deal with incremental debt, which will increase leverage.

NN expects to close the transaction by the end of October. This is a sizable acquisition for NN, and is about twice the price of its $300 million purchase of Autocam Corp. in 2014. Assuming that NN uses some of its cash on hand to finance the Precision acquisition, we expect pro forma leverage to increase to about 5.2x (including certain adjustments) from about 4.0x in June, before a recent debt paydown. With further growth and synergies, we expect NN to reduce debt/EBITDA after the Precision acquisition to below 5.0x by the end of 2016.

Upon completion of the Precision acquisition, NN’s annual revenue will increase to more than $900 million from about $660 million on a pro forma basis. The greater scale carries integration risks. Along with completing the integration of Autocam, the purchase will bring overlapping transportation and industrial businesses. NN has indicated that certain of Precision’s management will remain in place. Yet, there will be a number of moving parts, including consolidating financial reporting systems, purchasing and customer relationships.

The combination of the two companies will provide the benefit of customer end market diversification, expanding NN’s markets into the medical/surgical device and electrical markets. We expect sales to the light vehicle original equipment market to decline to about 54% of total sales from 70%. Other end markets served by the company will include aerospace/general industrial (19%), medical (12%), electrical (9%) and commercial transportation (6%).

Timothy Harrod Vice President - Senior Credit Officer +1.212.553.4488 [email protected]

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Surgery Partners’ Plan to Repay Debt Through IPO Is Credit Positive Last Monday, Surgery Center Holdings Inc. (B3 negative), also known as Surgery Partners, filed plans to sell shares of its common stock in an initial public offering (IPO). The proposed IPO is credit positive for Surgery Partners because it would lead to a meaningful reduction in debt, which would reduce downward pressure on its rating based on an existing debt load that is very high relative to its earnings.

Surgery Partners indicated that the proposed size of its offering would be approximately $431 million and specified that it plans to use the IPO proceeds to partially repay its $490 million senior secured second-lien term loan. We estimate that if Surgery Partners successfully completes its IPO and uses the proceeds to pay down its debt as planned, its pro forma debt/EBITDA would improve to 6.0x-6.5x for the period ended 30 June 2015 from about 8.7x. If these plans come to fruition, we would likely revise the rating outlook to stable from negative.

Going public would broaden Surgery Partners’ sources of capital for future funding requirements, including acquisitions. This is credit positive for a company that in the past has shown itself willing to increase leverage to high levels to fund acquisitions and shareholder-friendly financial policies. Earlier this year, Surgery Partners significantly increased its leverage to acquire Symbion Inc. for $792 million, which caused us to change its outlook to negative from stable.

Although an IPO is positive for Surgery Partner’s overall credit profile, changes in its capital structure could result in lower loss absorption for first-lien creditors. We estimate that if Surgery Partners were to repay more than $80 million on the second-lien term loan, it would result in a downgrade to B2 from B1 on the ratings of its senior secured first-lien credit facilities. This is because we expect the second-lien term loan to absorb losses before the first-lien loan. The remaining facilities would also constitute the preponderance of debt in Surgery Partners’ capital structure.

Surgery Partners, an operator of short-stay surgical facilities and physician practices, is primarily owned by private-equity firm H.I.G. Capital.

Ron Neysmith Vice President - Senior Analyst +1.212.552.1364 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

US Regulator Denies DISH Affiliates $3.3 Billion of Discounts, a Credit Negative Last Monday, the US Federal Communications Commission denied $3.3 billion in small-business discounts to two affiliates of DISH Network Corporation that had won government auctions for wireless-spectrum licenses in January, saying the companies did not qualify. The decision is credit negative for the company and will result in significant cash outlays that will weaken the balance sheet and liquidity and could ultimately pressure the ratings of subsidiary DISH DBS Corporation (Ba3 negative).

DISH Network, through its unrated affiliates SNR Wireless and Northstar Wireless, won the auction for AWS-3 spectrum licenses with a $13.3 billion bid. The companies claimed $3.3 billion in small-business discounts, making the licenses’ total purchase price approximately $10 billion, which was funded using most of DISH Network’s cash. However, the FCC has concluded that because the affiliates are essentially controlled by the much larger DISH Network, they are not eligible for the discounts.

This is a financial setback for DISH Network and payment of the remaining $3.3 billion would be a significant drain on its liquidity and an increase in debt leverage could lead to a downgrade for DISH DBS, the satellite broadcaster, depending on how the company chooses to fund it and manage its subsidiary’s balance sheet and credit metrics.

If the additional cost is financed by raising debt at DISH DBS, it would pressure the Ba3 corporate family rating, with Moody’s-adjusted debt/EBITDA leverage climbing to more than 5.5x from 4.6x as of 31 March 2015. If leverage remains at this level, it may prompt a review for downgrade of its Ba3 corporate family rating and bond ratings. Incremental debt at DISH DBS would weaken its credit quality, which is already constrained as a result of uncertainty about its DISH Network’s wireless strategy.

Should the transaction be funded by borrowing at DISH Network’s subsidiaries, where the spectrum assets are held, it would still be unfavorable for DISH DBS bondholders if the pay-TV business has to service the new debt. However, the financing would be credit neutral if the debt raised at the spectrum companies is over-collateralized to cover interest payments and if the debt instrument has a maturity of at least 10 years, such that DISH DBS is less likely to be required to repay the obligation over the next five years.

Alternatively, if the company puts in place guarantees from DISH Network, the parent, or the spectrum subsidiary for debt issued by DISH DBS, we believe it would mitigate the adverse effect of the additional debt and the guarantees would enhance DISH DBS’ credit quality given the spectrum’s considerable value.

Currently, all debt at DISH DBS is guaranteed by its subsidiaries, but not by DISH Network, and DISH DBS creditors have no recourse to assets held outside of DISH DBS. Consequently, the creditors remain exposed to the risk of cash being upstreamed to DISH Network from DISH DBS to fund transactions like this one and its future wireless strategy without any legal recourse to those assets. Therefore, we would view any downstream guarantees by DISH Network or guarantees from the spectrum subsidiary to DISH DBS as credit positive since DISH DBS creditors would then have a claim on the spectrum assets or equity value. If these issues are not appropriately addressed to protect the interests of DISH DBS bondholders, the incurrence of additional debt to fund the transaction would likely lead to a ratings downgrade.

Neil Begley Senior Vice President +1.212.553.7793 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Kirin’s Acquisition of Myanmar Brewery Is Credit Positive Last Wednesday, Kirin Holdings Company, Limited (A3 stable) said that it had acquired a 55% stake in Myanmar Brewery Limited (unrated) from Singapore food and beverage conglomerate Fraser and Neave Limited (unrated) for $560 million, financed entirely with debt. The acquisition is credit positive for Kirin, a holding company that owns Japan’s second-largest producer of alcoholic beverages by volume and is a major non-alcoholic beverage producer, because the strategic merits outweigh the effects of a slight increase in leverage. We affirmed Kirin’s ratings and outlook after the deal announcement.

Pro forma for the acquisition, Kirin’s leverage will rise to 3.4x from 3.2x for the 12 months that ended June 2015, based on Kirin’s EBITDA for the 12 months to June 2015, Myanmar Brewery’s EBITDA for the 12 months to September 2014, and the additional debt. However, we also expect that Kirin will derive additional profit from Myanmar Brewery and Kirin’s continued focus on debt reduction over the next 12 months will mitigate the increased leverage.

Myanmar Brewery has an 86% market share and a strong distribution network in Myanmar. Supported by its market position and robust growth in domestic demand, it is highly profitable and had a 35% EBITDA margin for the fiscal year that ended September 2014, according to Kirin. This is substantially higher than Kirin’s own reported EBITDA margin of 12% for the 12 months to June 2015. Myanmar Brewery also had a net cash position as of September 2014.

The purchase price was 10x Myanmar Brewery’s EBITDA for the 12 months to September 2015, which is lower than recent beverage industry acquisitions in Asia at multiples of 15x or more.

The acquisition is in a new market with country risk and a developing infrastructure, which presents operational challenges for Kirin. But it will help Kirin establish a foothold in the growing Myanmar market. According to Kirin, the total beer market in the country grew by more than 30% annually in 2013 and 2014, mirroring Myanmar Brewery’s sales and profit growth.

We expect that Myanmar Brewery’s growth will diminish somewhat in the next few years since it is likely to lose some of its existing licensing contracts with an operating company of Heineken N.V. (Baa1 stable), a Kirin global competitor, as it seeks standalone expansion. However, Myanmar Brewery will still be able to sustain decent growth and high margins with its own domestic brand, which comprises a substantial part of its revenue.

The acquisition, if successful, will also further diversify Kirin’s overseas operations. For the first half of 2015, Kirin’s overseas sales were 34% of total sales, lower than that of other major global alcoholic beverage companies such as Diageo PLC (A3 stable) and SABMiller Plc (A3 stable). At the same time, Kirin is focusing on reestablishing its domestic market share, and its increased marketing costs will weigh on its overall profitability. If Kirin does not maintain tight control over its total debt, or if profitability deteriorates and prevents an improvement in leverage, its credit metrics would be pressured, as would its rating.

Motoki Yanase Vice President - Senior Analyst +81.3.5408.4154 [email protected]

Mirai Kaneuchi Associate Analyst +81.3.5408.4026 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Brookfield Infrastructure Partners’ Proposed Acquisition of Asciano Is Credit Negative Last Monday, Asciano Limited (Baa2 negative), Australia’s largest national rail freight and ports operator, announced that it had entered into a binding agreement with Brookfield Infrastructure (unrated) and certain institutions to acquire Asciano for around AUD12 billion (including assumed debt). The acquisition is credit negative for Asciano because the acquirers said that they will partially fund the acquisition with AUD1.9 billion of debt with recourse only to the acquirer’s investment in Asciano. Additionally, we expect that the transaction will increase by AUD750-AUD800 million Asciano’s existing debt of around AUD3.3 billion as of 30 June 2015 to pay a special dividend to existing shareholders.

The deal risks raising Asciano’s existing debt to around AUD4.1 billion, if the buyers fully finance the dividend with debt, and up to AUD6.0 billion if the buyers transfer all the acquisition debt to Asciano over time. The exhibit below shows our pro forma estimate of the potential increase in Asciano’s financial leverage, as measured by debt/EBITDA, assuming that all additional debt is raised directly following a successful transaction.

Asciano’s Adjusted Debt/EBITDA Post Sale Under Different Debt Scenarios

Sources: Asciano Limited and Moody’s Investors Service estimates

The buyers propose setting up a new holding company that will establish the new acquisition debt facility and rely on dividends from Asciano to pay interest on, and ultimately repay, the facility. That creates a risk that the buyers will need to raise additional debt at Asciano to fund dividends to the new holding company if Asciano cannot provide sufficient dividends from its cash flow.

Additionally, the acquisition facility will also be structurally subordinate to Asciano’s other facilities, and we expect that it will require periodic refinancing. Based on experience during the global financial crisis, lenders have proven to be far more reluctant to refinance structurally subordinated debt than debt at the underlying operating company level. That suggests there is a possibility that adverse conditions in funding markets would increase the pressure on Asciano’s new owners to partially or wholly transfer the acquisition debt to Asciano.

The transaction remains subject to subject to various conditions, including Asciano shareholder approval, court approval, regulatory approvals, independent expert opinions, certain third-party consents, the listing of Brookfield units on the Australian Securities Exchange, and no material adverse change.

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

5.0x

FY2014 FY2015 FY2016F FY2017F

No New Debt at Asciano AUD800 Million New Debt At Asciano AUD1.9 Billion New Debt At Asciano

Matthew Moore Vice President - Senior Credit Officer +61.2.9270.8102 [email protected]

Shawn Xiong Associate Analyst +61.2.9270.1421 [email protected]

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Infrastructure

Energisa’s Acquisition of Celg Would Materially Increase Leverage, a Credit Negative Last Monday, Energisa S.A. (Ba1 stable) announced that it was evaluating a possible acquisition of Celg Distribuição S.A. (unrated), subject to undisclosed conditions. The acquisition would be credit negative for Energisa because it will increase the company’s pro forma net debt/EBITDA to approximately 3.4x from 2.9x as of 30 June 2015. We estimate that the purchase would raise Energisa’s debt by 36%, but would only raise EBITDA by 15%, based on Celg’s last-12-month to June 2015 EBITDA. Additionally, an acquisition would occur while Energisa is still in the process of improving the operational and financial performance of distribution company Rede Group, which Energisa acquired out of bankruptcy in April 2014.

A major factor in determining whether Energisa moves forward with an acquisition of Celg is the required terms and the minimum amount of capex imposed by Agencia Nacional de Energia Eletrica, Brazil’s national electricity regulator. The company would hope to complete the sale by the end of this year.

Celg, one of Centrais Eletricas Brasileiras SA - Eletrobras’ (Ba2 negative) subsidiaries, is the energy distribution company for the state of Goias, and serves 2.7 million customers. Celg is highly leveraged (it has net debt/EBITDA of 6.8x) and inefficient in terms of energy losses and the duration and frequency of service interruptions.

Energisa currently controls 13 electric distribution companies that serve 6.3 million customers across 19% of Brazil’s territory. Acquiring Celg would raise Energisa’s revenues by 40% to BRL13 billion. But we estimate that incorporating Celg’s debt would raise Energisa’s net debt to approximately BRL8.6 billion from BRL6.4 billion as of 30 June 2015. Celg generated last-12-month to June 2015 EBITDA of BRL334 million, a figure we estimate that Energisa can raise by at least 50% through synergies and operational efficiencies.

Energisa is a consolidator in the energy distribution sector following the Rede acquisition and the potential expansion of its existing franchise via other acquisitions. In May, we changed the company’s rating outlook to stable from negative after it sold its power generation companies to reduce debt and improve leverage. However, an acquisition of Celg would materially affect the company’s debt ratios and most likely lead us to reevaluate the company’s rating and outlook.

Marcos de Oliveira Assistant Vice President - Analyst +55.11.3043.7312 [email protected]

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Banks

By Selling, National Penn Solves a Credit-Negative Predicament Last Monday, BB&T Corporation (A2 stable) announced that it was acquiring National Penn Bancshares, Inc. (Baa2 review for upgrade), which has $9.6 billion in assets. National Penn’s creditors will benefit from the sale because the much larger BB&T is more diversified and higher rated. Following the announcement, we placed National Penn’s ratings under review for downgrade. But for us, the deal’s most interesting aspect is National Penn’s decision to sell, which highlights the credit-negative strategic dilemma facing all banks that stand on the cusp of $10 billion in assets.

The 2010 Dodd-Frank Act created the strategic dilemma facing US regional banks of National Penn’s size. The law introduced a number of provisions that take effect when a bank’s assets surpass the $10 billion mark. Some of these provisions materially raise banks’ costs, such as mandatory stress testing and supervision by the Consumer Financial Protection Bureau. Another provision reduces debit interchange fees by 45%.

Together, these provisions provide powerful incentives for banks approaching the threshold to either stunt their growth or leap well beyond it by acquiring other banks, which introduces integration risk. Indeed, before it agreed to sell, National Penn’s management had stated a desire to pursue bank acquisitions to go over the $10 billion mark “in a meaningful way,” a strategy that heightened the risk to its creditors.

The desire to exceed $10 billion in assets by a wide margin is understandable because it is the only realistic way for banks to generate the earnings power that can offset the added costs and lost revenue. Climbing over the threshold in a measured way through organic growth would subject banks to profitability pressures that may not be palatable to shareholders.

Given these choices, the option chosen by National Penn, which is selling for roughly 17x its first-half 2015 annualized earnings, may not be available to many other similarly situated banks. This is because larger US banks have been increasingly reticent about making acquisitions owing to their own regulatory concerns and the litigation risk they inherit and is often difficult to unearth during the due-diligence process.

Moreover, regulators have taken a more deliberative approach in approving acquisitions. BB&T is among the few large banks that have pursued sizable transactions and successfully closed them in a reasonable time period. As a result, most other banks nearing the $10 billion asset mark are unlikely to resolve their strategic dilemma in as credit friendly a manner as National Penn.

Allen Tischler Senior Vice President +1.212.553.4541 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Brazil’s Government Banks Extend Below-Market Credit Lines to Auto Industry, a Credit Negative Last week, Brazilian government-owned banks Caixa Economica Federal (Baa3/Baa3 stable, ba21) and Banco do Brasil S.A. (BB, Baa3 stable, baa3) announced that they will provide new credit lines to struggling auto makers and their suppliers. On Wednesday, Caixa said that it will extend up to BRL5 billion ($1.4 billion) in additional credit to the car industry at below-market interest rates for tenors of up to five years, provided that the borrowers agree to halt massive layoffs. On Thursday, BB said that it will lend BRL3.1 billion to auto industry suppliers backed by their receivables.

The loans are part of a government plan to support the automobile industry, whose sales and production have declined sharply since 2014, and the scheme is credit negative for the two banks because it will raise their exposure to high-risk borrowers struggling in Brazil’s economic recession.

Although the new credit lines are small relative to the banks’ total loan books of BRL617 billion for Caixa in March 2015 and BRL777 billion for BB in June 2015, the government previously had planned to slow loan growth at these institutions in order to reduce pressure on their capital and asset quality after years of rapid growth. Caixa’s overall loan growth is around 15% this year, down from average growth of 36% between 2008 and 2013. With this program, it appears that the government will continue to use the government-owned banks to stimulate the economy and support the financing needs of key industries, which will further strain the lenders’ already-pressured balance sheets.

Brazil’s car industry has experienced an especially steep performance decline over the past year. Production fell 18% in the first six months of 2015, while sales were off 21%. Consequently, these borrowers have less access to financing from private-sector lenders, which is challenging their ability to refinance existing lines of credit.

Although the government-owned banks will require high collateral from car producers and their suppliers, which will mitigate risks, the exposures will likely increase loan delinquencies. At Caixa, problem loans and credit costs have risen steadily over the past five quarters; its nonperforming loan (NPL) ratio rose to 3% in March 2015 from 2.3% in 2013 but still below the 3.6% average reported by its main private-sector peers in June 2015. However, Caixa’s aggressive loan growth of the past five years, primarily targeting low-income households, will pressure its asset quality indicators more than those of its peers as delinquencies continue to rise on loans extended during Brazil’s credit boom.

The new credit lines will weigh on the banks’ profitability as well. Caixa has announced that the loans will carry lower-than-market rates that range from 10% for working capital lines to 25% for long-term financing. By comparison, average lending rates on working capital loans with tenors of more than one year at Caixa and BB were around 38% as of July 2015. And, rates have been rising since Brazil’s central bank began tightening monetary policy in 2013. Brazil’s benchmark interest rate is currently 14.25%.

Unlike previous stimulus measures channeled through public banks, government funding will not directly subsidize these loans. Instead, Caixa will fund the new low-yielding credit lines from the Fundo do Amparo ao Trabalhador (a workers’ fund), which is a low-cost resource that the bank has typically used to finance home loans.

The banks have indicated that the programs may be expanded to eventually include other high-risk borrowers that have also been adversely affected by the recession. These may include small and midsize enterprises operating in the home appliance segment and larger companies in the telecom, construction, pulp and paper and chemicals sectors. BB has already announced that its program will be extended to other sectors and can be expanded to BRL9 billion in credit lines by the end of the year.

1 The bank ratings shown in this report are the bank’s deposit rating, senior unsecured debt rating (where available) and baseline

credit assessment.

Ceres Lisboa Senior Vice President +55.11.3043.7317 [email protected]

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Kazakhstan’s Currency Depreciation Is Credit Negative for Banks Last Thursday, Kazakhstan announced a shift in its currency and monetary policy, adopting a free-float regime for the country’s currency, the tenge, and targeting inflation rather than a specific exchange-rate range. Although the move will support government finances and competitiveness of local goods against imports from other countries in the region whose currencies have already depreciated, the weaker tenge will have a significant negative effect on the creditworthiness of Kazakhstani bank borrowers.

As the free-float became effective immediately, the tenge traded at 252 tenge per US dollar on Friday, a 26% depreciation from 188 tenge at the beginning of the week. Exhibit 1 shows the US dollar to tenge exchange rate since 2008.

EXHIBIT 1

US Dollar to Kazakhstani Tenge Exchange Rate

Sources: The National Bank of Kazakhstan and the Kazakhstan Stock Exchange

As of 1 June 2015, around 30% of net loans in Kazakhstan’s banking system were denominated in foreign currencies, mostly US dollars. Exhibit 2 shows the exposure of each bank. Many of these foreign-currency loans are to corporations and small and midsize enterprises that do not earn in foreign currency or hedge their exposure. These borrowers will find it more difficult to service their loans, and banks’ asset quality will suffer. Although large Kazakhstani resources firms that export may benefit from the currency depreciation, these firms tend to borrow overseas rather than from local banks.

020406080

100120140160180200220240260

Jan-

08

Apr-

08

Jul-

08

Oct

-08

Jan-

09

Apr-

09

Jul-

09

Oct

-09

Jan-

10

Apr-

10

Jul-

10

Oct

-10

Jan-

11

Apr-

11

Jul-

11

Oct

-11

Jan-

12

Apr-

12

Jul-

12

Oct

-12

Jan-

13

Apr-

13

Jul-

13

Oct

-13

Jan-

14

Apr-

14

Jul-

14

Oct

-14

Jan-

15

Apr-

15

Jul-

15

Semyon Isakov Assistant Vice President - Analyst +7.495.228.6061 [email protected]

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

EXHIBIT 2

Kazakhstani Banks’ Exposure to Foreign-Currency Loans as of the End of 2014 Ratio of foreign-currency loans to net loans.

Note: Data show the largest Kazakhstan banks with publicly available currency breakdown as of the end of 2014; Kazkommertsbank’s data are as of the end of 2013. The ratings shown are the bank’s deposit rating, senior unsecured debt rating (where available) and baseline credit assessment. Sources: Moody’s Investors Service and the banks’ IFRS data

The currency depreciation also lowers banks’ capital adequacy levels. Because Kazakhstani banks used swaps with the National Bank of Kazakhstan to minimize the currency mismatches on their balance sheets (about 53% of deposits in Kazakhstan were denominated in foreign currencies as of 1 July 2015, a higher level of dollarization than for banks’ assets), we estimate that amounts of capital in terms of tenge are broadly unaffected by the devaluation.2 Still, risk-weighted assets – the denominator of capital adequacy ratios – will increase in local-currency terms.

The inflationary effect of a weaker currency is negative for banks regardless of whether the new monetary policy is successful in containing inflation. If inflation targeting is successful, it will likely be at the cost of significantly higher interest rates that Kazakhstani banks will be unable to pass on to borrowers without adversely affecting asset quality. Higher inflation would be a further negative to asset quality, particularly for retail loans denominated in tenge because it erodes individuals’ real purchasing power.

2 All Kazakhstani banks were in compliance with the maximum regulatory limit on open short foreign currency positions when the

limit was halved to 12.5% of regulatory capital on 1 July 2015.

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55%

Kazkommertsbank (B2/Caa1 stable, caa1)

Tsesnabank (unrated)

ATF Bank (Caa1/Caa2 negative, caa2)

SB Sberbank JSC (Ba3 stable, b2)

Halyk Savings Bank of Kazakhstan (Ba2/Ba3 stable, ba3)

ForteBank JSC (Caa1/Caa2 stable, caa2)

Bank CenterCredit (B2 stable, b3)

Eurasian Bank (B2/B2 stable, b2)

Kaspi Bank JSC (B1/B2 negative, b2)

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

China Strengthens the Capital Base of Two Policy Lenders, a Credit Positive Last Tuesday, China’s official Xinhua News Agency reported that the People’s Bank of China (PBOC) had injected $48 billion of equity capital into China Development Bank Corporation (CDB, Aa3 stable) and $45 billion into The Export-Import Bank of China (CEXIM, Aa3 stable). The injections were made through Wutongshu Investment Platform Co. Ltd., an entity that invests China’s foreign currency reserves.

The massive equity infusions are credit positive for CDB and CEXIM. CDB’s capital adequacy ratio rises to about 11.8% from 9.1% under Basel III at year-end 2014, according to our estimates, while CEXIM’s capital adequacy ratio, which it does not disclose, rises significantly. The injections also add to both banks’ loss-absorption capacity. Against the backdrop of heightened asset-quality risks at domestic banks, we think the enhanced loss-absorption implies that regulators are likely to impose minimum capital requirements on the banks.

The capital infusions are consistent with the Chinese government’s goal to strengthen Chinese policy lenders’ capital positions. After the injections, both banks’ ratios of tangible common equity to tangible assets compare well with those of the rated Chinese large and national joint-stock commercial banks, as shown in Exhibit 1.

EXHIBIT 1

Chinese Banks’ Tangible Common Equity to Tangible Assets at 2014 After the capital infusion, CDB and CEXIM compare well with rated large banks and national joint-stock commercial banks.

Notes: ICBC = Industrial and Commercial Bank of China Ltd.; CCB = China Construction Bank Corporation; ABC = Agricultural Bank of China Limited; BOC = Bank of China Limited; BoCom= Bank of Communications Co., Ltd.; CMB=China Merchants Bank Co., Ltd.; SPDB = Shanghai Pudong Development Bank Co., Ltd.; CITICB = China CITIC Bank Corporation Limited; CEB = China Everbright Bank Company Limited; PAB = Ping An Bank Co., Ltd.; and CGB = China Guangfa Bank Co., Ltd. Sources: The banks and Moody’s Investors Service calculations

In the past several years, CDB and CEXIM have taken on key roles as policy-driven banks in financing priority projects and supporting the growth of Chinese corporates expanding overseas. For 2013-14, CDB’s compound annual asset growth rate was 17.1% and CEXIM’s 23.2%, compared with an average 13.6% rate for the Chinese banking industry during the same period (Exhibit 2).

0%1%2%3%4%5%6%7%8%9%

10%11%12%13%

CDB CEXIM ICBC CCB ABC BOC BoCom CMB SPDB CITICB CEB PAB CGB

Tangible Common Equity / Tangible Assets Capital Injection

Frank Wu Analyst +86.10.6319.6576 [email protected]

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

EXHIBIT 2

Chinese Banks’ Compound Annual Asset Growth Rate, 2013-14 CDB and CEXIM’s growth outpaced those of the domestic banking industry.

Notes: ICBC = Industrial and Commercial Bank of China Ltd.; CCB = China Construction Bank Corporation; ABC = Agricultural Bank of China Limited; BOC = Bank of China Limited; BoCom = Bank of Communications Co., Ltd.; CMB=China Merchants Bank Co., Ltd.; SPDB = Shanghai Pudong Development Bank Co., Ltd.; CITICB = China CITIC Bank Corporation Limited; CEB=China Everbright Bank Company Limited; PAB = Ping An Bank Co., Ltd.; and CGB = China Guangfa Bank Co., Ltd. Sources: The banks, China Banking Regulatory Commission and Moody’s Investors Service calculations

The capital injections demonstrate the Chinese government’s strong commitment to support the two lenders, whose policy roles are increasingly important for stimulating domestic economic growth. CDB and CEXIM are likely to take on greater credit exposure and their lending may have a greater strategic rationale rather than an economic one. For instance, the additional capital should facilitate CDB and CEXIM financing of overseas projects that are part of China’s One Belt, One Road initiative to boost infrastructure and economic connectivity across Eurasia.

Our assumption of a very high level of government support for CDB and CEXIM’s reflects strong government backing to offset their greater risks, given the two banks’ strategic importance as agents of the Chinese government in the implementation of development initiatives.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

CDB CEXIM ICBC CCB ABC BOC BoCom CMB SPDB CITICB CEB PAB CGB BankingIndustry

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Insurers

Higher Accident Frequency Is Credit Negative for US Auto Insurers On Monday, the National Safety Council (NSC) announced that US traffic deaths for the first six months of 2015 had risen by around 14% from a year ago, while serious injuries are up 30% over the same period. Increases in accident frequency and severity are credit negative because they can have a significant negative effect on personal auto writers given that about 78% of net premiums collected are used to pay claims and associated legal expenses.

The NSC’s report is directionally consistent with higher frequency and severity trends reported by auto insurers beginning in the fourth quarter of 2014, and which are prompting some auto insurers to increase rates. For example, The Allstate Corporation (A3 stable) reported increasing loss cost trends for personal auto for second-quarter 2015, with a 6.8% year-over-year increase in bodily injury claim frequency and a 6.9% year-over-year increase in property damage claim frequency (Exhibit 1).

EXHIBIT 1

Allstate’s Year-over-Year Change in Accident Frequency

Source: The Allstate Corporation

One of the largest factors is increased miles driven as the US economy continues to improve and gas prices fall. Other contributing factors include increased driver distraction from handheld devices, increased fraud and higher speed limits in certain states. Also, consumers may be more likely to report minor claims given the increasing share of leased vehicles.

Over the past several decades, accident frequencies have been in slow decline, in part because of an aging population that historically has exhibited better loss experience, safety improvements in cars and tougher drunk driving laws in certain states. However, accident frequencies occasionally shift.

Insurers respond to increased frequency and severity trends by increasing prices, but there is a time delay between when an accident uptick first occurs and the rate increases take effect, because it takes time for companies to measure the uptick, determine that it is not a blip, and then file, implement and earn the higher rates. Exhibit 2 shows the cost effect of a 2% increase in frequency trend on the top 10 personal auto insurers with a 12-month lag between the initial frequency uptick and the time when the rate increases are earned. The estimated combined effect on the personal auto industry is $2.9 billion (1.5 combined ratio points).

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015

Bodily Injury Property Damage

Jasper Cooper Assistant Vice President - Analyst +1.212.553.1366 [email protected]

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

EXHIBIT 2

Effect of a 2% Change in Accident Frequency on 10 Largest US Personal Auto Insurers

Insurance Financial Direct Premium

Written 2014 Loss Ratio Combined Ratio (CR)

Estimated Effect of 2% Increase in Frequency

Rank Company Strength Rating* $ Billions 2014 2014 $ Millions CR Points

1 State Farm Unrated $35.6 83.4% 109.1% $594 1.7%

2 GEICO Aa1 stable $20.5 79.6% 95.1% $327 1.6%

3 Allstate Aa3 stable $19.0 70.7% 97.5% $269 1.4%

4 Progressive Aa2 stable $16.6 73.7% 94.4% $244 1.5%

5 USAA Aaa stable $9.8 87.1% 104.0% $171 1.7%

6 Farmers A2 stable $9.7 71.4% 103.4% $139 1.4%

7 Liberty Mutual A2 stable $9.5 77.6% 104.3% $147 1.6%

8 Nationwide A1 stable $7.3 74.3% 106.8% $109 1.5%

9 American Family Unrated $3.5 74.3% 106.3% $52 1.5%

10 Travelers Aa2 stable $3.2 72.9% 101.9% $46 1.5%

Industry $190.6 77.2% 102.5% $2,943 1.5%

Note: *Insurance financial strength ratings apply to the rated insurance subsidiaries of the group.

Sources: SNL Financial LC and Moody’s Investors Service. Contains copyrighted and trade secret materials distributed under license from SNL, for recipient’s internal use only.

Increases in accident cost severity can have an even larger effect on aggregate costs than frequency trends because medical costs may continue for years after an accident. Potential reasons for increased severity include higher healthcare costs, increased medical fraud, a higher share of new cars on the road and higher repair labor costs. According to the North American Dealer Association, annual auto sales increased to a rate of 17.5 million in July 2015, versus 10.4 million in 2009. New cars are often more expensive to repair than older models because they have more expensive safety features, a higher share of expensive materials such as aluminum and sometimes fewer aftermarket replacement parts available.

Several large US auto insurers announced lower earnings in second-quarter 2015 as a result of higher frequency and/or severity, including Allstate, GEICO Corporation (Aa3 stable) and Infinity Property and Casualty Corporation (Baa2 stable). According to Allstate, the uptick in frequency and severity exceeded average auto premium increases, contributing to an increase in the auto combined ratio for the Allstate brand to 101.4% in second-quarter 2015 from 95.4% a year earlier. Similarly, GEICO’s combined ratio increased to 99.0% in second-quarter 2015 from 92.3% a year earlier, partially because of increased frequency and severity trends.

We expect that the larger personal auto insurers with sophisticated risk segmentation and analytical capabilities will respond to rising loss cost trends through targeted rate increases, which could slow new business growth, while boosting underwriting margins.

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Mexico City’s New Transit Regulation Is Credit Positive for Insurers Last Wednesday, Mexico City’s government announced a new transit regulation for the city that includes the mandated use of third-party insurance coverage for all vehicles, effective January 2016. This new requirement is credit positive for Mexico’s auto insurers because it will expand insurance protection, which has historically had very limited use in Mexico, and, given frequent car accidents and losses, has been a significant problem for the city’s population.

The new regulation is a positive development for the insurance industry because approximately 20% of total industry premiums are for auto insurance policies. In Mexico, more than 35 companies offer auto insurance. The companies that will benefit the most from this measure are the largest auto writers and those with extensive distribution and claim-servicing systems, including Qualitas, AXA Seguros, Grupo Nacional Provincial, ABA, Banorte and Mapfre Tepeyac (see exhibit).

Mexico’s Top 10 Auto Insurers as of March 2015

Company Total Premiums

MXN Million Auto and Truck Premiums

MXN Million Auto and Truck Premiums

Market Share

Auto and Truck Premiums as Percent of

Total Premiums

Quálitas 4,725 4,724 24% 100%

AXA Seguros 7,278 2,435 13% 33%

Grupo Nacional Provincial 11,460 2,365 12% 21%

ABA 1,824 1,589 8% 87%

Banorte 5,438 1,337 7% 25%

Mapfre Tepeyac 4,190 1,178 6% 28%

BBVA Bancomer 6,482 1,137 6% 18%

Inbursa 5,170 1,062 5% 21%

HDI 910 800 4% 88%

Zurich 1,455 591 3% 41%

Source: Mexico Comisión Nacional de Seguros y Fianzas

According to the insurance association Asociación Mexicana de Instituciones de Seguros (AMIS), only around 28% of all cars in Mexico have some kind of insurance protection and, in Mexico City, only 50% of vehicles have insurance. There are approximately 26 million vehicles in the country, about 12% of which are in Mexico City. Mexico is one of very few countries on the American continent that does not nationally mandate the use of third-party liability insurance for all vehicles. Fewer than 10 of Mexico’s 32 states mandate third-party liability insurance for all vehicles.

Although Mexico City required auto insurance coverage several years ago, the law has not been enforced, so many people remain uninsured. This new transit regulation contemplates specific fines for drivers without insurance coverage. AMIS estimates third-party auto premiums annual cost at approximately $60. Consequently, we expect that the industry’s automobile insurance premiums will increase by 2%-4% next year.

This new regulation will help to increase insurance penetration. Insurance premiums as percent of GDP were around 2.0% in 2014, according to statistics published by Swiss Re (Sigma), meaningfully below the region’s average of 2.5%. We believe Mexico City’s new local law is a constructive step toward the eventual enforcement of auto insurance protection throughout the country.

José Montaño Vice President - Senior Analyst +52.55.12.53.57.22 [email protected]

NEWS & ANALYSIS Credit implications of current events

19 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Sovereigns

Ecuador’s Reduced Spending Amid Difficult Economic Environment Is Credit Positive On Wednesday, the Government of Ecuador (B3 stable) announced that it would reduce its spending this year by $800 million (0.8% of GDP). This follows $1.4 billion in cuts announced in January, taking total spending cuts to 2.2% of 2014 GDP. The latest measures are credit positive and display the proactive and pragmatic policy that Ecuadorian authorities have pursued this year to address the drop in oil prices.

Government oil revenues in the first half of this year dropped 55% to $1.1 billion from the same period a year ago. Ecuador’s oil basket averaged $49 per barrel in January-August, but was lower than $40 per barrel last week, significantly below the $79.90 per barrel original estimate used in the 2015 budget and the $86.80 per barrel average for 2014.

Other measures that seek to limit the effect of lower oil revenues include a tax amnesty law that yielded $800 million in July, and increased import tariffs introduced in March that provide the government with some additional income but most importantly will limit the effect of lower oil export receipts on the current account deficit by lowering demand for imports.

Public investment is about half of total government spending, so Ecuador has greater flexibility to make adjustments than other sovereigns because capital expenditures tend to be less rigid. This flexibility is denoted in the composition of the cuts, as $700 million involved planned capital expenditures. Authorities have identified projects that can be delayed, while continuing to pursue key investments in the energy sector (34% of the initial $8 billion investment program for 2015). They also recently announced their intention to introduce legislation that would bolster private-public partnerships by providing tax concessions to both local and foreign companies interested in key public works projects. Should these incentives prove successful, public-private partnerships would allow the government to lower its capital spending going forward, thus reducing future fiscal deficits, without compromising the level of total investment.

Authorities have stated that the 2016 budget will likely include an oil price estimate of about $40 per barrel, and that it would target a deficit of 2.0%-2.5% of GDP next year. We had expected that starting next year the deficit would begin to fall from historical highs during 2013-15, as a series of large-scale public projects in the energy sector were completed. Overall, the authorities’ budgetary guidance implies faster deficit reduction.

Government gross financing needs for 2015 will amount to $9.5 billion including the December amortization of a $650 million global bond. The government has so far financed 52% of this amount via external sources: $1.2 billion from multilaterals, $500 million from bilateral loans, and $1.7 billion from global bond issuances. In addition, under the oil pre-sale scheme, it has received $1.4 billion from China and $500 million from Thailand. We expect that as fiscal deficits fall in future years, government financing needs will decrease significantly.

Although the cuts denote the government is prioritizing fiscal sustainability, lower spending will become a drag on the economy. Consequently, we are revising our growth forecast for 2015 to 1% from 2% previously. Lower economic activity could also exacerbate social discontent in the country. Although not related to the spending cuts, there were two large-scale demonstrations against government policies in June and August, with protesters opposing proposed increases to inheritance and capital gains taxes as well as extractive-industries projects in previously protected areas, among other issues. As the 2017 electoral cycle approaches amid a more difficult economic and social environment, the government’s policy-response capacity will be a key support of Ecuador’s creditworthiness.

Renzo Merino Analyst +1.212.553.0330 [email protected]

NEWS & ANALYSIS Credit implications of current events

20 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Greek Prime Minister Resigns, Clearing the Way for a Stronger Government Last Thursday, Greece (Caa3 review for downgrade) Prime Minister Alexis Tsipras stepped down as head of government and called for early elections. The prime minister’s resignation is credit positive for the sovereign because it offers the possibility of a new more cohesive government, which would improve prospects for implementing Greece’s third bailout package and reducing liquidity and funding risks.

We believe Mr. Tsipras called for a snap election now to seek a fresh mandate to implement the latest agreement with Greece’s creditors. Mr. Tsipras’ resignation offers the prospect of establishing a more effective government, perhaps involving a more moderate Syriza party governing alone or in a coalition with other pro-European parties. Whichever government emerges from the election, the next administration has little chance of being less cohesive than the present one. Several parliamentary votes on Greece’s third bailout package eroded the Syrzia governing coalition’s strength and support for the current government, particularly from within Syriza itself.

However, an election is not a foregone conclusion. According to the Greek constitution, the president must first offer the second- and third-largest parties in parliament the opportunity to form a government. Each party has three days in which to do so.

New Democracy has already been given the opportunity to explore the possibility of forming a government. If it fails, then a similar opportunity will be presented to the newly formed Popular Unity party, led by former energy minister Panagiotis Lafazanis. The party was formed after Mr. Tsipras resigned by 25 former Syriza members of parliament who are against euro area membership and the third bailout.

If Popular Unity fails to form a government, then Greece President Prokopis Pavlopoulos must call elections within 30 days. A caretaker government, under the head of the Supreme Court, would be in place until a new government is formed after the elections. Given these constitutional procedures, elections, if held, are unlikely to take place before late September.

Polls suggest that Mr. Tsipras remains popular among voters, and a second victory for Syriza is a possibility. Since the new elections will be held within around eight months of the previous ones, the constitution dictates that votes must be cast for party lists rather than for individual candidates. That would allow Syriza leaders, should they again win an electoral mandate, to remove the most radical elements of the party in forming a government. Even if Syriza does not win a majority, any outcome that allows and requires it to reach an accommodation with pro-bailout and pro-euro area parties would likely enhance political stability and ease programme implementation risks.

Mr. Tsiprias’ resignation creates an immediate political vacuum that will likely delay implementation of the bailout package until a new prime minister and elected government are in place. However, the effect on funding is limited, because the caretaker government steps in at a time when Greece’s liquidity needs are relatively modest. From September to the end of the year, financial obligations (amortization and interest payments) total €4.5 billion (see exhibit), €3.4 billion of which is to the International Monetary Fund (IMF). Only around €200 million is due to private-sector bondholders. Set against those needs, the European Stability Mechanism (Aa1 stable) on Wednesday approved a three-year, €86 billion bailout package and followed up the next day by disbursing the first cash tranche consisting of €13 billion. We understand that in addition to making a payment to the European Central Bank, this tranche will also cover repayments of €1.8 billion due to the IMF in August and September. A second tranche of €3 billion will be disbursed by the end of November, pending approval of prior actions by the Greek parliament. A further €6.7 billion is earmarked for before year-end.

Alpona Banerji Vice President - Senior Credit Officer +44.20.7772.1063 [email protected]

Stefan Triendl Associate Analyst +44.20.7772.5560 [email protected]

NEWS & ANALYSIS Credit implications of current events

21 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Greece’s Debt Repayment Schedule

Sources: Bloomberg, International Monetary Fund, European Commission, Public Debt Management Agency and Moody’s Investors Service

€0.00

€0.25

€0.50

€0.75

€1.00

€1.25

€1.50

€1.75

€2.00

Sep Oct Nov Dec

€Bi

llion

Private Sector Principal Private Sector Interest ECB Interest IMF Other

NEWS & ANALYSIS Credit implications of current events

22 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Kazakhstan’s Flexible Currency Will Help Economy Adjust to Lower Oil Prices Last Thursday, Kazakhstan (Baa2 stable) adopted a market-determined exchange rate, abandoning its previous practice of managing the foreign-currency value of the tenge. Consequently, the tenge depreciated 26% to 252 tenge per dollar from 188 earlier in the week. Although the currency depreciation will raise foreign currency debt repayment costs for corporates and weaken banks’ asset quality and capital adequacy ratios, it is credit positive for the sovereign because it allows the economy to adjust to a lower oil price. Flexible exchange rates help maintain trade competitiveness because they adjust according to trade and capital account flows. Moreover, whereas maintaining a stable exchange rate can deplete foreign exchange reserves, currency flexibility preserves reserves.

Since mid-2014, a sharp fall in the price of oil and a decline in the value of the Russian ruble, Ukrainian hryvnia and euro vis-à-vis the US dollar have damaged Kazakhstan’s external revenues, competitiveness and growth prospects. As oil revenue inflows fell and the Kazakhstani government undertook budget support and investment projects to counteract the economic decline, Kazakhstan’s sovereign wealth fund, the National Fund, recorded a drop in assets to $68 billion in July from $77 billion a year earlier (see Exhibit 1).

EXHIBIT 1

Kazakhstan’s Central Bank and Government External Assets

Sources: Haver Analytics and National Bank of Kazakhstan

Because Kazakhstan maintained a relatively stable value of the tenge against the dollar, while its trading partner currencies depreciated, Kazakhstan’s real effective exchange rate (REER) was 20% higher by the end of June 2015 than it was a year earlier (see Exhibit 2). This lowered trade competitiveness, reflected in a 27% decline in non-oil merchandise exports between January and April from a year earlier, although trading partners’ slowing economies was also a factor. In August, the devaluation of several emerging market currencies following the shift in the management of China’s yuan placed further upward pressure on Kazakhstan’s REER. Moreover, Kazakhstan has spent $28 billion since the beginning of 2014, mostly through currency swap contracts and repo agreements with commercial banks, to defend its stabilized exchange rate, and faced additional drains on central bank reserves. The likelihood of an interest rate rise in the US increases the potential costs of maintaining a stable exchange rate against the dollar.

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

Jan-2014 Mar-2014 May-2014 Jul-2014 Sep-2014 Nov-2014 Jan-2015 Mar-2015 May-2015 Jul-2015

$ Bi

llion

s

Foreign-Currency Reserves Gold Assets of the National Fund

Ernest Sergenti Assistant Vice President - Analyst +1.212.553.4196 [email protected]

Atsi Sheth Senior Vice President +65.6398.3727 [email protected]

Polina Gotmann Associate Analyst +49.69.7073.0725 [email protected]

NEWS & ANALYSIS Credit implications of current events

23 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

EXHIBIT 2

Kazakhstan’s Real Effective Exchange Rate Since June 2014

Sources: CEEMarketWatch

Against this backdrop, a shift to a flexible currency (and the consequent 26% depreciation in the tenge) will improve trade competitiveness and lower the need to tap foreign currency reserves to defend the currency. Moreover, tenge depreciation also raises the tenge value of oil revenues, offsetting to some degree the effect of lower oil prices on the state budget. This is important for Kazakhstan because 50% of its fiscal revenues come from the sale of oil.

Nevertheless, there are some near-term negative economic effects. Although the government’s own foreign currency liabilities are relatively modest, corporates’ foreign currency debt repayment costs will rise and banks’ asset quality and capital adequacy ratios will deteriorate. In addition, total government expenditures could rise given that recent announcements suggest that the government plans to compensate small tenge depositors for losses owing to the depreciation of the tenge, although the government’s commitment to lowering fiscal deficits by cutting other expenditures will alleviate the negative fiscal effect of such social support. Also, tenge depreciation could prompt inflationary pressures through higher import costs. Given the central bank’s commitment to inflation targeting, such pressure may result in higher interest rates, which, in turn, would further subdue growth.

Any growth effects would offset these negative effects. The sharp depreciation in the tenge may produce gains in the export sector, especially in the non-oil mining sector, and the move to a flexible currency may increase domestic and foreign investment because many businesses had been waiting for a resolution of the exchange rate issue before making new investments.

90

100

110

120

130

140

150

160

170

180

Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15

Inde

xed

to 1

00 a

t Jun

e 20

14

REER RUR EUR USD

NEWS & ANALYSIS Credit implications of current events

24 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Israel’s Second-Quarter Slump Suggests Fragile Government Majority Will Face Economic Headwinds On 16 August, Israel’s (A1 stable) Central Bureau of Statistics (CBS) released its preliminary estimate of second-quarter 2015 economic output, which revealed a surprisingly weak 0.3% annualized rise in real GDP from the previous quarter. The announcement prompted Finance Minister Moshe Kahlon to hold a special meeting of top officials in the Ministry of Finance the following day to determine whether government action is required to address the slowdown. Less than two weeks before, lengthy and contentious negotiations among cabinet ministers yielded budget agreements for 2015 and 2016 barely in time to avoid a government collapse. A sharp slowdown in growth, if it were to persist, would endanger the deficit targets set in the carefully crafted agreements and the government’s ability to gain approval for the budgets in the Knesset, a credit negative that would likely precipitate new elections.

The new coalition, which took nearly two months to form following the 17 March election, has a fragile one-person majority in the Knesset. The difficulty in reaching a budget compromise and now the news of sharply weaker growth are just some of the economic challenges we expect the new government to face and will repeatedly test the government’s ability to hold together. Moreover, fiscal authorities have little or no additional room to maneuver because spending ceilings have been set and the central bank policy rate is already virtually zero. As such, Mr. Kahlon’s quick mobilization of his team is unlikely to lead to concrete measures to support growth, at least over the next several months while the budget is being debated. That said, a recent weakening of the shekel exchange rate, if sustained on a trade-weighted basis, is likely to help the struggling export sector.

The poor economic results for the second quarter were broad-based, driven largely by a decline in consumer spending growth and contractions in both exports and investment. Private consumption was a leading driver of GDP growth in 2014, peaking at a 7.5% annual rate of growth in fourth-quarter 2014 before slowing to 5.5% in first-quarter 2015 and to 0.9% in second-quarter 2015.

The second-quarter slowdown in consumer spending largely showed up in durable and semi-durable purchases, so it was likely related to consumers’ expectation of changes in taxation on home purchases rather than a weakening of consumer confidence. Exports have been sluggish for nearly three years owing to declining global trade growth and the strong exchange rate. Exports contracted by 12.5% in the second quarter, having already declined at an 11.1% annual rate in the first quarter. Gross fixed capital formation fell 3.8%.

The weak second-quarter report came as a surprise in large part because it showed a steeper slowdown than suggested by coincident economic indicators from the labor market, where the unemployment rate continues to fall to all-time lows even as the participation rate rises, as well as from tax revenue, which has been very buoyant. These contradictions may mean that the second-quarter growth rate will be revised upward when the next estimates are published in a month.

Still, the first estimates for second-quarter GDP bring year-over-year growth in the first half of 2015 to just 2.6%, raising doubts about whether the Ministry of Finance’s forecasts – similar to our own – for yearly growth exceeding 3%, on which the new budgets are based, can be achieved in 2015 and 2016. Also making us cautious are the Bank of Israel’s latest surveys on inflation expectations, which indicate potential further weakening of the economy in the second half of this year. Based on these early challenges and in light of global economic conditions, we expect the current coalition to face significant economic turbulence throughout its tenure.

Kristin S. Lindow Senior Vice President +1.212.553.3896 [email protected]

Joshua Grundleger Associate Analyst +1.212.553.1791 [email protected]

NEWS & ANALYSIS Credit implications of current events

25 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Sri Lanka’s Election Outcome Improves the Government’s Ability to Pass Credit-Positive Reforms Last Friday, a coalition government led by the United National Party (UNP) took office in Sri Lanka (B1 stable), following 17 August parliamentary elections in which the UNP more than doubled its seats in parliament to 106 of 225 total seats. The UNP-led coalition will include the Sri Lanka People’s Freedom Party, the second-largest political party in parliament, of which former President Mahinda Rajapaksa is a member. The establishment of a coalition government with more than a two thirds parliamentary majority is credit positive for Sri Lanka because the government can now more easily enact policies that revive growth and address its large fiscal burden. This would address flagging business confidence and slowing foreign investment flows of the past six months.

Before the elections, the UNP and its allies controlled 26% of the seats in parliament. A UNP-led government led by Prime Minister Ranil Wikremesinghe was appointed in January by President Maithripala Sirisena, who in January 2015 unseated Mr. Rajapaksa, who had been in office since 2005. However, the UNP’s lack of a parliamentary majority slowed policymaking and resulted in a political environment characterized by fractious rhetoric between rival political factions. In an environment of slowing global growth, political gridlock in the first half of this year dampened business confidence, leading to a reversal of capital flows. Had these conditions persisted, they would likely have slowed domestic investment growth as well.

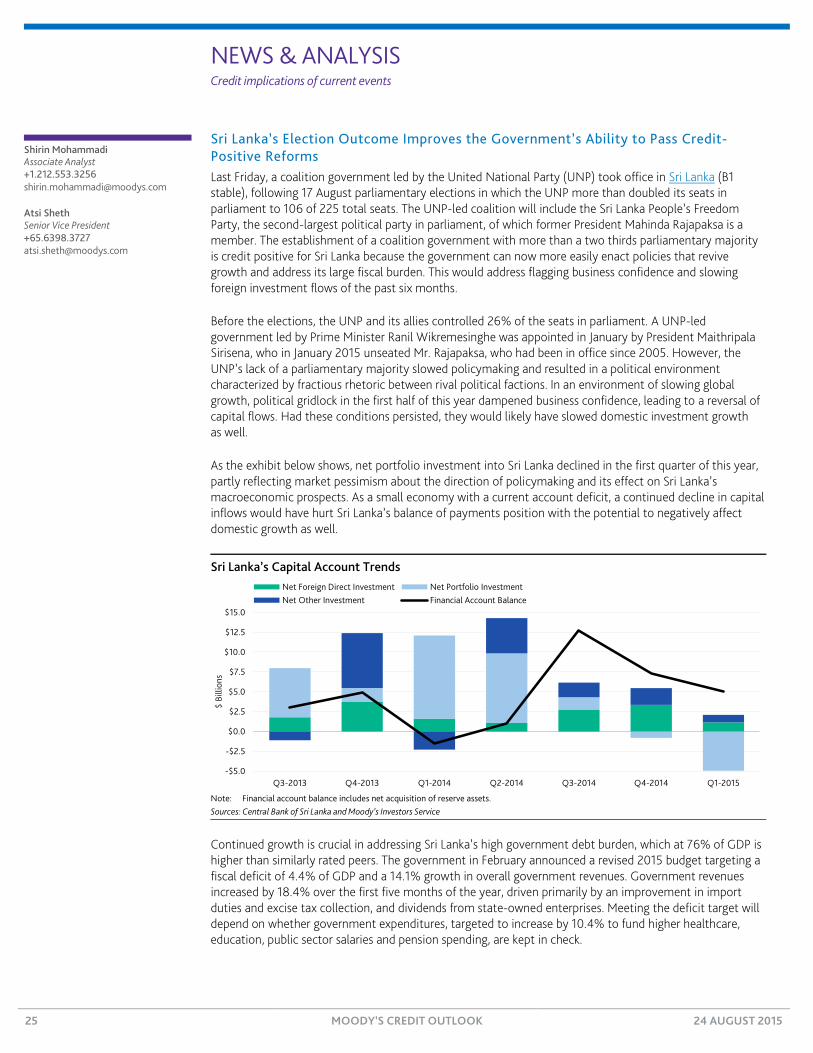

As the exhibit below shows, net portfolio investment into Sri Lanka declined in the first quarter of this year, partly reflecting market pessimism about the direction of policymaking and its effect on Sri Lanka’s macroeconomic prospects. As a small economy with a current account deficit, a continued decline in capital inflows would have hurt Sri Lanka’s balance of payments position with the potential to negatively affect domestic growth as well.

Sri Lanka’s Capital Account Trends

Note: Financial account balance includes net acquisition of reserve assets. Sources: Central Bank of Sri Lanka and Moody’s Investors Service

Continued growth is crucial in addressing Sri Lanka’s high government debt burden, which at 76% of GDP is higher than similarly rated peers. The government in February announced a revised 2015 budget targeting a fiscal deficit of 4.4% of GDP and a 14.1% growth in overall government revenues. Government revenues increased by 18.4% over the first five months of the year, driven primarily by an improvement in import duties and excise tax collection, and dividends from state-owned enterprises. Meeting the deficit target will depend on whether government expenditures, targeted to increase by 10.4% to fund higher healthcare, education, public sector salaries and pension spending, are kept in check.

-$5.0

-$2.5

$0.0

$2.5

$5.0

$7.5

$10.0

$12.5

$15.0

Q3-2013 Q4-2013 Q1-2014 Q2-2014 Q3-2014 Q4-2014 Q1-2015

$ Bi

llion

s

Net Foreign Direct Investment Net Portfolio InvestmentNet Other Investment Financial Account Balance

Shirin Mohammadi Associate Analyst +1.212.553.3256 [email protected]

Atsi Sheth Senior Vice President +65.6398.3727 [email protected]

NEWS & ANALYSIS Credit implications of current events

26 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Government policies are increasingly important in addressing Sri Lanka’s macroeconomic challenges, which stem from high government debt, subdued international trade, and the potential for capital outflows from emerging markets ahead of an increase in interest rates by the US Federal Reserve and China’s slowing economy. Sri Lanka’s growth, still robust relative to peers, has slowed to 6%-7% in recent years from more than 10% on average in the early 2000s.

Political gridlock before the election threatened to exacerbate the slowdown by thwarting investment. The UNP government’s reviews of projects approved by the previous government delayed their execution, while political opponents’ challenges to the appointments of officials by the UNP government diverted time and resources away from economic policy formulation and implementation. If the current structure of government limits the negative effect that such political differences had on business confidence, the economic outlook will improve.

NEWS & ANALYSIS Credit implications of current events

27 MOODY’S CREDIT OUTLOOK 24 AUGUST 2015

Sub-sovereigns

Financial Discipline Law for Mexican Sub-sovereigns Would Be Credit Positive Last Monday, Mexico President Enrique Pena Nieto presented the Financial Discipline Law for states and municipalities that will be submitted to Mexico’s congress. The proposed law requires positive budgetary balances, limits personnel spending growth to the lower of 3% or expected real GDP growth, improves the transparency and visibility of sub-sovereign debt and finances, and sets clear debt contracting and related definitions. Although we expect that Congress will modify the proposal before it is enacted, the proposed regulation is credit positive because it has the potential to improve the financial management of Mexico’s second-tier governments.

This initiative follows a constitutional reform approved by the congress on 25 May 2015 to incentivize sub-sovereigns to improve their financial management and transparency. The proposal sets out a series of financial ratios and parameters that sub-sovereigns must meet to progressively reach the complete application of the law by 2022. It also promotes fiscal planning over a five-year time horizon and good financial practices by requiring sub-sovereigns to set aside precautionary funds against natural disasters. This marks a structural change because over the past five years deficits have averaged 2% of total revenues for states and 3.7% for municipalities (see Exhibit 1).

EXHIBIT 1

Mexican Sub-sovereigns’ Average Consolidated Financing Results to Total Revenue

Source: Moody’s Investors Service based on rated issuers’ financial statements

The proposal establishes an alert system based on debt ratios that will be publicly available and will promote public scrutiny of sub-sovereign debt. The alert system will warn of high debt levels and prompt authorities to take corrective action. Additionally, the proposal sets limits on short-term debt and lays out a clear framework of debt-related definitions that will reduce the controversy and legal wrangling associated with debt authorizations and debt uses.

The proposed law also establishes procedures and conditions for local governments to obtain a debt guarantee from the federal government, which will reduce the cost of funding in exchange for a sub-sovereign’s commitment to improve its financial position.

After years of rapid debt growth (see Exhibit 2), and some cases of abrupt financial deterioration and defaults, this regulation is the final phase of a reform aimed at strengthening a legal and operative institutional framework that will sustain a healthy public debt market and keep Mexico’s financial system stable.

-5%

-4%

-3%