Embed Size (px)

Citation preview

PHOENIX PUBLIC

FINANCE

William C. DavisManaging Director

(602) [email protected]

Peter J. PhillippiManaging Director

(602) [email protected]

James B. Sult, Jr., VP(602) 808-5425

Greg G. Swartz, VP(602) 808-5426

Logan K. McKenzie, Associate(602) 808-5422

Helen Cregger, VP(303) 820-5856

PUBLIC FINANCE

BOND RATING BASICS

May 11, 2007

2

OVERVIEW

OVERVIEW

Understanding Bond Ratings

Understanding the Rating Process

What to Expect from your Banker

A Look at Arizona Ratings

A Surprise

3

BOND RATINGS

A relative measure of risk to bondholders that reflects an issuer’s willingness and ability to repay debt on time and in full.

Measure of financial strength that takes into account all of the resources of an issuer within given security provisions.

A measure of both what is known and unknown – a measure of uncertainty.

Ratings are comparative and relative.

Ratings are highly definitional – Anything Baa and above signifies essentially no probability of default; not just Aaa.

4

BOND RATINGS

While sound financial management is always a positive, rating criteria don’t necessarily correspond with your management priorities or the concerns of your community.

Ratings are certainly not intended to encapsulate all of the qualities of your community.

Ratings are larger than any particular individual, administration or legislative body.

5

BOND RATINGS

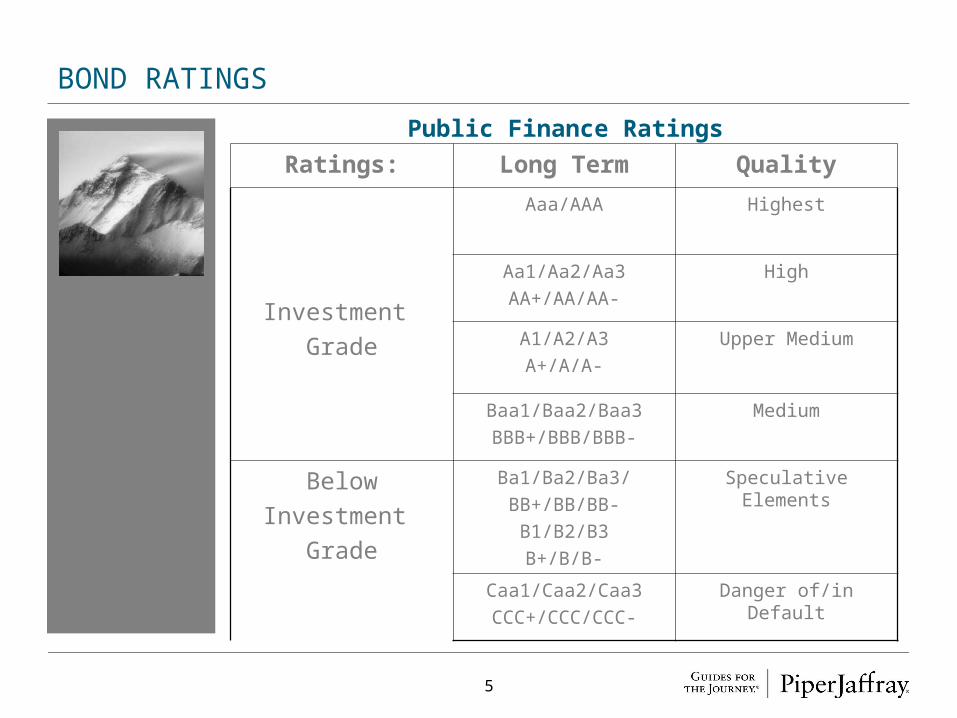

Public Finance Ratings

Ratings: Long Term Quality

Investment Grade

Aaa/AAA Highest

Aa1/Aa2/Aa3AA+/AA/AA-

High

A1/A2/A3A+/A/A-

Upper Medium

Baa1/Baa2/Baa3BBB+/BBB/BBB-

Medium

BelowInvestment

Grade

Ba1/Ba2/Ba3/BB+/BB/BB-

B1/B2/B3B+/B/B-

Speculative Elements

Caa1/Caa2/Caa3CCC+/CCC/CCC-

Danger of/in Default

6

GENERAL OBLIGATION BONDS

Full faith and credit of issuer with a pledge of either unlimited or limited property tax revenues

Generally the safest form of bond issue

Implied G.O. Rating = Issuer Rating

7

GENERAL OBLIGATION BONDS

Economy/Taxbase/Socio-economic factors

Management

Debt

Financial Performance

8

LEASE OBLIGATIONS

Typically secured by some form of general fund pledge to make lease payments for an asset

Issuing “shell” corporations

Specific asset lease vs. master lease

Value of asset(s) vs. par amount

9

LEASE OBLIGATIONS

Essentiality

Fixed asset vs. equipment

Rating typically “notched” off the GO/IR

General fund lease payment burden

Other Legal Covenants

• Insurance

• Reserve Funds

10

EXCISE TAX REVENUE BONDS

A gross or specific pledge of excise tax revenues

Excise tax revenue bonds

• Moody’s – rating “notched” off GO/IR

• These are typically general fund revenues

• Operations typically highly dependent upon these revenues for operations

• S&P – strength and consistency of revenue stream more important

• Evaluated separately from GO rating

Dedicated sales tax revenue bonds

• Not typically general fund revenues

• Often voter-approved for specific uses/projects

11

EXCISE TAX REVENUE BONDS

Historical Trend of Revenue Growth

Debt Service Coverage

Additional bonds tests and reserve funds

Non-impairment clauses and other legislative issues

12

ENTERPRISE REVENUE BONDS

Water & Sewer Bonds

Electric Revenue Bonds

Combined System Pledges

Other

13

REVENUE ENTERPRISES – AREAS OF ANALYSIS

Type of System

Economy/Service Area

Financial Performance (Including Key Measures and Ratios)

Management

Capital Needs

Covenants and Other Security Provisions

14

TAX INCREMENT FINANCING

Secured by property tax revenues generated by incremental growth

Redevelopment project areas

Taxpayer concentration and tax appeals

Plan limits

• Sunset date

• Debt limits

• Limits on amounts of incremental revenues which may be collected

15

TAX INCREMENT FINANCING

Additional bonds test

Multiple liens

Pass-through agreements, and housing set-asides

Often a passive revenue stream unless rates can be adjusted

Sometimes backed by broader pledge – other project areas or issuer/parent organization

Legislative issues

16

IMPROVEMENT DISTRICTS

Growing acceptance and activity by rating agencies

Municipal oversight enhances credit quality

Development agreements and step-up provisions can overcome risks

Concentration risks

High debt burden

Competitive tax rates and favorable location also strengthen credit evaluation

17

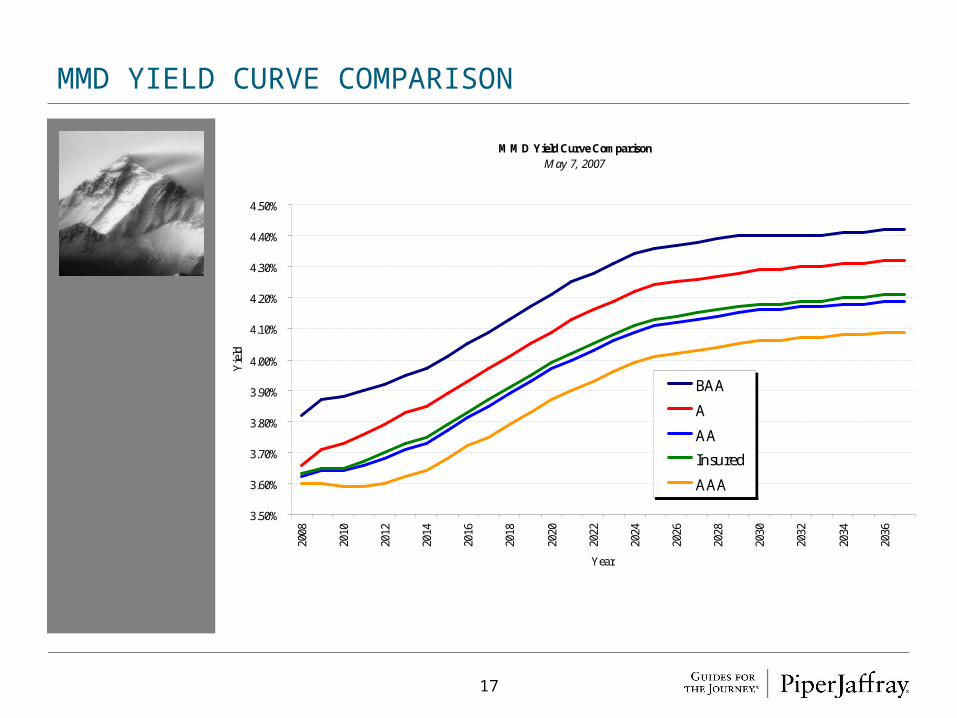

MMD YIELD CURVE COMPARISON

MMD Yield Curve ComparisonMay 7, 2007

3.50%

3.60%

3.70%

3.80%

3.90%

4.00%

4.10%

4.20%

4.30%

4.40%

4.50%

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

Year

Yie

ld

BAA

A

AA

Insured

AAA

18

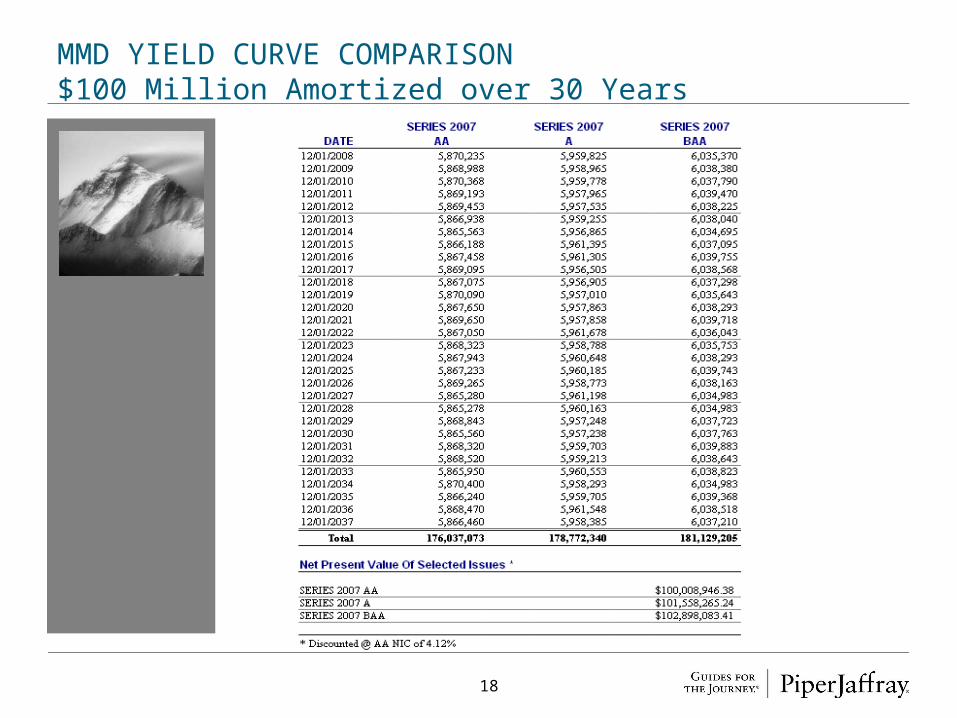

MMD YIELD CURVE COMPARISON$100 Million Amortized over 30 Years

19

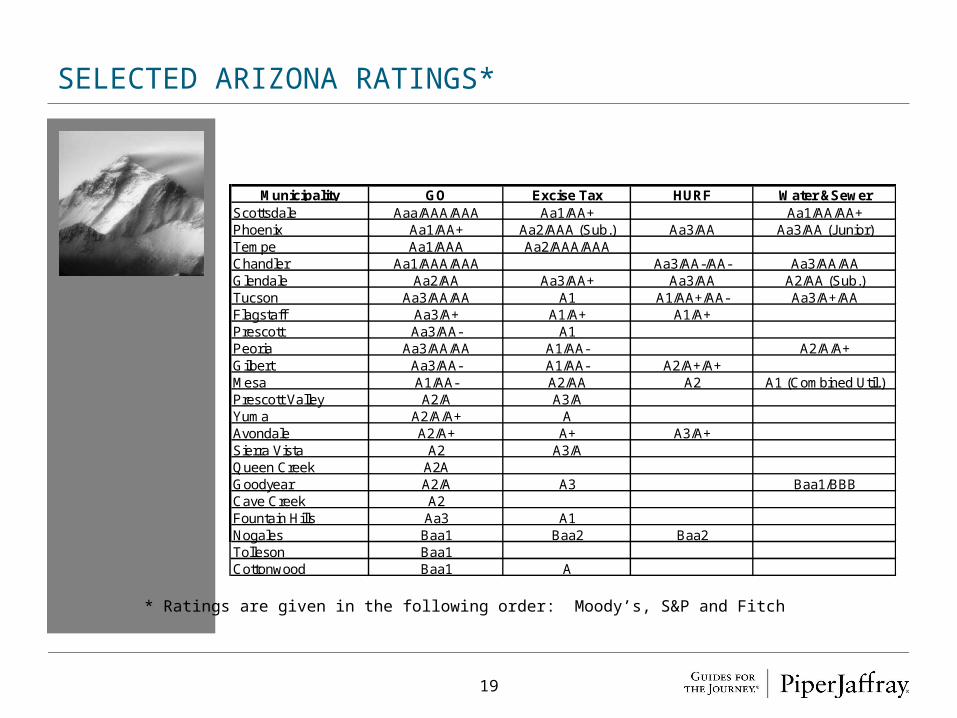

SELECTED ARIZONA RATINGS*

* Ratings are given in the following order: Moody’s, S&P and Fitch

Municipality GO Excise Tax HURF Water &SewerScottsdale Aaa/AAA/AAA Aa1/AA+ Aa1/AA/AA+Phoenix Aa1/AA+ Aa2/AAA (Sub.) Aa3/AA Aa3/AA (Junior)Tempe Aa1/AAA Aa2/AAA/AAAChandler Aa1/AAA/AAA Aa3/AA-/AA- Aa3/AA/AAGlendale Aa2/AA Aa3/AA+ Aa3/AA A2/AA (Sub.)Tucson Aa3/AA/AA A1 A1/AA+/AA- Aa3/A+/AAFlagstaff Aa3/A+ A1/A+ A1/A+Prescott Aa3/AA- A1Peoria Aa3/AA/AA A1/AA- A2/A/A+Gilbert Aa3/AA- A1/AA- A2/A+/A+Mesa A1/AA- A2/AA A2 A1 (Combined Util.)Prescott Valley A2/A A3/AYuma A2/A/A+ AAvondale A2/A+ A+ A3/A+Sierra Vista A2 A3/AQueen Creek A2AGoodyear A2/A A3 Baa1/BBBCave Creek A2Fountain Hills Aa3 A1Nogales Baa1 Baa2 Baa2Tolleson Baa1Cottonwood Baa1 A

20

ARIZONA CITY MOODY’S RATINGS

0

1

2

3

4

5

6

7

8

Aaa Aa1 Aa2 Aa3 A1 A2 A3 Baa1

# o

f Rat

ings

21

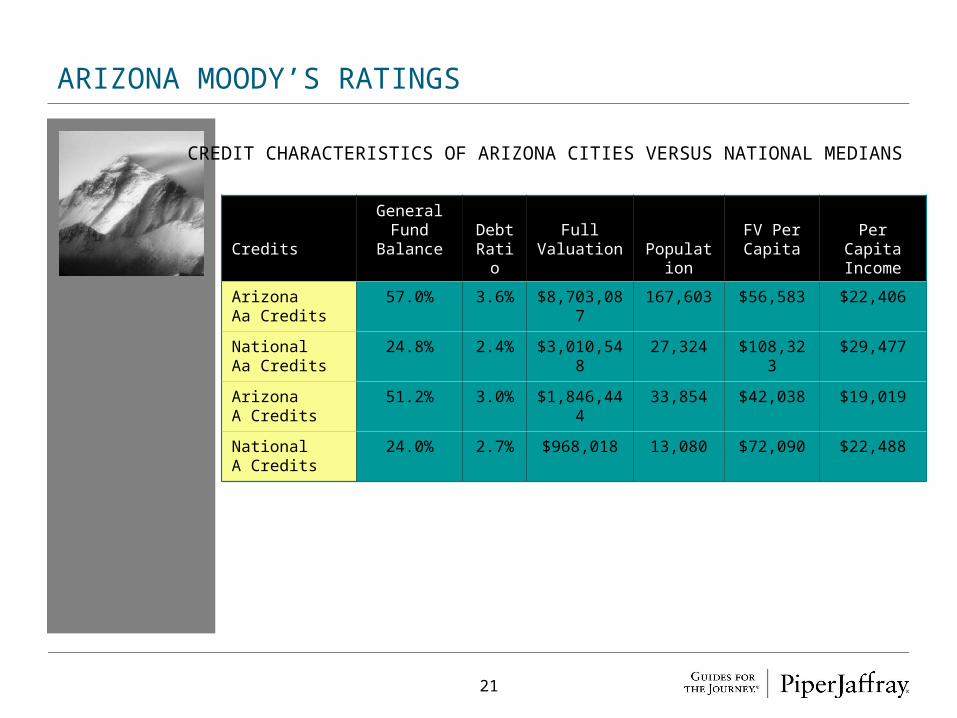

ARIZONA MOODY’S RATINGS

CREDIT CHARACTERISTICS OF ARIZONA CITIES VERSUS NATIONAL MEDIANS

Credits

General Fund

BalanceDebt Ratio

Full Valuation Populati

on

FV Per Capita

Per Capita Income

ArizonaAa Credits

57.0% 3.6% $8,703,087

167,603 $56,583 $22,406

National Aa Credits

24.8% 2.4% $3,010,548

27,324 $108,323

$29,477

ArizonaA Credits

51.2% 3.0% $1,846,444

33,854 $42,038 $19,019

National A Credits

24.0% 2.7% $968,018 13,080 $72,090 $22,488

22

THE RATING PROCESS

Rating committee is not intended to be a mysterious black hole. Rather, its intent is designed to:

• Maintain objectivity

• Maintain consistency among ratings nationally

• Ensure a broad perspective

• Leverage functional expertise of individual analysts

• Ensure quality control

23

THE RATING PROCESS continued

What’s not Fair:

• Asking an analyst what rating he or she is recommending.

• Asking which individuals will comprise the committee.

• Asking how the votes were placed.

24

THE RATING PROCESS continued

What is Fair:

• Asking the analyst for anticipated outcome of committee.

• Asking what credit strengths and weaknesses the analyst intends to highlight to committee.

• Asking the analyst what credits will be presented as comparables to committee.

• Requesting that specific comparables are presented to committee.

• Providing a list of credit strengths to be presented to committee.

• Requesting that a specific individual with unique knowledge of your credit represent at least one member of committee.

• Requesting a site visit or in-person meeting (acknowledging the limits of individual schedules).

25

WHAT TO EXPECT FROM YOUR BANKER

Their assessment of your credit.

Provision of comparable credits.

Benchmarking to enhance decision making.

Assistance in structuring transactions to ensure and maintain credit quality.

An advocate and cheerleader even outside of specific transactions.

Effective intermediary in communications.

26

![pdf [808 KB]](https://img.pdfslide.net/doc/110x75/58497be31a28aba93a8fae18/pdf-808-kb.jpg)