Embed Size (px)

Citation preview

AE-96101

Preliminary Analysis of the Feasibility of an Adult Day Care Center in

Madill, Oklahoma

by

Fred Eilrich - Assistant Research Specialist Oklahoma State University, Stillwater, OK

405-744-9814

Cheryl St. Clair - Extension Associate Oklahoma State University, Stillwater, OK

405-744-9824

Gerald A. Doeksen - Extension Economist Oklahoma State University, Stillwater, OK

405-744-6081

Jack Frye - Extension Rural Development Specialist Ada - 405-332-4100

Val Schott - Director

Oklahoma Office of Rural Health 405-820-9823

Diane Holmes - Chief of Staff

Oklahoma State Department of Health 405-271-6861

Rural Development Service Cooperative Extension Office

Oklahoma State University

October 1996

1

Preliminary Analysis of the Feasibility ofError! Bookmark not defined. an Adult Day Center in Madill, Oklahoma

Introduction

Aged population numbers have increased consistently with longer life expectancy. There are

now more people that require some assistance with health, physical, mental, and/or social needs.

Much of this assistance is long-term in nature and must be administered by either paid or unpaid

services. The rising costs of paid services through health and/or social services has forced a growing

trend toward unpaid services. These services must be contributed by family members and friends.

In 1988, it was estimated that there were more than 7 million unpaid caregivers in the United States

caring for an ill relative or friend (Felder, 1988). As the elderly population and number of

functionally impaired adults grows, more people will confront the need to give care to a loved one.

The additional obligations and sacrifices can be tremendous, especially when coupled with the

normal demands of everyday life.

Community based programs can provide useful services to assist both the members in need

as well as the caregivers currently providing the assistance. This is especially true in rural areas

where it is difficult to utilize existing health and social services alternatives due to travel distances.

Adult day services is one community based program that communities are considering. Adult day

services, commonly referred to as adult day care centers, function as a "respite" (relief) service to

provide safe, secure, therapeutic, and relatively low cost places for impaired family members while

caregivers work, go to school, shop, or simply have some time for themselves to recover from the

demands of caregiving (Travis, 1993).

2

The objective of this report is to provide a preliminary analysis of the feasibility of an adult

day care center for Madill, Oklahoma. More specifically the analysis contains:

1. summary of national study discussing costs and utilization of capacity;

2. estimated need, costs and revenue for a center in Madill;

a. estimated daily participation

b. projected capital and operating costs

c. estimated revenue

d. analysis of transportation costs

3. a brief description of Title XX Social Services Block Grant funds administered by

the Department of Human Services;

4. a brief description of Section 16(b)2 of the Urban Mass Transportation Act;

5. a brief description of the licensing and regulations administered by the Oklahoma

State Department of Health; and

6. a discussion of supplemental financial assistance.

There are several variables that can impact the operations and costs associated with an adult

day services center. The level of dependency or functional impairment of the participant mix greatly

effects staffing needs and other relevant costs. For example, social based centers with minimal,

daily-task dependent participants require the least number of staff and special services where as

dementia specific sites demand additional program services and more intensive specialized staffing

requirements. Utilization can also vary depending on the level of impairment. Continuous

intermixing of participants with contrasting dependency levels may generate frustrations and make

attracting the less dependent more difficult. Separate programs and staffing may be required for

those with greater impairment such as Alzheimer patients. Specialized services and programs

3

offered such as therapeutic treatments, and the variety and choices of individual and group activities

can also effect the number of people that will seek the services offered by the center. For this

preliminary analysis, several assumptions have been made as to the type of programs and

participant mix. Before a decision is made, local decision makers must carefully review these

assumptions, clarify local needs, and specify objectives. This analysis should be modified to

reflect specific local desires.

Summary of National Costs

Two critical aspects in determining the feasibility of an adult day care center are; assessing

the need associated with the venture, and estimating the average costs and revenues. The availability

of average cost data is restricted due to the relatively short time Oklahoma adult day care centers

have been licensed and because current national research is limited. Most literature concerning adult

day care centers focus on structural models and program issues but few studies were found that

addressed the financial aspects or included budget information. In 1986, national survey data were

used to comprehensively examine funding, operating expenses, and the possible effects of capacity

utilization for adult day care centers (Zelman, Elston, and Weissert, 1991). Center level data from

60 metropolitan located adult day care centers were collected, and although actual costs may not

translate to rural Oklahoma, financial profile and relative unit cost comparison information should

represent the entire industry. The following discussion summarizes the survey results.

Day care costs were divided into two general groupings; direct and indirect. Operational

expenses for personnel, equipment and supplies, and facility (direct) costs were separated from

overhead (indirect) costs. Inkind contributions such as volunteer services, donated supplies, and

loaned equipment or facilities were classified based on allocation. Expenses for utilities,

programming and development, etc. were aggregated and reported as other. The proportions of total

4

cost for each category are presented in Table 1. The largest expense category was direct labor

which accounted for slightly more than one-half of total operating expenses (54.4 percent) followed

by transportation costs (12.2 percent). Ninety three percent of the total operating expenses were

actual expenses with only seven percent inkind expenses.

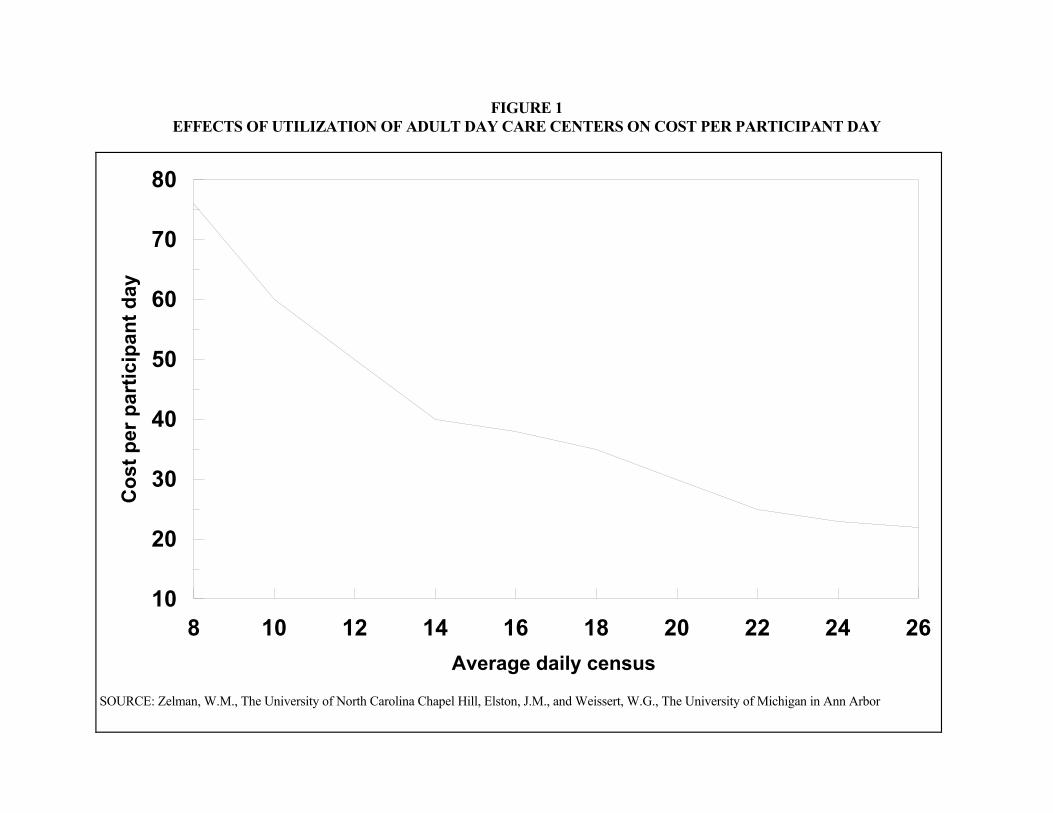

Efficient utilization of capacity was shown to dramatically impact daily participant costs.

Many of the adult day care costs within a given capacity are called "fixed costs". Fixed costs do not

increase with volume but rather decline considerably on a per unit basis as volume increases.

Surveyed centers reported the total number of participants that could be served in their present

location with current staffing levels. A model representative of a given capacity was developed to

illustrate the decreasing unit cost with increased utilization of capacity. The results are presented in

Figure 1. Data from this model illustrated that cost per participant day decreased from $44.35 when

operations were at 50 percent of capacity, to $23.48 when average daily census rose to reported full

capacity. These increased per unit costs at lower utilization rates reveal that it is important to

maintain attendance levels as high as possible to minimize and control costs per participant day.

5

TABLE 1 PERCENT DISTRIBUTION OF INDUSTRY EXPENDITURES FOR ADULT DAY CARE CENTERS AND PERCENT OF LINE ITEM INKIND, BY COST CATEGORY Percent Percent line item Cost category distribution inkind Total 100.0 11.9

Total direct 95.2 7.4

Labor 54.4 2.4

Transportation 12.2 5.2

Facility 10.5 29.6

Food 7.5 20.3

Administration 5.1 3.9

Other 5.5 5.2

Total Indirect 4.8 -----

SOURCE: Zelman, W.M., The University of North Carolina at Chapel Hill, Elston, J.M., and Weissert, W.G., The University of Michigan in Ann Arbor.

FIGURE 1 EFFECTS OF UTILIZATION OF ADULT DAY CARE CENTERS ON COST PER PARTICIPANT DAY SOURCE: Zelman, W.M., The University of North Carolina Chapel Hill, Elston, J.M., and Weissert, W.G., The University of Michigan in Ann Arbor

8 10 12 14 16 18 20 22 24 26Average daily census

10

20

30

40

50

60

70

80

Cos

t per

par

ticip

ant d

ay

7

Estimating Need, Costs and Revenue

Estimated Daily Participation

Two major questions must be answered before proceeding with the planning stages of an

adult day care center. How many potential participants will a given service area generate? How

many of those needing the service will be willing to attend the center? As previously stated, this

number can deviate depending on the mix of participants accepted and the type of programs offered.

Expected length of participation will vary as well. Some participants will only use the service for a

short rehabilitation period following surgery, while others will have a more long-term association.

Adult day care participants can usually be categorized into three groups: physically or mentally

impaired elderly; adults diagnosed as developmentally disabled; and adults with chronic mental

illness (Travis, 1993). The client base and mix will depend on the desires of the center. Because the

majority of adult day care center clients are elderly, the need assessment for Madill only included the

segment of population over 65. If specialization or diversification is desired, the expected need

might change slightly.

National data indicate that approximately 15 percent of the older adult population is

sufficiently impaired and could benefit from the services provided at an adult day care center, but for

various reasons only 1.25 percent can be expected to actually use them (Halpert and Isbell). The

assumed service area was Marshall County. U.S. Bureau of Census 1995 population age 65 and

over estimates for Marshall County are 2,691. If usage coefficients are applied to the estimates, an

estimated 34 (2,691 X .0125) people would use the center. If participant attendance averaged three

days per week, Marshall County service area could generate 5,304 annual participant days (34

participants X 3 days per week X 52 weeks per year). Most centers are operating five days a week

and closed on Thanksgiving, Christmas, New Years, Memorial Day, Labor Day and the Fourth of

8

July. Therefore daily full time equivalent (FTE) demand would be approximately 21 participants

(5,304/254 days per year). For planning purposes, it is usually better to start conservatively and then

expand as information and reputation increases usage. Therefore, for this analysis, two different

budget alternatives will be discussed. Alternative 1 will be based on an adult care center with an

average of five FTE participants per day. Alternative 2 will be based on an adult care center with

an average of ten FTE participants per day. A column (Alternative 3) has also been provided to

allow decision makers the opportunity to construct a budget that represents their specific

assumptions and needs.

Projected Capital and Operating Expenses

When considering an adult care center, the annual budget needed to provide for continued

operations is a major concern. The cost data used in this section are estimated average costs based

on an analysis of the actual Fiscal Year 1995 operating budgets for six adult day centers, as received

from the Oklahoma Inspector General's Office. Due to the small nature of both alternatives, separate

programs and staffing have not been included for mentally impaired participants. Capital and

operating costs associated with providing transportation are included in another section and are not

part of these budgets. If transportation services are provided, the costs will have to be combined.

These are the best cost estimates currently available. However, if local decision makers know actual

costs, the actual costs should be substituted into the budgets in this section (Tables 2 and 3).

9

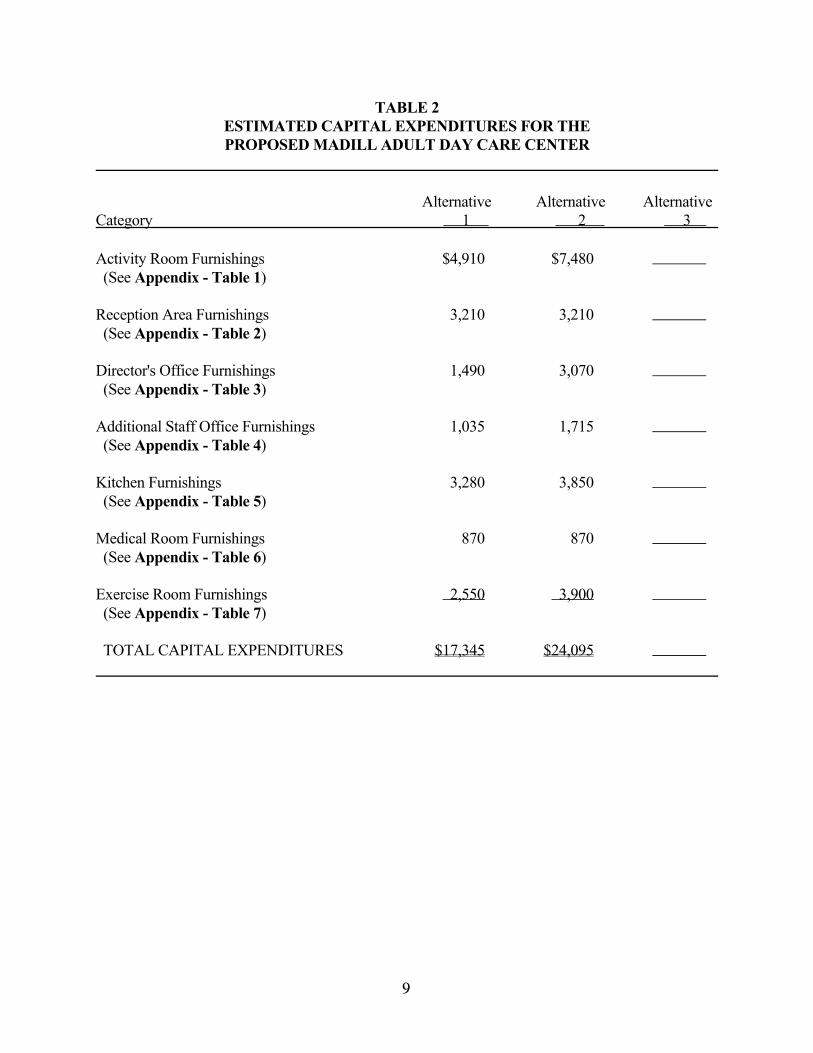

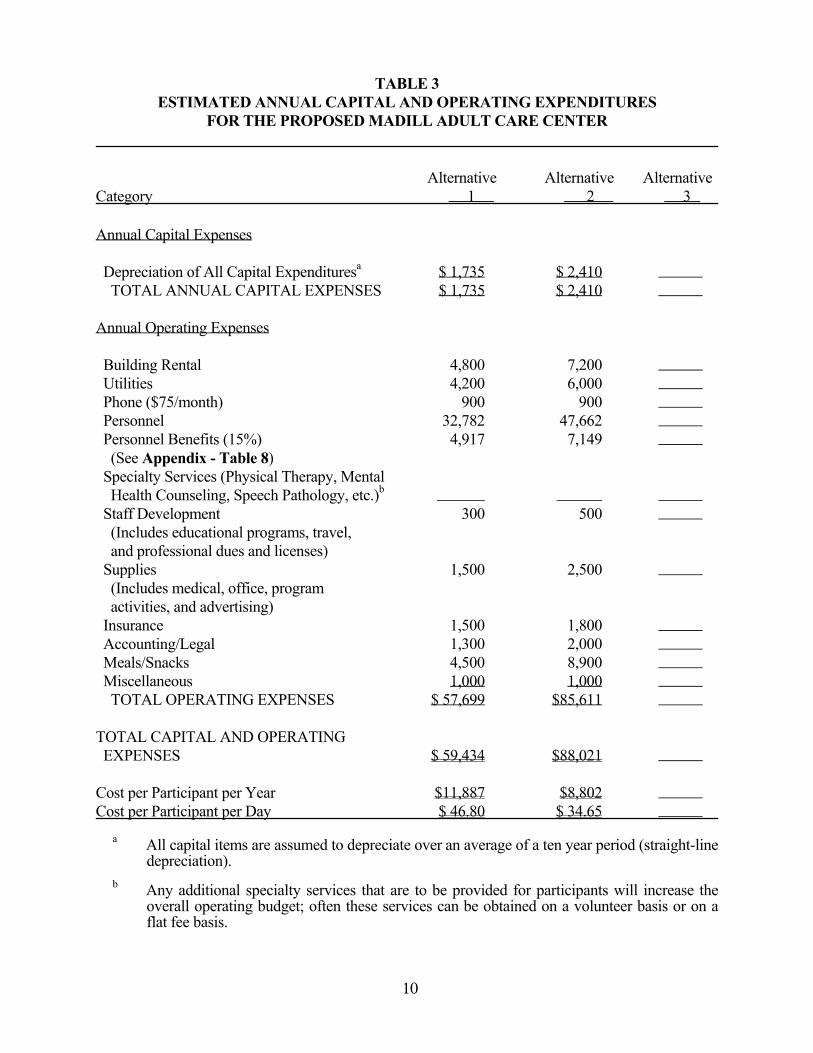

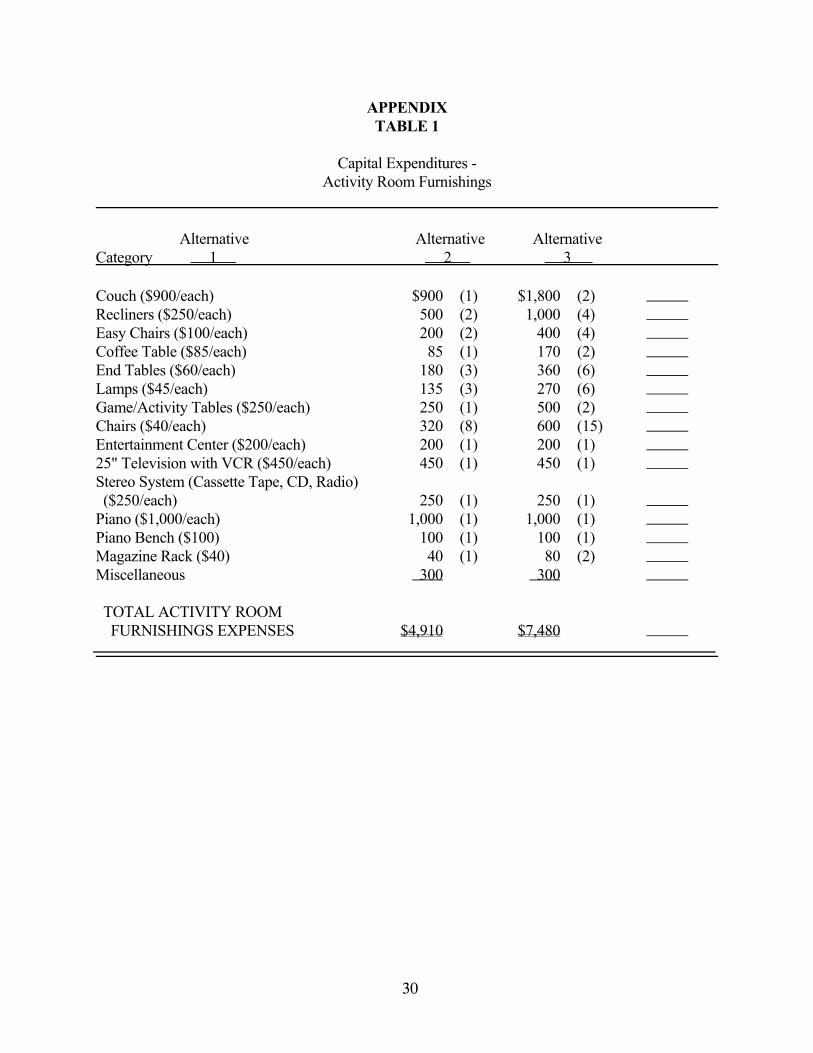

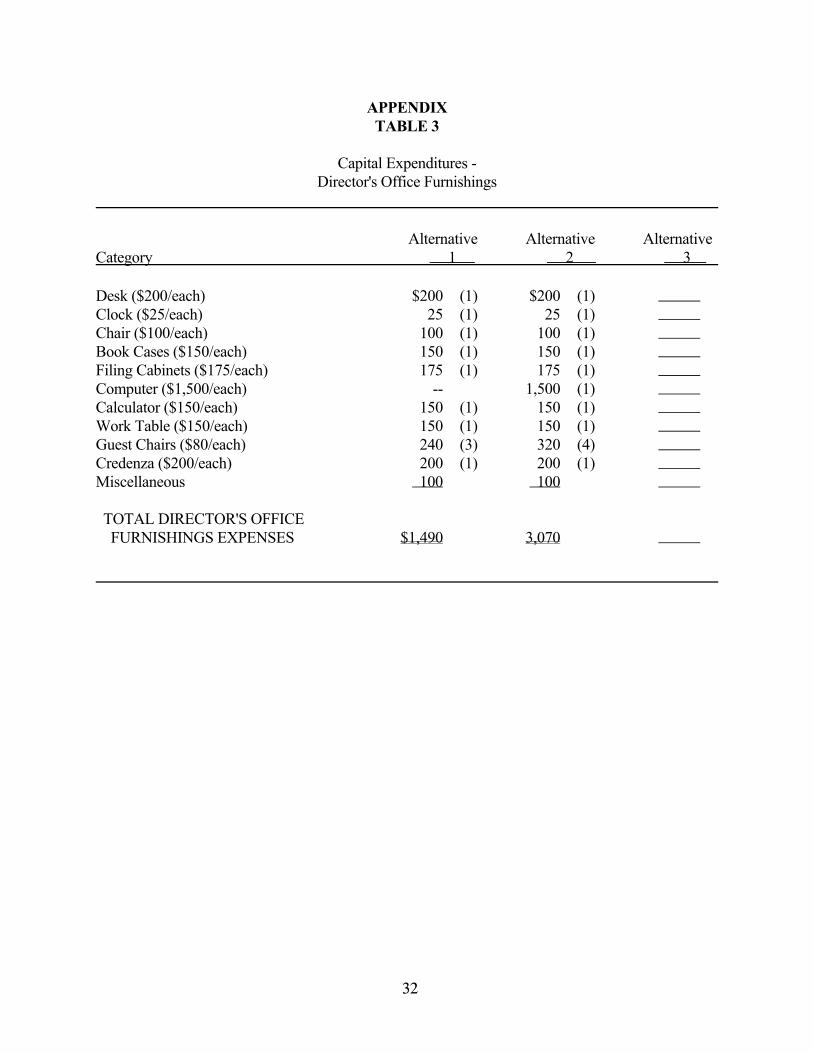

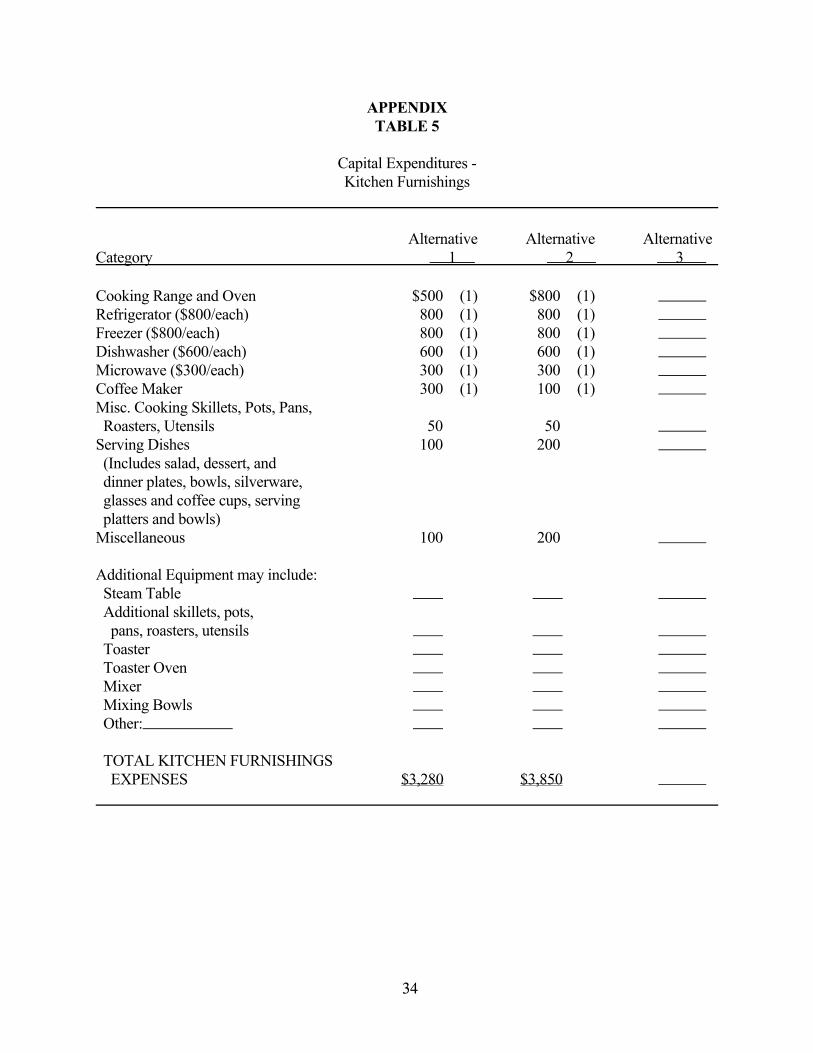

TABLE 2 ESTIMATED CAPITAL EXPENDITURES FOR THE PROPOSED MADILL ADULT DAY CARE CENTER Alternative Alternative Alternative Category 1 2 3 Activity Room Furnishings $4,910 $7,480 (See Appendix - Table 1) Reception Area Furnishings 3,210 3,210 (See Appendix - Table 2) Director's Office Furnishings 1,490 3,070 (See Appendix - Table 3) Additional Staff Office Furnishings 1,035 1,715 (See Appendix - Table 4) Kitchen Furnishings 3,280 3,850 (See Appendix - Table 5) Medical Room Furnishings 870 870 (See Appendix - Table 6) Exercise Room Furnishings 2,550 3,900 (See Appendix - Table 7) TOTAL CAPITAL EXPENDITURES $17,345 $24,095

10

TABLE 3 ESTIMATED ANNUAL CAPITAL AND OPERATING EXPENDITURES FOR THE PROPOSED MADILL ADULT CARE CENTER Alternative Alternative Alternative Category 1 2 3 Annual Capital Expenses Depreciation of All Capital Expendituresa $ 1,735 $ 2,410 TOTAL ANNUAL CAPITAL EXPENSES $ 1,735 $ 2,410 Annual Operating Expenses Building Rental 4,800 7,200 Utilities 4,200 6,000 Phone ($75/month) 900 900 Personnel 32,782 47,662 Personnel Benefits (15%) 4,917 7,149 (See Appendix - Table 8) Specialty Services (Physical Therapy, Mental Health Counseling, Speech Pathology, etc.)b Staff Development 300 500 (Includes educational programs, travel, and professional dues and licenses) Supplies 1,500 2,500 (Includes medical, office, program activities, and advertising) Insurance 1,500 1,800 Accounting/Legal 1,300 2,000 Meals/Snacks 4,500 8,900 Miscellaneous 1,000 1,000 TOTAL OPERATING EXPENSES $ 57,699 $85,611 TOTAL CAPITAL AND OPERATING EXPENSES $ 59,434 $88,021 Cost per Participant per Year $11,887 $8,802 Cost per Participant per Day $ 46.80 $ 34.65 a All capital items are assumed to depreciate over an average of a ten year period (straight-line

depreciation). b Any additional specialty services that are to be provided for participants will increase the

overall operating budget; often these services can be obtained on a volunteer basis or on a flat fee basis.

11

Capital expenditures for an adult care center will include furnishing the main activity

room, a reception area, the director's office, other staff offices, kitchen facilities, a medical room, and

an exercise room. The main activity room furnishings will include couches, recliners, easy chairs,

coffee tables, end tables, lamps, game/activity tables (double as dining room tables), chairs,

entertainment center including television with VCR, stereo with cassette tape, CD, and radio, piano

with bench, magazine racks, and miscellaneous.

A reception area will be needed, including seating for guests (chairs), and furniture for the

receptionist/secretary/administrative assistant including a desk, clock, typewriter, computer with

computer stand, printer, chair, book cases, filing cabinets, calculator, and miscellaneous. For a

smaller adult care center, one typewriter and one computer can be purchased to be shared by all staff

members.

The director's office will need a desk, clock, chair, book cases, filing cabinets, computer

(optional for a smaller adult care center), calculator, work table, extra guest chairs, credenza, and

miscellaneous. The other staff will require access to some office space and equipment. For a

smaller center, an extra desk or two for the activity director and social services director (and/or the

dietitian, LPN/RN, specialty program staff, and program/medical aides) to share would be useful

(i.e., desk, chairs, guest chairs, work table, filing cabinets, book cases, and miscellaneous). For a

larger center, the same furnishings would be needed, just in larger numbers for the desks, chairs, and

guest chairs.

A furnished kitchen will also be necessary containing; a cooking range and oven,

refrigerator, freezer, dishwasher, microwave, coffee maker, a variety of skillets, pots, pans, roasters,

and cooking utensils, serving dishes (salad, dessert, and dinner plates, serving platters, bowls),

silverware, glasses and coffee cups, and miscellaneous. Additional equipment may include a steam

12

table, additional skillets, pots, pans, roaster, cooking utensils, toaster, toaster oven, mixer, mixing

bowls, etc.

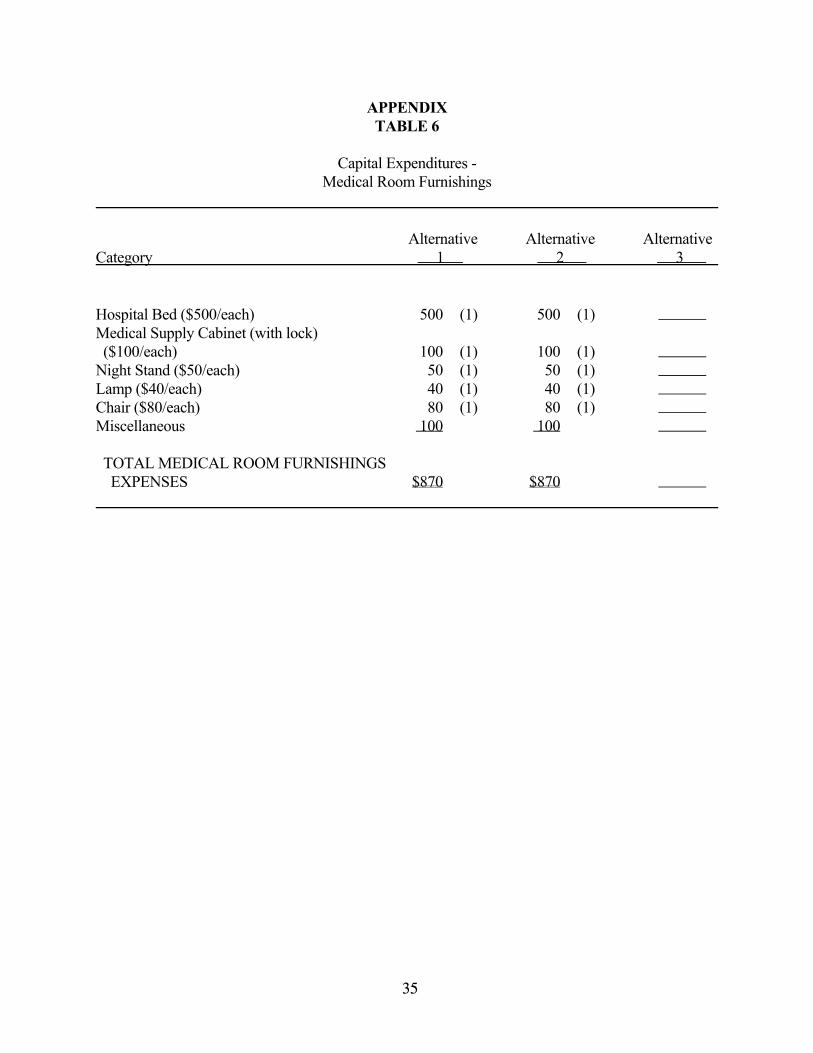

For the medical room, a hospital bed and medical supply cabinet (with lock) will be needed,

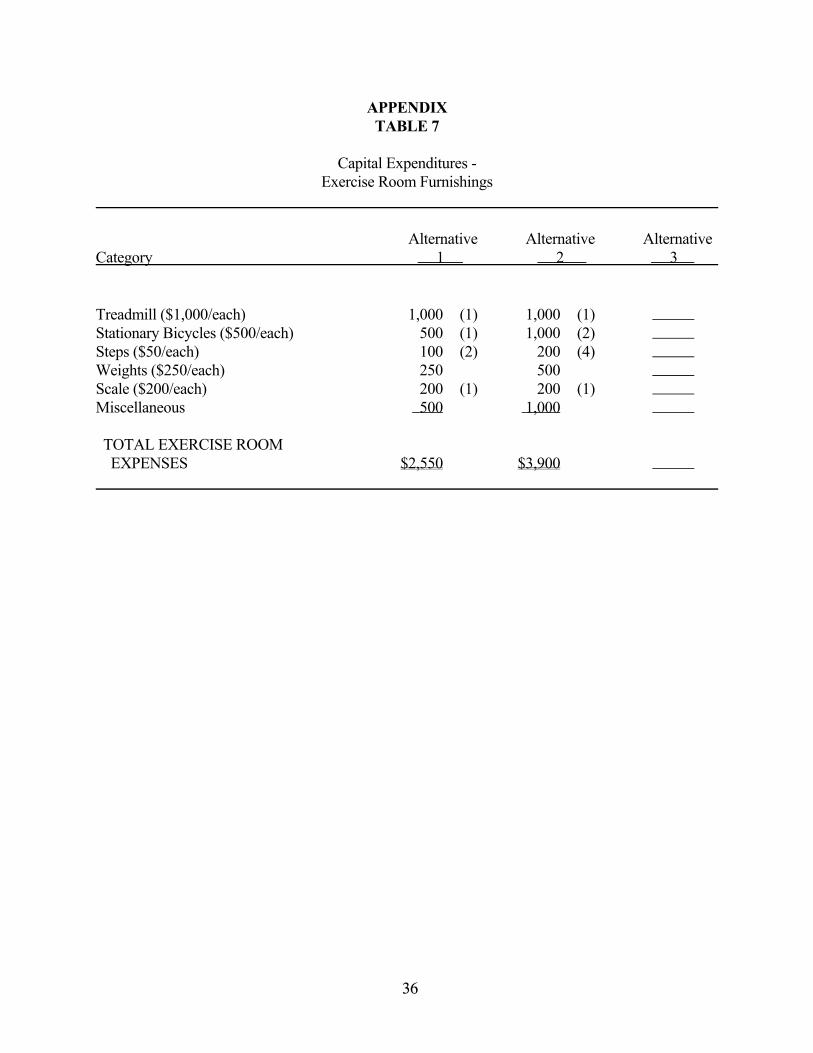

with a nightstand, lamp, chair, and miscellaneous. For the exercise room, appropriate equipment

will be needed (e.g., treadmill, stationary bicycles, steps, weights, scale).

The capital expenditures for Alternative 1 are summarized with estimated total costs in

Table 2. The detailed itemized listings with individual and total costs for each area are included in

Appendix - Tables 1 - 7. For Alternative 1, the total estimated capital expenditures for the activity

room furnishings (Appendix - Table 1) are $4,910, for the reception area (Appendix -Table 2),

$3,210, for the director's office (Appendix - Table 3), $1,490, and for the other staff office

(Appendix - Table 4), $1,035.

For Alternative 1, the total estimated capital expenditures for the kitchen furnishings

(Appendix - Table 5) are $3,280, for the medical room (Appendix - Table 6), $870, and for the

exercise room (Appendix - Table 7), $2,550. The total capital expenditures for Alternative 1 are

estimated at $17,345.

The capital expenditures for Alternative 2 are also summarized in Table 2. Detailed

itemized listings with individual and total costs for each area are provided in Appendix - Tables 1 -

7. For Alternative 2, the total estimated capital expenditures for the activity room furnishings

(Appendix - Table 1) are $7,480, for the reception area furnishings (Appendix - Table 2), $3,210,

for the director's office (Appendix - Table 3), $3,070, and for the additional staff office (Appendix

- Table 4), $1,715.

For Alternative 2, the total estimated capital expenditures for the kitchen furnishings

13

(Appendix - Table 5) are $3,850, for the medical room (Appendix - Table 6), $870, and for the

exercise room (Appendix - Table 7), $3,900. The total capital expenditures for Alternative 2 are

estimated to be $24,095

The capital expenditures can be significant, especially in the first year of operation. If capital

is not available, an agreement with a local financial lender will be required. If a loan is acquired, the

investment can be paid over a period of time at a guaranteed rate. Annual loan payments must be

included as annual operating expenses. In contrast, available sources can be used to purchase the

required capital items. In this case, the cash expense for capital items will not occur in the second

year of operation. Thus, in subsequent years, costs to the adult day center will be lower. A

depreciation fund should be maintained to accumulate replacement costs for new equipment

purchases. It has been assumed that the average life of all capital items is ten years, based on a

straight-line depreciation schedule. Therefore, one-tenth of the overall capital expenditure amount

should be placed in a depreciation fund each year to be available to replace the capital equipment

items as needed in the future. For Alternative 1, the depreciation of all capital expenditures is

estimated to be $1,735 annually (Table 2), as based on a ten-year straight-line depreciation. For

Alternative 2, the depreciation of all capital expenditures is estimated to be $2,410 annually (Table

2).

Annual operating expenditures include facility costs. If construction is required, all expenses

should be managed and depreciated as capital expenditures. For this analysis, it is assumed that rent

agreements for available space will reduce the required capital expenditures.

14

Building rent has been estimated for each alternative. Additional costs for the facility would include

utilities. A phone is estimated at $75 per month.

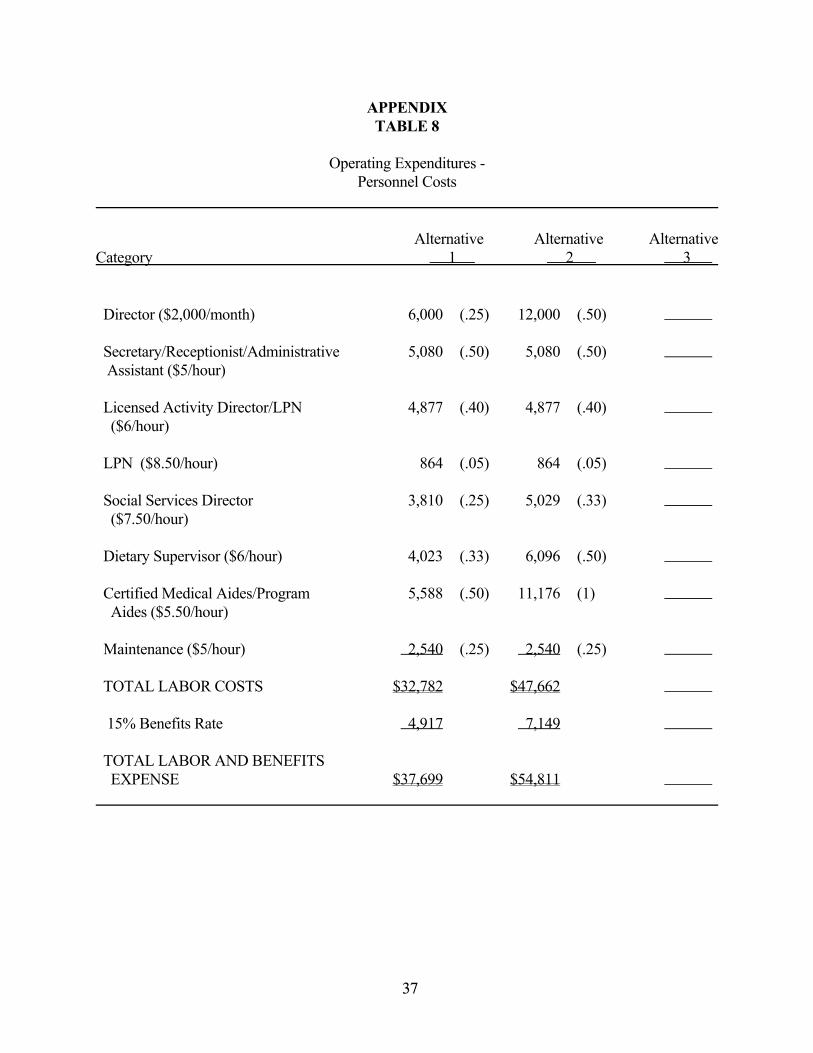

The largest expenditure of an adult care center are the personnel costs, including a director

($2,000 month), a secretary/receptionist ($5/hour), a licensed activity director ($6/hour) a licensed

practical nurse (LPN) ($8.50/hour), a social services director ($7.50/hour), a dietary supervisor

($6/hour), certified medical aides/program aides ($5.50/hour), and maintenance ($5/hour). Benefits

are calculated at the rate of 15% of the total personnel costs. Each center is custom-tailored to meet

the needs of the participants of the center. Specialty services may be needed in the form of physical

therapy, mental health counseling, speech pathology, etc., depending on the needs of the individual

participants at a particular center. These costs are not included in the budget alternatives, as they

will vary greatly from center to center. These costs also may be obtained on a volunteer basis or on

a flat fee basis. Each community adult care center will need to estimate these costs locally.

Staff development costs are included to cover educational programs, travel, and professional

dues and licenses for the staff of the center. Supplies are necessary and will include medical, office,

program activities, advertising, and other miscellaneous as needed. An insurance category is

necessary to cover liability for the staff and the patients. An accounting/legal fee is allotted to cover

necessary audits and legal advice.

Meals and snacks are budgeted; these costs could vary greatly depending on whether this

service is contracted out or provided internally. Due to necessary diets for participants, most centers

contract out for the lunch meal. A miscellaneous category is included to cover any other extraneous

costs.

The annual operating expenses for Alternative 1 are shown in Table 2. The building rent is

estimated at $400 per month, for an annual total of $4,800. Annual costs for utilities are estimated at

15

$4,200 or $350 per month. The phone total is $900 per year.

Referring to Appendix - Table 8, personnel costs were estimated for both alternatives based

on 2,032 hours per year (254 days X 8 hours per day). Costs were estimated for each staff

assignment. Staff members can serve in more than one position, if they meet the minimum stated

requirements. Alternative 1 includes a one quarter-time director, for an annual total of $6,000. The

cost for a half-time secretary/receptionist is estimated at $5,080. The licensed activity director is

estimated to cost $4,877 per year based on forty percent-time. Monthly consultation with a LPN

will cost $864 (five percent-time). A one quarter-time social services director is estimated at $3,810.

The dietary supervisor is assumed to be one third-time at an annual cost of $4,023. Certified

medical aide/program aides are assumed to be equivalent to one half-time position for an annual cost

of $5,588. The maintenance staff is estimated at one quarter-time for an annual cost of $2,540. The

total personnel costs for Alternative 1 are estimated to be $32,782 per year. The personnel benefits

are estimated at 15% of personnel costs for an annual total of $4,917.

The specialty services category in Table 2, Alternative 1 is left blank to be estimated by the

local decision makers. Staff development is estimated at an annual total of $300. Supplies are

estimated to cost $1,500 per year. Insurance is estimated at $1,500 per year and accounting/legal

costs, $1,300 per year.

Meals and snacks are estimated to cost $4,500 for Alternative 1. A miscellaneous category

totalling $1,000 is also included. The total annual operating expenses for Alternative 1 are $57,699,

with annual capital and operating expenses totalling $59,434. Annual cost per average number of

participants (5) are $11,887 yielding a daily cost per participants of $46.80.

The annual operating expenses for Alternative 2 are shown in Table 2. The building rent is

16

estimated at $600 per month, for an annual total of $7,200. Annual costs for utilities are estimated at

$6,000 or $500 per month. The phone total is $900 per year.

Referring to Appendix - Table 8, personnel for Alternative 2 includes a half-time director,

for an annual total of $12,000. Estimated annual costs of $5,080, $4,877, and $864 were again

included for a secretary/receptionist (half-time), licensed activity director (forty percent-time), and

LPN (five percent-time), respectively. Staffing time for the social services director was increased to

one third-time and estimated at $5,029. Alternative 2 assumed a half-time dietary supervisor at an

annual cost of $6,096. The certified medical aides/program aides are assumed to be equivalent to

one full-time positions for an annual cost of $11,176. The maintenance staffing cost remains at

$2,540. Total personnel costs for Alternative 2 are estimated to be $47,662 per year. Personnel

benefits are estimated at 15% of personnel costs or $7,149.

Staff development is estimated at an annual total of $500. Supplies are estimated to cost

$2,500 per year. Insurance is estimated at $1,800 per year and accounting/legal costs, $2,000 per

year. Meals and snacks are estimated to cost $8,900 for Alternative 2. Miscellaneous costs of

$1,000 are also included. The total annual operating expenses for Alternative 2 are $85,611, with

combined annual capital and operating expenses totalling $88,021. Annual cost per average number

of participants (10) is $8,802 or $34.65 per day per participants.

17

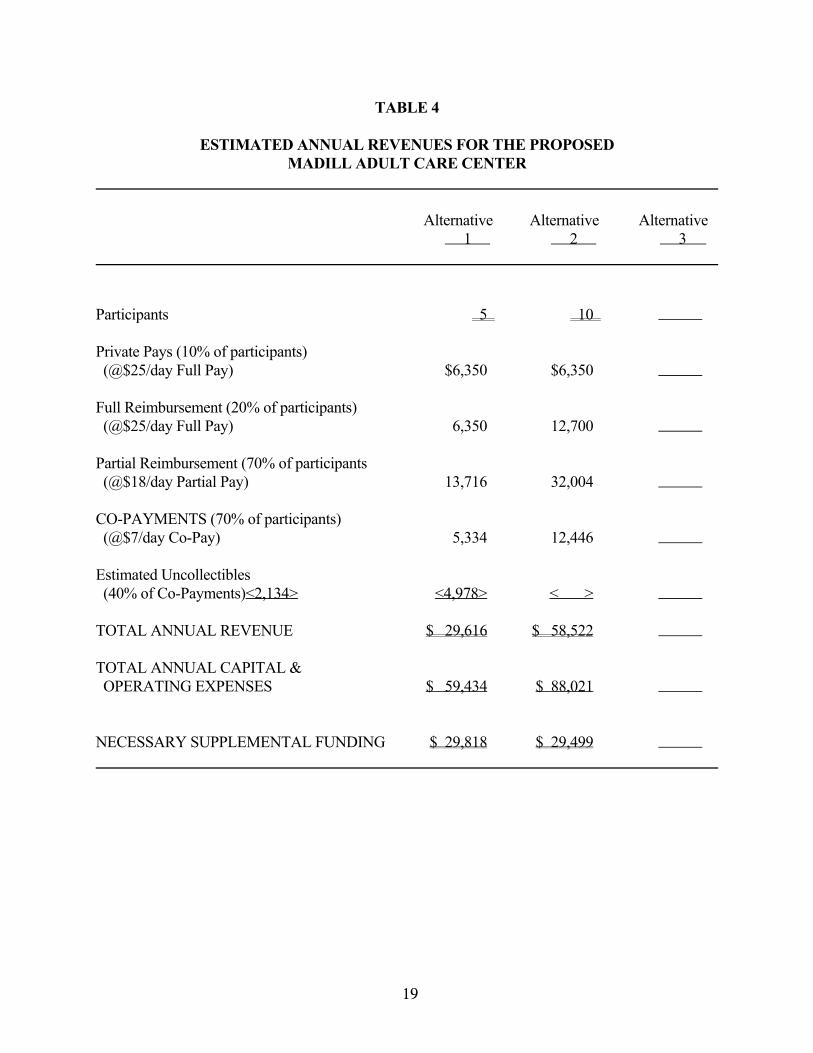

Estimated Revenue

Estimated revenues for the proposed Madill adult day center are based on $25 per day

participant fees. The economic eligibility or ability to pay for the services will vary significantly

among participants. Some will fully fund their visits while others will qualify for DHS (Title XX)

reimbursement. Participants that pay for the services without assistance are called private pays.

However, operators of Oklahoma adult day care centers expressed that the majority of their

participants are receiving some level of assistance. If a participant's financial welfare is low enough,

they can receive full reimbursement (currently based on $25 per day). Those participants that

qualify for assistance but do not qualify for full reimbursement will have a co-payment based on

their income. According to DHS, the average co-payment is $7. Two other typical reimbursement

programs are veterans entitlements and mental clinic referrals. Both programs contribute

reimbursement based on $25 per day. Currently, reimbursements from medicaid are not available

for adult day care services in Oklahoma.

The estimated annual revenues from patient fees (including reimbursements) are presented

in Table 4. It was estimated that 90 percent of the participants qualify for some assistance. Twenty

percent qualify for full reimbursement, while the other 70 percent will be responsible for a co-

payment. There was no distinction made as to the specific reimbursement program since most

programs use a $25 per day rate. The remaining 10 percent will be private pays. Total charges for a

center open 254 days would be $31,750 (5 X 25 X 254) with five FTE participants and $63,500 (10

X 25 X 254) with ten FTE participants. However, some level of uncollected fees should be

included. Periodically, participants will not be able to contribute their co-payment. To manage

daily attendance and to provide the service to those that need it, operators of adult day care centers

rarely turn participants away for lack of ability to pay. For this analysis, it was assumed that 40

18

percent of the co-payment revenue would not be collected. Therefore, total revenue from patient

fees is $29,616 with five FTE and $58,522 for a center with 10 FTE participants. With total

operating and capital expenses from Table 2, it is not possible to break even with only participant

fees. Supplemental funding alternatives must be acquired. A center providing services for five FTE

participants will require $29,818 supplemental assistance while a center providing services for ten

FTE will require $29,499. If transportation services are provided, necessary supplemental assistance

will increase. A discussion of Title XX and other financial alternatives are included in the

proceeding sections of this analysis.

19

TABLE 4 ESTIMATED ANNUAL REVENUES FOR THE PROPOSED MADILL ADULT CARE CENTER Alternative Alternative Alternative 1 2 3 Participants 5 10 Private Pays (10% of participants) (@$25/day Full Pay) $6,350 $6,350 Full Reimbursement (20% of participants) (@$25/day Full Pay) 6,350 12,700 Partial Reimbursement (70% of participants (@$18/day Partial Pay) 13,716 32,004 CO-PAYMENTS (70% of participants) (@$7/day Co-Pay) 5,334 12,446 Estimated Uncollectibles (40% of Co-Payments)<2,134> <4,978> < > TOTAL ANNUAL REVENUE $ 29,616 $ 58,522 TOTAL ANNUAL CAPITAL & OPERATING EXPENSES $ 59,434 $ 88,021 NECESSARY SUPPLEMENTAL FUNDING $ 29,818 $ 29,499

20

Analysis of Transportation Costs

Adult day care centers often provide services for those that need transportation to and from

the center. Regulations by the Oklahoma State Department of Health to ensure the health and safety

of the participants are summarized:

A. The number of passengers shall not exceed the vehicle's design;

B. The vehicle shall be equipped to accommodate those participants that require

equipment to assist with ambulation;

C. An opportunity to have a rest stop must be offered when the trip exceeds one hour;

D. At least one staff person in the vehicle must be trained in first aid and CPR;

E. The provider must conform to all state laws regarding regulations, driver, vehicles, and

insurance; and

F. The vehicle must be maintained in good repair.

Centers can provide transportation directly or by contractual agreements with existing

community carriers. A budget has been provided in Table 5 presenting both the estimated capital

costs and annual expenses (capital and operating). Cost data used in this report are best cost

estimates based on previous research and sources including; vehicle and communication equipment

dealers, and personnel from the Oklahoma Department of Transportation. Option 1 includes the

costs necessary to own and operate a transportation system. Costs are presented based on Section

16(b)2 Federal cost share ratios. (For more detail, refer to the section on Section 16(b)2

funding.) Option 2 has been provided to allow decision makers to design their own system or

include local costs.

21

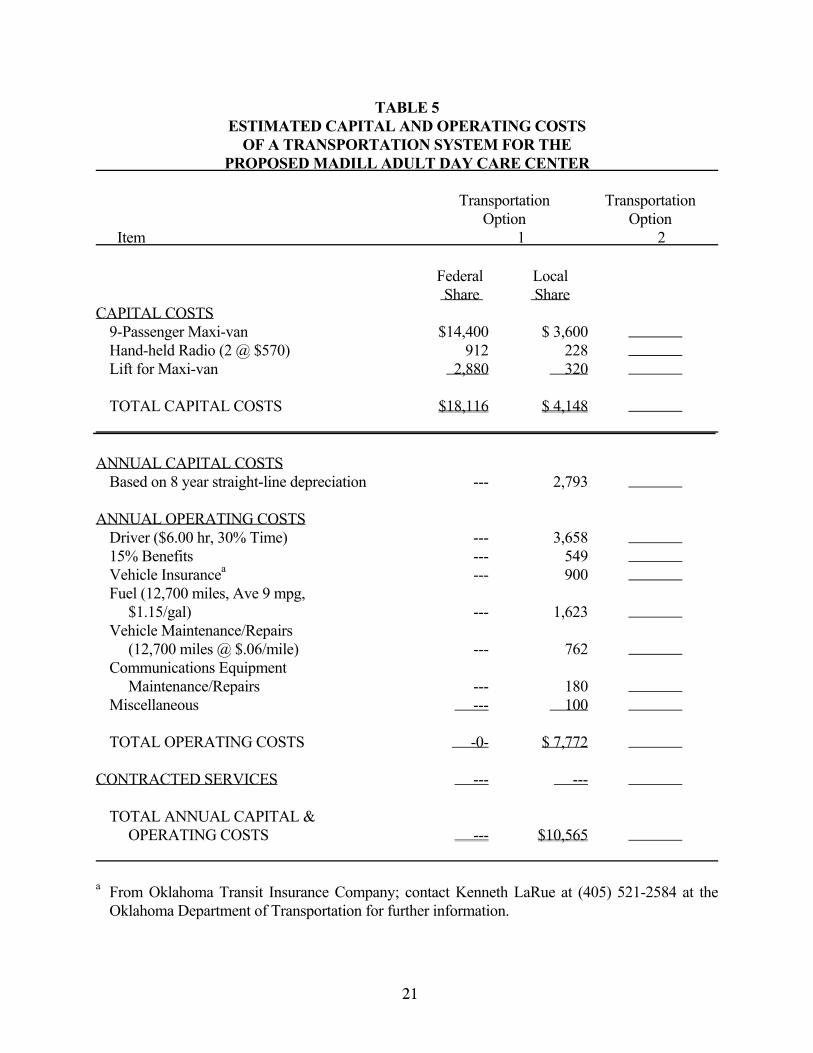

TABLE 5 ESTIMATED CAPITAL AND OPERATING COSTS OF A TRANSPORTATION SYSTEM FOR THE PROPOSED MADILL ADULT DAY CARE CENTER Transportation Transportation Option Option Item 1 2 Federal Local Share Share CAPITAL COSTS 9-Passenger Maxi-van $14,400 $ 3,600 Hand-held Radio (2 @ $570) 912 228 Lift for Maxi-van 2,880 320 TOTAL CAPITAL COSTS $18,116 $ 4,148 ANNUAL CAPITAL COSTS Based on 8 year straight-line depreciation --- 2,793 ANNUAL OPERATING COSTS Driver ($6.00 hr, 30% Time) --- 3,658 15% Benefits --- 549 Vehicle Insurancea --- 900 Fuel (12,700 miles, Ave 9 mpg, $1.15/gal) --- 1,623 Vehicle Maintenance/Repairs (12,700 miles @ $.06/mile) --- 762 Communications Equipment Maintenance/Repairs --- 180 Miscellaneous --- 100 TOTAL OPERATING COSTS -0- $ 7,772 CONTRACTED SERVICES --- --- TOTAL ANNUAL CAPITAL & OPERATING COSTS --- $10,565 a From Oklahoma Transit Insurance Company; contact Kenneth LaRue at (405) 521-2584 at the

Oklahoma Department of Transportation for further information.

22

Contractual arrangements between the proposed Madill Adult Day Care Center and other

organizations or entities may be worked out to pay for the transportation services. An important part

of the contract is the price to be paid for the service. One possible method of determining the value

of a contract for service is to relate the price to the cost of the service. No information on contractual

arrangements have been estimated; however, these arrangements can also be included in the budget

in Option 2.

Option 1 is based on the purchase of one vehicle with a handicap lift. If emergencies or

route changes occur, communication with the vehicle driver would be needed. Capital costs include

the purchase of one maxi-van that seats nine passengers ($18,000) with a handicap lift ($3,200).

Two hand-held radios were estimated at $1,140 ($570 each). Total costs for capital items are

$22,340.

In Table 5, the operating costs for Option 1 include labor, insurance, fuel, maintenance,

communication equipment, and miscellaneous. Option 1 assumes that a driver will need to be paid

an hourly wage for services plus benefits. Driver responsibilities are estimated to equal one 30

percent FTE employee. If the driver is paid $6.00 per hour with 15 percent benefits, total costs will

be $4,207. Transportation routes will need to be run once in the morning and once in the evening.

An assumed twenty-five mile route would total 12,700 annual miles (254 days). Based on mileage,

annual fuel and maintenance expenses would total $1,623 and $762, respectively. Other annual

operating costs include insurance ($900), maintenance and repair of communication equipment

($180), and miscellaneous (100). Therefore, total annual operating costs to own and operate a

transportation system are estimated at $7,772.

Annual capital (depreciation) costs should also be included in the annual budget. The cash

expense of capital purchases will not occur in the second year of operation. However, center

23

operators should maintain a depreciation fund to accumulate replacement costs for new equipment

purchases. Application for grant funds can be submitted to replace the equipment, but funds are not

guaranteed. Therefore, the depreciation fund should cover total replacement costs. A maxi-van has

a life expectancy of 100,000 miles. With an estimated annual usage of 12,700 miles, replacement is

expected every 8 years (100,000/12,700). The annual replacement costs with straight-line

depreciation are $2,250 ($18,000/8 years). The communication and lift equipment are also expected

to require replacement every 8 years requiring annual replacement costs of $140 and $400

respectively. Total annual depreciation allowance is $2,793. Annual capital and operating costs

total $10,565.

Providing transportation can significantly increase the operating budget of an adult day

center. However, it is often one of the services that are provided to better accommodate members of

the community. As with other operating expenses, decision makers should explore all supplemental

financial assistance alternatives if they decide to provide transportation.

24

Title XX Social Services Block Grant

Social Services Block Grant Funds are federal monies allocated each year and made

available through a performance based contract from the Department of Human Services (DHS).

Each participant's economic eligibility is evaluated and reimbursement is based on a sliding scale.

Currently, maximum reimbursement is $25 per day. Depending on the participant's income, a co-

payment may be required. Participants must apply through their local County DHS office. If

approved for contract, the Adult Day Services Center will bill monthly to the Oklahoma DHS for

each eligible participant that amount which is reimbursable. Funds are limited and contracts are

renewed annually. For more information contact the Department of Human Services, Special Unit

on Aging, P.O. Box 25352, Oklahoma City, OK 73125, (405) 521-2327.

Section 16(b)2 Funding

Section 16(b)2 of the Urban Mass Transportation Act offers financial assistance to enhance

the transportation opportunities of the elderly and/or handicapped. Under provisions of this section,

the federal government may award grants that will pay for 80 percent of the eligible capital items

needed to provide the service -- vehicles, communications equipment, etc. Vehicle related

equipment required to comply with Americans with Disabilities Act (ADA) or the Clean Air Act

may be funded at 90 percent Federal Share. The balance (10 or 20%) for capital items and all of the

operating costs are the responsibility of the sponsoring agency. Any private nonprofit organization

can be the sponsoring agency of a 16(b)2 transportation system

There are no urban/rural restrictions on the 16(b)2 program. The main purpose of the

program is to serve the elderly and/or the handicapped. The Oklahoma program is administered by

the Department of Human Services, Special Unit on Aging, P.O. Box 25352, Oklahoma City, OK

73125, (405) 521-4214.

25

Licensing and Regulations

Licensing requirements for Adult Day Care Centers are administered by the Oklahoma State

Department of Health. Regulations and standards are provided for by the "Adult Day Care" Act

made effective in 1989. Any facility except for retirement centers and senior citizens centers which

provide basic day care services to four or more unrelated impaired adults for more than four hours in

a twenty-four hour period must be licensed. The license for operation of a center shall be issued by

the Department and shall be subject to annual review. The Department shall at least annually, and

whenever it deems necessary, inspect each adult day care center to determine compliance with the

Adult Day Care Act (Oklahoma Department of Health, 1994).

Many of the regulations are very flexible to allow centers of different sizes and programs to

develop their services accordingly. There are some specific regulations in the area of staffing and

facilities. A sufficient number of direct care staff must be on duty at all times with a minimum of

one full-time equivalent direct care staff person for every eight participants. As functional

impairments increase, the staff-participant ratio must be adjusted. As a minimum, each center must

have a director, activity director, social worker, dietary supervisor, and medical staff. Each center

shall have additional staff, such as nurses, therapists, consultants, drivers, etc. based on the program

plan for the center. Staff can serve in more than one position as long as qualifications are met and

time is documented for each position.

At least one-half of the daily activities must be planned and a minimum of one meal daily

must be arranged for or provided for all participants who attend the center for four or more hours. A

minimum of 40 square feet of space is required for each participant, excluding hallways, storage

areas, offices, rest rooms, and kitchens. Finally, any additional services such as transportation and

special therapies have requirements that must be met if provided.

26

Complete regulations, standards, and requirements are defined concerning organization,

staffing (ratios and qualifications), services, and facilities. For complete regulation details or for

more information, contact the Oklahoma State Department of Health, Special Health Services, 1000

Northeast Tenth Street, Oklahoma City, OK 73117-1299, (405) 271-6868.

Supplemental Financial Assistance

A discussion with many operators of Adult Day Care Centers in Oklahoma revealed that

typically the standard fee for services is $25 per day. Many center operators feel that an increase

above that rate would severely limit participation in the program with the current DHS Title XX,

Veterans Entitlement, and Mental Program reimbursement rates set at $25 per day. However, this

fee level is not enough to cover total operating costs. Additional funds, community assistance,

and/or partnerships are necessary. Furthermore, many participants are not able to contribute their

total co-payment. Most contacted centers stated that rather than refuse clients, additional funds were

sought. The following is a short discussion on some of the supplemental assistance alternatives

discovered. Soliciting and securing assistance can be one of the more challenging tasks, but the

number of alternatives is only limited by the creativity and efforts of the administration, staff and

community members.

Assistance can be received in an assortment of ways and can be generated from a variety of

sources. Everything from facilities, utilities, equipment, and supplies, to labor and consultation can

be pursued. State and local government agencies, local organizations, and private corporations often

contribute available funding for specific programs. Assistance can also be in the form of subsidies

such as staffing assistance from JTPA, Work Study, and Action programs, or food donations from

the local food bank. Affiliations and/or partnerships with other entities can be mutually beneficial

through the sharing of facilities, utilities, staffing, transportation, etc. and thereby, reduce total

27

operating costs. Community and center fund raising activities are a good alternative for financing

and in-kind donations. An example of sources of assistance are:

1. State and local government agencies

A. Oklahoma Department of Health

B. Oklahoma Department of Education

C. Oklahoma Department of Transportation

D. Oklahoma Department of Agriculture

E. Oklahoma Employment Security Commission (JTPA program)

E. CACFP food program

F. University Work Study Programs and Student Practicums

2. Private and local organizations

A. United Way

B. Food Bank

C. Private corporations

D. Civic groups

E. Churches

F. Home Health Care

G. Local governments

3. Affiliations and partnerships

A. Hospitals

B. Home Health Care Providers

C. Educational Institutions; Area Vo-Tech Schools, Universities, etc.

D. Churches

E. Nursing Homes

Finally, volunteer services are often available from community organizations, churches,

professional staff, and community members. There are always generous community members and

caregivers that enjoy donating their time and services. Volunteer services give the entire community

the opportunity to contribute to the care and needs of fellow community members that require

mental, physical, and social assistance.

28

Summary

Estimated budgets for an adult day care center in Madill reveal that it will not break even

with patient revenues. Supplemental financial assistance will have to be explored. Providers of

related services should also be contacted to examine all possible alternatives. Adult day care centers

currently operating in Oklahoma expressed their reliance on reimbursements. Future Federal and

State money may be limited and availability must be verified before proceeding.

It must be emphasized that this is a preliminary analysis based on assumptions of service

area, services provided, and client base and mix. All assumptions should be closely examined by

local decision makers to verify that they reflect local conditions and objectives. For example, the

service area depicted here may change due to transportation considerations or the creation of

additional centers. National utilization coefficients may overestimate the demand in some rural

areas due to family preferences for providing the service themselves or cost barriers. Likewise,

specialization and/or diversification decisions could increase or decrease utilization rates. This

analysis was based on current regulations and the best available cost and revenue data. If additional

local data are available, they should be included to arrive at the most realistic analysis possible.

Furthermore, if licensing or operation requirements change, budget adjustments might be required.

No recommendations have been made. The information is designed to help decision makers plan

and develop an Adult Day Center in Madill Oklahoma.

29

References

Felder, L., "Caregiver Support Programs Spreading Nationwide", The Aging Connection, 9(2), April/May, 1988.

Halpert, B. and L. Isbell, Adult Day Care: "Will it Work for Your Community?", University

Cooperative Extension Service, University of Missouri-Columbia, (Supplement to GH 6748, Adult Day Care.

Oklahoma State Department of Health, "Adult Day Care Center Regulations", Chapter 605,

Oklahoma State Department of Health, Special Health Services, August 1, 1994. Travis, Shirley S., Commonwealth Adult Day Care Technical Assistance Manual, Virginia

Cooperative Extension, 1993. Zelman, William M., Jennifer M. Elston, and William G., Weissert, "Financial Aspects of Adult Day

Care: National Survey Results", Health Care Financing Review, Volume 12 Number 3, Spring, 1991, pp. 27-36.

30

APPENDIX TABLE 1 Capital Expenditures - Activity Room Furnishings Alternative Alternative Alternative Category 1 2 3 Couch ($900/each) $900 (1) $1,800 (2) Recliners ($250/each) 500 (2) 1,000 (4) Easy Chairs ($100/each) 200 (2) 400 (4) Coffee Table ($85/each) 85 (1) 170 (2) End Tables ($60/each) 180 (3) 360 (6) Lamps ($45/each) 135 (3) 270 (6) Game/Activity Tables ($250/each) 250 (1) 500 (2) Chairs ($40/each) 320 (8) 600 (15) Entertainment Center ($200/each) 200 (1) 200 (1) 25" Television with VCR ($450/each) 450 (1) 450 (1) Stereo System (Cassette Tape, CD, Radio) ($250/each) 250 (1) 250 (1) Piano ($1,000/each) 1,000 (1) 1,000 (1) Piano Bench ($100) 100 (1) 100 (1) Magazine Rack ($40) 40 (1) 80 (2) Miscellaneous 300 300 TOTAL ACTIVITY ROOM FURNISHINGS EXPENSES $4,910 $7,480

31

APPENDIX TABLE 2 Capital Expenditures - Reception Area Furnishings Alternative Alternative Alternative Category 1 2 3 Guest Chairs ($80/each) $160 (2) $160 (2) Desk ($200/each) 200 (1) 200 (1) Clock ($25/each) 25 (1) 25 (1) Typewriter ($200/each) 200 (1) 200 (1) Computer ($1,500/each) 1,500 (1) 1,500 (1) Printer ($300/each) 300 (1) 300 (1) Computer Stand ($150/each) 150 (1) 150 (1) Chair ($100/each) 100 (1) 100 (1) Book Cases ($150/each) 150 (1) 150 (1) Filing Cabinets ($175/each) 175 (1) 175 (1) Calculator ($150/each) 150 (1) 150 (1) Miscellaneous 100 100 TOTAL RECEPTION AREA FURNISHINGS EXPENSES $3,210 $3,210

32

APPENDIX TABLE 3 Capital Expenditures - Director's Office Furnishings Alternative Alternative Alternative Category 1 2 3 Desk ($200/each) $200 (1) $200 (1) Clock ($25/each) 25 (1) 25 (1) Chair ($100/each) 100 (1) 100 (1) Book Cases ($150/each) 150 (1) 150 (1) Filing Cabinets ($175/each) 175 (1) 175 (1) Computer ($1,500/each) -- 1,500 (1) Calculator ($150/each) 150 (1) 150 (1) Work Table ($150/each) 150 (1) 150 (1) Guest Chairs ($80/each) 240 (3) 320 (4) Credenza ($200/each) 200 (1) 200 (1) Miscellaneous 100 100 TOTAL DIRECTOR'S OFFICE FURNISHINGS EXPENSES $1,490 3,070

33

APPENDIX TABLE 4 Capital Expenditure - Other Staff Office Furnishings Alternative Alternative Alternative Category 1 2 3 Desks ($200/each) 200 (1) 600 (3) Chairs ($100/each) 100 (1) 300 (3) Guest Chairs ($80/each) 160 (2) 240 (3) Work Tables ($150/each) 150 (1) 150 (1) Filing Cabinets ($175/each) 175 (1) 175 (1) Book Cases ($150/each) 150 (1) 150 (1) Miscellaneous 100 100 TOTAL OTHER STAFF OFFICE FURNISHINGS EXPENSES $1,035 $1,715

34

APPENDIX TABLE 5 Capital Expenditures - Kitchen Furnishings Alternative Alternative Alternative Category 1 2 3 Cooking Range and Oven $500 (1) $800 (1) Refrigerator ($800/each) 800 (1) 800 (1) Freezer ($800/each) 800 (1) 800 (1) Dishwasher ($600/each) 600 (1) 600 (1) Microwave ($300/each) 300 (1) 300 (1) Coffee Maker 300 (1) 100 (1) Misc. Cooking Skillets, Pots, Pans, Roasters, Utensils 50 50 Serving Dishes 100 200 (Includes salad, dessert, and dinner plates, bowls, silverware, glasses and coffee cups, serving platters and bowls) Miscellaneous 100 200 Additional Equipment may include: Steam Table Additional skillets, pots, pans, roasters, utensils Toaster Toaster Oven Mixer Mixing Bowls Other: TOTAL KITCHEN FURNISHINGS EXPENSES $3,280 $3,850

35

APPENDIX TABLE 6 Capital Expenditures - Medical Room Furnishings Alternative Alternative Alternative Category 1 2 3 Hospital Bed ($500/each) 500 (1) 500 (1) Medical Supply Cabinet (with lock) ($100/each) 100 (1) 100 (1) Night Stand ($50/each) 50 (1) 50 (1) Lamp ($40/each) 40 (1) 40 (1) Chair ($80/each) 80 (1) 80 (1) Miscellaneous 100 100 TOTAL MEDICAL ROOM FURNISHINGS EXPENSES $870 $870

36

APPENDIX TABLE 7 Capital Expenditures - Exercise Room Furnishings Alternative Alternative Alternative Category 1 2 3 Treadmill ($1,000/each) 1,000 (1) 1,000 (1) Stationary Bicycles ($500/each) 500 (1) 1,000 (2) Steps ($50/each) 100 (2) 200 (4) Weights ($250/each) 250 500 Scale ($200/each) 200 (1) 200 (1) Miscellaneous 500 1,000 TOTAL EXERCISE ROOM EXPENSES $2,550 $3,900

37

APPENDIX TABLE 8 Operating Expenditures - Personnel Costs Alternative Alternative Alternative Category 1 2 3 Director ($2,000/month) 6,000 (.25) 12,000 (.50) Secretary/Receptionist/Administrative 5,080 (.50) 5,080 (.50) Assistant ($5/hour) Licensed Activity Director/LPN 4,877 (.40) 4,877 (.40) ($6/hour) LPN ($8.50/hour) 864 (.05) 864 (.05) Social Services Director 3,810 (.25) 5,029 (.33) ($7.50/hour) Dietary Supervisor ($6/hour) 4,023 (.33) 6,096 (.50) Certified Medical Aides/Program 5,588 (.50) 11,176 (1) Aides ($5.50/hour) Maintenance ($5/hour) 2,540 (.25) 2,540 (.25) TOTAL LABOR COSTS $32,782 $47,662 15% Benefits Rate 4,917 7,149 TOTAL LABOR AND BENEFITS EXPENSE $37,699 $54,811