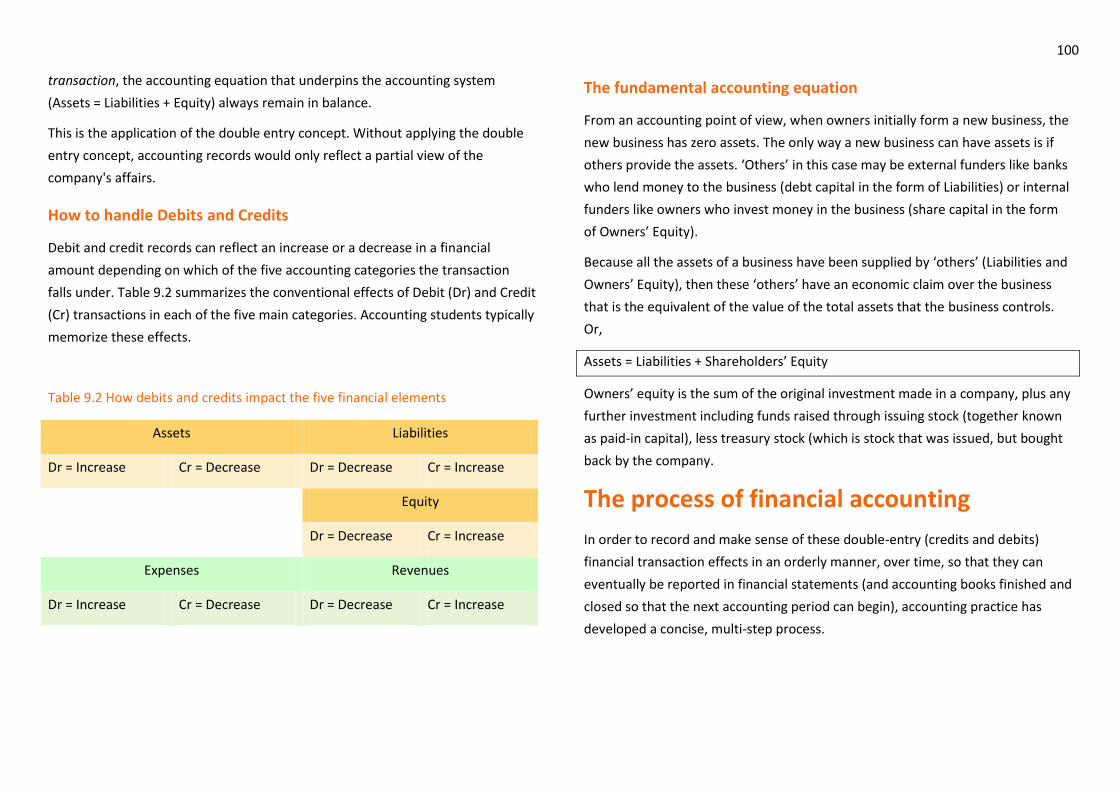

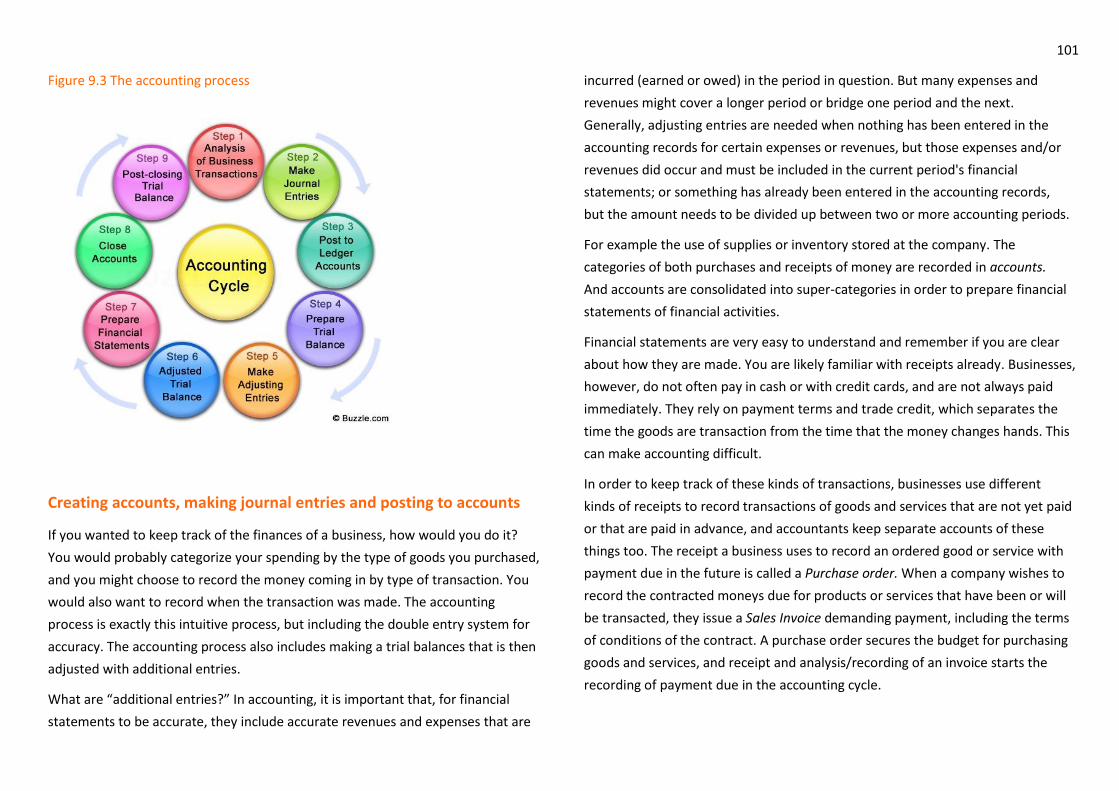

Embed Size (px)

Citation preview

Student name/ ID

Principles of Management

A case-led introduction to the environment,

functional areas and interactions involved

in everyday business.

Professor Karin McDonald

Office: Room L513

https://piazza.com/dongguk/spring2014/dba200107/home

BED01 Professor K.McDonald

Contents

BED01 Professor K.McDonald

Contents

Table of Contents

Introduction i

Unit 1: Business Basics I 1

Unit 2: Business Basics II 11

Unit 3: The Operations Department 23

Unit 4: The Marketing Department 35

Unit 5: Supply Chain and Channel Management, Category Management, etc. 46

Unit 6: Reaching Global Markets 56

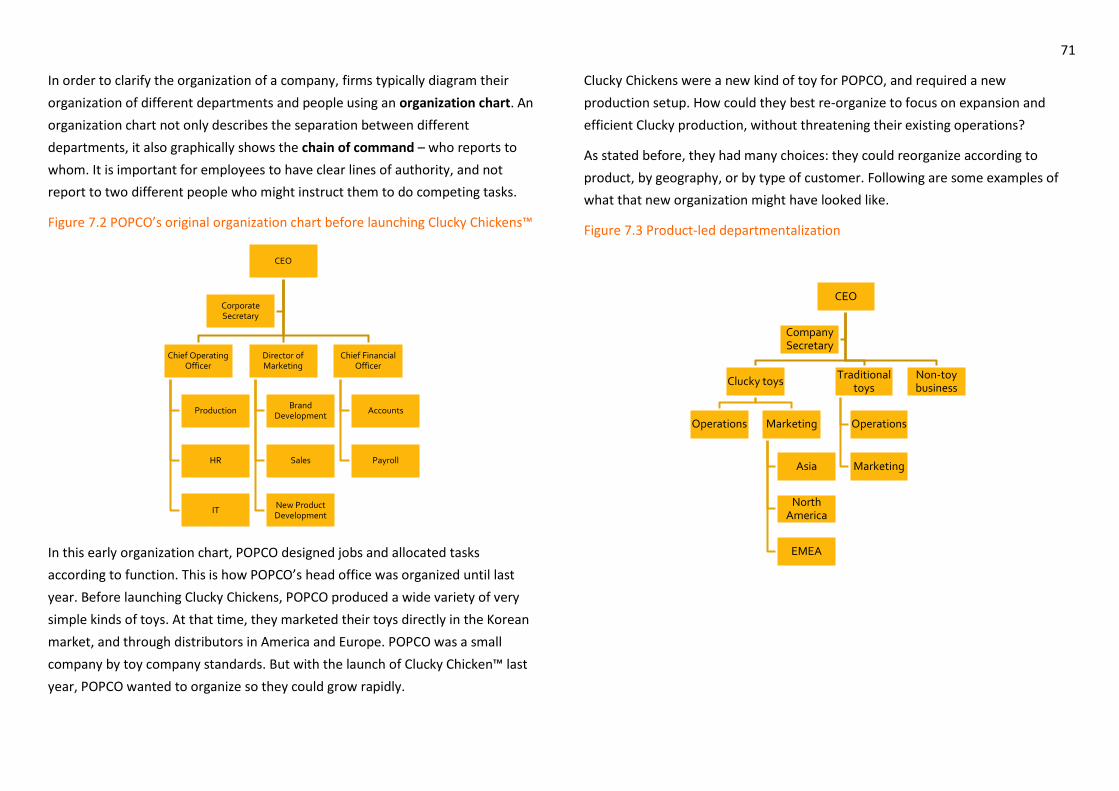

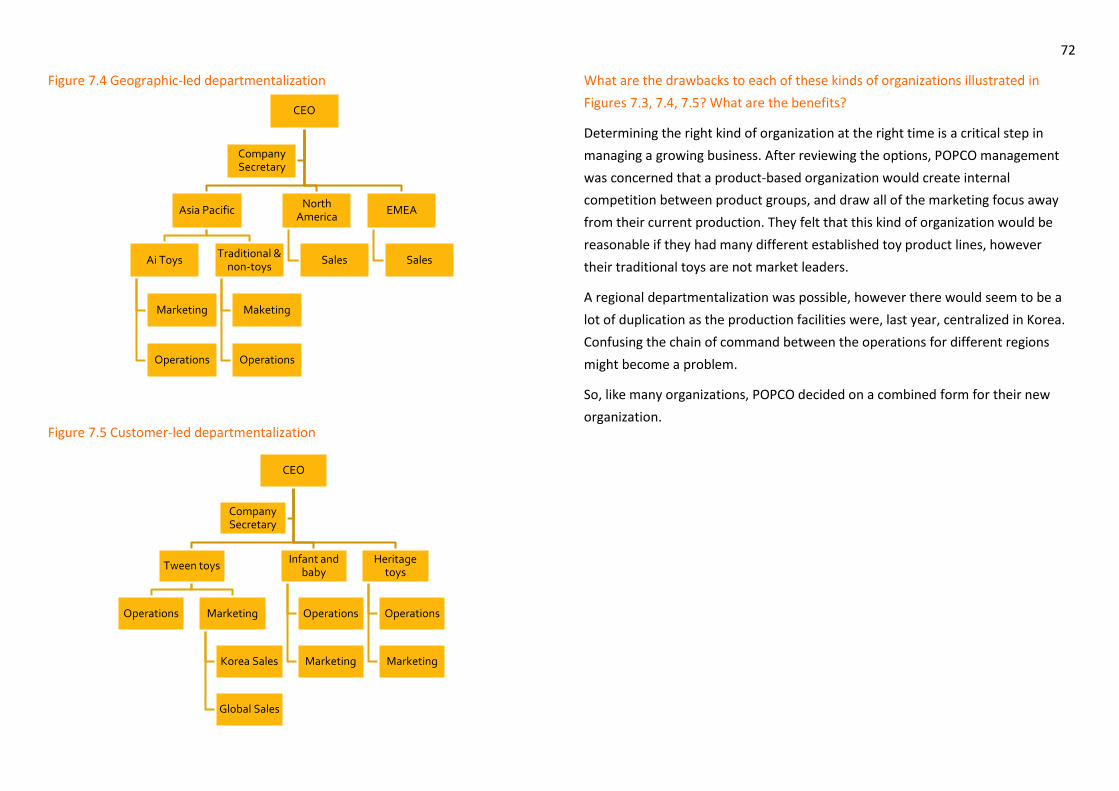

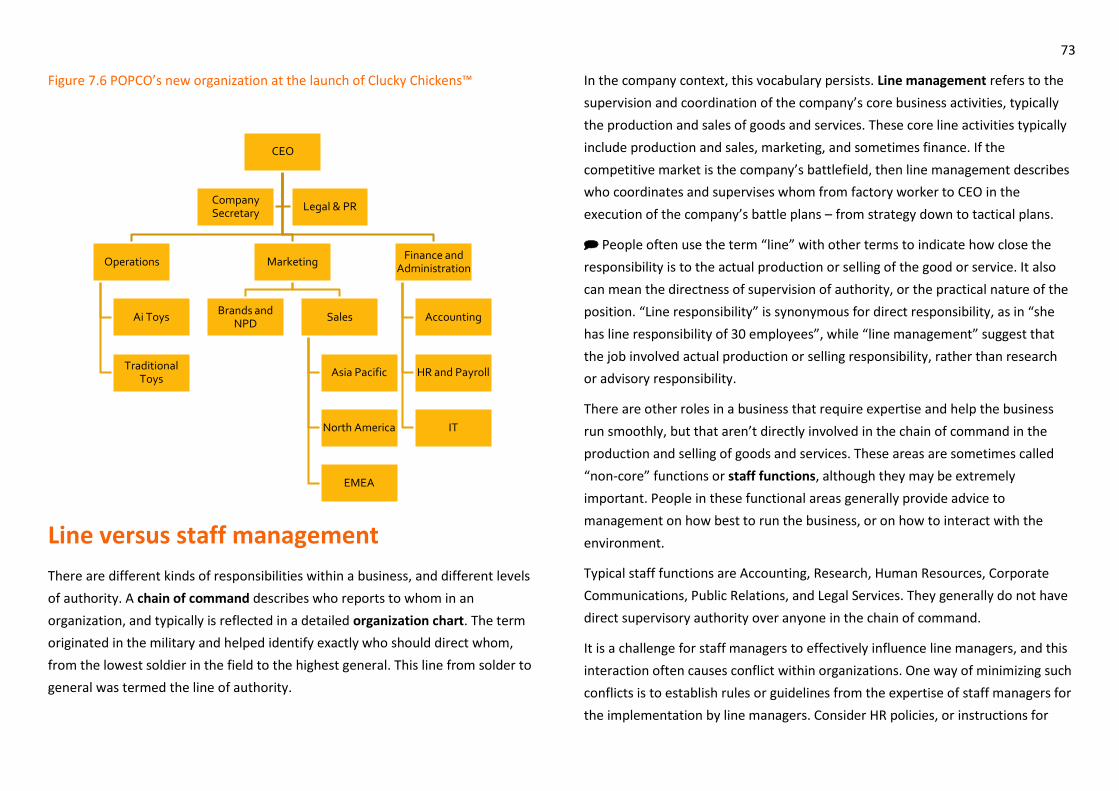

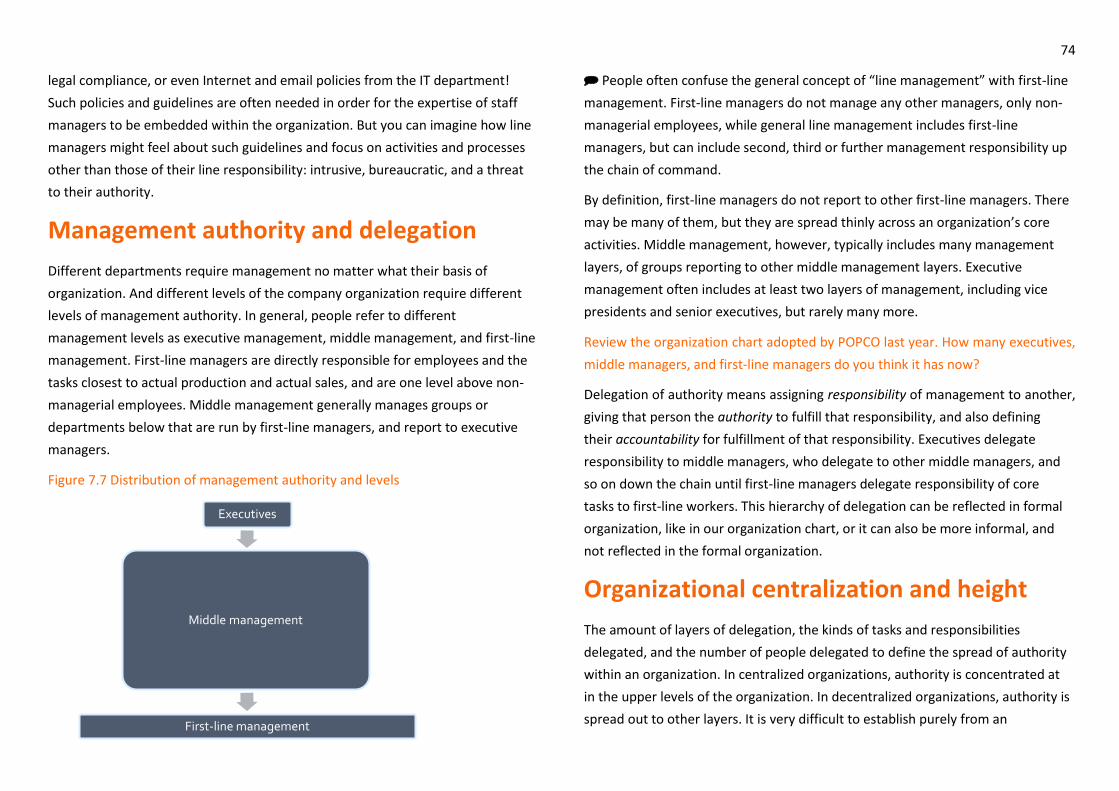

Unit 7: Corporate Organization and Planning 68

Unit 8: The Finance Department 80

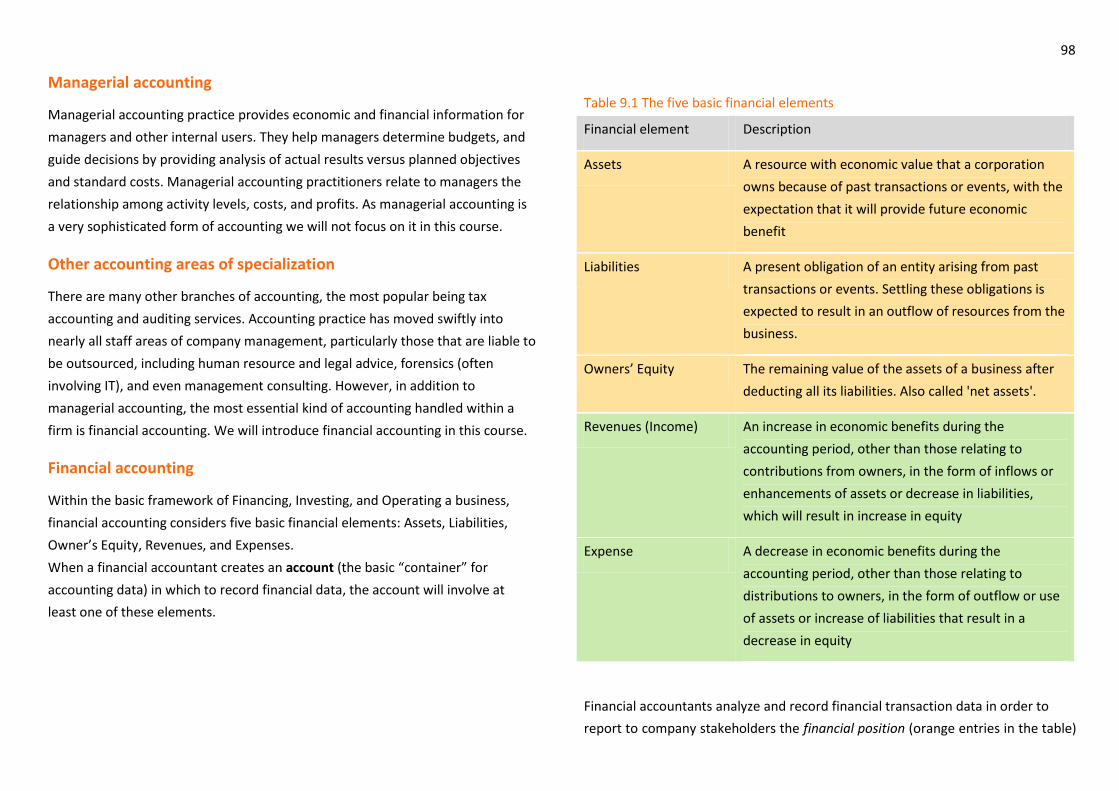

Unit 9: The Accounting Team and Financial Statements 94

Unit 10: The Human Resources Department 112

i

Introduction

Welcome to POPCO

For the purpose of this class, you should now consider yourself an intern at the

fictional manufacturing company, POPCO. POPCO is a Korean-based toy company

that started in the 1980s. They make a variety of toys and traditional Korean

games. Their main products are soft toys (in English language, “stuffed animals”).

They have recently launched a product called Clucky Chicken®. Clucky Chicken is

an “artificially intelligent” chicken soft toy. It relies on basic computer

programming via a computer chip inside the stuffed toy to interact with

consumers. POPCO launched the Clucky Chicken toy to compete with the wildly

successful Zhu Zhu Pets™ line of toy hamsters.

Class discussion and exercises will focus on POPCO to describe theories and

principles. Your job as an intern is to participate in helping the company make

good decisions, considering the new theories and principles you have learned.

Later, you will spend a week or two learning about the way each different area of

POPCO’s business works, including the types of jobs in each department, and

their responsibilities and activities. We will discuss in class how these jobs,

responsibilities and activities might be different in different kinds of companies.

POPCO®

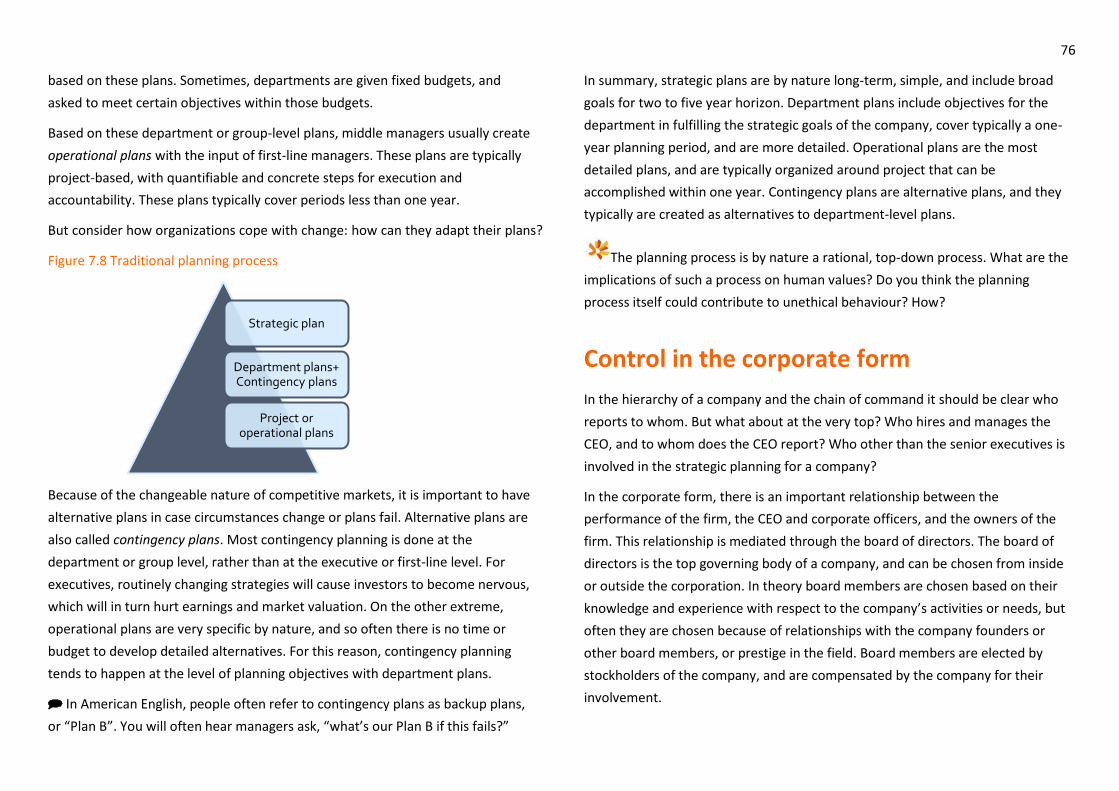

Worksheets

The purpose of worksheets is to help you check your understanding of the

concepts and skills in the reading, so that in class we can demonstrate and

practice applying that learning. Worksheet problems and questions are very

similar to those on the quizzes, although the quiz problems and questions are a

little bit harder.

Ethical questions

Included in this CP are questions that raise ethical issues. Ethics are a key

consideration of the global business environment and interactions within and

without a business. Ethics are more than just corporate social responsibility,

though. We will discuss ethical issues in business throughout the course as time

allows. Ethics-related questions are marked by a Dongguk lotus emblem:

Terminology

Like any field of study, business has its own jargon, and requires learning a lot of

vocabulary. To avoid confusion where the business meaning of a common English

term may be different from the definition you know, or where common usage of

a business term may lead to confusion, this CP includes common terminology

explanations marked with a speech bubble:

1

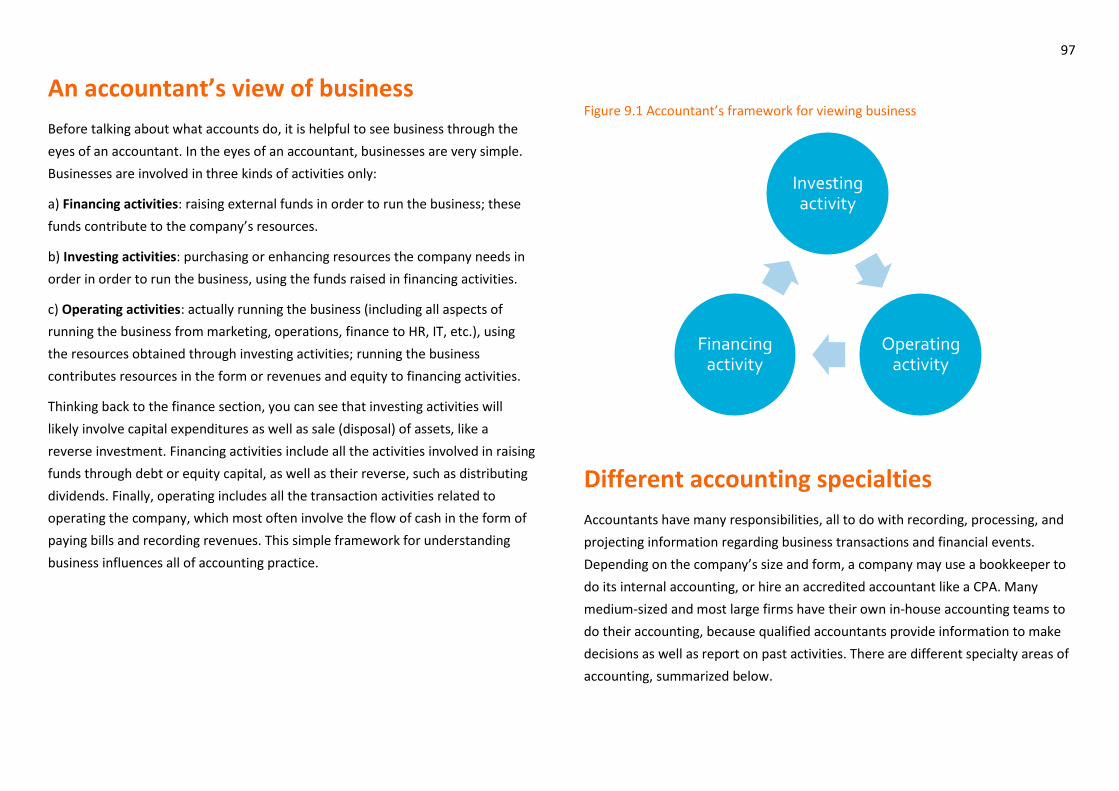

Unit 1

Business Basics I

Learning objectives of this unit

In this unit you will learn the following concepts:

What is the goal of a business? What are the resources it uses? (in class: resource diagram)

What is profit, and who receives it? (in class: profit calculation)

What is a competitive market, and how does supply and demand work? (in class: graphing supply and demand)

How do businesses interact with households and governments (in class: circular flow diagram)

with regards to resources?

What trends are common to competitive market economies? (in class: productivity calculation)

What are economies of scale, and how can a company get them? (in class: economies of scale diagram)

2

Unit 1 Vocabulary

Factors of production (생산요소): Things of economic value needed to produce

goods and services

제품이나 서비스의 생산에 필요한 자본이나 노동 등의 요소

Net Profit (순이익): The money a business earns when revenues are greater than

expenses

총 이익에서 원가를 차감한 뒤에 남는 이익

Revenues (수익): The money a business earns from activities like selling goods or

services

영업활동 과정에서 상품의 매출액과 서비스 제공을 통해 얻어지는

경제가치로서 자기자본을 증가시키는 이익

Expenses (비용): The economic costs that a business incurs through its

operations in order to earn revenues

기업이 수익을 창출하기 위해 운영을 통해 부과하는 경제적 대가(원가

Supply and demand (수요와 공급): Supply is how much quantity that sellers in

the market can offer of a specific good or service at each of various prices, and

demand is how much quantity of a good or service buyers are willing to buy at

each of various prices in that market.

수요: 경제재 또는 용역에 대한 인간의 욕망, 청구/ 공급: 어느 제조업자 또는

판매업자가 판매에 제공하는 경제재의 양, 소모품

Households (가구, 가족, 가정): The population of an economy that consumes

goods and services and also own and contribute other factors of production

가구는 개인으로 구성되며, 제품 및 서비스의 소비자일뿐만 아니라 생산 요소

일부의 소유자

Stockholder (주주): A person who owns stock in a corporation

주식회사의 주식을 한 주 이상 소유한 법적 소유자

Stakeholder (이해당사자): The different people who are affected by an

organization’s activities and decisions

기업의 활동이나 정책에 의해서 이익 또는 손실을 입게 되는 모든 사람들

Productivity (생산성): The amount of output produced by a given amount of

factors of production input; often measured in quantity per unit of time.

주어진 생산 요소를 투입하여 생산해낸 결과물의 양

Economies of Scale (규모의 경제): The cost advantage that arises with increased

output of a product. For many (but not all) firms the greater the quantity of a

good produced, the lower the per-unit fixed cost because these costs are shared

over a larger number of goods.

생산요소투입량의 증대에 따른 생산비 절약 또는 수익향상의 이익

Specialization (특화): A method of production where a business or area focuses

on the production of a limited scope of products or services in order to gain

greater degrees of productive efficiency.

최대한의 생산 효율을 얻기 위한 생산활동의 분업

Growth (Globalization) (성장 (세계화)): The tendency of investment funds and

businesses to move beyond domestic and national markets to other markets

around the globe, thereby increasing the interconnectedness of different markets.

다양한 시장이 상호 연결되어 투자 기금과 기업들이 세계의 다른 시장으로 움직이는

과정

3

What makes a “Business”

There are many ways to define business. One way is to combine the purpose of

business in a definition with the resources required by business activities, and the

goal of those activities. Below is a common definition of business.

Business is an organized effort to combine and manage resources in a

profitable way in order to produce products and services that satisfy the

needs of customers.

Purpose: The definition of the purpose of business has changed over the years

with changes in economic and business thought. However, most people today

define the purpose of business as satisfying the needs of customers by producing

and selling products (also called “goods”) and services.

Resources: No matter what type of country or political system you are working in,

business activity requires the organization and management of resources.

Generally, you can categorize resources as material, human, financial, or

information resources.

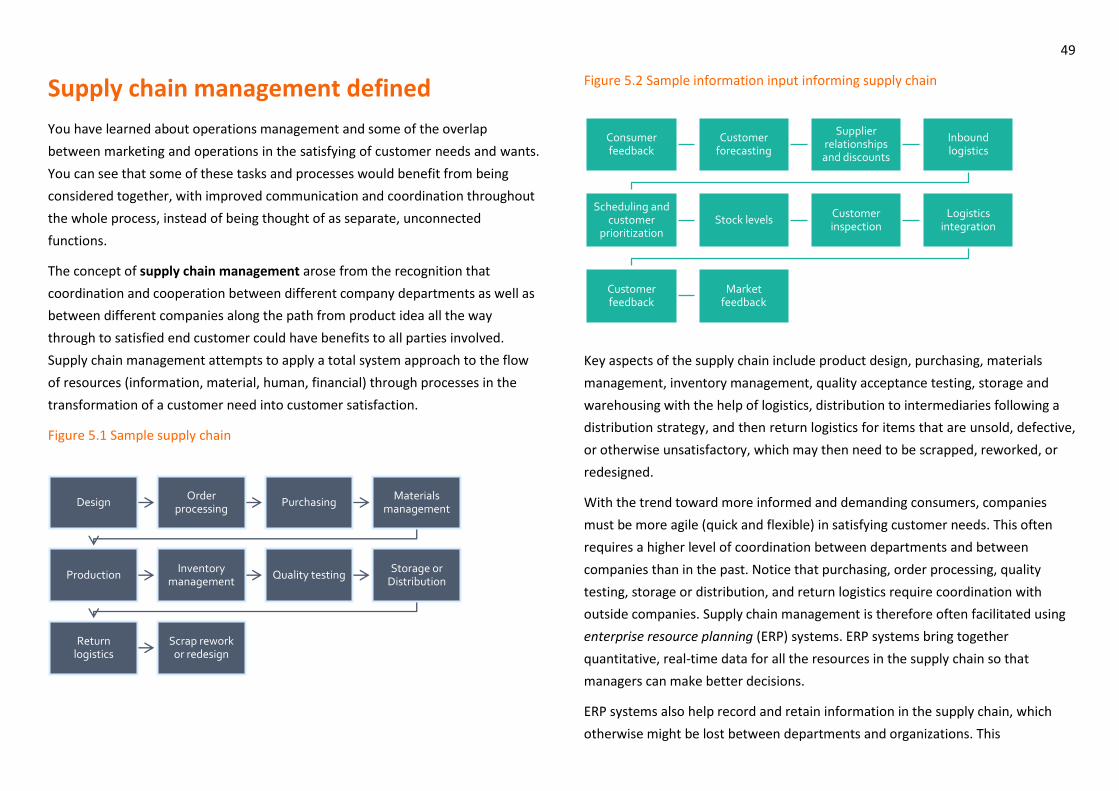

What are the specific resources a toy company requires to produce and sell toys?

In economics class, you probably learned to remember the categories of “land,

labor, and capital” resources, also called factors of production since they are

required to produce goods and services. Sometimes these are referred to as

factor inputs.

Historically, different theorists have emphasized different factors of production

when considering what makes a strong national economy. With increasing study

into the factors of production and political economy, academics today also

include the categories “knowledge / information” and “entrepreneurship” as

important factors of production.

More and more, technology is also an important factor of production. People still

measure the economic strength of a country according to the factors of

production it has and how the country’s political system manages those resources

to meet the needs of its own customers: society.

Goal: Most people consider that the goal of business is to make a profit. But

many businesses do not always make a profit every year. And some businesses

are started to make a profit for some owners this year, but do not have the

resources or management to be successful long-term, creating losses for often

different owners in future years.

The general term profit simply means that, in a given time period, a business’s

sales revenues are greater than its expenses. Sales revenues minus expenses

equals profit.

How would you calculate profit for your own activities?

People often use the general term “revenues” instead of sales revenues.

There are many words and phrases that mean the same as “profit”: earnings,

income, and “the bottom line” all mean profit (specifically net profit). But be

aware – the terms operating profit and gross profit represent different amounts.

We will learn more about these terms in the accounting unit.

Who gets the profit? Profit is often invested back into the business. It can also be

distributed to owners of the business. Most people think of business owners as

those who manage the business day-to-day. But this is not typically the case. Any

person or group that invests in a business is an owner of that business. Typically

they give money to the business in exchange for ownership, or perform some

other valuable service. For publicly traded companies, these people are referred

to as stockholders. Don’t confuse this term with the very similar term

stakeholders. A stakeholder is anyone who is affected by a business’s activities.

Who are all the stakeholders in Dongguk’s business?

4

Notice that the kinds of needs customers might have are very different, and

there is not a distinction between a “need” and a “want”, or between a true need

versus an impulse. Is the need to survive from starvation the same as the need to

have a fashionable handbag? In its definition and response to “needs”, business

treats both the same: an opportunity for activity and profit. Are there needs that

products, services and business activities do not satisfy well? Is profit the best

motive for all of society’s needs?

The simplest business interaction: a market

With the definition of what a business is, we can review how a business interacts

with the world outside. The typical way for this to happen is in a market. A market

is a medium that allows those that supply products and services (also called

“producers”) to find and transact with those who demand them (“buyers” or

“customers”). Supply and demand in a competitive market is the fundamental

theory of modern economics.

In economic terms, supply and demand refer to quantities: the supply of a

product or service is the quantity that suppliers are willing to sell at each of

various prices, and the demand is the quantity that buyers are willing to purchase

at each of various prices. If, however, economists talk about “demand” alone they

are referring to the relationship of price and quantity demanded, not just

quantity.

Why do we say “at various prices”? Because in the economics of supply and

demand we speculate on how much producers and buyers would transact at not

just one but at many prices. For producers, they would sell more at a higher price

if they could, and fewer at a lower price. But for buyers, the opposite would likely

be true: the lower the price, the more buyers there would be demanding the

product or service, and lesser and lesser demand as the price increased.

This assumes that producers and buyers make rational decisions in their selling

and buying activities, which many behavioral economists now recognize is not

strictly true. But in principle, there is a theoretical selling / buying price mismatch

between producers and sellers at most quantities – imagine people walking away

from making deals. In fact, in a general supply and demand market, there is only

one price/quantity point that truly satisfies both producer and buyer at the same

time – the equilibrium, or market price. And according to economists, the forces

of supply and demand in a simple free market will guide the price and quantity to

that market equilibrium.

Too much quantity of a good will drive down prices, and not enough supply of

what buyers want will drive up prices that buyers are willing to pay. Note that no

matter whether there is a shift in supply, demand, or both supply and demand,

the market will adjust to an equilibrium price.

As this is an introductory course, we will not cover topics related to micro or

macroeconomics in depth. If you want to pursue any of these topics further or in

theoretical depth, you can review macro and microeconomics.

What happens when a business has too much (a surplus) of products to sell?

What happens when there is not enough (a shortage) of a product to buy?

The forces of supply and demand are credited in classical economics with driving

the quantities sold and prices paid in markets. In truth, many forces can impact

the prices charged (and paid) in markets, especially in mixed market economies

like Korea’s. But for markets to work effectively, buyers and producers must have

some freedom in making choices regarding their business activities, and they

must be able to compete with other producers or other buyers to make those

transactions.

Some theorists believe that developed societies are now too dominated by

the concept of “the market.” Thinkers like Harvard’s Michael Sandel believe that

5

“markets” should be a tool of society for responding to specific needs or

problems. Not the purpose of societies. What do you think?

People often use the phrase “the market” to describe the stock market, rather

than product or factor markets. Stocks represent quantifiable ownership of

businesses. They can be bought and sold like other goods and services for publicly

traded companies.

Markets, buyers and sellers:

the Circular Flow

A simple way to understand the role of business around you is to look at the flow

of economic value that is transacted in markets to and from the main consumers

(buyers – “demand”) and producers (sellers – “suppliers”) of the factors of

production, products and services. Using very general terms, the primary

consumers and producers include businesses (also called “firms”), governments,

and households. People refer to these as the main sectors in an economy.

In a society who are the “buyers” and who are the “sellers”?

One way of categorizing markets is by what they sell and for what purpose:

factor or resource markets are primarily for the buying and selling of the factors

of production. This kind of market transacts the inputs for creating other products

and services. It’s not only for things like raw materials, though; it also includes

things like labor wages, the cost of finance, and other factors of production from

the previous section. Another kind of market is primarily for the buying and

selling of finished goods and services. These product markets deal in the outputs

of economic activity.

For example, individuals in a household provide their working time in exchange

for wages in a factor market. They then use their wages to buy finished goods and

services to satisfy their needs from product markets.

Students often overlook the role of government in economies. Governments are

often the biggest consumers in factors markets and in product markets, but they

also are producers in both markets as well.

Furthermore, remember that the flow of transactions and economic value is

ongoing and interdependent. In other words, one sector of the economy will

affect the other sectors if it experiences change. Besides competition for scarce

resources, the primary cause of change affecting the sectors of an economy and

the markets through which economic value flows is the business environment.

Governments are supposed to voice the needs of society as a whole. As a

“customer” of firms in product and factor markets, do governments do a good job

representing the needs of societies? Would individuals do better representing

their own interests directly?

Three trends of competitive markets

Three key trends of competitive market economies that shape business are

productivity, specialization, and growth (which these days means globalization).

Supply and demand market forces, the changing external environment (see next

unit), and the interdependence of the government-household-business flow

require that businesses constantly adapt. To adapt most effectively, businesses

follow one or more of these trends.

Productivity is simply the goal to be most efficient at producing and delivering

products and services. It is typically measured in the product or service output of

a business, workforce, or worker per unit of input (sometimes called factor

inputs), usually time. Businesses can increase efficiency by lowering costs of

resources (called factor inputs), or increasing the amount of output given the

same level of factor input.

6

There are many ways to increase productivity or the rate of output. For example,

you could improve the way tasks are completed, or automate tasks using

machinery. Rapid productivity increases can often lead to layoffs and increased

unemployment unless demand also increases at the same time.

Another key way to increase productivity is to reduce the cost of factor inputs.

Often businesses achieve input cost savings by negotiating with multiple suppliers

for the best value.

In terms of increasing productivity through reducing the cost of inputs, not all

input costs are the same. Some input costs rise and fall with the amount of goods

or services produced, while some costs are required no matter how much output

is produced. Costs that rise and fall with the level of output are variable costs

(they vary with production), and those that do not change no matter the level of

output are fixed costs. Note that these are general terms and not related to

accounting expense categories.

As a company produces and sells output (products and services) in the market,

the fixed costs are spread over the number of products or services sold: the more

output sold, the less the fixed cost represents as a percentage of the total unit

cost of each product or service. In other words, the more a company sells, the

more profit they can make per unit of output sold. This is referred to as

economies of scale (economies refers to cost savings, and scale refers to the large

amount of output), and is one main contributing factor towards the drive towards

productivity and growth in competitive markets.

http://www.investopedia.com/video/play/what-is-economies-of-scale/

Note that at a certain point, theoretically companies also experience

diseconomies of scale, in other words when producing additional units actually

increases the cost per unit of production.

Specialization is the trend towards producing a limited scope of products or

services to achieve greater production efficiency. Specialization can refer to labor

specialization of a job or task, or of a company’s output, or a nation’s output. The

drive to specialize is a result of comparative advantage, where the opportunity

cost for one group to produce one item is lower than to produce another item,

when compared to the opportunity costs of another producer. By each group

specializing, the whole system is more productive.

Companies that specialize increase their knowledge and experience, which

increases their productivity and negotiating power. However, companies that

specialize without continuing to look at the business environment and

competitive forces can quickly become insular (inward-looking) and

uncompetitive. Larger companies may combine many different specializations

under one corporation or group of companies (called a conglomerate) so that

they can earn profits from one business area while another business area is

adapting and may be less profitable or competitive. Conglomerates can use many

different resources from all of their companies to balance their resources.

Growth is the result of the trend toward productivity (including economies of

scale) and specialization (including the trend towards creating large

conglomerates). Growth enhances a company’s ability to gain economies of scale,

increases their negotiating power, and gives the corporation or conglomerate

more ways to balance revenues and losses across companies and business areas

among other advantages.

These days, with improved communications and logistical infrastructure for things

like shipping and cargo, growth usually means globalization. Globalization simply

refers to a business operating in global resource and/or factor markets.

Theoretically, a company that can operate globally is likely to be much more

competitive than a company that is limited to local resources and markets. Small

and medium sized companies must find ways to specialize to meet local demands,

or find assistance in reaching global factor and product markets.

7

What are the negative aspects of globalization in your mind? Is it possible for

a company to not globalize and remain competitive? How?

Summary: Business Basics I

In this unit you have learned about:

The goal of business and the resources it uses

The definition of profit, stakeholder, and stockholder

The equilibrium price nature of competitive markets

The interdependent flow of value in society between businesses,

governments, and households

The market economy trend towards productivity, specialization, and

growth

If you are unfamiliar with microeconomics (including the basics of supply,

demand, market equilibrium, comparative advantage, specialization, etc.), I

strongly encourage you to view the videos at the link below (Korean

subtitled!)

https://www.khanacademy.org/economics-finance-domain/microeconomics

8

blank page for your notes

9

Worksheet 1 (front)

Matching: Match the POPCO resource with the resource category that applies.

You can choose more than one kind of categorization.

a) Land b) Labor c) Capital d) Knowledge/Information e) Entrepreneurship

f) Information g) Material h) Financial i) Human

1)___ Fuzzy yellow material to make Clucky Chickens®

2)___ The minimum wage in Korea

3)___ Market price survey of artificially intelligent toys for next Christmas

4)___ Interest rates

5)___ The availability of factory real estate plots in Korea

6)___ Our factory buildings

7)___ Initiative by our marketing team to crowdsource toy ideas

True or False

8)___ Profit is the same as Gross Profit

9)___ Sales revenues minus the bottom line equals earnings

Fill in the blank

10) Another name for an owner of a publicly traded business (ownership through

investment or providing another valuable service) is a ___________________.

Circle the best answer

11) If the quantity supplied of toys stays the same and the quantity demanded

increases, prices will go: up / down

12) If the quantity demanded for board games decreases the equilibrium price will

eventually go: up / down

13) Name one reason why toy demand quantity might go down:

______________________

Multiple choice. Circle the one best answer

14) Productivity is generally measured as:

(a) output / input

(b) hours per product

(c) costs / revenues

(d) cost / worker

15) Economies of scale are achieved by:

(a) Reducing the per unit productivity

(b) Reducing the variable costs to produce each product

(c) Spreading the fixed costs of production over many units

(d) Spreading the variable costs of production over many units

True or False

16) ____Specialization benefits larger companies because more specialized areas

make them more profitable.

17) ____One way a medium size company like POPCO can compete against giant

globalized toy conglomerates is to specialize in high quality stuffed animals or

get support to sell overseas from the Korean government.

18) On the next page, map all of the stakeholders in POPCO’s business you can think

of, and the resources we transact with them (buy and sell). Assume we sell our

toys in the EU, North America, and Korea, and that our main factory is in Korea.

10

Worksheet 1 (back)

Map all of the stakeholders you can think of for the POPCO business. Do we

transact (buy or sell) with all our stakeholders? _______ (yes or no)

Note the resources we transact with stakeholders we do buy and sell with.

11

Unit 2

Business Basics II

Learning objectives of this unit

In this unit you will learn the following concepts:

What are the environmental forces that affect business? (in class: forces discussion)

What is Gross Domestic Product (GDP)? (in class: example using flow image and formula)

What is the business cycle, and what happens during different phases? (in class: GDP x time graph, body analogy)

How do governments and financial institutions respond to change? (in class: fiscal and monetary policy problem)

What is the social responsibility of business in a competitive global market? (in class: review of flow model versus time, GDP & standard of living, goals)

12

Unit 2 Vocabulary

GDP(국내총생산): The monetary value of all the finished goods and services produced within a country's borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments, and exports, less imports that occur within a defined territory.

한나라의 국경 안에서 일정한 기간(보통 1 년)에 걸쳐 생산한 재화와 용역의

부가가치 또는 가계,대중 소비, 정부 경비, 투자와 수입비용을 뺀 수출 등을

화페단위로 합산한 것을 말한다.

The Business Cycle (경기변동): The recurring and fluctuating levels of economic activity that an economy experiences over a long period of time. The five stages of the business cycle are growth (expansion), peak, recession (contraction), trough and recovery.

경제 활동의 반복적인 변화. 확장, 절정, 침체, 골, 그리고 회복으로 구분되어 있다

(Price) Inflation (인플레이션): The rate at which the general level of prices for goods and services is rising, and, subsequently, purchasing power is falling.

화폐가치가 하락하여 물가가 전반적, 지속적으로 상승하는 경제현상

http://www.investopedia.com/video/play/what-is-inflation/

Deflation (디플레이션): A general decline in prices, often caused by a reduction in the supply of money or credit. Deflation can be caused also by a decrease in government, personal or investment spending.

경기가 하강하면서 물가도 하락하는 경제현상. 정부,개인 또는 투자 소비에 의해

유발되어 진다

Monetary Policy (화폐 정책): The actions of a central bank, currency board or other regulatory committee that determine the size and rate of growth of the money supply, which in turn affects interest rates. Monetary policy is maintained through actions such as manipulating the interest rate, buying or selling government securities, or changing the amount of money banks need to keep in the vault (bank reserves or deposit ratios).

중앙은행이 이자율에 영향을 끼치는 통화 공급량의 크기와 성장률을 결정하는 정책.

이자율 증가 또는 은행 지급 준비금을 통하여 유지된다

Fiscal Policy (재정 정책): Government spending policies that influence tax rates, interest rates and government spending, in an effort to control the economy.

경제를 조정하기 위해 세율, 이자율과 정부 지출에 영향을 미치는 정책

Standard of living (생활수준): The level of wealth, comfort, material goods and necessities available to a certain socioeconomic class in a certain geographic area,

often measured in GDP per capita 사람들이 자신이 보유한 돈을 가지고 살 수

있는 제품과 서비스의 양

Quality of life (삶의 질): In addition to material well-being it includes such intangible things as the quality of the environment, national security, personal safety, and political and economic freedoms

물질적인 요소 뿐만 아니라 무형적인 환경, 국가적 안보, 개인의 안전 그리고

정치, 경제의 자유의 행복수준

Social responsibility (사회적 책임): The recognition that business activities have an impact on society and the consideration of that impact in business decision making

기업의 활동이 사회에 영향을 끼친다는 사실을 인지하고 이를 의사 결정에

반영

13

The business environment: force for change

The business environment – the external forces affecting business markets,

activities and performance – is a multi-layered, always changing setting in which

business must adapt in order to compete. Particularly in a global business

environment, environmental forces may change significantly and often. These

forces greatly affect the markets and circular flow of value in economies.

Types of environmental forces affecting business include: demographic trends like

birthrates and living locations; social customs and cultural norms; laws and

regulations; global economic conditions like financial conditions and currency

rates; security and law enforcement conditions; the political situation;

technological innovations and availability; ecological environmental conditions;

public opinion; and ethical considerations.

You will often be asked to analyze “environmental trends” or “the environmental

forces” affecting a business, because they can so quickly and significantly affect

the markets and activities of business. This is often referred to as PEST analysis,

an acronym for Political, Economic, Social, and Technological forces. There are

several environmental forces beyond those four. Some people remember them

with STEEPLE – including “Ethical”, “Legal” and “Ecological” forces.

What are some specific environmental forces that affect POPCO as a toy business?

People often use the phrase “the environment” to describe the external

context of the activities they are talking about, rather than the more common

meaning about the ecological context. In our class, when we discuss “the

environment” we will usually be talking about the external context in which

business operates, unless mentioned otherwise.

GDP

When looking at a circular flow of value for, say, a country, how do you measure

that value in economic terms? Economists and business people use the term

Gross Domestic Product, or GDP, to measure that value. GDP measures the total

market value of all finished goods and services produced within a country’s

borders in a given period of time, usually a year. GDP places a value on a

country’s economic output and is often compared historically to previous years’,

a base year, and to other countries’ GDPs.

Notice that the market value is the tradable value, rather than the cost of goods.

And these are finished goods – because the value of intermediate goods is

captured in the value of the finished good within one country’s borders. Also

notice that it is produced within one country – not managed by one country. The

production is accounted for in the location where it is produced, not where it is

owned or managed.

GDP tends to increase gradually over time due to increases in productivity.

Increases in productivity are typically due to technology innovations, to discovery

or increase in the value of held resources, or because of new processes.

The business cycle

The interdependence of different sectors (the circular flow) of the economy,

coupled with the anticipation of supply and demand by looking at the past, tend

to create repeating cycles of expansion and contraction in economic activity. This

is the business cycle. The business cycle can be pictured as the fluctuations in

GDP over time.

The business cycle reflects periods of economic growth and contraction in

business production, wages, incomes and employment, spending, borrowing and

investment. While governments, businesses and households would all prefer

14

stable prices, growth, and full employment, the business cycle adapts according

to market forces. Yet, “market forces” really refer to supply and demand, and

those are greatly affected by people’s emotional attitudes about what has

happened in the past, and what they expect to happen in the future.

What part of the business cycle is Korea in now?

Typically, investors, governments, businesses and consumers will react and adapt

in reaction to what has recently just happened in anticipation of the direction of

change of the business cycle, and so often act with too much optimism or

pessimism.

Price inflation

One of the biggest triggers to affect households, businesses, and governments in

their every day economic decision-making is the price of things. The general

increase in prices over time is called price inflation. Inflation measures the rate at

which the general level of prices for goods and services is rising, and,

subsequently, purchasing power is falling. So as prices go up, the money you have

today is worth less tomorrow. Often you see inflation at the peak of business

cycle growth.

When you see headlines that talk about inflation, they are usually talking

about price inflation.

In general, prices will rise steadily and slowly over time. Economists disagree

about the causes of this, but generally agree that in the long run price inflation is

related to monetary inflation, or the increase in the money supply in the

economy. (In the short run, it could be due to a sudden loss of supply of a key

good like oil, because of more overall demand in the economy as it grows and the

three sectors spend more, or because the vicious cycle of workers trying to keep

their wages above price levels, which in turn leads to an increase in goods prices.)

Inflation is measured by the Consumer Price Index (CPI), which measures the

relative increase in cost of an averaged “basket of finished goods” over time.

There is a related Producer Price Index (PPI), which measures the same but for

factor inputs.

What goods have you noticed that have increased in price in your lifetime?

Deflation is a general decline in prices, often caused by a reduction in the supply

of money or credit. Deflation can be caused also by a decrease in government,

personal or investment spending. The opposite of inflation, deflation leads to

increased unemployment since there is a lower level of demand in the economy,

which can lead to a downward spiral and economic depression.

Countries will try and control excess inflation and deflation through monetary and

fiscal policy.

Controlling the economy: monetary policy

Governments and financial institutions respond to cyclical economic changes

through two different kinds of policies: monetary policy and fiscal policy. While

economists and politicians may debate how much of a role governments should

play in responding to markets and the business cycle, most agree that

government should play some role in preventing extremes of the business cycle.

Monetary policy is the policy of controlling the money supply in an economy. This

affects interest rates, and eventually, demand. Monetary policy is not set by the

representative government, but by central banks and their boards. Some central

banks are controlled fully by their respective governments, some are partially

controlled by the government and partially by private interests, usually the

boards of other banks. People set and administer monetary policy, not markets.

The stated purpose of most central banks is to stabilize prices (control inflation)

and in some cases, target full employment. Central banks control the money

15

supply by using three tools: 1) controlling the money supply and interest rates by

buying or selling government securities (typically short-term treasury securities

like treasury bills and bonds) from its member banks through open market

operations; 2) controlling banking risk and the impact of open market operations

on the money supply by setting the amount of money a bank must keep in

reserve and not lend, called the reserve requirement; and 3) controlling money

demand by manipulating the interest banks for banks that must borrow from the

bank of last resort, the central bank (called the discount rate);

“Open market operations” (and how it effects interest rates) is the most popular

tool employed by central banks. For example, when the central bank wants to

stimulate an economy, it will typically buy short term government securities from

the market via its member banks, and pay for these by adding a credit to the

seller’s bank account for the amount purchased. This deposit goes towards that

bank’s reserves. The bank has to keep a certain percentage of these new funds in

reserve, but can lend the excess money to another bank in the overnight lending

market between banks. In the example above, the bank has a credit to its

reserves, which means it can lend more money. The money banks can lend to

each other overnight is called the federal funds market in the US.

Why would banks want to lend money to each other overnight? It has to do with

the reserve requirement. Banks’ reserves of money – the money the bank must

keep and not lend, called the reserve requirement – is kept at their local central

bank office or in cash in the member bank’s vault. The bank must keep in reserve

a certain percentage in order to pay for its daily operations. For the bank, it

means it cannot easily make a profit on this “reserved” money because it cannot

be lent. Reserve requirements must be met by the close of the day.

But banks do lend more to their customers than their reserves allow them to in

order to make more profit. To do this without breaking the law and risking

penalties, the bank will borrow funds from another bank overnight to meet the

reserve requirement (or lend to another bank that is not meeting its reserve

requirement – which also gives them a profit). The funds they borrow or lend

each night are called Fed funds in the US, and the interest rate charged on these

funds between banks overnight is called the Fed funds rate in the US (in Korea,

previously the overnight call rate and now the base rate).

The central bank targets a specific lending rate or funds rate they feel is right for

the economy, and then uses open market operations to affect this rate. The rate

itself “floats.” How does the increase or decrease in banks’ funds using open

market operations affect the funds lending rate? Think of it in terms of supply and

demand. The price of the money available to borrow from other banks is the

interest rate. Banks can earn money on money they lend, so there is stable

demand. With increased supply in money available to lend, the price (interest

rate on the fed funds) goes down. When this rate falls (or rises), the price of other

kinds of borrowing and lending changes too, causing interest rates on things like

credit cards, business loans, and mortgages to also fall (or rise).

People often use the general term “interest rates” when talking about

monetary policy, when actually they mean the central bank’s overnight lending

rate, which in the US is called the Federal Reserve rate. Yet the Federal Reserve

rate, which is only available to the largest and most creditworthy lending

institutions like large banks, is used to lend to other banks over night to keep

their balances and reserves square. This interest rate is not available to

households or other businesses. The interest rate that banks charge their most

creditworthy customers, usually large corporations, is the prime interest rate, or

prime rate. The prime rate is set according to the federal funds rate. Retail banks

base the interest rates they charge to small businesses and individuals for

personal loans and mortgages on the prime rate. In this way, the Federal Reserve

rate as set by a central bank has a domino effect on lending and the money

supply in an economy.

The central bank can also change the reserve requirement. If the percentage of

deposits banks are required to keep in reserve, as set by the central bank,

16

increase or decrease, you can see how this would affect the money available to

borrow and lend in the economy as every deposit can be then used to lend which

can then be used to lend, which can then be used to lend, etc. (minus the reserve

requirement). This is known as the multiplier effect. The money multiplier of

deposits to reserves is simply the amount of total deposits divided by the reserve

requirement percentage. So if banks have a reserve requirement of 20% and total

deposits are $100, then the actual money that could be circulating in this tiny

economy is $500.

Finally, central banks may use the discount rate to control the money supply.

Occasionally, banks may exceed their reserve requirements, but find that no

other banks will lend to them overnight. In this case the banks must turn to the

central bank itself to lend them money. The rate the central bank charges to

banks for such lending is called the discount rate. The discount rate is higher than

the funds rate charged between banks, making the central bank the bank of last

resort for borrowing.

Typically, central banks effectively decrease the money supply by effectively

raising interest rates via selling government securities like Treasury bonds or

through repo agreements (securities with an agreement to repurchase). This will

filter through the economy as an increase in the interest rate for lending. Raising

interest rates discourages borrowers and lenders, and selling government bonds

removes money from circulation (puts the bond in circulation, and takes the

money out).

In situations where inflation is low but economic activity is slow and growth is flat,

central banks may increase the money supply in order to stimulate demand. They

do this via the opposite path of the above, by buying government bonds or other

low risk securities from banks or dealers. This has the effect of lowering short-

term interest rates, which in turn acts as a signal to businesses and institutions to

consider borrowing and investing.

http://education-portal.com/academy/topic/central-bank-and-the-money-

supply.html

But what about if the interest rate is already near zero? In that case the central

bank may instead buy particular kinds of securities that may not be as low risk, or

target specific assets and parts of the economy where credit isn’t flowing

smoothly. This does not directly affect the funds rate charged between banks.

This puts more money into circulation with banks, encouraging them to lend. It

raises the risk of inflation, however, as more money is directed into the economy

with the same short-term demand for goods. And banks may choose to keep the

new money in reserve rather than lend it. This overall strategy is called

Quantitative easing. Quantitative easing is a controversial strategy for many

economists and investors.

https://www.khanacademy.org/economics-finance-domain/core-finance/money-

and-banking/federal-reserve/v/

Fiscal policy is where the government uses its power as both producer and buyer

in factor, product and service markets to impact economic outcomes. Fiscal policy

is also known as “tax and spend” policy: the government redistributes income it

collects in taxes by buying products and services, paying wages, and selling or

leasing resources. In this way the government influences supply and demand in

markets. Politicians disagree on whether increasing taxes and then increasing

government spending in the economy, or reducing taxes and hoping for firms and

households to spend that available income in the economy is better at

stimulating economic activity.

Fiscal policy is typically set through the representative body of government with

the approval of the central government authority. Governments can also raise

money to spend by selling debt in the form of Treasury bills and bonds (borrowing

from investors) when tax revenues are not sufficient or there is a budget deficit.

What are the current monetary and fiscal policies of Korea? Of other countries?

17

What is the goal of an economy?

Most governments and their central banks want their economies to grow and be

healthy. They want their societies to improve, and do their best using fiscal and

monetary policies to make that happen. Common measurements that allow

governments to assess the health and improvement experienced by their citizens

are socio economic indices.

Indices is the plural of index.

Socioeconomic indices are by nature subjective in design, and do not generally

reflect cultural values. Two commonly cited socioeconomic indices are standard

of living and quality of life.

Standard of living is a measure of the level of wealth, comfort, material goods

and necessities available to a certain socioeconomic class in a certain geographic

area. It emphasizes the material choices available for consumption, and people’s

economic ability to consume. Some simply calculate the GDP per capita (per

person) for standard of living. But in reality, it includes variables such as: average

incomes, employment availability, poverty rates, quality and affordability of

housing, life expectancy, literacy rates, cost of goods and services, affordability

and access to healthcare, availability of infrastructure like energy and

transportation, etc. Standard of living measures are typically easy to quantify. By

participating in trade and economic activity, the standard of living within an

economy typically improves.

Quality of life measures aspects of society such as: quality of the environment,

freedom from corruption, sense of security, religious and political freedom, equal

protection under the law, equal pay for equal work, freedom from torture,

freedom of movement, right to be treated equally without discrimination, right to

privacy and freedom of expression, right to leisure, right to education, etc.

Quality of life is less easy to quantify, and very difficult to compare between

cultures with different norms of social behavior and different kinds of

expectations.

The question of social responsibility

One of the purposes of government is to ensure the health of the society it

governs. And households have a responsibility as citizens to uphold society by

abiding by laws and respecting the rights and freedoms of other citizenry. So

what is the responsibility of business to society?

There are two general views on what the social responsibility of business is. On

one side, there is a purely economic view of business’s social responsibility:

business exists to make profit, and by making economic profit, paying taxes, and

participating in markets, business contributes wages and income to those in a

market economy, which in turn contributes to the standard of living of those who

participate in that economy. In this view, the social responsibility of business is to

do what it does best – earn profit – and to not intervene in other, non-profitable

ways in society. Every social issue is a business opportunity waiting for someone

to combine the factors of production effectively and make a profit from that

social demand. Paying taxes and returning profit to stockholders is the primary

job of business.

There are merits to this view, particularly in a global context. It is difficult to argue

that market economies have not increased the standard of living of those in

developing economies, for instance. Despite the seeming unfairness in the

difference between incomes and standards experienced by those in developed

and developing nations, participation in a global marketplace provides more

opportunities for people to raise their standard of living.

However, standard of living measures traditionally do not include measures of

sustainability, nor do they measure the more subjective quality of life variables

that many feel are essential to a healthy life. Sustainability is an extremely

18

important measure, because market economies in any context encourage

consumption, and some factor resources – like natural resources, for instance,

are finite (limited).

Those who hold an economic view of business’s social responsibility claim that

entrepreneurship and technology will step in to fix social problems due to

unsustainable practices as soon as it is profitable to do so. They do not feel that

businesses should operate in a socially responsible manner until it makes business

sense to do so.

The socio-economic view is different. In this view, businesses are actually a

contributing member of society and should thus work for the long-term benefit of

society, not just for their own profit. Businesses have a responsibility not just to

stockholders, but to all stakeholders because business benefits directly from

social and government contributions such as infrastructure, political freedoms,

security, an educated and healthy workforce, and other social conditions that

they do not necessarily directly pay for.

The socio-economic view also sees sustainability as a necessary objective of all

sectors of the economy to avoid tipping-point scenarios, where the social

problems created by economies are too big for even technology to fix. Those who

hold the socio-economic view point out issues that business and economic

markets have failed to address effectively with a profit motive, like global

warming, poverty, income disparity, under education, and lack of affordable

healthcare. They view these issues as significant barriers to society’s well being.

They claim that only businesses working together with government, targeting

sustainability and social well being, will have the resources needed to solve some

of these grave problems.

Business ethics

Many people believe that ethical problems in business arise from individuals

breaking the law. This is only one standard of ethical behavior – there are several

more. But many ethical challenges in business arise with the tension between the

needs and stockholders versus the needs of business stakeholders. A business

decision that clearly benefits stockholders may harm stakeholders, and the

opposite in many cases may be true.

Risk management is the business practice of weighing the possibility of bad

outcomes against the potential benefits. Often the possibility of bad outcomes is

at the expense of stakeholders, while the beneficiaries of potential benefits are

typically stockholders.

Unfortunately comparison of possible outcomes depends very much on your

point of view, and whether you prioritize stockholders or stakeholders. This leads

to ethical dilemmas for the people actually making the risk assessments: do they

act for the company, or as a stakeholder in society? One person’s acceptable risk

is far beyond what another person might consider acceptable. Because

businesses have low incentive to account for risks as viewed by all stakeholders,

they do not often prioritize or even consider non-owner stakeholder concerns in

their risk calculations, despite the slogans or vision statements in the company

annual report.

For this reason, society demands and governments often implement regulation of

industries. The purpose of regulation is not to harm business, but to ensure that

businesses and industries meet the needs of stakeholders and not just

stockholders.

In many cases, industries will regulate themselves. While some view this as

positive social responsibility, others believe that businesses pursue self-regulation

in order to avoid more strict regulatory standards. Those from the economic view

19

of social responsibility (and free-market supporters) claim that regulation is not

necessary because buyers and producers will make their demands known through

their actions as consumers and purchasing agents. However, this point of view

over estimates the power and motives of uninformed, misinformed, and

independent agents in markets.

What ethical issues exist in the toy industry, where the profit motive of

stockholders might compete with the interests of stakeholders? What regulations

are in place to manage these issues?

Summary: Business Basics II

In this unit you have learned about:

The environmental forces that affect business

GDP and the business cycle

Monetary and fiscal policy

Considerations about social responsibility and business ethics

If you are unfamiliar with microeconomics (including the basics of supply,

demand, market equilibrium, comparative advantage, specialization, etc.), I

strongly encourage you to view the videos at the link below (Korean

subtitled!)

https://www.khanacademy.org/economics-finance-

domain/macroeconomics/gdp-topic/circular-econ-gdp-tutorial/v/parsing-gross-

domestic-product

https://www.khanacademy.org/economics-finance-

domain/macroeconomics/aggregate-supply-demand-topic/monetary-fiscal-

policy/v/monetary-and-fiscal-policy

20

21

Worksheet 2 (front)

Fill in the blank.

1) The global financial crisis of 2009 was a/an __________ environmental force

that affected most global corporations.

2) Relaxing import regulations on toys imported into the EU is a/an

___________ environmental force that may affect POPCO’s overseas sales.

Select the one best answer.

3) One possible cause of high inflation is:

a. High unemployment

b. Low investment

c. Too easy credit

d. Low GDP

Identify the following as related to fiscal or monetary policy.

4) _____President’s budget proposal

5) _____Central bank’s open market operations

6) _____Tax increase

7) _____Government subsidies

8) _____Quantitative easing

9) ____Interest rates

Circle the correct answer about monetary and fiscal policy.

10) If a central bank uses open market operations to sell treasury bills or bonds, it

is trying to stimulate / slow down an economy.

11) If a central bank lowers the reserve requirement for banks, it is attempting to

stimulate / slow down an economy.

12) The primary way a government raises money is through taxes / lending

money.

True or False.

13) _____The socio-economic view of social responsibility believes that

businesses should prioritize the needs of all stockholders in their operations.

14) _____The economic view of social responsibility believes that technology plus

entrepreneurship will eventually solve all the issues and needs of society, and

so sustainability should only be pursued if it’s profitable.

15) _____The interest rate banks can charge each other overnight for meeting

their reserve requirements is called the prime rate.

16) _____The interest rate the central bank charges to banks that it lends to is

called the Fed Funds Rate in the US.

17) _____The reason a bank will borrow from another bank overnight is so they

can lend that money to their customers the next day.

Headline explanation.

18) On the following page, explain in your own words what is meant in the

following business headline. Explain why it is happening, and what the terms

mean. Is this monetary or fiscal policy? Where is the money for the fiscal

package coming from? Who are the investors, borrowers, and lenders? What

is the purpose of the money?

22

Worksheet 2 (back)

Explain the headline from Bloomberg news according to what you have learned in

this unit.

23

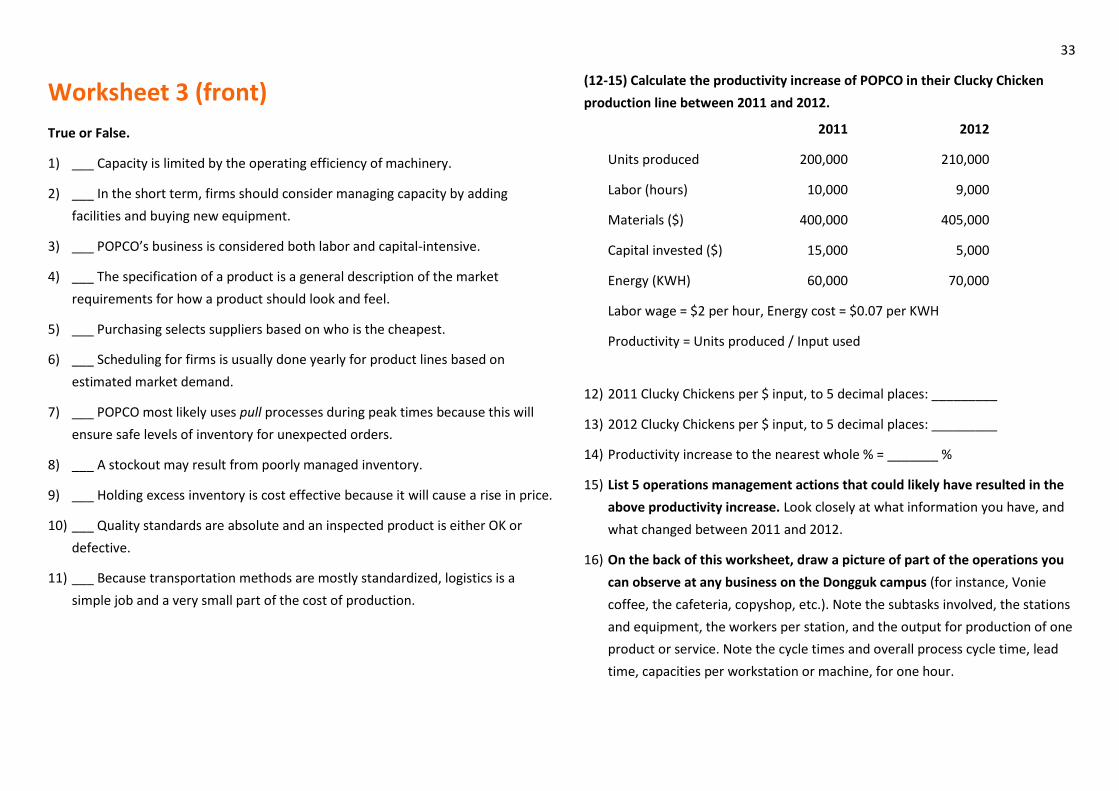

Unit 3

The Operations Department

Learning objectives of this unit

In this unit you will learn the following concepts:

What are the different roles and functions within an operations department? (in class: diagram)

What is productivity, and what is capacity? (in class: calculating)

What processes are involved in production management? (in class: POPCO exercise)

24

Unit 3 Vocabulary

Cycle time (사이클 타임): the time required to complete one cycle of an operation, or to complete a task, job, or function start to finish

어떤 한 공정에서 하나의 제품이 나오는 데 경과되는 시간을 말한다.

Lead time (선행기간): the time required to complete all cycles for an order plus any waiting time between tasks, cycles, etc.

상품의 주문일시와 인도일시 사이에 경과된 시간을 말한다.

Capacity (수용력): the amount of products or services that a plant or enterprise can produce in a given time using current resources

공장이나 기업이 주어진 시간 동안 갖고 있는 resource 를 이용하여 만들 수

있는 제품이나 서비스의 양

Productivity (생산성): an economic measure of output per unit of input, where output may be revenues, goods or services, and inputs are labor and capital

인풋당 아웃풋의 경제척도. 아웃풋은 수익, 제품 또는 서비스, 인풋은 노동

또는 자본이 될 수도 있다.

Labor-intensive (노동집약형): a process where people must do most of the work to generate output

사람들이 아웃풋을 만들어내기 위해 대부분의 일을 하는 과정.

Capital intensive (자본집약적): a process where output is generated mostly from plant and equipment

공장이나 장비를 통해 대부분의 생산량을 만들어내는 과정

Specification (설명서 ): a written statement of an item's required characteristics and design. A specification is documented in a manner that allows purchasing to find appropriate suppliers, and production to make and test the item's quality.

어떤 물품에 대해 요구되는 특징이나 디자인에 관한 진술서. 설명서는 적당한

공급자를 찾고 물품의 품질을 확인하고 실험할 수 있는 구매 방식을

용납하게끔 문서화 되어있다.

Purchasing (구매): all the activities involved in identifying suppliers, negotiating price, and obtaining required materials, supplies, components and parts from other firms based on a specification

설명서에 근거하여 공급자 식별, 가격 협상, 그리고 다른 회사로 부터 필요한

자재, 저장품 그리고 부품을 얻는 것과 관련된 모든 활동.

Inventory (재고): the raw materials, work-in-process goods and completely finished goods that are considered to be the portion of a business's assets that are ready or will be ready for sale.

판매를 위해 준비 되었거나 준비될 회사의 자산의 일부분으로 여겨지는

원자재, 재공품 그리고 완제품

Inventory management (재고관리): the process of managing inventories to minimize costs, including holding and stock-out costs

가격을 최소화 시키기 위한 재고관리 과정으로써 보유 비용 또는

재고부족보충을 위한 조달비용도 포함되있다.

Stock out (재고부족): A situation in which the demand or requirement for an item cannot be fulfilled from the current inventory

현재의 재고로부터 아이템의 수요나 필요사항이 충족될 수 없는 상황

Just in time (적기공급생산): An inventory strategy companies employ to increase efficiency and decrease waste by receiving goods only as they are needed in the production process, thereby reducing inventory costs.

생산과정에 필요한 제품만 받아서 효율성을 높이거나 낭비를 줄이기 위해

회사들이 이용하는 재고전략, 결과적으로 재고 비용을 줄인다

Quality control (품질관리): The process of ensuring that goods and services are produced according to specifications.

설명서에 따라서 제품이나 서비스가 생산되었는지를 보장하는 과정

25

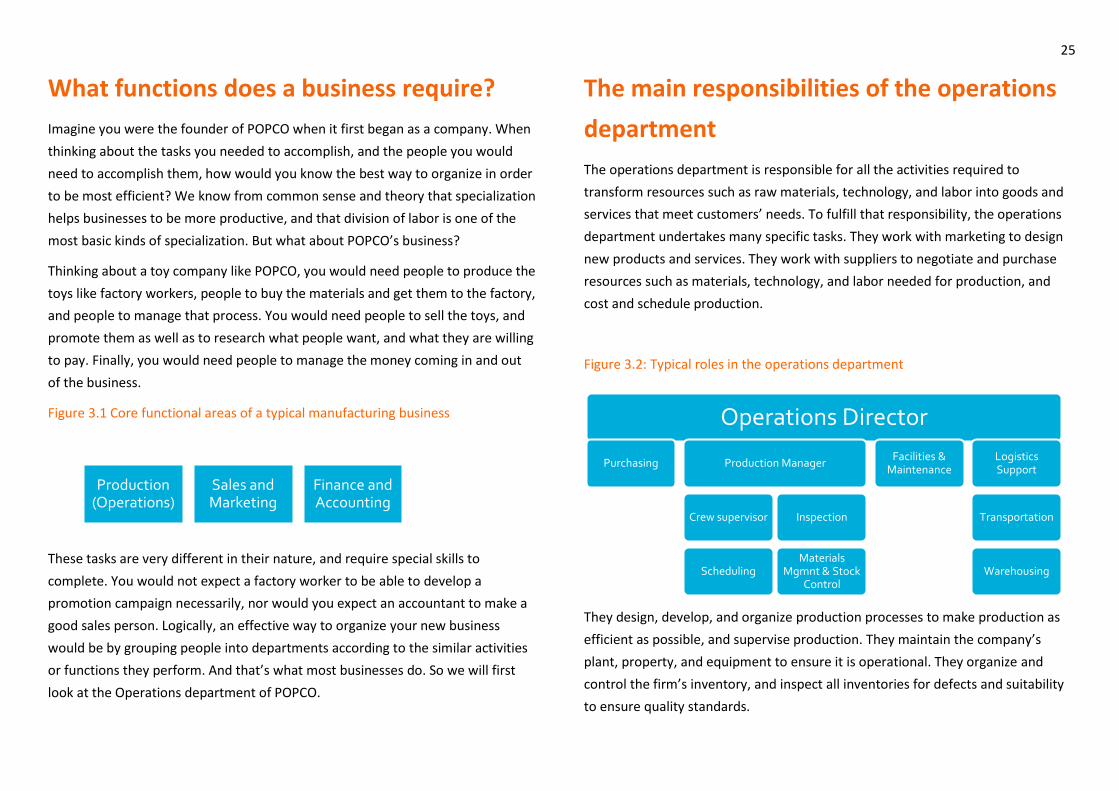

What functions does a business require?

Imagine you were the founder of POPCO when it first began as a company. When

thinking about the tasks you needed to accomplish, and the people you would

need to accomplish them, how would you know the best way to organize in order

to be most efficient? We know from common sense and theory that specialization

helps businesses to be more productive, and that division of labor is one of the

most basic kinds of specialization. But what about POPCO’s business?

Thinking about a toy company like POPCO, you would need people to produce the

toys like factory workers, people to buy the materials and get them to the factory,

and people to manage that process. You would need people to sell the toys, and

promote them as well as to research what people want, and what they are willing

to pay. Finally, you would need people to manage the money coming in and out

of the business.

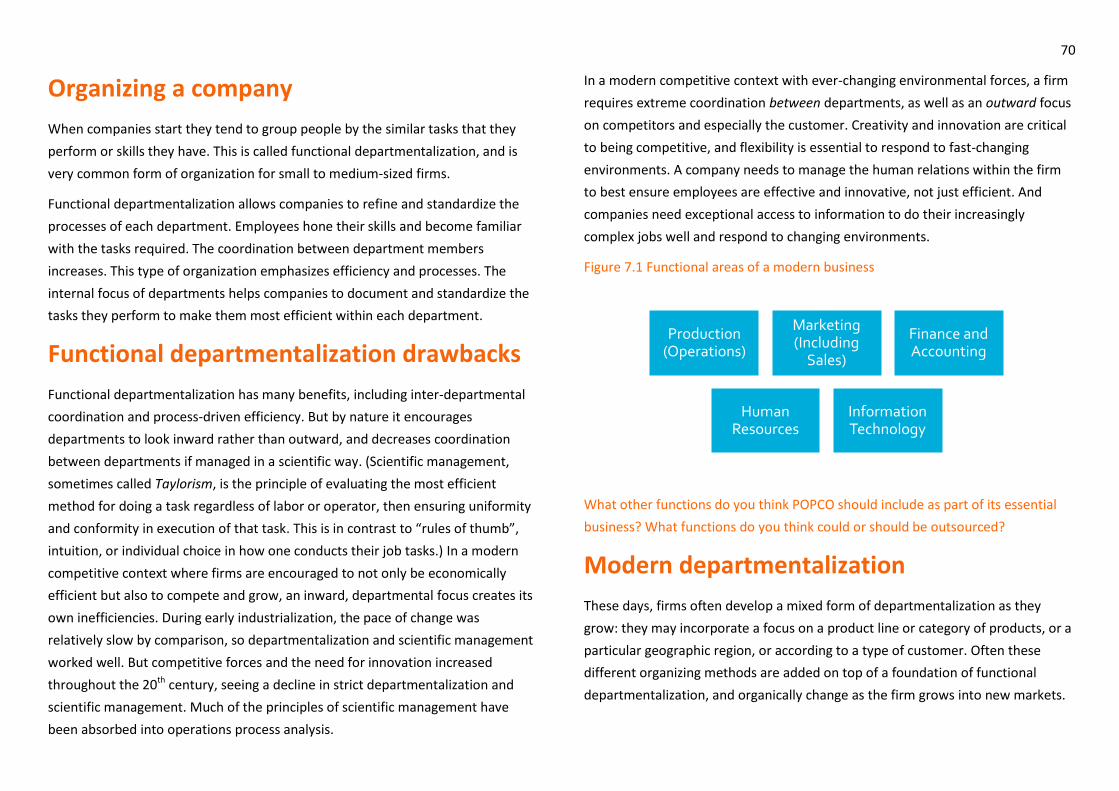

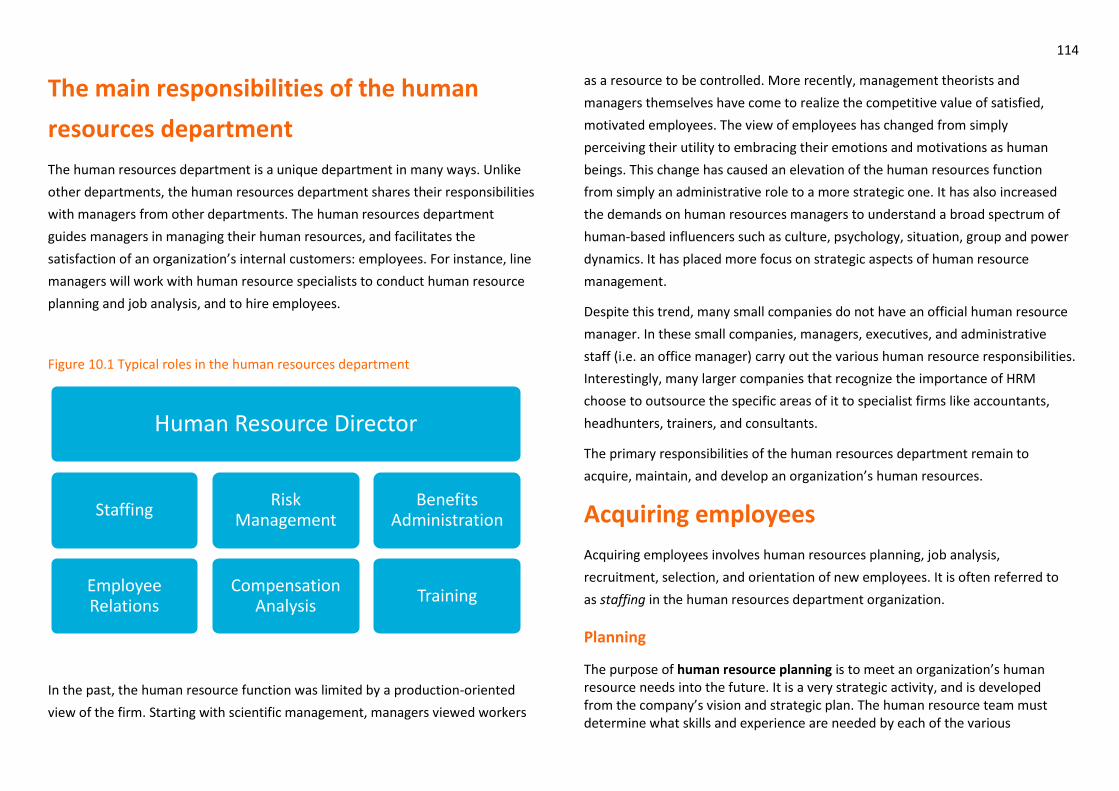

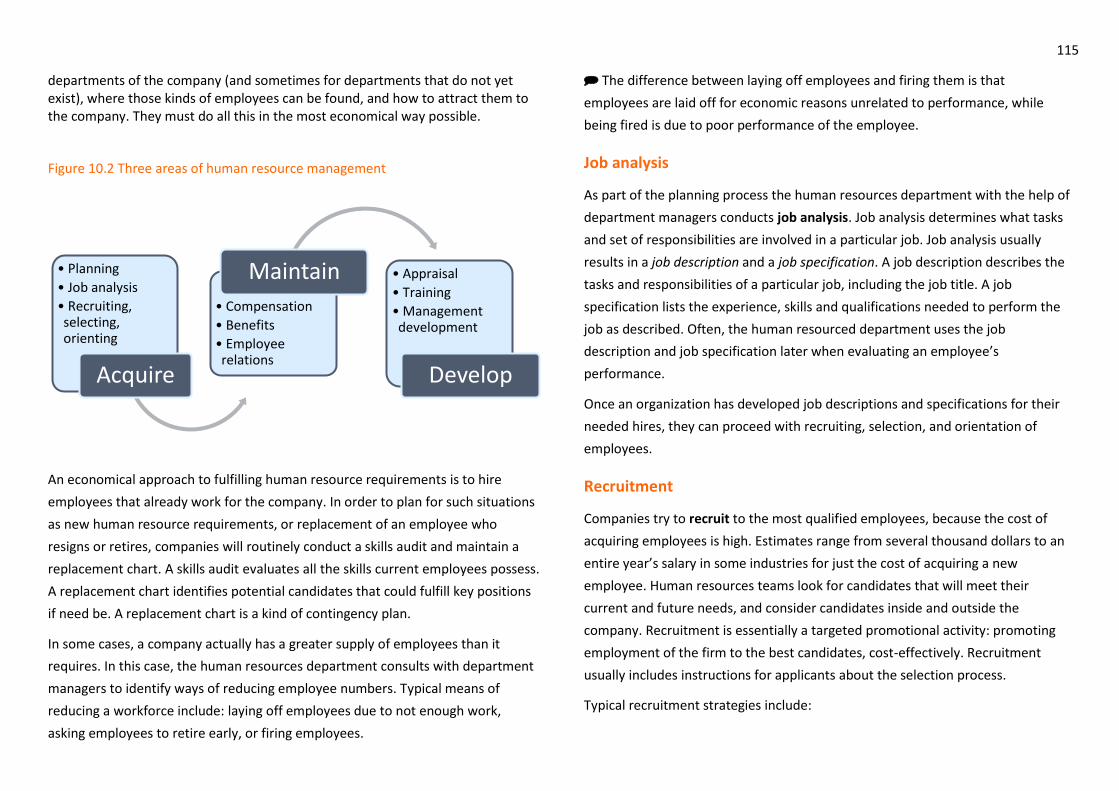

Figure 3.1 Core functional areas of a typical manufacturing business

These tasks are very different in their nature, and require special skills to

complete. You would not expect a factory worker to be able to develop a

promotion campaign necessarily, nor would you expect an accountant to make a

good sales person. Logically, an effective way to organize your new business

would be by grouping people into departments according to the similar activities

or functions they perform. And that’s what most businesses do. So we will first

look at the Operations department of POPCO.

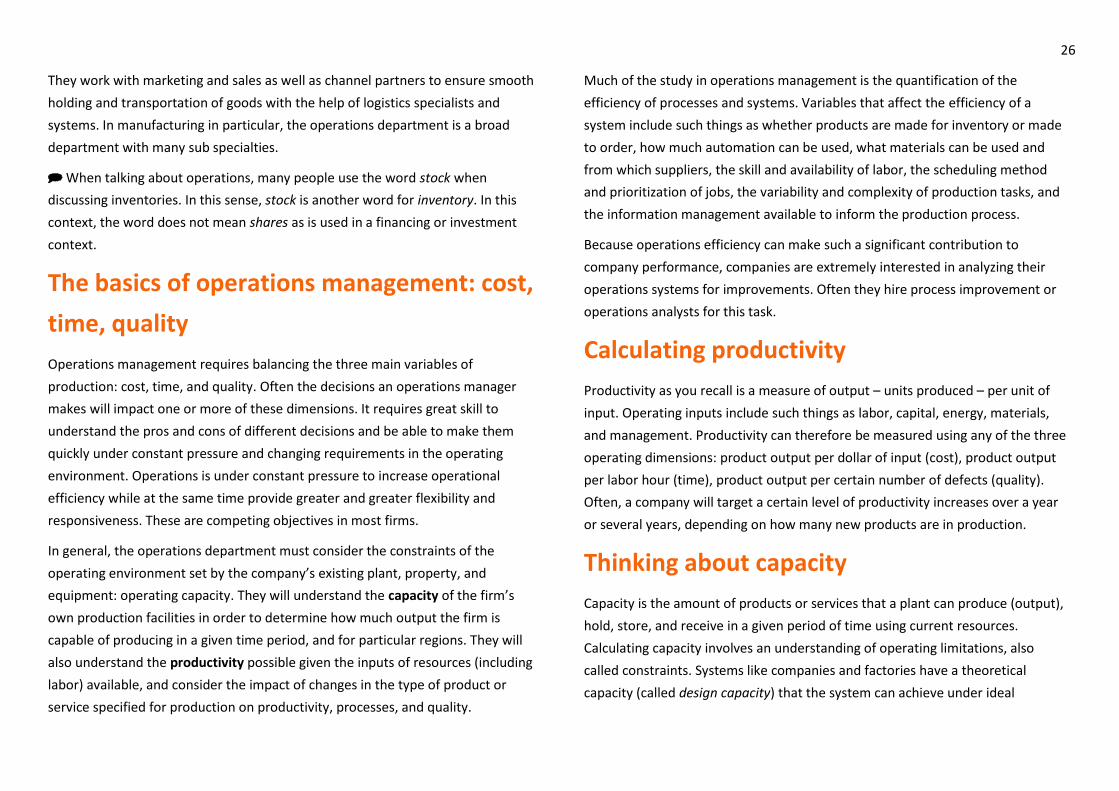

The main responsibilities of the operations

department

The operations department is responsible for all the activities required to

transform resources such as raw materials, technology, and labor into goods and

services that meet customers’ needs. To fulfill that responsibility, the operations

department undertakes many specific tasks. They work with marketing to design

new products and services. They work with suppliers to negotiate and purchase

resources such as materials, technology, and labor needed for production, and

cost and schedule production.

Figure 3.2: Typical roles in the operations department

They design, develop, and organize production processes to make production as

efficient as possible, and supervise production. They maintain the company’s

plant, property, and equipment to ensure it is operational. They organize and

control the firm’s inventory, and inspect all inventories for defects and suitability

to ensure quality standards.

Operations Director

Purchasing Production Manager

Crew supervisor

Scheduling

Inspection

Materials Mgmnt & Stock

Control

Facilities & Maintenance

Logistics Support

Transportation

Warehousing

Production (Operations)

Sales and Marketing

Finance and Accounting

26

They work with marketing and sales as well as channel partners to ensure smooth

holding and transportation of goods with the help of logistics specialists and

systems. In manufacturing in particular, the operations department is a broad

department with many sub specialties.

When talking about operations, many people use the word stock when

discussing inventories. In this sense, stock is another word for inventory. In this

context, the word does not mean shares as is used in a financing or investment

context.

The basics of operations management: cost,

time, quality

Operations management requires balancing the three main variables of

production: cost, time, and quality. Often the decisions an operations manager

makes will impact one or more of these dimensions. It requires great skill to

understand the pros and cons of different decisions and be able to make them

quickly under constant pressure and changing requirements in the operating

environment. Operations is under constant pressure to increase operational

efficiency while at the same time provide greater and greater flexibility and

responsiveness. These are competing objectives in most firms.

In general, the operations department must consider the constraints of the

operating environment set by the company’s existing plant, property, and

equipment: operating capacity. They will understand the capacity of the firm’s

own production facilities in order to determine how much output the firm is

capable of producing in a given time period, and for particular regions. They will

also understand the productivity possible given the inputs of resources (including

labor) available, and consider the impact of changes in the type of product or

service specified for production on productivity, processes, and quality.

Much of the study in operations management is the quantification of the

efficiency of processes and systems. Variables that affect the efficiency of a

system include such things as whether products are made for inventory or made

to order, how much automation can be used, what materials can be used and

from which suppliers, the skill and availability of labor, the scheduling method

and prioritization of jobs, the variability and complexity of production tasks, and

the information management available to inform the production process.

Because operations efficiency can make such a significant contribution to

company performance, companies are extremely interested in analyzing their

operations systems for improvements. Often they hire process improvement or

operations analysts for this task.

Calculating productivity

Productivity as you recall is a measure of output – units produced – per unit of

input. Operating inputs include such things as labor, capital, energy, materials,

and management. Productivity can therefore be measured using any of the three

operating dimensions: product output per dollar of input (cost), product output

per labor hour (time), product output per certain number of defects (quality).

Often, a company will target a certain level of productivity increases over a year

or several years, depending on how many new products are in production.

Thinking about capacity

Capacity is the amount of products or services that a plant can produce (output),

hold, store, and receive in a given period of time using current resources.

Calculating capacity involves an understanding of operating limitations, also

called constraints. Systems like companies and factories have a theoretical

capacity (called design capacity) that the system can achieve under ideal

27

conditions. However, because production is complex and involves so many

variables, this theoretical capacity is rarely, if ever, reached.

Companies talk in terms of effective capacity or throughput instead of design

capacity. Effective capacity is the output the firm expects to achieve given the

expected and anticipated operating efficiency of the equipment and constraints

of the system (constraints such as asset maintenance, labor time for completing

standard tasks, shut down time, lunch breaks, etc., which are usually arrived at by

looking at historical data). It is a measure in units or time that it is expected to

move an order from receipt to delivery in a “realistic” calculation. The efficiency

of a company or system is calculated as the actual output / effective capacity x

100%. Actual output will always be less than effective capacity because of

unanticipated issues such as machine breakdowns, inventory management issues,

and quality problems. However, firms should strive for 100% efficiency of

operations. This does not always mean cutting costs, as investments can increase

output at a greater rate than the required increase in costs.

The extent that a company such as POPCO or an industry as a whole actually uses

its available capacity at any given time is called utilization. The utilization of a

factory is measured as a percentage of its theoretical design capacity, actual

output / design capacity x 100%. Utilization will naturally be less than 100%

because every system requires upkeep and cannot run 100% of the time.

Occasionally economists will look at utilization to analyze the state of demand

and inflation.

For POPCO, a meaningful measure of capacity of our factory might be the number

of Clucky Chickens produced per labor hours, or per sewing machine operating

hours. Constraints determining our effective capacity might be the standard

operating efficiency of our sewing machines in a 60 hour work week, the stock of

materials readily available, and the experience of workers doing the tasks.

Constraints that might reduce our operating efficiency below 100% might include

strikes by workers, unreliable electricity supply to the factory, unexpected sewing

machine breakdowns, errors in the production process, etc.

Effective capacity for POPCO

Consider the different processes involved in producing Clucky Chickens (called

“sub tasks”): cutting fabric, sewing fabric, assembling plastic parts and inserting

computer chip components, stuffing and gluing, labeling, testing. Each of these

processes is unique, and varies in the types of materials involved, the standard

operating efficiency of the equipment, the amount and skill of labor required, the

time it takes for task completion, and the productivity of the sub-task in terms of

units output per labor hour. Each sub task has its own effective capacity.

For each sub task, the time required to produce one unit of output per operator

or workstation is called its cycle time. The lower the cycle time the higher the sub

task’s effective capacity. For some tasks, adding additional operators can increase

the output per subtask and therefore its capacity. But not for all.

The total time of all the cycle times in this process is called its processing time.

There may be waiting time between sub tasks that affect the overall output of the

whole toy assembly process. The waiting time plus the processing time is called

the lead time. Often this is the order processing time.

The interaction of these different processes will have an impact on the overall

output of our factory, and its effective capacity, even though none of these

variables is unexpected or a problem. The limitations of necessary sub process

capacities limit the effective capacity. For instance, if one fabric cutting machine

worked by one factory worker can cut 15,000 Clucky Chickens’ worth of fabric

pieces per day as its standard operating efficiency (a cycle time of 2.4

seconds/unit for a 10-hour workday), it does not necessarily mean our effective

capacity is 15,000 Clucky Chickens per day. Our team of five gluing workers might

only be able to glue and complete 5,000 Clucky Chickens per day in total working

at maximum speed for minimum defective products. That does not mean our

28

gluing workers are slow, it means that that process has a lower capacity than the

fabric cutting process, and so is an effective constraint on overall output. Gluing

may be our bottleneck task in our toy assembly process.

Capacity, productivity and inventory

management

Considering the fabric-cutting example, what would happen if POPCO worked in

that manner for a week? In one week we would have an enormous build-up of

inventory of cut fabric. Short-term materials management would help ensure that

this material was used effectively over time, but the operations manager might

want to consider how to balance the activities of fabric cutting with the other

activities of Clucky Chicken production to avoid the costs of excessive materials

management and inventory holding costs. Both of these cost money, and that

cash resource might be better spent elsewhere.

Marketing and operations will work together to identify the capacity required by

estimated or actual sales orders. Operations will then determine whether the

current plant and facilities’ available capacity is sufficient to meet the demand

even at peak periods, or if additional capacity is required.

In the short-term, scheduling and allocation of equipment and resources can help

use more of existing capacity. In the medium-term, it may be necessary to

increase capacity by adding labor or shifts, improving assets, or outsourcing.

Better management of materials and inventory can improve the utilization of

increased capacity. In the long-term, the firm must consider adding facilities and

equipment in order to increase capacity. All of these changes to utilize and

increase capacity can have an impact on productivity, and it is not always positive.

Adding workers can slow down efficient production teams, as new workers must

be trained. Outsourced activities may have quality control issues. Adding shifts

may destabilize work relations. Using more capacity might threaten capacity

availability during peak periods, slowing down throughput overall. Operations

managers must consider the best use of capacity given all the demands on the

system.

Labor intensive or capital intensive

For manufacturers especially, a key consideration of operating efficiency and

efficiency improvement will depend on whether the firm’s operations are labor-

intensive or capital-intensive processes. Labor-intensive processes require

manual labor to complete, while capital-intensive processes are usually heavily

automated. POPCO’s production is extremely labor-intensive, although we do use

machinery. Most operations requiring sewing and mixed-materials assembly are

labor-intensive. Capital and labor-intensive processes have different costs and

risks associated with them. Capital-intensive processes have high initial costs

compared to labor-intensive processes, but their running costs and operating

risks are lower over time.

The operations process

Consider the following situation: POPCO’s Clucky Chicken toys are selling very

well, so POPCO plans to extend its artificial intelligence toy product line by adding

a new toy: Rolly Rabbits. As marketing establishes requirements for the product,

the operations process begins. The following outlines the basic processes of

operations:

1. Develop specification

2. Purchase materials, organize resources, design processes

3. Schedule production, manage and control materials

4. Oversee production and move inventories

5. Store and transport goods

29

Specification

The specification defines the exact design, capabilities, and materials required of

a product or service. While the specification must be exact, it is based on

requirements from the marketing department that may be descriptive in nature.

Descriptions can be subjective. For that reason, the operations team (or

sometimes a product development team) will quickly design and produce a

limited amount of the product based on the requirements. These one-off

products are called prototypes, and are usually created with the help of computer

aided design technology. Prototypes allow operations and marketing to test,

evaluate, and clarify the best design, capabilities, and materials for the market’s

needs and firm’s unit cost limitations.

Once a completed specification is available, the firm can fully engage in the

operations process. One risk is that marketing requirements will change once the

operations process has begun. Changes to requirements usually demand changes

to the specification and therefore changes to purchases, design, materials, etc.

These changes can be extremely costly. To manage such risks, companies try to

develop fast prototyping capabilities, more reliable market data and testing

techniques, and more flexible operations processes.

Purchasing and resource organization

Next, companies will purchase required materials and organize all materials,

inventories, equipment, and labor for production. While labor is acquired with

the help of the human resources department and equipment and machinery

required is managed through facilities, purchasing is an often-overlooked key

aspect of operational efficiency. The purchasing team will identify multiple

suppliers based on their cost, reliability, and reputation for quality. Then they will

negotiate amongst suppliers for the best deal. Often cost is not the most

important factor.