Embed Size (px)

Citation preview

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 1/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Building the Baltic grids.

What needs to be done ?

LitPol and SwedLit interconnections or competitive solutions.

Can truly independent tr ansmission grids can be realized ?

Current challenges and future opportunities

The impact of poor governance and lack of political clarity.

Piotr Syryczyski

WS Atkins ± Polsk

a

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 2/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Introduction

The ideas developed in the North Sea

What needs to be done ?

Bottlenecks on Polish side of the Baltic Sea

Economy, stupid !

Destabilization of the equilibrium during next years

2800 MW through the Baltic Sea ?

Competitive solutions, What can be done later ?

Fast DC breakers

Can truly independent transmission grids can be realized ?

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 3/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Lack of general plan

Synchronization of Baltic electricity market with European electricity market ishindered due to lack of sufficient interconnections and clear rules on allocationof capacity, on

management of congestion and on balancing; BEMIP High level group is nowdiscussing this issue, but there is up to now no agreements made on further

steps; BEMIP planned activities include setting timeframe for de-synchonizationof Baltic network operation from Russia and Belarus as well as EU-level discussions with Russia on implementing internal electricity market rules also onRussian side;

Additional asynchronous cables connecting Baltic States with Poland, Swedenand Finland will be ready by the end of 2015 as planned in the BEMIP;

presentation by Gatis Abele in Baltic electricity infrastructure, synchronization withEuropean Power Network

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 4/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

North Sea Countries Offshore Grid Initiative (NSCOGI)

The report http://www.offshoregrid.eu indicates the need for:

wind f arm hubs: the joint connection of various f arms;

tee-in connections; the connection of various producers (say wind

f a

rms) toa

pre-existing or pla

nned tra

nsmissionline orinterconnector between countries;

hub-to-hub connection: This can be also interpreted as analternative to a direct interconnector between the countries inquestion.

The authors had proposed The Split Design starting by buildinglower-cost interconnectors by splitting wind f arm connections inorder to connect them to two shores. Integrated solutions andmeshed links would be applied.

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 5/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

What needs to be done ?

the cooperation between the parties is very low

the dominance of dual cross-border connections

under the full supervision and political control of governments

Development plans are treated as confidential

We cannot verif y whether our Client has a real

chances for connection to high voltage grid in

2015 or 2017 or 2020

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 6/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

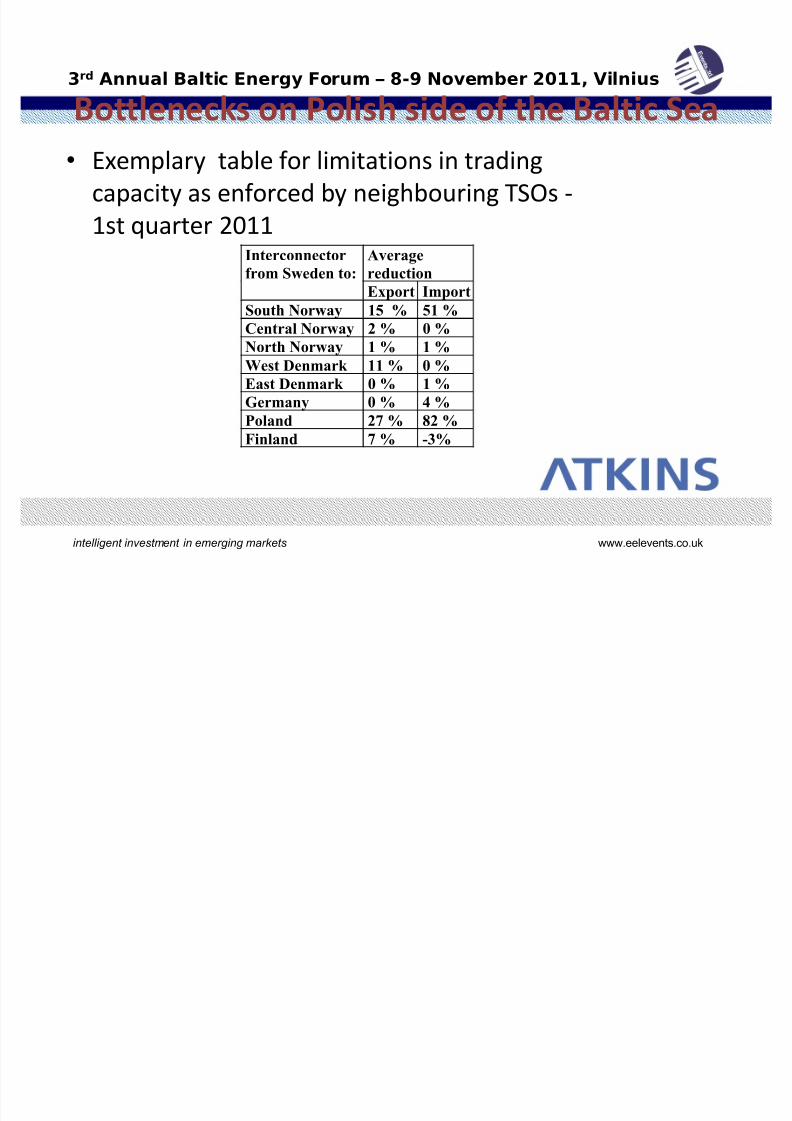

Bottlenecks on Polish side of the Baltic Sea

Exemplary table for limitations in trading

capacity as enforced by neighbouring TSOs -

1st quarter 2011

Average

reduction

Interconnector

from Sweden to:Export Import

South Norway 15 % 51 %

Central Norway 2 % 0 %

North Norway 1 % 1 %

West Denmark 11 % 0 %

East Denmark 0 % 1 %

Germany 0 % 4 %

Poland 27 % 82 %

Finland 7 % -3%

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 7/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Bottlenecks on Polish side of the Baltic Sea

1353 negativedecisions in the period2009-2010 for newconnection contractsfor the total amount of

9745 MW electrical power. Gdansk (225 -3179 MWel), Poznan(428 - 2968 MWel), Szczecin (318 - 1233MWel) andWrocaw

(185 - 1060 MWel).

9 Energia w dobrych rkach

Obszary lokalizacji farm wiatrowych do roku 2020

9

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 8/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Economy, stupid!

2*900 MW Opole coal fired unit ?

Vatenf all Polish assets transaction ?

modernization of Dolna Odra power plant inSzczecin near the Baltic Sea ?

ZE PAK and Konin mines ?

Who wi

llpay 5,6 b

ln Euro for

land

lines

and440/220 kV substations investments ?

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 9/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Destabilization of the equilibrium

Phasing out the German nuclear plants will cause several disturbances for grid stability ;

Lower CO2 limits and IED Directive will phase out at least 1800MW or 3000 MW in coal-fired units in Poland around the

2014-2016 period ; Wind energy program as blockage of long term transmission

contracts through Poland

No import from Belarus to Poland?

Second nuclear unit in Kaliningrad will destabilize the local

grids if this unit will NOT be connected both to Polish andLithuanian grids

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 10/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Destabilization of the equilibrium

2800 MW through the Baltic Sea ?

Environmental decision in 6 months ?

The impact of poor governance and lack of political

clarity In post 2016 period Polish government cannot guarantee

real transfer of electricity in the amount of 3.000 MW-4.000 MW from east to west due to lack of real powerover the timeline of the investment processes for new

400 kvlines

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 11/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

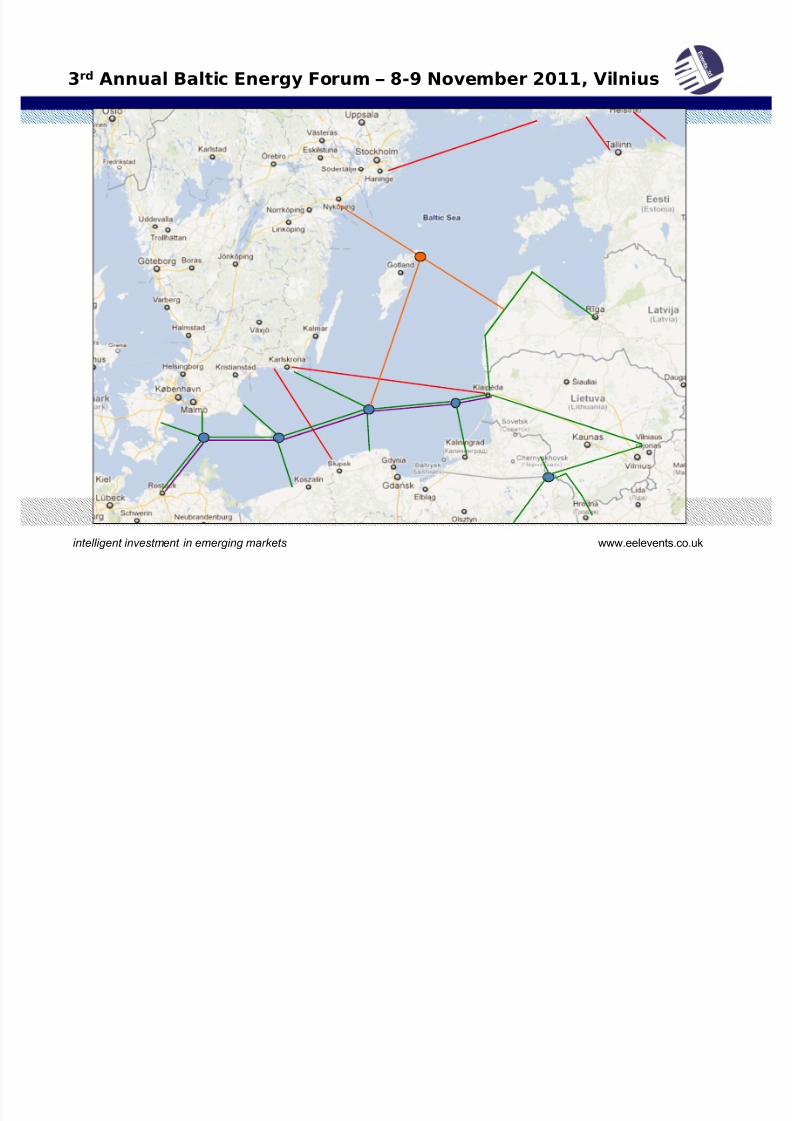

Competitive solutions

Competitive solutions: Five new hubs idea

Hub nr 1 : 55 N, 13,3 E (Kriegers Flak)

Hub nr 2 : 55 N, 15,3 E (Bornholm area) Hub nr 3 : 55,6 N, 17,7 E

Hub nr 4 : 55,6 N, 20,3 E

Hub nr 5 : 54,39 N, 22,87 E

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 12/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 13/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Additional ideas

Hubs and the first west-east cable through the hubs is one

entity

2100 MW additional west-east cables will be built as

three separated projects (merchant cables)

Hubs number 1-4 should have the capacity to connect at

least 400 MW offshore wind f arms or more

Baltic Grid cannot be built tomorrow. It should be slowly

constructed but it can be based on a real technical

program

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 14/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

FHS system and its future

The proposed Five Hub System [FHS] includingadditional lines to these hubs,700 MW NordBaltline, 500 MW PolLit line, and three new 700 MW

(in total 2100 MW) energetic backbone acrossBaltic Sea will probably allow synchronousconnection between Lithuania, Latvia and UCPTEso at this moment the disconnection from IPS/UPS

system can be performed. Kaliningrad area can join the system as well

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 15/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Fast DC breakers

T he safe multi-terminal operation of such an offshore grid based onHVDC VSC technology requires fast DC breakers, which are still inthe development phase at end of 2011. So far, f ast DC breakersare not fully developed and multi-terminal operation is not possible.

In case of an offshore grid failure the complete grid has to be de-energised, the fault has to be isolated, and only then can theoffshore grid be loaded again. T his can also have serious impact onthe onshore grid stability due to frequency problems. Furthermore it should be highlighted that T SOs do not have any experience withmulti-terminal operation based on HVDC VSC technology .

Offshore Grid report, October 2011 http://www.offshoregrid.eu/

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 16/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Fast DC breakers

T he statement youre quoting is partially correct. Interruption of HVDC fault currents is an extremely challenging task and the topicof research for many manufacturers and universities world-wide. Inmy group were studying arcs for HVDC switchgear and try simulatethe short-circuits in VSC based HVDC networks. In the moment, nocommercially available HVDC circuit breaker exists that would fit for VSC networks. It is even so dramatic, that nobody is able to give therequirement specifications for these breakers.

In September 2011, on the Cigre-conference in Bologna, the first (at least to my knowledge) prototype of a fast (based onsemiconductors) HVDC circuit breaker was presented.

Christian M. Franck, Assistant Professor, Dr. rer. nat.

ETH Zürich - High Voltage Laboratory

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 17/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Conclusions

Can truly independent transmission grids be realized ?

± Yes, it needs time and effort and designing new technical

solutions above the heads of politicians. If not, we can

discuss for ages on the subject of dual cross-border lines.With politically nominated TSO managers at the end of

each line we will have an inefficient and costly system

with many bottlenecks due to the various unspecified

reasons.

How to proceed quickly?

8/3/2019 P_Syryczynski Baltic Energy Forum Nov 2011 Vilnius

http://slidepdf.com/reader/full/psyryczynski-baltic-energy-forum-nov-2011-vilnius 18/18

3rd Annual Baltic Energy Forum 8-9 November 2011, Vilnius

www.eelevents.co.ukintelligent investment in emerging markets

Conclusions

Lets write together an application for EU funds forsimilar project. Lets say clearly that this project is fortransit of energy to Central Europe from new plants

located in the east. Lets agree on principles without typical attempt to

block each other country

Lets construct each hub for multiple connection with

three or four land TSOs, lets invite the best technical firms for solving the necessary technical problems

with such new layout