Embed Size (px)

Citation preview

--

"

SICAL COFFEE DAY CO:

.,~ " ..,'

: ,:.;

:." .~

- :~

=.~

-.~

~. CHAPTER-7 ::;:, -~ FINANCIALS =4 ~

=--.~

. -.':)

..-' -.~

.~

,:j

.:')

'I, ,

Sir:allron OrA TArmin~IR I imitAri

I

SICAL COFFEE DAY Co.

'. ........

''''''l

~ .., ~::.

-.~

~

=~ =::,

~

~

-.~

::...~

- ,~

~.~

~:,

.-~

.~

.~

. .- .... ';;

~

f ~ r

CHAPTER 7: FINANCIALS

&!!

•7.1.0 Project Cost Estimate•

7.2.0 Financial Projections•

•7.3.0 Financial Workings•

I I

I ! I

II

I

"

,I'I

I I I,

I,

11 II'

l!, ;1III II

i[

!

il;

III

if II!

:,'I :, I'

I

SICAL COFFEE DAY Co.

·, W"

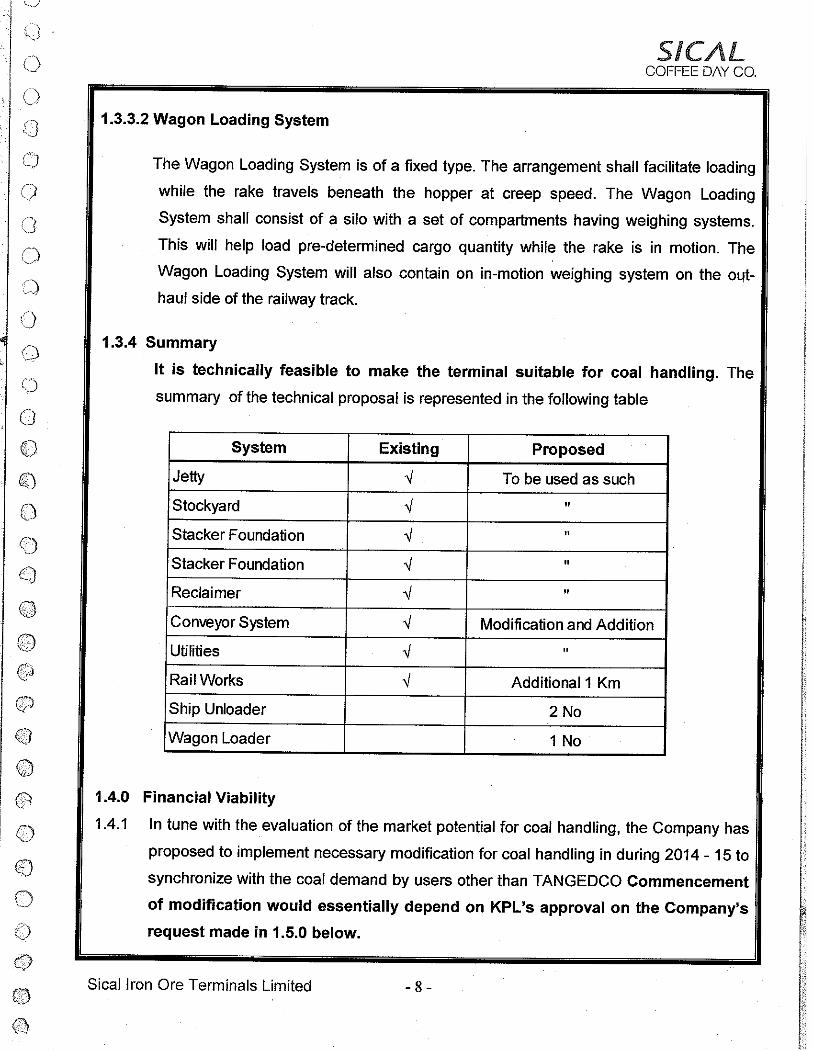

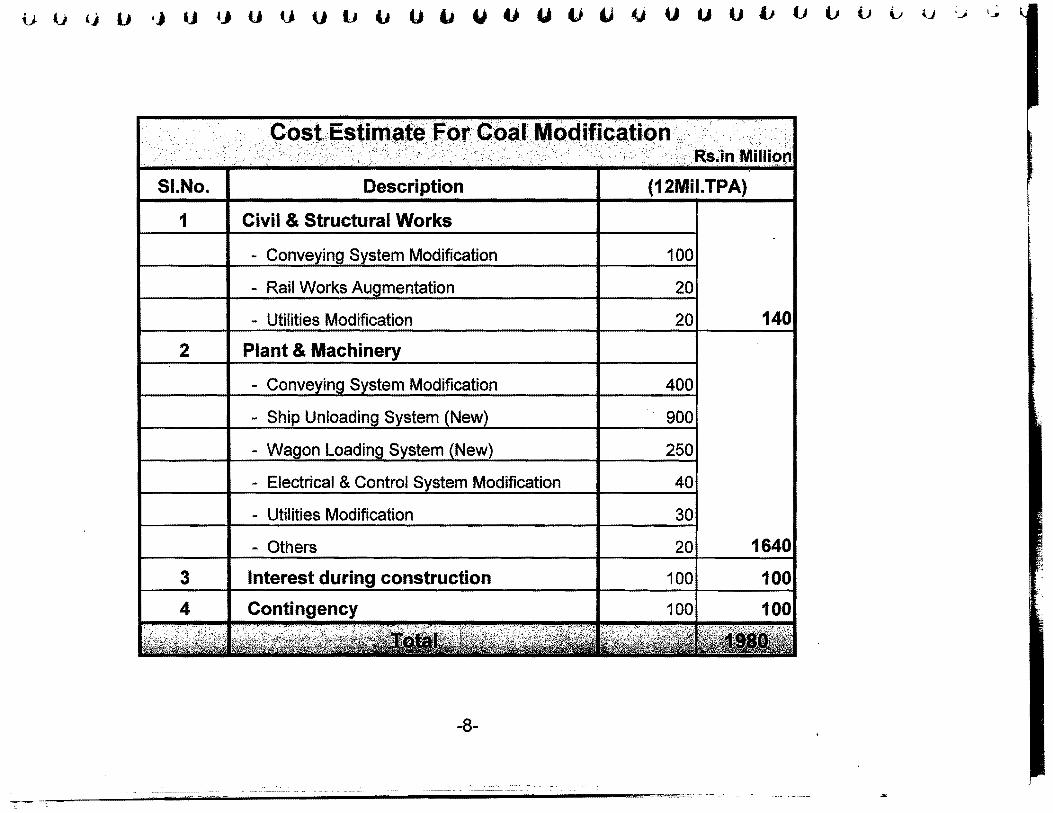

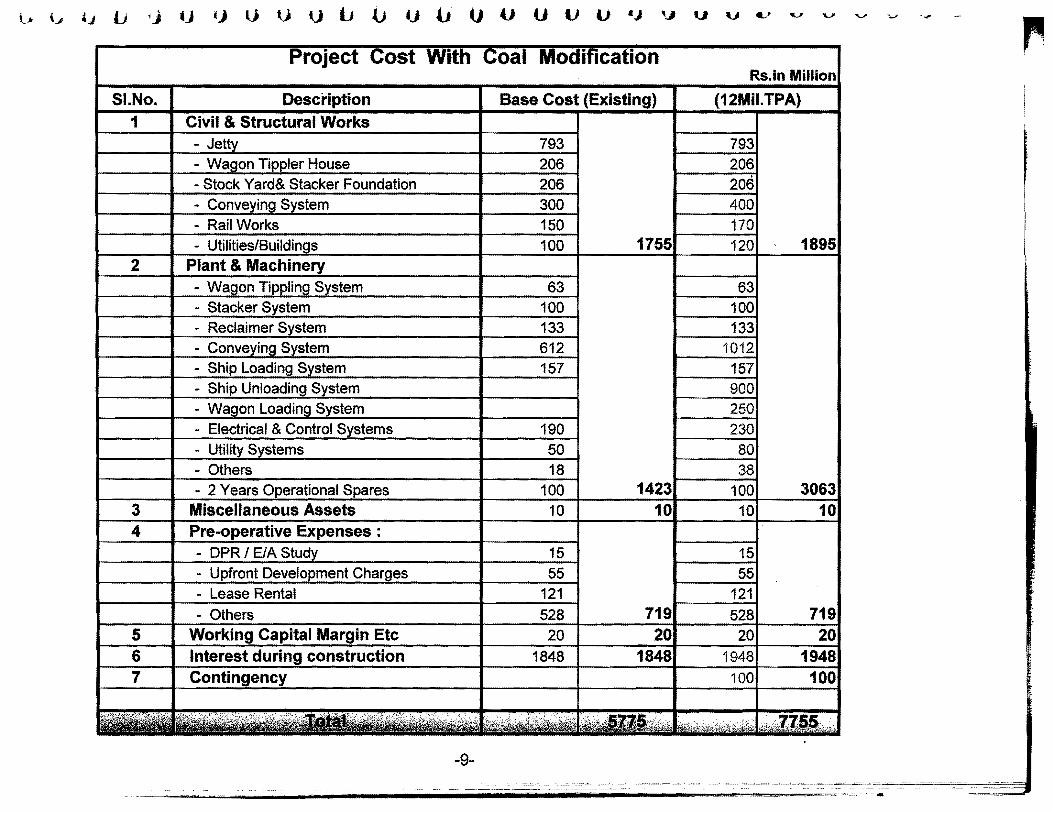

7.1.0 PRO..IECT COST ESTIMATE ....-..-... 7.1.1 Cost Heads

The estimated cost of the modification for coal handling (corresponding to an annual ""..

'

'

throughput capacity of 12 million MT) works out to RS.1980 million. The total project

cost-after modification would be RS.7755 million including the base cost of RS.5775

million for the facilities of the terminal already built. The estimate has covered all the

relevant Systems I Equipments and other cost heads, which fall under the following

.~ broad categories . ,.., I,

11

1) Civil and Structural Works !

1

I2) Plant and Machinery

3) Miscellaneous Assets ~:~

4) Pre-operative Expenses -:::;: 5) Working Capital Margin

::~ 6) Interest during Construction

~.~

7) Contingency

8) Debt Service Reserve ~

7.1.2 Civil and Structural Works

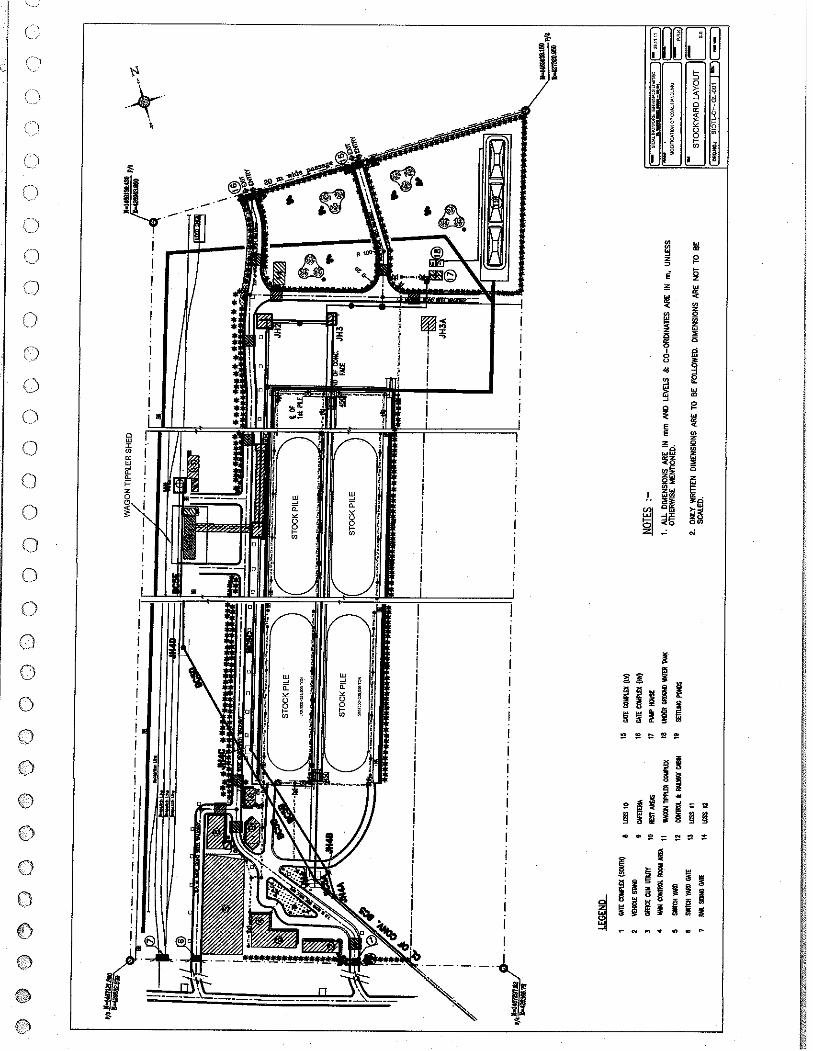

7.1.2.1 The cost of Civil and Structural Works for the project is estimated at Rs.1895

million consisting of the following: - .... -- .....,.) 1) Jetty with all fixtures (already built)

2) Wagon Tippler House including the tunnel works

(already built but will not be used)

3) Stock Yard preparation & Stacker I Reclaimer foundation with the rail

(already built)

4) Road Works within the premises (already built)

5) Junction Houses and Conveyor Gallery structures & foundations for the

Conveying System covering a total length of 6 Km. (already built. Partial

modification and augmentation required).

...~ SICAL

COFFEE DAY Co.

.

, -.,.'

..,

'<Ill.... .~....

~:~

-:~

---. '" ~."

-....-1.- .. -..:~

~

:...~

. .. -"'-"-.'

- .~

:...~

-'. ~

~

.~

7.1.2.2

7.1.2.3

7.1.2.4

6) Railway Siding complete with the foundation and the rail tracks. (already built,

only marginal augmentation required).

7) Utilities I Buildings covering Control Room, Electrical Sub-Stations,

Pump Houses, Office and other Utility areas (already built, only marginal ,

augmentation required).

For each of the above works, the actual cost incurred for the total completion have been

duly considered along with the estimate for the following three items which call for

modification, requiring additional amount of Rs.140 million over the existing cost

of Rs.550 million. p!

1. Conveyor System : Civil Works modification estimated at RS.100 million over

and above RS.300 million already incurred for the existing system.

2. Rail Works : Provision of RS.20 million for additional 1 Km of Rail Siding over

and above the existing 6Km (Rs.150million).

3. Utilities I Buildings: Provision of RS.20 million for minor modification to the

existing utilities for over and above RS.100 million already incurred for the

existing Utilities I Buildings.

The following facilities have already been built and do not call for any

modification. The actual cost incurred are as below:

1. Jetty : RS.793 Million

2. Stockyard & Stacker Foundation: RS.206 Million

3. Total : Rs.999 Million

The only facility built at a cost of RS.206 million but will not be useable for coal handling

operation is the Wagon Tippler House (an underground structure with the shed provided

above the ground level).

.J

,~

..j

:,..;; ='.~

:::'.-~

~.~~

,.~

~

:;)

::to

~

:;a

~

:.:J

~

~

.... '

SICAL COFFEE DAY Co.

7.1.2.5 In summary, the total Civil Works cost already incurred is Rs.1755 million and the

additional cost to be incurred is Rs.140 million .

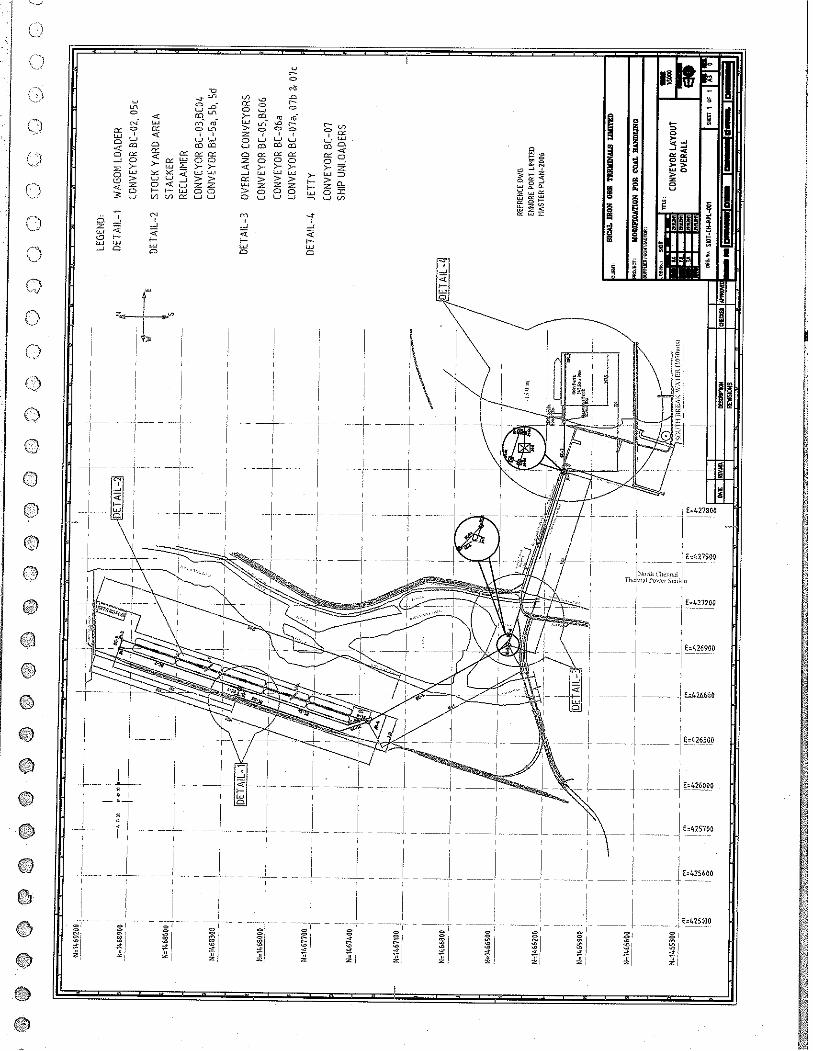

7.1.3 Plant and Ma,chinery

7.1.3.1 The cost of Plant and Machinery for the project is estimated at Rs.3063 million

consisting of the following:

1) Wagon Tippling System (already installed but will not be used)

2) Stacker System (already installed)

3) Reclaimer System (already in'Stalled)

4) Conveying System covering a total length of 6 km. (already installed. Partial

modification required)

5) Ship Loading System. (already installed but will not be used).

6) Utilities I Electrical Systems covering Control Room, Electrical Sub-Stations etc

(already installed, only marginal modification required).

7) Ship Unloading System (to be installed, 2 Nos)

8) Wagon Loading System (to be installed, 1 No).

7.1.3.2 For each of the above systems, the actual cost incurred for the total completion have I i

been duly considered along with the estimate for the following items which call for

modification I addition, requiring additional amount of Rs.1640 million over the

existing cost of Rs.870 million.

1. Conveyor System: Modification estimated at RS.400 million over and above

RS.612 million already incurred for the existing system.

2. Utilities I Electricals: Provision of RS.90 million for minor modifications to the

existing Utilities I Electricals over and above Rs.258 million already incurred

for the existing Utilities I Electricals .

::;

..)

.;)

.:J

~

~

~

~

~

~

--..-';'

~

:~

~

~

~

~

~

:> !'

~

~

~

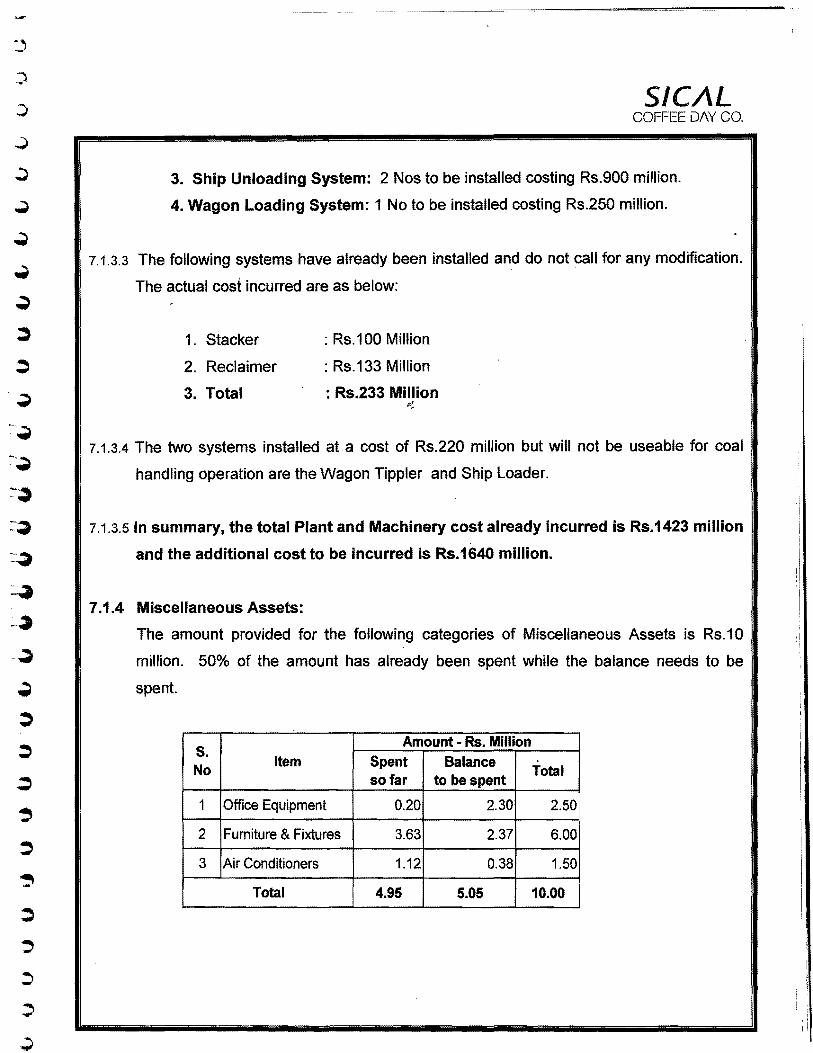

3. Ship Unloading System: 2 Nos to be installed costing RS.900 million.

4. Wagon Loading System: 1 No to be installed costing RS.250 million .

7.1.3.3 The following systems have already been installed and do not call for any modification.

The actual cost incurred are as below:

1. Stacker

2. Reclaimer

3. Total

: RS.100 Million

: RS.133 Million

: Rs.233 Million IP!

7.1.3.4 The two systems installed at a cost of RS.220 million but will not be useable for coal

handling operation are the Wagon Tippler and Ship Loader.

7.1.3.5 In summary, the total Plant and Machinery cost already incurred is Rs.1423 million

and the additional cost to be incurred is Rs.1640 million.

7.1.4 Miscellaneous Assets:

The amount provided for the following categories of Miscellaneous Assets is RS.10

million. 50% of the amount has already been spent while the balance needs to be

spent.

S. Amount - Rs. Million

Item Spent BalanceNo Total

so far to be spent

1 Office Equipment 0.20 2.30 2.50

2 Furniture & Fixtures 3.63 2.37 6.00

3 Air Conditioners 1.12 0.38 1.50

Total 4.95 5.05 10.00

SICAL COFFEE D/\Y CO .

,I 1

:; SICAL COFFEE DAY Co.

I I

7.1.5 Pre-operative Expenses

A provision of RS.719 million has been made to cater to the expenses relating to I I

DPR I EIA Studies, Bank Guarantee Margin I Charges, Up-front Development Charges,

Lease Rentals, Staff Expenses, Overhead Expenses etc. Most of these expenses have

already been incurred to the tune of Rs,423 million so far and provision of RS.296

million made against expenses to be incurred by the Company during the remaining

period till the year 2015.

7.1.6 Working Capital Margin

Working Capital Margin is provided at RS.20 million, considering the total operating

expenses required for one month and one year Lease Rental payable to EPL in

advance as detailed under Financial Workings attached in this section.

7.1.7 Interest

Based on the actual funds requirement for the project so far in tune with the

physical progress and the actual inflow of funds through equity and term loan,

interest and financing charges have worked out to RS.1848 million till now. Considering

further the interest cost to be incurred on RS.2324 million of Term Loan already availed

for the remaining period till 2015 and the balance Loan to be availed for conversion of

the project, additional sum of RS.100 million has been estimated at the rate of 12.75%

p.a

7.1.8 Contingency

.~ Contingency of Rs.1 00 million has been considered for conversion on the basis of 5% of

project cost .of Rs.1980 million.

Sicallron Ore Terminals Limited - 5

)

SICAL COFFEE DAY Co.

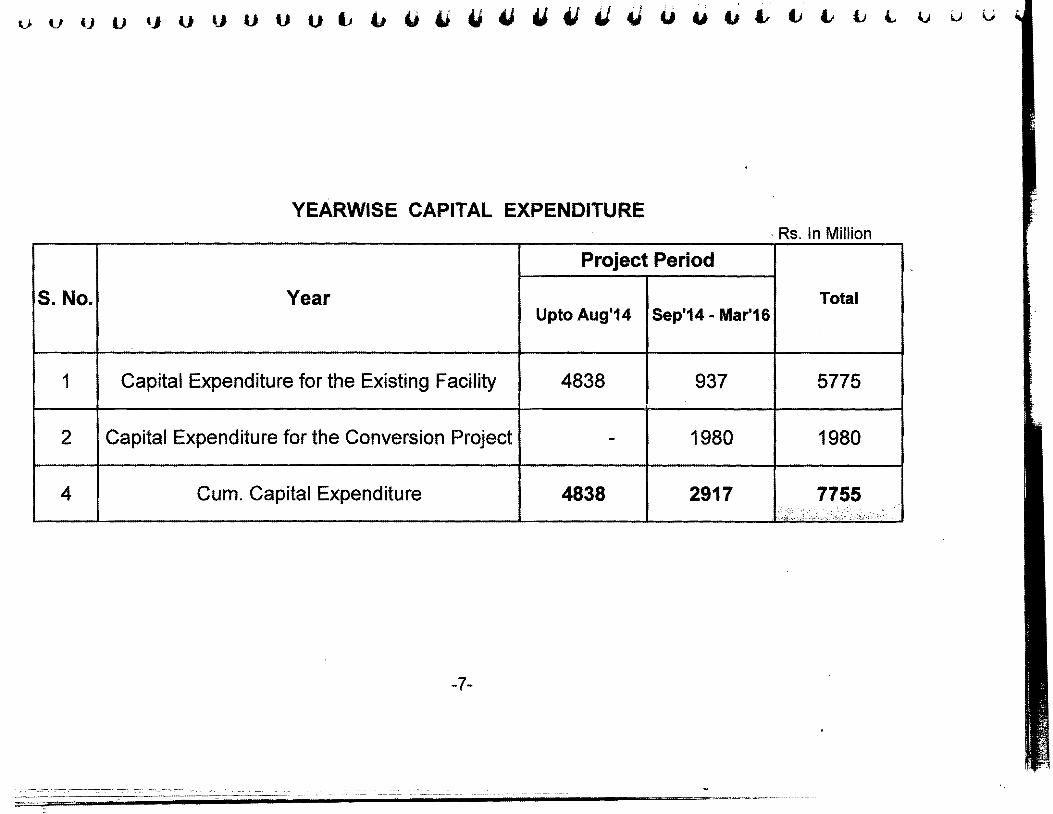

7.1.9 Capital Additions

Cost of additional equipment considered during conversion (corresponding to an

annual throughput capacity of 12 million MT ) along with associated Civil & Structural

Works is estimat~d at Rs. 1980 million as per the break up given, in this section. Year

wise Capital Expenditure of the Company is given in the table attached in this section.

7.1.10 Comparison of Project Cost (after modification) with Grass Root Terminal Cost

The total project cost after implementing modification would be RS.7755 million. It is

however a fact that a substantial portion of the project (Rs.5775 million) has already

been built based on the Contract Prices fixed as early as 2008 and since then there has

been a steep increase in all input costs as detailed in the statement attached to this

section. With an increase of over 50% in Concrete Works Prices, over 50% in Steel

Prices and over 67% in all other input prices and Labour costs etc, a Grass Root

Terminal, if built today would certainly be more than Rs. 8000 million for 12 million

tonnes capacity as per the break up given in the statement attached. Hence SIOTL's

Terminal Cost of RS.7755 million after modification is very much comparable to a Grass

Root Facility.

u v U U Y U v U u U L ~ U ~ ~ ~ U ~ ~ ~ ~ ~ ~ ~ ~ L L L ~ u U

YEARWISE CAPITAL EXPENDITURE - Rs. In Million

S. No. Year

Project Period

Total Upto Aug'14 Sep'14 - Mar'16

1 Capital Expenditure for the Existing Facility 4838 937 5775

2 Capital Expenditure for the Conversion Project - 1980 1980

4 Cum. Capital Expenditure 4838 2917 .

7755 '~;>....." ......... ;, ..~+;./••~ .

.'

-7

-

U U tJ lJ ~J U ~J U U 0 tJ 1I U u u u U tJ ~ V 0 U tJ lJ tJ () t.J V V i~ 1 __

SI.No. I Description I (12MiI.TPA) i

1 I Civil & Structural Works

m Modification I 100- - -- Rail Works Auamentation 20

- Utilities Modification 201 1

2 Plant & Machi

Modification 400

- Ship Unloading System (Newl 900

250

- Electrical &Control S stem Modification 40

- Utilities Modification 30

- Others 20 1640

3 Interest durina construction 100 100

-8

t» (.., 'J {) ;J U .J U U \J tJ u U u (} u u u U tJ \I U U 'V" '-' '-'/IV '-"

~ Rs.in Million

Base Cost ''''Yletolnn (12Mil.

206

100 1755 1895

100 1423 3063 10 10 10

4

121 528 719 719

5 M:arnin Etc 20 20 20 6 1848 1848 1948 7 100

-9

~ -,~,--,--,--~--~---

lJ. l.t iJ j) VU~JUuviJ~ ~ L U ~ u u ~ ~ u u u ~ v v ~ v .......

Description

Project Cost ~nrnn!:llri~nn Modification Vs Grass Root

SIOTL Grass Root

Rs.in Million

Basis of Estimate for Grass Root Facility

increase in cost of Concrete . increase in cost of Steel Plates increase in cost of Steel Rebars increase in cost of Structural Steel increase in cost of other inputs such as Sand, Murrum,

ult:oel. Consumables, labour etc.

increase in cost of Steel Plates increase in cost of Structural Steel increase in cost of other inputs such as Diesel,

It.:lf'trif'gll:! consumbles, components, labour etc.

30% (Average) increase in Cost

ote: Out of Rs.7755 million with modification, Rs.4838 million is actual based on Contract prices fixed in 2008. Since then, there has been a significant escalation in all input costs as detailed above.

-10

J

....-----~- .~. --~..-- -======='=============

I JI ;1\

SleAL COFFEE DAY Co.

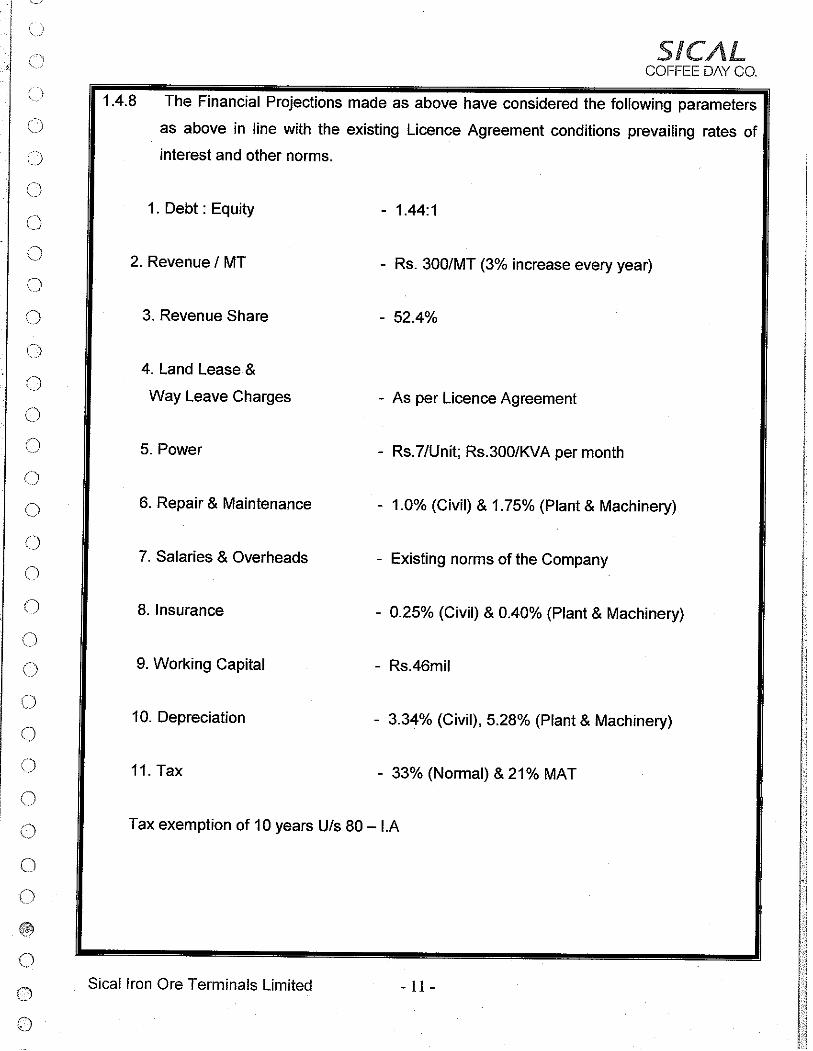

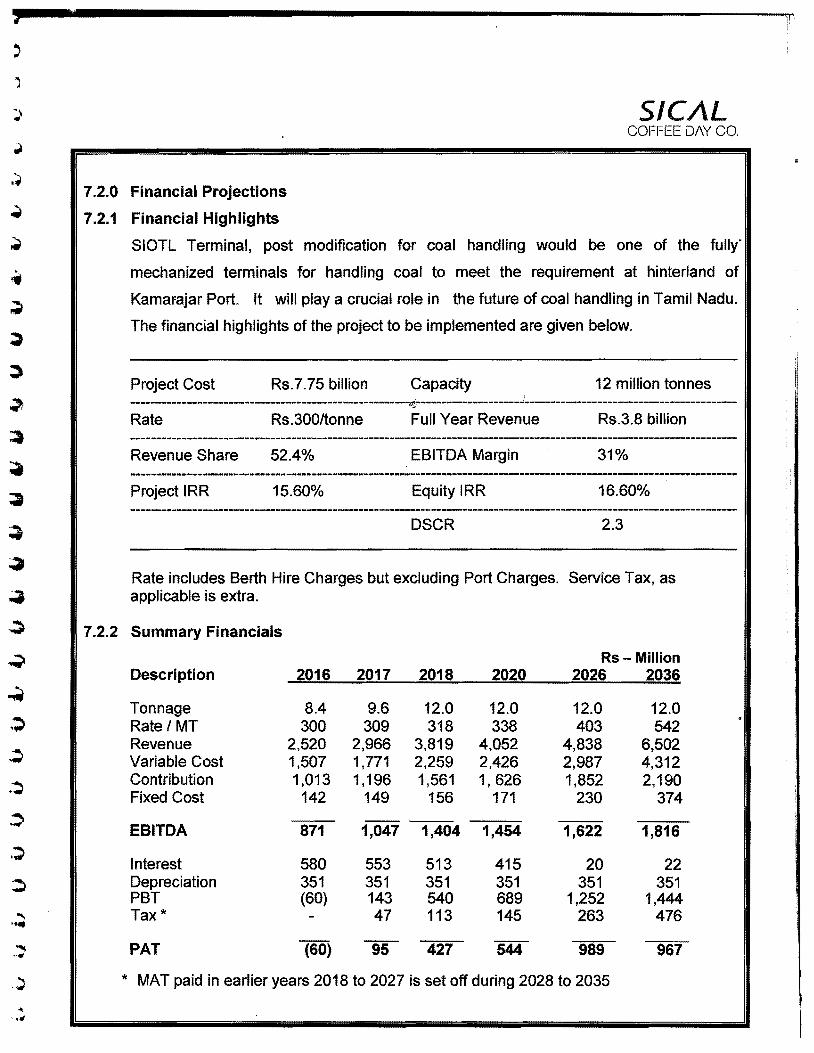

7.2.0

7.2.1

7.2.2

Financial Projections

Financial Highlights

SIOTL Terminal, post modification for coal handling would be one of the fullt

mechanized terminals for handling coal to meet the requirement at hinterland of

Kamafajar Port. It will playa crucial role in the future of coal handling in Tamil Nadu.

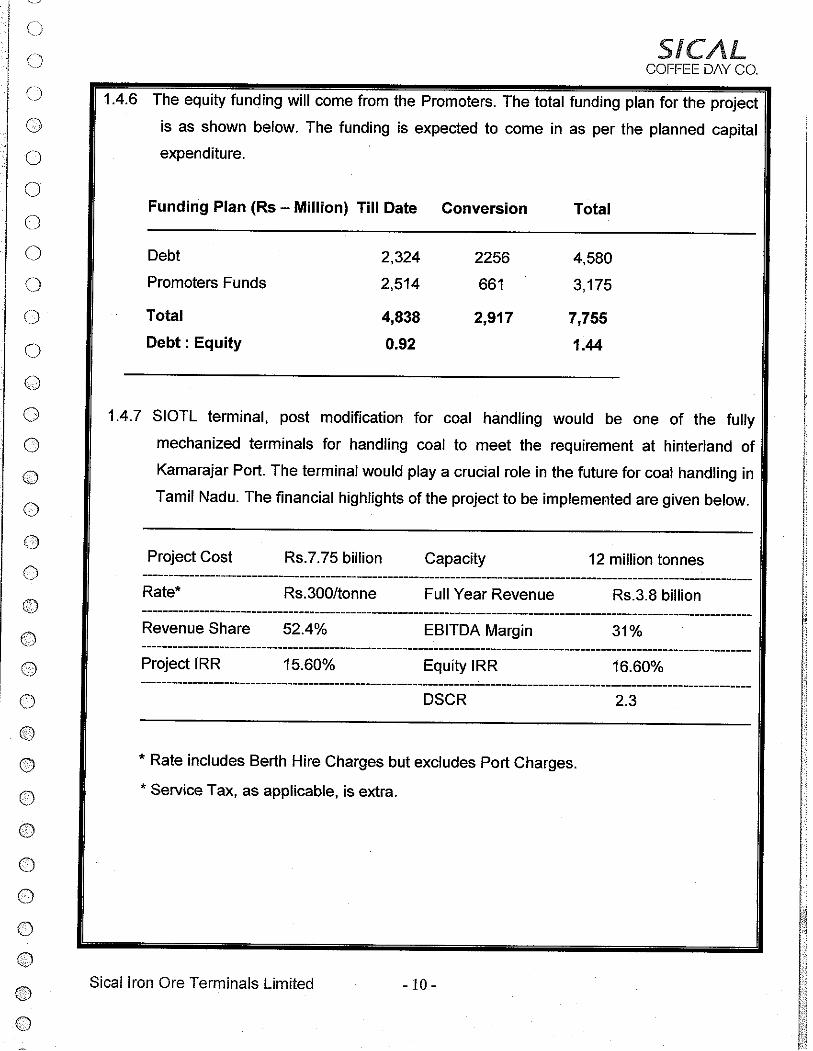

The financial highlights of the project to be implemented are given below.

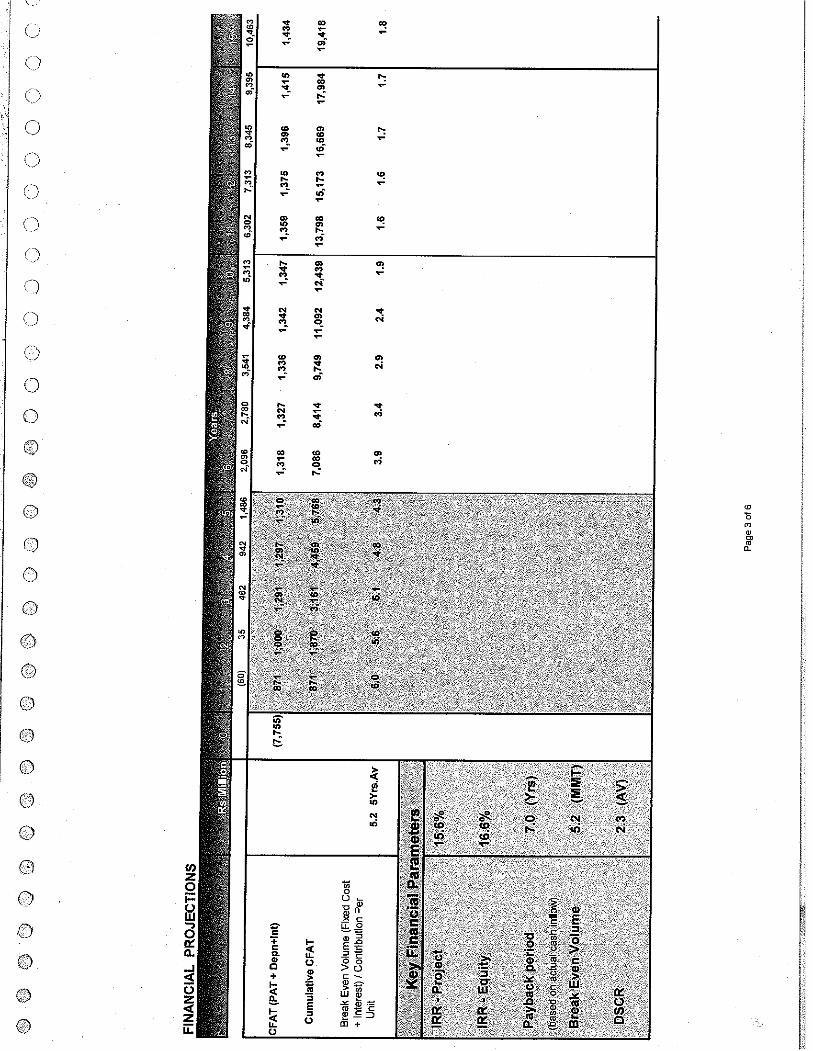

Project Cost RS.7.75 billion Capacity 12 million tonnes . )

------------------------------------------------------~--------------------------------------------------------------Rate RS.300!tonne FuJI Year Revenue RS.3.8 billion

Revenue Share 52.4% EBITDA Margin 31%

Project IRR 15.60% Equity IRR 16.60%

DSCR 2.3

Rate includes Berth Hire Charges but excluding Port Charges. Service Tax, as applicable is extra.

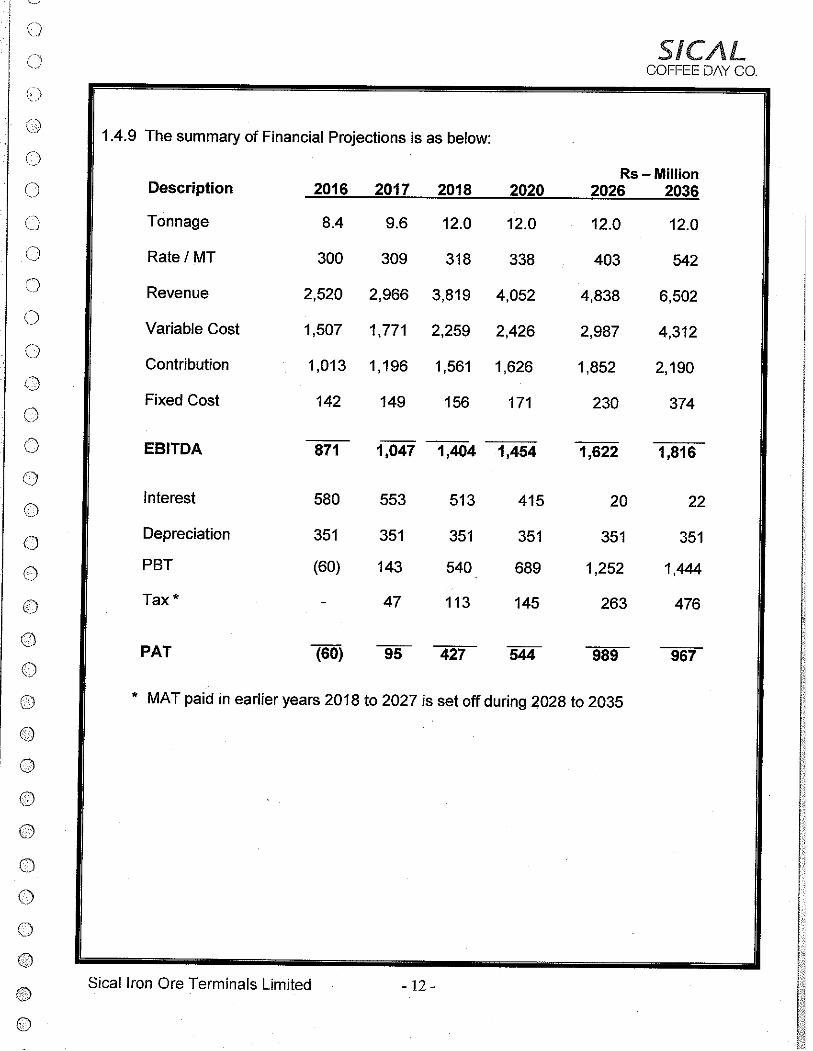

Summary Financials

Rs Million Description 2016 2017 2018 2020 2026 2036

Tonnage 8.4 9.6 12.0 12.0 12.0 12.0 Rate! MT 300 309 318 338 403 542 Revenue 2,520 2,966 3,819 4,052 4,838 6,502 Variable Cost 1,507 1,771 2,259 2,426 2,987 4,312 Contribution 1,013 1,196 1,561 1,626 1,852 2,190 Fixed Cost 142 149 156 171 230 374

EBITDA 871 1,047 1,404 1,454 1,622 1,816

Interest 580 553 513 415 20 22 Depreciation 351 351 351 351 351 351 PBT (60) 143 540 689 1,252 1,444 Tax * 47 113 145 263 476

PAT (60) 95 427 544 989 967

* MAT paid in earlier years 2018 to 2027 is set off during 2028 to 2035

.. , "If

SICAL COFFEE DAY Co.

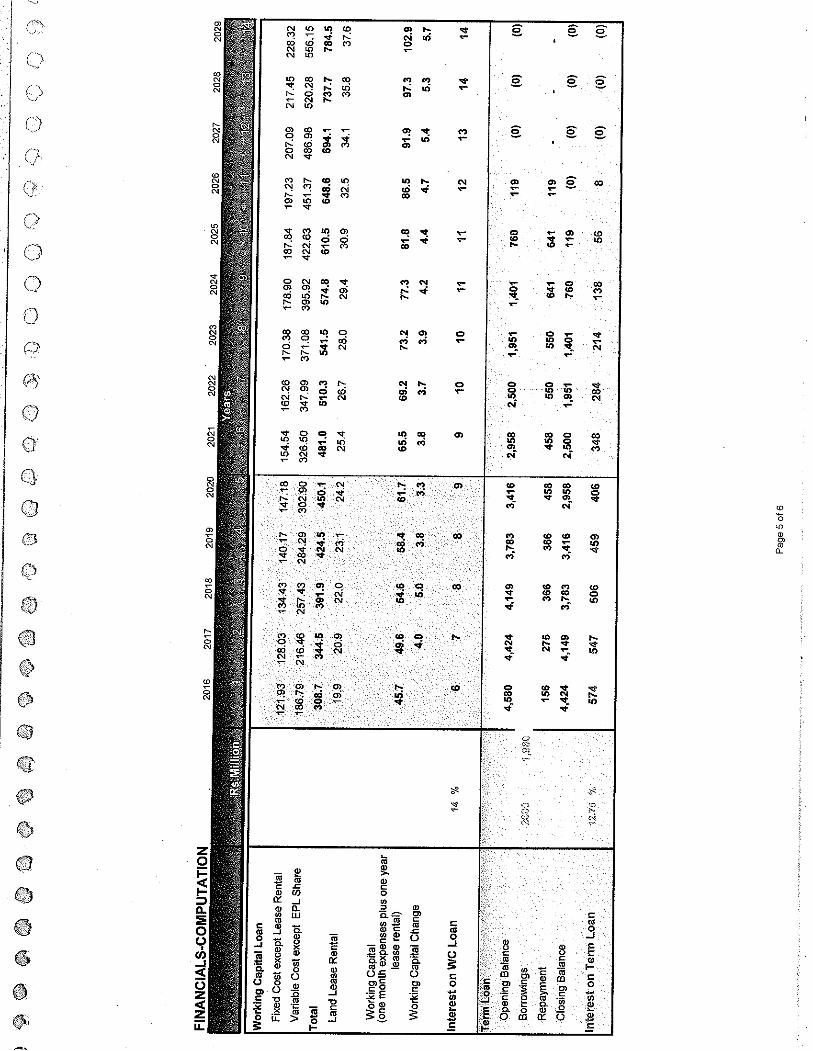

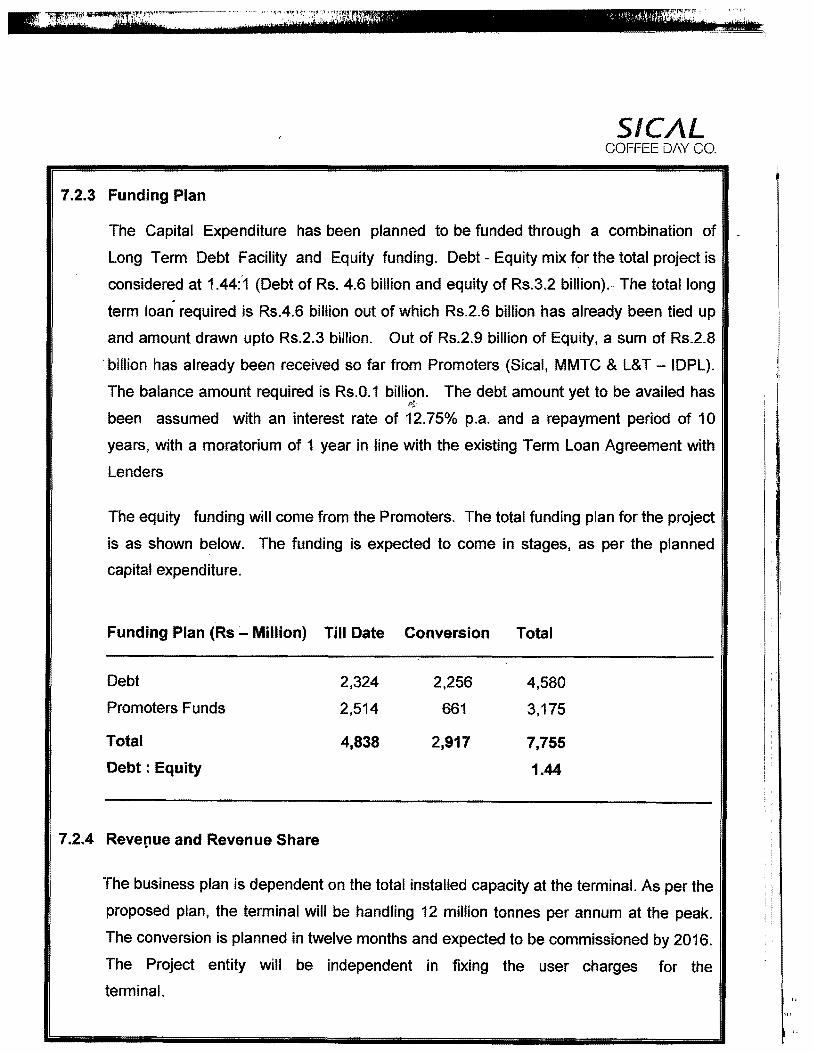

7.2.3 Funding Plan

The Capital Expenditure has been planned to be funded through a combination of

Long Term Debt Facility and Equity funding. Debt - Equity mix for the total project is

considered at 1.44:'1 (Debt of Rs. 4.6 billion and equity of RS.3.2 billion). 1 The total long

term loan required is Rs.4.6 billion out of which Rs.2.6 billion has already been tied up

and amount drawn upto Rs.2.3 billion. Out of Rs.2.9 billion of Equity, a sum of Rs.2.8

. billion has already been received so far from Promoters (Sical, MMTC & L&T - IDPL).

The balance amount required is Rs.0.1 billion. The debt amount yet to be availed has >'!

been assumed with an interest rate of 12.75% p.a. and a repayment period of 10

years, with a moratorium of 1 year in line with the existing Term Loan Agreement with

Lenders

The equity funding will come from the Promoters. The total funding plan for the project

is as shown below. The funding is expected to come in stages, as per the planned

capital expenditure.

Funding Plan (Rs - Million) Till Date Conversion Total

Debt 2,324 2,256 4,580

Promoters Funds 2,514 661 3,175

Total 4,838 2,917 7,755

Debt: Equity 1.44

7.2.4 Revepue and Revenue Share

The business plan is dependent on the total installed capacity at the terminal. As per the

proposed plan, the terminal will be handling 12 million tonnes per annum at the peak.

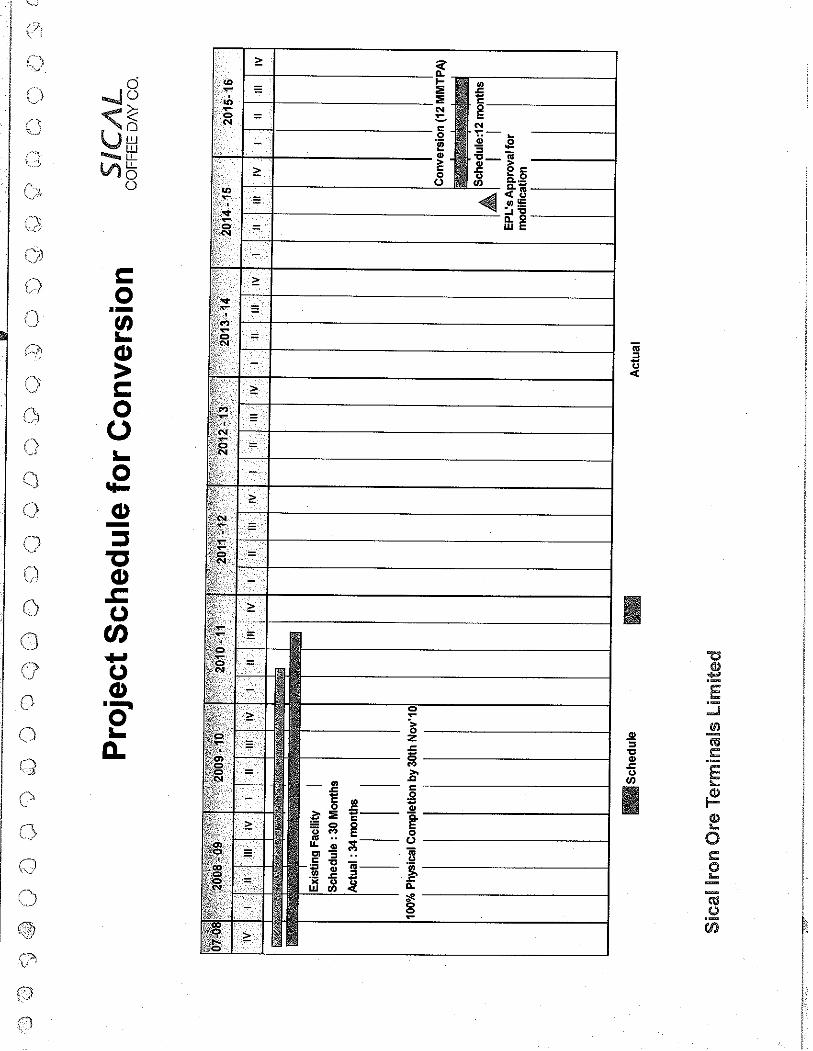

The conversion is planned in twelve months and expected to be commissioned by 2016.

The Project entity will be independent in fixing the user charges for the

terminal.

I

,I

, , I

Hi

.. SICAL-COFFEE DAY Co.

.,.....

.-.,-.

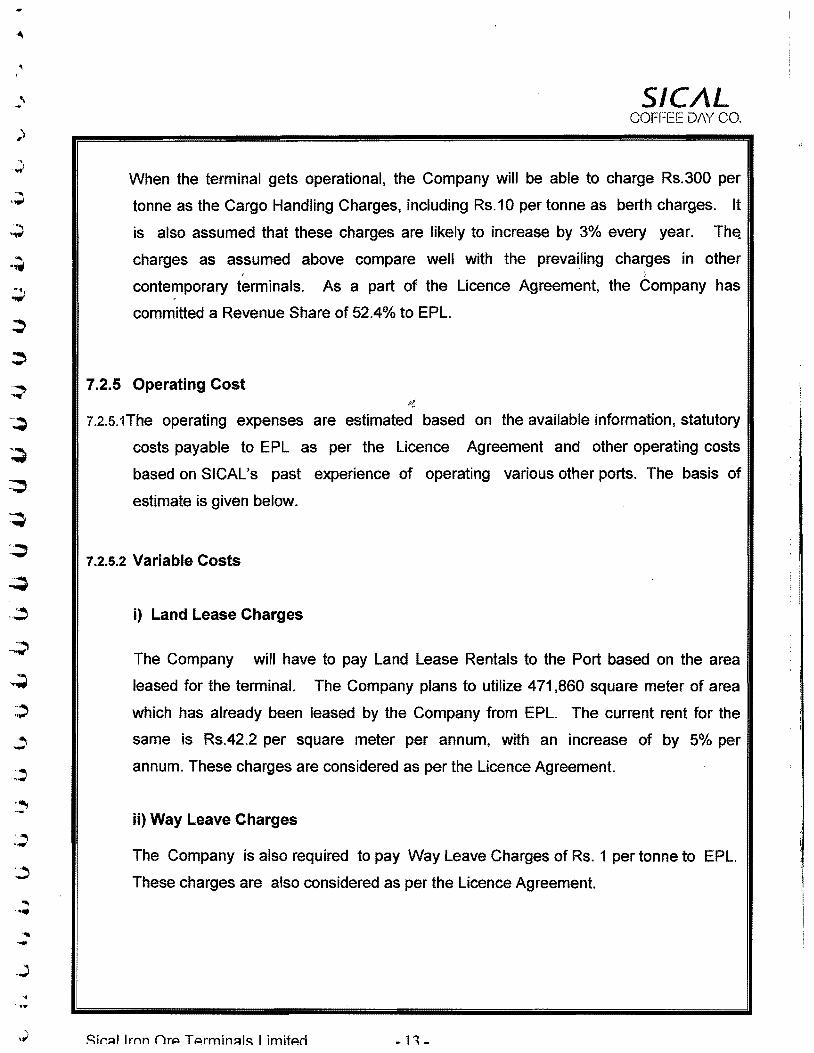

When the terminal gets operational, the Company will be able to charge RS.300 per

tonne as the Cargo Handling Charges, including Rs.10 per tonne as berth charges. It

is also assumed that these charges are likely to increase by 3% every year. The.

charges as assumed above compare well with the prevai.ling charges in other )

contemporary terminals. As a part of the Licence Agreement, the Company has

committed a Revenue Share of 52.4% to EPL.

7.2.5 Operating Cost

7.2.5.1The operating expenses are estimated based on the available information, statutory

costs payable to EPL as per the Licence Agreement and other operating costs

based on SICAL's past experience of operating various other ports. The basis of

estimate is given below.

7.2.5.2 Variable Costs

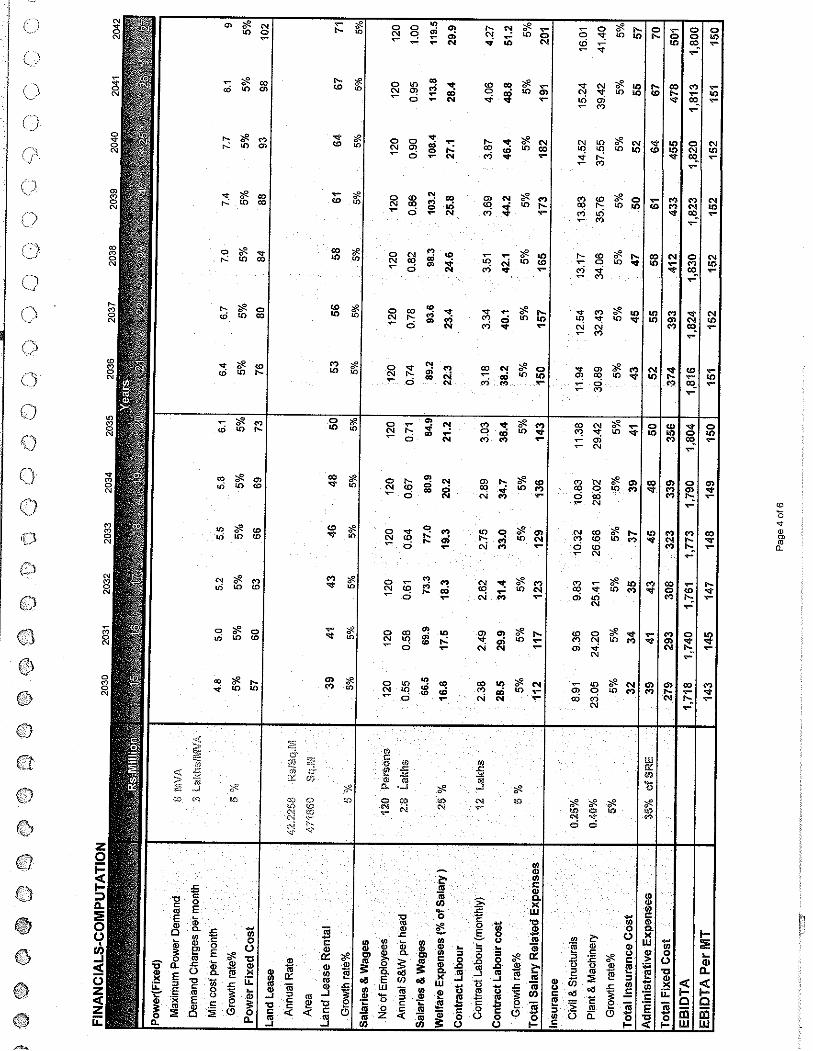

i) Land Lease Charges

The Company will have to pay Land Lease Rentals to the Port based on the area

leased for the terminal. The Company plans to utilize 471,860 square meter of area

which has already been leased by the Company from EPL. The current rent for the

same is RS.42.2 per square meter per annum, with an increase of by 5% per

annum. These charges are considered as per the Licence Agreement.

ii) Way Leave Charges

The Company is also required to pay Way Leave Charges of Rs. 1 per tonne to EPL.

These charges are also considered as per the Licence Agreement.

,.-

~ir.~llrnn ()rA TArmin~l~ I imitAri - n

.~

.:)

.~

~

~

~

~

=:J

~

-,.:,

-~

.~

:~

~

:.~

""I.....

. ""

SICAL COFFEE DAY Co.

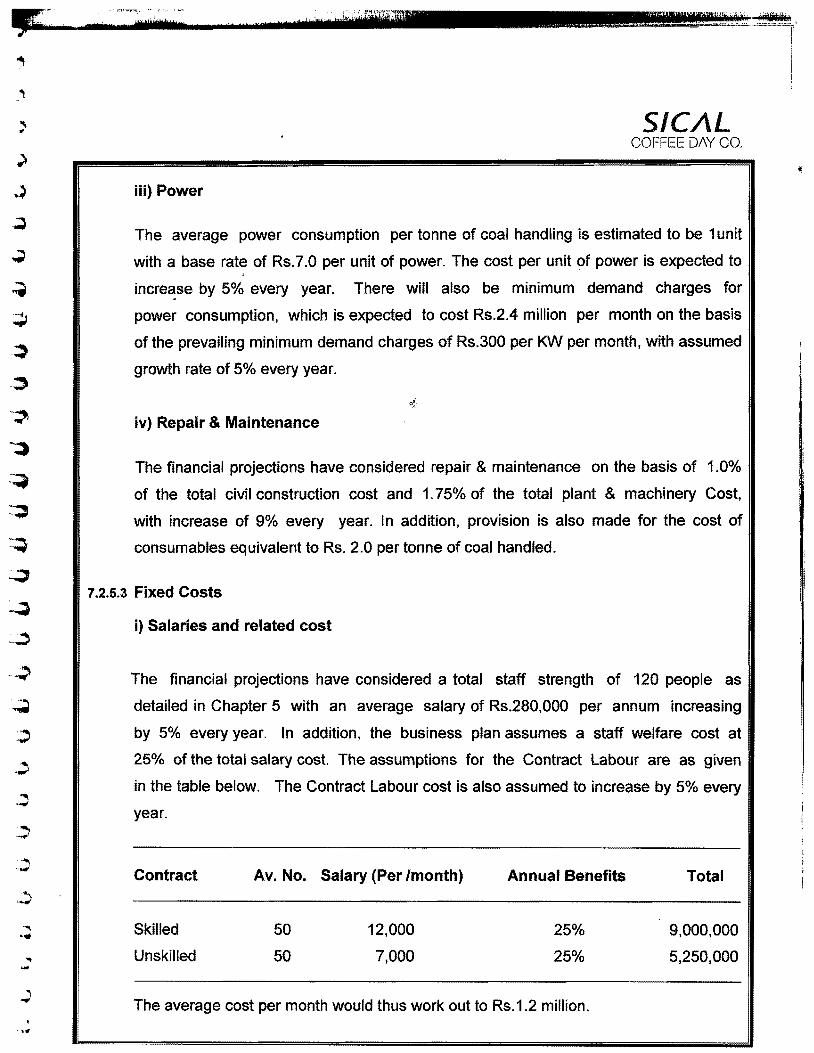

iii) Power

The average power consumption per tonne of coal handling is estimated to be 1 unit

with a base rate of RS.7.0 per unit of power. The cost per unit of power is expected to

incre~se by 5% every year. There will also be minimum demand charges for

power consumption, which is expected to cost RS.2.4 million per month on the basis

of the prevailing minimum demand charges of RS.300 per KW per month, with assumed

growth rate of 5% every year.

iv) Repair & Maintenance

The financial projections have considered repair & maintenance on the basis of 1.0%

of the total civil construction cost and 1.75% of the total plant & machinery Cost,

with increase of 9% every year. In addition, provision is also made for the cost of

consumables equivalent to Rs. 2.0 per tonne of coal handled.

7.2.5.3 Fixed Costs

i) Salaries and related cost

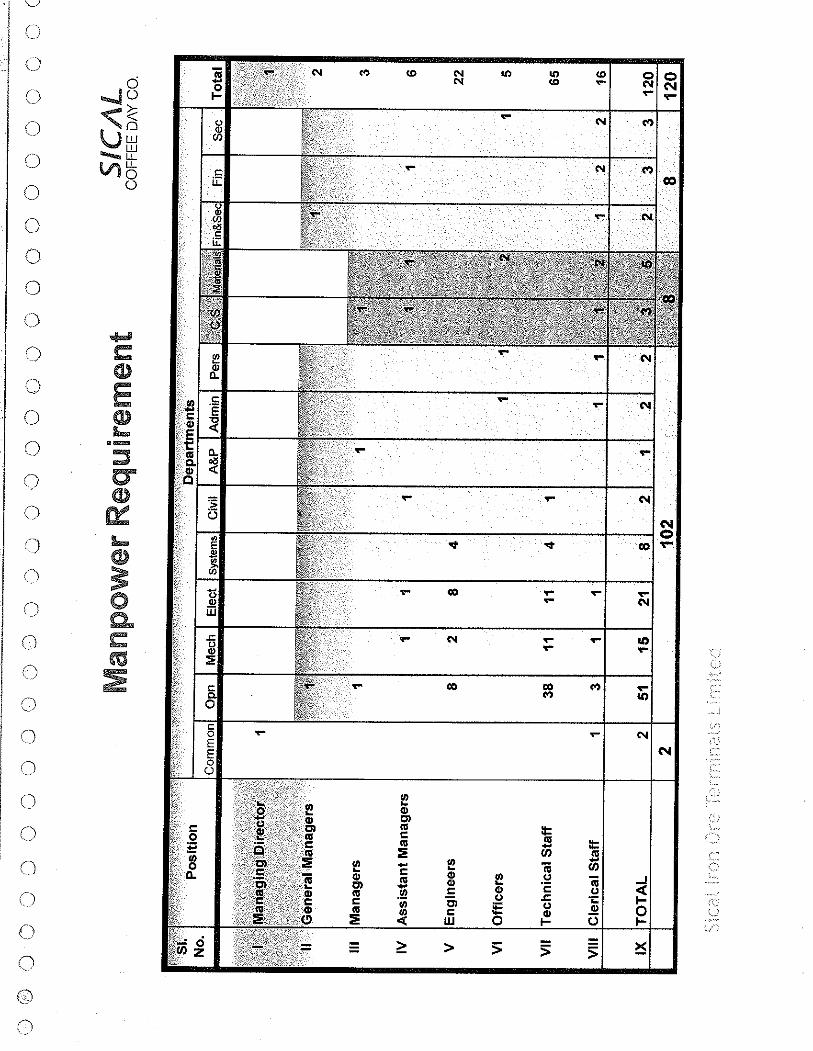

The financial prOjections have considered a total staff strength of 120 people as

detailed in Chapter 5 with an average salary of Rs.280,000 per annum increasing

by 5% every year. In addition, the business plan assumes a staff welfare cost at

25% of the total salary cost. The assumptions for the Contract Labour are as given

in the table below. The Contract Labour cost is also assumed to increase by 5% every

year.

Contract Av. No. Salary (Per Imonth) Annual Benefits

Skilled 50 12,000 25%

Unskilled 50 7,000 25%

The average cost per month would thus work out to RS.1.2 million .

Total

9,000,000

5,250,000

'.1' .'

SICAL COFFEE DAY Co.

ii) Insurance

The financial projections have considered insurance cost on Civi.l Works as well as

Plant &. Machinery. The annual premium of insurance for Industrial All Risk Policy

(IAR), covering Fire, Machinery Break Down (MBD), Fire Loss of Profit (FLOP), Loss of

Profit on Machinery Break Down (LOP), Public Liability etc computed based on the

quotes works out to 0.25% on Civi.l Cost and 0.40% on Plant & Machinery.

iii) Administration Overheads

A provision of 35% of Salaries & Wages cost is made towards Administrative

Overheads as per the break up given in the table attached in this section. An increase

of 5% is considered every year.

7.2.6 Working Capital

It is assumed that the working capital requirement of the business would be met by

availing working capital facility from a Bank .. The interest cost has been assumed at

14% p.a. on the basis of prevailing rates. The working capital requirement would

be for meeting one month operating expenses (excluding revenue share to EPL)

and one year Land Lease Rentals (as per Licence Agreement, annual land lease

charges to be paid to EPL in advance). , I

The working capital requirement will increase with the increase in the quantity handled.

Working capital requirement would be Rs.46 million during first year of operations.

7 .2. 7 Depreciation

Depreciation

7.2.8 Tax

Corporate Tax

income tax

7.3.0

SICAL COFFEE DAY CO.

The

on the total capital cost has been considered on the basis of

following standard norms.

i). CiviJ & Structurals : 3.34% p.a

ii). Plant & Machinery : 5.28 % p.a

rate has been computed at 33% and MAT at 21%, after considering

the surcharge and education cess as per the existing norms.. The project is eligible for

benefit under 80-IA for a period of continuous 10 years in a block of

15 years from COD by virtue of being an infrastructure development project.

financial model has accordingly captured this benefit.

Financial WO,rkings

Detailed Financial Workings made for the total duration of licence Period are given in

the attached statements in the following order.

1. Basis for Financial Projections

2. Financial Projections

3. Cash Flow

•-. 4. Sensitivity Analysis

"

'"

Ric~llron OrA TArmin~l~ I imit.:::>n

I

. " !' l' I' I I I I J . , •i

"L' .. '• ~ _ • _ _ ~ W ~ ~ • ~ ~ ~ ~ U U ~ ~ ~ ij u '- ".. v

~

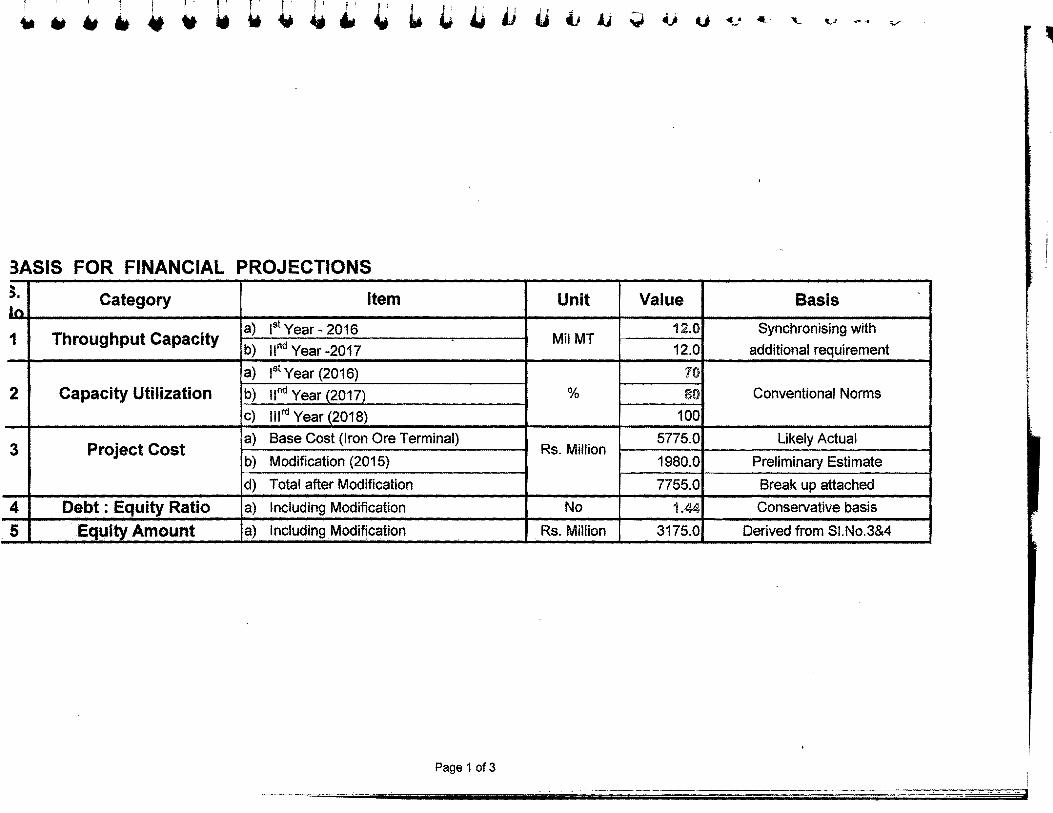

3ASIS FOR FINANCIAL PROJECTIONS .. ). CategoryIn

Item Unit Value Basis

1 Throughput Capacity a) 1st Year - 2016

MilMT 12.0 Synchronising with

b) lind Year -2017 12.0 additional requirement

a) 1st Year (2016) 70 2 Capacity Utilization b) lind Year (2017) % SO Conventional Norms

c) IIIrd Year (2018) 100

3 Project Cost a) Base Cost (Iron Ore Terminal) 5775.0 Likely Actual

Rs. Million b) Modification (2015) 1980.0 Preliminary Estimate

d) Total after Modification 7755.0 Break up attached

4 Debt: Equity Ratio a) Including Modification No 1.44 Conservative basis

5 Equity Amount a) Including Modification Rs. Million 3175.0 Derived from SI.No.3&4

Page 1 of3

,~~,---

.-~-.--~... = -~---.

f: f)" , J ,r I' Jf If 'I r, If 11 if If "

iJ (j 4J L u V U u \I 4.i &" .., U ~ ~ V ~ ~ ~ ~ U U ~ ~ ~ L L '.... v .I v

't,

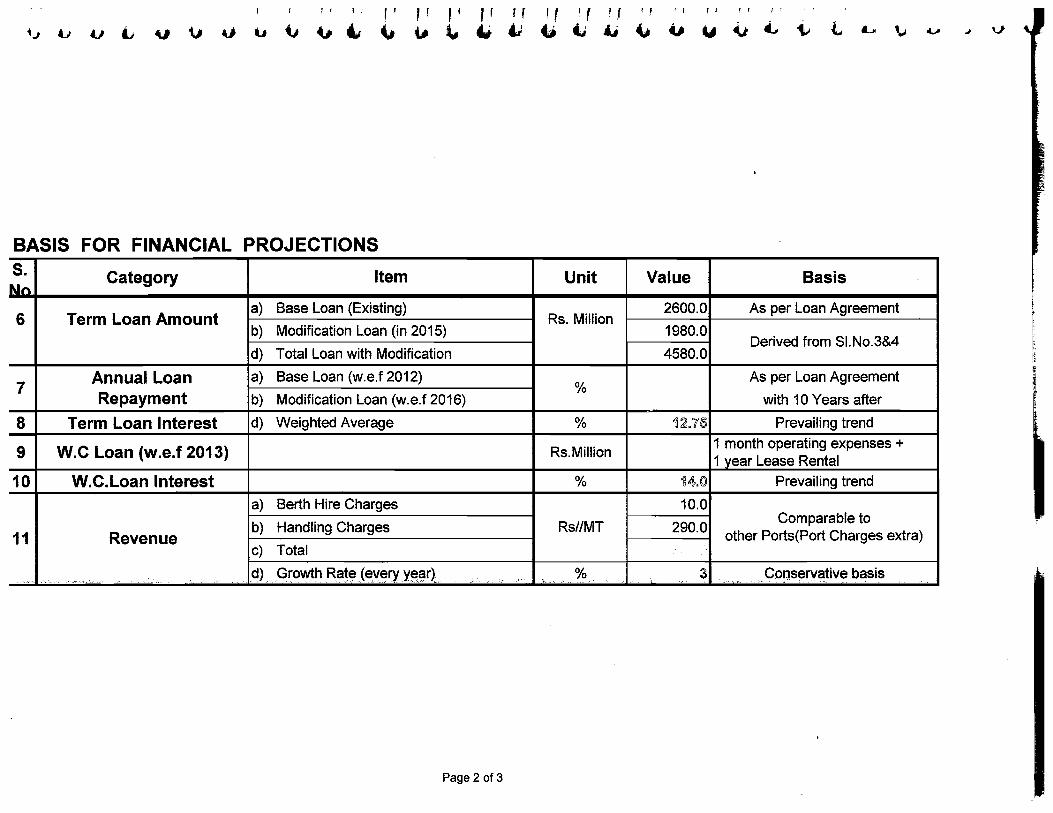

BASIS FOR FINANCIAL PROJECTIONS S. Category Item Unit Value BasisNn

6 Term Loan Amount a) Base Loan (Existing) 2600.0 As per Loan Agreement

Rs. Million b) Modification Loan (in 2015) 1980.0

Derived from SI.No.3&4 d) Total Loan with Modification 4580.0

7 Annual Loan a) Base Loan (w.e.f 2012)

% As per Loan Agreement

Repayment b) Modification Loan (w.e.f 2016) with 10 Years after

8 Term Loan Interest d) Weighted Average % 12.15 Prevailing trend

9 W.C Loan (w.e.f 2013) Rs.Million 1 month operating expenses + 1 year Lease Rental

10 W.C.Loan Interest % 14.01 Prevailing trend

a) Berth Hire Charges 10.0

b) Handling Charges RslIMT 290.0 Comparable to

11 Revenue other Ports(Port Charges extra) c) Total

",'" d) Growth Rate (every year) % 3 COllservative basis

,< c. . .,", ,_'.. ' ... ;. '0 "_:._ "., ..."... ',,>..' "0_ JL ' ,

Page 2 of 3

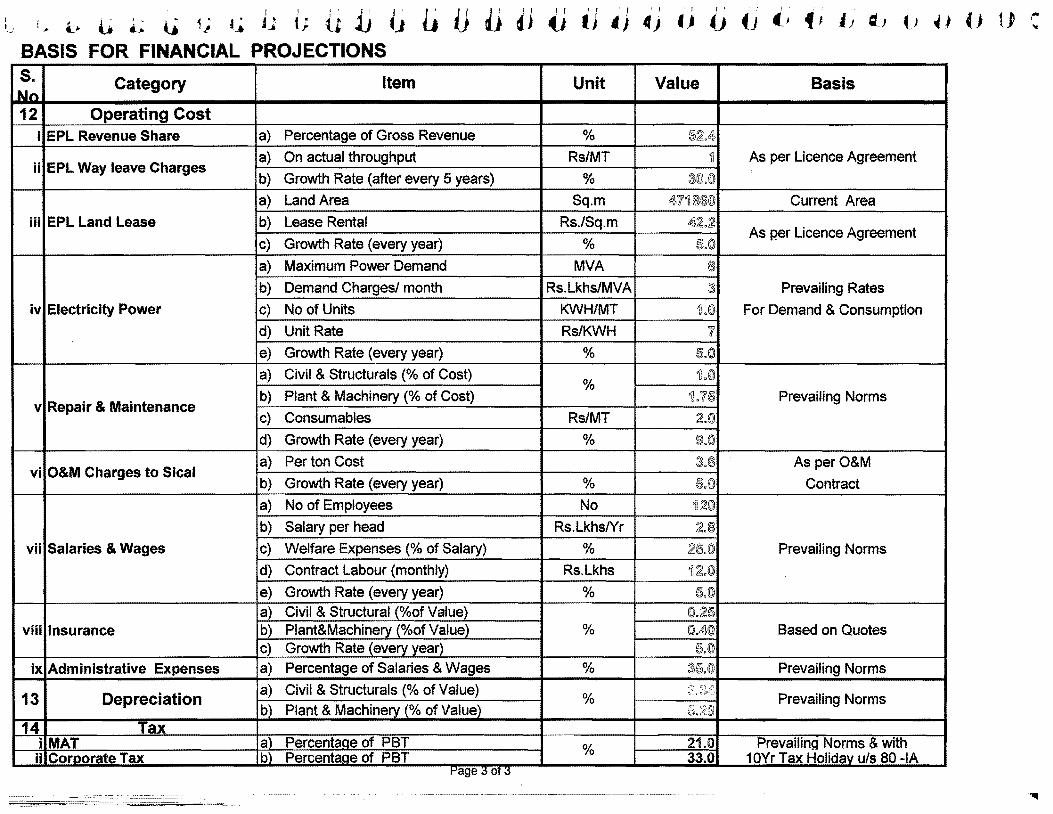

i,j i .. L~ L .; It 1; !~ '1 i; U iJ (J (j U 0 J) (J (J .; 4') ,J (J .J f,1 i I iJ ~) (J ~) (J tJ ~ BASIS FOR FINANCIAL PROJECTIONS s. Nn

Category Item Unit Value Basis

12 Operating Cost i EPL Revenue Share a) Percentage of Gross Revenue % l'iitt~

As per Licence Agreement Iii EPL Way leave Charges

a) On actual throughput Rs/MT ~

b) Growth Rate (after every 5 years) % 3(Ql.(Ql

iii EPL Land Lease

a) Land Area Sq.m &1)'1~1ilJ®(Ql Current Area

b) Lease Rental Rs./Sq.m &1)~.~ As Rer Licence Agreement

c) Growth Rate (every year) % @,(Ql

iv Electricity Power

a) Maximum Power Demand MVA ~

Prevailing Rates

For Demand & Consumption

b) Demand Chargesl month RS.Lkhs/MVA 3 c) No of Units KWH/MT VI» d) Unit Rate Rs/KWH '1

e) Growth Rate (every year) % (5,(Ql

v Repair & Maintenance

a) Civil & Structurals (% of Cost) %

~,(Ql

Prevailing Norms b) Plant & Machinery (% of Cost) 'L115

c) Consumables Rs/MT 2.(Ql

d) Growth Rate (every year) % ®,(Ql

vi O&M Charges to Sical a) Per ton Cost 3,@ AsperO&M

Contractb) Growth Rate (every year) % (5,(Ql

vii Salaries &Wages

a) No of Employees No 1~(Ql

Prevailing Norms

b) Salary per head RS.LkhslYr 2,~

c) Welfare Expenses (% of Salary) % 215.(Ql

d) Contract Labour (monthly) RS.Lkhs 12,(Ql

e) Growth Rate (every year) % @,(Ql

viii Insurance a) Civil & Structural (%of Value)

% (Ql,2~

Sased on Quotesb) Plant&Machinery (%of Value) (Ql,&1)(Ql

c) Growth Rate (every year) 15,(Ql

ix Administrative Expenses a) Percentage of Salaries & Wages % 3@,(!)) Prevailing Norms

13 Depreciation a) Civil & Structurals (% of Value)

% {~, ::£,l:i.

Prevailing Norms b) Plant & Machinery (% of Value) @.28

14 Tax i MAT a) Percentage of PST % 21.0 Prevailing Norms & with

10Yr Tax Holidav u/s 80 -IA ii Coroorate Tax b) Percentage of PST -- 33.0 .....9

-- '111