Embed Size (px)

Citation preview

11/30/2009

Live Case Study

Homam Alattar; Anthony Ragoo; Nader Taghavi; Ramla Nur; Yazen Alkodmani; and Zabiha Zabih

BUSI 4510: M&A ACQUISITION TEAM PROJECT

Acquisition Team Project Disney + Marvel

ii

DISCLAIMER This report was created by students enrolled in the “Mergers & Acquisitions” corporate finance course instructed by Dr. Isaac Otchere at the Sprott School of Business, Carleton University. The intent of this project is to give students the opportunity to apply learned tools by analyzing a merger and acquisition event, real or hypothetical. This involves the preparation of a business plan followed by an acquisition plan. The report reflects the sole opinion of its authors and is by no means a solicitation for action or a reliable source of information. Unless otherwise noted, facts and figures included in this report are from publically available sources. This report is not a complete compilation of data and its accuracy is not guaranteed. Unless otherwise noted, dollar amounts are in USD.

ASSESSMENT OF THE PROJECT Your feedback is greatly appreciated.

Criteria Marks & Comments

1. Completeness:

How well did the team address each point on the syllabus outline for the project?

out of 30%

2. Quality of Application:

Did the team apply correctly the tools and concepts learned in this course?

HINT – Each team member should apply a number of different tools and concepts in each section for which they are responsible.

out of 30%

3. Creativity:

Did the team specify clearly the acquirer’s and the target’s objectives and needs?

Did the team address common deal structuring questions?

How successful was the team in meeting the highest priority needs of both parties?

Was the proposed deal structure realistic?

out of 30%

4. Presentation

out of 10%

Total out of 100%

Acquisition Team Project Disney + Marvel

iii

ACQUISITION TEAM

HOMAM ALATTAR Business plan – Industry definition; Internal Analysis: strengths and weaknesses; SWOT

Matrix; DCF valuations/pro forma financials; and risk assessment. Acquisition plan – resource evaluation; initial price; and negotiation strategy: deal

structure. Executive summary; epilogue; and final editing and quality control. Template design and formatting.

ANTHONY RAGOO Business plan – Intro, mission/vision, Business Strategy and implementation. Acquisition plan – Search plan; Negotiation strategy: Buyer/Seller Issues.

NADER TAGHAVI Business plan – relative valuation. Acquisition plan – relative valuation; and financing plan.

RAMLA NUR Business plan – Industry definition; Opportunities & Threats. Acquisition plan – Search plan; and integration plan

YAZEN ALKODMANI Business plan – quantified strategic objectives. Acquisition plan – time table

ZABIHA ZABIH

Business plan – External analysis Acquisition plan – plan objectives; and management preferences.

Acquisition Team Project Disney + Marvel

iv

TABLE OF CONTENTS

1. Quick Facts ............................................................................................................................................ 1

2. Executive Summary ............................................................................................................................... 2

3. Business Plan ......................................................................................................................................... 4

3.1. Industry and Market Definition .................................................................................................................... 4

3.2. External Analysis (Porter’s Five Forces)........................................................................................................ 5

3.3. Internal Analysis ........................................................................................................................................... 7

3.4. External Environment................................................................................................................................. 10

3.5. Business Mission and Vision ....................................................................................................................... 11

3.6. Quantified Strategic Objectives ................................................................................................................. 12

3.7. Business strategy ........................................................................................................................................ 13

3.8. Implementation Strategy ........................................................................................................................... 14

3.9. Business Plan Financials and Valuation ...................................................................................................... 15

3.10. Risk Assessment ......................................................................................................................................... 16

4. Acquisition Plan ................................................................................................................................... 18

4.1. Plan objectives ........................................................................................................................................... 18

4.2. Timetable ................................................................................................................................................... 18

4.3. Resource Evaluation ................................................................................................................................... 19

4.4. Management Preferences .......................................................................................................................... 20

4.5. Search Plan ................................................................................................................................................. 20

4.6. Negotiation Strategy .................................................................................................................................. 23

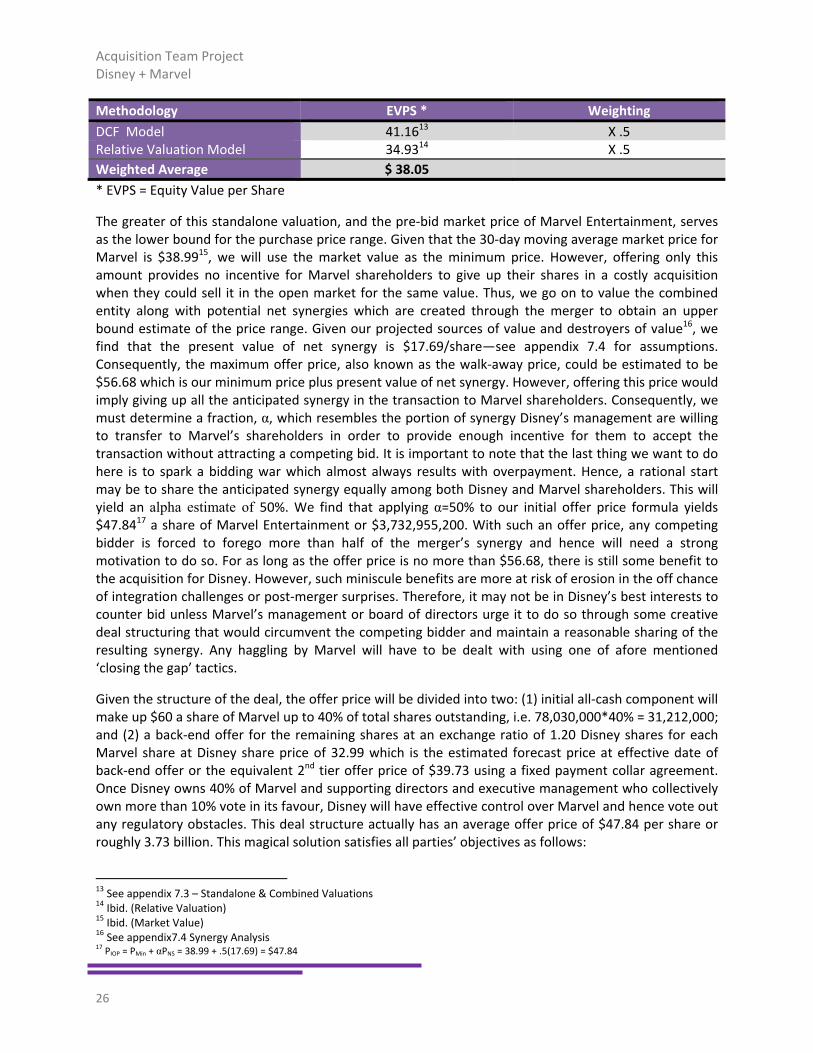

4.7. Initial Offer Price ........................................................................................................................................ 25

4.8. Financing Plan ............................................................................................................................................ 27

4.9. Integration Plan .......................................................................................................................................... 28

5. Epilogue ............................................................................................................................................... 30

6. References .......................................................................................................................................... 32

7. Appendices .......................................................................................................................................... 34

7.1. Industry & Market Exhibits ........................................................................................................................ 34

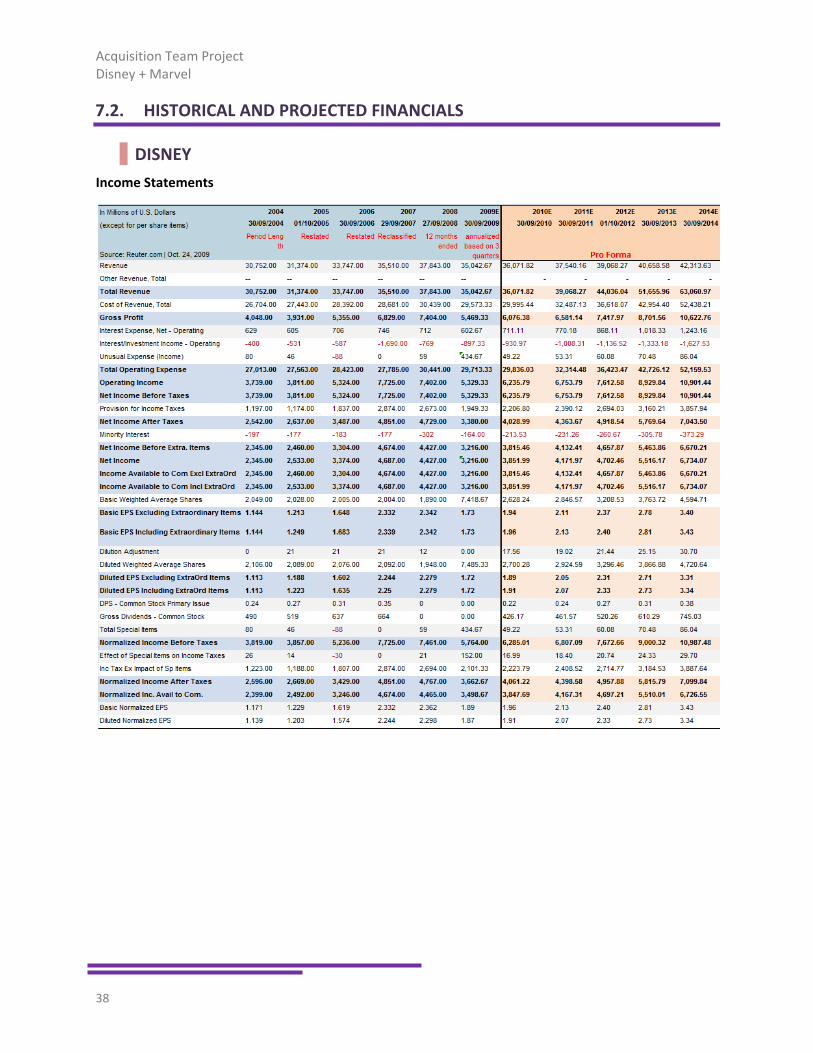

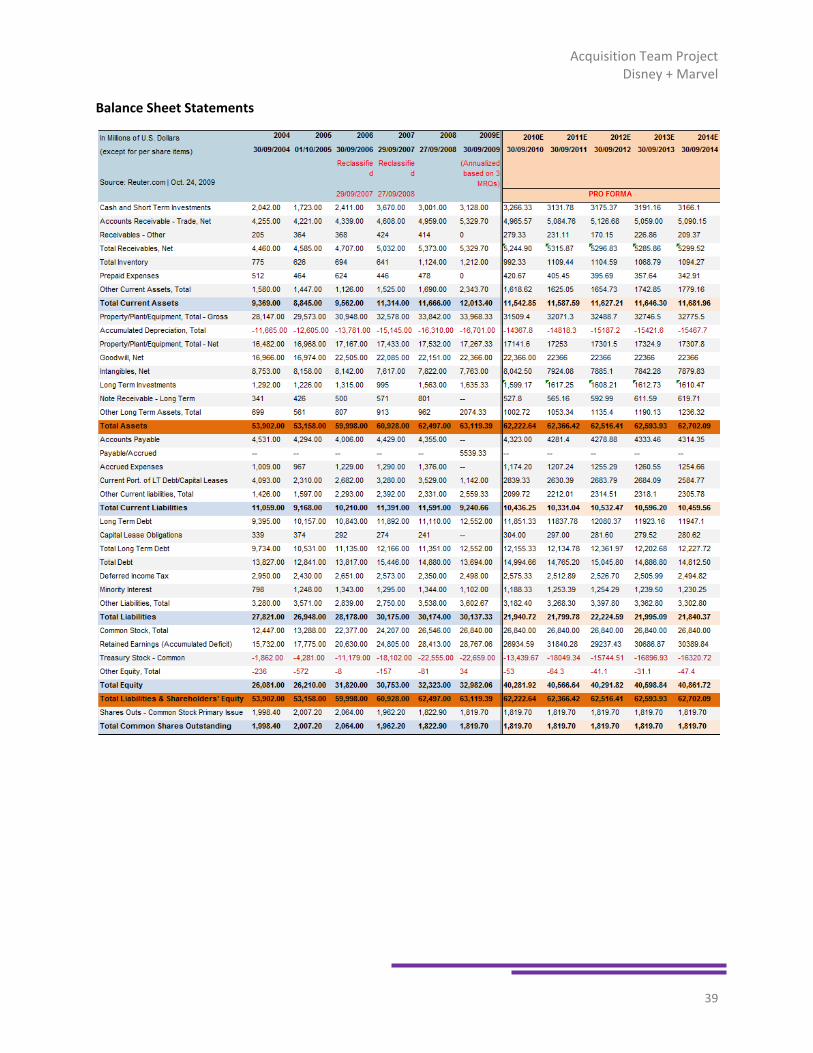

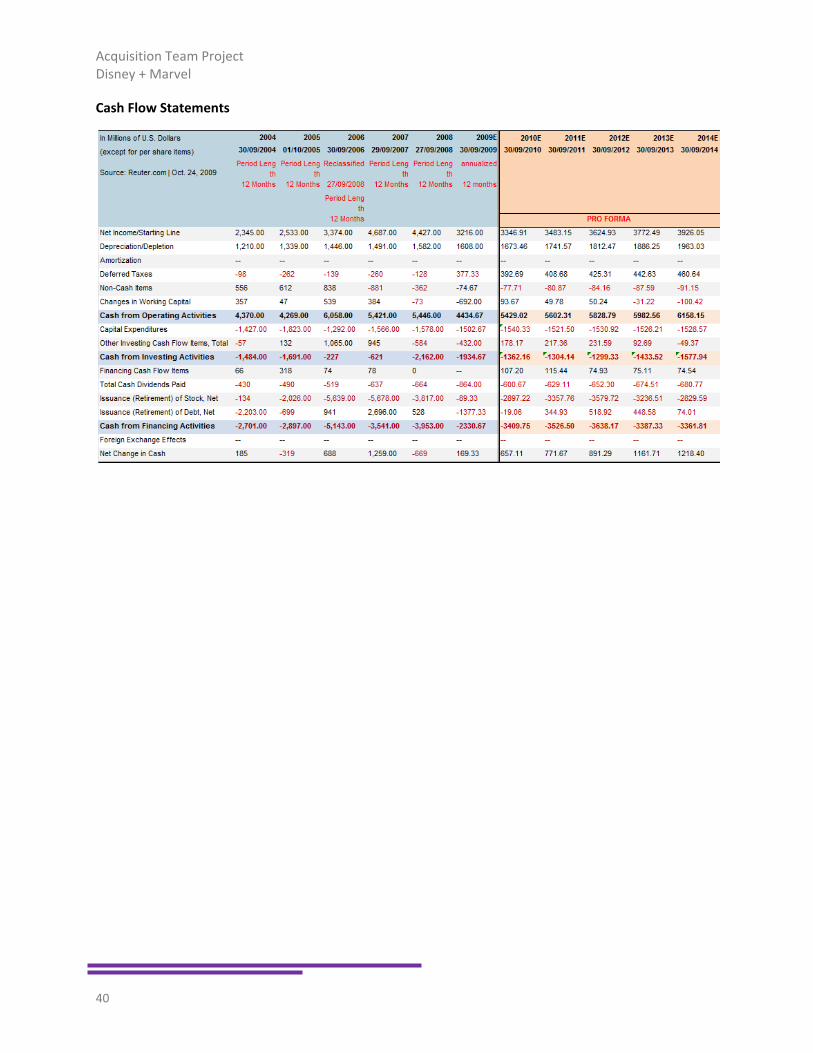

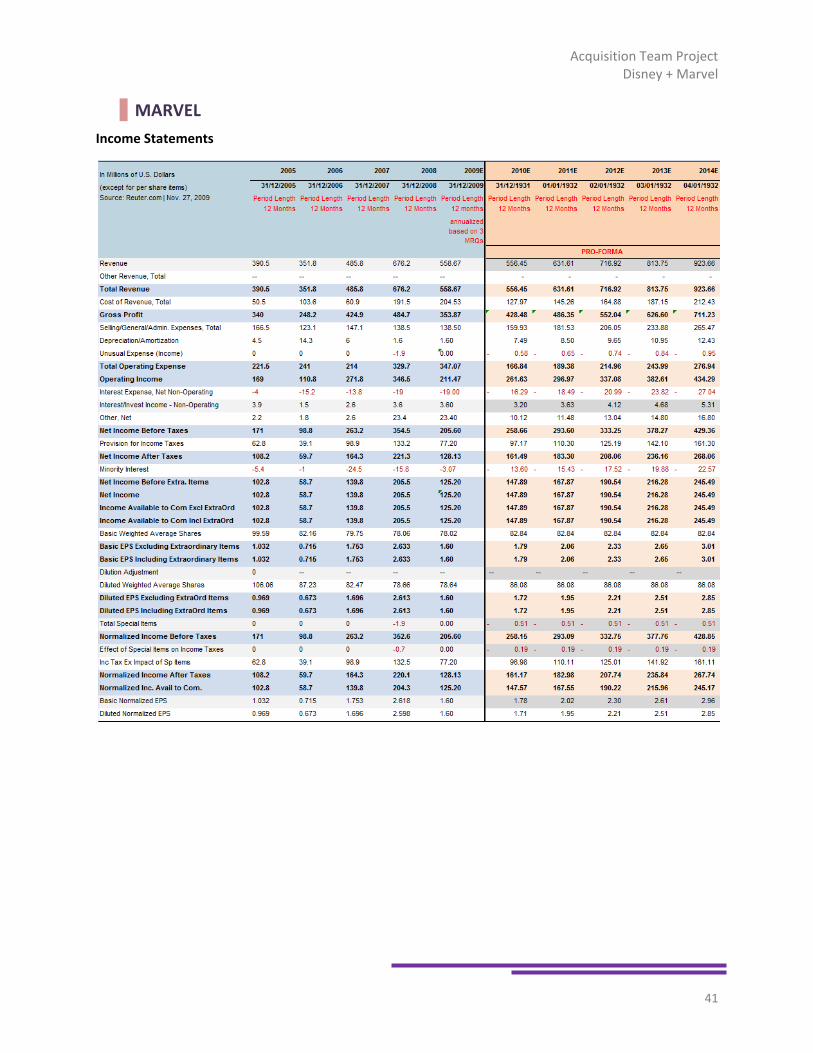

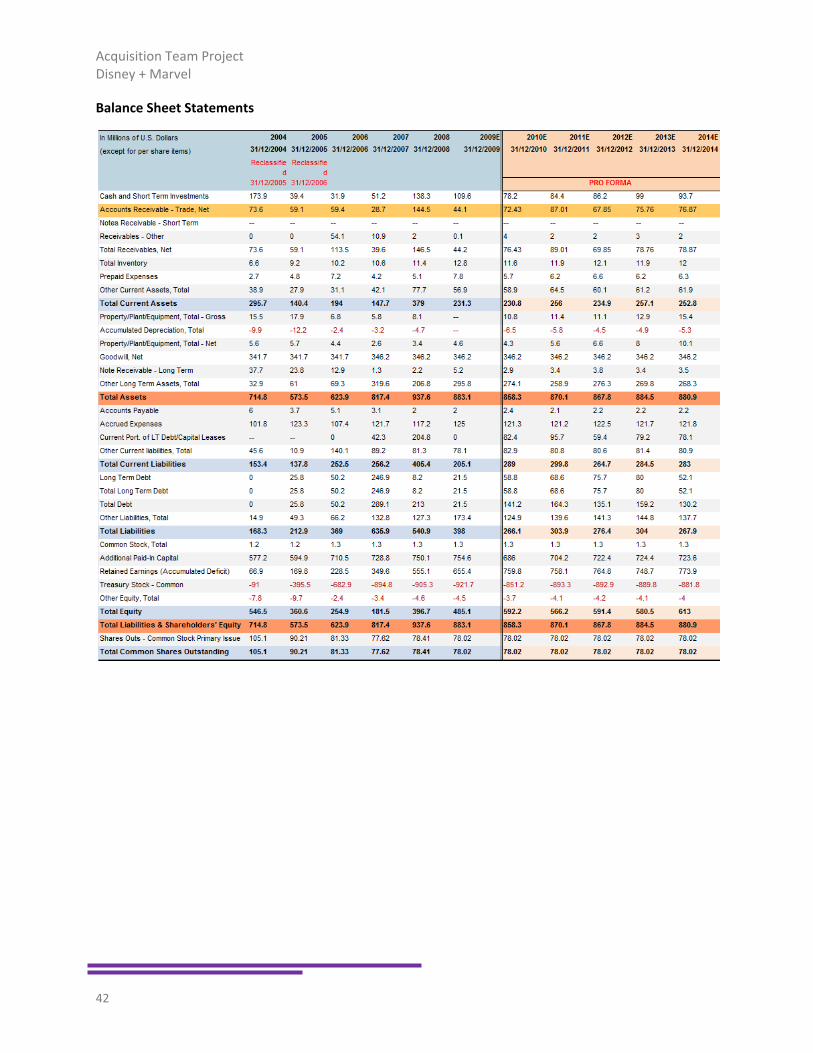

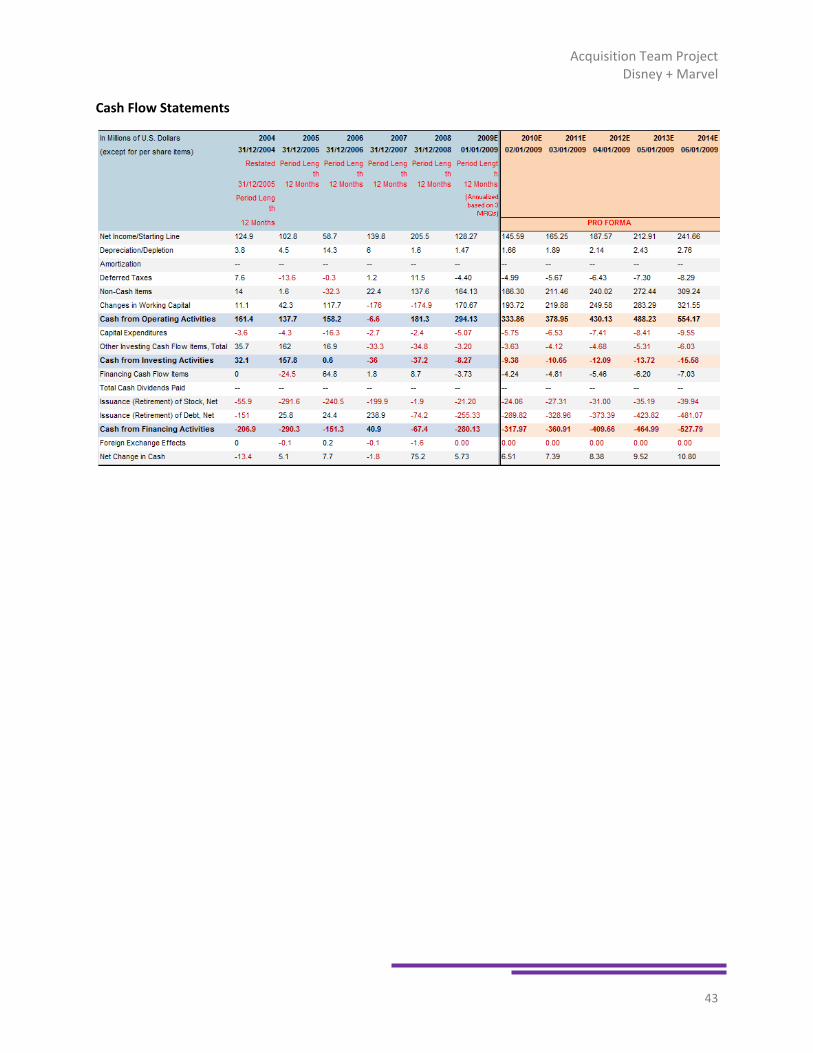

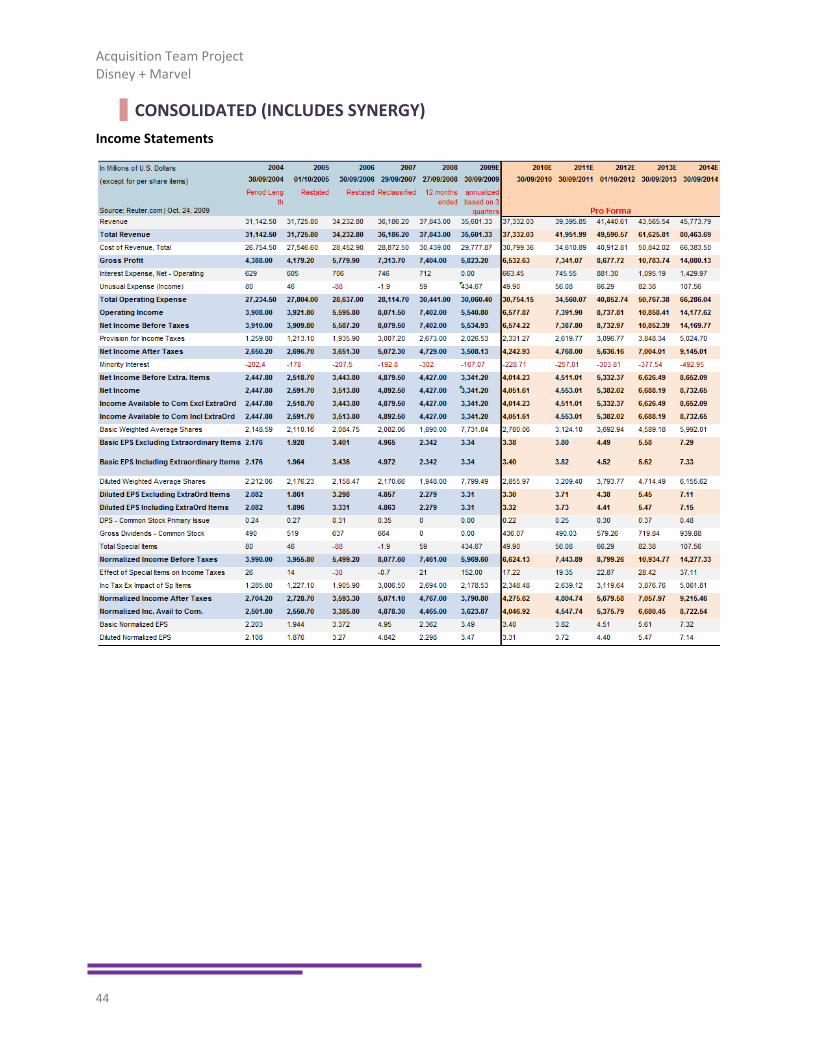

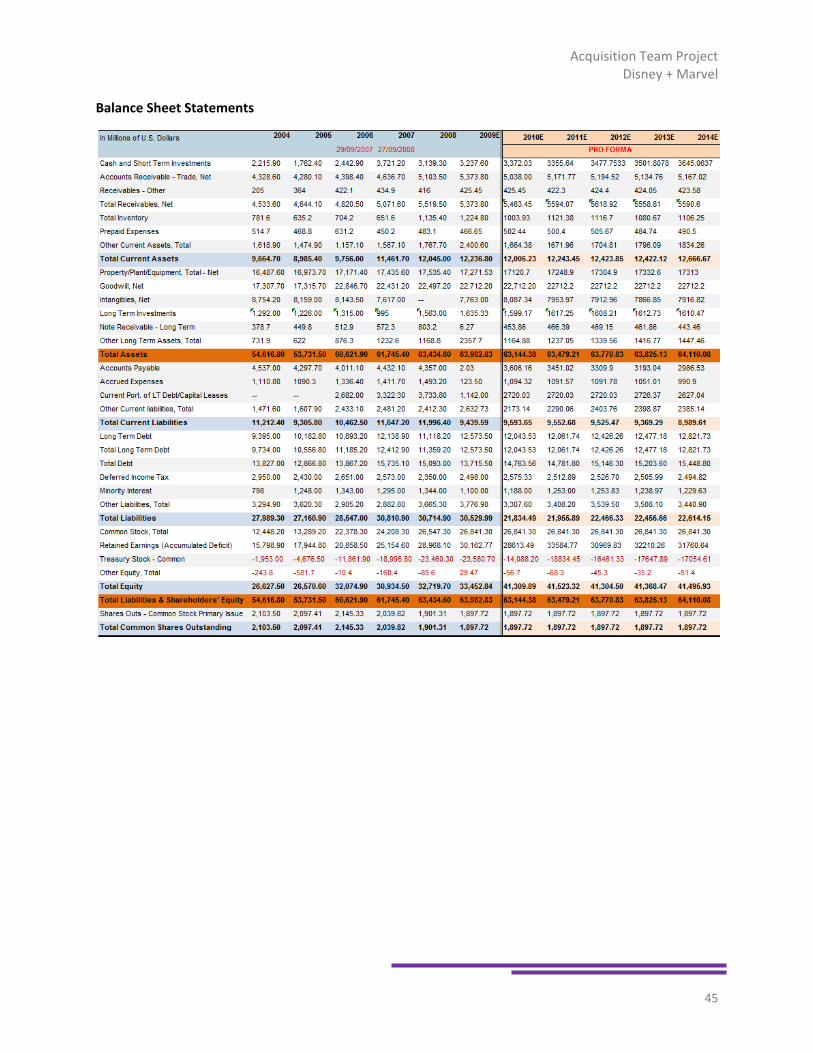

7.2. Historical and Projected Financials ............................................................................................................ 38

7.3. Standalone & Combined Valuations .......................................................................................................... 47

7.4. Synergy Analysis ......................................................................................................................................... 52

7.5. Marvel Shareholdings ................................................................................................................................ 53

7.6. Disney’s Board of Directors and Executive Team ....................................................................................... 54

7.7. Marvel’s Board of Directors and Executive Team ...................................................................................... 55

Acquisition Team Project Disney + Marvel

1

1. QUICK FACTS

Bidder Firm: Walt Disney Corporation

Head Office: 500 South Buena Vista Street,

Burbank, California 91521

Market Capitalization: USD $52.47 Billion

Target Firm: Marvel Entertainment, Inc.

Head Office: 417 5th Avenue,

New York, NY 10016

Market Capitalization: USD $3.04 Billion

Acquisition Team Project Disney + Marvel

2

2. EXECUTIVE SUMMARY

INTRODUCTION

The Walt Disney Company is a globally diversified entertainment company with operations in North America, Europe, Asia Pacific, Latin America and others. Walt Disney is the second largest media and entertainment conglomerate in the world. It is headquartered in the United States, specifically Burbank, California, and employs roughly 150,000 people as at September, 2008. Its Walt Disney Studios produces films through Walt Disney Pictures, Touchstone, Pixar, and Miramax. It also has interests in TV and cable networks, theme parks and resorts, consumer products, and interactive media. Disney distributes and markets filmed products principally through its own distribution and marketing channels in North America. In the international market, Walt Disney distributes filmed products both directly and through independent foreign distribution companies. Disney defines itself as one of the largest media and entertainment conglomerates in the world. It is comprised of five main divisions stretching out operations through all types of media outlets across the world. Walt Disney Studio Entertainment manages all motion pictures and music productions as all corresponding merchandizing is handled by Disney Consumer Products. Holiday resorts and theme parks are administered by Walt Disney Parks and Resorts which was once the most profitable sector of the Disney Company until 1996 where Disney Media Networks, a compilation of numerous television‐broadcast stations, prevailed with higher revenues. Finally there is the Disney Interactive Media Group that deals with various internet websites. Collectively, these divisions have pulled in over 37 billion US dollars in revenue in FYE 2008. The company has proven to be a prosperous corporation with continuous growth since 1923 up until today. In 2008, Disney’s annual reports showed a net income of $4,427 million dollars and an annual growth rate of 6.6%. In the stock market, Disney is selling over 13,627,900 shares on the New York Stock Exchange with a 52 week range between $15.14 and $32.59 as at Nov. 30, 2009. Within the industry of entertainment conglomerates, Disney’s major competitors are CBS Corp, News Corp, and of course the largest entertainment conglomerate in the world, Time Warner.

HISTORY

The company was founded in 1923 by Walt and Roy Disney as the Disney Brothers Studio in Hollywood, California. It released its first cartoon, i.e. “Plane Crazy”, which was directed by Walt Disney in 1928. The studio released its first animated feature film, i.e. “Snow White and the Seven Dwarves”, in 1937. The company went public in 1944. Disneyland Theme Park was opened in 1955 and later Disney World opened in Florida in 1971. In 1984, the Bass family of Texas acquired a controlling interest in alliance with the Disney brothers. Through the 1980’s the company launched the Disney Channel and opened a theme park in Tokyo, Japan. In 1985, the company acquired Disney MGM studio, and a year later, changed its name to “The Walt Disney Company”. In 1992, Disneyland Paris was opened in France substantiating Disney’s continued international expansion. In 1996, the company acquired Capital Cities/ABC for $19 billion which included 10 TV stations, 21 radio stations, seven daily news papers, and ownership positions in cable networks such as A&E, Lifetime, History Channel, and the powerhouse sports network, ESPN.

FUTURE

Disney’s future is full of Pixar’s 3D animations featuring Marvel superheroes, awesome video games for the boys’ long neglected (by Disney) market segment, all‐new Marvel rides and attractions at Disney’s theme parks, and much more on TV and the internet.

Acquisition Team Project Disney + Marvel

3

PROPOSAL

In Disney’s pursuit to be the global leader in producing and providing entertainment and information through growth and differentiation, Marvel appears to have some major contributions. Those contributions look just as attractive from Marvel’s point of view. Using Disney’s proven strengths in the entertainment and media industry and in an attempt to curb the feisty competition, Disney appears to be the perfect home for Marvel’s 5000+ characters and original stories. Indeed, Disney is unparalleled when it comes to highly differentiated, top quality, and globally renowned brands and intellectual properties. By having a two‐tiered staged acquisition that maximizes the benefits for all parties involved, Marvel could be tucked‐into Disney’s global portfolio of intellectual pioneers and quality brands with little integration and full rewards.

SYNERGIES

Both companies will benefit the most from Disney’s broad and sophisticated marketing resources and distribution channels allowing Marvel to access foreign markets and allowing Disney to compete in those markets more fiercely. We believe that it was Marvel’s people who are the greatest asset in this acquisition. They will all remain at Marvel and will help guide us best integrate Marvel into other business segments such as theme parks, interactive media / gaming, media networks, and consumer products. We are looking forward to see the results of this marriage in some truly exciting new products and services.

CONCLUSION

Disney’s acquisition is partially based on a true event, but some acquisition assumptions have been manipulated to create a challenging case for this study report. Our final result was an average offer price of $47.84 per share of Marvel in a two‐tiered acquisition and a holding company structure with Disney acquiring all outstanding shares of Marvel in two stages. The post merger Disney share price is estimated to go as high as $36 per share in 12 months from the consummation of the transaction. Despite potential challenges inherent in pre‐existing Marvel rights and licensing agreements with Disney competitors which may lead to protracted lawsuits in the worst case scenario, we are sure that Disney will have the last laugh in the end and many synergies delayed for some time will be realized sooner or later. In fact, there are so many advantageous that they outweigh those inherent challenges. The integration plan is minimal and extended over a long period of time to substantiate the amount of revenue and cost savings sources which will be achieved without the need to substantial integration among the operations of the two companies. This, per se, reflects on Disney’s achieved objectives in Marvel’s acquisition which follow the ‘hands‐off’ approach of buying well established companies that are self‐reliant and which can benefit from Disney’s wide range of resources and infrastructural support with minimum interference. This report will cover a top‐down market analysis laid out in a business plan followed by an acquisition plan with details that include: objectives, timetable, management preferences, available resources, search plan, negotiations strategies, deal structuring, initial price determination, financing, and integration plan by function.

Acquisition Team Project Disney + Marvel

4

3. BUSINESS PLAN

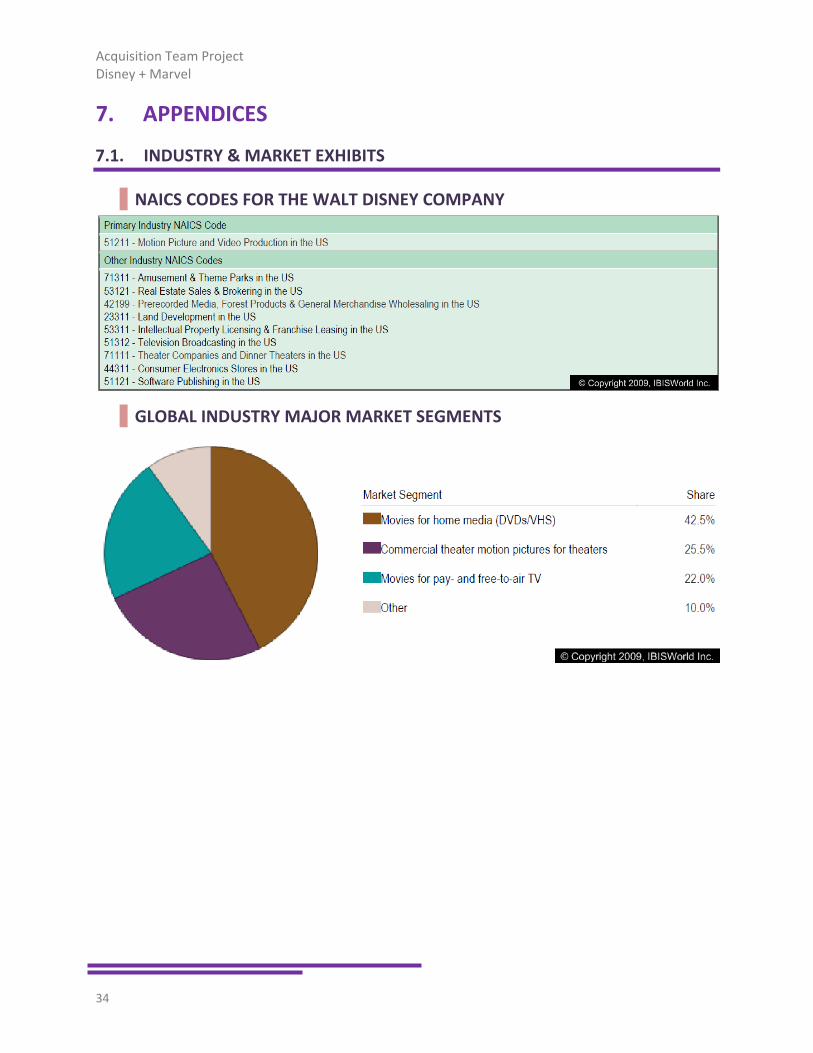

3.1. INDUSTRY AND MARKET DEFINITION

The Walt Disney Company operates in the global entertainment industry through five major business segments: Media Networks; Parks and Resorts; Entertainment Studios; Consumer Products; and Interactive Media. Walt Disney’s primary industry is considered to be Motion Pictures and Video Production which corresponds to the North American Industry Classification Standards code of 51211 (see NAICS codes in appendix). However, the company’s large scale of operations involves other industries including: Amusement and Theme Parks; Real Estate Sales & Brokering; Pre‐recorded Media; Land Development; Intellectual Property Licensing & Franchise Leasing; Television Broadcasting; Consumer Electronics Stores; and Software Publishing. The global entertainment industry is characterized by strong vertical integration especially in the major market of the United States. For example, the major movie producers and distributors ‐ Fox, Time Warner, Sony, Universal, Paramount, and Disney ‐ and the American broadcast networks ‐ CBS, NBC, ABC, FOX and WB ‐ have the same parent companies. This is replicated in Europe with Vivendi (part owner of NBC Universal) owning Canal Group and pay‐TV group.

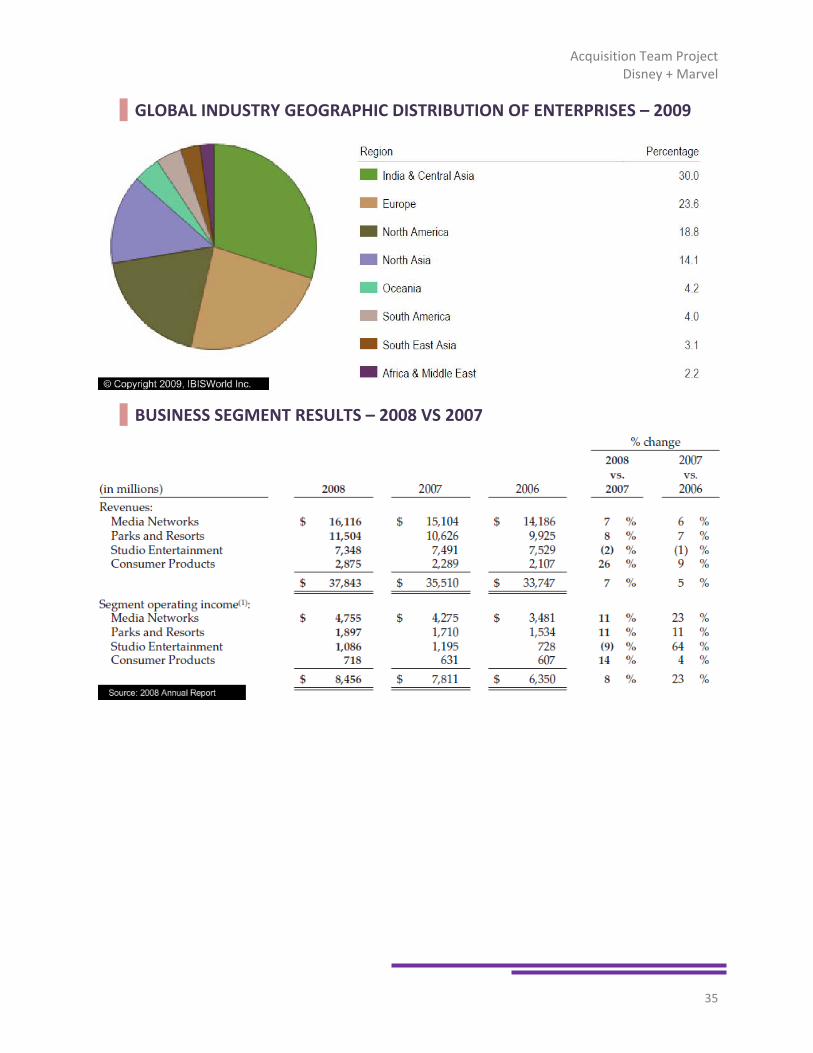

The global movie production and distribution industry is comprised of establishments primarily engaged in producing, or producing and distributing motion pictures and home media entertainment products, such as DVDs or Blue Rays. Movie producers also hold movie libraries that reap revenue from cable and network TV. The primary activities of this industry are feature movie and long documentary productions. The major products and services are: R‐rated Movies; PG‐rated Movies; PG‐13‐rated Movies; G‐rated Movies; and NC‐17‐rated Movies. In 2008, the industry generated $109,415.2 million in revenues and employed roughly 841,849 people. The industry is still in its growth stage of its life cycle with rates far above those of real GDP growth. Over the five‐year period ending with 2009, the industry revenues experienced growth rates of 12.6%, 10%, 5.9%, ‐1.2%, and ‐2.6% respectively with the negative rates coinciding with the recent economic recession of 2008/2009. However, the industry revenue growth is forecast to turn positive in 2010 with 3.3% followed by 4.3% in 2011. The industry involves three major market segments: movies for home media; commercial theatre motion pictures; movies for pay‐ or free‐to‐air TV; and others (see appendix). The Global Movies Production and Distribution industry is relatively evenly spread around the world and emerging markets are well represented in terms of enterprise numbers―notably India and China (see appendix). The Indian movie industry (also known as Bollywood) is one of the largest and most celebrated in the world and produces more films annually than the United States. Technology has significant influence on the industry's future, with pay‐per‐view and video‐on‐demand likely to have strong penetration of households, together with the use of digital TV and satellite/cable networks. This will open a significant new revenue stream for movie producers, but its growth may be offset by cannibalization of revenues from video stores, retailers, and box office receipts. There is a growing use of computer animation and computer‐generated imagery (CGI) which has produced increasingly realistic visual effects with some correlation between movie budget and box office success.

Acquisition Team Project Disney + Marvel

5

3.2. EXTERNAL ANALYSIS (PORTER’S FIVE FORCES)

CUSTOMERS

Disney’s target market often goes beyond young children to include the decision makers―parents. Hence, the Walt Disney Company markets most of its products and services to families as a whole. Disney’s customers are best described by Walt Disney’s quotes: “We believe in our idea – a family park where parents and children could have fun together”; and “You’re dead if you aim only for kids. Adults are only kids grown up, anyway.”

Since switching costs are relatively low for the entertainment industry, customers have certain power in the industry. However, Disney’s highly differentiated brands and quality products and services have lead to significant customer loyalty and repeat business, i.e. parents who have been to Disney parks and resorts as kids are more likely to take their kids to such parks and resorts. Factors that influence Disney’s ability to reach their customers may have detrimental effects on the company’s market position and profitability.

COMPETITORS

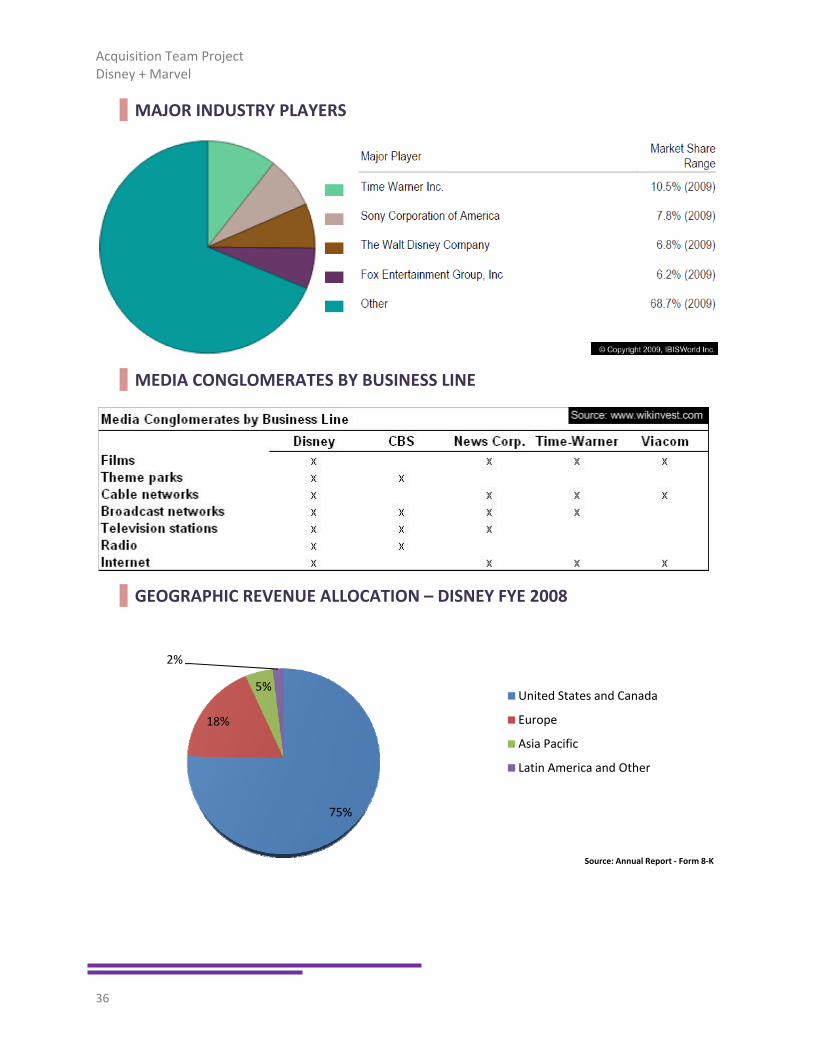

In general, competition in the industry is high and increasing due to the large size of major industry players and the large number of smaller operators. Market concentration is low in the global market but high in North America with the top four players accounting for about 72% of the industry’s total market share in 2009. The North American market constituted 75.3% of Disney’s total revenues in FY2008. There are several key players in the industry1:

Time Warner Inc. It is the world’s largest entertainment conglomerate that operates in cable TV, films,

publishing and some online services. New Line Cinema and Warner Bros are part of its film and TV production companies. To reduce the cost of production, and financial risk Warner Bros is under co‐financing arrangement with other companies, and distributes feature films to over 125 international territories. The film entertainment segment’s major source of revenue comes from the Theatrical Films, TV Licensing, Home Videos, TV Products, and others.

Time Warner Inc. has the highest market share in the global movie production and distribution industry, i.e. 10.5% of the market share in 2009. This is greater than Disney’s 6.8% of market share.

Sony Corporation of America Sony is a leading manufacturer of audio, video, communications and information

technology products for both consumer and professional markets. Sony Corporation of U.S includes Sony Electronics Inc., Sony Pictures Entertainment Inc., Sony Computer Entertainment America Inc., and Sony Music Entertainment. Sony is one of the largest recorded music companies in the world. It had an annual sale of over $88 billion in 2008. Sony Picture entertainment (SPE) is the television and film production unit of Sony Corp. of America. Under SPE operations devoted to Sony Picture TV, Sony Pictures Home Entertainment and Sony Picture Digital. Another distribution unit is Sony Picture Classics (also known as Columbia TriStar Motion Picture Group).

1 See appendix 7.1 – Major Industry Players

Acquisition Team Project Disney + Marvel

6

Sony Corporation of America has 7.8% of the global movie production and distribution industry market share, which is greater than Walt Disney’s market share of 6.8%.

Fox Entertainment Group Inc. It is an American entertainment company that operates through four segments: Film

Entertainment, Television Station, Television Broadcast Network, and Cable Network Programming. The Filmed Entertainment segment comprises live action and animated motion pictures for distribution in all formats in the entertainment media worldwide market. This segment of the company includes such movie studios as Fox 2000, Fox Searchlight, and its flagship imprint Twentieth Century Fox. Fox Entertainment Group Inc. operates as a subsidiary of News Corporation.

The company holds 6.2% of the global industry market share. General Electric

GE is a diversified holding company and manufacturer of various industrial goods and equipment. The company is composed of a number of primary business units each of which is a vast enterprise per se. The list of GE businesses varies over time as the result of acquisitions, divestitures and organizational restructuring. GE has four primary divisions: Technology Infrastructure; Energy Infrastructure; GE Capital; and NBC Universal (owned 80% by GE). The NBC Universal includes the NBC family of broadcast and cable networks, and the Universal movie studio. More than 9% of GE revenue comes from the NBC Universal division.

Estimated market share of GE in the global movie production and distribution industry is about 5%.

Viacom Inc. The company’s main activity is to produce and distribute television programming,

motion pictures and other entertainment in the United States, Europe and other countries. It operates through two segments: Media Networks and Filmed Entertainment. The Filmed Entertainment Segment distributes motion pictures and other entertainment content under the Paramount Pictures, Paramount Vantage™ (focusing on foreign language and documentary titles) Paramount Classics™, MTV Films, and Nickelodeon Movies™ brands.

Viacom Inc. holds 4.2% of the overall global movie production and distribution industry market share.

POTENTIAL MARKET ENTRANTS

Since Disney occupies a very large and distinctive niche in the entertainment industry, the entrance barriers are relatively high. Disney has been able to grow positively over time to form one of the largest entertainment media conglomerates in the world by focusing exclusively on the kids and family market segment. Disney’s management has become very familiar with what the targeted customers want, i.e. kids and families. Thus, the company dominates the family entertainment Industry. This makes it very difficult for a new organization to develop a good image and brand recognition in this market. The major barriers to new entry in this industry relate to the position of the major US studios2. Those studios form a barrier because they spend significant financial resources on marketing and advertising that draws the major crowds away from films with smaller budgets, e.g. in 2005 a member of the MPAA spent an average $36.2 million marketing a new feature film. Also, they are highly vertically integrated and have global distribution arms ‐ that often provide pre‐finance for a film ‐ thereby mitigating the problems of

2 See competitors

Acquisition Team Project Disney + Marvel

7

finding up front finance (the lag time between a movie’s conception and commercialization is a major barrier). Furthermore, major studios ‐ as the primary supplier to exhibitors ‐ have significant sway over cinema owners; this ensures that studio releases get screen priority and long run times. They may also have relationships with major cast names that prevent talent from working on films for other studios and independent productions. However, Disney’s most likely market entrants are those same major industry players with the resources, distribution channels and industry relationships to enter into the Disney‐dominated family entertainment market segment if they deem it necessary.

PRODUCT AND SERVICE SUBSTITUTES

The threat of substitute product or services in Disney is moderately low due to Disney’s highly differentiated products and services. Perhaps any kind of kid‐or‐family‐oriented characters, movies, and theme parks can influence, and access the market in which Disney is operating in, but this is not representing any significant threat to Disney. It is because Disney has highly differentiated products and services catering to a focused niche market segment, i.e. kids and families. In addition, Disney has already placed price ceilings on many of its product lines, and is thus able to meet and exceed any competition. However the threat of substitution requires that Disney hedge against such risks by maintaining its operating efficiency and diligently maintaining the quality of its brands.

SUPPLIERS

The bargaining power of Disney’s suppliers is moderate. The company is operating in highly concentrated industry with high switching costs due to the long‐term nature of contracts. However, Disney’s stability and reliability makes it an attractive customer for many suppliers. Furthermore, the sheer size of Disney is certainly a significant negotiating point for supplier contracts. By virtue of Disney’s leading market position and size of operations, the company can take advantage of volume discounts and establish long‐term relationships with key suppliers.

3.3. INTERNAL ANALYSIS

STRENGTHS

The Walt Disney Company boasts a portfolio of products and services that enjoys significant breadth and depth. This together with Disney’s globally renowned brands and large scale of operations provide it with considerable strength in the industry. Compared to its competition, Disney has the third largest global market share in the diversified entertainment industry3, and above industry average operating margin of 15.76% compared to 14.75% for the industry. Disney’s wide diversification and distribution network are especially helpful in the entertainment industry which is characterized by high seasonality. Walt Disney’s key strengths include the following:

Robust Imagination and Unique Creative Skills. From 1940’s classic “Fantasia” to more recent releases such as “Aladdin” and “Toy Story”, Walt Disney has never been less committed to envisioning the wildest things through the minds of its pioneers and their infinite imagination and creativity. Indeed, it has always been and will be the driving force of the Walt Disney Company and what truly differentiates it from the competition. This is also what attracts Disney’s loyal customers. In fact, many aspects of Walt Disney’s products and services have

3 See appendix 7.1 Industry & Market Exhibits – Major Industry Players

Acquisition Team Project Disney + Marvel

8

become associated with expressions such as “Only Disney can do that!” which is most substantiated in Disney’s dream‐like theme parks and resorts.

World‐renowned, High Quality Brands. Walt Disney enjoys strong global recognition for its broad array of outstanding brands. In fact, the company owns one of the most powerful brands in the entertainment business and the world: Disney™. The Disney brand was ranked 9th in the Top 100 Global Brands ranking of the BusinessWeek magazine and Interbrand. Its value was estimated to be $29.251 billion in 2008. Furthermore, the company has several other high quality brands such as ESPN within its portfolio. ESPN, for example, is one of the largest and most popular sports channels in the world. Others include Miramax, Touchstone, and Pixar, all of which enjoy strong brand equity and global recognition. In addition, Disney stands out from its competitors with its wide array of well‐recognized characters such as Mickey Mouse, Donald Duck, Goofy and others, which still generate smiles on customers’ faces in Disney’s resorts and revenues in its books. Strong brand image allows Walt Disney to gain consumer acceptance of new products easily. This also provides Walt Disney the option to leverage its strong brand to enter new businesses.

Unparalleled Portfolio of Entertainment Properties, Licenses, and 3rd Party Relationships. The company’s offerings can be broadly classified into five segments: media networks; theme parks and resorts; studio entertainment; interactive media; and consumer products. Under the media networks segment, Walt Disney owns and operates television, radio, and cable properties in the United States and other countries. Through the parks and resorts segment, the company owns and operates the Walt Disney World resort, the Disneyland resort in California, ESPN facilities in several states, and the Walt Disney Cruise Line in Florida. The studio entertainment segment involves producing and acquiring live‐action and animated motion pictures, animated direct‐to‐video programming, musical recordings and live‐stage plays. The consumer products segment partners with licensees, manufacturers, publishers and retailers to promote, design and sell products based on existing Disney characters, brands and other intellectual properties.

Large Scale of Operations and Global Reach. The company has 2nd largest scale of operations when compared to its competitors in the market. Many of its competitors, such as CBS and Liberty Media are much smaller in size and in terms of revenues. CBS recorded revenues of $13,950.4 million and employed 25,920 people in FY2008. Similarly, Liberty Media recorded revenues of $10,084 million and employed 22,000 people during the same period. Walt Disney, in contrast, recorded revenues of $37.843 billion and employed 150,000 people in FY2008. Large scale of operations enhances the company's market penetration and gives it substantial bargaining power. Widely deployed infrastructure, marketing and distribution channels provide considerable leverage in promoting, marketing and distributing newly developed or strategically acquired brands.

Strong Media Networks Segment. In FY2008, Walt Disney’s media networks segment generated the largest portion of total revenues with 42.6% and revenue growth equal to $1.0 billion or 7% (see business segment results in appendix). Walt Disney’s cable networks and international broadcasting operations are mainly involved in the distribution of television programming, the licensing of programming to domestic and international markets, and investing in foreign television broadcasting, production and distribution entities. Typically, the cable networks segment produces its own programs or acquires programming rights from other producers and network programming rights holders.

Strong Brand Equity in Theme Parks and Resorts Operations. Walt Disney has a strong presence in the parks and resorts business. In FY2008, about 30.4% of total revenue came from parks and resorts business segment. The company's parks and resorts segment consists of the Walt Disney World Resort, the Disneyland Resort, the Disney Vacation Club, the Disney Cruise

Acquisition Team Project Disney + Marvel

9

Line, Adventures by Disney, and ESPN Zone. The Walt Disney World Resort is located in Florida, on approximately 25,000 acres of Disney owned land. The resort includes theme parks, hotels, vacation club properties, retail, dining and entertainment complex, sports complex, water parks and other recreational facilities. The Disneyland Resort owns 461 acres and has the rights under long‐term lease for use of an additional 49 acres of land in Anaheim, California. It includes two theme parks, three hotels and Downtown Disney, a retail, dining and entertainment district.

Multi‐industry Synergistic Business Structure. Disney’s five complementary business segments: Media Networks; Theme Parks and Resorts; Entertainment Studios; Interactive Media; and Consumer Products, work together to provide significant value‐added to virtually any Disney‐owned brand. Walt Disney’s mix of horizontally and vertically integrated business segments in the entertainment and media industry provides many operating and financial synergies and helps maximize the value of creative or intellectual properties across multiple platforms and geographic markets. Synergies include economies of scale and scope exemplified in strong bargaining power and lower costs along with utilizing existing creative skills, market research, and distribution channels. Furthermore, Disney’s strong credit rating and large scale and diversification of its operations allows for a lower cost of capital relative to the competition. Disney is the most diversified and integrated among its competitors in terms of the breadth and depth of its business lines4.

Proven ability to grow and expand content creation and licensing businesses whether developed in‐house or strategically acquired. Disney’s track record is full of highly successful endeavours in developing and strategically acquiring entertainment businesses. The company’s strategic acquisition of Pixar Studios in May 5th of 2006 greatly substantiates this ability. Even though the market perceived Pixar’s acquisition as a tad too pricy for Disney at the time, post‐merger film productions such as 2008’s “WALL‐E” was an outstanding success. In addition, Walt Disney has acquired several companies in recent years to expand its position in the kids and families media market. For instance, in December 2008, it acquired the shares of Jetix Europe, a pan‐European media company comprised of television channels, program distribution and consumer products businesses. Jetix Europe operates in the kids aged 6‐14 and family media business, and reaches a combined 137 million television households in 58 countries and 18 languages. In FY2007, the company acquired Club Penguin, one of the fastest‐growing online virtual worlds. The addition of Club Penguin to Disney's existing online assets enhanced the company's position in the online virtual worlds for kids and families.

WEAKNESSES

The Walt Disney Company has few but critical weaknesses that could hinder the company’s market position relative to its competition. Key weaknesses include:

Weak Performance in the Studio Entertainment Segment. The studio entertainment segment has witnessed a declining revenue growth in the last three years (see business segment results in appendix). The studio entertainment segment recorded revenues of $7,348.0 million in FY2008, a decrease of 1.9% over FY2007. The percentage contribution of the segment to the total revenue has also declined from 22.3% in FY2006 to 19.4% in FY2008. However, this is more reflective of the growth in other segments than decline in the entertainment studios segment. Continued weak performance of the studio entertainment segment would adversely affect the company's overall revenues and profitability relative to the competition.

4 See appendix 7.1 – Media Conglomerates by Business Line

Acquisition Team Project Disney + Marvel

10

Overdependence on the North American Market. Walt Disney has its operations all across the world spanning North America, Europe, Asia Pacific and Latin America. But, the company derives the majority of its revenues from North American markets, which does not truly reflect its global presence. In other words, Walt Disney has a large exposure to the North American market with respect to its overall geographic coverage. The company derived 75.3% of its revenues from the US and Canada in FY2008. Disney has little presence in the emerging markets like Asia Pacific, Latin America and others, which accounted for only 6.7% of the company's total revenue in FY2008. Concentrating on maturing markets like the US and Canada, which are already witnessing economic slowdown and not expanding in emerging markets would limit the company's overall revenue growth and weaken its international market position.

3.4. EXTERNAL ENVIRONMENT

OPPORTUNITIES

Online Television Trend – Numerous companies such as AT&T and Verizon are now delivering television programming via high‐speed Internet connections5. This new distribution channel threatens traditional cable and satellite TV firms for market share. As this new trend coincides with new consumer preferences, the Walt Disney Company is required to compete aggressively to utilize this opportunity through its Interactive Media business segment.

Piracy Clampdown – Walt Disney, a member of the media and entertainment industry, is set to benefit from increased regulation of piracy. Specifically, the new laws allow products created (i.e. movies, films, images, music, etc) to be subject to protection from unauthorized copying. Consequently, the media and entertainment industry will enhance its revenues.

Ultra‐low Interest Rates – The benefits of low interest rates for Walt Disney are twofold. Firstly, The Walt Disney Corporation, will have a greater ability for innovation and growth as more low interest rates provide cheaper financing options and lower weighted‐average cost of capital. Secondly, consumers will also benefit from lower interest rates as they are able to borrow at lower rates, resulting in higher purchasing power and demand for goods. Unfortunately, the recession has left many without jobs which reduces counteracts the positive effects of low interest rates on consumers and encourages high saving by those who still have jobs out of prudence. Current interest rates are projected to mildly increase in the mid to long‐term as the global economy recovers.

Weak US Dollar – The weakening dollar will make movie production cheaper for Disney especially when financed with strengthening foreign currencies. Given that 75% of Disney`s revenues are generated in the US market, Disney will benefit as its products and services become cheaper relative to foreign competition. Disney might also transfer some of these cost savings to consumers to enhance its competitive position in Europe and Asia.

High Growth in Emerging Markets – The movie production industry has the largest number of enterprises in India and Central Asia. The industry in those markets is still young with much room for growth and development and Disney could play a big role in this process6. Outside of the US, India is one of the largest markets, where Disney invested in local production. Disney Channel and Jetix have over 6,000 episodes of trans‐created content. Through the terrestrial network, Disney Channel reaches over 122 million homes in India alone.

5 Plunkett Research, Ltd. 6 See appendix 7.1 – Global Industry Geographic Distribution of Enterprises

Acquisition Team Project Disney + Marvel

11

Positive Market Outlook for Entertainment Media – The global media industry has been growing significantly in the recent past. As shown on the Datamonitor's report on "Global Media", October 2008, the global media industry generated total revenues of $938,900 million in 2008. The performance of the industry is forecast to improve further and reach the value of $1,104,200 million by the end of 2013. In FYE2008, the Walt Disney Company generated only 25% of its total revenues outside of the United States and Canada. This provides an opportunity for further growth by expanding foreign market share.

THREATS

High Global Competition – There is strong competition in many of Disney's key industries. Its broadcasting services compete for viewers with other television networks, cable television, satellite television, videocassettes, DVDs, and internet. This high level of competition is particularly important with respect to advertising revenues, where it also competes with other media such as newspapers, magazines, radio and billboards. Disney's broadcasting division competes with organizations such as CBS and Fox. Disney`s key competitors are comparably large and pose significant threat. The parks and resorts segment competes with other operators such as Xanterra Parks & Resorts and local amusement parks for visitors. Intense competition threatens to erode the company's market share in all its different lines of business.

Weak US Dollar – Disney will find it more expensive to use income and capital generated in US dollars to finance foreign projects. Hence, it is critical for Disney to expand its foreign market share as early as possible to help in financing foreign projects with foreign capital.

Reduced Consumer Confidence – As a result of the recent economic crisis global economies are experiencing abnormally high levels of unemployment. This poses a threat for the entertainment and media industry as consumers typically spend less on entertainment during such times. The U.S. jobless rate in August jumped to 9.7 percent, the highest since 1983, and employers cut another 216,000 jobs, highlighting threats to consumer spending7. During times of economic downturn, individuals conserve resources and shy away from inessential goods. Consumers suffering from job insecurity/loss and diminishing savings whether in the stock or real estate markets are less inclined to spend on discretionary items such as new consumer electronics, movie tickets and travel to entertainment venues such as Las Vegas ("Plunkett Research, Ltd."). However, the global economy is forecast to begin a slow recovery in 20108.

Ailing Retail Industry – The retail industry has experienced severe turmoil. This results in increased risk of companies who use retail outlets as distribution channels. Many major retail firms had gone bankrupt in 2008, with more to follow in 2009, (“Plunkett Research, Ltd.”). Disney uses many retail outlets to provide merchandise for their consumers.

Higher Taxes in the Near Future – The fiscal policies implemented by federal governments to counteract the recession have drastically increased public debt and budget deficits. Consequently, nations are likely to raise future taxes. Higher taxes will have a detrimental impact on consumer disposable income and purchasing power.

3.5. BUSINESS MISSION AND VISION

Since its founding in 1923, The Walt Disney Company and its affiliated companies have remained faithful to their commitment to produce unparalleled entertainment experiences based on the rich legacy of

7 Source: www.tradingeconomics.com 8 Ibid.

Acquisition Team Project Disney + Marvel

12

quality creative content and exceptional storytelling. Today, the Walt Disney Company’s vision is to be one of the world's leading producers and providers of entertainment and information. To achieve this, we use our global portfolio of high quality brands to differentiate our content, services and consumer products. We seek to develop the most creative, innovative and profitable entertainment experiences and related products in the world. At Disney, we strive to create exceptional entertainment content, experiences and products that are embraced by consumers around the world and to do so in a manner that delivers long‐term shareholder value. Our primary financial goals are to maximize earnings and cash flow, and to allocate capital profitably toward growth initiatives that will drive long‐term shareholder value. Moreover, we are fully committed to being a good corporate citizen. It is not just the right thing to do, but it benefits our guests, our employees and our businesses. It makes the Company a desirable place to work, reinforces the attractiveness of our brands and products and strengthens our bonds with consumers and neighbours in communities across the globe. To put it shortly, our mission is to make people happy.

3.6. QUANTIFIED STRATEGIC OBJECTIVES

NON‐FINANCIAL

Given that Walt Disney's long‐term objective is to be one of the world's leading producers and providers of entertainment and information, in order to achieve and maintain this presence in the long run, Disney aims to create high‐quality creative work and invest in promising international markets. In addition, Disney continues to invest in digital and interactive media to be able to stay ahead of rapid developments in technology as it realises the importance of this segment in its long term objectives.

Some selected Non‐Financial Objectives to be achieved by FYE2013:

Become the global market share leader in all aspects of the entertainment media industry. Continuously access new markets that offer high growth potential preferably through

acquisitions and investments/collaborations in promising firms. Show continuous, annual improvements in client‐base, viewership and rating figures by

remaining relevant to the future generations. Develop and invest in new technologies that will enable efficient production and distribution of

products. Take full advantage of new mediums (i.e. internet) and create great content from technological

innovation. Achieve leadership in environmental and social aspects of the business through good corporate

citizenship regardless of location around the globe.

FINANCIAL

Disney’s primary financial goals are to maximize earnings and cash flow, and to allocate capital profitability toward growth initiatives that will drive long‐term shareholder value. Goals include:

Achieve $45B in Revenues by 2013. Increase annual sales growth to match industry average of 10% and exceed it. Reward shareholders by seeking to enhance Price to Earnings ratio. Disney’s P/E ranges from a

high of 25.72 to a low of 8.01 in the last five years. The industry average ranges from a high of 14.24 to a low of 2.51 in the last five years.

Maintain above industry average operating profit margins.

Acquisition Team Project Disney + Marvel

13

Maintain above industry average ROA, and ROE. Currently the trail‐twelve‐month estimates fall short of the 5‐yr average for Disney which can be explained by the recent credit crises and global economic slowdown. Our goal will be to bring these rates back to their long‐term average if not exceed it within the next five years.

Maintain D/E ratio provided it is at or near optimal. Industry average D/E is slightly higher which indicates some room for Disney to increase leverage if necessary, especially considering Disney’s large portfolio of real estate and present ultra‐low interest rates. According to Reuters Research, Disney’s Debt‐to‐Equity ratio is 36.60 and the industry’s average is 42.34 based on most recent quarters as at October 22, 2009. In our financial strategy we will target a meagre rise in debt relative to equity to maintain future financial flexibility.

CRITERIA 2009 2010 2011 2012 2013

Revenue $38.5 B $40.5 B $42 B $43.5 B $45 B

Earnings‐Per‐Share $2.43 $2.63 $2.83 $3.03 $3.23

Sales Growth 7.5% 8% 9% 10% 11%

P/E 17.43 18 19 20 22.50

Operating Profit Margin 17% 17.55% 18% 18.5% 19%

LT Debt‐to‐Equity 36.60 36.65 36.70 36.75 36.80

ROA 5.53 5.83 6.03 6.53 6.83

ROE 9.46 10.46 11.46 12.46 13.46

3.7. BUSINESS STRATEGY

We believe the integrated manner in which we manage our brands and franchises gives us the opportunity to generate exceptional returns on our creative content. Our results over the past several years reflect the power of our brands and franchises, and our ability to develop and leverage high‐quality content across multiple creative platforms and global markets. This franchise development process has enabled us to build an extensive portfolio of brands, led by Disney and ESPN, and intellectual properties that include enduring characters like Mickey Mouse and Winnie the Pooh, as well as thriving new ones like Disney Fairies, Cars, Toy Story, High School Musical and Hannah Montana.

Our brands and integrated set of creative assets and businesses provide us with competitive advantages that we feel can deliver long‐term value to our shareholders. Disney’s overall business strategy is differentiation with focus on leveraging and extending these advantages. It consists of three major components: investing in the strength of our brands and the quality of our products; leveraging technology to provide consumers with entertainment when and where they want it; and expanding globally to better reach consumers around the world.

We recognize that allocating capital profitably and managing our business to drive creative and financial success are the most important ways that we serve the owners of our Company. Our first priority in allocating capital is to fund strategically attractive investments that can drive future growth and provide strong returns over time. These opportunities can include internal investment in existing and new businesses or acquisitions. We plan to continue expanding our creative pipeline of high‐quality content and to strengthen our brands and reach on a global basis. These internal growth initiatives include investment in television, films, digital media and video game development. We will also continue to invest in developing local, Disney‐branded content and expanding the reach of our Disney and ESPN‐

Acquisition Team Project Disney + Marvel

14

branded channels around the world. We recently released films made for China and India and currently have films in production for China, India and Russia. In addition to internal reinvestments, we look for attractive external investment opportunities that meet our financial and strategic objectives. During the year, we made investments in content companies in India and China. We also made acquisitions to enhance our position in youth‐oriented sports and the online sports community. In addition, we acquired three promising start‐up companies which help position us to participate in growth opportunities on digital platforms.

3.8. IMPLEMENTATION STRATEGY

To achieve the goals which are set out in our business strategy with minimum risks, we require a high level of control. This is why acquisitions are the form of investments which we have used heavily in the past and continue to use. The recipe to success in the entertainment business is talent, and for Disney to obtain these talents they require control over these firms. Having full control over investments allows Disney to fully utilize its resources and maximise returns on its investments. The ability to guide and direct talents with full control of the investment allows for less resistance and more security for Disney.

When considering what sort of corporate level strategy Disney is using, the answer seems to be clear cut. It’s inevitable that Disney is, and has been for quite some time now, constantly pursuing growth, both organic and through acquisitions. Disney has grown to become a highly diversified multi‐industry conglomerate over the years. This was especially the case during the 1970s when it was fashionable to diversify across non‐related industries. However, Disney never diversified into completely non‐related industries like many other conglomerates had done. Instead, every industry which Disney expanded into is highly synergetic to its existing operations and follows its overall theme, philosophy and brand quality. Today, international expansion is a primary strategic focus when it comes to creating shareholder value and achieving growth. Hence, our main focus is to acquire firms that will increase return on invested capital, enhance free cash flow, and grow our market share across the world. In other words, acquisitions that will enhance shareholder “value” which could be expressed as share price and quality where quality denotes long‐term price momentum as opposed to ephemeral price spikes. Disney could realize many advantages from pursuing an acquisitions strategy over plain Greenfield projects which are often more costly and risky due to management’s limited experience in new or foreign markets. Acquiring a pre‐established business with strong prospects allows Disney to benefit from the existing talent while supporting it to enhance combined growth. Furthermore, expenditures such as training, R&D, advertising, and promotion to build brand recognition, are all avoided by acquiring well established firms. In this way, we simply need to continue operations as is, with minor alterations or eliminations that suit both companies’ best interests.

Disney does have several alternatives when selecting a corporate level strategy. We could attempt to enter desired markets by ourselves, i.e. solo ventures, or through partnerships, i.e. alliances, licensing, minority holdings, and joint ventures. But going solo is more costly and risky, and venturing with a partner has limited control, and consequently, slower decision making if not conflicts. Building from the ground up also means we must invest in timely and costly operations using limited expertise. Another option to reducing the cost of operations is to simply invest in other companies through minority shareholdings. Even though it is quick and easy, it has a high risk of failure due to the lack of control. Finally there are collaborative agreements, licensing, franchising or swapping assets, which once again are fairly cost‐effective but may compromise trade secrets, violate intellectual property rights, and lead to protracted legal battles. It is worth noting that many of these alternative strategies are good initial strategies which lead into future acquisitions if results are superior. Franchising, licensing, minority

Acquisition Team Project Disney + Marvel

15

shareholdings, marketing collaborations and joint‐ventures are in fact common initial strategies which we often utilize to pursue a potential future acquisition/merger.

Disney’s differentiation strategy allows for maintaining some element of independence across its business segments to ensure high brand quality. By keeping separate brand images for some of its media networks, Disney could effectively cater to different groups of customers. For example, Disney avoids using its name or logo when distributing ESPN. This is because the general target market for ESPN is most likely not too fond of a family brand such as Disney, and more fond of masculine, macho‐like, sport related brands. Disney does this to strategically obtain maximum revenues in each of their business sectors without the interference of their parent company. Basically, Disney ensures that firms acquired have a solid foundation for brand recognition from the get‐go.

FUNCTIONAL TACTICAL STRATEGIES

Research and Development is done independently by each business sector. It is not top priority as many of their business activities are already established. Most R&D is completed to slightly improve upon current products. Disney acquires human intellect through acquisitions to keep their research and development department strong.

Marketing and Sales is once again not as crucial as it would be if they were to indulge in a solo corporate strategy. Each business segment does independent marketing for their products but keep in mind that most of these products are backed by well recognized brands.

Human Resources are done accordingly through each business sector. When Disney acquires a firm they usually bring in top employees from these respective firms. The company will operate more or less as it did before Disney acquires them and therefore they coordinate hiring as necessary. Depending on intended level of integration, some restructuring may be necessary in which redundant jobs are eliminated. In addition, Disney installs or reinforces strategic controls such as incentive systems, retention bonuses, and monitoring systems.

Finance is absolutely essential for Disney. With so many acquisitions, free cash flows and revenues in the billions, Disney’s accounting and in‐house investors must be at top of their game. Tax savings alone can amount to millions of dollars not to mention the savings incurred by funding high cost expenditures correctly. Disney’s international access to capital provides Disney the opportunity to raise money where it is cheapest in order to fund acquisitions.

Disney also heavily relies on their Legal Department. Through acquisitions, high‐calibre lawyers handle the deal structuring and due diligence of all targets. In addition, Disney encounter a fair amount of lawsuits which require the legal department’s expertise.

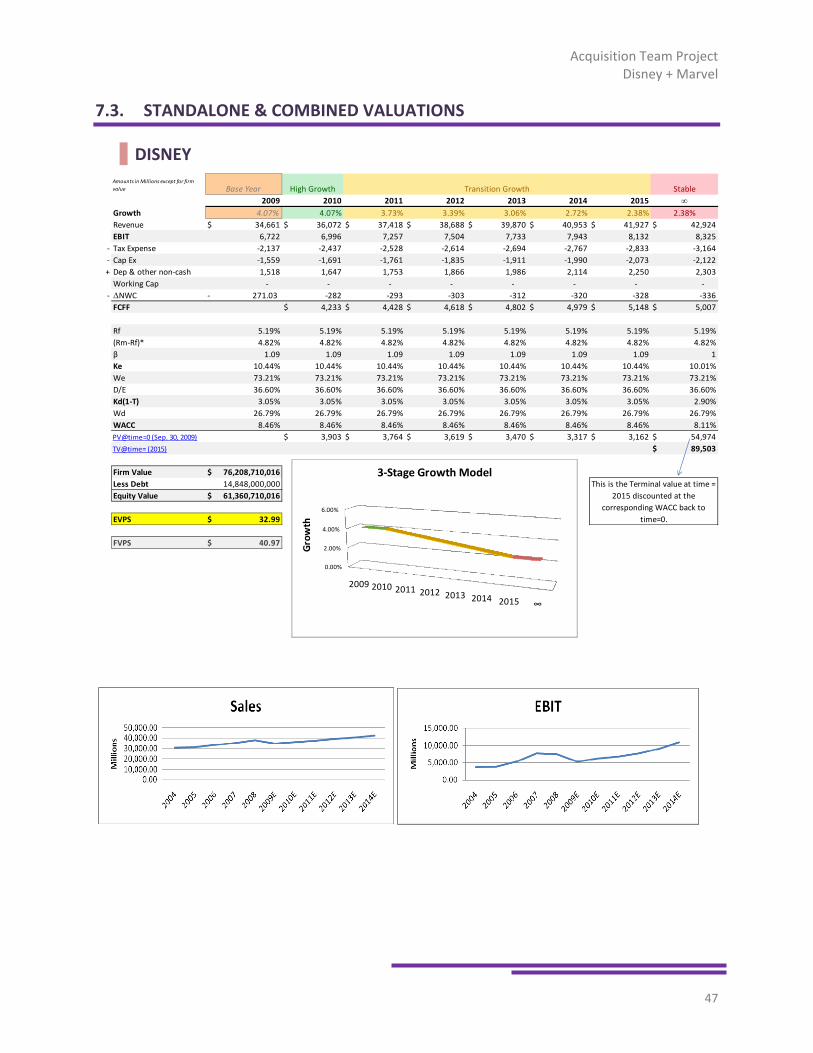

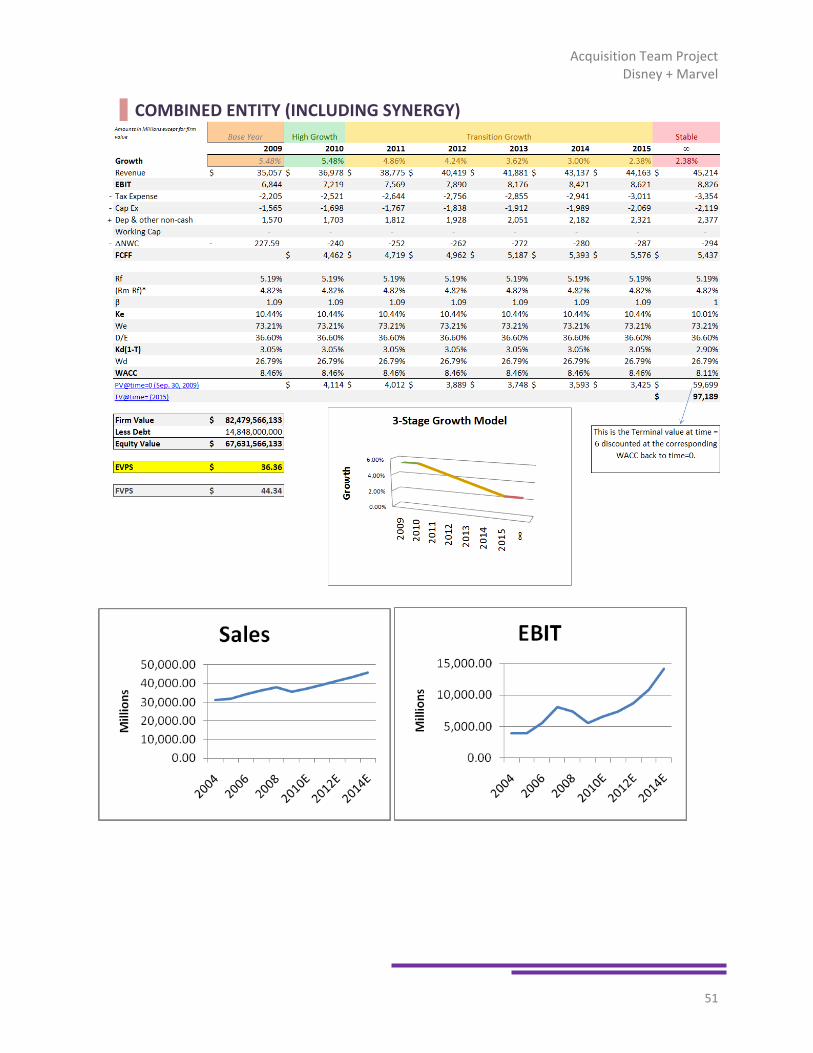

3.9. BUSINESS PLAN FINANCIALS AND VALUATION

BUSINESS VALUATION

After carefully reviewing Disney’s financial statements from FYE 2004 to FYE 2008 and Interim Financial Statements for the year 2009, we projected the company’s future financial performance given industry

Acquisition Team Project Disney + Marvel

16

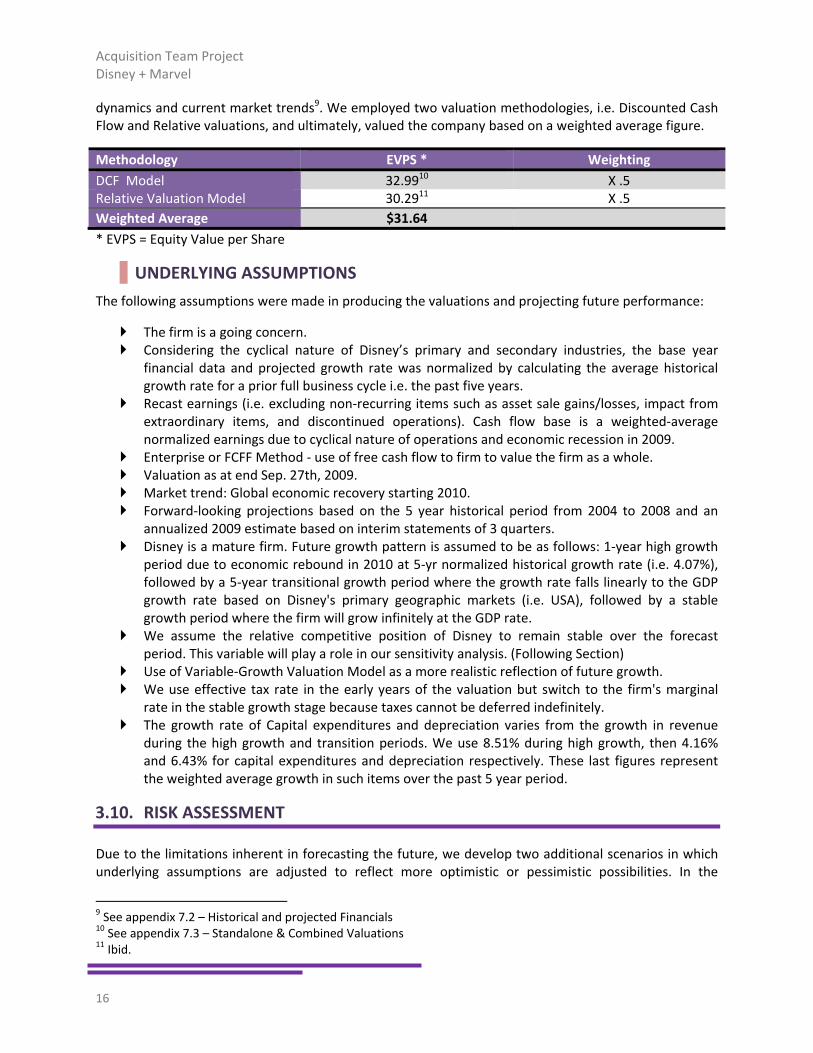

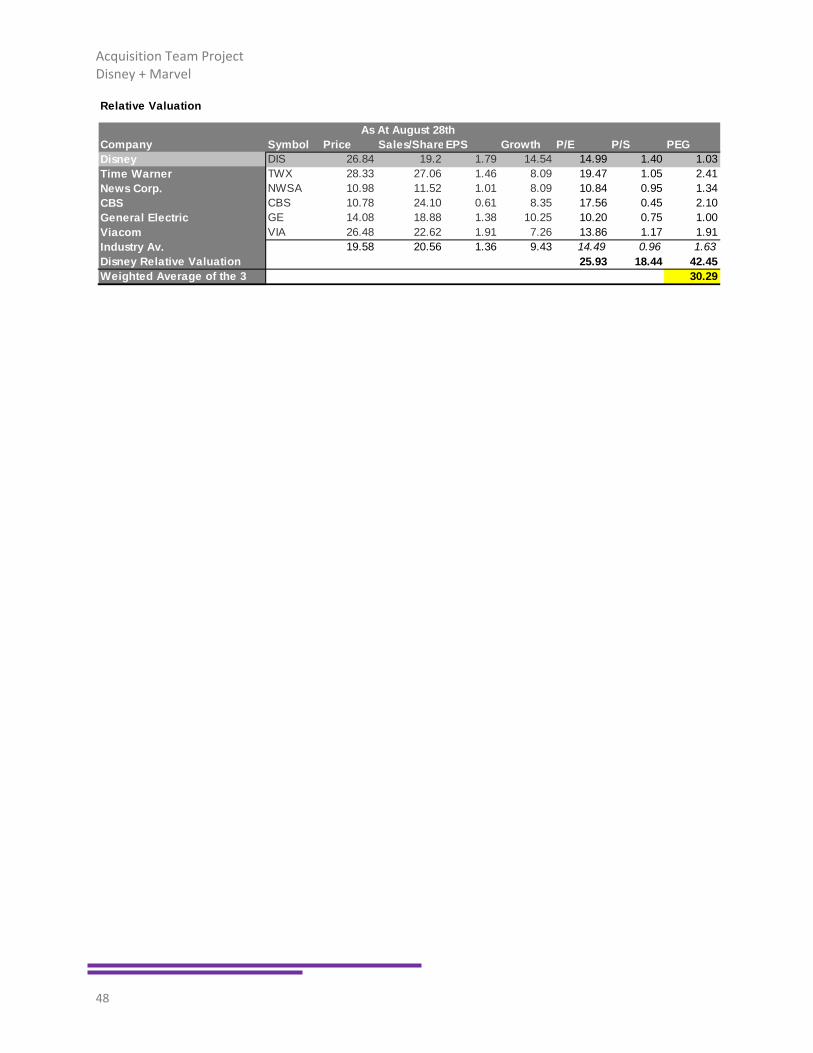

dynamics and current market trends9. We employed two valuation methodologies, i.e. Discounted Cash Flow and Relative valuations, and ultimately, valued the company based on a weighted average figure.

Methodology EVPS * Weighting DCF Model 32.9910 X .5 Relative Valuation Model 30.2911 X .5 Weighted Average $31.64 * EVPS = Equity Value per Share

UNDERLYING ASSUMPTIONS

The following assumptions were made in producing the valuations and projecting future performance:

The firm is a going concern. Considering the cyclical nature of Disney’s primary and secondary industries, the base year

financial data and projected growth rate was normalized by calculating the average historical growth rate for a prior full business cycle i.e. the past five years.

Recast earnings (i.e. excluding non‐recurring items such as asset sale gains/losses, impact from extraordinary items, and discontinued operations). Cash flow base is a weighted‐average normalized earnings due to cyclical nature of operations and economic recession in 2009.

Enterprise or FCFF Method ‐ use of free cash flow to firm to value the firm as a whole. Valuation as at end Sep. 27th, 2009. Market trend: Global economic recovery starting 2010. Forward‐looking projections based on the 5 year historical period from 2004 to 2008 and an

annualized 2009 estimate based on interim statements of 3 quarters. Disney is a mature firm. Future growth pattern is assumed to be as follows: 1‐year high growth

period due to economic rebound in 2010 at 5‐yr normalized historical growth rate (i.e. 4.07%), followed by a 5‐year transitional growth period where the growth rate falls linearly to the GDP growth rate based on Disney's primary geographic markets (i.e. USA), followed by a stable growth period where the firm will grow infinitely at the GDP rate.

We assume the relative competitive position of Disney to remain stable over the forecast period. This variable will play a role in our sensitivity analysis. (Following Section)

Use of Variable‐Growth Valuation Model as a more realistic reflection of future growth. We use effective tax rate in the early years of the valuation but switch to the firm's marginal

rate in the stable growth stage because taxes cannot be deferred indefinitely. The growth rate of Capital expenditures and depreciation varies from the growth in revenue

during the high growth and transition periods. We use 8.51% during high growth, then 4.16% and 6.43% for capital expenditures and depreciation respectively. These last figures represent the weighted average growth in such items over the past 5 year period.

3.10. RISK ASSESSMENT

Due to the limitations inherent in forecasting the future, we develop two additional scenarios in which underlying assumptions are adjusted to reflect more optimistic or pessimistic possibilities. In the

9 See appendix 7.2 – Historical and projected Financials 10 See appendix 7.3 – Standalone & Combined Valuations 11 Ibid.

Acquisition Team Project Disney + Marvel

17

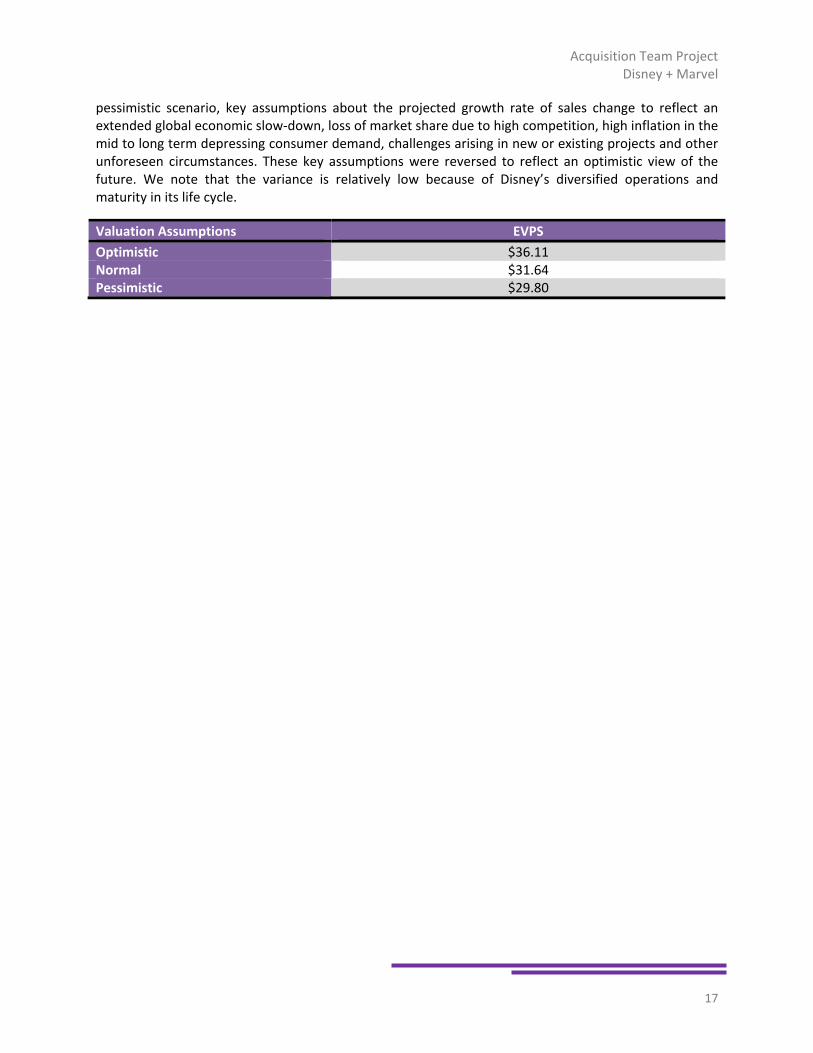

pessimistic scenario, key assumptions about the projected growth rate of sales change to reflect an extended global economic slow‐down, loss of market share due to high competition, high inflation in the mid to long term depressing consumer demand, challenges arising in new or existing projects and other unforeseen circumstances. These key assumptions were reversed to reflect an optimistic view of the future. We note that the variance is relatively low because of Disney’s diversified operations and maturity in its life cycle.

Valuation Assumptions EVPS Optimistic $36.11 Normal $31.64 Pessimistic $29.80

Acquisition Team Project Disney + Marvel

18

4. ACQUISITION PLAN

4.1. PLAN OBJECTIVES

Disney’s objectives in pursuing an acquisition are:

To enhance market share and penetration Disney has been particularly overlooking the young boys market.

To enhance growth in the Entertainment Studios and Interactive Media business segments The entertainment studios business segment has been experiencing flat to negative

growth in the past 5 years. Disney needs to support its newly launched Interactive Media business segment which

anticipates high growth and positive market trends. Acquisition must address Disney’s strategic focus on quality branded content, technological

innovation, and international expansion to build long term shareholder value. The acquisition must help Disney achieve its business strategy by focusing on its

strengths in managing intellectual properties and technological innovations such as Pixar’s 3D animations in the Entertainment Studios business segment.

Disney is looking for acquisitions that enhance its competitive position in the global market by warding off high competition and building on what the Walt Disney Company does best12.

Disney stands out with its robust imagination and unique creative skills, highly differentiated and globally renowned brands, well‐established and far‐reaching distribution network, and unparalleled portfolio of entertainment properties, licenses, and 3rd party relationships.

The acquisition must take full advantage of current environmental opportunities such as online entertainment trends and cheaper movie production costs in the United States due to currency depreciation while addressing threats such as rising global competition.

Acquisition must enhance Disney’s presence outside of the North American market: With three quarters of Disney’s revenue coming from the United States and Canada,

Disney is seeking new opportunities in high growth emerging markets around the globe. Diversification of revenue sources helps to hedge against economic slowdowns in any

single region and reduces overall volatility which enhances shareholder value.

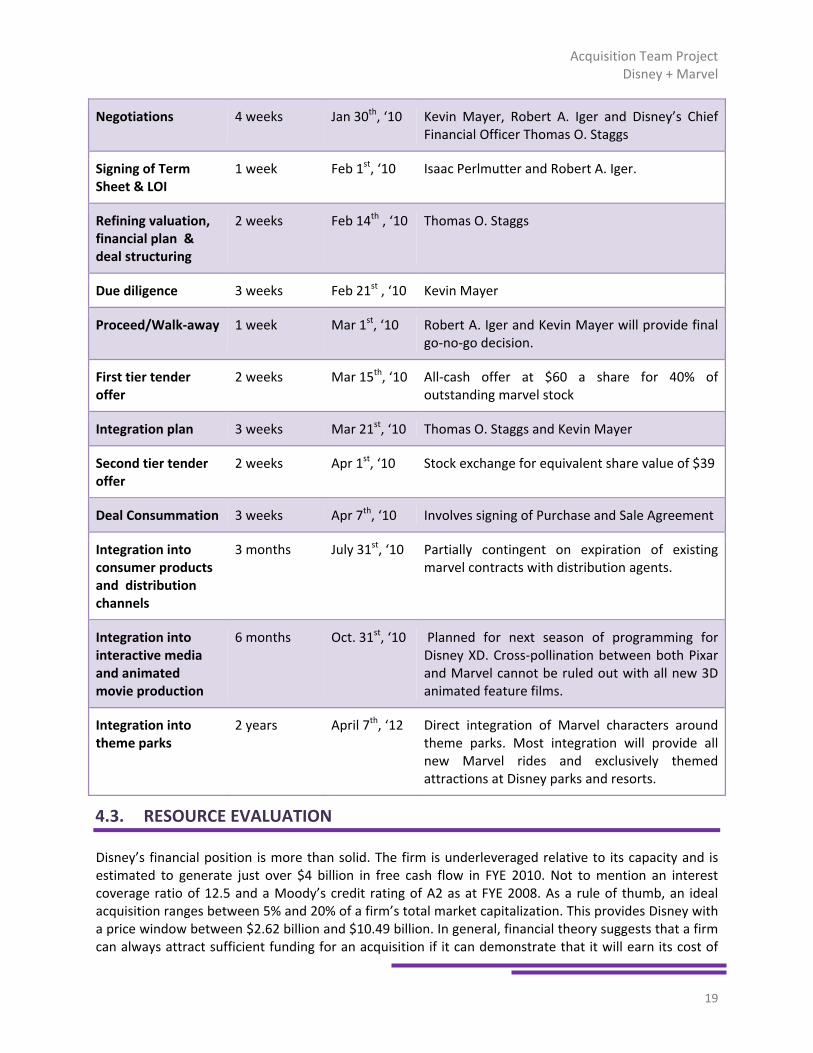

4.2. TIMETABLE

ACTIVITIES DURATION DEADLINE DESCRIPTION

First Contact 1 week Dec 14th,’09 Disney’s president and CEO, Robert A. Iger, will contact Marvel’s CEO and Chairman, Isaac Perlmutter.

Signing of Standstill and Non‐Disclosure Agreements

1 week Dec 21st, ‘09 Isaac “Ike” Perlmutter and Kevin Mayer, Disney’s Executive Vice President for Corporate Strategy

12 See appendix 7.1 – SWOT matrix

Acquisition Team Project Disney + Marvel

19

Negotiations 4 weeks Jan 30th, ‘10 Kevin Mayer, Robert A. Iger and Disney’s Chief Financial Officer Thomas O. Staggs

Signing of Term Sheet & LOI

1 week Feb 1st, ‘10 Isaac Perlmutter and Robert A. Iger.

Refining valuation, financial plan & deal structuring

2 weeks Feb 14th , ‘10 Thomas O. Staggs

Due diligence 3 weeks Feb 21st , ‘10 Kevin Mayer

Proceed/Walk‐away 1 week Mar 1st, ‘10 Robert A. Iger and Kevin Mayer will provide final go‐no‐go decision.

First tier tender offer

2 weeks Mar 15th, ‘10 All‐cash offer at $60 a share for 40% of outstanding marvel stock

Integration plan 3 weeks Mar 21st, ‘10 Thomas O. Staggs and Kevin Mayer

Second tier tender offer

2 weeks Apr 1st, ‘10 Stock exchange for equivalent share value of $39

Deal Consummation 3 weeks Apr 7th, ‘10 Involves signing of Purchase and Sale Agreement

Integration into consumer products and distribution channels

3 months July 31st, ‘10 Partially contingent on expiration of existing marvel contracts with distribution agents.

Integration into interactive media and animated movie production

6 months Oct. 31st, ‘10 Planned for next season of programming for Disney XD. Cross‐pollination between both Pixar and Marvel cannot be ruled out with all new 3D animated feature films.

Integration into theme parks

2 years April 7th, ‘12 Direct integration of Marvel characters around theme parks. Most integration will provide all new Marvel rides and exclusively themed attractions at Disney parks and resorts.

4.3. RESOURCE EVALUATION

Disney’s financial position is more than solid. The firm is underleveraged relative to its capacity and is estimated to generate just over $4 billion in free cash flow in FYE 2010. Not to mention an interest coverage ratio of 12.5 and a Moody’s credit rating of A2 as at FYE 2008. As a rule of thumb, an ideal acquisition ranges between 5% and 20% of a firm’s total market capitalization. This provides Disney with a price window between $2.62 billion and $10.49 billion. In general, financial theory suggests that a firm can always attract sufficient funding for an acquisition if it can demonstrate that it will earn its cost of

Acquisition Team Project Disney + Marvel

20

capital. However, in practice, it is management’s risk tolerance that really determines how much Disney can truly afford. In terms of operating risk, Disney’s acquisitions team is highly experienced and its management expertise is unquestionable. Hence, as long as the target firm is in charted waters operating risk is minimal. On the other hand, financial risk is at a minimum by virtue of afore mentioned facts. Finally, overpayment risk is subject to many factors and has lingering effects of growth capping and EPS dilution. Overpayment may occur due to bidding wars, management hubris, poor deal structuring or negotiations. Ultimately, overpayment risk is the one risk that Disney should be most concerned about.

4.4. MANAGEMENT PREFERENCES

Management would prefer the following:

Acquisition in a related industry, preferably entertainment studios due to laggard growth; Total transaction size of no more than $10 billion and no less than $2 billion; Since management’s time is costly and constrained, a ‘friendly’ acquisition with a higher chance

of consummation is preferred to a ‘hostile’ one; Full ownership and control of target firm; To limit overpayment, control premium should be no more than 90% of net synergy; In current market conditions, management believes Disney’s stock is undervalued, and

therefore, cash is preferred to stock financing, specifically, ultra‐low interest rates provide strong incentive for cash financing of acquisitions. Disney is also concerned for EPS dilution and therefore stock financing should be avoided if possible;

Acceptable sources of financing include secured debt, subordinated debt, unsecured 5 year and 10 year corporate bonds, seller financing (VTB), and as a means of last resort equity issues conditional on repurchase of all equity offerings within 1 year of issue;

Acquisition team should not expend more than 2.5% of total transaction size in transaction costs and fees;

Acquisition team should utilize outside consultants wherever necessary and must include PR representatives, lawyers, investment bankers, tax strategists and financial analysts;

Broad due diligence; Sourcing will take the form of soliciting board members, analyzing competitors, contacting

brokers, investment bankers, lenders, law firms, and the trade press; and Target firm must contribute to Disney’s growth corporate strategy and address its key business

strategic focus of quality brands, technological innovation, and international expansion.

4.5. SEARCH PLAN

PRIMARY SEARCH CRITERIA

In parallel with management preferences:

Target must be in the entertainment media industry, preferably entertainment studios/movie production.

Increase Disney’s brands/characters across all aspects of the business: TV, movies, books, music, consumer products and online mediums.

Increase quality of branded content, add‐value through technological innovation and enhance international expansion through increasing Disney’s global competitiveness.

Acquisition Team Project Disney + Marvel

21

Allow extending presence in various entertainment markets such as video games, major production movies, theme park attendance, licensing, and publishing.

Increase Disney’s reach in the young boys and teenager male demographic. Forecast sales growth of 10% minimum. Strong market shareholding ‐‐‐ market leaders are preferred. EBIT or operating income margin of 30% minimum. Less than optimal debt‐to‐equity ratio. Total market capitalization between $2 and $10 billion.

SEARCH STRATEGY

Our search strategy entails initially utilizing computerized databases and directory services such as Disclosure, Dun & Bradstreet, Standard and Poor’s Corporate Register, Thomas’ Register, and Million Dollar Directories to identify qualified candidates.

The initial search strategy generated a list including: Marvel Comics, DC Comics, Dark Horse Comics, Image Comics, and IDW Publishing each holding a market share of 42.90%, 34.52%, 4.84%, 3.80%, and 2.83% respectively in 2008. These top 5 comic book publishers total 88.89% of the market share of the international comic book and magazine industry.

The market leader, Marvel entertainment, has some existing licensing agreements with Disney. About 20 hours of Marvel cartoons are played a week on Disney XD channel. Thus acquiring Marvel would increase the control Disney has over its business operations, reduces the costs and creates value for both companies.

SECONDARY SCREENING CRITERIA

The target must have considerable brand equity, and strong growth potential. Target must afford Disney a competitive blow to its competition; DC comics were acquired by

Time Warner to generate corporate synergy. Coincidently Time Warner is in direct competition with Disney as being massive media conglomerates. A target company similar to DC Comics could serve to maintain Disney’s competitive market position.

Disney must not buy only great characters, stories and brands but also have the right people who have known and had a part of the development of these characters to guide their directions within other media.

By acquiring a company that would afford Disney an enticing licensing opportunity. Target firm must have sufficient independence where Disney has a hands‐off relationship in

operations and instead focuses on utilizing their massive marketing resources to enhance the brand recognition; allowing both companies to expand individually and together.

TARGET SELECTION

Marvel Entertainment, Inc. has been chosen due to its well established over 5000 original characters that hold both quality brand recognition and great background stories. Marvel meets or exceeds all afore mentioned criteria. Marvel has successfully maintained the largest market share in the comic book industry totalling 42.90%. Further, DC comics, Marvel’s main rival, has been acquired by Time Warner, Disney’s industry rival, indicating that such an acquisition of Marvel would allow Disney to maintain its competitive position within the entertainment and media industry. Marvel has major opportunities to team up with Pixar, also a Disney subsidiary, and collaborate to benefit both parties without the friction

Acquisition Team Project Disney + Marvel

22

of working as separate entities. Marvel already has distribution deals with Paramount to release certain movies in the works. Likewise, Marvel also has similar deals with some of the best video game producers and publishers to create future video games based on Marvel characters. Disney praises these deals and views them as key business prospects.

The following discusses the implications of marvel’s acquisition on various operations of the Walt Disney Company. With respect to movie production, adaptation of comic‐book characters into a big screen movie can translate into big returns for Disney. Specifically, according to Box Office Mojo, comic‐book adaptations make an average lifetime gross of around $96.8 million. Sales of products featuring entertainment characters totalled $9.88 billion, 2008, of this it is estimated that Disney accounted for 35%‐40%. Further, it has been estimated that one character can generate up to $1billion in revenue over under Disney’s reign. Thus embarking on this acquisition adds 5000+ characters to Disney’s portfolio, increasing licensing opportunities. In 2008 Marvel controlled 41% of the dollar share of comics sold indicating large publishing opportunities for Disney. Moreover, Disney airs 20hours of Marvel cartoons a week on Disney XD channel. Hence, Disney will not incur the costs related to using Marvel programming, and can in fact take advantage of using the 5000 characters that are acquired to produce new televisions programming, cartoons or drama series. Further, the use of Marvel comics for new rides or to increase attendance can potentially increase Disney’s revenue from theme parks and resorts. Currently, Disney is lacking support from the 18‐34 year old male market, hindering Disney from reaching the organizational vision of providing legendary entertainment for the whole family. The use of marvel characters to produce video games can essentially correct Disney’s boy problem. Since 1995 superhero licensed games have grossed over $1.5 billion and U.S. computer and video‐game‐software sales grew 22.9% in 2008. Indicating that the purchase of Marvel can increase Disney’s presence in the male market, and also align business product offers with the increasing trend of video game demand. Essentially, this transaction combines Marvel’s strong global brand and popular library of characters with Disney's creative skills, marketing resources, portfolio of entertainment property, financial capacity and international reach. The deal is attractive not just because of buying great characters, stories and brand, but also acquiring the people who know these characters best and how best to work with them in other media and entertainment venues. In addition, the deal is expected to benefit Marvel’s retail efforts, being able to leverage Disney’s shelf space and relationships with major chains and distributors. Ultimately, this provides Disney with a greater ability to provide quality branded content to a larger more diverse audience while enhancing Marvel’s and its Entertainment Studios’ growth. To deal with potential licensing challenges, Disney will ensure the following:

Existing licensing and distribution deals remain where they are. With respect to Paramount’s distribution deal with Marvel and the Iron Man franchise, Disney

will respect the deal that’s in place, but overtime, Disney will become the sole distributor of Marvel films.

FIRST CONTACT

Given management preferences of a ‘friendly’ acquisition and target firm being publically traded, the first contact should be initiated through an intermediary at the highest level possible. Extreme discretion should be exercised in order not to put Marvel “into play” without its consent. Once Marvel’s chairman opens up to the prospect, a meeting is arranged between Robert Iger, President and CEO of Disney and Isaac Perlmutter, Chairman and CEO of Marvel. During this meeting no mention of offer price should be made. Instead, a value range could be implied. The focus of the meeting should be on future plans, synergy, and relationship building among both management teams. Discussions can revolve with regards to the benefits each company could have by merging. No sensitive information is disclosed until

Acquisition Team Project Disney + Marvel

23