Embed Size (px)

Citation preview

Telkom South Africa

Madiba Magic

James BarberAngela Fung

Sandeep ToshniwalBecky Voorheis

Case Background• Setting

– February 1997– Post-apartheid, privatization phase in South

Africa– Bidding war for 30% ownership in Telkom

• currently owned 100% by the SA government

• Protagonists– South African government– SBC Communications Inc.– Telekom Malaysia

Major Themes

I.Opportunity

II. Risks &Concerns

III. Thintana Consortium

IV. Valuation

Major Themes

I.Opportunity

II. Risks &Concerns

III. Thintana Consortium

IV. Valuation

I. Opportunity

• Telecommunications • Telkom• South Africa

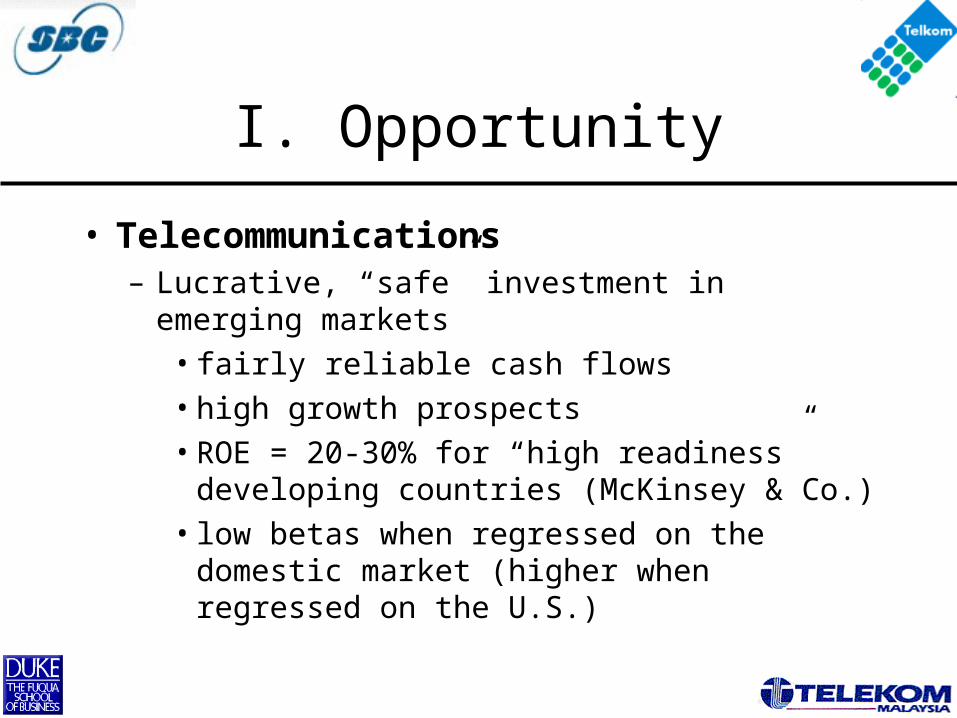

I. Opportunity

• Telecommunications – Lucrative, “safe” investment in emerging

markets• fairly reliable cash flows• high growth prospects • ROE = 20-30% for “high readiness”

developing countries (McKinsey & Co.)• low betas when regressed on the

domestic market (higher when regressed on the U.S.)

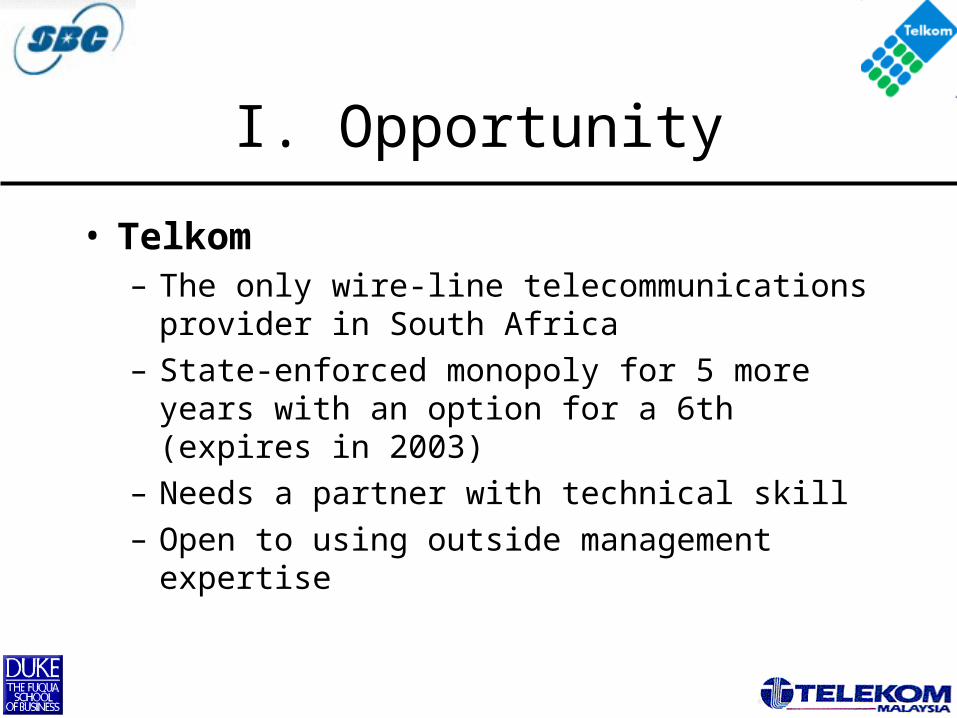

I. Opportunity

• Telkom– The only wire-line telecommunications

provider in South Africa– State-enforced monopoly for 5 more years

with an option for a 6th (expires in 2003)– Needs a partner with technical skill– Open to using outside management

expertise

I. Opportunity• South Africa

– End of apartheid opened SA to foreign investment• new government friendly to foreign investment

– A hybrid of the 1st and 3rd worlds• highly developed manufacturing sector, infrastructure

– A “gateway” to Africa• “Sets the pace for the rest of Africa.” • the most diverse, advanced economy in Africa• 40% of telecom traffic in all of Africa

– Real option

• an export/import platform into Africa, Mid-East, Asia

I. Opportunity

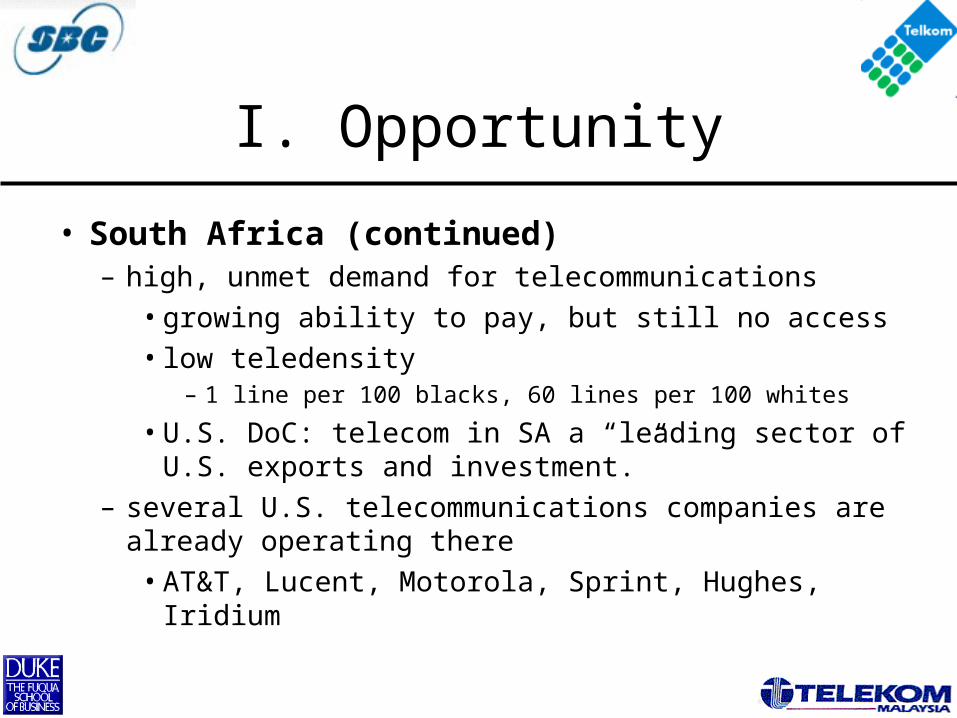

• South Africa (continued)– high, unmet demand for telecommunications

• growing ability to pay, but still no access• low teledensity

– 1 line per 100 blacks, 60 lines per 100 whites

• U.S. DoC: telecom in SA a “leading sector of U.S. exports and investment.”

– several U.S. telecommunications companies are already operating there• AT&T, Lucent, Motorola, Sprint, Hughes, Iridium

Major Themes

I.Opportunity

II. Risks &Concerns

III. Thintana Consortium

IV. Valuation

II. Risks & Concerns

• Country Risks • Company Risks

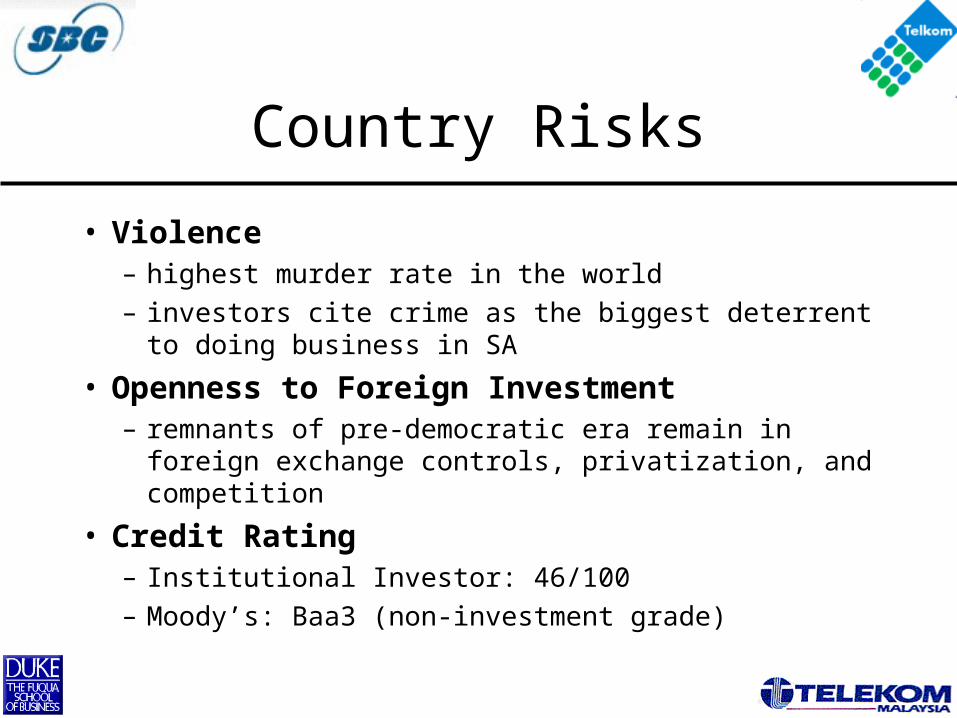

Country Risks

• Violence– highest murder rate in the world– investors cite crime as the biggest deterrent to

doing business in SA

• Openness to Foreign Investment– remnants of pre-democratic era remain in foreign

exchange controls, privatization, and competition

• Credit Rating– Institutional Investor: 46/100– Moody’s: Baa3 (non-investment grade)

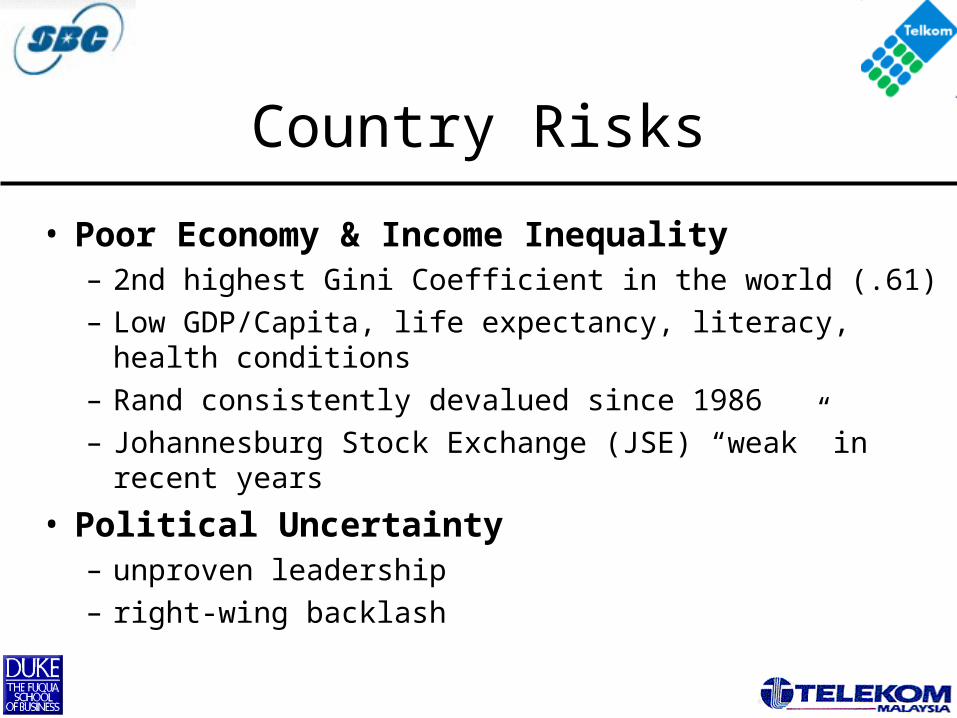

Country Risks

• Poor Economy & Income Inequality– 2nd highest Gini Coefficient in the world (.61)– Low GDP/Capita, life expectancy, literacy, health

conditions– Rand consistently devalued since 1986– Johannesburg Stock Exchange (JSE) “weak” in recent

years

• Political Uncertainty– unproven leadership– right-wing backlash

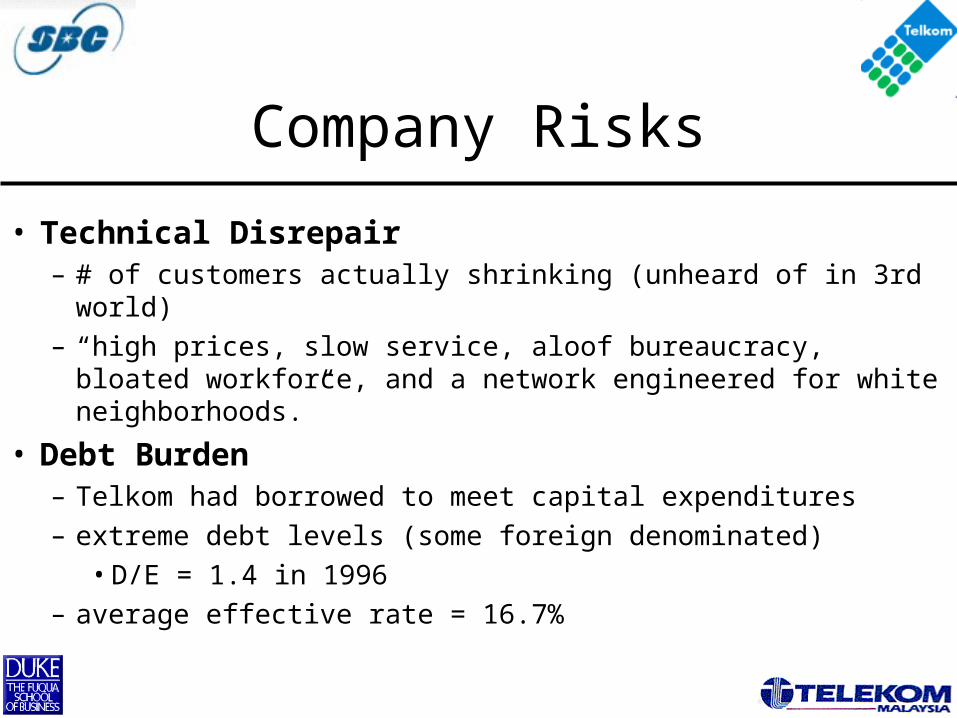

Company Risks

• Technical Disrepair– # of customers actually shrinking (unheard of in 3rd world)– “high prices, slow service, aloof bureaucracy, bloated

workforce, and a network engineered for white neighborhoods.”

• Debt Burden– Telkom had borrowed to meet capital expenditures– extreme debt levels (some foreign denominated)

• D/E = 1.4 in 1996– average effective rate = 16.7%

Company Risks

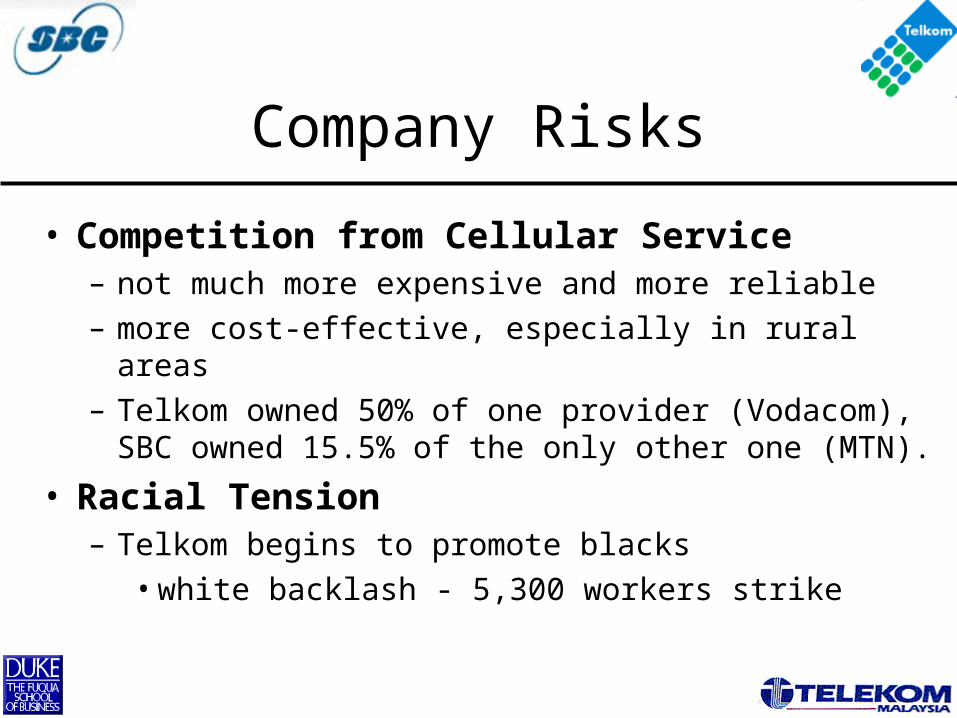

• Competition from Cellular Service– not much more expensive and more reliable– more cost-effective, especially in rural areas– Telkom owned 50% of one provider (Vodacom),

SBC owned 15.5% of the only other one (MTN).

• Racial Tension– Telkom begins to promote blacks

• white backlash - 5,300 workers strike

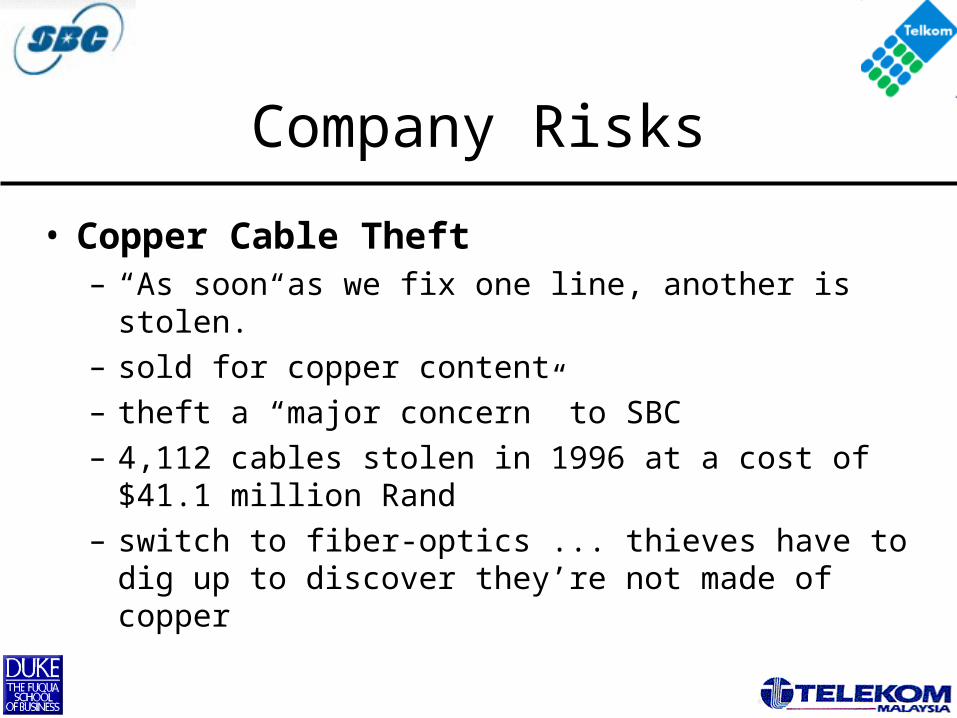

Company Risks

• Copper Cable Theft– “As soon as we fix one line, another is stolen.”– sold for copper content– theft a “major concern” to SBC– 4,112 cables stolen in 1996 at a cost of $41.1

million Rand– switch to fiber-optics ... thieves have to dig up to

discover they’re not made of copper

Major Themes

I.Opportunity

II. Risks &Concerns

III. Thintana Consortium

IV. Valuation

III. Thintana Consortium

• Rationale & Structure• Telekom Malaysia• SBC Communications, Inc.

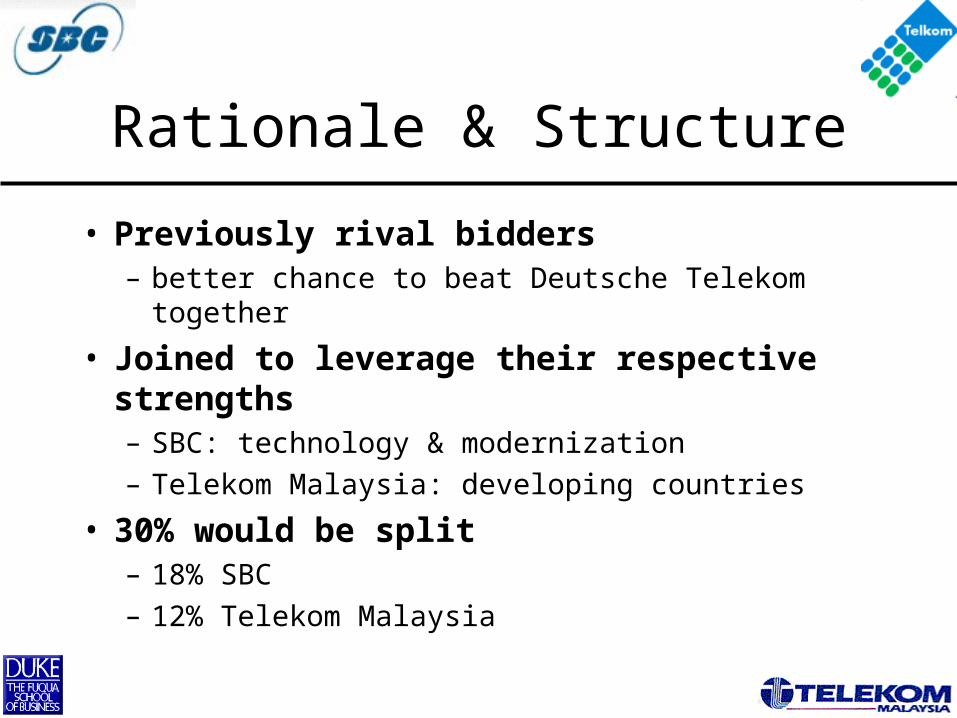

Rationale & Structure

• Previously rival bidders– better chance to beat Deutsche Telekom

together

• Joined to leverage their respective strengths– SBC: technology & modernization– Telekom Malaysia: developing countries

• 30% would be split– 18% SBC– 12% Telekom Malaysia

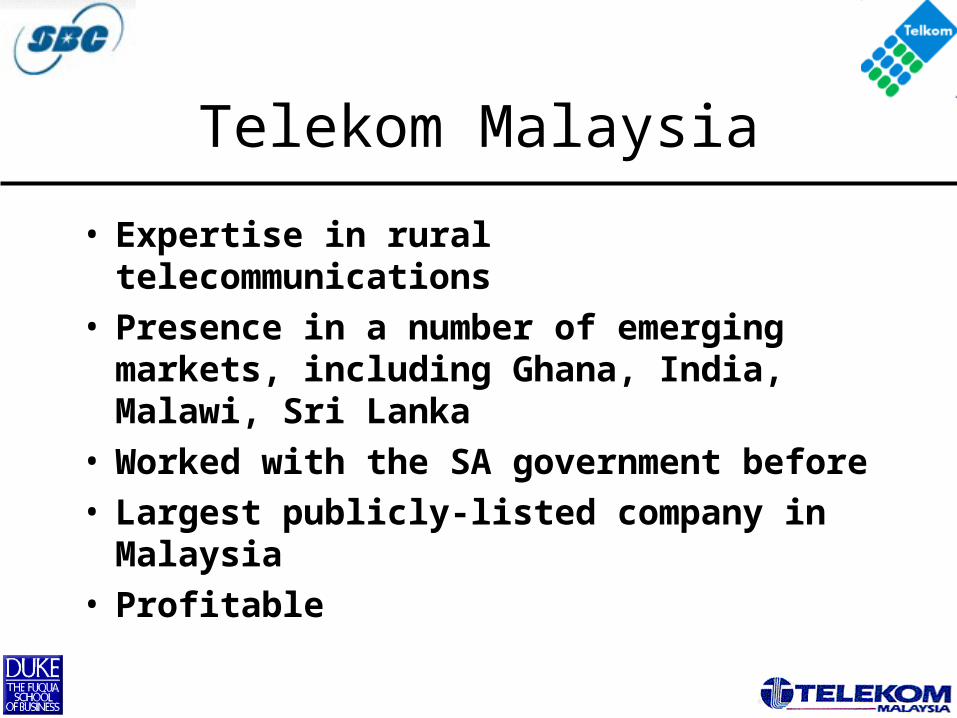

Telekom Malaysia

• Expertise in rural telecommunications• Presence in a number of emerging

markets, including Ghana, India, Malawi, Sri Lanka

• Worked with the SA government before

• Largest publicly-listed company in Malaysia

• Profitable

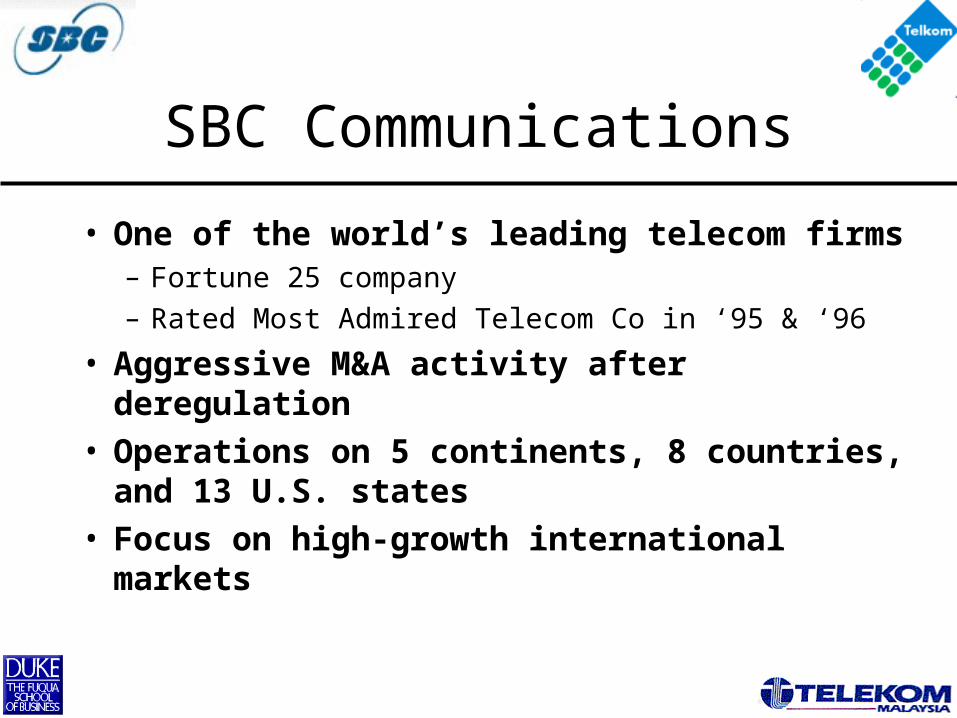

SBC Communications

• One of the world’s leading telecom firms– Fortune 25 company– Rated Most Admired Telecom Co in ‘95 & ‘96

• Aggressive M&A activity after deregulation

• Operations on 5 continents, 8 countries, and 13 U.S. states

• Focus on high-growth international markets

Major Themes

I.Opportunity

II. Risks &Concerns

III. Thintana Consortium

IV. Valuation

IV. Valuation

• Major uncertainties

• What actually happened & our model

Discussion

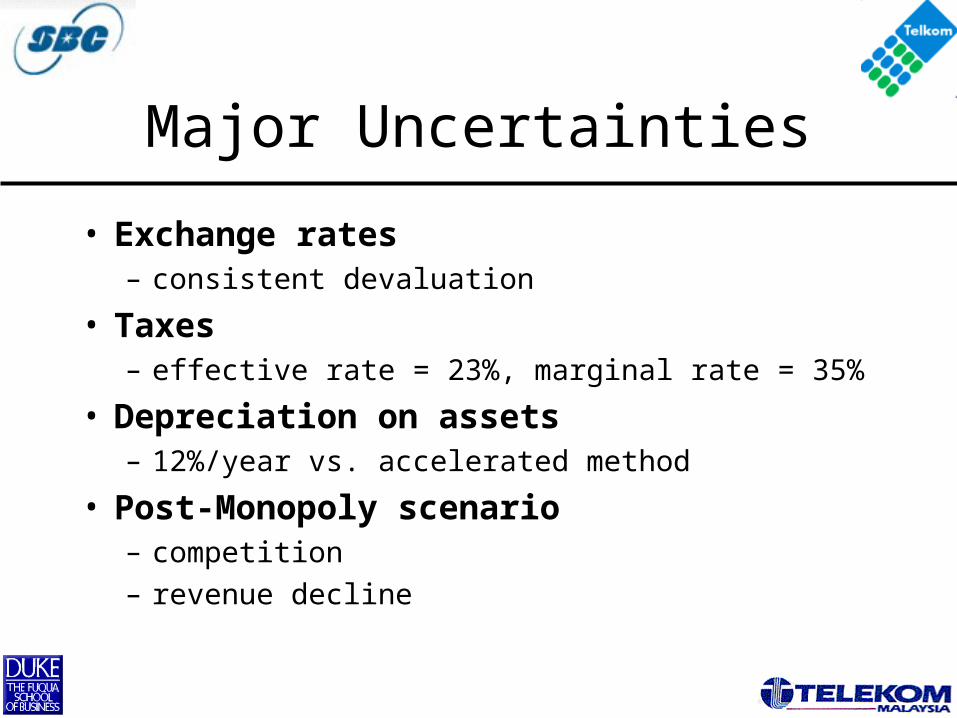

Major Uncertainties

• Exchange rates– consistent devaluation

• Taxes– effective rate = 23%, marginal rate = 35%

• Depreciation on assets– 12%/year vs. accelerated method

• Post-Monopoly scenario– competition– revenue decline

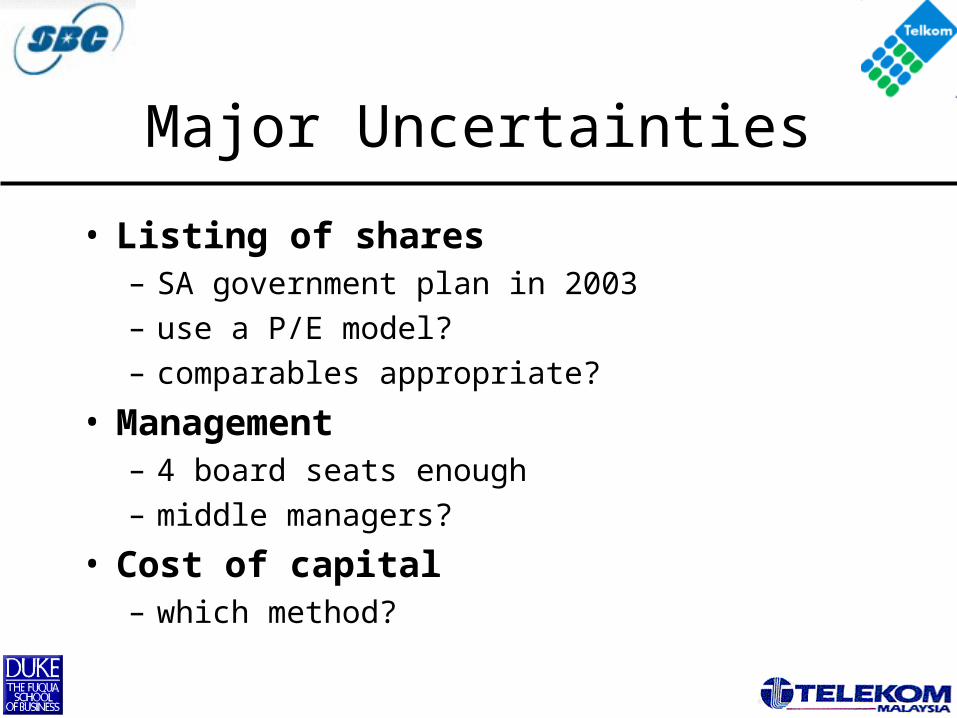

Major Uncertainties

• Listing of shares– SA government plan in 2003– use a P/E model?– comparables appropriate?

• Management– 4 board seats enough– middle managers?

• Cost of capital– which method?

Discussion

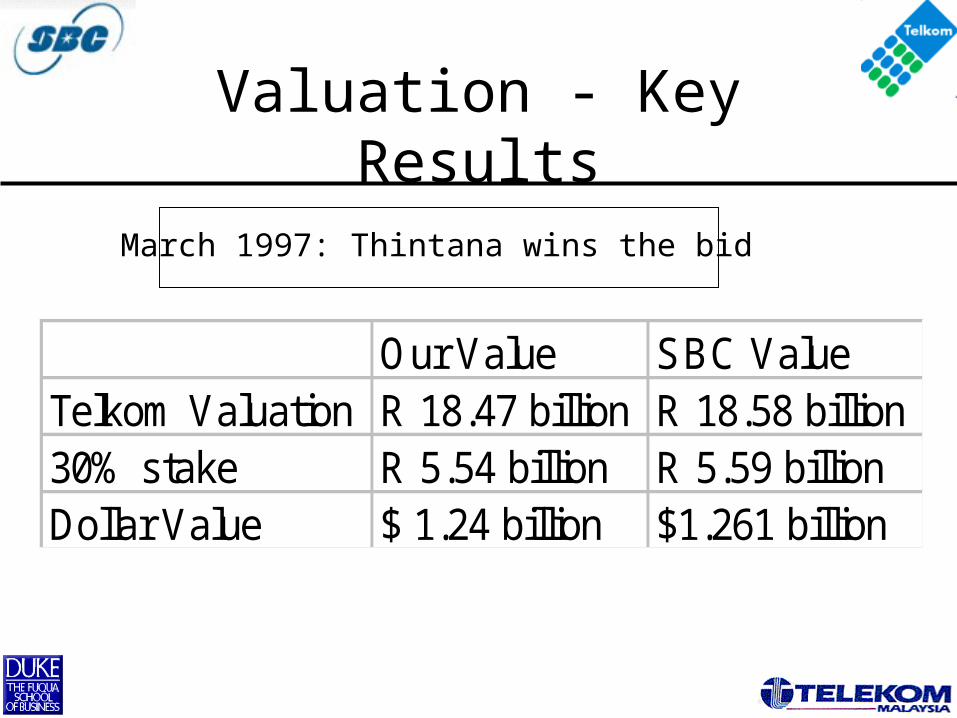

Valuation - Key Results

Our Value SBC ValueTelkom Valuation R 18.47 billion R 18.58 billion30% stake R 5.54 billion R 5.59 billionDollar Value $ 1.24 billion $1.261 billion

March 1997: Thintana wins the bid

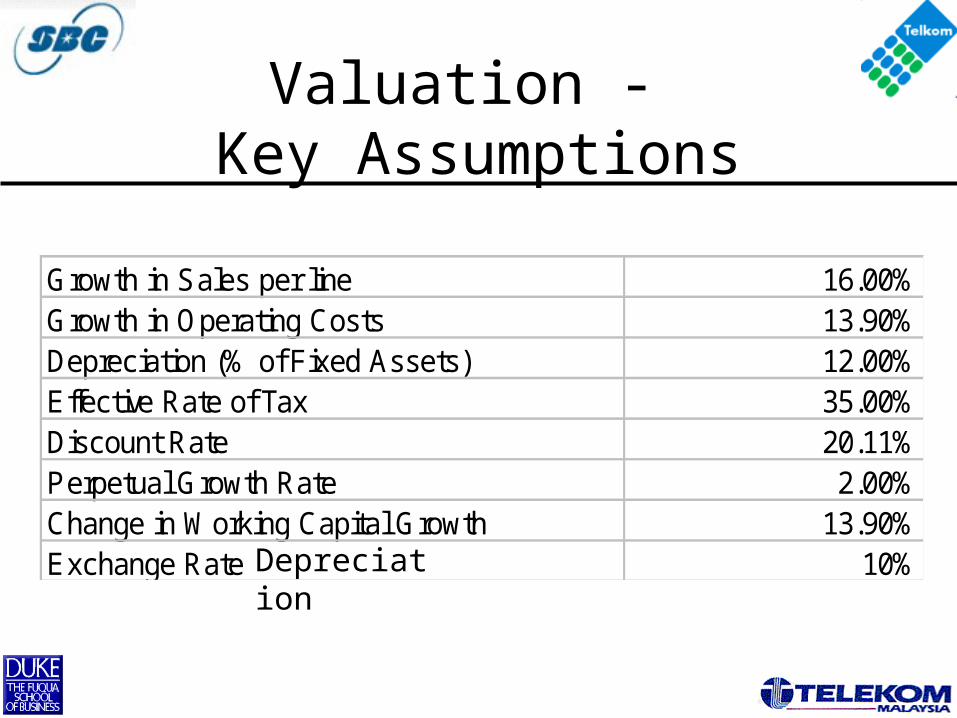

Valuation - Key Assumptions

Growth in Sales per line 16.00%Growth in Operating Costs 13.90%Depreciation (% of Fixed Assets) 12.00%Effective Rate of Tax 35.00%Discount Rate 20.11%Perpetual Growth Rate 2.00%Change in Working Capital Growth 13.90%Exchange Rate 10%Depreciation

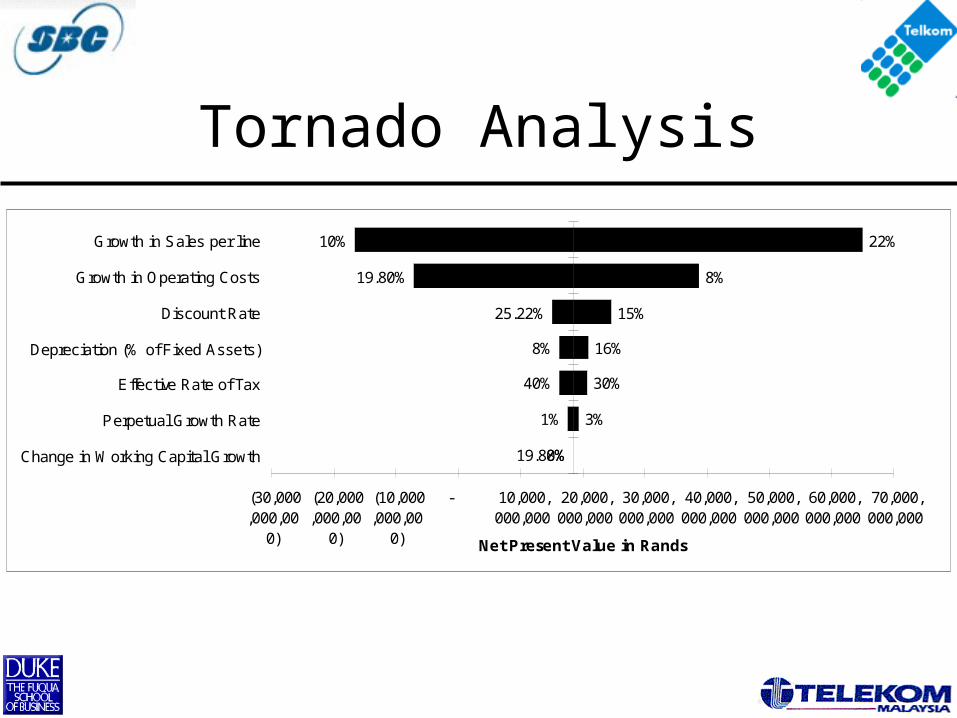

Tornado Analysis

10%

8%

15%

8%

30%

1%

8%

22%

19.80%

25.22%

16%

40%

3%

19.80%

(30,000,000,00

0)

(20,000,000,00

0)

(10,000,000,00

0)

- 10,000,000,000

20,000,000,000

30,000,000,000

40,000,000,000

50,000,000,000

60,000,000,000

70,000,000,000

Growth in Sales per line

Growth in Operating Costs

Discount Rate

Depreciation (% of Fixed Assets)

Effective Rate of Tax

Perpetual Growth Rate

Change in Working Capital Growth

Net Present Value in Rands

Assumptions

• Growth in sales and costs per line– Based on historical figures and Telkom’s

statements

• Depreciation– Allowed rate of depreciation by South Africa

• Tax Rate– Maximum tax rate applicable in South Africa

• Change in Working Capital– Linked to operating costs

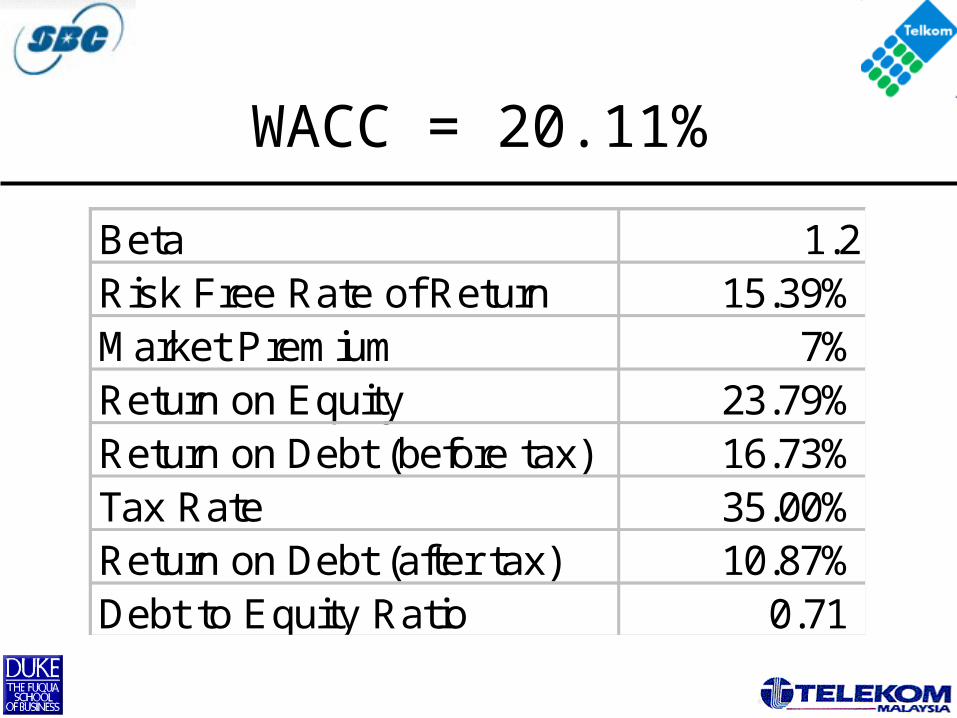

WACC = 20.11%

Beta 1.2Risk Free Rate of Return 15.39%Market Premium 7%Return on Equity 23.79%Return on Debt (before tax) 16.73%Tax Rate 35.00%Return on Debt (after tax) 10.87%Debt to Equity Ratio 0.71

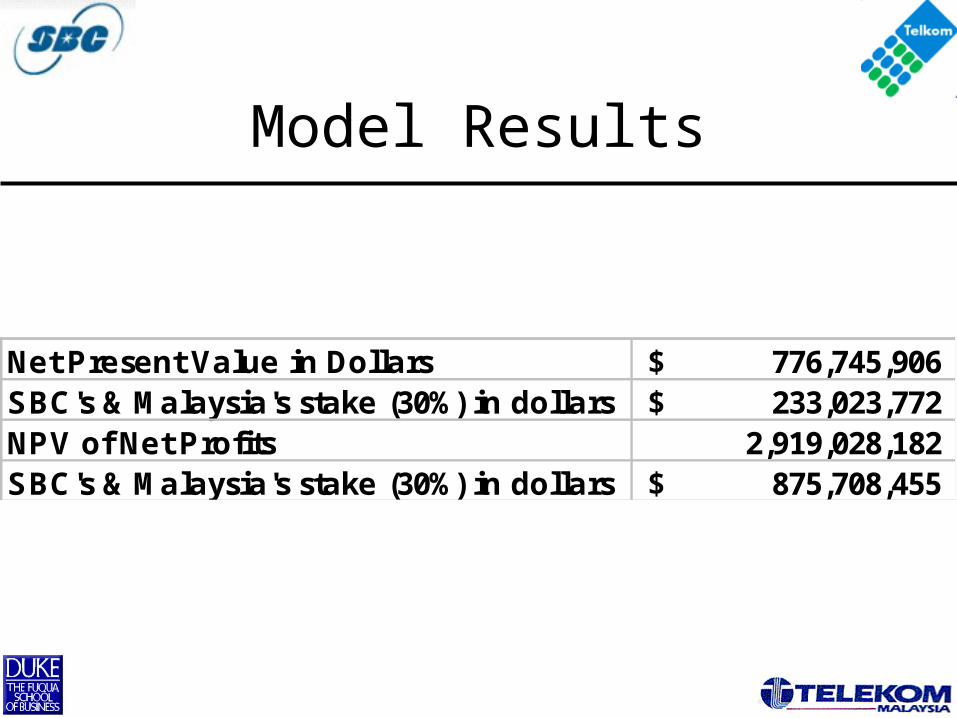

Model Results

Net Present Value in Dollars 776,745,906$ SBC's & Malaysia's stake (30%) in dollars 233,023,772$ NPV of Net Profits 2,919,028,182 SBC's & Malaysia's stake (30%) in dollars 875,708,455$