Embed Size (px)

Citation preview

MALAYSIASMALL AND MEDIUM ENTERPRISES BUILDING AN ENABLING ENVIRONMENT

MALAYSIASMALL AND MEDIUM ENTERPRISESBUILDING AN ENABLING ENVIRONMENT

Published by the

United Nations Development Programme (UNDP), Malaysia

© UNDP. All rights reserved

First published in January 2007

ISBN 983-40995-8-4

United Nations Development Programme

Wisma UN, Block C, Kompleks Pejabat Damansara

Jalan Dungun, Damansara Heights, 50490 Kuala Lumpur, Malaysia

www.undp.org.my

Design: Thumb-Print Studio Sdn Bhd

Printed in Malaysia

Foreword

iii

Globalization has brought about many changes for both developed and developing

countries. Greater access to global markets has allowed countries to increase

economic growth and reduce poverty rates. In an increasingly globalized and

competitive world economic environment, Malaysia’s commitment to international trade has

seen the country transform itself from an economy dependent on rubber and tin production,

to one of the world’s leading exporters of electrical and electronic products.

In this rapidly changing global economy, Small and Medium Enterprises (SMEs) are

increasingly a force for national economic growth. The development of diverse and

competitive SMEs is crucial for creating economic resilience and contributing towards growth.

Since independence Malaysia has achieved many national development goals and

nearly all of the Millennium Development Goals (MDGs). For example, the MDG target to

reduce the proportion of the population living below the poverty line by 50 per cent between

1990 and 2015 was achieved in 1999 when Malaysia’s poverty rate fell from 16.5 per cent in

1990 to just 7.5 per cent. By 2006 the national poverty rate was just 5 per cent. The growth

and development of Malaysia’s SMEs have markedly contributed to employment creation and,

through it, poverty reduction.

Malaysia has established SME business incubation centres, and an SME Bank to meet

the financing needs of SMEs. SMEs are contributing significantly to the growth and value

added of the services and manufacturing sectors, and they form the seedbed from which

future Malaysian global corporations can arise. They can and do play a central role in the

deepening of key industries through inter-firm backward and forward linkages.

This publication outlines Malaysia’s success in developing SMEs. It begins by providing

some basic background on SMEs, the challenges they face in the light of globalization and

technological change and how these challenges are being supported by government. It also

provides a summary of current policy on SMEs wherein the Ninth Malaysia Plan (NMP)

2006–2010 strategises for the development of a competitive, innovative and technologically

strong SME base.

UNDP Malaysia is actively engaged in supporting national efforts in promoting

interregional South-South Cooperation, particularly Asia-Africa partnerships to strengthen

SME development. For example, UNDP is currently working with the Development Bank of

Malaysia to share good practices in Credit Analysis and Development Finance for SMEs in

nine countries in Sub-Saharan Africa. UNDP Malaysia would like to express its sincere

appreciation to the Special Unit for South-South Cooperation for its continued encouragement

and support for such partnerships.

I would like to conclude by thanking Mr. Mohd Ghazali Mohd Yunos, Standard and

Industrial Research Institute of Malaysia (SIRIM); Professor Suresh Narayanan, University Sains

Malaysia; Ms. Wong Lai Sum, Malaysia External Trade Development Corporation and

Ms. Harbans Kaur, Programme Associate, UNDP Malaysia, for their good inputs towards the

preparation of this publication. I would also like to thank Bank Negara Malaysia for providing

comments on an earlier draft. I hope this publication will prove useful to policymakers in

developing countries looking to strengthen the SME sector.

iv

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

Richard Leete PhD

UN Resident Coordinator

UNDP Resident Representative for Malaysia, Singapore and Brunei Darussalam

November 2006

v

Foreword ...iii

List of Boxes, Figures and Tables ...vi

List of Abbreviations ...vii

Chapter 1: SMEs in Malaysia ...1

Chapter 2: Challenge of Globalization for SMEs ...8

Chapter 3: SME Policy and Institutional Framework ...14

Chapter 4: Practices to Promote SME Growth ...25

Chapter 5: Conclusions ...30

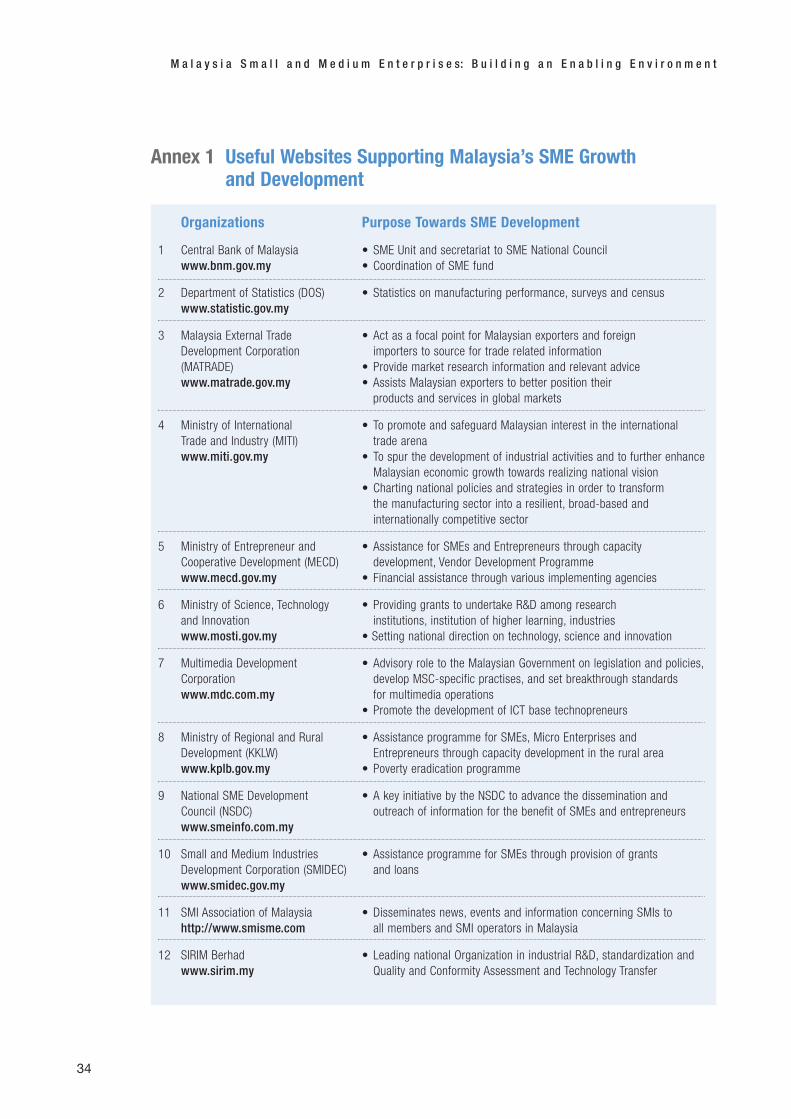

Annex 1 Useful Websites Supporting Malaysia’sSME Growth and Development ...34

References ...35

Contents

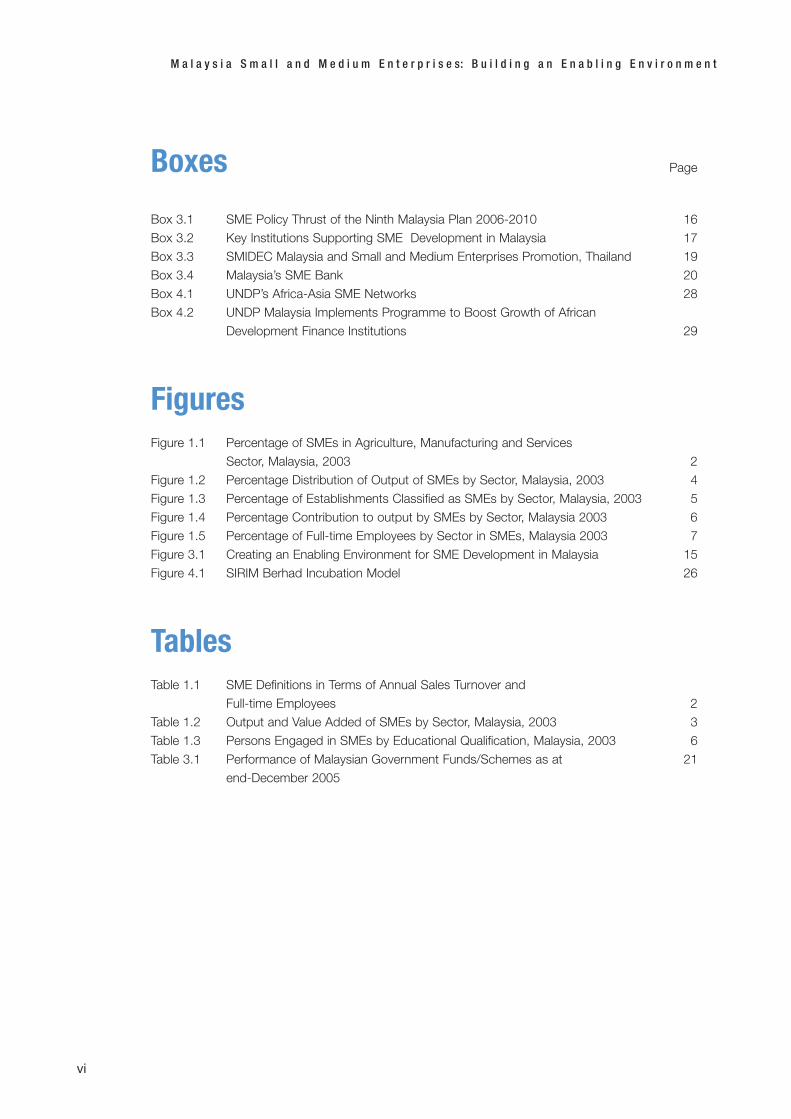

Boxes Page

Box 3.1 SME Policy Thrust of the Ninth Malaysia Plan 2006-2010 16

Box 3.2 Key Institutions Supporting SME Development in Malaysia 17

Box 3.3 SMIDEC Malaysia and Small and Medium Enterprises Promotion, Thailand 19

Box 3.4 Malaysia’s SME Bank 20

Box 4.1 UNDP’s Africa-Asia SME Networks 28

Box 4.2 UNDP Malaysia Implements Programme to Boost Growth of African

Development Finance Institutions 29

FiguresFigure 1.1 Percentage of SMEs in Agriculture, Manufacturing and Services

Sector, Malaysia, 2003 2

Figure 1.2 Percentage Distribution of Output of SMEs by Sector, Malaysia, 2003 4

Figure 1.3 Percentage of Establishments Classified as SMEs by Sector, Malaysia, 2003 5

Figure 1.4 Percentage Contribution to output by SMEs by Sector, Malaysia 2003 6

Figure 1.5 Percentage of Full-time Employees by Sector in SMEs, Malaysia 2003 7

Figure 3.1 Creating an Enabling Environment for SME Development in Malaysia 15

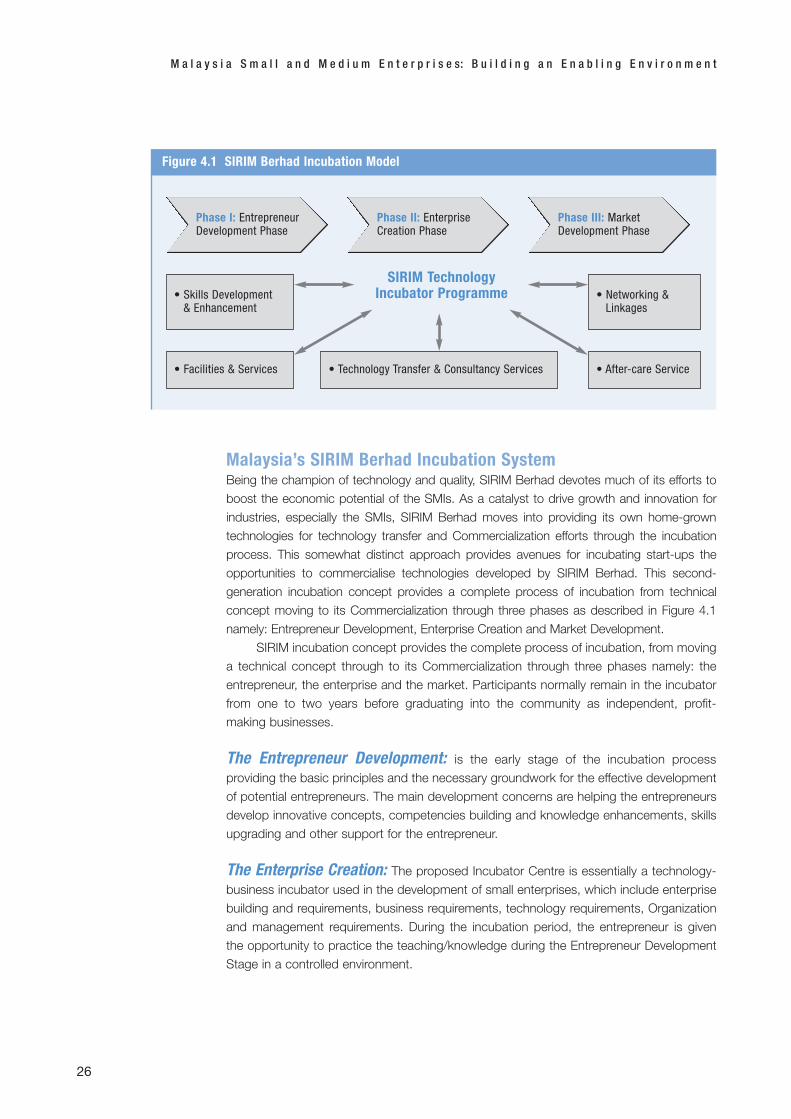

Figure 4.1 SIRIM Berhad Incubation Model 26

TablesTable 1.1 SME Definitions in Terms of Annual Sales Turnover and

Full-time Employees 2

Table 1.2 Output and Value Added of SMEs by Sector, Malaysia, 2003 3

Table 1.3 Persons Engaged in SMEs by Educational Qualification, Malaysia, 2003 6

Table 3.1 Performance of Malaysian Government Funds/Schemes as at 21

end-December 2005

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

vi

Abbreviations

AASME Africa-Asia SME Network Programme

AFTA Asean Free Trade Area

ASEAN Association of Southeast Asian Nations

B2B Business to Business

B2C Business-to-Consumer

BCIC Bumiputra Commercial and Industrial Community

CAD Computer Aided Design

CGC Credit Guarantee Corporation Malaysia

CNC Computer Numerically Controlled

CRDF Commercialization of Research and Development Fund

CRM Customer Relationship Management

DOS Department of Statistics

E&E Electrical and Electronic

EMP Eighth Malaysia Plan

ERP Enterprise Resource Planning

FDI Foreign Direct Investments

GDP Gross Domestic Product

GLCs Government-linked companies

HRDF Human Resource Development Fund

ICA Industrial Control Act

ICT Information and Communication Technology

IGS Industry Grant Scheme

IMP2 Second Industrial Master Plan

IT Information Technology

ITAF Industrial Technical Assistance Fund

IRPA Intensification of Research in Priority Areas

JICA Japan International Cooperation Agency

LAN Local Area Network

LCR Local Content Requirement

LMCP Local Material Content Programme

MARA Majlis Amanah Rakyat

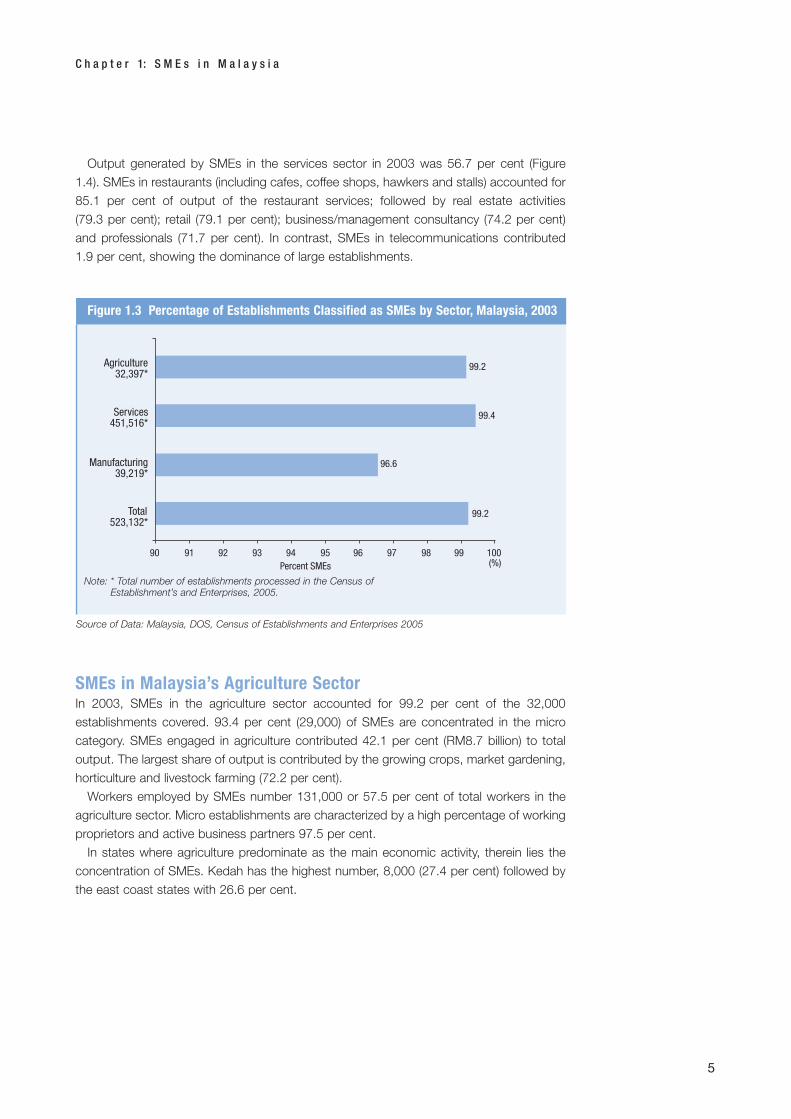

MATRADE Malaysia External Trade Development Corporation

MDGs Millennium Development Goals

MECD Ministry of Entrepreneur and Co-operative Development

MGS Multimedia Super Corridor Research and Development Grant Scheme

MIDA Malaysian Industrial Development Authority

MDC Multimedia Development Corporation

MITI Ministry of International Trade and Industry

MNCs Multinational Corporations

MSC Multimedia Super Corridor

MTDC Malaysian Technology Development Corporation

vii

Abbreviations (cont’d)NEPAD New Partnership for Africa’s Development

NITA National IT Agenda

NMP Ninth Malaysia Plan

NSDC National SME Development Council

OBMs Original Brand Manufacturers

ODMs Original Design Manufacturers

OEMs Original Equipment Manufacturers

PDC Penang Development Corporation

PSDC Penang Skills Development Corporation

PROTON Perusahaan Otomobil Nasional Berhad

R&D Research and Development

RRIM Rubber Research Institute of Malaysia

S&T Science and Technology

SCM Supply Chain Management

SEDC State Economic Development Corporations

SME Small and Medium Enterprises

SMI Small and Medium Sized Industries

SMIDEC Small and Medium Industries Development Corporation

SIRIM Standard and Industrial Research Institute of Malaysia

SMP Seventh Malaysia Plan

TAF Technology Acquisition Fund

TDF Technopreneur Development Flagship

TNCs Transnational Corporations

UNDP United Nations Development Programme

VDP Vendor Development Programme

WTO World Trade Organization

viii

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

SMEs in Malaysia

1

Over the years, SMEs in Malaysia have evolved to become key suppliers and

service providers to large corporations, inclusive of multinational and trans-

national corporations. Principally, they have contributed to:

• Expanding output;

• Providing value-added activities in the manufacturing sector;

• Creating employment opportunities especially in the services sector; and

• Contributing to broadening Malaysia’s export base.

The 2005 Census of Establishment and Enterprises1 indicates that 99 per cent of 519,000

business establishments in Malaysia are small and medium enterprises, of which 412,000

are micro enterprises. Most of these SMEs are in the services sector, particularly in retail,

restaurant and wholesale businesses. Total employment in SMEs accounted for more than

3 million workers, and generated RM 154 billion of value-added in 2003.

Definitions of SMEs2

Before the formation of the National SME Development Council (NSDC) in June 2004,

there was no standard definition of SMEs in use in Malaysia. Different agencies defined

SMEs based on their own criteria, usually benchmarking against annual sales turnover,

number of full-time employees and/or shareholders funds. For example, the Small and

Medium Industries Development Corporation (SMIDEC) defined SMEs as enterprises with

annual sales turnover not exceeding RM25 million3 and with full-time employees not

exceeding 150. Bank Negara Malaysia (Central Bank), defined SMEs as enterprises with

shareholders funds of less than RM10 million (NSDC 2005).

The absence of a standard definition prevented the collection and compilation of

uniform SME data for assessment of development needs and business performance

across the economic sectors. In order to assist in the better identification of SMEs across

all sectors, and for more effective targeting of SMEs with respect to the design of policies

and programmes, in 2005 the NSDC introduced a new definition for SMEs in the

manufacturing, manufacturing related services, primary agriculture and services sector

(NSDC 2005).

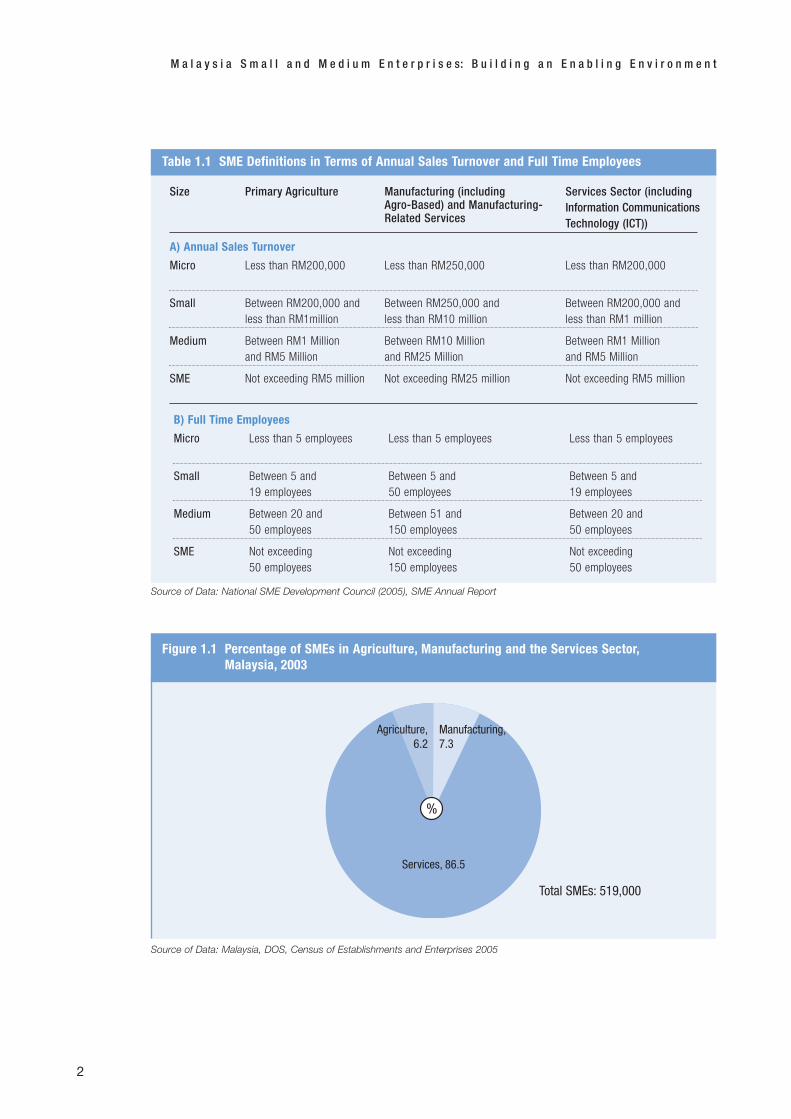

The criteria used in defining SMEs are based on annual sales turnover and number

of employees of the SMEs (Table 1.1). A broad definition of SMEs is provided, along with

specific definitions for micro, small and medium enterprises. For wider coverage,

businesses are considered as SMEs as long as they meet either the threshold set for

annual sales turnover, or in terms of the number of full-time employees (NSDC 2005).

1 Preliminary Assessment2 The Guideline on “Definitions of SMEs in Malaysia” was issued by the Secretariat, Bank Negara Malaysia

on 13 September 2005 for circulation to Ministries and Agencies, as well as financial institutions.3 In November 2005 the exchange rate for the Malaysian Ringgit is approximately MYR3.60 to USD1.00.

2

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

Source of Data: National SME Development Council (2005), SME Annual Report

Table 1.1 SME Definitions in Terms of Annual Sales Turnover and Full Time Employees

Size

Micro

Small

Medium

SME

Less than RM200,000

Between RM200,000 and less than RM1million

Between RM250,000 andless than RM10 million

Between RM10 Millionand RM25 Million

Not exceeding RM25 million

Between RM200,000 andless than RM1 million

Between RM1 Millionand RM5 Million

Not exceeding RM5 million

Less than RM250,000 Less than RM200,000

Between RM1 Millionand RM5 Million

Not exceeding RM5 million

Primary Agriculture

A) Annual Sales Turnover

Manufacturing (including Agro-Based) and Manufacturing-Related Services

Services Sector (includingInformation CommunicationsTechnology (ICT))

Micro

Small

Medium

SME

Less than 5 employees

Between 5 and 19 employees

Between 5 and 50 employees

Between 51 and 150 employees

Not exceeding 150 employees

Between 5 and 19 employees

Between 20 and 50 employees

Not exceeding 50 employees

Less than 5 employees Less than 5 employees

Between 20 and 50 employees

Not exceeding 50 employees

B) Full Time Employees

Source of Data: Malaysia, DOS, Census of Establishments and Enterprises 2005

Services, 86.5

Agriculture,6.2

Manufacturing,7.3

%

Figure 1.1 Percentage of SMEs in Agriculture, Manufacturing and the Services Sector,Malaysia, 2003

Total SMEs: 519,000

Profile of Malaysia’s SMEsSMEs in Malaysia account for 99 per cent or 519,000 of total establishments in the three

main economic sectors of manufacturing, services and agriculture. (Figure 1.1) Large

establishments numbering 4,100 accounted for the remaining 0.8 per cent. Most of the

SMEs are found in the services sector, accounting for 86.5 per cent (Normah 2006).

In 2003 employment created by Malaysia’s SMEs was approximately 3.0 million

workers (65.1 per cent of the total employment of 4.6 million engaged in the three main

sectors). The services sector employed the largest number, 2.2 million, manufacturing,

740,000 and agriculture 131,000. 2.3 million (76.5 per cent) are full-time employees

while self-employed workers are 16.7 per cent and part-time workers, the remainder

(Normah 2006).

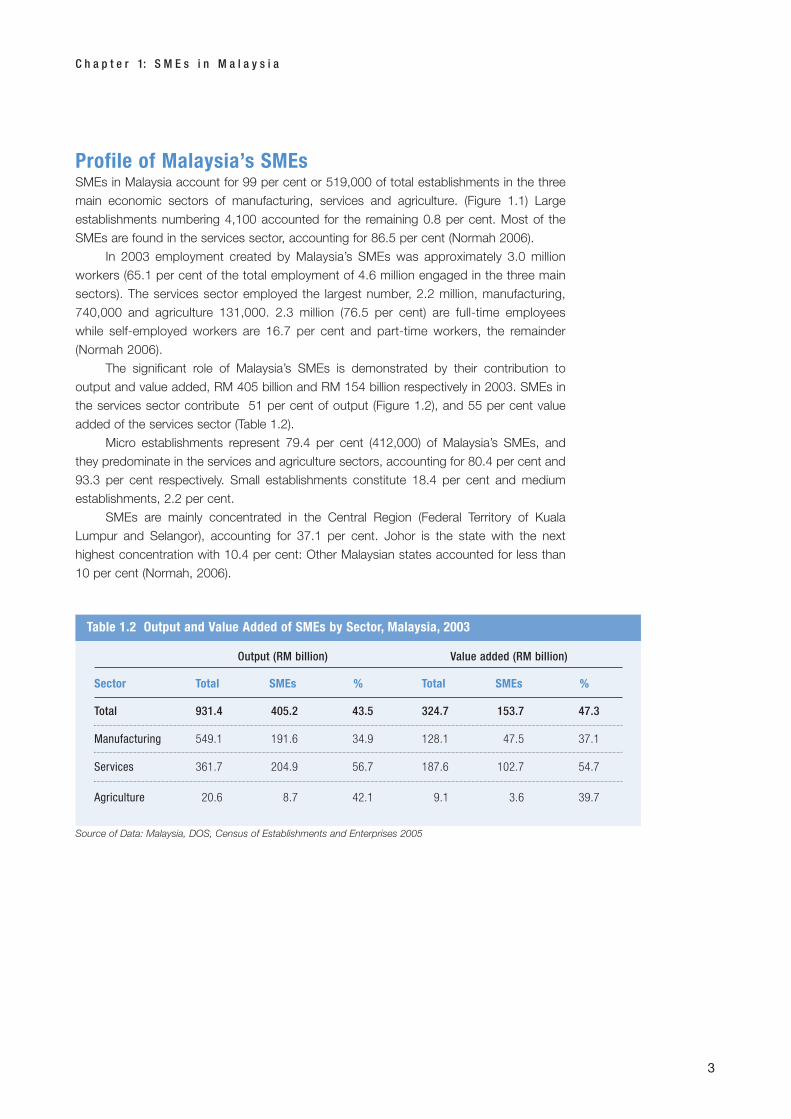

The significant role of Malaysia’s SMEs is demonstrated by their contribution to

output and value added, RM 405 billion and RM 154 billion respectively in 2003. SMEs in

the services sector contribute 51 per cent of output (Figure 1.2), and 55 per cent value

added of the services sector (Table 1.2).

Micro establishments represent 79.4 per cent (412,000) of Malaysia’s SMEs, and

they predominate in the services and agriculture sectors, accounting for 80.4 per cent and

93.3 per cent respectively. Small establishments constitute 18.4 per cent and medium

establishments, 2.2 per cent.

SMEs are mainly concentrated in the Central Region (Federal Territory of Kuala

Lumpur and Selangor), accounting for 37.1 per cent. Johor is the state with the next

highest concentration with 10.4 per cent: Other Malaysian states accounted for less than

10 per cent (Normah, 2006).

C h a p t e r 1: S M E s i n M a l a y s i a

3

Source of Data: Malaysia, DOS, Census of Establishments and Enterprises 2005

Table 1.2 Output and Value Added of SMEs by Sector, Malaysia, 2003

Output (RM billion)

Total 931.4 405.2 43.5 324.7 153.7 47.3

Manufacturing 549.1 191.6 34.9 128.1 47.5 37.1

Services 361.7 204.9 56.7 187.6 102.7 54.7

Agriculture 20.6 8.7 42.1 9.1 3.6 39.7

Sector Total SMEs % Total SMEs %

Value added (RM billion)

SMEs in Malaysia’s Manufacturing SectorIn 2003, SMEs in the manufacturing sector accounted for 96.6 per cent (38,000) of total

establishments. Micro establishments constituted 55.3 per cent with a contribution of just

2.3 per cent to output, and 1.6 per cent to value added. Conversely, medium-sized

establishments (5.2 per cent) accounted for 62.1 per cent of output and 51.0 per cent of

value added.

In 2003, 34.9 per cent of the output of the manufacturing sector was contributed by

SMEs (Table 1.2). The contribution by medium establishments was 62.1 per cent, and by

small establishments was 35.6 per cent. Micro establishments accounted 55.3 per cent of

total SMEs; its contribution in terms of output was only 2.3 per cent.

The largest number of SMEs in the manufacturing sector is found in the traditional

sectors of textiles and apparel (23.2 per cent), metal and non-metallic mineral products

(16.7 per cent) and food and beverages (15.0 per cent), whereby collectively they

generate more than half of the total value added of the sector.

In terms of employment generation, the four sub-sectors of food and beverages; wood

products and furniture; metal and non-metallic mineral products; and rubber and plastic

products contributed more than half of the employment of SMEs.

SMEs in Malaysia’s Services SectorIn 2003, SMEs accounted for 99.4 per cent (449,000) of total establishments in the

services sector (Figure 1.3). Their profile indicates that 80.4 per cent of these SMEs

are characterized as micro, 17.6 per cent as small, and 2.0 per cent as medium. More

than half of service sector SMEs are concentrated in the wholesale and retail sector,

14.5 per cent in restaurants and hotels and 6.2 per cent in transport and communications.

4

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

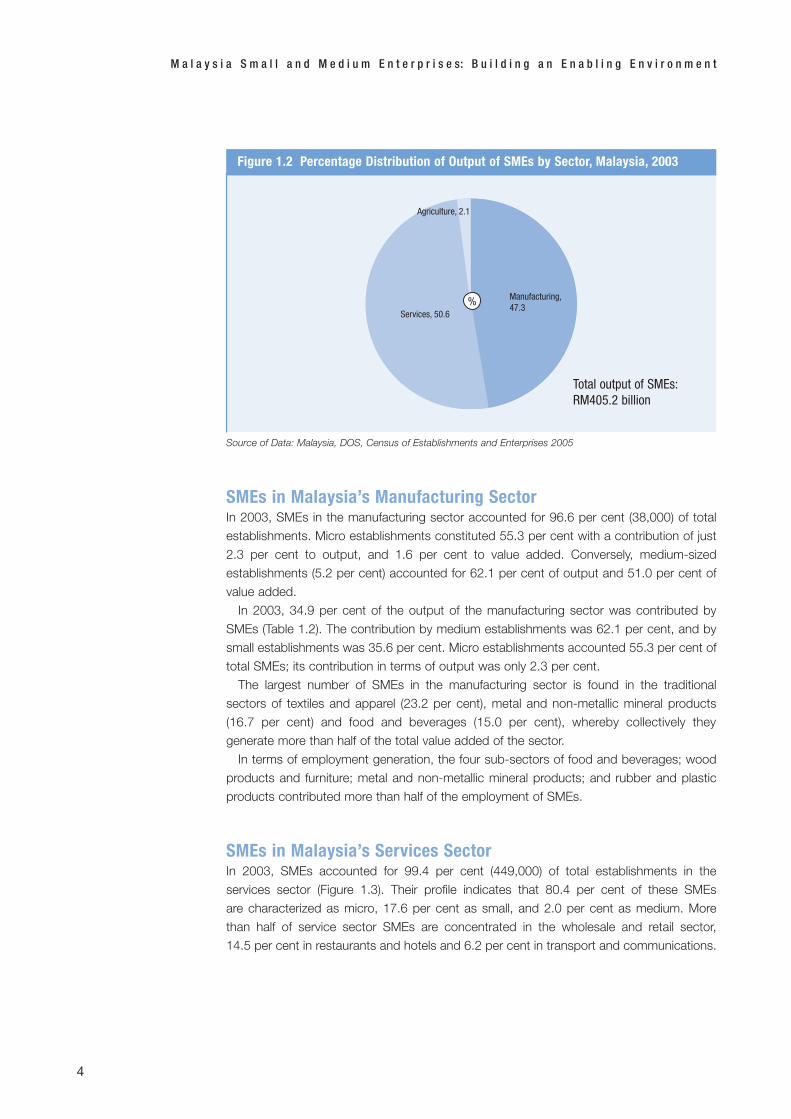

Source of Data: Malaysia, DOS, Census of Establishments and Enterprises 2005

Services, 50.6

Agriculture, 2.1

% Manufacturing,47.3

Figure 1.2 Percentage Distribution of Output of SMEs by Sector, Malaysia, 2003

Total output of SMEs:RM405.2 billion

Output generated by SMEs in the services sector in 2003 was 56.7 per cent (Figure

1.4). SMEs in restaurants (including cafes, coffee shops, hawkers and stalls) accounted for

85.1 per cent of output of the restaurant services; followed by real estate activities

(79.3 per cent); retail (79.1 per cent); business/management consultancy (74.2 per cent)

and professionals (71.7 per cent). In contrast, SMEs in telecommunications contributed

1.9 per cent, showing the dominance of large establishments.

C h a p t e r 1: S M E s i n M a l a y s i a

5

Source of Data: Malaysia, DOS, Census of Establishments and Enterprises 2005

99.2

99.4

96.6

99.2

100(%)

99 9897Percent SMEs

96 9594 93 92 91 90

Agriculture32,397*

Services451,516*

Manufacturing39,219*

Total523,132*

Figure 1.3 Percentage of Establishments Classified as SMEs by Sector, Malaysia, 2003

Note: * Total number of establishments processed in the Census ofEstablishment’s and Enterprises, 2005.

SMEs in Malaysia’s Agriculture Sector In 2003, SMEs in the agriculture sector accounted for 99.2 per cent of the 32,000

establishments covered. 93.4 per cent (29,000) of SMEs are concentrated in the micro

category. SMEs engaged in agriculture contributed 42.1 per cent (RM8.7 billion) to total

output. The largest share of output is contributed by the growing crops, market gardening,

horticulture and livestock farming (72.2 per cent).

Workers employed by SMEs number 131,000 or 57.5 per cent of total workers in the

agriculture sector. Micro establishments are characterized by a high percentage of working

proprietors and active business partners 97.5 per cent.

In states where agriculture predominate as the main economic activity, therein lies the

concentration of SMEs. Kedah has the highest number, 8,000 (27.4 per cent) followed by

the east coast states with 26.6 per cent.

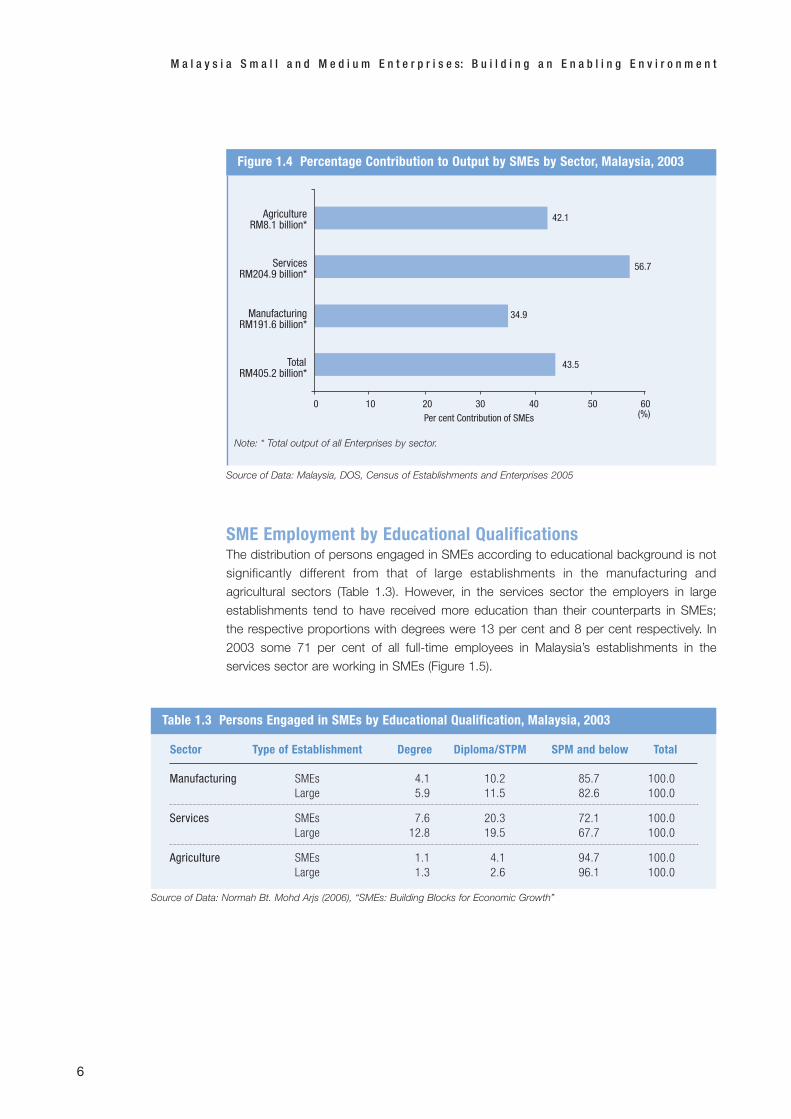

SME Employment by Educational QualificationsThe distribution of persons engaged in SMEs according to educational background is not

significantly different from that of large establishments in the manufacturing and

agricultural sectors (Table 1.3). However, in the services sector the employers in large

establishments tend to have received more education than their counterparts in SMEs;

the respective proportions with degrees were 13 per cent and 8 per cent respectively. In

2003 some 71 per cent of all full-time employees in Malaysia’s establishments in the

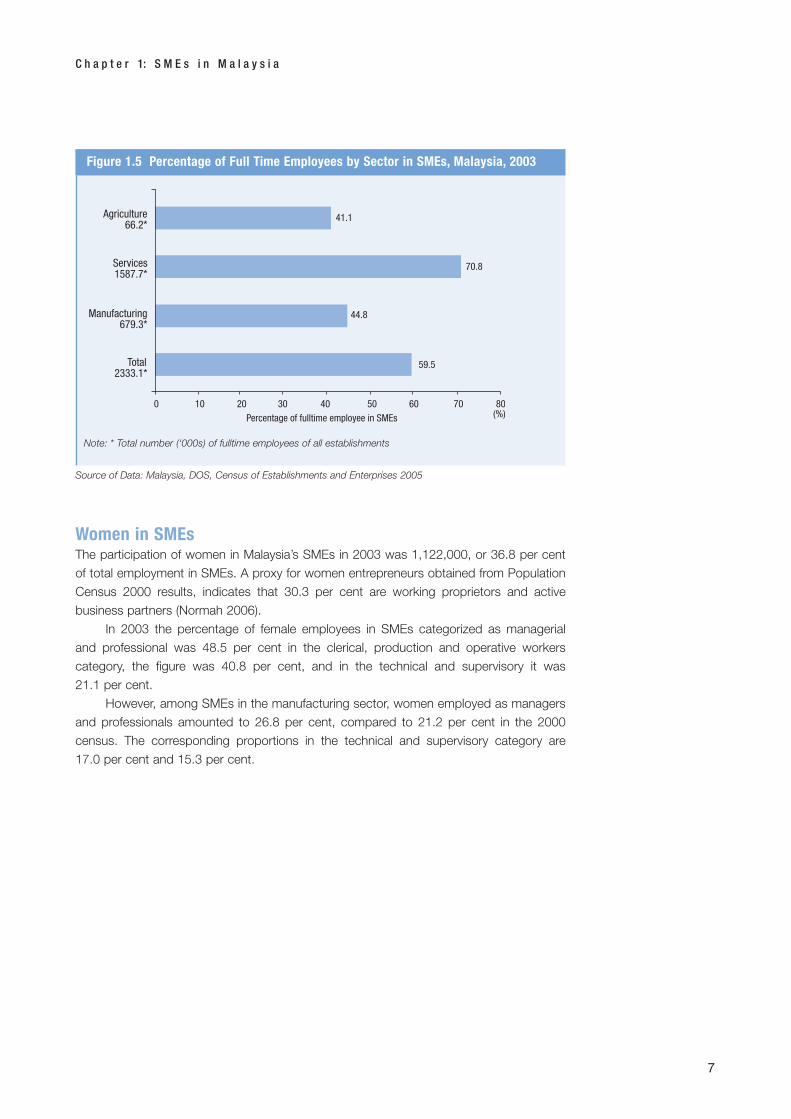

services sector are working in SMEs (Figure 1.5).

6

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

Source of Data: Malaysia, DOS, Census of Establishments and Enterprises 2005

42.1

56.7

34.9

43.5

60(%)

5040Per cent Contribution of SMEs

30 20100

AgricultureRM8.1 billion*

ServicesRM204.9 billion*

ManufacturingRM191.6 billion*

TotalRM405.2 billion*

Figure 1.4 Percentage Contribution to Output by SMEs by Sector, Malaysia, 2003

Note: * Total output of all Enterprises by sector.

Source of Data: Normah Bt. Mohd Arjs (2006), “SMEs: Building Blocks for Economic Growth”

Table 1.3 Persons Engaged in SMEs by Educational Qualification, Malaysia, 2003

SMEsLarge

SMEsLarge

SMEsLarge

4.15.9

10.211.5

85.782.6

100.0100.0

Manufacturing

Services

Agriculture

7.612.8

20.319.5

72.167.7

100.0100.0

1.11.3

4.12.6

94.796.1

100.0100.0

Sector Type of Establishment Degree Diploma/STPM SPM and below Total

Women in SMEsThe participation of women in Malaysia’s SMEs in 2003 was 1,122,000, or 36.8 per cent

of total employment in SMEs. A proxy for women entrepreneurs obtained from Population

Census 2000 results, indicates that 30.3 per cent are working proprietors and active

business partners (Normah 2006).

In 2003 the percentage of female employees in SMEs categorized as managerial

and professional was 48.5 per cent in the clerical, production and operative workers

category, the figure was 40.8 per cent, and in the technical and supervisory it was

21.1 per cent.

However, among SMEs in the manufacturing sector, women employed as managers

and professionals amounted to 26.8 per cent, compared to 21.2 per cent in the 2000

census. The corresponding proportions in the technical and supervisory category are

17.0 per cent and 15.3 per cent.

C h a p t e r 1: S M E s i n M a l a y s i a

7

Source of Data: Malaysia, DOS, Census of Establishments and Enterprises 2005

41.1

70.8

44.8

59.5

80(%)

5040Percentage of fulltime employee in SMEs

30 20100

Agriculture66.2*

Services1587.7*

Manufacturing679.3*

Total2333.1*

60 70

Figure 1.5 Percentage of Full Time Employees by Sector in SMEs, Malaysia, 2003

Note: * Total number (‘000s) of fulltime employees of all establishments

The world’s business and trade landscape continue to evolve rapidly with increasing

globalization, with implications for Malaysia’s SMEs. Among them is the growing

competition in the domestic and international markets. Whilst in the past,

Malaysia’s SMEs were to some extent “protected” through tariff and non-tariff measures

that enabled them to garner significant market share in the country, this is no longer the

case. Malaysia’s SMEs can no longer orientate their business merely towards the

domestic domain, but must seek opportunities in the global marketplace.

The proliferation of free trade agreements bilaterally, regionally and multilaterally has

brought about trade rules that are complex and difficult for SMEs to follow. The lack of

understanding often creates a feeling of being marginalized by such arrangements, rather

than being elated at the opportunities that are created by them. Increasingly, tariffs are

being reduced, and trading procedures altered, causing concern to domestic players.

Meanwhile, trade impediments in the form of trade conditionalities and other non-tariff

measures, such as labor, social, security and environmental issues continue to complicate

market access for exporters worldwide.

In Malaysia, Small and Medium Industries Development Corporation (SMIDEC)

identified some of the challenges facing SMEs, in the light of the changing global market

(SMIDEC, 2002). These include the ability to compete globally, move up the value chain

and embrace ICT and e-commerce. These challenges are closely interlinked. In order to

compete on the basis of quality, cost, reliability and speedy delivery in the global market,

SMEs must reap economies of scale. This, in turn, calls for a shift in focus from the

domestic market, towards a niche in the global supply chain.

The rapid rate of technological change implies that in order to compete globally,

SMEs must be able to adapt to keep pace with technological progress. Strong ICT

capabilities are therefore crucial because global corporations are relying increasingly on

internet-based business-to-business (B2B) community portals to source intermediate

inputs and services. In fact, the B2B systems are the fastest growing components of the

electronic-business markets. Conversely even if Malaysia’s SMEs are content to only serve

the larger, foreign owned corporations based in the country, they still need to transform

themselves to keep pace with the changes occurring in the MNCs.

Globalization and trade liberalization present two immediate challenges. First,

internet-technology and the information age have made knowledge an important input in

production. The volume of e-commerce was put at US$137 billion in 1999 and was

projected to surge to US$1.3 trillion by 2003. This is an impressive figure given that

international trade in 1998 was valued at US$10.1 trillion. B2B revenue in 2000 was

estimated at US$110 billion or 85 per cent of total e-commerce revenue. The rest

comprised of business-to-consumer (B2C) and e-commerce (Yeap, 2000). Second, a

freer and more liberalized trading environment brings new players who, alongside

strongly entrenched existing ones, threaten traditional market shares. But a more

8

Challenge of Globalization for SMEs

integrated global market also presents new opportunities and greater market access for

those who are proactive. The level of preparedness of SMEs to face these two

challenges is examined briefly below.

ICT and E CommerceAccording to the Small and Medium Industries (SMI) Association of Malaysia most local

SMEs had not installed an internal Information Technology (IT) infrastructure, such as Local

Area Network (LAN)4, and fewer than 20 per cent of SMEs had access to the Internet. In

contrast, 85 per cent of the over 7.6 million SMEs in the United States of America use the

Internet (quoted in Moreira, nd). A survey of 12,000 SMEs in Malaysia indicated that only

16 per cent had a web presence, compared to 80 per cent of similar enterprises in Europe

and North America (cited in Patrick, nd). IT implementation among SMEs in Malaysia

remains at a very basic level with most relying on computers only for simple accounting

and word processing. Usage of sophisticated applications such as Enterprise Resource

Planning (ERP), Supply Chain Management (SCM) and Customer Relationship

Management (CRM) are uncommon because their usefulness has not been fully

appreciated (Patrick, nd).

The initial outlay of installing hardware coupled with the high cost of software and

system maintenance has inhibited adoption of ICT infrastructure. The SMI Association of

Malaysia estimates that the purchase of ICT systems from big name vendors could cost

between RM10,000 to RM30,000 - beyond the budget of many SMEs unless they receive

financial assistance. Additionally, the recurring costs of ownership, such as annual licence

and maintenance fees, are also burdensome (Moreira, nd). And despite the fact that prices

have been falling, applications such as Enterprise Resource Planning (ERP) still cost

around RM40,000 (Microsoft, 2002). This is compounded by the fact that most SMEs still

depend on internal sources of financing, indirect financing and personal guarantees for

their funds (Lim, 2000). Banks, on the other hand, demand collateral before giving out

loans and many SMEs do not have savings to access loans.

Low Level of Participation in E-Commerce E-commerce has not adequately caught on among SMEs in Malaysia at present. Instead,

local SMEs have greater confidence with the more familiar regional and international trade

shows, rather than B2B portals that have a greater potential to sell their products.

Since the SMI Development Plan has identified SMEs in the Electrical and Electronic

(E&E) sector for special attention, it is necessary to evaluate their preparedness for e-

commerce. Studying SMEs in the E&E sector in Penang, Malaysia’s Silicon Island, is

particularly instructive for several reasons. First, there are more indigenously owned SMEs

within the E&E sector in Penang than in other parts of the country. Second, the majority of

the indigenous SMEs gained access to technology through the provision of ancillary

services to the MNCs. This suggests stronger linkages between the SMEs and the MNCs

in Penang than elsewhere. Third, technology transfer and diffusion have proceeded further

among the SMEs in Penang, relative to even the Klang Valley.

C h a p t e r 2: C h a l l e n g e o f G l o b a l i z a t i o n f o r S M E s

9

4 Usually made up of servers, workstations, printers, network operating systems and a communications link.

A study of SMEs in the E&E sector in Penang by How (2001) examined several aspects

pertaining to their readiness to participate in e-commerce. She surveyed 50 SMEs drawn

from the E&E sub-sector (42 per cent of the sample), metal fabrication sub-sector (30 per

cent of the sample) and plastics (28 per cent of the sample). All SMEs were serving larger

MNCs. Of the sample, 33 firms (66 per cent) were locally owned, while the rest were foreign

controlled. About 86 per cent of the sample has been in operation for over five years. In

terms of the degree of preparedness to participate in e-commerce, she investigated three

aspects: the ICT infrastructure in place, ICT related training, and the utilization of ICT-related

incentives offered by the government. The main findings from the study were:

• Nearly 73 per cent of the firms interviewed had very little or no basic ICT

infrastructure in place. These firms had no web sites, had no access to LAN and

their workers had little or no access to computers. Computers were generally

reserved for management staff or used for administrative purposes. And in many

firms computer literacy was not only poor among workers but management staff

appeared ill informed about ICT facilities. Not surprisingly, a larger proportion of

the firms with little or no ICT infrastructure were small, locally owned and located

in the plastics and metal fabrication sub sectors.

• Some 76 per cent of SMEs provided no form of ICT-related training, whether

formal or informal, to their workforce. In fact, only 14 per cent of the firms

provided formal training.

• Only 10 per cent of SMEs took advantage of incentives offered to upgrade

their preparation for e-commerce, while 44 per cent were unaware of the

incentives in place.

• Only four per cent of the firms reported involvement in e-transactions, and about

10 per cent of the firms had strategies for future participation. In fact, more than

half the firms rated their possible participation in e-commerce as very low.

The reluctance among SMEs to participate in e-commerce arise at two levels. At one level,

firms are not convinced of the benefits of e-commerce. SME owners are convinced that

their traditional customers are sufficiently numerous and will remain loyal to them, making

it unnecessary to experiment with e-commerce. Others are willing to consider switching

only if their own customers and suppliers make the switch before them. Thus, many SMEs

seem not to have appreciated fully the new opportunities that e-commerce will generate;

rather they view it as merely replacing current modes of doing business.

At another level, obstacles to adopting e-commerce relate to factors such as the

lack of trained staff, the lack of capital and apparent failure after a brief period of

experimentation, and reservation regarding the security of e-transactions.

The lack of awareness of government incentives to support the adoption of new

technology suggests that the mechanisms to publicise these incentives are faulty or

lack coverage.

Conversely, firms who have not taken advantage of the incentives, despite knowing

about them, cite several factors. First, the procedures are tedious and require intensive

documentation. Second, bureaucracy and red tape delays the processing of applications.

Undue delays reduce the usefulness of incentives. Third, many who are aware of the

incentives are unclear about the procedures of applications.

10

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

Lack of Awareness of BenefitsMalaysia’s SMEs have also been slow to capitalise on initiatives and training programmes.

For example, in 1997, seven skills development centres were set up and RM2.9 million

in grants was channeled into a sponsorship scheme for the use of SMEs. But up to

August 31, 2001, only 39.2 per cent of these grants was used for industrial automation,

Computer Aided Design, (CAD) Computer Numerically Controlled (CNC) and industrial

engineering (Moreira, nd). Of the 5,600 SMEs registered with the Human Resource

Development Fund (HRDF), 66 per cent were utilizing less than half of their levy, reflecting

an underdeveloped culture among them (Fong, 2000).

Among current SME owners, is a group that began in industry as apprentices,

lacking much formal education. According to the SMI Association, more than 60 per cent

of the SMEs owners and executives do not understand English language. Hence, they do

not attend technology conferences, seminars or exhibitions organized by big vendors—

either because they assume these are targeted at large scale enterprises or because they

are conducted in English (Moreira, nd2). There is thus an information gap about how

heavy investments in ICT can transform their operations or increase productivity. Many

firmly believe they can survive by just strengthening their links in the domestic market,

without the need for ICT. The bewildering range of choices available and the very little help

being offered in choosing the technology best suited to a particular enterprise further

hampers adoption. The longer they wait the steeper the learning curve they will face with

IT and e-commerce (cited in Microsoft, 2002)

Lack of ICT PersonnelThe lack of IT-trained personnel deprives SMEs of the capacity to oversee the

implementation of ICT systems, which typically takes six months to a year. They also

lack sales and marketing personnel who can take orders electronically, process them

and ship out the products to their customers. Some also do not have the production

capacity to meet large orders. Furthermore, the high turnover of trained personnel

inhibits investment in training.

SMEs and Malaysia’s Automotive Industry The automotive industry has been identified as a strategic industry that has great potential

to create linkages critical to Malaysia’s industrialization. Two policy instruments were

utilized to foster SMEs in the automotive industry: the Local Material Content Programme

(LMCP) and the Vendor Development Programme (VDP). The former was aimed primarily

at local assemblers of foreign cars, although the national car producers were also included

in the programme. The latter, however, was conceived as a means for the national car

producers to nurture Bumiputra auto parts and component suppliers. Thus, both

programmes contributed to the fostering of domestic SMEs in the automotive sector - one

indirectly, and the other, directly.

The LMCP requires that automotive assemblers (and later, national car producers)

substitute imported components with locally produced equivalents. However, although

C h a p t e r 2: C h a l l e n g e o f G l o b a l i z a t i o n f o r S M E s

11

this idea was formulated in the early 1970s, the promotion of local content remained

minimal well into the 1980s, primarily because numerous inefficient domestic component

suppliers produced overpriced parts of low quality. The LCR programme received a

significant boost when the first national car project undertaken by Perusahaan Otomobil

Nasional Berhad (Proton) came on stream in 1985 and was followed by a second national

car project in 1993. Both ventures benefited from heavy protection and provided new

impetus to the development of local parts and components manufacturers.

Since 1988, the VDP has been pursued aggressively to spur the growth of

Bumiputra suppliers to the automotive industry. Besides guaranteeing markets for the

output of these SMEs, they were offered financial and technical assistance by the anchor

(or parent) company. Proton also arranged for many of the SMEs to forge partnerships

with reputable foreign auto part makers in order to strengthen the technological

capabilities of the local SMEs. As of 1998, Proton had initiated 219 partnerships for its

vendors, mostly (56 per cent) with Japanese companies (Paramjit, 2000).

By 1998, a total of 4,319 parts were sourced domestically by Proton, up from the

228 parts it sourced in 1985, when it first started. Similarly, the number of supporting firms

nurtured under Proton’s VDP increased impressively – from 17 in 1985 to 188 firms by

1998, of which 93 were Bumiputra owned. At present, some 350 firms are reportedly

making components and parts for Malaysia’s automotive sector, about 70 per cent of

which are OEMs. The apparent success of the two programmes are largely due to the fact

that the SMEs focused on producing a range of relatively low-technology accessories and

peripheral items such as plastic injection molded parts, wire harnesses, wipers, lamps,

radio cassettes, air conditioners, and metal stamped and pressed parts.

A study by Leutert and Sudhoff (1999) found that Proton component suppliers had

low levels of automation and outdated technology; and because more than 300 supplier

firms had mushroomed to serve the various component needs of Proton, few secured the

volume necessary to invest in scale expansion and modern technology. Consequently, the

SMEs were unable to reap economies of scale. Furthermore, these suppliers depended

heavily on technology suppliers and principal assemblers for design. The heavy reliance of

the SMEs on Proton for orders, coupled with the volatility of such orders, undermined their

incentive to undertake heavy reinvestments in upgrading their production processes. The

SME suppliers of Proton were also bogged down by problems of low quality, high prices,

marketing snags and the inability to meet delivery deadlines.

Malaysia’s SMEs engaged in the automobile industry are not actively involved in

exports. The small share of exports undertaken by SME suppliers underscore their lack of

competitiveness. A 1990 study by the Federation of Malaysian Manufacturers (cited by

Leutert and Sudhoff, 1999) reported that although 80 per cent of the auto parts and

accessory suppliers had exported abroad, the exports accounted for less than 20 per

cent of their turnover. The remaining 20 per cent of the suppliers produced entirely for the

domestic market.

The state of preparedness of SMEs in the automotive sector was an issue investigated

by Rokiah and Syzelin (2001). In 2000, they surveyed 98 auto component suppliers

to Proton in Selangor and Kuala Lumpur, 68 per cent of whom were SMEs. They noted:

12

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

• SMEs relied more heavily on Proton, which absorbed three-quarters of their

output. In contrast, non-SMEs supplied less than 50 per cent of their output

to Proton.

• On the challenge posed by the scrapping of the LCR scheme and trade

liberalization in 2005, they found a surprisingly low degree of awareness among

the SMEs regarding these imminent changes. Approximately 75 per cent of SMEs

appeared unaware that the LCR would be abolished by 2004. Consequently, they

had no strategies to cope with the challenges that were unfolding before them.

• When the full implications of the removal of the LCR were explained to them,

68 per cent of the respondent firms affirmed that they would be affected

adversely. Of the 14 per cent who felt that the removal would yield a positive effect

on them, the large majority comprised firms that were not totally reliant on Proton

for their domestic sales, and who were already exporting independently.

The researchers concluded that the majority of local firms, dominated by SMEs,

would not be able to survive in a freer trading environment on account of several factors:

• Most of them were still young (being in business for ten years or less), and lack the

experience and expertise to compete globally.

• Having become accustomed to a protected environment they have not been

subject to pressures to upgrade their products or production processes.

• Because of dependence on the limited domestic market, scale economies have

not been reaped. Thus products are not competitively priced, and quality and

reliability are continuing issues.

• Undue concentration on the domestic market has also resulted in other aspects,

such as labor costs, the logistics of on-time delivery, brand building and marketing

being neglected.

• Their over-reliance on Proton puts them in a position of uncertainty since the long-

term future of Proton itself is uncertain in the highly competitive global automobile

trading environment.

• With the removal of the LCR, major carmakers tend to revert to traditional

suppliers or subsidiaries with whom they have had long and trusted trading links,

thus sidelining local SMEs.

• Some major automakers have already established their production bases in

Thailand, which will give Thai parts and component suppliers an advantage that

Malaysian SMEs will have to overcome.

While SMEs in the automobile parts sub-sector have made gains in skills,

technological capabilities and forays into foreign markets, these firms grew behind heavy

trade protection and have grown dependant on the domestic market.

C h a p t e r 2: C h a l l e n g e o f G l o b a l i z a t i o n f o r S M E s

13

Malaysia has given priority to SMEs and has put in place a policy and institutional

framework that addresses their developmental needs. Strategies during the

Eighth Malaysia Plan (8MP) (2001–2005) emphasized the development of SMEs

in the manufacturing sector, and in particular the development of a competitive Bumiputra

Commercial and Industrial Community (BCIC).

Funding to address critical issues in promoting and developing SMEs was made

available through agencies like Malaysia External Trade Development Corporation

(MATRADE), Malaysia Technology Development Corporation (MTDC), Small and Medium

Industries Development Corporation (SMIDEC) and Standards and Industrial Research

Institute of Malaysia (SIRIM) Berhad. SMEs were encouraged to invest in R&D, upgrade

their technology and improve their marketing and distribution channels.

A study conducted in 2001 by the Central Bank of Malaysia showed: (i) the low

contribution of SMEs to GDP; (ii) their domestic-market orientation; (iii) the constraints they

face in terms of capacity, level of technology, access to markets and resources to upgrade

skills and production process; and (iv) limited access to finance. To address these

challenges, measures are underway aimed at:

• strengthening the enabling infrastructure;

• building capacity of SMEs;

• enhancing access to financing;

• increasing market access; and

• enhancing growth and competitiveness

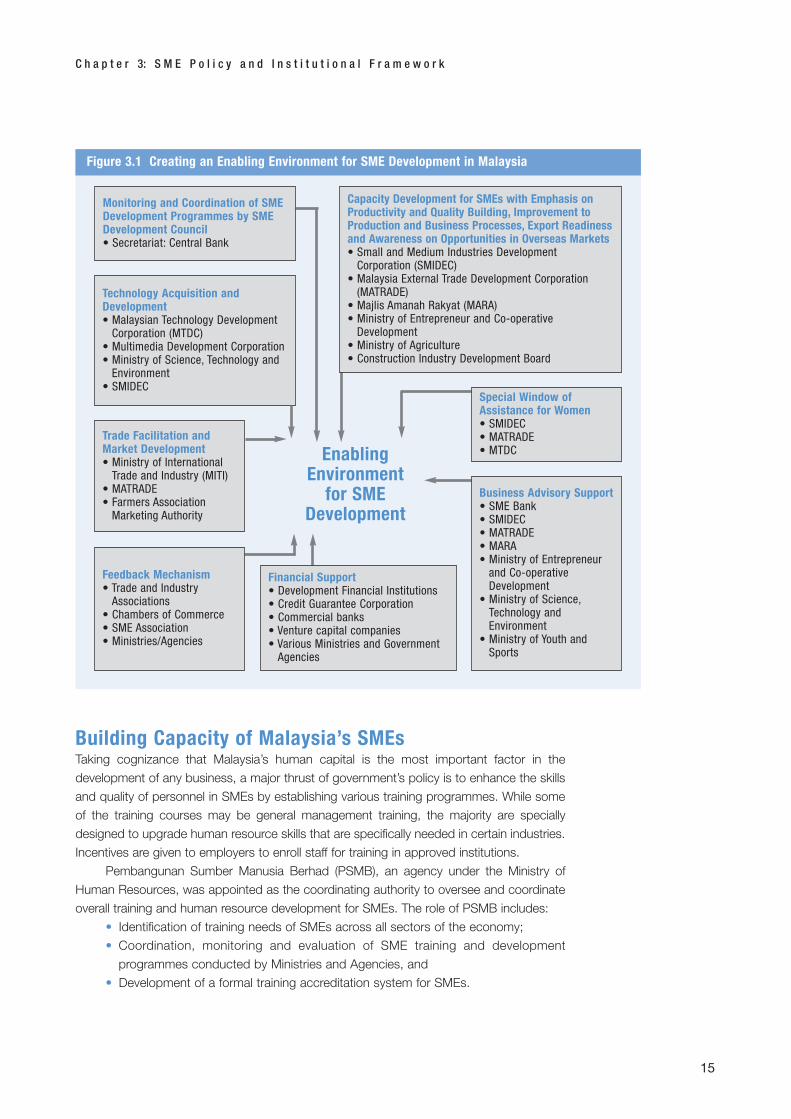

The enabling environment for SME development in Malaysia is shown in Figure 3.1.

To ensure that SME development plans are focused, in 2004 the Malaysian government

set up a National SME Development Council, chaired by the Prime Minister. Regular

meetings are held with agencies, ministries, banks and financial institutions that provide

support for SMEs, and a reporting mechanism for monitoring outcomes of activities and

providing feedback have been established. This is among the measures taken to enhance

transparency and accountability amongst policy implementers. The National SME

Development Council represents the highest policy-making body and charts the future

direction and strategies for SME development. The Council is responsible for formulating

broad policies and strategies to facilitate SME development, and for ensuring the effective

implementation of the policies and action plans. There are many ministries and institutions

involved to support and strengthen SME Development in Malaysia. Box 3.2 highlights the

key institutions.

The policy thrust for SME development in the Ninth Malaysia Plan (9MP) 2006-2010

is highlighted in Box 3.1. Strategies will focus on establishing high performance and high

value-added SMEs with strong technical, competitive and innovative capability as well as

managerial and business skills.

14

SME Policy and InstitutionalFramework

Building Capacity of Malaysia’s SMEsTaking cognizance that Malaysia’s human capital is the most important factor in the

development of any business, a major thrust of government’s policy is to enhance the skills

and quality of personnel in SMEs by establishing various training programmes. While some

of the training courses may be general management training, the majority are specially

designed to upgrade human resource skills that are specifically needed in certain industries.

Incentives are given to employers to enroll staff for training in approved institutions.

Pembangunan Sumber Manusia Berhad (PSMB), an agency under the Ministry of

Human Resources, was appointed as the coordinating authority to oversee and coordinate

overall training and human resource development for SMEs. The role of PSMB includes:

• Identification of training needs of SMEs across all sectors of the economy;

• Coordination, monitoring and evaluation of SME training and development

programmes conducted by Ministries and Agencies, and

• Development of a formal training accreditation system for SMEs.

C h a p t e r 3: S M E P o l i c y a n d I n s t i t u t i o n a l F r a m e w o r k

15

Figure 3.1 Creating an Enabling Environment for SME Development in Malaysia

Technology Acquisition andDevelopment• Malaysian Technology Development

Corporation (MTDC)• Multimedia Development Corporation• Ministry of Science, Technology and

Environment• SMIDEC

EnablingEnvironment

for SMEDevelopment

Capacity Development for SMEs with Emphasis onProductivity and Quality Building, Improvement toProduction and Business Processes, Export Readinessand Awareness on Opportunities in Overseas Markets• Small and Medium Industries Development

Corporation (SMIDEC)• Malaysia External Trade Development Corporation

(MATRADE)• Majlis Amanah Rakyat (MARA)• Ministry of Entrepreneur and Co-operative

Development• Ministry of Agriculture• Construction Industry Development Board

Special Window ofAssistance for Women• SMIDEC• MATRADE• MTDC

Business Advisory Support• SME Bank• SMIDEC• MATRADE• MARA• Ministry of Entrepreneur

and Co-operativeDevelopment

• Ministry of Science,Technology andEnvironment

• Ministry of Youth andSports

Monitoring and Coordination of SMEDevelopment Programmes by SMEDevelopment Council• Secretariat: Central Bank

Trade Facilitation andMarket Development• Ministry of International

Trade and Industry (MITI)• MATRADE• Farmers Association

Marketing Authority

Feedback Mechanism• Trade and Industry

Associations• Chambers of Commerce• SME Association• Ministries/Agencies

Financial Support• Development Financial Institutions• Credit Guarantee Corporation• Commercial banks• Venture capital companies• Various Ministries and Government

Agencies

To facilitate SMEs to access information and register for training, the Human

Resources Development Portal (HRD Portal), a web-based training portal, was launched in

2005. The main objective of this portal is to facilitate training activities among training

providers and employers by leveraging on the usage of ICT. The portal also encourages

employers to retrain and upgrade the skills of their employers, particularly SMEs, to retrain

and upgrade skills of employees to increase competitiveness and productivity.

In January 2006 the SMEinfo Portal was launched. This portal is a one-stop online

information gateway which provides information on SME development, including financing

and training as well as on support and development programmes, financing,

advisory services and training programmes. The portal also features a free SME Directory

which allows SMEs to advertise their companies and products to potential clients.

(www.smeinfo.com.my).

The availability of relevant and timely information on SMEs, including their operational

conditions, financial status and development requirements, is important to facilitate better

policy formulation in promoting SME development. The role of the Secretariat under Bank

Negara Malaysia has been enhanced to include the function of overseeing and

coordinating the monitoring, evaluation and publication of SME statistics and reports.

Apart from meeting the information requirements of SME policymakers, the Secretariat is

16

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

During the 9MP period the principal SME policy thrust

is the development of a competitive, innovative and

technologically strong SME sector. During the plan period, high

priority will be accorded to strengthen the technological capability

and capacity of SMEs to meet the challenges of globalization and

increasing competition. Towards this end, strategies will be

directed at acquiring technologies that will propel SMEs up the

value chain in the manufacturing, agriculture and services sector.

To fast-track domestic technology development capabilities of

SMEs, specific programmes will be implemented to nurture local

SMEs as R&D partners to tap the opportunities of R&D outsourcing

by MNCs and GLCs. Measures will also be undertaken to encourage

collaborative ventures among MNCs, GLCs and SMEs, to facilitate

technology transfer and skills development as well as marketing.

The strategy will be to focus on creating high performance

and resilient SMEs, equipped with strong technical and innovation

capability as well as managerial and business skills to realise new

job opportunities and improved market access.

Inter-firm linkages among and between SMEs as well as with

large domestic companies, including GLCs and foreign entities, will

be further strengthened to enable SMEs to become more

competitive, innovative and reliable suppliers for global outsourcing

networks thereby facilitating entry into new export markets.

Towards this end, the Government will promote the setting up

of technology incubators for the purpose of nurturing new firms

and entrepreneurs as well as expanding capacity of innovations

and related services.

On-going entrepreneurship programmes, including advisory

and outreach services, will be expanded to equip SMEs with new

and improved management and business practices and methods

in production, quality improvement, marketing and distribution, in

order to raise productivity, efficiency and profit levels.

Efforts will be undertaken to assist SMEs to further develop

technical skills, especially in generating innovation and creating

economic value from knowledge application.

The above measures aimed at the internationalization of

business will generate new opportunities for SMEs to compete in

globalmarkets.

Box 3.1 SME Policy Thrust of the Ninth Malaysia Plan 2006–2010

Source: Based mainly on the Ninth Malaysia Plan (2006-2010)

C h a p t e r 3: S M E P o l i c y a n d I n s t i t u t i o n a l F r a m e w o r k

17

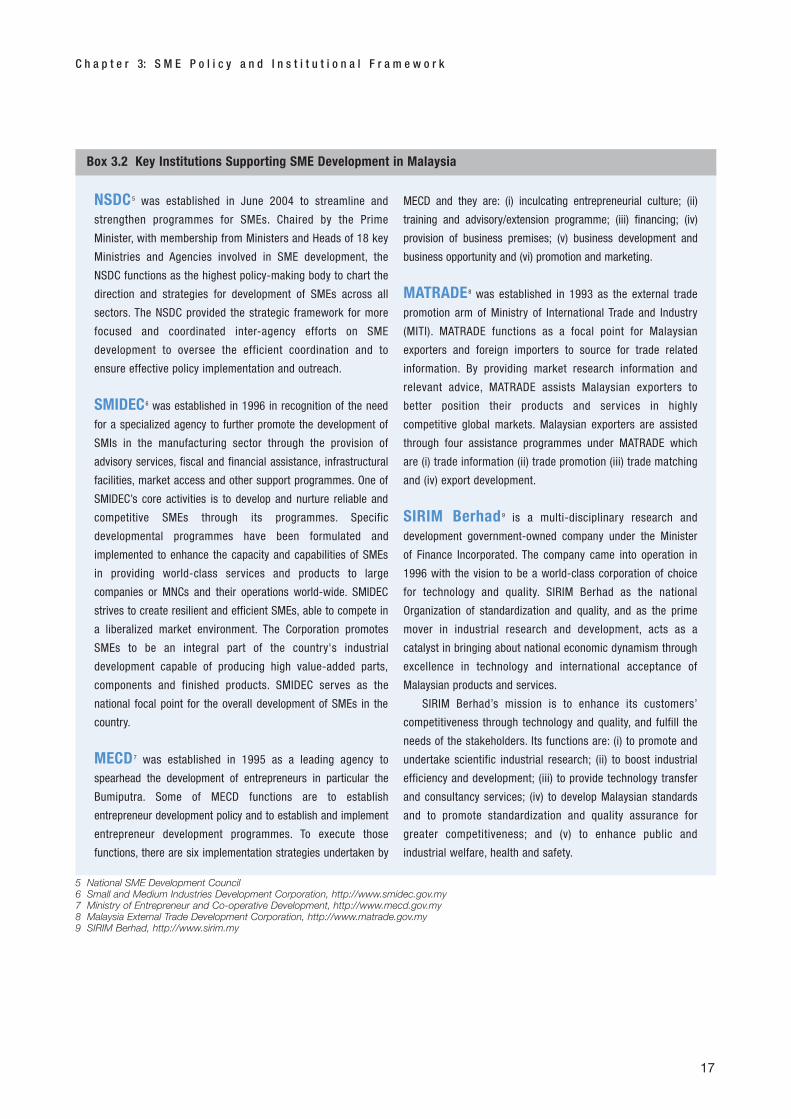

NSDC 5 was established in June 2004 to streamline and

strengthen programmes for SMEs. Chaired by the Prime

Minister, with membership from Ministers and Heads of 18 key

Ministries and Agencies involved in SME development, the

NSDC functions as the highest policy-making body to chart the

direction and strategies for development of SMEs across all

sectors. The NSDC provided the strategic framework for more

focused and coordinated inter-agency efforts on SME

development to oversee the efficient coordination and to

ensure effective policy implementation and outreach.

SMIDEC 6 was established in 1996 in recognition of the need

for a specialized agency to further promote the development of

SMIs in the manufacturing sector through the provision of

advisory services, fiscal and financial assistance, infrastructural

facilities, market access and other support programmes. One of

SMIDEC’s core activities is to develop and nurture reliable and

competitive SMEs through its programmes. Specific

developmental programmes have been formulated and

implemented to enhance the capacity and capabilities of SMEs

in providing world-class services and products to large

companies or MNCs and their operations world-wide. SMIDEC

strives to create resilient and efficient SMEs, able to compete in

a liberalized market environment. The Corporation promotes

SMEs to be an integral part of the country's industrial

development capable of producing high value-added parts,

components and finished products. SMIDEC serves as the

national focal point for the overall development of SMEs in the

country.

MECD 7 was established in 1995 as a leading agency to

spearhead the development of entrepreneurs in particular the

Bumiputra. Some of MECD functions are to establish

entrepreneur development policy and to establish and implement

entrepreneur development programmes. To execute those

functions, there are six implementation strategies undertaken by

MECD and they are: (i) inculcating entrepreneurial culture; (ii)

training and advisory/extension programme; (iii) financing; (iv)

provision of business premises; (v) business development and

business opportunity and (vi) promotion and marketing.

MATRADE 8 was established in 1993 as the external trade

promotion arm of Ministry of International Trade and Industry

(MITI). MATRADE functions as a focal point for Malaysian

exporters and foreign importers to source for trade related

information. By providing market research information and

relevant advice, MATRADE assists Malaysian exporters to

better position their products and services in highly

competitive global markets. Malaysian exporters are assisted

through four assistance programmes under MATRADE which

are (i) trade information (ii) trade promotion (iii) trade matching

and (iv) export development.

SIRIM Berhad 9 is a multi-disciplinary research and

development government-owned company under the Minister

of Finance Incorporated. The company came into operation in

1996 with the vision to be a world-class corporation of choice

for technology and quality. SIRIM Berhad as the national

Organization of standardization and quality, and as the prime

mover in industrial research and development, acts as a

catalyst in bringing about national economic dynamism through

excellence in technology and international acceptance of

Malaysian products and services.

SIRIM Berhad’s mission is to enhance its customers’

competitiveness through technology and quality, and fulfill the

needs of the stakeholders. Its functions are: (i) to promote and

undertake scientific industrial research; (ii) to boost industrial

efficiency and development; (iii) to provide technology transfer

and consultancy services; (iv) to develop Malaysian standards

and to promote standardization and quality assurance for

greater competitiveness; and (v) to enhance public and

industrial welfare, health and safety.

5 National SME Development Council6 Small and Medium Industries Development Corporation, http://www.smidec.gov.my7 Ministry of Entrepreneur and Co-operative Development, http://www.mecd.gov.my8 Malaysia External Trade Development Corporation, http://www.matrade.gov.my9 SIRIM Berhad, http://www.sirim.my

Box 3.2 Key Institutions Supporting SME Development in Malaysia

also responsible for developing key performance indicators to monitor and evaluate the

progress of SME development, and will oversee the management of the National SME

Database. The Secretariat together with relevant Ministries and agencies has outlined an

annual report on SMEs.

Some additional government measures undertaken to enhance the capability of SMEs

to produce products and services that meet global market requirements are:

• Undertaking product and market studies in international markets on behalf of SMEs

by trade promotion organizations, such as MATRADE;

• Supply studies by domestic industries undertaken by MIDA and SMIDEC;

• Dissemination of information on international standards and changes in global

demand from the network of Malaysian missions and Trade Commissioners abroad

• Making certification to international standards available to SMEs by setting up

certification bodies such as SIRIM Berhad, and other testing facilities in Ministries

such as Ministry of Health and Ministry of Agriculture;

• Benchmarking studies and analysis by respective promotional agencies and

productivity institutions such as the National Productivity Centre (NPC); and

• Assisting SMEs to undertake research in product development by establishing R&D

Centres such as Malaysia Research Oil Palm Centre (MPOPC), the Rubber Research

Institute (RRI) and SIRIM Berhad. A Commercialization of Research and Technology

Fund has also been set up to accelerate commercialization of R&D results by local

universities, companies and individual researchers or inventors and to facilitate

technology roll-out especially for indigenous industries.

Capacity and Technology DevelopmentThe National Science and Technology Policy has been formulated to provide strategic

direction for the country towards achieving the national vision of becoming a fully developed

country by 2020. The 1st National Science and Technology Policy (DSTN 1), 1986 and the

Industrial Technology Development, A National Plan of Action (TAP), 199010 have developed

Science and Technology (S&T) into a coherent system. DSTN 1 achievements include:

Integration of S&T in national development planning; Funding and management of R&D;

Strengthening S&T infrastructure; and Establishing S&T advisory system.

The 2nd Science and Technology Policy (DSTN 2) focuses on the establishment of

an integrated approach in S&T development between the public sector and industries,

which is different from DSTN 1 in terms of emphasis towards the partnership between

public sector & industries in S&T development; Stress on measures to strengthen the S&T

institutional framework; the active role of the private sector; Emphasis on entrepreneur

development; Enhancement on life long learning; Accentuate on S&T capability

development based on indigenous technology; and Focus on product development.

The specific objectives of DSTN 2 are to increase R&D expenditure to at least

1.5 per cent of GDP by 2010 and achieve a competent work force of at least 60 researchers

per 10,000 labor force by 2010.

18

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

10 Ministry of Science, Technology and Innovation, http://www.mosti.gov.my

The specific objectives of DSTN 2 also provides a framework for improved

performance and long-term growth of the Malaysian economy. The policy aims to:

• Increase the national capability & capacity for R&D, technology development and

acquisition.

• Encourage partnerships between public funded organizations and industry as well

as between local and foreign companies.

• Enhance the transformation of knowledge in products, processes, services or

solutions that add value.

• Position Malaysia as a technology provider in the key strategic knowledge

industries such as biotechnology, advanced materials, advanced manufacturing,

micro-electronics, ICT, aerospace, energy, pharmaceuticals, nanotechnology and

photonics.

• Foster societal values and attitudes that recognize S&T as critical to future

prosperity.

• Ensure that the utilization of S&T accords emphasis towards approaches that are

in conformity with sustainable development goals.

• Develop knowledge based industries.

Enhancing Access to SME Financing A lack of sufficient finance and access to credit are often cited as major handicaps to the

development of SMEs, particularly in their early growth stages. For instance, it is estimated

that close to 95 per cent of all SMEs rely on the personal resources of their owners and/or

loans from friends and relatives to finance such enterprises. Thus one of the factors

hampering SME growth is access to financing. To provide greater financial accessibility the

Malaysian government through its agencies, offers various grants and incentives to help

SME development.

Malaysian SMEs can seek financing from various types of financial institutions,

including banking institutions, development financial institutions, leasing and factoring

companies, as well as venture capital companies, which provide equity financing. In

addition, SMEs can also make use of various specific-purpose special funds set up by

the government.

C h a p t e r 3: S M E P o l i c y a n d I n s t i t u t i o n a l F r a m e w o r k

19

In July 2006 SMIDEC Malaysia and the Small and Medium

Enterprises Promotion, Thailand, signed a deal to enhance SME

competitiveness through an SME network. Thailand has indicated

that it wants to cooperate in the agriculture and food segments of

Malaysia, especially in Halal food, as Thai investors are urged to

launch Malaysia-based ventures.

Investors from Malaysia will channel funds into Thailand’s

agricultural market. Exchange of market-entry information,

business knowledge and technology will also be made and

SMEs in the E&E industry, automotive and food sector will be

of main focus.

Box 3.3 SMIDEC Malaysia and Small and Medium Enterprises Promotion, Thailand

Recent trends have shown a marked improvement in terms of financing provided to

SMEs. All main providers of funds have registered significant increases in the financing

provided by SMEs. The banking system loans to SMEs accounted for 42.6% of total

business loans outstanding at end-2005, compared with 30.1 per cent at end-1999.

Bank Negara Malaysia has a number of special funds aimed at enhancing access to

finance at reasonable costs for SMEs. The Bank in 2005 has five special funds with

lending rates ranging from 3.75 per cent to 6.00 per cent. The funds are channeled

through participating institutions comprising banking institutions, Development Finance

Institutions (DFIs), and ERF Sdn. Bhd. They are:

• Fund for Small and Medium Industries 2 (fund size: RM6.75 billion);

• New Entrepreneurs Fund 2 (fund size: RM2.85 billion);

• Fund for Food (fund size: RM1.3 billion);

• Rehabilitation Fund for Small Businesses (fund size: RM200 million); and

• Bumiputra Entrepreneurs Project Fund (fund size: RM300 million)

As at the end-2005, RM 11.22 billion has been approved to 24,503 SME accounts under

these five funds.

In addition to financing from the commercial sector, the government also provides

funds for SMEs for nurturing and developmental purposes. As at end-December 2005,

there were 81 government funds/financing schemes for SMEs with a total allocation of

RM 12.7 billion. Of the 81 funds and schemes, 49 were in the form of soft loans, while

the remaining were in the form of grants (20), equity financing (5) and venture capital

funds (7). These funds and schemes have various objectives that could be

summarized as follows:

• To encourage SMEs to be more innovative in using and adapting to the existing

and new technologies and processes;

• To improve product quality;

20

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

The SME Bank commenced operations on 3 October 2005. The

SME Bank focuses on the provision of both financial and non-

financial services for SMEs that are underserved by commercial

banks. It currently has 14 branches nationwide and plans are

under way to set up a new financial centre for these branches.

The SME Bank complements the role of existing financial

providers of SME loans. It focuses on businesses with growth

potential but which may be seen as not viable by commercial

banks. As outlined by the National SME Development Council,

the Bank will eventually become a one-stop centre for all SMEs

in the manufacturing and services sectors – that is for those

with annual revenue ranging from RM200,000 to RM25 million.

The SME Bank and the National SME Development Council

are currently setting up an advisory network, which involves

collaboration with key service providers within the local and

multinational risk management services, commercial banks,

ministries and agencies.

Apart from the SME Bank, the Central Bank is actively

involved in the development of SMEs to increase their

participation and contribution to the economy. The Bank also

serves as the Secretariat to the National SME Development

Council which is chaired by the Prime Minister and is comprised

of Ministers and Heads of 18 key Ministries. In 2005 new

initiatives were announced to improve SME activities, including

new trade financing products.

Box 3.4 Malaysia’s SME Bank

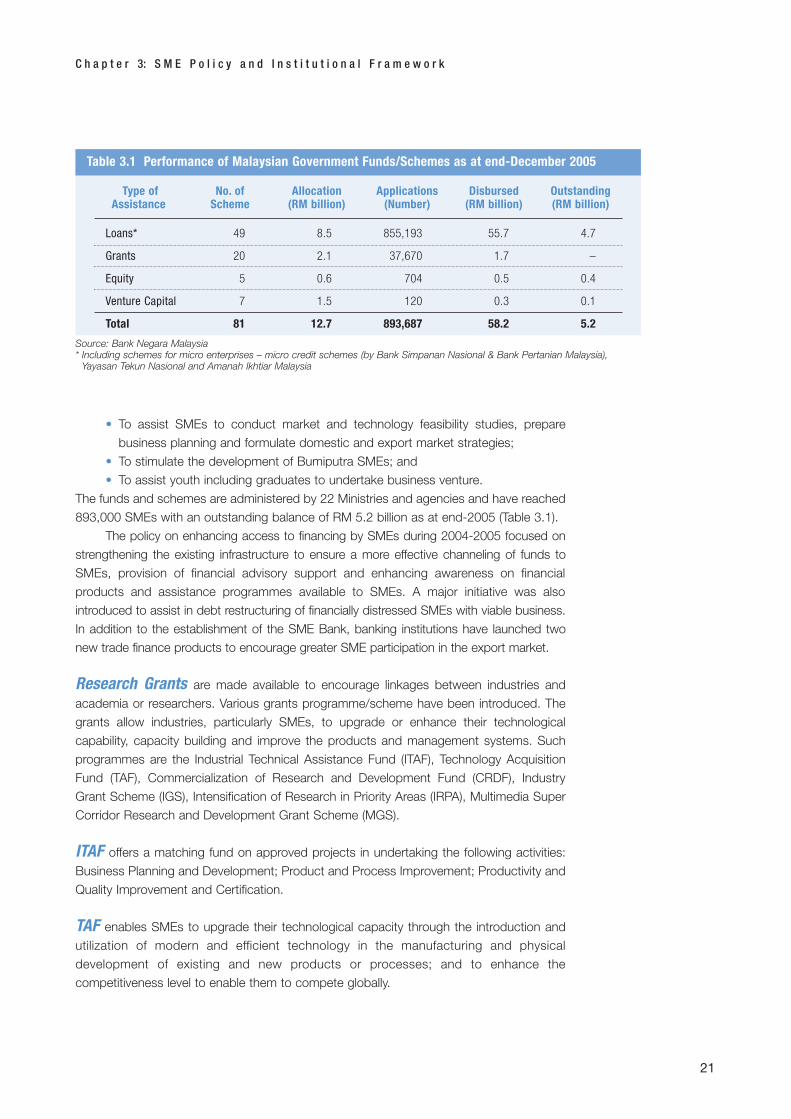

• To assist SMEs to conduct market and technology feasibility studies, prepare

business planning and formulate domestic and export market strategies;

• To stimulate the development of Bumiputra SMEs; and

• To assist youth including graduates to undertake business venture.

The funds and schemes are administered by 22 Ministries and agencies and have reached

893,000 SMEs with an outstanding balance of RM 5.2 billion as at end-2005 (Table 3.1).

The policy on enhancing access to financing by SMEs during 2004-2005 focused on

strengthening the existing infrastructure to ensure a more effective channeling of funds to

SMEs, provision of financial advisory support and enhancing awareness on financial

products and assistance programmes available to SMEs. A major initiative was also

introduced to assist in debt restructuring of financially distressed SMEs with viable business.

In addition to the establishment of the SME Bank, banking institutions have launched two

new trade finance products to encourage greater SME participation in the export market.

Research Grants are made available to encourage linkages between industries and

academia or researchers. Various grants programme/scheme have been introduced. The

grants allow industries, particularly SMEs, to upgrade or enhance their technological

capability, capacity building and improve the products and management systems. Such

programmes are the Industrial Technical Assistance Fund (ITAF), Technology Acquisition

Fund (TAF), Commercialization of Research and Development Fund (CRDF), Industry

Grant Scheme (IGS), Intensification of Research in Priority Areas (IRPA), Multimedia Super

Corridor Research and Development Grant Scheme (MGS).

ITAF offers a matching fund on approved projects in undertaking the following activities:

Business Planning and Development; Product and Process Improvement; Productivity and

Quality Improvement and Certification.

TAF enables SMEs to upgrade their technological capacity through the introduction and

utilization of modern and efficient technology in the manufacturing and physical

development of existing and new products or processes; and to enhance the

competitiveness level to enable them to compete globally.

C h a p t e r 3: S M E P o l i c y a n d I n s t i t u t i o n a l F r a m e w o r k

21

Source: Bank Negara Malaysia* Including schemes for micro enterprises – micro credit schemes (by Bank Simpanan Nasional & Bank Pertanian Malaysia),

Yayasan Tekun Nasional and Amanah Ikhtiar Malaysia

Table 3.1 Performance of Malaysian Government Funds/Schemes as at end-December 2005

Loans* 49

20

5

7

81

Grants

Equity

Venture Capital

Total

Type of Assistance

No. of Scheme

8.5

2.1

0.6

1.5

12.7

855,193

37,670

704

120

893,687

55.7

1.7

0.5

0.3

58.2

4.7

–

0.4

0.1

5.2

Allocation(RM billion)

Applications(Number)

Disbursed(RM billion)

Outstanding(RM billion)

CRDF is made available to encourage and accelerate the Commercialization of R&D

results undertaken by local universities and research institutions, companies and individual

researchers or inventors. It is expected that CRDF will enhance the competitiveness and

capability of the Malaysian Industrial sector by promoting the Commercialization of

indigenous technology. Among the main activities can be undertaken are Market Survey

and Research; Product/Process Design and Development; Standards and Regulatory

Compliance and Intellectual Property Protection and Demonstration of Technology.

IGS aims to enhance R&D in the private sector and promote closer co-operation between

the private sector and the public institutions and agencies through collaborative linkages.

The IGS encourages Malaysian companies to be more innovative in using and adopting

existing technologies in creating new technologies, products and processes that will

benefit the national economy.

IRPA grant focuses on R&D activities in areas that have potential for enhancing the

national socio-economic position. In allocating grants for R&D projects, the National

Council for Scientific Research and Development (MPKSN) adheres to several principles.

These are: (i) to fund projects which are of high national priority and commercially viable;

(ii) to fund projects which address the needs of Malaysia industry; (iii) to encourage

collaborative efforts among research institutions; and (iv) to enhance R&D linkages

between the public and private sectors. The bulk of IRPA funding is allocated to activities

that will lead to Commercialization. However, in the interest of generating more capabilities

and expertise within the country, some funding allocation has also been given to research

activities directed towards knowledge advancement even though they are presently not

seen as commercially viable. This is a long-term measure for knowledge advancement

within the research communities in Malaysia.

Enhancing Product Packaging, Design and Labeling Capabilities Grantprovides assistance to SMEs to acquire and improve product packaging, design and

labeling. It enables companies to improve their product packaging to enhance product

appearance and comply with market regulations.

Development and Promotion of Halal Product Grant in the development and

promotion of halal products (food and non-food). This is in effort towards development

and promoting Malaysia as the Halal Hub. Some of the non-food products are

pharmaceutical, herbal supplements, gelatin products, leather, aromatherapy, perfumery

and toiletries.

Market Development Grant to assist SMEs in export promotion activities which

include participation in international trade missions, specialized selling missions,

international trade fairs, exhibition of export in the Malaysian trade centre overseas,

preparation of promotional items, promotion of brand names overseas, designing and

improving packaging of products and participation in overseas international tenders.

22

M a l a y s i a S m a l l a n d M e d i u m E n t e r p r i s e s: B u i l d i n g a n E n a b l i n g E n v i r o n m e n t

Brand Promotion Grant to assist industries in particular SMEs to develop and

promote brand names owned by Malaysian companies for products and services

originating from Malaysia in the international market.

Market Access ProgrammesAmong the early market access opportunities introduced in Malaysia is the Integrated

Marketing Programme or Umbrella Programme of the 1980s. Through these programmes,

technical agencies work closely with agencies and established anchor companies to assist

SMI companies to manufacture quality products for both domestic and export markets.

The anchor company provides the marketing and technical agencies related

technical/technological know-how and support to assist SMI companies become more

efficient to penetrate the export market. Among the early product based were furniture,

food and beverages, office stationery and office furniture.

An anchor-vendor (or sub-contracting) arrangement programme aims to accelerate

the development of SMIs as ancillary industries to complement activities with large-scale

industries, especially MNCs. To remain competitive, small component suppliers are

encouraged to upgrade and enhance their management capability together with

product quality.

Another coordinated and integrated approach by government technical institutions and

private companies is to bring Malaysia’s food and confectionary into the hypermarket.

Through this arrangement, agencies such as SIRIM Berhad, help manufacturers and

producers to upgrade product standards, improve and enhance product packaging, assist

SMEs to meet technical and regulatory requirements such as food safety requirements,

comply to national product standards, product testing in particular food safety, nutritional

content and analysis and product promotion and branding. Agencies such as MECD and

SMIDEC and the Ministry of Domestic Trade and Consumer Affairs provide financial

support and assistance packages to bring SME products to the market place.

Industrial Linkage ProgrammeThe Industrial Linkage Programme (ILP) under the MITI is a development programme for

SMEs. SMIDEC implements this scheme, which is aimed at redefining SMEs, as a core

programme. SMIDEC identifies potential products, components and parts required by the

larger companies. ILP was designed as an integrated cluster-based industrial