Embed Size (px)

Citation preview

Vision• To ensure universal access to banking & other financial services at

reasonable distance and affordable cost.

• Make financial inclusion an enabler for inclusive growth.

6 PillarsUnorganized sector

Pension scheme

Micro - Insurance

Financial LiteracyProgramme

Creation of CreditGuarantee Fund

Providing Basic BankingAccounts with overdraftfacility and RuPay Debit

card.

Universal access tobanking facilities

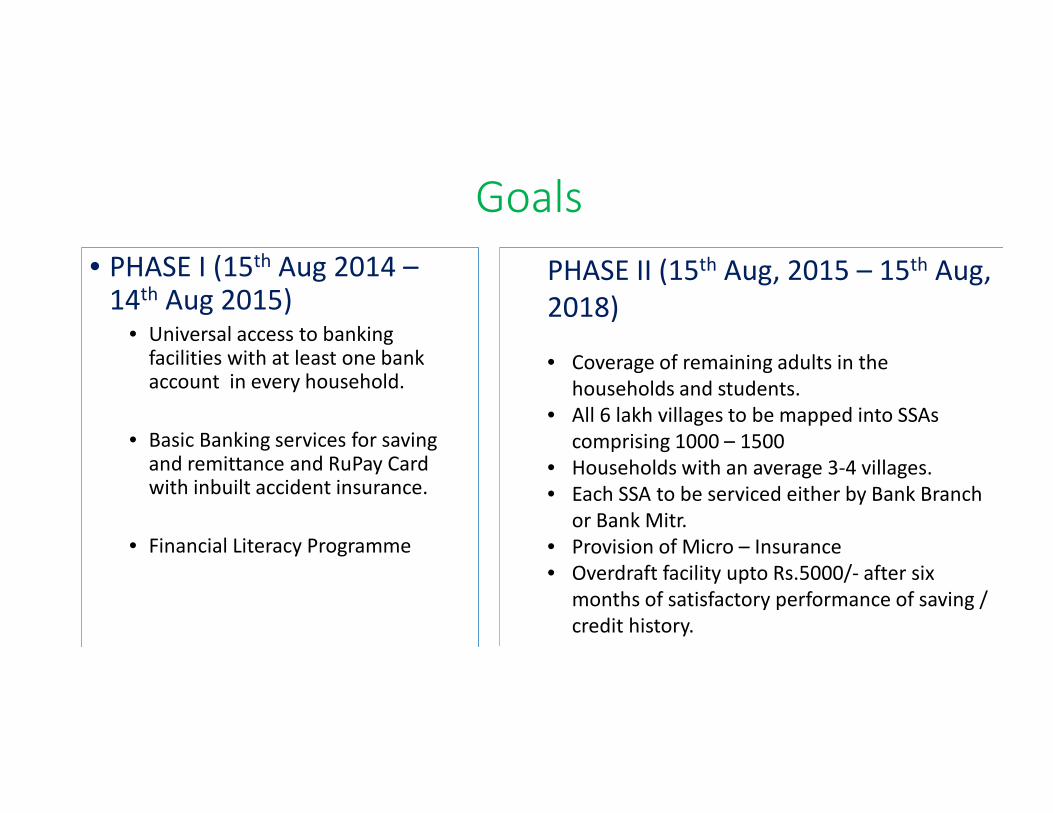

Goals

• PHASE I (15th Aug 2014 –14th Aug 2015)

• Universal access to bankingfacilities with at least one bankaccount in every household.

• Basic Banking services for savingand remittance and RuPay Cardwith inbuilt accident insurance.

• Financial Literacy Programme

PHASE II (15th Aug, 2015 – 15th Aug,2018)

• Coverage of remaining adults in thehouseholds and students.

• All 6 lakh villages to be mapped into SSAscomprising 1000 – 1500

• Households with an average 3-4 villages.• Each SSA to be serviced either by Bank Branch

or Bank Mitr.• Provision of Micro – Insurance• Overdraft facility upto Rs.5000/- after six

months of satisfactory performance of saving /credit history.

Achievements – Phase I• Household coverage achieved by target date

31.01.2015 by opening 12.55 Crore PMJDYaccounts.

• Coverage confirmed through surveys, certificationby Gram Panchayats and issuance of PublicChallenge.

• Another Public Challenge proposed to be issuedthrough SLBCs shortly for left out households, ifany

• 11.08 Crore Rupay cards issued.

• Mapping of 1,59,786 SSAs done in Phase I itself forcoverage through 32,535 existing branches and1,27,251 Bank Mitr.

• Financial literacy undertaken through 718 FinancialLiteracy & Credit counselling centres (FLCCs).

• Strategy formulated to link FLCCs to SkillingCentres.

Banking NetworkBranches ATMs Bank Mitr134014 201861 126495

Rural Semi Urban Urban Metro50421 36056 25062 22475

10.00

12.55

Target Achievement

PMJDY Accounts opened (in Cr.)

11.08

13.15

31.01.2015 31.03.2015

Rupay cards issued (in Cr.)

Achievements under Phase II so far

• PHASE II• Accounts – 25.32 crore

• Zero Balance – 5.93 crore

• Deposit – Rs.44867 crore

• Rupay Card – 19.39 crore

• OD Availed - 43.18 lac

• OD Amount – 315.82 crore

14.72

21.43

25.32

31.03.2015 31.03.2016 31.10.2016

Accounts

13.15

17.7519.39

31.03.2015 31.03.2016 31.10.2016

RuPay Card Issued

8.52(57.9)

5.87(27.39)

5.93(23.44)

31.03.2015 31.03.2016 31.10.2016

Zero Balance Accounts

15,670.29

35,672.00

44,867.28

31.03.2015 31.03.2016 31.10.2016

Deposits

Achievements – Bank Mitr Activity

59.52

80.26

104.52

Dec'15 Jun'16 Oct'16

Bank Mitr transactions per week (in lac)

19.83

43.72

52.64

Dec'15 Jun'16 Oct'16

Bank Mitr Aadhaar On-US Transactionsper week (in lac)

0.14

0.96

2.52

Dec'15 Jun'16 Oct'16

Bank Mitr aadhaar Off-US Transactionsper week (in lac)

2.01

4.05

5.76

Dec'15 Jun'16 Oct'16

Bank Mitr Rupay card Transactions per week(in lac)

Microsave Wave III Bank Mitr Assessment

73%

27%

% of BMs who received financial literacytraining

Received training Never received training

3,8213,460

4,3304,692 4,601 4,865

Average monthlyincome (Overall)

Average monthlyincome (BCNM)

Average monthlyincome (Bank)

Average monthly income of BM

Wave-II Wave-III

125

677

89

975

173

785

128

1116

Average DepositNumber

Average depositvalue (INR)

Averagewithdrawal

number

Averagewithdrawal value

(INR)

Average transaction

Wave-II Wave-III

Financial Literacy

Type of Skilling Centre(SC) / schools

No. of SCmapped

No. ofsession

conducted

No. ofparticipant

sSkilling Centre (ITI,

VTPs, OCs)17,422 9197 7.00 lac

Schools 24815 31.17 lac

Total 34012 38.17 lac

As on 31st Oct 2016 a total of 17422 skillingcentres have been successfully mapped withbranches and Financial Literacy Centres wheresessions have been conducted in 9197 skillingcentres imparting financial literacy to 7 lacstudents.

FL Material converted in10 regional languages

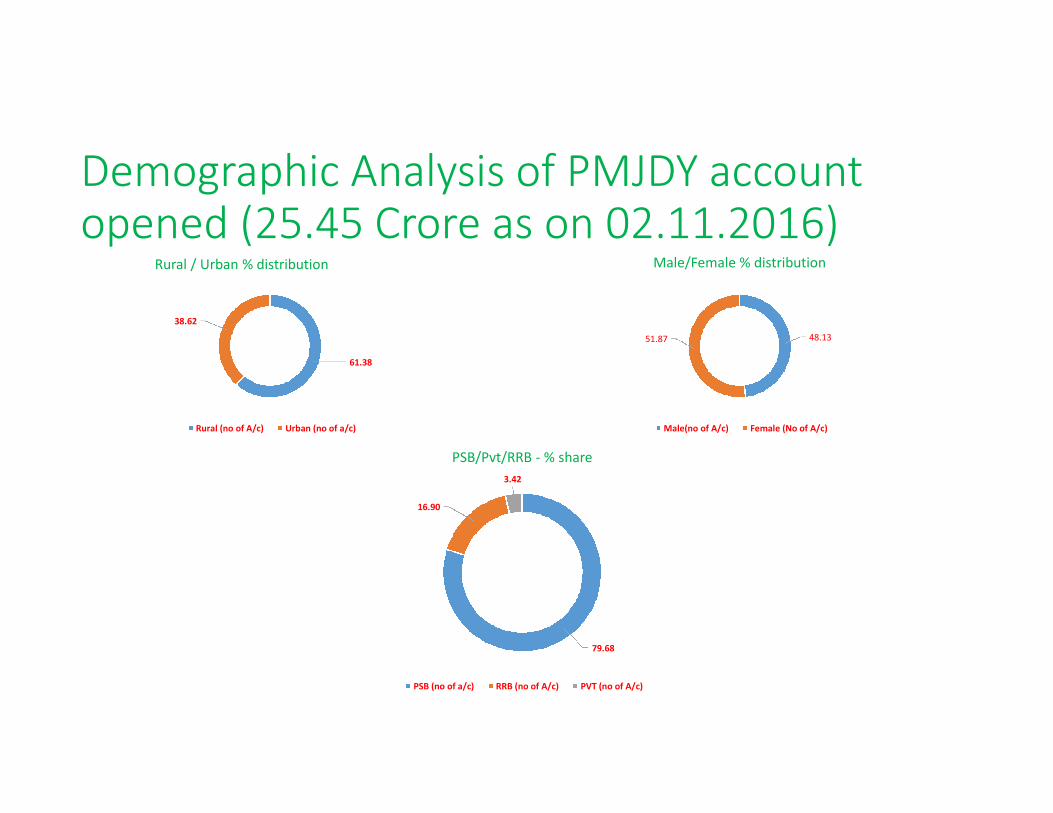

Demographic Analysis of PMJDY accountopened (25.45 Crore as on 02.11.2016)

61.38

38.62

Rural / Urban % distribution

Rural (no of A/c) Urban (no of a/c)

48.1351.87

Male/Female % distribution

Male(no of A/c) Female (No of A/c)

79.68

16.90

3.42

PSB/Pvt/RRB - % share

PSB (no of a/c) RRB (no of A/c) PVT (no of A/c)

Micro InsurancePMJJBY PMSBY

MAR 2016 JUN 2016 OCT 2016

29548597

30085885

30652201

Enrollments

22212

32861

46490

19409

28796

42229

MAR 2016 JUN 2016 OCT 2016

Reported Paid

Claims

MAR 2016 JUN 2016 OCT 2016

94048480

94999832

97526192

Enrollm…

4566

6533

9262

MAR 2016 JUN 2016 OCT 2016

Reported Paid

Way Forward Challenges

• Strengthening of Bank MitrNetwork in all SSAs for regular anddependable services.

• Ensure full interoperability (Onus and Off us) at all Bank Mitrlocations on Biometric as well asRuPay card devices for improvingviability and ease of banking.

• Aadhaar Seeding of all PMJDYaccounts by 31.03.2017.

• Network issues in Dark Areas (withno connectivity) & Grey Areas (withintermittent connectivity)

• Unviability of operations in lowpopulation density areas.

• Frequent attrition among Bank Mitr.

• Challenges in legacy accounts forAadhaar seeding restricting AEPSinteroperability.

• Inter-se restrictions imposed bybanks on Off-us transactions.

• Weak resolution mechanism infailed AEPS transactions.

Strategy: Strengthening Bank Mitr Network

• Network issues being resolved through installation of VSATs by banks.

• PDS shops proposed as additional channel for Bank Mitr services forensuring uninterrupted basic banking services.

• Weekly monitoring of Bank Mitr activity being done with banks.

• A digital dashboard under development to monitor bank mitr activity.

• RBI/IBA in process of creating Bank Mitr registry.

AEPS Interoperability

• Interactions with CEOs of major banks held in areas of concern

• NPCI and IBA advised to improve resolution mechanism & remove inter-serestrictions.

Strategy: AEPS Interoperability

• Interactions with CEOs of major banks held in areas of concern

• NPCI and IBA advised to improve resolution mechanism & removeinter-se restrictions.

• SOPs for interoperable Aadhaar seeding being standardised.

Strategy: Aadhaar seeding

• Focussing on states having drag i.e. percentage share in Aadhaarseeding being less than % share in PMJDY accounts: UP, Bihar, WestBengal, Odisha & Tamilnadu.

• Activation of SLBCs for seeding of MNREGA accounts through dailymonitoring.

• Improving interoperability for seeding.