Embed Size (px)

Citation preview

10-1Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

FINANCIAL ACCOUNTING THEORYCraig Deegan

Slides written by Craig Deegan

CHAPTER 10Reactions of capital markets to financial reporting

10-2Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Learning objectives10.1 Understand the role of capital markets research in assessing

the information content of accounting disclosures.

10.2 Understand the difference between capital markets research (which explores the response of ‘the market’ in aggregate) and behavioural research (which explores the actions of individuals).

10.3 Understand the assumptions of market efficiency typically adopted in capital markets research.

10.4 Understand the basics of the ‘market model’ as derived from the capital assets pricing model.

10.5 Understand the difference between capital markets research that looks at the information content of accounting disclosures, and capital markets research that uses share price data as a benchmark for evaluating accounting disclosures.

continued

10-3Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Learning objectives (cont.)

10.6 Understand how, and why, some researchers use market-based data (such as share prices and share returns) to evaluate the ‘value relevance’ of accounting-based information.

10.7 Be able to explain why unexpected accounting earnings and abnormal share price returns are expected to be related.

10.8 Be able to outline the major results of capital markets research into financial accounting and disclosure.

10.9 Be aware of debates that challenge long-held beliefs about ‘market efficiency’.

10-4Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Capital market research—introduction• Explores the role of accounting and other financial

information in equity markets

• Involves examining statistical relations between financial information and share prices

• Reactions of investors evident from capital market transactions

• No share price change implies no reaction to particular information – that there is no information content

10-5Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Capital market versus behavioural research• Capital market research (the topic of this lecture)

– assesses the aggregate effect of financial reporting on investors

– considers only investors

• Behavioural research (the topic of the next lecture), by contrast:

– analyses individual responses to financial reporting

– examines decision-making by many groups

e.g. bank managers, loan officers, auditors

10-6Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Reasons for capital market research

• Information about earnings and its components is the primary purpose of financial reporting. As the IASB Conceptual Framework states:

– The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity.

continued

10-7Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Reasons for capital market research (cont.)• The use of accounting information by investors is

therefore of central importance to the accounting profession, in particular, the issue of whether accounting information is used by investors in their decision making processes

– capital markets research explores the market’s (investors in aggregate) reaction to various releases of information – including accounting information – and therefore capital markets research should be of interest to the accounting profession

• Earnings is the number most analysed and forecast by security analysts

• Reliable data on earnings is readily available

10-8Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

So…the questions often asked by capital markets researchers are…

• What is the impact of the release of accounting information on share returns?

• Which accounting information is

relevant for valuing shares in a

company?

10-9Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Underlying assumption of CMR—EMH

• CMR relies on the assumption that equity markets are efficient

– in accordance with Efficient Market Hypothesis (EMH)

• Efficient market defined as a market that adjusts rapidly to fully impound information into share prices when the information is released

10-10Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Three forms of market efficiency• Weak form prices reflect information about past

prices and trading volumes

• Semi-strong form all publicly available information is rapidly and fully impounded into share prices in an unbiased manner when released

– most relevant for accounting-based capital market research

• Strong form security prices reflect all information (public and private)

10-11Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Assumptions about market efficiency• Any assumptions about market efficiency are simply that –

assumptions that are used within a model – and as we have emphasised throughout this course/subject, models or theories will not always fully reflect what actually happens in the ‘real world’.

– indeed, there have been many researchers who have rejected claims that securities markets are efficient

• Assumptions about market efficiency have implications for accounting.

– if markets are efficient, they will use information from various sources when predicting future earnings, and hence when determining current share prices

– if accounting information does not impact on share prices, then, assuming semi-strong-form efficiency, it would be deemed not to provide any information over and above that currently available

– at the extreme, accounting’s survival would be threatened

10-12Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Market efficiency—implications for accounting

• If markets are efficient they will use information from various sources when predicting future earnings

• If accounting information does not impact on share prices then it is deemed not to have any information value above that currently available

10-13Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Market efficiency – share prices react to information from various sources

• For example, material provided within the textbook indicates that share prices have been found to react not only to earnings data but also to such things as:

– news about senior executive resignations

– takeover rumours posted to internet discussion sites

which raises possible issues about the regulation of information provided on such sites

– concerns raised by auditors, particularly in relation to going concern considerations (unless anticipated by the market)

– industry-wide changes, such as the implications associated with the introduction of particular legislations (such as the Sarbanes-Oxley Act in the US)

continued

10-14Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Share prices react to information from various sources (cont.)

• Again, a share price reaction indicates that the ‘news’ has ‘information content’

– But remember, the information might later prove to be either correct or incorrect (something that becomes known with hindsight)

• Conversely, no share price reaction indicates that the news or event did not act to cause the market to revise any previous expectations held about a firm’s future cash flows

– the absence of share price movement indicates either that the information is irrelevant or that it confirms market expectations

10-15Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Event studies• Studies which look at the changes in share prices around a

particular event, such as the release of accounting information, are often referred to as ‘events studies’.

• According to Kothari (2001):

– in an event study, one infers whether an event, such as an earnings announcement, conveys new information to market participants as reflected in changes in the level or variability of security prices or trading volume over a short time period around the event

– if the level or variability of prices changes around the event date, then the conclusion is that the accounting event conveys new information about the amount, timing, and/or uncertainty of future cash flows that revised the market’s previous expectations

– the maintained hypothesis in an event study is that capital markets are informationally efficient in the sense that security prices are quick to reflect the newly arrived information

10-16Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Confounding events• Within event studies there is typically a risk of ‘confounding

events’

• It should be noted that across time there will be many events that will affect share prices and trading volumes

• One of the difficult tasks in undertaking ‘event studies’ that review share price reactions to particular announcements is to try to ensure that there have been no other (confounding) events around the same time which might also have influenced share prices

• For example, if accounting profits are announced on the same day that the chief executive officer has resigned then it would be difficult to determine what caused any possible share price reaction – was it the profits, or the resignation?

10-17Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Earnings/return relation

• Share prices are the sum of expected future cash flows from dividends, discounted to their present value using a rate of return commensurate with the company’s risk

• Dividends are a function of accounting earnings

• Unexpected earnings rather than total earnings expected to be associated with a change in share price

10-18Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Earnings/return relation—the market model• Used to separate out firm-specific share price

movements from market-wide movements

– derived from the Capital Asset Pricing Model

• Assumes investors are risk averse and have homogeneous expectations

• Its use allows the researcher to focus on share price movements due to firm-specific news

continued

10-19Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Earnings/return relation—market model (cont.)

• Total or actual returns can be divided into

– normal (expected) returns given market-wide movements

– abnormal (unexpected) returns due to firm-specific share price movements

• Abnormal returns used as an indicator of information content of announcements

10-20Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

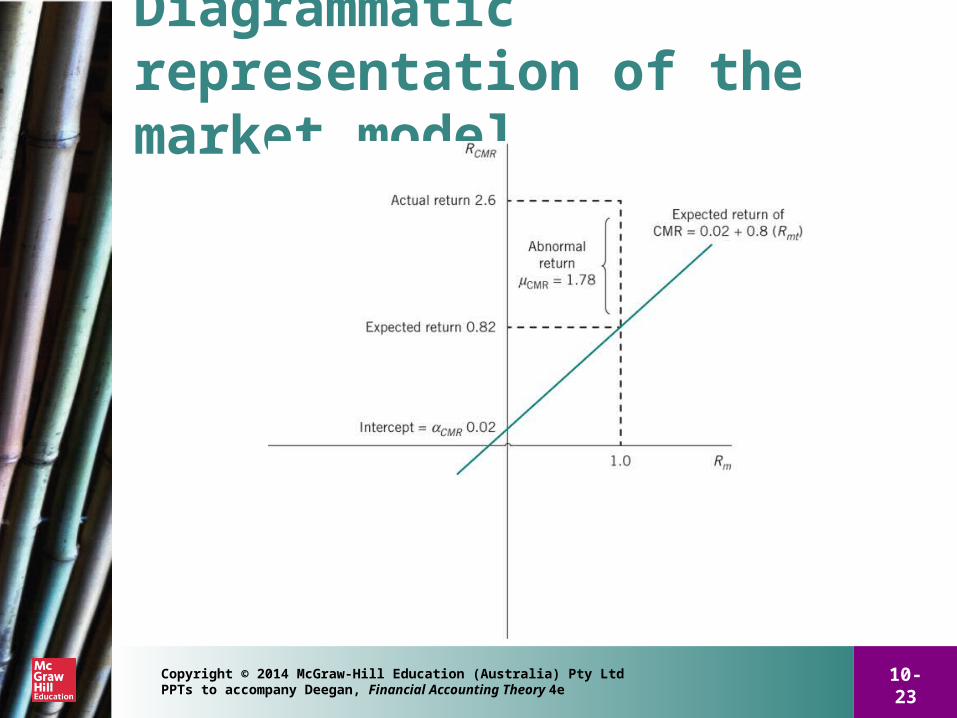

the relationship between changes in share price and returns to investors

• The previous slide referred to share ‘returns’

• Returns (to shareholders) are a function of share price

Return = End Price + Dividends – Beginning price

Beginning price

• Returns are generally calculated over periods of between one day and one year

• If no dividend is paid, returns are simply equal to percentage change in price

– e.g. if a company’s share price increased from $5.42 to $5.56 during the day when earnings were announced, the daily return is:

(RCMR) = (5.56 – 5.42)/5.42 or 2.6%

10-21Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

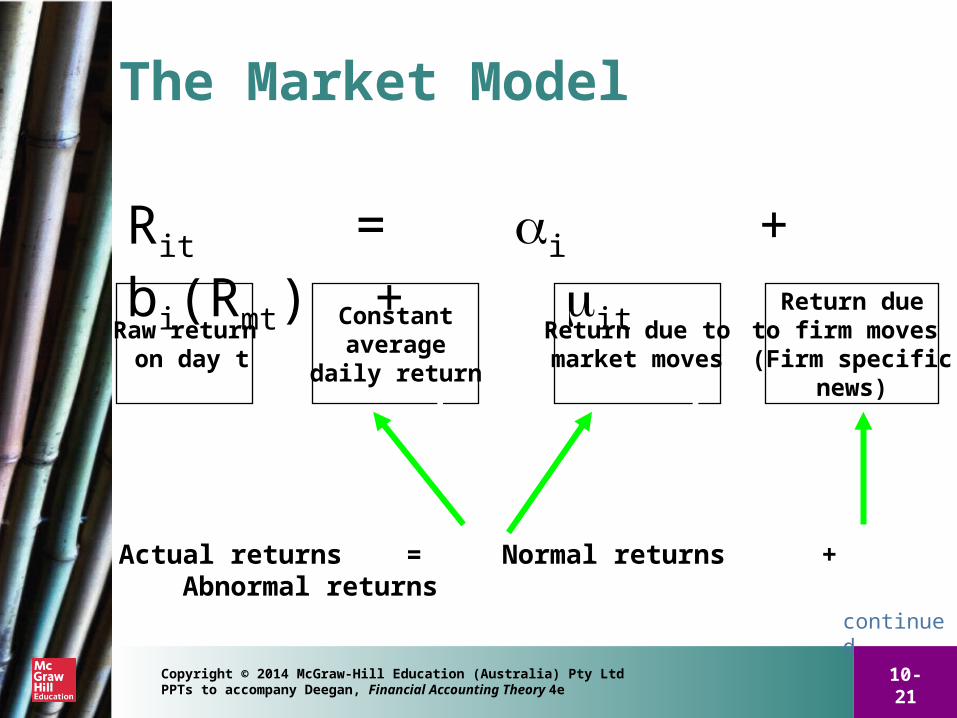

The Market Model

Raw return on day t

Constantaverage

daily return

Return due tomarket moves

Return dueto firm moves (Firm specific

news)

= + +

Rit = i + bi(Rmt) + it

Actual returns = Normal returns + Abnormal returns

continued

10-22Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

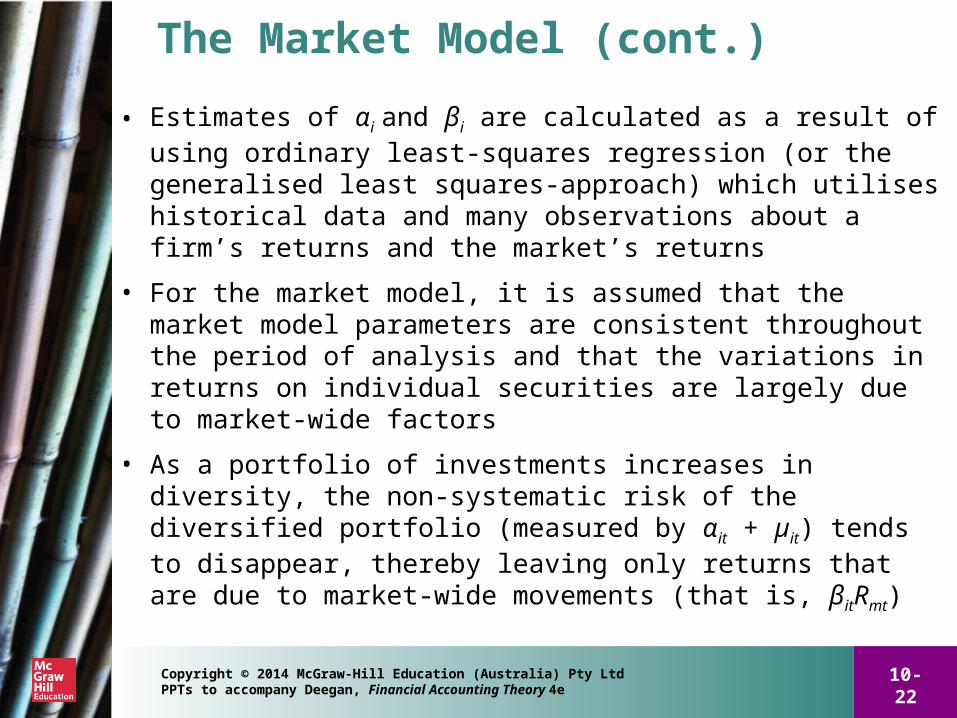

The Market Model (cont.)

• Estimates of αi and βi are calculated as a result of using ordinary least-squares regression (or the generalised least squares-approach) which utilises historical data and many observations about a firm’s returns and the market’s returns

• For the market model, it is assumed that the market model parameters are consistent throughout the period of analysis and that the variations in returns on individual securities are largely due to market-wide factors

• As a portfolio of investments increases in diversity, the non-systematic risk of the diversified portfolio (measured by αit + µit) tends to disappear, thereby leaving only returns that are due to market-wide movements (that is, βitRmt)

10-23Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Diagrammatic representation of the market model

10-24Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

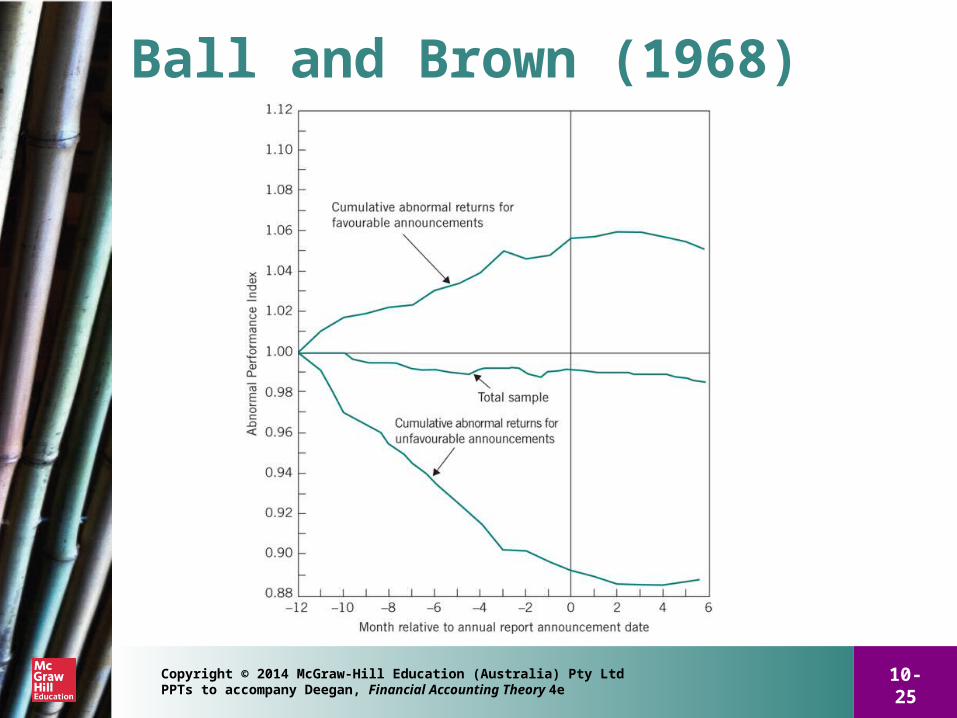

Results of CMR—Ball and Brown (1968) study• One of the most highly cited papers in the accounting

literature

• Examined data from 261 US firms

• Tested whether firms with unexpected increases in accounting earnings had positive abnormal returns, and firms with unexpected decreases had negative abnormal returns

• Found that:

– information contained in the annual report, prepared using historical cost was useful to investors

– 85 to 90% of earnings announcement is anticipated by investors

– much of information is obtained from other sources

10-25Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Ball and Brown (1968)

10-26Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—extent of alternative information sources• Information content varies between countries and

companies

• Compared to US markets, Australian market had slower adjustments during the year with larger adjustments at earnings announcement

– less alternative sources of information for Australian market

• Less alternative sources of information for smaller firms than larger firms

10-27Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—permanent and temporary changes• Research examined relationship between the

magnitude of unexpected changes in earnings (EPS) and magnitude of abnormal returns

– known as the earnings response coefficient

– some research has shown that a 1% unexpected change in earnings associated with 0.1 to 0.15% abnormal return

– depends on whether earnings increases expected to be permanent or temporary

10-28Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—relative magnitudes of cash and accruals

• Earnings persistence depends on proportion of accruals relative to cash flows

– firms with large accruals relative to actual cash flows unlikely to have persistently high earnings

• Share prices found to act as if investors ‘fixate’ on reported earnings without considering relative magnitudes of cash and accrual components

10-29Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—information announcements of other firms

• Earnings announcements by one firm also results in abnormal returns to other firms in the same industry

– known as ‘information transfer’ effect

• Related to whether the news reflects a change in conditions for the entire industry, or changes in relative market share within the industry

• For example, if an organisation within an industry is the first to prepare its financial results for the year, and it reports record profits (lower profits) that were unexpected by the market, then this would often cause share price increases (decreases) across the industry

– for example, Accounting Headline 10.7 shows that when Target reported a lower than expected earnings forecast it sparked declines in the share prices of other retail organisations

10-30Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—information content of earnings forecasts

• Announcements of expected earnings rather than actual earnings are associated with share returns

• Management and security analysts both make forecasts

10-31Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—benefits of voluntary disclosure• Voluntary disclosures include those in annual reports

as well as media releases etc.

• Firms with more disclosure policies have

– larger analyst following and more accurate analyst earnings forecasts

– increased investor following

– reduced information asymmetry

– reduced costs of equity capital

10-32Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—recognition versus footnote disclosure

• Recognising an item in the financial statements is perceived differently to disclosure in footnotes

• Investors place greater reliance on recognised amounts than on disclosed amounts

10-33Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—size

• Relationship between earnings announcements and share price movements is inversely related to the size of the entity

• Earnings announcements found to have a greater impact on share prices of smaller firms than larger firms

• More information generally available for larger firms

10-34Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—unexpected changes in earnings vs unexpected changes in expenses

• If ‘earnings surprises’ are accompanied by revenue surprises of similar magnitude in the same direction, then the earnings surprises are driven by revenue growth rather than by a reduction in expenses

• Researchers expect earnings growth driven by revenue growth to exhibit a different level of persistence compared with earnings growth driven by expense reduction

• Jegadeesh and Livnat's (2006) results indicate that the market does tend to react more to unexpected earnings when these 'surprises' are due to increases in revenues

10-35Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Do current prices anticipate future announcements? • As firm size increases, share prices incorporate

information from wider number of sources

– relatively less unexpected information when earnings are announced

• May be able to argue that share prices anticipate future earnings announcements for larger firms with some accuracy

10-36Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Accounting earnings reflecting information (value relevance research)

• Rather than determining whether earnings announcements provide information, recent research also examines whether earnings announcements reflect information that has been already used by investors

– ‘looking back the other way’

– market prices viewed as leading accounting earnings

continued

10-37Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Accounting earnings reflecting information (cont.)

• Share prices are considered as benchmark measures of firm value

• Share returns are considered as benchmark measures of firm performance

• Benchmarks are then used to compare usefulness of alternative accounting and disclosure methods

• Based on premise that market values and book values are both measures of firm value

continued

10-38Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Accounting earnings reflecting information (cont.)

• If market value is related to book value, returns should be related to accounting earnings per share, divided by price at the beginning of the accounting period

– provides an underlying reason why we should expect returns to be related to earnings over time

10-39Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—accounting earnings reflecting information

• Beaver, Lambert and Morse (1980) found share prices and related returns were related to accounting earnings

• Because of various information sources, price appeared to anticipate future accounting earnings

• Supported by Beaver, Lambert and Ryan (1987)

continued

10-40Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR—accounting earnings reflecting information (cont.)

• Dechow (1994) found over short intervals earnings are more strongly associated with returns than are realised cash flows

– the ability of cash flows to measure firm performance increases as the measurement interval increases

continued

10-41Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Results of CMR —accounting earnings reflecting information (cont.)

• Studies examining which asset value approaches provide accounting figures that best reflect market valuation found:

– fair value estimates of bank’s financial instruments seem to provide a better explanation of bank share prices than historical cost (Barth, Beaver & Landsman 1996)

– revaluation of assets results in better alignment of market and book values (Easton, Eddy & Harris 1993)

10-42Copyright © 2014 McGraw-Hill Education (Australia) Pty Ltd PPTs to accompany Deegan, Financial Accounting Theory 4e

Relaxing assumptions about market efficiency• Recent years have seen a number of researchers

questioning some assumptions about market efficiency

• Market reactions to information often found to be longer than would be anticipated from an ‘efficient market’. Also market found to sometimes ‘under-react’ to particular announcements

• Created new areas for research—for example what factors influence ‘earnings drift’

• So, should we reject research that has embraced the EMH?