Embed Size (px)

Citation preview

© Metso

Forward looking statements

It should be noted that certain statements herein which are not historical facts, including, without limitation, those regardingexpectations for general economic development and the market situation, expectations for customer industry profitability and investment willingness, expectations for company growth, development and profitability and the realization of synergy benefits and cost savings, and statements preceded by ”expects”, ”estimates”, ”forecasts” or similar expressions, are forward looking statements. These statements are based on current decisions and plans and currently known factors. They involve risks and uncertainties which may cause the actual results to materially differ from the results currently expected by the company.

Such factors include, but are not limited to:

1) general economic conditions, including fluctuations in exchange rates and interest levels which influence the operating environment and profitability of customers and thereby the orders received by the company and their margins

2) the competitive situation, especially significant technological solutions developed by competitors

3) the company’s own operating conditions, such as the success of production, product development and project management and their continuous development and improvement

4) the success of pending and future acquisitions and restructuring.

2

© Metso

50

100

150

200

250

300

350

400

0

2

4

6

8

10

12

14

Lost time incident frequency (LTIF)

Total number of lost time incidents

3 * LTIF September 2016

Safety is an important driver for successContinuous focus on safety leads to results

• Safe working environment for all employees• Improved safety performance supports

productivity• Demand from customers: license to operate• Actions leading to improvement:

• Active and visible management support

• Safety being part of every decision• Safety included in incentive plans• Continuous development of safety

culture • High focus on safe working methods• Continuous learning

LTIF2.6 *

© Metso

Third quarter 2016 in brief

• Market environment continued to be challenging

• Minerals equipment orders increased 19%

• Flow Control saw weakening in the oil and gas sector

• Profitability at a healthy level

• Good free cash flow

• Strong balance sheet

4 Figures in brackets refer to the corresponding period in 2015, unless otherwise stated.

Orders received:EUR 628 million, -3%

Net sales:EUR 638 million, -6%

Adjusted EBITA margin:12.1% (13.6%)

Free cash flow:EUR 106 million (117 million)

Net gearing:5.1% (15.0%)

© Metso

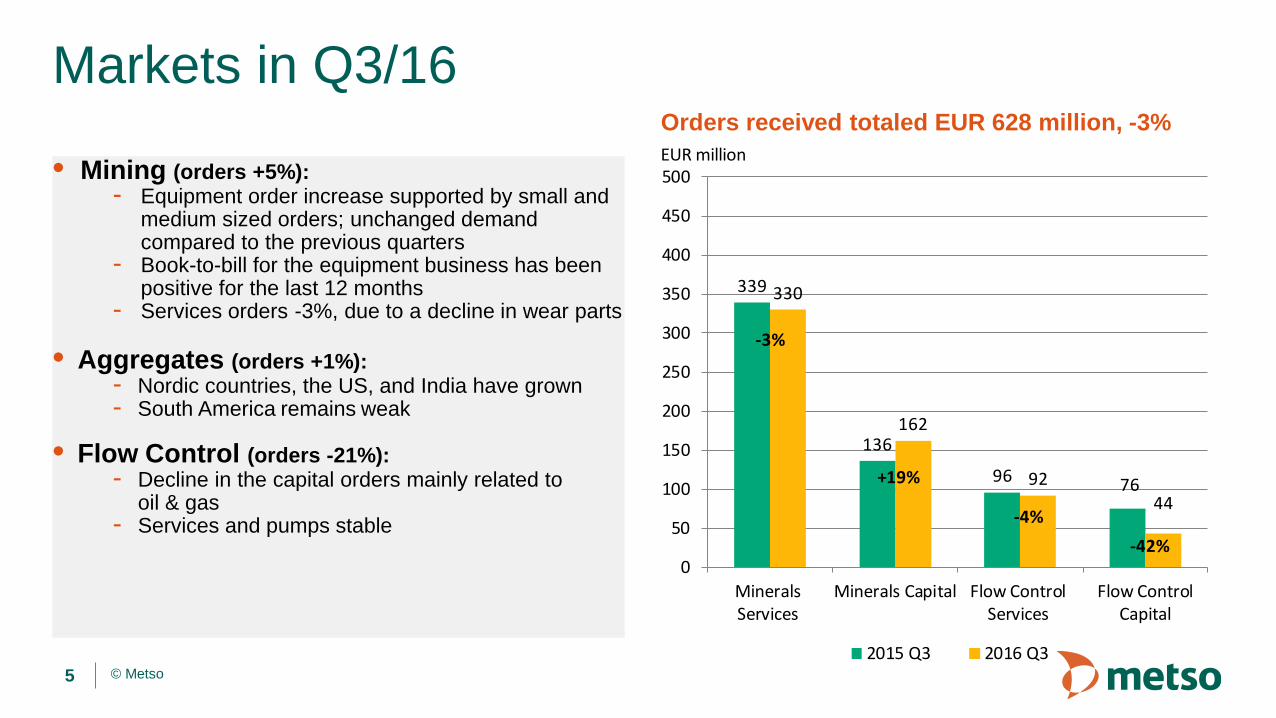

• Mining (orders +5%):- Equipment order increase supported by small and

medium sized orders; unchanged demand compared to the previous quarters

- Book-to-bill for the equipment business has been positive for the last 12 months

- Services orders -3%, due to a decline in wear parts

• Aggregates (orders +1%):- Nordic countries, the US, and India have grown- South America remains weak

• Flow Control (orders -21%):- Decline in the capital orders mainly related to

oil & gas- Services and pumps stable

Markets in Q3/16

5

Orders received totaled EUR 628 million, -3%

339

136

96 76

330

162

9244

0

50

100

150

200

250

300

350

400

450

500

MineralsServices

Minerals Capital Flow ControlServices

Flow ControlCapital

2015 Q3 2016 Q3

-3%

+19%

-4%-42%

EUR million

© Metso

Orders received by market area

6

North America Q3/ EUR 134 million, -4%Q1-Q3/ EUR 420 million, -13%

South and Central AmericaQ3/ EUR 114 million, -9%Q1-Q3/ EUR 444 million, -6%

Europe Q3/ EUR 179 million, +16%Q1-Q3/ EUR 522 million, +3%

Africa and Middle EastQ3/ EUR 61 million, +2%Q1-Q3/ EUR 208 million, -2%

China Q3/ EUR 34 million, -4%Q1-Q3/ EUR 119 million, -31%

Asia-PacificQ3/ EUR 106 million, -20%Q1-Q3/ EUR 339 million, -6%

48% from the emerging markets (Q3/2016)

© Metso

Financial highlights• Healthy profitability in the current market

situation- 12.1% adjusted EBITA margin

• Services margins remain good

• Cost control measures have delivered results and actions will continue

• Strong cash flow and balance sheet

7

791 834728 721 737

823

647

758

663761

628757

885800

921

733756

680 754

601671 638

11.4

13.7

12.413.0

10.6

12.4

13.6

12.0

9.3

11.512.1

0

2

4

6

8

10

12

14

0

200

400

600

800

1,000

1,200

1,400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2014 2015 2016

Orders received Net sales Adjusted EBITA %

EUR million %

Eeva SipiläCFO

Financial performance

© Metso

Minerals quarterly performance• Equipment orders increased 19 percent while

services orders decreased 3 percent

• EBITA remained at a good level even with lower volumes, thanks to sales mix and cost control

• Equipment business is making small profit with current volumes

• Cost efficiency actions continue

• Strong cashflow

9

597662

558 544 558642

475

585494

593492

608706

619 743 563

560501 574

453504 477

11.3

13.6

11.9

13.5

9.910.8 11.2

12.1

8.2

10.8 10.8

0

2

4

6

8

10

12

14

16

0

100

200

300

400

500

600

700

800

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2014 2015 2016

EUR million

Minerals Orders Received Minerals Net SalesMinerals adjusted EBITA %

%

© Metso

Flow Control quarterly performance• Order intake was low in the quarter driven by

oil & gas, both projects and day-to-day business were affected

• Service orders stable

• Net sales down 10 percent y-o-y reflecting lower North American order backlog

• Healthy profitability in the quarter- Decline of year-to-date profitability remains

volume driven, as gross margins are holding up

• Cost-efficiency actions continue

10

194172 172 178 179 181 172 173 169 168

136149

177185

173 170

194179 180

148 167 161

14.2

17.3

20.2

14.2

16.718.6

20.7

13.1 12.8 13.2

17.5

0

5

10

15

20

25

0

50

100

150

200

250

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2014 2015 2016

EUR million

Flow Control Orders Received Flow Control Net SalesFlow Control adjusted EBITA %

%

© Metso

Volume decline biggest single factor in profitability

11

Note: Graph is illustrative: Volume, margin and SG&A changes have been calculated with constant currencies. Currency impact is included in ’FX rates & Others’.

262 210

0

50

100

150

200

250

300

Q1-Q3/2015 AdjustedEBITA

Volume Margin S, G & A FX rates & Others Q1-Q3/2016 AdjustedEBITA

EUR million

© Metso

Gross margin is holding up despite lower volume

• Healthy product margins in all businesses despite lower volume indicate successful cost and pricing management in challenging markets

• Ongoing cost actions in businesses continue to improve structure going forward

• COGS headcount is down by over 600 persons year-to-date 2016

- approx. 1,800 down since beginning of 2015

• Procurement savings target is similar as last year (EUR 50 million)

12

211

252240

261

222235

224 220

176196

181

27.9 28.430.0

28.330.3 31.2

32.9

29.2 29.2 29.2 28.4

0

5

10

15

20

25

30

35

0

50

100

150

200

250

300

350

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2014 2015 2016Gross profit Gross margin

EUR million %

© Metso

SG&A costs flat in proportion to sales

• Efficiency measures have reduced SG&A headcount by over 300 persons year-to-date 2016

- over 900 reduction since the beginning of 2015

• Actions will continue but also incur restructuring costs in fourth quarter

• Discretionary spend controls continue

• No significant credit losses

13

139151

142

167

147 147

127

149

126 130 125

18.417.0 17.7 18.1

20.1 19.418.6

19.820.9

19.4 19.6

0

5

10

15

20

25

0

50

100

150

200

250

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2014 2015 2016

EUR million

SGA SGA %

%

© Metso

Healthy cash flow and solid financial position

EUR million Q3/2016 Q3/2015 Change % Q1-Q3/ 2016 Q1-Q3/ 2015 Change % 2015

EBIT 63 76 -17 183 488* -63 555*

Earnings per share, EUR 0.24 0.29 -17 0.70 2.60* -73 2.95*

Free cash flow 106 117 -9 242 282 -14 341

* Including capital gain from divestment of PAS14

Sep 30, 2016 Dec 31, 2015

Return on equity (ROE), annualized, % 9.8 33.1*

Return on capital employed (ROCE) before taxes, annualized, % 11.2 25.7*

Gearing at the end of the period, % 5.1 10.6

Cash conversion, % 233 180

Equity to assets ratio at the end of the period, % 48.1 48.3

© Metso

592 598 609 588 550

537 590 626511 620

552 550 542541

537

345 343 330331 310

181 186 185193 180

2,207 2,267 2,2922,164 2,197

0

500

1,000

1,500

2,000

2,500

Q3 Q4 Q1 Q2 Q3

2015 2016

EUR Million

Capital employed and net working capital

15

Net working capital

Cash

Intangible assets

Tangible assets

Other

Net working capital

Inventories

Trade payables

Advances + POC

Other

Trade receivables

752 715 726 728 709

486 482 450 476 459

-279 -249 -234 -255 -241

-155 -128 -133 -152 -173

-212 -222 -200 -209 -204

592 598 609 588 550

-1,000

-500

0

500

1,000

1,500

Q3 Q4 Q1 Q2 Q3

2015 2016

EUR million

Matti Kähkönen President and CEO

Outlook and backlog

© Metso

24% of net sales of which 60% services*

Outlook:• Satisfactory for products related to

customers’ new investments as well as services

• Increased uncertainty in the oil & gas market

*Based on rolling 12 months net sales

Short-term market outlook largely unchanged

17

50% of net sales of which 70% services*

Outlook:• Weakness to continue in the

equipment and systems business• Order pipeline consists of small and

midsize orders• Demand for services satisfactory;

activity in engineered services is soft and miners’ cost actions continue

23% of net sales of which 45% services*

Outlook:• Satisfactory for both equipment and

services• The Nordics, North America and India

remain positive• Brazil continues to be weak

Mining Aggregates Flow Control

© Metso

Order backlog

18

Flow ControlMinerals, services

• Backlog 3% higher compared to the end of 2015• Deliveries for the following year 18% higher year-on-year• Market uncertainties causing some delays in deliveries

Minerals, capital

1,780 1,735 1,672

1,402 1,445 1,4111,289 1,268 1,300

1,3991,305

0

500

1,000

1,500

2,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2014 2015 2016

EUR Million

Deliveries in 2016

Deliveries after 2016

Deliveries in 2015

Deliveries after 2015

0

200

400

600

800

1,000

1,200

1,400

Order backlog Sep 30, 2015 Order backlog Sep 30, 2016

EUR million

© Metso19

Outlook for 2016

Metso’s overall trading conditions will be somewhat weaker in 2016 compared to 2015. Demand for our products and services is expected to develop as follows:

• remain weak for mining equipment and satisfactory for mining services • remain satisfactory for aggregates equipment and services• remain satisfactory for Flow Control products related to customers’ new

investments and has changed to satisfactory (previously: good) for Flow Control services, with increased uncertainty in the oil & gas market

At the end of September 2016, our backlog for the remainder of 2016 totaled approximately EUR 680 million but due to current market conditions we expect some deliveries to be postponed into 2017.

Internal efficiency actions will continue to improve competitiveness, resulting in net adjustment items of approximately EUR 30 million in 2016. Capital expenditure excluding acquisitions is expected to be lower than in 2015. Net financial costs are expected to be on the same level as in 2015.

company/metso metsogroup metsoworldmetsoworld metsogroup

www.metso.com

Appendix

© Metso

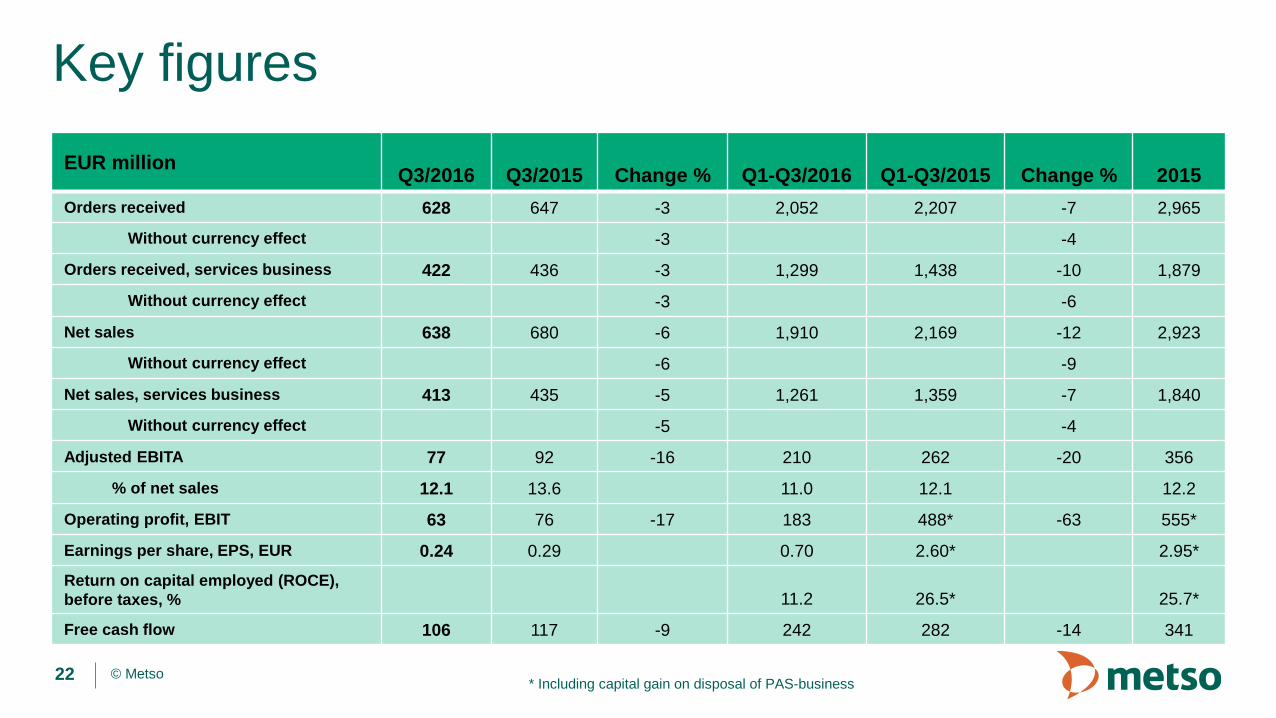

Key figures

22 * Including capital gain on disposal of PAS-business

EUR million Q3/2016 Q3/2015 Change % Q1-Q3/2016 Q1-Q3/2015 Change % 2015Orders received 628 647 -3 2,052 2,207 -7 2,965

Without currency effect -3 -4

Orders received, services business 422 436 -3 1,299 1,438 -10 1,879

Without currency effect -3 -6

Net sales 638 680 -6 1,910 2,169 -12 2,923

Without currency effect -6 -9

Net sales, services business 413 435 -5 1,261 1,359 -7 1,840

Without currency effect -5 -4

Adjusted EBITA 77 92 -16 210 262 -20 356

% of net sales 12.1 13.6 11.0 12.1 12.2

Operating profit, EBIT 63 76 -17 183 488* -63 555*

Earnings per share, EPS, EUR 0.24 0.29 0.70 2.60* 2.95*

Return on capital employed (ROCE), before taxes, % 11.2 26.5* 25.7*

Free cash flow 106 117 -9 242 282 -14 341