Embed Size (px)

Citation preview

17 March 2017

Scania AB (publ) 151 87 Södertälje Tel. +46 8 553 810 00

Corporate identity number Sweden Fax +46 8 553 810 37

556184-8564 www.scania.com

Scania Year-end Report January–December 2016

Summary of the full year 2016

• Operating income excluding items affecting comparability rose by 6 percent to SEK 10,184 m. (9,641), resulting in

an operating margin of 9.8 (10.2) percent

• Operating income amounted to SEK 6,384 m. (9,641) and was negatively impacted by a provision of SEK 3.8

billion related to the European Commission’s competition investigation

• Net sales rose by 10 percent to a record high SEK 103,927 m. (94,897)

• Cash flow amounted to SEK 3,427 m. (4,376) in Vehicles and Services

Comments by Henrik Henriksson, President and CEO: “Scania’s net sales rose to a record level of nearly SEK

104 billion. Total deliveries of trucks and buses and

coaches reached all-time high levels. Service revenue

amounted to a record of almost SEK 22 billion, an

increase of 5 percent (7 percent in local currency). The

company’s operational performance was strong. Higher

vehicle volume in Europe and higher service volume

impacted earnings positively but this was partly offset by

negative currency rate effects, lower deliveries in Latin

America (mainly related to Brazil), and by the high cost of

investments related to Scania’s new truck generation.

Scania’s position in the European market remains strong

with a market share of 16.5 percent. The replacement

need and economic situation in Europe continues to have

a positive impact on demand for trucks. Order bookings in

Latin America remain at a low level, mainly due to the very

uncertain situation in Brazil. In Eurasia, order bookings

increased somewhat and Russia appears to have

bottomed out. Demand for buses and coaches remains at

a high level in Europe. In Engines, demand for industrial

and marine engines is good, while remaining weak on the

power generation side. The success of the new generation

of Scania trucks has been immediate and the truck has

outperformed the competition in all trade press tests it has

entered. Nearly all aspects have been praised – the

powertrain, performance, comfort, braking capacity,

visibility and steering. Combined with Scania Maintenance

with Flexible Plans, our new tailor-made service enabled

by continual monitoring of connected vehicles’ operating

data, customer earning potential is enhanced. When every

truck receives exactly the maintenance it needs, the

customer enjoys maximum vehicle uptime.“

Financial overview Full year 2016 Q4

Trucks and buses, units 2016 2015

Change,

% 2016 2015

Change,

%

Order bookings 85,527 77,091 11 23,262 19,199 21

Deliveries 81,346 76,561 6 22,614 21,626 5

Net sales and earnings

EUR

m.*

Net sales, Scania Group, SEK m. 10,863 103,927 94,897 10 28,718 25,211 14

Operating income, Vehicles and Services, SEK m. 561 5,369 8,601 -38 2,401 2,349 2

Operating income, excl. items affecting comparability,

vehicles and Services, SEK m. 958 9,169 8,601 7 2,401 2,349 2

Operating income, Financial Services, SEK m. 106 1,015 1,040 -2 250 246 2

Operating income, SEK m. 667 6,384 9,641 -34 2,651 2,595 2

Income before taxes, SEK m. 623 5,963 9,109 -35 2,520 2,420 4

Net income for the period, SEK m. 339 3,243 6,753 -52 1,816 1,813 0

Operating margin, % 6.1 10.2 9.2 10.3

Operating margin, excl. items affecting comparability, % 9.8 10.2 9.2 10.3

Return on capital employed, Vehicles and Services, % 14.0 19.3

Return on capital employed, excl. items affecting

comparability, Vehicles and Services, % 21.5 19.3

Cash flow, Vehicles and Services, SEK m. 358 3,427 4,376 -22 3,619 3,156 15

* Translated to EUR solely for the convenience of the reader at a closing day rate of SEK 9,5672 = EUR 1.00.

Unless otherwise stated, all comparisons refer to the corresponding period of the preceding year.

This interim report has not been subject to review by the company’s auditors. This report is also available on www.scania.com

Scania Year-end Report January-December 2016

Business overview

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

24,000

27,000

Q1 Q2 Q3 Q4

Number of vehicles delivered2013 2014 2015 2016

0

5,000

10,000

15,000

20,000

25,000

30,000

Q1 Q2 Q3 Q4

Net sales, SEK m.2013 2014 2015 2016

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

Q1 Q2 Q3 Q4

Operating income, SEK m.2013 2014 2015 2016

Sales performance

During the full year 2016, total vehicle deliveries increased by 6 percent to 81,346 (76,561) units,

compared to 2015, which was an all-time high level. Net sales rose by 10 percent to SEK 103,927 m.

(94,897), the highest level in Scania’s history. Currency rate effects had a negative impact on sales of

2 percent.

Order bookings increased by 11 percent to 85,527 (77,091) vehicles, compared to the full year 2015.

Higher demand in nearly all regions in the fourth quarter

Total order bookings for trucks were higher in the fourth quarter of 2016 than the year-earlier period and

the increase was seen in all regions, apart from Africa and Oceania. Demand in Europe remained strong

during the fourth quarter, supported by a replacement need and a positive economic situation. In Eurasia,

demand rose compared to the same period of 2015, mainly related to Russia, a market that now appears

to have bottomed out. In Latin America, order bookings rose compared to the fourth quarter last year. The

increase was due to an upturn in Argentina and Chile, and also in Brazil, which increased somewhat

compared to the extremely low level in the fourth quarter last year. Order bookings also rose in Asia,

primarily related to increases in China, Hong Kong, Iran and India. In the Africa and Oceania region, order

bookings decreased, primarily related to South Africa.

Total order bookings for trucks rose sequentially in the fourth quarter (compared to the previous quarter of

2016), thanks to continued strong demand in Europe and the normal seasonal pattern in the European

market.

Through its global production system, Scania is able to balance the industrial system relatively well by

utilising free production capacity in Brazil in order to export more to Africa, the Middle East and Asia.

Demand for used vehicles in Europe remains strong.

Market share in Europe remains high

Scania’s market share for trucks in Europe was 16.5 percent during the period January to December 2016

compared to 16.4 percent during the same period of 2015. The continued high level confirms that the

current Scania truck range delivers a level of quality and performance that customers highly appreciate. It

is also connected to the early and very successful introduction of the Euro 6 range and Scania’s broad

engine range for alternative fuels. Increased sales activities in new segments have also contributed to the

high market share in Europe.

A successful new truck generation

In August, Scania launched its new truck range and the first deliveries to customers were made during the

fourth quarter of 2016.

The new truck generation has been an immediate success and the new Scania truck has outperformed the

competition in all of the prestigious comparative and individual trade press tests that it has entered.

The new truck generation has been praised in almost every respect – for its powertrain, performance,

comfort, braking capacity, visibility and steering. “High performance with low fuel consumption, the best

driving characteristics, a high level of comfort and a better place to work – that skilfully paves the way for

the new S-class,” wrote the leading German trade magazine Lastauto Omnibus when summarising the

Excluding items affecting comparability (Q2 2016)

2

Scania Year-end Report January-December 2016

demanding comparative 1,000 point test. It further reported, “Scania excels in lateral stability with precise

steering and an overall feeling of control.”

In another comparative test led by German trade magazine KFZ-Anzeiger, the Scania S 500 was found to

be “sensationally economical”. In fact, it was the first truck to register under 30 litres/100 km on their test

route. Definitely value for money, was the verdict.

The excellent fuel economy performance was also confirmed in Routes’ test, the leading trade magazine in

France. It subjected the new Scania R 500 to rigorous tests along a 419-kilometre route in south-eastern

France. Over the five hours of testing, the new generation Scania R 500 recorded the lowest-ever average

fuel consumption of 28.4 litres/100 km.

The truck market Order bookings

Scania’s order bookings rose during the fourth quarter of 2016 and totalled 21,727 (17,044) trucks. Order

bookings in Europe increased by 19 percent to 13,871 (11,660) units, compared to the fourth quarter of

2015. Demand rose in several major European markets such as Great Britain, Germany, Poland and

France. Order bookings rose sequentially (compared to the previous quarter) in Europe in line with the

seasonal pattern in the European market.

Order bookings in Latin America increased during the fourth quarter of 2016 compared to the same period

of the previous year, mainly due to increases in Brazil, Argentina and Chile. Order bookings also rose

somewhat sequentially in Latin America. The outlook for the region remains uncertain due to low economic

growth.

In Eurasia, total order bookings rose during the fourth quarter and amounted to 1,582 (340) trucks. The

upturn was mainly attributable to Russia. Order bookings also rose sequentially in Eurasia. The outlook for

the region remains uncertain due to geopolitical turbulence.

In Asia, demand during the quarter increased by 23 percent compared to the year-earlier period and order

bookings amounted to 2,912 (2,367) units. Compared to the third quarter of 2016, order bookings also

rose.

In Africa and Oceania, order bookings were lower at 1,194 (1,284) units compared to the fourth quarter of

2015, mainly related to a downturn in South Africa. Order bookings also decreased sequentially in Africa

and Oceania.

Deliveries

Scania's total truck deliveries increased by 2 percent to 20,033 (19,601) units during the fourth quarter

compared to the year-earlier period. In Europe, deliveries rose by 3 percent to 12,877 (12,462) units

compared to the fourth quarter of 2015. In Eurasia, deliveries rose to 1,335 (672) trucks. In Latin America,

deliveries rose by 2 percent to 2,077 (2,038) units compared to the fourth quarter of 2015. In Asia,

deliveries decreased compared to the fourth quarter of 2015 to 2,490 (3,003) trucks. Deliveries in Africa

and Oceania decreased by 12 percent to 1,254 (1,426) trucks.

Sales

Net sales of trucks rose by 7 percent to SEK m. 65,615 (61,250) during the full year 2016. During the fourth

quarter, sales increased by 9 percent to SEK m. 18,557 (17,046).

The total European market for heavy trucks

The total market for heavy trucks in 25 of the European Union member countries (all EU countries except

Greece, Bulgaria and Malta) plus Norway and Switzerland increased by 12.4 percent to about 300,200

(267,100) units during the full year 2016. Scania truck registrations amounted to some 49,500 (44,100)

units, equivalent to a market share of about 16.5 (16.4) percent.

3

Scania Year-end Report January-December 2016

Scania trucks Order bookings Deliveries

12 months

2016

12 months

2015

Change,

%

12 months

2016

12 months

2015

Change,

%

Europe 51,569 47,692 8 49,102 43,082 14

Eurasia 4,016 1,962 105 3,233 2,583 25

America* 7,232 7,438 -3 7,022 8,118 -14

Asia 9,834 8,349 18 9,287 11,514 -19

Africa and Oceania 4,992 4,658 7 4,449 4,465 0

Total 77,643 70,099 11 73,093 69,762 5

*Refers to Latin America

The bus and coach market Order bookings

Order bookings for buses and coaches during 2016 increased compared to the previous year to

7,884 (6,992) units.

Scania has increased its market share in buses and coaches in Europe to 7.1 percent, compared to

6.8 percent in 2015.

In the fourth quarter order bookings in Europe decreased and totalled 669 (691). The decrease mainly

occurred in Sweden, Poland and Germany. In Latin America, order bookings fell by 47 percent to 276 (525)

units compared to the fourth quarter of 2015. In Asia, order bookings fell to 360 (616) buses and coaches

compared to the fourth quarter of 2015. Order bookings in Africa and Oceania decreased to 228 (320)

buses and coaches.

Deliveries

Scania’s bus and coach deliveries totalled 2,581 (2,025) units during the fourth quarter. In Europe,

deliveries increased by 9 percent to 587 (537) units compared to the fourth quarter of 2015. In Latin

America, deliveries rose by 19 percent to 751 (629). In Asia, deliveries sharply increased to 949 (553),

while deliveries of buses and coaches in Africa and Oceania decreased during the fourth quarter to 265

(285) units. Deliveries to Eurasia increased to 29 (21) units.

Net sales

Net sales of buses and coaches rose by 21 percent to SEK 10,867 m. (8,994) during the full year 2016.

During the fourth quarter, sales increased by 32 percent to SEK 3,335 m. (2,524).

Scania buses and coaches

Order bookings Deliveries

12 months

2016

12 months

2015

Change,

%

12 months

2016

12 months

2015

Change,

%

Europe 2,185 1,937 13 2,094 1,917 9

Eurasia 57 80 -29 62 94 -34

America* 2,559 2,275 12 2,350 2,123 11

Asia 2,226 1,828 22 2,568 1,806 42

Africa and Oceania 857 872 -2 1,179 859 37

Total 7,884 6,992 13 8,253 6,799 21

*Refers to Latin America

4

Scania Year-end Report January-December 2016

Engines Order bookings

In Engines, demand for industrial and marine engines is good, while remaining weak on the power

generation side. Total engine order bookings fell by 6 percent to 7,611 (8,140) units during 2016 compared

to 2015. During the fourth quarter, order bookings increased by 6 percent to 1,838 (1,726) units.

Deliveries

Engine deliveries decreased by 8 percent to 7,800 (8,485) units during the full year 2016. During the fourth

quarter, deliveries rose by 29 percent to 2,380 (1,846) units.

Net sales

During the full year, net sales decreased by 1 percent to SEK 1,647 m. (1,656). Net sales in the fourth

quarter amounted to SEK 517 m. (369), an upturn of 40 percent.

Services Record high revenue

Service revenue amounted to a record high SEK 21,611 m. (20,585) during the full year 2016, an increase

of 5 percent. Higher volume, mainly in Europe, had a positive impact, while currency rate effects were

negative. In local currencies, revenue increased by 7 percent. During the fourth quarter, revenue rose by

10 percent to SEK 5,782m. (5,260). In local currency, the upturn was 6 percent.

In Europe, service revenue rose by 6 percent to SEK 15,020 m. (14,180) compared to the full year 2015.

In Latin America, revenue decreased by 1 percent to SEK 2,660 m. (2,698) and revenue in Asia was 11

percent higher than the previous year at SEK 1,998 m. (1,800). In Africa and Oceania, service revenue

rose by 4 percent to SEK 1,393 m. (1,337), while in Eurasia it decreased by 5 percent to SEK 540 m. (570)

compared to the full year 2015.

Earnings Vehicles and Services Full year 2016

Operating income in Vehicles and Services amounted to SEK 5,369 m. (8,601) during the full year 2016.

It was negatively impacted by a provision of SEK 3.8 billion related to the European Commission’s

competition investigation. Adjusted for items affecting comparability, operating income in Vehicles and

Services amounted to SEK 9,169 m. (8,601) during the full year 2016. Higher vehicle volume in Europe

and higher service volume impacted earnings positively but this was partly offset by negative currency rate

effects, lower deliveries in Latin America (mainly related to Brazil), and by the high cost of investments

related to Scania’s new truck generation.

Compared to the full year 2015, the total currency rate effect was negative and amounted to about

SEK 900 m.

Scania’s research and development expenditures amounted to SEK 7,199 m. (7,043). After adjusting for

SEK 1,682 m. (1,863) in capitalised expenditures and SEK 387 m. (393) in depreciation of previously

capitalised expenditures, recognised expenses increased to SEK 5,904 m. (5,573).

The fourth quarter

Operating income in Vehicles and Services totalled SEK 2,401 m. (2,349) during the fourth quarter. Higher

vehicle volume in Europe, high service volume and currency rate effects had a positive impact on earnings.

The high cost of investments related to Scania’s new truck generation and lower deliveries in Latin America

(mainly related to Brazil), had a negative effect.

Compared to the fourth quarter of 2015, the total currency rate effect was positive and amounted to about

SEK 225 m.

5

Scania Year-end Report January-December 2016

Scania’s research and development expenditures amounted to SEK 1,893 m. (1,968). After adjusting for

SEK 449 m. (568) in capitalised expenditures and SEK 102 m. (100) in depreciation of previously

capitalised expenditures, recognised expenses increased to SEK 1,546 m. (1,500).

Financial Services Customer finance portfolio

At the end of 2016, the size of Scania’s customer finance portfolio amounted to SEK 67.9 billion, which

was SEK 11.4 billion higher than the end of 2015. In local currencies, the portfolio increased by SEK 8.0

billion, equivalent to 14.2 percent.

Penetration rate

The penetration rate was 43 (42) percent during the full year 2016 in those markets where Scania has its

own financing operations. The increase was mainly attributable to the market mix.

Operating income

Operating income in Financial Services decreased to SEK 1,015 m. (1,040) for the full year 2016,

compared to 2015. A larger portfolio had a positive impact on earnings while lower margins and negative

currency rate effects had an adverse impact. Bad debt expenses decreased somewhat. In the fourth

quarter, operating income rose by 2 percent to SEK 250 m. (246).

Scania Group During the full year 2016, Scania’s operating income amounted to SEK 6,384 m. (9,641). Operating margin

amounted to 6.1 (10.2) percent. Operating income was negatively impacted by a provision of SEK 3.8

billion related to the European Commission’s competition investigation. Adjusted for items affecting

comparability, operating income amounted to SEK 10,184 m. (9,641) during 2016. Scania’s net financial

items amounted to SEK -421 m (-532).

The Scania Group’s tax expense amounted to SEK 2,720 m. (2,356), equivalent to 27.9 (25.9) percent of

income before taxes when adjusted for items affecting comparability.

Net income for the period totalled SEK 3,243 m. (6,753), equivalent to a net margin of 3.1 (7.1) percent.

Adjusted for items affecting comparability, net income for the period totalled SEK 7,043 m. (6,753),

equivalent to a net margin of 6.8 (7.1) percent.

Cash flow Vehicles and Services Scania’s cash flow in Vehicles and Services amounted to SEK 3,427 m. (4,376) for the full year 2016.

Tied-up working capital decreased by SEK 878 m (1,656).

Net investments amounted to SEK 7,864 m. (7,737) including SEK 1,682 m. (1,863) in capitalisation of

development expenses. At the end of the fourth quarter of 2016, the net cash position in Vehicles and

Services amounted to SEK 10,954 m. compared to a net cash position of SEK 7,579 m. at the end of 2015.

Scania Group Scania’s cash flow in Financial Services amounted to SEK -7,784 m. (-3,816) during the full year 2016 due

to a growing customer finance portfolio. The Group’s net debt increased by about SEK 7.6 billion compared

to the end of 2015 mainly due to investments in the Financial Services portfolio which was partly offset by a

positive cash flow.

6

Scania Year-end Report January-December 2016

Parent Company The assets of the Parent Company, Scania AB, consist of shares in Scania CV AB. Scania CV AB is the

Parent Company of the Group that comprises all production and sales and service companies as well as

other companies. Income before taxes of Scania AB totalled SEK 0 m. (0) during 2016.

Miscellaneous Number of employees At the end of 2016, the number of employees totalled 46,243 compared to 44,409 on the same date in

2015.

Material risks and uncertainty factors The section entitled “Risks and risk management” in Scania’s Annual and Sustainability Report for 2015

describes Scania’s strategic, operational, legal and financial risks. Note 2 of the same report provides a

detailed account of key judgements and estimates. Note 27 of the same report describes the financial

risks, such as currency risk and interest rate risk. The risks that have the greatest impact on financial

performance and on reporting for the Group and the Parent Company are summarised as follows:

a) Sales with obligations

About 15 percent of the vehicles Scania sells are delivered with residual value obligations or repurchase

obligations. These are recognised as operating lease contracts, with the consequence that recognition of

revenue and earnings is allocated over the life of the obligation (contract). If there are major changes in the

market value of used vehicles, this increases the risk of future losses when selling returned vehicles. When

a residual value obligation is deemed likely to cause a future loss, a provision is made in cases where the

expected loss exceeds the as-yet-unrecognised profit on the vehicle.

b) Credit risks

In its Financial Service operations, Scania has an exposure in the form of contractual future payments.

This exposure is reduced by the collateral Scania has in the form of the right to repossess the underlying

vehicle. In case the market value of the collateral does not cover the exposure to the customer, Scania

runs a credit risk. Reserves for probable losses in Financial Service operations are set aside in the

estimated amounts required.

Accounting principles Scania applies International Financial Reporting Standards (IFRSs) as adopted by the EU. This Interim

Report for the Scania Group has been prepared in accordance with IAS 34, “Interim Financial Reporting”

and the Annual Accounts Act. New and revised standards and interpretations that have been applied from

1 January 2016 have not had any significant impact on Scania’s financial statements. Accounting principles

and calculation methods are unchanged from those applied in the Annual Report for 2015.

The Year-end Report for the Parent Company, Scania AB, has been prepared in accordance with the

Annual Accounts Act and recommendation RFR 2, “Accounting for Legal Entities” of the Swedish Financial

Reporting Board.

Dividend and Annual General Meeting Scania held an Extraordinary General Meeting in December 2015 and decided on a dividend of

SEK 9,600 m. The dividend of SEK 9,600 m. corresponded to approximately 50 percent of the net income

for the financial years of 2013, 2014 and 2015.

Scania’s Annual General Meeting for the financial year 2015 was held in Södertälje, Sweden on 11 May

2016.

7

Scania Year-end Report January-December 2016

The board decided on a dividend proposal of SEK 0 for the financial year of 2016. The dividend policy of

distributing approximately 50 percent of the net income over time is still valid, why future dividends can

comprise accumulated earnings from several years.

Contact persons

Susanna Berlin

Investor Relations

Tel. +46 8 553 861 12

Mobil tel. +46 70 086 05 02

Erik Ljungberg

Corporate Relations

Tel. +46 8 553 835 57

Mobile tel. +46 73 988 35 57

8

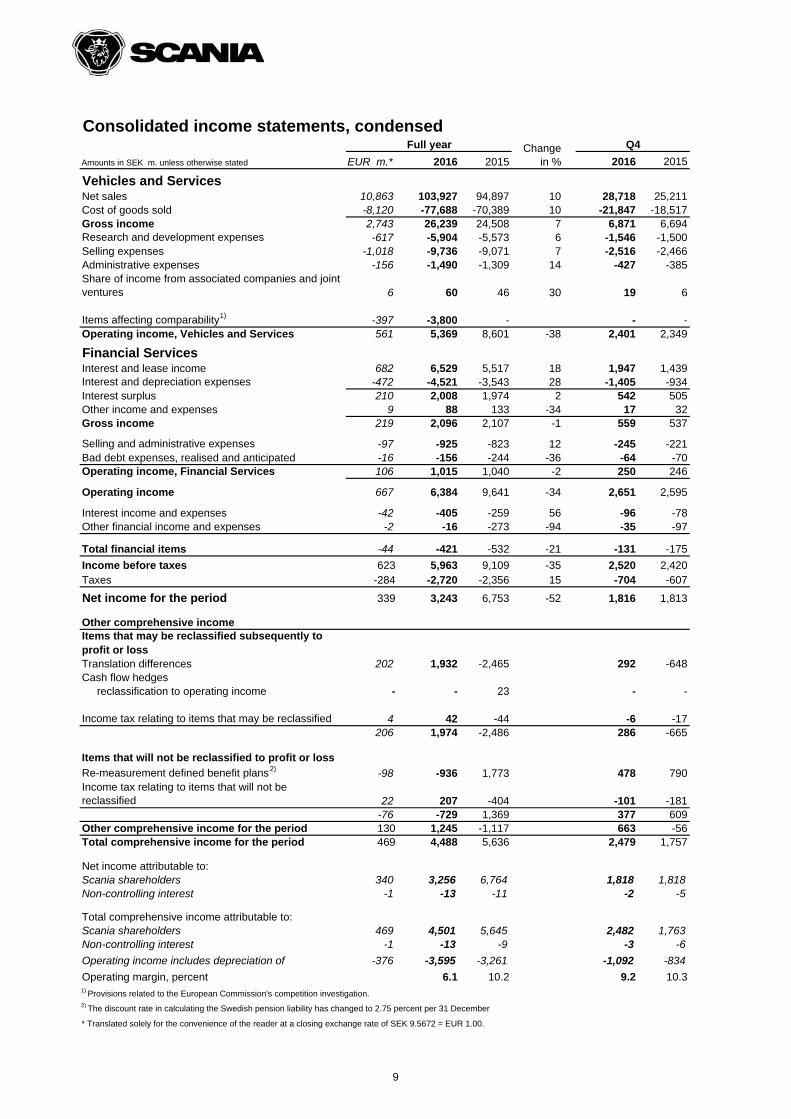

Consolidated income statements, condensed

EUR m.* 2016 2015 2016 2015

Vehicles and ServicesNet sales 10,863 103,927 94,897 10 28,718 25,211Cost of goods sold -8,120 -77,688 -70,389 10 -21,847 -18,517Gross income 2,743 26,239 24,508 7 6,871 6,694Research and development expenses -617 -5,904 -5,573 6 -1,546 -1,500Selling expenses -1,018 -9,736 -9,071 7 -2,516 -2,466Administrative expenses -156 -1,490 -1,309 14 -427 -385Share of income from associated companies and joint ventures 6 60 46 30 19 6

Items affecting comparability1) -397 -3,800 - - -Operating income, Vehicles and Services 561 5,369 8,601 -38 2,401 2,349

Financial ServicesInterest and lease income 682 6,529 5,517 18 1,947 1,439Interest and depreciation expenses -472 -4,521 -3,543 28 -1,405 -934Interest surplus 210 2,008 1,974 2 542 505Other income and expenses 9 88 133 -34 17 32Gross income 219 2,096 2,107 -1 559 537

Selling and administrative expenses -97 -925 -823 12 -245 -221Bad debt expenses, realised and anticipated -16 -156 -244 -36 -64 -70Operating income, Financial Services 106 1,015 1,040 -2 250 246

Operating income 667 6,384 9,641 -34 2,651 2,595

Interest income and expenses -42 -405 -259 56 -96 -78Other financial income and expenses -2 -16 -273 -94 -35 -97

Total financial items -44 -421 -532 -21 -131 -175

Income before taxes 623 5,963 9,109 -35 2,520 2,420Taxes -284 -2,720 -2,356 15 -704 -607

Net income for the period 339 3,243 6,753 -52 1,816 1,813

Other comprehensive incomeItems that may be reclassified subsequently to profit or lossTranslation differences 202 1,932 -2,465 292 -648Cash flow hedges reclassification to operating income - - 23 - -

Income tax relating to items that may be reclassified 4 42 -44 -6 -17206 1,974 -2,486 286 -665

Items that will not be reclassified to profit or loss

Re-measurement defined benefit plans2) -98 -936 1,773 478 790Income tax relating to items that will not be reclassified 22 207 -404 -101 -181

-76 -729 1,369 377 609Other comprehensive income for the period 130 1,245 -1,117 663 -56Total comprehensive income for the period 469 4,488 5,636 2,479 1,757

Net income attributable to:Scania shareholders 340 3,256 6,764 1,818 1,818Non-controlling interest -1 -13 -11 -2 -5

Total comprehensive income attributable to:Scania shareholders 469 4,501 5,645 2,482 1,763Non-controlling interest -1 -13 -9 -3 -6

Operating income includes depreciation of -376 -3,595 -3,261 -1,092 -834

Operating margin, percent 6.1 10.2 9.2 10.31) Provisions related to the European Commission's competition investigation.2) The discount rate in calculating the Swedish pension liability has changed to 2.75 percent per 31 December

* Translated solely for the convenience of the reader at a closing exchange rate of SEK 9.5672 = EUR 1.00.

Amounts in SEK m. unless otherwise stated

Change in %

Q4Full year

9

Net sales and deliveries, Vehicles and Services

Amounts in SEK m. unless otherwise stated EUR m. 2016 2015 2016 2015

Net salesTrucks 6,858 65,615 61,250 7 18,557 17,046Buses* 1,136 10,867 8,994 21 3,335 2,524Engines 172 1,647 1,656 -1 517 369Service-related products 2,259 21,611 20,585 5 5,782 5,260Used vehicles 674 6,452 6,236 3 1,772 1,661Miscellaneous 288 2,753 1,836 50 481 352Delivery sales value 11,387 108,945 100,557 8 30,444 27,212

Revenue deferrals1) -524 -5,018 -5,660 -11 -1,726 -2,001Net sales 10,863 103,927 94,897 10 28,718 25,211

Net sales2)

Europe 7,126 68,174 59,880 14 17,652 16,203Eurasia 344 3,291 2,623 25 1,359 680America** 1,120 10,713 11,781 -9 3,215 2,843Asia 1,379 13,194 13,055 1 3,853 3,438Africa and Oceania 894 8,555 7,559 13 2,639 2,046Net sales 10,863 103,927 94,897 10 28,718 25,211

Total delivery volume, unitsTrucks 73,093 69,762 5 20,033 19,601Buses* 8,253 6,799 21 2,581 2,025Engines 7,800 8,485 -8 2,380 1,846

1) Refers to the difference between sales value based on deliveries and revenue recognised as income2) Revenues from external customers by location of customers

* Including body-built buses and coaches

** Refers mainly to Latin America

Full year Change in %

Q4

10

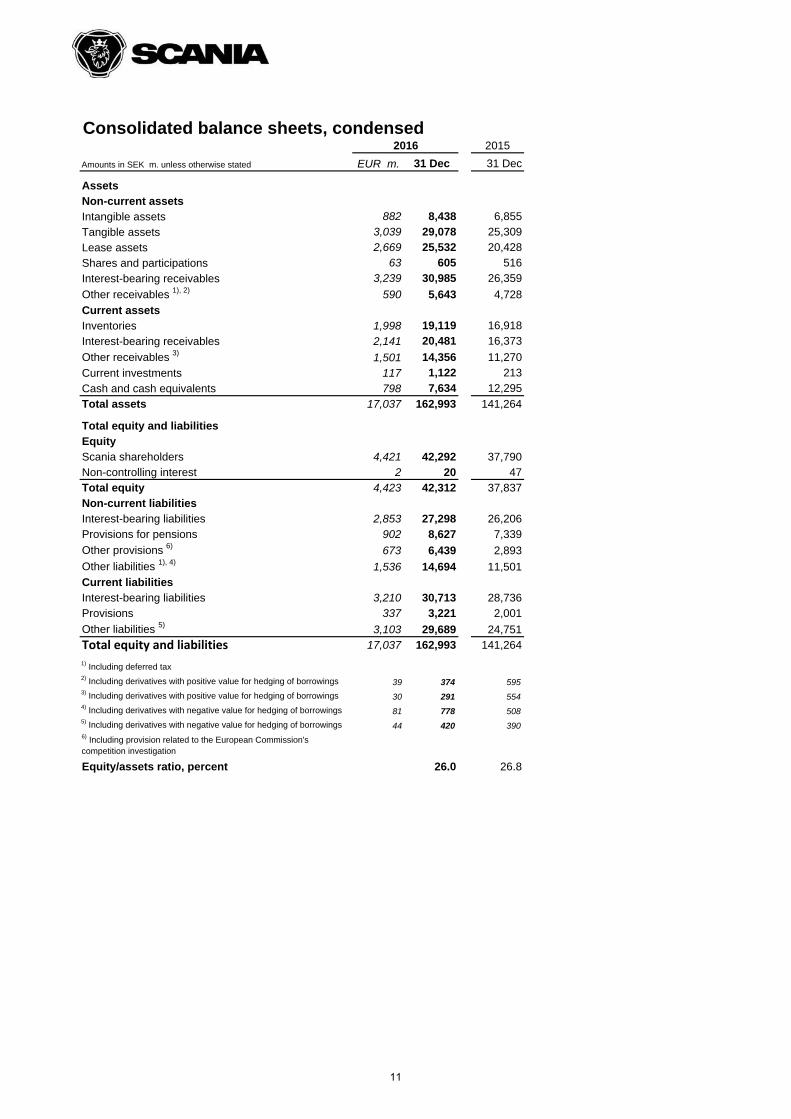

Consolidated balance sheets, condensed

EUR m. 31 Dec 31 Dec

AssetsNon-current assetsIntangible assets 882 8,438 6,855

Tangible assets 3,039 29,078 25,309

Lease assets 2,669 25,532 20,428

Shares and participations 63 605 516

Interest-bearing receivables 3,239 30,985 26,359

Other receivables 1), 2) 590 5,643 4,728

Current assetsInventories 1,998 19,119 16,918

Interest-bearing receivables 2,141 20,481 16,373

Other receivables 3) 1,501 14,356 11,270

Current investments 117 1,122 213

Cash and cash equivalents 798 7,634 12,295

Total assets 17,037 162,993 141,264

Total equity and liabilitiesEquityScania shareholders 4,421 42,292 37,790Non-controlling interest 2 20 47Total equity 4,423 42,312 37,837Non-current liabilitiesInterest-bearing liabilities 2,853 27,298 26,206Provisions for pensions 902 8,627 7,339

Other provisions 6) 673 6,439 2,893

Other liabilities 1), 4) 1,536 14,694 11,501Current liabilitiesInterest-bearing liabilities 3,210 30,713 28,736Provisions 337 3,221 2,001

Other liabilities 5) 3,103 29,689 24,751

Total equity and liabilities 17,037 162,993 141,264

1) Including deferred tax2) Including derivatives with positive value for hedging of borrowings 39 374 5953) Including derivatives with positive value for hedging of borrowings 30 291 5544) Including derivatives with negative value for hedging of borrowings 81 778 5085) Including derivatives with negative value for hedging of borrowings 44 420 3906) Including provision related to the European Commission's competition investigation

Equity/assets ratio, percent 26.0 26.8

2016

Amounts in SEK m. unless otherwise stated

2015

11

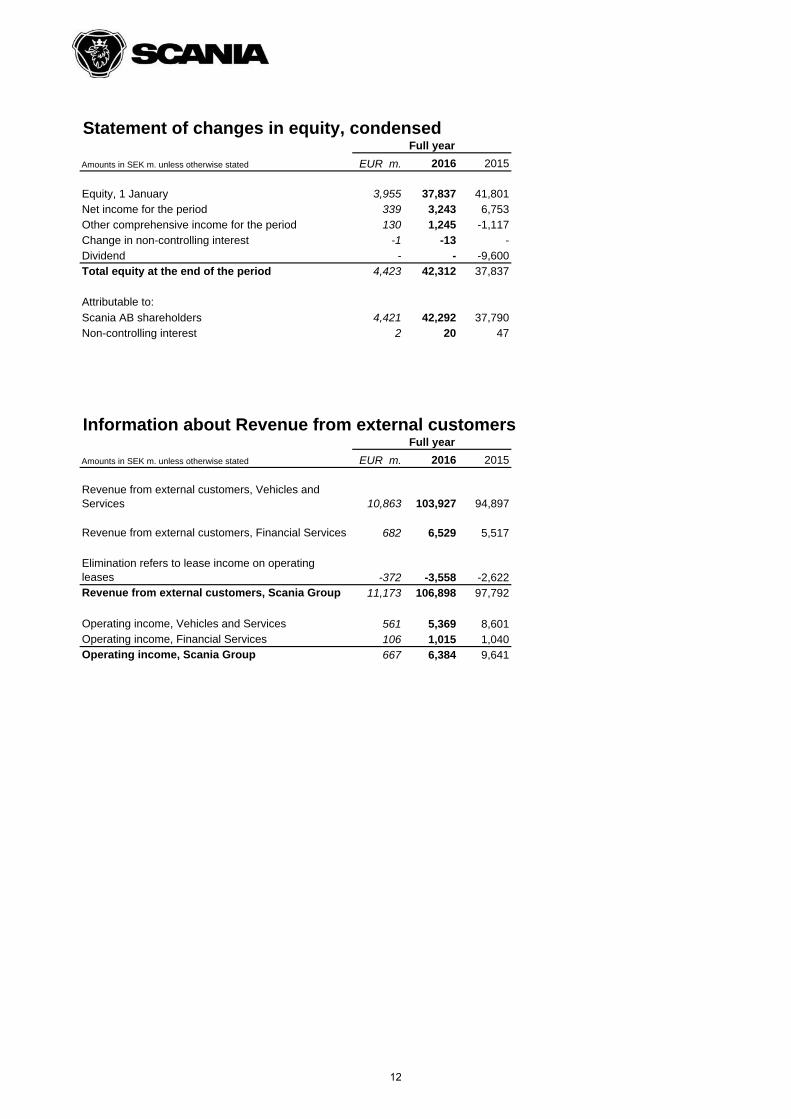

Statement of changes in equity, condensed

Amounts in SEK m. unless otherwise stated EUR m. 2016 2015

Equity, 1 January 3,955 37,837 41,801Net income for the period 339 3,243 6,753Other comprehensive income for the period 130 1,245 -1,117Change in non-controlling interest -1 -13 -Dividend - - -9,600Total equity at the end of the period 4,423 42,312 37,837

Attributable to:

Scania AB shareholders 4,421 42,292 37,790Non-controlling interest 2 20 47

Information about Revenue from external customers

Amounts in SEK m. unless otherwise stated EUR m. 2016 2015

Revenue from external customers, Vehicles and Services 10,863 103,927 94,897

Revenue from external customers, Financial Services 682 6,529 5,517

Elimination refers to lease income on operating leases -372 -3,558 -2,622Revenue from external customers, Scania Group 11,173 106,898 97,792

Operating income, Vehicles and Services 561 5,369 8,601Operating income, Financial Services 106 1,015 1,040Operating income, Scania Group 667 6,384 9,641

Full year

Full year

12

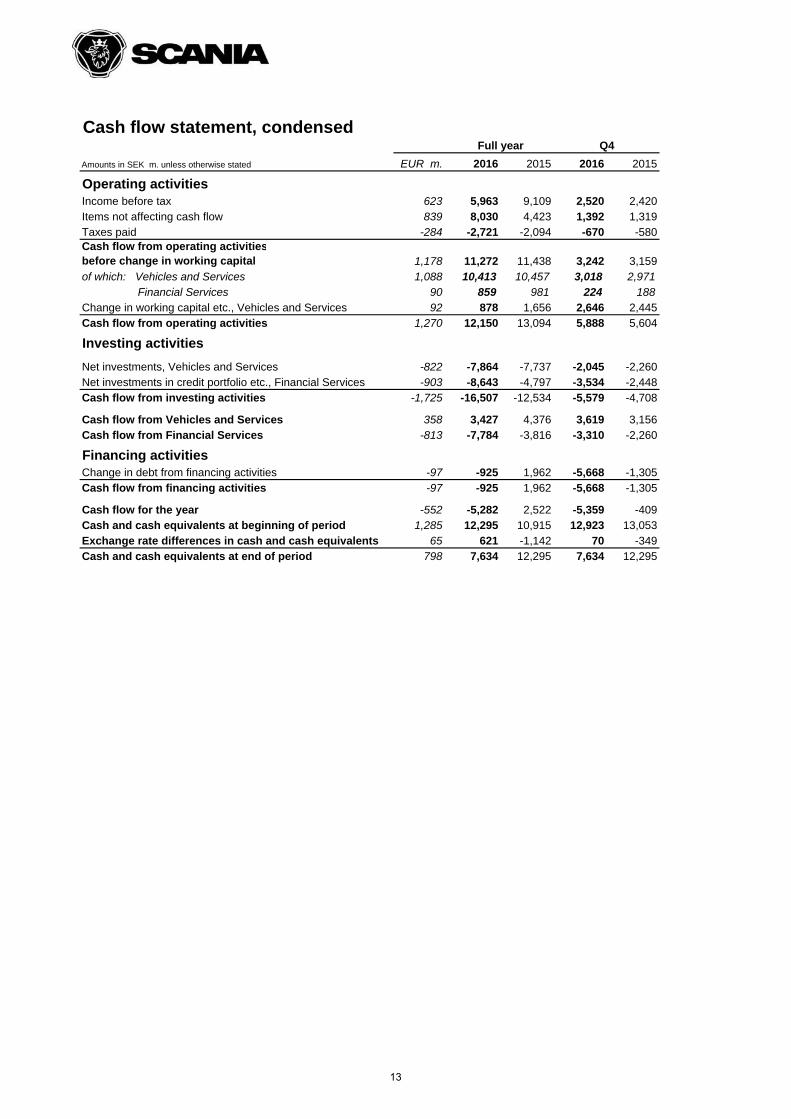

Cash flow statement, condensed

EUR m. 2016 2015 2016 2015

Operating activitiesIncome before tax 623 5,963 9,109 2,520 2,420Items not affecting cash flow 839 8,030 4,423 1,392 1,319Taxes paid -284 -2,721 -2,094 -670 -580Cash flow from operating activitiesbefore change in working capital 1,178 11,272 11,438 3,242 3,159of which: Vehicles and Services 1,088 10,413 10,457 3,018 2,971 Financial Services 90 859 981 224 188Change in working capital etc., Vehicles and Services 92 878 1,656 2,646 2,445Cash flow from operating activities 1,270 12,150 13,094 5,888 5,604

Investing activities

Net investments, Vehicles and Services -822 -7,864 -7,737 -2,045 -2,260Net investments in credit portfolio etc., Financial Services -903 -8,643 -4,797 -3,534 -2,448Cash flow from investing activities -1,725 -16,507 -12,534 -5,579 -4,708

Cash flow from Vehicles and Services 358 3,427 4,376 3,619 3,156Cash flow from Financial Services -813 -7,784 -3,816 -3,310 -2,260

Financing activitiesChange in debt from financing activities -97 -925 1,962 -5,668 -1,305Cash flow from financing activities -97 -925 1,962 -5,668 -1,305

Cash flow for the year -552 -5,282 2,522 -5,359 -409Cash and cash equivalents at beginning of period 1,285 12,295 10,915 12,923 13,053Exchange rate differences in cash and cash equivalents 65 621 -1,142 70 -349Cash and cash equivalents at end of period 798 7,634 12,295 7,634 12,295

Amounts in SEK m. unless otherwise stated

Full year Q4

13

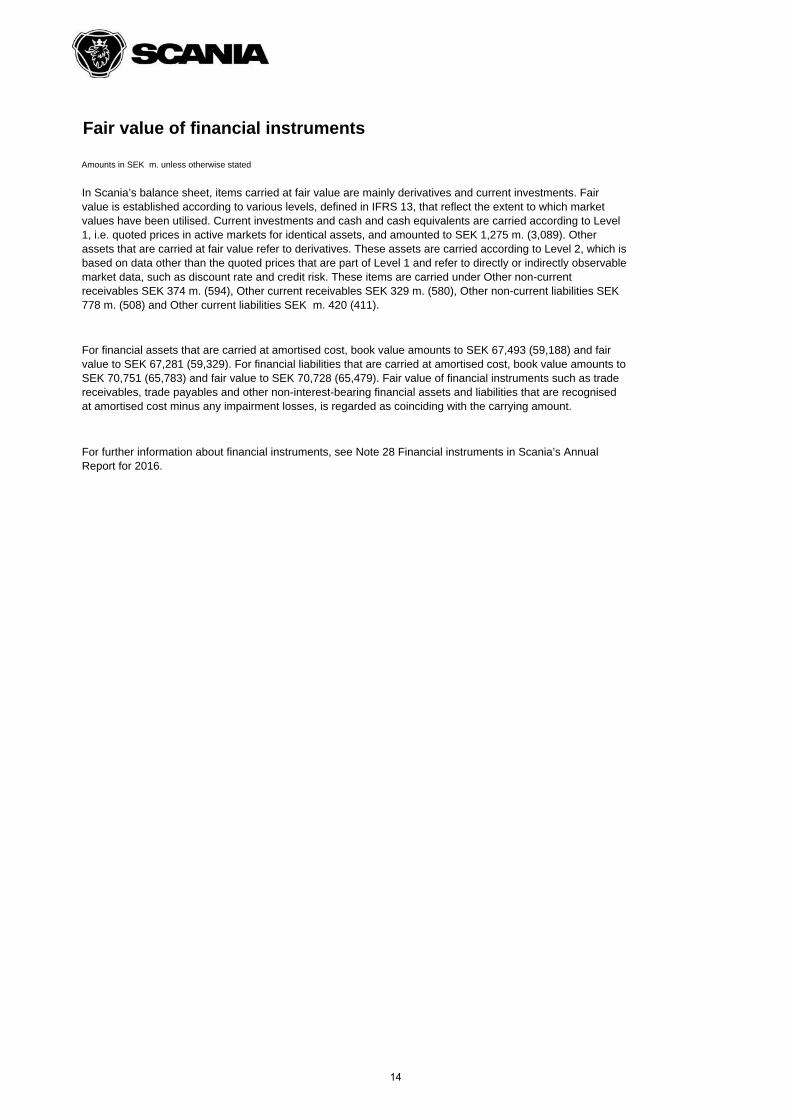

Fair value of financial instruments

Amounts in SEK m. unless otherwise stated

For further information about financial instruments, see Note 28 Financial instruments in Scania’s Annual Report for 2016.

In Scania’s balance sheet, items carried at fair value are mainly derivatives and current investments. Fair value is established according to various levels, defined in IFRS 13, that reflect the extent to which market values have been utilised. Current investments and cash and cash equivalents are carried according to Level 1, i.e. quoted prices in active markets for identical assets, and amounted to SEK 1,275 m. (3,089). Other assets that are carried at fair value refer to derivatives. These assets are carried according to Level 2, which is based on data other than the quoted prices that are part of Level 1 and refer to directly or indirectly observable market data, such as discount rate and credit risk. These items are carried under Other non-current receivables SEK 374 m. (594), Other current receivables SEK 329 m. (580), Other non-current liabilities SEK 778 m. (508) and Other current liabilities SEK m. 420 (411).

For financial assets that are carried at amortised cost, book value amounts to SEK 67,493 (59,188) and fair value to SEK 67,281 (59,329). For financial liabilities that are carried at amortised cost, book value amounts to SEK 70,751 (65,783) and fair value to SEK 70,728 (65,479). Fair value of financial instruments such as trade receivables, trade payables and other non-interest-bearing financial assets and liabilities that are recognised at amortised cost minus any impairment losses, is regarded as coinciding with the carrying amount.

14

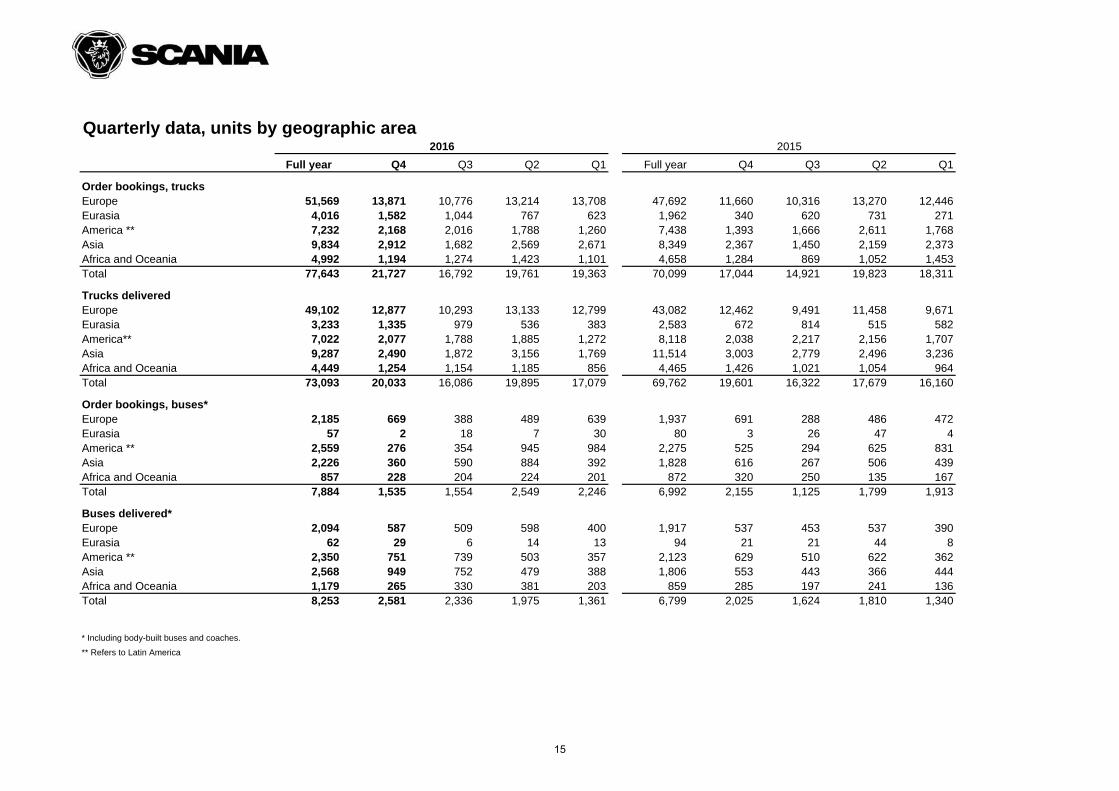

Quarterly data, units by geographic area

Full year Q4 Q3 Q2 Q1 Full year Q4 Q3 Q2 Q1

Order bookings, trucksEurope 51,569 13,871 10,776 13,214 13,708 47,692 11,660 10,316 13,270 12,446Eurasia 4,016 1,582 1,044 767 623 1,962 340 620 731 271America ** 7,232 2,168 2,016 1,788 1,260 7,438 1,393 1,666 2,611 1,768Asia 9,834 2,912 1,682 2,569 2,671 8,349 2,367 1,450 2,159 2,373Africa and Oceania 4,992 1,194 1,274 1,423 1,101 4,658 1,284 869 1,052 1,453Total 77,643 21,727 16,792 19,761 19,363 70,099 17,044 14,921 19,823 18,311

Trucks deliveredEurope 49,102 12,877 10,293 13,133 12,799 43,082 12,462 9,491 11,458 9,671Eurasia 3,233 1,335 979 536 383 2,583 672 814 515 582America** 7,022 2,077 1,788 1,885 1,272 8,118 2,038 2,217 2,156 1,707Asia 9,287 2,490 1,872 3,156 1,769 11,514 3,003 2,779 2,496 3,236Africa and Oceania 4,449 1,254 1,154 1,185 856 4,465 1,426 1,021 1,054 964Total 73,093 20,033 16,086 19,895 17,079 69,762 19,601 16,322 17,679 16,160

Order bookings, buses*Europe 2,185 669 388 489 639 1,937 691 288 486 472Eurasia 57 2 18 7 30 80 3 26 47 4America ** 2,559 276 354 945 984 2,275 525 294 625 831Asia 2,226 360 590 884 392 1,828 616 267 506 439Africa and Oceania 857 228 204 224 201 872 320 250 135 167Total 7,884 1,535 1,554 2,549 2,246 6,992 2,155 1,125 1,799 1,913

Buses delivered*Europe 2,094 587 509 598 400 1,917 537 453 537 390Eurasia 62 29 6 14 13 94 21 21 44 8America ** 2,350 751 739 503 357 2,123 629 510 622 362Asia 2,568 949 752 479 388 1,806 553 443 366 444Africa and Oceania 1,179 265 330 381 203 859 285 197 241 136Total 8,253 2,581 2,336 1,975 1,361 6,799 2,025 1,624 1,810 1,340

* Including body-built buses and coaches.

** Refers to Latin America

20152016

15

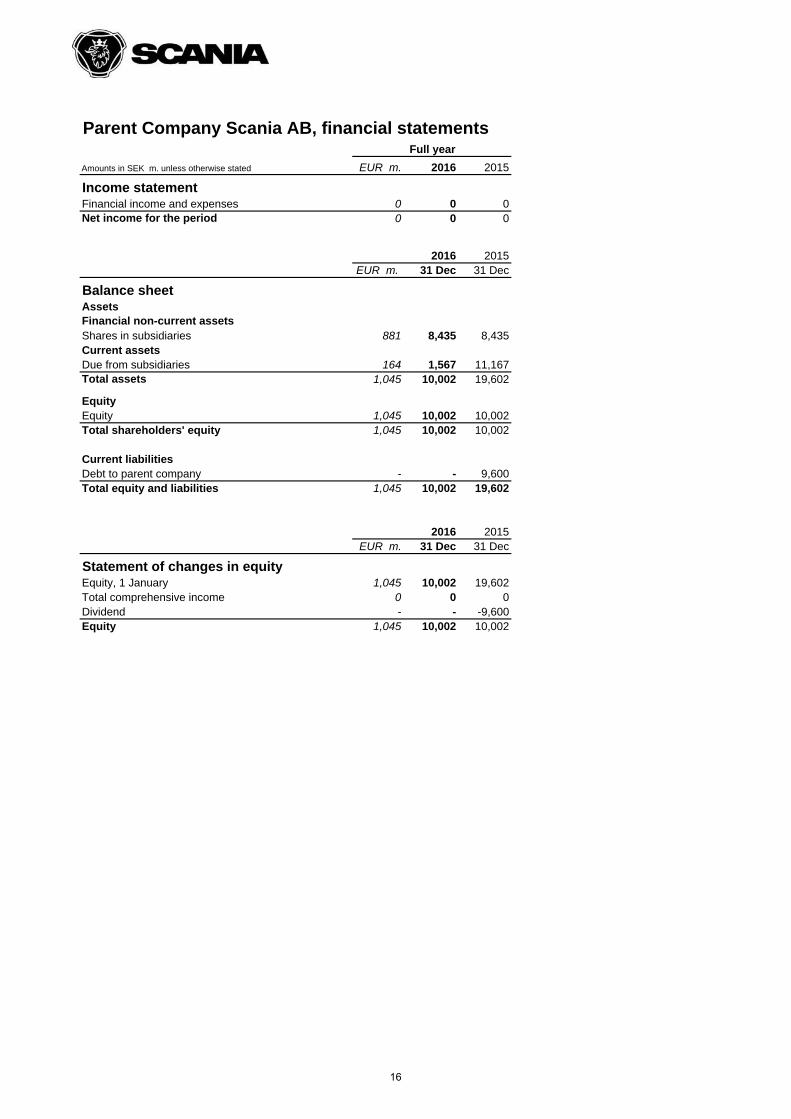

Parent Company Scania AB, financial statements

EUR m. 2016 2015

Income statementFinancial income and expenses 0 0 0Net income for the period 0 0 0

2016 2015EUR m. 31 Dec 31 Dec

Balance sheetAssetsFinancial non-current assetsShares in subsidiaries 881 8,435 8,435Current assetsDue from subsidiaries 164 1,567 11,167Total assets 1,045 10,002 19,602

EquityEquity 1,045 10,002 10,002Total shareholders' equity 1,045 10,002 10,002

Current liabilitiesDebt to parent company - - 9,600Total equity and liabilities 1,045 10,002 19,602

2016 2015EUR m. 31 Dec 31 Dec

Statement of changes in equityEquity, 1 January 1,045 10,002 19,602Total comprehensive income 0 0 0Dividend - - -9,600Equity 1,045 10,002 10,002

Amounts in SEK m. unless otherwise stated

Full year

16

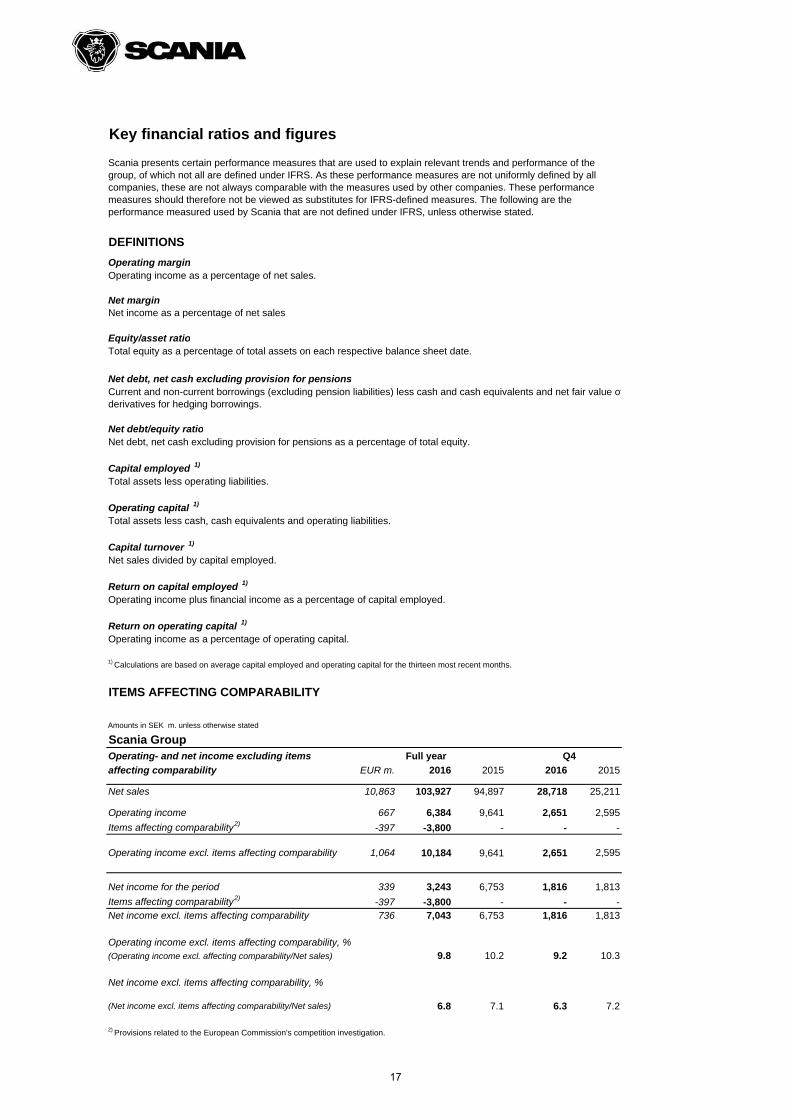

Key financial ratios and figures

DEFINITIONS

Operating margin

Net marginNet income as a percentage of net sales.

Equity/asset ratio

Net debt/equity ratio

Capital employed 1)

Operating capital 1)

Capital turnover 1)

Return on capital employed 1)

Return on operating capital 1)

ITEMS AFFECTING COMPARABILITY

Amounts in SEK m. unless otherwise stated

Scania GroupOperating- and net income excluding items

affecting comparability EUR m. 2016 2015 2016 2015

Net sales 10,863 103,927 94,897 28,718 25,211

Operating income 667 6,384 9,641 2,651 2,595

Items affecting comparability2) -397 -3,800 - - -

Operating income excl. items affecting comparability 1,064 10,184 9,641 2,651 2,595

Net income for the period 339 3,243 6,753 1,816 1,813

Items affecting comparability2) -397 -3,800 - - -Net income excl. items affecting comparability 736 7,043 6,753 1,816 1,813

Operating income excl. items affecting comparability, %(Operating income excl. affecting comparability/Net sales) 9.8 10.2 9.2 10.3

Net income excl. items affecting comparability, %

(Net income excl. items affecting comparability/Net sales) 6.8 7.1 6.3 7.2

2) Provisions related to the European Commission's competition investigation.

Q4

Scania presents certain performance measures that are used to explain relevant trends and performance of the group, of which not all are defined under IFRS. As these performance measures are not uniformly defined by all companies, these are not always comparable with the measures used by other companies. These performance measures should therefore not be viewed as substitutes for IFRS-defined measures. The following are the performance measured used by Scania that are not defined under IFRS, unless otherwise stated.

Operating income as a percentage of net sales.

Total equity as a percentage of total assets on each respective balance sheet date.

Current and non-current borrowings (excluding pension liabilities) less cash and cash equivalents and net fair value ofderivatives for hedging borrowings.

Net debt, net cash excluding provision for pensions as a percentage of total equity.

Total assets less operating liabilities.

Total assets less cash, cash equivalents and operating liabilities.

Net sales divided by capital employed.

Operating income plus financial income as a percentage of capital employed.

Operating income as a percentage of operating capital.

Net debt, net cash excluding provision for pensions

1) Calculations are based on average capital employed and operating capital for the thirteen most recent months.

Full year

17

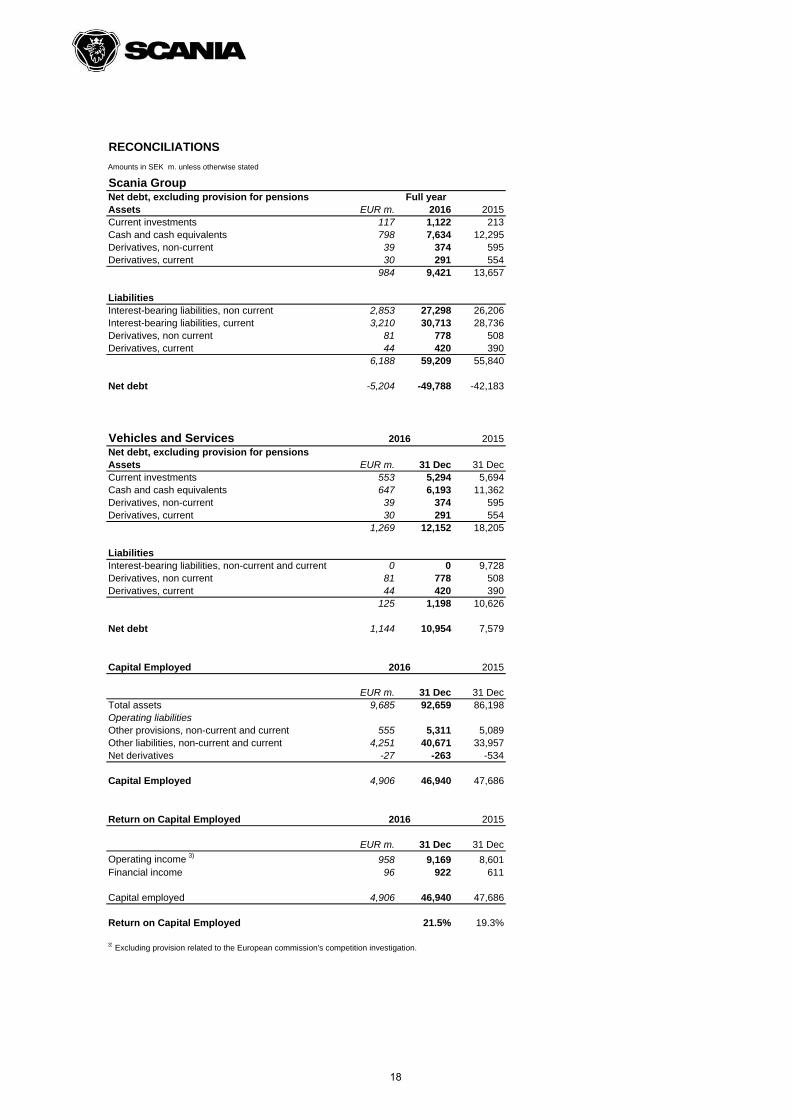

RECONCILIATIONS

Amounts in SEK m. unless otherwise stated

Scania GroupNet debt, excluding provision for pensionsAssets EUR m. 2016 2015Current investments 117 1,122 213Cash and cash equivalents 798 7,634 12,295Derivatives, non-current 39 374 595Derivatives, current 30 291 554

984 9,421 13,657

LiabilitiesInterest-bearing liabilities, non current 2,853 27,298 26,206Interest-bearing liabilities, current 3,210 30,713 28,736Derivatives, non current 81 778 508Derivatives, current 44 420 390

6,188 59,209 55,840

Net debt -5,204 -49,788 -42,183

Vehicles and Services 2015Net debt, excluding provision for pensionsAssets EUR m. 31 Dec 31 DecCurrent investments 553 5,294 5,694Cash and cash equivalents 647 6,193 11,362Derivatives, non-current 39 374 595Derivatives, current 30 291 554

1,269 12,152 18,205

LiabilitiesInterest-bearing liabilities, non-current and current 0 0 9,728Derivatives, non current 81 778 508Derivatives, current 44 420 390

125 1,198 10,626

Net debt 1,144 10,954 7,579

Capital Employed 2015

EUR m. 31 Dec 31 DecTotal assets 9,685 92,659 86,198Operating liabilitiesOther provisions, non-current and current 555 5,311 5,089Other liabilities, non-current and current 4,251 40,671 33,957Net derivatives -27 -263 -534

Capital Employed 4,906 46,940 47,686

Return on Capital Employed 2015

EUR m. 31 Dec 31 Dec

Operating income 3) 958 9,169 8,601Financial income 96 922 611

Capital employed 4,906 46,940 47,686

Return on Capital Employed 21.5% 19.3%

3) Excluding provision related to the European commission's competition investigation.

Full year

2016

2016

2016

18