Embed Size (px)

Citation preview

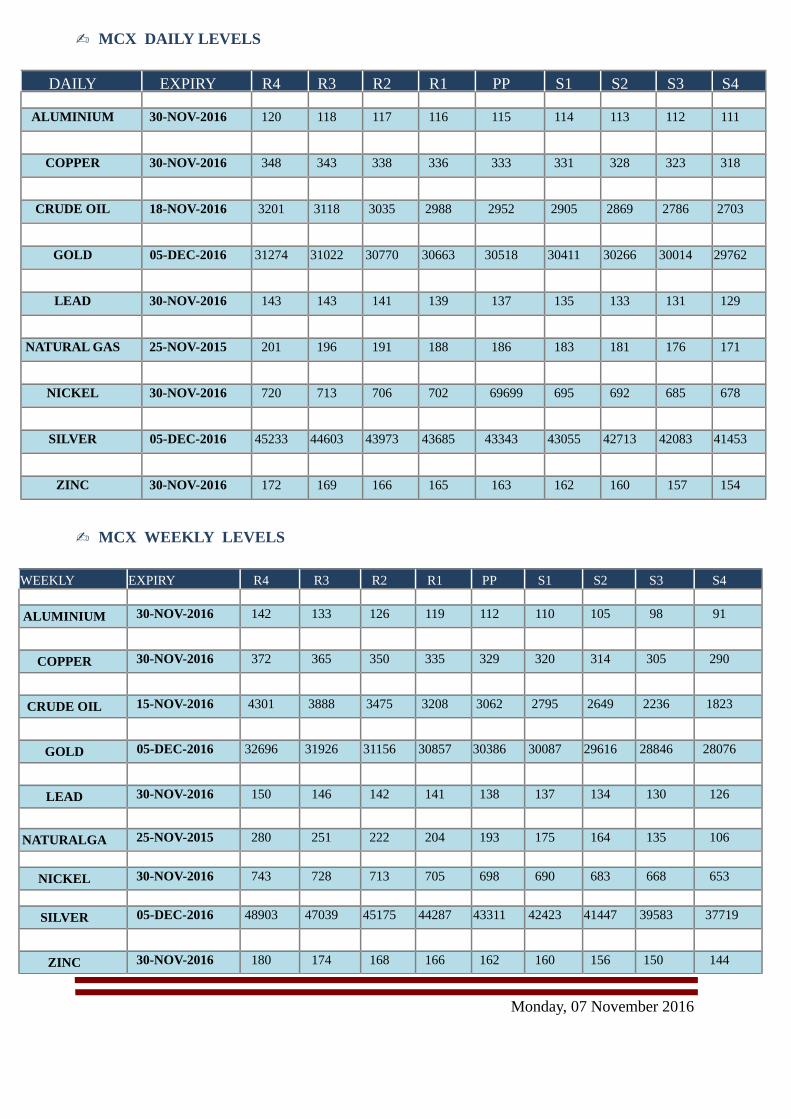

MCX DAILY LEVELS ✍

DAILY EXPIRY R4 R3 R2 R1 PP S1 S2 S3 S4

ALUMINIUM 30-NOV-2016 120 118 117 116 115 114 113 112 111

COPPER 30-NOV-2016 348 343 338 336 333 331 328 323 318

CRUDE OIL 18-NOV-2016 3201 3118 3035 2988 2952 2905 2869 2786 2703

GOLD 05-DEC-2016 31274 31022 30770 30663 30518 30411 30266 30014 29762

LEAD 30-NOV-2016 143 143 141 139 137 135 133 131 129

NATURAL GAS 25-NOV-2015 201 196 191 188 186 183 181 176 171

NICKEL 30-NOV-2016 720 713 706 702 69699 695 692 685 678

SILVER 05-DEC-2016 45233 44603 43973 43685 43343 43055 42713 42083 41453

ZINC 30-NOV-2016 172 169 166 165 163 162 160 157 154

MCX WEEKLY LEVELS ✍

WEEKLY EXPIRY R4 R3 R2 R1 PP S1 S2 S3 S4

ALUMINIUM 30-NOV-2016 142 133 126 119 112 110 105 98 91

COPPER 30-NOV-2016 372 365 350 335 329 320 314 305 290

CRUDE OIL 15-NOV-2016 4301 3888 3475 3208 3062 2795 2649 2236 1823

GOLD 05-DEC-2016 32696 31926 31156 30857 30386 30087 29616 28846 28076

LEAD 30-NOV-2016 150 146 142 141 138 137 134 130 126

NATURALGAS

25-NOV-2015 280 251 222 204 193 175 164 135 106

NICKEL 30-NOV-2016 743 728 713 705 698 690 683 668 653

SILVER 05-DEC-2016 48903 47039 45175 44287 43311 42423 41447 39583 37719

ZINC 30-NOV-2016 180 174 168 166 162 160 156 150 144

Monday, 07 November 2016

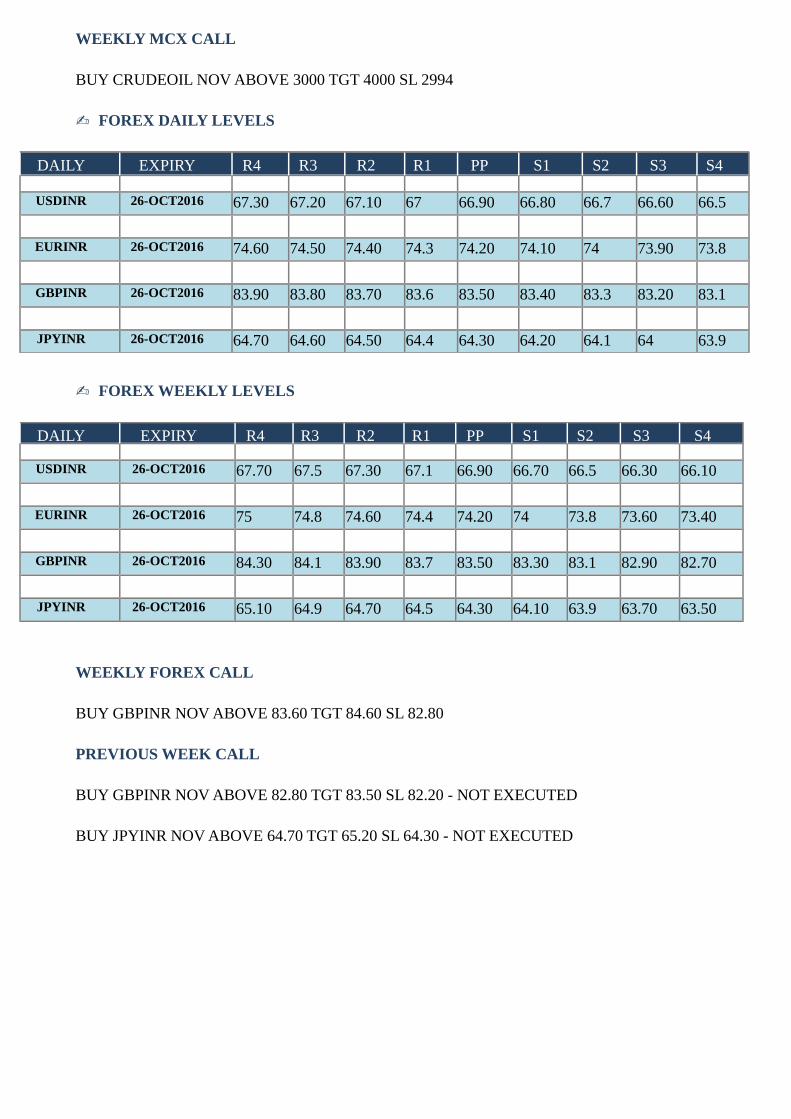

WEEKLY MCX CALL

BUY CRUDEOIL NOV ABOVE 3000 TGT 4000 SL 2994

FOREX DAILY LEVELS ✍

DAILY EXPIRY

DATE

R4 R3 R2 R1 PP S1 S2 S3 S4

USDINR 26-OCT2016 67.30 67.20 67.10 67 66.90 66.80 66.70

66.60 66.50

EURINR 26-OCT2016 74.60 74.50 74.40 74.30

74.20 74.10 74 73.90 73.80

GBPINR 26-OCT2016 83.90 83.80 83.70 83.60

83.50 83.40 83.30

83.20 83.10

JPYINR 26-OCT2016 64.70 64.60 64.50 64.40

64.30 64.20 64.10

64 63.90

FOREX WEEKLY LEVELS✍

DAILY EXPIRY R4 R3 R2 R1 PP S1 S2 S3 S4

USDINR 26-OCT2016 67.70 67.50

67.30 67.10

66.90 66.70 66.50

66.30 66.10

EURINR 26-OCT2016 75 74.80

74.60 74.40

74.20 74 73.80

73.60 73.40

GBPINR 26-OCT2016 84.30 84.10

83.90 83.70

83.50 83.30 83.10

82.90 82.70

JPYINR 26-OCT2016 65.10 64.90

64.70 64.50

64.30 64.10 63.90

63.70 63.50

WEEKLY FOREX CALL

BUY GBPINR NOV ABOVE 83.60 TGT 84.60 SL 82.80

PREVIOUS WEEK CALL

BUY GBPINR NOV ABOVE 82.80 TGT 83.50 SL 82.20 - NOT EXECUTED

BUY JPYINR NOV ABOVE 64.70 TGT 65.20 SL 64.30 - NOT EXECUTED

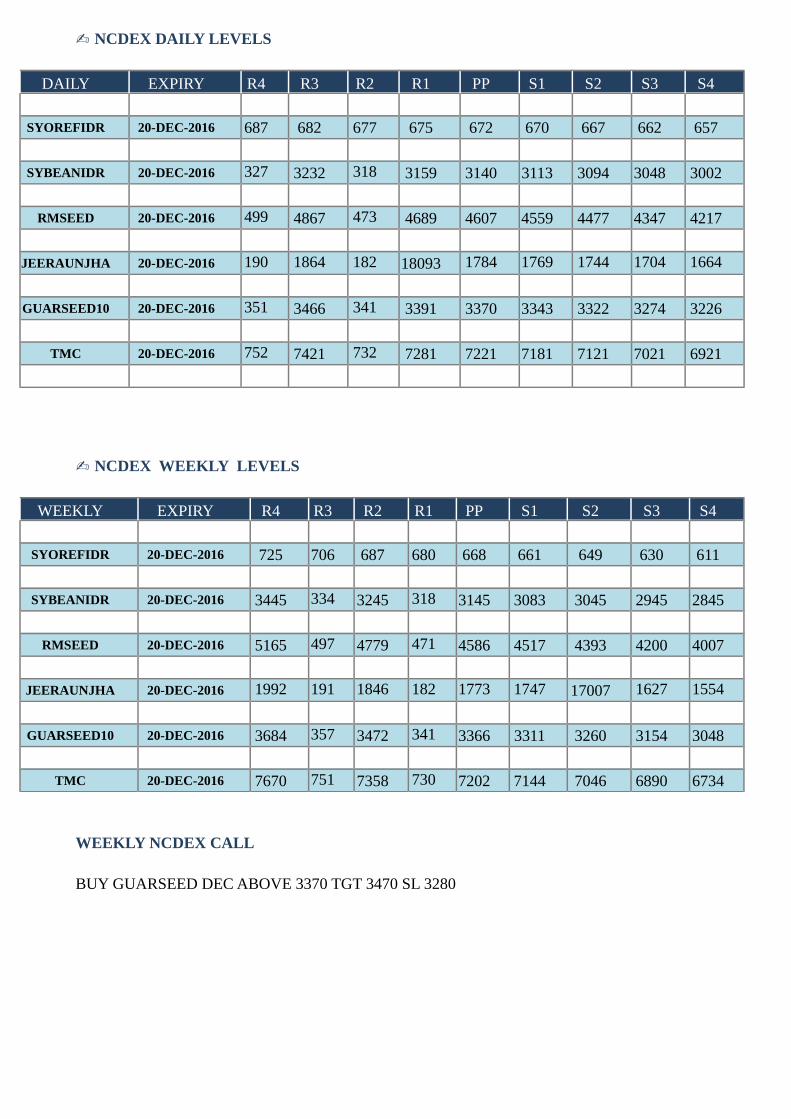

NCDEX DAILY LEVELS✍

DAILY EXPIRY

DATE

R4 R3 R2 R1 PP S1 S2 S3 S4

SYOREFIDR 20-DEC-2016 687 682 677 675 672 670 667 662 657

SYBEANIDR 20-DEC-2016 3278

3232 3186

3159 3140 3113 3094 3048 3002

RMSEED 20-DEC-2016 4997

4867 4737

4689 4607 4559 4477 4347 4217

JEERAUNJHA 20-DEC-2016 19047

18647

18247

18093 17847

17693

17447

17047

16647

GUARSEED10 20-DEC-2016 3514

3466 3418

3391 3370 3343 3322 3274 3226

TMC 20-DEC-2016 7521

7421 7321

7281 7221 7181 7121 7021 6921

NCDEX WEEKLY LEVELS✍

WEEKLY EXPIRY

DATE

R4 R3 R2 R1 PP S1 S2 S3 S4

SYOREFIDR 20-DEC-2016 725 706 687 680 668 661 649 630 611

SYBEANIDR 20-DEC-2016 3445 3345

3245 3183

3145 3083 3045 2945 2845

RMSEED 20-DEC-2016 5165 4972

4779 4710

4586 4517 4393 4200 4007

JEERAUNJHA 20-DEC-2016 19927

19197

18467

18203

17737

17473

17007 16277

15547

GUARSEED10 20-DEC-2016 3684 3578

3472 3417

3366 3311 3260 3154 3048

TMC 20-DEC-2016 7670 7514

7358 7300

7202 7144 7046 6890 6734

WEEKLY NCDEX CALL

BUY GUARSEED DEC ABOVE 3370 TGT 3470 SL 3280

MCX - WEEKLY NEWS LETTERS

✍ BULLION

Gold edged higher on Thursday in response to a lower dollar and also uncertainty about the

outcome of a tight U.S. presidential race. Democrat Hillary Clinton maintained her narrow lead

over Republican rival Donald Trump just days ahead of the Nov. 8 election, according to two

polls released on Thursday. helped the dollar to recover from multi-week lows, although it

remained 0.1 percent lower against a basket of six main currencies. "Risk-off sentiment has

helped gold above $1,300 yesterday ... and as long as uncertainty around the outcome of U.S.

elections continues, we can see support," Saxo Bank head of research Ole Hansen said. Spot gold

XAU= , lower initially, rose 0.2 percent to $1,298.91 an ounce at 1537 GMT. It touched a one-

month high of $1,307.76 in the previous session, before retreating as Federal Reserve signalled it

could raise interest rates next month. The Fed kept rates unchanged on Wednesday, but said the

economy had gathered steam and job gains remained solid. Policymakers also expressed more

optimism that inflation was moving toward their 2 percent target. gold futures GCcv1 fell 1.4

percent to $1,289.30. "The fact that the Fed made some hawkish comments opening up to a rate

increase in December could be seen as a negative for gold," Mitsubishi Corp analyst Jonathan

Butler said. Gold is highly sensitive to rising rates, which lift the opportunity cost of holding

non-yielding assets, while also boosting the dollar, in which the metal is priced. "But the

narrowing of the polls between Clinton and Trump is more important in terms of gold's

positioning this week. We could see more gains before Tuesday, as the dollar retreats and safe

havens such us the Japanese yen or the Swiss franc increase." The market will now focus on non-

farm payrolls data, which will be released on Friday. FRX/ are expected to have added 175,000

jobs in October, according to the median estimate of 106 economists polled by Reuters. "Even

bad data won't change the idea of a rate hike as the Fed has shown that there is a high probability

for a rate hike in December," Jiang Shu of Shandong Gold Group said. Among other precious

metals, silver XAG= fell 1.1 percent to $18.23, retreating from a high of about $18.73 on

Wednesday, its best level since Oct. 4. Platinum XPT= was up 0.6 percent at $991.40 and

palladium XPD= dropped 0.8 percent to $623.25.

✍ ENERGY

Oil prices edged up in early trading on Friday, stabilising after five straight days of falls triggered

by a surge in U.S. crude inventories and doubts over the ability of oil producers to coordinate an

output cuts. International Brent crude oil futures LCOc1 were trading at $46.50 per barrel at

0036 GMT, up 15 cents, or 0.3 percent, from their last close. U.S. West Texas Intermediate

futures were at $44.83, up 17 cents, or 0.4 percent. Despite the slight increases, traders said

market sentiment was bearish. Brent futures fell for the past five straight trading sessions and is

down about 13.5 percent since its most recent peak in mid-October. Analysts said markets were

also weighed down by traders pulling out money from crude futures ahead of the upcoming U.S.

presidential elections, which are seen as a risk to global markets. "I suspect the main drivers are

that risk is being taken off the table ahead of next week's election and the continuance of long

liquidation," said Jeffrey Halley, senior market analyst at OANDA brokerage in Singapore.

Beyond concerns ahead of the U.S. elections, traders said oil market fundamentals were also

weak, with U.S. crude stocks surging, demand growth low, and doubts that the Organization of

the Petroleum Exporting Countries and non-OPEC producer Russia can agree on a meaningful

output cut later this month."Crude oil continued to sell off with new data raising concerns of an

expanding surplus... Investors also continued to fret about OPEC failing to reach an agreement

on production cuts," ANZ bank said on Friday.

U.S. crude oil stockpiles soared more than 14 million barrels last week, the largest weekly build

since the U.S. Energy Department started keeping records in 1982, highlighting that a global fuel

supply overhang is far from over. oil production remains near records and inventories are high,

British bank Barclays said demand growth was timid. "Q3 16 demand growth rate is less than

one-third that of the same quarter last year," Barclays bank said in a note to clients, estimating

last quarter's growth below 1 million barrels per day (bpd). It said consumption increases for the

last quarter of the year would not be much higher, before averaging 1.3 million bpd in 2017.

Oil prices settled down more than 1 percent on Thursday as investors reeled from a record

weekly surge in U.S. crude inventories, and remained skeptical about whether OPEC can

actually implement its planned output cap.U.S. crude CLc1 fell 68 cents, or 1.5 percent, to settle

at $44.66 per barrel. At one point, oil had fallen more than $1 a barrel and hit a session low of

$44.37. Brent crude LCOc1 was down 51 cents, or 1.1 percent, at $46.35 a barrel. It hit a session

low of 45.99.Traders said energy monitoring service Genscape reported a weekly build of 1.2

million barrels at the U.S. delivery base in Cushing, Oklahoma. That kept a lid on oil prices a

day after crude fell to a five-week low, when U.S. data on Wednesday showed stockpiles of oil

surged a record 14 million barrels last week. Thursday, prices were also pressured as U.S.

equities fell, with the S&P 500 stock index headed for its longest losing streak since the 2008

financial crisis. Oil ministers from the Organization of the Petroleum Exporting Countries

(OPEC) meet on Nov. 30 in Vienna to agree on a production cap to reduce a global glut and

combat low prices.Market watchers have grown skeptical that a concrete deal can be reached or

enforced. OPEC has not made clear how much each member should cut, and several have been

resistant. A Reuters survey this week based on shipping data and industry sources indicated that

OPEC output probably set a record high in October. got this rally a few weeks ago, recent weeks

on the expectation that we'll see some cohesive cut coming through from OPEC, but that's been

slowly unwound," said Matt Smith, director of commodity research at energy data provider

ClipperData. News of an attack on a Nigerian pipeline, which sources say cut output by at least

200,000 barrels, lent some support to crude prices. Nigeria, Africa's largest crude producer, has

been hamstrung in months by rebel activity. prices have been falling for four days and have not

recovered to levels reached in October after the preliminary agreement by OPEC to cap

production, reached at a meeting in Algiers. "If there were broadly three drivers propelling oil

prices from about $45 per barrel ahead of Algiers to $53 - OPEC expectations, inventories and a

more or less benign macro environment - they suddenly seem spent," Credit Suisse analysts said

in a note.

✍ BASE METAL

Copper futures traded a shade lower at Rs 328.20 per kg as speculators trimmed positions,

tracking a weak trend overseas and muted spot demand. At the Multi Commodity Exchange,

copper for delivery in current month declined by 15 paise or 0.05 per cent to Rs 328.20 per kg in

business turnover of 854 lots. Similarly, the metal for delivery in February contracts shed 15

paise or 0.04 per cent to Rs 333.65 per kg in 4 lots. Analysts attributed the fall in copper futures

to weak trend in global markets where copper weakened and fall in demand at the domestic spot

markets here. Meanwhile, Copper for delivery in three month fell 0.4 per cent at the London

Metal Exchange.

Nickel prices went up 0.96 per cent to Rs 703 per kg in futures trade as speculators raised their

bets, driven by rising demand at the domestic spot markets amid a firming trend in base metals at

the London Metal Exchange. In futures trading at the Multi Commodity Exchange, nickel for

delivery in November spurted Rs 6.70, or 0.96 per cent, to Rs 703 per kg, in a business turnover

of 898 lots. The metal for delivery in December was trading higher by Rs 6.70, or 0.95 per cent,

to Rs 708.50 per kg in 11 lots. Analysts said the rise in nickel prices at futures trade was mostly

attributed to strong demand from alloy makers at the domestic spot markets coupled with a

strength in base metals at the London Metal Exchange (LME) after China's economy stabilised in

the third quarter, to bolster the outlook for commodities demand. Nickel prices went up by 0.56

per cent to Rs 694.80 per kg in futures trade as speculators raised their bets, driven by a firming

trend at the domestic spot markets on pick-up in demand. In futures trading at the Multi

Commodity Exchange, nickel for delivery in current month spurted Rs 3.90, or 0.56 per cent, to

Rs 694.80 per kg, in a business turnover of 985 lots. The metal for delivery in December was

trading higher by Rs 3.40, or 0.49 per cent, to Rs 700 per kg in 22 lots. Analysts said a firming

trend at the domestic spot markets following increased demand from alloy-makers mainly

pushed up nickel prices at futures trade here.

Aluminium prices edged lower by 0.39 per cent to Rs 115.50 in futures trade as speculators

booked profits at prevailing levels. At the Multi Commodity Exchange, aluminium for delivery

in November eased by 45 paise, or 0.39 per cent to Rs 115.50 per kg in a business turnover of

704 lots. Similarly, the metal for delivery in December shed 25 paise, or 0.21 per cent to Rs

116.05 per kg in 6 lots. Market analysts said besides profit-booking by participants, fall in

demand from consuming industries in the spot market, mainly influenced aluminium prices at

futures trade. At the Multi Commodity Exchange, zinc for delivery in December was trading

higher by Rs 1.05, or 0.64 per cent, to Rs 165.50 per kg, in a business turnover of 59 lots. The

metal for delivery in November rose Re one, or 0.61 per cent, to trade at Rs 164.90 per kg in

1,009 lots. Globally, zinc for delivery in three months rose 2.6 per cent to settle at USD 2,458 per

tonne at the London Metal Exchange yesterday, after touching USD 2,479.50, the highest since

August 2011. Market analysts attributed the rise in zinc futures to fresh bets created by

participants on the back of rising demand at the domestic spot market and metal climbing to over

five-year highs at the LME with investors betting that a rebound in demand from China will

underpin prices.

NCDEX - WEEKLY MARKET REVIEW

Heavy rain forecast for AP, Odisha coasts as depression lingers in Vicinity The depression in the

west-central Bay of Bengal lay 240 km south-east of Visakhapatnam and 520 km south-

southwest of Paradip on Friday evening. It was 880 km south-southwest of Khepupara in

Bangladesh, where it is headed for landfall as a deep depression, a stepdown from a tropical

cyclone forecast earlier. The intensification may happen after it recurves away to the North-East

from the Andhra Pradesh coast, skirting both the Odisha and Bengal coasts, according to the Met

Department. The proximity to the East Coast should bring light to moderate, at times heavy, rain

to the coastal areas of these three States until Sunday, the Met said. The US Joint Typhoon

Warning Centre , too, has officially cancelled its outlook for any further strengthening of the

depression. It is noted that the system is encountering increasing wind shear as it prepares to

recurve to the North-East. Wind shear refers to the sudden change in wind speed and direction

with height.

Rabi sowing 8.3% lower on drop in acreage of pulses, coarse cereals Sowing of key rabi crops

(winter crops), such as wheat, mustard and gram, has begun in major producing States.

According to the Agriculture Ministry, sowing has taken place so far on about 81.55 lakh ha,

which is about 8.3 per cent lower than the corresponding period last year. Rabi planting generally

starts in early October and goes on till late January. The decline in acreage so far is largely

because of a drop in the area under pulses and coarse cereals. However, sowing is expected to

accelerate as the season advances. The acreage under wheat — the main rabi cereal — as on

November 4 stood at 4.28 lakh hectares, higher than the 2.76 lakh hectares sown during the same

period last year. Planting of rice stood at 9.51 lakh ha (6.25 lakh ha). The acreage under oilseeds

was highest at 29.79 lakh ha (19.91 lakh ha). Mustard is the main oilseed crop grown during the

rabi season, while chana or gram is the main pulses crop. Sowing of pulses was down at 24.16

lakh ha (30.07 lakh ha). Coarse cereal acreage declined to 13.84 lakh ha (29.92 lakh ha). A near

normal South-West monsoon this year after two consecutive droughts has led to improved soil

moisture levels and comfortable water storage levels across major parts of the country, which

should aid the rabi planting. Delayed crushing in western States pulls down Oct sugar production

Sugar production in the country in October 2016 -- the first month of the ongoing sugar season --

dropped sharply by 44 per cent to 1.04 lakh tonnes compared to the same month last year as

Maharashtra and Gujarat delayed production. v“In all, 28 mills have started crushing as on

October 31 2016, as against 65 in 2015-16 sugar season same time,” according to industry body

Indian Sugar Mills Association. During 2016-17, Maharashtra mills delayed their crushing

operations to get the cane matured further to get better sugar recovery from standing cane,

according to an official release. “These mills are now expected to start crushing from November

5, 2016. Similarly, Gujarat mills are expected to start this week,” the release added. With the

carryover stock of 77 lakh tonnes as on October 1 2016 and estimated sugar production of 234

lakh tonnes, total sugar available in the country during 2016-17 sugar season would be around

311 lakh tonnes against the estimated consumption of 255 lakh tonnes, according to ISMA

estimates.

✍ Sugar

Sugar Futures closed down last week due to subdued physical demand and expectation of

sufficient supplies in the country. However, the price recovered on Friday on reports of lower

sugar production in October compared to last year. The most-active December sugar contract

closed 0.44% higher on Friday to settle at 3,441 per quintal. Sugar production in the country in

October 2016 -- the first month of the ongoing sugar season -- dropped sharply by 44 per cent to

1.04 lakh tonnes compared to the same month last year as Maharashtra and Gujarat delayed

production As per ISMA’s first media release, during 2016-17 SS, Maharashtra mills delayed

their starting so as to get the cane matured further to get better sugar recovery from standing

cane. These mills are now expected to start crushing from 5th November, 2016. Similarly,

Gujarat mills are expected to start this week. The carryover stock as on 1st October is pegged at

77 lt and production is estimated at 234 lt in 2016-17 SS. Thus, total sugar available in the

country during 2016-17 SS would be around 311 lt, against the estimated consumption of 255 lt.

Moreover, government is looking to enhance domestic supplies by reduce import duty if the

prices domestic market increase. Central government is exploring the option of lowering the 40%

import duty on the sweetener in its raw form. Due to droughts, sugar production in Maharashtra

is likely to drop nearly 40 percent to 5 million tonnes in the 2016/17 season started on Oct. 1

compared with a year earlier.

✍ Soybean

Soybean futures closed lower last week due to higher arrivals of soybean in the physical markets.

The prices have dropped below the MSP in States of MP and Gujarat. The most-active Nov’16

delivery contract closed 1.45% down last week to settle at Rs. 3,069 per quintal. The harvesting

of soybean in full swing and supplies are strong in the physical market. As per SEA recent survey

soybean production in 2016- 17 forecasted at 10.9 mt, up 58% from the last year.

CBOT soybean rose for the second straight session on Friday as investors turned their attention

to export data after a price slide fuelled by big harvest supplies. The USDA’s weekly export sales

report support prices, led by brisk Chinese buying of U.S. soybeans. As per USDA, net sales of

2.5 mt for 2016/2017--a marketing-year high--were up 28% from the previous week and 34%

from the prior 4-week average. U.S. soy harvest was 87% complete as on 30 Oct, ahead of the

five-year average of 85 percent but in line with an average of trade expectations. Soybean traders

are also watching crop prospects in South America and expectations for a big Brazilian harvest

are being reinforced by rapid planting followed by beneficial rainfall.

✍ Mustard Seed

Mustard seed futures gain last week due to increase in demand from the industrial consumer for

crushing as winter sets in. However,reports of good progress of sowing in Rajasthan capped

further rise. The Nov’16 contract ended 2.74% higher last week to settle at Rs.4,650/quintal. As

per agriculture ministry data, all-India acreage of mustard in the ongoing rabi season was nearly

2.73 mln ha as on Nov 04 up 80% from a year ago. The country's production of rapeseed is

expected to increase by 12.5% to 6.3 mt from a year earlier. The rabi sowing in the largest

mustard producing state, Rajasthan has started. According to government data, Rajasthan has

sown 13.7 lakh hectares as on 24th Oct 2016, up by 191.5% higher compared to last year

acreage.As per the latest USDA monthly report, global rapeseed production for 2016/17 is

forecast at 67.6 mt, up from 66.9 mt last month and down 3 % from 2015/16. Larger crops are

expected from Canada, Australia, and the United States offset a slight decrease for Russia.

✍ Refined Soy Oil

Refined soy oil futures closed lower last week due to pressure on domestic soybean and

International edible oil prices. The most active,Ref Soy oil Nov’16 expiry contract closed 0.19%

down to settle at Rs. 667.9 per quintal last week. Though the tariff value of crude soyoil were

raised by $8 per tn to $853 which was the third increase in two month by the government the

domestic prices were traded lower on steady demand and good stocks. Since January 2016, the

base import prices for crude soy oil increase by more than 20% from $720 per tonnes. As per

SEA data, India September crude soyoil import 469,564 tonnes, an increase of 46 % compared to

321,062 tonnes year ago while, India Nov-Sep crude soyoil import 3.96 mt vs 2.58 mt – an

increase of 53% y/y for the current oil year. Earlier, India has cut import taxes on both crude

palm oil and refined edible oils by 5% points to 7.5 and15 % respectively.

✍ Jeera

Jeera futures gain for third consecutive day on Friday to close higher last week due to pickup in

physical demand and lower level buying by the market participants. NCDEX Nov’16 Jeera

closed 1.75% higher last week to close at Rs 17,715 per quintal..The price trend on the chart

looks positive on reports of dwindling physical supplies and slow start to the new season sowing

in Gujaratand Rajasthan. Moreover, pickup in physical demand and expecting dwindling supplies

in the physical market pushed the prices higher. According Department of commerce data, the

exports of Jeera in the first five months (Apr-Aug) of 2016-17 is at 60,907 tonnes, higher by 62%

compared to last year same time. The exports of jeera during August 2016 increase 65% m/m to

9,003 tonnes while there is also increase exports y/y by 65.7%.

✍ Turmeric

Turmeric futures closed higher during the last week and continue its positive trend due to good

demand from the local buyers as well as expectation of demand upcountry buyers as supplies

may dwindle during next month. Turmeric Nov’16 delivery contract on NCDEX closed 1.12%

higher last week to settle at Rs 7,414 per quintal. Currently the supplies are for medium and poor

quality during the restof the season till new crop arrived which may keep the prices sideways to

higher. It is expected that the demand from the industrial buyers will support the prices just

before new season harvesting. On the export front, country exported about 51,147 tonnes of

turmeric during April-August period up by 32% compared last year, as per department of

commerce data. Expectations of increasing production in coming harvesting season and lowering

export demand in recent months are putting pressure on turmeric prices at higher levels.

Turmeric acreage in Telangana and Andhra Pradesh was higher this year as compared last year.

✍ Kapas

Cotton complex prices closed lower last week due to higher arrivals in the physical market

coupled with lower off take from the buyers as prices were at higher levels. Last week, NCDEX

Kapas for Apr’17 closed 0.28% lower while MCX Oct’16 cotton closed 1.50% down%. The

arrivals have begun in Gujarat, Madhya Pradesh and are expected to pick in Haryana where the

ginners have called off their strike. Industry expects the cotton output to surpass 35-36 million

bales this season. Despite less area under cotton, good monsoon expected to rescue the 2016-17

production. industry are estimating 355 lakh bales 170 kg each for the season 2016-17 (Oct-Sep),

as against the government’s first estimate of 321.2 lakh bales. As per CAB, India's cotton output

is seen at 351 lakh bales (1 bale = 170 kg), up 4% from 338 lakh bales a year ago due to good

monsoon and minimum pest infestation. Cotton area is down by 11.6% at 105.6 lh against 116 lh

last year.For the current season, cotton arrivals in the country are pegged at 21 lakh bales as on 2

nd November, 2016. In October, Punjab, Haryana and Rajasthan together account for at 5.82 lakh

bales while Gujarat and Maharashtra added 7.3 lakh bales. Madhya Pradesh too seen about 1.82

lakh bales arrivals. In South India, about 3.36 lakh bales arrivals have been recorded. According

to USDA, production in India is forecast at 26.5 million bales 5.77 mt, up marginally from

2015/16. A rebound in India’s yield is expected to offset a 10-percent reduction in cotton area

this season.

LEGAL DISCLAIMER

This Document has been prepared by Ways2Capital (A Division of High Brow Market Research

Investment Advisor Pvt Ltd). The information, analysis and estimates contained herein are based

on Ways2Capital Equity/Commodities Research assessment and have been obtained from

sources believed to be reliable. This document is meant for the use of the intended recipient only.

This document, at best, represents Ways2Capital Equity/Commodities Research opinion and is

meant for general information only. Ways2Capital Equity/Commodities Research, its directors,

officers or employees shall not in any way to be responsible for the contents stated herein.

Ways2Capital Equity/Commodities Research expressly disclaims any and all liabilities that may

arise from information, errors or omissions in this connection. This document is not to be

considered as an offer to sell or a solicitation to buy any securities or commodities.

All information, levels & recommendations provided above are given on the basis of technical &

fundamental research done by the panel of expert of Ways2Capital but we do not accept any

liability for errors of opinion. People surfing through the website have right to opt the product

services of their own choices.

Any investment in commodity market bears risk, company will not be liable for any loss done on

these recommendations. These levels do not necessarily indicate future price moment. Company

holds the right to alter the information without any further notice. Any browsing through website

means acceptance of disclaimer.

DISCLOSURE

High Brow Market Research Investment Advisor Pvt. Ltd. or its associates does not do business

with companies covered in research report nor is associated in any manner with any issuer of

products/ securities, this ensures that there is no actual or potential conflicts of interest. To ensure

compliance with the regulatory body, we have resolved that the company and all its

representatives will not make any trades in the market.

Clients are advised to consider information provided in the report as opinion only & make

investment decision of their own. Clients are also advised to read & understand terms &

conditions of services published on website. No litigations have been filed against the company

since the incorporation of the company.

Disclosure Appendix:

The reports are prepared by analysts who are employed by High Brow Market Research

Investment Advisor Pvt. Ltd. All the views expressed in this report herein accurately reflects

personal views about the subject company or companies & their securities and no part of

compensation was, is or will be directly or indirectly related to the specific recommendations or

views contained in this research report.

Disclosure in terms of Conflict of Interest:

(a) High Brow Market Research Pvt. Ltd. or his associate or his relative has no financial interest

in the subject company and the nature of such financial interest;

(b) High Brow Market Research Pvt. Ltd. or its associates or relatives, have no actual/beneficial

ownership of one percent or more in the securities of the subject company,

(c) High Brow Market Research Pvt. Ltd. or its associate has no other material conflict of interest

at the time of publication of the research report or at the time of public appearance;

Disclosure in terms of Compensation:

High Brow Market Research Investment Advisor Pvt. Ltd. policy prohibits its analysts,

professionals reporting to analysts from owning securities of any company in the analyst's area of

coverage.

Analyst compensation: Analysts are salary based permanent employees of High Brow Market

Research Pvt. Ltd.

Disclosure in terms of Public Appearance:

(a) High Brow Market Research Pvt. Ltd. or its associates have not received any compensation

from the subject company in the past twelve months;

(b) The subject company is not now or never a client during twelve months preceding the date of

distribution of the research report.

(c) High Brow Market Research Pvt. Ltd. or its associates has never served as an officer, director

or employee of the subject company; (d) High Brow Market Research Pvt. Ltd. has never been

engaged in market making activity for the subject company.