Embed Size (px)

Citation preview

A PROCESS VIEW OF ALLIANCE CAPABILITY:

GENERATING VALUE IN ALLIANCE PORTFOLIOS

MB Sarkar

Assistant Professor Department of Management

College of Business Administration University of Central Florida

Orlando, FL 32816-1400 Phone: (407) 823 5699

email: [email protected]

Preet S. Aulakh

Pierre Lassonde Chair in International Business Schulich School of Business

York University Toronto, ON M3J 1P3, Canada

email: [email protected]

Anoop Madhok

David Eccles Fellow and Associate Professor Department of Management

1645 E Campus Center Dr Rm 104 University of Utah

Salt Lake City, UT 84112 email: [email protected]

ACKNOWLEDGEMENTS

We are indebted to the Queen’s Center for Knowledge-based Enterprises and the Alliance-Edge program (http://business.queensu.ca/kbe) for generous support of this project. The first author would also like to acknowledge support of this project from the Center for International Business Education Research at Michigan State University, and the Institute for the Study of Business Markets at Pennsylvania State University.

A PROCESS VIEW OF ALLIANCE CAPABILITY:

GENERATING VALUE IN ALLIANCE PORTFOLIOS

ABSTRACT

This paper investigates the source of heterogeneity in the distribution of alliance capabilitiesamong firms, and relates it to business processes that enable firms to generate collaborative value. Complementing the existing view of dyadic value creation, and the emerging experience and structural perspectives of alliance capabilities, we argue the importance of examining such a capability through the lens of organizational processes. Based on a theoretical framework of collaborative rents, we identify three processes – namely alliance proactiveness, relationalorientation and portfolio coordination as constituting such a capability. Using data from 235 firms, and controlling for alliance experience and the presence of a dedicated alliance function, we show that the three processes play an important role in enhancing a firm’s alliance portfoliocapital. Further, we find that the alliance portfolio capital has a positive impact on firm performance. Thus we find evidence of heterogeneity in deriving value from alliance portfoliosthrough an alliance capability emanating from organizational processes.

1

While the benefits of inter-organizational alliances have long been recognized, recent

evidence suggests that some firms are better able to create and capture value through their

alliances than other (Harbison and Pekar, 1998; Anand and Khanna, 2000; Kale, Dyer, and

Singh, 2002). From a resource-based perspective, such performance differentials reflect firm

heterogeneity in alliance capability, or the set of organizational and strategic routines used by

firms to develop and implement alliance strategies. In other words, the fountainhead of superior

collaboration-based outcome and resultant competitive advantage is arguably the set of high-

performance alliance routines operating inside the firm (Teece, Pisano, and Schuen, 1997).

However, in spite of growing interest on an alliance capability-based framework, we lack a

systematic understanding of this capability, and its underlying processes (Simonin, 1997;

Madhok and Tallman, 1998; Gulati, 1998). Aiming to address this gap, our study addresses three

questions: What are the organizational processes that constitute alliance capability? How does

formal institutionalization of an alliance function impact the outcome of these processes? What

is the relationship between the outcome of alliance capability and firm performance?

Within the rich traditions of voluntary inter-firm cooperation, two streams of research

have focused specifically on collaborative wealth generation and capture by firms. The first

stream of research focuses on dyadic ties between alliance partners in an effort to examine the

relational and governance aspects of collaborations, and their impact on value creation in

interdependent situations (Madhok and Tallman, 1998; Dyer and Singh, 1998). As a result, such

studies have provided useful insights into the life cycles of individual alliances in terms of partner

selection, relationship structure and governance modes, and performance implications of bilateral

collaborative relationships. The second more recent stream of research focuses on the firm as a unit

of analysis. Here the effort is to scientifically examine the intriguing possibility of differences in

2

firms’ ability to create and capture value at an organizational level, or heterogeneity in alliance

capabilities among firms. In particular, two recent studies identify alliance experience (Anand and

Khanna, 2000) and a dedicated alliance function (Kale, Dyer, and Singh, 2002) as demographic and

structural proxies of alliance capability.

We identify two areas that remain underdeveloped in the literature. First, an endemic

problem with the former stream of research which focuses on individual alliances is the fallacious

assumption that a firm’s set of alliances is independent (Koka and Prescott, 2002; Gulati 1998).

To the contrary, it has been noted that alliance success is not only a function of a firm’s

individual alliances, but also related to the design and management of alliance strategies across

the entire portfolio of partners (Parise and Casher, 2003). Coordinating knowledge and resource

flows across the different constituent elements of a firm’s alliance portfolio may be a value

creating mechanism in itself, since the possibility of synergy is likely to increase the portfolio

potential beyond the mere sum total of the individual alliances. In other words, the traditional

dyadic approach misses the possibility that the portfolio as a whole may become more imbued

with value as a result of holistic and inclusive management mechanisms and processes across

alliance (Dyer and Nobeoka, 2000).

Second, the emerging literature on alliance capabilities seems to be characterized by an

over-emphasis on structure, and a relative disregard of organizational processes. For example,

recent studies have considered alliance experience (Anand and Khanna, 2000) and a dedicated

alliance function (Kale, et al. 2002) as surrogates of alliance capability. However, given that

learning curves tend to vary significantly across firms (Argote, 1999), differences in alliance

outcomes could be explained by variance in organizational routines and processes that reflect

superior capability to design and manage alliance networks. Accordingly, experience, or internal

3

legitimization, may not be enough to guarantee future collaborative performance without the

explicit consideration of organizational routines and processes (Simonin, 1997). The need to

adopt a process mode of competitive advantage is further reinforced by the literature on dynamic

capabilities (Eisenhardt and Martin, 2000), and the associated idea that the competitive potential

of a firm’s resources and capabilities can only be realized through business processes (Ray,

Barney, and Muhanna, 2004).

In other words, the existing structural view of alliance capabilities do not explain the

underlying processes through which firms create and capture value from multiple alliances. This

under-emphasis is surprising given anecdotal evidence that some firms have developed and

refined their alliance routines so much so that it is now a part of their core competency (Harbison

and Pekar, 1998). In fact, both Anand and Khanna (2000) and Kale et al. (2002) point to the need

for further research to unpack the processes underlying alliance capabilities that do not get

captured either through accumulated experience, or institutionalization of the alliance function.

Finding that unobservables impact a firm’s alliance success rate, Kale et al. (2002) suggest that

“such unobservable characteristics relate to some firms being more learning and coordination

oriented than other firms, which in turn influences their alliance success rates” (p. 762).

Similarly, Anand and Khanna (2002) point out that although their study establishes the

“existence of differences in ‘alliance capabilities’ across firms” (p. 313-314), future work needs

to “explore the organizational determinants of this capability” (p. 314).

Our paper addresses these gaps by identifying organizational processes that create value

in the context of a firm’s portfolio of alliances. We first discuss “alliance portfolio capital” as the

value that resides in a firm’s set of alliances. Next, we identify organizational processes that

enhance the focal firm’s portfolio capital, as well as examine the contingent role of an

4

institutionalized alliance function on the link between organizational processes and alliance

portfolio capital. Finally, we link the alliance portfolio capital to firm performance.

ALLIANCE PORTFOLIO CAPITAL AND ORGANIZATIONAL PROCESSES

Alliance Portfolio Capital

Measuring the performance of dyadic alliances and the collaborative value that they

generate is an issue that has perplexed both academic researchers and practitioners for years

(Alliance Analyst, 1998; Geringer and Hebert, 1991). This problem is exacerbated while

assessing the performance of a firm’s alliance portfolio, where firms may have multiple alliances

at different phase of the life-cycle and operating at various stages of the value-chain. Evaluating

the performance of the portfolio through simple aggregation of the performance of individual

alliances may be erroneous because the portfolio members may contribute tangible and

intangible flows that spill-over beyond the dyadic relationship and create synergy. In other

words, since a “portfolio can be more than the sum of its parts” (Bamford and Ernst, 2002: 38), it

is important to consider an outcome that relates to the portfolio as a whole rather than its

constituent parts.

Accordingly, we consider the value created and captured by a firm through its alliances in

terms of its “alliance portfolio capital.” In conceptualizing this variable, we consider three

aspects that have been highlighted in the inter-firm collaboration literature (Parise and Casher,

2003). First, we consider the compositional element, and thereby the competitive strength of the

of portfolio members. This is important since “a firm’s portfolio of collaborations is both a

resource and a signal to markets, as well as to other potential partners, of the quality of the firm’s

activities and products” (Powell, 1998: 229). Therefore, a high-quality portfolio will not only

offer access to better resources, but is also likely to result in future accrual of better resources by

5

attracting stronger prospective partners. Second, in keeping with the rich tradition of relational

rents (Dyer and Singh, 1998) we consider the strength of the firm’s relationship with individual

partners within the portfolio. Third, we consider the strength of the firm’s affiliation of

partnerships as a whole. In sum, we consider the equity of the focal firm as a potential partner,

the competitiveness of the affiliation group, and the resilience of a focal firm’s ties with each

member as a firm’s alliance portfolio capital. In a sense, alliance portfolio capital captures the

“health/vigor” of a firm’s alliances, and thereby would reflect the degree to which it has been

able to create and capture value from its alliances.

Conceptualizing Alliance Capability

Extant literature suggests that collaborations present a firm with two potential routes to

value, namely common and private benefits (Khanna, Gulati, and Nohria, 1994; Khanna, 1998).

First, common benefits are those that accrue collectively to alliance partners. These composite

quasi-rents, or value generated by a firm’s resources in continued association with that of another

(Hill, 1990), enable firms to create value that individually, they would be unable to accomplish.

Private benefits refer to value generated for the firm through its alliance outside the focal

collaboration, for instance when knowledge-based spillovers from an alliance enriches a firm’s

stock of know-how in adjacent areas.

Importantly though, these benefits have been addressed mainly within the domain of

activities of a specific alliance. Yet, the argument also applies at the alliance portfolio level,

where a central firm forms multiple alliances that complement one another, and can benefit both

jointly and privately from each of these. The two levels are not disassociated from one another.

At the dyadic level, knowledge flows from individual collaborations can collectively and

dynamically coalesce with the focal firm’s own knowledge base in a synergistic way that is

6

singularly distinctive and not available to any other partner. Moreover, as Dyer and Nobeoka

(2000) found, common benefits also become available at the portfolio level when a focal firm

runs its alliances in an inclusive and participative way, and actively leverages relevant

knowledge generated from any one alliance across the portfolio. Logically then, if portfolio

members were to benefit more from their participation with a particular nodal firm relative to its

competitors, because of the focal firm’s particular competence at managing collaborations, this

would attract stronger partners.

However, in spite of the potential for both private and common benefits at both dyadic

and portfolio levels, firms often fail to translate such potential into realized benefits (Madhok

and Tallman, 1998). This can occur for various reasons: First, the choice of partners may be sub-

optimal. Second, systemic relationship imperfections, such as lack of trust and commitment and

inadequate coordination routines for sharing knowledge, can prevent partners from combining

their resources and capabilities optimally. Third, firms may fail to fully leverage knowledge from

their individual alliances across the portfolio. Given this distinction between the potential of a

firm’s alliance portfolio and its ability to translate this potential into realized collaborative

benefits, firms need to operate on multiple fronts and engage in a coherent set of inter-related

activities in order to maximize the value derived from its alliance portfolio. In this light, effective

collaboration routines become critical not only to maximize the potential value of the alliance

portfolio, but also to narrow the gap between the potential and realized value.

Put differently, the variance in how firms manage their resource re-configuration through

linking to bilateral and portfolio-level strategic assets in their search for new value-creating

strategies provides a basis for understanding why firms derive different levels of value through

their alliances. In other words, performance differentials across firms with respect to their

7

alliance portfolios may occur due to differences in the embedded potential of a firm’s alliances,

as well as varying degrees of success in translating this potential into realized collaborative

benefits.

The implications from the above discussion are as follows: One, collaborative rents are

created by processes that enable a firm to identify and form relationships with partners with

whom alliances would have high value-creating potential. Second, firms can develop process

skills in managing cooperative relationships that facilitate the intermingling of joint and often

interdependent resources and capabilities, thus enabling them to exploit the underlying potential

(Dyer and Singh, 1998). Third, above and beyond this, firms need to engage in cross-alliance

knowledge transferring mechanisms and thus create synergy across its portfolio of alliances

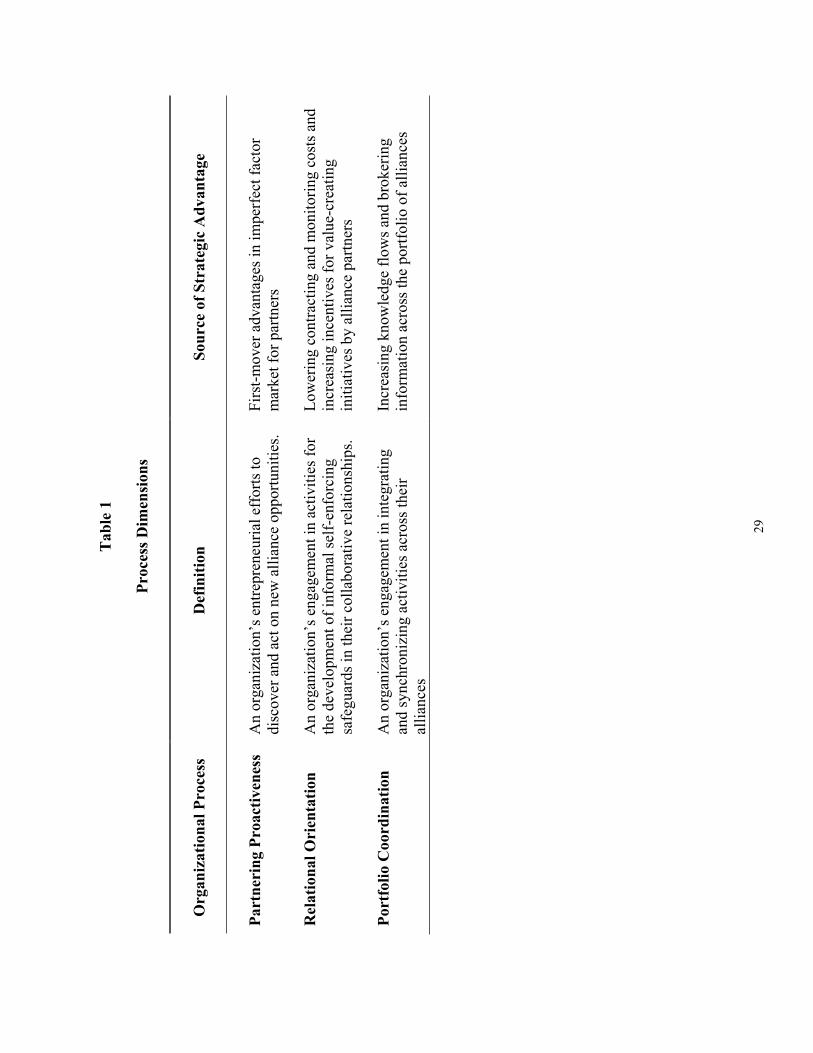

(Gulati, 1998). These three processes and their underlying properties are summarized in Table 1.

In the following section, we elaborate on each and develop the hypotheses.

-------------------------------------Insert Table 1 Here

--------------------------------------

HYPOTHESES

Alliance Capability and Portfolio Capital

Alliance Proactiveness: We conceptualize alliance proactiveness as a firm’s efforts to

discover and act on new alliance opportunities. Encompassing opportunity sensing and response

capabilities, this dimension of includes organizational processes to identify new and potentially

valuable partnering opportunities, and preemptive actions to respond to such opportunities. Firms

that are proactive in identifying and acting on partnering opportunities are likely to enjoy pre-

emptive first-mover advantages in the ‘market for partners’. This in turn is likely to increase the

value creating potential of their alliances.

8

The relevant strategic factor market for a firm wishing to augment its internally owned

and controlled resources and capabilities through alliances is the market for partners. The

strategic factor market for partners, defined as the set of potential collaborator firms that are

compatible and possess required strategic resources, is likely to be imperfect for several reasons.

First, there is likely to be asymmetric information and differing expectations among competitor

firms about the future value of a specific alliance. Better-informed firms may be able to exploit

imperfections in their favor. Second, a potential ‘small numbers’ problem may lead to a scarcity

of potential alliance partners, and leave late movers with sub-optimal options (Sarkar,

Echambadi and Harrison, 2001).

Therefore, alliance proactiveness is likely to result in preemptive benefits, enabling such

firms to capture advantageous positions in partner space, which consists of the set of suitable

firms that possess the required set of complementary strategic assets. Gomes-Casseres (1996)

calls this “strategic gridlock,” referring to a situation of supply-side scarcity in which partnership

options are used up as alliances proliferate in an industry, and where resulting preemption of

valuable and scarce resources in partner space becomes a source of strategic advantage. As a

result, a stronger and more competitive portfolio is likely to possess greater underlying potential

to create value through the alliances. The unique resource configurations or “constellations” that

result from proactive alliance activity may be difficult to imitate, leading to sustainable

differences in the value of the alliance portfolio in which firms are embedded (Gomes-Casseres,

1996). Therefore, we hypothesize:

H1: Alliance proactiveness will be positively associated with alliance portfolio capital.

Relational Orientation: An organization’s willingness to make relational investments reflects

its level of commitment to the relationships, and the extent to which individual partners are

9

valued. Accordingly, the relational dimension refers to the extent to which partners are mutually

oriented towards one another. A relational orientation tends to be characterized by greater trust,

flexibility and resilience (Dyer and Singh, 1998) and is manifested through the extent to which

an organization engages in informal interactions and normative mechanisms that are cooperative

in nature and serve to bind partners together through shared understandings and norms. In such

cases, any contracts between the partners are supported and supplemented through normative

mechanisms, whereby the partners concerned are willing to initiate unilateral commitments in

the interests of the relationships. A relational orientation enables partners to engage in a more

dynamic process of interaction and value creation than would be the case in situations where

there are significant imperfections in the relationship. One critical systemic relational

imperfection is the fear of opportunism, which creates a fundamental safeguarding problem in

relationships where partners have to make exchange-specific investments (Williamson, 1985).

Both formal and informal safeguards are appropriate mechanisms to minimize the threat

of opportunistic behavior in interorganizational relationships, and may even complement one

another (Poppo and Zenger, 2002). However, besides cost and efficiency implications as a result

of lower contracting and monitoring costs, informal normative safe-guards characterized by trust

relations provide superior incentives for value-creating initiatives by alliance partners, such as

sharing fine-grained tacit knowledge, exchanging resources that are difficult to price, or offering

innovations or responsiveness beyond the contract (Dyer and Singh, 1998). In other words, given

that “the production of a collective good is inextricably intertwined with the underlying

dynamics of exchange” (Madhok and Tallman, 1998: 327), the value of a partnership is likely to

depend on the relational investments and patterns of interaction among the partners.

10

The main difference between these approaches is that the former is purely self-interested

point of view of a focal firm whereas the latter is much more dyadic in its orientation (Zajac and

Olsen, 1993). To the extent that a firm’s partners can also benefit in their alliances with the firm

as a result of its relational orientation, the firm becomes an attractive partner. Other things being

equal, potential partners would be drawn to enter into partnerships with a focal firm over its

competitors if there is a greater probability in benefiting from it, as evidenced by its prior track

record, and would also be more willing to act relationally from the outset. Skills at managing

partnerships, as well as availability and willingness of partners of choice, should result in joint

value creation to the benefit of all partners (Madhok, 2002). Thus,

H2: Relational orientation will be positively associated with alliance portfolio capital.

Alliance Portfolio Coordination: Portfolio coordination comprises the processes by

which the focal firm engages in integrating and synchronizing activities, strategies, and

knowledge flows across their alliance networks. In place of a discrete, atomistic view of

alliances, or what Granovetter (1992) has termed ‘dyadic atomization,’ this perspective eschews

the reductionism that occurs when an analyzed pair of firms is abstracted out of their embedded

context. Instead, it emphasizes a holistic view of an organization’s network. Due to the

possibility of knowledge spillovers, the value potential of the alliance portfolio is greater than the

sum of individual alliances (Anderson, Hakansson, and Johanson, 1994; Koka and Prescott,

2002).

As “interstices between firms, universities, research laboratories, suppliers and

customers" become sources of innovation (Powell, Koput, and Smith-Doerr, 1996: 118), any

single breakthrough involves a wide range of organizations (Hargadorn and Sutton, 1997).

Accordingly, the locus of value creation becomes the collective entity, rather than an individual

11

firm. In response to such complex task requirements, firms need to integrate many different

specialist organizations into a large, modular system of grouped value-adding activities.

Managing such complex interdependencies across multiple external partners necessitates

extensive coordination among constituent firms. Coordinating and aligning strategies with the set

of partners becomes key to a firm’s response capability to leverage the entire alliance portfolio

(Lei, Hitt, and Goldhar, 1996; Gomes-Casseres, 1996). Further, increasing diversity in source of

innovations implies opportunities to create value by brokering information and coordinating

knowledge flows across structural holes, or disconnects in knowledge structures through

information access, timing, referrals, and control (Burt, 1992; Achrol and Kotler, 1999).

In essence, multiple interdependencies and associated knowledge flows across the

portfolio of alliances potentially generates collaborative synergies. In order to realize this

synergy, however, firms need to systematically manage the interdependencies and flow of

resources between their inter-organizational resource clusters. They need to coordinate, integrate,

and transform resources housed in different 'partner silos' in their internal networks the portfolio.

That is, through inter-alliance coordination, a firm can adapt and recombine know-how of

partners into unique market opportunities, and thus create synergistic value for the whole

portfolio (Parise and Casher, 2003).

In fact, managing the portfolio as a collective and generating synergy across the entire

network should benefit the participants more than if each were managed separately. In the case

of Toyota’s network, for example, Dyer and Nobeoka (2000) found that knowledge sharing

mechanisms at the portfolio level, together with a strong network identity, such as a partners’

association, benefited both Toyota and its partners. This further increased their willingness to

share knowledge with one another. Through such processes, the portfolio evolved from a

12

collection of dyadic ties with the nodal firm to also include multilateral ties among portfolio

members. Moreover, reputational mechanisms work more readily in such interdependent

alliance portfolios, which also prevents free-riding and opportunism. The authors demonstrated

how this ultimately led to productivity benefits and made the portfolio as a whole more

competitive.

H3: Alliance portfolio coordination will be positively related to alliance portfolio capital.

The Contingent Role of Alliance Function

Our arguments till now have centered on the premise that firm heterogeneity in acquiring

and deploying collaborative processes accounts for the generation of alliance portfolio capital.

The three processes clearly reinforce one another. The combination – discovery of partnering

opportunities and partners, managing each partnership in a way that both partners enjoys robust

benefits from partnership, and managing them collectively so that benefits within partnerships

are also shared for network synergies where available - contribute to the value of a firm’s

alliance portfolio capital, i.e. enhance alliance portfolio capital.

Recent research has proposed that a centralized point of coordination, expressed through

a separate and dedicated alliance function, may enhance a firm’s alliance capabilities by

facilitating the transformation of experience into know-how, ensuring resource flows, and

improving coordination processes. In support, Kale, Dyer, and Singh (2002) found that a formal,

dedicated alliance function is associated with superior alliance performance. However, reflecting

their interest in the performance aspects, these authors just asserted that an alliance function

would facilitate alliance coordination. Rather than make such an assumption, we test this

argument and examine whether and how a dedicated alliance program interacts with the

collaborative routines underlying the above three dimensions in the creation of value.

13

We adopt the viewpoint that a formal alliance program has a synergistic effect with

collaborative routines, and accordingly propose that the effect of the alliance management

processes strengthens in the presence of structural support as manifested through an

institutionalized alliance program. This is so since, besides a legitimizing role that signals the

importance of alliances and also has resource implications, an alliance function also has a

learning role (Kale, Dyer, and Singh, 2002). A centralized center of competency development is

likely to enable a firm to convert its alliance experiences into an organization-wide know-how.

An organization with a dedicated alliance program is more likely to engage in systematic efforts

to capture, interpret, and codify alliance experiences into a shared organizational repository of

alliance management knowledge. As a result, the effectiveness of organizational routines that

underlie the three aspects of portfolio management above would be further enhanced where there

is a formalized alliance program. In other words, collaborative routines and organizational

structure share a complementary, or co-specialized relationship in that the value of one increases

in the presence of the other. Accordingly, we hypothesize that:

H4a-4c: The relationship between alliance proactiveness, relational orientation, and

portfolio coordination and the alliance portfolio capital will be moderated by alliance

function, such that these relationships will be stronger as the level of institutionalization

of the alliance function increases.

Alliance Portfolio Capital and Firm Performance

While the previous hypotheses related three process dimensions to alliance portfolio

capital from the perspective of a focal firm, a critical issue that demands further investigation is

whether the value created through strengthening the portfolio impacts firm performance. We

suggest that a firm’s alliance portfolio capital represents a valuable, rare and non-imitable

resource and thus will positively impact performance. First, the value of extra-firm resources

accessed through alliances and other affiliations has been well documented (Kale et al., 2002;

14

Anand and Khanna, 2000; Tsai and Ghoshal, 1998), with respect to both private as well as

common benefits (Dyer and Nobeoka, 2000). In the context of our study, a strong alliance

portfolio would enable the focal firm to gain access and deploy economic and knowledge

resources through its partners that help it maintain and enhance competitive advantage. Second,

such portfolio capital has rareness property because of the small numbers problem of quality

partnering opportunities. Therefore, a firm that becomes a partner of choice in imperfect partner

markets is able to build strong individual relations, as well as synergistically combine resources

from different parts of the portfolio and create a rare, firm specific advantage. Finally, alliance

portfolio capital is simultaneously located in discrete, identifiable dyads, and as a generalized

resource gained through membership in portfolio that actors may draw on. The co-production

and consumption of this alliance capital makes it not only time-dependent but also sticky, due to

which it is difficult to transfer and imitate. Accordingly, we hypothesize that:

H5: Alliance portfolio capital will be positively related to firm performance.

METHOD

Questionnaire Development

The study was conducted in two stages using a discovery-oriented approach. In stage one,

after a review of the literature, measures were developed through an iterative modification

process and in-depth interviews with 25 senior managers with alliance responsibilities from 21

firms across diverse industries1. Our respondents were identified through three sources: corporate

1 We approached executives/companies through three sources: Corporate members of a research institute of a largemid-western University, searches on electronic databases such as Lexis/Nexis and Proquest with keywords such as ‘alliance managers’ and ‘director alliances’ and contacts of some practitioners who presented and conductedsessions at the strategic alliances seminars for the Conference Board. Firms from various industries wereinterviewed: advisory and consultation, computer software, pharmaceutical, chemicals, mining and manufacturing,building-materials and glass for telecommunication, scientific/ photo/ control/equipment, motor vehicles and parts,collectible motorsports and consumer products, computers/office equipment, and network communication. Fifteen

15

members of a research institute of a large mid-western university, searches on Lexis/Nexis and

Proquest with keywords such as ‘alliance managers’ and ‘director alliances,’ and through

contacts of practitioners who had participated at strategic alliances seminars for The Conference

Board. Scales were borrowed and adapted from existing literature. In those instances where no

previous scales existed, measures were developed using a framework proposed by DeVellis

(1991). For new scales, we drew on the expertise of our interview informants to develop a pool

of items. The instrument incorporated their language to reflect the exact nuances of the variable

in question. This initial item pool was reviewed by academic experts, and returned to the

industry informants who were now asked to evaluate and modify the items where they felt it was

necessary. The scale length was optimized, subsequent to which the draft questionnaire was

administered to a second panel of executives, and their concerns noted through follow-up

discussions. The discussions focused on ambiguous items, instrument length, and format. Once

again, items were either modified or deleted based on this feedback, and the questionnaire

finalized.

Sampling Frame and Data Collection

Data for testing the hypotheses were collected through a mail survey. First, 1800 firms

with annual sales over $25 million were drawn randomly from the CorpTech Directory of

Technology Companies.2 We sent a letter and return envelope to CEOs requesting participation

and asking for the contact details of senior-level executives knowledgeable about the company's

strategic alliance-related processes and activities (the CEO could also identify himself/herself).

Thirty seven surveys were undelivered and 110 companies responded that for various reasons

of them had substantial global networks, of which seven were large Fortune 500 companies, and six were ranked inGlobal 500.2 The firms were from the following primary SIC codes: SIC 28-Chemicals and allied products; SIC 35 - Industrialand machinery equipment; SIC 36-Electronic and other electric equipment; SIC 38-Instruments and relatedproducts; SIC 73-Computer and data processing; SIC 87-Engineering and management services.

16

they were unable to participate. From the effective sampling frame of 1653, 293 firms agreed to

participate in the survey.

In the second stage, we mailed the survey, along with a cover letter and a business reply

envelope, to the 293 executives. This was followed by a telephone/e-mail reminder two weeks

after the first mailing, and then a second mailing was done about three weeks later. In both the

cover letter and the instructions on the questionnaire, respondents were reminded that the survey

deals with their respective firms’ alliance related activities. Accordingly, they were told to focus

on their firms’ alliances along the different value-chain activities (i.e., new product development,

marketing, distribution, manufacturing, R&D, suppliers, customers). Further, the respondents

were provided with a working definition of alliances in the above mentioned domains as

“relatively enduring cooperative arrangements, equity-based or otherwise, involving

interdependence and resource-linkages, having the express purpose of joint accomplishment of

goals linked to the corporation mission of each firm.” After the two mailings, a total of 184

companies responded. Subsequently, we electronically mailed the surveys to the non-responding

informants and through this process received additional responses from 53 firms. Thus, we

received responses from 237 firms for an effective response rate of 14.34%. Two of these

returned surveys were discarded due to excess amount of missing data. From 28 firms, we

received two responses. In subsequent analysis we used the response from the more senior

manager. In effect, the final sample size is 235 different firms.

Validity of Responses

While survey research has been useful in understanding organizational behavior, and in

certain contexts, may be the only feasible way to get the desired information (Huber and Power,

1985; Dess and Robinson, 1984), there are several concerns related to the validity of this data

collection methodology. In particular, three issues have been raised: (i) selection of key

17

informants and informant bias in responding to the survey; (ii) non-response bias which leads to

a systematic exclusion of firms from the population; and (iii) problems related to common

method variance (Huber and Power, 1985; Podsakoff and Organ, 1986).

Survey methodology was used in this study because our focus on organizational

processes which are difficult to ascertain from archival sources. However, we were cognizant of

the above mentioned problems related to perceptual measures and took careful steps both prior to

collecting the data and questionnaire design, and through post hoc procedures, First, in designing

the survey, as suggested by Parkhe (1993), the measures for dependent variables related to

performance preceded the independent variables. Second, in order to further minimize effects of

consistency artifacts, open-ended questions were interspersed throughout the instrument and the

anchors for scales varied for certain constructs (i.e., use of both Likert scales and indices).

Regarding issues related to key informants, we targeted managers who were explicitly

responsible for the respective firm’s alliance operations.

Respondents were mostly senior level executives, with the following breakdown:

CEO/President – 17.6%; Vice-President - 54.5%; Director – 23.2%; Manager – 4.7%. The

respondents on average had 10.3 years of experience with their current firms. To assess non-

response bias, early and late responders were compared on sales volume, number of employees,

and the items used to measure market performance (Armstrong and Overton, 1977). The results

indicate no statistically significant difference between these groups.

Finally, we examined the common method variance issue through three post hoc

statistical tests. First, we used Harman’s one-factor test. The logic behind this test is that if

common method variance is a serious issue in the data, a single factor will emerge or one general

factor will account for most of the covariance in the independent and dependent variables

(Aulakh and Kotabe, 1997; Podsakoff and Organ, 1986). We performed a factor analysis on

items related to the partnering proactiveness, relational orientation, portfolio coordination and

alliance portfolio capital, extracting four factors with eigen values greater than one.

Furthermore, no general factor was apparent in the unrotated factor structure, with Factor 1

18

accounting for only 17% of the variance. Second, we conducted Wilcoxon Signed-Ranks Test for

paired sample data that came from multiple respondents on matched firms. In all, we identified

28 companies that had two respondents. We did the Wilcoxon signed-ranks tests in two steps. In

the first step, tests were conducted at the item-level on the various independent and dependent

variables. The null hypotheses, that there is no difference in response between the respondents,

could not be rejected for any of the items. In the second stage, we summated the individual

items to create the constructs used in our study and conducted the Wilcoxon signed-ranks tests

on these constructs. All the null hypotheses were not rejected.

Finally, our sample contained inputs from 94 public firms, of which 12 reported that they

were responding at the business-unit level. For the remaining 82 firms, we collected

performance data from the COMPUSTAT database. We collected data on commonly used

measures of performance – Return on Assets (ROA), Return on Equity (ROE), Return on

Investment (ROI) and Sales Growth (SG) for 1996, 1997 and 1998. We subtracted the industry

average from each firm’s ROA, ROE, ROI and SG to control for industry effects (Agle, Mitchell

and Sonnenfield 1999). We then averaged three years of performance data and correlated the

four with perceptual measure of market performance. The correlations between market

performance and averaged ROA, ROE, ROI and SG are 0.45, 0.41, 0.44, 0.31, respectively, all

significant at p < .05. The above-described tests indicate satisfactory validation of our survey

measures.

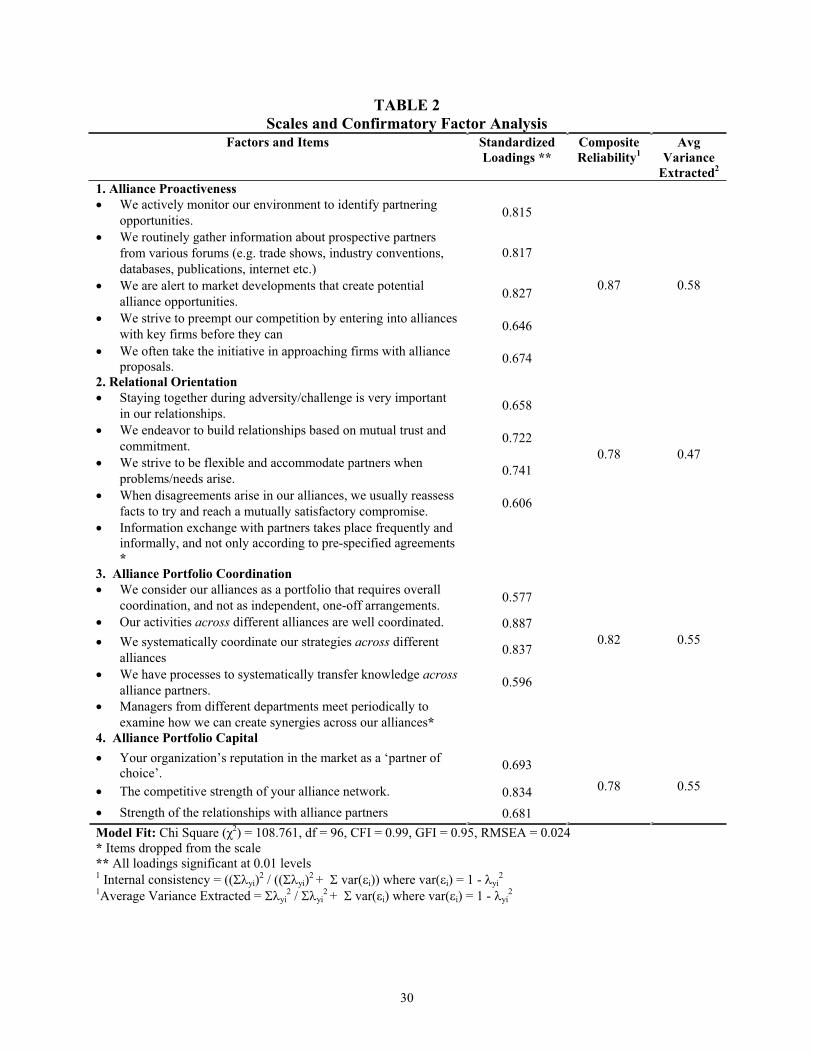

--------------------------------Insert Table 2 Here

-------------------------------------

Measures

Table 2 reports individual items and their loadings on relevant constructs. The 5-item likert scale

for alliance proactiveness ( = .83) tapped a firm’s efforts to collect information from diverse

channels about alliance opportunities, and its general state of alertness in sensing and responding

to partnering opportunities. The 5-item relational orientation likert scale ( = .79) was adapted

19

from Heide and John (1992), and measured the cooperative, long-term approach of relationship

building with alliance partners. The 5-item likert scale for portfolio coordination ( = .82)

measured the extent to which a firm integrated its activities, strategies, and knowledge flows

across its alliance portfolio. Alliance portfolio capital ( = .78) was measured as a firm’s

partnering reputation as a reliable network member (Benjamin and Podolny, 1999), the

relationships the firm has accumulated over time (Granovetter, 1985), and the competitiveness of

the firm’s alliance network. The dichotomous alliance function scale is similar to Kale, Dyer,

and Singh (2002). Respondents were asked whether their organization had a formal, dedicated

program that was responsible for overseeing the firm’s alliances. For firm market performance,

we adapted Venkatraman and Ramanujam's (1986) formative scale and measured four aspects,

namely market share, sales growth, market development and product development. Respondents

rated their performance, relative to competitors to control for industry effects (Judge and

Douglas, 1998) on a 5-point scale with the anchors being 'Much Worse' and 'Much Better'.

Controls: Firm size is operationalized as the natural logarithm of total sales. Industry effect is

controlled through the inclusion of a variable, resource munificence, operationalized from a four-

item scale which measures the extent to which resources for growth are available in the firm’s

industry. Alliance experience was measured as the natural logarithm of the total number of a

firm’s alliances. Alliance diversity was operationalized as a variation of Blau’s index.

Respondents were asked to note their number of alliances in each of the following areas: New

Product Development, R&D/Technology, Marketing/Distribution, Supplier, Manufacturing, and

Customer. We then computed alliance portfolio diversity for each firm by adapting Powell et

al’s. (1996) network portfolio diversity measure, as follows: D is the diversity measure and p the

proportion of the firm’s alliances in each of the 6 alliance categories.

6

D = 1- pi2

j=1

20

Measurement Model

We use confirmatory factor analysis techniques using the maximum likelihood estimation

in EQS v 5.7b to check for convergent and discriminant validity as well as factor structure of our

four critical self-reported scales, namely the three process variables and alliance portfolio capital.

Through a series of iterations, some items that were either cross-loading or not loading on to the

intended construct adequately were eliminated. The refined measurement model indicates

acceptable fit ( = 108.76, d.f. = 1.14, GFI = 0.95, CFI = 0.99, RMSEA = 0.024). Convergent

validity was indicated by the fact that all standardized loadings were above .58 and significant (p

< .01), and lack of cross-loadings. Composite reliabilities ranged from .78 to .83, well above the

recommended .6 cut-off. Inter-factor correlations were significant and positive, ranging from .37

to .54, indicating nomological validity. Discriminant validity was assessed in two ways. Chi-

square difference tests, in which correlation between pairs of constructs were freely estimated

and then constrained to 1 (Joreskog, 1971), were conducted. In each instance, the difference in

chi-square from the baseline four-factor model was significant, thus indicating both discriminant

validity as well as support for a four-factor structure modeli. Further, average variance extracted

(AVE), which measures the amount of variance captured by a construct’s measures relative to

measurement error, all achieved recommended levels of .5, with the exception of relational

orientation which was marginally lower at .47 (Fornell and Larcker, 1981). The squared

correlation between pairs of constructs, which ranged between .14 and .25, was compared with

AVE. The AVE of each construct turned out to be greater than its squared correlation with any

other factor, thus further indicating discriminant validity. Therefore, it appears that the scale

measures are internally consistent, able to discriminate, and provide a good fit of the model to

the data.

21

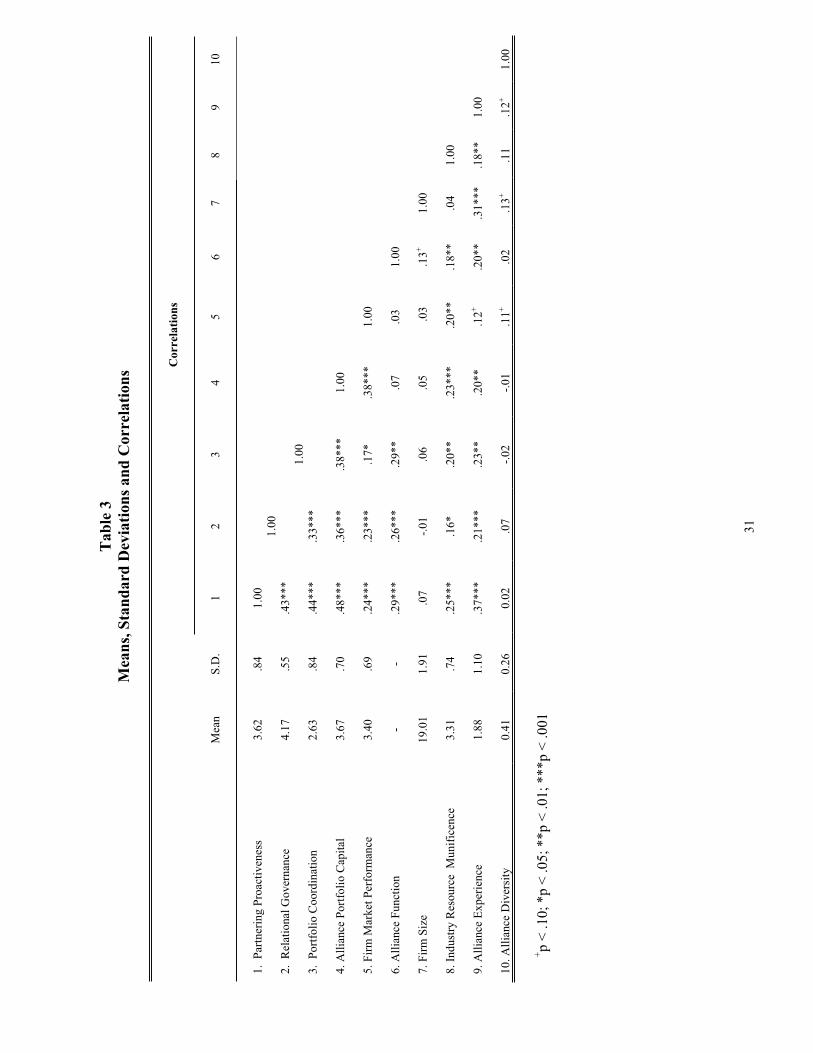

--------------------------------Insert Table 3 Here

--------------------------------------

RESULTS

The hypotheses were tested through ordinary least squares regression. The descriptive

statistics and correlations of the summated scores are provided in Table 3. We performed

collinearity diagnostics by examining the bivariate correlations and variance inflation factors

(VIFs). None of VIFs in all the regression equations was more than 2.0, well below the accepted

cut-of 10. Furthermore, assumptions of equality of variance, independence of error, and

normality of the distribution of errors were met for all regression equations. The hypotheses

were tested in two stages: first, the antecedents of alliance portfolio capital, and second, the

relationship between alliance portfolio capital and the firm’s market performance.

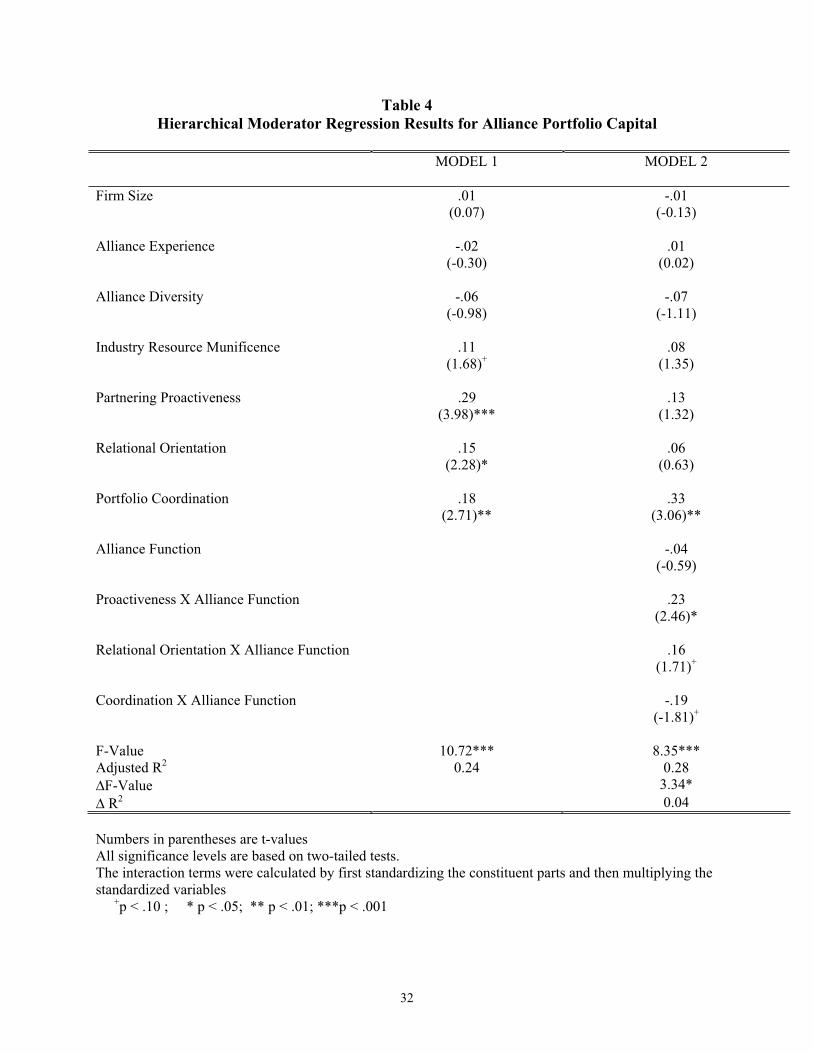

--------------------------------Insert Table 4 Here

--------------------------------------

In the first stage, the hypotheses related to the direct impact of the three process aspects

(partnering proactiveness, relational orientation and portfolio coordination) (H1 to H3) as well as

the moderating role of alliance function (H4a-H4c) were tested through OLS hierarchical

regression. Accordingly, a two step model was run with alliance portfolio capital as the

dependent variable and the three process aspects, moderator, three interactions, and three

controls as the independent variables. Results are provided in Table 4

--------------------------------Insert Table 4 Here

--------------------------------

As shown in the table, the Model 1 is significant (F(7, 202) = 10.72, p < .001) and the set of

independent variables explain 24% variance in alliance portfolio capital. In terms of individual

22

hypotheses, the beta coefficient for partnering proactiveness is positive and significant ( = .29,

p < .001), thus supporting H1. We also find support for the positive relationship ( = .15, p <

.05) between relational orientation and alliance portfolio capital thus supporting H2. H3 is also

supported as the beta coefficient for portfolio coordination is positive and significant ( = .18, p

< .01). Thus, we find strong support for the direct impact of the three process aspects identified

in this study in enhancing the firm’s alliance portfolio capital.

In model 2, we added the moderator variable (alliance function) and the three interactions

to examine the incremental impact on model fit and test. As shown in the table, this significantly

improves the model fit. The overall model is significant (F(11, 198) = 8.35, p < .001), the change in

F-value is significant ( F=3.34, p < .05) and there is a significant increased in explained

variance (adjusted r-square = .28). In terms of the individual interactions, as expected, the beta

coefficient for the interaction between partnering proactiveness and alliance function is positive

and significant ( = .23, p < .05), thus supporting H4a. Similarly the interaction term for

relational orientation and alliance function is positive and significant ( = .16, p < .10)

supporting H4b. Contrary to our hypothesized relationship, we find that alliance function

negatively moderates the relationship between portfolio coordination and alliance portfolio

capital ( = -.19, p < .10) thus contradicting H4c.

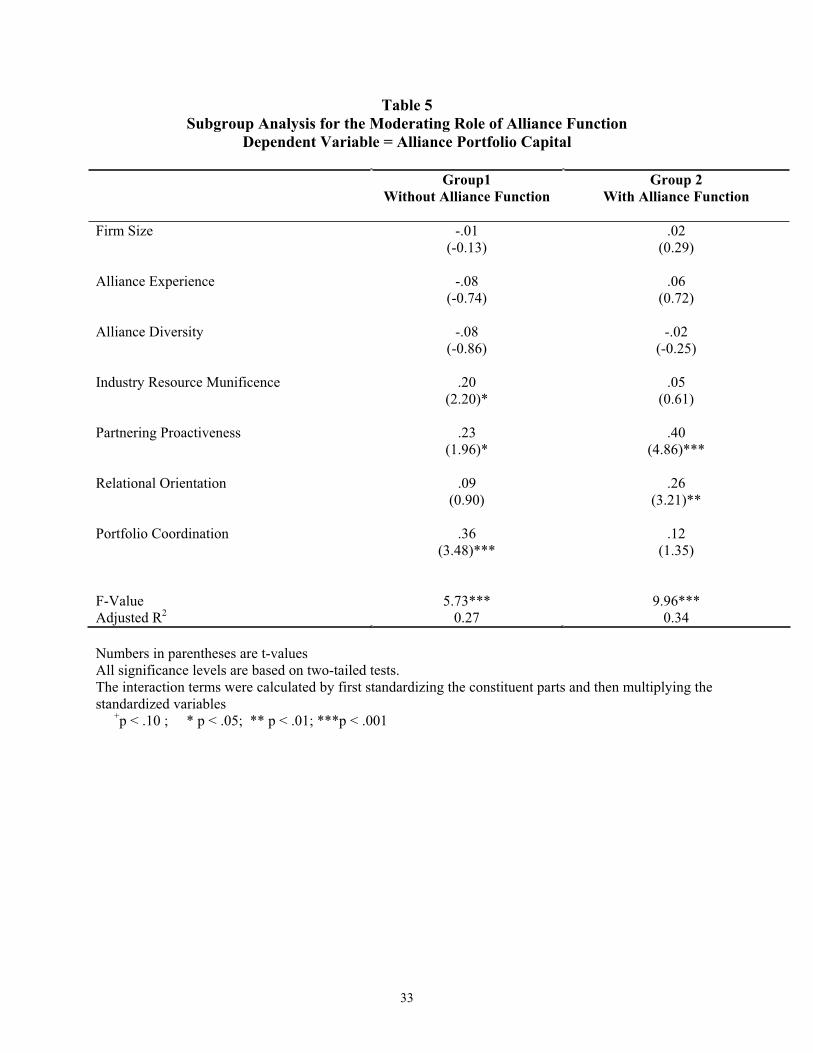

To evaluate the moderating effect of alliance function further, we performed sub-group

analyses, the results of which are provided in Table 5. We divided the sample into two groups

(Group 1 being firms without a dedicated alliance function and Group 2 consisting of firms with

a dedicated alliance function). Subsequently, we ran two regression models for the two groups

whereby alliance portfolio capital is regressed on the three process variables and the four

controls. While both models are significant, we find that the explained variance is higher for the

23

group with the alliance function (Adjusted R2Group2 = 0.34) than for the group without an alliance

function (Adjusted R2Group1 = 0.27) and the overall Chow test shows significant differences

(F(7,214) = 3.12, p < .05). We also find that proactiveness has a consistent positive effect on

alliance portfolio capital although the effect is stronger for Group 2 ( = .40, p < .001) than for

Group 1 ( = .23, p < .05). Similarly, for relational orientation, the effect is stronger for Group 2

( = 0.26, p < .01) than for Group 1 ( = .09, p > .10). Thus, as expected in H4a and H4b, we

find a positive moderating effect of alliance function. For portfolio coordination, we find that

the effects for Group 1 with no alliance function ( = 0.36, p < .001) is stronger than for Group 2

with an alliance function ( = 0.12, p > .10) which suggests a negative moderation. These

findings are discussed in the next section.

--------------------------------Insert Table 5 Here

--------------------------------

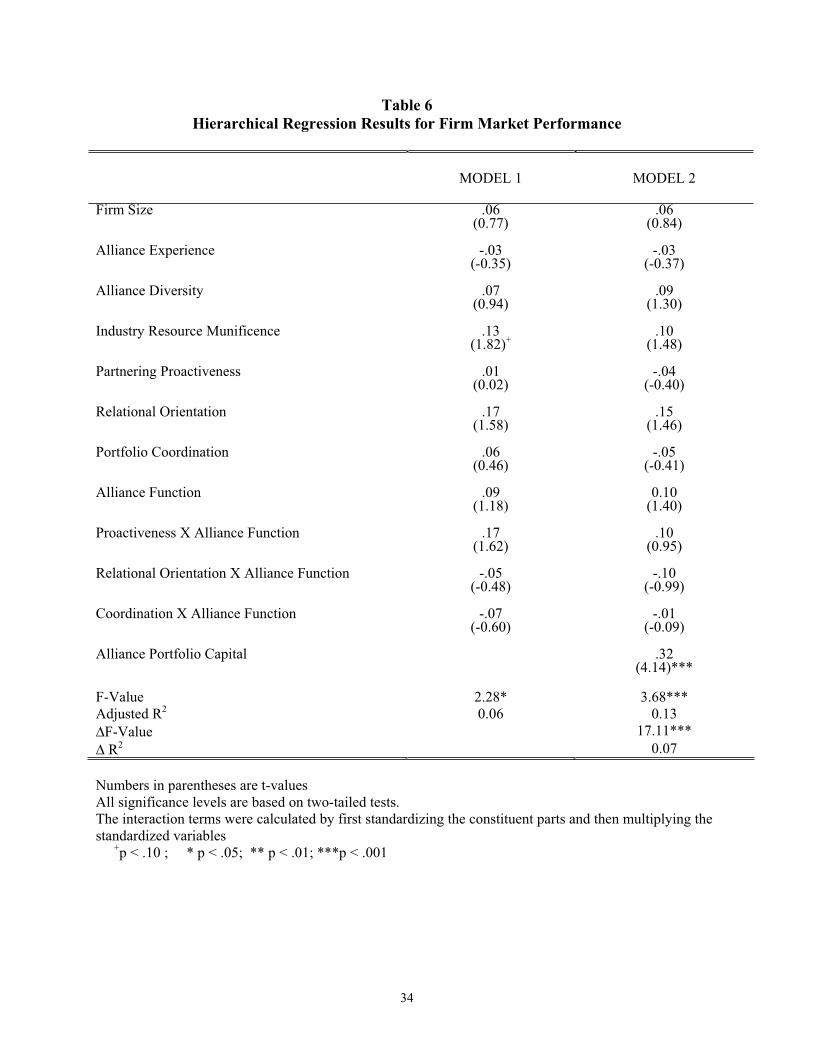

To test H5, which relates to the impact of a firm’s portfolio capital on its market

performance, we ran a hierarchical regression model. In Model 1, we regressed market

performance on the four control variables, the three process aspects, alliance function, and the

three interactions. In Model 2, alliance portfolio capital was added to the equation. This

approach allowed us to assess whether there were any direct effects of partnering proactiveness,

relational orientation, portfolio coordination as well as alliance function on market performance

or if these effects were mediated by alliance portfolio capital. Results are provided in Table 6.

The overall models are significant at p < .001 level, the explained variance is 6% and

13%, respectively for the two models and the change in r-square (7%) is significant at p < .001.

In terms of H5, we find a positive and significant relationship ( = .32, p < .001) between firm’s

alliance portfolio capital and market performance. Furthermore, the results also show that the

24

alliance portfolio capital mediates the relationship between the three alliance process aspects

identified in this paper and market performance (there is no significant coefficient in Model 2).

--------------------------------Insert Table 6 Here

--------------------------------

DISCUSSION

As firms transform from atomistic units into ones with flexible boundaries, their ability to

design, manage, and leverage their portfolio of strategic partnerships assumes increasing

relevance in explaining heterogeneous outcomes from their alliance networks. This is so since

managing a particular alliance relationship as part of an interconnected portfolio of relationships

could yield performance advantages over firms that manage them atomistically. However, while

the strategic importance of being able to access and leverage partner resources and capabilities

has never been higher, it is intriguing that most of the literature on alliances that examines

processes does so at the dyadic level (i.e., within a particular partnership). In contrast, the

alliance capability literature has tended to implicitly assume, or at least downplay, the role of

process. This is all the more significant since processes form the bedrock of competitive

advantage (Ray, Barney and Muhanna, 2004).

One reason for this lacuna may be that the alliance portfolio literature is as yet incipient.

Our research was motivated by the need to complement existing studies on the topic. Although

the literature rooted in firm capabilities does point to the importance of focusing on firms’

alliancing routines and processes, our understanding however of what exactly underlies such

capabilities is limited. This paper makes a contribution by more carefully and systematically

investigating underlying processes which contribute to the strengthening of alliance portfolio

capital, which in turn has implications for competitive advantage and ultimately performance. In

25

this regard, we link alliance portfolio capital to its processes encompassing proactive portfolio

formation, relationship management, and network coordination.

In essence, the positive relationship between a firm’s alliance portfolio capital and its

market performance supports some recent theoretical linkages in the network literature between

social capital and rent generation and appropriation (Blyler and Coff, 2003). As we move

towards a greater understanding of portfolios and networks as resource and knowledge

repositories, Pettigrew, Thomas and Whittington’s (2001: 18) contention that participation in

networks and skills in operating within them “are now seen to be key additional factors in

explaining the old strategy questions of ‘why do firms differ in their conduct and profitability’”

acquires even greater import. Overall, to derive sustainable competitive advantage, a firm needs

to not only develop a network of alliances but also to develop processes needed to build and

strengthen their alliance portfolio capital. The link between such processes and firm performance

is an important area for future research. Recent empirical findings of fixed-firm effects in

individual firms’ alliance performance seems to indicate heterogeneity in firms’ alliance

capabilities, since such effects existed even after controlling for alliance experience (Anand and

Khanna, 2000).

While we find no direct relationship between an alliance function and alliance portfolio

capital, our findings regarding the contingency impact of a dedicated alliance function on the

relationship of these three processes on alliance portfolio capital are mixed. The lack of a direct

relationship of an alliance function on alliance portfolio capital is intriguing. It appears that

creating an alliance function is unlikely to have much impact on desired organizational outcomes

since it is by itself not a driver of alliance portfolio capital, and again focuses us back on

processes. However, we find that the relationships between proactiveness and alliance portfolio

26

capital and between relational orientation and alliance portfolio capital strengthen in the presence

of an alliance program. Therefore, there appears to be a synergistic relationship where proactive

alliance opportunity and relational oriented processes share a co-specialized relationship with an

institutionalized formalization of the function, where one builds on the other. On the other hand,

its negative moderating effect on the relationship between coordination process and alliance

portfolio capital is intriguing in that it suggests the following: although portfolio coordinating

activities serve to enhance alliance portfolio capital, the incremental value of investing in such

processes diminishes in the presence of a dedicated alliance function. One possible interpretation

of this finding is that coordination processes and formalization of the alliance function are

substitutable, with the former being the organizational routine equivalent of a structural

mechanism.

Our findings need to be interpreted in the context of the potential limitations inherent in

this research. Since our research is survey-based, the data is perceptual in nature. Yet this

perhaps is not so significant an issue, especially in the light of findings of a high correlation

between subjective and objective measures of performance in research on joint ventures and

alliances (Geringer and Hebert, 1991; Kale et al., 2002). Besides, since our data is cross-

sectional in nature and was collected at one point in time, no inferences of causality can be

conclusively established, nor can we discount the possibility of reverse causality. Also,

formation and management processes typically occur at different stages of the life-cycle of an

alliance network, thus raising the question whether there is a multi-stage sequence wherein

process leads to structure, which in turn triggers off processes, and so on. For both these

concerns, a longitudinal design, cross-validation of findings, and additional sources of data

would enable us to further assess the causality of the hypothesized relationships. A related issue

27

is that of common method variance. While we have taken ample steps to reduce the concern that

this may be a problem, more elaborate research designs could have assuaged such concerns.

In summary, we note that there is little formalization of a framework that links

organizational processes to alliance portfolio capital derived from a firm’s network of alliance

relationships. Our research is a step forward in this direction.

28

Ta

ble

1

Pro

cess

Dim

ensi

on

s

Org

an

iza

tio

na

l P

roce

ssD

efin

itio

nS

ou

rce

of

Str

ate

gic

Ad

va

nta

ge

Pa

rtn

erin

g P

roa

ctiv

enes

s A

n o

rgan

izat

ion

’s e

ntr

epre

neu

rial

eff

ort

s to

d

isco

ver

an

d a

ct o

n n

ew a

llia

nce

op

po

rtu

nit

ies.

Fir

st-m

ov

er a

dv

anta

ges

in

im

per

fect

fac

tor

mar

ket

fo

r p

artn

ers

Rel

ati

on

al

Ori

enta

tio

nA

n o

rgan

izat

ion

’s e

ng

agem

ent

in a

ctiv

itie

s fo

r th

e d

evel

op

men

t o

f in

form

al s

elf-

enfo

rcin

g

safe

gu

ard

s in

th

eir

coll

abo

rati

ve

rela

tio

nsh

ips.

Lo

wer

ing

co

ntr

acti

ng

an

d m

on

ito

rin

g c

ost

s an

d

incr

easi

ng

in

cen

tiv

es f

or

val

ue-

crea

tin

g

init

iati

ves

by

all

ian

ce p

artn

ers

Po

rtfo

lio

Co

ord

ina

tio

nA

n o

rgan

izat

ion

’s e

ng

agem

ent

in i

nte

gra

tin

g

and

sy

nch

ron

izin

g a

ctiv

itie

s ac

ross

th

eir

alli

ance

s

Incr

easi

ng

kn

ow

led

ge

flo

ws

and

bro

ker

ing

in

form

atio

n a

cro

ss t

he

port

foli

o o

f al

lian

ces

29

TABLE 2

Scales and Confirmatory Factor Analysis

Factors and Items Standardized

Loadings **

Composite

Reliability1

Avg

Variance

Extracted2

1. Alliance Proactiveness

We actively monitor our environment to identify partnering

opportunities.0.815

We routinely gather information about prospective partners

from various forums (e.g. trade shows, industry conventions,

databases, publications, internet etc.)

0.817

We are alert to market developments that create potential

alliance opportunities.0.827

We strive to preempt our competition by entering into alliances

with key firms before they can0.646

We often take the initiative in approaching firms with allianceproposals.

0.674

0.87 0.58

2. Relational Orientation

Staying together during adversity/challenge is very important

in our relationships.0.658

We endeavor to build relationships based on mutual trust and

commitment.0.722

We strive to be flexible and accommodate partners when

problems/needs arise. 0.741

When disagreements arise in our alliances, we usually reassess

facts to try and reach a mutually satisfactory compromise.0.606

0.78 0.47

Information exchange with partners takes place frequently andinformally, and not only according to pre-specified agreements*

3. Alliance Portfolio Coordination

We consider our alliances as a portfolio that requires overall

coordination, and not as independent, one-off arrangements.0.577

Our activities across different alliances are well coordinated. 0.887

We systematically coordinate our strategies across different

alliances0.837

We have processes to systematically transfer knowledge across

alliance partners.0.596

0.82 0.55

Managers from different departments meet periodically to

examine how we can create synergies across our alliances*

4. Alliance Portfolio Capital

Your organization’s reputation in the market as a ‘partner ofchoice’.

0.693

The competitive strength of your alliance network. 0.834

Strength of the relationships with alliance partners 0.681

0.78 0.55

Model Fit: Chi Square ( 2) = 108.761, df = 96, CFI = 0.99, GFI = 0.95, RMSEA = 0.024* Items dropped from the scale** All loadings significant at 0.01 levels1 Internal consistency = (( yi)

2 / (( yi)2 + var( i)) where var( i) = 1 - yi

2

1Average Variance Extracted = yi2 / yi

2 + var( i) where var( i) = 1 - yi2

30

Ta

ble

3

Mea

ns,

Sta

nd

ard

Dev

iati

on

s an

d C

orr

elati

on

s

Co

rrel

ati

on

s

Mea

nS

.D.

12

34

56

78

910

1. P

artn

erin

g P

roac

tiv

enes

s3

.62

.84

1.0

0

2. R

elat

ional

Go

ver

nan

ce

4.1

7.5

5.4

3*

**

1.0

0

3. P

ort

foli

o C

oord

inat

ion

2.6

3.8

4.4

4*

**

.33

**

*1

.00

4.

All

iance

Po

rtfo

lio

Cap

ital

3.6

7.7

0.4

8*

**

.36

**

*.3

8*

**

1.0

0

5.

Fir

m M

ark

et P

erfo

rman

ce3

.40

.69

.24

**

*.2

3*

**

.17

*.3

8*

**

1.0

0

6.

All

iance

Fu

nct

ion

-

-.2

9*

**

.26

**

*.2

9*

*.0

7.0

31

.00

7.

Fir

m S

ize

19

.01

1.9

1.0

7-.

01

.06

.05

.03

.13

+1

.00

8.

Ind

ust

ry R

esou

rce

Mu

nif

icen

ce3

.31

.74

.25

**

*.1

6*

.20

**

.23

**

* .

20

**

.1

8*

*.0

41

.00

9.

All

iance

Ex

per

ien

ce1

.88

1.1

0.3

7*

**

.21

**

*.2

3*

*.2

0*

*.1

2+

.20

**

.31

**

*.1

8*

*1

.00

10

. A

llia

nce

Div

ersi

ty0

.41

0.2

60

.02

.07

-.0

2-.

01

.11

+.0

2.1

3+

.11

.12

+1

.00

+p

< .

10

; *

p <

.0

5;

**

p <

.01

; *

**

p <

.0

01

31

Table 4

Hierarchical Moderator Regression Results for Alliance Portfolio Capital

MODEL 1 MODEL 2

Firm Size .01(0.07)

-.01(-0.13)

Alliance Experience -.02(-0.30)

.01(0.02)

Alliance Diversity -.06(-0.98)

-.07(-1.11)

Industry Resource Munificence .11(1.68)+

.08(1.35)

Partnering Proactiveness .29(3.98)***

.13(1.32)

Relational Orientation .15(2.28)*

.06(0.63)

Portfolio Coordination .18(2.71)**

.33(3.06)**

Alliance Function -.04(-0.59)

Proactiveness X Alliance Function .23(2.46)*

Relational Orientation X Alliance Function .16(1.71)+

Coordination X Alliance Function -.19(-1.81)+

F-Value 10.72*** 8.35***Adjusted R2 0.24 0.28

F-Value 3.34*

R2 0.04

Numbers in parentheses are t-values All significance levels are based on two-tailed tests.The interaction terms were calculated by first standardizing the constituent parts and then multiplying the standardized variables

+p < .10 ; * p < .05; ** p < .01; ***p < .001

32

Table 5

Subgroup Analysis for the Moderating Role of Alliance Function

Dependent Variable = Alliance Portfolio Capital

Group1

Without Alliance Function

Group 2

With Alliance Function

Firm Size -.01(-0.13)

.02(0.29)

Alliance Experience -.08(-0.74)

.06(0.72)

Alliance Diversity -.08(-0.86)

-.02(-0.25)

Industry Resource Munificence .20(2.20)*

.05(0.61)

Partnering Proactiveness .23(1.96)*

.40(4.86)***

Relational Orientation .09(0.90)

.26(3.21)**

Portfolio Coordination .36(3.48)***

.12(1.35)

F-Value 5.73*** 9.96***Adjusted R2 0.27 0.34

Numbers in parentheses are t-values All significance levels are based on two-tailed tests.The interaction terms were calculated by first standardizing the constituent parts and then multiplying the standardized variables

+p < .10 ; * p < .05; ** p < .01; ***p < .001

33

Table 6

Hierarchical Regression Results for Firm Market Performance

MODEL 1 MODEL 2

Firm Size .06(0.77)

.06(0.84)

Alliance Experience -.03(-0.35)

-.03(-0.37)

Alliance Diversity .07(0.94)

.09(1.30)

Industry Resource Munificence .13(1.82)+

.10(1.48)

Partnering Proactiveness .01(0.02)

-.04(-0.40)

Relational Orientation .17(1.58)

.15(1.46)

Portfolio Coordination .06(0.46)

-.05(-0.41)

Alliance Function .09(1.18)

0.10(1.40)

Proactiveness X Alliance Function .17(1.62)

.10(0.95)

Relational Orientation X Alliance Function -.05(-0.48)

-.10(-0.99)

Coordination X Alliance Function -.07(-0.60)

-.01(-0.09)

Alliance Portfolio Capital .32(4.14)***

F-Value 2.28* 3.68***Adjusted R2 0.06 0.13

F-Value 17.11***

R2 0.07

Numbers in parentheses are t-values All significance levels are based on two-tailed tests.The interaction terms were calculated by first standardizing the constituent parts and then multiplying the standardized variables

+p < .10 ; * p < .05; ** p < .01; ***p < .001

34

References

Achrol RS, Kotler P. 1999. Marketing in the network economy. Journal of Marketing 63(SpecialIssue): 146-63.

Alliance Analyst. 1998. Measuring alliance performance. August 1998. NewCap Communications: Philadelphia, PA.

Anand BN, Khanna T. 2000. Do firms learn to create value? The case of alliances. Strategic

Management Journal 21(Special Issue): 295-315.

Anderson JC, Hakansson H, Johanson J. 1994. Dyadic business relationships within a business network context. Journal of Marketing 58(4): 1-16.

Argote L. 1999. Organizational Learning: Creating, Retaining and Transferring Knowledge.Kluwer Academic Publishers: Boston, MA.

Armstrong JS, Overton TS. 1977. Estimating nonresponse bias in mail surveys. Journal of

Marketing Research 14(3): 396-402.

Aulakh PS, Kotabe M. 1997. Antecedents and performance implications of channel integration in foreign markets. Journal of International Business Studies 28(1): 145-175.

Bamford J, Ernst D. 2002. Managing an alliance portfolio. The McKinsey Quarterly 3: 29-39.

Benjamin BA, Podolny JM. 1999. Status, quality, and social order in the California wineindustry. Administrative Science Quarterly 44(3): 563-89.

Blyler M, Coff RW. 2003. Dynamic capabilities, social capital, and rent appropriation: Ties thatsplit pies. Strategic Management Journal 24: 677-686.

Burt RS. 1992. Structural holes: The social structure of competition. Harvard University Press: Boston, MA

Dess G, Robinson RB Jr. 1984. Measuring organizational performance in the absence of objective measures: The Case of the privately-held firm and conglomerate business unit. Strategic Management Journal 5(3): 265-273.

DeVellis RF. 1991. Scale development: Theory and applications. Sage: Newbury Park, CA.

Dyer JH, Singh H. 1998. The Relational view: Cooperative strategy and sources of interorganizational competitive advantage. Academy of Management Review 23(4): 660-79.

Dyer JH, Nobeoka K. 2000. Creating and managing a high-performance knowledge-sharing network: The Toyota case. Strategic Management Journal 21(3): 345-367.

35

Eisenhardt KM, Martin JA. 2000. Dynamic capabilities: what are they? Strategic Management

Journal 21(10-11): 1105-1121.

Fornell C, Larcker DF. 1981. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. Journal of Marketing Research 18(February): 39-50.

Geringer JM. 1988. Selection of partners for international joint ventures. Business Quarterly

53(2): 31-37.

Geringer JM, Hebert L. 1991. Measuring Performance of International Joint Ventures. Journal of

International Business Studies 2: 249-263.

Gomes-Casseres B. 1996. The Alliance revolution: The new shape of business rivalry. Harvard University Press: Cambridge, MA

Granovetter M. 1985. Economic action and social structure: The problem of embeddedness.American Journal of Sociology 91(3): 481-510.

Granovetter M. 1992. Networks and organizations: structure, form, and action. Harvard Business School Press: Boston, MA

Gulati R. 1998. Alliances and networks. Strategic Management Journal 19: 293-317.

Harbison JR, Pekar P Jr. 1998. Smart alliances: A practical guide to repeatable success. Josey-Bass: San Francisco, CA

Hargadon A, Sutton RI. 1997. Technology brokering and innovation in a product developmentfirm. Administrative Science Quarterly 42: 716-749.

Heide JB, John G. 1992. Do norms matter in marketing relationships? Journal of Marketing

56(2): 32-45.

Hill CWL. 1990. Cooperation, opportunities, and the invisible hand: Implication for transactioncost theory. Academy of Management Review 15(3): 500-13.

Huber GP, Power DJ. 1985. Retrospective reports of strategic-level managers: Guidelines for increasing their accuracy. Strategic Management Journal 6(2): 171-181.

Joreskog KG. 1971. Simultaneous factor analysis in several populations. Psychometrika 36: 409-426.

Judge WQ Jr, Douglas TJ. 1998. Performance implications of incorporating natural environmental issues into the strategic planning process: An empirical assessment. The

Journal of Management Studies 35(2): 241-262.

36

Kale P, Dyer JH, Singh H. 2002. Alliance capability, stock market response, and long-termalliance success: The role of the alliance function. Strategic Management Journal 23(8): 747-67.

Khanna T, Gulati R, Nohria N. 1994. Unilateral commitments and the importance of process inalliances. Sloan Management Review 35: 61-69.

Khanna T. 1998. The scope of alliances. Organization Science 9(3): 340-55.

Koka BR, Prescott JE. 2002. Strategic alliances as social capital: A multidimensional view.Strategic Management Journal 29(9): 795-816.

Madhok A. 2002. Reassessing the fundamentals and beyond: Ronald Coase, the transaction cost and resource-based theories of the firm and the institutional structure of production. Strategic

Management Journal 23(6): 535-550.

Madhok A, Tallman SB. 1998. Resources, transactions, and rents: Managing value throughinterfirm collaborative relationships. Organization Science 9(3): 326-339.

Parise S, Casher A. 2003. Alliance portfolios: Designing and managing your network of business-partner relationships. Academy of Management Executive 17(4): 25-39.

Parkhe A. 1993. Strategic alliance structuring: A game theory and transaction cost examinationof interfirm cooperation. Academy of Management Journal 36: 794-829.

Pettigrew AM, Thomas H, Whittington R. 2001. Strategic Management: The Strengths and Limitations of a field. In Handbook of strategy and management, Pettigrew AM, Thomas H, Whittington R. (Eds.). Sage: London; 3-30.

Podsakoff P, Organ D. 1986. Reports in organizational research: Problems and prospects. Journal of Management Studies 27: 305-327.

Poppo L, Zenger TR. 2002. Do Formal Contracts and Relational Governance Function as Substitutes or Complements? Strategic Management Journal 23(8).

Powell W. 1998. Learning from Collaboration: Knowledge and Networks in the Biotechnology and Pharmaceutical Industries. California Management Review 40(3): 228-240.

Powell W, Koput KW, Smith-Doerr L. 1996. Interorganizational collaboration and the locus of innovation: Networks of learning in biotechnology. Administrative Science Quarterly 41(1):116-45.

Ray G, Barney JB, Muhanna WA. 2004. Capabilities, business processes, and competitiveadvantage: Choosing the dependent variable in empirical tests of the resource-based view. Strategic Management Journal 25: 23-37.

37

Sarkar MB, Echambadi R, Harrison J. 2001. Alliance Entrepreneurship and Firm Market Performance. Strategic Management Journal 22(6/7): 701-711.

Simonin BL. 1997. The importance of collaborative know-how: An Empirical test of the learning organization. Academy of Management Journal 40(5): 1150-74.

Teece DJ, Pisano G, Shuen A. 1997. Dynamic capabilities and strategic management. Strategic

Management Journal 18: 509-33.

Tsai W, Ghoshal S. 1998. Social capital and value creation: The Role of interfirm networks. Academy of Management Journal 41(4): 359-374.

Williamson OE. 1985. The Economic Institutions of Capitalism. The Free Press: New York

Venkatraman N, Ramanujam V. 1986. Measurement of business performance in strategy research: A Comparison of approaches. The Academy Of Management

Review 11(4): 801-15.

Zajac EJ, Olsen CP. 1993. From transaction cost to transactional value analysis: Implications for the study of interorganizational strategies. The Journal of

Management Studies 30(1): 131-146.

38