Embed Size (px)

Citation preview

Analytical presentation of the

taxation system in Cyprus for the

purposes of the workshop

‘Market Value-Based Taxation of

Real Property: Lessons from

International Experience’.

Mar 17–21, 2014, Ljubljana, Slovenia

Market Value–Based Taxation of Real Property CYPRUS CASE

AUTHORS: VARNAVAS PASHOULIS & THOMAS DIMOPOULOS

1

CONTENTS

A. ANNUAL TAXES ON LAND & BUILDINGS (REAL PROPERTY) .................................................................. 2

1) Immovable property tax (Law 24/1980) ........................................................................................... 2

2) Municipal Rates (law 111/1985) ....................................................................................................... 4

3) Communal Rates (law 86(Ι)/1999) .................................................................................................... 5

4) Sewage Rate (Sewage Law 1971) ...................................................................................................... 6

5) Other property taxes (indirect) ......................................................................................................... 6

6) Proposals for Reform ........................................................................................................................ 7

B. REVENUE INFORMATION ...................................................................................................................... 8

C. TAX & VALUATION ADMINISTRATION .................................................................................................. 9

D. PRIVATISATION & PRIVATE OWNERSHIP OF PROPERTY ..................................................................... 12

E. DEVELOPMENT OF MARKET VALUE-BASED SYSTEM FOR TAXATION OF LAND AND/OR BUILDINGS 15

F. SPECIFIC QUESTIONS / ISSUES FOR DISCUSSION ................................................................................ 16

G. APPENDIX 1 (transactions record) ...................................................................................................... 17

2

A. ANNUAL TAXES ON LAND & BUILDINGS (REAL PROPERTY)

The main annual real property taxes enforced in Cyprus are the following:

1) Immovable Property Tax (Law 24/1980)

2) Municipal Rates - Municipalities Law (Law 111/1985)

3) Communal Rates – The Communal Law (Law 86(Ι)/1999)

4) Sewerage Rate - The Sewerage Law (1971)

5) Other property taxes

All of them are presented analytically below:

1) IMMOVABLE PROPERTY TAX (LAW 24/1980)

1.1 This tax is regulated by the law 24/1980. The objects of the tax are considered all

immovable properties as they defined under Section 2 of the Immovable Property Law (Tenure,

Registration and valuation), Cap. 224.

1.2 Objects subject to this tax are:

a) Land

b) Buildings and other erections, structures or fixtures affixed to any land or to any building

or other erection or structure;

c) Trees, vines, and any other thing whatsoever planted or growing upon any land and any

produce thereof before severance

d) Springs, wells, water and water rights whether held together with, or independently of,

any land

e) Privileges, liberties, easements and any other rights and advantages whatsoever

appertaining or reputed to appertain to any land or to any building or other erection or

structure;

f) An Undivided share in any property hereinbefore set out

g) Land which is created after the reclamation of the sea h) Sea area which is declared as marina for the purpose of creating a backfill for new land

1.3 The tax base is the Market Value as defined in Section 2 of the aforementioned law, and

is “the amount which the immovable property, if sold in the open market by a willing seller to a

willing buyer, might be expected to realize”.

3

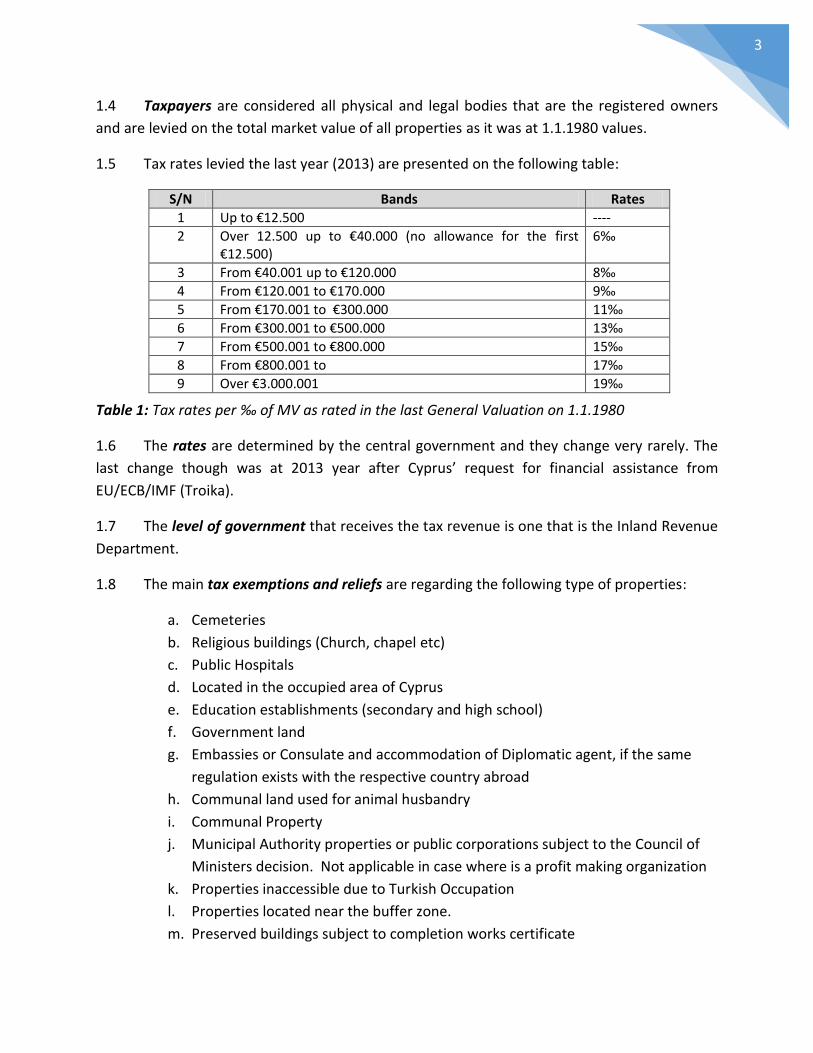

1.4 Taxpayers are considered all physical and legal bodies that are the registered owners

and are levied on the total market value of all properties as it was at 1.1.1980 values.

1.5 Tax rates levied the last year (2013) are presented on the following table:

S/N Bands Rates

1 Up to €12.500 ----

2 Over 12.500 up to €40.000 (no allowance for the first €12.500)

6‰

3 From €40.001 up to €120.000 8‰

4 From €120.001 to €170.000 9‰

5 From €170.001 to €300.000 11‰

6 From €300.001 to €500.000 13‰

7 From €500.001 to €800.000 15‰

8 From €800.001 to 17‰

9 Over €3.000.001 19‰

Table 1: Tax rates per ‰ of MV as rated in the last General Valuation on 1.1.1980

1.6 The rates are determined by the central government and they change very rarely. The

last change though was at 2013 year after Cyprus’ request for financial assistance from

EU/ECB/IMF (Troika).

1.7 The level of government that receives the tax revenue is one that is the Inland Revenue

Department.

1.8 The main tax exemptions and reliefs are regarding the following type of properties:

a. Cemeteries

b. Religious buildings (Church, chapel etc)

c. Public Hospitals

d. Located in the occupied area of Cyprus

e. Education establishments (secondary and high school)

f. Government land

g. Embassies or Consulate and accommodation of Diplomatic agent, if the same

regulation exists with the respective country abroad

h. Communal land used for animal husbandry

i. Communal Property

j. Municipal Authority properties or public corporations subject to the Council of

Ministers decision. Not applicable in case where is a profit making organization

k. Properties inaccessible due to Turkish Occupation

l. Properties located near the buffer zone.

m. Preserved buildings subject to completion works certificate

4

n. Agricultural properties, where owners are employed in the agricultural industry.

2) MUNICIPAL RATES (LAW 111/1985)

2.1 This tax is regulated by the Municipalities Law 111/1985. The objects of the tax are all

immovable properties as defined under Section 2 of the Immovable Property Law (Tenure,

Registration and valuation), Cap. 224. This has already being described in the previous property

tax (see 1.1 -1.4). The same applies for the tax base.

2.2 The annual rate is levied on each property that falls within the administrative

boundaries of a municipal authority of any owner or legal body and is based again on 1.1.1980

values. The current rate is flat at 1,5‰ and is fixed by law. The rate is rarely changed.

2.3 Revenue is received from the municipal authorities.

2.4 The main tax exemptions and reliefs are regarding the following type of properties:

a. Cemeteries

b. Religious buildings (Church, chapel etc)

c. Public Hospitals

d. Preserved buildings and archeological sites

e. Located in the occupied area of Cyprus

f. Education establishments (secondary and high school)

g. Charity organizations

h. Property owned by government and Municipal Authorities

i. Sports club and its related land activities

j. Communal land used for animal husbandry

k. Communal Property

2.5 The rate has to be paid by 30 June of every year.

5

3) COMMUNAL RATES (LAW 86(Ι)/1999)

3.1 This tax is regulated by the Communal 86(I)/1999. The objects of the tax are all

immovable properties as defined under Section 2 of the Immovable Property Law (Tenure,

Registration and valuation), Cap. 224. This has already being described in the previous property

tax (see 1.1 -1.4). The same applies for the tax base.

3.2 The annual rate is levied on each property that is within the administrative boundaries

of a communal authority of any owner or legal body and is also based on 1.1.1980 values. The

by-law maximum rate that can be imposed by the Communal Authority is 10‰, but is

commonly levied a rate of 1,5‰. The rate is rarely changed.

3.3 The rate is levied and collected by the Communal Authorities.

3.4 The main tax exemptions and reliefs are regarding the following type of properties:

a. Cemeteries

b. Religious buildings (Church, chapel etc)

c. Public Hospitals

d. Preserved buildings and archeological sites

e. Located in the occupied area of Cyprus

f. Education establishments (secondary and high school)

g. Charity organizations

h. Property owned by government and Municipal Authorities

i. Sports club and its related land activities

j. Communal land used for animal husbandry

k. Communal Property

3.5 The rate has to be paid by 30 June of every year.

6

4) SEWAGE RATE (SEWAGE LAW 1971)

4.1 This tax is regulated by the Sewerage Law 1/1971. The objects of the tax are all

immovable properties as defined under Section 2 of the Immovable Property Law (Tenure,

Registration and valuation), Cap. 224. This has already been described in the previous property

tax (see 1.1 -1.4). The same applies for the tax base.

4.2 This rate is levied on each property that is falling within the administrative boundaries of

a Sewerage Authority of any physical or legal body or occupier.

4.3 The rate is decided by each Sewerage Authority, levied and collected by them.

4.4 The rate is about 5‰ of Market Values based on 1.1.1980. However it may vary

depending on the property type (hotel, commercial etc).

4.5 The levy has to be paid by the end of October each year.

4.6 Additionally, an extra levy is charged based on the consumption of the water and not on

the market value of the property on 1.1.1980.

4.7 There are no exceptions to this levy, other than agricultural properties, where owners

are employed in the agricultural industry.

5) OTHER PROPERTY TAXES (INDIRECT)

5.1 There are further property taxes that are not imposed annually or recurrently. These are

indirect taxes presented below:

a) Transfer fees

b) Capital gains tax,

c) VAT on new developments.

5.2 A new law that is under evaluation regards a ‘planning improvement rate’ and is related

to the upgrading of planning zones.

7

6) PROPOSALS FOR REFORM

6.1 Under the Financial Memorandum of Understanding prepared by troika from Cyprus

and specifically under measure 3.9, the following provisions should be implemented as part of

the Immovable Property Tax Reform.

“implement by Q2-2015 the recommendations of a study on the scope for consolidating the

collection and administration of the municipal recurrent property tax and sewage tax. The study

will also review existing exemptions and derogations from property taxation. It will also report

on the scope for shifting revenues from transaction fees and taxes to recurrent taxation”

6.2 It should be noted that at this point in time the government is examining the

reorganization of the local government and therefore the immovable property reform will need

to take into consideration the final structure of the local government. Further, the reform will

need to take into consideration the new tax rates as the existing ones are based on 1980 prices

and the new level of tax revenue will have to be decided.

8

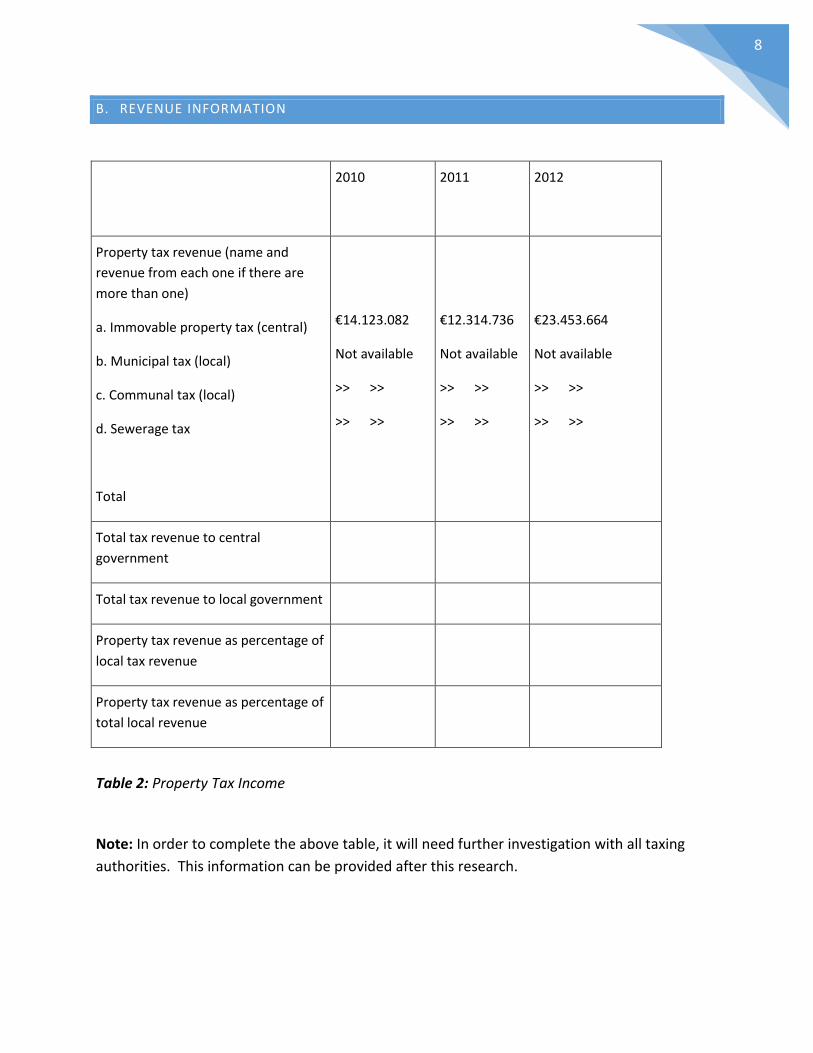

B. REVENUE INFORMATION

2010 2011 2012

Property tax revenue (name and

revenue from each one if there are

more than one)

a. Immovable property tax (central)

b. Municipal tax (local)

c. Communal tax (local)

d. Sewerage tax

Total

€14.123.082

Not available

>> >>

>> >>

€12.314.736

Not available

>> >>

>> >>

€23.453.664

Not available

>> >>

>> >>

Total tax revenue to central

government

Total tax revenue to local government

Property tax revenue as percentage of

local tax revenue

Property tax revenue as percentage of

total local revenue

Table 2: Property Tax Income

Note: In order to complete the above table, it will need further investigation with all taxing

authorities. This information can be provided after this research.

9

C. TAX & VALUATION ADMINISTRATION

7.1 The authorities that collect and maintain data on tax objects are the Department of

Lands and Surveys (DLS), the Inland Revenue Department (IRD), the Municipal and Communal

Authorities and the Sewerage Boards.

7.2 The taxpayer provides information as regards, its identification number and contact

address as well as any other proof for exemption purposes.

7.3 As regards the immovable property tax, the owner is obligated to declare all its

properties by the end of each September to the IRD, if the property has been altered for any

reason.

7.4 Furthermore, when a new general valuation is ordered by the Council of Ministers

(under Section 69 of Cap. 224, Section 70), the owners are obligated to provide information as

regards their property (plans, valuation reports) upon the request of the valuers

7.5 The DLS is the official government body that has the responsibility to maintain and

perform updated general valuations for the Republic. A CAMA system has been development

in the Department of Lands and Surveys so that the general valuations can be performed in an

automated way. The major components of this fiscal system are as follows:

i. Maintain a property file for all properties in Cyprus

ii. Maintain planning zones for the whole of Cyprus

iii. Maintain property restrictions

iv. Maintain a sales and rental information file

v. GIS tools are applied to support mass valuation procedures

10

7.6 Various Valuation Methods have been developed and are described below:

1. Base Models

Land Models

Base Residential/Commercial building site

Base Industrial building site

Base Undeveloped field

Base Agricultural/Livestock fields

Unit Models

Base Residential/Commercial

Base Hotels/Tourist Establishments

Base Schools/Hospitals/Clinics

Base Livestock Units

Other Models

Base Plantation/tree

Base borehole

2. Base Cost Models

Retail Cost model

Office Cost model

Industrial Cost model

3. Direct Sales Comparison Method

Direct Comparison Models

Direct Rental Comparison Method and Income Capitalization Method

Simple and Multiple Regression Analysis Models

11

7.7 The base models are the ones selected to perform the updated general valuation for the

country on 1.1.2013 values. The other methods will be considered in future updated valuations.

7.8 The tax collection system needs to be improved, bearing in mind that a taxpayer has to

pay each tax at a different taxing authority. Today, the majority of the payments can be made

through internet payment systems to the taxing authorities.

7.9 In all property tax legislations there is a provision that if the tax is not paid on time or

not paid at all, the taxpayer is liable to pay a fine. Additionally, the property can be noted in

the Land Registry records that there is a pending payment in taxes and therefore the property

cannot be transferred to another party without first getting a clearance from all taxes.

7.10 The process of estimating the parameter values at this stage is done manually, however

the next step is to use MRA for this analysis. The process of mass valuation is automated after

the parameter values are determined and imported into the CAMA system. GIS is also used in

the process of defining location areas as well as for assisting the valuers to visualize sales and

other property information. Further, GIS applications will assist the valuers in conducting

quality assurance checks (ratio studies).

7.11 The DLS will publish an electronic catalogue of all properties and their respective values

that fall under specific geographical area in all municipalities and communal authorities. The

taxpayers are free to request a report of all the properties and values under their name. The

DLS is obliged to make an announcement in the official gazette of the Republic and to inform

the public through press publications. Furthermore, the taxpayer will have the capability to

extract the aforementioned information through the website of the DLS.

7.12 The taxpayer can object for the tax amount to the IRD and for the general valuation of

his/her property to the Valuation Authority, which is the DLS. If no agreement is reached

between the parties, the owner or the Valuation Authority can apply to the court for the

determination of the final assessment of the property (section 70 or 71 of Cap. 224). There is a

small fee that has to be paid before the objection is lodged at the DLS, by the owner.

12

D. PRIVATISATION & PRIVATE OWNERSHIP OF PROPERTY

8.1 All properties in Cyprus that do not fall within the following categories can be privately

owned:

a) Vakf properties (Religious property administration)

b) Communal property

c) Government land

8.2 All properties in Cyprus (including those located at the occupied part which is

inaccessible due to the Turkish invasion in 1974) are registered or recorded in the District Lands

Office. The total number of registrations on the free government side is about 1.2 million. The

total number of units are estimated to be about 0,5 million. At this stage the information as

regards the privately owned land has to be extracted from the LIS.

8.3 Residential and tourist houses are the most frequently properties sold and rented in the

open market.

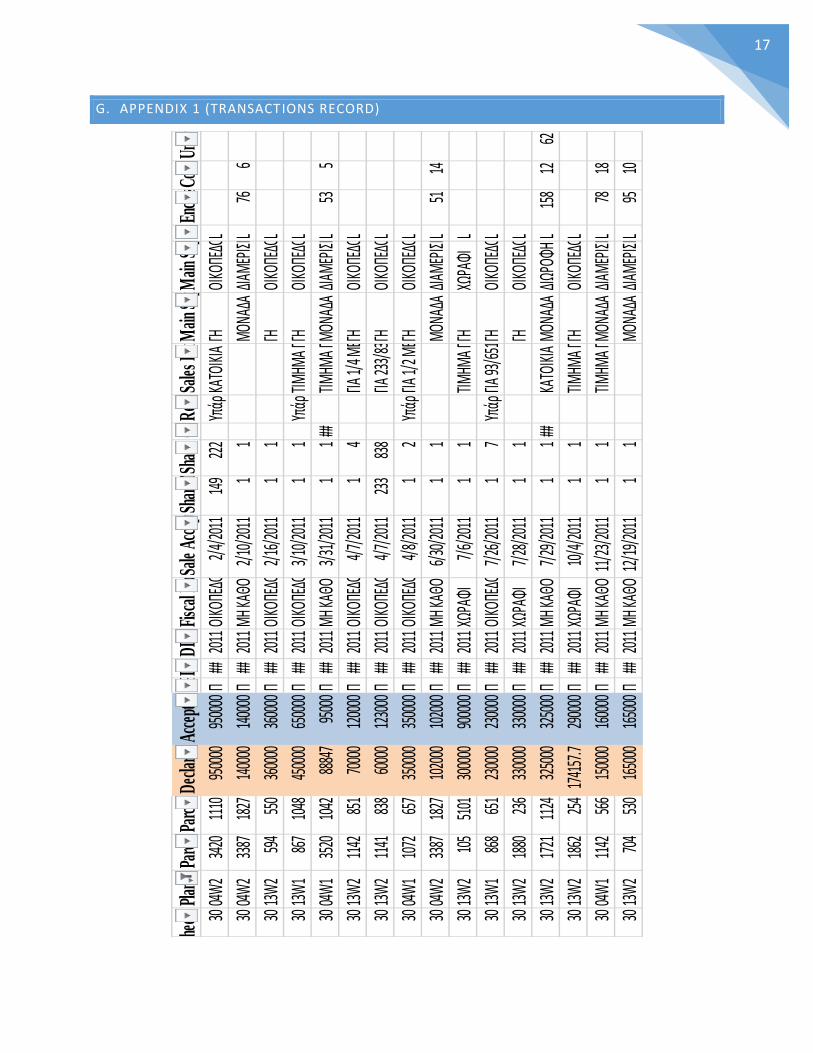

8.4 The sale transactions are recorded in the DLS and under Cap. 219 (Fees and charges).

The Department is estimating the market value of every property for the purpose of receiving

transfer fees. The reliability of sales depends on whether the seller/buyer declared the true

value of the transaction. In Cyprus, the transfer fees are considered high, beginning from 3% up

to the first €85.430, 5% for the next €85.430 and 8% for the value over €170.860.

8.5 For this reason, sellers/buyers tend to declare a rather smaller amount than the real

one. The greater the number of transactions in an area the closer the sale price is to the actual

market value. As noted before, the DLS execute its own market valuation (desktop valuation

using comparative evidence from past transactions) for the transaction and this is recorded

differently from the declared value of the seller/buyer (see appendix A).

8.6 The real estate market information can be gathered from various resources. The major

source of information as regards the certificate of registrations, the ownership as well as the

availability of cadastral maps is from the DLS. Additionally, the DLS provides an electronic

13

format of all planning zones in Cyprus in cooperation with the Town Planning Department.

Sales information is only available to certified valuers who pay an annual subscription in order

to get the recorded sales (declared & accepted price) on a quarterly basis. Also, the DLS in its

website provides a free service to the citizens in identifying any of their property with the basic

information, including electronic cadastre plan and google map identification (see

http://parcel.dls.moi.gov.cy/search/default.aspx).

8.7 Market information currently collected and analysed for use in taxation is also used for

other public valuation purposes as described below:

a) Compulsory purchase and compensation purposes and appearance in the Court as

expert witness.

b) Assist the Rent control Court in the determination of market values

c) Assist an advisory committee under the Ministry of Finance that is dealing with the

agreement of new tenancies (relocating or negotiating rent reviews) in order to

accommodate government departments.

d) Assist the Social Insurance Department of the purpose of granting special subsides in

relation to the property ownership.

e) Valuations for the purpose of granting, leasing or exchanging government land

f) Provide valuation services to other government departments

g) Provide quality assurance umbrella of property valuations that are requested by the

semi government organizations and implemented by the private sector valuers.

h) Provide valuations on behalf of the government for the purpose of the European Court

of Human Rights, in cases where Cypriots have claimed compensation for the illegal use

or for interfering in the right of enjoyment of their properties, by Turkey

i) Availability of market data to private valuers

j) Producing housing indices by the Central Bank and Statistics Department

k) Assisting the Town Planning Department in the preparation of updated local plans as

well as in supporting new land policies.

14

l) Assisting the Energy Department and the Town Planning Department in estimating the

level of incentives (additional building density) in case of photovoltaic installation in

buildings.

8.8 One of the major issues that the government is determined to encourage real estate

market development is to speed up the issuance of certificates of registration (title deeds). In

order to achieve this, the planning authorities have a major role to play and especially the

issuance of the certificate of final approval of any development. Additionally, the government

has introduced a new legislation as regards the process of issuance of the certificate of

registration.

8.9 Furthermore, the existing Specific Performance Law has been improved so as to provide

additional protection to the buyer and is guaranteed upon the full payment of the price that a

certificate of registration will be issued under his/her name. In addition, the revised law on the

issuance of certificates of registration provides for additional powers to enforce the owners in

proceeding with the application to obtain certificates of approval of their development and

thereafter to lodge an application to the DLS for the issuance of an up today certificate of

registration.

8.10 Moreover, the government is in the process of introducing a new legislation regarding

the financial instrument of leasing and an updated legislation on forced sales.

8.11 From the planning perspective, the Town Planning Authority is making efforts to

introduce new land policies that would promote sustainable development and support

economic activity on the island (e.g. extraction of natural gas) on the island, while at the same

time safeguarding protected areas of nature beauty. A further action is to improve the existing

system of development control.

15

E. DEVELOPMENT OF MARKET VALUE-BASED SYSTEM FOR TAXATION OF LAND AND/OR

BUILDINGS

If your country plans to use market values as a basis for the property tax (or already uses them),

please describe:

9.1 The DLS currently uses the legal framework of market value based approach, with some

limitations faced due to the financial crisis that the island is experiencing. The greatest

challenge to implementing a value-based taxation system is the quality of the appraisals. This is

based on the quality and the availability of the data. It is believed that the market value based

system for land and building is the most fair and equitable to the taxpayers.

9.2 The proposals to reform the tax system should focus on the following principles:

a) Fair and equitable and should be based on the ability to pay (PAE)

b) The property tax should be neutral

c) Low cost operation and easy to administer

d) The tax should be specific, simple and the time that is becoming payable

e) It should be used as a fiscal instrument to promote sustainability and investment activity

on the island

f) The taxation system should be flexible and should be easily realigned to meet the

socioeconomic needs of the society.

g) Tax reliefs and exceptions should be focused and should promote incentives and

disincentives where this is appropriate to improve the property market efficiency.

h) Take full advantage of the all the available technology and systems for the best interest

of the public.

i) The tax system should be transparent and the public be kept informed of his rights and

obligations.

16

F. SPECIFIC QUESTIONS / ISSUES FOR DISCUSSION

1) How other countries deal with leasehold interests or even subleases that are

registered and hold a title in respect to the market value and tax burden.

2) Are there any special land or valuation tribunals established that deal specifically

with general valuation cases? If yes, what is the structure of such Court?

3) Within the current (existing) legislation, is there a proviso that would allow the

valuation authority to correct omissions/mistakes even after the deadline of

objections has been expired?

4) Any good practices regarding the objection procedure; Does the taxpayer pays for

the right to object; if yes, how the level of fees are charged;

5) Any bad practices that a country could avoid in doing so.

6) Are there any practices adopted where the tax payer declaring its own property

characteristics?

7) If a property is in co-ownership, how the market value for general valuation

purposes is shared. Is there a problem with undivided shares in property who pays

and how much is paid? What is the obligation of each co-owner or all?

8) Is there any methodology adopted in verifying (estimating) ‘true’ market value of

sale transactions?

9) Are there any indices (public or private) and how (if) they are involved in the

taxation procedure

10) Equity / Fairness / Cost. How these major factors are measured on different

practices.

11) Public relations and media campaigns before, during and after updated general

valuations.

17

G. APPENDIX 1 (TRANSACTIONS RECORD)

Shee

t:Pl

an:

Parc

el No

:Pa

rcel

Exte

nt:

Decla

red P

rice:

Acce

pted

Pric

e:DL

O Fi

le:DLO

File

No.:

DLO

File

Year

:Fi

scal

Prop

erty

Typ

e:Sa

le Ac

cept

ance

Dat

e:Sh

are N

umer

ator

: Sh

are D

enom

inato

r:CO

S Ag

reem

ent D

ate:

Rema

rk:

Sales

Rem

ark:

Main

Sbp

Cat

.:M

ain S

bp. K

ind:

Stat

us:

Enclo

sed E

xt.:

Cove

red E

xt.:

Unco

vere

d Ext

.:

3004

W2

3420

1110

9500

0095

0000

Π##

2011

ΟΙΚΟ

ΠΕΔΟ

2/4/

2011

149

222

Υπάρ

χουν

κτίρι

α που

δεν α

ναφέ

ροντ

αι στ

ην εγ

γραφ

ήΚΑ

ΤΟΙΚΙ

Α 300

ΤΜ. Γ

ΙΑ 14

9/22

2 ΜΕΡ

. ΓΗΣ

ΚΑΙ Κ

ΤΙΡΙΑ

ΓΗΟΙ

ΚΟΠΕ

ΔΟL

3004

W2

3387

1827

1400

0014

0000

Π##

2011

ΜΗ ΚΑ

ΘΟΡΙΣ

ΜΕΝΟ

Σ2/

10/2

011

11

ΜΟΝΑ

ΔΑΔΙΑ

ΜΕΡΙΣ

ΜΑL76

6

3013

W2

594

550

3600

0036

0000

Π##

2011

ΟΙΚΟ

ΠΕΔΟ

2/16

/201

11

1ΓΗ

ΟΙΚΟ

ΠΕΔΟ

L

3013

W1

867

1048

4500

0065

0000

Π##

2011

ΟΙΚΟ

ΠΕΔΟ

3/10

/201

11

1Υπ

άρχο

υν κτ

ίρια π

ου δε

ν ανα

φέρο

νται

στην

εγγρ

αφή

ΤΙΜΗΜ

Α ΠΩΛ

ΗΣΗΣ

4500

00 ΕΥ

ΡΩΓΗ

ΟΙΚΟ

ΠΕΔΟ

L

3004

W1

3520

1042

8884

795

000Π

##20

11ΜΗ

ΚΑΘΟ

ΡΙΣΜΕ

ΝΟΣ

3/31

/201

11

1##

ΤΙΜΗΜ

Α ΠΩΛ

ΗΣΗΣ

8884

7 ΕΥΡ

ΩΜΟ

ΝΑΔΑ

ΔΙΑΜΕ

ΡΙΣΜΑL

535

3013

W2

1142

851

7000

012

0000

Π##

2011

ΟΙΚΟ

ΠΕΔΟ

4/7/

2011

14

ΓΙΑ 1/

4 ΜΕΡ

. ΤΙΜ

ΗΜΑ Π

ΩΛΗΣ

ΗΣ 70

000 Ε

ΥΡΩ

ΓΗΟΙ

ΚΟΠΕ

ΔΟL

3013

W2

1141

838

6000

012

3000

Π##

2011

ΟΙΚΟ

ΠΕΔΟ

4/7/

2011

233

838

ΓΙΑ 23

3/83

8 ΜΕΡ

. ΓΗΣ

ΓΗΟΙ

ΚΟΠΕ

ΔΟL

3004

W1

1072

657

3500

0035

0000

Π##

2011

ΟΙΚΟ

ΠΕΔΟ

4/8/

2011

12

Υπάρ

χουν

κτίρι

α που

δεν α

ναφέ

ροντ

αι στ

ην εγ

γραφ

ήΓΙΑ

1/2 Μ

ΕΡ. Γ

ΗΣ ΚΑ

Ι ΚΑΤ

ΟΙΚΙΑ

Σ, 18

0 ΤΜ.

ΓΗΟΙ

ΚΟΠΕ

ΔΟL

3004

W2

3387

1827

1020

0010

2000

Π##

2011

ΜΗ ΚΑ

ΘΟΡΙΣ

ΜΕΝΟ

Σ6/

30/2

011

11

ΜΟΝΑ

ΔΑΔΙΑ

ΜΕΡΙΣ

ΜΑL51

14

3013

W2

105

5101

3000

0090

0000

Π##

2011

ΧΩΡΑ

ΦΙ7/

6/20

111

1ΤΙΜ

ΗΜΑ Π

ΩΛΗΣ

ΗΣ 30

0000

ΕΥΡΩ

ΓΗΧΩ

ΡΑΦΙ

L

3013

W1

868

651

2300

0023

0000

Π##

2011

ΟΙΚΟ

ΠΕΔΟ

7/26

/201

11

7Υπ

άρχο

υν κτ

ίρια π

ου δε

ν ανα

φέρο

νται

στην

εγγρ

αφή

ΓΙΑ 93

/651

ΜΕΡ

. ΓΗΣ

ΚΑΙ Δ

ΙΑΜΕ

Ρ. 72

ΤΜ.

ΓΗΟΙ

ΚΟΠΕ

ΔΟL

3013

W2

1880

236

3300

0033

0000

Π##

2011

ΧΩΡΑ

ΦΙ7/

28/2

011

11

ΓΗΟΙ

ΚΟΠΕ

ΔΟL

3013

W2

1721

1124

3250

0032

5000

Π##

2011

ΜΗ ΚΑ

ΘΟΡΙΣ

ΜΕΝΟ

Σ7/

29/2

011

11

##ΚΑ

ΤΟΙΚΙ

Α 178

ΤΜ.

ΜΟΝΑ

ΔΑΔΙΩ

ΡΟΦΗ

ΚΑΤΟ

ΙΚΙΑ

L15

812

62

3013

W2

1862

254

1741

57.7

2900

00Π

##20

11ΧΩ

ΡΑΦΙ

10/4

/201

11

1ΤΙΜ

ΗΜΑ Π

ΩΛΗΣ

ΗΣ ^1

7415

7,74

. ΟΙΚΙ

Α 160

ΤΜΓΗ

ΟΙΚΟ

ΠΕΔΟ

L

3004

W1

1142

566

1500

0016

0000

Π##

2011

ΜΗ ΚΑ

ΘΟΡΙΣ

ΜΕΝΟ

Σ11

/23/

2011

11

ΤΙΜΗΜ

Α ΠΩΛ

ΗΣΗΣ

1500

00 ΕΥ

ΡΩΜΟ

ΝΑΔΑ

ΔΙΑΜΕ

ΡΙΣΜΑL

7818

3013

W2

704

530

1650

0016

5000

Π##

2011

ΜΗ ΚΑ

ΘΟΡΙΣ

ΜΕΝΟ

Σ12

/19/

2011

11

ΜΟΝΑ

ΔΑΔΙΑ

ΜΕΡΙΣ

ΜΑL95

10