Embed Size (px)

Citation preview

A Drive for Consolidation and Building Core CompetenciesA study on how an Indian Conglomerate andthe Retail and Telecom Sector consolidated and built competencies

5/15/2013PGPM912 ACAD GRP 8 DIV ADEEP DEY AJIT MISHRA EDWARD MARTIS ASHWIN LALCHANDANI ADIT PAUL DEBNATH ROYCHOWDHURY

Table of ContentsReport Objective...................................................3Core Competency – A definition.....................................3

The Tata Group Post Liberalization – A quantum leap................4Consolidation....................................................4

Globalization and Acquisition Strategy...........................5Brand Management.................................................6

Evolution of the Tata Group post liberalisation..................7The Indian Telecommunication Sector...............................10

Drivers for Consolidation in Indian Telecom Sector..............11How Consolidation can complement Core-Competencies?.............12

Mergers and Acquisitions........................................13Regulatory Changes..............................................14

Recent Developments.............................................15Introduction to Indian Retail.....................................16

Strategies for Core Competence and Competitive Advantage........16Challenges......................................................17

Product Differentiation – Key to success........................18Specialty Retailing.............................................18

Signs of Consolidation in the Retail industry in India..........19Conclusion........................................................19

1

Report Objective

Indian Conglomerates have evolved from being local giants in thedays of the License Raj to internationally recognized global brands.At the same time, the core industrial sectors such as Telecom andRetail have also evolved in parallel from being a closed sectorapprehensive of growth to a more globally integrated market.

The objective of this report is to explore one of the underlyingthemes – drive for consolidation and building of core competencies,responsible for this remarkable transformation against the backdropof the following:

Evolution of the Tata Group Evolution of the Indian Telecom sector Evolution of the Indian Retail sector

Core Competency – A definition

A core competency is something that a firm can do well and thatmeets the following three conditions specified by Hamel and Prahlad(1990):

It provides customer benefits

2

It is hard for competitors to imitate It can be leveraged widely to many products and markets.

A core competency can take various forms, includingtechnical/subject matter know how, a reliable process, and/or closerelationships with customers and suppliers (Mascarenhas et al.1998). It may also include product development or culture such asemployee dedication. Modern business theories suggest that mostactivities that are not part of a company's core competency shouldbe outsourced.

If a core competency yields a long term advantage to the company, itis said to be a sustainable competitive advantage.

A competitive advantage exists when the firm is able to deliver thesame benefits as competitors but at a lower cost (cost advantage),or deliver benefits that exceed those of competing products(differentiation advantage). Thus, a competitive advantage enablesthe firm to create superior value for its customers and superiorprofits for itself.

The Tata Group Post Liberalization – A quantum leap

The Tata Group has, over the past decade-and-a-half, changed morethan ever before in its long and illustrious history. Rejuvenating

3

existing businesses, entering new ones, manufacturing breakthroughproducts and expanding into foreign markets are among theinitiatives the Group has undertaken with vigor during this period.

It all started in 1991 when post liberalisation taking the newly-opened economy into account, the Tata group shifted its focus totechnology-driven leadership, global competitiveness and being amongthe top three domestically, regardless of the line of business.Liberalization was both an opportunity and a threat. It was anopportunity because it set Tata free: the economy had been sotightly regulated that you could be fined or even imprisoned forexceeding your output quotas. It was a threat because Tata wasvulnerable

That meant rationalising the Tata business structure. The remnantsof the era of government controls combined with independentfunctioning of group companies in past decades could be seen in theway the group had grown till then -- unstructured, with overlappingbusiness across multiple companies.When Ratan Tata took over, there were three group companiesmanufacturing cement; five were involved in pharmaceuticals, whilenine companies operated in the IT space. One of his first acts wasto sell Tomco; swift exits from pharma and textiles and, later,cement, followed. Management consultancy McKinsey was brought onboard to help with the reorganisation.Mr. Tata set aboutstreamlining with a vengeance. He focused the group on sixindustries that have provided most of its revenues since 2000—steel,motor vehicles, power, telecoms, information technology (IT) andhotels—and increased its often paltry shareholding in these corebusinesses.

The Tata Group is still a diversified, salt-to-software group, butnow there is a method to the business expansion. It functions as acohesive unit; the consolidation of the Tata group postliberalization is explained in greater detail in the sections below.

Consolidation

In response to the challenges the Tata Group faced in the 1990s,Ratan Tata undertook a program of consolidation followed by anambitious global acquisition program. As a result, Tata Sons'gradually rebuilt its ownership stake in the core Tata companies,took greater control of the other Tata companies, and increased theTata Group’s revenues 40-fold from 1991 to 2009.

To achieve these goals, Ratan Tata implemented a three-partstrategy. First, he shook up the Tata Group's portfolio of

4

companies, announcing a goal that all Tata companies would be in thetop two or three in their respective industries. His attempts tosell companies he thought could not meet this standard met withresistance at first, but he succeeded in moving the Tata Group outof legacy industries like soap, textiles, and cement.

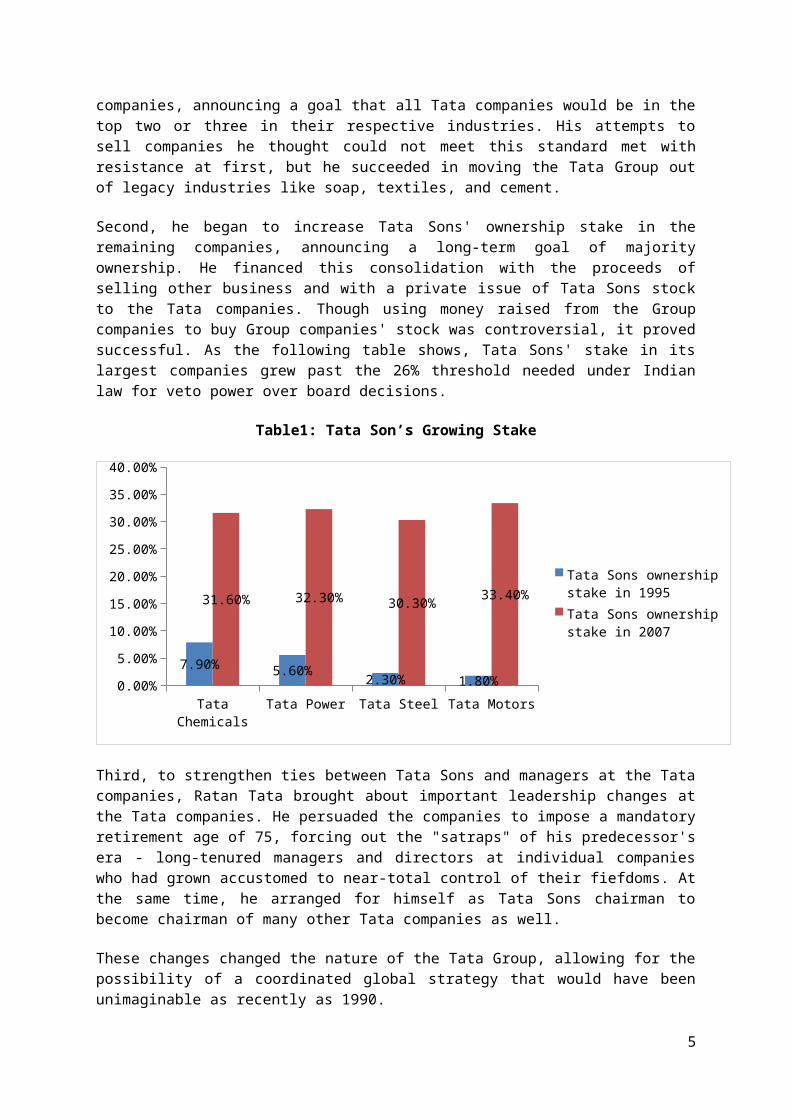

Second, he began to increase Tata Sons' ownership stake in theremaining companies, announcing a long-term goal of majorityownership. He financed this consolidation with the proceeds ofselling other business and with a private issue of Tata Sons stockto the Tata companies. Though using money raised from the Groupcompanies to buy Group companies' stock was controversial, it provedsuccessful. As the following table shows, Tata Sons' stake in itslargest companies grew past the 26% threshold needed under Indianlaw for veto power over board decisions.

Table1: Tata Son’s Growing Stake

Tata Chemicals

Tata Power Tata Steel Tata Motors0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

7.90% 5.60% 2.30% 1.80%

31.60% 32.30% 30.30% 33.40%Tata Sons ownership stake in 1995Tata Sons ownership stake in 2007

Third, to strengthen ties between Tata Sons and managers at the Tatacompanies, Ratan Tata brought about important leadership changes atthe Tata companies. He persuaded the companies to impose a mandatoryretirement age of 75, forcing out the "satraps" of his predecessor'sera - long-tenured managers and directors at individual companieswho had grown accustomed to near-total control of their fiefdoms. Atthe same time, he arranged for himself as Tata Sons chairman tobecome chairman of many other Tata companies as well.

These changes changed the nature of the Tata Group, allowing for thepossibility of a coordinated global strategy that would have beenunimaginable as recently as 1990.

5

Globalization and Acquisition Strategy

Though Ratan Tata aimed to reduce the number of Tata companies andthe number of industries they operated in, he did not intend theTata Group to shrink. Instead, the Group embarked on an ambitiousacquisition strategy both in India and internationally that helpedincrease its revenue forty-fold during Ratan Tata's tenure andincrease the footprint of the group globally. This strategy ofacquisition was made possible only due to liberalization.

In India, Tata Sons increased its investment in the communicationssector by buying a 47% share of government-owned telecommunicationsprovider VSNL (now Tata Communications) for $532 million in 2002,shortly after Tata Teleservices bought a majority stake in HughesTelecom for roughly $180 million. Tata Chemicals merged with HindLever Chemicals in 2004, and Trent (Tata Retail Enterprises) boughta majority share of Indian retailer Landmark in 2005.

Outside India, the Tatas' buying spree was much larger. In 2000, theEuropean press toke note when Tata Tea bought Tetley Teas, an oldand respected English brand. Since then, various Tata companies havebought such large and prominent firms as Korea's Daewoo CommercialVehicle Company; America's Tyco Global Network and Eight O’clockCoffee Company; and Britain's Jaguar Land Rover and Corus Steel.Boston's Ritz-Carlton became the Taj Boston. The total cost of theseacquisitions lay somewhere between $15 and $20 billion. The pace offoreign acquisitions grew dramatically: in 1995-2003 Tata companiesmade, on average, one purchase a year; in 2004 they made six; and in2005-06 more than 20. Today it earns about three-fifths of itsrevenue abroad and employs more British workers than any othermanufacturer, and two of its biggest companies, Tata Motors and TataCommunications, are listed on the New York Stock Exchange.

On the whole, the acquisition strategy was seen as a success. Someof the purchases were poorly timed, coming at the peak of the boommarket in 2005-2007, and with demand dropping during the recession,Tata Steel announced it would close a Corus steel plant and TataMotors petitioned the U.K. government for a bailout for Jaguar LandRover (which ultimately proved unnecessary). But by mid-2010 profitsfor both companies had rebounded--Jaguar Land Rover showed a 70%sales increase in a single year--and Tata Motors stock rose to arecord high.

6

Brand Management

The second prong of Ratan Tata's strategy to unify the Tata Groupand protect it from hostile capital consisted of building,controlling, and taking advantage of a unified Tata brand.

When Ratan Tata became chairman in 1991, the Tata Group had made noattempt to create and manage a single Tata brand. Some Tatacompanies bore the Tata name only as the first letter of theiracronym: in 1991, Tata Steel was known as TISCO (Tata Iron and SteelCompany), Tata Motors was TELCO (Tata Engineering and LocomotiveCompany), and the soap business Ratan Tata sold to Unilever bore thename TOMCO (Tata Oil Mills Company).

The new chairman pushed for more Group companies to use the Tataname and logo, but this greater association with Tata Sons would notbe costless. Tata Sons asserted its rights to the Tata brand andpersuaded the Tata companies to sign a "Brand Equity and BusinessPromotion Agreement." To use "Tata" in its name, each company wouldhave to pay Tata Sons 0.25% of total revenue, with a cap at 5% ofnet profit. Tata companies that did not use "Tata" in their nameswould pay a lesser fee of 0.15% or 0.1%. The proceeds were used toincrease Tata Sons' holdings in the other companies and to financeattempts to build brand equity.

In addition to paying the fee, the Tata companies contracted tofollow a lengthy code of conduct, addressing issues ranging fromcorporate purpose to conflicts of interest to whistleblowerprotection and an absolute prohibition on bribery.

Finally, in an arrangement some called a "brand pill" after thefamous "poison pill" takeover defense employed by American firms,the Tata brand agreement provided that in the event of a hostiletakeover, a company wrested from Tata control would no longer bepermitted to use the Tata name.

These efforts proved massively successful, taking advantage ofTata's already sterling reputation to build the most valuable brandin India and one of the 60 most valuable brands in the world. A 2010report by Brand Finance estimated the total worth of the Tata Brandat $11.2 billion.

Evolution of the Tata Group post liberalisation

1996

7

Tata Teleservices (TTSL) is established to spearhead thegroup's foray into the telecom sector

1998 Tata Indica — India's first indigenously designed and

manufactured car — is launched by Tata Motors, spearheadingthe group's entry into the passenger car segment

1999 The new Tata group corporate mark and logo are launched

2000 Tata Tea (now known as Tata Global Beverages) acquires the

Tetley group, UK. This is the first major acquisition of aninternational brand by an Indian business group

2001 Tata AIG — a joint venture between the Tata group and American

International Group Inc (AIG) — marks the Tata re-entry intoinsurance. (The group's insurance company, New IndiaAssurance, set up in 1919, was nationalised in 1956)

TCS consolidates market leadership through CMC acquisition

2002 Tata Sons acquires a controlling stake in VSNL (now known as

Tata Communications) India’s leading internationaltelecommunications service Provider

2003 Tata Consultancy Services (TCS) becomes the first Indian

software company to cross one billion dollars in revenues Tata Teleservices launches Tata Indicom mobile service

(consolidated with Tata DOCOMO in 2011) in Mumbai

2004 Tata Motors is listed on the world's largest bourse, the New

York Stock Exchange, the second group company to do so afterVSNL (now known as Tata Communications)

Tata Motors acquires the heavy vehicles unit of Daewoo Motors,South Korea

8

TCS goes public in July 2004 in the largest private sectorinitial public offering (IPO) in the Indian market, raisingnearly $1.2 billion

Indian Hotels unveils IndiOne (now known as Ginger hotels), afirst-of-its-kind chain of Smart Basics hotels

2005 Tata Steel acquires Singapore-based steel company NatSteel by

subscribing to 100 per cent equity of its subsidiary, NatSteelAsia

VSNL (now known as Tata Communications) acquired Tyco GlobalNetwork, making it one of the world's largest providers ofsubmarine cable bandwidth

Taj group takes over management of The Pierre, NY Taj group acquires a hotel run by Starwood, Sydney (now Blue) Tata Motors creates a new mini-truck segment in India with the

launch of Tata Ace Trent acquires strategic interest in Landmark chain of

bookstores

2006 Tata Sky satellite television service launched across the

country Taj group acquires the Ritz-Carlton, Boston (now known as Taj

Boston) Tata Chemicals acquires controlling stake in Brunner Mond

Group, UK (now known as Tata Chemicals Europe) Infiniti Retail launches Croma, India's first national chain

of multi brand outlets for consumer electronics and durableproducts

2007 Tata Steel acquires the Anglo-Dutch company Corus (now known

as Tata Steel Europe), making it the world's fifth-largeststeel producer

TCS inaugurates TCS China — a joint venture with the Chinesegovernment and other partners

The Taj group acquires Campton Place Hotel in San Francisco(now known as Taj Campton Place)

Tata Capital established as a new Tata company in thefinancial sector

9

2008 Tata Motors unveils Tata Nano, the People’s Car, at the 9th

Auto Expo in Delhi on January 10, 2008 Tata Motors acquires the Jaguar and Land Rover brands from the

Ford Motor Company Tata Chemicals acquires General Chemical Industrial Products

Inc (now known as Tata Chemicals North America)

2009 Tata Motors announces commercial launch of the Tata Nano;

delivers first Tata Nano in the country in Mumbai Tata Teleservices announces pan-India GSM service with NTT

DOCOMO TRF acquires Dutch Lanka Trailer Manufacturers (DLT), Sri

Lanka, a world-class trailer manufacturing company Tata Housing makes waves with its launch of low cost housing

in Mumbai

2010 TRF acquires UK-based Hewitt Robins International Tata Tea group rebrands itself as Tata Global Beverages,

headquartered in London Tata Chemicals acquires 100-per-cent stake in leading vacuum

salt producer British Salt, UK

2011 Tata Chemicals rebrands its global subsidiaries in the UK, the

US and Kenya under the Tata Chemicals corporate brand The Tata brand soars into the top 50 club of global brands Tata Medical Centre, a comprehensive cancer care and treatment

facility established in Kolkata, is inaugurated by Tata SonsChairman Ratan Tata

Tata BP Solar becomes wholly owned Tata company (now known asTata Power Solar Systems)

2012 Tata Global Beverages and Starbucks form joint venture to open

Starbucks cafés across India. First outlet launched in Octoberin Mumbai

10

Tata Communications completes world’s first wholly-owned cablenetwork ring around the world

Tata AIG Life Insurance Company to be now called Tata AIA LifeInsurance Company

Tata Steel expands aerospace activities in China Cyrus P Mistry takes over as Chairman, Tata Sons from Ratan N

Tata

2013 Tata Motors’ Jamshedpur plant rolls out its two millionth

truck TCS adds over $1 billion in brand value; consolidates position

as one of the 'Big Four' IT services brands Tata Sons announces formation of the Group Executive Council Tata Technologies acquires Cambric, a premier US-based

engineering services company TCS acquires IT services firm Alti to help drive long-term

growth in France

The Indian Telecommunication Sector

The Indian Telecom sector has witnessed tremendous growth over thelast decade. Currently, India has a total of 892.02 millionsubscribers out of which 861.66 are mobile subscribers while theremaining 30.36 million are wireline subscribers. In fact, with atele-density of 70.57%, India has the second largest network in theworld and also one of the world’s fastest growing telecom markets.This has resulted in massive investments in the industry both by theprivate and the government sector. The telecom sector havecontributed significantly in effecting socio-economic development ofIndia especially in the arena of education, commercial, medical andgovernmental activities. As of now, 3% of India’s GDP comes from theTelecom sector. Also, after services and computer software sector,

11

Telecom is the third largest sector which attracts Foreign DirectInvestment (FDI) up to 74%.

The immense potential of the sector fuelled by liberalization hasserved to attract newer players in the industry which in turn hasintensified the competition. Consequently, Average Revenue Per User(ARPU) has lowered as consumer benefits have maximized which isevident from a huge fall in tariffs. At the same time, the emergenceof new technologies as manifested by the convergence of voice anddata, introduction of high-end smartphones, advancement towards 3Gand increased focus on Value Added Services (VAS) has prompted theservice operators to differentiate themselves in their servicequality and offering. On the other hand, regulatory issues,decreasing EBITDA margin, the fight for spectrum allocation andinfrastructure cost minimization have given birth to consolidationtrends in the Indian Telecom sector.

Table 2: Telecom Growth in India

Drivers for Consolidation in Indian Telecom Sector

12

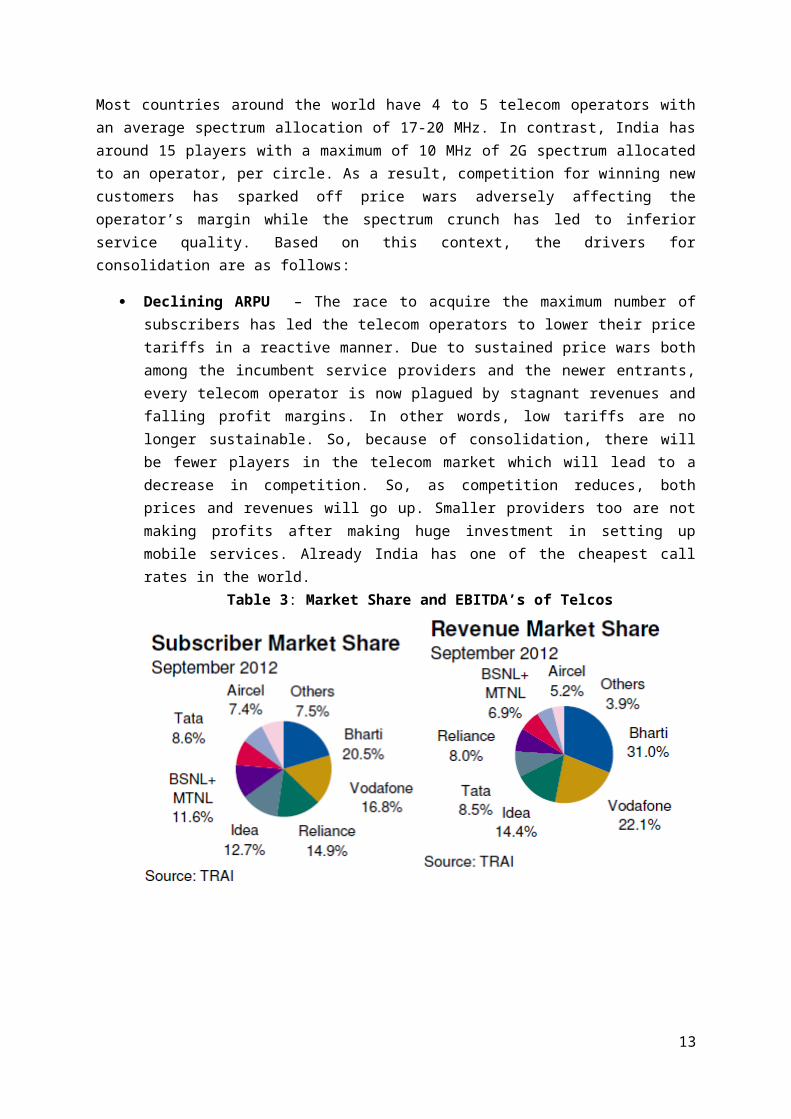

Most countries around the world have 4 to 5 telecom operators withan average spectrum allocation of 17-20 MHz. In contrast, India hasaround 15 players with a maximum of 10 MHz of 2G spectrum allocatedto an operator, per circle. As a result, competition for winning newcustomers has sparked off price wars adversely affecting theoperator’s margin while the spectrum crunch has led to inferiorservice quality. Based on this context, the drivers forconsolidation are as follows:

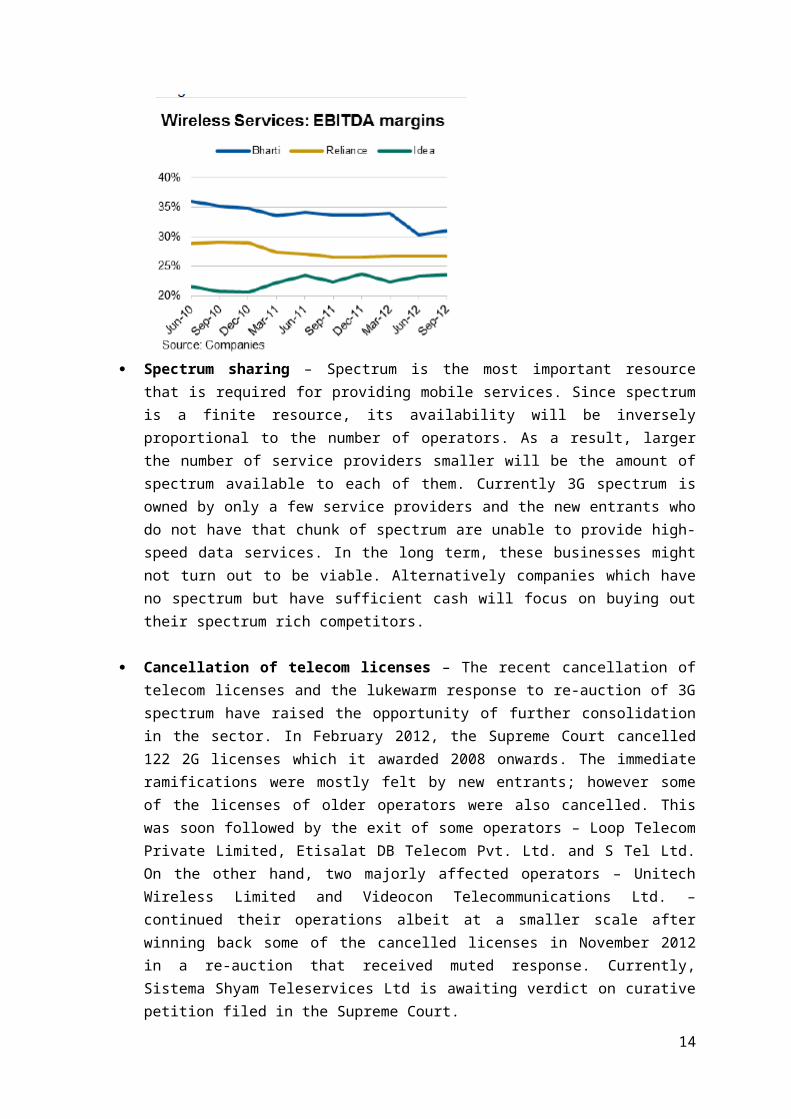

Declining ARPU – The race to acquire the maximum number ofsubscribers has led the telecom operators to lower their pricetariffs in a reactive manner. Due to sustained price wars bothamong the incumbent service providers and the newer entrants,every telecom operator is now plagued by stagnant revenues andfalling profit margins. In other words, low tariffs are nolonger sustainable. So, because of consolidation, there willbe fewer players in the telecom market which will lead to adecrease in competition. So, as competition reduces, bothprices and revenues will go up. Smaller providers too are notmaking profits after making huge investment in setting upmobile services. Already India has one of the cheapest callrates in the world.

Table 3: Market Share and EBITDA’s of Telcos

13

Spectrum sharing – Spectrum is the most important resourcethat is required for providing mobile services. Since spectrumis a finite resource, its availability will be inverselyproportional to the number of operators. As a result, largerthe number of service providers smaller will be the amount ofspectrum available to each of them. Currently 3G spectrum isowned by only a few service providers and the new entrants whodo not have that chunk of spectrum are unable to provide high-speed data services. In the long term, these businesses mightnot turn out to be viable. Alternatively companies which haveno spectrum but have sufficient cash will focus on buying outtheir spectrum rich competitors.

Cancellation of telecom licenses – The recent cancellation oftelecom licenses and the lukewarm response to re-auction of 3Gspectrum have raised the opportunity of further consolidationin the sector. In February 2012, the Supreme Court cancelled122 2G licenses which it awarded 2008 onwards. The immediateramifications were mostly felt by new entrants; however someof the licenses of older operators were also cancelled. Thiswas soon followed by the exit of some operators – Loop TelecomPrivate Limited, Etisalat DB Telecom Pvt. Ltd. and S Tel Ltd.On the other hand, two majorly affected operators – UnitechWireless Limited and Videocon Telecommunications Ltd. –continued their operations albeit at a smaller scale afterwinning back some of the cancelled licenses in November 2012in a re-auction that received muted response. Currently,Sistema Shyam Teleservices Ltd is awaiting verdict on curativepetition filed in the Supreme Court.

14

How Consolidation can complement Core-Competencies?

The trend of consolidation in the telecom sector will usher in a newwave of measures to improve the core competencies of the telecomoperators.

Improved Customer Service – Most of the incumbent GSM operators witha high subscriber base have almost exhausted their spectrumreserves. In contrast, the newer entrants have a low subscriber basebecause of which their spectrum allocation remains idle. In thiscontext, consolidation will help the operators to optimally use thespectrum and deliver superior service quality by preventing networkcongestions.

Economies of Scale – Telecom towers comprise the primary componentof telecom infrastructure and hence require significant capitalexpenditure. Due to lesser number of telecom operators brought aboutby consolidation, there will be increased opportunity for lowercapital expenditure. This is so because each tower including itsequipment will then be fully utilised, even though most of thetowers are shared between the operators. Presently, only the toweris being shared while every operator has to deploy one’s own set ofradio equipment which in most cases goes under-utilised. Thisincreases the cost per subscriber which can be brought down to agreat extent by consolidation.

Reduced Tariff – Although reduced competition brought about byconsolidation coupled with incremental regulatory expenses mayprompt the incumbent operators to raise their tariffs but in thelong run the costs incurred due to sales, marketing and maintenancewill be reduced substantially. As a result, the cost of service willgo down and this will lead to lower tariffs.

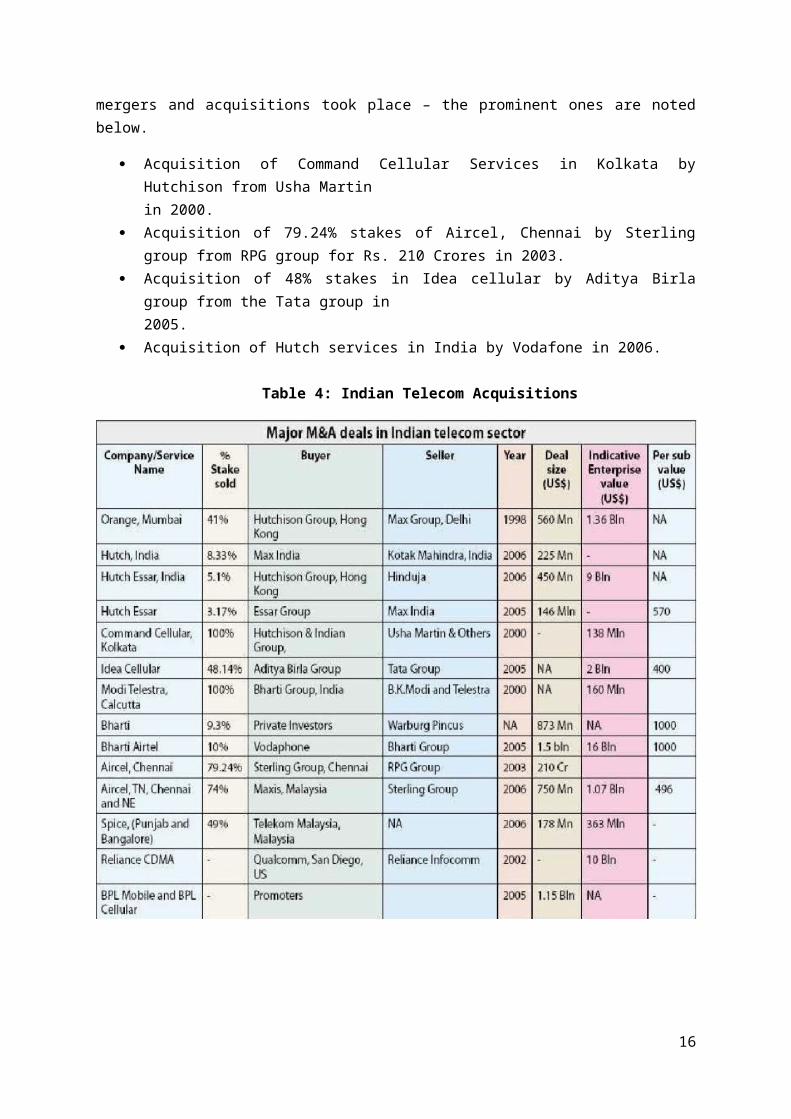

Mergers and Acquisitions

The first merger and acquisition deal in the Indian telecom industryoccurred in 1998 between Max Group of Delhi and Hutchison Group ofHong Kong. Similarly, Hutchison acquired from Max 41% of stakes ofOrange services in Mumbai. In the subsequent years several other

15

mergers and acquisitions took place – the prominent ones are notedbelow.

Acquisition of Command Cellular Services in Kolkata byHutchison from Usha Martin in 2000.

Acquisition of 79.24% stakes of Aircel, Chennai by Sterlinggroup from RPG group for Rs. 210 Crores in 2003.

Acquisition of 48% stakes in Idea cellular by Aditya Birlagroup from the Tata group in 2005.

Acquisition of Hutch services in India by Vodafone in 2006.

Table 4: Indian Telecom Acquisitions

16

Regulatory Changes

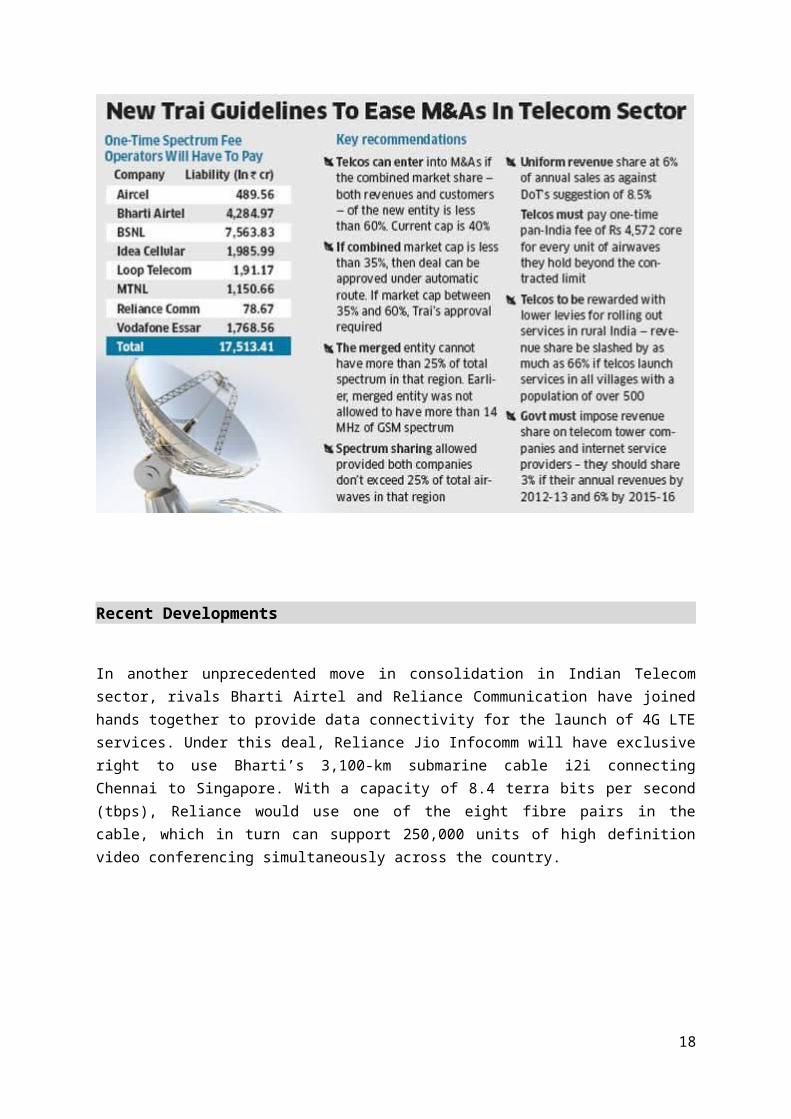

Over the years, the Telecom Regulatory Authority of India (TRAI) hasevolved to facilitate effective policy formation and execution.However, its’ policies have always been beset with uncertainties.This is evident from the tax dispute arising out of Vodafone’sacquisition of Hutchison and the consequent establishment ofretrospective cost. Additionally, the 2G scam has also put aquestion mark on the role of the regulatory which has furtherdeterred M&A activity. Having said that, the proposed newregulations from TRAI seems to be a step forward in encouragingconsolidation in the already crowded and ultra-competitive 15 playertelecom market. Some of the important regulation reforms proposedare as follows:

Increase in Market Share of merged entity - As per the newregulations, the wireless service providers can merge theiroperations if the combined market share of the new entity is lessthan 60%, a substantial increase over the current 40% ceiling. Thecombined revenue market share of India's largest operators, BhartiAirtel and Vodafone India, is 51% and so as such the new rules willenable any large operator in the country to acquire smalleroperators, thus reducing the total number of players in the fray.

Spectrum Sharing – As per the new regulations, spectrum sharingamong different operators has been permitted as long as the extentof frequencies shared does not exceed 25% of the available airwavesin the region. This has been welcomed by the telecom operators asmany new operators have unused capacity while the incumbents havechoked networks. Massive capital expenditure can be avoided throughsuch sharing of spectrum.

Table 5: Regulatory Changes

17

Recent Developments

In another unprecedented move in consolidation in Indian Telecomsector, rivals Bharti Airtel and Reliance Communication have joinedhands together to provide data connectivity for the launch of 4G LTEservices. Under this deal, Reliance Jio Infocomm will have exclusiveright to use Bharti’s 3,100-km submarine cable i2i connectingChennai to Singapore. With a capacity of 8.4 terra bits per second(tbps), Reliance would use one of the eight fibre pairs in thecable, which in turn can support 250,000 units of high definitionvideo conferencing simultaneously across the country.

18

Introduction to Indian Retail

Retailing is still in its infancy in India. In the name ofretailing, the unorganised retailing has dominated the Indianlandscape so far. According to an estimate the unorganized retailsector has 97% presence whereas the organized accounts for merely 3%. Industry has already predicted a trillion dollar market in retailsector in India by 2010. However, the retail industry in India isundergoing a major shake-up as the country is witnessing a retailrevolution. The old traditional formats are slowly changing intomore complex and bigger formats. Malls and mega malls are coming up

19

in almost all the places be it – metros or the smaller cities,across the length and breadth of the country.

A McKinsey report on India (2004) says organized retailing wouldincrease the efficiency and productivity of entire gamut of economicactivities, and would help in achieving higher GDP growth. At 6%,the share of employment of retail in India is low, even whencompared to Brazil (14%), and Poland (12%).Govt of India's plan ofchanging the FDI guidelines in this sector speaks of the importanceattached to retailing. Recently moves by big corporate houses likeReliance Industries has further fuelled the major investments inretail sector. A strategic alliance, land acquisitions in primeareas give the essence of the mood in this sector.

Strategies for Core Competence and Competitive Advantage

Right Positioning

The effectiveness of the mall developer's communication of theoffering to the target customers determines how well the mall getspositioned in their minds. At this stage, the communication has tobe more of relative nature. This implies that the message conveyedto the target customers must be effective enough in differentiatingthe mall's offering from that of its competitors without even namingthem. The message should also clearly convey to the target audiencethat the mall offers them exactly what they call the completeshopping-cum-entertainment point that meets all their expectations.The core purpose is to inform the target customers about theoffering of the mall, persuade them to visit the mall and remindthem about the mall. The mall developer can create awareness aboutthe offering among the target customers in a number of ways. Variouscommunication tools available to the mall developer for this purposemay include advertising, buzz marketing (WoM), celebrityendorsement, use of print media, press releases and viralmarketing .Once the message is being conveyed through thesechannels, the mall developer must add a personal touch to hismessage by carrying out a door-to-door campaign in order toreinforce the message.

Effective Visual Communication

20

Retailer has to give more emphasis on display visual merchandising,lighting, signages and specialized props. The visual communicationstrategy might be planned and also be brand positioned. Theme orlifestyle displays using stylized mannequins and props, which arebased on a season or an event, are used to promote collections andhave to change to keep touch with the trend. The merchandisepresentation ought to be very creative and displays are often onnon-standard fixtures and forms to generate interest and add onattitude to the merchandise.

Strong Supply Chain

Critical components of supply chain planning applications can helpmanufacturers meet retailers' service levels and maintain profitmargins. Retailer has to develop innovative solution for managingthe supply chain problems. Innovative solutions like performancemanagement, frequent sales operation management, demand planning,inventory planning, production planning, lean systems and staffshould help retailers to get advantage over competitors.

Changing the Perception

Retailers benefit only if consumers perceive their store brands tohave consistent and comparable quality and availability in relationto branded products. Retailer has to provide more assortments forprivate level brands to compete with supplier's brand. New productdevelopment, aggressive retail mix as well as everyday low pricingstrategy can be the strategy to get edge over supplier's brand.

Challenges

Modern retailing is all about directly having "first-handexperience" with customers, giving them such a satiable experiencethat they would like to enjoy again and again. Providing greatexperience to customers can easily be said than done. Thuschallenges like retail differentiation, merchandising mix, supplychain management and competition from supplier's brands are the talkof the day. In India, as we are moving to the next phase of retaildevelopment, each endeavour to offer experiential shopping. One ofthe key observations by customers is that it is very difficult to

21

find the uniqueness of retail stores. The problem: retaildifferentiation.

The next problem in setting up organized retail operations is thatof supply chain logistics. India lacks a strong supply chain whencompared to Europe or the USA. The existing supply chain has toomany intermediaries: Typical supply chain looks like:- Manufacturer- National distributor - Regional distributor - Local wholesaler -Retailer - Consumer. This implies that global retail chains willhave to build a supply chain network from scratch. This might runfoul with the existing supply chain operators. In addition tofragmented supply chain, the trucking and transportation system isantiquated. The concept of container trucks, automated warehousingis yet to take root in India. The result: significant losses/damagesduring shipping.

Merchandising planning is one of the biggest challenges that anymulti store retailer faces. Getting the right mix of product, whichis store specific across organization, is a combination of customerinsight, allocation and assortment techniques.

The private label will continue to compete with brand leaders. Sosupplier's brand will take their own way because they have aestablished brand image from last decades and the reasons can beattributed to better customer experience, value vs. price,aspiration, innovation, accessibility of supplier's brand.

Product Differentiation – Key to success

As the retail industry is in the nascent stage it is unlikely thatplayers will play the price war, which usually takes place in amature industry. The players will however try to win the customersby product differentiation or by providing a unique shoppingexperience. Only basic daily usage high frequency- low value itemswould be sold at lower prices and once the market gets saturatedprice war may be witnessed in the other product categories also.

Specialty Retailing

22

Learning from western countries, players are trying to capture themarket share bringing out formats catering to single verticals.Such chains are called specialty retailers or category killers. inthe West. Many specialized stores have been set up with variousfood, apparel and footwear brands (both Indian and foreign) andcompanies like Godrej have already started furniture stores.

Hindustan Lever Ltd, the FMCG major, is considering a retail chainfor laundry products. Big players such as the Dubai-based JumboGroup, Tatas and some small players are entering the electronicsspace. Other categories being explored by retailers are officeproducts, toys, lingerie, chocolates, electrical products, paperproducts, stationery and furnishings. As these stores do not requiremuchspace, they will be set up as stores in malls rather than asstandalone stores. To summarize, retail sector is set to see whopping growth in nextfew years and the organized retail-pie is going to get bigger asurbanization of new cities take place. But for growth, large scaleinvestments are required.

23

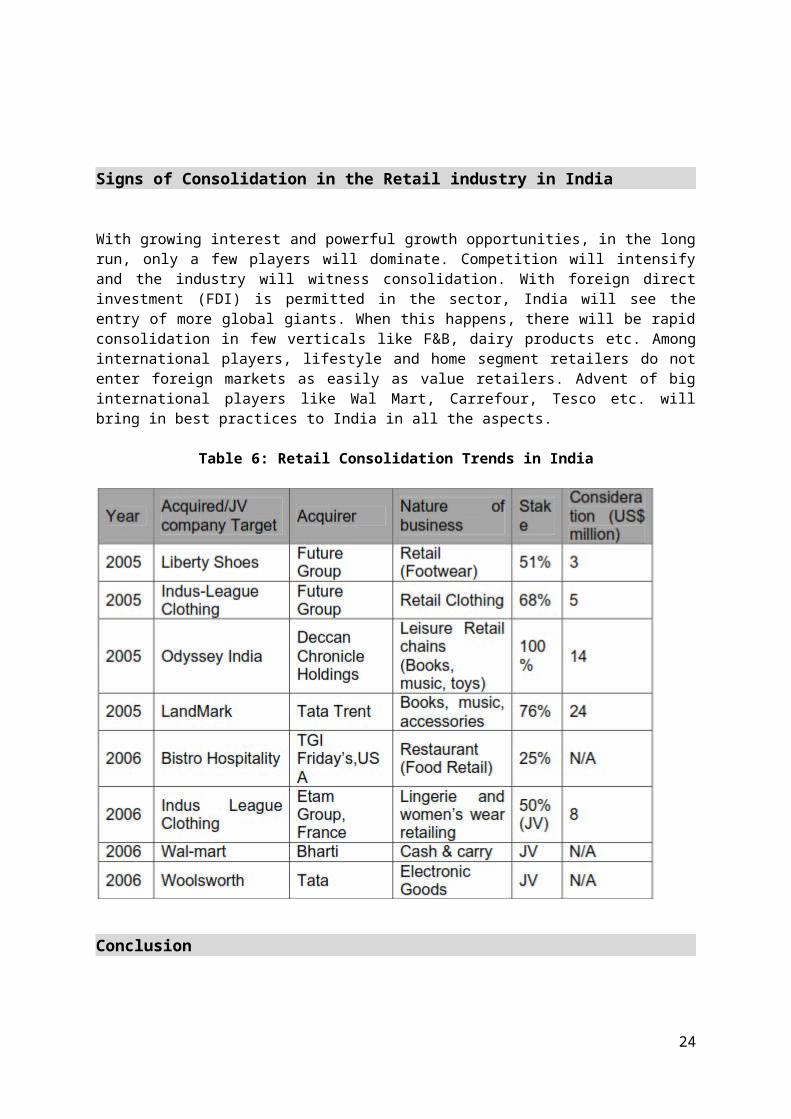

Signs of Consolidation in the Retail industry in India

With growing interest and powerful growth opportunities, in the longrun, only a few players will dominate. Competition will intensifyand the industry will witness consolidation. With foreign directinvestment (FDI) is permitted in the sector, India will see theentry of more global giants. When this happens, there will be rapidconsolidation in few verticals like F&B, dairy products etc. Amonginternational players, lifestyle and home segment retailers do notenter foreign markets as easily as value retailers. Advent of biginternational players like Wal Mart, Carrefour, Tesco etc. willbring in best practices to India in all the aspects.

Table 6: Retail Consolidation Trends in India

Conclusion

24

The success of the Tata Corporation serves as a reminder to thepotential of Indian firms in acquiring core competencies whileattaining consolidation to become bigger and better organizations.In the same context, certain industry sectors such as Telecom andRetail will continue to show signs of further consolidation which inthe future will lead to further growth, stable environment, bettercustomer service and improved organizational efficiency.

25