Embed Size (px)

Citation preview

CapitalMarketsDay 2019

4 June 2019Bangkok, Thailand

ticker symbol: DTAC

Alexandra ReichCEO

Prathet TankuranumCTO

Dilip PalCFO

Rajiv BawaCCAO, CBO

Nardrerdee Arj-harnwongseCPO

HowLih RenCMO

Tipayarat KaewsringarmCSO

/agenda

Welcome, dtac’s TurnaroundAlexandra ReichCEO

13:30 Financial UpdateDilip PalCFO

15:30

Customer Centric NetworkPrathet TankuranumCTO

14:00 Final RemarksAlexandra ReichCEO

15:50

Win Back B2CHow Lih Ren & Tipayarat KaewsringarmCMO, CSO

14:30 Q&A16:00

Address B2B OpportunityRajiv BawaCBO

15:00

Registration13:00 Break15:15

Welcome, dtac’sturnaround

Alexandra Reich Chief Executive Officer

0

2

4

6

8

10

2018 OECD average dtac 2018 dtac Q1'19

Data

cons

umpt

ion

(GB/

mon

th)

/contextThais are some of the world’s heaviest data users…

Smartphone penetration 81%

Average 9hrs per day using internet

Bangkok #1 city in the world for Facebook users

Thailand is among the top 10 countries in for Youtube watch hours

Increasing willingness to pay for convenience and reliability

5

20142013 2015 20172016 Q118 Q218 Q119

End of concession

/context…but dtac failed to capture market growth

22.5%

31.5% Reduction of spectrum

End of concession

Remedy

9002x5MHz

18002x5MHz

2300MHz

Revenue market share (Service rev ex. IC)

Alexandra starts

Q318 Q41815 Sep 15 DecApr Aug Oct

Network issues & competitive pressure

6

\

/responseGet things done

Manage the crisis

Build the fundamentals

open, transparent communication

Turn crisis into an opportunity

New sites and spectrum acquisition

Customer-focused

Hypothesis Quantitative data Behavioral Research

crisis

!

7

/responseNever Stop Improving…

Complex

NonTransparent

Technology Driven

Trust

Individual appreciation

Simple

Honest

Human

Customers want

dtac needs to be

Marketis

Convenience

8Em

otio

nal p

ositi

onin

g

Functional positioning

Consistent network &

competitive price

Simple,Honest, Human

Best coverage &premium price

Fast network &attractive

promotions

Lifestyle

Best & biggest

/responseBuilding the platform for growth in the middle of the crisis

Removed involuntary CPA

Transparent promo-end renewal

No discrimination of existing vs. new

customers

Q3’18 Q4’18 Q1’19

Billing & pricing complaints

Jan-18

Oct-18

Apr-18

Jan-19

Jul-18

Apr-19

Monthly CPA revenues

Recall of the “We Will Never Stop” campaign across users from all

operators

92 94123

Q1’19Q3’18 Q4’18

Postpaid net adds (‘000)

79%-22%

+16%

Transparent communication

Complaints: -75%

Q1’19 vs 2018

Postpaid churn: -3%

Q1’19 vs Q3’18

9

/peopleGain trust, mobilize, empower

PHASE IListen and Gain Trust• Openly share challenges• Clarify want to stand for • Set expected behavior

PHASE IIMobilize

• Own the challenges• Create a common belief in success• Give proof points• Set the right incentives

PHASE IIIEmpower• Change the way we work• Design end to end experiences• Frontline empowerment

We’re here!

10

20212017 2018 2019 2020

/ambitionGet back to growth!

Turnaround pillars

dtac service rev ex. IC

Consistent Customer Centric Network Experience

Win Back B2C

Address B2B Opportunity

Stop the bleeding Stabilize

Change the trend

11

Customer Centric Network

Prathet TankuranunChief Technology Officer

/spectrumIncreased spectrum holdings by 10% Largest download bandwidth in Thailand

dtac spectrum position vs. competition (2018)

* based on 45MHz D/L bandwidth on 2300MHz network

dtac spectrum portfolio evolution (in MHz by band)

Q1 2018

850/900

110

Q1 2019

1800

2300

2100

100

+10%

3.3

1.51.9

Operator Xdtac* Operator Y

70.060.0 55.0

Operator Ydtac* Operator X

Total download bandwidth (in MHz)

Download bandwidth / mn. customers (in MHz)

13

/networkIncreased number of sites by over 50% in 3 years

2016

91

71

20182017 Q1 2019

61

94

Number of sites by band (in thousands)

4G 2300MHz 4G 2100MHz 2G 1800MHz4G 1800MHz 3G 2100MHz 3G 850MHz

• Massive densification of 2100 network ->18k additional 2100MHz base stations installed in since 2016

• Launch of first TD-LTE network in Thailand in 2018

15.4k 2300MHz base stations installed at end of Q119

Deployment of 64T64R Massive MIMO with 3.5x capacity enhancement in terms of user throughput

8.0m subs on 2300MHz network

+55%

14

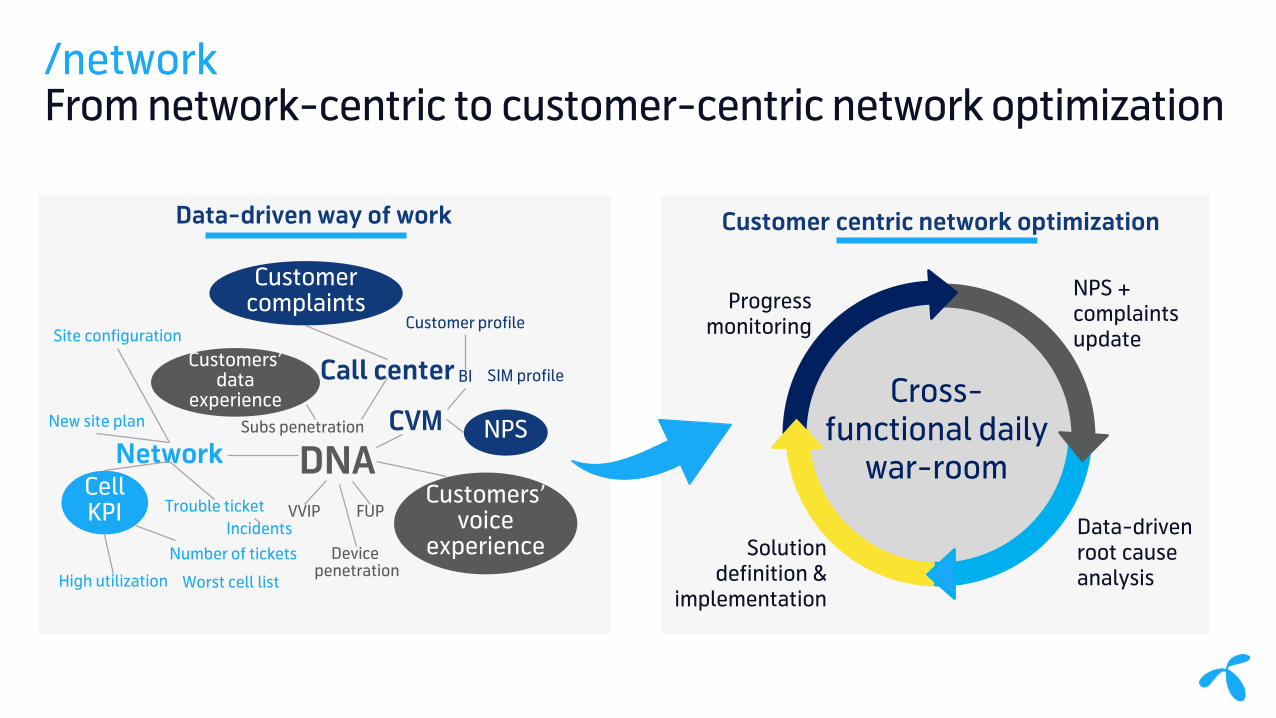

/networkFrom network-centric to customer-centric network optimization

Customer centric network optimizationData-driven way of work

Progressmonitoring

Solution definition &

implementation

NPS + complaints update

Cross-functional daily

war-roomData-driven root causeanalysisHigh utilization Worst cell list

Cell KPI

Network DNA

Site configuration

New site plan

Trouble ticket

Number of ticketsIncidents

Customers’ data

experienceSubs penetration

VVIP

Device penetration

FUPCustomers’

voice experience

CVMBI

Customer profile

SIM profileCall center

Customercomplaints

NPS

15

/networkVery encouraging signs that we are on the right track

Average daily network complaints

#1 Operator in Thailand for download speed and video

experience(2)

(1) excl. AOU <30 Days(2) Source: Manager Online, Prachachat Turakij quoting “OpenSignal”

Jan-17 Jan-18 Jul-18Jul-17 Jan-19 Apr-19

-28%

Network NPS(1)

Jul-18Jan-17 Jul-17 Jan-18 Jan-19 Apr-19

x2

16

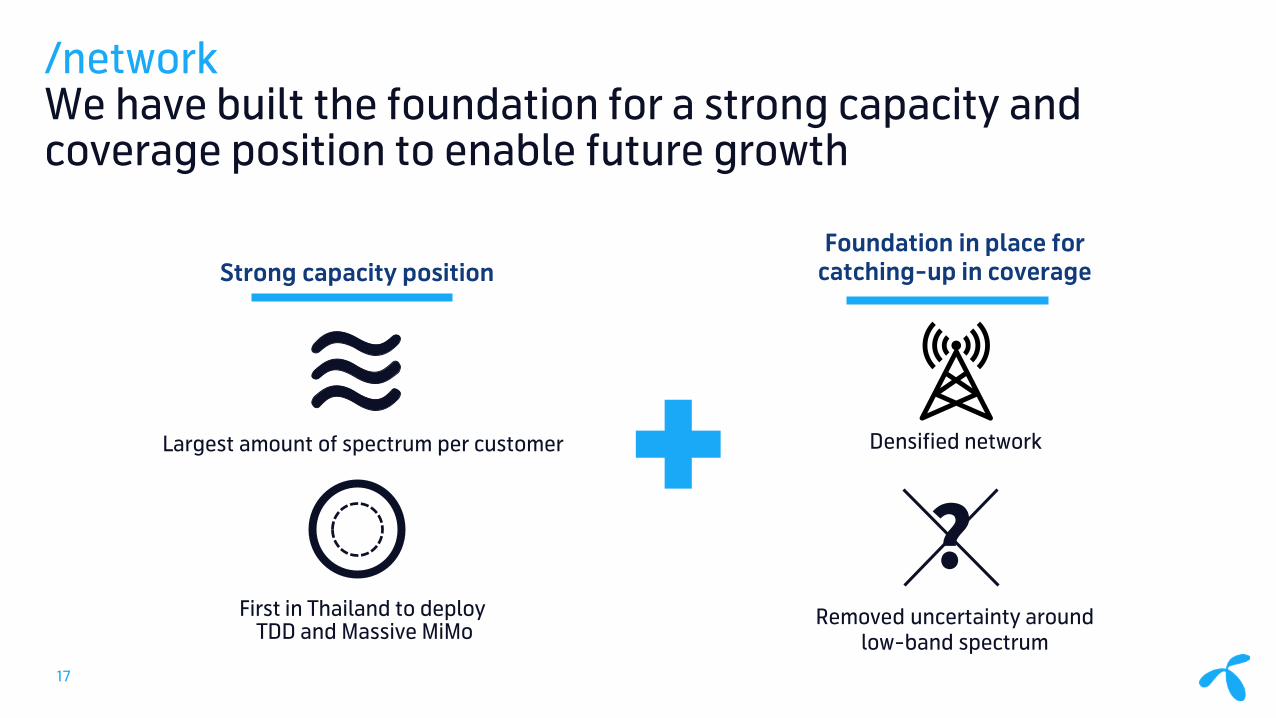

/networkWe have built the foundation for a strong capacity and coverage position to enable future growth

?

Strong capacity positionFoundation in place for

catching-up in coverage

Densified network

Removed uncertainty around low-band spectrum

Largest amount of spectrum per customer

First in Thailand to deployTDD and Massive MiMo

17

/network visionConsistent customer-centric network experience

Unbuffered video experience nationwide

Competitive capacityHD video

Consistent coverage nationwide, indoor & outdoor

Leading technology position, enabling customer-centric

innovations

18

/networkClear roadmap to execute against this vision

Q2-19 Q3-19 H2-20H1-20Q4-19 2020+

Expand TDD footprint

Fix coverage in existing footprint

Sunset 2G

Continue to drive 5G readiness

IT transformation

Upgrade capacity to improve quality

Fix quality in existing footprint Increase coverage

Swap 850-900 MHz spectrum and increase coverage

19

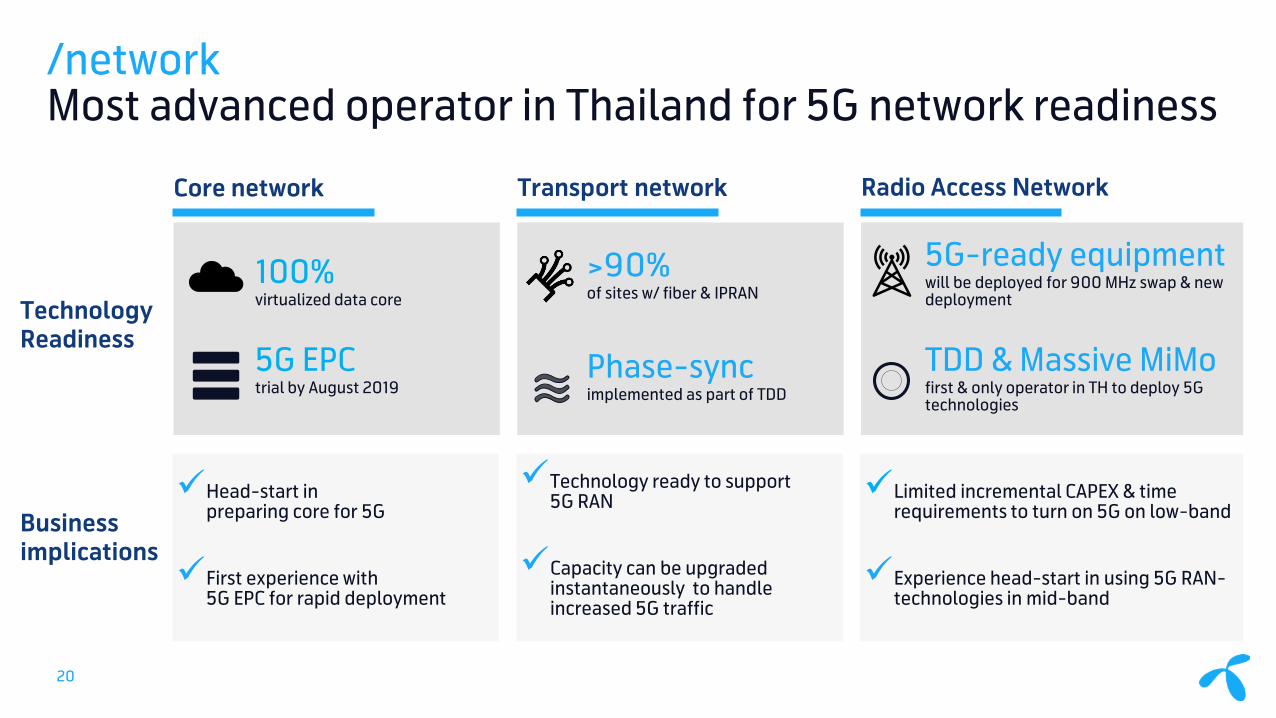

/networkMost advanced operator in Thailand for 5G network readiness

Head-start in preparing core for 5G

First experience with 5G EPC for rapid deployment

Technology ready to support 5G RAN

Capacity can be upgraded instantaneously to handle increased 5G traffic

Limited incremental CAPEX & time requirements to turn on 5G on low-band

Experience head-start in using 5G RAN-technologies in mid-band

100% virtualized data core

5G EPC trial by August 2019

>90% of sites w/ fiber & IPRAN

Phase-sync implemented as part of TDD

5G-ready equipmentwill be deployed for 900 MHz swap & new deployment

TDD & Massive MiMofirst & only operator in TH to deploy 5G technologies

TechnologyReadiness

Business implications

Core network Transport network Radio Access Network

20

/ITConstant progress in our IT transformation to support business, with clear focus areas for 2019-2020

Digitization of our core

Competency & people

Business security

Agile transformation

& business model

Data-driven company

21

Win Back B2C

Tipayarat KaewsringarmChief Sales Officer

How Lih RenChief Marketing Officer

Market slowing down but still growing…

…driven by strong customer demand for data consumption

2017 2018 2019 2020

5.7%

2.6%

48% 52%

52% 48%

2017 Q1’19

prepaid

postpaid

Quarterly reports - dtac, AIS, True, and others.

…and migration from prepaid to postpaid…

Market Revenue MixMarket Revenue Growth (est.)

6

910

20182017 Q1’19Data consumption / user / month (GB)

Source: dtac internal

+29%

/mobile consumer marketStill a growing market driven by strong demand for data and shift to postpaid

23

Revenue market growth includes AIS, True, dtac.2019 and 2020 figure is based on IFRS15 accounting standard which lead to negative impact on YoY comparison as 2018 was based on IAS18 accounting standard.

ARPU(THB)

155

538

147

502

/mobile consumer marketIn a complex market, dtac will be simple, honest and human

Add-on

144

Operator X Operator Y

131

Operator Z

85

Main plan

Add-on

SIM

149177

120

Postpaid

Prepaid

Source: Company websites; lit search - Mar 2018

Emot

iona

l pos

ition

ing

Functional positioning

Consistent network &

competitive price

Simple,Honest, Human

Best coverage &premium price

Fast network &attractive

promotions

Lifestyle

Best & biggest

Operator X Operator Y Operator Z

24

/win backOur 2019 priorities

Enhance customer experience across touch points

Stabilize prepaid

Keep momentum on postpaid

25

/prepaidSigns of stabilization

After a long struggle we see signs of stabilization

Heavy handsets subsidies from competition

NW issues

Sales execution issues

Market mostly pulled back from prepaid device subsidies

Revitalize distribution

Key drivers of decline Current situation

68 67 6864 65 65

55

60

65

70

Oct-18 Jan-19Nov-18 Feb-19Dec-18 Mar-19

Prepaid Daily Revenue (THB mln)

Distribution challenges

Network issues

Distribution challenges

Network NPS doubled since Jan’19

Revitalize distribution

inte

rnal

fact

ors

Heavy handsets subsidies from competition

“Race to the bottom” on pricing

Market mostly pulled back from prepaid device subsidies

Market pulled back from unlimited in 2019

exte

rnal

fact

ors

26

/prepaidPull back from unlimited offer for acquisition topping

Market is pulling back from unlimited offers

Unlimited internet with low price

May’19 Stopped unlimited acquisition toppingIntroduced fixed speed with fair-use policy (FUP)

2018

Unlimited data at flat speed, without fair-use policy (FUP)

New! Fixed quota at flat speed, with FUP

27

Launched bite-size fixed speed with FUP2019

/prepaidRevitalize distribution

Revitalize distribution… …while focusing on quality… …and keep expanding our footprint

Q4’18 Q1’19

# prepaid GA at retailer

Q1’19Q4’18

Survival rate at month 3

• Re-activate retailers and new retailer expansion

• Onboarding distributors in selected provinces

• Introduction of mini distributor/hub in rural areas

+14%

+14%

28

/prepaidHyperlocal approach to fix distribution holes

Leveraging direct sales to penetrate key areas

New commission and incentives Re-engaging customers in areas with network improvements

Q4’19 Q1’19

Prepaid inflow revenues by direct sales

+7%% increase in inflow revenues

Q119 vs Q418Localized marketing & sales activities

+24%

29

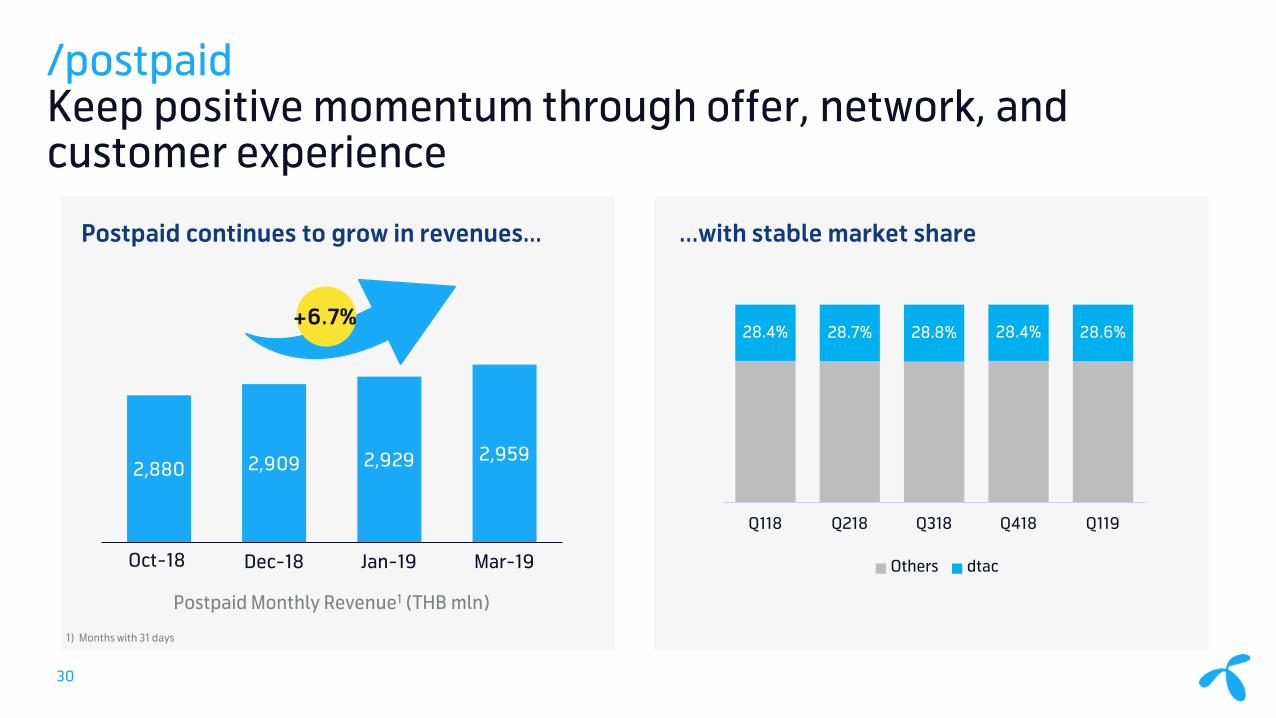

28.4% 28.7% 28.8% 28.4% 28.6%

Q118 Q218 Q318 Q418 Q119

Others dtac

2,880 2,909 2,929 2,959

Jan-19Dec-18 Mar-19

Postpaid Monthly Revenue1 (THB mln)

...with stable market sharePostpaid continues to grow in revenues…

1) Months with 31 days

/postpaidKeep positive momentum through offer, network, and customer experience

+6.7%

30

Oct-18

Take a position not to discriminate existing vs new customers

… Capture additional value through TDD migration

Individual:

Migration to TDD

Gain back trust in service through network experience improvement

Postpaid NPS

Non TDD TDDAverage ARPU TDD vs

non-TDD 4G active callers

+7pp

in 3 months

+15%

/postpaidRetain customers through trust and caring while monetizing higher data usage

31

/postpaidWin customers through clear proposition and strong sale executionBuild trust on our network through honest communication

…

• Churn stabilization

Strong focus on sales execution and service quality

Clear position on competitive offers and taking care of customers

32

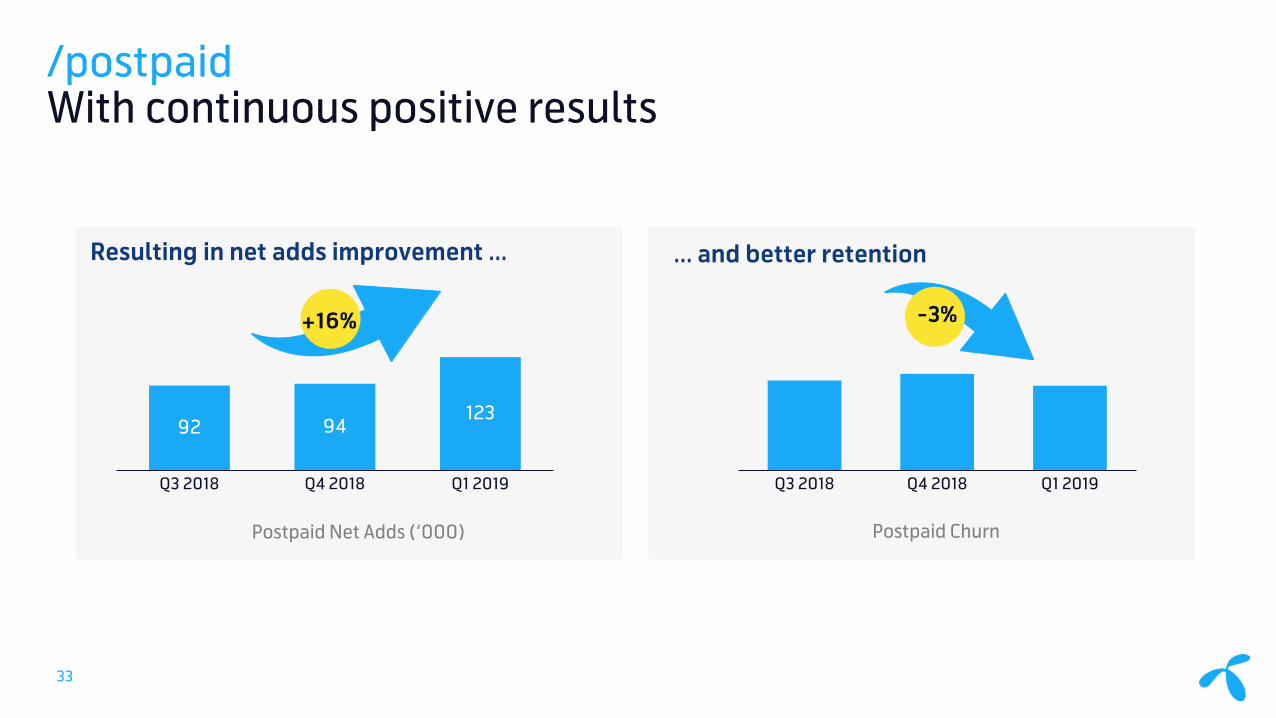

/postpaidWith continuous positive results

92 94123

Q3 2018 Q4 2018 Q1 2019 Q4 2018Q3 2018 Q1 2019

Resulting in net adds improvement … … and better retention

Postpaid ChurnPostpaid Net Adds (‘000)

+16% -3%

33

Digitize to amplify best

service at dtac

Best experience in digital channels

Personalize by being data-

driven

Embrace omni-channel

approach

/enhance customer experienceCombine digital and human touch

34

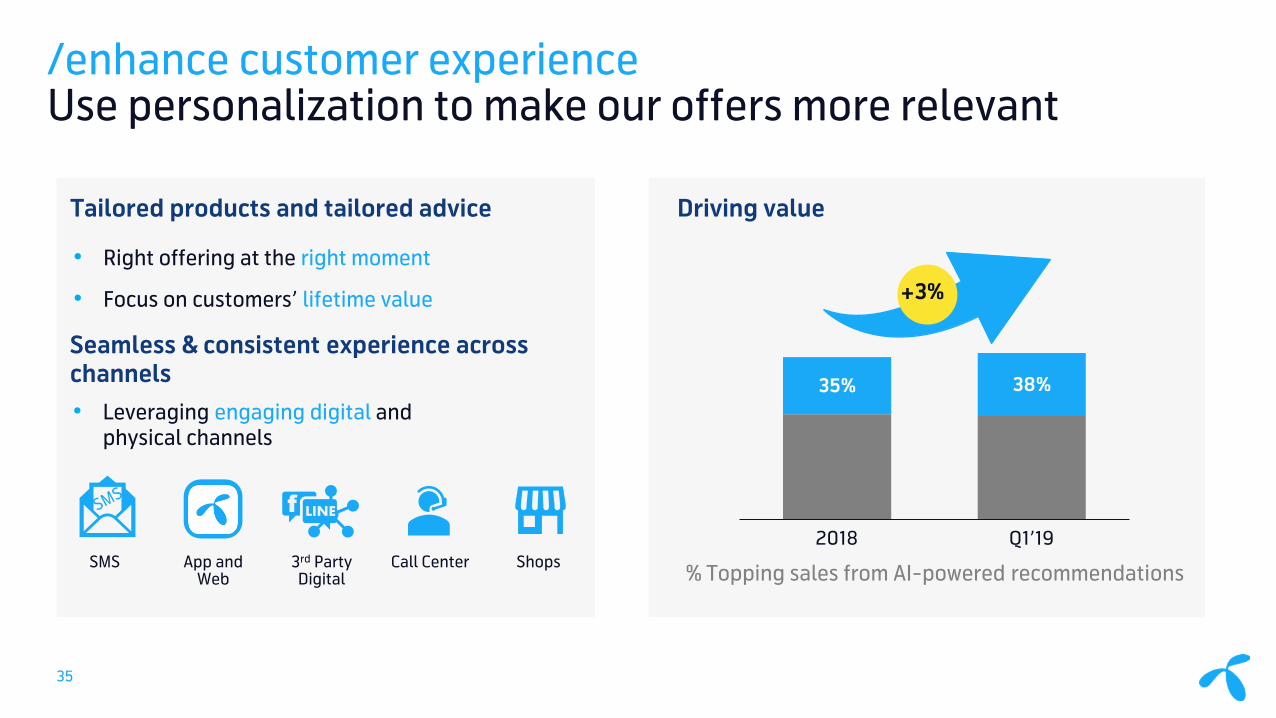

/enhance customer experienceUse personalization to make our offers more relevant

Driving value

Q1’19

35%

2018

38%

% Topping sales from AI-powered recommendations

+3%

35

Tailored products and tailored advice

• Right offering at the right moment

• Focus on customers’ lifetime value

App and Web

3rd Party Digital

ShopsCall CenterSMS

Seamless & consistent experience across channels• Leveraging engaging digital and

physical channels

f LINE

/enhance customer experienceMeet customer needs of simplicity and convenience

-23%

In our shops…. …and in our retailers

• Digitize payment through kiosk

• Prepaid / Postpaid registration on mobile devices through mobile application

• Start Mobility in store

Average waiting time in shops

• Simplify sales process through mobile application for retailers

• Engage and communicate with retailers through retailer application

Active retailers who perform transactions on our retailer app

Q4'18 Q1'19

Q1’19 vs. Q4’18

Time to register a new SIM on retailer app

+20%

<30s

36

/enhance customer experienceResulting in more satisfied customers

• One Stop Service: First-time resolution rate increased

• Feedback call and visit customers: Follow up and feedback all complaint cases to customer

• Uplift agent skills & Knowledge

• Never stop caring campaign

• Regular localized customer activities

Q4/2018 Q1/2019 Q4/2018 Q1/2019

CSAT at Call Center Number of customer complaints

Q4/2018 Q1/2019 Q4/2018 Q1/2019 Q4/2018 Q1/2019

CSAT at Service Hall

CSAT at dtac Center - FOFO

CSAT at dtac Center - COCO

Call center excellence Branded shops

+2% +3% +1% +4%-26%

37

AddressB2B Opportunity

Rajiv BawaChief Business Officer

/mobile B2B marketA virtually untapped opportunity for dtac – especially in the mid-market segment

dtac<10%THB ~22bn

Total addressable mobile B2B market in Thailand Current market offerings

?Mid-Market

SoHo

Large Enterprises

Source: Analysys Mason

Complex customized solutionsbought by IT-departments

Consumer postpaid plans39

/dtac positioningSimple, modular services with consistent experience & competitive prices

Startup Medium EnterpriseTraditional small Business

Our key target segment needs Our value proposition

Flexibility,long-term, no fixed cost & contract lock-in

Smooth connectivityto keep business running

Manage employeemobile usage and contain costs

We help our customers run their businesses more efficiently & effectively by offering simple & honest, worry-free, standardized & best value products.

40

/building capabilitiesWe are focusing on fundamentals in four key areas

Organization Portfolio Customer Journey Distribution

• End-to-end accountability

• Streamlined processes & operations

• Ongoing capability uplift

• Simplified core portfolios + add-ons

• New services together with partners (incl. IoT & IPLC)

• Digitalized sales & service channels

• Enhancement of in-store visibility (own + partner)

• Increased distribution reach (own + dealers)

• New innovative partnerships

1 2 3 41 2 3 4

41

/portfolioWe have launched a simplified core portfolio with simple & easy add-on services

42

Simplified core portfolio… …and simple & easy add-on services

+

/customer journey & distributionDigitalizing sales and service channels to enhance customer experience, improve sales and streamline operations

New salesUpsell

VASTop-ups

Manage own acc & subsProactive AdvisoryBilling/usage info

Customer careMigrate/renew

Acquisition Farming Self-care / CC

Tele Hunters

KAMsTele Farmers E-care Customer

Care

Direct Sales

Dealers

Digital sales (Web)

Branded Retail

Account Managers43

/portfolioWe are working with partners to expand our product portfolio and capture further growth opportunities

International Private Leased Circuit (IPLC)Smart Industry – MDB Care IoT

dtac• Project Management• Mobile & Web App• Marketing• Billing & Collection

• Embedded Software• IoT Devices

• Bundling of solution with MDB• Sale to end customer

44

/resultsWe see early signs of success

+200%

Monthly customer acquisition(1)

+17%

Avg. inflow pack fee(1)

+25%

Customer base(1)

Note: (1) SME segment, May ’19 vs. May ‘18

45

FinancialUpdate

Dilip PalChief Financial Officer

Top line growth has been a challenge

64.7 64.863.0

2016 2017 2018

Service revenues ex. IC (THB bln)

Despite the revenue challenge, dtac delivered strong financial results

27.9 30.4 28.4

33.8%

38.9% 38.6%

2016 2017 2018

EBITDA (THB billion) EBITDA margin

/financials Financial discipline is a core tenet of dtac’s corporate strategy

47

Revenue development was affected by prepaid sub loss, CPA cleanup, and unlimited data price plans

/financials Underlying reasons of revenue challenge are improving

Dec-17

21,8

6,15,6

15,7

6,25,9

17,0 16,1

5,7

Mar-18 Jun-18

6,0

15,3

Sep-18

15,1

Dec-18

14,5

Mar-19

22,7 21,6 21,3 21,2 20,7

Postpaid

PrepaidSubscribers (mln)

237 240248 247 243 242

Mar-19Dec-17 Jun-18Mar-18 Sep-18 Dec-18

ARPU Exc. IC

Q117 Q217 Q317 Q417 Q118 Q218 Q318 Q418 Q119

CPA revenues

What Happened Where are we now

Prepaid sub loss

• Network issues• Device subsidies• High S&M spending

• dtac Network is improving significantly

• Competition subsidy and offers getting rational

Loss of high value customer

• Concession related issues

• Concession related uncertainties are over

• Improvement in Port out and churn from high value

CPA cleanup • High no. of complaints related to CPA services

• Significant reduction in no. of complaints

• CPA loss has bottomed out

Aggressive acquisition price plans

• Unlimited fixed-speed data price plans on both prepaid and postpaid

• Unlimited acquisition plans have been pulled out

Drivers

48

2016 2017 2018 Q119

24.015 21.702

3.642

17.889

-26%

20182016 2017 Q119

16.804 14.404 13.993

3.514

-17%

2016 2017 2018

26.498

Q119

23.137 25.061

3.738

• Regulatory costs dropped to approx. 4% of service revenues ex. IC

• Net CAT lease and TOT roaming costs take full year impact in 2019. YoY net cost increase in Q1’19 is THB 1.9bn for CAT lease and TOT deal combined

• D&A charges dropped sharply after end of the concession

Cost of Service (Excl. CAT, TOT & D&A)

SG&A (Excl. D&A)

D&A

/financials 2018 initiatives delivered on efficiency ambition, 2019 starts with a reset of cost baseline

49

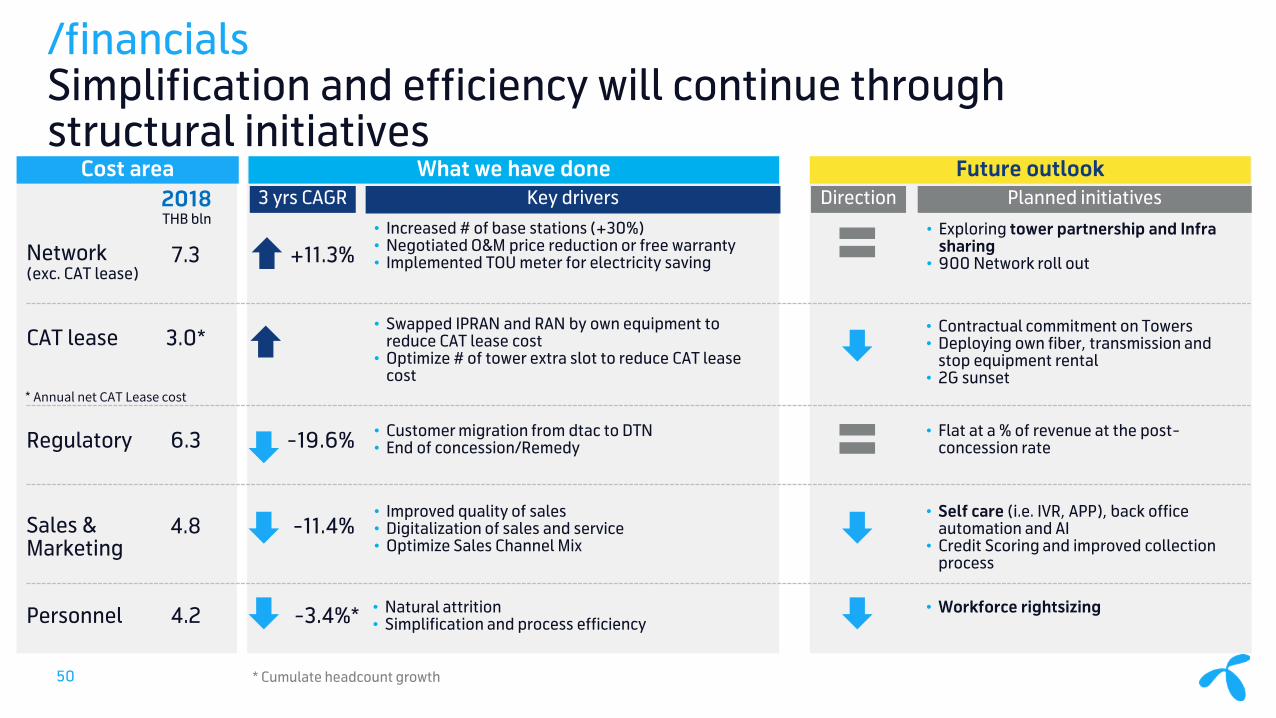

/financials Simplification and efficiency will continue through structural initiatives

Cost area3 yrs CAGR Key drivers

What we have done Future outlook

Network (exc. CAT lease)

CAT lease

Regulatory

Sales & Marketing

Personnel

• Increased # of base stations (+30%)• Negotiated O&M price reduction or free warranty • Implemented TOU meter for electricity saving

6.3

4.2

2018THB bln

7.3

4.8

-19.6%

-3.4%*

+11.3%

-11.4%

• Customer migration from dtac to DTN• End of concession/Remedy

• Improved quality of sales • Digitalization of sales and service• Optimize Sales Channel Mix

• Natural attrition• Simplification and process efficiency

• Exploring tower partnership and Infra sharing

• 900 Network roll out

• Contractual commitment on Towers• Deploying own fiber, transmission and

stop equipment rental• 2G sunset

• Flat at a % of revenue at the post-concession rate

• Self care (i.e. IVR, APP), back office automation and AI

• Credit Scoring and improved collection process

• Workforce rightsizing

Planned initiativesDirection

3.0*• Swapped IPRAN and RAN by own equipment to

reduce CAT lease cost • Optimize # of tower extra slot to reduce CAT lease

cost* Annual net CAT Lease cost

* Cumulate headcount growth50

Financial RatiosNet Debt

30.7 23.0

32.9 34.2

2016 2017 2018 Q1-19

1.1

0.8

1.5 1.4

1.1

0.8

1.2 1.3

2016 2017 2018 Q1-19Net Debt : Equity Net Debt : EBITDA

Interest Bearing Debt by Maturity

11.5

6.0

1.5

4.0

13.0 10.0

2.5 3.0 1.5

0.5

6.0

1.0

7.0

2.5

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

Loan Debenture

Note: as of 31 Mar. 19, the loan includes Revolving Credit Facilities for THB 5.5 billion

THB billion

THB billion

Operating Cash FlowTHB billion

7.613.9

8.91.7

20.416.5

19.6

4.4

27.9 30.4 28.5

6.1

2016 2017 2018 Q1-19Operating CF (EBITDA - CAPEX) CAPEX

Capex

20.3 16.5 19.5 4.4

24.6% 21.1%26.5% 24.9%

2016 2017 2018 Q119

CAPEX (THB billion)

/financials A well-managed debt profile will support flexibility for necessary investment

51

Debt Funding Dividend Leverage

• Continue to deliver positive operating cash flow which will support building liquidity cushion over time

• Expected increase in net debt/EBITDA level in 2019-2020 due to one-off CAT settlement and payment for spectrum licenses

• Manage net debt/EBITDA to be below 3x

• Access to both bank loan and bondto diversify funding source as well tooptimize the funding cost

• Affirmed credit rating at AA withstable outlook by TRIS at 5th April2019

• Secure long term funding to matchlong term investment

• Ensure well spread debt maturityprofile to manage refinancing risk

• Policy takes into consideration both the financial positions and investment required

• Maintain current dividend policy i.e. not less than 50% of company’s net profit

• Aiming for semi-annual dividend payment

/financialsMaintain necessary financial flexibility to support long-term strategic ambitious and offer good shareholder remuneration

52

Guidance RationaleService revenueexcl. IC

Low single-digit decline • Impact from end of the concession still persisted in Q1-19• Efforts to ensure best customer experience have some short

term adverse impact on revenue development• Expect sequential service revenue growth

EBITDA THB 24 – 25 billion • 2019 is the first full year of new cost base after end of the concession

• Dynamic and competitive S&M expenses• Ongoing implementation of operational efficiency

measuresCAPEX THB 13 – 15 billion • Mainly for the expansion of 2300MHz network

• Capacity expansion to address data usage

/2019 guidance Reflects concession-end revenue impact and new cost baseline for 2019

53

Ambition Rationale

Service revenues excl. IC

Low single digit growth • In line with market growth

EBITDA growth Above service revenue growth • Ongoing implementation of operational efficiency measures

CAPEX* In line with 2019 level • Coverage on par with peers

* Excluding spectrum payment.

/medium-term ambitionConfident to get back to growth in both Revenue and EBITDA

54

Final Remarks

Alexandra Reich Chief Executive Officer

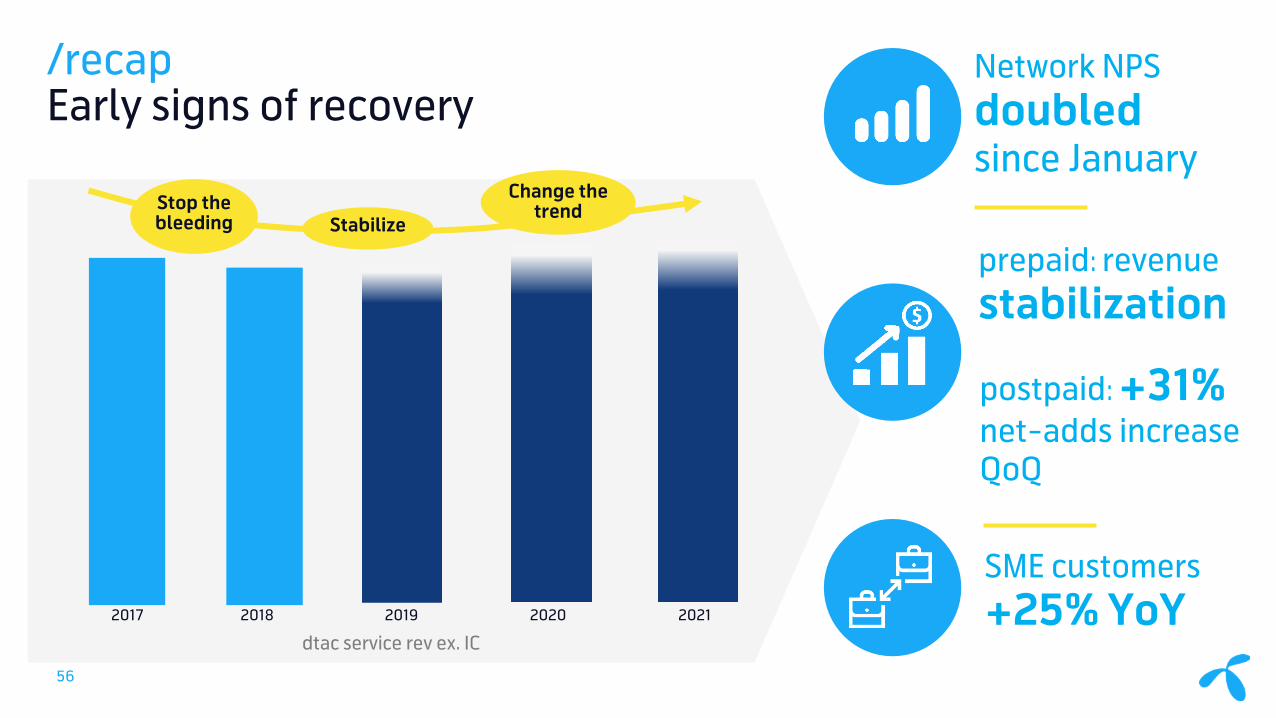

20212017 2018 2019 2020

dtac service rev ex. IC

Stop the bleeding Stabilize

Change the trend

56

/recapEarly signs of recovery

Network NPS doubled since January

prepaid: revenue stabilization

postpaid: +31% net-adds increase QoQ

SME customers +25% YoY

/innovationWe will never stop…

Electric VehiclePlatform

5G57 dtac@home

57

/disclaimer

Certain forward looking statements may be made in the course of the presentation. These forward-looking statements generally can be identified by use of statements that include words or phrases such as dtac or its management “believes”, “expects”, “anticipates”, “intends”, “plans”, “foresees”, or other words or phrases of similar import. Similarly, statements that describe dtac’s objectives, plans or goals also are forward-looking statements.

All such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those contemplated by the relevant forward-looking statement. The forward-looking statements contained in the slides are not and should not be constructed as representations of the future performance of dtac and that such statements are an expression of the Company’s reviews based on its current view and certain assumptions including, but not limited to, prevailing economic and market conditions and currently available information.

Investor RelationsE: [email protected] T: +662 202 8882

![[ppt] Powerpoint Template - Kansas Healthcare Collaborative](https://img.pdfslide.net/doc/110x75/63178f13c72bc2f2dd0584e1/ppt-powerpoint-template-kansas-healthcare-collaborative.jpg)

![[ PowerPoint Template ]](https://img.pdfslide.net/doc/110x75/631afe995d5809cabd0fa04b/-powerpoint-template-.jpg)