Embed Size (px)

Citation preview

Headline Verdana BoldUnderstand. Reflect. Respond. Kenya Budget Analysis SeminarJune 2018

Budget Analysis Seminar 2018 2

• Economic overview

• Budget overview

• Direct tax measures

• Indirect tax measures

• East Africa tax measures

• Questions & answers

Contents

Contents

3Budget Analysis Seminar 2018

Economic Overview

Gladys Makumi

Budget Analysis Seminar 2018 4

2.8% 2.8%

2.4%

3.0%3.1%

3.0%

2.3%

0%

1%

1%

2%

2%

3%

3%

4%

2014 2015 2016 2017 2018F 2019F 2020F

Gro

wth

ra

te (

%)

Global real GDP growth rates

Source: Economist Intelligence Unit

F denotes f orecast

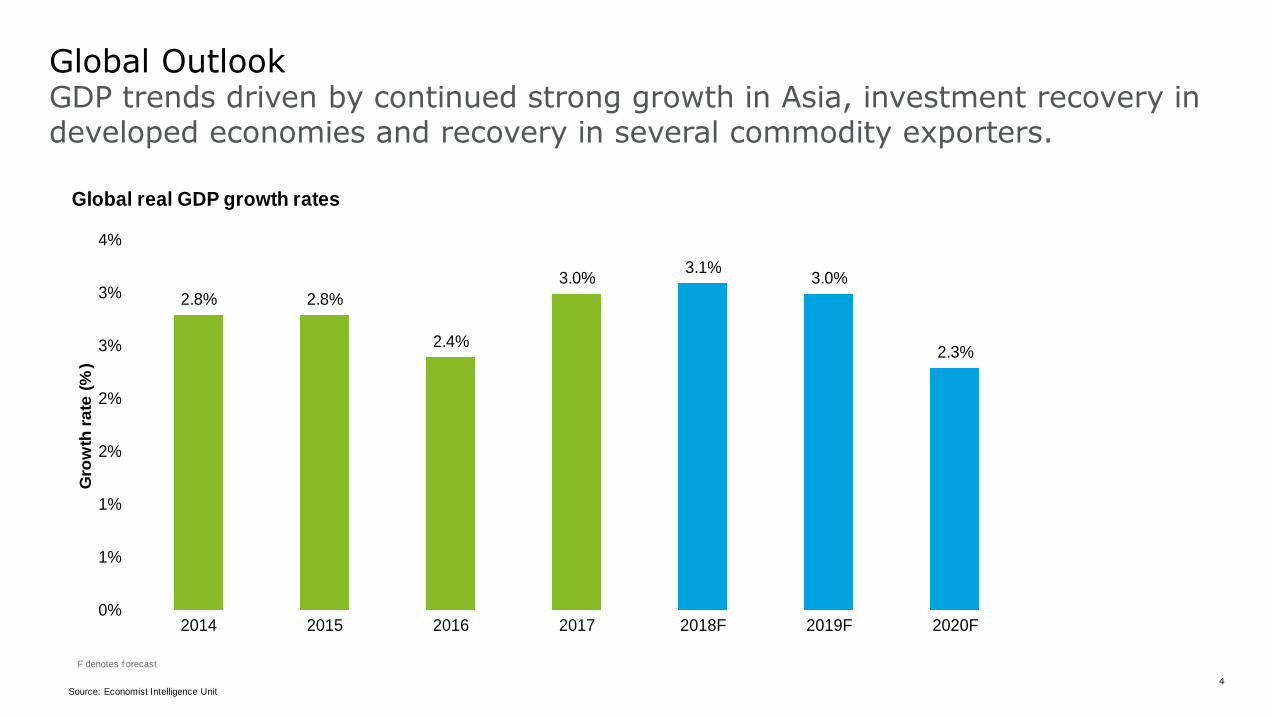

GDP trends driven by continued strong growth in Asia, investment recovery in developed economies and recovery in several commodity exporters.

Global Outlook

Budget Analysis Seminar 2018 5

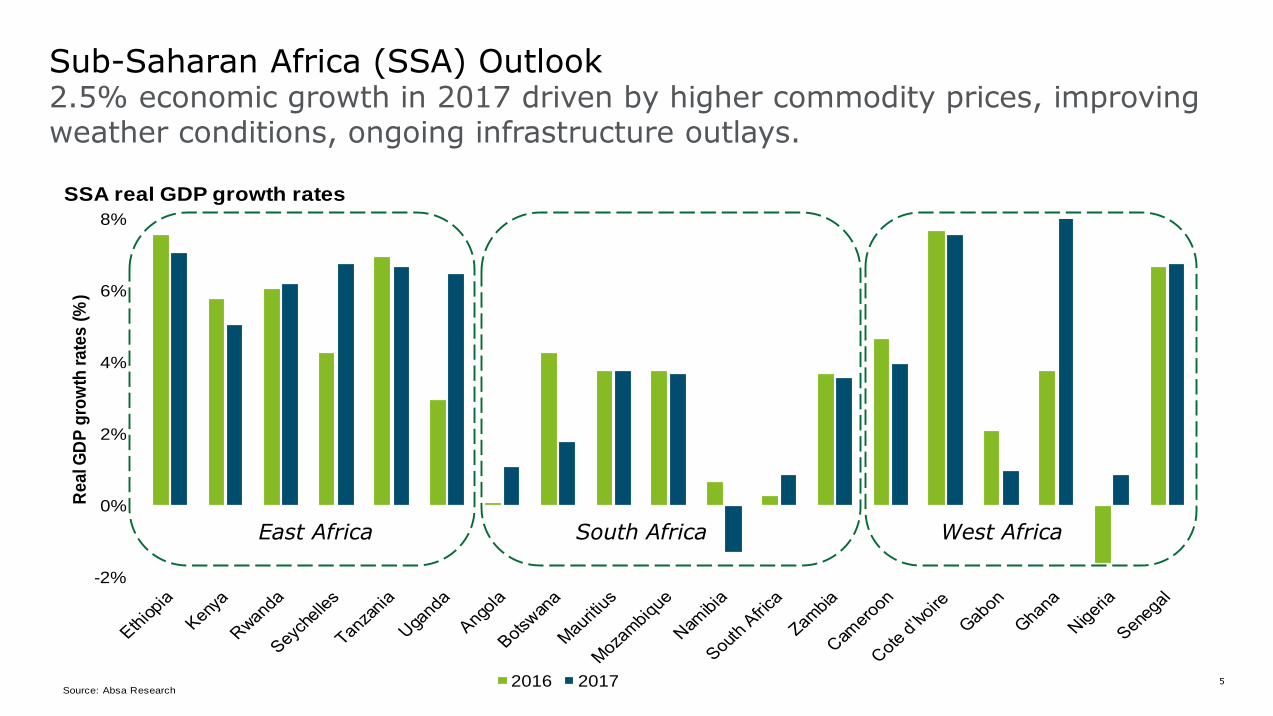

2.5% economic growth in 2017 driven by higher commodity prices, improving weather conditions, ongoing infrastructure outlays.

Sub-Saharan Africa (SSA) Outlook

-2%

0%

2%

4%

6%

8%

Re

al G

DP

gro

wth

ra

tes

(%

)

SSA real GDP growth rates

2016 2017Source: Absa Research

East Africa South Africa West Africa

Budget Analysis Seminar 2018 6

5.6% 5.6% 3.0%

6.5% 6.8% 7.0% 7.3%

7.0% 7.0%

7.0%

6.7% 7.2% 7.6% 7.8%

5.3% 5.6%

5.8%

5.1% 5.8% 5.8% 5.5%

7.0% 6.9%

6.6%

6.5%

7.0% 8.1% 8.6%

2014 2015 2016 2017 2018F 2019F 2020F

Re

al G

DP

gro

wth

ra

tes

(%)

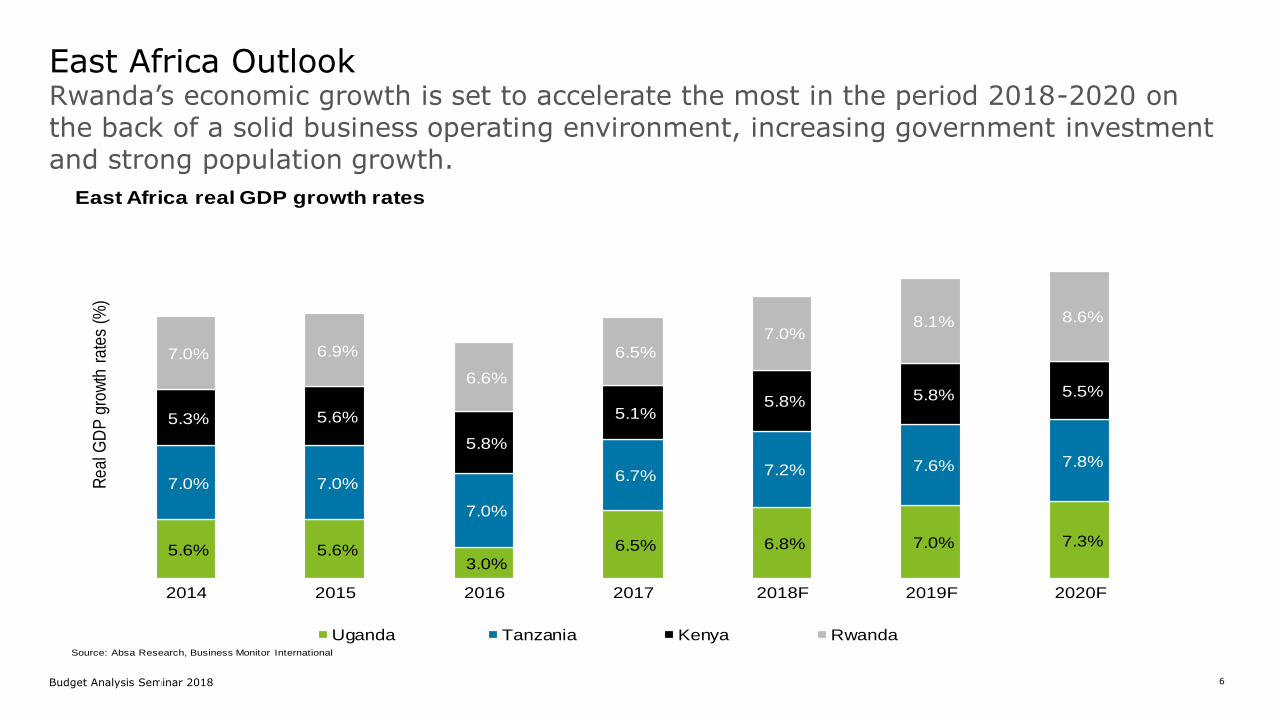

East Africa real GDP growth rates

Uganda Tanzania Kenya RwandaSource: Absa Research, Business Monitor International

East Africa OutlookRwanda’s economic growth is set to accelerate the most in the period 2018-2020 on the back of a solid business operating environment, increasing government investment and strong population growth.

Budget Analysis Seminar 2018 7

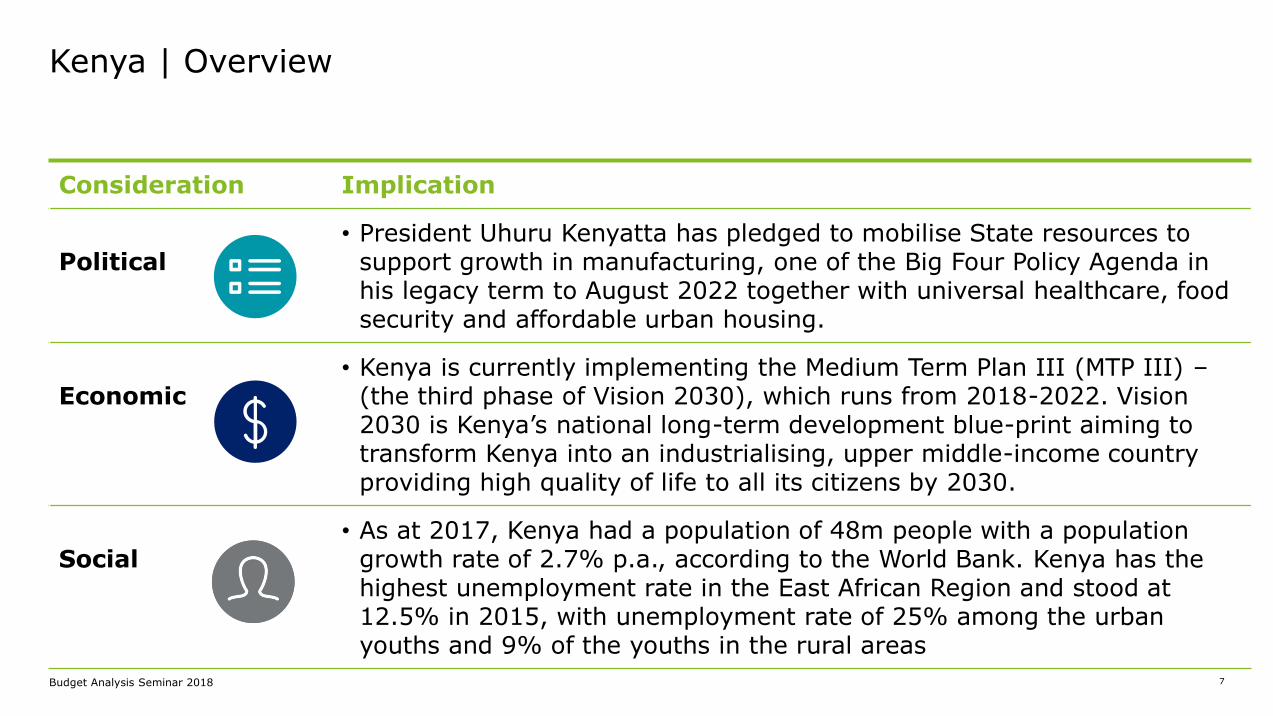

Consideration Implication

Political• President Uhuru Kenyatta has pledged to mobilise State resources to

support growth in manufacturing, one of the Big Four Policy Agenda in his legacy term to August 2022 together with universal healthcare, food security and affordable urban housing.

Economic• Kenya is currently implementing the Medium Term Plan III (MTP III) –

(the third phase of Vision 2030), which runs from 2018-2022. Vision 2030 is Kenya’s national long-term development blue-print aiming to transform Kenya into an industrialising, upper middle-income country providing high quality of life to all its citizens by 2030.

Social• As at 2017, Kenya had a population of 48m people with a population

growth rate of 2.7% p.a., according to the World Bank. Kenya has the highest unemployment rate in the East African Region and stood at 12.5% in 2015, with unemployment rate of 25% among the urban youths and 9% of the youths in the rural areas

Kenya | Overview

Budget Analysis Seminar 2018 8

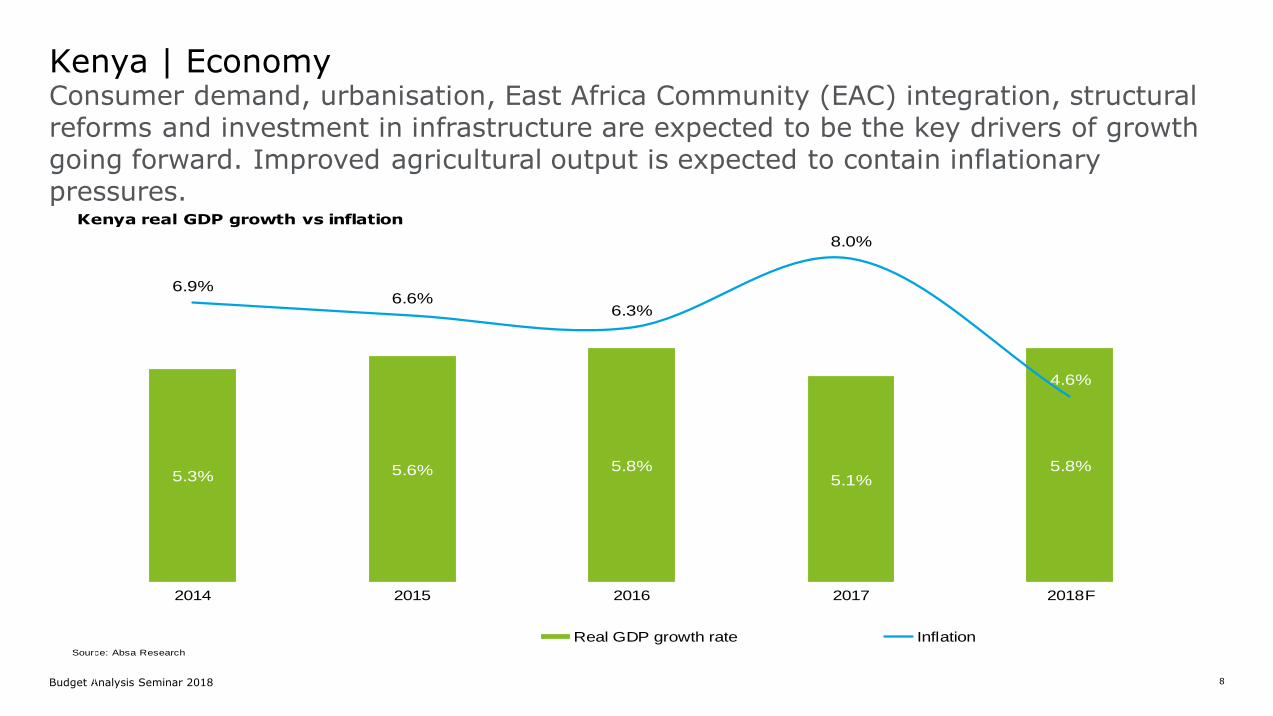

5.3% 5.6% 5.8%5.1%

5.8%

6.9%6.6%

6.3%

8.0%

4.6%

2014 2015 2016 2017 2018F

Kenya real GDP growth vs inflation

Real GDP growth rate InflationSource: Absa Research

Kenya | EconomyConsumer demand, urbanisation, East Africa Community (EAC) integration, structural reforms and investment in infrastructure are expected to be the key drivers of growth going forward. Improved agricultural output is expected to contain inflationary pressures.

Budget Analysis Seminar 2018 9

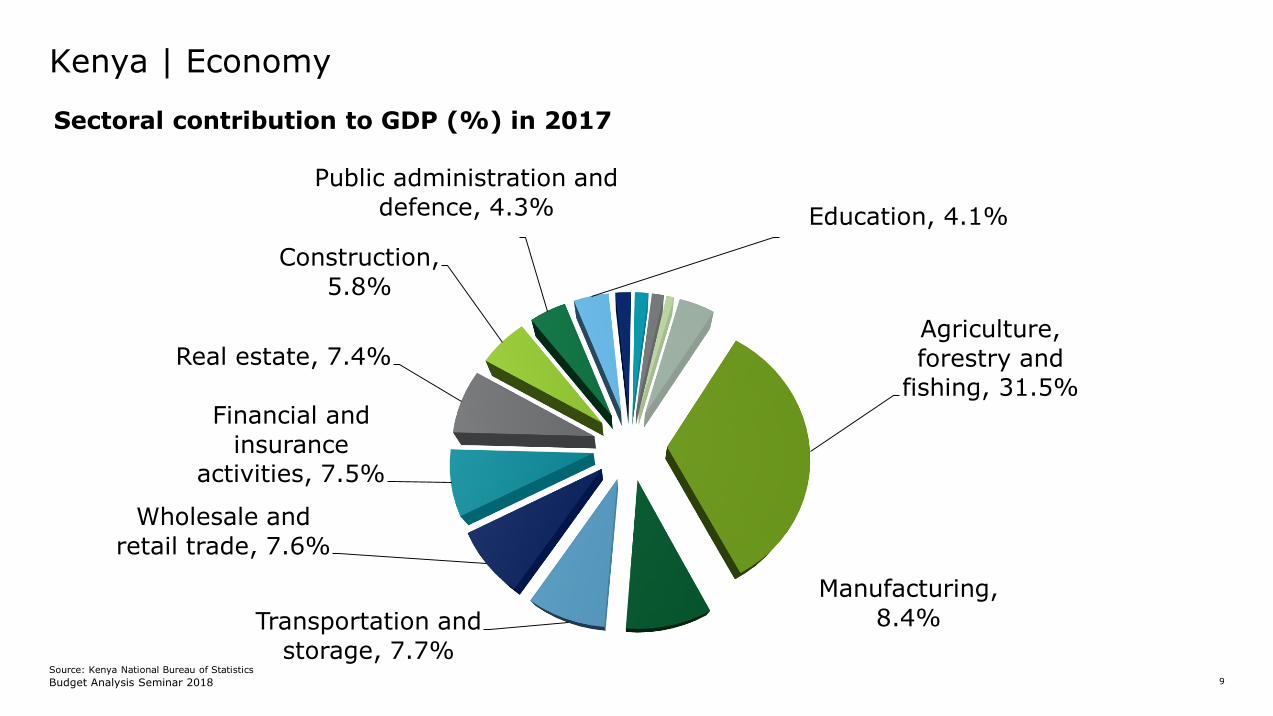

Agriculture,

forestry and fishing, 31.5%

Manufacturing,

8.4%Transportation and

storage, 7.7%

Wholesale and

retail trade, 7.6%

Financial and

insurance activities, 7.5%

Real estate, 7.4%

Construction,

5.8%

Public administration and

defence, 4.3% Education, 4.1%

Sectoral contribution to GDP (%) in 2017

Source: Kenya National Bureau of Statistics

Kenya | Economy

Budget Analysis Seminar 2018 10

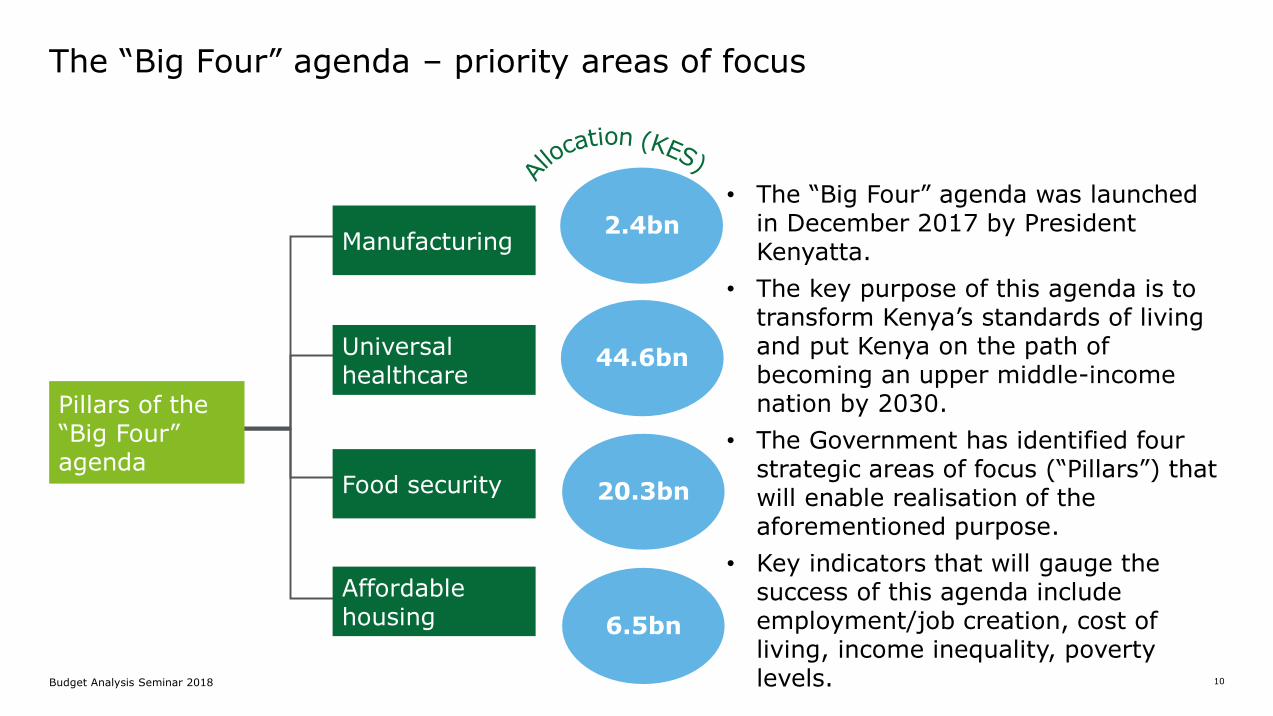

Pillars of the “Big Four” agenda

Manufacturing

Universal healthcare

Food security

Affordable housing

• The “Big Four” agenda was launched in December 2017 by President Kenyatta.

• The key purpose of this agenda is to transform Kenya’s standards of living and put Kenya on the path of becoming an upper middle-income nation by 2030.

• The Government has identified four strategic areas of focus (“Pillars”) that will enable realisation of the aforementioned purpose.

• Key indicators that will gauge the success of this agenda include employment/job creation, cost of living, income inequality, poverty levels.

2.4bn

44.6bn

20.3bn

6.5bn

The “Big Four” agenda – priority areas of focus

Budget Analysis Seminar 2018 11

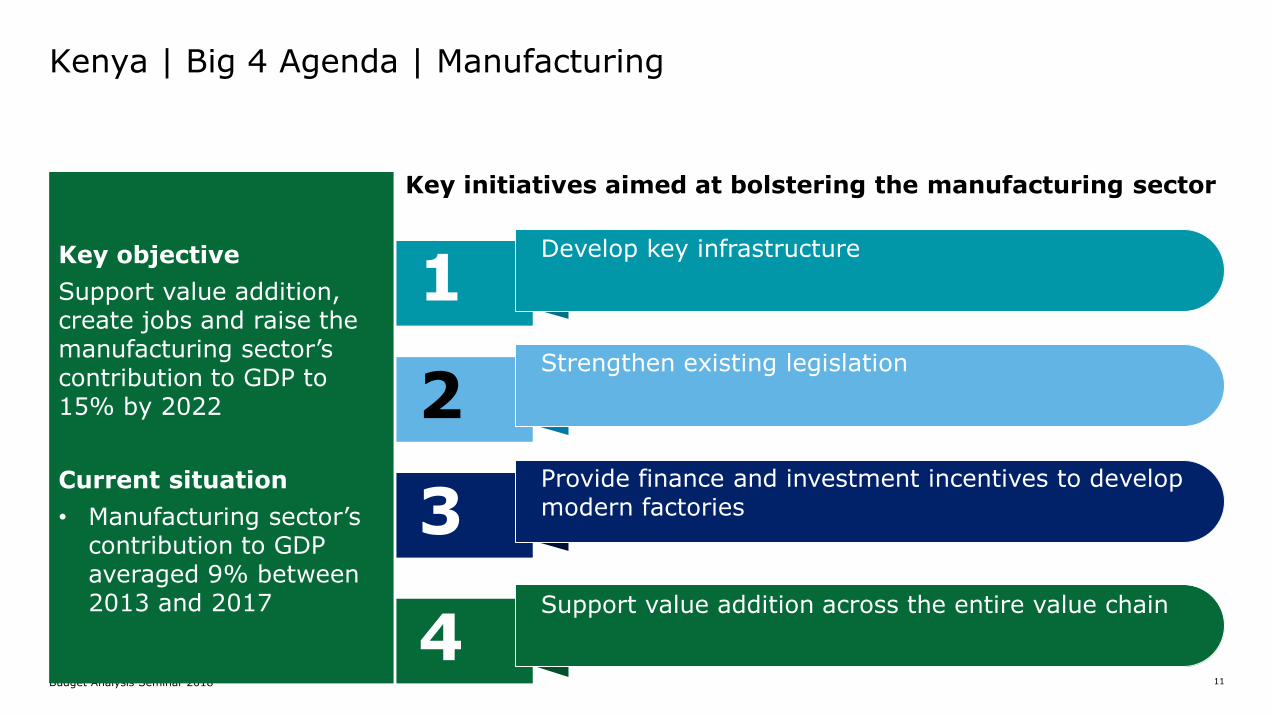

Key objective

Support value addition, create jobs and raise the manufacturing sector’s contribution to GDP to 15% by 2022

Current situation

• Manufacturing sector’s contribution to GDP averaged 9% between 2013 and 2017

Key initiatives aimed at bolstering the manufacturing sector

1

2

3

4

Develop key infrastructure

Strengthen existing legislation

Provide finance and investment incentives to develop modern factories

Support value addition across the entire value chain

Kenya | Big 4 Agenda | Manufacturing

Budget Analysis Seminar 2018 12

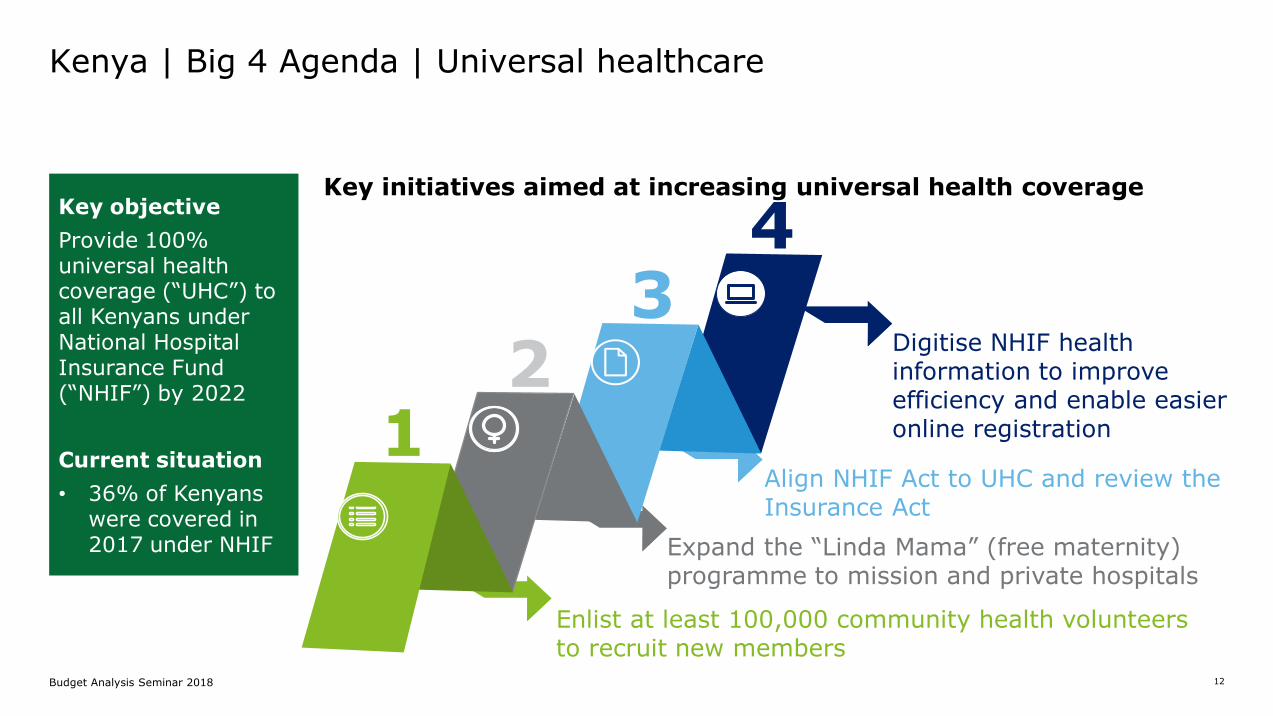

Key objective

Provide 100% universal health coverage (“UHC”) to all Kenyans under National Hospital Insurance Fund (“NHIF”) by 2022

Current situation

• 36% of Kenyans were covered in 2017 under NHIF

Key initiatives aimed at increasing universal health coverage

Enlist at least 100,000 community health volunteers to recruit new members

Align NHIF Act to UHC and review the Insurance Act

Expand the “Linda Mama” (free maternity) programme to mission and private hospitals

Digitise NHIF health information to improve efficiency and enable easier online registration1

23

4

Kenya | Big 4 Agenda | Universal healthcare

Budget Analysis Seminar 2018 13

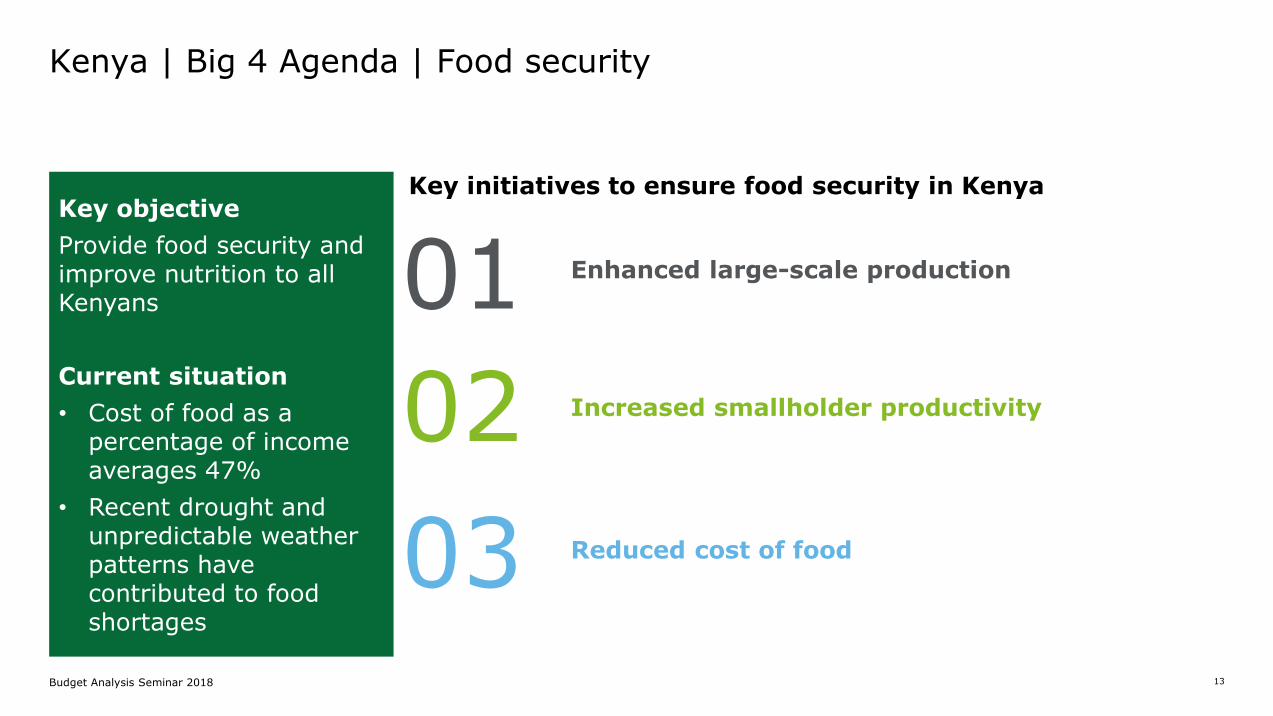

Key objective

Provide food security and improve nutrition to all Kenyans

Current situation

• Cost of food as a percentage of income averages 47%

• Recent drought and unpredictable weather patterns have contributed to food shortages

Key initiatives to ensure food security in Kenya

Enhanced large-scale production

02

01

03

Increased smallholder productivity

Reduced cost of food

Kenya | Big 4 Agenda | Food security

Budget Analysis Seminar 2018 14

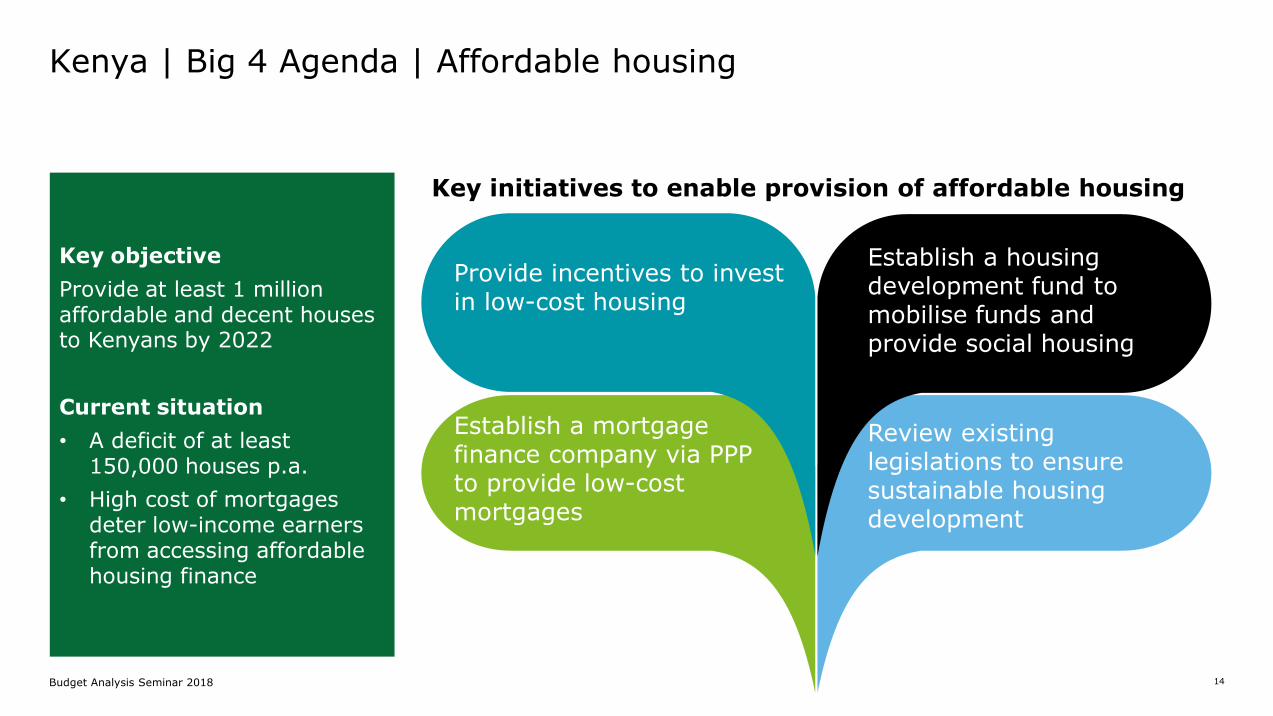

Establish a mortgage finance company via PPP to provide low-cost mortgages

Review existing legislations to ensure sustainable housing development

Provide incentives to invest in low-cost housing

Establish a housing development fund to mobilise funds and provide social housing

Key initiatives to enable provision of affordable housing

Key objective

Provide at least 1 million affordable and decent houses to Kenyans by 2022

Current situation

• A deficit of at least 150,000 houses p.a.

• High cost of mortgages deter low-income earners from accessing affordable housing finance

Kenya | Big 4 Agenda | Affordable housing

Budget Analysis Seminar 2018 15

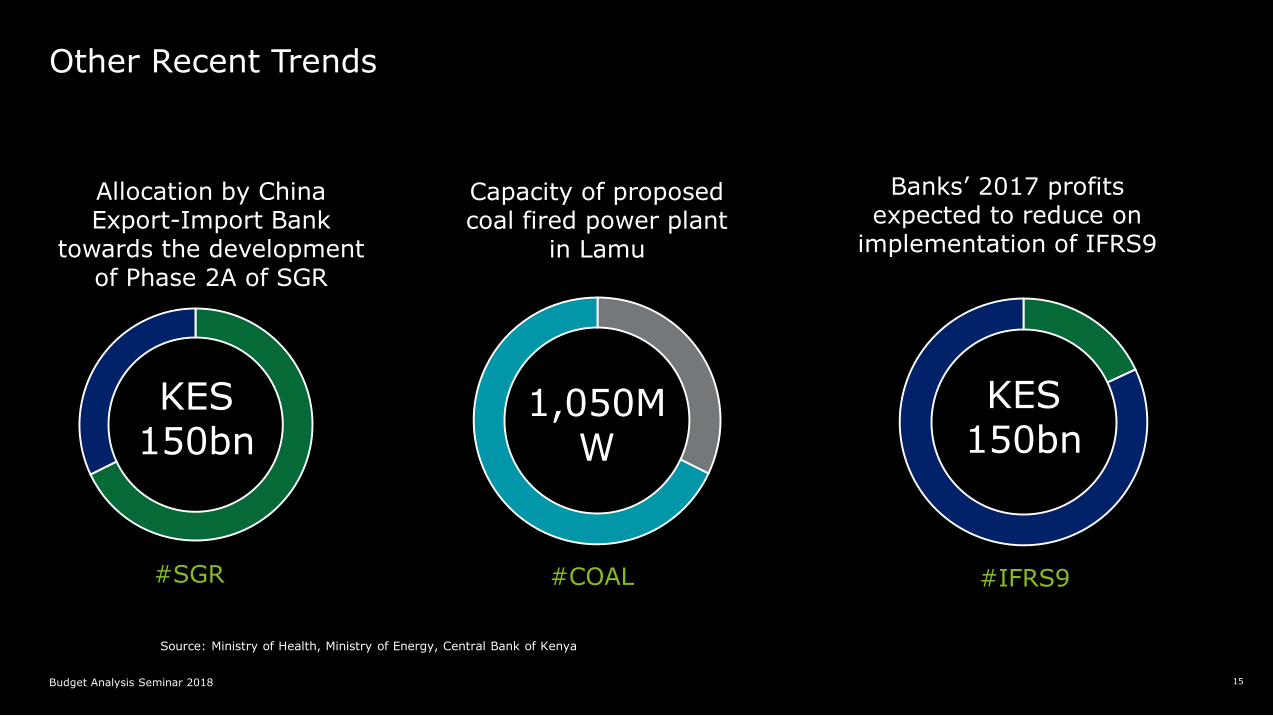

Allocation by China Export-Import Bank

towards the development of Phase 2A of SGR

Capacity of proposed coal fired power plant

in Lamu

Banks’ 2017 profits expected to reduce on

implementation of IFRS9

Source: Ministry of Health, Ministry of Energy, Central Bank of Kenya

#SGR #COAL #IFRS9

KES 150bn

1,050MW

KES 150bn

Other Recent Trends

Budget Analysis Seminar 2018 15

16Budget Analysis Seminar 2018

Budget Overview

Fred Omondi

16

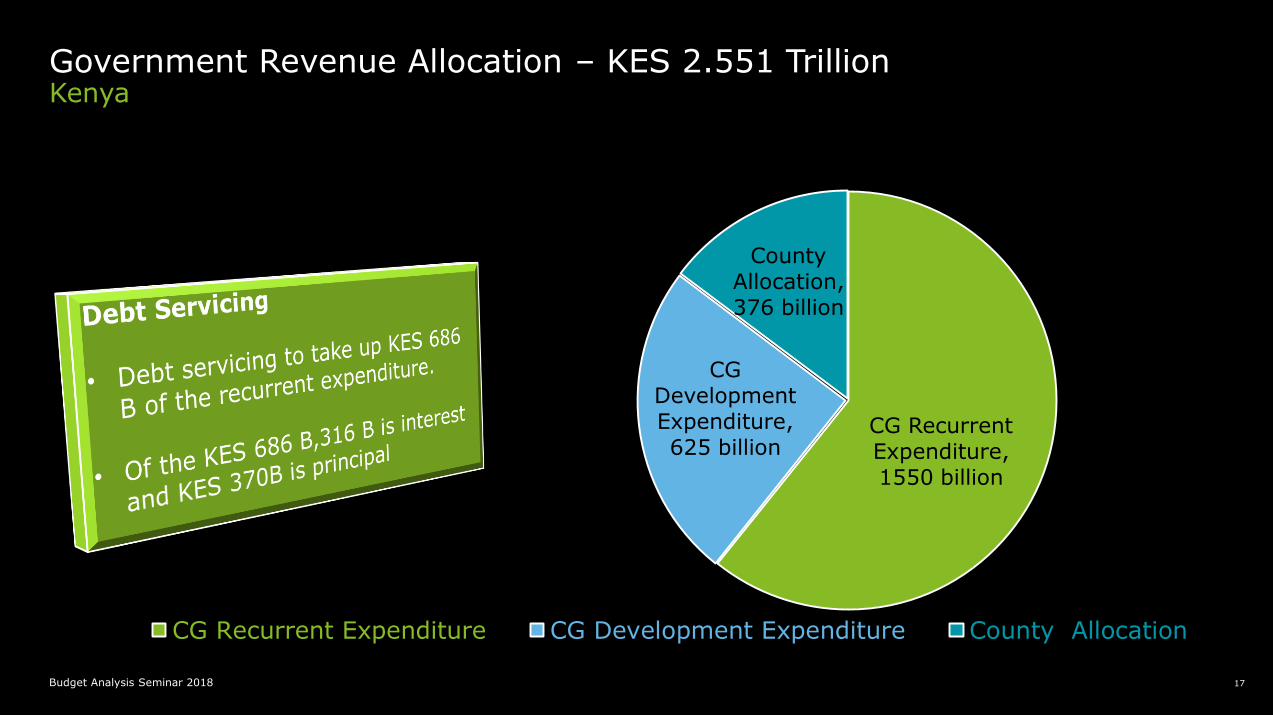

Budget Analysis Seminar 2018 17

CG Recurrent Expenditure, 1550 billion

CG Development Expenditure, 625 billion

County Allocation, 376 billion

CG Recurrent Expenditure CG Development Expenditure County Allocation

KenyaGovernment Revenue Allocation – KES 2.551 Trillion

Budget Analysis Seminar 2018 17

Budget Analysis Seminar 2018 18

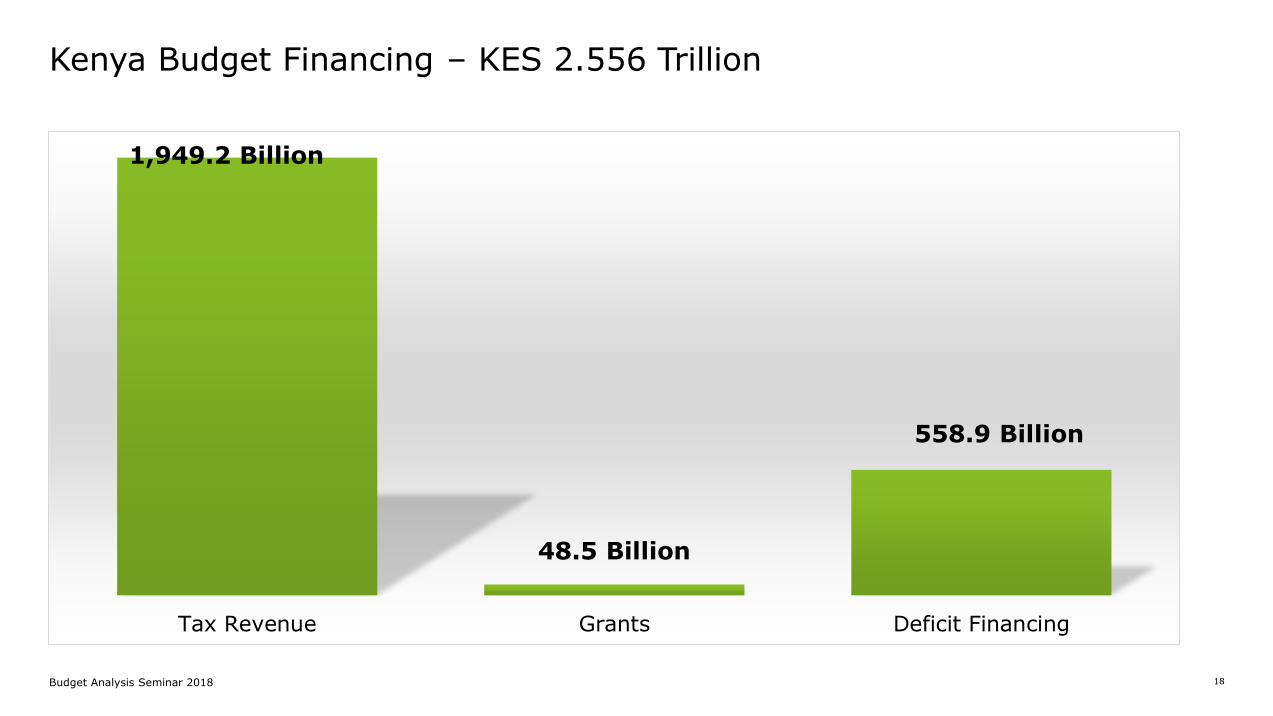

Kenya Budget Financing – KES 2.556 Trillion

1,949.2 Billion

48.5 Billion

558.9 Billion

Tax Revenue Grants Deficit Financing

Budget Analysis Seminar 2018 19

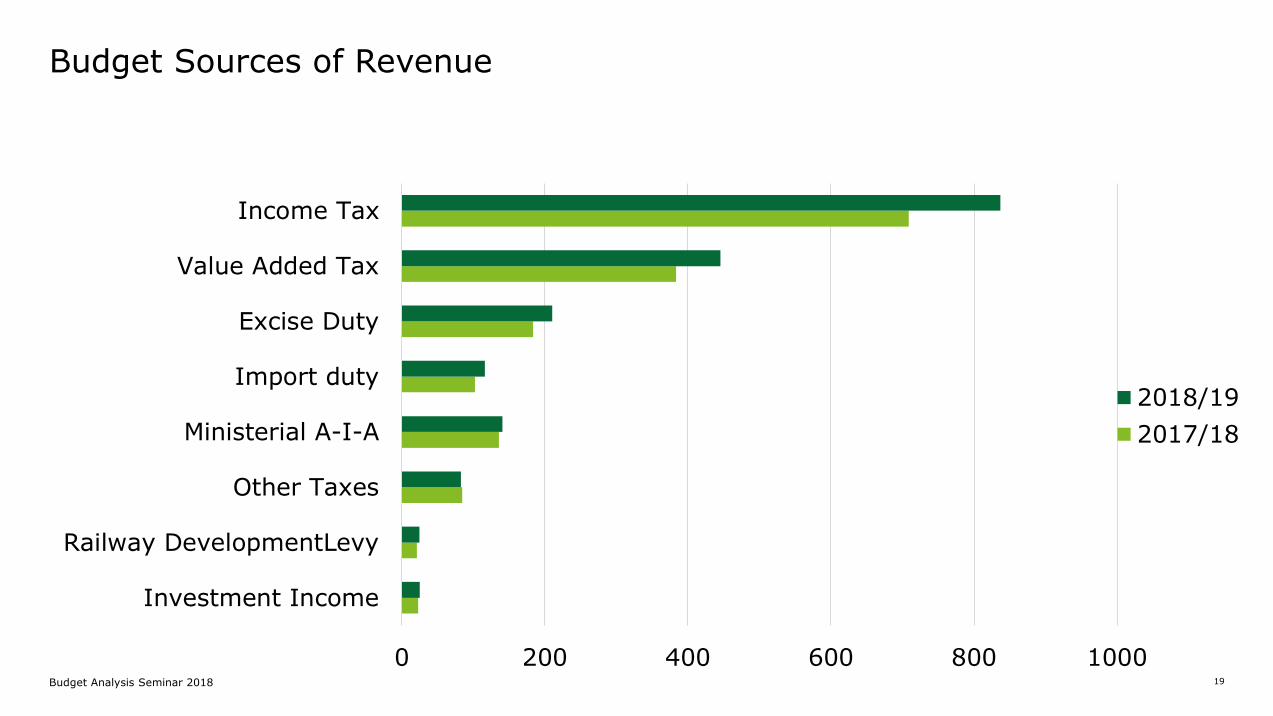

Budget Sources of Revenue

0 200 400 600 800 1000

Investment Income

Railway DevelopmentLevy

Other Taxes

Ministerial A-I-A

Import duty

Excise Duty

Value Added Tax

Income Tax

2018/19

2017/18

Budget Analysis Seminar 2018 20

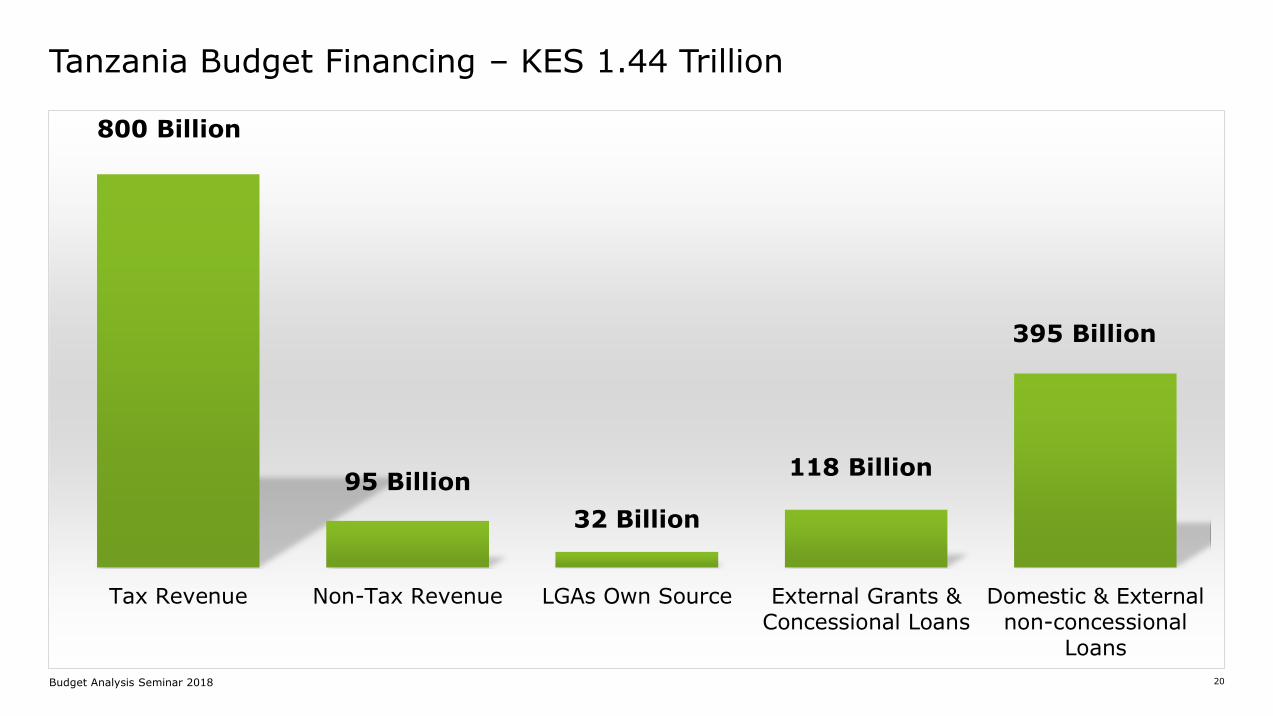

Tanzania Budget Financing – KES 1.44 Trillion

800 Billion

95 Billion

32 Billion

118 Billion

395 Billion

Tax Revenue Non-Tax Revenue LGAs Own Source External Grants &Concessional Loans

Domestic & Externalnon-concessional

Loans

Budget Analysis Seminar 2018 21

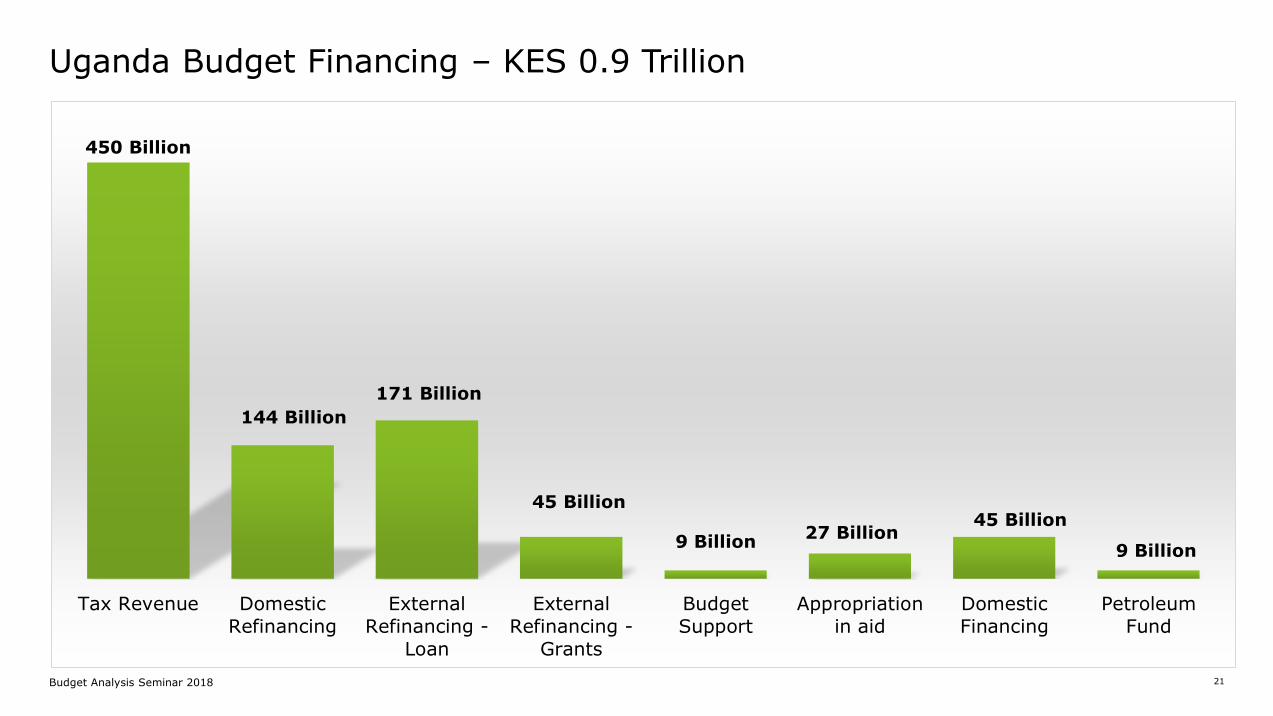

Uganda Budget Financing – KES 0.9 Trillion

450 Billion

144 Billion

171 Billion

45 Billion

9 Billion27 Billion

45 Billion

9 Billion

Tax Revenue Domestic

Refinancing

External

Refinancing -

Loan

External

Refinancing -

Grants

Budget

Support

Appropriation

in aid

Domestic

Financing

Petroleum

Fund

Budget Analysis Seminar 2018 22

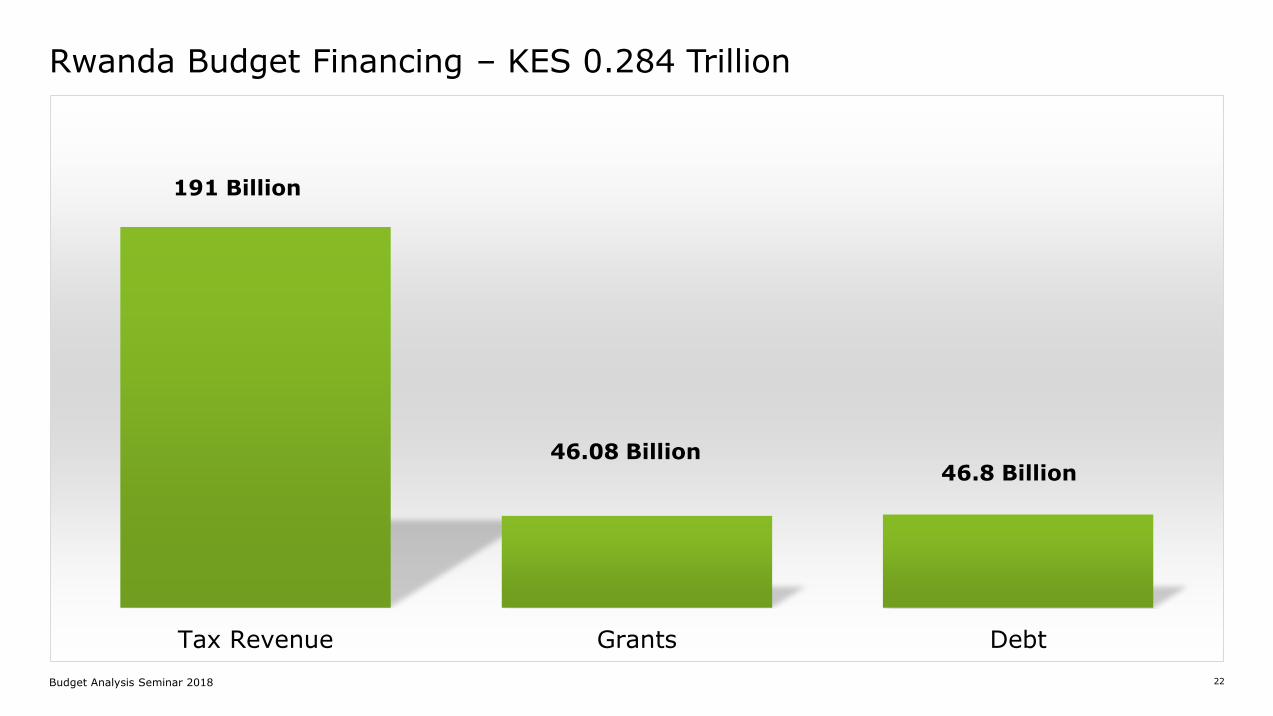

Rwanda Budget Financing – KES 0.284 Trillion

191 Billion

46.08 Billion46.8 Billion

Tax Revenue Grants Debt

23Budget Analysis Seminar 2018

Direct Tax Measures

Budget Analysis Seminar 2018 24

Corporate Income Tax

• Manufacturers to be eligible to claim an additional 30% of their electricity bills subject to conditions set by the Ministry of Energy.

• Clarification that transfer of property by general insurance companies to be taxed as capital gains.

• Deemed dividends to include distribution of any cash or assets to a shareholder or person related to the shareholder, discharge of any obligation or settlement of debt on behalf of a shareholder or use of any amount for the benefit of the shareholder or related person.

• Replacing the compensating tax provisions with corporate tax on dividends paid out of untaxed profits.

Budget Analysis Seminar 2018 25

• Withholding tax of 20% introduced on demurrage charges paid to non-residents.

• 5% withholding tax introduced on insurance premiums paid to non-residents excluding insurance premiums paid for insurance of aircrafts

Withholding Tax

Budget Analysis Seminar 2018 26

• Presumptive tax of 15% of the business permit or license fee introduced for businesses whose turnover is below KES 5 Million per annum.

• Does not apply to corporate entities; rental income or income from management and professional services.

Presumptive Income Tax

Budget Analysis Seminar 2018 27

• The proposal to introduce a 35% tax rate on individuals earning more than KES 750,000 per month under the draft Income Tax Bill 2018 has been dropped. The current top rate of 30% will be maintained.

• Amendment of the Employment Act to introduce a 1.0% contribution on employee’s gross monthly salary and a matching contribution by the employers to go into the National Housing Development Fund.

PAYE

Budget Analysis Seminar 2018 28

• The period of tax amnesty on foreign incomes has been extended from 30 June 2018 to 30 June 2019.

• Under the tax amnesty, only income accrued up to 31 December 2017 is eligible. The returns and accounts for the year 2017 have to be filed before the deadline and the income declared must be transferred back to Kenya.

• Funds declared under the amnesty will be exempt from provisions of the Proceeds of Crime and Anti-Money Laundering Act or any other act relating to reporting and investigation of financial transactions. The exemption will not apply to proceeds of terrorism, poaching and drug trafficking.

Tax Amnesty

Budget Analysis Seminar 2018 29

Tax Dispute Resolution

• Tribunal proceedings shall not be adjourned where a panel member is not available or ceases to be a member.

• Settlement of tax disputes outside the Tribunal is now set to be embedded in law. The time to be taken in such an arrangement shall be excluded from the 90 day period allowed for a Tribunal to issue a ruling.

Budget Analysis Seminar 2018 30

• Late payment interest increased from 1% to 2%.

• Late payment penalty of 20% re-introduced.

• Late filing penalty for individuals reduced to 5% of tax due or KES 2,000 whichever is higher.

• Applications for extension of due dates for tax returns filing to be made at least 15 days before due date for monthly returns and 30 days for annual returns and Commissioner to respond at least 5 days before due date.

Tax Procedures ActTax Administration

Budget Analysis Seminar 2018 31

• Late filing penalty for income tax returns:

• For corporate bodies, the penalty will be 5% of tax payable or KES 20,000, whichever is higher, whereas for individuals, the penalty will be 5% of tax payable or KES 2,000, whichever is higher.

• Limited grounds for waiver of penalty or interest, i.e. hardship or equity, impossibility or undue difficulty or expense of recovery.

Tax Procedures ActTax Administration

Budget Analysis Seminar 2018 32

• Objection to an assessment to remain valid where a person applies for extension to pay tax not in dispute.

• Obligations of tax representatives restricted to the specific taxes for which they are appointed.

• New provisions and penalties introduced in relation to unauthorized access or improper use of computerized tax systems.

Tax Procedures ActTax Administration

Budget Analysis Seminar 2018 33

• 20% penalty and 2% interest introduced on late payment of Betting, Lotteries, Gaming and Prize Competitions tax.

Betting and Gaming Taxes

Budget Analysis Seminar 2018

Budget Analysis Seminar 2018 34

• The Stamp Duty Act to be amended to include exemption from stamp duty on instruments executed for purposes of collection and recovery of tax.

• The Stamp Duty Act to be amended to exempt stamp duty from instruments relating to activities of Special Economic Zones.

Stamp Duty

Budget Analysis Seminar 2018 35

• The Banking Act to be amended by repealing Section 33B thus lifting the capping of interest rates.

• A Robin Hood Tax at the rate of 0.05% to be introduced on any amounts of KES 500,000 or more transferred through banks and other financial institutions.

• Proposed increase of the capital gains tax rate from 5% to 20% in the Income Tax Bill, 2018 to be dropped.

Other Key Changes

36Budget Analysis Seminar 2018

Income Tax Measures

Key changes under the Income Tax Bill, 2018

Budget Analysis Seminar 2018 37

• The corporate tax rate of 30% to apply on taxable income of up to KES 500m. Any amount in excess of KES 500m to be liable to 35% tax.

• Newly listed companies to be liable to a lower corporate tax rate of 25% for the subsequent 5 years if at least 40% of the issued shares are listed.

• Branch taxation: same corporate tax rate as a local company, i.e. at 30%/ 35%; however additional repatriation tax of 10% will be imposed on the after tax profits and change in net assets.

Key changes under the Income Tax Bill, 2018Corporate Income Tax

Budget Analysis Seminar 2018 38

• Deemed interest provisions to apply to any loan from a controlling non-resident advanced at a lower rate that the market interest rate applicable in the lender’s country.

• Thin capitalisation ratio reduced to 2:1.

• No deduction shall be allowed in respect of payments made by a taxpayer, which are subject to withholding tax if the taxpayer fails to withhold tax on them as required.

• Capital allowances provisions to be overhauled.

Corporate Income TaxKey changes under the Income Tax Bill, 2018

Budget Analysis Seminar 2018 39

• Transactions between resident entities or PEs and a non-resident person located in a preferential tax regime subject to TP.

• Transactions with non-resident entities where the transaction or the non-resident person lacks economic substance will be subject to TP.

• Introduction of a penalty of 2% of the value of the controlled transaction for failure to maintain TP documentation.

• Information for the foreign entities involved in intercompany transaction shall be availed to the Commissioner upon request.

• Country-by-country reports to be filed with the KRA within twelve months after the financial year-end.

• Prescribed TP for commodities and exports through related agents

Key changes under the Income Tax Bill, 2018Corporate Tax - Transfer pricing

Budget Analysis Seminar 2018 40

Key changes under the Income Tax Bill, 2018Withholding Tax

• Increase the withholding tax rate from 5% to 10% for payments to non-resident television, radio, internet and satellite operators.

• Withholding tax rate reduced from 12.5% to 10% in respect of management and professional fees paid by licensed petroleum contractors and mining companies to non-resident subcontractors.

• Increase in withholding tax rate from 5% to 10% for dividends paid to resident persons by a co-operative society including SACCOs.

• Increase the withholding tax rate from 2.5% to 3% on the income of non-resident aircraft or ship owners, operators or charterers.

Budget Analysis Seminar 2018 41

• Non-taxable per diems which were previously capped at KES 2,000 per day will be aligned to the Public Service prescribed rates.

• Taxable benefits under Employee Share Option Schemes (ESOPs) registered with the Commissioner shall accrue to the employee at the date of exercising the option.

• The tax rate applicable to pensions or retirement annuities received by non-resident individuals has been increased from 5% to 10%.

• The minimum taxable threshold for Non-cash benefits of KShs. 36,000 p.a. has been done away with.

• Pensions earned in respect of employment in other East Africa Community states will not be taxable in Kenya.

Key changes under the Income Tax Bill, 2018PAYE

42Budget Analysis Seminar 2018

East Africa: Key Direct Tax Measures

Budget Analysis Seminar 2018 43

• The 10 year Income Tax exemption /Holiday which was granted to SACCOs in 2017 has been repealed. SACCOs will now be required to pay tax.

• Income tax holiday granted to industrial park or free zone developers as follows:

− 10 year holiday if capital is USD 200 million or more.

− 5 year holiday if capital is USD 30 million or in the case of a Ugandan citizen investor, USD 10 million.

• “Group” entities interest deduction capped to 30% of tax earnings before Interest, Tax, Depreciation and Amortization (EBITDA) with excess allowed for carry forward for up to 3 years; Thin capitalization rules scrapped.

• Entities with successive tax losses for seven years to pay turnover tax of 0.5%.

• A direct or indirect change of 50% or more within a 3 year period for an entity to be considered a sale subject to Income Tax in Uganda.

• The Inter-Governmental Agreement on the East African Crude Oil Pipeline to have the same status as a Double Taxation Agreement (DTA).

Income Tax - Uganda

Budget Analysis Seminar 2018 44

• Introducing a different withholding tax rate of 1% for agricultural supplies above UGX 1 million made to designated agents instead of the 6% withholding tax that was previously applicable.

• Introducing a 10% final withholding tax on all commissions paid by telecom companies for airtime distribution or provision of mobile money services.

• African Trade Insurance Agency exempted from Income Tax.

• Taxes due and unpaid by Government as at 30 June 2018 to be waived.

• Mediation introduced as one of the mechanisms for resolving tax disputes brought before the Tax Appeals Tribunal (TAT).

• TAT given powers similar to the High Court to award damages, interest or any other remedy against any party.

• Inclusion of the weekly and monthly return filling requirements for persons in the Gaming and Betting industry.

Income Tax - Uganda

Budget Analysis Seminar 2018 45

• Reduction of corporate income tax rate from 30% to 20% for new investors in the pharmaceutical and leather industries for five years from 2018/2019 to 2022/2023.

• The Minister responsible for finance will no longer be restricted from providing income tax exemption to government projects financed by non-concessional loans i.e. loans with market based interest rates. The current provisions of the income tax legislation limits the Minister’s power to exempt income derived from such projects.

• Introduction of withholding tax exemption on interest paid on Government loans provided by Banks and Financial Institutions to finance government projects.

• The Government intends to introduce 100% tax amnesty on interest and penalties to encourage compliance. The amnesty will be valid from 1 July 2018 to 31 December 2018.

Income Tax - Tanzania

Budget Analysis Seminar 2018 46

Some of the changes introduced in the new law are:

• Introduction of capital gains tax on the transfer of shares at a rate of 5%.

• Bringing the indirect transfer of shares into the scope of taxation in Rwanda.

• Capping of the deductibility of service payments to non-residents (related and unrelated) to 25 of the turn-over.

• Bringing director’s fees into the scope of withholding tax at 30%.

• Introducing the requirement for companies to maintain transfer pricing documentation.

• Requirement to withhold tax on dividends paid to resident companies.

• The widening of the definition of paid to include accruals for services that are held for more than 6 months in a tax period.

There were no measures on income taxes in this years budget. Rwanda introduced a new Income tax Law (Law No 016/2018 of 13/04/2018 establishing taxes on income)

Income Tax - Rwanda

47Budget Analysis Seminar 2018

Indirect Tax Measures

Lillian Kubebea

48Budget Analysis Seminar 2018

Kenya

Budget Analysis Seminar 2018 49

• Equipment for the construction of grain storage facilities.

• Additional raw materials for the manufacture of animal feeds.

• Parts imported or purchased locally for the assembly of computers.

VAT exemption introduced on the following items

Value Added Tax

Budget Analysis Seminar 2018 50

• Taxable value of mobile cellular to be determined in accordance with the VAT Act.

• Late filing penalty to be moved from the VAT Act to the Tax Procedures Act but penalty remains the same.

• Wheat and barley seed which are currently VAT-able to be exempt.

• Maize (corn) seed to be subject to VAT.

• Garments and leather footwear manufactured in an EPZ to be VAT-able upon importation.

• Transportation of cargo to destinations outside Kenya to be deleted from exempt schedule.

• Alcoholic and non-alcoholic beverages supplied to DEFCO to be exempt.

• Exemption of goods and services for direct and exclusive use in projects under special operating framework with the Government.

• Exemption of postal services (postage, rental of post boxes and mail bags).

Other key changesValue Added Tax

Budget Analysis Seminar 2018 51

Customs Duty

• Grant of stay of application on the following products:

− Assorted range of metal and metal products at varying increased rates.

− Non electric cooking appliances at 35%.

− Leather and footwear at 35% or USD 10 per pair.

− Refined edible oil products at 35% or USD 500/MT.

− New textiles and apparels at 35% or USD5/Kg.

− Particle boards, Medium Density Fibre board (MDFs), plywood & block boards at various rates.

− Aluminium Roll on Pilfer Proof (Bottle Tops) at 35% or USD 0.01 per piece.

− Assorted paper and paperboard products at 35%.

Stay of application of the CET

Budget Analysis Seminar 2018 52

• Extension of stay of application of the CET rate on rice, products of iron or non alloy steel of heading 7209, LPG, leaf springs, worn clothing, road tractors for semi-trailers, safety matches, and styrene acrylic.

Stay of application of the CETCustoms Duty

Budget Analysis Seminar 2018 53

• Introduction of export levy on copper waste and scrap at 20%.• Exemption of goods imported for implementation of projects under special operating

framework arrangement with the Government from RDL and IDF.

Miscellaneous Fees & Levies

Budget Analysis Seminar 2018 54

• Increase of excise duty on:

− private passenger motor vehicles (diesel powered of above 2500cc and petrol powered of above 250cc) from 20% to 30%.

− fees charged for money transfer services by cellular phone service providers from 10% to 12%.

− kerosene from Kshs. 7,205 per 1000 litres to Kshs. 10,305 per 1,000 litres.

• Introduction of a Robin Hood Tax of 0.05% on any amounts of KShs 500,000 or more transferred by banks, money transfer agencies and other financial service providers.

• Introduction of excise duty on sugar confectionery and chocolate at Kshs. 20 per Kg

• Inflationary adjustment of specific rates to be effected annually.

Excise Duty

Budget Analysis Seminar 2018 55

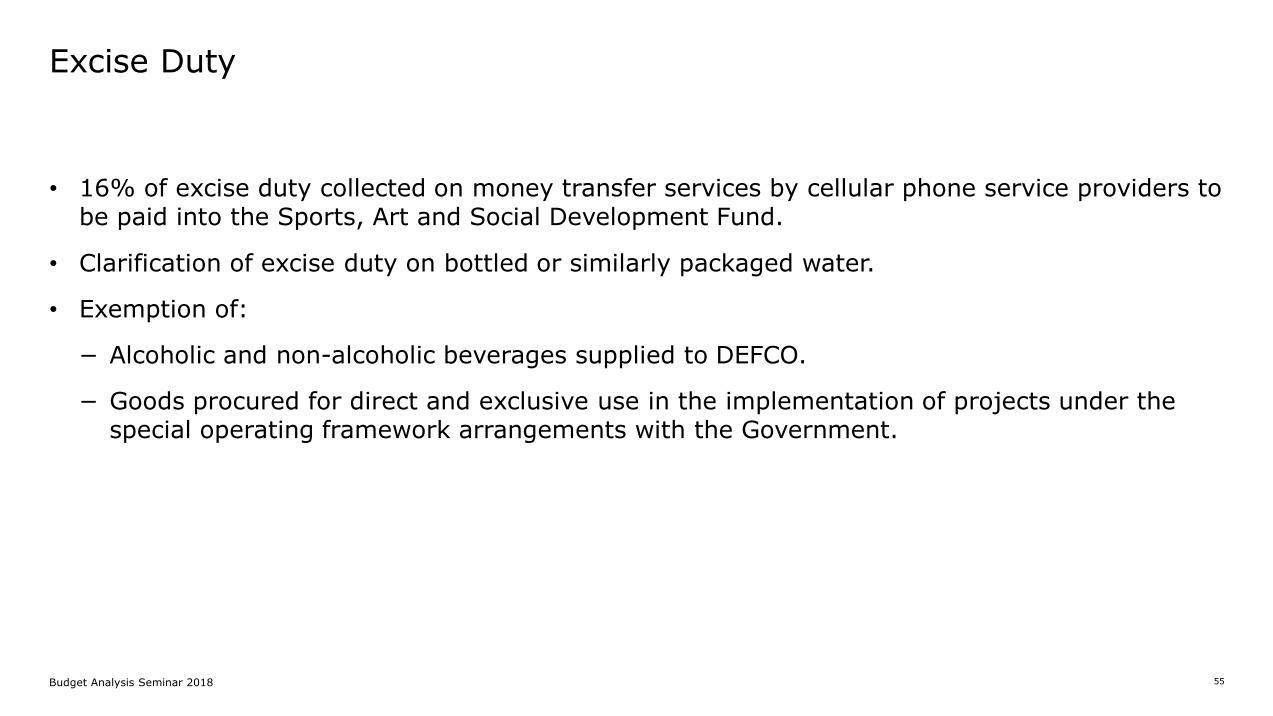

• 16% of excise duty collected on money transfer services by cellular phone service providers to be paid into the Sports, Art and Social Development Fund.

• Clarification of excise duty on bottled or similarly packaged water.

• Exemption of:

− Alcoholic and non-alcoholic beverages supplied to DEFCO.

− Goods procured for direct and exclusive use in the implementation of projects under the special operating framework arrangements with the Government.

Excise Duty

Budget Analysis Seminar 2018 56

Customs Duty

Budget Analysis Seminar 2018 57

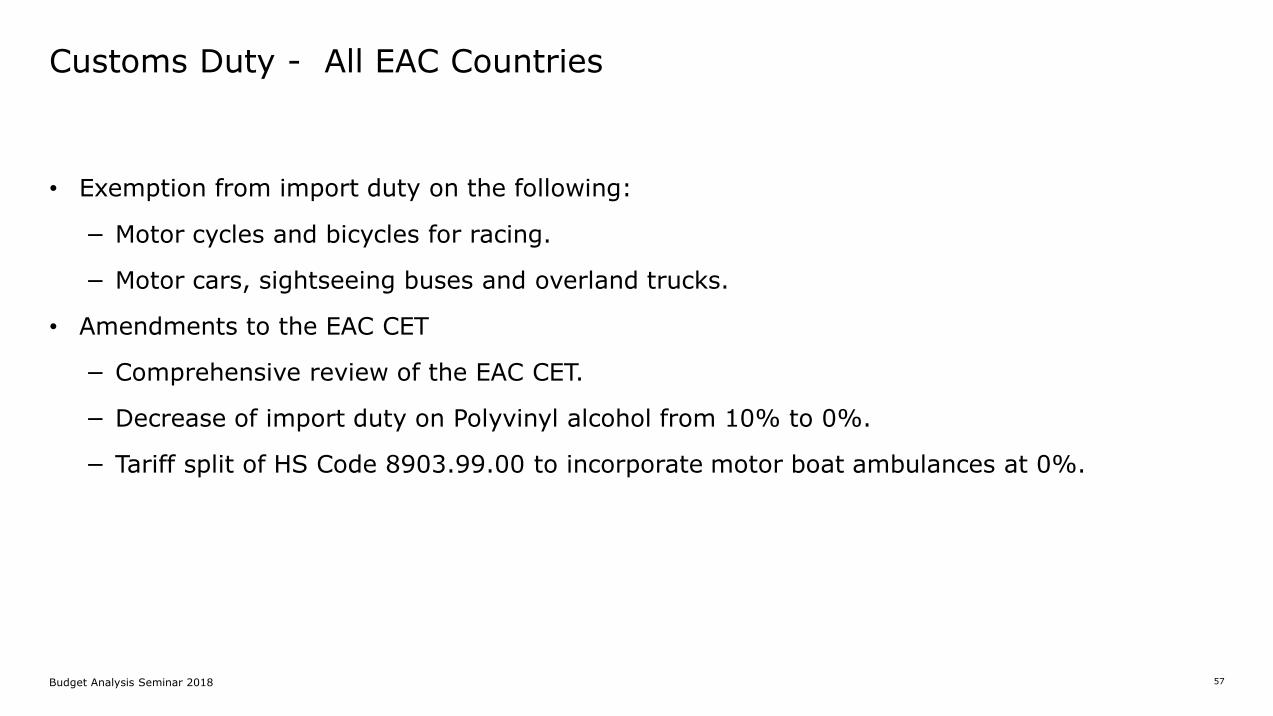

• Exemption from import duty on the following:

− Motor cycles and bicycles for racing.

− Motor cars, sightseeing buses and overland trucks.

• Amendments to the EAC CET

− Comprehensive review of the EAC CET.

− Decrease of import duty on Polyvinyl alcohol from 10% to 0%.

− Tariff split of HS Code 8903.99.00 to incorporate motor boat ambulances at 0%.

Customs Duty - All EAC Countries

Budget Analysis Seminar 2018 58

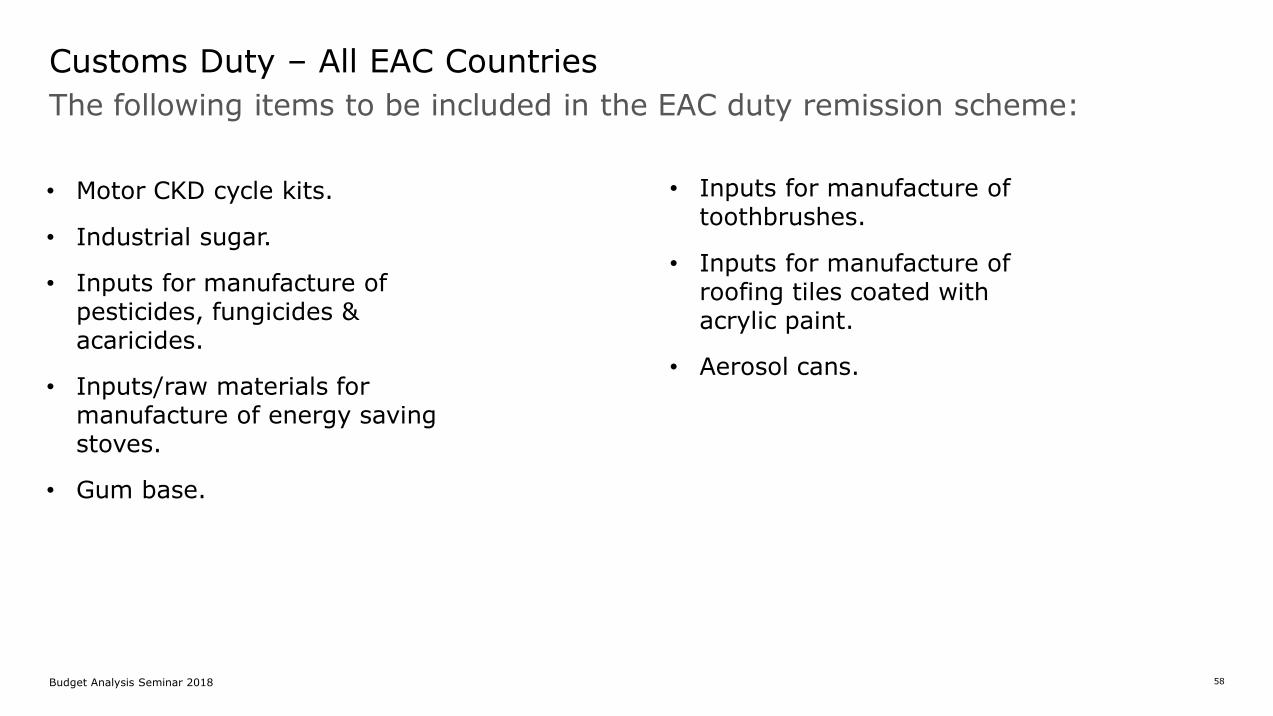

The following items to be included in the EAC duty remission scheme:

Customs Duty – All EAC Countries

• Motor CKD cycle kits.

• Industrial sugar.

• Inputs for manufacture of pesticides, fungicides & acaricides.

• Inputs/raw materials for manufacture of energy saving stoves.

• Gum base.

• Inputs for manufacture of toothbrushes.

• Inputs for manufacture of roofing tiles coated with acrylic paint.

• Aerosol cans.

Budget Analysis Seminar 2018 59

• Grant of stay of application of CET rate on flat-rolled products of iron or non-alloy steel at 10% or 250 per MT instead of 10%.

Stay of application of CET Rates

Customs Duty – All EAC Countries

Budget Analysis Seminar 2018 60

• Gypsum powder.

• Crude palm oil, crude edible oils semi-refined & refined edible oils.

• Nails, tacks, drawing pins, corrugated nails & staples .

• Safety matches.

• Potatoes.

Customs Duty – Tanzania

Extension of stay of application of the CET on wheat grain and Electronic Fiscal Devices (EFD’s) used to collect Government Revenue.

• Chewing gum & other sugar confectionary.

• Tomato sauce.

• Mineral water.

• Meat and edible offal.

• Sausages and similar products.

Grant of stay of application on the following products:

Budget Analysis Seminar 2018 61

The following items were included in the duty remission scheme

• Paper used to manufacture exercise books and textbooks.

• Paper used as raw materials for manufacturing of gypsum.

• Self-adhesive label.

• Printed aluminum barrier laminates (ABL).

• Inputs used to manufacture pesticides, fungicides, insecticides, and acaricides.

• RBD Palm stearin (palm oil).

Imposition of import duty at 35% of consumption sugar imported under specific arrangements.

Customs Duty – Tanzania

Budget Analysis Seminar 2018 62

• Road tractors.

• Transport vehicles with carriage capacity of over 5 tons.

• Public transport vehicles that carry over 25 persons.

• Processing machines and other materials to be used in textile and hides manufacture.

Customs Duty – Rwanda

Reduction of duty on bicycles used for championships from 20% to 0%.

• ICT equipment.

• Equipment used by banks in money circulation (ATM cards, PoS, etc.)

• Second hand clothes & shoes.

• Imported rice and sugar.

• Imported products designated for army shops.

•

Grant of stay of application on the following products:

Budget Analysis Seminar 2018 63

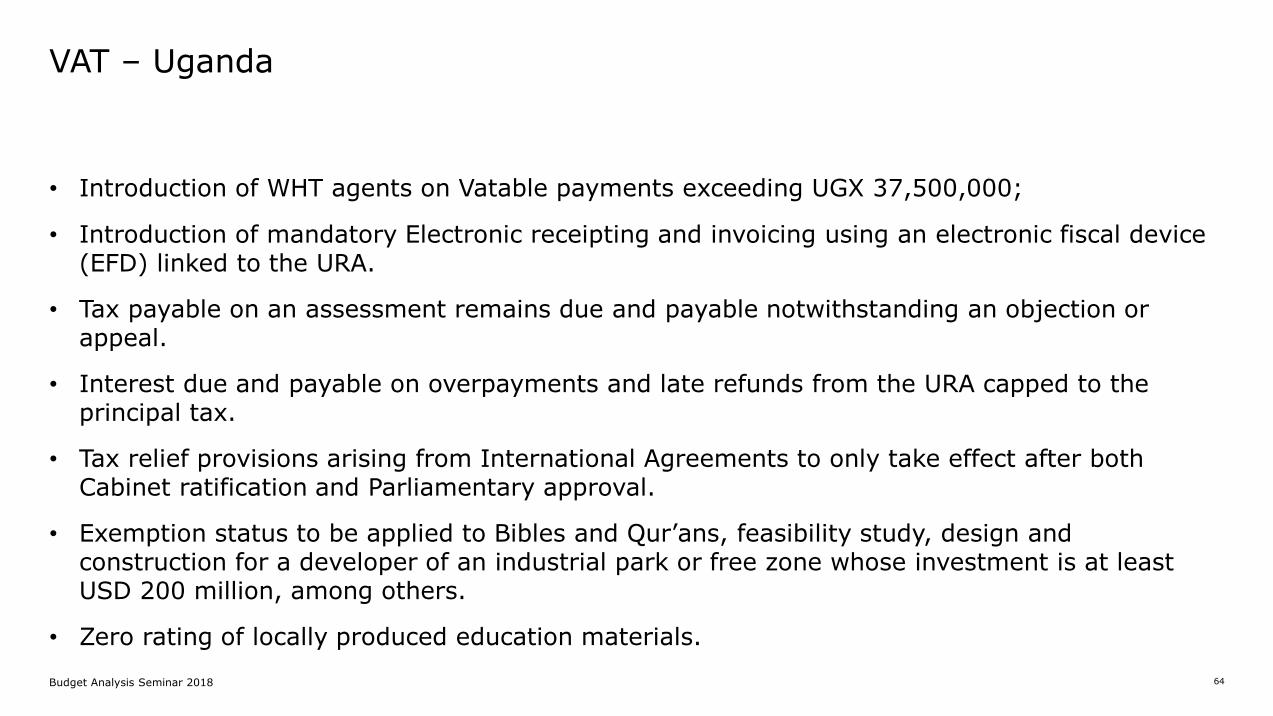

VAT

Budget Analysis Seminar 2018 64

• Introduction of WHT agents on Vatable payments exceeding UGX 37,500,000;

• Introduction of mandatory Electronic receipting and invoicing using an electronic fiscal device (EFD) linked to the URA.

• Tax payable on an assessment remains due and payable notwithstanding an objection or appeal.

• Interest due and payable on overpayments and late refunds from the URA capped to the principal tax.

• Tax relief provisions arising from International Agreements to only take effect after both Cabinet ratification and Parliamentary approval.

• Exemption status to be applied to Bibles and Qur’ans, feasibility study, design and construction for a developer of an industrial park or free zone whose investment is at least USD 200 million, among others.

• Zero rating of locally produced education materials.

VAT – Uganda

Budget Analysis Seminar 2018 65

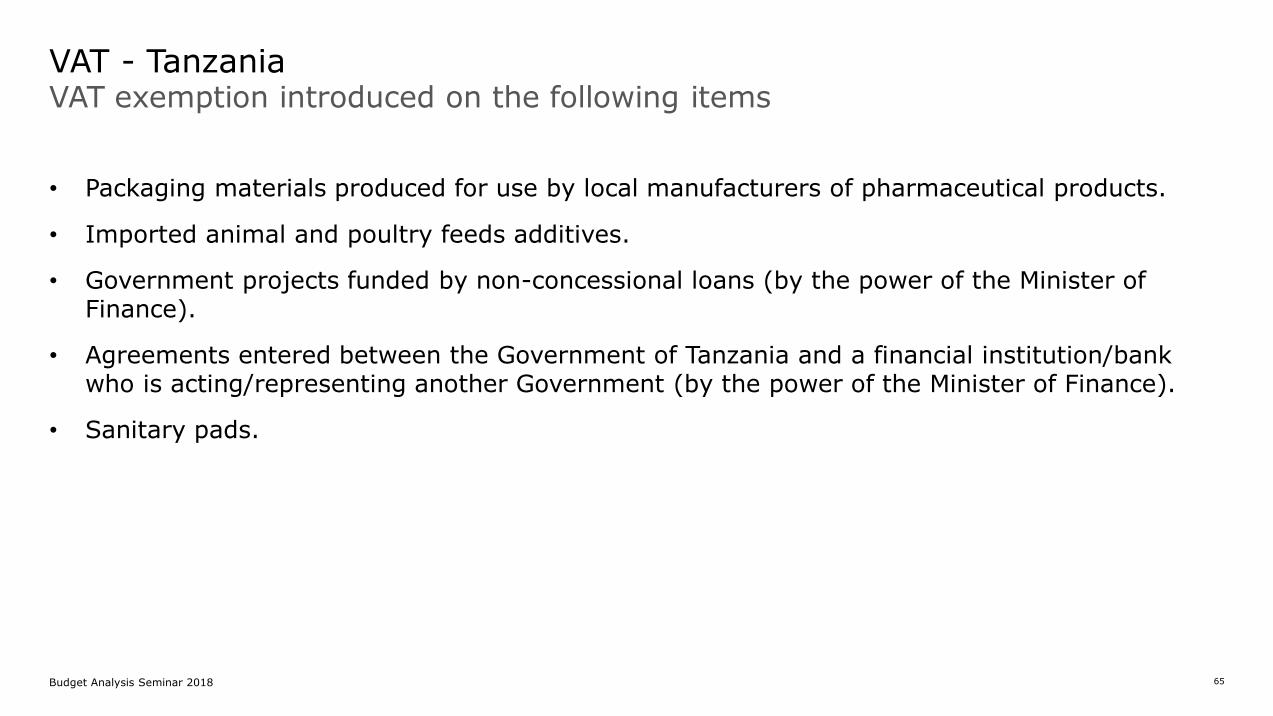

• Packaging materials produced for use by local manufacturers of pharmaceutical products.

• Imported animal and poultry feeds additives.

• Government projects funded by non-concessional loans (by the power of the Minister of Finance).

• Agreements entered between the Government of Tanzania and a financial institution/bank who is acting/representing another Government (by the power of the Minister of Finance).

• Sanitary pads.

VAT exemption introduced on the following items VAT - Tanzania

Budget Analysis Seminar 2018 66

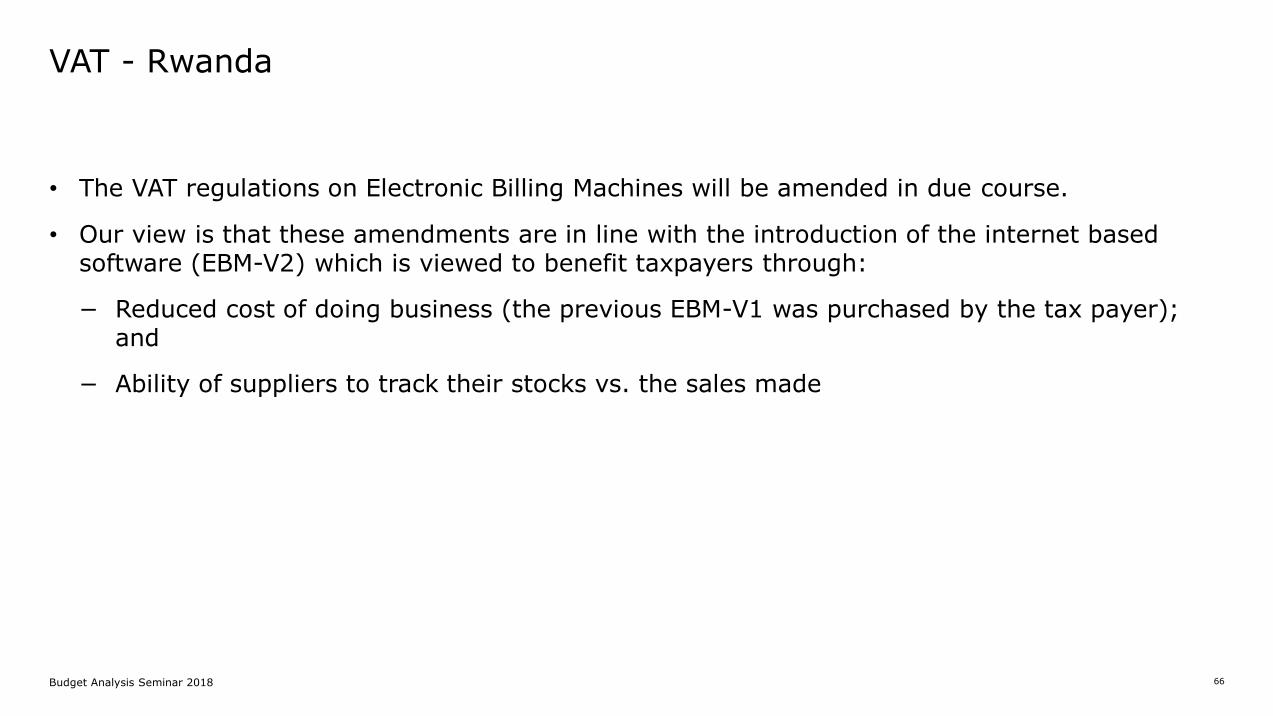

• The VAT regulations on Electronic Billing Machines will be amended in due course.

• Our view is that these amendments are in line with the introduction of the internet based software (EBM-V2) which is viewed to benefit taxpayers through:

− Reduced cost of doing business (the previous EBM-V1 was purchased by the tax payer); and

− Ability of suppliers to track their stocks vs. the sales made

VAT - Rwanda

Budget Analysis Seminar 2018 67

Excise Duty

Budget Analysis Seminar 2018 68

• Excise duty on use of internet at UGX 200 per user per day of access.

• Refund of excise duty paid on goods that are later exported.

• Amendment to penalty related provisions.

• Amendment of excise duty from ad valorem to hybrid rates on some spirits and wine.

• Excise duty rates increased on various financial and telecommunication services.

• Introduction of excise duty on opaque beer, powder for making juice or taste drinks, motor cycles, cooking oil, mobile money transactions.

• Excise duty removed on some construction materials, furnishings and fittings.

Excise Duty - Uganda

Budget Analysis Seminar 2018 69

• Increase in excise duty on imported water, beer, non-alcoholics, fruit juices, wine, spirits, cigarettes, cut rag or cut filler.

• Introduction of excise duty on wine produced with domestic fruits other than grapes e.g. bananas, tomatoes.

• Introduction of Electronic Tax Stamp from 1 September 2018.

Excise Duty - Tanzania

Budget Analysis Seminar 2018 70

• Amendment of the consumption tax law to increase consumption tax on cigarettes and alcoholic beverages.

Excise Duty - Rwanda

Budget Analysis Seminar 2018 71

Questions and Answers

Disclaimer

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or its and their affiliates are, by means of this publication, rendering

accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be

used as a basis for any decision or action that may affect your finances or your business. Before making any decision or taking any action that may affect your finances or your business,

you should consult a qualified professional adviser.

None of Deloitte Touche Tohmatsu Limited, its member firms, or its and their respective affiliates shall be responsible for any loss whatsoever sustained by any person who relies on this

publication.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private Company limited by guarantee, and its network of member firms, each of which is a legally separate and

independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more

than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte's

approximately 263,900 professionals are committed to becoming the standard of excellence.

© 2018 Deloitte Consulting Limited. Member of Deloitte Touche Tohmatsu Limited

![[ppt] Powerpoint Template - Kansas Healthcare Collaborative](https://img.pdfslide.net/doc/110x75/63178f13c72bc2f2dd0584e1/ppt-powerpoint-template-kansas-healthcare-collaborative.jpg)