Embed Size (px)

Citation preview

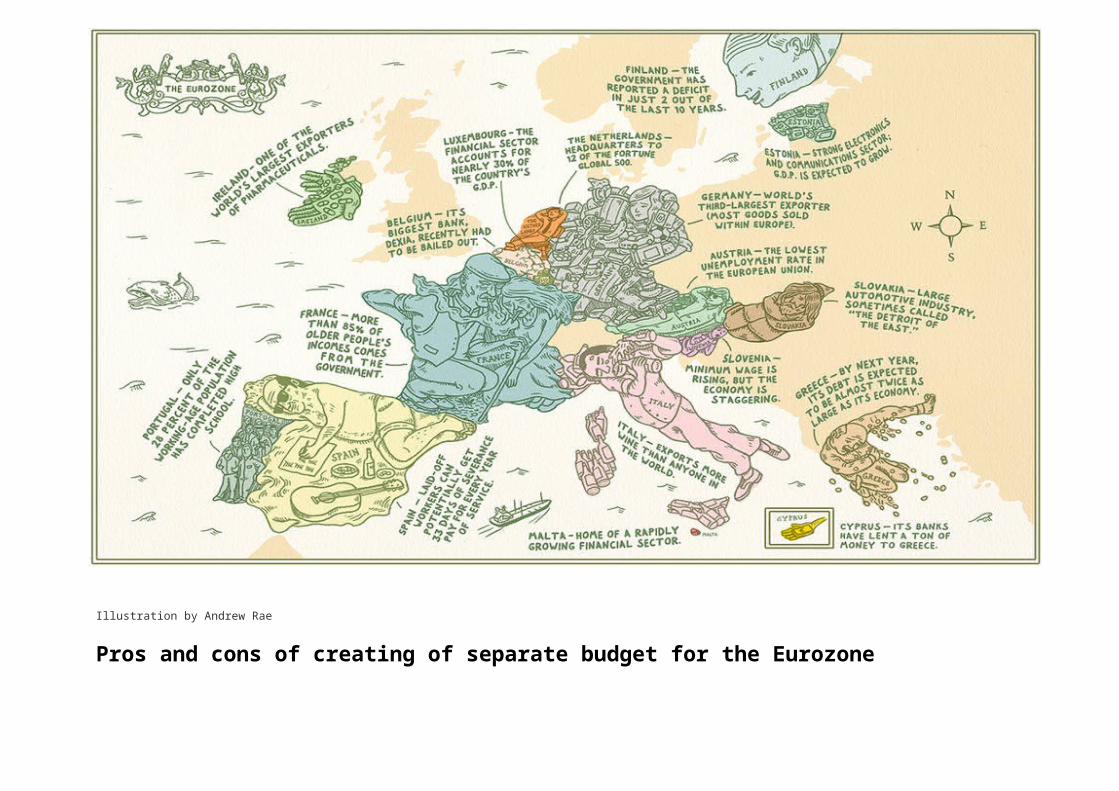

Illustration by Andrew Rae

Pros and cons of creating of separate budget for the Eurozone

Economic dimension of EU integration internal market and the EMU

Kyan Mortazavi March 2014

Towards a single budget for the Eurozone

Herman Van Rompuy in his report “Towards a Genuine Economic and Monetary Union1”,published June 2012, suggested a medium term perspective in which the roleand function of a central budget for the Eurozone in the climate of afiscal union could be specified. Following H.V. Rompuy’s report of June2012, the debate over a separate budget for the Eurozone gained momentumand it influenced the subsequent EU summit, which was held on 18/19 October2012. The result of this summit was a draft of conclusion2, dated 19October 2012, in which it was stated that an integrated budgetary frameworkfor the Eurozone3 is a part of an economic and monetary union, therefore,in the context of a fiscal union, further mechanisms4 for the Eurozonewould be explored to achieve this goal.

The European Council, in the summit of October 2012, also confirmed that:“it looks forward to a specific and time-bound roadmap to be presented at its December 2012meeting, so that it can move ahead on all essential building blocks on which a genuine EMU shouldbe based.” This proves that they genuinely were willing to proceed with it.

Subsequently, H.V. Rompuy in his comprehensive report of December 20125

drew the map of paving this road and set out four steps in order to getthere:

Integrated Financial Framework Integrated Budgetary Framework Integrated Economic Policy Democratic legitimacy/accountability

In the area of an integrated financial framework, the intention is not onlyto bring a greater discipline into public finances, but also to develop thespectrum of existing instruments for fiscal policy in the Eurozone.Ultimately, in order to reach a fiscal capacity at the last stage in theEuropean Monetary Union, a full fiscal and economic union would bedesirable which would finally lead to a political union and a subsequentcentral budget. This union, therefore, can enforce the decisions ineconomic and budgetary areas on its member states. The deeper the union inthe case of economy and budgetary integration would be, the larger thecentral budget seems to get. If this level of deep integration would be

1 http://ec.europa.eu/economy_finance/crisis/documents/131201_en.pdf2 http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ec/133004.pdf3 It shall exclude the Union’s Multiannual Financial Framework (MFF).4 Including an appropriate fiscal capacity5 http://www.consilium.europa.eu/uedocs/cms_Data/docs/pressdata/en/ec/134069.pdf

achieved, therefore, a condition in which the debt issuance is mutualisedwould be created.67

The Blueprint of the Commission, dated 30 November 2012, calls for aconstitution of an autonomous fiscal capacity which is not correlated tothe already existing EU budget. The Blueprint goes further to describe howit would function. It states: “It should be autonomous in the sense that its revenueswould rely solely on own resources, and it could eventually resort to borrowing.” In the opinionof the Commission, the central budget should “provide sufficient resources to supportimportant structural reforms in a large economy under distress.” Ultimately, the Commissionhopes to establish in the long term a central budget to stabilise theEurozone in the context of macroeconomics.

The Commission suggested some proposals as how to achieve a separate budgetfor the Eurozone. The given time frame proposals are supposed to take placein the range of medium to long term, however, considering the time frameand the negotiation around it, the priority certainly is given to theBanking Union.8

What is the Eurozone budget intended for?

The Commission in its Blueprint report9, which is up to now the mostcomprehensive guide on this matter, explicitly expressed that the mainreason for introducing a central budget for the Eurozone, is to insurenecessary and needed stabilisation. It means that in times of crisis, thisbudget would absorb the shock in the countries hit by crisis. In a monetaryunion, reaction to the external shock10 would not be flexible, whereas in anon-member state, it would be easier to react to such a shock, for exampleby devaluing the currency. Therefore, in a monetary union, a mechanismshould be implemented to help, at least temporarily, to ease the effects ofexternal shocks.

Philipp Engler and Simon Voigts claim11 that the advantages of such atransfer mechanism are simple to perceive. Foremost, through implementationof a common monetary policy, it relieves the economic fluctuations in both

6 http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2011:0818:FIN:EN:PDF7 Through Stability Bonds.8 http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2012:0777:REV1:EN:PDF9 http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2012:0777:REV1:EN:PDF10 Sudden changes in international capital flows or in international trade. See: http://www.wright.edu/~tdung/trade_glossary.htm11 http://edocs.fu-berlin.de/docs/servlets/MCRFileNodeServlet/FUDOCS_derivate_000000002425/discpaper2_2013.pdf?hosts=.

states. Because the transfer does not depend on a national budget,therefore, it does not harm the economic situation of the state which makesthis transfer. Hence, when there would be an extreme economic downfallsituation, no issue would arise as a consequence of the amount of thetransfer and subsequently the mechanism itself. They also believe that “in(the) long run this mechanism might not be needed due to a deeper (fiscal) integration reduces theasymmetry of business cycles in the presence of asymmetric shocks.”

The more competitive Eurozone countries, for example Germany, enjoy a lowerexchange rate, where dealing with non-euro countries, compared to thoseless competitive countries of the Eurozone. This artificial low exchangerate is indebted, obviously, to the weak growth performance of crisiscountries. This leads to achieving surpluses in stronger performing membersand losses in the weaker performing members. Therefore, in a deep economicand budgetary integration, a formal transfer mechanism12 is vitally neededto prevent the divergence of economic performance.

Redistribution of the Eurozone budget amongst economically low performingmembers is what makes the introduction of the Eurozone budget veryimportant. Furthermore, Janis A. Emmanouilidis and Fabian Zuleeg believethat the budget could simultaneously function as an incentive and also as asupport to structural and public finance reforms in crisis member states.13

This means that members of the EMU, through a contractual arrangement vis-à-vis the EU Commission, must bind themselves to take up structuralreforms, where they eventually, in exchange, would be able to access somefinancial aid to implement these reforms and/or as a reward for havingimplemented these structural reforms.

Unfortunately, a central budget for the Eurozone, in the Maastricht Treaty,was not set out. The assumption was based on the understanding, that thestabilisation would be achieved at the national level, where the memberstates could borrow from credit markets to control national economicshocks. However, credit markets usually pull away from crisis regions witha big external debt and recession becomes unavoidable due to lack ofinvestors to lend. Therefore, national fiscal and monetary policy becomesunable to handle the situation and this is where the need for a centralbudget for the Eurozone again becomes noticeable.

Guntram Wolff set forth, that in the above mentioned situation where anational economic shock, in the Eurozone, happens and is addressed,

12 “If countries of a monetary union differ in their state of the business cycle, for example onecountry growing below trend while the rest of the union growing above trend, the poorly performingcountry would receive a transfer from the booming part of the union. Thereby aggregate demandcould be increased in the first and reduced in the second”, Philipp Engler and SimonVoigts explain.13 http://www.epc.eu/pub_details.php?cat_id=4&pub_id=2998&year=2012

subsequently by the member in crisis, all the efforts at the national levelwould be fruitless. It is due to the fact that each of the member stateslimits their participation to help, thinking that other member states wouldreact instead. Therefore, this situation needs to be controlled via anintegrated and central fiscal policy with a central budget providing aquick, however temporary, release to the affected member states in the formof resources and/or credit.14

The Euro Area summit statement, dated 29 June 201215, persists in breakingthe circle, which is described as vicious, between banks and states, andsubsequently taxpayers. In order to achieve this, it was proposed toimplement a single supervisory mechanism as soon as possible, by the end of2012, by involving the ECB. The ECB would be given the authority torecapitalise those Eurozone banks which were in need. Therefore, the memberstates would not be involved in the bank crisis and did not have to borrowfrom credit markets to help the national banks. In this case the stateswould not be hit by more external debt. Thus, recapitalising those Eurozonebanks in crisis would call for a central Eurozone budget.

Another function that is envisaged for creating a separate budget for theEurozone is to support creation of a joint unemployment fund for theEurozone members. This unemployed insurance would help to remove thepressure from the members’ national budget by committing to fund the shortterm unemployment benefits during a crisis.16

Since the beginning of the debate over a separate budget for the Eurozone,many scholars and researchers have based their analysis and research of theEconomic Monetary Union on the Centralised model of the USA, given that theEurozone budget is way smaller than the USA’s federal budget. However, thefederal budget in the USA is intended for stabilisation of the economy,which is exactly why a separate budget for the Eurozone is needed in anEMU.

Why a separate budget for the Eurozone is not a good idea?

As mentioned previously, the Centralised American model certainlyrepresents an efficient current model, however, it is believed that many

14 http://www.euinside.eu/en/analyses/for-an-against-a-common-eurozone-budget15 http://www.consilium.europa.eu/uedocs/cms_Data/docs/pressdata/en/ec/131359.pdf16 http://online.wsj.com/news/articles/SB10000872396390444813104578018162989166622

features of this system have been misinterpreted in order to be implementedinto the Eurozone.

The fact that in the American model, the federal government, the same as inmost federated states such as Germany, Australia, Canada…, redistributesthe revenue across regions and states, does not infer that it functionsexactly the same as a shock absorber, however, it offsets, to some extent,the economic differences between states. The USA’s federal budget’sredistribution of funds, mainly, includes mandatory social entitlements,for example Social security1718 and Medicare19. Some parts of thisredistribution, for example in the form of Supplemental NutritionAssistance Program20, could be affected, not to a large extent, by theregional and ultimately local business cycle. In reality this means thatpensioners of the USA, or for that matter most federated countries, in anystate will still receive their pension income and this is not affected bythe statewide performance of the economy. Therefore, the pension incomeneither increases when the state performs well economically nor decreaseswhen the state does not perform well. However, It is also possible that thepension income, countrywide, can be adjusted, a raise, based on the nation-wide inflation rate and this depends on aggregation of each of theindividual states performance, driving the economy. Therefore,redistribution of income tax, in the form of social security payments, doesnot create a bulwark against economic shocks.

In the same context, it should be considered that the US federal budgetstill offsets a considerable amount of differences in the income per capitaper state, due to the fact that a low performing state’s contribution

17 In the United States, Social Security is primarily the Old-Age, Survivors, and Disability Insurance (OASDI) federal program. See: http://www.law.cornell.edu/uscode/text/42/401#a18 http://www.ssa.gov/OP_Home/ssact/title04/0401.htm19 Medicare is the federal health insurance program for people who are 65 orolder, certain younger people with disabilities, and people with End-Stage Renal Disease (permanent kidney failure requiring dialysis or a transplant,sometimes called ESRD). See: http://www.medicare.gov/sign-up-change-plans/decide-how-to-get-medicare/whats-medicare/what-is-medicare.html20 SNAP offers nutrition assistance to millions of eligible, low-incomeindividuals and families and provides economic benefits to communities.SNAP is the largest program in the domestic hunger safety net. The Food andNutrition Service works with State agencies, nutrition educators, andneighborhood and faith-based organizations to ensure that those eligiblefor nutrition assistance can make informed decisions about applying for theprogram and can access benefits. FNS also works with State partners and theretail community to improve program administration and ensure programintegrity. See: http://www.fns.usda.gov/snap/supplemental-nutritionassistance-program-snap

towards income tax is lower than what they receive back as social securitypayments.

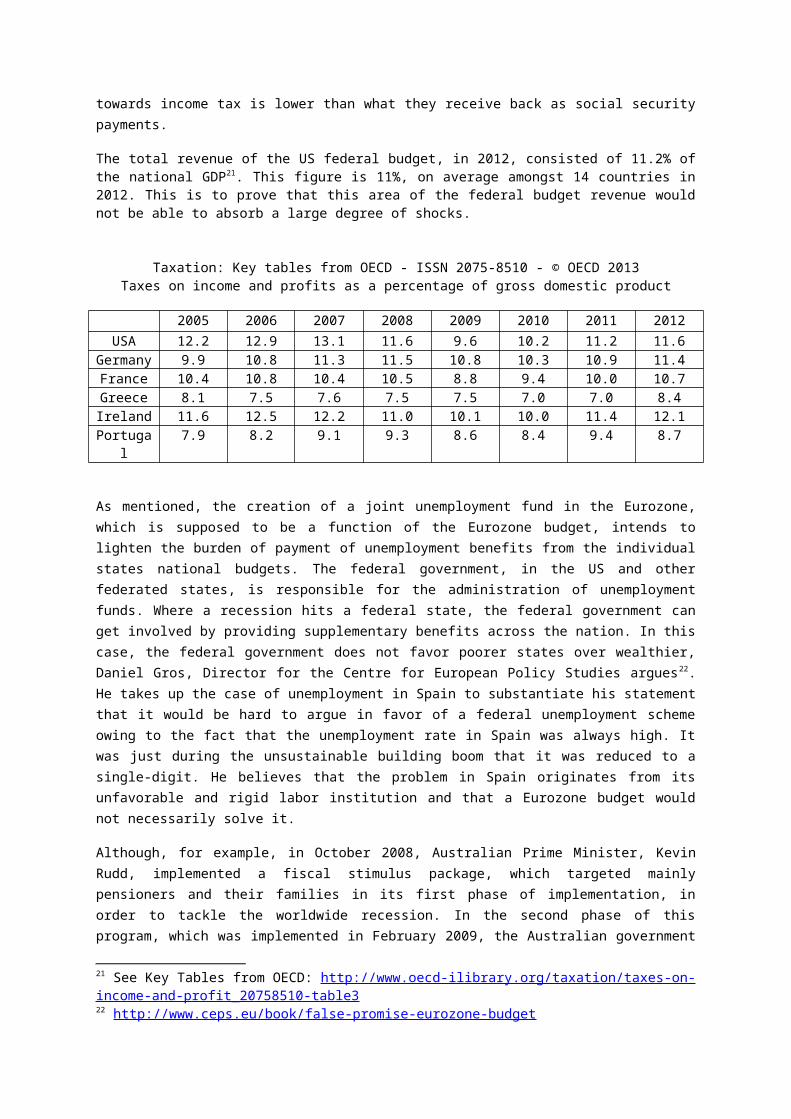

The total revenue of the US federal budget, in 2012, consisted of 11.2% ofthe national GDP21. This figure is 11%, on average amongst 14 countries in2012. This is to prove that this area of the federal budget revenue wouldnot be able to absorb a large degree of shocks.

Taxation: Key tables from OECD - ISSN 2075-8510 - © OECD 2013Taxes on income and profits as a percentage of gross domestic product

2005 2006 2007 2008 2009 2010 2011 2012USA 12.2 12.9 13.1 11.6 9.6 10.2 11.2 11.6

Germany 9.9 10.8 11.3 11.5 10.8 10.3 10.9 11.4France 10.4 10.8 10.4 10.5 8.8 9.4 10.0 10.7Greece 8.1 7.5 7.6 7.5 7.5 7.0 7.0 8.4Ireland 11.6 12.5 12.2 11.0 10.1 10.0 11.4 12.1Portuga

l7.9 8.2 9.1 9.3 8.6 8.4 9.4 8.7

As mentioned, the creation of a joint unemployment fund in the Eurozone,which is supposed to be a function of the Eurozone budget, intends tolighten the burden of payment of unemployment benefits from the individualstates national budgets. The federal government, in the US and otherfederated states, is responsible for the administration of unemploymentfunds. Where a recession hits a federal state, the federal government canget involved by providing supplementary benefits across the nation. In thiscase, the federal government does not favor poorer states over wealthier,Daniel Gros, Director for the Centre for European Policy Studies argues22.He takes up the case of unemployment in Spain to substantiate his statementthat it would be hard to argue in favor of a federal unemployment schemeowing to the fact that the unemployment rate in Spain was always high. Itwas just during the unsustainable building boom that it was reduced to asingle-digit. He believes that the problem in Spain originates from itsunfavorable and rigid labor institution and that a Eurozone budget wouldnot necessarily solve it.

Although, for example, in October 2008, Australian Prime Minister, KevinRudd, implemented a fiscal stimulus package, which targeted mainlypensioners and their families in its first phase of implementation, inorder to tackle the worldwide recession. In the second phase of thisprogram, which was implemented in February 2009, the Australian government

21 See Key Tables from OECD: http://www.oecd-ilibrary.org/taxation/taxes-on-income-and-profit_20758510-table322 http://www.ceps.eu/book/false-promise-eurozone-budget

provided immediate one-off payments, to the maximum of AUD 900, to thoseAustralians who were employed, had school-age children, were farmers orsingle income families and those who were studying and being trained. Theresult was that Australia could manage successfully to avoid therecession23242526.

Another interesting point in rejecting the idea of creating a separatebudget for the Eurozone is a comparison between the building boom inIreland and Spain against the state of Nevada in the US. The rise andfailure of real-estate sector in Nevada, Ireland and Spain was similar,however, the shock which the banking sector in the state of Nevada, whichis almost the same size of Ireland, suffered from was absorbed by theAmerican Banking Union institutions, such as the Federal Deposit InsuranceCorporation (FDIC)2728 and the federal mortgage-refinancing agencies29.Therefore, the state of Nevada did not suffer from internal shock and thefederal government did not have to bail it out. If a banking union in theEurozone existed, then Ireland would not have had suffered as much and itwould have been in a better shape, Daniel Gros averts30.

Therefore, accordingly, in the long run, economic stability in the Eurozonecould arise from a strong and sustainable banking union rather than aseparate Eurozone budget.

Banking union in short term vs. fiscal union in long term

Herman Van Rompuy, president of the European Council, in his letter, dated13 December 2013, to the members of the European Council, sets the priorityon the task of completing a banking union. He confirms that this challengeshould be accomplished in order to bring the stability to Europe’sfinancial sector31. As mentioned previously, even the Commission’s suggested

23 http://www.news.com.au/national/no-loosening-of-purse-strings-poll/story-e6frfkp9-111111874078224 http://news.bbc.co.uk/2/hi/8080446.stm25 http://www.news.com.au/finance/ber-bungle-saved-australian-economy/story-e6frfm1i-122587472564426 http://www.abc.net.au/unleashed/2829090.html27 The Federal Deposit Insurance Corporation (FDIC) preserves and promotespublic confidence in the U.S. financial system by insuring deposits inbanks and thrift institutions for at least $250,000; by identifying,monitoring and addressing risks to the deposit insurance funds; and bylimiting the effect on the economy and the financial system when a bank orthrift institution fails.28 http://www.fdic.gov/29 Fannie Mae and Freddie Mac30 http://www.voxeu.org/article/banking-union-if-ireland-were-nevada31 http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ec/140073.pdf

time frame to achieve a European Monetary union the precedence is given tothe Banking Union. Creating a separate budget for the Eurozone is a longterm goal, beyond five years.

A banking union might be the solution to the Eurozone economic problem ifits implementation results in a stable Eurozone. Therefore, at this earlystage, it is difficult to say whether a separate budget for the Eurozoneworks or not as much still remains unclear. Bringing in line those membersof the Eurozone which have to accept the largest financial burden offunding this budget is a political challenge. After overcoming thischallenge, it is a huge responsibility to make the Eurozone budget a bonafide to tackle impact of the economic crisis in the Euro area.

It is very soon to decide on its details, however, it should be kept inmind that when it comes to think, analyze and decide on this matter: theEuropean integration should be given priority and should not be hindered atall. The dignity of the people in the crisis member states should berespected by not imposing tough measures and conditions, and it shouldalways contain a message of solidarity. Any measures leading to a divisionbetween the Eurozone members and other European Union members shouldstrongly be avoided and hopefully this is how it might be able to succeed.

Bibliography

"$42 Billion Spent to Kickstart Economy with Budget Going into Deficit andHandouts for Many." NewsComAu. February 03, 2009. Accessed March 06,2014. http://www.news.com.au/national/no-loosening-of-purse-strings-poll/story-e6frfkp9-1111118740782.

Allard, Céline, Petya Koeva Brooks, John C. Bluedorn, Fabian Bornhorst,

Katharine Christopherson, Franziska Ohnsorge, and Tigran Poghosyan."Towards a Fiscal Union for the Euro Area." IMF STAFF DISCUSSION NOTE,September 2013, 1-29. Accessed March 6, 2014. doi:SDN/13/09.

"Australia Able to Avoid Recession." BBC News. March 06, 2009. Accessed

March 06, 2014. http://news.bbc.co.uk/2/hi/8080446.stm. Baetz, Juergen. "Eurozone Needs Common Budget to Protect against Shocks:

IMF Experts." CTVNews. September 25, 2013. Accessed March 06, 2014.http://www.ctvnews.ca/business/eurozone-needs-common-budget-to-protect-against-shocks-imf-experts-1.1469877.

Cornell University Law School. "42 U.S. Code § 401 - Trust Funds." LII /

Legal Information Institute. Accessed March 06, 2014.http://www.law.cornell.edu/uscode/text/42/401#a.

Corner, Worden's. "The Worden Report: A Separate “Eurozone” Budget: Two-

Track Federalism." The Worden Report: A Separate “Eurozone” Budget:Two-Track Federalism. October 07, 2012. Accessed March 06, 2014.http://thewordenreport.blogspot.de/2012/10/a-separate-eurozone-budget-two-track.html.

Emmanuilidis, Janis A., and Fabian Zuleeg. "A Budget for the Euro Zone?"

European Policy Centre (EPC). October 15, 2012. Accessed March 06,2014. http://www.epc.eu/pub_details.php?cat_id=4&pub_id=2998&year=2012.

Engler, Philipp, and Simon Voigts. A Transfer Mechanism for a Monetary Union. DIE

FREIEN UNIVERSITÄT BERLIN. DOKUMENTENSERVER DER FREIEN UNIVERSITÄTBERLIN. March 5, 2013. Accessed March 6, 2014. http://edocs.fu-berlin.de/docs/servlets/MCRFileNodeServlet/FUDOCS_derivate_000000002425/discpaper2_2013.pdf?hosts=.

"Euro Area Summit Statement." CONSILIUM. June 29, 2012. Accessed March 6,

2014.http://www.consilium.europa.eu/uedocs/cms_Data/docs/pressdata/en/ec/131359.pdf.

The European Commission. "A Blueprint for a Deep and Genuine Economic and

Monetary Union Launching a European Debate." Access to European UnionLaw. November 30, 2012. Accessed March 6, 2014. http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2012:0777:REV1:EN:PDF.

The European Commission. "GREEN PAPER on the Feasibility of Introducing

Stability Bonds." Access to European Union Law. November 23, 2011.Accessed March 6, 2014.http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2011:0818:FIN:EN:PDF.

"Federal Deposit Insurance Corporation." FDIC: Federal Deposit Insurance

Corporation. Accessed March 06, 2014. http://www.fdic.gov/. Food and Nutrition Service. "Supplemental Nutrition Assistance Program

(SNAP)." Food and Nutrition Service. Accessed March 6, 2014.http://www.fns.usda.gov/snap/supplemental-nutrition-assistance-program-snap.

General Secretariat of the Council. "EUROPEAN CONUCIL 18/19 OCTOBER 2012

CONCLUSIOS." CONSILIUM. October 19, 2012. Accessed March 6, 2014.http://www.consilium.europa.eu/.

Gros, Daniel. "Banking Union: If Ireland Were Nevada." VOX. September 27,

2012. Accessed March 06, 2014. http://www.voxeu.org/article/banking-union-if-ireland-were-nevada.

Gros, Daniel. "The False Promise of a Eurozone Budget." Centre for EuropeanPolicy Studies (CEPS). December 07, 2012. Accessed March 6, 2014.http://www.ceps.eu/book/false-promise-eurozone-budget.

Kates, Steven. "The Australian Stimulus and the Damage It Caused - The Drum

Opinion (Australian Broadcasting Corporation)." The Drum Opinion.August 08, 2011. Accessed March 06, 2014.http://www.abc.net.au/unleashed/2829090.html.

"Kevin Rudd's BER Bungle May Have Saved Australian Economy." News.com.au.

June 03, 2010. Accessed March 6, 2014.http://www.news.com.au/finance/ber-bungle-saved-australian-economy/story-e6frfm1i-1225874725644.

Mackintosh, James. "Banking Union: Nevada vs Ireland." FT Long Short.

October 19, 2012. Accessed March 6, 2014. http://blogs.ft.com/ft-long-short/2012/10/19/banking-union-nevada-vs-ireland/.

Marini, Adelina. "For and Against a Common Eurozone Budget." EU Inside.

January 17, 2013. Accessed March 06, 2014.http://www.euinside.eu/en/analyses/for-an-against-a-common-eurozone-budget.

McDonnell, Eion, Daniel O'Callaghan, Paddy Buckenham, James Kilcourse, Eva

Barrett, and Andrew Gilmore. "Completing the Banking Union TakesPriority as European Council Convenes." The Institute ofInternational and European Affairs (IIEA). December 19, 2013.Accessed March 06, 2014. http://www.iiea.com/blogosphere/completing-the-banking-union-takes-priority-as-european-council-convenes.

OECD ILibrary. "Taxation: Key Tables from OECD." Taxes on Income and Profit

As a Percentage of Gross Domestic Product. January 17, 2014. AccessedMarch 06, 2014. http://www.oecd-ilibrary.org/taxation/taxes-on-income-and-profit_20758510-table3.

Rubio, Eulalia. "EUROZONE BUDGET: 3 FUNCTIONS, 3 INSTRUMENTS." Tribune Notre

Europe - Jacques Delors Institut, November 15, 2012, 1-4. Accessed March 6,2014. http://www.notre-europe.eu/media/eurozonebudget-rubio-ne-jdi-nov12.pdf?pdf=ok.

Steinhauser, Gabriele. "Euro Zone Considers Central Budget to Fix Cracks."

The Wall Street Journal. September 25, 2012. Accessed March 06, 2014.http://online.wsj.com/news/articles/SB10000872396390444813104578018162989166622.

USA Medicare. "What Is Medicare?" Medicare.gov: The Official U.S.

Government Site for Medicare. Accessed March 6, 2014.http://www.medicare.gov/sign-up-change-plans/decide-how-to-get-medicare/whats-medicare/what-is-medicare.html.

USA Social Security Administration. "Part A—BLOCK GRANTS TO STATES FORTEMPORARY ASSISTANCE FOR NEEDY FAMILIES." Official Social SecurityWebsite. Accessed March 06, 2014.http://www.ssa.gov/OP_Home/ssact/title04/0401.htm.

Van Rompuy, Herman, Jose Manuel Barroso, Jean-Claude Juncker, and Mario

Draghi. "TOWARDS A GENUIE ECONOMIC AD MONETARY UNION." CONSILIUM.December 05, 2012. Accessed March 6, 2014.http://www.consilium.europa.eu/uedocs/cms_Data/docs/pressdata/en/ec/134069.pdf.

Van Rompuy, Herman. "Letter by President of the European Council."

CONSILIUM. December 13, 2013. Accessed March 6, 2014.http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ec/140073.pdf.

Van Rompuy, Herman. "TOWARDS A GENUINE ECONOMIC AND MONETARY UNION." The

European Commission. June 26, 2012. Accessed March 6, 2014.http://ec.europa.eu/economy_finance/crisis/documents/131201_en.pdf.

Wolff, Guntram B. "A Budget for Europe's Monetary Union." BRUEGEL POLICY

CONTRIBUTION, 2012th ser., no. 22 (December 2012): 1-13. AccessedMarch 6, 2014. http://www.bruegel.org/publications/publication-detail/publication/762-a-budget-for-europes-monetary-union/.

Wright State University. "Glossary." Glossary. Accessed March 06, 2014.

http://www.wright.edu/~tdung/trade_glossary.htm. Wright State University. "Glossary." Glossary. Accessed March 06, 2014.

http://www.wright.edu/~tdung/trade_glossary.htm.