Embed Size (px)

Citation preview

Taxation and Development

Henrik KlevenLondon School of Economics

June 2016

1 / 51

What Separates PF-Devo From PF?

I PF-Devo is more than just “studying taxation in developingcountries”

I Focus on tax enforcement and administration:I Traditional PF assumes perfect enforcement and administration

(zero evasion at zero administrative costs)I In PF-Devo, enforcement/administration are central objects of

interest

I Focus on the long-run of development:Tax system� economic development

I Implicit notion that more tax revenue is a good thing

2 / 51

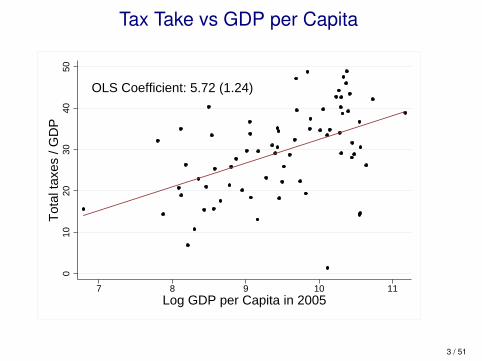

Tax Take vs GDP per Capita

OLS Coefficient: 5.72 (1.24)

010

2030

4050

Tot

al ta

xes

/ GD

P

7 8 9 10 11Log GDP per Capita in 2005

3 / 51

Theories of Government Growth

1. Demand for public goods has an income elasticity above one[Wagner’s law]

2. Stagnating productivity in the public sector [Baumol’s costdisease]

3. Ratchet effect theory whereby temporary shocks (e.g. wars)raise government expenditure, which do not fall back after theshock

4. Political economy aspects (e.g. democratization)

5. Tax enforcement improves with development

4 / 51

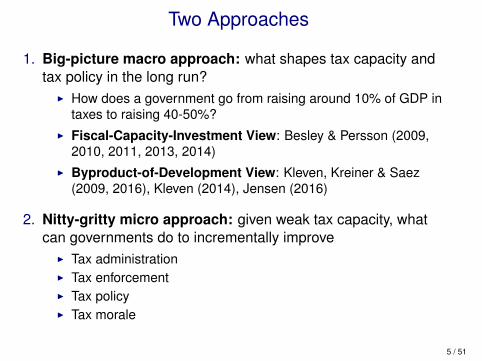

Two Approaches

1. Big-picture macro approach: what shapes tax capacity andtax policy in the long run?

I How does a government go from raising around 10% of GDP intaxes to raising 40-50%?

I Fiscal-Capacity-Investment View: Besley & Persson (2009,2010, 2011, 2013, 2014)

I Byproduct-of-Development View: Kleven, Kreiner & Saez(2009, 2016), Kleven (2014), Jensen (2016)

2. Nitty-gritty micro approach: given weak tax capacity, whatcan governments do to incrementally improve

I Tax administrationI Tax enforcementI Tax policyI Tax morale

5 / 51

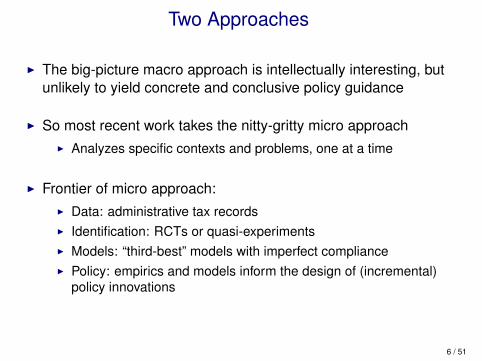

Two Approaches

I The big-picture macro approach is intellectually interesting, butunlikely to yield concrete and conclusive policy guidance

I So most recent work takes the nitty-gritty micro approachI Analyzes specific contexts and problems, one at a time

I Frontier of micro approach:I Data: administrative tax recordsI Identification: RCTs or quasi-experimentsI Models: “third-best” models with imperfect complianceI Policy: empirics and models inform the design of (incremental)

policy innovations

6 / 51

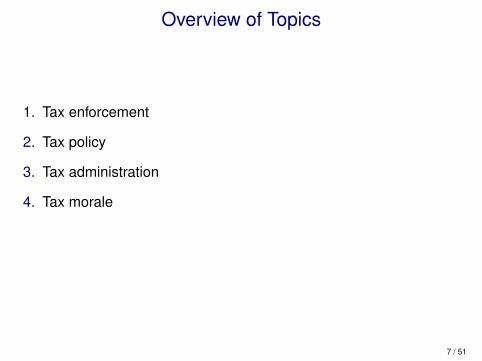

Overview of Topics

1. Tax enforcement

2. Tax policy

3. Tax administration

4. Tax morale

7 / 51

Tax Enforcement

8 / 51

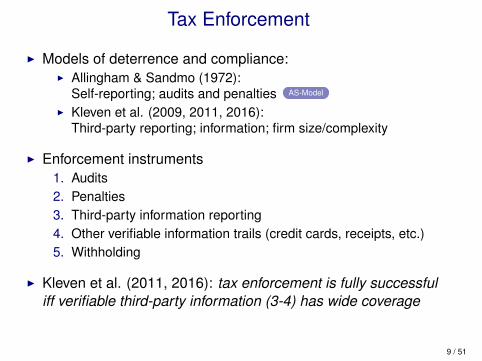

Tax Enforcement

I Models of deterrence and compliance:I Allingham & Sandmo (1972):

Self-reporting; audits and penalties AS-Model

I Kleven et al. (2009, 2011, 2016):Third-party reporting; information; firm size/complexity

I Enforcement instruments1. Audits2. Penalties3. Third-party information reporting4. Other verifiable information trails (credit cards, receipts, etc.)5. Withholding

I Kleven et al. (2011, 2016): tax enforcement is fully successfuliff verifiable third-party information (3-4) has wide coverage

9 / 51

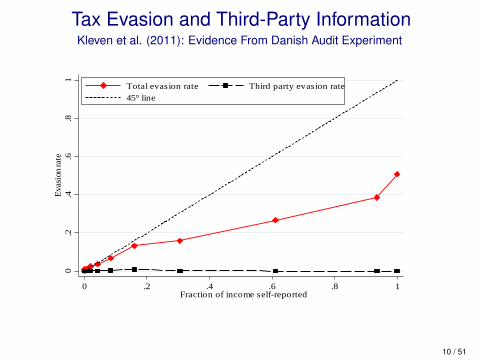

Tax Evasion and Third-Party InformationKleven et al. (2011): Evidence From Danish Audit Experiment

Figure 1: Evasion by Fraction of Income Self‐Reported

Notes: the source is Kleven et al. (2011). The figure displays estimates of the total evasion rate (fraction of total income undeclared)and the third‐party evasion rate (fraction of third‐party reported income undeclared), conditional on having positive evasion, bydeciles of the fraction of income self‐reported. Further details can be found in the original source.

0.2

.4.6

.81

Evas

ion

rate

0 .2 .4 .6 .8 1Fraction of income self-reported

Total evasion rate Third party evasion rate45° line

10 / 51

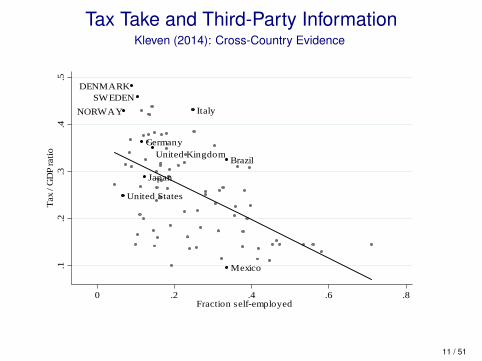

Tax Take and Third-Party InformationKleven (2014): Cross-Country EvidenceFigure 2: Tax Take and Third‐Party Reporting across Countries

Notes: Country‐level observations, latest available year. Countries with GDP per capita below $5000 (in 2005 PPP terms) or naturalresource rents as a fraction of GDP above 20% are excluded from the sample. Tax/GDP ratio is the share of tax revenue in a givencountry's nominal GDP in 2012 (source: Index of Economic Freedom, Heritage Foundation). In both panels, the "fraction self‐employed" is defined crudely as all non‐employees (self‐employed, employers, and non‐classifiable workers) as a fraction of theworkforce (source: World Bank). In Panel B, the "fraction of employees in evasive jobs" is defined as the fraction of the workforcewho are employees in sectors that (in part) provide labor intensive consumer services (source: ILO). These evasive sectors are definedaccording to ISIC codes 4F: construction, 4G: retail, wholesale, and repair of motor vehicles, motorcycles and personal and householdgoods, 4I: hotels and restaurants, 4S: other service activities, and 4T: employees of private households (nannies, cooks, gardeners,etc.). Regression line is plotted in each panel.

Panel B: Tax Take vs Fraction of Self‐Employed and Employees in Evasive Jobs

Panel A: Tax Take vs Fraction Self‐Employed

Brazil

Germany

Italy

Japan

Mexico

United Kingdom

United States

DENMARK

NORWAYSWEDEN

.1.2

.3.4

.5Ta

x / G

DP

ratio

.2 .4 .6 .8Fraction of self-employed and employees in evasive jobs

Brazil

Germany

Italy

Japan

Mexico

United Kingdom

United States

DENMARK

NORWAYSWEDEN

.1.2

.3.4

.5Ta

x / G

DP

ratio

0 .2 .4 .6 .8Fraction self-employed

11 / 51

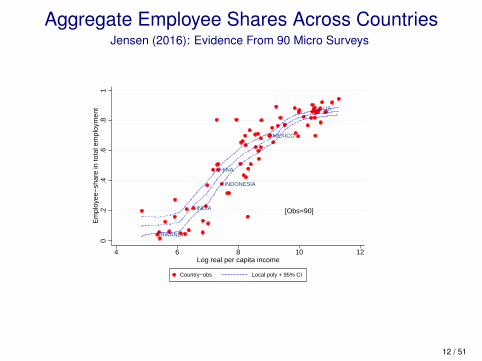

Aggregate Employee Shares Across CountriesJensen (2016): Evidence From 90 Micro Surveys

Start point: aggregate employee-share ↑ over development

RWANDA

INDIA

CHINA

INDONESIA

MEXICO

US

[Obs=90]

0.2

.4.6

.81

Em

ploy

ee−

shar

e in

tota

l em

ploy

men

t

4 6 8 10 12Log real per capita income

Country−obs Local poly + 95% CI

DENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARK

INDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIA

RWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDA

SOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICA

US1870

US1910

US1920US1930

US1940US1950

US1960US1970US1980US1990US2000US2010

0.2

.4.6

.81

Em

ploy

ee−

shar

e in

em

ploy

men

t

6 7 8 9 10 11Log real per capita income (Maddison data)

Cross−cty obs [n=67] Within−cty obs: US 1870−2010 [n=12]

12 / 51

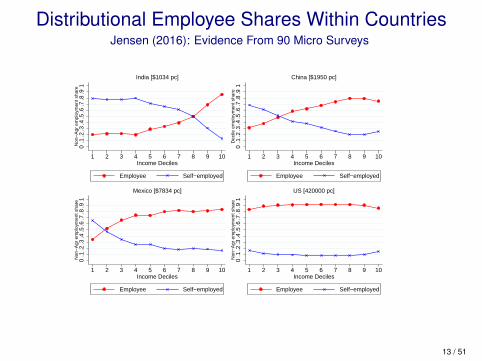

Distributional Employee Shares Within CountriesJensen (2016): Evidence From 90 Micro SurveysDescriptive evidence: new stylized facts

0.1

.2.3

.4.5

.6.7

.8.9

1N

on−

Agr

em

ploy

men

t sha

re

1 2 3 4 5 6 7 8 9 10Income Deciles

Employee Self−employed

India [$1034 pc]

0.1

.2.3

.4.5

.6.7

.8.9

1D

ecile

em

ploy

men

t sha

re

1 2 3 4 5 6 7 8 9 10Income Deciles

Employee Self−employed

China [$1950 pc]0

.1.2

.3.4

.5.6

.7.8

.91

Non

−A

gr e

mpl

oym

ent s

hare

1 2 3 4 5 6 7 8 9 10Income Deciles

Employee Self−employed

Mexico [$7834 pc]

0.1

.2.3

.4.5

.6.7

.8.9

1N

on−

Agr

em

ploy

men

t sha

re

1 2 3 4 5 6 7 8 9 10Income Deciles

Employee Self−employed

US [420000 pc]

13 / 51

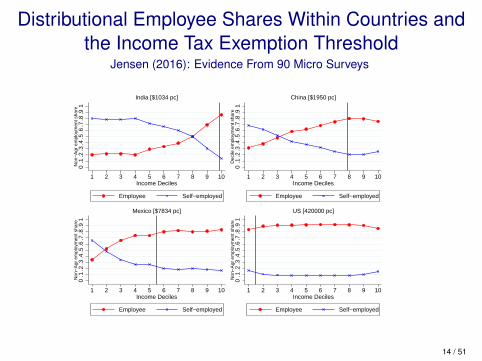

Distributional Employee Shares Within Countries andthe Income Tax Exemption Threshold

Jensen (2016): Evidence From 90 Micro SurveysDescriptive evidence: new stylized facts0

.1.2

.3.4

.5.6

.7.8

.91

Non

−A

gr e

mpl

oym

ent s

hare

1 2 3 4 5 6 7 8 9 10Income Deciles

Employee Self−employed

India [$1034 pc]

0.1

.2.3

.4.5

.6.7

.8.9

1D

ecile

em

ploy

men

t sha

re

1 2 3 4 5 6 7 8 9 10Income Deciles

Employee Self−employed

China [$1950 pc]

0.1

.2.3

.4.5

.6.7

.8.9

1N

on−

Agr

em

ploy

men

t sha

re

1 2 3 4 5 6 7 8 9 10Income Deciles

Employee Self−employed

Mexico [$7834 pc]

0.1

.2.3

.4.5

.6.7

.8.9

1N

on−

Agr

em

ploy

men

t sha

re

1 2 3 4 5 6 7 8 9 10Income Deciles

Employee Self−employed

US [420000 pc]

14 / 51

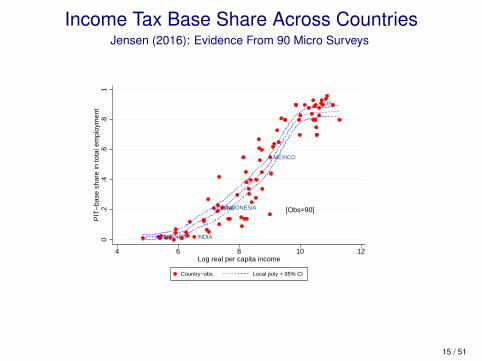

Income Tax Base Share Across CountriesJensen (2016): Evidence From 90 Micro Surveys

Fact #2 across and within country

RWANDA INDIA

CHINAINDONESIA

MEXICO

US

[Obs=90]

0.2

.4.6

.81

PIT

−ba

se s

hare

in to

tal e

mpl

oym

ent

4 6 8 10 12Log real per capita income

Country−obs Local poly + 95% CI

DENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARK

INDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIARWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDA

SOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICA

US1930

US1950

US1960

US1970US1980US1990

US2000US2010

0.2

.4.6

.81

PIT

−ba

se s

hare

in to

tal e

mpl

oym

ent

6 7 8 9 10 11Log real per capita income (Maddison data)

Cross−cty obs [n=67] Within−cty obs: US 1870−2010 [n=12]

15 / 51

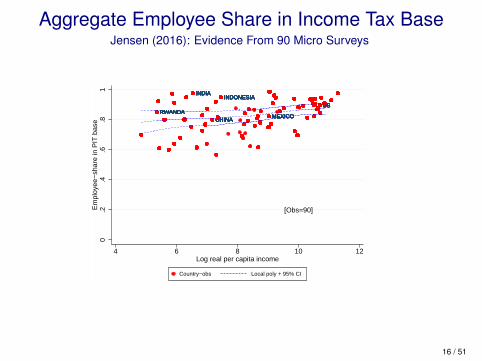

Aggregate Employee Share in Income Tax BaseJensen (2016): Evidence From 90 Micro Surveys

Fact #3 across and within country

RWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDA

INDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIA

CHINACHINACHINACHINACHINACHINACHINACHINACHINACHINA

INDONESIAINDONESIAINDONESIAINDONESIAINDONESIAINDONESIAINDONESIAINDONESIAINDONESIAINDONESIA

MEXICOMEXICOMEXICOMEXICOMEXICOMEXICOMEXICOMEXICOMEXICOMEXICO

USUSUSUSUSUSUSUSUSUS

[Obs=90]

0.2

.4.6

.81

Em

ploy

ee−

shar

e in

PIT

bas

e

4 6 8 10 12Log real per capita income

Country−obs Local poly + 95% CI

DENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARKDENMARKINDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIAINDIA

RWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDARWANDASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICAUS1930

US1950

US1960US1970US1980

US1990US2000US2010

0.2

.4.6

.81

Em

ploy

ee−

shar

e in

PIT

bas

e

6 7 8 9 10 11Log real per capita income (Maddison data)

Cross−cty obs [n=67] Within−cty obs: US 1870−2010 [n=12]

16 / 51

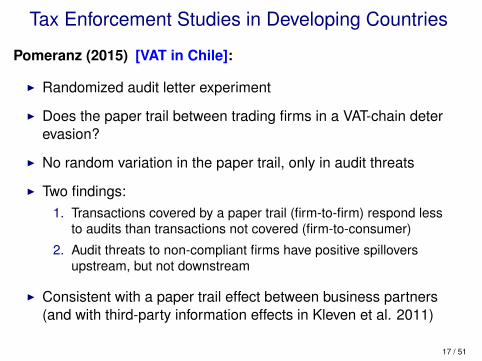

Tax Enforcement Studies in Developing Countries

Pomeranz (2015) [VAT in Chile]:

I Randomized audit letter experiment

I Does the paper trail between trading firms in a VAT-chain deterevasion?

I No random variation in the paper trail, only in audit threats

I Two findings:1. Transactions covered by a paper trail (firm-to-firm) respond less

to audits than transactions not covered (firm-to-consumer)

2. Audit threats to non-compliant firms have positive spilloversupstream, but not downstream

I Consistent with a paper trail effect between business partners(and with third-party information effects in Kleven et al. 2011)

17 / 51

Tax Enforcement Studies in Developing Countries

Kumler, Verhoogen, and Frias (2013) [Payroll Tax in Mexico]:I Substantial underreporting of wages by firms, with evasion

being declining in firm sizeI Giving employees incentives to ensure accurate employer

reports improve compliance

Carillo, Pomeranz, and Singhal (2014) [CIT in Ecuador]:I Third-party information is ineffective if taxpayers can make

offsetting adjustments on less verifiable marginsI Evidence from rich countries (with high 3rd-party coverage)

may not reveal marginal effect where coverage is very low

Naritomi (2015) [VAT in Brazil]:I Providing incentives for consumers to ask for VAT receipts and

whistleblow non-compliant firms improves compliance18 / 51

Tax Policy

19 / 51

Tax Policy: Traditional Analysis

Traditional PF analysis builds on three classic contributions:1. Diamond-Mirrlees (1971): commodity taxes, prod. efficiency2. Mirrlees (1971): income taxes3. Atkinson-Stiglitz (1976): income vs commodity taxes

Policy recommendations coming out of this literature:1. Use progressive income taxes2. Use uniform VAT/sales tax3. Do not use differentiated commodity taxes

(except for externalities/internalities)4. Do not use capital taxes (?)5. Do not use taxes on turnover, trade, and intermediate inputs

20 / 51

Tax Policy: Theory vs Reality in Poor Countries

I Low-income countries tend to rely on the “wrong tax policies”(Gordon & Li 2009) Tax Structures

I Two responses:1. Policies should be changed (Newbery & Stern 1987)2. The models are wrong, not the policies

I Traditional models assume:I Full set of tax instruments (except for taxes on innate ability)I Perfect enforcement of these tax instruments

I Implications of informality or evasion for optimal tax policy:I Informality (extensive margin): Emran & Stiglitz (2005); Keen

(2006); Gordon & Li (2009)I Evasion (intensive margin): Best, Brockmeyer, Kleven,

Spinnewijn & Waseem (2015)

21 / 51

From Tax Rates to Tax Instruments

I Much academic work studies the pattern of optimal tax ratesI Taking the tax instrument as given (e.g., nonlinear income tax)I Allowing for lots of flexibility in tax instruments

I This is second-order for developing economiesI Here the choice between tax instruments is keyI Which instruments represent the best trade-off between

standard efficiency-equity concerns and compliance concerns?

I Taxonomy of Taxes:I Modern: income taxes, social security taxes, VATI Traditional: property taxes, wealth transfer taxes, excises,

tariffs, etc.

22 / 51

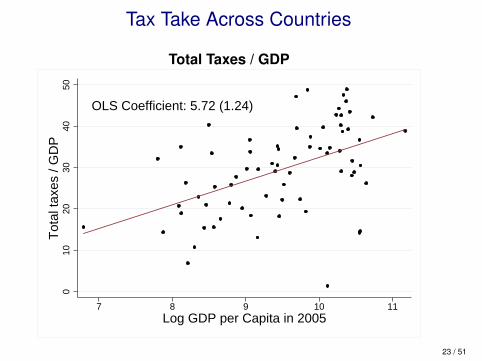

Tax Take Across Countries

Total Taxes / GDP

OLS Coefficient: 5.72 (1.24)

010

2030

4050

Tot

al ta

xes

/ GD

P

7 8 9 10 11Log GDP per Capita in 2005

23 / 51

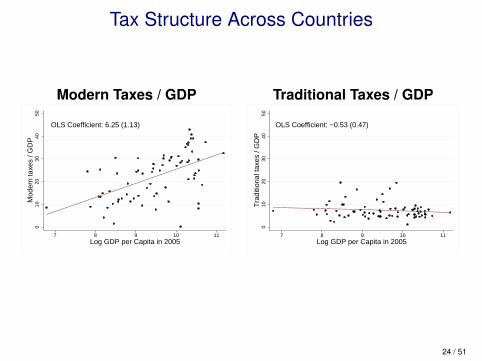

Tax Structure Across Countries

Modern Taxes / GDP Traditional Taxes / GDP

OLS Coefficient: 6.25 (1.13)

010

2030

4050

Mod

ern

taxe

s / G

DP

7 8 9 10 11Log GDP per Capita in 2005

OLS Coefficient: −0.53 (0.47)

010

2030

4050

Tra

ditio

nal t

axes

/ G

DP

7 8 9 10 11Log GDP per Capita in 2005

24 / 51

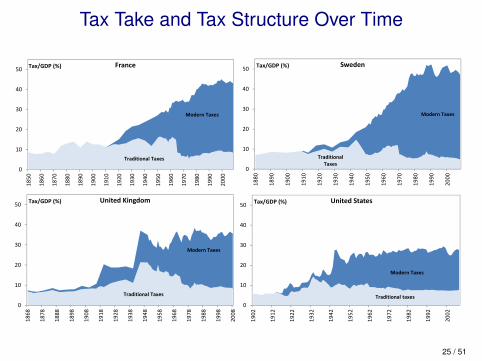

Tax Take and Tax Structure Over Time

Traditional Taxes

Modern Taxes

0

10

20

30

40

50

1850

1860

1870

1880

1890

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

Tax/GDP (%) France

Traditional Taxes

Modern Taxes

0

10

20

30

40

50

1868

1878

1888

1898

1908

1918

1928

1938

1948

1958

1968

1978

1988

1998

2008

Tax/GDP (%) United Kingdom

Modern Taxes

0

10

20

30

40

50

1902

1912

1922

1932

1942

1952

1962

1972

1982

1992

2002

Tax/GDP (%) United States

Traditional taxes

Traditional Taxes

Modern Taxes

0

10

20

30

40

50

1880

1890

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

Tax/GDP (%) Sweden

25 / 51

From Macro to MicroBest, Brockmeyer, Kleven, Spinnewijn & Waseem (2015)

I Production Efficiency Theorem:Any second-best optimal tax system maintains productionefficiency

I Policy implication:Firms should be taxed on their profits, not on their turnover

I Ubiquitous production inefficient tax scheme:Minimum Tax Scheme (MTS) that taxes firms on either profitsor turnover depending on which tax liability is larger

I Such schemes are motivated by the idea that turnover taxesare harder to evade than profits taxes

I Best et al. (2015) analyze the MTS on corporations in Pakistan

26 / 51

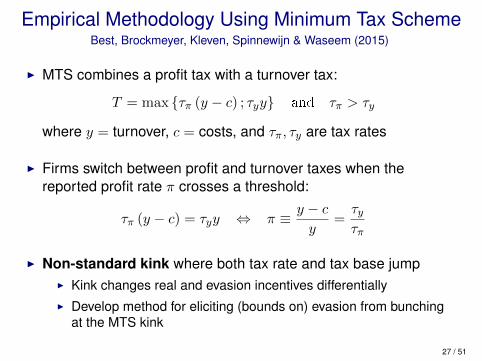

Empirical Methodology Using Minimum Tax SchemeBest, Brockmeyer, Kleven, Spinnewijn & Waseem (2015)

I MTS combines a profit tax with a turnover tax:

T = max {τπ (y − c) ; τyy} and τπ > τy

where y = turnover, c = costs, and τπ, τy are tax rates

I Firms switch between profit and turnover taxes when thereported profit rate π crosses a threshold:

τπ (y − c) = τyy ⇔ π ≡ y − cy

=τyτπ

I Non-standard kink where both tax rate and tax base jumpI Kink changes real and evasion incentives differentiallyI Develop method for eliciting (bounds on) evasion from bunching

at the MTS kink

27 / 51

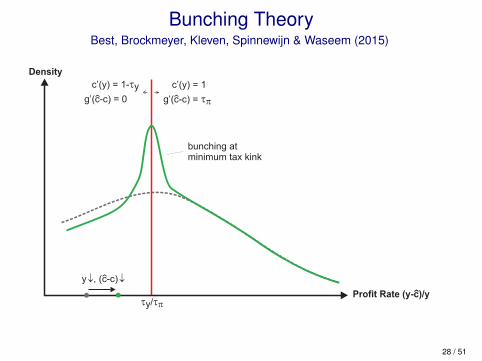

Bunching TheoryBest, Brockmeyer, Kleven, Spinnewijn & Waseem (2015)

bunching atminimum tax kink

Density

Profit Rate (y-c)/y

‹

t ty/ p

c’(y) = 1-ty

g’(c-c) = 0

‹

c’(y) = 1

g’(c-c) = tp

‹

y , (c-c)¯ ¯

‹

28 / 51

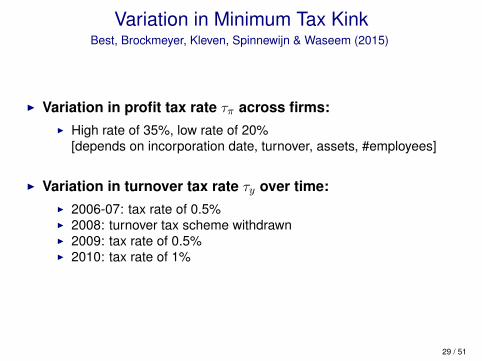

Variation in Minimum Tax KinkBest, Brockmeyer, Kleven, Spinnewijn & Waseem (2015)

I Variation in profit tax rate τπ across firms:I High rate of 35%, low rate of 20%

[depends on incorporation date, turnover, assets, #employees]

I Variation in turnover tax rate τy over time:I 2006-07: tax rate of 0.5%I 2008: turnover tax scheme withdrawnI 2009: tax rate of 0.5%I 2010: tax rate of 1%

29 / 51

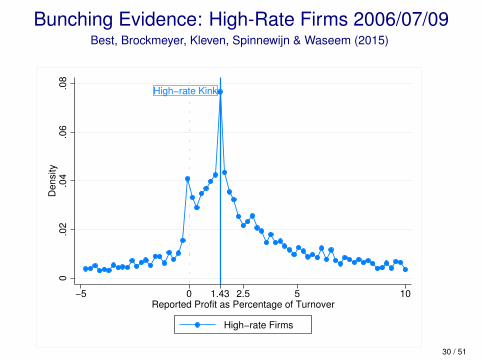

Bunching Evidence: High-Rate Firms 2006/07/09Best, Brockmeyer, Kleven, Spinnewijn & Waseem (2015)

High−rate Kink

0.0

2.0

4.0

6.0

8D

ensi

ty

−5 0 1.43 2.5 5 10Reported Profit as Percentage of Turnover

High−rate Firms

30 / 51

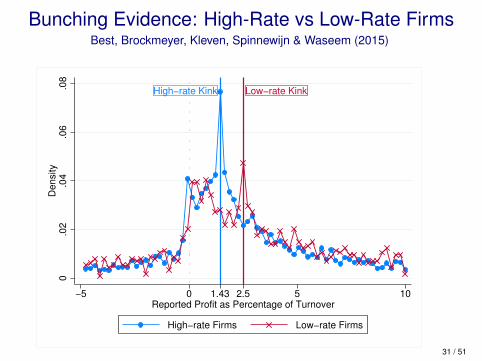

Bunching Evidence: High-Rate vs Low-Rate FirmsBest, Brockmeyer, Kleven, Spinnewijn & Waseem (2015)

High−rate Kink Low−rate Kink

0.0

2.0

4.0

6.0

8D

ensi

ty

−5 0 1.43 2.5 5 10Reported Profit as Percentage of Turnover

High−rate Firms Low−rate Firms

31 / 51

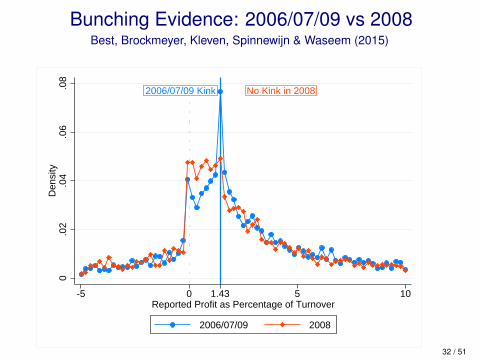

Bunching Evidence: 2006/07/09 vs 2008Best, Brockmeyer, Kleven, Spinnewijn & Waseem (2015)

2006/07/09 Kink No Kink in 2008

0.0

2.0

4.0

6.0

8D

ensi

ty

-5 0 1.43 5 10Reported Profit as Percentage of Turnover

2006/07/09 2008

32 / 51

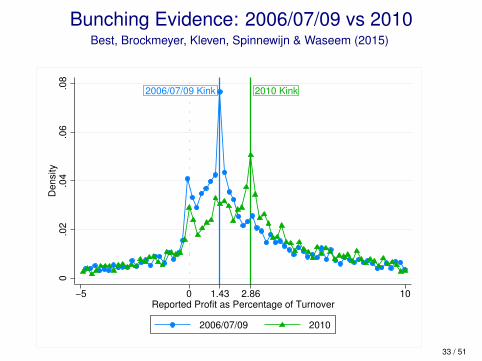

Bunching Evidence: 2006/07/09 vs 2010Best, Brockmeyer, Kleven, Spinnewijn & Waseem (2015)

2006/07/09 Kink 2010 Kink

0.0

2.0

4.0

6.0

8D

ensi

ty

−5 0 1.43 2.86 10Reported Profit as Percentage of Turnover

2006/07/09 2010

33 / 51

Summary of ResultsBest, Brockmeyer, Kleven, Spinnewijn & Waseem (2015)

I Bunching at MTS kink + model→ evasion responses toswitches between profit and turnover taxation

I Turnover taxes reduce evasion by up to 60-70% of corporateincome

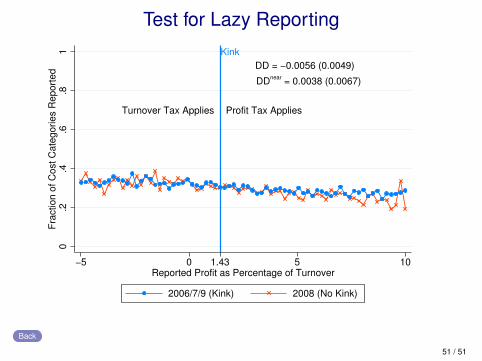

I Competing hypothesis: filing costs / lazy reporting Lazy Reporting

I Use empirical estimates and model to analyze the optimalchoice of tax instrument

I Switch from pure profit tax to pure turnover tax can increaserevenues by 74% without decreasing aggregate after-tax profits(i.e., a welfare gain)

I Does not include welfare cost from GE cascading

I So it may be worthwhile to deviate from production efficiencyto improve compliance

34 / 51

Tax Administration

35 / 51

Tax Administration

I In developing countries, incentives for civil servants are poor:I Pay is relatively lowI Pay is untied to performanceI Career advancement opportunities are limited/uncertainI Non-pecuniary job benefits (e.g. social status or influence) and

corruption can be substantial

I Research on public sector incentives in education and health

I Little research incentives and corruption in taxadministration

36 / 51

Pakistan Performance Pay ProjectKhan, Khwaja & Olken (2016)

I RCT in collaboration with the Excise & Taxation Department inPunjab, Pakistan

I Focus on the local property tax in Punjab

I Implement performance pay for tax officials in order to:I Raise tax revenueI With minimum cost (wage outlays, taxpayer dissatisfaction)

I Randomly allocate tax officials to different incentive schemes:I RevenueI Revenue PLUS (adjusts for accuracy and taxpayer satisfaction)I Flexible Bonus (wider set of criteria, subjective adjustments)

37 / 51

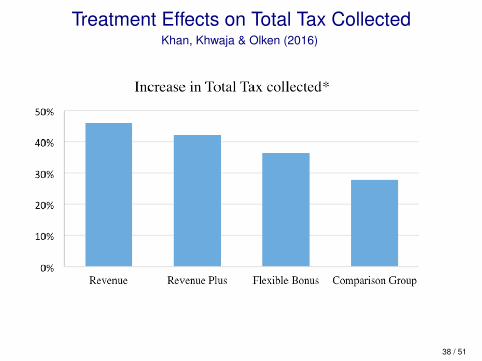

Treatment Effects on Total Tax CollectedKhan, Khwaja & Olken (2016)

26

IGC Project: Pakistan Performance Pay Project

Source: Khan, Khwaja, Olken (2014)

38 / 51

Corruption?Khan, Khwaja & Olken (2016)

I Revenue gains come from a small fraction of properties (3%)that become taxed at their true value

I In a survey, these taxpayers report not paying larger bribes

I The vast majority of properties in treated areas do not payhigher taxes, but instead report higher bribes

I This is roughly consistent with a collusion story:Performance pay increases tax collectors’ bargaining powerover taxpayers, who either have to pay higher bribes tocontinue evading or pay substantially higher taxes if collusionbreaks down

39 / 51

Tax Morale

40 / 51

Tax Morale

I Taxonomy of tax morale (Luttmer & Singhal 2014):I Intrinsic motivation (innate preference)I Social norms (depend on other individuals)I Reciprocity (depends on the state)I Culture (long-run societal effect)

I We know relatively little about such effects:I What is the quantitative importance of tax morale mechanisms?I Can policy makers affect tax morale through policy design?

I What we can say is that tax take and compliance arecorrelated with proxies for tax morale across countries

41 / 51

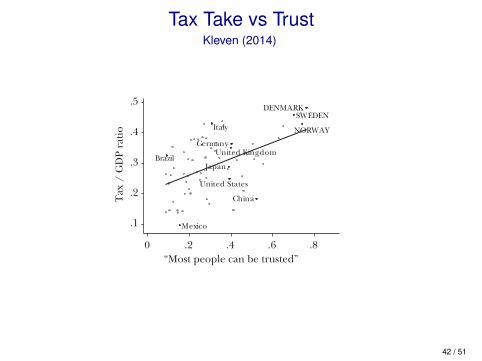

Tax Take vs TrustKleven (2014)

94 Journal of Economic Perspectives

Figure 6 Tax Take versus Social and Cultural Indicators across Countries

Notes and Sources: The figure shows the country-level observations, latest available year. Countries with GDP per capita below $5,000 (in 2005 PPP terms) or natural resource rents as a fraction of GDP above 20 percent are excluded from the sample. Tax/GDP ratio is the share of tax revenue in a given country’s nominal GDP in 2012 (source: Index of Economic Freedom, Heritage Foundation). Panel A: weighted-average survey response to the question of whether most people can be trusted, on a binary scale (source: WVS). Panel B: weighted-average survey response to the question of whether people live in need because of laziness or lack of willpower, or because of circumstances beyond individual control (injustice, luck, etc.). Panel C: social capital index is obtained from a principal component analysis of the following variables: 1) civic participation: weighted-average of a binary indicator for active membership of an organization (latest available year, source: WVS, various waves), 2) average voter turnout in elections held after 2000, excluding the European Parliament elections (source: Voter Turnout Database, IDEA), and 3) the inverse of the homicide rate (latest available year, source: UNODC). Panel C includes only democratic countries, defined as those with a Polity2 score above zero (source: Polity IV). Panel D: share of people donating money to charitable organizations in 2012 (source: World Giving Index, Charities Aid Foundation). A regression line is plotted in each panel.

Brazil

China

Germany

Italy

Japan

Mexico

United Kingdom

United States

DENMARK

NORWAY

SWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

0 .2 .4 .6 .8“Most people can be trusted”

Brazil

DENMARK

Germany

Italy

Japan

Mexico

United Kingdom

United States

NORWAY

SWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

0 .2 .4 .6 .8“People in need because of laziness,

lack of willpower”

A: Tax Take versus Trust

D: Tax Take versus Charitable DonationsC: Tax Take versus Social Capital Index(Civic Participation, Voter Turnout, Crime)

B: Tax Take versus Beliefs about the Poor

Germany

Italy

Japan

United Kingdom

United States

DENMARK

NORWAY SWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

−2 −1 0 1 2 3Social capital index

Brazil

China

Germany

Italy

Mexico

United Kingdom

United States

DENMARK

NORWAYSWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

0 .2 .4 .6 .8Fraction of people donating

money to charity

42 / 51

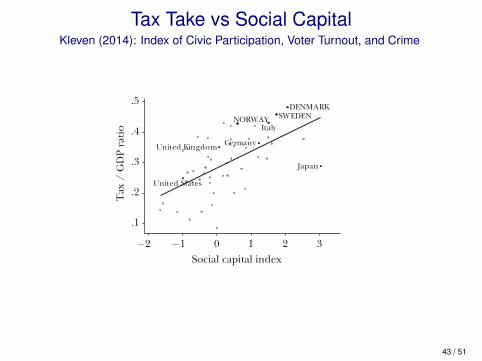

Tax Take vs Social CapitalKleven (2014): Index of Civic Participation, Voter Turnout, and Crime

94 Journal of Economic Perspectives

Figure 6 Tax Take versus Social and Cultural Indicators across Countries

Notes and Sources: The figure shows the country-level observations, latest available year. Countries with GDP per capita below $5,000 (in 2005 PPP terms) or natural resource rents as a fraction of GDP above 20 percent are excluded from the sample. Tax/GDP ratio is the share of tax revenue in a given country’s nominal GDP in 2012 (source: Index of Economic Freedom, Heritage Foundation). Panel A: weighted-average survey response to the question of whether most people can be trusted, on a binary scale (source: WVS). Panel B: weighted-average survey response to the question of whether people live in need because of laziness or lack of willpower, or because of circumstances beyond individual control (injustice, luck, etc.). Panel C: social capital index is obtained from a principal component analysis of the following variables: 1) civic participation: weighted-average of a binary indicator for active membership of an organization (latest available year, source: WVS, various waves), 2) average voter turnout in elections held after 2000, excluding the European Parliament elections (source: Voter Turnout Database, IDEA), and 3) the inverse of the homicide rate (latest available year, source: UNODC). Panel C includes only democratic countries, defined as those with a Polity2 score above zero (source: Polity IV). Panel D: share of people donating money to charitable organizations in 2012 (source: World Giving Index, Charities Aid Foundation). A regression line is plotted in each panel.

Brazil

China

Germany

Italy

Japan

Mexico

United Kingdom

United States

DENMARK

NORWAY

SWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

0 .2 .4 .6 .8“Most people can be trusted”

Brazil

DENMARK

Germany

Italy

Japan

Mexico

United Kingdom

United States

NORWAY

SWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

0 .2 .4 .6 .8“People in need because of laziness,

lack of willpower”

A: Tax Take versus Trust

D: Tax Take versus Charitable DonationsC: Tax Take versus Social Capital Index(Civic Participation, Voter Turnout, Crime)

B: Tax Take versus Beliefs about the Poor

Germany

Italy

Japan

United Kingdom

United States

DENMARK

NORWAY SWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

−2 −1 0 1 2 3Social capital index

Brazil

China

Germany

Italy

Mexico

United Kingdom

United States

DENMARK

NORWAYSWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

0 .2 .4 .6 .8Fraction of people donating

money to charity

43 / 51

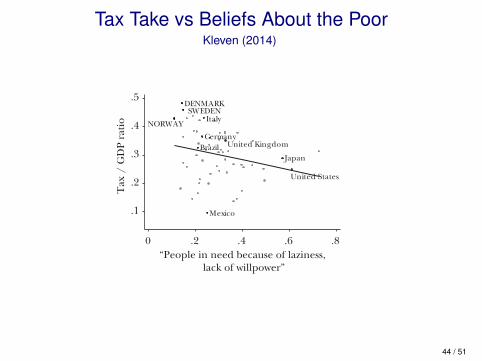

Tax Take vs Beliefs About the PoorKleven (2014)

94 Journal of Economic Perspectives

Figure 6 Tax Take versus Social and Cultural Indicators across Countries

Notes and Sources: The figure shows the country-level observations, latest available year. Countries with GDP per capita below $5,000 (in 2005 PPP terms) or natural resource rents as a fraction of GDP above 20 percent are excluded from the sample. Tax/GDP ratio is the share of tax revenue in a given country’s nominal GDP in 2012 (source: Index of Economic Freedom, Heritage Foundation). Panel A: weighted-average survey response to the question of whether most people can be trusted, on a binary scale (source: WVS). Panel B: weighted-average survey response to the question of whether people live in need because of laziness or lack of willpower, or because of circumstances beyond individual control (injustice, luck, etc.). Panel C: social capital index is obtained from a principal component analysis of the following variables: 1) civic participation: weighted-average of a binary indicator for active membership of an organization (latest available year, source: WVS, various waves), 2) average voter turnout in elections held after 2000, excluding the European Parliament elections (source: Voter Turnout Database, IDEA), and 3) the inverse of the homicide rate (latest available year, source: UNODC). Panel C includes only democratic countries, defined as those with a Polity2 score above zero (source: Polity IV). Panel D: share of people donating money to charitable organizations in 2012 (source: World Giving Index, Charities Aid Foundation). A regression line is plotted in each panel.

Brazil

China

Germany

Italy

Japan

Mexico

United Kingdom

United States

DENMARK

NORWAY

SWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

0 .2 .4 .6 .8“Most people can be trusted”

Brazil

DENMARK

Germany

Italy

Japan

Mexico

United Kingdom

United States

NORWAY

SWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

0 .2 .4 .6 .8“People in need because of laziness,

lack of willpower”

A: Tax Take versus Trust

D: Tax Take versus Charitable DonationsC: Tax Take versus Social Capital Index(Civic Participation, Voter Turnout, Crime)

B: Tax Take versus Beliefs about the Poor

Germany

Italy

Japan

United Kingdom

United States

DENMARK

NORWAY SWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

−2 −1 0 1 2 3Social capital index

Brazil

China

Germany

Italy

Mexico

United Kingdom

United States

DENMARK

NORWAYSWEDEN

.1

.2

.3

.4

.5

Tax

/ G

DP

rati

o

0 .2 .4 .6 .8Fraction of people donating

money to charity

44 / 51

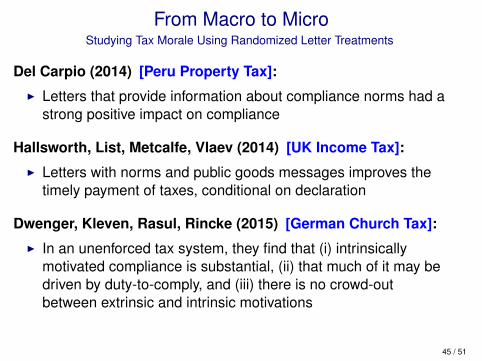

From Macro to MicroStudying Tax Morale Using Randomized Letter Treatments

Del Carpio (2014) [Peru Property Tax]:

I Letters that provide information about compliance norms had astrong positive impact on compliance

Hallsworth, List, Metcalfe, Vlaev (2014) [UK Income Tax]:

I Letters with norms and public goods messages improves thetimely payment of taxes, conditional on declaration

Dwenger, Kleven, Rasul, Rincke (2015) [German Church Tax]:

I In an unenforced tax system, they find that (i) intrinsicallymotivated compliance is substantial, (ii) that much of it may bedriven by duty-to-comply, and (iii) there is no crowd-outbetween extrinsic and intrinsic motivations

45 / 51

Conclusion

I PF-Devo was under-researched for a long time, but is nowquickly growing

I Recent work is fueled by the increasing availability ofadministrative data and a wealth of quasi-experimental variation

I Rather than relying on off-the-shelf developed countrysolutions, the literature takes a more “nitty-gritty microapproach” grounded in the specific context and constraints ofdeveloping countries

I There are still many unanswered questions, so hopefully wewill see much more work on this in the future

46 / 51

Appendix Graphs

47 / 51

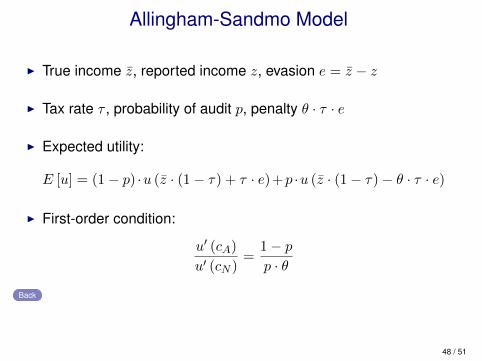

Allingham-Sandmo Model

I True income z̄, reported income z, evasion e = z̄ − z

I Tax rate τ , probability of audit p, penalty θ · τ · e

I Expected utility:

E [u] = (1− p) ·u (z̄ · (1− τ) + τ · e)+p ·u (z̄ · (1− τ)− θ · τ · e)

I First-order condition:

u′ (cA)

u′ (cN )=

1− pp · θ

Back

48 / 51

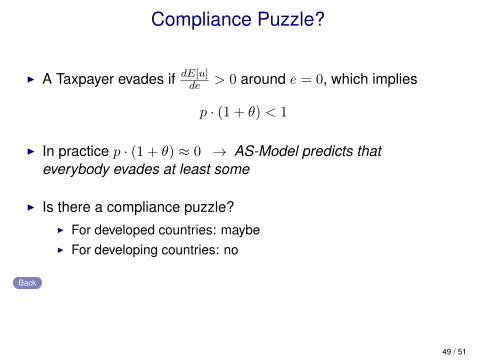

Compliance Puzzle?

I A Taxpayer evades if dE[u]de > 0 around e = 0, which implies

p · (1 + θ) < 1

I In practice p · (1 + θ) ≈ 0 → AS-Model predicts thateverybody evades at least some

I Is there a compliance puzzle?I For developed countries: maybeI For developing countries: no

Back

49 / 51

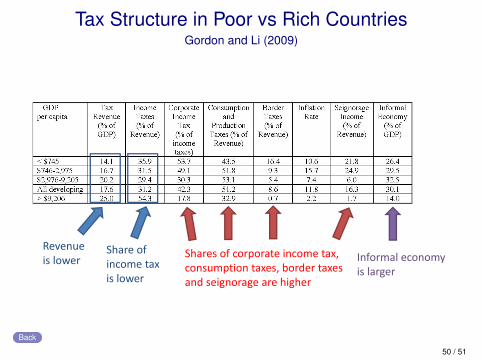

Tax Structure in Poor vs Rich CountriesGordon and Li (2009)

Revenue is lower

Share of income tax is lower

Shares of corporate income tax, consumption taxes, border taxesand seignorage are higher

Informal economyis larger

Back

50 / 51

Test for Lazy Reporting

DD = −0.0056 (0.0049)

DDnear = 0.0038 (0.0067)

Turnover Tax Applies Profit Tax Applies

Kink0

.2.4

.6.8

1Fr

actio

n of

Cos

t Cat

egor

ies

Rep

orte

d

−5 0 1.43 5 10Reported Profit as Percentage of Turnover

2006/7/9 (Kink) 2008 (No Kink)

Back

51 / 51