Embed Size (px)

Citation preview

Airplanes

Sierra Prochna, Elise Lepe, Louis Hwang, Evanka Weerasinghe, and

Stephanie Wilson

Competition and Landing Fee Emergence

Airline competition 20 years ago

• Most airports were public sector owned (gov’t)

• Regulation/specific agreements held landing fees to nonprofit levels (couldn’t bargain/change)

• Competition between airports didn’t exist

Changes now• Market structure: low cost airlines have brought

new, often non-central airports, into effective competition

• Privatization: 55 countries have partially or totally privatized their airports

• Regulation: currently a series of major regulatory changes proposed to airports

• Congestion: airports have increasingly become more congested, raising additional problems in short-run landing fee pricing but also long-run capacity expansion

Competition

• Extent to which passengers are willing to travel between alternative airports offering overlapping routes• Lower landing fees when airports

face airport competition

Countervailing Power

• The balancing of the market power of one group by that of another group

• Airports charge airlines for routes • In non-congested airports, the charge for

routes is cheaper in comparison to high-congested airports.

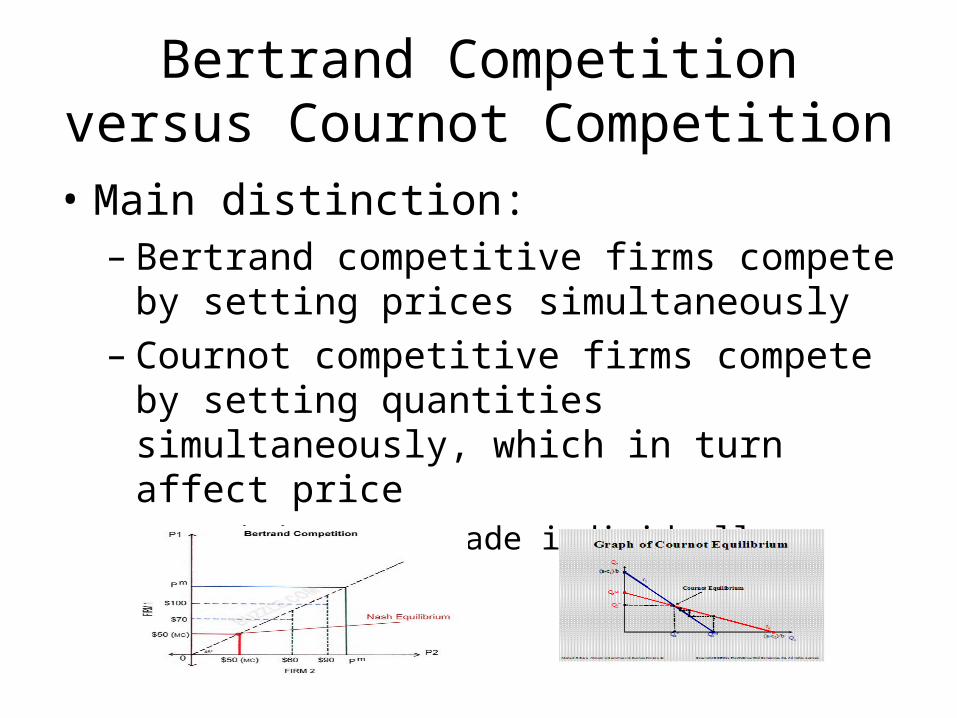

Bertrand Competition versus Cournot Competition

• Main distinction:– Bertrand competitive firms compete by setting

prices simultaneously– Cournot competitive firms compete by setting

quantities simultaneously, which in turn affect price• Decisions are made individually

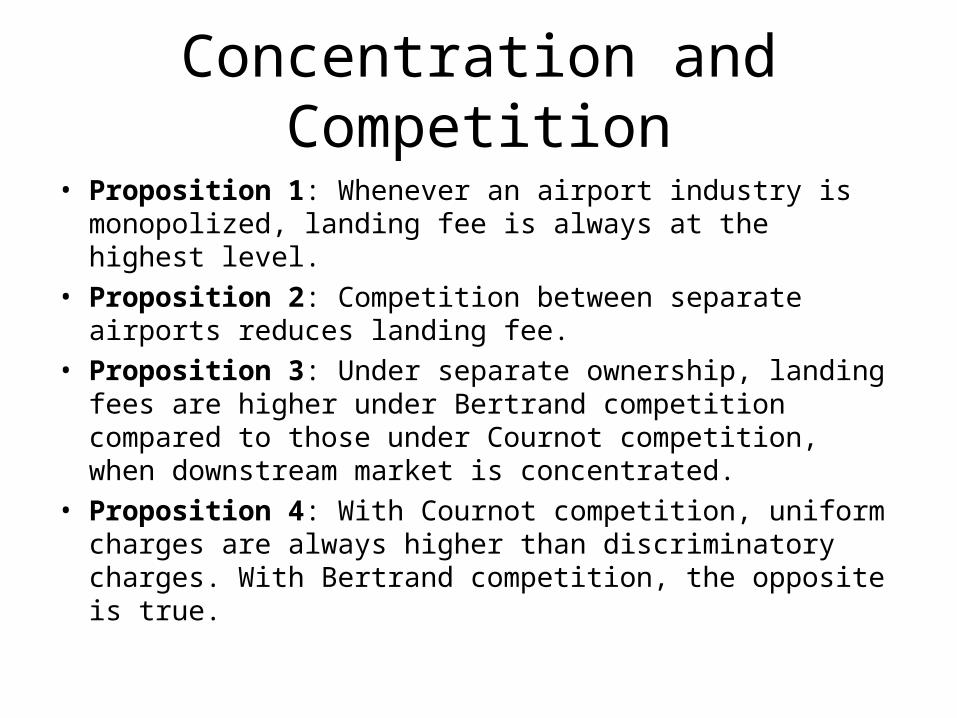

Concentration and Competition

• Proposition 1: Whenever an airport industry is monopolized, landing fee is always at the highest level.

• Proposition 2: Competition between separate airports reduces landing fee.

• Proposition 3: Under separate ownership, landing fees are higher under Bertrand competition compared to those under Cournot competition, when downstream market is concentrated.

• Proposition 4: With Cournot competition, uniform charges are always higher than discriminatory charges. With Bertrand competition, the opposite is true.

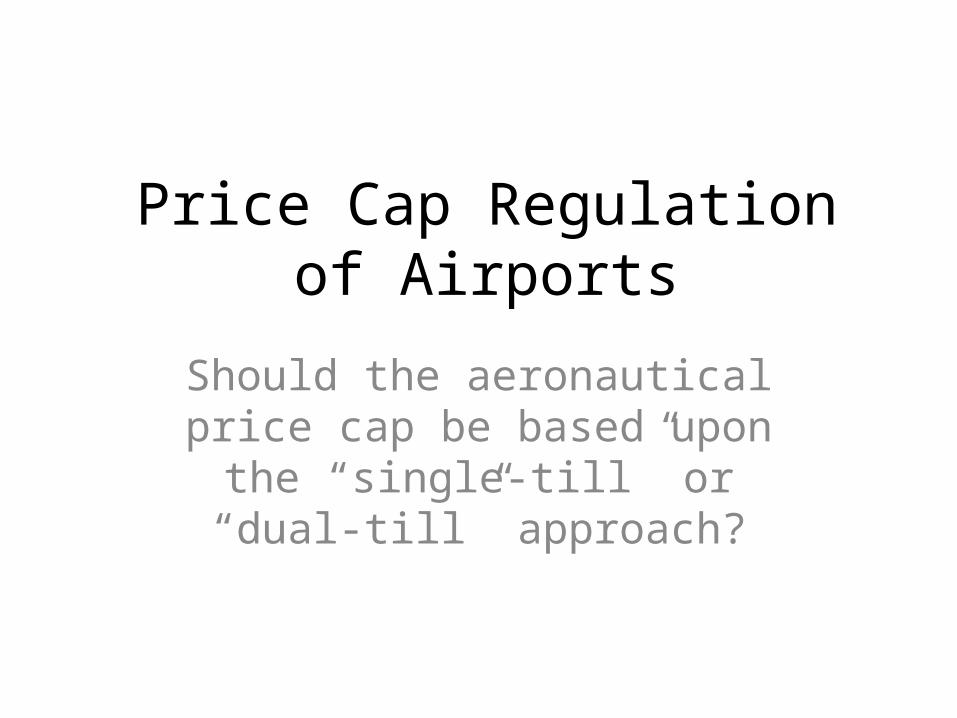

Price Cap Regulation of Airports

Should the aeronautical price cap be based upon the “single-till” or “dual-

till” approach?

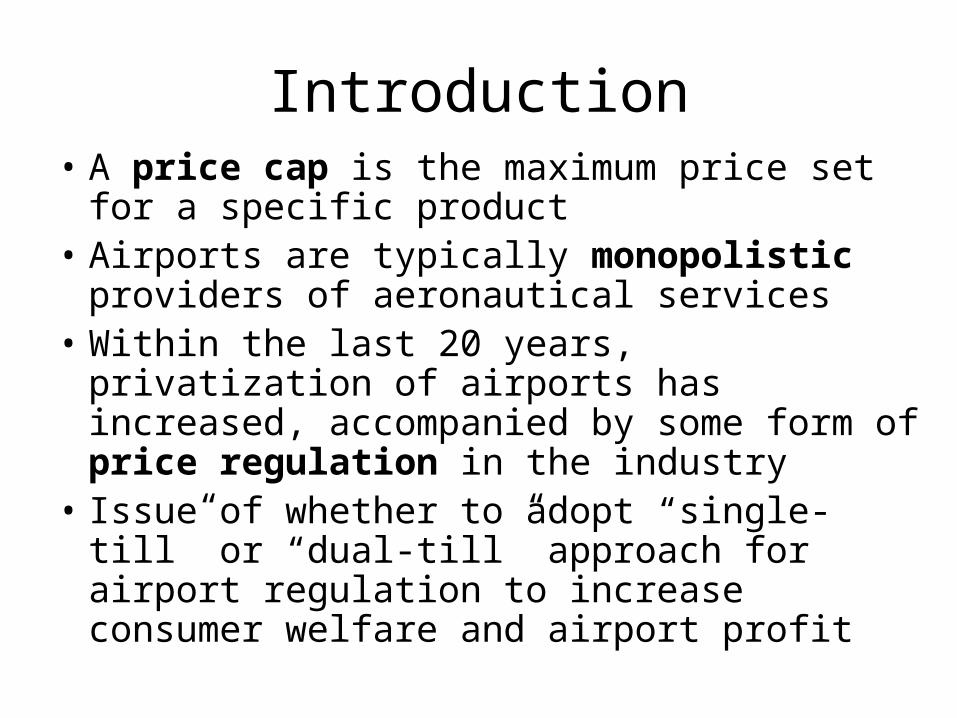

Introduction• A price cap is the maximum price set for a

specific product• Airports are typically monopolistic providers of

aeronautical services• Within the last 20 years, privatization of

airports has increased, accompanied by some form of price regulation in the industry

• Issue of whether to adopt “single-till” or “dual-till” approach for airport regulation to increase consumer welfare and airport profit

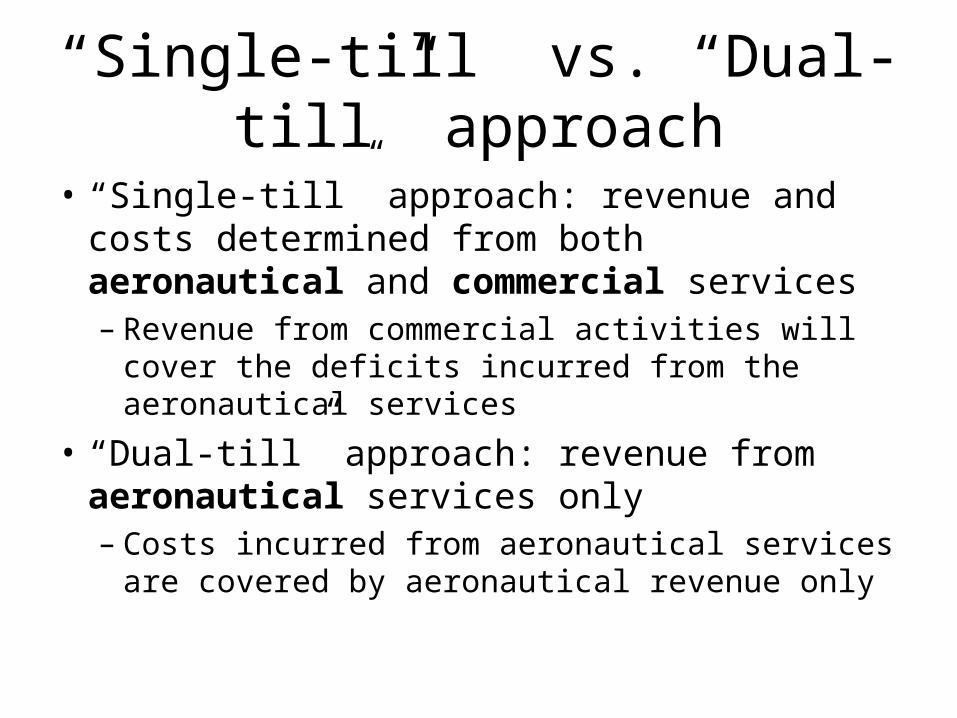

“Single-till” vs. “Dual-till” approach

• “Single-till” approach: revenue and costs determined from both aeronautical and commercial services– Revenue from commercial activities will cover the

deficits incurred from the aeronautical services

• “Dual-till” approach: revenue from aeronautical services only– Costs incurred from aeronautical services are

covered by aeronautical revenue only

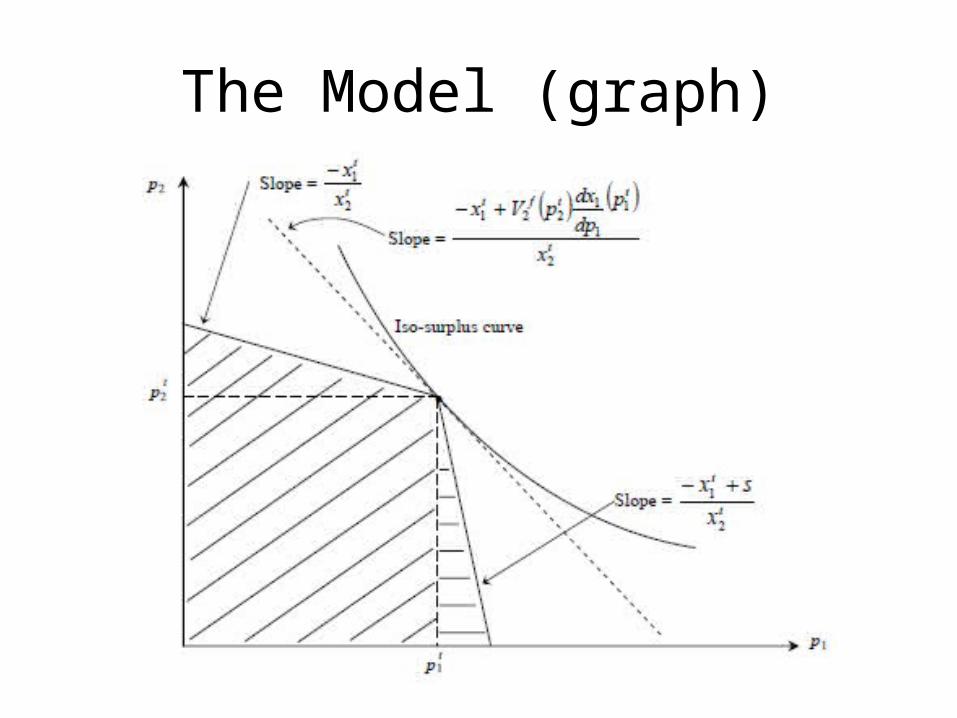

The Model (graph)

Determining Factors for the Model

1) the price elasticity of demand for aeronautical services

2) the consumer surplus for commercial services when both aeronautical and commercial services are priced as marginal cost

Results

• Brings the price of commercial services into the sphere of regulatory control

• Improves the boundaries of:– the demand for aeronautical services– the value of consumer surplus for commercial services

• Requires the regulator to determine:– a lower bound on the slope of the demand for

aeronautical services– an upper bound on the level of consumer surplus for

commercial services

Airplanes and Comparative Advantage

Transportation: Air vs. Surface

• Demand side: Consumers are most concerned with timely delivery

• Supply side: Producers are most concerned with transportation cost

• Transportation by air depends on value to weight ratio– Air shipping costs increase faster with weight than

surface shipping costs– Therefore, goods with a higher value to weight ratio

will most likely be shipped by air

Comparative Advantage

• Textbook definition: – “The ability to be better suited to the production of one

good than to the production of another good.”• Heavy goods (low value to weight ratio)– High cost for air shipping– Slow delivery– Comparative advantage for nearby suppliers

• Lightweight goods (high value to weight ratio)– Relatively low air shipping costs– Air suppliers can match timely delivery– Comparative advantage for distant suppliers

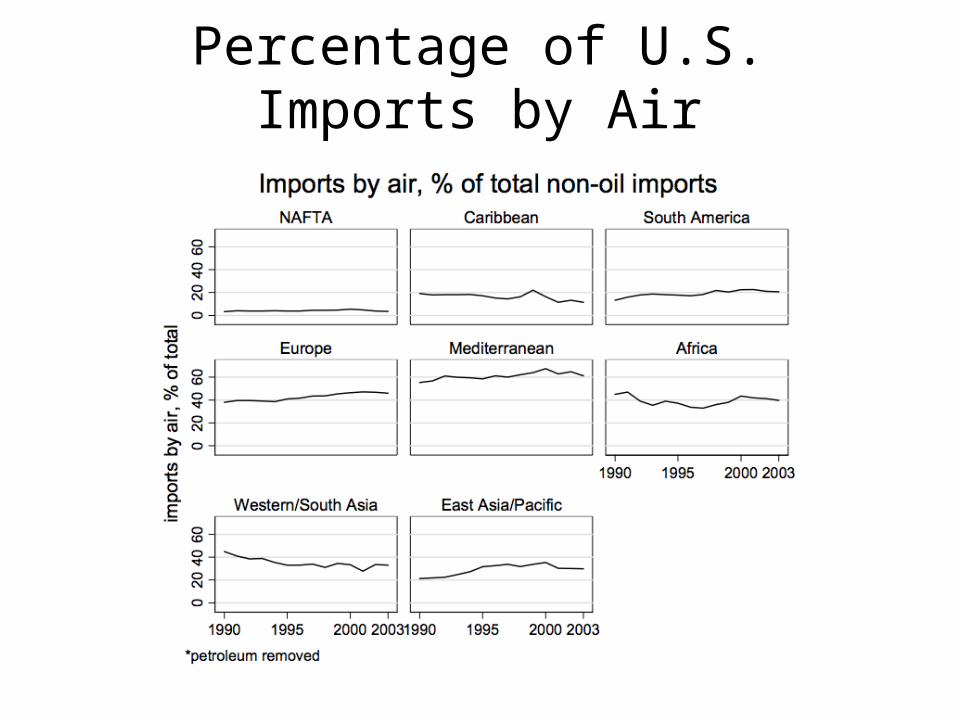

Percentage of U.S. Imports by Air

Specialization- Distance Matters!

• Falling air transport costs– Benefit all suppliers, but they benefit far away

suppliers disproportionally– Lead to greater specialization for distant producers

• With regards to U.S. imports, Canada and Mexico have higher market shares (greater comparative advantage) in goods which other countries do not ship by air

• The probability of air shipment is strongly related to distance and unit value

The Southwest Effect

Southwest• Operates in dense, short-haul markets where

it can provide frequent service• 50-70% lower unit costs than other major US

airlines• Dominates market share virtually everywhere

it serves– Most markets include another airline’s hub city– Controlled or strongly affected price for more

than 60% of travelers in dense markets under 500 miles

Main Points

• Return to profitability depends on developing lower-cost services in the short haul (0-500 miles) and increasing fares in the longer-haul (500+) markets.

• Competition sharply declined• Inability to continue charging relatively high fares in

short-haul markets would force a correction in the domestic industry’s long-haul pricing structure where fares were low in relation to costs

• The government needs to encourage low-cost, new entry

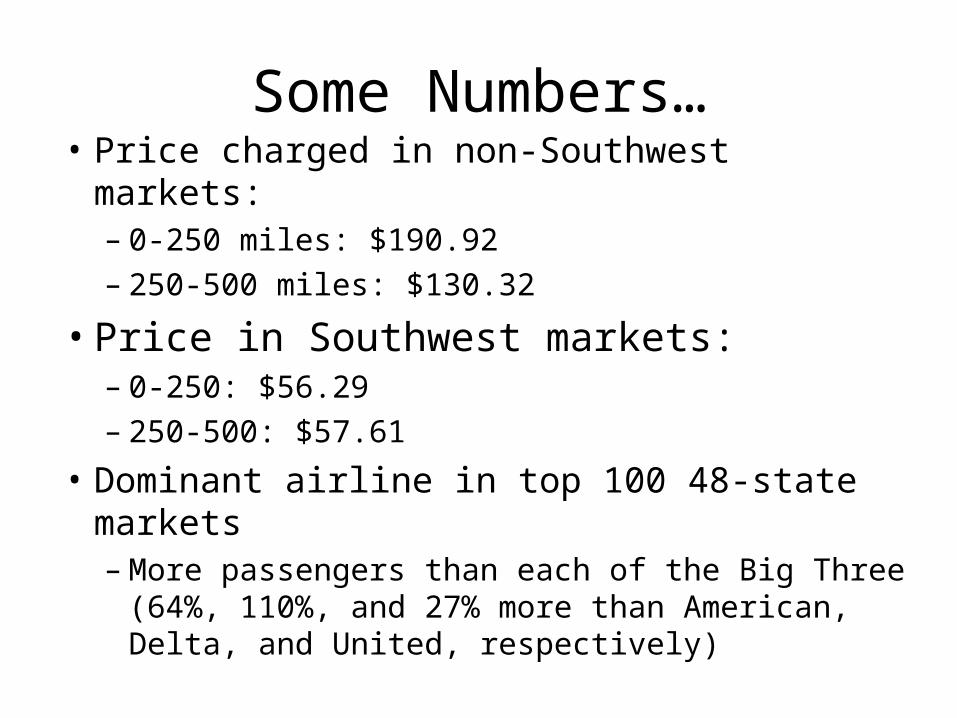

Some Numbers…• Price charged in non-Southwest markets:– 0-250 miles: $190.92– 250-500 miles: $130.32

• Price in Southwest markets:– 0-250: $56.29– 250-500: $57.61

• Dominant airline in top 100 48-state markets– More passengers than each of the Big Three (64%,

110%, and 27% more than American, Delta, and United, respectively)

• Other airlines had stopped trying to compete with Southwest for market share– Since Southwest entered airports, carriers either

exited or started to significantly increase prices due to a major loss of traffic

• Industry profitability had declined

Effects of Southwest’s Entry

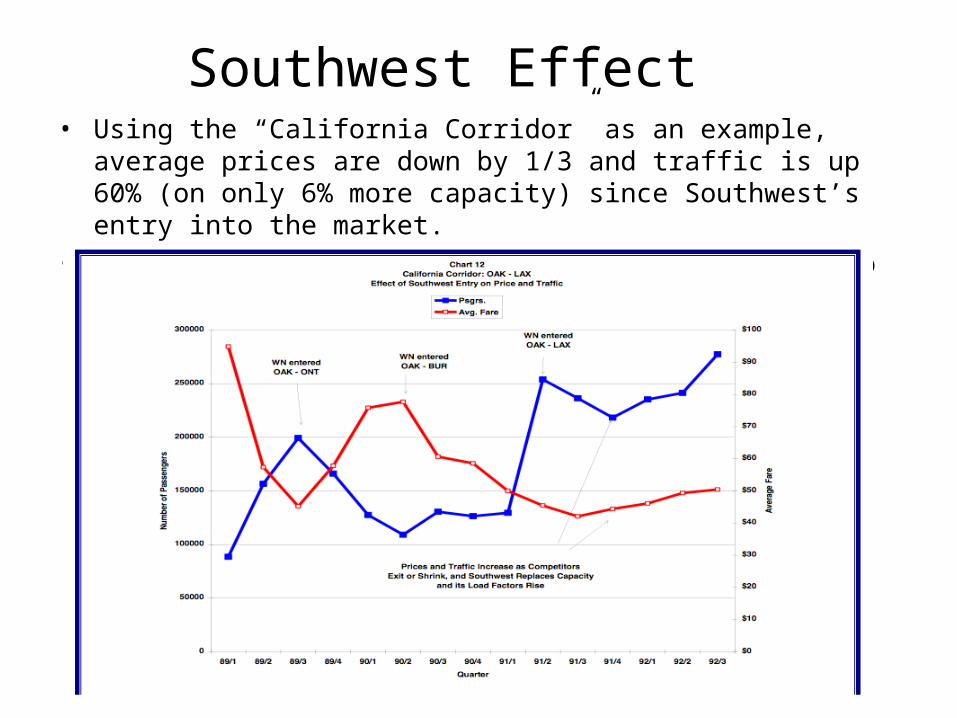

Southwest Effect• Using the “California Corridor” as an example, average prices are down by

1/3 and traffic is up 60% (on only 6% more capacity) since Southwest’s entry into the market.

• Average load factors have risen from under 50% to 67%

Importance of New Entrants

• New entrants will be the only way to• 1. replace the service lost when airlines exited markets

dominated by Southwest• 2. Exert cost competition on Southwest, which is

fading• 3. Extend low-fare services to other markets• Without new entrants, Southwest’s fares will increase

to cover costs and to start extracting monopoly profits. – Southwest’s costs have already increased in markets

where it has pushed out competitors and attained a relatively full load level

Bibliography• Haskel, J., AIozzi, A. and Valletti, T. “Market Structure, Countervailing Power and

Price Discrimination: The Case of Airports.” CEPR Discussion: http://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=4&ved=0CDoQFjAD&url=http%3A%2F%2Fwww.esrc.ac.uk%2Fmy-esrc%2Fgrants%2FRES-062-23-2099%2Foutputs%2FDownload%2F7ea08d70-351d-4fda-8558-a66f156889a1&ei=1bRvT-HTBsHL0QH01o29Bg&usg=AFQjCNEpMshvxUgEFx8IdGOb95VXbyfDtA

• Currier, Kevin. “Price Cap Regulation of Airports: A New Approach.” Economics Bulletin. Vol. 12, No. 8. (2008): pp. 1-7. http://www.accessecon.com/pubs/EB/2008/Volume12/EB-08L50001A.pdf.

• Harrigan, James. "Airplanes and Comparative Advantage." NBER Working Paper Series W11688 (2005).EconLit. 25 Mar. 2012. http://search.proquest.com/docview/56383287?accountid=14678

• Bennett, Randall. “The Southwest Effect.” Office of Aviation Analysis. May 1993: https://docs.google.com/a/virginia.edu/viewer?a=v&q=cache:4BUFbLMPXIIJ:ostpxweb.dot.gov/aviation/X-50%2520Role_files/Southwest%2520Effect.DOC+&hl=en&gl=us&pid=bl&srcid=ADGEESjqmeEQuxj-Rf84dn4Ajjq_zRfv2YIpnjUPfNhCNTIQTJiap_5DsoxYsyl6G8Xs9i6YD2XYDmxGsV5IMYYPgNYBM_A7TKvnXy7rm43jVwVa3AWnErXbnsVq0s9qxlUO4SWqPQ9i&sig=AHIEtbTflNJgQd8Eu6P00dBSLtUpzVt1uw&pli=1