Embed Size (px)

Citation preview

P a g e | 1

ECONOMIC & FINANCIAL MARKET ROUNDUP

Saturday, March 02, 2019

Economy ‖ Equity ‖ Money Market …Financial Possibilities

ECONOMIC REVIEW Nigeria’s lopsided GDP growth pattern magnified by Income and Expenditure approach estimates Over the past two weeks, the attention of all Nigerians and the international community

was largely focused on the presidential election which took place last Saturday and won

by the incumbent, Muhammadu Buhari (GCFR). While it is set that the ship of the Nigeria

economy will be sailed by the incumbent for another four years (in the absence of any

upset), a major issue that needs to be tackled headlong by this administration is the lopsided

nature of the Gross Domestic Product (GDP) growth pattern.

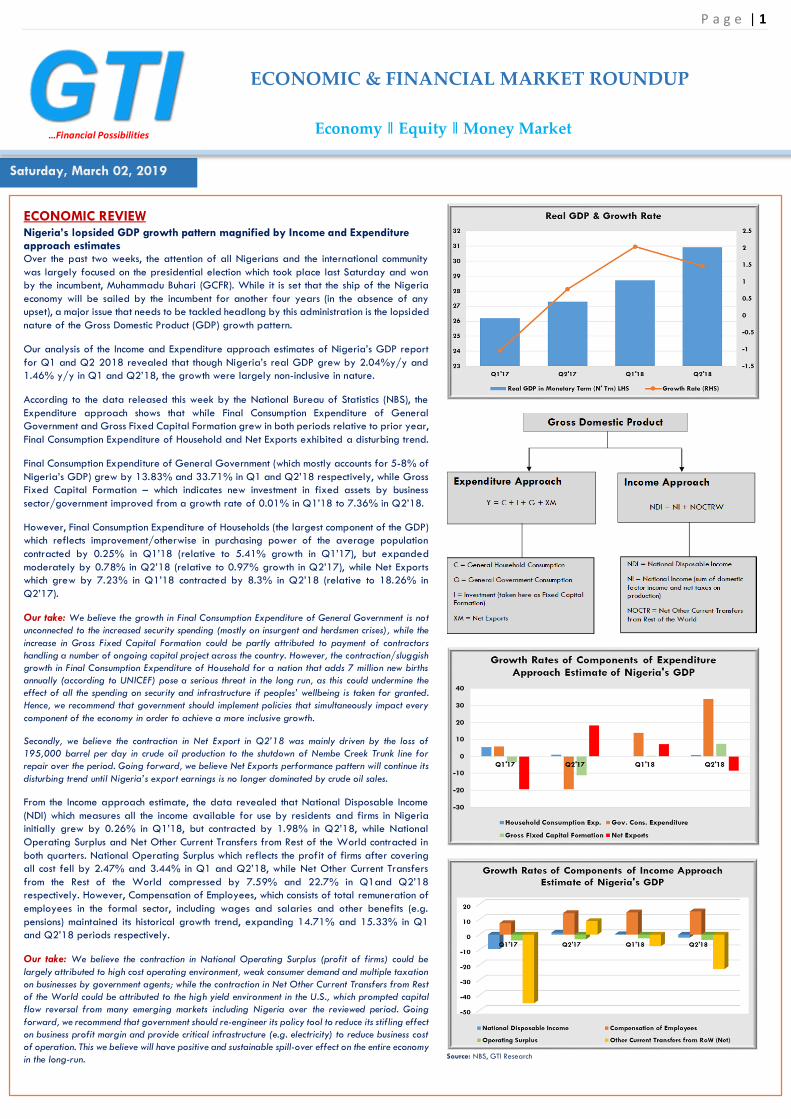

Our analysis of the Income and Expenditure approach estimates of Nigeria’s GDP report

for Q1 and Q2 2018 revealed that though Nigeria’s real GDP grew by 2.04%y/y and

1.46% y/y in Q1 and Q2’18, the growth were largely non-inclusive in nature.

According to the data released this week by the National Bureau of Statistics (NBS), the

Expenditure approach shows that while Final Consumption Expenditure of General

Government and Gross Fixed Capital Formation grew in both periods relative to prior year,

Final Consumption Expenditure of Household and Net Exports exhibited a disturbing trend.

Final Consumption Expenditure of General Government (which mostly accounts for 5-8% of

Nigeria’s GDP) grew by 13.83% and 33.71% in Q1 and Q2’18 respectively, while Gross

Fixed Capital Formation – which indicates new investment in fixed assets by business

sector/government improved from a growth rate of 0.01% in Q1’18 to 7.36% in Q2’18.

However, Final Consumption Expenditure of Households (the largest component of the GDP)

which reflects improvement/otherwise in purchasing power of the average population

contracted by 0.25% in Q1’18 (relative to 5.41% growth in Q1’17), but expanded

moderately by 0.78% in Q2’18 (relative to 0.97% growth in Q2’17), while Net Exports

which grew by 7.23% in Q1’18 contracted by 8.3% in Q2’18 (relative to 18.26% in

Q2’17).

Our take: We believe the growth in Final Consumption Expenditure of General Government is not

unconnected to the increased security spending (mostly on insurgent and herdsmen crises), while the

increase in Gross Fixed Capital Formation could be partly attributed to payment of contractors

handling a number of ongoing capital project across the country. However, the contraction/sluggish

growth in Final Consumption Expenditure of Household for a nation that adds 7 million new births

annually (according to UNICEF) pose a serious threat in the long run, as this could undermine the

effect of all the spending on security and infrastructure if peoples’ wellbeing is taken for granted.

Hence, we recommend that government should implement policies that simultaneously impact every

component of the economy in order to achieve a more inclusive growth.

Secondly, we believe the contraction in Net Export in Q2’18 was mainly driven by the loss of

195,000 barrel per day in crude oil production to the shutdown of Nembe Creek Trunk line for

repair over the period. Going forward, we believe Net Exports performance pattern will continue its

disturbing trend until Nigeria’s export earnings is no longer dominated by crude oil sales.

From the Income approach estimate, the data revealed that National Disposable Income

(NDI) which measures all the income available for use by residents and firms in Nigeria

initially grew by 0.26% in Q1’18, but contracted by 1.98% in Q2’18, while National

Operating Surplus and Net Other Current Transfers from Rest of the World contracted in

both quarters. National Operating Surplus which reflects the profit of firms after covering

all cost fell by 2.47% and 3.44% in Q1 and Q2’18, while Net Other Current Transfers

from the Rest of the World compressed by 7.59% and 22.7% in Q1and Q2’18

respectively. However, Compensation of Employees, which consists of total remuneration of

employees in the formal sector, including wages and salaries and other benefits (e.g.

pensions) maintained its historical growth trend, expanding 14.71% and 15.33% in Q1

and Q2’18 periods respectively.

Our take: We believe the contraction in National Operating Surplus (profit of firms) could be

largely attributed to high cost operating environment, weak consumer demand and multiple taxation

on businesses by government agents; while the contraction in Net Other Current Transfers from Rest

of the World could be attributed to the high yield environment in the U.S., which prompted capital

flow reversal from many emerging markets including Nigeria over the reviewed period. Going

forward, we recommend that government should re-engineer its policy tool to reduce its stifling effect

on business profit margin and provide critical infrastructure (e.g. electricity) to reduce business cost

of operation. This we believe will have positive and sustainable spill-over effect on the entire economy

in the long-run.

Source: NBS, GTI Research

P a g e | 2

EQUITY MARKET REVIEW

The Nigeria equity market this week closed three of the five trading session’s negative.

This was partly driven by low market upbeat in the aftermath of the highly tensed

presidential election and the drift of foreign inflows to the fixed income segment. As such,

the All-Share Index (ASI) and Market Capitalization value fell by 2.12% w/w to close at

31,827.24 points and ₦11.87 trillion respectively as against 32,515.52 points and

₦12.13 trillion in the previous week. In monetary terms, this translates to a week-on-week

decline of ₦256.67 billion in the Market Capitalization, while the ASI Year-To-Date (YTD)

index declined from 3.45% last Friday to 1.26%.

On week-on-week basis, two sectors – Insurance (+3.0%w/w) and Industrial goods

(+0.9%w/w) recorded gains, while loses were recorded by Banking (-5.9%w/w),

Consumer goods (-2.9%w/w) and Oil & Gas (-0.24%w/w) sector.

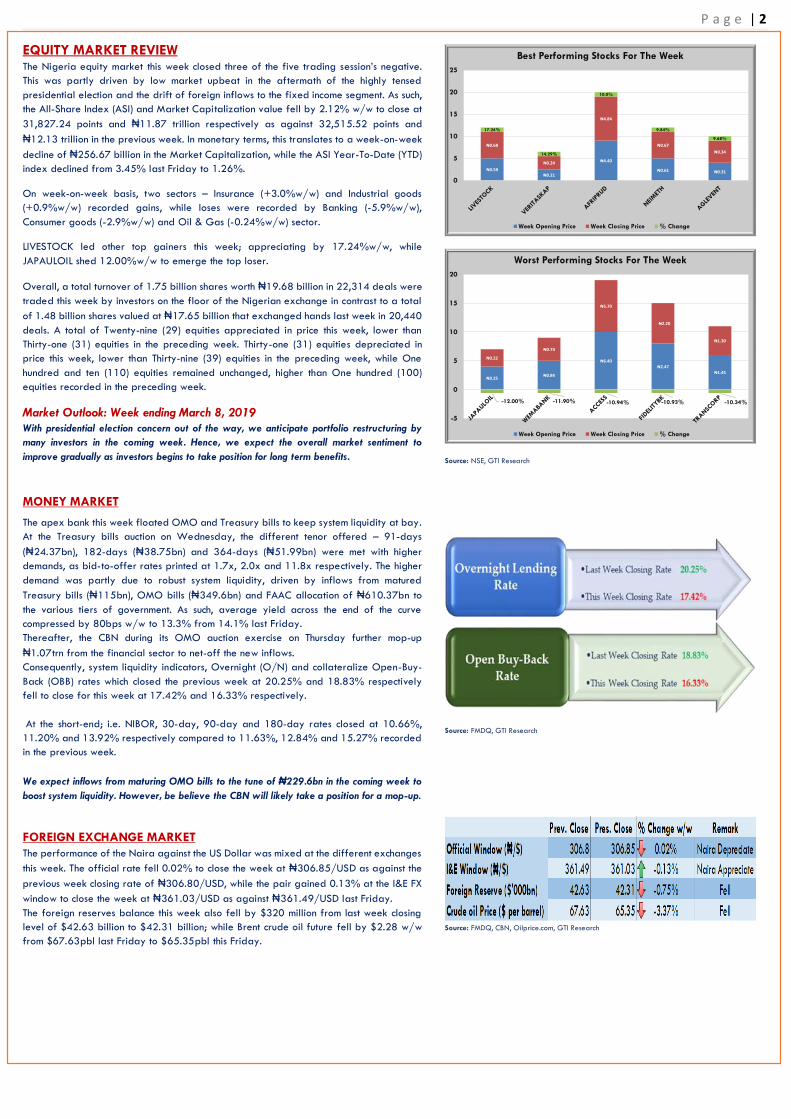

LIVESTOCK led other top gainers this week; appreciating by 17.24%w/w, while

JAPAULOIL shed 12.00%w/w to emerge the top loser.

Overall, a total turnover of 1.75 billion shares worth ₦19.68 billion in 22,314 deals were

traded this week by investors on the floor of the Nigerian exchange in contrast to a total

of 1.48 billion shares valued at ₦17.65 billion that exchanged hands last week in 20,440

deals. A total of Twenty-nine (29) equities appreciated in price this week, lower than

Thirty-one (31) equities in the preceding week. Thirty-one (31) equities depreciated in

price this week, lower than Thirty-nine (39) equities in the preceding week, while One

hundred and ten (110) equities remained unchanged, higher than One hundred (100)

equities recorded in the preceding week.

Market Outlook: Week ending March 8, 2019

With presidential election concern out of the way, we anticipate portfolio restructuring by

many investors in the coming week. Hence, we expect the overall market sentiment to

improve gradually as investors begins to take position for long term benefits.

MONEY MARKET

The apex bank this week floated OMO and Treasury bills to keep system liquidity at bay.

At the Treasury bills auction on Wednesday, the different tenor offered – 91-days

(₦24.37bn), 182-days (₦38.75bn) and 364-days (₦51.99bn) were met with higher

demands, as bid-to-offer rates printed at 1.7x, 2.0x and 11.8x respectively. The higher

demand was partly due to robust system liquidity, driven by inflows from matured

Treasury bills (₦115bn), OMO bills (₦349.6bn) and FAAC allocation of ₦610.37bn to

the various tiers of government. As such, average yield across the end of the curve

compressed by 80bps w/w to 13.3% from 14.1% last Friday.

Thereafter, the CBN during its OMO auction exercise on Thursday further mop-up

₦1.07trn from the financial sector to net-off the new inflows.

Consequently, system liquidity indicators, Overnight (O/N) and collateralize Open-Buy-

Back (OBB) rates which closed the previous week at 20.25% and 18.83% respectively

fell to close for this week at 17.42% and 16.33% respectively.

At the short-end; i.e. NIBOR, 30-day, 90-day and 180-day rates closed at 10.66%,

11.20% and 13.92% respectively compared to 11.63%, 12.84% and 15.27% recorded

in the previous week.

We expect inflows from maturing OMO bills to the tune of ₦229.6bn in the coming week to

boost system liquidity. However, be believe the CBN will likely take a position for a mop-up.

FOREIGN EXCHANGE MARKET

The performance of the Naira against the US Dollar was mixed at the different exchanges

this week. The official rate fell 0.02% to close the week at ₦306.85/USD as against the

previous week closing rate of ₦306.80/USD, while the pair gained 0.13% at the I&E FX

window to close the week at ₦361.03/USD as against ₦361.49/USD last Friday.

The foreign reserves balance this week also fell by $320 million from last week closing

level of $42.63 billion to $42.31 billion; while Brent crude oil future fell by $2.28 w/w

from $67.63pbl last Friday to $65.35pbl this Friday.

Source: NSE, GTI Research

Source: FMDQ, GTI Research

Source: FMDQ, CBN, Oilprice.com, GTI Research

₦0.58₦0.21

₦4.40

₦0.61 ₦0.31

₦0.68

₦0.24

₦4.84

₦0.67

₦0.34

17.24%

14.29%

10.0%

9.84%

9.68%

0

5

10

15

20

25

Best Performing Stocks For The Week

Week Opening Price Week Closing Price % Change

₦0.25₦0.84

₦6.40₦2.47

₦1.45

₦0.22

₦0.74

₦5.70

₦2.20

₦1.30

-12.00% -11.90% -10.94% -10.93% -10.34%

-5

0

5

10

15

20

Worst Performing Stocks For The Week

Week Opening Price Week Closing Price % Change

P a g e | 3

DISCLOSURE

Conflict of Interest

GTI Securities Ltd and its sister companies within the GTI Group may execute transactions in securities of companies mentioned

in this document and may also perform or seek to perform investment banking services for those companies mentioned herein.

Trading desks may trade, or have traded, as principal on the basis of the research analyst(s) views and report(s).

Analyst Certification

Where applicable, the views expressed in this report accurately reflect the analysts' views about any and all of the investments

or issuers to which the report relates, and no part of the analysts' compensation was, is, or will be, directly or indirectly, related

to the specific recommendations, views or corporate finance transactions expressed in the report.

Disclaimer

This report by GTI Securities Ltd is for information purposes only. While opinions and estimates therein have been carefully

prepared, the company and its employees do not guaranty the complete accuracy of the information contained herewith as

information was also gathered from various sources believed to be reliable and accurate at the time of this report. We do not

take responsibility therefore for any loss arising from the use of the information.

For enquires/research queries, please send an email to [email protected]

Analyst

Damilare Asimiyu | +234 806 0722 944