Embed Size (px)

Citation preview

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 1/12

Ankit Tiwari (R#7) Avneesh Munjal (R#18)Meenakshi Deshpande

(R#34)Sanket Tandon (R# 52)Sobhit Agarwal (R# 56)

Indian Institute of ForeignTrade

MBA(IB) 2013-15

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 2/12

Industry Overview

Major Players in the Industry

Performance Overview

Recent Happenings

Major Events in Aviation Industry

Porter Analysis

Aero Turbine Fuel (ATF)

Policy Support

Future Outlook

AGENDA

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 3/12

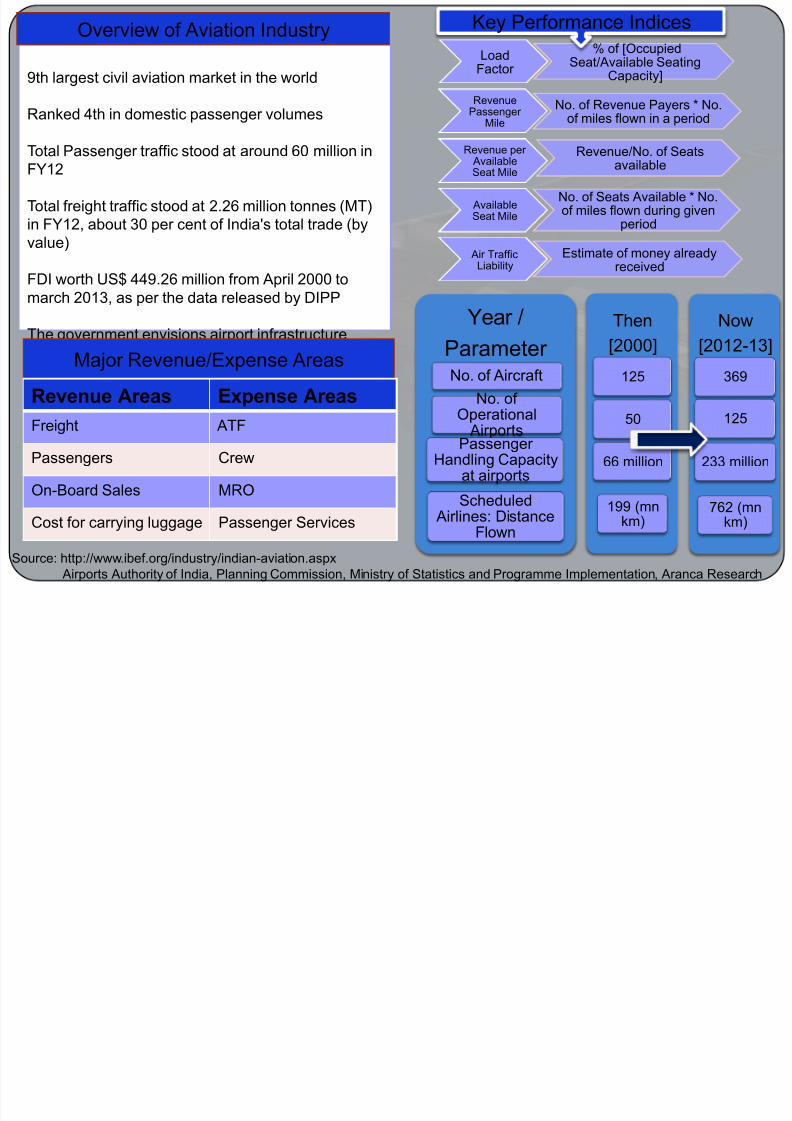

9th largest civil aviation market in the world

Ranked 4th in domestic passenger volumes

Total Passenger traffic stood at around 60 million inFY12

Total freight traffic stood at 2.26 million tonnes (MT)in FY12, about 30 per cent of India's total trade (byvalue)

FDI worth US$ 449.26 million from April 2000 tomarch 2013, as per the data released by DIPP

The government envisions airport infrastructureinvestment of US$11.4 billion under the 12th FiveYear Plan (2012-17)

Year /

Parameter No. of Aircraft

No. of

Operational Airports

Passenger Handling Capacity

at airports

Scheduled Airlines: Distance

Flown

Then

[2000]

125

50

66 million

199 (mnkm)

Now

[2012-13]

369

125

233 million

762 (mnkm)

Source: http://www.ibef.org/industry/indian-aviation.aspx Airports Authority of India, Planning Commission, Ministry of Statistics and Programme Implementation, Aranca Research

LoadFactor

% of [OccupiedSeat/Available Seating

Capacity]

RevenuePassenger

Mile

No. of Revenue Payers * No.of miles flown in a period

Revenue per AvailableSeat Mile

Revenue/No. of Seatsavailable

AvailableSeat Mile

No. of Seats Available * No.of miles flown during given

period

Air TrafficLiability

Estimate of money alreadyreceived

Key Performance IndicesOverview of Aviation Industry

Major Revenue/Expense Areas

Revenue Areas Expense Areas

Freight ATF

Passengers Crew

On-Board Sales MRO

Cost for carrying luggage Passenger Services

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 4/12

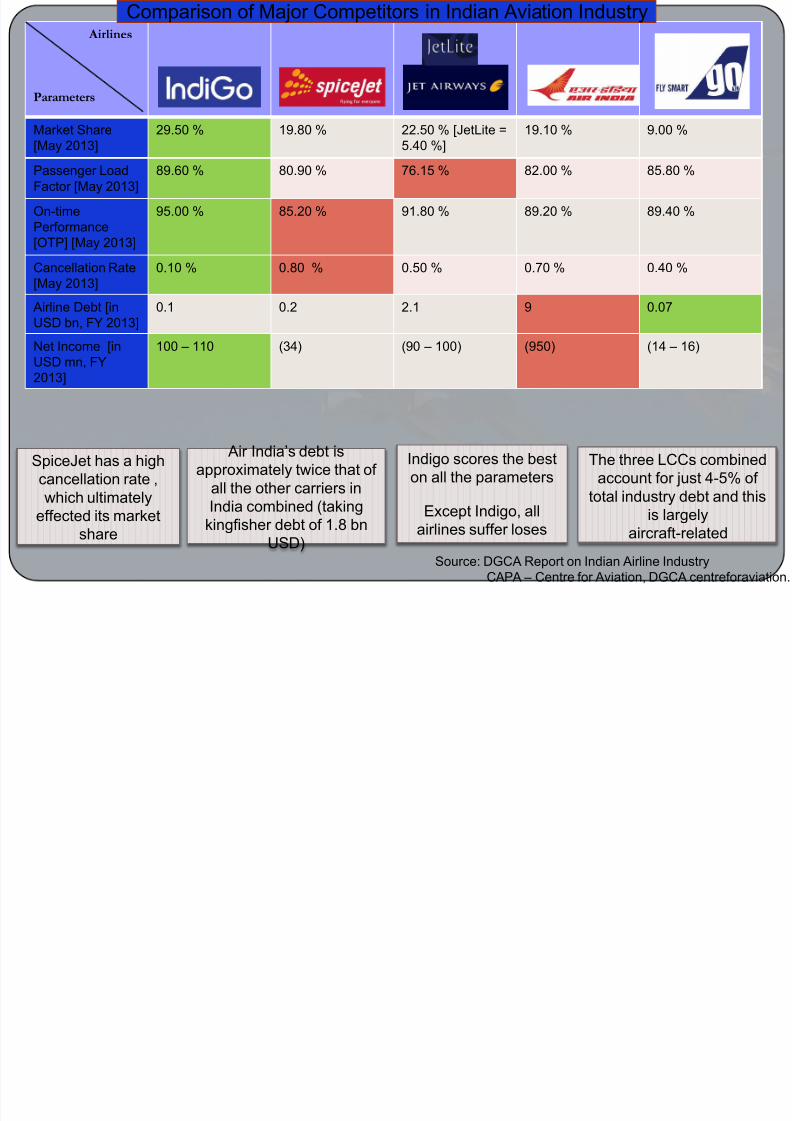

Airlines

Parameters

Market Share[May 2013]

29.50 % 19.80 % 22.50 % [JetLite =5.40 %]

19.10 % 9.00 %

Passenger LoadFactor [May 2013]

89.60 % 80.90 % 76.15 % 82.00 % 85.80 %

On-timePerformance[OTP] [May 2013]

95.00 % 85.20 % 91.80 % 89.20 % 89.40 %

Cancellation Rate[May 2013]

0.10 % 0.80 % 0.50 % 0.70 % 0.40 %

Airline Debt [inUSD bn, FY 2013]

0.1 0.2 2.1 9 0.07

Net Income [inUSD mn, FY2013]

100 – 110 (34) (90 – 100) (950) (14 – 16)

Source: DGCA Report on Indian Airline IndustryCAPA – Centre for Aviation, DGCA centreforaviation.

Indigo scores the beston all the parameters

Except Indigo, allairlines suffer loses

SpiceJet has a highcancellation rate ,which ultimately

effected its marketshare

Air India’s debt is approximately twice that of

all the other carriers inIndia combined (taking

kingfisher debt of 1.8 bnUSD)

The three LCCs combinedaccount for just 4-5% of

total industry debt and thisis largely

aircraft-related

Comparison of Major Competitors in Indian Aviation Industry

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 5/12

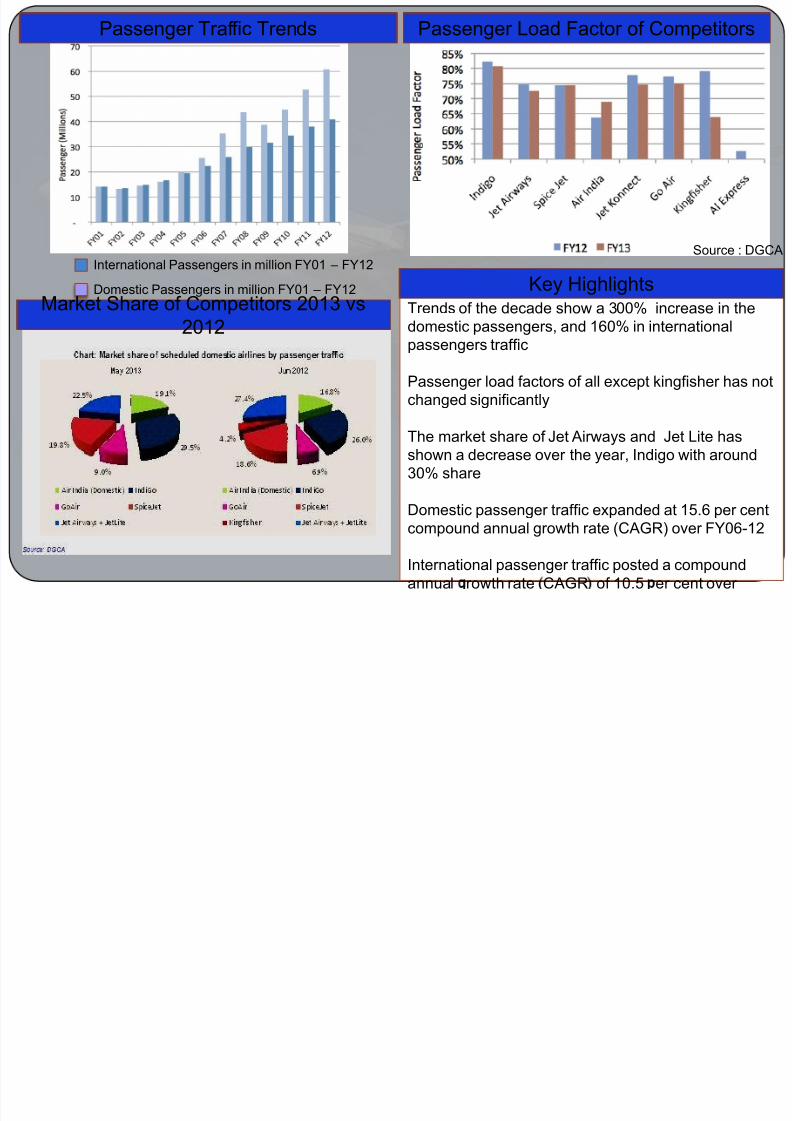

Trends of the decade show a 300% increase in thedomestic passengers, and 160% in internationalpassengers traffic

Passenger load factors of all except kingfisher has notchanged significantly

The market share of Jet Airways and Jet Lite hasshown a decrease over the year, Indigo with around30% share

Domestic passenger traffic expanded at 15.6 per centcompound annual growth rate (CAGR) over FY06-12

International passenger traffic posted a compoundannual rowth rate CAGR of 10.5 er cent over

Domestic Passengers in million FY01 – FY12

International Passengers in million FY01 – FY12Source : DGCA

Key Highlights

Passenger Traffic Trends Passenger Load Factor of Competitors

Market Share of Competitors 2013 vs2012

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 6/12

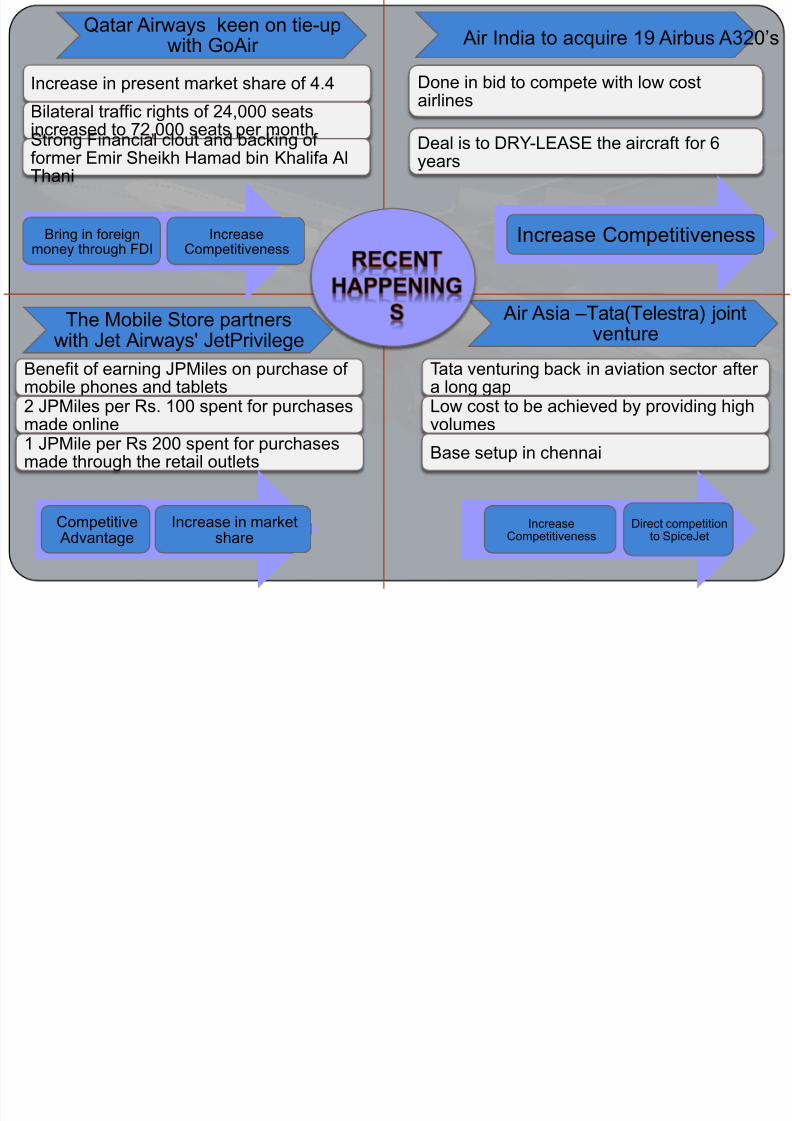

Qatar Airways keen on tie-upwith GoAir

Increase in present market share of 4.4

Bilateral traffic rights of 24,000 seats

increased to 72,000 seats per month

Strong Financial clout and backing of former Emir Sheikh Hamad bin Khalifa AlThani

Bring in foreignmoney through FDI

IncreaseCompetitiveness

Done in bid to compete with low costairlines

Deal is to DRY-LEASE the aircraft for 6years

Increase Competitiveness

The Mobile Store partnerswith Jet Airways' JetPrivilege

Air Asia –Tata(Telestra) jointventure

Benefit of earning JPMiles on purchase of mobile phones and tablets

2 JPMiles per Rs. 100 spent for purchasesmade online

1 JPMile per Rs 200 spent for purchasesmade through the retail outlets

Tata venturing back in aviation sector after a long gap

Low cost to be achieved by providing highvolumes

Base setup in chennai

Competitive Advantage

Increase in marketshare

IncreaseCompetitiveness

Direct competitionto SpiceJet

Air India to acquire 19 Airbus A320’s

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 7/12

Major Events In AviationIndustry

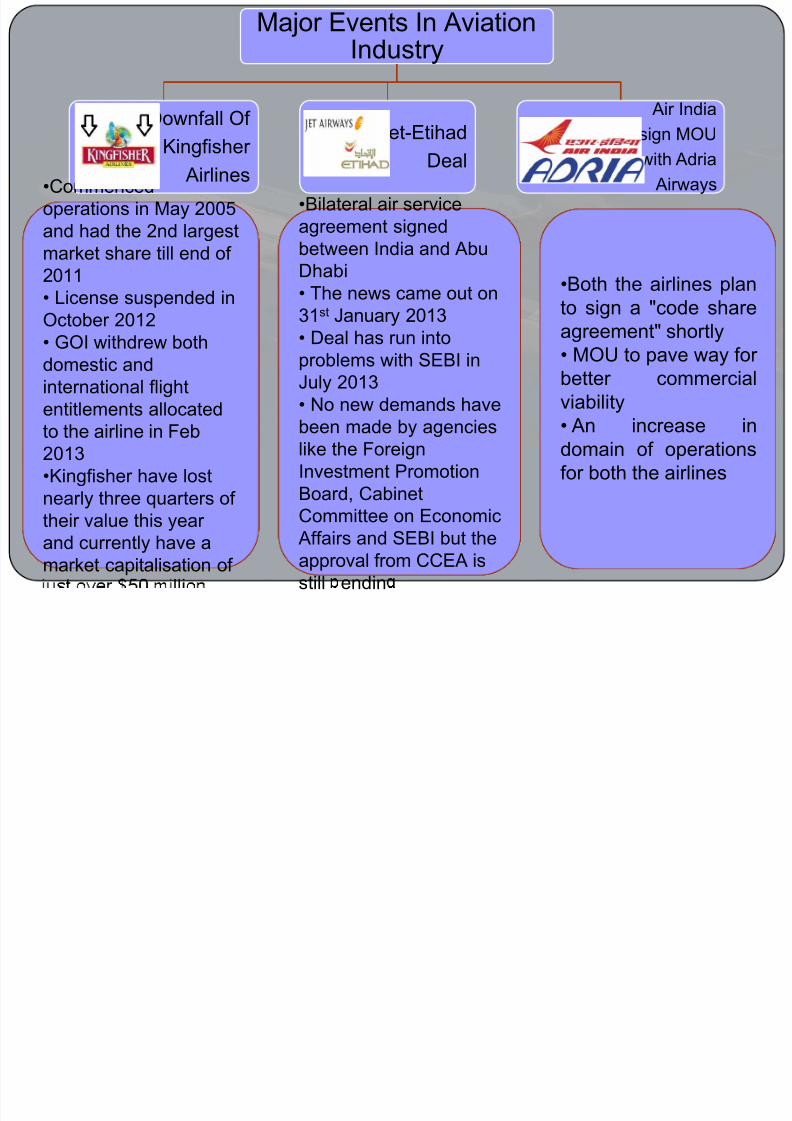

Downfall Of

Kingfisher

Airlines

Jet-EtihadDeal

Air India

sign MOUwith Adria

Airways•Commencedoperations in May 2005and had the 2nd largestmarket share till end of

2011• License suspended inOctober 2012• GOI withdrew bothdomestic andinternational flight

entitlements allocatedto the airline in Feb2013•Kingfisher have lostnearly three quarters of their value this year

and currently have amarket capitalisation of

•Bilateral air serviceagreement signedbetween India and Abu

Dhabi• The news came out on31st January 2013• Deal has run intoproblems with SEBI inJuly 2013•

No new demands havebeen made by agencieslike the ForeignInvestment PromotionBoard, CabinetCommittee on Economic

Affairs and SEBI but theapproval from CCEA isstill endin

•Both the airlines planto sign a "code shareagreement" shortly• MOU to pave way for better commercialviability• An increase indomain of operationsfor both the airlines

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 8/12

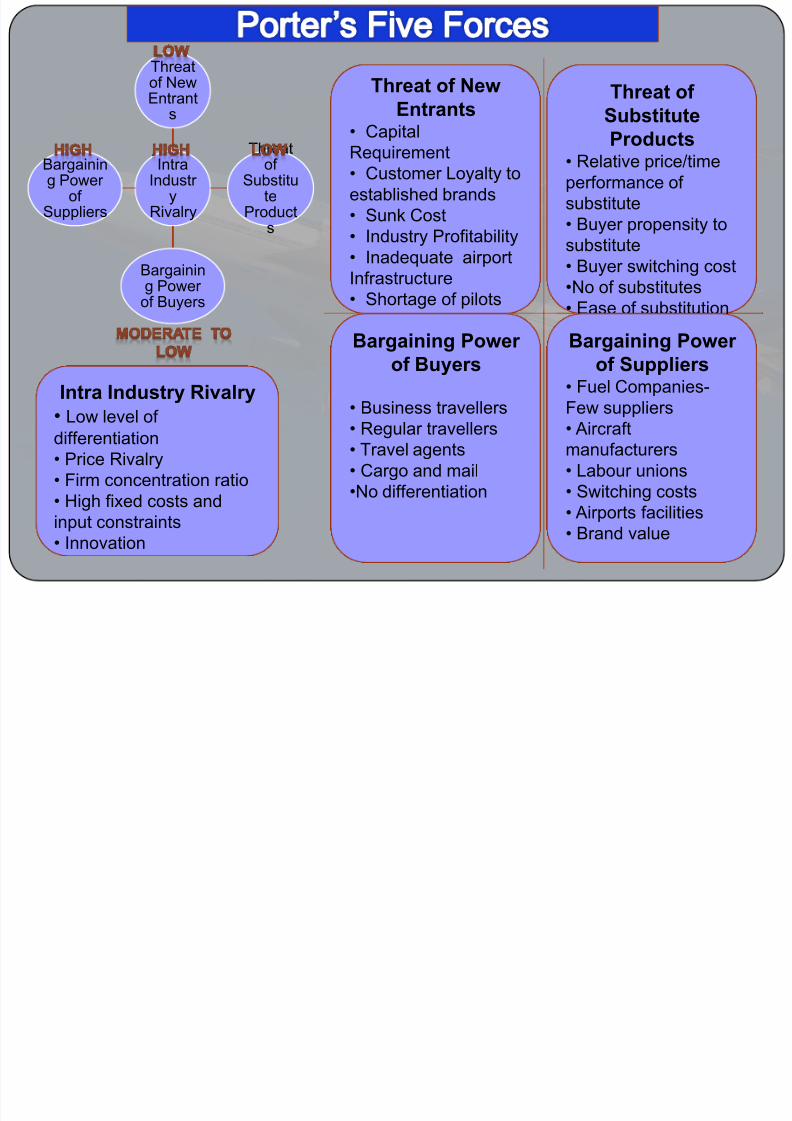

IntraIndustr

yRivalry

Threatof NewEntrant

s

Threatof

Substitute

Products

Bargaining Power of Buyers

Bargaining Power

of Suppliers

Threat of

Substitute

Products• Relative price/timeperformance of substitute• Buyer propensity tosubstitute

• Buyer switching cost •No of substitutes

• Ease of substitution• Video conferencing,railways.

Threat of New

Entrants

• CapitalRequirement• Customer Loyalty toestablished brands• Sunk Cost• Industry Profitability• Inadequate airport

Infrastructure• Shortage of pilotsand high fuel cost.

Bargaining Power

of Suppliers• Fuel Companies-

Few suppliers • Aircraftmanufacturers

• Labour unions

• Switching costs

• Airports facilities

• Brand value

Bargaining Power

of Buyers

• Business travellers • Regular travellers

• Travel agents

• Cargo and mail•No differentiation

Intra Industry Rivalry

• Low level of differentiation

• Price Rivalry

• Firm concentration ratio• High fixed costs andinput constraints• Innovation

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 9/12

(ATF)Financial

Highlights

Recent NewsImplications

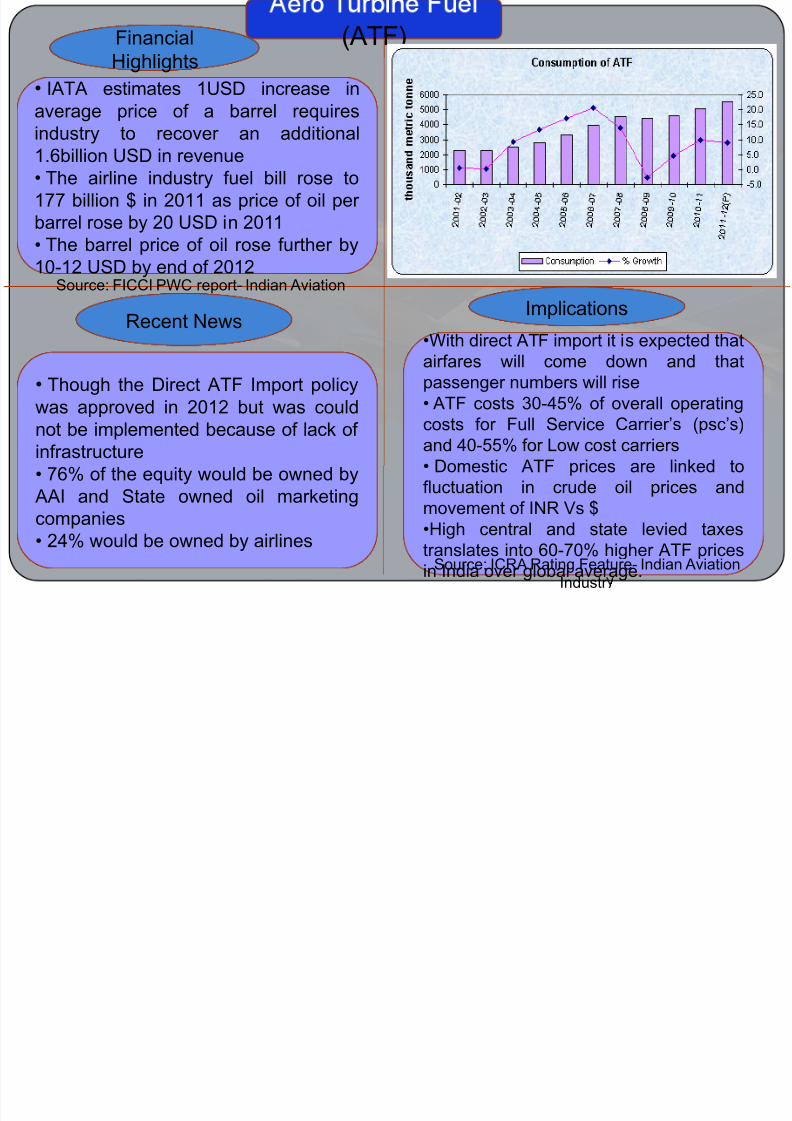

• IATA estimates 1USD increase inaverage price of a barrel requires

industry to recover an additional1.6billion USD in revenue• The airline industry fuel bill rose to177 billion $ in 2011 as price of oil per barrel rose by 20 USD in 2011• The barrel price of oil rose further by

10-12 USD by end of 2012

• Though the Direct ATF Import policy

was approved in 2012 but was couldnot be implemented because of lack of infrastructure• 76% of the equity would be owned by

AAI and State owned oil marketingcompanies• 24% would be owned by airlines

•With direct ATF import it is expected thatairfares will come down and thatpassenger numbers will rise• ATF costs 30-45% of overall operatingcosts for Full Service Carrier’s (psc’s)and 40-55% for Low cost carriers• Domestic ATF prices are linked tofluctuation in crude oil prices andmovement of INR Vs $•High central and state levied taxes

translates into 60-70% higher ATF pricesin India over global average.

Source: FICCI PWC report- Indian Aviation

Source: ICRA Rating Feature- Indian AviationIndustr

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 10/12

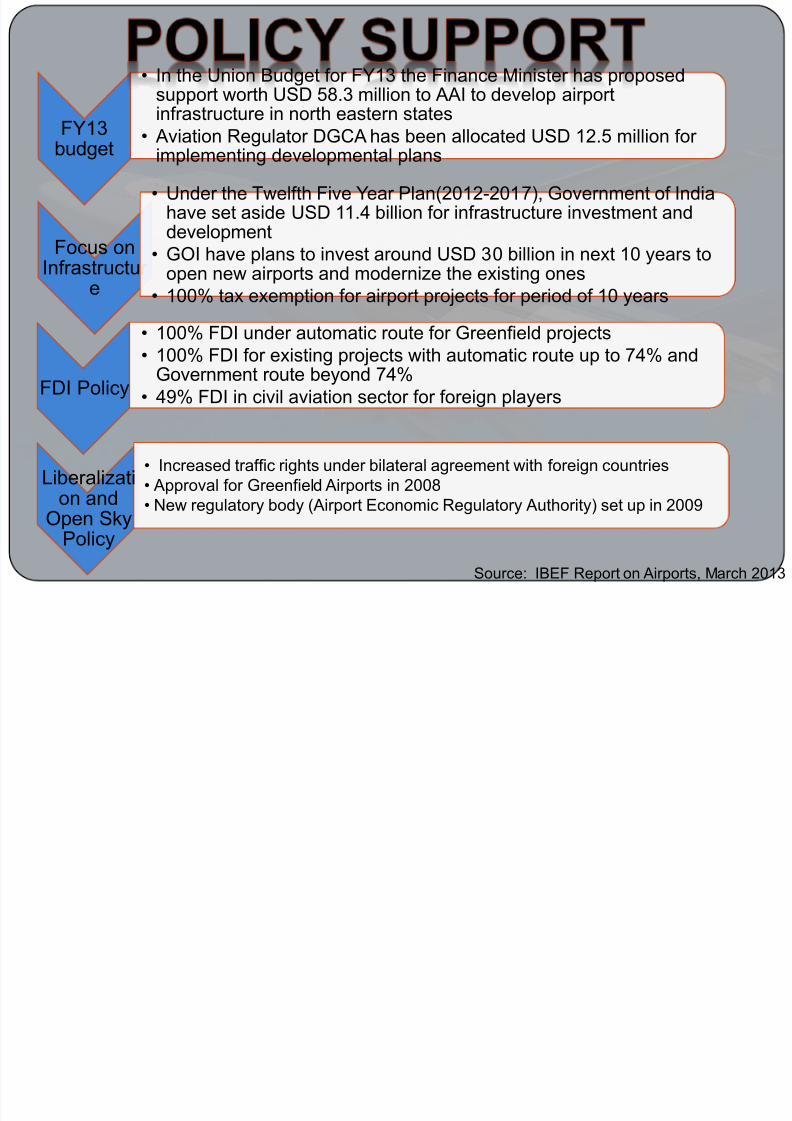

FY13budget

• In the Union Budget for FY13 the Finance Minister has proposedsupport worth USD 58.3 million to AAI to develop airportinfrastructure in north eastern states

• Aviation Regulator DGCA has been allocated USD 12.5 million for implementing developmental plans

Focus on

Infrastructur e

• Under the Twelfth Five Year Plan(2012-2017), Government of Indiahave set aside USD 11.4 billion for infrastructure investment anddevelopment

• GOI have plans to invest around USD 30 billion in next 10 years to

open new airports and modernize the existing ones• 100% tax exemption for airport projects for period of 10 years

FDI Policy

• 100% FDI under automatic route for Greenfield projects• 100% FDI for existing projects with automatic route up to 74% and

Government route beyond 74%• 49% FDI in civil aviation sector for foreign players

Liberalization and

Open SkyPolicy

• Increased traffic rights under bilateral agreement with foreign countries• Approval for Greenfield Airports in 2008• New regulatory body (Airport Economic Regulatory Authority) set up in 2009

Source: IBEF Report on Airports, March 2013

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 11/12

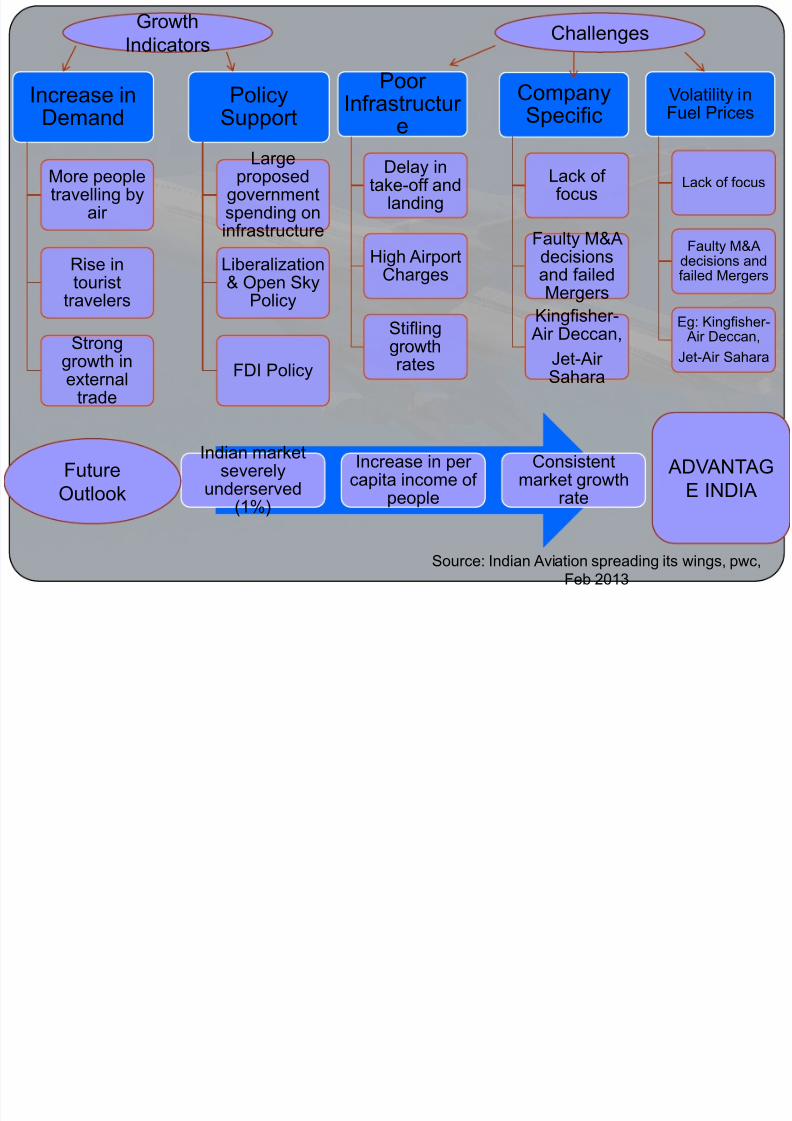

Increase inDemand

More peopletravelling by

air

Rise intourist

travelers

Stronggrowth inexternal

trade

PolicySupport

Largeproposed

governmentspending oninfrastructure

Liberalization& Open Sky

Policy

FDI Policy

GrowthIndicators

Poor Infrastructur

e

Delay intake-off and

landing

High Airport

Charges

Stiflinggrowthrates

CompanySpecific

Lack of focus

Faulty M&Adecisions

and failedMergers

Kingfisher- Air Deccan,

Jet-Air Sahara

Volatility inFuel Prices

Lack of focus

Faulty M&Adecisions and

failed Mergers

Eg: Kingfisher- Air Deccan,

Jet-Air Sahara

Challenges

Indian marketseverely

underserved(1%)

Increase in per capita income of

people

Consistentmarket growth

rate

FutureOutlook

ADVANTAGE INDIA

Source: Indian Aviation spreading its wings, pwc,Feb 2013

7/30/2019 Final Aviation Industry

http://slidepdf.com/reader/full/final-aviation-industry 12/12