Embed Size (px)

Citation preview

Helping Individuals Manage Risks

Robert J. ShillerStanley B. Resor Professor of Economics, Yale University

Professor of Finance, Yale UniversityChief Economist, MacroMarkets LLC

BEFI 2008, Coral Gables FLMarch 27, 2008

Some Risks that Matter toIndividuals

• Home Price Risk

• Personal Income Risks

• Longevity Risks

I. Home Price Risks

• History of development of real estatederivatives and price indices

• Obstacles to real estate derivatives

• Optimism for future

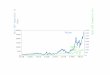

Real Home Prices, Building Costs,Population, Interest Rates

As of 2007-IV

0

50

100

150

200

1880 1900 1920 1940 1960 1980 2000 2020

Year

Ind

ex o

r In

tere

st R

ate

0

100

200

300

400

500

600

700

800

900

1000

Popula

tion i

n M

illi

ons

Home Prices

Building CostsPopulation

Interest Rates

US Real Price, Rent and Building CostsQuarterly 1987-I to 2007-II

0

20

40

60

80

100

120

140

160

180

1985 1990 1995 2000 2005 2010

Date

In

dex

19

87

-I=

10

0

Real Price

Real Rent

Real Building Costs

Comparing Real Home Prices inGreater London and Greater

Boston 1983-2007

0

50

100

150

200

250

300

350

400

1980 1985 1990 1995 2000 2005 2010

Date

Rea

l P

ric

e In

dex

Gr. Boston

Gr. London

Real Home Prices Netherlands,Norway, USA 1890 to 2004-5-7

0

50

100

150

200

250

300

350

1890 1910 1930 1950 1970 1990 2010

Year

Rea

l H

om

e P

ric

e I

nd

ex

, 1

89

0=

10

0

Netherlands

USA

Norway

S&P/Case-Shiller San Francisco Real TieredHome Price Indices through Dec 2007

0

50

100

150

200

250

300

350

1985 1990 1995 2000 2005 2010

Low

Middle

High

S&P/Case-Shiller Las Vegas Real TieredHome Price Indices through Dec 2007

0

50

100

150

200

250

300

350

1990 1995 2000 2005 2010

Low

Middle

High

S&P/Case-Shiller Chicago Real TieredHome Price Indices through Dec 2007

0

50

100

150

200

250

300

350

1990 1995 2000 2005 2010

Low

Middle

High

S&P/Case-Shiller MiamiReal Tiered Home Price Indices through Dec 2007

0

50

100

150

200

250

300

350

1985 1990 1995 2000 2005 2010

Low

Middle

High

Home Equity Insurance

• Risks to values of homes greater thanrisks by fire

• Oak Park Illinois, 1977• Chicago Home Equity Assurance Program

1988• Index-based insurance, Shiller and Weiss

1994• Yale-Syracuse-NRC program, 2002

London Futures and OptionsExchange 1991

• Property futures markets, both residentialand commercial

• Trading suspended within months

Goldman Sachs Covered Warrants

• Launched 2003 London Stock Exchange

Investment Property Databank(IPD)

• London, commercial property

• Global notional outstanding value ofproperty derivatives trades has reached£11.5 billion

HEDGESTREET MARKETS• Energy/Metals

Crude Oil, Natural Gas, Gold, SilverCurrenciesEUR/USD, GBP/USD, USD/YEN and more

• Economic Events/Interest RatesInitial Claims, Nonfarm Payrolls, Core CPI, Fed Fund Rate

• Housing PricesChicago, New York, San Francisco, and more

• Mergers and AcquisitionsNews Corp/Dow Jones, Microsoft/Yahoo!, NASDAQ/PHLX, andmore

• HurricanesNamed Atlantic Storms once they form

Cantor Index

• Cantor Index is a leading financial spread bettingcompany, established in 2000. Cantor Indexoffers spread bets on a wide range of marketsfrom shares and indices to bonds andcommodities.

• Affilicated with Cantor Fitzgerald

• "What price will the Average Greater LondonHouse price be as determined by the HalifaxQuarterly House Price Survey?

Spread Betting

• Let's say that we predict that there will be 3 goals in afootball match. You reckon that there will be more so youbet higher with a stake of £10 for every goal above 3.

• If there were 5 goals in the game, you would have won(5 - 3) x your stake = 2 x £10 = £20.

• If only 2 goals had been scored in the game, you wouldhave lost (3 - 2) x your stake = 1 x £10 = £10.

• A spread will always have a Buy price and a Sell price. Ifyou think that the outcome of the event will be higher (ormore) than the Buy price then you will Buy.If you think that the outcome of the event will be lower(or less) than the Sell price then you will Sell.

http://www.cantorspreadfair.co.uk/London Home Prices Dec 7, 2007

271268Dec-10

285277Dec-09

298296Dec-08

302.5299Sep-08

308307Jun-08

312.5311Mar-08

317316Dec-07

BuySell

Commission on Home Prices atSpreadfair

Charging: Commission on house prices ischarged differently to other Spreadfairmarkets. There will be an annualcommission charge on each market of 1unit per year, which will be deducted on aquarterly basis based on your averageopen position, whether long or short. Inaddition, commission of 3-5% of netwinnings on the market is applied at thetime of settlement, according to yourcommission rate.

Chicago Mercantile Exchange FuturesChicago Mercantile Exchange FuturesMarkets Launched May 2006Markets Launched May 2006

DMSP Satellite Composite ImageDMSP Satellite Composite Image

On May 22, 2006, The Chicago Mercantile Exchange launched the firstsuccessful futures and options market for home prices. The contractscurrently settle on 11 different S&P/Case-Shiller® Home Price Indices. Thecombined cumulative notional value traded in the CME housing products(both futures and options) in the first year exceeded $500mm, a period overwhich these products were limited to a maximum one-year term. OnSeptember 17, 2007, the CME began listing longer-dated contracts (up to 5years) to meet market demand for greater product utility.

“Financial Engineering comes toreal estate at last, and the housingmarket will never be the same.”

-Barron’s 5.15.06

CME Housing Futures and OptionsCME Housing Futures and Options

UPDATE THIS

Cumulative CME Housing Futures Notional Traded (Since Inception, May 2006)

$0

$50

$100

$150

$200

$250

$300

$350

5/2

2/2

006

6/0

1/2

006

6/1

2/2

006

6/2

1/2

006

6/3

0/2

006

7/1

2/2

006

7/2

1/2

006

8/0

1/2

006

8/1

0/2

006

8/2

1/2

006

8/3

0/2

006

9/1

1/2

006

9/2

0/2

006

9/2

9/2

006

10/1

0/2

006

10/1

9/2

006

10/3

0/2

006

11/0

8/2

006

11/1

7/2

006

11/2

9/2

006

12/0

8/2

006

12/1

9/2

006

12/2

9/2

006

1/1

1/2

007

1/2

3/2

007

2/0

1/2

007

2/1

2/2

007

2/2

2/2

007

3/0

5/2

007

3/1

4/2

007

3/2

3/2

007

4/0

3/2

007

4/1

3/2

007

4/2

4/2

007

5/0

3/2

007

5/1

4/2

007

5/2

3/2

007

6/0

4/2

007

6/1

3/2

007

6/2

2/2

007

7/0

3/2

007

7/1

3/2

007

$ in M

illio

ns

S&P/Case-ShillerS&P/Case-Shiller®® Home Price MacroShares Home Price MacroShares®®

Home Price FuturesHome Price FuturesPercent Discount of CME Housing Futures from S&P/Case-Shiller HPI Levels Percent Discount of CME Housing Futures from S&P/Case-Shiller HPI Levels –– as ofas of

January 3January 3rdrd, 2008., 2008.

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

Feb-08 May-08 Aug-08 Nov -08 Feb-09 May-09 Nov -09 May-10 Nov -10 Nov -11 Nov -12

CME Futures Contract Expiration

%

dis

co

unt

v.

S&

P/C

ase-S

hille

r H

om

e

Pri

ce

Index

Boston

Chicago

Denver

LV

LA

Miami

NY

SD

SF

Wash DC

Comp-10

Futures Price and Latest Home PriceFutures Price and Latest Home PriceIndexIndex

Daily, May 2006 Daily, May 2006 –– February 2008 February 2008S&P/Case-Shiller Composite- 10: Expected Change Within One Year, by Trading Day:

Through February 14, 2008

180

190

200

210

220

230

240

250

260

5/19/2006 8/1/2006 10/11/2006 12/21/2006 3/7/2007 5/17/07 7/30/07 10/09/2007 12/19/2007

*Data derived from the asking price of the long-dated CME futures contract and prevailing S&P/Case-Shiller Home Price Incex level on each trading day.

CME Composite-10 Futures

S&P/CSI Composite-10 Index

Problems Getting Market StartedOpen Interest May 2006 to Nov

2007

$0

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

5/22/2006

6/12/2006

6/30/2006

7/21/2006

8/10/2006

8/30/2006

9/20/2006

10/10/2006

10/30/2006

11/17/2006

12/08/2006

12/29/2006

1/23/2007

2/12/2007

3/05/2007

3/23/2007

4/13/2007

5/03/2007

5/23/2007

6/13/2007

7/03/2007

7/24/2007

8/13/2007

8/31/2007

9/21/2007

10/11/2007

10/31/2007

11/20/2007

Obstacles to Real Estate Markets

• Regret theory

• Lack of hedging demand (Sinai-Soulelis)

• Liquidity

Case-Shiller Homebuyers Survey2007

• If your property did not sell, presumably it mighthave if you had lowered the asking price more. Ifyou considered doing so but decided not to, canyou say why?

• 1. My house is worth more than people seem tobe willing to pay right now

• 2. I can't afford to sell at a lower price• 3. By holding out, I will be able to get more later• 4. I didn’t want to pay off my low rate mortgage• 1. 33% 2. 33% 3 11% 4. 0% 5. (other) 22%

II Personal Income Risk Markets

• Subprime crisis could have been avertedwith income-linked (and real estate pricelinked) mortgages

• Such retail products require the creation ofmarkets

Livelihood Insurance

• Replaces life insurance in dealing with largestrisks

• Livelihood insurance: long-term policies basedon occupational indexes

• Repeated measures occupational indexes:Robert Shiller and Ryan Schneider Rev. Incomeand Wealth 1998

• Powerful impact on conservatism in life’sdecisions, makes for more risk taking

Income-Linked Loans

• Milton Friedman, Capitalism and Freedom1962: individuals sell shares in their futureearnings, but feared “irrational publiccondemnation” and feared it would bedifficult to track people and enforcecontracts

• Changing times• Such loans should be based partly on

income indexes, to reduce moral hazard

Income-Linked Personal Loans

• Yale Tuition Postponement Option 1971-78

• Yale Law School Career OptionsAssistance Program 1988-today

• David Bowie bonds, David Pullman 1997

• Australian Higher Education ContributionScheme (HECS) is dominant form ofstudent loans in Australia today

Subprime Crisis Initiatives

• FHASecure

• Home Now Initiative

• Proposed changes in bankruptcy laws

• Project Lifeline– All of these are risk management of a sort

– None of these is modeled after market basedrisk management

The Need for Better PersonalIncome Indices

• Need repeated measure indices ofoccupational income

• Settling contracts based on nearest matchoccupational indices

• Futures and other markets for these

III. Longevity Risk

♣ Life annuities are an excellent old idea, rarely embracedby the public

♣ Wishful thinking bias, mental framing

♣ Public pension funds

♣ Private annuities

♣ Problem: annuity providers have to manage aggregatelongevity risk

U.S. Life Expectancy, 1900-2001U.S. Life Expectancy, 1900-2001

0

10

20

30

40

50

60

70

80

90

1880 1900 1920 1940 1960 1980 2000 2020

Ag

e

at

Death

Female

Male

Problems Inhibiting LongevityBonds

• EIB Bonds were nominal bonds, should bereal

• UK Issuers of life annuities were notseriously enough interested in this smallissue to take fast action

• Those who would take other side are noteasily found, need to look at prices in anestablished market

Efforts to Create Markets forLongevity Risk

♣ Swiss Re longevity bond, 2003♣ European Investment Bank-BNP Paribas

longevity bond 2004♣ Swiss Re, takes on £1.7 billion of longevity from

Friends Provident in UK♣ JP Morgan Launches International Longevity

and Mortality Index – LifeMetrics Index, March2007

♣Goldman Sachs Launches Tradeable Index forLongevity and Mortality Risks Dec. 2007

![The Final Blockchain PPT.pptx [Read-Only]...educational organization dedicated to the teaching and study of insurance and risk management. ... Case‐Shiller Home Price Index Effective](https://img.pdfslide.net/doc/110x75/5ea8e23c518c9a623952904c/the-final-blockchain-pptpptx-read-only-educational-organization-dedicated.jpg)