Embed Size (px)

Citation preview

Month &Year-EndProcessing

Slideshow 9

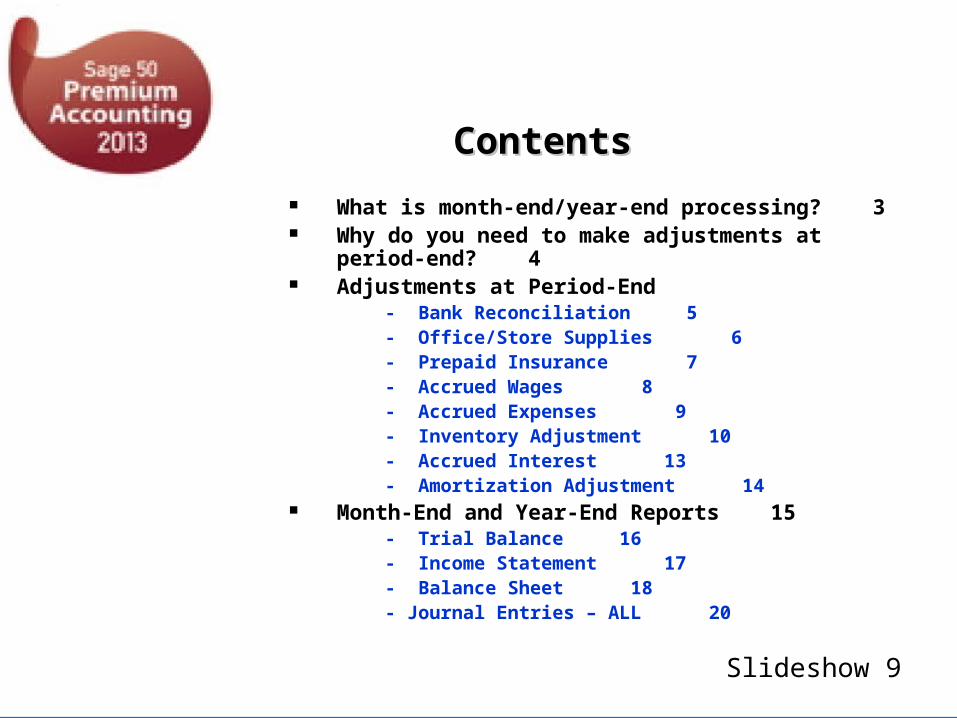

What is month-end/year-end processing? 3 Why do you need to make adjustments at period-end? 4 Adjustments at Period-End

- Bank Reconciliation 5- Office/Store Supplies 6- Prepaid Insurance 7- Accrued Wages 8- Accrued Expenses 9- Inventory Adjustment 10- Accrued Interest 13- Amortization Adjustment 14

Month-End and Year-End Reports 15- Trial Balance 16- Income Statement 17- Balance Sheet 18- Journal Entries – ALL 20

ContentsContents

Slideshow 9

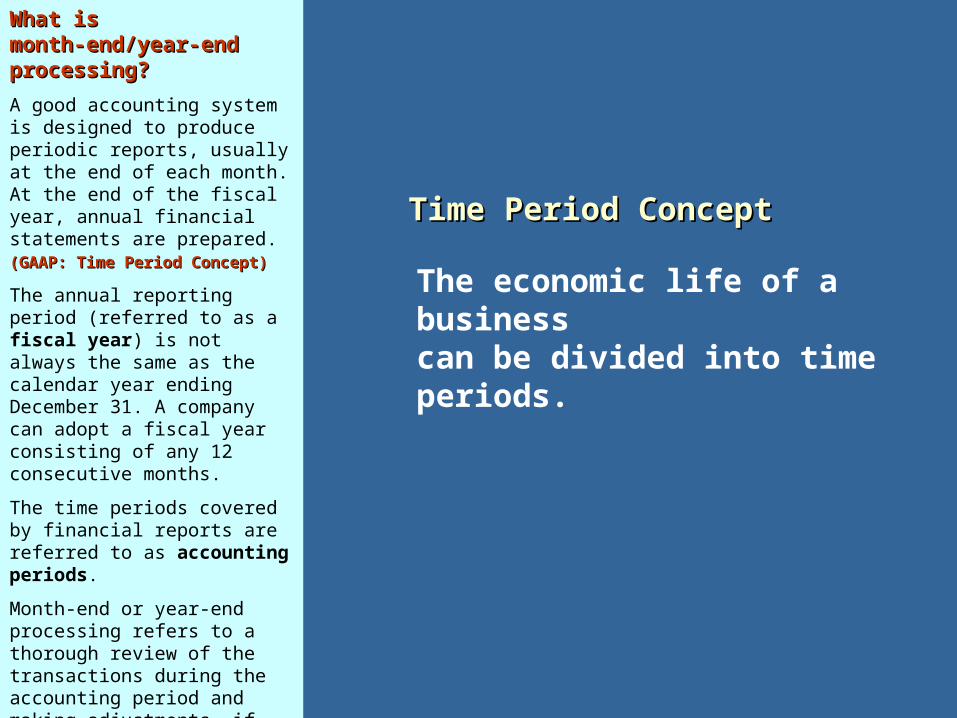

What is month-end/year-What is month-end/year-end processing?end processing?

A good accounting system is designed to produce periodic reports, usually at the end of each month. At the end of the fiscal year, annual financial statements are prepared. (GAAP: Time Period (GAAP: Time Period

Concept)Concept)

The annual reporting period (referred to as a fiscal year) is not always the same as the calendar year ending December 31. A company can adopt a fiscal year consisting of any 12 consecutive months.

The time periods covered by financial reports are referred to as accounting periods.

Month-end or year-end processing refers to a thorough review of the transactions during the accounting period and making adjustments, if necessary.

Click to continue.

The economic life of a businesscan be divided into time periods.

Time Period ConceptTime Period Concept

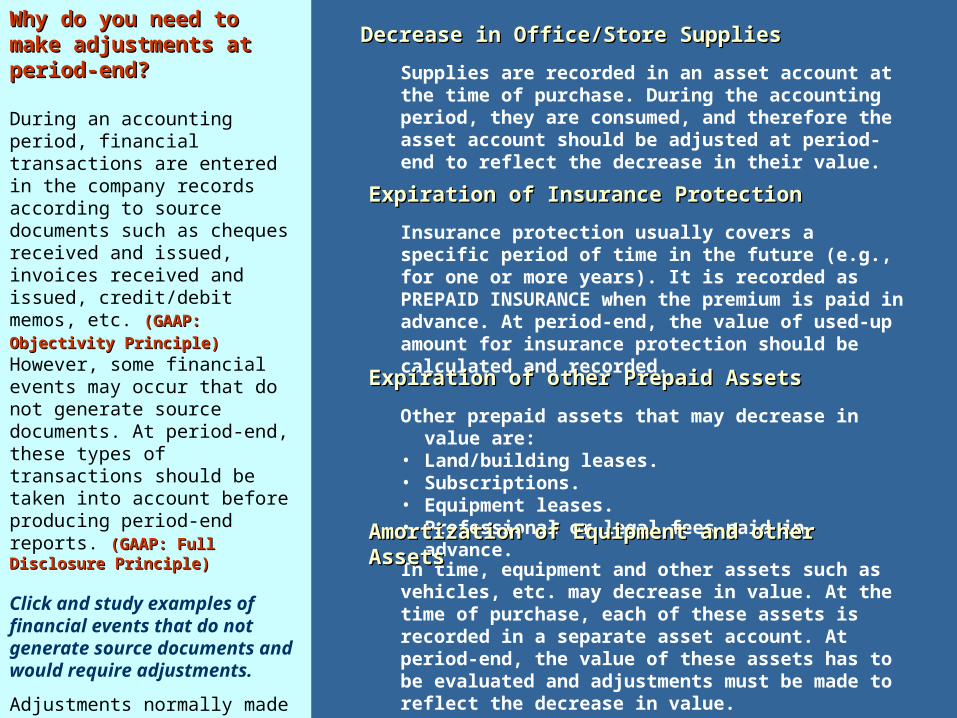

Why do you need to make Why do you need to make adjustments at period-end?adjustments at period-end?

During an accounting period, financial transactions are entered in the company records according to source documents such as cheques received and issued, invoices received and issued, credit/debit memos, etc. (GAAP: (GAAP:

Objectivity Principle)Objectivity Principle) However, some financial events may occur that do not generate source documents. At period-end, these types of transactions should be taken into account before producing period-end reports. (GAAP: Full Disclosure Principle)(GAAP: Full Disclosure Principle)

Click and study examples of financial events that do not generate source documents and would require adjustments.

Adjustments normally made during period-end are discussed in the slides that follow.

Click to continue.

Supplies are recorded in an asset account at the time of purchase. During the accounting period, they are consumed, and therefore the asset account should be adjusted at period-end to reflect the decrease in their value.

Decrease in Office/Store SuppliesDecrease in Office/Store Supplies

Insurance protection usually covers a specific period of time in the future (e.g., for one or more years). It is recorded as PREPAID INSURANCE when the premium is paid in advance. At period-end, the value of used-up amount for insurance protection should be calculated and recorded.

Expiration of Insurance ProtectionExpiration of Insurance Protection

Other prepaid assets that may decrease in value are:• Land/building leases.• Subscriptions.• Equipment leases.• Professional or legal fees paid in advance.

Expiration of other Prepaid AssetsExpiration of other Prepaid Assets

In time, equipment and other assets such as vehicles, etc. may decrease in value. At the time of purchase, each of these assets is recorded in a separate asset account. At period-end, the value of these assets has to be evaluated and adjustments must be made to reflect the decrease in value.

Amortization of Equipment and other Amortization of Equipment and other AssetsAssets

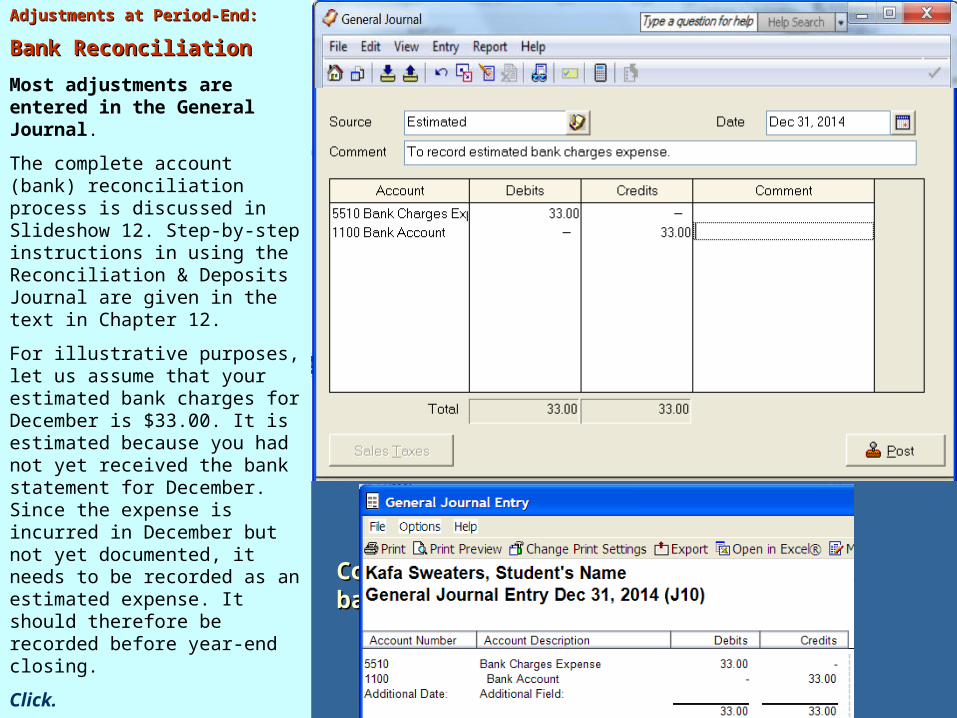

Adjustments at Period-End:Adjustments at Period-End:

Bank ReconciliationBank Reconciliation

Most adjustments are entered in the General Journal.

The complete account (bank) reconciliation process is discussed in Slideshow 12. Step-by-step instructions in using the Reconciliation & Deposits Journal are given in the text in Chapter 12.

For illustrative purposes, let us assume that your estimated bank charges for December is $33.00. It is estimated because you had not yet received the bank statement for December. Since the expense is incurred in December but not yet documented, it needs to be recorded as an estimated expense. It should therefore be recorded before year-end closing.

Click.

Study the appropriate General Journal entry to record the estimated bank charges expense.

Click to continue.

Company may need to make adjustments in the company records due to:• Bank charges/interest

charges

• Interest earned

• NSF cheques

• Company’s bookkeeping errors

Company may need to adjust the calculation of the cash balance on the bank statement to account for:

• Outstanding cheques

• Deposits in transit

• Bank errors

Company cash account = Adjusted bank Company cash account = Adjusted bank balancebalance

(Adjusted cash balance)(Adjusted cash balance)

Bank (Account) ReconciliationBank (Account) Reconciliation

Original Purchase Journal EntryOriginal Purchase Journal Entry

DR Prepaid Office Supplies 600.00

CR Accounts Payable 600.00

Month-End AdjustmentMonth-End Adjustment

DR Office Supplies Expense 285.00

CR Prepaid Office Supplies 285.00

Prepaid Office Supplies Office Supplies Expense

Dec 1 600.00 Dec 31 285.00 Dec 31 285.00

Balance 315.00

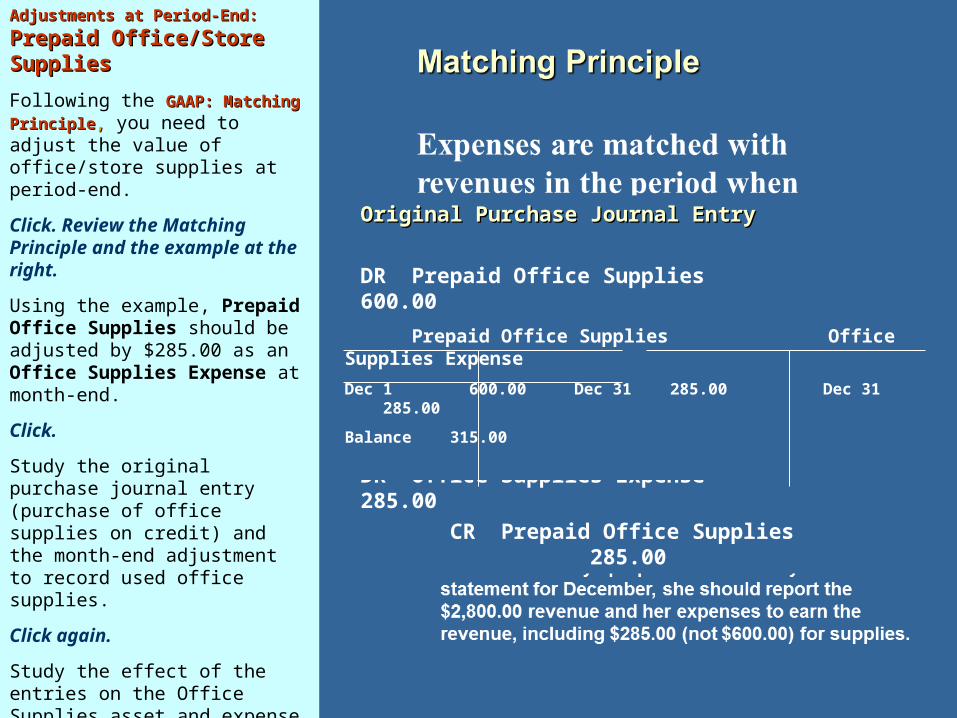

Adjustments at Period-End:Adjustments at Period-End:

Prepaid Office/Store Prepaid Office/Store SuppliesSupplies

Following the GAAP: Matching GAAP: Matching PrinciplePrinciple,, you need to adjust the value of office/store supplies at period-end.

Click. Review the Matching Principle and the example at the right.

Using the example, Prepaid Office Supplies should be adjusted by $285.00 as an Office Supplies Expense at month-end.

Click.

Study the original purchase journal entry (purchase of office supplies on credit) and the month-end adjustment to record used office supplies.

Click again.

Study the effect of the entries on the Office Supplies asset and expense accounts at period-end.

Click to continue.

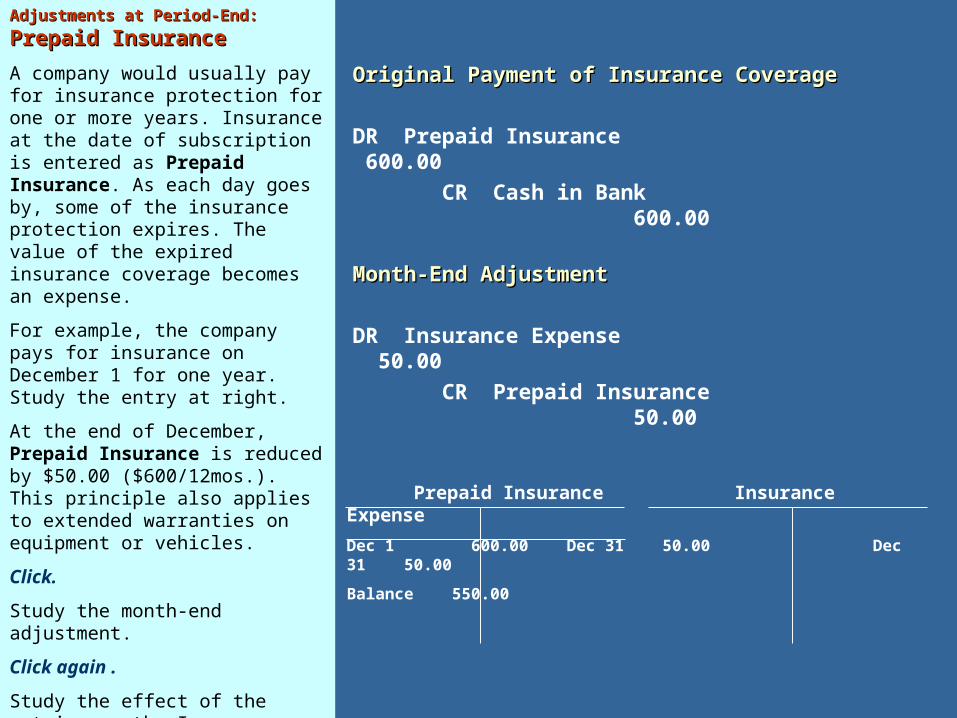

Adjustments at Period-End:Adjustments at Period-End:

Prepaid InsurancePrepaid Insurance

A company would usually pay for insurance protection for one or more years. Insurance at the date of subscription is entered as Prepaid Insurance. As each day goes by, some of the insurance protection expires. The value of the expired insurance coverage becomes an expense.

For example, the company pays for insurance on December 1 for one year. Study the entry at right.

At the end of December, Prepaid Insurance is reduced by $50.00 ($600/12mos.). This principle also applies to extended warranties on equipment or vehicles.

Click.

Study the month-end adjustment.

Click again .

Study the effect of the entries on the Insurance asset and expense accounts.

Click to continue.

Original Payment of Insurance CoverageOriginal Payment of Insurance Coverage

DR Prepaid Insurance 600.00

CR Cash in Bank 600.00

Month-End AdjustmentMonth-End Adjustment

DR Insurance Expense 50.00

CR Prepaid Insurance 50.00

Prepaid Insurance Insurance Expense

Dec 1 600.00 Dec 31 50.00 Dec 31 50.00

Balance 550.00

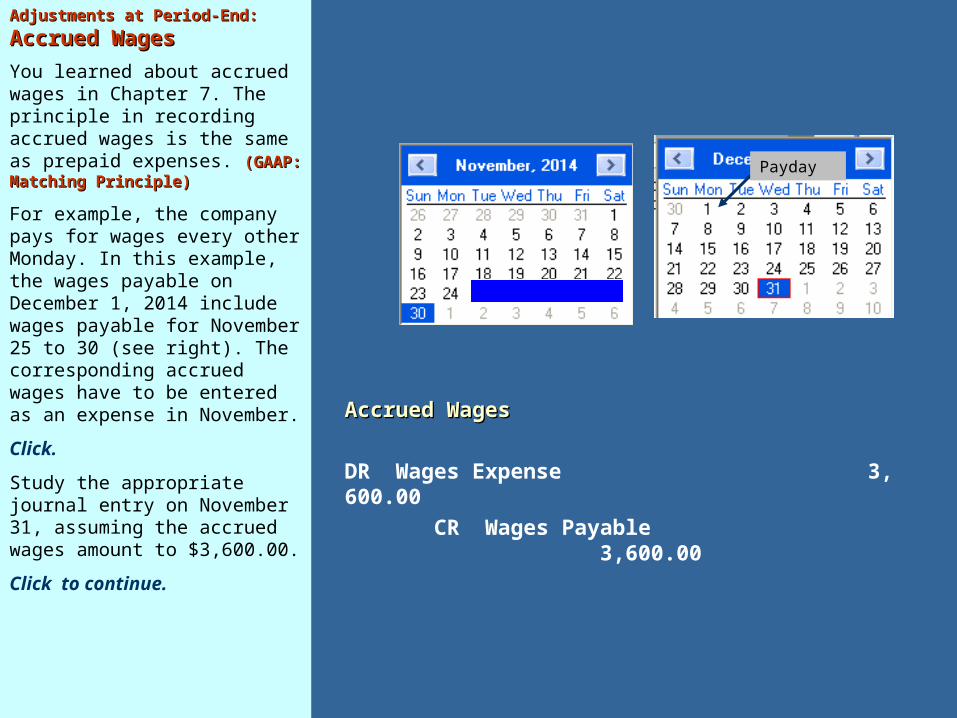

Adjustments at Period-End:Adjustments at Period-End:

Accrued WagesAccrued Wages

You learned about accrued wages in Chapter 7. The principle in recording accrued wages is the same as prepaid expenses. (GAAP: Matching Principle)(GAAP: Matching Principle)

For example, the company pays for wages every other Monday. In this example, the wages payable on December 1, 2014 include wages payable for November 25 to 30 (see right). The corresponding accrued wages have to be entered as an expense in November.

Click.

Study the appropriate journal entry on November 31, assuming the accrued wages amount to $3,600.00.

Click to continue.

Accrued WagesAccrued Wages

DR Wages Expense 3, 600.00

CR Wages Payable 3,600.00

PaydayPayday

Adjustments at Period-End:Adjustments at Period-End:

Accrued ExpensesAccrued Expenses

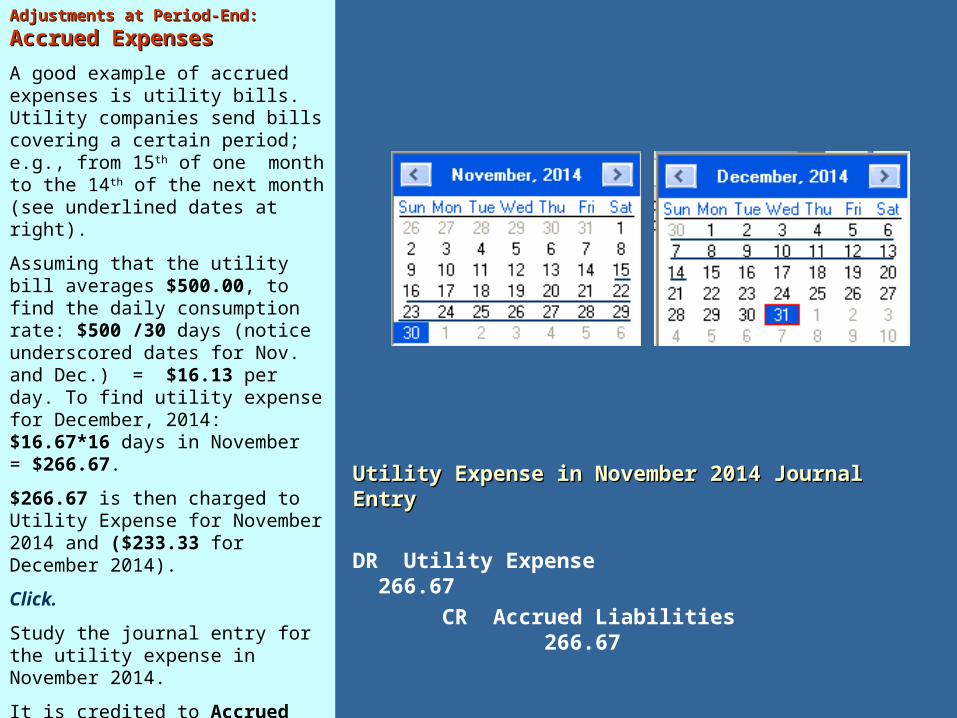

A good example of accrued expenses is utility bills. Utility companies send bills covering a certain period; e.g., from 15th of one month to the 14th of the next month (see underlined dates at right).

Assuming that the utility bill averages $500.00, to find the daily consumption rate: $500 /30 days (notice underscored dates for Nov. and Dec.) = $16.13 per day. To find utility expense for December, 2014: $16.67*16 days in November = $266.67.

$266.67 is then charged to Utility Expense for November 2014 and ($233.33 for December 2014).

Click.

Study the journal entry for the utility expense in November 2014.

It is credited to Accrued Liabilities because the expense is a payable amount at this time. Accrued Liabilities will be explained further in the next slideshow.

Click to continue.

Utility Expense in November 2014 Journal Utility Expense in November 2014 Journal EntryEntry

DR Utility Expense 266.67

CR Accrued Liabilities 266.67

Adjustments at Period-End:Adjustments at Period-End:

Periodic InventoryPeriodic Inventory

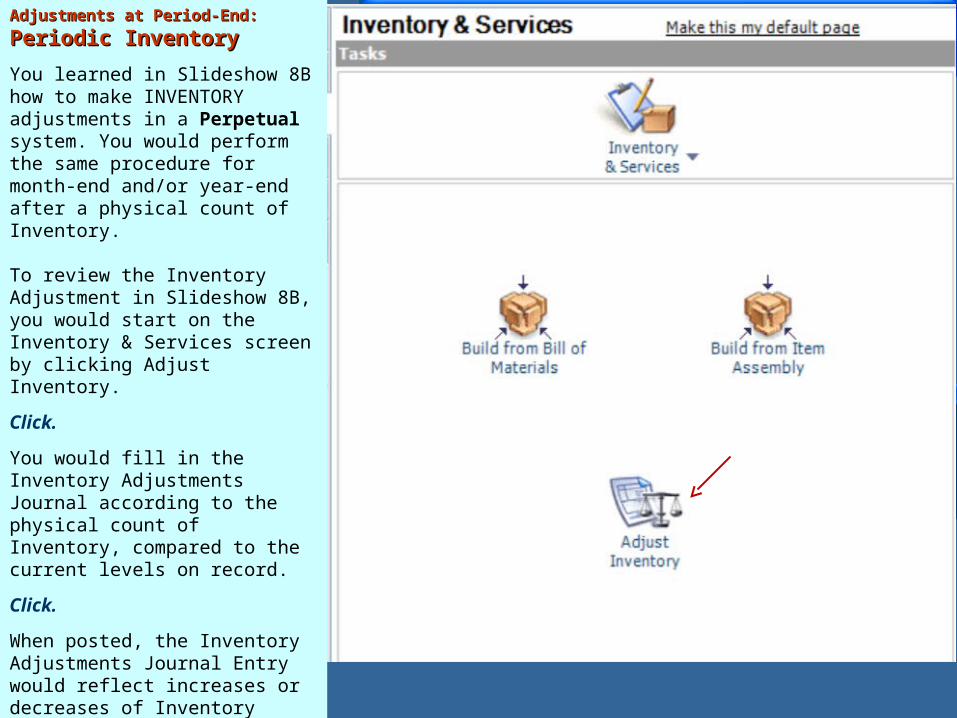

You learned in Slideshow 8B how to make INVENTORY adjustments in a Perpetual system. You would perform the same procedure for month-end and/or year-end after a physical count of Inventory.

To review the Inventory Adjustment in Slideshow 8B, you would start on the Inventory & Services screen by clicking Adjust Inventory.

Click.

You would fill in the Inventory Adjustments Journal according to the physical count of Inventory, compared to the current levels on record.

Click.

When posted, the Inventory Adjustments Journal Entry would reflect increases or decreases of Inventory according to the Inventory Adjustments Journal.

Click to continue.

Adjustments at Period-End:Adjustments at Period-End:

Accrued InterestAccrued Interest

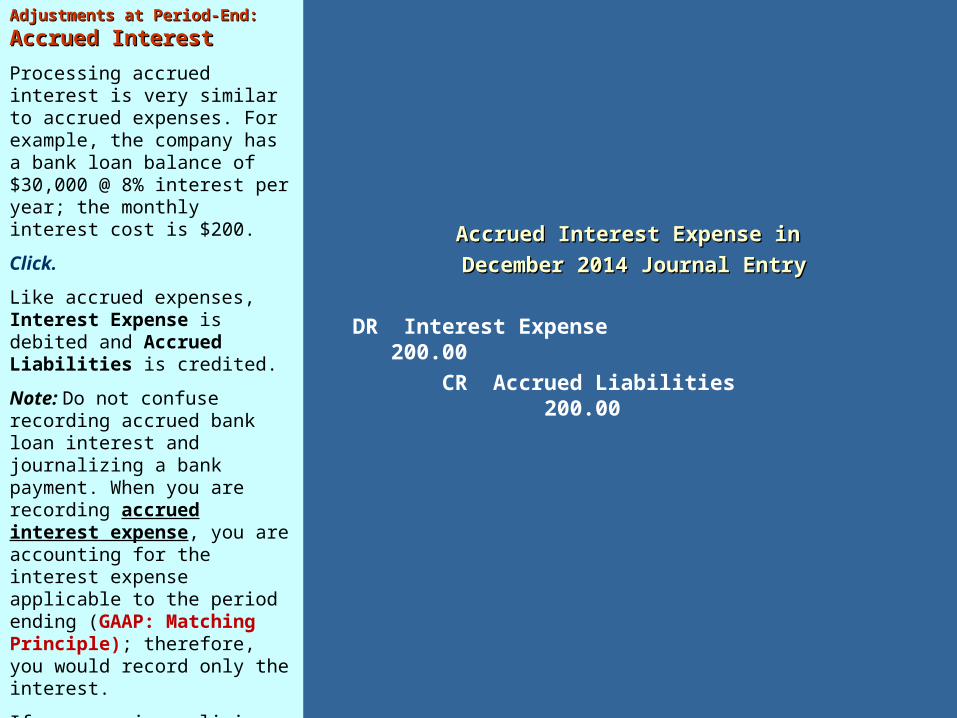

Processing accrued interest is very similar to accrued expenses. For example, the company has a bank loan balance of $30,000 @ 8% interest per year; the monthly interest cost is $200.

Click.

Like accrued expenses, Interest Expense is debited and Accrued Liabilities is credited.

Note: Do not confuse recording accrued bank loan interest and journalizing a bank payment. When you are recording accrued interest expense, you are accounting for the interest expense applicable to the period ending (GAAP: Matching Principle); therefore, you would record only the interest.

If you are journalizing a loan payment with interest, you need to record both the principal amount of loan paid off and the interest applicable.

Click to continue.

Accrued Interest Expense in Accrued Interest Expense in

December 2014 Journal EntryDecember 2014 Journal Entry

DR Interest Expense 200.00

CR Accrued Liabilities 200.00

Adjustments at Period-End:Adjustments at Period-End:

DepreciationDepreciation

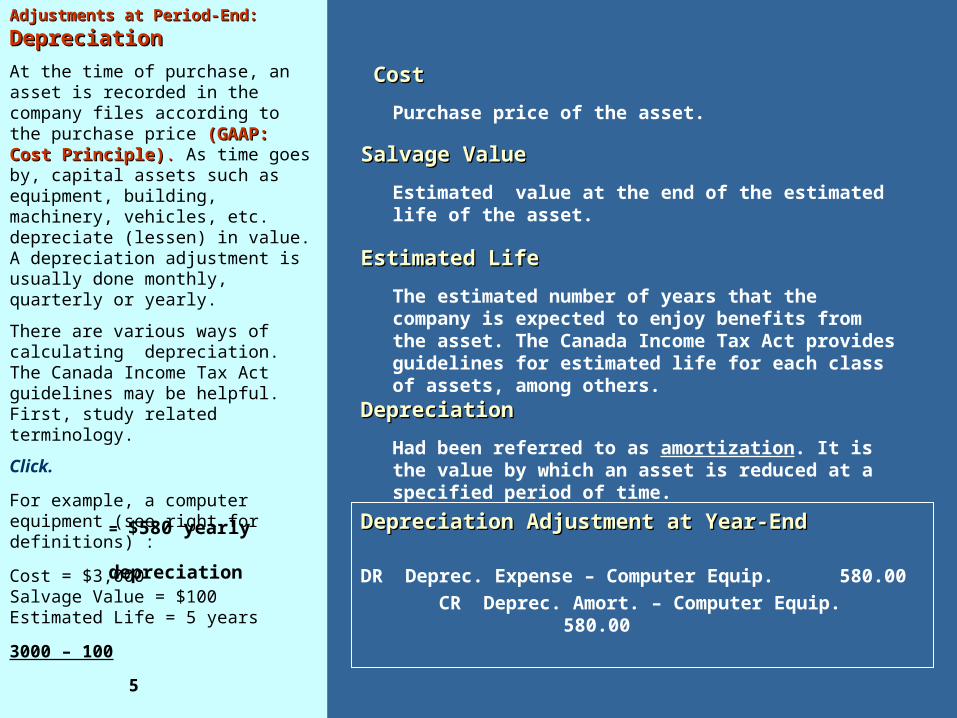

At the time of purchase, an asset is recorded in the company files according to the purchase price (GAAP: Cost (GAAP: Cost Principle)Principle).. As time goes by, capital assets such as equipment, building, machinery, vehicles, etc. depreciate (lessen) in value. A depreciation adjustment is usually done monthly, quarterly or yearly.

There are various ways of calculating depreciation. The Canada Income Tax Act guidelines may be helpful. First, study related terminology.

Click.

For example, a computer equipment (see right for definitions) :

Cost = $3,000Salvage Value = $100Estimated Life = 5 years

3000 – 100

5

Click.

Study the journal entry for the depreciation adjustment.

Click to continue.

Purchase price of the asset.

CostCost

Estimated value at the end of the estimated life of the asset.

Salvage ValueSalvage Value

The estimated number of years that the company is expected to enjoy benefits from the asset. The Canada Income Tax Act provides guidelines for estimated life for each class of assets, among others.

Estimated LifeEstimated Life

Had been referred to as amortization. It is the value by which an asset is reduced at a specified period of time.

DepreciationDepreciation

Depreciation Adjustment at Year-EndDepreciation Adjustment at Year-End

DR Deprec. Expense – Computer Equip. 580.00

CR Deprec. Amort. – Computer Equip. 580.00

= $580 yearly depreciation

Month-End ReportsMonth-End Reports

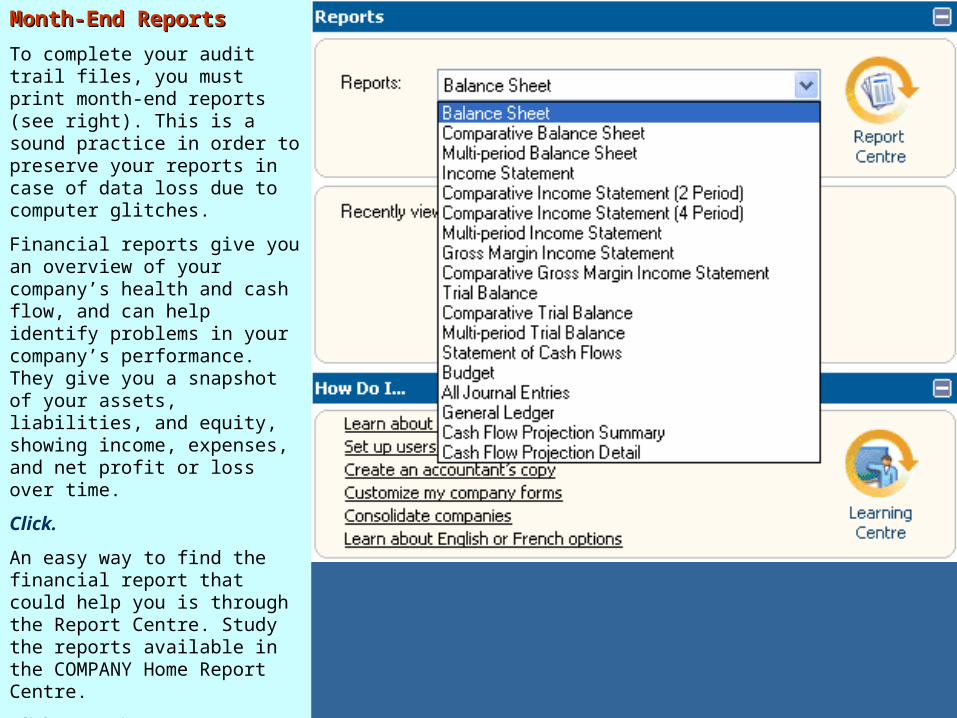

To complete your audit trail files, you must print month-end reports (see right). This is a sound practice in order to preserve your reports in case of data loss due to computer glitches.

Financial reports give you an overview of your company’s health and cash flow, and can help identify problems in your company’s performance. They give you a snapshot of your assets, liabilities, and equity, showing income, expenses, and net profit or loss over time.

Click.

An easy way to find the financial report that could help you is through the Report Centre. Study the reports available in the COMPANY Home Report Centre.

Click to continue.

Month-End ReportsMonth-End Reports

1.1. Trial BalanceTrial Balance

2.2. Balance SheetBalance Sheet

3.3. Income StatementIncome Statement

4.4. Journal Entries – ALLJournal Entries – ALL

5.5. General Ledger Listing - DetailGeneral Ledger Listing - Detail

Month-End Month-End ReportsReports:: Trial Balance Trial Balance

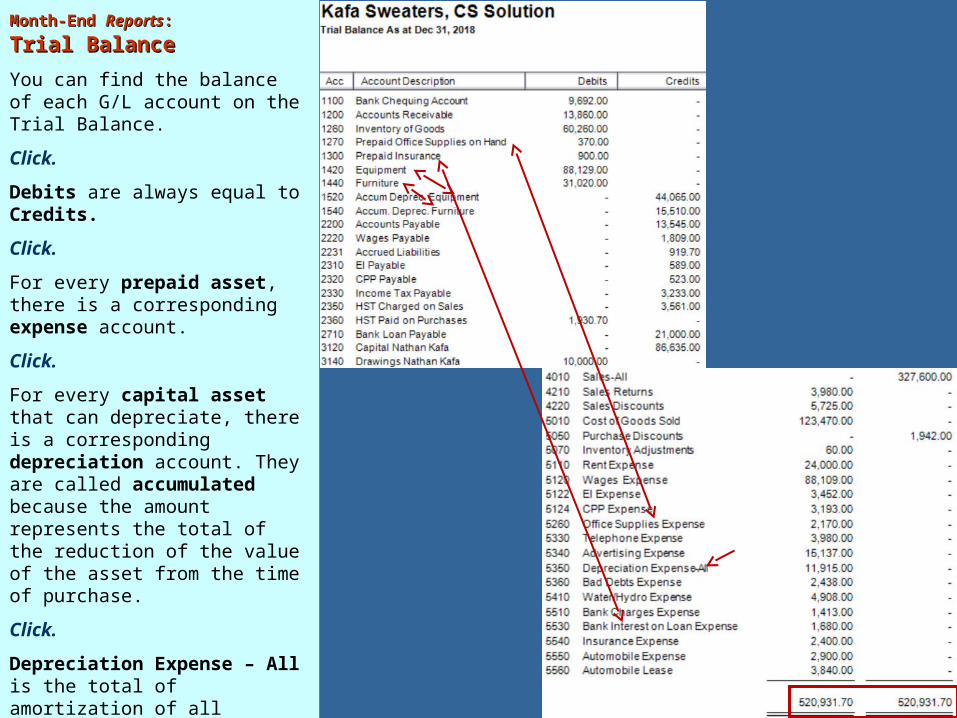

You can find the balance of each G/L account on the Trial Balance.

Click.

Debits are always equal to Credits.

Click.

For every prepaid asset, there is a corresponding expense account.

Click.

For every capital asset that can depreciate, there is a corresponding depreciation account. They are called accumulated because the amount represents the total of the reduction of the value of the asset from the time of purchase.

Click.

Depreciation Expense – All is the total of amortization of all capital assets during the current accounting period.

Click to continue.

Month-End Reports:Month-End Reports: Income StatementIncome Statement

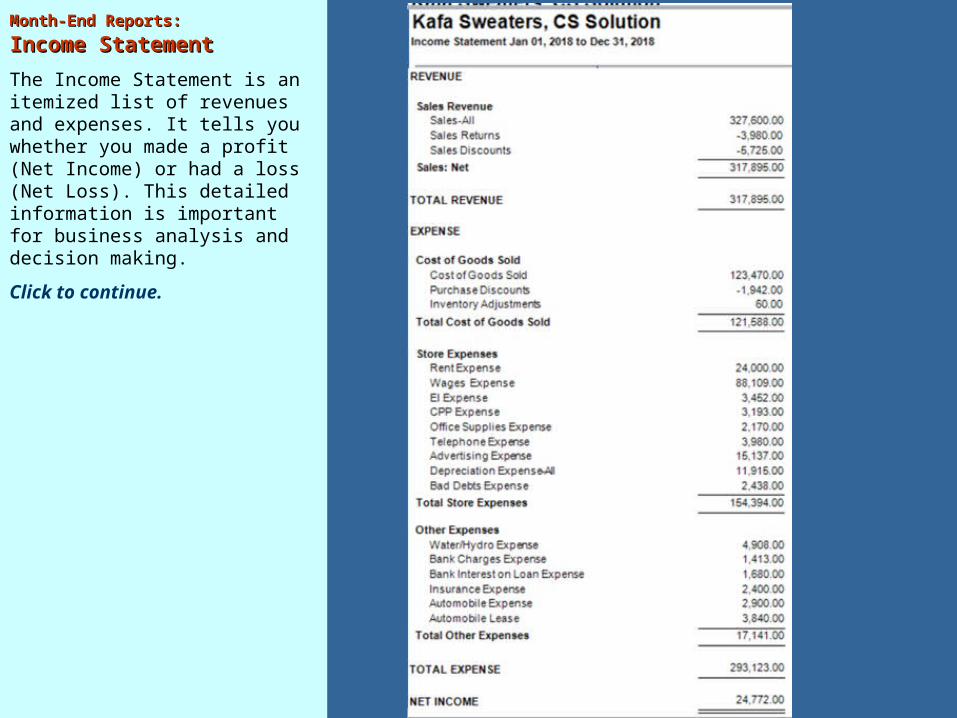

The Income Statement is an itemized list of revenues and expenses. It tells you whether you made a profit (Net Income) or had a loss (Net Loss). This detailed information is important for business analysis and decision making.

Click to continue.

Month-End Reports:Month-End Reports: Balance SheetBalance Sheet

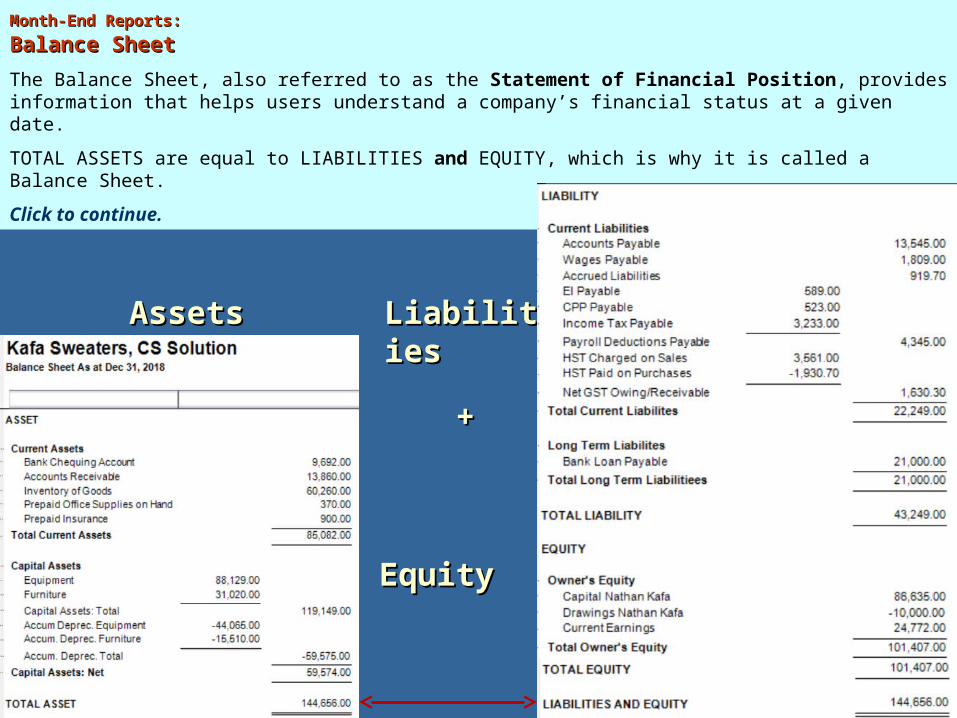

The Balance Sheet, also referred to as the Statement of Financial Position, provides information that helps users understand a company’s financial status at a given date.

TOTAL ASSETS are equal to LIABILITIES and EQUITY, which is why it is called a Balance Sheet.

Click to continue.

Assets = Assets = Liabilities Liabilities

EquityEquity

+ +

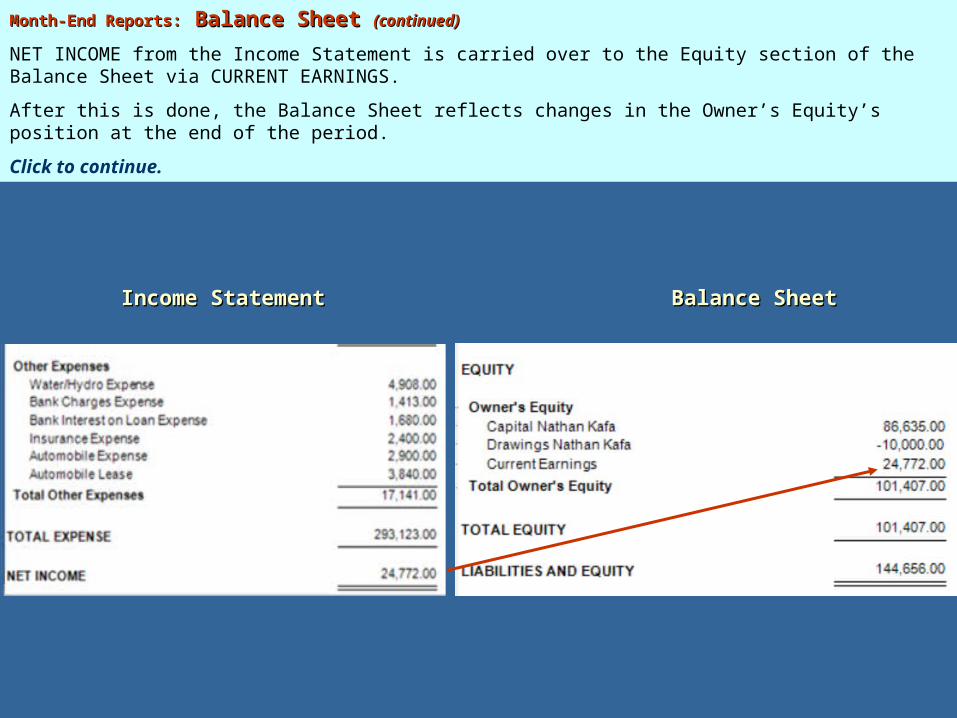

Month-End Reports:Month-End Reports: Balance Sheet Balance Sheet (continued)(continued)

NET INCOME from the Income Statement is carried over to the Equity section of the Balance Sheet via CURRENT EARNINGS.

After this is done, the Balance Sheet reflects changes in the Owner’s Equity’s position at the end of the period.

Click to continue.

Income StatementIncome Statement Balance SheetBalance Sheet

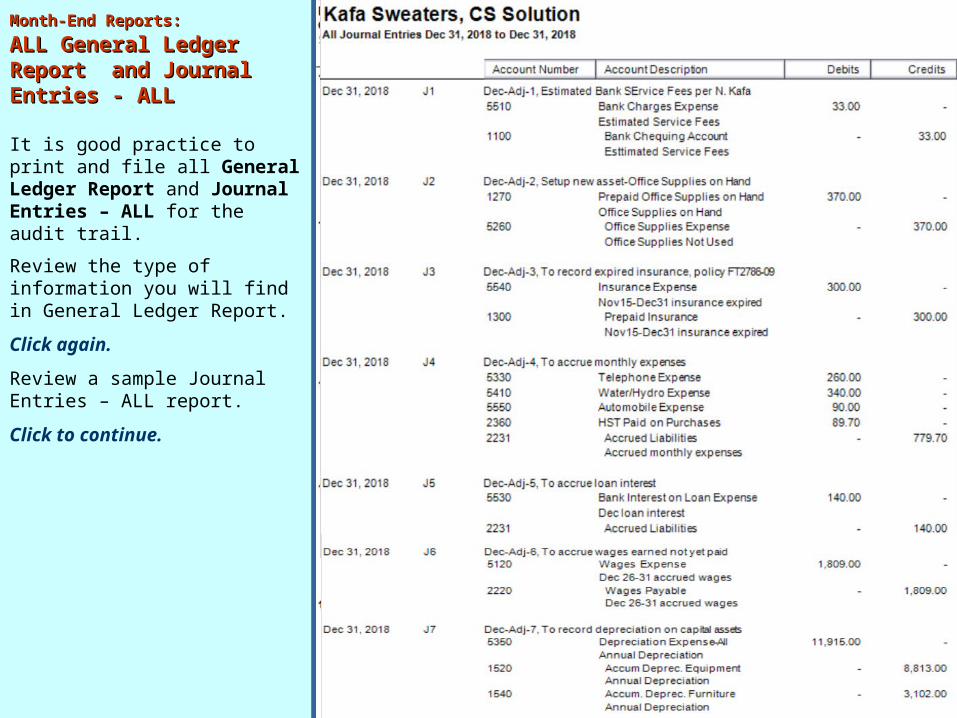

Month-End Reports:Month-End Reports: ALL General Ledger ALL General Ledger Report and Journal Report and Journal Entries - ALLEntries - ALL

It is good practice to print and file all General Ledger Report and Journal Entries – ALL for the audit trail.

Review the type of information you will find in General Ledger Report.

Click again.

Review a sample Journal Entries – ALL report.

Click to continue.

EXIT

More…More…

Go back to your text and proceed from where you have left off.

Review this slideshow when you finish the chapter to better prepare yourself for the next chapter.

Press ESC now, then click the EXIT button.