Embed Size (px)

Citation preview

MOODYS.COM

12 DECEMBER 2016

NEWS & ANALYSIS Corporates 2 » Go Daddy's Planned Acquisition of Host Europe Group Is

Credit Negative » Roper Technologies' Planned Acquisition of Deltek Is

Credit Negative » JBS' IPO of Its Subsidiary Will Reduce Its Leverage » Localiza's Acquisition of Hertz Brazil Boosts Brand Name

without Weakening Credit Quality » Solvay's Sale of Its Acetow Unit Supports Deleveraging, a

Credit Positive » Ahold Delhaize's 2017 Share Buyback Program Is

Credit Negative » Mauser Subsidiary's Acquisitions of Total Container and

Advantage IBC Are Credit Positive » Guangzhou R&F's Korean Ventures Are Credit Negative

Infrastructure 10 » Consumers Energy and Entergy Benefit from Early Closure of

Nuclear Plant in Michigan » ViaLagos Extends Toll Road Concession Contract, a

Credit Positive » National Grid's Gas Networks Sale Lowers Dividend Cost and

Raises Retained Cash » Origin's Proposed Divestment of Conventional Oil and Gas

Assets Is Credit Positive

Insurers 15 » Liberty Mutual's Acquisition of Ironshore Is Credit Negative for

It, Positive for Ironshore

Security Firms 17 » UK's Proposed Contracts-for-Difference Trading Rules Are

Credit Negative for Spread-Betting Firms

Sub-sovereigns 19 » Brazilian States Will Benefit from BRL5 Billion Federal

Revenue Transfer

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Thursday’s Credit Outlook 21 » Go to Last Thursday’s Credit Outlook

Click here for Weekly Market Outlook, our sister publication containing Moody’s Analytics’ review of market activity, financial predictions, and the dates of upcoming economic releases.

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Corporates

Go Daddy’s Planned Acquisition of Host Europe Group Is Credit Negative Last Tuesday, Go Daddy Operating Company LLC (Ba3 stable) said that it had agreed to acquire Host Europe Group (HEG, unrated) for about $1.79 billion, including the assumption of HEG’s net debt. The planned transaction, which Go Daddy expects to close in the second quarter of 2017, is credit negative because it will be funded entirely with debt. Following the announcement of the deal, we affirmed Go Daddy’s Ba3 corporate family rating and changed the outlook to stable from positive.

Go Daddy plans to fund the acquisition with about $1.4 billion of incremental term loans and a $530 million bridge loan. We estimate that Go Daddy’s leverage (total debt to cash flow from interest plus interest expense, including our adjustments for stock-based compensation and capitalized operating leases) will increase by about 2x to 5.1x. We expect leverage to decline to the low 4x range by the end of 2017.

The planned acquisition will significantly enhance Go Daddy’s operating scale in Europe and provide opportunities to accelerate revenue growth on the continent from cross-selling products and leveraging Go Daddy’s technology platform and customer care services. Go Daddy will retain HEG’s mass-market Web services business, which focuses on small and midsize enterprises, and over the next year plans to divest HEG’s PlusServer managed hosting services business, which focuses on large enterprises.

The acquisition marks a shift in Go Daddy’s growth strategy, which had relied on the organic acquisition of customers and acquisitions of smaller products and technology assets to enhance product capabilities. The proposed acquisition will be Go Daddy’s largest to date and the risk of integrating a large customer base and operations will be high over the next 12-18 months.

Go Daddy operates in the highly competitive markets of domain name registration, web hosting and other online services. But both Go Daddy and HEG have high customer retention rates (about 85% for Go Daddy and around 88% for HEG). We expect Go Daddy’s unlevered cash flow (as reported by the company) to grow by about 20% in 2017 on an organic basis and estimate that its free cash flow will be in the mid-teen percentages of total debt in 2017, pro forma for the acquisition of HEG’s Web services business.

Raj Joshi Vice President - Senior Analyst +1.212.553.2883 [email protected]

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Roper Technologies’ Planned Acquisition of Deltek Is Credit Negative Last Tuesday, Roper Technologies Inc. (Baa3 stable) said it had agreed to acquire Deltek Inc. (B2 stable), a provider of project-focused enterprise software, for about $2.8 billion. The planned acquisition, which Roper expects to close by the end of the year, is credit negative because it will be financed almost entirely with debt. Following the announcement of the deal, we downgraded Roper’s senior unsecured rating to Baa3 with a stable outlook, from Baa2.

The acquisition will double Roper’s reported debt to $6.1 billion from $3.1 billion as of year-end 2016. Pro forma for the acquisition, we expect the company’s Moody’s-adjusted debt/EBITDA to increase to nearly 4x, from 2.46x as of 30 September. The Deltek transaction caps a two-year period during which Roper made multiple acquisitions well beyond the bounds of its internally generated cash flow. This meaningfully weakened the company's balance sheet and indicates a higher tolerance for financial risk better reflected at the Baa3 rating level.

Roper has a strong competitive position across a diverse range of products, services and end-markets with an increasing focus on the medical and radio frequency identification (RFID) sectors. The company’s profitability metrics are robust, with operating margins likely to remain in the high-20% range. Roper generates about half of its revenue from subscription-based services and recurring consumables, such as certain industrial and energy products, which support relatively stable earnings. This helps mitigate cyclicality in some of the company's industrial end-markets such as oil and gas (9% of sales), which will remain under pressure over the coming quarters.

Cash flow generation remains strong, underpinned by high margins and modest capital expenditures. We expect free cash flow (after dividends) of around $900 million in 2017, compared to about $800 million expected in 2016. Over the next 12-18 months, we expect the company to use most of its free cash flow to pay down debt and reduce leverage to more sustainable levels. While we anticipate only light acquisition activity during this period, M&A will remain central to Roper’s operating strategy, with the company likely to pursue opportunistic acquisitions in 2018 and beyond, albeit at a level that maintains leverage in the 3x range.

Eoin Roche Vice President - Senior Analyst +1.212.553.2868 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

JBS’ IPO of Its Subsidiary Will Reduce Its Leverage On Tuesday, Brazil-based JBS S.A. (Ba2 stable) announced an initial public offering of shares in its Dutch subsidiary JBS Foods International N.V. (JBSFI, unrated). The move is credit positive for JBS, which will use proceeds from the IPO to reduce debt, diminishing its leverage in 2017.

JBS, the world’s largest protein producer by revenue, has not disclosed information on the possible size of the IPO. We estimate that a flotation of 15% of JBSFI’s equity on the New York Stock Exchange could raise around $1.4 billion, based on a 7.0x enterprise value/EBITDA multiple for JBSFI, compared to a 5.5x enterprise value/EBITDA multiple for JBS. If the IPO draws about $1.4 billion, JBS can reduce its gross leverage to a debt/EBITDA ratio as low as 3.5x, which is better than our earlier projection of 3.8x for 2017, and well below its 4.8x ratio for the 12 months through September 2016.

Under the terms of the IPO, JBSFI will hold all of JBS’ assets except for the Brazilian beef operations that make up about 19% of EBITDA. The assets going to JBSFI include Seara, JBS USA, Pilgrim’s Pride Corporation, USA Pork, Moy Park, and the South American beef operations excluding Brazil. JBS reported net revenues of BRL175.9 billion ($49.7 billion) with an adjusted EBITDA margin of 6.9% for the 12 months through September 2016.

Before the IPO, JBS plans to reallocate debt among the companies in order to rebalance leverage within the different structures. JBSFI will no longer have direct access to cash flows from JBS’ Brazilian beef assets for servicing debt, but it will also carry only part of the debt now held at JBS. JBSFI will also assume the bonds issued by JBS Investments GmbH, and guarantee the bonds issued by JBS USA Lux S.A./JBS USA Finance Inc, if bondholders consent to the shift.

In a shift from the initial restructuring proposal, JBSFI will be a subsidiary controlled by JBS S.A. via a dual class structure and listed on the New York Stock Exchange after a primary IPO to float its shares. BNDES Participações S.A. (Ba2 negative), a JBS shareholder with 21.4% stake, had vetoed the original proposal, which would have made JBSFI the parent company of the whole group, and scotched a primary IPO.

Erick Rodrigues Vice President - Senior Analyst +55.11.3043.7345 [email protected]

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Localiza’s Acquisition of Hertz Brazil Boosts Brand Name without Weakening Credit Quality Localiza Rent a Car S.A. (Ba2 negative) on Tuesday said that it had planned to buy the Brazilian operations of The Hertz Corporation (B1 negative) for an estimated BRL337 million ($100 million) in cash. The acquisition is credit positive for Localiza because it will increase its scale in its highly fragmented home market and boost its international brand exposure without weakening its credit metrics. A November debt issuance increased Localiza’s cash balance to a level far above the purchase price.

Under the terms of the deal, Localiza’s subsidiary Localiza Fleet S.A. (unrated) will acquire a 99.99% stake of Hertz Brazil’s Car Rental Systems do Brasil Locação de Veículos Ltda. (unrated) in equity and debt. As part of the transaction, the two operations will combine their Brazilian brand name as Localiza Hertz, and Hertz will display the Localiza brand name in select US and European airports with high numbers of Brazilian customers. The deal also includes a 20-year agreement to exchange inbound and outbound reservations between Localiza and Hertz.

Some consolidation in this extremely fragmented industry in Brazil will also benefit Localiza, the market leader in its home country, and will help improve fortunes for the sector generally. Localiza Fleet will acquire Hertz Brazil’s 42 locations, with about 3,700 cars in Hertz Brazil’s fleet-rental division and about 5,500 cars in the car-rental division. The acquisitions equal roughly a 7.5% increase in Localiza’s 122,000-vehicle fleet as of September 2016.

The newly acquired vehicles should generate the same 7.5% boost for Localiza’s consolidated net revenues, which were about BRL4.1 billion for the 12 months through September 2016, and its EBITDA of about BRL1.3 billion for that period, including our adjustments.

The cash transaction will not affect Localiza’s liquidity significantly. Localiza’s cash balance will reach about BRL1.9 billion at the end of December 2016, pro forma for the issuance of BRL750 million in debentures announced in November. That issuance would be more than enough to cover the BRL337 million acquisition price for Hertz Brazil, and BRL922 million in debt that matures by the end of 2018. Localiza will repay all of Hertz Brazil’s debt once the transaction is completed, so the deal will not worsen its leverage.

Marcos Schmidt Vice President - Senior Analyst +55.11.3043.7310 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Solvay’s Sale of Its Acetow Unit Supports Deleveraging, a Credit Positive Last Wednesday, Solvay SA (Baa2 negative), one of Europe’s leading chemical companies, announced that it had agreed to sell its cellulose acetate tow business, Acetow, to private-equity funds managed by The Blackstone Group for an enterprise value of about €1 billion. The transaction, whose price equals around 7x Acetow’s 2016 EBITDA, is credit positive because we expect Solvay to use the sale proceeds to reduce debt, which will support its deleveraging efforts. The company expects to complete the sale in the first half of 2017, subject to customary regulatory approvals.

Despite the loss of Acetow’s EBITDA contribution (around €140 million based on the 7x multiple indicated by Solvay), the divestiture will help Solvay strengthen its credit metrics, which significantly weakened following the company’s 2015 acquisition of Cytec. Although we expect Solvay to report a year-on-year increase in underlying EBITDA of 7%-8% (i.e., as if Cytec was consolidated from 1 January 2015) to €2.5 billion in 2016, we estimate that its Moody’s-adjusted net debt/EBITDA ratio will be around 3.5x at year- end 2016.

We expect Solvay’s underlying performance to further benefit from ongoing efficiency initiatives and cost synergies arising from the Cytec merger. This should help keep the company’s EBITDA roughly stable (in euro terms) in 2017 compared with 2016, despite the loss of Acetow’s profit contribution. Based on this assumption, a gross debt reduction of €1 billion would allow Solvay to lower its net debt/EBITDA to around 3.0x from our estimate of 3.5x for 2016, and increase retained cash flow/net debt close to 17% in 2017 from our estimate of 15% for 2016. This would bring metrics more in line with our quantitative guidance for a stable outlook on Solvay’s Baa2 rating.

The announcement follows the completion of the divestment of the company’s 50% stake in Inovyn Limited (B2 stable), a PVC producer. This builds on Solvay’s strategy to reduce its exposure to low-growth, commoditised businesses. Based on our estimates, Acetow will have revenues of approximately €550 million in fiscal 2016, constituting less than 5% of Solvay’s total sales of around €11.7 billion.

Although Acetow generates a healthy EBITDA margin of around 25%, it is a mature business whose performance has been negatively affected by excess capacity in recent years. Its revenues declined by 15% year-on-year to €542 million in fiscal 2015. Acetow is also exposed to a fairly concentrated customer base comprising the world’s major cigarette producers including Philip Morris International Inc. (A2 stable) and British American Tobacco plc (A3 review for downgrade), which have significant pricing power.

Francois Lauras Vice President - Senior Credit Officer +44.20.7772.5397 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Ahold Delhaize’s 2017 Share Buyback Program Is Credit Negative Last Wednesday, Koninklijke Ahold Delhaize N.V. (Baa2 positive) announced a €1 billion share buyback program for 2017. The sizable share buyback comes just after European food retailers Koninklijke Ahold N.V. and Delhaize Group merged in June 2016 to create Ahold Delhaize and is credit negative because it will reduce cash just as they are merging their operations. However, we do not think that the share buyback programme will materially affect Ahold Delhaize’s currently strong financial profile given the €3.5 billion of cash on its balance sheet as of 9 October and the company’s expectation of €1.6 billion of free cash flow in 2017.

In addition to the share buyback announcement, Ahold Delhaize’s management clarified its dividend policy, stating that it intends to sustain a payout ratio of 40%-50%, which is in line with Ahold’s previous dividend target, but less conservative than Delhaize’s previous 35%. In our view, these announcements imply that Ahold Delhaize is leaning toward Ahold’s pre-merger shareholder-friendly financial policy.

Ahold Delhaize targets post-merger annual synergies of €500 million by 2019. The savings (only €20 million this year) will increase to €220 million in 2017 and €420 million in 2018. Meanwhile, integration costs will total €350 million, with 78% of the total over the next two years. The company’s US operations, which contributed 65% of 2015 revenues pro forma for the merger, will account for 65%-70% of the savings.

Although Ahold Delhaize said that it will turn all the synergies into higher earnings, we believe that part of them may finance price cuts, notably in the US, where the company faces its greatest competition. However, management said that it will make additional cost savings if further price cuts are required.

Despite the new share buyback program, Ahold Delhaize’s credit ratios remain strong. We forecast that Moody’s-adjusted gross debt/EBITDA will stabilize at 3.0x-3.3x over the next 12 months, and Moody’s-adjusted retained cash flow/net debt will stay in the 27%-32% range. Additionally, Ahold Delhaize is now one of Europe’s largest food retailers and has a legacy of high cash flow generation (see exhibit).

Ahold’s, Delhaize’s and Ahold Delhaize’s Reported Free Cash Flow, Dividends and Share Buybacks

Note: In 2014, Ahold sold its 60% stake in Swedish food retailer ICA for €2.5 billion. Sources: The companies and Moody’s Investors Service

€ 0.0

€ 0.5

€ 1.0

€ 1.5

€ 2.0

€ 2.5

€ 3.0

2012 2013 2014 2015 (Pro Forma) 2016 Forecast 2017 Forecast

€Bi

llion

s

Ahold Delhaize Ahold Delhaize

Div. & sharebuybacks

Div. & sharebuybacks

Div. & sharebuybacks

Div. & sharebuybacks

Div. & sharebuybacks

Div. & sharebuybacks

FCF FCF FCF FCF FCF FCF

Vincent Gusdorf, CFA Vice President - Senior Analyst +33.1.53.30.10.56 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Mauser Subsidiary’s Acquisitions of Total Container and Advantage IBC Are Credit Positive On 5 December, Mauser Corporate GmbH (B3 stable), an industrial packaging producer, announced that its reconditioning subsidiary National Container Group (NCG) had again expanded its North American operations through its acquisition of Total Container Group (TCG, unrated) and Advantage IBC (unrated). The transaction will reduce Mauser’s Moody’s-adjusted gross leverage because the company plans to fund the acquisitions almost entirely through existing cash reserves. The transactions are also credit positive because they will improve Bruhl, Germany-based Mauser’s geographic footprint and provide benefits through cost synergies.

The incorporation of TCG and Advantage IBC will more strongly position Mauser’s reconditioning of intermediate bulk containers services business, its most profitable business at around 17%-18% EBITDA margin, and enable it to expand its reconditioning capabilities in the US. In addition, we expect the company will achieve significant post-acquisition synergies in plant consolidation, procurement and freight optimisation, resulting in post-synergy acquisition leverage of around 6x compared with current Moody’s-adjusted leverage of around 7x.

The acquisitions’ integration risk is low given that Mauser has completed approximately 30 acquisitions over the past 10 years and has a good track record of integrating similar bolt-on businesses. Acquisitions add footprint, which improves the company’s proximity to its customers. This is particularly important because Mauser’s products are large and bulky, and a larger footprint helps ensure freight optimization.

The acquisitions will constrain Mauser’s liquidity by reducing available cash balances to around €40 million, although we expect liquidity to remain adequate, supported by the €150 million revolver that was undrawn at 30 September, a €50 million capex facility with around €20 million availability, and a €100 million accounts receivable securitization facility with headroom of approximately €15 million at 30 September.

Mauser Group is a worldwide leading producer of industrial packaging products with over 5,000 employees and consolidated revenue of over €1.5 billion. Mauser is a portfolio company of Clayton, Dubilier & Rice.

Martin Chamberlain Vice President - Senior Analyst +44.20.7772.5213 [email protected]

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Guangzhou R&F’s Korean Ventures Are Credit Negative On 5 December, Guangzhou R&F Properties Co., Ltd. (Ba3 stable) announced that its wholly owned subsidiary R&F Properties (HK) Company Limited (R&F HK, B1 stable) agreed with Caesars Korea Holding Company, LLC (unrated) to set up a 50-50 joint venture to develop, own and operate a resort in Incheon. The resort will have a total gross floor area of 170,000 square meters (sqm), is scheduled to open by 2020, and will have facilities such as a foreigner-only casino, a luxury hotel and serviced residences. Guangzhou R&F will also acquire a 50,806.3 sqm land parcel adjacent to the resort and plans to develop residential properties there. The transactions are subject to various conditions, including Korean regulatory approvals and the issuance of the final gaming license.

Guangzhou R&F’s investment in the Korean ventures is credit negative since the projects are likely to increase its financial leverage and raise its business and execution risks. Guangzhou R&F is new to both the gaming and residential development businesses in Korea. It will take time for the company to understand Korean market dynamics and customer preferences, as well as the regulatory regime. The company’s performance will be subject to the market’s competitive landscape, Korea’s tourism industry and the travel policies of its neighboring countries, especially China (Aa3 negative). In addition, the long-term investment in the resort and the longer cash collection cycle for property sales in Korea relative to residential developments in China will also increase the company’s funding needs for its Korean projects.

Although Caesars Korea, a wholly owned subsidiary of Caesars Entertainment Corporation (CEC, unrated), will help manage the development and operating risks of the new integrated resorts, the US debt restructuring of CEC and its subsidiary, Caesars Entertainment Operating Company, Inc. (unrated), adds uncertainties about Caesars Korea’s ability to provide timely funding to the joint venture.

Nevertheless, we expect any such effect on Guangzhou R&F’s credit profile will be manageable, given the moderate scale of the investments relative to its assets. We estimate that investment costs for both the resort, including the share of Caesars Korea, and the residential development project will total around $1.0-$1.2 billion (RMB6.9-RMB8.2 billion), or around 3%-4% of Guangzhou R&F’s total assets of RMB206 billion at 30 June, and 6%-7% of its reported debt (including perpetual capital securities) as of the same date.

The company held RMB37.3 billion in cash on hand at 30 June, more than sufficient to cover the investments. Although Guangzhou R&F is likely to fund part of its investments with debt, its key financial metrics will weaken only modestly, partly because the investment will be in stages, reducing the immediate funding needs.

We expect the company’s revenue/debt ratio will continue to improve over the next 12-18 months, registering 55%-60% from 48% at 30 June, while its interest coverage will improve to 2.5x-3.0x from 2.4x over the same period, supported by revenue growth, solid contracted sales growth and lower interest costs.

The company had 24% year-on-year growth in contracted sales during the first 11 months of 2016 to RMB56.13 billion, indicating that it is on track to meeting its 2016 full-year target of RMB60 billion.

Kaven Tsang Vice President - Senior Credit Officer +852.3758.1304 [email protected]

Victor Wong Associate Analyst +852.3758.1569 [email protected]

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Infrastructure

Consumers Energy and Entergy Benefit from Early Closure of Nuclear Plant in Michigan On 8 December, Entergy Corporation (Baa3 positive) and Consumers Energy Company ((P)A3 positive) announced an agreement to terminate their contract for the purchase and sale of power (PPA) from the Palisades Nuclear Energy Plant in Michigan in 2018 rather than 2022. The earlier termination is credit positive for Consumers and Entergy.

Consumers is no longer obliged to purchase electricity from Palisades at prices of about $58 per megawatt hour (MWh) and can now purchase energy and capacity at current market prices of around $44/MWh. The company estimates that the early contract termination will save customers as much as $45 million a year, or $172 million over the remaining four years.

For Entergy, the agreement allows it to permanently retire the Palisades nuclear power plant in October 2018, reducing its business risk. Palisades is an unregulated, single-unit plant with increasing costs. The decline in Entergy’s business risk offsets the loss of a consistent revenue stream at above-market rates.

The Consumers and Entergy agreement provides for a plant refueling in the spring of 2017 with operations continuing through the end of the one-and-a-half-year fuel cycle and permanent shutdown on 1 October 2018. The two companies expect around $344 million of total value for the transaction. Half will be paid to Entergy for the early termination of the PPA, and the other half reducing Consumers’ 2018-22 customer bills. Entergy will use the proceeds to fund severance plans and a decommissioning trust as it transitions the plant and its employees to decommissioning mode.

Execution of the termination agreement is subject to the approval of the Michigan Public Service Commission (MPSC). Consumers intends to request MPSC authorization in 2017 for the recovery and securitization of the $172 million payment to Entergy. A securitization would lower the payment’s financing cost, reducing costs to customers. Consumers expects to ultimately replace the lost Palisades supply with a mix of energy efficient, demand response, and new renewable and natural gas capacity.

For Entergy, closing a roughly 800 MW single-unit reactor with increasing costs and declining value is credit positive. For example, Entergy took a nearly $400 million impairment on Palisades in the fourth quarter of 2015, recognizing the pressures the plant has faced since the PPA was originally signed in 2007. Low natural gas prices, stagnant customer demand for electricity, and the introduction of cheaper alternative generation have reduced wholesale power prices, which has hurt Palisades’ market position. Furthermore, Entergy recently introduced a plan to improve the performance of its entire nuclear fleet, increasing the plant’s capital and operating costs. The added costs would exacerbate Palisades’ loss of operating cash flow and value after the original PPA expires in 2022.

Because of the transaction, Entergy stands to lose $350-$400 million of revenue a year over the four-year period, but gains the offsetting improvement in its longer-term business risk profile, which is congruent with its broader strategy of reducing its unregulated footprint, a credit positive. Other steps the company has taken toward this end include the sale of a merchant gas plant in December 2015, the in-progress sale of its James A. Fitzpatrick nuclear plant to Exelon Corporation (Baa2 stable), and the scheduled early retirement of its Pilgrim Nuclear Facility in 2019.

Ryan Wobbrock Vice President - Senior Analyst +1.212.553.7104 [email protected]

Laura Schumacher Vice President - Senior Credit Officer +1.212.553.3853 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

ViaLagos Extends Toll Road Concession Contract, a Credit Positive On Friday, Brazilian toll road concessionaire Conc da Rodovia dos Lagos S.A. (ViaLagos) (Ba3 negative) announced a 10-year extension of its concession contract to 2047 as compensation for additional investments in the road. According to our projections, lengthening the concession life by 10 years to 2047 will increase ViaLagos’ debt service coverage ratio to around 2.2x in the next 12-18 months, which is above our previous forecast of 1.9x and the company´s historical average of 1.5x as of December 2015. In addition, we see some improvement in the concession life coverage ratio to 3.3x from 2.6x in our prior forecast and 2.5x as of December 2015.

We deem the long remaining concession life one of the key credit strengths of the concessionaire together with its relative strong concession fundamentals. ViaLagos’ road system has a total extension of 57 kilometers and serves the Região dos Lagos region, which is a regional and national tourist destination in the state of Rio de Janeiro. The area receives a large number of vacationers who use the ViaLagos road, which tends to be more volatile than commuter traffic relative to the GDP performance.

The state of Rio de Janeiro, through its regulatory agency AGETRANSP, has been supportive of privately managed toll road concessionaires as demonstrated by this contract amendment, which restores the economic and financial equilibrium of the original concession contract. Compensation for additional investments or any changes in business circumstances are generally subject to negotiation, which has been successful with several concessions.

Although the contract amendment is credit positive, ViaLagos’ ratings are somewhat constrained by Brazil’s (Ba2 negative) rating outlook, as well as by the challenging local economy after contracting by 3.8% in 2015 and our forecasted 3.5% decline in 2016.

ViaLagos is a privately managed toll road concessionaire that holds a 40-year concession extended for additional 10 years to operate and maintain the 57-kilometer RJ-124 road until 2047, which connects the municipality of Rio Bonito to São Pedro da Aldeia in the northeast part of the state of Rio de Janeiro. ViaLagos is an operating subsidiary of CCR S.A. (Ba3 negative), one of Brazil's largest infrastructure concession groups, which operates and maintains 3,265 kilometers of toll road concessions. ViaLagos accounts for approximately 1.5% of CCR’s consolidated gross operating revenues and reported net revenues of BRL100 million and EBITDA of BRL61 million as of December, 2015, according to our standard adjustments.

Aneliza Crnugelj Analyst +55.11.3043.6063 [email protected]

Camila Yochikawa Associate Analyst +55.11.3043.6079 [email protected]

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

National Grid’s Gas Networks Sale Lowers Dividend Cost and Raises Retained Cash On Thursday, National Grid Plc (Baa1 stable) announced that it had sold 61% of the UK’s largest gas distribution business, National Grid Gas Distribution Ltd. (NGGD, A3 review for downgrade), to a consortium of infrastructure funds led by Macquarie Infrastructure and Real Assets. Although National Grid previously stated that all of the net proceeds would be returned to shareholders, the company now says that it will retain around £700 million to reduce net debt, a credit positive. Additionally, given that National Grid sold the stake at a 52% premium to its regulated asset value (RAV), higher than suggested by preceding transactions, the potential share repurchase and associated reduction in National Grid’s dividend will be larger, improving retained cash flow in future periods.

The consortium will own NGGD through a holding company that, according to Thursday’s announcement, will be geared at 85% of RAV, above the 65% gearing of the NGGD operating company. Although we expect that the structure will include features that restrict the new owners’ ability to add leverage, the company provided no further details. As a result, NGGD’s A3 rating remains on review for downgrade.

We had expected National Grid to distribute to shareholders all of the cash received from the sale net of debt, which at the realised price would have been £4.7 billion, less transaction costs. The company’s decision to define net proceeds based on a theoretical calculation that considers the company’s pro rata share of the holding company’s additional gearing means distributions will be only £4 billion less costs, with National Grid retaining the remaining £700 million.

We believe the 52% premium to RAV is a record for a large regulated network, and is higher than the 44% premium achieved when SSE plc sold a similar asset, a stake in Scotia Gas Networks, in October (see exhibit).

Estimated Premium to Regulated Asset Value and Comparison with Sale of Scotia Gas Networks

National Grid Sale of National Grid Gas Distribution

SSE Sale of Scotia Gas Networks

March 2016 Regulated Asset Value Iinflated to Current Prices £8,838 £5,108

Value of Stake Sold £4,698 £621

Percent Sold 61% 17%

Implied Market Value of Equity £7,702 £3,719

Third Party Net Debt at Book Value £5,745 £3,632

Enterprise Value Based on Book Value of Debt £13,447 £7,351

Achieved Premium to RAV on Book Value 52% 44%

Enterprise Value Based on Fair Value of Debt £13,847 £8,076

Achieved Premium to RAV at Fair Value of Debt 57% 58%

Note: Data excludes fair value of debt adjustment. Sources: National Grid, Office of Gas and Electricity Markets and Moody’s Investors Service analysis

This higher premium reflects, in part, the business’ extremely low cost of debt. Since the majority of the company’s debt has been issued in the past month, its borrowing costs are, and will likely remain, well below the regulator’s allowances, which implicitly assume that debt has been issued steadily over the past 10 years. Excluding the effect of embedded debt costs, we estimate that National Grid received a 57% premium, very similar to the 58% premium that SSE received on an equivalent basis.

Graham Taylor Vice President - Senior Analyst +44.207.772.5206 [email protected]

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

At least £3 billion of the distribution will be made via a special dividend, with the remainder distributed in a share buyback. However, the company has announced that the special dividend will be accompanied by a share consolidation, which will reduce the future dividend burden and support National Grid’s retained cash flow, a key credit metric.

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Origin’s Proposed Divestment of Conventional Oil and Gas Assets Is Credit Positive Last Tuesday, Origin Energy Limited (Baa3 negative) announced plans to sell its conventional oil and gas assets to a newly formed publicly listed company or “NewCo.” Although Origin will not retain any equity interest in NewCo, it intends to purchase gas produced by NewCo under gas offtake arrangements. The gas fields earmarked for divestment equal around 10%-20% of Origin’s existing gas supply portfolio.

The transaction is credit positive for Origin because the company plans to use the sale proceeds to reduce its existing debt, which amounted to AUD12 billion at the 2016 fiscal year end, 30 June 2016 (including its share of a project finance facility at its subsidiaries). Origin’s credit quality has been under pressure in recent years because of the additional debt and interest expense it incurred to fund its 37.5% share of the Australia Pacific liquefied natural gas (APLNG) export project amid increasing competition in its retail business, which put downward pressure on margins.

We estimate that the company’s fiscal 2017 financial leverage, as measured on a consolidated basis (i.e., including its pro-rata share of APLNG) by the ratio of funds from operations (FFO) to debt, could increase by up to two percentage points to 19% based on assumed sales proceeds in recent media articles. The exact effect depends on gas and equity market conditions at the time of the divestment, which will drive the upfront proceeds, as well as the terms of the new gas supply arrangement between Origin and NewCo. The sale will reduce Origin’s FFO because of the loss of the post-tax cash contribution from these divested gas assets and incremental gas purchase costs, partially reducing the effect of lower interest expense.

The sale also demonstrates Origin’s commitment to focus on its core and more stable domestic energy markets business (see exhibit), in which it has a leading market position in Australia’s more populous east coast. Origin will also be relieved of the future capital investments required to further develop these gas fields, a factor that will increase the company’s flexibility to invest in its identified strategic focus area of new technology and renewables.

Origin’s EBITDA from Energy Markets and LNG Increase Post Transaction

Sources: Origin Energy and Moody’s Investors Service

The terms of the new gas arrangements will determine Origin’s ongoing cost of gas and certainty of supply, and are a key support for Origin’s integrated gas operations in Australia’s east coast. Origin Energy relies on gas from third-party producers and its own gas fields to support its energy retail and power generation needs, and its ongoing access to flexible and low cost gas supply is one of its key competitive advantage in the market.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 Post Transaction

Energy Market Upstream LNG

Spencer Ng Vice President - Senior Analyst +612.92.708.191 [email protected]

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Insurers

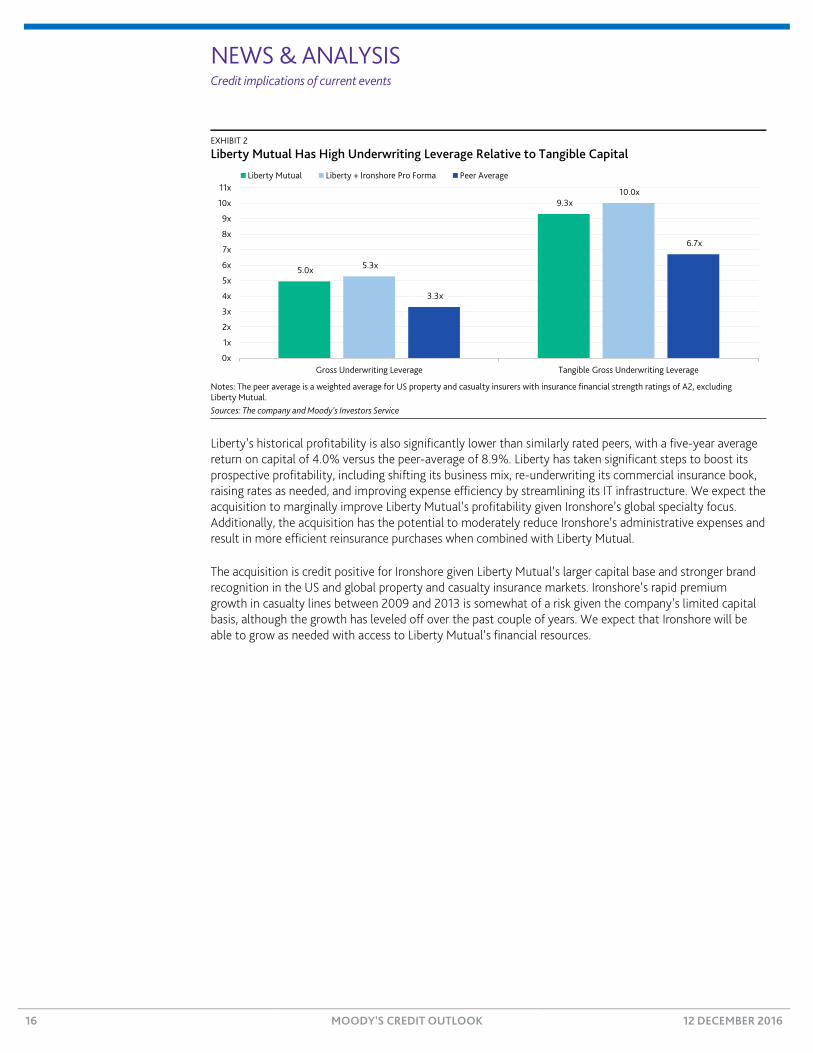

Liberty Mutual’s Acquisition of Ironshore Is Credit Negative for It, Positive for Ironshore Last Monday, Liberty Mutual Group Inc. (Baa2 stable) announced that it had signed an agreement to acquire Ironshore Holdings (U.S.) Inc. (Baa3 review for upgrade), a global specialty property/casualty insurance company, from Fosun International Limited for about $3 billion in cash. Although the proposed acquisition has strategic benefits for Liberty by significantly expanding Liberty’s global specialty operations, particularly in the US excess and surplus (E&S) lines market, the transaction is credit negative because we expect that it will increase underwriting leverage relative to tangible capital. The acquisition also incrementally raises Liberty’s underwriting and reserving risk profile, including marginally higher catastrophe risk.

The companies expect to close the transaction in the first half of 2017, subject to regulatory approvals in various jurisdictions, and the parties expect Ironshore’s management to remain following the deal’s close. This would help mitigate integration and execution risks associated with the transition.

As the 10th largest US E&S writer, Ironshore would provide Liberty with additional specialty underwriting and distribution capabilities and earnings potential, with the combined operation ranking as one of the top five US E&S carriers. The E&S market focuses on specialty markets that are often more profitable but carry higher risk profiles and underwriting challenges than the standard insurance lines. Global specialty insurance has been a profitable and growing market for Liberty, and we expect that this acquisition would help Liberty boost this business to about 18% of premiums pro forma from 14% for 2015 (see Exhibit 1).

EXHIBIT 1

Ironshore Acquisition Enhances Liberty Mutual’s Net Written Premiums in Global Specialty Operations

Sources: The company and Moody’s Investors Service

Liberty Mutual’s capital adequacy, as measured by gross underwriting leverage (premiums and reserves relative to capital), was 5.0x at year-end 2015 compared with similarly rated peers at 3.3x (see Exhibit 2). When looking at the metric on a tangible basis (premiums and reserves relative to tangible capital), Liberty’s leverage increased to 9.3x at year-end 2015 relative to peers’ 6.7x. Part of what is behind Liberty’s relatively high underwriting leverage is its sizable long-tail reserve base (especially workers’ compensation liabilities), which is partially mitigated by a retroactive reinsurance agreement. These metrics will deteriorate moderately following the Ironshore acquisition, with gross underwriting leverage rising to 5.3x and leverage on a tangible basis rising to 10.0x, although they could improve as policyholders’ equity grows over time.

U.S. Consumer Markets49%

Intl. Consumer Markets10%

Commercial27%

Global Specialty14%

Liberty Mutual Actual 2015

U.S. Consumer Markets47%

Intl. Consumer Markets10%

Commercial25%

Global Specialty18%

Liberty Mutual and Ironshore Pro Forma, 2015

Jasper Cooper Vice President - Senior Analyst +1.212.553.1336 [email protected]

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

EXHIBIT 2

Liberty Mutual Has High Underwriting Leverage Relative to Tangible Capital

Notes: The peer average is a weighted average for US property and casualty insurers with insurance financial strength ratings of A2, excluding Liberty Mutual. Sources: The company and Moody’s Investors Service

Liberty’s historical profitability is also significantly lower than similarly rated peers, with a five-year average return on capital of 4.0% versus the peer-average of 8.9%. Liberty has taken significant steps to boost its prospective profitability, including shifting its business mix, re-underwriting its commercial insurance book, raising rates as needed, and improving expense efficiency by streamlining its IT infrastructure. We expect the acquisition to marginally improve Liberty Mutual’s profitability given Ironshore’s global specialty focus. Additionally, the acquisition has the potential to moderately reduce Ironshore’s administrative expenses and result in more efficient reinsurance purchases when combined with Liberty Mutual.

The acquisition is credit positive for Ironshore given Liberty Mutual’s larger capital base and stronger brand recognition in the US and global property and casualty insurance markets. Ironshore’s rapid premium growth in casualty lines between 2009 and 2013 is somewhat of a risk given the company’s limited capital basis, although the growth has leveled off over the past couple of years. We expect that Ironshore will be able to grow as needed with access to Liberty Mutual’s financial resources.

5.0x

9.3x

5.3x

10.0x

3.3x

6.7x

0x

1x

2x

3x

4x

5x

6x

7x

8x

9x

10x

11x

Gross Underwriting Leverage Tangible Gross Underwriting Leverage

Liberty Mutual Liberty + Ironshore Pro Forma Peer Average

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Security Firms

UK’s Proposed Contracts-for-Difference Trading Rules Are Credit Negative for Spread-Betting Firms Last Tuesday, the UK Financial Conduct Authority (FCA) published its proposal for enhancing the rules governing trading of contracts for difference (CFDs). The proposal includes restricting leverage to 25x for inexperienced retail investors (i.e., those with fewer than four quarters of trading experience in CFDs or similar products over the past three years) from over 200x currently.

Such limitations, should they be implemented, are credit negative for the UK’s spread-betting firms such as CMC Markets plc (unrated) and IG Group (unrated) because they are likely to lower industry trading volumes, profitability and growth prospects. The proposed limits will adversely affect the industry leaders, CMC and IG, and weaker players even more. The more entrenched firms that have a greater proportion of experienced retail clients may be less affected by these measures.

The more limited leverage may lead smaller firms to leave the industry, which would benefit larger firms’ competitive positioning. We would expect firms with other, non-spread-betting product offerings, such as retail brokerage, to invest in these businesses in order to diversify their businesses. Still, we expect the negative effect on client trading volumes because of these proposals to outweigh these relative benefits.

CFDs as an investment tool have gained traction in the UK because profits are not liable for taxation. The FCA found in its study that 82% of retail investors lost money on this product throughout the course of a year, with the average loss totalling £2,200. Preventing the retail investor from such losses will reduce spread-betting firms’ client risk exposures. While client margin has historically limited the extent of losses faced by the spread-betting firms, there have been instances where market moves have led to client position losses greater than client margin, creating potential losses for the spread-betting firms.

Following the Swiss National Bank’s decision to remove the currency peg against the euro in January 2015, firms lost money because of client risk exposures that faced losses greater than client margin, owing to the sudden market move and compounded by high levels of leverage. By lowering leverage, the FCA will minimize the effect such negative shocks have on retail clients and these firms.

Compared with international standards, allowable leverage in the UK is considerably higher (see exhibit). CFDs offer investors the opportunity to leverage their investment exposures, without owning the underlying products.

Maxwell Price Associate Analyst +44.20.7772.1778 [email protected]

Michael C. Eberhardt, CFA Vice President - Senior Credit Officer +44.20.7772.8611 [email protected]

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Comparison of International Leverage Regulation The UK is notably more liberal with its regulation of leverage for CFDs.

Note: Red highlights the potential decrease in allowable leverage from existing practice. Source: Financial Conduct Authority

The FCA is also analysing binary betting, to assess whether it is a necessary form of financial risk management, or effectively gambling on the stock market. Given their characteristics, this has led the Treasury to consult on whether to bring binary bets into the scope of FCA regulation. As part of the transposition of Markets in Financial Instruments Directive (MiFID II), a European Commission opinion concluded that they should be considered as MiFID financial instruments.

0x

20x

40x

60x

80x

100x

120x

140x

160x

180x

200x

UK US Japan Hong Kong Singapore Poland Israel

Contracts for Differences FX

US Hong Kong Singapore Poland IsraelJapan

NEWS & ANALYSIS Credit implications of current events

19 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Sub-sovereigns

Brazilian States Will Benefit from BRL5 Billion Federal Revenue Transfer Last Wednesday, Brazil’s federal government announced that it will transfer to Brazilian states BRL5 billion of proceeds it received from its amnesty program for taxpayers repatriating undeclared tax assets from abroad, in exchange for a commitment from state governors to implement fiscal reforms, including limits on current expenses and pension reform. The federal government expects that the commitment from all state governors will materialize into a public declaration in the coming days.

The transfer is credit positive for the states because it will provide cash relief at a time when they face liquidity pressure amid dwindling revenues because of Brazil’s recession. Liquidity is particularly dire at this time of year because personnel expenses are high owing to payment of the 13th-month salary (a gratuity given widely in Brazil that equals a month’s salary and is paid in two installments in November and December). The amount of cash relief will vary depending on the importance of federal transfers for each state’s revenues, with northeastern states such as Maranhao (Ba3 negative) and Bahia (Ba3 negative) benefiting more than Sao Paulo (Ba2 negative), Parana (Ba3 negative) and Minas Gerais (B1 negative) (see exhibit).

Repatriation of Undeclared Tax Assets to Brazilian State as Percent of 2015 Revenues

Sources: Brazilian national treasury and Moody’s Investors Service

States’ commitment to implement fiscal measures as a condition of receiving the extra revenue is also credit positive because it will help rebalance states’ fiscal position by reducing the growth of expenses such as salaries and pension-related payments. On an aggregate basis across the five states that we rate, personnel expenses were 48% of total expenses in August 2016, up from 41% in December 2010, reducing their fiscal space. The agreed measures include increasing state pension contributions to 14% of salary payments from 11%, and capping current expense growth to inflation of the prior year for a period of 10 years.

The announcement also demonstrates the Brazilian government’s continued commitment to enforce fiscal discipline among the states. Last June, the government was able to pass only part of the fiscal measures it proposed in exchange for extending the maturity of state debt owed to the federal government by up to 20 years. Some of the rejected measures are now part of this agreement.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0%

10%

20%

30%

40%

50%

60%

Minas Gerais Parana Maranhao Sao Paulo Bahia

Tax Asset Repatriation Fines - right axis Tax Asset Repatriation Excluding Fines - right axisIntergovernmental Transfer/ 2015 Operating Revenue - left axis

Paco Debonnaire Analyst +55.11.3043.7341 [email protected]

Cintia Nazima Associate Analyst +55.11.3043.6091 [email protected]

NEWS & ANALYSIS Credit implications of current events

20 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

Although months of further deterioration in states’ fiscal balances and liquidity has increased public awareness of the need for structural reforms, the implementation of unpopular measures across all states will depend on the approval of each state’s legislative assembly, which will continue to face challenges.

Additionally, success in implementing pension reforms at the state level will largely depend on pension reforms at the federal level. The Brazilian government recently chose to exclude firefighters and military personnel from its pension reform proposal, leaving states, which have little political ability to push through the reforms, the responsibility for doing so.

RECENTLY IN CREDIT OUTLOOK Select any article below to go to last Thursday’s Credit Outlook on moodys.com

21 MOODY’S CREDIT OUTLOOK 12 DECEMBER 2016

NEWS & ANALYSIS Corporates 2 » Historic Auctions Mark Leap in Mexico's Drive to Lure Big

Foreign Oil, a Credit Positive » Lukoil's Sale of Its Diamond Business Is Credit Positive » Obrascon Huarte Lain's Sale of a Stake in Its Mayakoba,

Mexico, Hotels Is Credit Positive » Fosun's Proposed Sale of Ironshore Is Credit Positive

Infrastructure 7 » Illinois' Passage of Nuclear Subsidy Is Credit Positive for Exelon » UK Cap on Interest Deductions Is Credit Negative for

Infrastructure Issuers » Korea's Approval to Restart Nuclear Reactors Is Credit

Positive for KHNP and KEPCO

Banks 10 » Bank of Nova Scotia Sells HollisWealth, a Credit Negative » RBS Settlement Related to 2008 Rights Issue Is Credit Positive » Uzbekistan Proposes Broad Currency Liberalization, a Credit

Negative for National Bank of Uzbekistan

Sovereigns 15 » Poland's Economic Slowdown Poses Risks to Potential

Growth and Fiscal Outlook » Iran Proposes Credit-Positive Reforms in Its Fiscal 2017 Budget » Uzbekistan's Smooth Presidential Succession and Policy

Initiatives Are Credit Positive » China's Latent Capital Account Pressures Are Credit Negative

US Public Finance 23 » Orange County, Florida, Repays Orlando's Portion of Tourist

Development Tax Bonds, a Credit Positive for City

Securitization 25 » Marketplace Loan ABS Would Benefit from a Bank Charter

for US Financial Technology Companies

MOODYS.COM

Report: 193593

© 2016 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (“MOODY’S PUBLICATIONS”) MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating, agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be reckless and inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or other professional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

EDITORS SENIOR PRODUCTION ASSOCIATE Elisa Herr and Jay Sherman Sol Vivero